Embed Size (px)

Citation preview

Sampo Group Debt Investor PresentationPrepared February 10, 2016Figures December 31, 2015

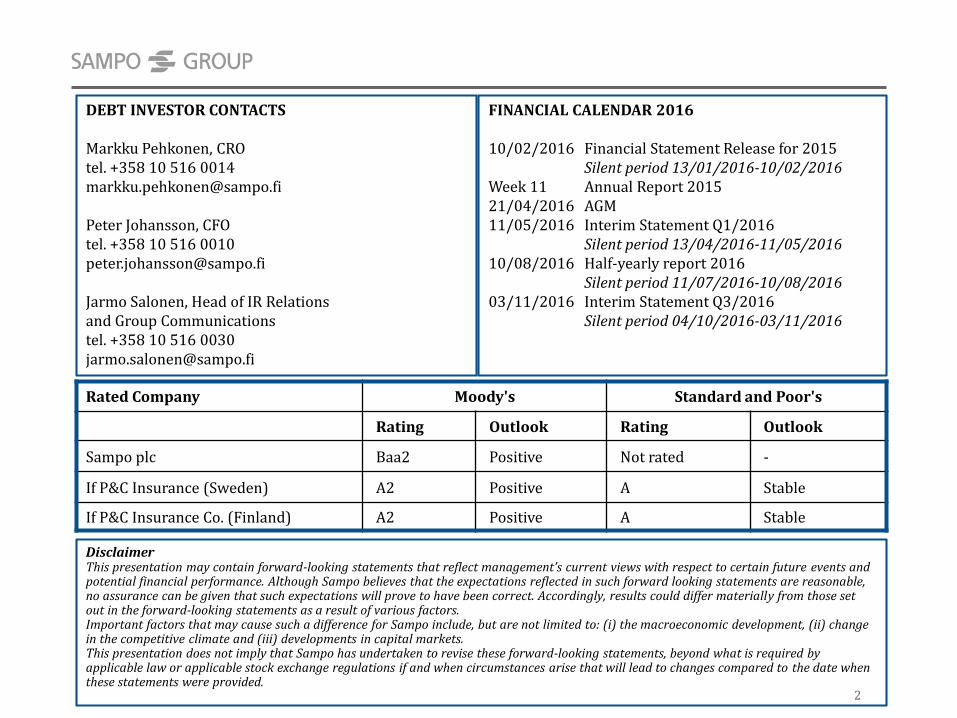

DEBT INVESTOR CONTACTS

Markku Pehkonen, CROtel. +358 10 516 [email protected]

Peter Johansson, CFOtel. +358 10 516 [email protected]

Jarmo Salonen, Head of IR Relations and Group Communicationstel. +358 10 516 [email protected]

FINANCIAL CALENDAR 2016

10/02/2016 Financial Statement Release for 2015Silent period 13/01/2016-10/02/2016

Week 11 Annual Report 201521/04/2016 AGM11/05/2016 Interim Statement Q1/2016

Silent period 13/04/2016-11/05/201610/08/2016 Half-yearly report 2016

Silent period 11/07/2016-10/08/201603/11/2016 Interim Statement Q3/2016

Silent period 04/10/2016-03/11/2016

Rated Company Moody's Standard and Poor's

Rating Outlook Rating Outlook

Sampo plc Baa2 Positive Not rated -

If P&C Insurance (Sweden) A2 Positive A Stable

If P&C Insurance Co. (Finland) A2 Positive A Stable

DisclaimerThis presentation may contain forward-looking statements that reflect management’s current views with respect to certain future events and potential financial performance. Although Sampo believes that the expectations reflected in such forward looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forward-looking statements as a result of various factors.Important factors that may cause such a difference for Sampo include, but are not limited to: (i) the macroeconomic development, (ii) change in the competitive climate and (iii) developments in capital markets.This presentation does not imply that Sampo has undertaken to revise these forward-looking statements, beyond what is required by applicable law or applicable stock exchange regulations if and when circumstances arise that will lead to changes compared to the date when these statements were provided.

2

Sampo Group Basic Facts 3-10If P&C The Leading Nordic P&C Insurer 11-19Mandatum Life A Finish Financial Services Company 20-28Sampo Group A Productive Value Creator 29-36Sampo plc The Listed Parent Company – A Stable Dividend Payer 37-43

Appendix 44-57

3

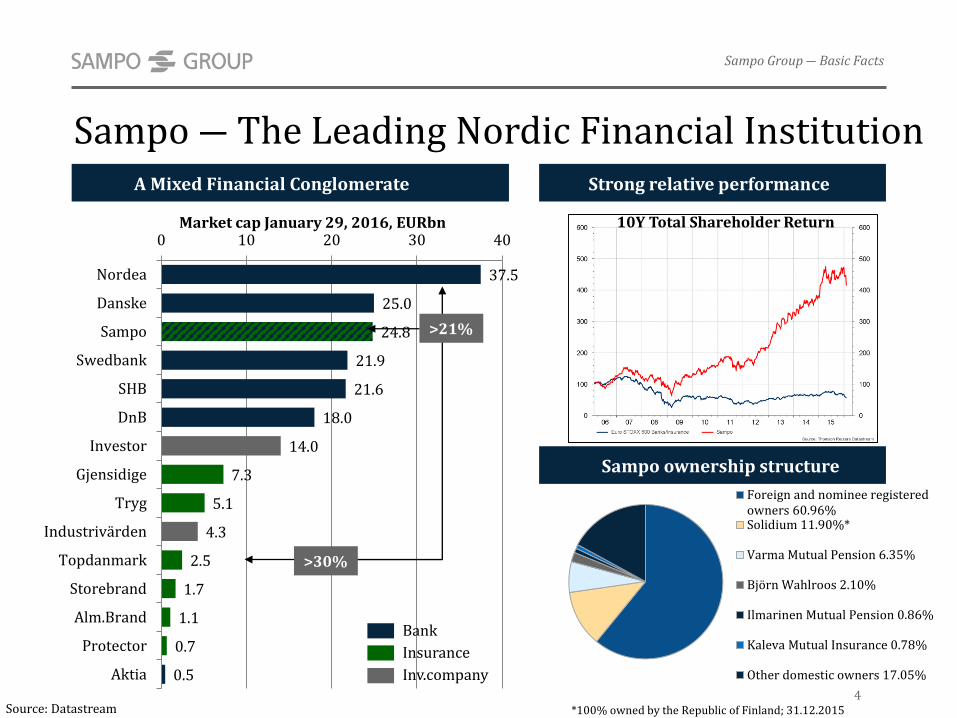

37.5

25.0

24.8

21.9

21.6

18.0

14.0

7.3

5.1

4.3

2.5

1.7

1.1

0.7

0.5

0 10 20 30 40

Nordea

Danske

Sampo

Swedbank

SHB

DnB

Investor

Gjensidige

Tryg

Industrivärden

Topdanmark

Storebrand

Alm.Brand

Protector

Aktia

Sampo ― The Leading Nordic Financial Institution

Source: Datastream

>30%

>21%

Sampo ownership structure

*100% owned by the Republic of Finland; 31.12.2015

Market cap January 29, 2016, EURbn

Strong relative performance

4

Sampo Group ― Basic Facts

10Y Total Shareholder Return

A Mixed Financial Conglomerate

Bank

Insurance

Inv.company

Foreign and nominee registeredowners 60.96%Solidium 11.90%*

Varma Mutual Pension 6.35%

Björn Wahlroos 2.10%

Ilmarinen Mutual Pension 0.86%

Kaleva Mutual Insurance 0.78%

Other domestic owners 17.05%

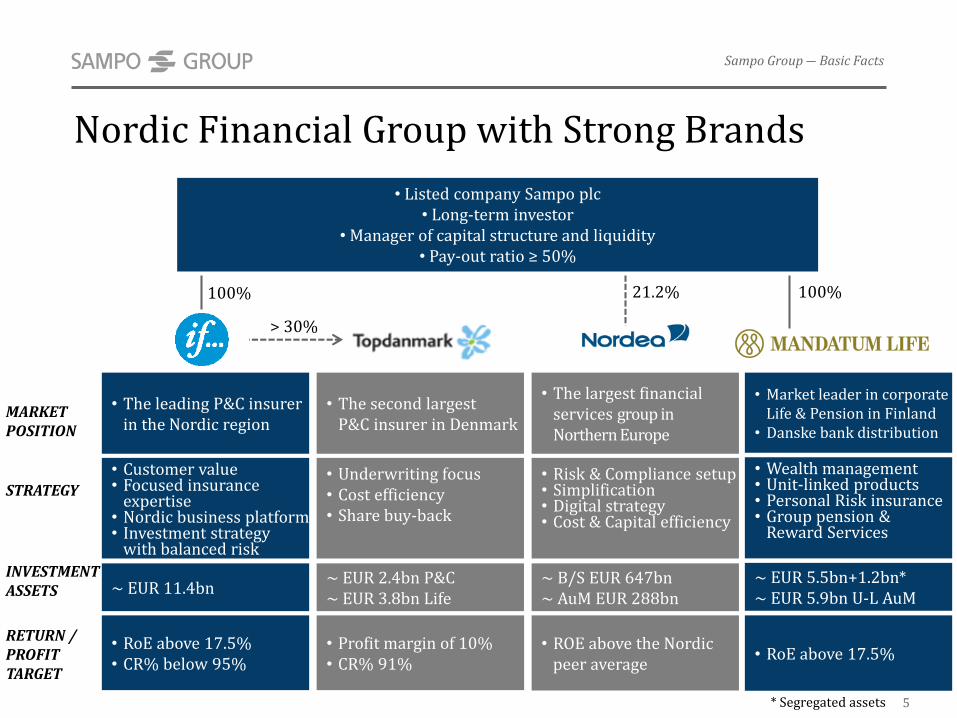

• Listed company Sampo plc• Long-term investor

• Manager of capital structure and liquidity• Pay-out ratio ≥ 50%

Nordic Financial Group with Strong Brands

Sampo Group ― Basic Facts

5

MARKET POSITION

STRATEGY

INVESTMENT ASSETS

RETURN /PROFITTARGET

21.2%

• The leading P&C insurerin the Nordic region

• Customer value• Focused insurance

expertise• Nordic business platform• Investment strategy

with balanced risk

~ EUR 11.4bn

• RoE above 17.5%• CR% below 95%

> 30%

100%

• The largest financialservices group inNorthern Europe

• Risk & Compliance setup• Simplification • Digital strategy• Cost & Capital efficiency

~ B/S EUR 647bn~ AuM EUR 288bn

• ROE above the Nordicpeer average

• The second largest P&C insurer in Denmark

• Underwriting focus• Cost efficiency• Share buy-back

~ EUR 2.4bn P&C~ EUR 3.8bn Life

• Profit margin of 10%• CR% 91%

• Wealth management• Unit-linked products• Personal Risk insurance • Group pension &

Reward Services

• Market leader in corporateLife & Pension in Finland

• Danske bank distribution

~ EUR 5.5bn+1.2bn*~ EUR 5.9bn U-L AuM

• RoE above 17.5%

* Segregated assets

100%

Sampo Group Steering Model and Principles• Non-complex structures and only minor contagion risks

– three separate and independent business areas

– straightforward and transparent legal structure combined with limited intragroup exposures

• General Principles of Business activities

– clear responsibilities

– simple and flat operational structures

• Parent company gives guidance to the subsidiaries by setting

– targets for capitalization and ROE

– group principles for Risk Management, Remuneration, Compliance, Code of Conduct

• Subsidiaries organize underwriting activities independently taking into account

