Embed Size (px)

DESCRIPTION

Invasive Species | Heat Pumps | Chile's Red Gold | The Value of Nature | The Canary Project and more!

Citation preview

WWF’s Seize Your Power campaigncalls on investors globally to act on climate change by committing $40 billion to new investments in renewable energy within one year.

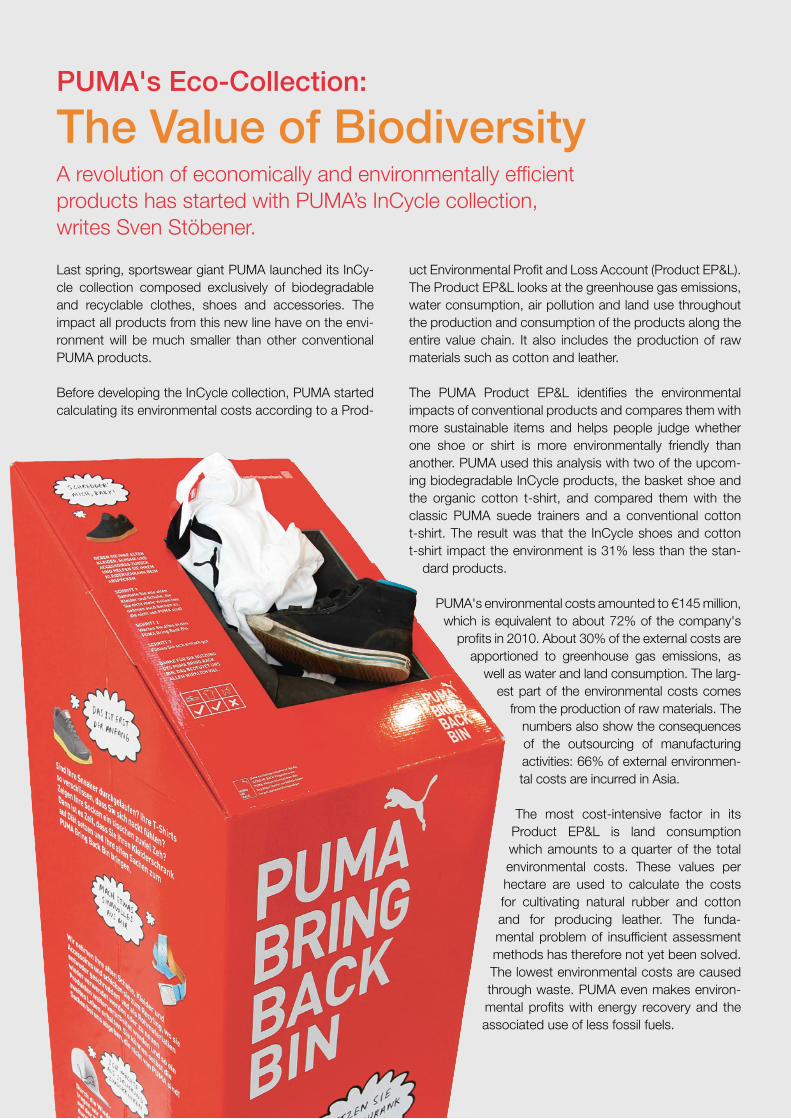

The Value of NatureBusiness and Biodiversity

Chile’s Red GoldExploiting Atacama Desert

Heat PumpsRenewable by Nature

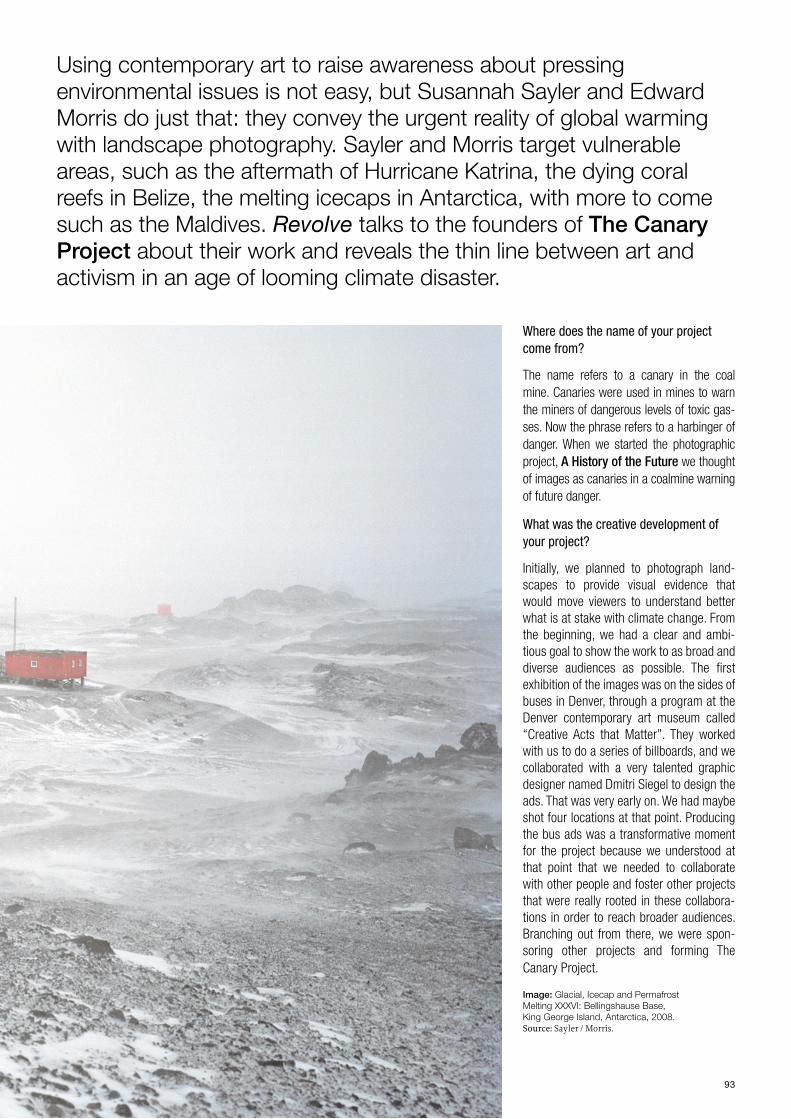

The Canary ProjectClimate Change Art

Invasive Species

N°9 | FA

LL 2013

N°9 | FALL 2013

! 8 / £ 6,5

For more information on how to participate:

E: [email protected] T: +32 2 353 05 84

www.revolve-magazine.com

Following the success of the Visualizing Energy photo exhibition launched during the 2013 EU Sustainable Energy Week and seen by over 120,000 people throughout the summer in Brussels, Revolve is proud to present the 2014 sequel: The Rise of Renewables.

Expanding coverage to include renewable energy workers and projects from around the world, The Rise of Renewables highlights innovative regional and national initiatives, bringing together the actors, pioneers, and investors that are shaping a more sustainable future.

Connecting Europe and the Middle East by showing the human dimension of the energy transition internationally, The Rise of Renewables will be the official media event of the Abu Dhabi Sustainability Week and once again of the EU Sustainable Energy Week in Brussels!

Join

us

and

star

t rev

olvi

ng!

5

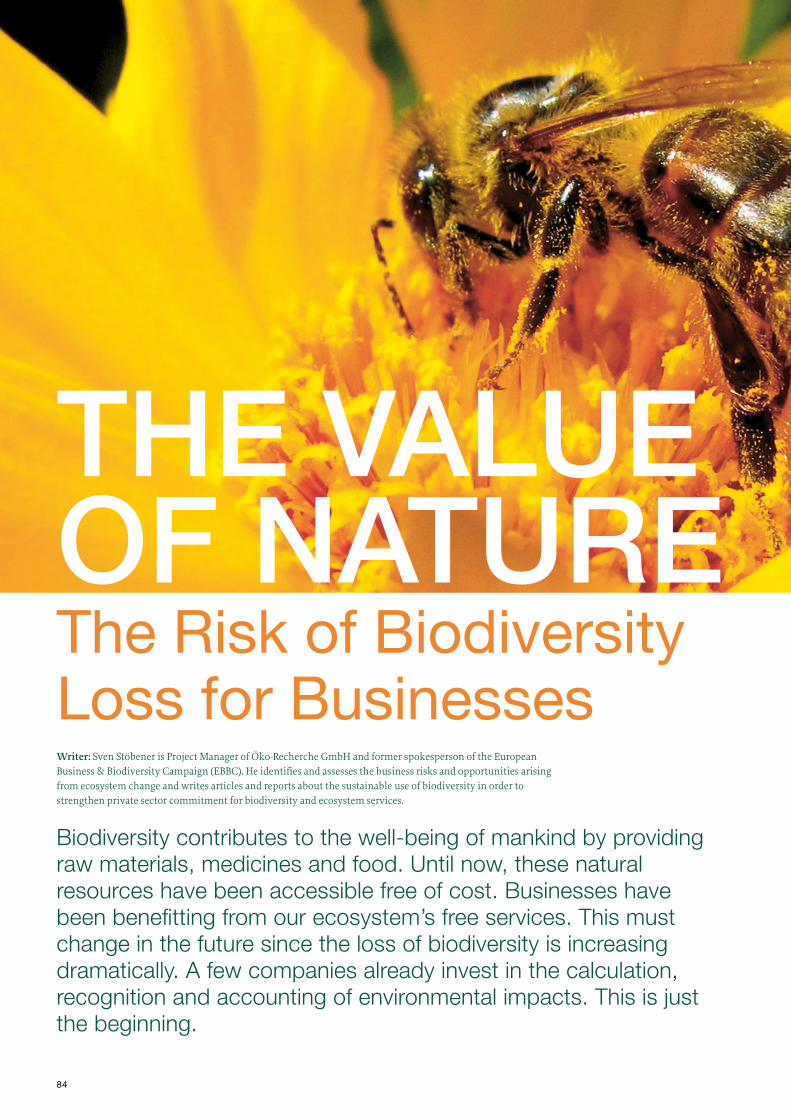

The global environmental, social and economic challenges faced by societies currently will accelerate over time as the world’s population is set to grow to 9 billion by 2050. Water scarcity and pollution, competing use of natural resources such as land, climate change and variability, demographic changes and globalizing supply chains are all underpinned by social challenges such as increasing poverty and social marginalization. A better understanding of the impacts and dependencies on our natural and human capital is needed along with how it relates to globalization trends.

Where does the private sector and specially, the financial sector, fit into this picture? Finan-cial institutions are increasingly called upon to play a role in addressing these sustainability challenges. The idea of having private sector participation is not new; there have been count-

less initiatives by governments and multilateral organizations promoting this idea, such as Goal 8 of the Millennium Develop-ment Goals which calls for a global partnership for development.

What has changed is the shift from viewing financial institu-tions as financiers to legitimate partners for development as

witnessed through the forthcoming Responsible Agricultural Investment principles (FAO) and Sustainable Agricultural Principles (UN Global Compact). The financial sector is at the table with companies, governments and civil society to set forth guiding principles for sustainable agricultural practices.

There are other important trends in financing sustainability: financial institutions are no lon-ger only providers of capital but facilitators for new ideas and trends in the market. The Dutch food and agricultural bank, Rabobank’s formal partnership with WWF, has enabled the development of sustainable salmon aquaculture industry in Chile through better farm-ing practices and certification at a time when the industry was on the verge of collapse due to unsustainable aquaculture practices. The circular economy is a key pillar of the bank’s sustainability strategy.

They are not alone, numerous banks and investment firms now finance sustainable solutions such as renewable energy. According to 2012 report by UNEP on global trends in renewable energy investment, the appetite for these types of investments has grown with over $244 billion in new investment in renewable energy solutions such as carbon capture and storage, energy access to wind, solar and geothermal energy among others. This signals a move-ment from financing fringe technologies with little uptake to mainstream solutions that are an important part of the global energy mix.

Special Guest Editorial

Lara YacobProgram Manager Corporate Engagements

Sustainable Financing, Financing Sustainability

N°9 | FALL 2013

The circular economy is a key pillar of the bank’s sustainability strategy.

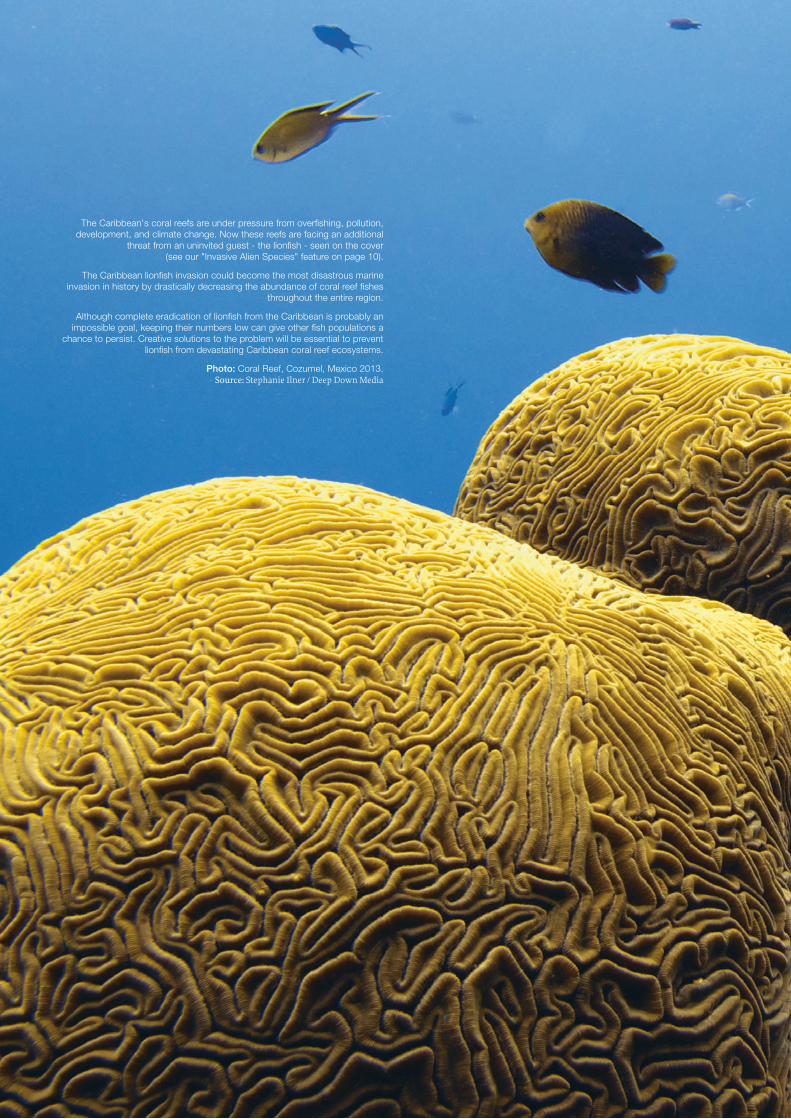

The Caribbean's coral reefs are under pressure from overfishing, pollution, development, and climate change. Now these reefs are facing an additional

threat from an uninvited guest - the lionfish - seen on the cover (see our "Invasive Alien Species" feature on page 10).