– the specific characteristics of their operations

– the above guidance from parent company

– the stakeholders’ expectations and external regulation6

Sampo Group ― Basic Facts

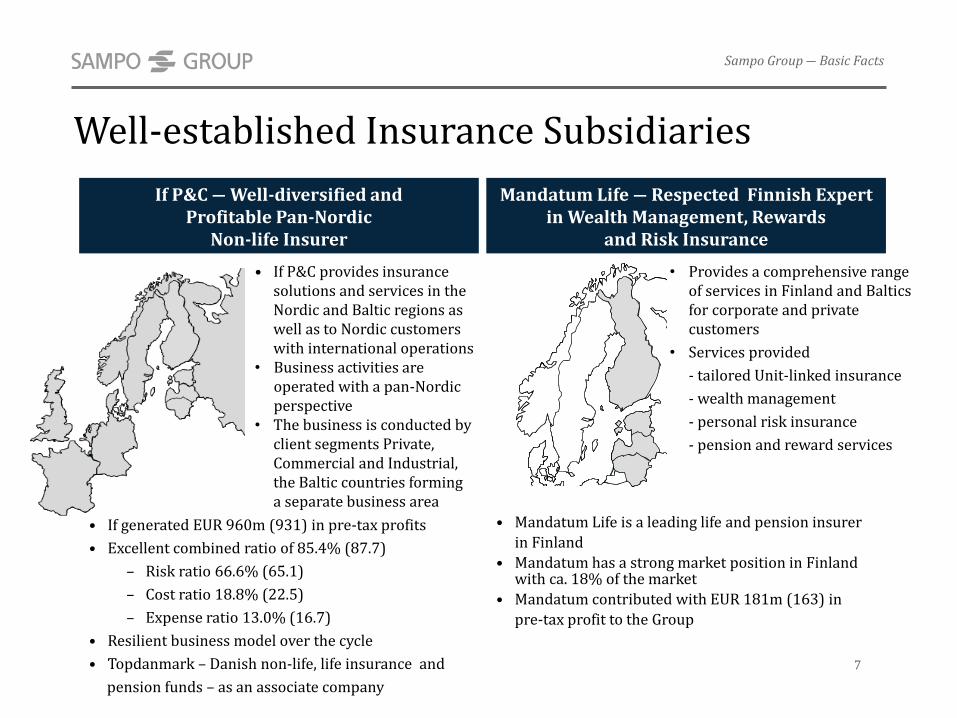

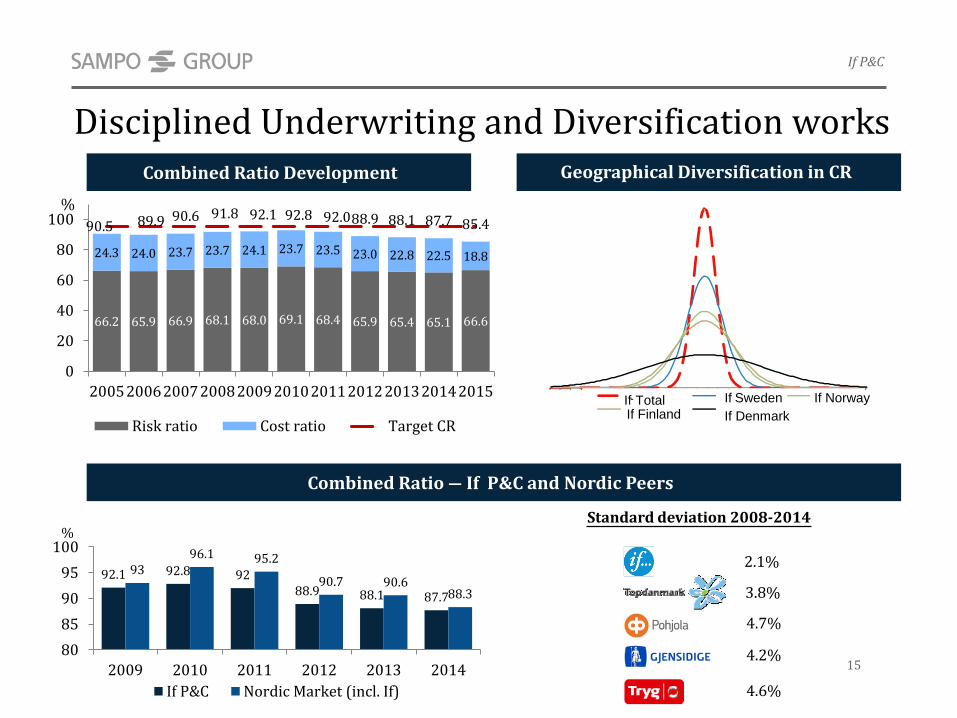

• If generated EUR 960m (931) in pre-tax profits

• Excellent combined ratio of 85.4% (87.7)

– Risk ratio 66.6% (65.1)

– Cost ratio 18.8% (22.5)

– Expense ratio 13.0% (16.7)

• Resilient business model over the cycle

• Topdanmark – Danish non-life, life insurance and

pension funds – as an associate company

If P&C ― Well-diversified and Profitable Pan-Nordic

Non-life Insurer

• If P&C provides insurance solutions and services in the Nordic and Baltic regions as well as to Nordic customers with international operations

• Business activities are operated with a pan-Nordic perspective

• The business is conducted by client segments Private, Commercial and Industrial, the Baltic countries forming a separate business area

Well-established Insurance Subsidiaries

• Mandatum Life is a leading life and pension insurer

in Finland

• Mandatum has a strong market position in Finland with ca. 18% of the market

• Mandatum contributed with EUR 181m (163) in

pre-tax profit to the Group

Mandatum Life ― Respected Finnish Expert in Wealth Management, Rewards

and Risk Insurance

• Provides a comprehensive rangeof services in Finland and Balticsfor corporate and privatecustomers

• Services provided

- tailored Unit-linked insurance

- wealth management

- personal risk insurance

- pension and reward services

Sampo Group ― Basic Facts

7

Sampo Group ― Basic Facts

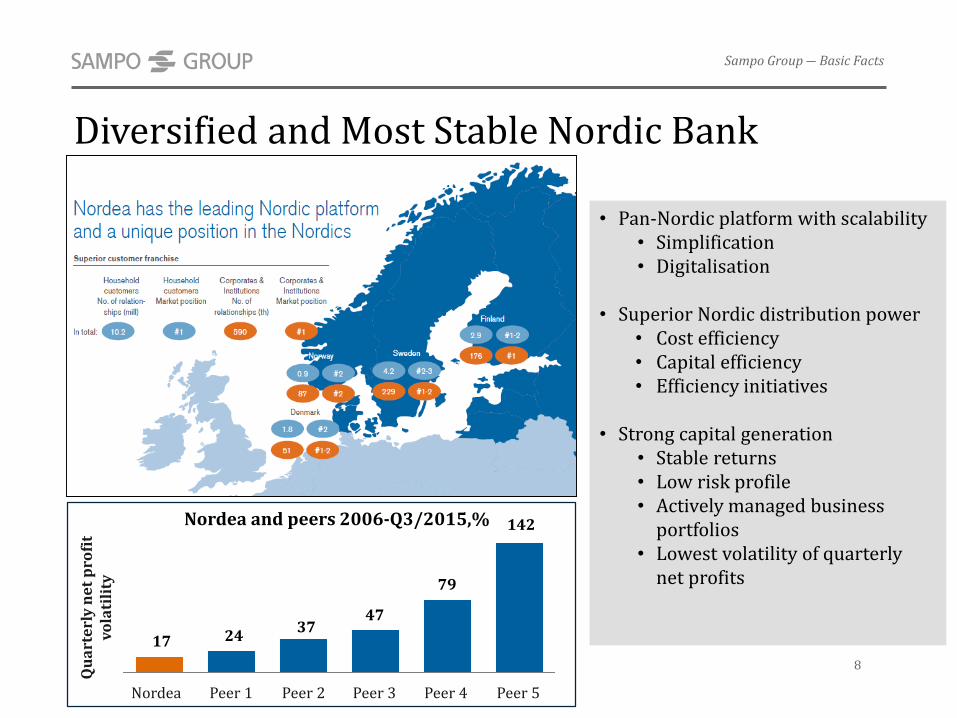

Diversified and Most Stable Nordic Bank

• Pan-Nordic platform with scalability• Simplification• Digitalisation

• Superior Nordic distribution power• Cost efficiency• Capital efficiency• Efficiency initiatives

• Strong capital generation• Stable returns• Low risk profile• Actively managed business

portfolios• Lowest volatility of quarterly

net profits

17 24 37

47

79

142

Nordea Peer 4Peer 3Peer 1 Peer 5Peer 2

Qu

art

erl

y n

et

pro

fit

vola

tili

ty

Nordea and peers 2006-Q3/2015,%

8

Danish Insurer with a Robust Business Model

9

Sampo Group ― Basic Facts

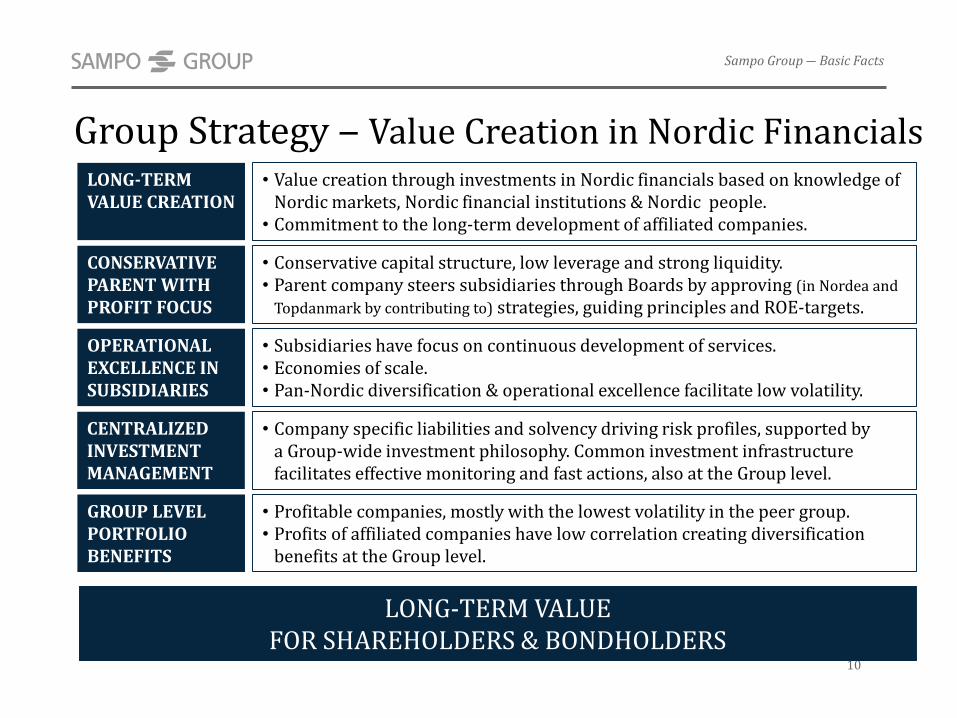

Group Strategy ‒ Value Creation in Nordic Financials

10

Sampo Group ― Basic Facts

LONG-TERM VALUE CREATION

• Value creation through investments in Nordic financials based on knowledge of Nordic markets, Nordic financial institutions & Nordic people.

• Commitment to the long-term development of affiliated companies.

OPERATIONAL EXCELLENCE IN SUBSIDIARIES

• Subsidiaries have focus on continuous development of services.• Economies of scale.• Pan-Nordic diversification & operational excellence facilitate low volatility.

CONSERVATIVE PARENT WITH PROFIT FOCUS

• Conservative capital structure, low leverage and strong liquidity.• Parent company steers subsidiaries through Boards by approving (in Nordea and

Topdanmark by contributing to) strategies, guiding principles and ROE-targets.