The Caribbean lionfish invasion could become the most disastrous marine invasion in history by drastically decreasing the abundance of coral reef fishes

throughout the entire region.

Although complete eradication of lionfish from the Caribbean is probably an impossible goal, keeping their numbers low can give other fish populations a

chance to persist. Creative solutions to the problem will be essential to prevent lionfish from devastating Caribbean coral reef ecosystems.

Photo: Coral Reef, Cozumel, Mexico 2013. Source: Stephanie Ilner / Deep Down Media

8

CO

NTE

NTS

CONTRIBUTORS

Joelle Rizk Lara YacobMarcello Cappellazzi Michela PfeiferRuth GamanoValentina Pinzuti

PHOTOGRAPHERS

Andreas Arianna PaganiBrian GratwickeDaniel PlumerDon DeBold Don MacauleyEdward MorrisE. DronkertJames ByrumJans CanonJ. PetersenKitten WantsMarino CarlosOlivier ErvynPatrick Bingham-HallRobert TaylorSarahStephanie IlnerSusannah SaylerTed

GRAPHIC DESIGN

Filipa Rosa

ENERGY ASSISTANT

Edoardo De Silva

ASSISTANT | RESEARCHER

Marcello Cappellazzi

EDITOR-AT-LARGE

Bostjan Videmsek

MANAGING CONSULTANT

Joelle Rizk

REGIONAL MANAGERS

Rajnish Ahuja (India | Asia)

FOUNDING EDITOR

Stuart Reigeluth

REVOLVE Magazine (ISSN 2033-2912) is registered in Belgium, BE 0828.676.740.

Revolve Magazine is printed with vegetable-based ink on chlorine-free paper.

www.revolve-magazine.com

ENVIRONMENT

10 | Invasive Alien Species Introduced intentionally or not, foreign species are altering

eco-systems with devastating results for indigenous plants, fish and animals that are pushed out or killed off.

ANALYSIS

18 | Chile’s Red Gold Michela Pfeifer travels to the land of the biggest man-made

hole on Earth where the copper industry is blossoming into another natural resource curse.

FOCUS

27 | Heat Pumps Usually eclipsed by wind mills and solar panels, heat

pumps use many different sources of renewable energy and are pivotal to more efficient livelihoods and cities.

CITIES

39 | Singapore’s Green Architecture The ultra luxury hotel PARKROYAL on Pickering by

WOHA Architects won this year’s Green Mark Platinum, Singapore’s highest environmental certificate.

08

27

Cover image: The Red Lionfish (Pterois volitans) is one of two Indo-Pacific lionfish species, seen here in Tasik Ria, Manado, Indonesia. Source: J. Petersen / Wikipedia.

Very colorful and beautiful, the lionfish is a highly invasive and threatening species. Voracious eaters, they impact on local ecosystems and they put swimmers, snorkelers, divers, and fishermen at risk from their painful, venomous sting.

9

“few of us stop to consider how just about every facet of our lives is built around our

energy consumption. Nearly everything we do is inextricably bound to our use of energy.”

Jeff Rubin, Why your world is about to get a whole lot smaller (2010).

VIEWS

51 | Ghana’s Waste-Pickers In the town of Koforidua, Belgian photographer, Olivier Ervyn,

captures the essence of a business based on scavenging for hard plastic and cans to resell.

GEOPOLITICS

51 | Afghanistan’s Extractive Industry Located at the epicenter of trade and travel in Central and

Southern Asia, Afghanistan could emerge as a regional hub – if its minerals are managed properly.

WATER

76 | Liguria: Preserving the Land Two years after Cinque Terre was hit by flash floods, Revolve

visits the north-western region of Italy to see reconstruction and prevention efforts.

BUSINESS

84 | The Value of Nature Sven Stöbener describes why companies should invest more

in environmentally-friendly models of doing business: it’s simply more sustainable.

CULTURE

92 | The Canary Project Juxtaposing art and activism, photographers Susannah

Sayler and Edward Morris offer an engaging new dimension to addressing climate change.

39

51

67

96

Climate change, habitat loss, and pollution are environmental challenges defining the 21st century; another less well-known but equally related aspect is the proliferation of invasive alien species. While the migration and ‘invasion’ of species is nothing new, two reports by the European Environment Agency (EEA) turn the spotlight on how alien species are intentionally introduced to new places while many other introductions are unintentional. Ruth Gamano looks at the reasons, the effects and future of species invasions.

10

Introduced intentionally or accidentally by human activity, invasive alien species are animals, plants, fungi and micro-organisms which cause adverse effects on their new habitat or bio-region; for example, by out-competing or predating native species, which evolved without specific adaptations to cope with them. Once established in their new environment, such species can be extremely difficult or even impossible to eradicate and can lead to the devastation of populations of

native species, causing harm economically, environmentally and ecologically.

For these reasons, invasive alien spe-cies have been recognized as one of the most serious threats to biodiversity at the global level, second only to habitat loss and destruction (“Status, impacts and trends of alien species that threaten ecosystems, habitats and species”, Convention on Bio-logical Diversity, 2001)

Writer: Ruth Gamano is an independent contributor to Revolve.

Lionfish (Pterois miles and P. volitans) are predatory fish native to the Indo-Pacific. It is believed that they were introduced to the Caribbean in the early 1990s from local aquariums or fish hobbyists in Florida. Once loose in the marine environment their numbers began exploding. Lionfish are known for eating anything they can fit in their mouths and seem to eat nearly constantly leaving native reef fish populations and coral reef community stability at great risk.

Photo: Lionfish in Mexico. Source: Stephanie Ilner / Deep Down Media

Invasive AlienSpecies

An Alien Species is “an organism which humans have introduced, intentionally or accidentally, outside its previous range”. Those alien species which cause negative impacts on biodiversity, socio-economy or human health are considered to be Invasive.

Conference of the Parties to the Convention on Biological Diversity, 2002

12

The full extent of the threat posed by Invasive Alien Species is becoming better understood thanks to various scientific studies that have been undertaken in recent years. Between 1994 and 2006, the European Commission funded 90 research projects related to, or dealing entirely with the issue, with a total budget of more than !88 million. These projects included ALARM, IMPASSE and DAISIE (Delivering Alien Invasive Species in Europe). DAISIE supports a comprehensive review of the scale of, and ecological and economic impacts caused by, invasive alien spe-cies of all types in Europe. Data collected through this project shows that of all alien species in Europe at least 11% are known to have negative ecological impacts and 13% negative economic impacts. Of the 395 European native species listed as critically endangered on the IUCN Red List

of Threatened Species, 110 are at risk due to invasive alien species.

Many non-native species are introduced to new areas, therefore being ‘alien’, with-out being invasive. Sometimes, they fail to adapt sufficiently to their new environment to establish self-sustaining populations and eventually die off. This is true of spe-cies such as crocodiles and pythons, some of which have been released or escaped in Europe, but have not become problematic in the long-term. In other cases, species are introduced and inhabit new eco-systems without damaging them. They co-exist with native species without competing with them. The Corsican ‘Red’ deer, which is thought to have been introduced to Corsica by humans in ancient times, is even protected by EU legislation as a valued aspect of the island’s environmental and cultural heritage.

The introduction of alien species can bring enormous economic benefits in certain sec-tors, such as agriculture, animal farming, fishing, wood production, medicine, hunting, and the ornamental plant trade. Alien spe-cies can even sometimes offer benefits to the natural environment of their new habitats by being food sources for native species and by replacing previously lost vegetation cover. However, this is misleading since such appar-ently beneficial effects can still harm the nat-ural balance of eco-systems in the long-term. While bringing short-term socio-economic profit, some alien species turn out to be invasive, damaging biodiversity and natural resources in the long-term. One example is the Red Swamp Crayfish, which brings beneficial fishing opportunities in areas like southern Spain, but also carries the crayfish plague pathogen that can drive native cray-fish species populations to extinction.

Impacts of Invasive Alien Species

lower level of awareness about associated problems in comparison to other areas of the globe. The introduction rate of inva-sive species to Europe is accelerating but insufficient care and concern is shown with regards to this threat. This is gradually changing now and increasing recording and publicity of the associated impacts are raising awareness of the issue, especially in relation to human health, biodiversity and the environment.

Historically SpeakingDamage caused by invasive species has been chronicled throughout history. In 77 AD, Pliny the Elder, a learned natural philosopher of the early Roman Empire, wrote in his encyclopedia Natural History about the rabbit invasion of the Balearic Islands, describing it as such a drastic problem that the help of the Emperor Augustus and the Roman Army was sought to control them. Even then inva-sive species were not new; some human-

initiated introductions are known to date back to Neolithic times, especially around the Mediterranean. Such species as the pheasant, originatedly from Asia, have been introduced around the world and became integral parts of their adopted habitats to the extent that they seem native today.

The long history of species introductions to Europe may be responsible for the

While bringing short-term socio-economic profit, some alien species turn out to be invasive, damaging biodiversity and

natural resources in the long-term.

Kudzu (Pueraria Lobata) has been spreading in the south of the U.S. at the rate of 61,000 hectares annually and has produced devastating environmental consequences, earning it the nickname: "the vine that ate the South." $6 million are spent annually for controlling its spread.

Source: Kitten Wants / Flickr

13

Prolific and aggressive, the Red Swamp Crayfish originates from north-east-ern Mexico and south-central USA. Intentionally introduced for aquaculture, consumption, use as bait and pet trade, it lives today in all continents except Antarctica and Australia.

Source: E. Dronkert / Flickr

The Ring-Necked Parakeet (Psittacula Krameri), native to Africa and Asia, is world’s most widespread wild parrot species. Its first observation in the wild in countries like Belgium and England happened in the end of the 1960's.

Source: Jans Canon / Flickr

The ‘Red’ Deer, which is thought to have been introduced to Corsica by humans in ancient times, is as example of an alien species that inhabit new eco-systems without damaging them. They co-exist with native species without competing with them.

Source: Don Macauley / Flickr

1890 saw 60 European Starlings introduced to Central Park, New York. Numbers are estimated to have now reached 200 million; they are collectively capable of

consuming 20 tons of potatoes a day.

Source: Don DeBold / Flickr

14

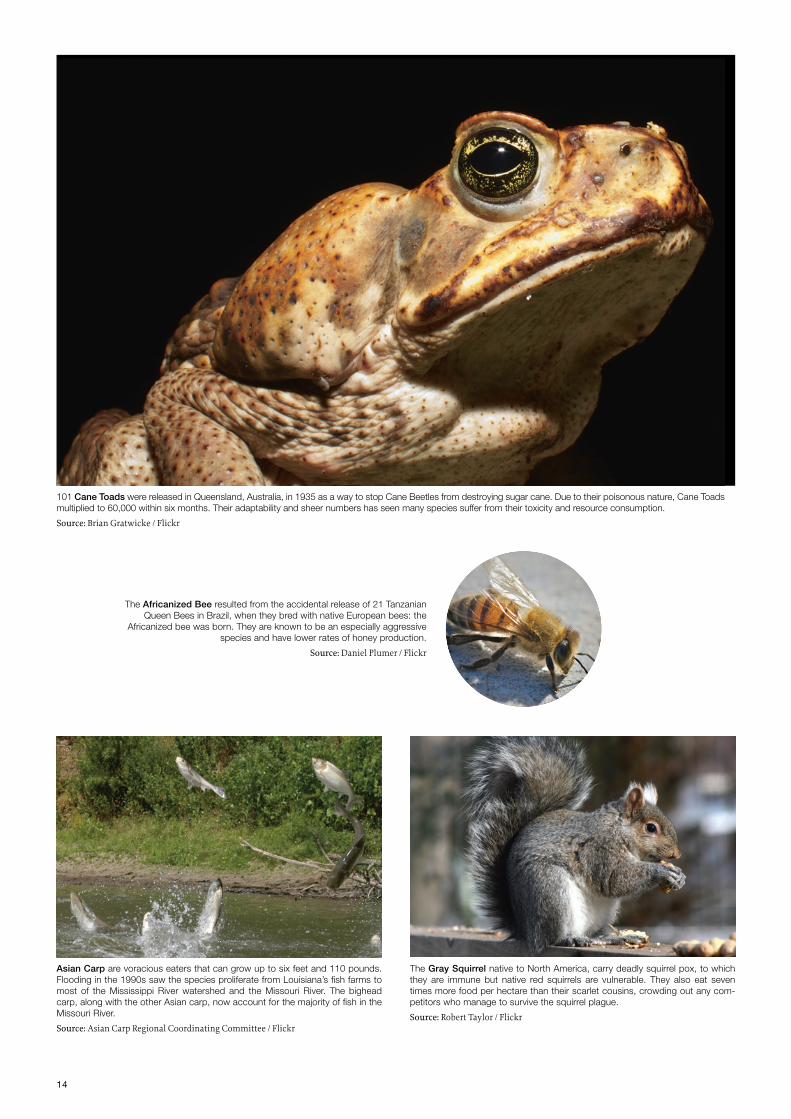

101 Cane Toads were released in Queensland, Australia, in 1935 as a way to stop Cane Beetles from destroying sugar cane. Due to their poisonous nature, Cane Toads multiplied to 60,000 within six months. Their adaptability and sheer numbers has seen many species suffer from their toxicity and resource consumption.