GROUP LEVEL PORTFOLIO BENEFITS

• Profitable companies, mostly with the lowest volatility in the peer group.• Profits of affiliated companies have low correlation creating diversification

benefits at the Group level.

LONG-TERM VALUE FOR SHAREHOLDERS & BONDHOLDERS

CENTRALIZEDINVESTMENT MANAGEMENT

• Company specific liabilities and solvency driving risk profiles, supported bya Group-wide investment philosophy. Common investment infrastructure facilitates effective monitoring and fast actions, also at the Group level.

11

Sampo Group Basic Facts 3-10If P&C The Leading Nordic P&C Insurer 11-19Mandatum Life A Finnish Financial Services Company 20-28Sampo Group A Productive Value Creator 29-36Sampo plc The Listed Parent Company – A Stable Dividend Payer 37-43

Appendix 44-57

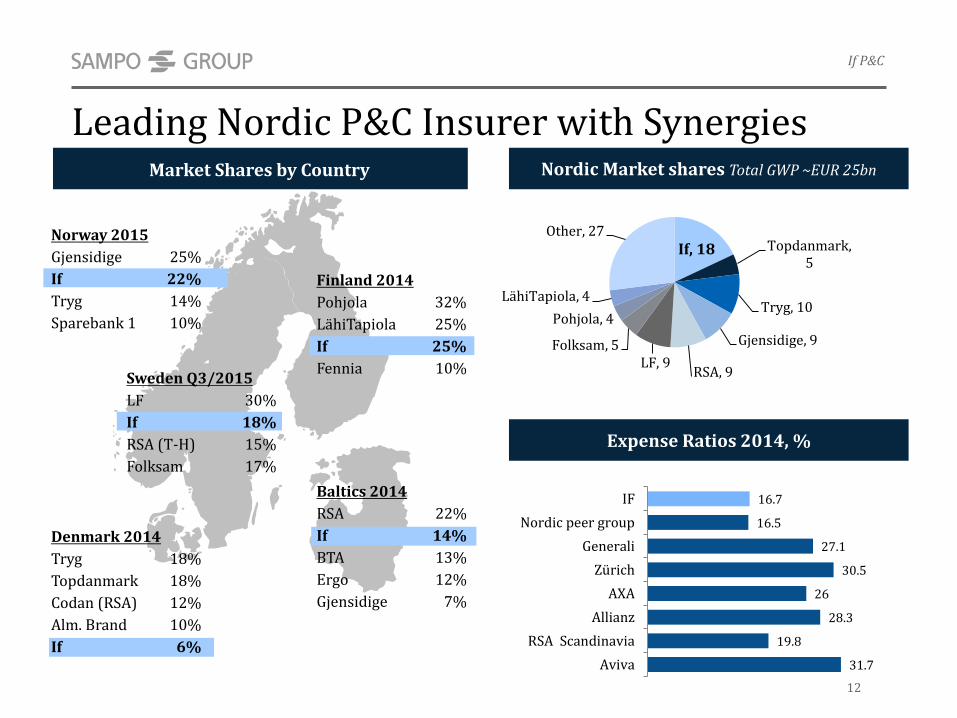

Expense Ratios 2014, %

Leading Nordic P&C Insurer with Synergies

Norway 2015

Gjensidige 25%

If 22%

Tryg 14%

Sparebank 1 10%

Denmark 2014

Tryg 18%

Topdanmark 18%

Codan (RSA) 12%

Alm. Brand 10%

If 6%

Finland 2014

Pohjola 32%

LähiTapiola 25%

If 25%

Fennia 10%Sweden Q3/2015

LF 30%

If 18%

RSA (T-H) 15%

Folksam 17%

Baltics 2014

RSA 22%

If 14%

BTA 13%

Ergo 12%

Gjensidige 7%

Market Shares by Country

If, 18 Topdanmark, 5

Tryg, 10

Gjensidige, 9

RSA, 9LF, 9

Folksam, 5

Pohjola, 4

LähiTapiola, 4

Other, 27

16.7

16.5

27.1

30.5

26

28.3

19.8

31.7

IF

Nordic peer group

Generali

Zürich

AXA

Allianz

RSA Scandinavia

Aviva

If P&C

12

Nordic Market shares Total GWP ~EUR 25bn

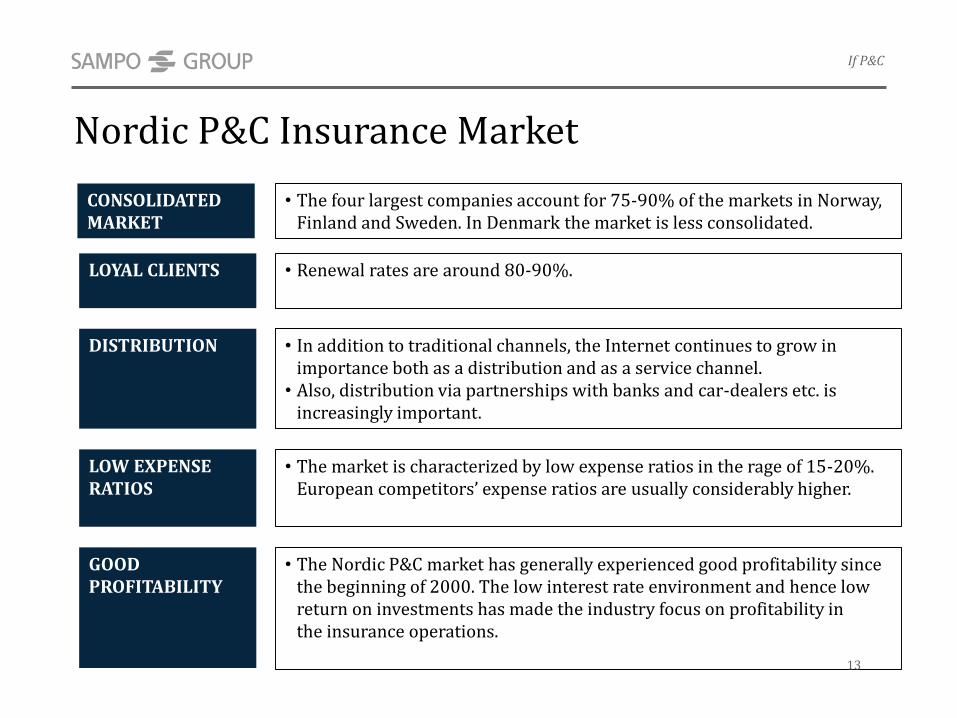

Nordic P&C Insurance Market

CONSOLIDATED MARKET

LOW EXPENSE RATIOS

• In addition to traditional channels, the Internet continues to grow in importance both as a distribution and as a service channel.

• Also, distribution via partnerships with banks and car-dealers etc. is increasingly important.

GOOD PROFITABILITY

• The Nordic P&C market has generally experienced good profitability since the beginning of 2000. The low interest rate environment and hence low return on investments has made the industry focus on profitability in the insurance operations.

• Renewal rates are around 80-90%.LOYAL CLIENTS

DISTRIBUTION

• The market is characterized by low expense ratios in the rage of 15-20%. European competitorsʼ expense ratios are usually considerably higher.

• The four largest companies account for 75-90% of the markets in Norway, Finland and Sweden. In Denmark the market is less consolidated.

13

If P&C

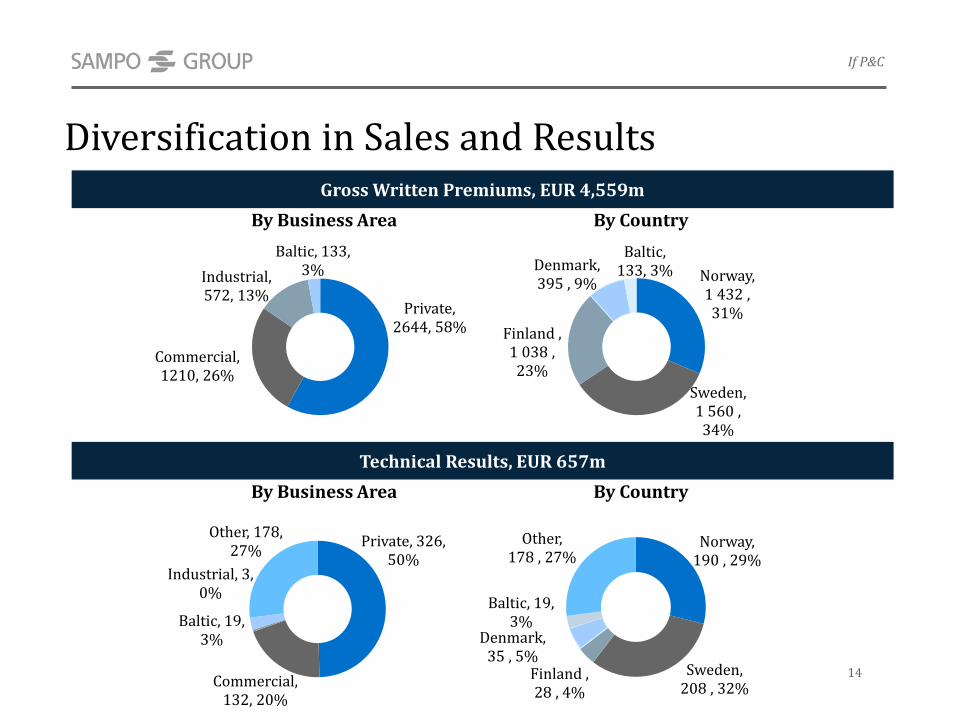

By Business Area By Country

Private, 326, 50%

Commercial, 132, 20%

Industrial, 3, 0%

Baltic, 19, 3%

Other, 178, 27%

Technical Results, EUR 657m

Norway, 190 , 29%

Sweden, 208 , 32%

Finland , 28 , 4%

Denmark, 35 , 5%

Baltic, 19, 3%

Other, 178 , 27%

Gross Written Premiums, EUR 4,559m

By Business Area By Country

Private, 2644, 58%

Commercial, 1210, 26%

Industrial, 572, 13%

Baltic, 133, 3% Norway,

1 432 , 31%

Sweden, 1 560 , 34%

Finland , 1 038 , 23%

Denmark, 395 , 9%

Baltic, 133, 3%

If P&C

14

Diversification in Sales and Results

If- Total If Sweden If Norway

If Finland If Denmark

Geographical Diversification in CR

Combined Ratio ― If P&C and Nordic Peers

Combined Ratio Development

Standard deviation 2008-2014

2.1%

4.6%

4.2%

4.7%

3.8%

66.2 65.9 66.9 68.1 68.0 69.1 68.4 65.9 65.4 65.1 66.6

24.3 24.0 23.7 23.7 24.1 23.7 23.5 23.0 22.8 22.5 18.8

90.5 89.9 90.6 91.8 92.1 92.8 92.088.9 88.1 87.7 85.4

0

20

40

60

80

100

20052006200720082009201020112012201320142015

%

Risk ratio Cost ratio Target CR

15

If P&C

92.1 92.8 9288.9 88.1 87.7

9396.1 95.2

90.7 90.688.3

80

85

90

95

100

2009 2010 2011 2012 2013 2014

%

If P&C Nordic Market (incl. If)

Disciplined Underwriting and Diversification works

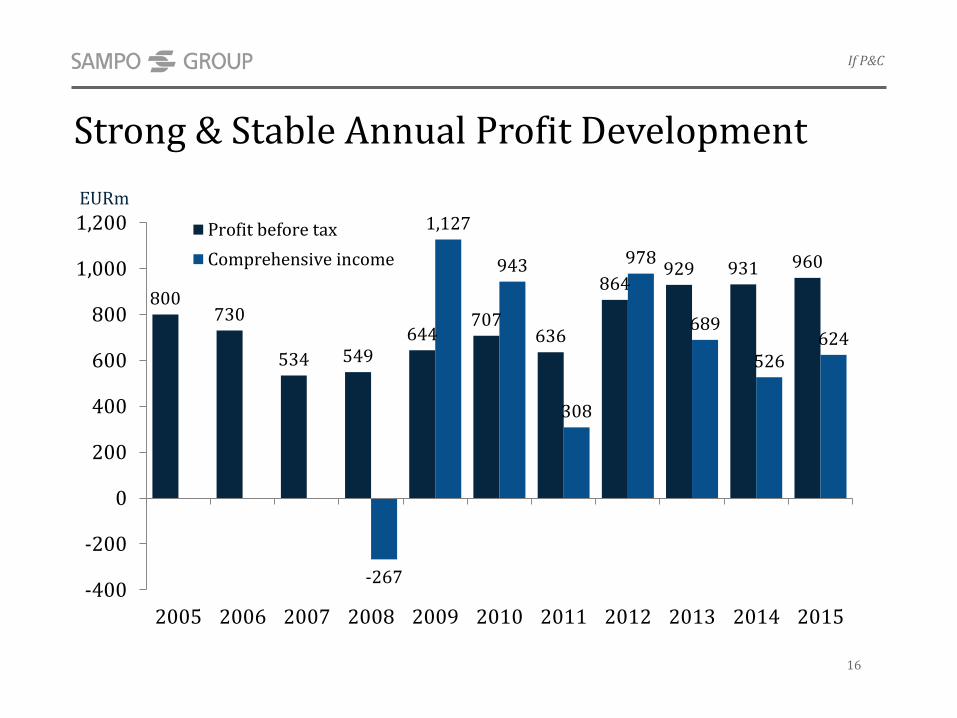

Strong & Stable Annual Profit Development

800730

534 549644

707636

864929 931 960

-267

1,127

943

308

978

689

526624

-400

-200

0

200

400

600

800

1,000

1,200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Profit before tax

Comprehensive income

EURm

16

If P&C

0

50

100

150

200

250

300

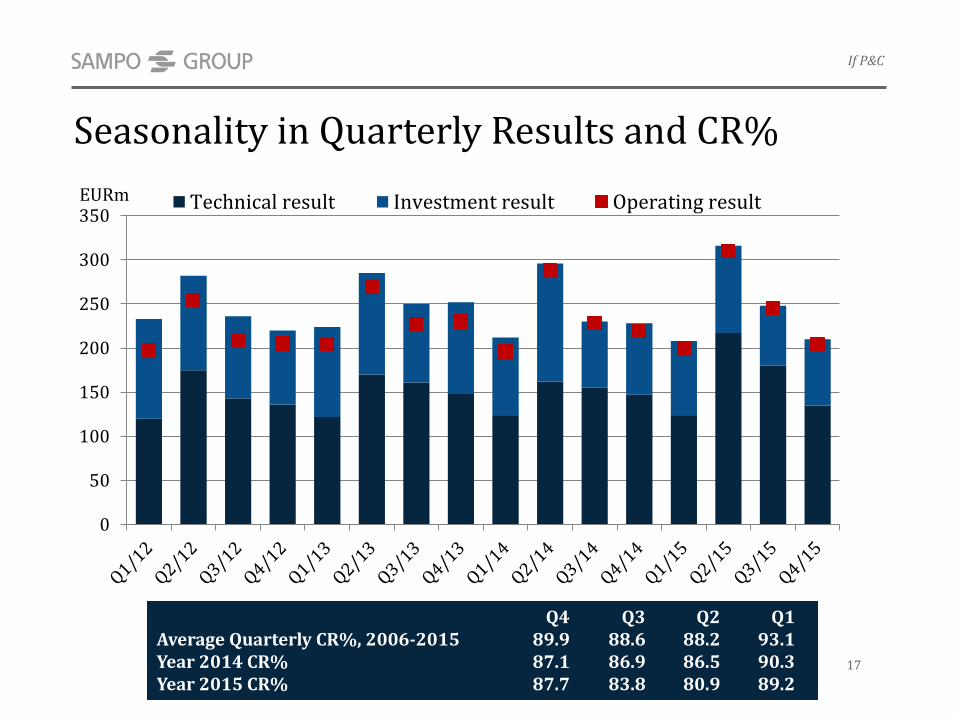

350Technical result Investment result Operating result

Seasonality in Quarterly Results and CR%

Q4 Q3 Q2 Q1Average Quarterly CR%, 2006-2015 89.9 88.6 88.2 93.1Year 2014 CR% 87.1 86.9 86.5 90.3Year 2015 CR% 87.7 83.8 80.9 89.2

If P&C

17

EURm

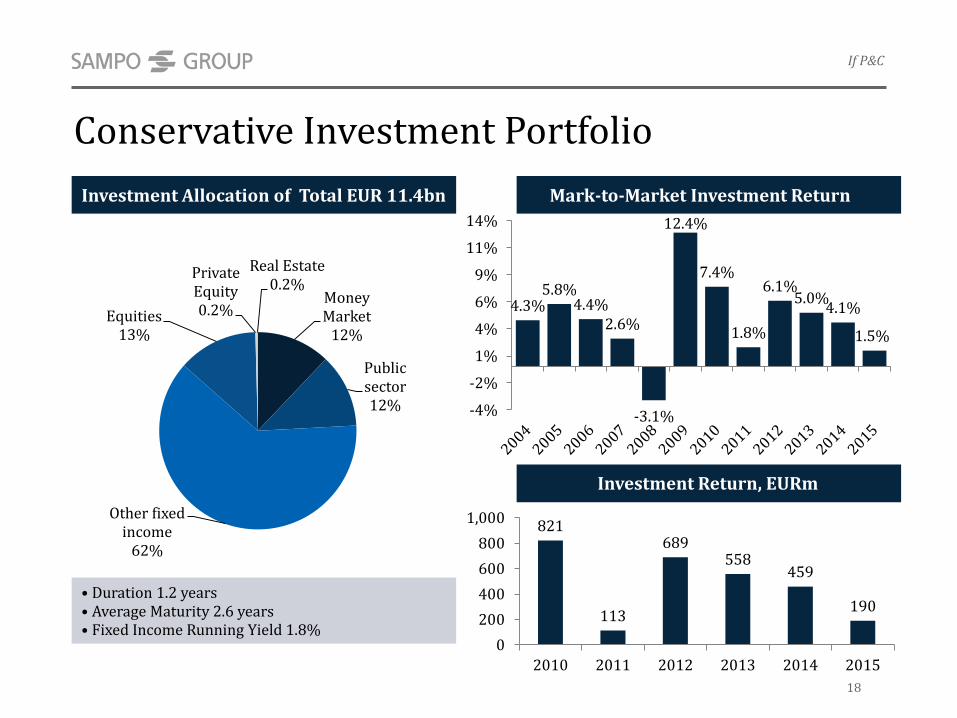

Conservative Investment Portfolio

• Duration 1.2 years• Average Maturity 2.6 years• Fixed Income Running Yield 1.8%

Mark-to-Market Investment ReturnInvestment Allocation of Total EUR 11.4bn

4.3%5.8%

4.4%2.6%

-3.1%

12.4%

7.4%

1.8%

6.1%5.0%

4.1%

1.5%

-4%

-2%

1%

4%

6%

9%

11%

14%

Money Market

12%

Public sector12%

Other fixed income

62%

Equities13%

Private Equity0.2%

Real Estate0.2%

18

If P&C

821

113

689558

459

190

0

200

400

600

800

1,000

2010 2011 2012 2013 2014 2015

Investment Return, EURm

75

7

1,3

88

211

82

8

176 139 128

1,6

92

3,3

77

3,0

58

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Partial Internal Model (PIM)EURm

If P&C

19

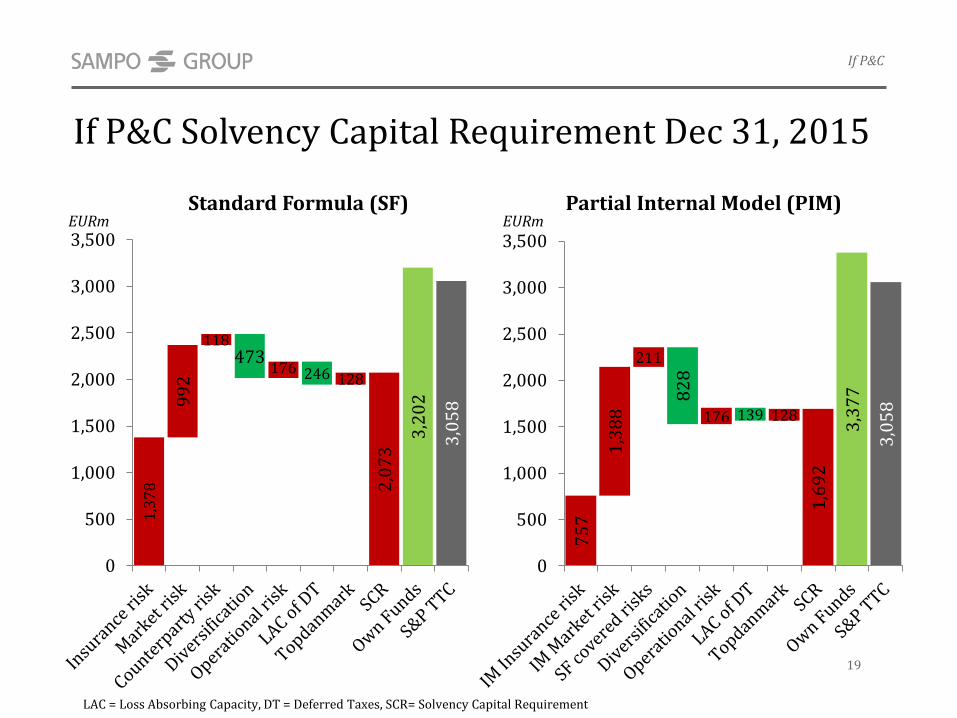

If P&C Solvency Capital Requirement Dec 31, 20151

,37

8

99

2

118473

176 246 1282

,07

3

3,2

02

3,0

58

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Standard Formula (SF)

LAC = Loss Absorbing Capacity, DT = Deferred Taxes, SCR= Solvency Capital Requirement

EURm

20

Sampo Group Basic Facts 3-10If P&C The Leading Nordic P&C Insurer 11-19Mandatum Life A Finnish Financial Services Company 20-28Sampo Group A Productive Value Creator 29-36Sampo plc The Listed Parent Company – A Stable Dividend Payer 37-43