Source: Brian Gratwicke / Flickr

Asian Carp are voracious eaters that can grow up to six feet and 110 pounds. Flooding in the 1990s saw the species proliferate from Louisiana’s fish farms to most of the Mississippi River watershed and the Missouri River. The bighead carp, along with the other Asian carp, now account for the majority of fish in the Missouri River.

Source: Asian Carp Regional Coordinating Committee / Flickr

The Gray Squirrel native to North America, carry deadly squirrel pox, to which they are immune but native red squirrels are vulnerable. They also eat seven times more food per hectare than their scarlet cousins, crowding out any com-petitors who manage to survive the squirrel plague.

Source: Robert Taylor / Flickr

The Africanized Bee resulted from the accidental release of 21 Tanzanian Queen Bees in Brazil, when they bred with native European bees: the

Africanized bee was born. They are known to be an especially aggressive species and have lower rates of honey production.

Source: Daniel Plumer / Flickr

15

Global patterns suggest that the numbers of alien species and their impacts will increase (‘Global Biodiversity: Indicators of Recent Declines’, Science, Butchart et al., 2010,). Invasive alien species are likely to cause increased fragmentation, destruc-tion, alteration and replacement of habi-tats, which will affect even more species and eco-systems. Many past invasions could have been prevented and measures for early detection and rapid responses

must be implemented now to help pre-vent and control future invasions. Species which have already invaded new habitats must be controlled and, where appropriate and possible, eradicated. Long-term spe-cies management should be a last resort.

Eradication of invasive alien species is widely viewed as the most effective way to conserve endangered species, with more than 1,000 successful eradications

recorded worldwide. The conservation statuses of 11 bird, five mammal, and one amphibian globally threatened species have improved as direct results of such programmes (“Global indicators of biologi-cal invasion: species numbers, biodiversity impact and policy responses”, Diversity and Distributions, McGeoch et al., 2010).

This is one of the greatest environmen-tal challenges of modern times, and one

Addressing the Invasion Debt

There are various ways a species can cause harm in its new environment, there-fore being invasive rather than simply non-native. The EEA reports identify 14 types of Invasive Alien Species impacts and classify them into 4 groups:

providing habitats for migratory species and gene pool viability maintenance;

Cultural services: recreational, religious, spiritual and intellectual enrichment, and other non-material benefits gained from eco-systems.

3. Impacts on Human Health

Invasive alien species which have negative effects on eco-systems, in turn have negative effects on human well-being through the disruption of these services. Human health can be affected either directly or as vectors of specific diseases. Such problems include skin lesions upon contact with giant hogweed sap, rhino-conjunctivi-tis and asthma through contact with common ragweed allergenic pollen, and the chikungunya virus spread by the tiger mosquito.

4. Impacts on Economic Activities

Invasive alien species can cause dam-age to infrastructure, landscapes and agriculture. In Australia, Brazil, India, South Africa, the United Kingdom and the United States, related losses have been calculated as approximately $300 billion per year (‘Update on the environmental and economic costs associated with alien-invasive species in the United States’, Ecological Eco-nomics Pimentel et al., 2005). This is probably an underestimation, as socio-economic consequences are difficult

1. Impacts on Biodiversity

Invasive alien species can affect bio-logical diversity at gene, species and eco-system levels.

Competition, predation, hybridization and disease transmission are common and can endanger native species. In isolated eco-systems this is known to affect all levels of local food webs.

2. Impacts on Eco-system Services

Eco-system services are direct and indirect contributions of eco-systems to human well-being, and are classi-fied in four sub-categories:

Provisioning services: products obtained from ecosystems such as water, food, genetic resources, wood, fiber and medicines;

Regulating services: beneficial regulatory effects of ecosystem processes such as climate stability, natural hazard regulation (flood control), water purification, waste management, pollination, and pest control;

Supporting (habitat) services: soil formation and nutrient cycling,

to quantify in financial terms, and eco-nomic and environmental impacts are unknown for many alien species (‘How well do we understand the impacts of alien species on ecosystem services? A pan-European cross-taxa assess-ment’, Frontiers in Ecology and the Environment, Vilà et al., 2010).

Source : Sarah / Flickr

• Asian Carp

• Rabbits

• Cane Toads

• Kudzu

• Gray Squirrel

• Killer Bees

• Starlings

• Northern Snakehead

• Zebra Mussels

• Burmese PythonTop

10 In

vasi

ve S

peci

es

Sour

ce : T

IME

Mag

azin

e

16

The invasive 'Killer' Shrimp were discovered in UK waters for the first time in 2010. They kill a range of native species such as shrimp, young fish and insect larvae, often leaving them uneaten.

Source: Lancanshire Invasive Species Project

Burmese Pythons have thrived and multiplied, particularly in the Everglades of the Southern Unites States, posing a potential threat to humans and feeding on native endangered species, such as Key Largo wood rats, round-tailed muskrats and even alligators.

Source: Ted / Flickr

Native to drainage basins of the Aral, Black and Caspian Seas, the Zebra Mussel (Dreissena Polymorpha) was introduced to Europe and America in the 19th and 20th centuries.

They can filter up to a liter of water per day to eat the plankton. They also form colonies inside pipes clogging them. Zebra mussels cannot be controlled in the wild as the chemicals used

to kill the larva would affect fish and native mussels. The spread of zebra mussels can only be prevented by draining all of the water from boats, live wells and bait wells.

Source: Wisconsin Department of Natural Resources / Flickr

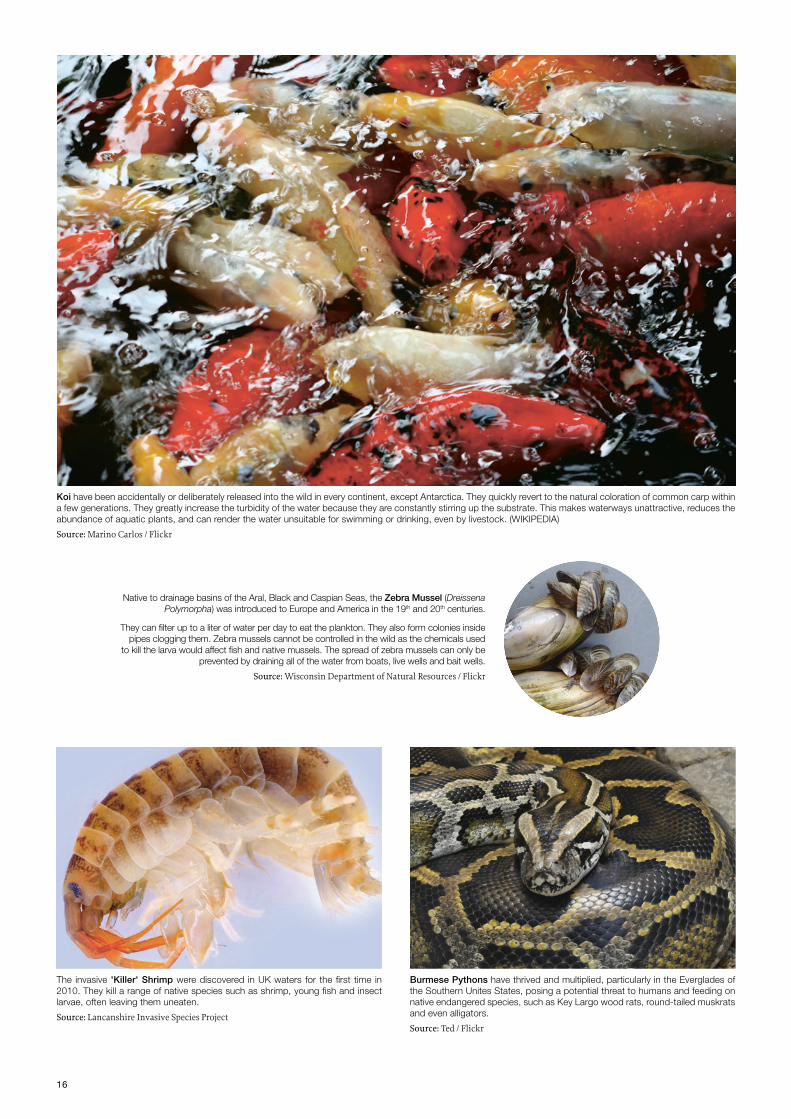

Koi have been accidentally or deliberately released into the wild in every continent, except Antarctica. They quickly revert to the natural coloration of common carp within a few generations. They greatly increase the turbidity of the water because they are constantly stirring up the substrate. This makes waterways unattractive, reduces the abundance of aquatic plants, and can render the water unsuitable for swimming or drinking, even by livestock. (WIKIPEDIA)

Source: Marino Carlos / Flickr

17

which various agencies and authorities are now addressing. In the publication “Our life insurance, our natural capital: an EU bio-diversity strategy to 2020”, the European Commission aims:

By 2020, Invasive Alien Species (IAS) and their pathways are identified and prioritised, priority species are controlled or eradicated, and pathways are managed to prevent the introduction and establishment of new IAS.

The EEA has contributed extensively to work in this field, including the technical report “Towards an early warning and information system for invasive alien species threaten-ing biodiversity in Europe”, which assesses the options for a European early warning system, identifying key challenges and pre-senting estimated costs.

Due to the multiple shared borders, moun-tain ranges and water courses in Europe, invasive alien species are easily spread between countries. This makes a harmo-nized pan-European strategy, necessitating legislative frameworks at both regional and local levels, vital to effectively manage them.

Globalization and international trade are also major contributors to the movement of species and are therefore important fac-tors in invasive alien species control. Many species are intentionally moved and traded internationally and other species are trans-ferred accidentally as a consequence of such trade. The EEA reports state that 90% of world trade is carried by sea and by 2018, the world fleet could increase by nearly 25% with volumes nearly doubling compared to 2008. In addition, approximately 650 million people travel internationally every year. Both greatly increase the risk of unintentional species transfers. These conditions need improved coordination between national authorities, including reinforced controls at airports, harbors and other entry points, with resources such as scanners and sniffer dogs, targeted training, and powers of con-signment seizure and destruction.

In their 2011 paper “Socioeconomic legacy yields an invasion debt”, Essl et al. coined the term “invasion debt”, highlighting that current patterns and impacts of alien spe-cies reflect past activities and migrations

rather than current patterns. Many of the most damaging alien species invaded their new habitats many years ago. It will there-fore be impossible to judge the effects of current activities until decades in the future.

The boom in biofuels correlates invasive alien species and climate change. In the fight against climate change, fossil fuels are increasingly being replaced by biofuels. The 2009 EU Renewable Energy Directive (RED) endorses a mandatory 10% minimum target for the share of biofuels used in transportation by 2020. Biofuel crops may provide opportunities for alien species to invade new territories, as they are planted on large scales and are usually fast growing and highly competitive species. Apart from deforestation and land change brought about for their production, there is a high risk of such crop species spreading outside their official production areas. This means carrying out risk assessments before selecting biofuel species for specific areas.

Climate change is an environmental phenomenon with varied effects, includ-ing changing which species are able and

unable to thrive in specific areas. Native species which fail to adapt to the new envi-ronmental conditions of their native territory are likely to die out and be replaced by bet-ter adapted alien species. Climate change is also expected to affect the distribution and impacts of existing invasive alien species. Many are highly adaptable and are likely to cope better than native species, increasing the likelihood of their dominance. Natural disasters such as floods and fires which destroy or displace native species may also allow new species to replace them.

One problem in dealing with this issue is the lack of globally accepted, reliable indicators of biological invasions. The EEA project, “Streamlining European 2010 Biodiversity

Indicators” assesses progress towards halting the loss of biodiversity in Europe by 2010. A response indicator measuring the “Trends in invasive alien species in Europe” was developed as part of this process, and consisted of two elements:

1. Cumulative number of alien species in Europe since 1900

2. Worst invasive alien species threatening biodiversity in Europe

This indicator is considered to be effective, but needs further improvement. A lack of consensus about the definition of invasive species, the lack of reliable data about both native and invasive species, and the vari-ety of species involved and the problems they cause all make establishing reliable indicators difficult. Many projects continue to work on this issue and much more work remains to be done.

It will therefore be impossible to judge the effects of current activities until decades in the future.

18

CHILE’S RED GOLDExploiting the Atacama DesertWriter / Photographer: Michela Pfeifer is an independent contributor to Revolve. She travelled across Chile between January and April 2013.

Driving north on the Panamericana highway from Santiago to the Atacama Desert, the incredible amount of mining sites attests to the major role the industry plays in Chile. Talking to Chileans, literally everyone seems to have relatives or friends working in one of the mines; if not presently, then from previous generations. While mining in Chile is equated with many positive superlatives as a success story, it does not apply to everyone. Copper and lithium have brought enormous wealth, but Chile’s dependence on mineral exports could now be refered to as the “Chilean Disease”. The effects of mining permeate Chile’s society, economy and politics with grave consequences for the environment.

Chile is only 177 kilometers wide on average and has a coastline of 6,435 km. Bordering Bolivia and Peru in the north, and Argentina all along the eastern natural border of the Andes mountain range, 80% of Chile is mountains, counting over 600 volcanos. Only about 3% of the land in Chile is arable. Along this long strip of territory, the Atacama Desert occupies most of the north and does not receive any rain at all, while the south is one of the most rainiest areas of the world.

19

The 1990s marked the beginning of a boom in Chile’s copper mining industry. Accord-ing to the Organization for Economic Coop-eration and Development (OECD), mining comprised 19% of Chile’s GDP in 2010. The primary mining regions include the northern Atacama Desert and the Andean Cordillera. Copper and sub-products of copper production such as molybdenum – a metal used in arms and tools production – are by far the most important products, but Chile is also mining big quantities of gold, silver and non-metal products such as salpetre (potassium nitrate) and, more recently, lithium (used in batteries).