Appendix 44-57

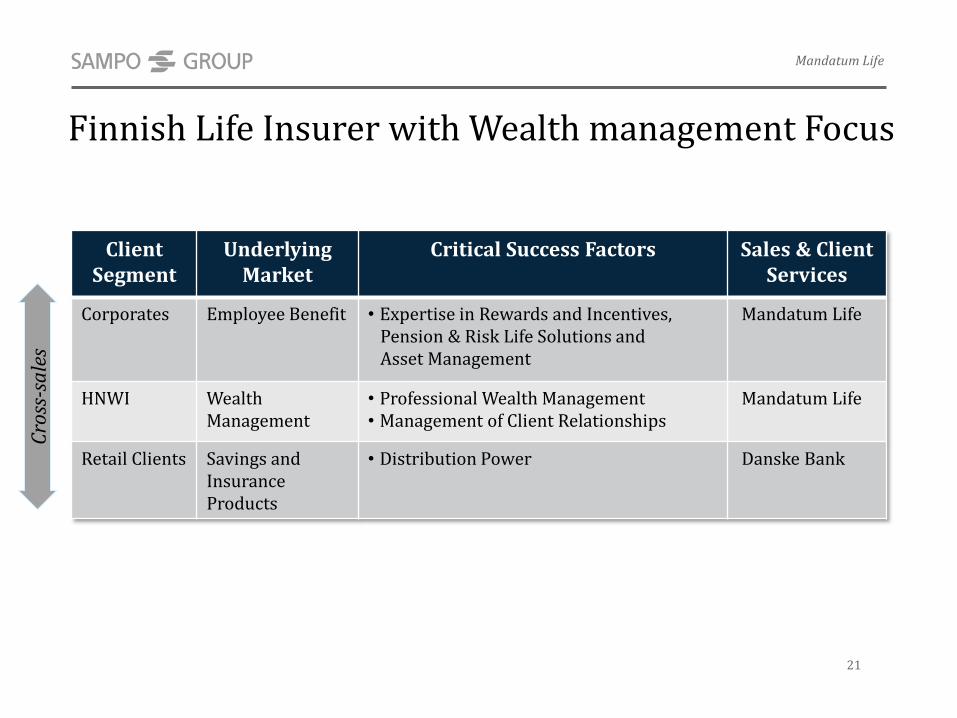

Finnish Life Insurer with Wealth management Focus

ClientSegment

UnderlyingMarket

Critical Success Factors Sales & ClientServices

Corporates Employee Benefit • Expertise in Rewards and Incentives, Pension & Risk Life Solutions and Asset Management

Mandatum Life

HNWI WealthManagement

• Professional Wealth Management• Management of Client Relationships

Mandatum Life

Retail Clients Savings and Insurance Products

• Distribution Power Danske Bank

Mandatum Life

21

Cro

ss-s

ale

s

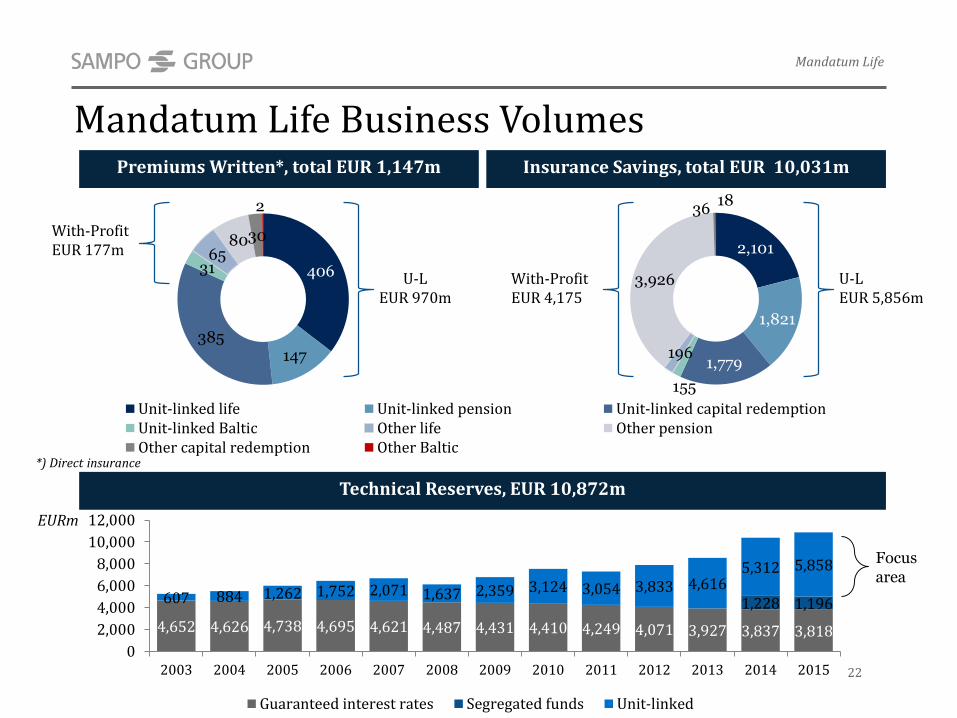

Premiums Written*, total EUR 1,147m Insurance Savings, total EUR 10,031m

*) Direct insurance

406

147385

3165

8030

2

Unit-linked life Unit-linked pension Unit-linked capital redemptionUnit-linked Baltic Other life Other pensionOther capital redemption Other Baltic

2,101

1,821

1,779

155

196

3,926

3618

Mandatum Life Business Volumes

U-LEUR 5,856m

With-ProfitEUR 4,175

U-L EUR 970m

With-ProfitEUR 177m

Focus area

4,652 4,626 4,738 4,695 4,621 4,487 4,431 4,410 4,249 4,071 3,927 3,837 3,818

1,228 1,196607 884 1,262 1,752 2,071 1,637 2,359 3,124 3,054 3,833 4,6165,312 5,858

0

2,000

4,000

6,000

8,000

10,000

12,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Guaranteed interest rates Segregated funds Unit-linked

Technical Reserves, EUR 10,872m

EURm

Mandatum Life

22

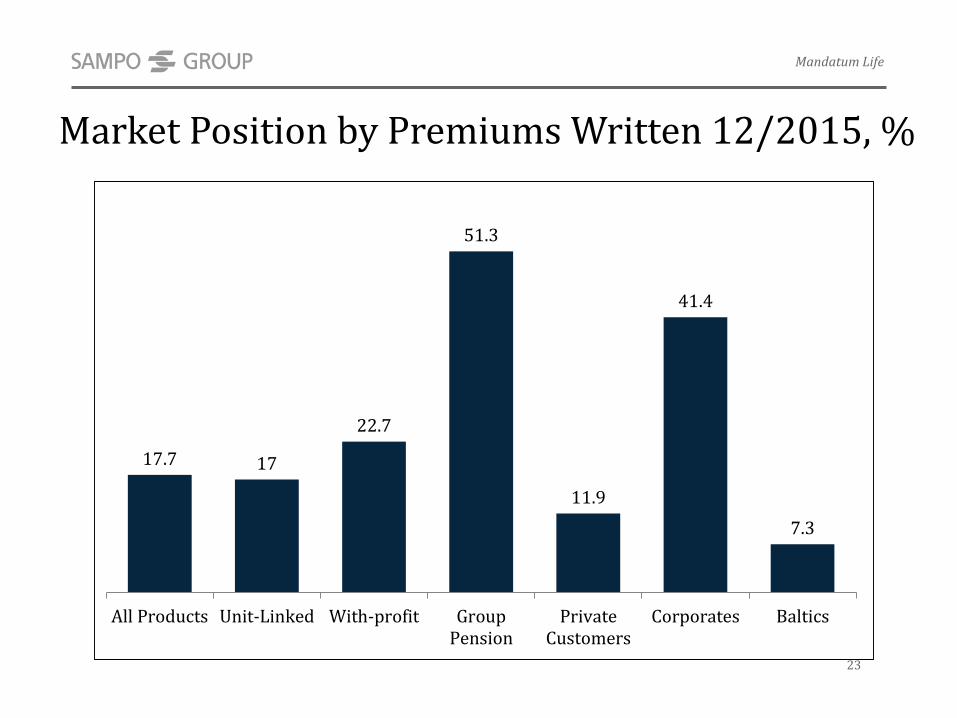

Market Position by Premiums Written 12/2015, %

Market Shares in Finland

Mandatum Life

23

17.7 17

22.7

51.3

11.9

41.4

7.3

All Products Unit-Linked With-profit GroupPension

PrivateCustomers

Corporates Baltics

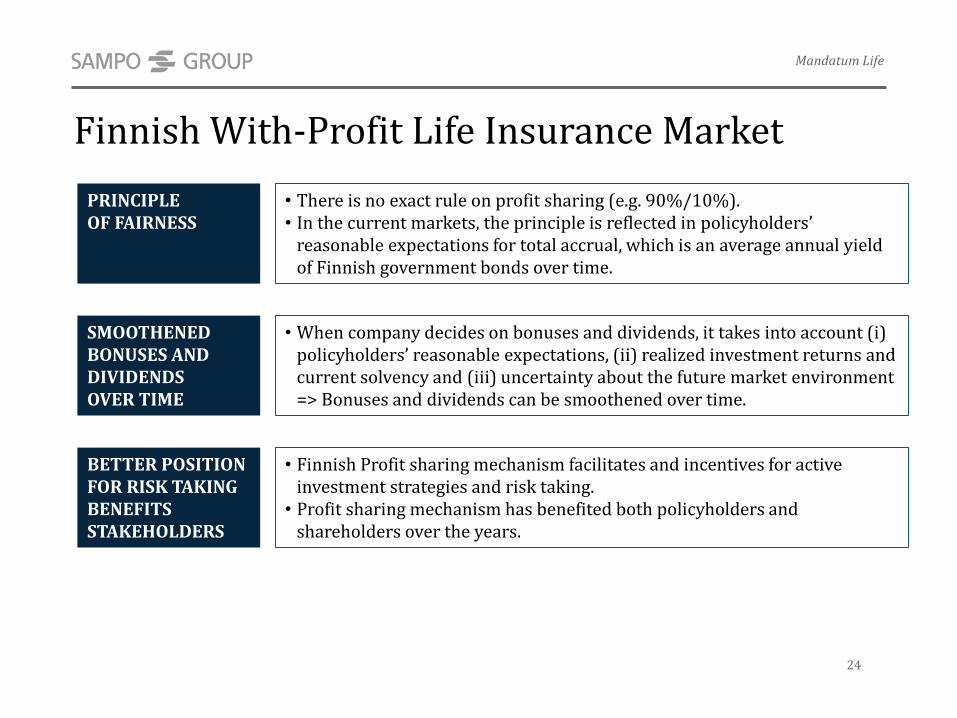

Finnish With-Profit Life Insurance Market

PRINCIPLE OF FAIRNESS

• There is no exact rule on profit sharing (e.g. 90%/10%). • In the current markets, the principle is reflected in policyholdersʼ

reasonable expectations for total accrual, which is an average annual yield of Finnish government bonds over time.

SMOOTHENED BONUSES AND DIVIDENDS OVER TIME

• When company decides on bonuses and dividends, it takes into account (i) policyholdersʼ reasonable expectations, (ii) realized investment returns and current solvency and (iii) uncertainty about the future market environment => Bonuses and dividends can be smoothened over time.

BETTER POSITION FOR RISK TAKING BENEFITS STAKEHOLDERS

• Finnish Profit sharing mechanism facilitates and incentives for active investment strategies and risk taking.

• Profit sharing mechanism has benefited both policyholders and shareholders over the years.

Mandatum Life

24

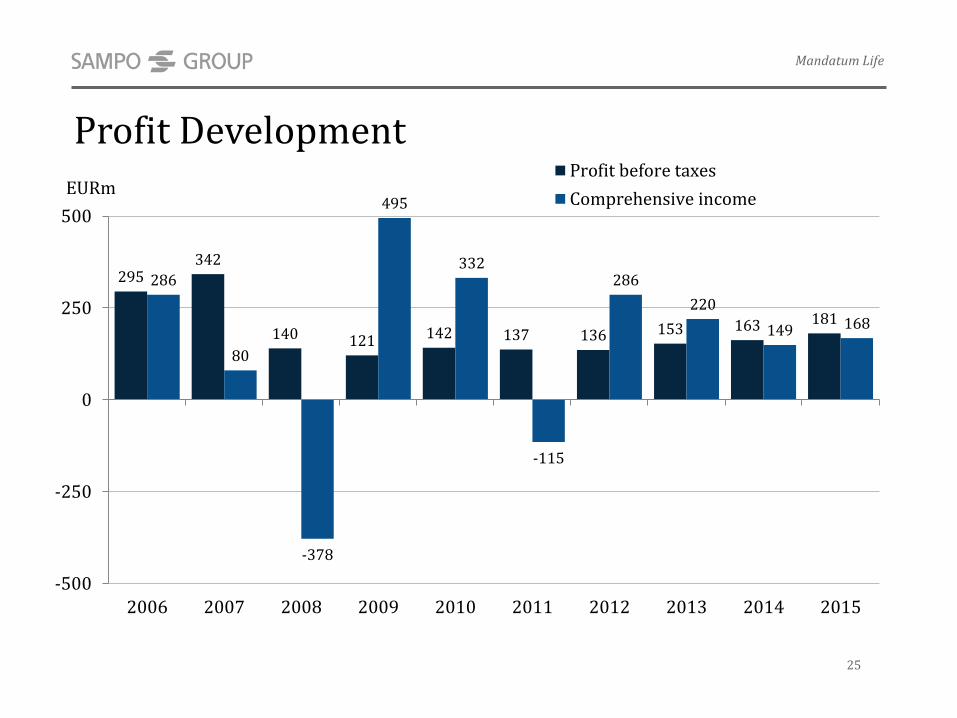

Profit Development

295342

140 121 142 137 136 153 163 181

286

80

-378

495

332

-115

286

220

149 168

-500

-250

0

250

500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

EURmProfit before taxes

Comprehensive income

Mandatum Life

25

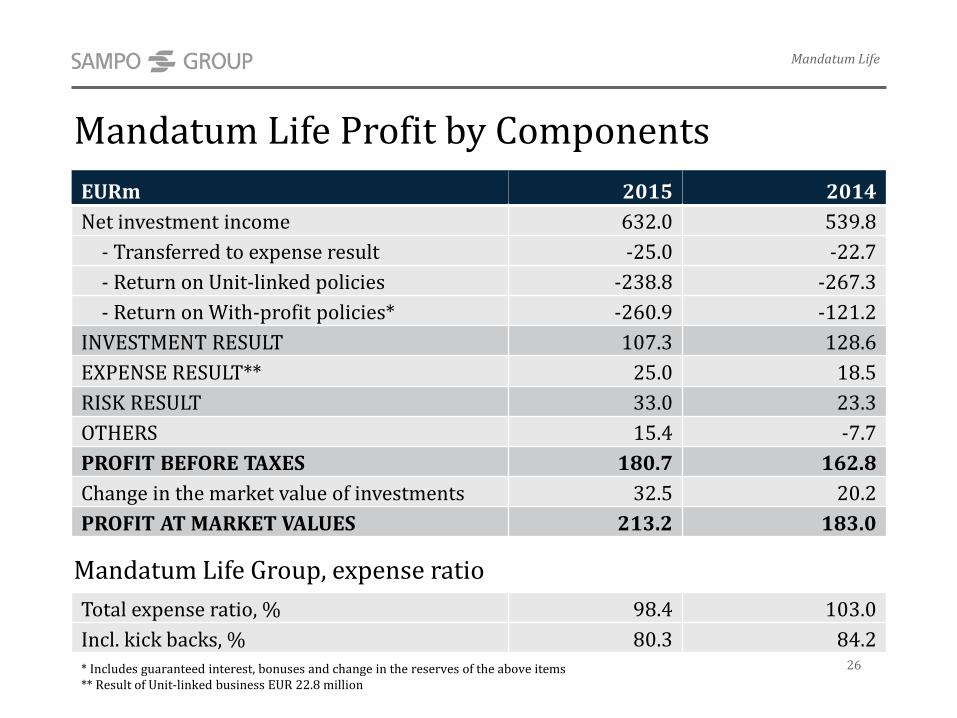

Mandatum Life Profit by Components

Mandatum Life Group, expense ratio

Mandatum Life

26

Total expense ratio, % 98.4 103.0

Incl. kick backs, % 80.3 84.2

* Includes guaranteed interest, bonuses and change in the reserves of the above items** Result of Unit-linked business EUR 22.8 million

EURm 2015 2014

Net investment income 632.0 539.8

- Transferred to expense result -25.0 -22.7

- Return on Unit-linked policies -238.8 -267.3

- Return on With-profit policies* -260.9 -121.2

INVESTMENT RESULT 107.3 128.6

EXPENSE RESULT** 25.0 18.5

RISK RESULT 33.0 23.3

OTHERS 15.4 -7.7

PROFIT BEFORE TAXES 180.7 162.8

Change in the market value of investments 32.5 20.2

PROFIT AT MARKET VALUES 213.2 183.0

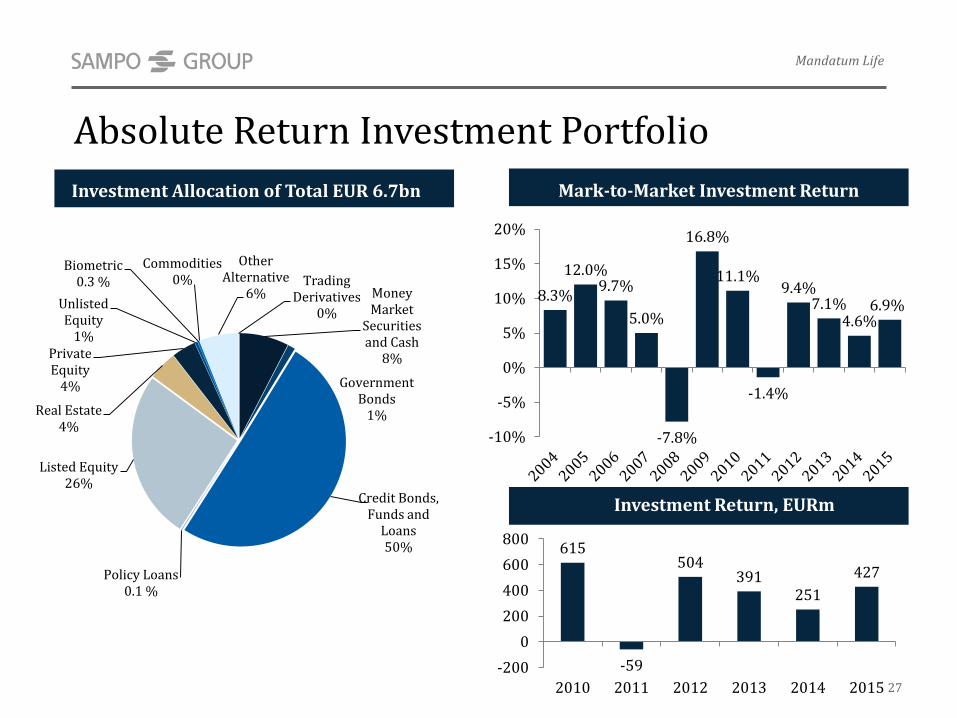

Absolute Return Investment Portfolio

Mark-to-Market Investment ReturnInvestment Allocation of Total EUR 6.7bn

8.3%

12.0%9.7%

5.0%

-7.8%

16.8%

11.1%

-1.4%

9.4%7.1%

4.6%6.9%

-10%

-5%

0%

5%

10%

15%

20%

Mandatum Life

27

615

-59

504391

251

427

-200

0

200

400

600

800

2010 2011 2012 2013 2014 2015

Investment Return, EURm

Money Market

Securities and Cash

8%

Government Bonds

1%

Credit Bonds, Funds and

Loans50%

Policy Loans0.1 %

Listed Equity26%

Real Estate4%

Private Equity

4%

Unlisted Equity

1%

Biometric0.3 %

Commodities0%

Other Alternative

6%Trading

Derivatives0%

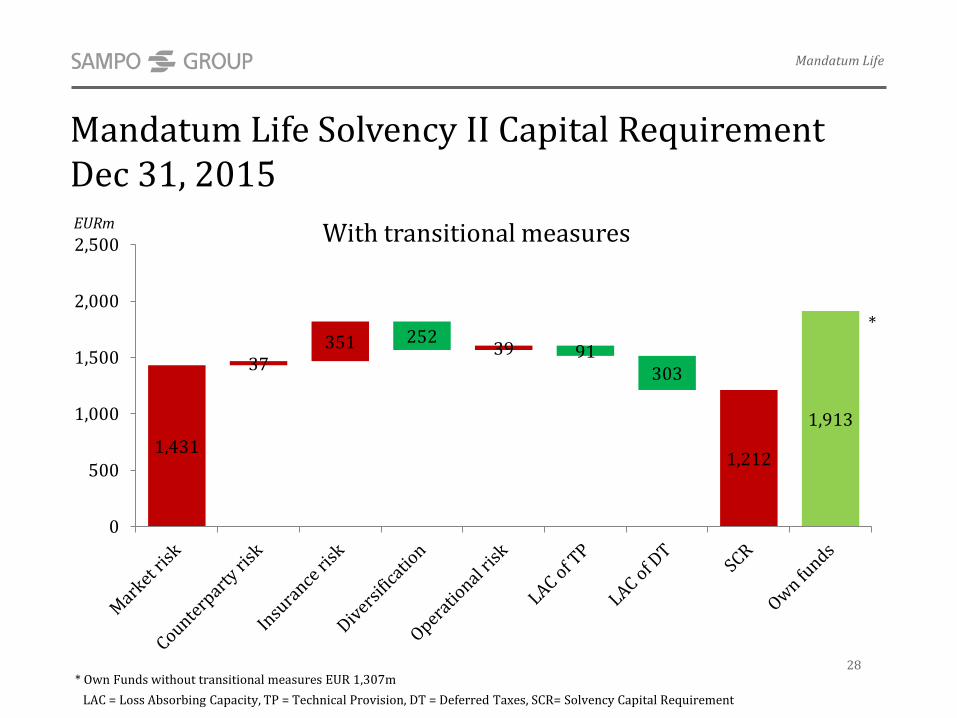

Mandatum Life Solvency II Capital RequirementDec 31, 2015

LAC = Loss Absorbing Capacity, TP = Technical Provision, DT = Deferred Taxes, SCR= Solvency Capital Requirement

*

* Own Funds without transitional measures EUR 1,307m

EURm

Mandatum Life

28

1,431

37351 252

39 91303

1,212

1,913

0

500

1,000

1,500

2,000

2,500 With transitional measures

29

Sampo Group Basic Facts 3-10If P&C The Leading Nordic P&C Insurer 11-19Mandatum Life A Finnish Financial Services Company 20-28Sampo Group A Productive Value Creator 29-36Sampo plc The Listed Parent Company - A Stable Dividend Payer 37-43