Chile is the biggest copper producer in the world with an output of 16 million tons in

2011, representing over 1/3 of global pro-duction. Despite going down from the 75% peak of Chile’s foreign trade in 1990, cop-per still comprises nearly 60% of Chile’s exports. Around 40% of the world’s known copper reserves are located in Chile.

Copper production really started after World War I, when the Chilean salpetre market collapsed. Salpetre was used for fertilizers and explosives. The collapse was due to sci-entific progress and the artificial production of the mineral. Demand for natural salpetre crashed while demand for copper rose with the emergence of the electric industry. With the price of copper nearly back to record highs after a crash in 2008, Chile’s future looks bright, at first glance...

In northern Chile, the state-owned Chuqui-camata – or “Chuqui“ according to Chil-eans – is the world’s largest open-pit copper mine. “La Escondida”, a privately-owned mine, is the world’s biggest for cur-rent production. And with 2,400 kilometers of underground galeries, “El Teniente” near Santiago, is the biggest sub-terranean cop-per mine. Chuqui and El Teniente are the oldest mines in operation, since 1910 and 1905 respectively, and are advertised by the largest copper producer, “Corporación Nacional del Cobre de Chile” (CODELCO), as the “Orgullo de todos” – the pride of the nation. CODELCO is entirely state-owned and the world’s biggest copper mining operation. It has 20,000 employees pro-ducing 10% of global copper.

20

distributing any compensation. In a speech at the United Nations in 1972, he justified Chile’s action by estimating the profit com-panies had made during their exploitation – 3 years later he was deposed in a military coup.

General Pinochet came to power and insti-tuted free market reform (turning Chile into a laboratory of neo-liberal teachings after the Chicago Boys). Paradoxically, he did not re-privatize the mines. Instead, he merged them into the single state-owned company, later known as CODELCO, and decreed that 10% of the mines’ annual turnover would

be allocated to the country’s armed forces. In 1982, Pinochet re-opened the copper market to foreign investors.

Chile’s copper market was divided into pub-lic and private sectors until the early 1990s, but CODELCO’s production has been very stagnant since and private output has over-taken and actually doubled. Eager to collect tax revenues, the state-owned company has neglected investments to balance climbing production costs, making it difficult to com-pete with the private sector.

To revive CODELCO, a series of reforms have been proposed, including the expan-

Chile’s copper market was nationalized in the late 1960s. With the rise and fall of salpetre mining, Chilean leaders realized that they needed to make better use of their natural wealth to benefit national develop-ment. Most extracting companies were for-eign and the wealth generated from Chilean minerals was leaving the country while for-eign companies paid modest royalties.

In 1970, Salvador Allende was elected president of Chile. As part of his program of socialist reform, he nationalized the U.S.-owned copper mines in the country – without

Chile’s Copper Market

21

sion of El Teniente and additional under-ground pit exploitation of Chuqui so far, open ground only, in order to reduce energy costs. Overhead expenses have become an increasing concern to mining companies striving to find cheaper alternative sources of energy to maintain extraction levels for consumption and trade.

A potential listing of CODELCO on the stock market suggested by Chile’s president, Sebastián Piñera, would solve many of the company’s current debt problems. However, most analysts estimate that the company which owns an enormous 1⁄3 of Chile’s cop-per reserves could double its debt burden.

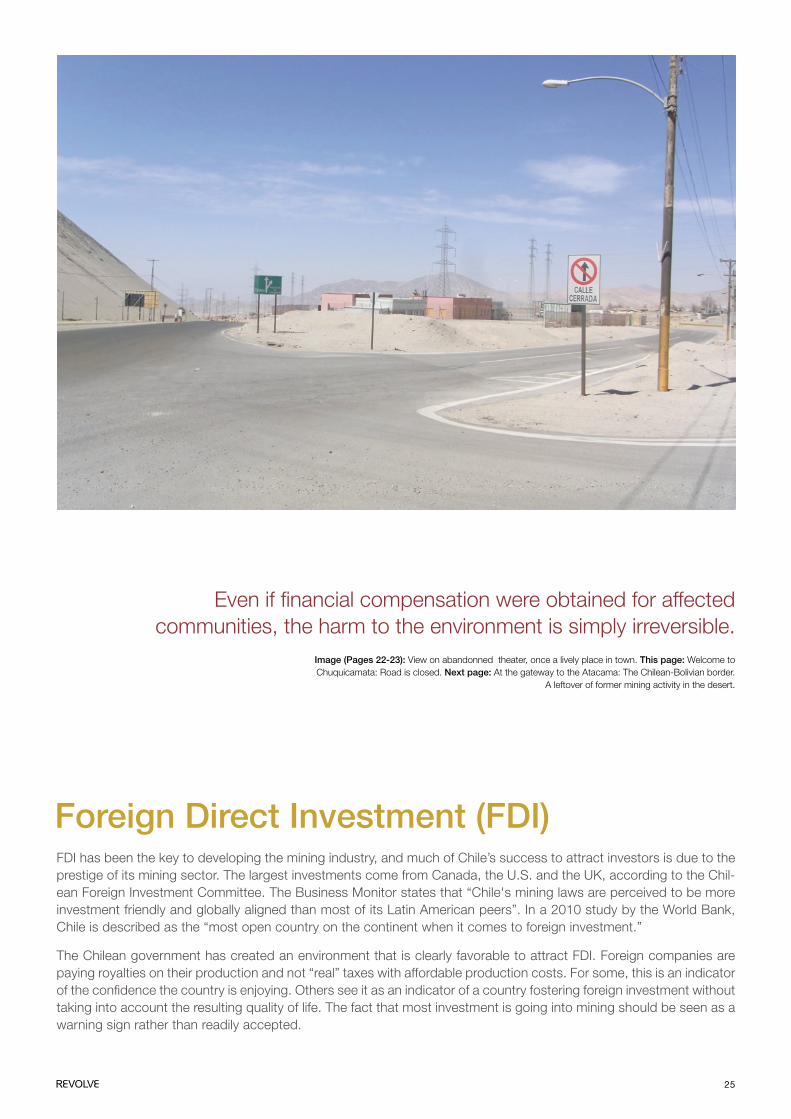

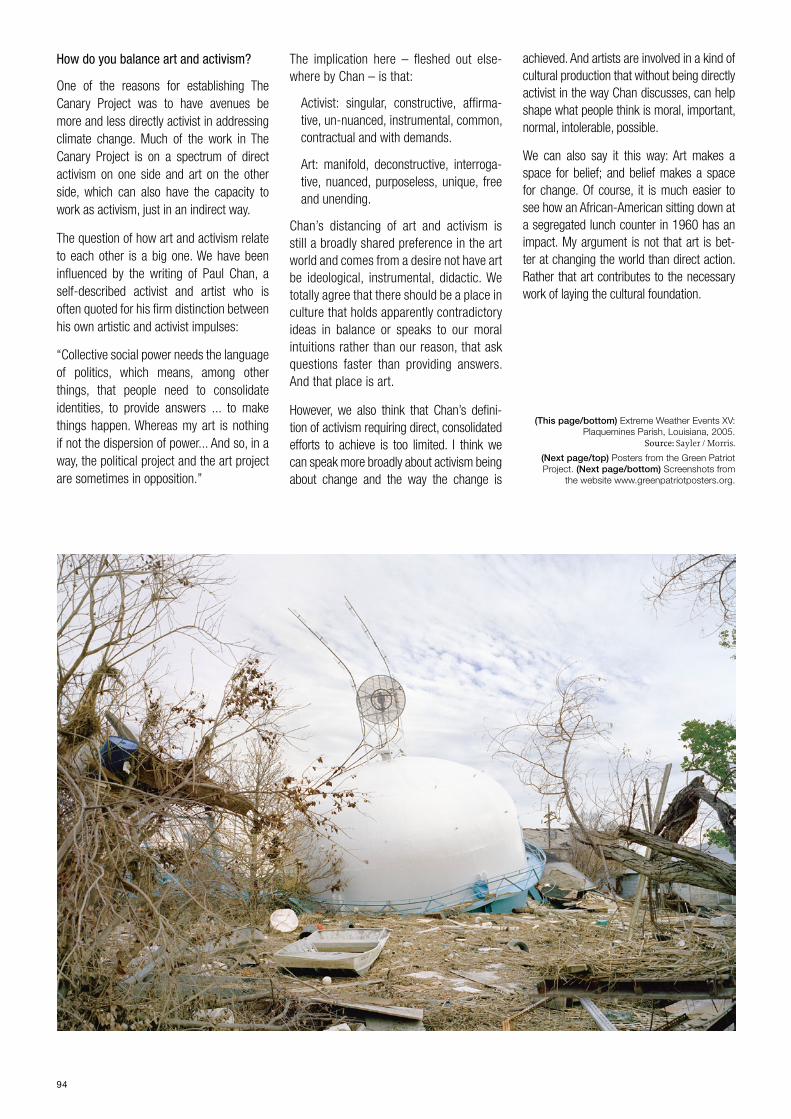

Image (Pages 18-19): “Keep out!” – Huge empty areas in Chuquicamata are blocked off separately from the fence that surrounds the whole town. Often, toxic waste has come too close. This page (left): “Vamos

Chuqui”. Empty single appartments for miners. This page (top): CODELCO advertising for its “Fatalidad Cero” policy, the company’s motto. Safety at work is one of CODELCO’s priorities.

In his famous “Motorcycle Diaries”, Che Guevara recounts the plight of unem-ployed migrant workers at the Chuqui mine – and one can only wonder what he would think today if he saw this massive hole: over 4 km long, 3 km wide, and up to 850 meters deep. With a surface area of 8 km!, it would take over an hour to cross on foot.

In 2011, Chuqui produced 700,000 tons of copper, comprising " of the world’s copper and # of its molib-denum production, repre-senting 20% of CODELCO’s total income. The first tests for CODELCO’s “Chuquica-mata Subterranea” projects are underway. The new mine should be in operation by 2018 and enable the company to reduce by half its energy con-sumption and still keep the same high levels of production. Source: James Byrum / Flickr

The Biggest Hole on Earth

Chile is the biggest copper producer in the world.

22

The fate of mining towns is usually the same: they rise and fall with their adjacent mines, and usually have no other employ-ment opportunities or economic prospects. The high income differences between CODELCO workers and those otherwise employed led to social differences. Accord-ing to CODELCO, an average 70% of the mining staff are subcontractors, who do not enjoy CODELCO privileges salaries.

When the mines close, the towns empty. The Atacama Desert is dotted with ghost towns, a legacy of the salpetre rush in Chile. A contemporary example of the fate of such a mining town is Chuqui next to Chuquica-

mata mine. For over 100 years, it was home to the miners and their families. But it has become so polluted that under the new environmental standards it has become unsafe for people to live there. Chuqui is a ghost town, fenced with barbed wire; it will be buried under a giant slag heap and with it a century of history.

In 2003, thousands of its inhabitants relocated to Calama, 17 km away, where CODELCO has built houses for its workers, but the numerous subcontractors have been less fortunate. They did not receive any of the generous compensations that CODELCO paid its staff for leaving their homes.

Dirty Old Town

Cleaning up the Waste?In copper production, only 1% of the rock is actually copper; the other 99% is considered waste. As a result, huge piles of toxic waste accumulate. In Chuquicamata, the amount of such rock waste occupies a surface of 50 km2. About half of this waste is toxic due to chemicals used for the extraction of copper as well as the toxic acids created through oxygen reacting in the piled up rock, polluting the soil and water, despite the depth of ground water in the Atacama Desert. The heavy water usage in mining has devastating consequences on local water resources.

Chile is the biggest copper producer in the world with an output of 16 million

tons in 2011, representing over 1⁄3 of global production

23

24

While other countries in South America, notably Bolivarian Alliance for the Ameri-cas (ALBA) members Cuba, Venezuela and Bolivia, are following more protectionist policies to manage their resources, Chile – despite the importance of its state-owned mining industry – is forming part of another alliance that has surged on the continent.

Together with Colombia, Mexico, Peru and Brazil, Chile is becoming increasingly dedicated to free trade and economic integration as part of the creation of a “Pacific Alliance” – a strategy following the policies of the World Bank and similar organizations, such as the Inter-American Development Bank, which stated in its Country Strategy Chile 2011-2014 report: “The country’s main challenge consists in boosting overall economic production and diversifying its exports to meet OECD

industry in Chile to the next level.” (The Santiago Times, 26 January 2013.)

The EU’s strategy on resources is based on the 2008 “EU Raw Materials Initiative” aimed at ensuring the EU’s “access to raw materials on global markets through Raw Materials Diplomacy and strategic part-nerships”. Not surprisingly, Chile has been identified as one of the target countries, but the initiative has been heavily criticized in the NGO world. As a rebuttal, the European Commission explains quite clearly its inten-tions: “as global raw material markets are increasingly distorted by protectionist trade policies, maintaining fair and undistorted access to these materials for EU industry and citizens is increasingly difficult. Within the EU, exploration and extraction have to face increased competition for different land uses and a highly regulated environment.”

standards, encouraging the country to facilitate trade and make better use of free trade agreements.” Chile is now part of the OECD, the club of the richest countries, regardless of the fact that it remains below basic development indicators. The World Bank and other international organizations play a crucial role in promoting private sector investment in Chile.

In January 2013, Chile’s capital, Santiago, hosted the summit of the “CELAC-EU”, an inter-governmental assembly bringing together the heads of states and govern-ments of EU countries and their Latin American and Carribean counterparts with the outcome of a new cooperation agree-ment, notably in mining and technology transfer, signed with Germany and Finland, amongst others. Germany’s Chancellor, Angela Merkel, hopes to “take the mining

Developing Trade

The air quality of Chuquicamata has been regulated since 1991, after the installation of a surveillance system a few years ear-lier. A depollution plan helped decrease by 70% the emissions of sulfur dioxide (SO2), according to the OECD.

In 2009, Calama’s air quality was found to be saturated by “material with breathable particles”. According to the newspaper El Mercurio de Calama, 90% of the pollution in Calama is of mining origin. Nonethe-less, efforts undertaken by CODELCO are notable. They announced in their 2011 Sus-tainability Report that they re-entered the International Council on Mining and Metals (ICMM), a “quality certificate” for companies that are leading in sustainability and high standards of production.