Appendix 44-57

948

1,295 1,353

870 825

1,320 1,228

1,622 1,668 1,759 1,888

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

P&C Life Banking Nordea dividends Other

Stable Development of Profit before Taxes

* One-off item – sale of Sampo Bank

EURm

*• If P&C• Mandatum Life• Sampo Bank

• If P&C• Mandatum

Life• Nordea /

Investment

• If P&C• Topdanmark / Associated• Mandatum Life• Nordea / Associated

Sampo Group ― Results, Capitalisation and Investments

30

3,833

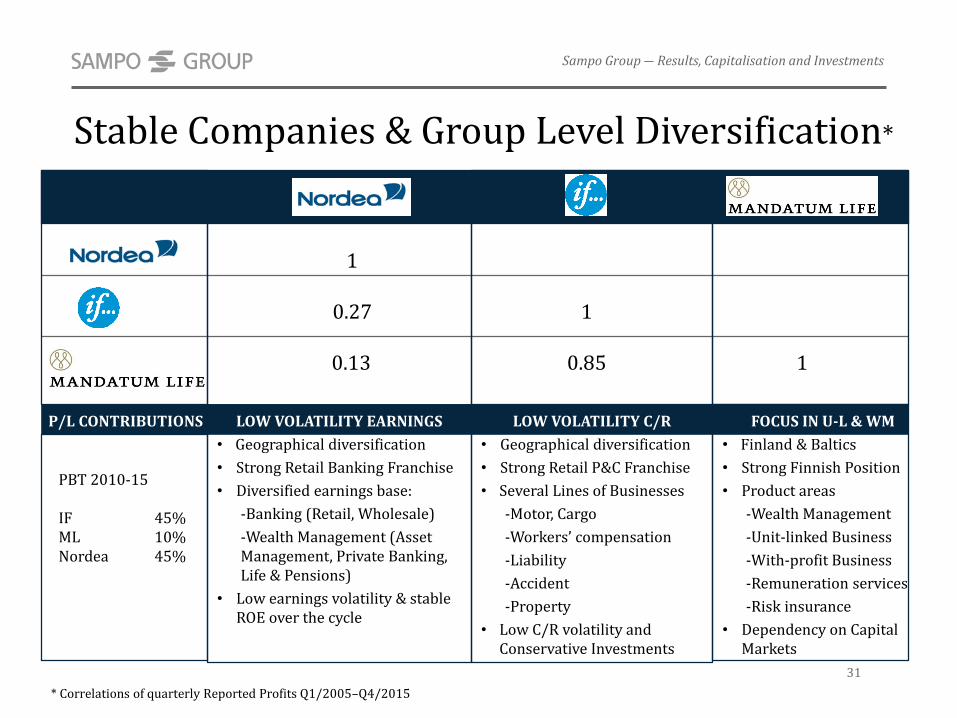

Stable Companies & Group Level Diversification*

LOW VOLATILITY EARNINGS

• Geographical diversification

• Strong Retail Banking Franchise

• Diversified earnings base:

-Banking (Retail, Wholesale)

-Wealth Management (AssetManagement, Private Banking, Life & Pensions)

• Low earnings volatility & stableROE over the cycle

LOW VOLATILITY C/R

• Geographical diversification

• Strong Retail P&C Franchise

• Several Lines of Businesses

-Motor, Cargo

-Workersʼ compensation

-Liability

-Accident

-Property

• Low C/R volatility and Conservative Investments

FOCUS IN U-L & WM

• Finland & Baltics

• Strong Finnish Position

• Product areas

-Wealth Management

-Unit-linked Business

-With-profit Business

-Remuneration services

-Risk insurance

• Dependency on Capital Markets

1

0.27 1

0.13 0.85 1

* Correlations of quarterly Reported Profits Q1/2005–Q4/2015

PBT 2010-15

IF 45%ML 10%Nordea 45%

P/L CONTRIBUTIONS

Sampo Group ― Results, Capitalisation and Investments

31

2,073

1,212

3,770

59

7,114

10,294

0

2,000

4,000

6,000

8,000

10,000

12,000

If P&C Mandatum Life Sampo plc'sshare of Nordea

Sampo plc Total capitalrequirement

GroupSolvency Capital

881269

3,770

59

4,983

9,599

0

2,000

4,000

6,000

8,000

10,000

12,000

If P&C Mandatum Life Sampo plc'sshare of Nordea

Sampo plc Total capitalrequirement

GroupSolvency Capital

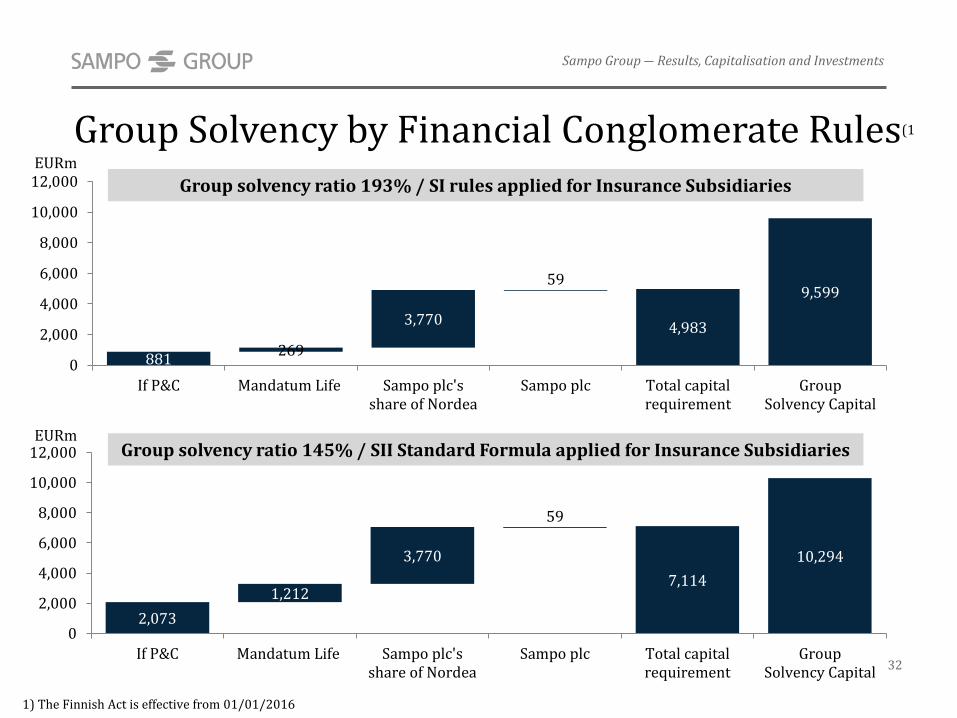

Group Solvency by Financial Conglomerate Rules(1

Sampo Group ― Results, Capitalisation and Investments

32

EURmGroup solvency ratio 145% / SII Standard Formula applied for Insurance Subsidiaries

1) The Finnish Act is effective from 01/01/2016

Group solvency ratio 193% / SI rules applied for Insurance Subsidiaries

EURm

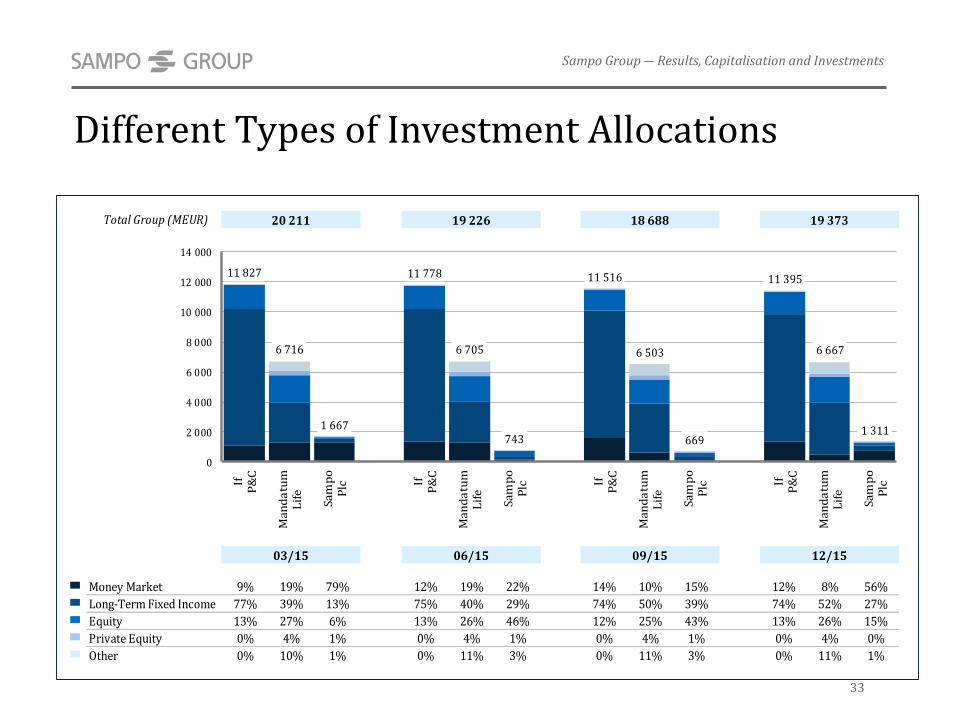

Different Types of Investment Allocations

Sampo Group ― Results, Capitalisation and Investments

33

Total Group (MEUR) 20 211 19 226 18 688 19 373

03/15 06/15 09/15 12/15

Money Market 9% 19% 79% 12% 19% 22% 14% 10% 15% 12% 8% 56%

Long-Term Fixed Income 77% 39% 13% 75% 40% 29% 74% 50% 39% 74% 52% 27%

Equity 13% 27% 6% 13% 26% 46% 12% 25% 43% 13% 26% 15%

Private Equity 0% 4% 1% 0% 4% 1% 0% 4% 1% 0% 4% 0%

Other 0% 10% 1% 0% 11% 3% 0% 11% 3% 0% 11% 1%

11 827

6 716

1 667

11 778

6 705

743

11 516

6 503

669

11 395

6 667

1 311

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

IfP

&C

Man

da

tum

Lif

e

Sam

po

Plc If

P&

C

Man

da

tum

Lif

e

Sam

po

Plc If

P&

C

Man

da

tum

Lif

e

Sam

po

Plc If

P&

C

Man

da

tum

Lif

e

Sam

po

Plc

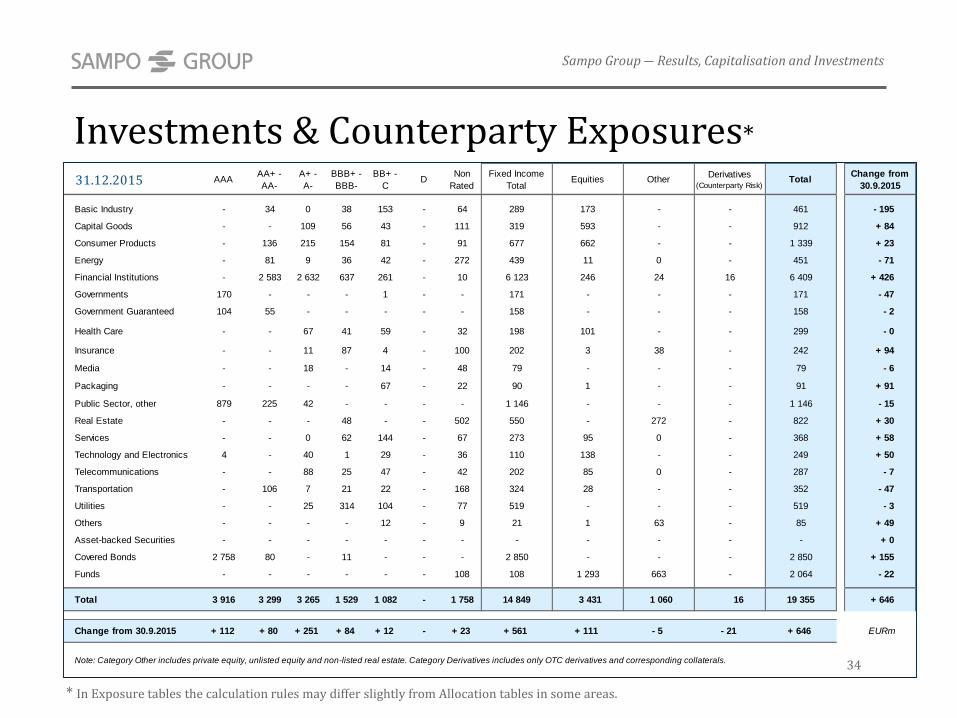

Investments & Counterparty Exposures*

* In Exposure tables the calculation rules may differ slightly from Allocation tables in some areas.