A first wave of anti-pollution measures in Chile was implemented in the early 1990s. Now, Chile is entering a different era with the cre-

Foreign investment projects have to undergo assessment tests, but only very rarely is a mining project refused due to environment concerns. Between 2005 and 2012, only 39 out of over 620 min-ing projects evaluated by the “Servicio de Evaluación Ambiental” were rejected. Chile provides an entire system of legal recourse for foreign companies, if they can prove a breach in one of the numer-ous free trade agreements the country has signed. The system is built in a manner that evaluates impacts gradually, making the total impact of the initiatives often not visible. While in the Pascua Lama case, environmentalists were concentrating on saving the glaciers, a series of other proj-ects were approved.

ation of new environmental tribunals. They will be authorized to take away permits previously granted, rather than only fining companies for damages. Initially, implementation was tar-geted for the end of 2012, but only one of the three tribunals is functional since March 2013.

Even if financial compensation were obtained for affected communities, the harm to the environment is irreversible. The case of Pascua Lama, a highly controversial gold mining project in the southern Atacama, owned by Barrick Gold Corporation, a Cana-dian mining giant, highlights the ineptitude of even the most elaborate environmental protection legislation. The project is not yet entirely approved by the state. It passed the environmental impact assessment even with the removal of 20 hectares of ice to gain access to gold deposits. The company further suggested moving three glaciers to another location – after the impact assess-ment tests were made.

Protecting the Environment

25

Even if financial compensation were obtained for affected communities, the harm to the environment is simply irreversible.

Foreign Direct Investment (FDI)FDI has been the key to developing the mining industry, and much of Chile’s success to attract investors is due to the prestige of its mining sector. The largest investments come from Canada, the U.S. and the UK, according to the Chil-ean Foreign Investment Committee. The Business Monitor states that “Chile's mining laws are perceived to be more investment friendly and globally aligned than most of its Latin American peers”. In a 2010 study by the World Bank, Chile is described as the “most open country on the continent when it comes to foreign investment.”

The Chilean government has created an environment that is clearly favorable to attract FDI. Foreign companies are paying royalties on their production and not “real” taxes with affordable production costs. For some, this is an indicator of the confidence the country is enjoying. Others see it as an indicator of a country fostering foreign investment without taking into account the resulting quality of life. The fact that most investment is going into mining should be seen as a warning sign rather than readily accepted.

Image (Pages 22-23): View on abandonned theater, once a lively place in town. This page: Welcome to Chuquicamata: Road is closed. Next page: At the gateway to the Atacama: The Chilean-Bolivian border.

A leftover of former mining activity in the desert.

26

In Chile, environmental protection is based on a system that regulates air quality instead of emissions. Decontamination plans are employed once air pollution is too high; companies’ environment protection budgets are dedicated essentially to air purification. It would render companies more respon-sible to introduce uniform emission norms for all state-owned and foreign companies.

Due to the particularity of the Chilean cop-per market, such a system has been omit-ted so far, as most of the emissions were caused by a small number of state-owned mining companies. While in 1990, 77% of the total Chilean copper production was still provided by state-owned mines, today it is a mere third. Times have changed as has the country’s copper market and pollution has grown with production. A general reform of the copper market structure and the system of royalties would be useful.

able and economic development with their social and environmental needs. Real equality within Chilean society will need to include respect for the Mapuches, Chile’s last indigenous people. If Chile does not want to witness another “eco-cide” of a civilization, then they must consider the viability of their eco-system. In the early first millennium, the “Rapa Nui”, a Polyne-sian people, colonized the Chilean Easter Island. Their civilization was eclipsed after nearly 900 years due to over-population which destroyed their eco-system through deforestation and over-exploitation of natural resources.

While all minerals found in Chilean soil are property of the state, companies can exploit resources by paying licences. A system based on real gains would bring enormous gains to the state given the high copper prices through the last decade. Several attempts to change this system of royalties for a more realistic taxation system were aborted by the Congress; the law remains unchanged since 1983.

Rather than financing the army with a 10% CODELCO-tax, the Chilean govern-ment should invest in its desolate educa-tion system. Chile spends most of its bud-get on defence and permits universities to make profits, resulting in education for the privileged.

Trends in Chile now show that non-mining exports such as wood, seafood, fruit and wine are increasing. As with so many countries, Chile must balance sustain-

A Sustainable Future?

28

HEAT PUMPSRenewable by Nature, Sustainable for Europe

29

Heat pumps are usually overlooked as a technology that uses renewable energy because they operate in the dark. Hidden in basements, on roofs or in machine rooms, they do in fact use renewable energy from air, water and ground. This makes the technology an essential element of the energy transition, particularly in cities due to its ability to provide greater efficiency as well as to connect electricity and thermal energy grids.

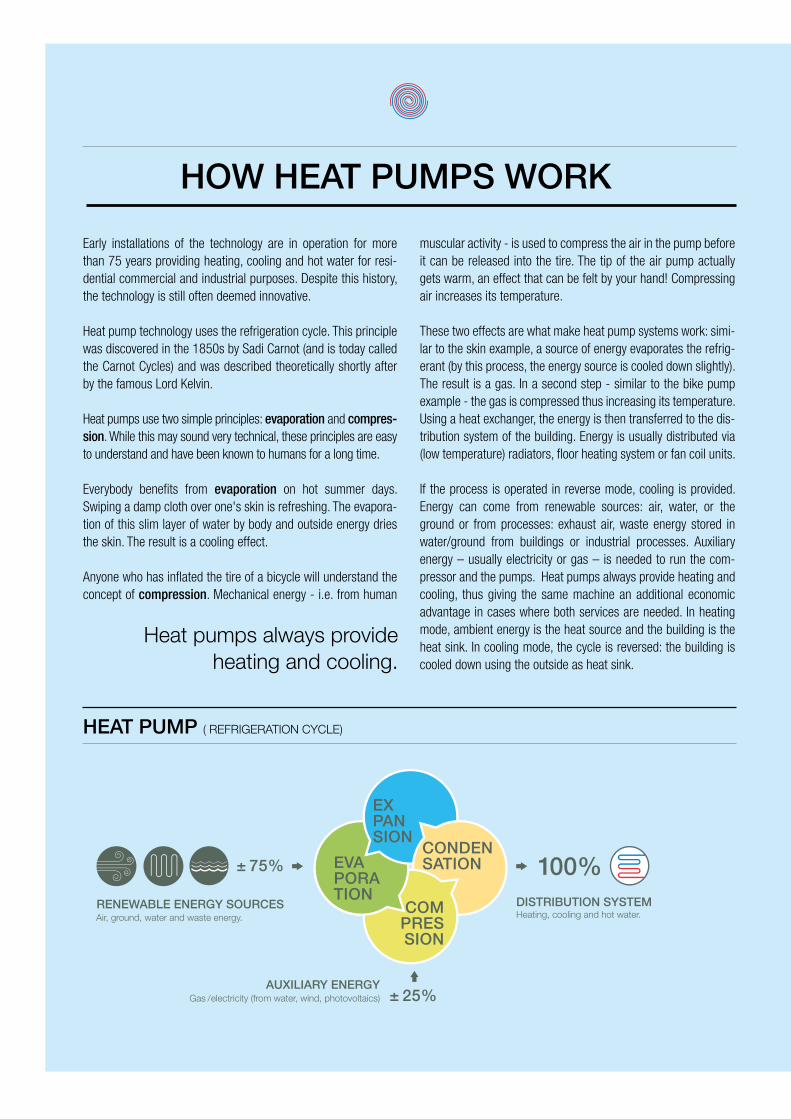

HOW HEAT PUMPS WORK

HEAT PUMP ( REFRIGERATION CYCLE)

Early installations of the technology are in operation for more than 75 years providing heating, cooling and hot water for resi-dential commercial and industrial purposes. Despite this history, the technology is still often deemed innovative.

Heat pump technology uses the refrigeration cycle. This principle was discovered in the 1850s by Sadi Carnot (and is today called the Carnot Cycles) and was described theoretically shortly after by the famous Lord Kelvin.

Heat pumps use two simple principles: evaporation and compres-sion. While this may sound very technical, these principles are easy to understand and have been known to humans for a long time.

Everybody benefits from evaporation on hot summer days. Swiping a damp cloth over one's skin is refreshing. The evapora-tion of this slim layer of water by body and outside energy dries the skin. The result is a cooling effect.

Anyone who has inflated the tire of a bicycle will understand the concept of compression. Mechanical energy - i.e. from human

muscular activity - is used to compress the air in the pump before it can be released into the tire. The tip of the air pump actually gets warm, an effect that can be felt by your hand! Compressing air increases its temperature.

These two effects are what make heat pump systems work: simi-lar to the skin example, a source of energy evaporates the refrig-erant (by this process, the energy source is cooled down slightly). The result is a gas. In a second step - similar to the bike pump example - the gas is compressed thus increasing its temperature. Using a heat exchanger, the energy is then transferred to the dis-tribution system of the building. Energy is usually distributed via (low temperature) radiators, floor heating system or fan coil units.

If the process is operated in reverse mode, cooling is provided. Energy can come from renewable sources: air, water, or the ground or from processes: exhaust air, waste energy stored in water/ground from buildings or industrial processes. Auxiliary energy – usually electricity or gas – is needed to run the com-pressor and the pumps. Heat pumps always provide heating and cooling, thus giving the same machine an additional economic advantage in cases where both services are needed. In heating mode, ambient energy is the heat source and the building is the heat sink. In cooling mode, the cycle is reversed: the building is cooled down using the outside as heat sink.

Heat pumps always provide heating and cooling.

Air, ground, water and waste energy.

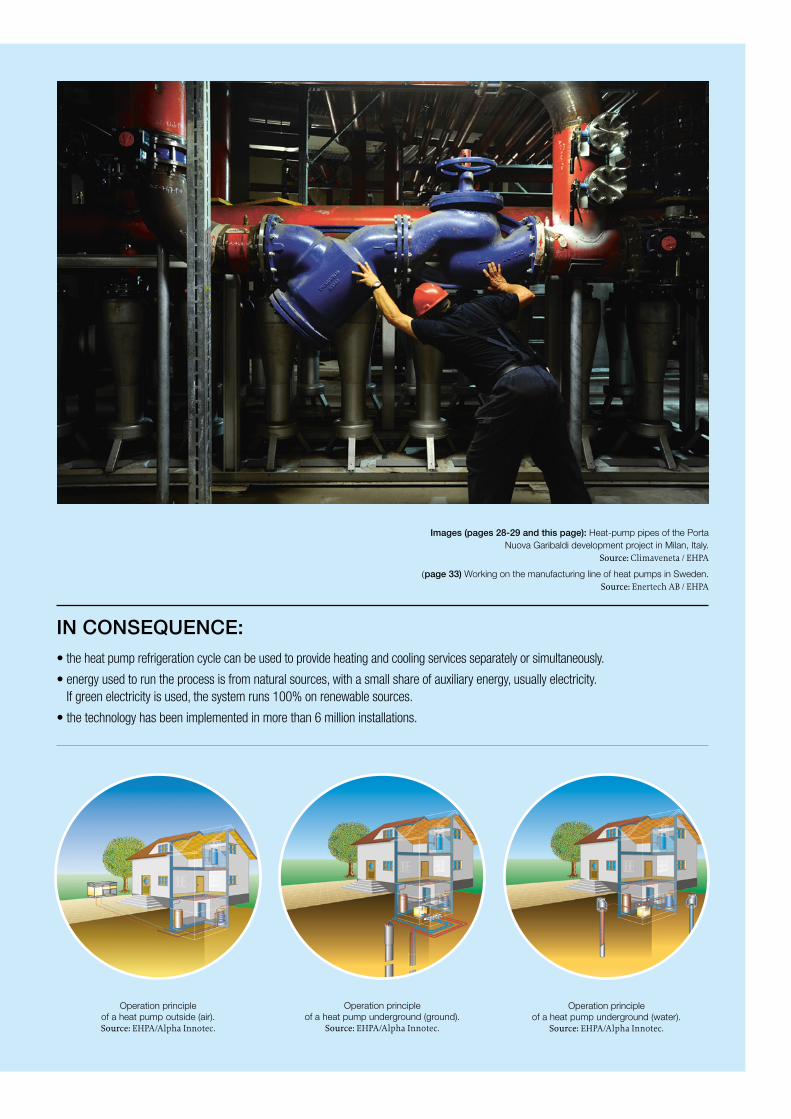

Operation principle of a heat pump outside (air). Source: EHPA/Alpha Innotec.

Operation principle of a heat pump underground (ground).

Source: EHPA/Alpha Innotec.

Operation principle of a heat pump underground (water).

Source: EHPA/Alpha Innotec.

IN CONSEQUENCE: • the heat pump refrigeration cycle can be used to provide heating and cooling services separately or simultaneously.

• energy used to run the process is from natural sources, with a small share of auxiliary energy, usually electricity. If green electricity is used, the system runs 100% on renewable sources.

• the technology has been implemented in more than 6 million installations.

Images (pages 28-29 and this page): Heat-pump pipes of the Porta Nuova Garibaldi development project in Milan, Italy.

Source: Climaveneta / EHPA

(page 33) Working on the manufacturing line of heat pumps in Sweden. Source: Enertech AB / EHPA

32

Heat Pumps Technology Potential

Sustainable for Europe

Heat pump units can individually provide heating alone, or heating and cooling, as well as hot water. Combined units can pro-vide a comination of these three. The heat pump market is usually divided in 6 seg-ments (single family and multi-family resi-dential buildings and industrial applications are further distinguished between new and existing buildings) which have reached dif-ferent stages of development.

The heat pump industry is local to Europe. Most manufacturers originate and set-up shop in Europe. The manufacturing of parts, components and systems has spread from Spain to Sweden and from France to Poland. Research and development is executed by companies, institutes and universities. Heat pump know-how is European know-how and European manufacturers are market leaders in many segments, even on the world level.

Heat pump technology is easiest to employ in new buildings which are optimal for effi-cient heat pump operation. The application potential in new buildings is nearly 100% and it is these buildings where the technol-ogy has reached the largest market pene-tration. By now, heat pumps are a standard in new residential buildings and they are increasingly used in industrial applications. Applying heat pumps in renovated buildings

is a bigger challenge: simply replacing gas boilers with a heat pump, for example, will most likely result in a sub-optimal system. The energetic optimization of the building envelope is necessary to overcome this lim-itation. Technological developments in heat pumps aim to provide output temperatures of 65-90°C to enlarge the possible field of efficient applications. In industrial applica-tions, the aim is to reach 200°C.

Installing heating and cooling systems is done by local installers. Using heat pumps contributes to energy efficiency. It reduces energy demand, in particular demand for non-renewable, fossil sources and shifts money flows from paying for energy imports to other means. Local purchas-ing power is increased. Supporting heat pumps means supporting local infrastruc-ture and employment.

With Europe's shift of energy supply to renewable sources in full swing, a specific challenge occurs in integrating surplus electricity in the grid and in bal-ancing supply and demand. Heat pumps provide a tremendous storage potential to this challenge. In Germany for example, the storage potential of heat pump sys-tems surpasses available pumped hydro!

HE

AT P

UM

PS

TRIP

LE D

IVID

EN

D supply security

local investment and local labor

maintain know how

balance supply and demand in smart grids

use renewable energy from air, water and the ground

reduce final and primary energy demand

reduce greenhouse gas (GHG) emissions 3

2

1

Renewable by NatureHeat pumps can use energy from the air, water and ground. The origin of this energy can either be from natural sources or waste energy. In the first case, energy stored in the air or in bodies of water is the result of solar irradiation; energy stored in the ground is a mix of energy from solar irradiation, rainwa-ter and geothermal energy. If air, water or ground are used to discharge energy from cooling or from industrial processes, this energy can be re-used by heat pumps and thus increases the efficiency of any process.

The debate over whether or not heat pumps actually use renewable energy is over; it ended when the European Union passed its legislation encouraging the use of renewable energy sources (RES) in 2009 (2009/28/EC). The RES Direc-tive's article two defines which sources of energy are deemed renewable. It includes aerothermal (energy stored in air), hydrothermal (energy stored in water) and geothermal (energy stored below the earth’s crust). The Directive

explicitly recognizes heat pump technol-ogy as necessary to make use of these renewable sources.

This recognition is the basis for all other legislation affecting heat pumps and it certainly influences perceptions in the market place, where the benefits and possible contribution of heat pumps to overall energy demand in the heating and cooling sector is still underestimated or often overlooked.

33

36

20%

30%

40%

50%

60%

70%

80%

Primary Energy Savings

Final Energy Savings

RES Contribution

GHG Savings20-49%

67-79%

65-78%

49-68%

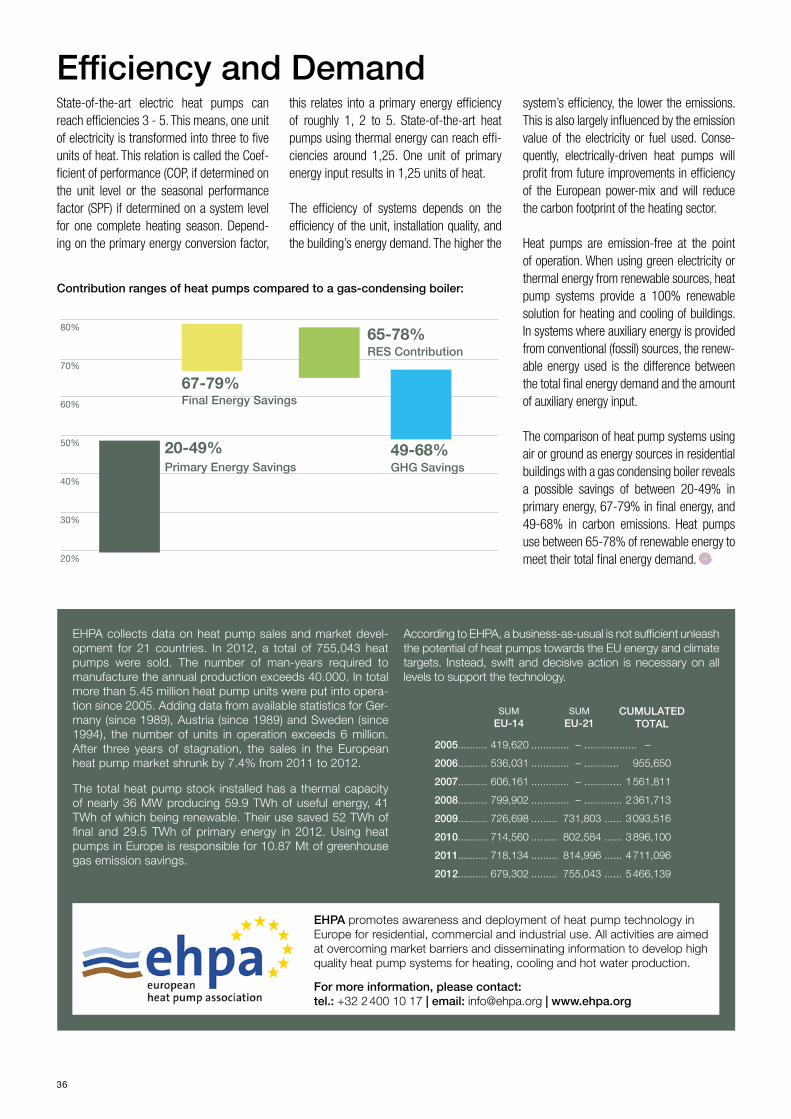

Efficiency and DemandState-of-the-art electric heat pumps can reach efficiencies 3 - 5. This means, one unit of electricity is transformed into three to five units of heat. This relation is called the Coef-ficient of performance (COP, if determined on the unit level or the seasonal performance factor (SPF) if determined on a system level for one complete heating season. Depend-ing on the primary energy conversion factor,

this relates into a primary energy efficiency of roughly 1, 2 to 5. State-of-the-art heat pumps using thermal energy can reach effi-ciencies around 1,25. One unit of primary energy input results in 1,25 units of heat.

The efficiency of systems depends on the efficiency of the unit, installation quality, and the building’s energy demand. The higher the

system’s efficiency, the lower the emissions. This is also largely influenced by the emission value of the electricity or fuel used. Conse-quently, electrically-driven heat pumps will profit from future improvements in efficiency of the European power-mix and will reduce the carbon footprint of the heating sector.

Heat pumps are emission-free at the point of operation. When using green electricity or thermal energy from renewable sources, heat pump systems provide a 100% renewable solution for heating and cooling of buildings. In systems where auxiliary energy is provided from conventional (fossil) sources, the renew-able energy used is the difference between the total final energy demand and the amount of auxiliary energy input.

The comparison of heat pump systems using air or ground as energy sources in residential buildings with a gas condensing boiler reveals a possible savings of between 20-49% in primary energy, 67-79% in final energy, and 49-68% in carbon emissions. Heat pumps use between 65-78% of renewable energy to meet their total final energy demand.

EHPA promotes awareness and deployment of heat pump technology in Europe for residential, commercial and industrial use. All activities are aimed at overcoming market barriers and disseminating information to develop high quality heat pump systems for heating, cooling and hot water production.

For more information, please contact:tel.: +32 2 400 10 17 | email: [email protected] | www.ehpa.org

EHPA collects data on heat pump sales and market devel-opment for 21 countries. In 2012, a total of 755,043 heat pumps were sold. The number of man-years required to manufacture the annual production exceeds 40.000. In total more than 5.45 million heat pump units were put into opera-tion since 2005. Adding data from available statistics for Ger-many (since 1989), Austria (since 1989) and Sweden (since 1994), the number of units in operation exceeds 6 million. After three years of stagnation, the sales in the European heat pump market shrunk by 7.4% from 2011 to 2012.

The total heat pump stock installed has a thermal capacity of nearly 36 MW producing 59.9 TWh of useful energy, 41 TWh of which being renewable. Their use saved 52 TWh of final and 29.5 TWh of primary energy in 2012. Using heat pumps in Europe is responsible for 10.87 Mt of greenhouse gas emission savings.

According to EHPA, a business-as-usual is not sufficient unleash the potential of heat pumps towards the EU energy and climate targets. Instead, swift and decisive action is necessary on all levels to support the technology.

Contribution ranges of heat pumps compared to a gas-condensing boiler:

SUM

EU-14SUM

EU-21CUMULATED

TOTAL

2005.......... 419,620 ............. – .................. –

2006.......... 536,031 ............. – ............ 955,650

2007.......... 606,161 ............. – ............. 1 561,811

2008.......... 799,902 ............. – ............. 2 361,713

2009.......... 726,698 ......... 731,803 ...... 3 093,516

2010.......... 714,560 ......... 802,584 ...... 3 896,100

2011.......... 718,134 ......... 814,996 ...... 4 711,096

2012.......... 679,302 ......... 755,043 ...... 5 466,139

Emerson Climate Technologies – European Headquarters – Pascalstrasse 65 – 52076 Aachen, GermanyWeb: www.emersonclimate.eu – Tel. +49 (0) 2408 929 0The Emerson Climate Technologies logo is a trademark and service mark of Emerson Electric Co. Emerson Climate Technologies Inc. is a subsidiary of Emerson Electric Co. Copeland is a registered trademark and Copeland Scroll is a trademark of Emerson Climate Technologies Inc.

E M E R S O N . C O N S I D E R I T S O L V E D ™.

The heating market needs a solution which adapts the amount of heat generated to the heat load, yet remains highly efficient. Emerson’s ZHW Copeland Scroll™ Variable Speed compressors adapt speed continuously

between 30 and 117 Hz thanks to a highly efficient inverter drive and motor combination. Unique Copeland Enhanced Vapor Injection technology allows production of water up to 68°C. Furthermore our variable speed solution incorporates intelligent controllers which use

sensors, as well as serial communication to manage compressor speed and operating envelopes.

For maximum efficiency, you can choose between a simple compressor and drive, or a full solution which includes compressor, drive and controller. This is what will make your heat pump so efficient.

WHAT MAKES YOUR HEAT PUMP SO EFFICIENT ?

39

GREEN ARCHITECTURESINGAPORE

40

41

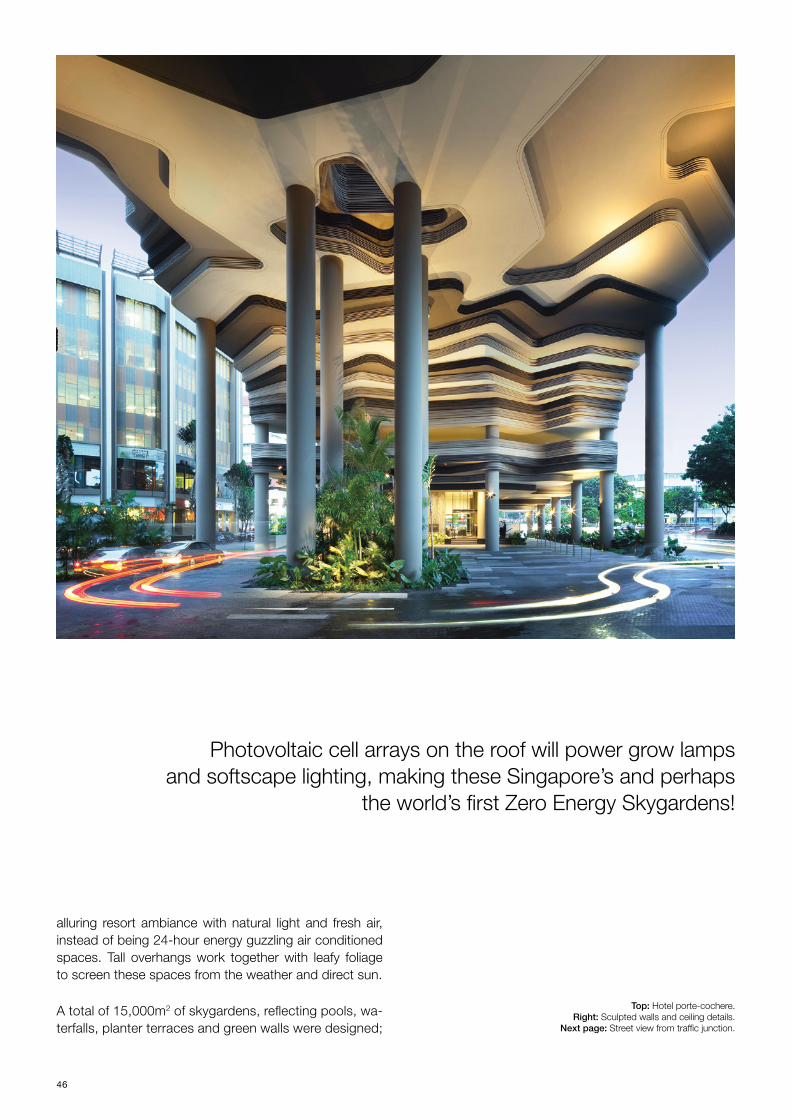

Located in central Singapore, the site is at a junction be-tween the CBD and the colorful districts of Chinatown and Clark Quay, and faces Hong Lim Park. A contoured podium responds to the street scale, drawing inspiration from a combination of landscaped bonsai arrangements that are modelled, chiselled and spliced to mimic natural landscapes and mountain rock formations as well as that of the contoured padi fields of Asia. These contours are precast concrete elements of modular radii, allowing the complex, sculptural podium to be put together from a ba-sic ‘kit of parts’.

The hotel Parkroyal on Pickering officially opened in January 2013. Designed by WOHA Architects, the project was awarded Singapore’s Green Mark Platinum, the nation’s highest environmental certification.

“Designed as a hotel and office in a garden, the project at Upper Pickering Street is a study of how we can not only conserve our greenery in a built-up high-rise city centre but multiply it in a manner that is architecturally striking, integrated and sustainable.”

All photos by Patrick Bingham-Hall.Image: Cavernous hotel entrance and drop-off.

42

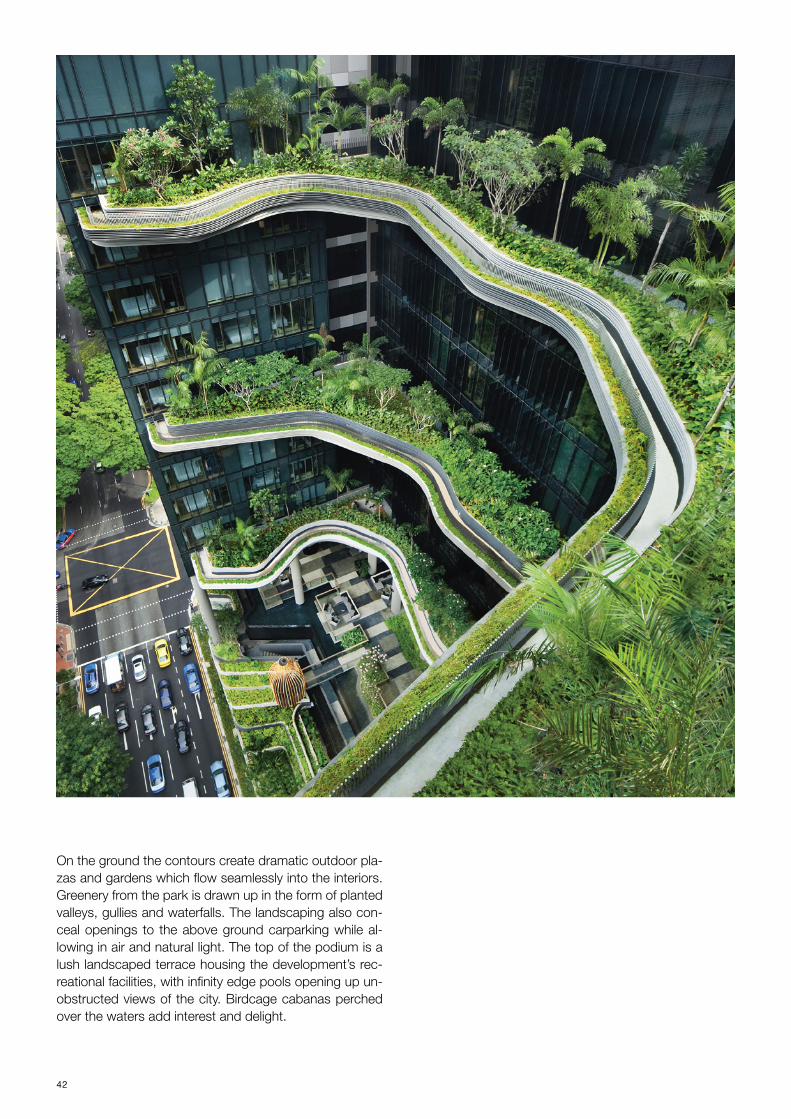

On the ground the contours create dramatic outdoor pla-zas and gardens which flow seamlessly into the interiors. Greenery from the park is drawn up in the form of planted valleys, gullies and waterfalls. The landscaping also con-ceal openings to the above ground carparking while al-lowing in air and natural light. The top of the podium is a lush landscaped terrace housing the development’s rec-reational facilities, with infinity edge pools opening up un-obstructed views of the city. Birdcage cabanas perched over the waters add interest and delight.

43

Birdcage cabanas perched over the waters add interest and delight.

Previous page: View of sky terraces from club lounge. This page: View from 5th floor

looking up to underside of sculpted sky terraces.

44

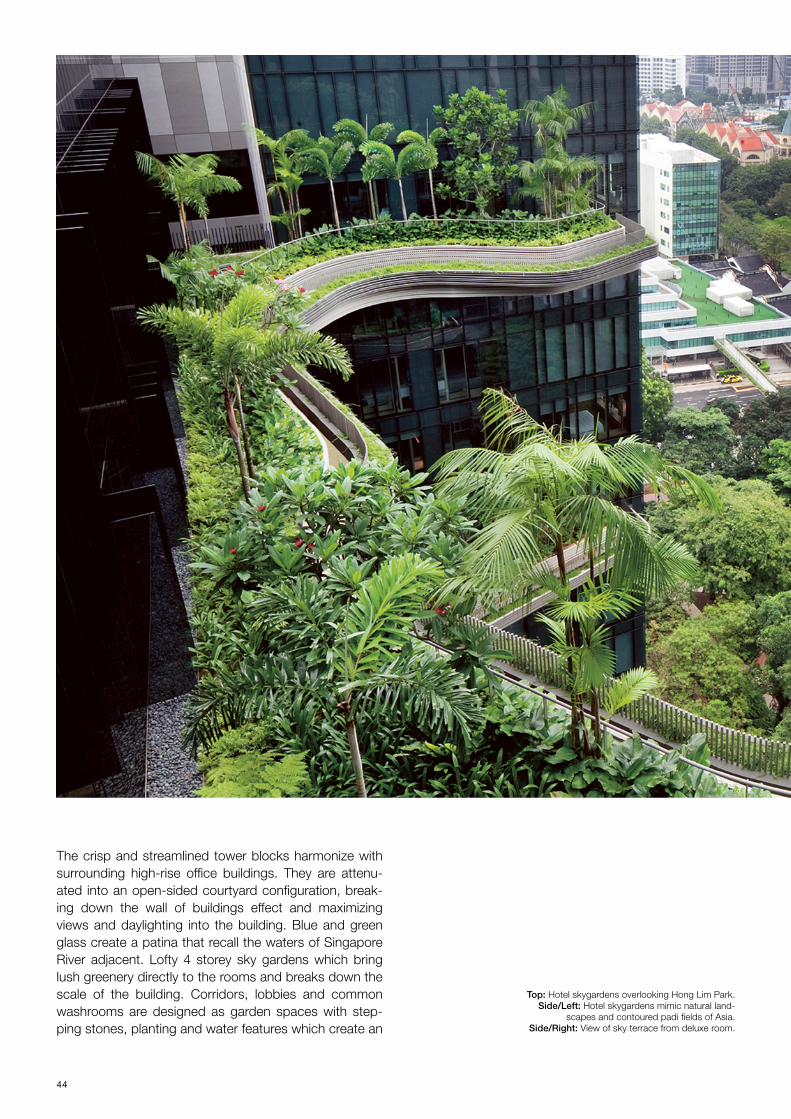

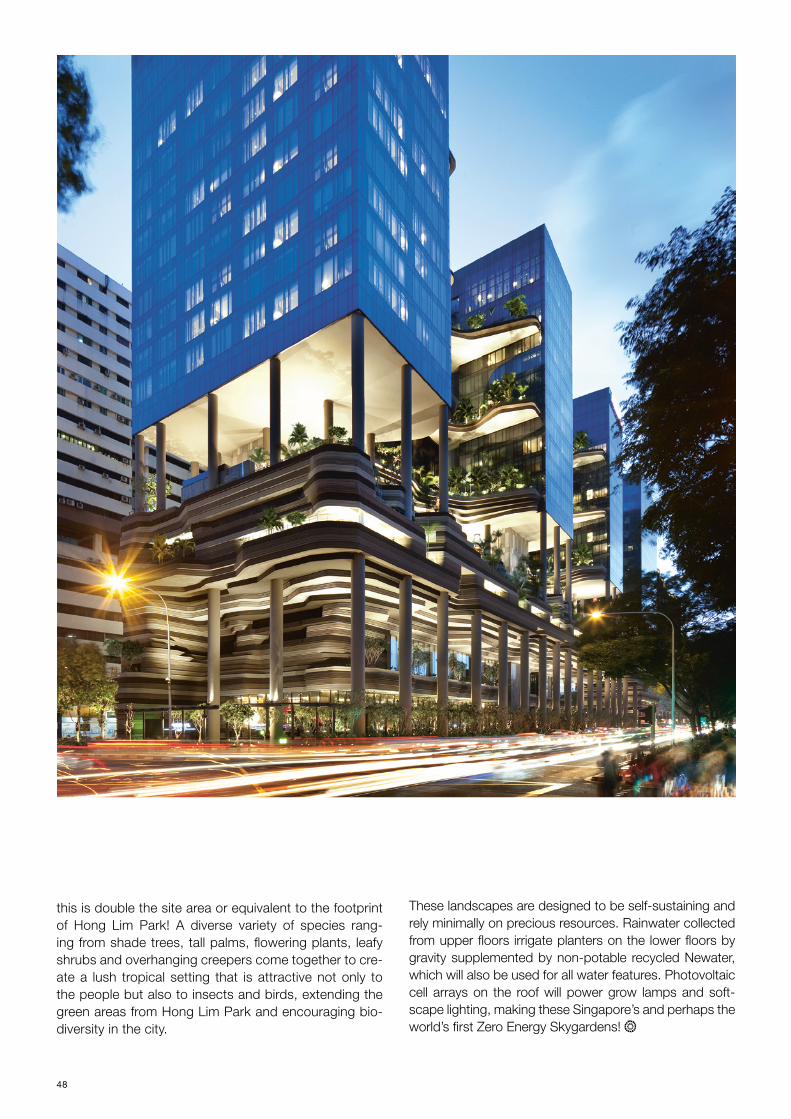

The crisp and streamlined tower blocks harmonize with surrounding high-rise office buildings. They are attenu-ated into an open-sided courtyard configuration, break-ing down the wall of buildings effect and maximizing views and daylighting into the building. Blue and green glass create a patina that recall the waters of Singapore River adjacent. Lofty 4 storey sky gardens which bring lush greenery directly to the rooms and breaks down the scale of the building. Corridors, lobbies and common washrooms are designed as garden spaces with step-ping stones, planting and water features which create an

Top: Hotel skygardens overlooking Hong Lim Park. Side/Left: Hotel skygardens mimic natural land-

scapes and contoured padi fields of Asia. Side/Right: View of sky terrace from deluxe room.

45

46

Photovoltaic cell arrays on the roof will power grow lamps and softscape lighting, making these Singapore’s and perhaps

the world’s first Zero Energy Skygardens!

alluring resort ambiance with natural light and fresh air, instead of being 24-hour energy guzzling air conditioned spaces. Tall overhangs work together with leafy foliage to screen these spaces from the weather and direct sun.

A total of 15,000m2 of skygardens, reflecting pools, wa-terfalls, planter terraces and green walls were designed;

Top: Hotel porte-cochere. Right: Sculpted walls and ceiling details.

Next page: Street view from traffic junction.

47

48

this is double the site area or equivalent to the footprint of Hong Lim Park! A diverse variety of species rang-ing from shade trees, tall palms, flowering plants, leafy shrubs and overhanging creepers come together to cre-ate a lush tropical setting that is attractive not only to the people but also to insects and birds, extending the green areas from Hong Lim Park and encouraging bio-diversity in the city.

These landscapes are designed to be self-sustaining and rely minimally on precious resources. Rainwater collected from upper floors irrigate planters on the lower floors by gravity supplemented by non-potable recycled Newater, which will also be used for all water features. Photovoltaic cell arrays on the roof will power grow lamps and soft-scape lighting, making these Singapore’s and perhaps the world’s first Zero Energy Skygardens!

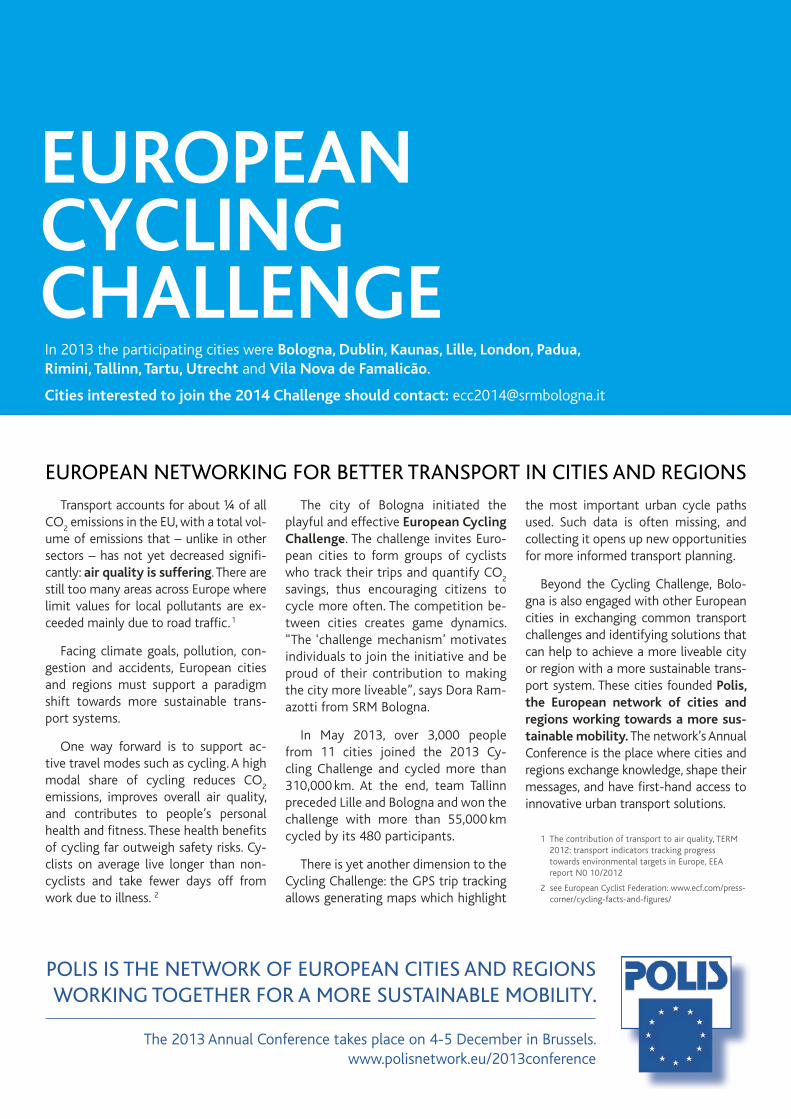

Transport accounts for about ! of all CO2 emissions in the EU, with a total vol-ume of emissions that – unlike in other sectors – has not yet decreased signifi-cantly: air quality is suffering. There are still too many areas across Europe where limit values for local pollutants are ex-ceeded mainly due to road traffic. 1

Facing climate goals, pollution, con-gestion and accidents, European cities and regions must support a paradigm shift towards more sustainable trans-port systems.

One way forward is to support ac-tive travel modes such as cycling. A high modal share of cycling reduces CO2 emissions, improves overall air quality, and contributes to people’s personal health and fitness. These health benefits of cycling far outweigh safety risks. Cy-clists on average live longer than non-cyclists and take fewer days off from work due to illness. 2

The city of Bologna initiated the playful and effective European Cycling Challenge. The challenge invites Euro-pean cities to form groups of cyclists who track their trips and quantify CO2 savings, thus encouraging citizens to cycle more often. The competition be-tween cities creates game dynamics. “The ‘challenge mechanism’ motivates individuals to join the initiative and be proud of their contribution to making the city more liveable”, says Dora Ram-azotti from SRM Bologna.

In May 2013, over 3,000 people from 11 cities joined the 2013 Cy-cling Challenge and cycled more than 310,000 km. At the end, team Tallinn preceded Lille and Bologna and won the challenge with more than 55,000 km cycled by its 480 participants.

There is yet another dimension to the Cycling Challenge: the GPS trip tracking allows generating maps which highlight

the most important urban cycle paths used. Such data is often missing, and collecting it opens up new opportunities for more informed transport planning.

Beyond the Cycling Challenge, Bolo-gna is also engaged with other European cities in exchanging common transport challenges and identifying solutions that can help to achieve a more liveable city or region with a more sustainable trans-port system. These cities founded Polis, the European network of cities and regions working towards a more sus-tainable mobility. The network’s Annual Conference is the place where cities and regions exchange knowledge, shape their messages, and have first-hand access to innovative urban transport solutions.

1 The contribution of transport to air quality, TERM 2012: transport indicators tracking progress towards environmental targets in Europe, EEA report N0 10/2012

2 see European Cyclist Federation: www.ecf.com/press-corner/cycling-facts-and-figures/

EUROPEAN NETWORKING FOR BETTER TRANSPORT IN CITIES AND REGIONS

POLIS IS THE NETWORK OF EUROPEAN CITIES AND REGIONS WORKING TOGETHER FOR A MORE SUSTAINABLE MOBILITY.

The 2013 Annual Conference takes place on 4-5 December in Brussels. www.polisnetwork.eu/2013conference

In 2013 the participating cities were Bologna, Dublin, Kaunas, Lille, London, Padua, Rimini, Tallinn, Tartu, Utrecht and Vila Nova de Famalicão.

Cities interested to join the 2014 Challenge should contact: [email protected]

abudhabiartfair.ae

51

VI WS

Emanuel, 18, and his sister have been picking waste with their mother, Georgina, since they were kids. They live in the outskirts of Koforidua and commute every day to work. Both would like to go to school but can't afford it.

Olivier Ervyn

GHANAWaste-picking in Koforidua

52

The harvest is stockpiled by the main access road. Once a month, a buyer comes round and purchases the metal and plastic pickers have accumulated.

“Bwala five five” is the name given by waste pickers to the main dumpsite of Koforidua, a town of 130,000 inhabitants in eastern Ghana. On a regular working day, about 15 women and children work on the site, picking whatever may have some value from the rubbish deposited by municipal garbage trucks. They come equipped with nothing but a piece of bent steel, used as a hook, wear gloves made out of old socks, use electric cables to secure their trousers and usually have to start the day by looking for wearable shoes in the dump.

They collect hard plastic and cans, which they sell once a month to a processing company. Plastic is worth 50 pesewas a kilo (0,20!) while metal only brings 20 pesewas a kilo (0,08!).

The work is physically demanding and dangerous, as only those who get very close to the truck as it dumps its load can grab the best and larger pieces of plastic. Trucks come in at all times, zigzagging between people, sheep, cows and vultures, emptying their load of waste and speeding back to town for the next collection round. The whole area

53

is heavily polluted, covered in the toxic smoke of slow fires that seem to burn night and day. Finding metal in burnt out sections is of course easier but breathing the fumes day after day is costly. Those who spe-cialize in such work complain of breathing problems and often spend most of the little profit they make on medicines and medical fees.

None of the adult waste pickers of Koforidua believe they will ever find a "real" job, away from the dumpsite. None of the children who work there go to school.

Olivier Ervyn (b.1970) is a Belgian documentary photographer. Based in Brussels, he has travelled extensively throughout Africa to document everyday life. The Ghana series is part of a wider project to document people at work and the extent to which some take risks to earn a living. He is currently working on two other projects, one on African churches in Europe and the other on new forms of poverty in developed economies.

To learn more, visit: www.revolve-magazine.com

54

Georgina lives in town. She says her job is slowly killing her and that more people "in other countries" should know how wastepickers live.

55

Sundays, when fewer pickers come to work, can be a good day for those who do turn up, with potentially rich pickings.

56

Jacob, 12. Ghana and this fast-moving economy attracts thousands of migrants from all over West Africa. A French-speaking immigrant from Togo, Jacob came to Ghana with his father but, as he said, they have not yet been able to find "un bon travail". They both have been working at the dumpsite since they arrived in Ghana, several years ago.

57

58

Smoke from burning waste covers large sections of the dumpsite. Methane produced by rotting organic waste and tons of plastic shopping bags compacted throughout the area create an ideal environment for fire. Once set alight, waste can burn for weeks.

59

60

Work starts at 6am every day and often continues late into the evening.

61

62

Georgina is another of the many women who pick waste at Bwala 55.

63

Awa lives in a small settlement on the edge of the landfill. She says people there drink, cook and wash with contaminated water. Moving is not an option and picking waste is the only job available to them. Ghana's economy is moving forward (+7.9% GDP in 2012) but the country continues to struggle with relatively high inflation and unemployment levels.

64

Georgina, 47, prefers working on her own in the most remote sections of the dumpsite, where fire has cleared up most of the waste. She suffers from breathing problems and is often too tired and unwell to come to work.

65

66

Felicia has been a wastepicker for 18 years. She acts as the unofficial leader of the Koforidua waste pickers and is very aware of the dangers and health risks she and her co-workers face on a daily basis.

Why join EREC2013?EREC2013 is a unique platform to reach key decision makers in the renewable energy sector. Partners gain exposure in a high level environment and enhance their company’s image as a key actor in the renewable energy market.

Launched in April 2013 at the Renewable Energy House in Brussels, this EREC report sets out the reasons why European climate and energy policy should be based on a hat-trick of targets for renewable energy, energy efficiency and greenhouse gas (GHG) reduction.

To download the publication, visit www.erec.org

EREC2013 Europe’s Renewable Energy Policy Conference

www.erec2013.org

28 November 2013, Brussels, Belgium

Join Europe’s leading biennial Renewable Energy Policy Conference, EREC2013, that has grown since its first edition in 2004 to become Europe’s major occasion for exchange and interaction between industry, research and policy.

EREC2013 will feature:• boosting jobs, growth and innovation by investing in renewable energies • the question of whether Europe is on track to meet its 2020 targets • the ambitious 2030 framework to provide stability for investors

For sponsorship opportunities, please contact Marianne Rygaerts from Downtown Europe: +32 2 732 35 20.

If you want to lower costs, create jobs, replace fossil fuel imports and drive innovation, competitiveness and investment, then a hat-trick of climate and energy goals works best.

www.erec.org

68

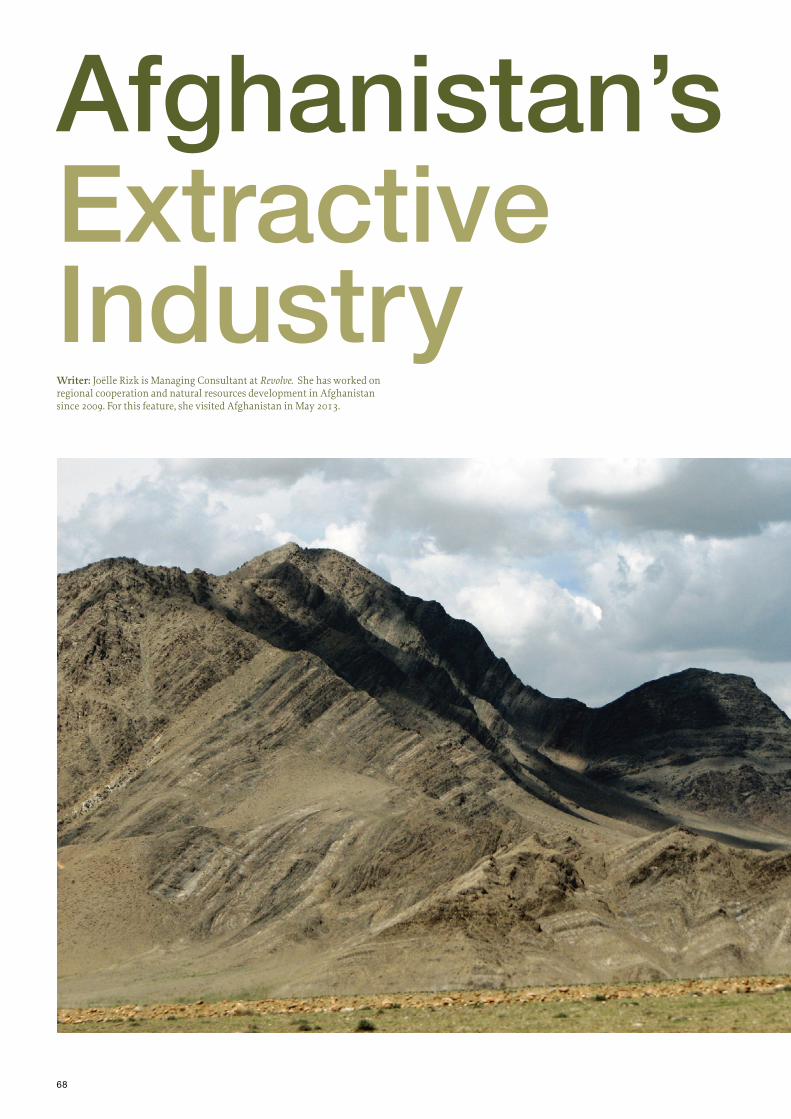

Writer: Joëlle Rizk is Managing Consultant at Revolve. She has worked on regional cooperation and natural resources development in Afghanistan since 2009. For this feature, she visited Afghanistan in May 2013.

Afghanistan’s ExtractiveIndustry

69

Extracting Afghanistan’s minerals is believed by many to be the gateway to economic prosperity in Afghanistan and to economic connectivity in Central Asia. Developing Afghanistan’s mining into a regional Resource Corridor is a major task ahead for the Afghan government. There are many governance, security and political challenges, and the extractive industry is still far from maturing. However, Afghanistan has made remarkable progress, and continues the process of building an enabling environment for Direct Foreign Investment. Is Afghanistan ready to become an international mining nation? Will Afghanistan re-invest mining revenues in its population and sustain its economy?

Mining has been taking place in Afghanistan for thousands of years – whether it was gold, copper, iron or lapis-lazuli, emerald and tourmaline. For centuries, Afghanistan has been known as a mineral rich country with vast exploitable resources. Alexander the Great, the British, the Soviets and the Taliban all tried to tap into Afghan natural resources.

Shortly after U.S. officials tagged Afghani-stan’s minerals with a $1 trillion value, the Afghan Minister of Mines, Wahidullah Shah-rani, tripled that with an estimate of $3 tril-lion. With the support of the World Bank,

$1 trillion worth of undeveloped mineral resources: this figure has become a com-mon reference to describing the potential of Afghanistan’s extractive industry. Refer-ring to Soviet maps that were saved and preserved by Afghan geologists, the United States Geological Survey (USGS) team sur-veyed Afghanistan between 2004 and 2007 to map its mineral potentials. Data collection and site exploration were simultaneously done by both British and Afghan Geological Surveys. It then became clear that Afghani-

Afghanistan is keen to develop a “Resource Corridor” whereby investment will be multi-sectorial. This would induce growth of extrac-tive activities and develop infrastructure, services, trade and agriculture, thus boosting Afghanistan’s domestic revenue. While data is not clear as to precise projections, esti-mates are that net revenue earning potential from extractives could reach $1 billion by 2017 and contribute 2-3% of the GDP.

In addition to the digital mapping of Afghani-stan’s minerals and to updating some of the existing data, the USGS and the U.S. Army

stan’s mineral riches are far beyond what the Survey was initially assessing. In 2010, while the world was desperate to hear good news from Afghanistan, the figures were pub-lished, which appeared to be an economic bonanza for Afghanistan. Then, in the midst of the hype about the transition process and worries about the economic future of Afghan-istan once foreign troops withdraw by 2014 and international aid declines, the mining sector emerged as the solution to ensuring stability and economic growth in the country.

The Good Old News from Afghanistan

70

Not Another Saudi Arabia Additionally, the variety of commodities in Afghanistan’s minerals, while perceived as richness, does not actually help reduce pro-duction costs. There will be an array of varied requirements among minerals: specialized man-power, extraction methods, processing, storage facilities and transportation, which could multiply the costs.

Based on rough calculations of gross value and estimated production rates, some experts conclude that in the case of Afghanistan, where hard and soft mining infrastructure is lacking, the net value of an extractive project might not exceed 4% of the gross value of its undeveloped mineral resources (Lipow & Melese, 2012). It is then important to real-ize that even an optimistic development of Afghanistan’s extractive industry might only have a moderate economic output: the boom is expected to generate 120,000 jobs at best – the World Bank estimates no more than 20,000 jobs for currently known depos-

ments (LREE) grading 2.77% and 15 million tons grading 3.28% (MoM, 2012). It is also believed that Afghanistan has world class reserves of lithium, estimated at 350,000 tons (MoM, 2012), which can pos-sibly bring Afghanistan to the forefront of mining nations.

its. For a population of over 30 million with an unemployment rate of 35%, this figure, despite being positive, is very modest.