Sampo Group ― Results, Capitalisation and Investments

34

31.12.2015 AAAAA+ -

AA-

A+ -

A-

BBB+ -

BBB-

BB+ -

CD

Non

Rated

Fixed Income

TotalEquities Other

Derivatives (Counterparty Risk)

TotalChange from

30.9.2015

Basic Industry - 34 0 38 153 - 64 289 173 - - 461 - 195

Capital Goods - - 109 56 43 - 111 319 593 - - 912 + 84

Consumer Products - 136 215 154 81 - 91 677 662 - - 1 339 + 23

Energy - 81 9 36 42 - 272 439 11 0 - 451 - 71

Financial Institutions - 2 583 2 632 637 261 - 10 6 123 246 24 16 6 409 + 426

Governments 170 - - - 1 - - 171 - - - 171 - 47

Government Guaranteed 104 55 - - - - - 158 - - - 158 - 2

Health Care - - 67 41 59 - 32 198 101 - - 299 - 0

Insurance - - 11 87 4 - 100 202 3 38 - 242 + 94

Media - - 18 - 14 - 48 79 - - - 79 - 6

Packaging - - - - 67 - 22 90 1 - - 91 + 91

Public Sector, other 879 225 42 - - - - 1 146 - - - 1 146 - 15

Real Estate - - - 48 - - 502 550 - 272 - 822 + 30

Services - - 0 62 144 - 67 273 95 0 - 368 + 58

Technology and Electronics 4 - 40 1 29 - 36 110 138 - - 249 + 50

Telecommunications - - 88 25 47 - 42 202 85 0 - 287 - 7

Transportation - 106 7 21 22 - 168 324 28 - - 352 - 47

Utilities - - 25 314 104 - 77 519 - - - 519 - 3

Others - - - - 12 - 9 21 1 63 - 85 + 49

Asset-backed Securities - - - - - - - - - - - - + 0

Covered Bonds 2 758 80 - 11 - - - 2 850 - - - 2 850 + 155

Funds - - - - - - 108 108 1 293 663 - 2 064 - 22

Total 3 916 3 299 3 265 1 529 1 082 - 1 758 14 849 3 431 1 060 16 19 355 + 646

Change from 30.9.2015 + 112 + 80 + 251 + 84 + 12 - + 23 + 561 + 111 - 5 - 21 + 646 EURm

Note: Category Other includes private equity, unlisted equity and non-listed real estate. Category Derivatives includes only OTC derivatives and corresponding collaterals.

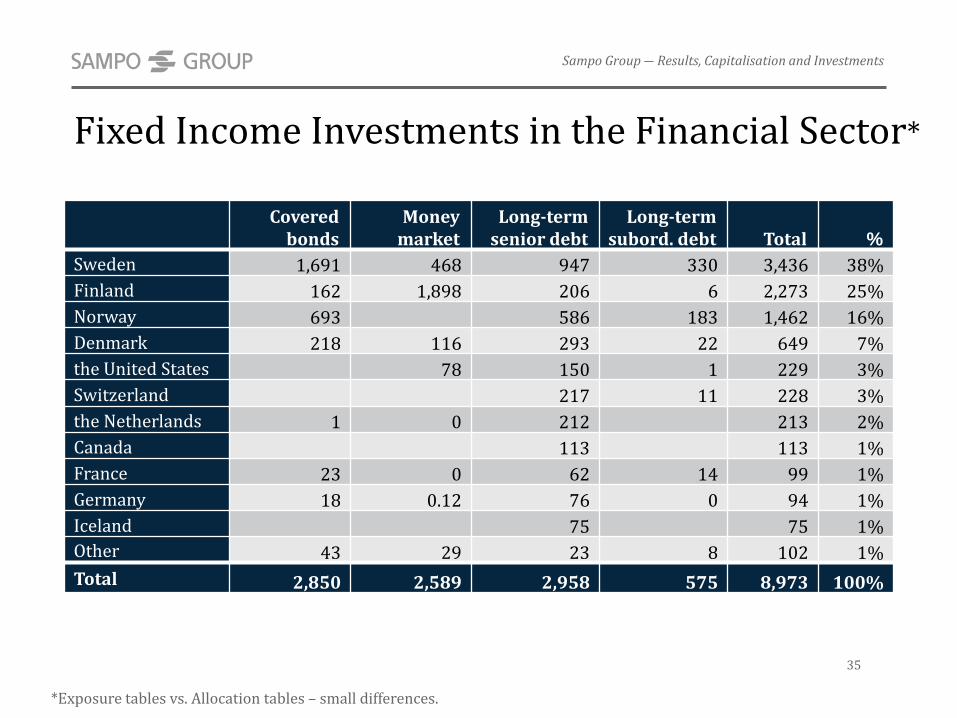

Fixed Income Investments in the Financial Sector*

*Exposure tables vs. Allocation tables – small differences.

Sampo Group ― Results, Capitalisation and Investments

35

Covered bonds

Money market

Long-term senior debt

Long-term subord. debt Total %

Sweden 1,691 468 947 330 3,436 38%

Finland 162 1,898 206 6 2,273 25%

Norway 693 586 183 1,462 16%

Denmark 218 116 293 22 649 7%

the United States 78 150 1 229 3%

Switzerland 217 11 228 3%

the Netherlands 1 0 212 213 2%

Canada 113 113 1%

France 23 0 62 14 99 1%

Germany 18 0.12 76 0 94 1%

Iceland 75 75 1%

Other 43 29 23 8 102 1%

Total 2,850 2,589 2,958 575 8,973 100%

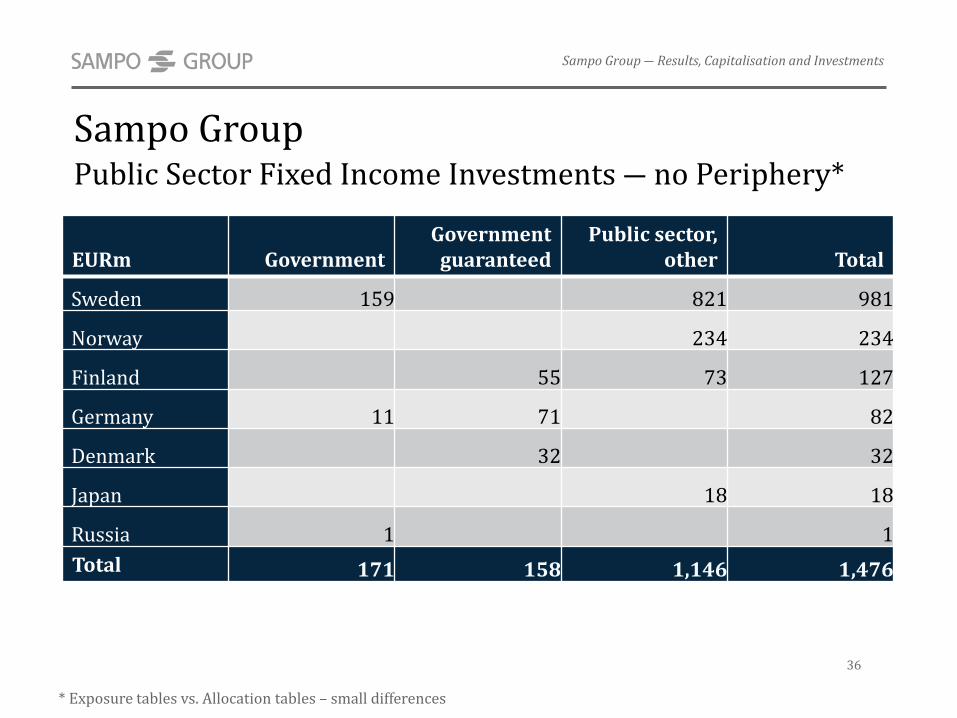

Sampo Group Public Sector Fixed Income Investments ― no Periphery*

* Exposure tables vs. Allocation tables – small differences

36

Sampo Group ― Results, Capitalisation and Investments

EURm GovernmentGovernment

guaranteedPublic sector,

other Total

Sweden 159 821 981

Norway 234 234

Finland 55 73 127

Germany 11 71 82

Denmark 32 32

Japan 18 18

Russia 1 1

Total 171 158 1,146 1,476

37

Sampo Group Basic Facts 3-10If P&C The Leading Nordic P&C Insurer 11-19Mandatum Life A Finnish Financial Services Company 20-28Sampo Group A Productive Value Creator 29-36Sampo plc The Listed Parent Company – A Stable Dividend Payer 37-43

Appendix 44-57

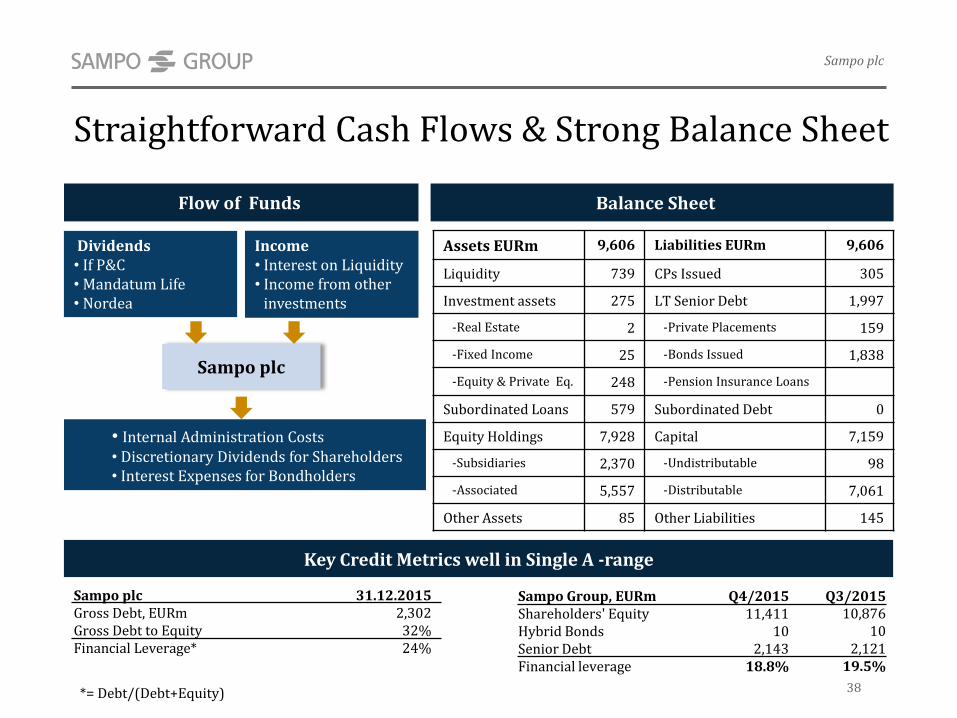

Straightforward Cash Flows & Strong Balance Sheet

Dividends • If P&C• Mandatum Life• Nordea

• Internal Administration Costs• Discretionary Dividends for Shareholders• Interest Expenses for Bondholders

Income• Interest on Liquidity • Income from other

investments

Sampo plc

Assets EURm 9,606 Liabilities EURm 9,606

Liquidity 739 CPs Issued 305

Investment assets 275 LT Senior Debt 1,997

-Real Estate 2 -Private Placements 159

-Fixed Income 25 -Bonds Issued 1,838

-Equity & Private Eq. 248 -Pension Insurance Loans

Subordinated Loans 579 Subordinated Debt 0

Equity Holdings 7,928 Capital 7,159

-Subsidiaries 2,370 -Undistributable 98

-Associated 5,557 -Distributable 7,061

Other Assets 85 Other Liabilities 145

Flow of Funds Balance Sheet

Key Credit Metrics well in Single A -range

Sampo plc 31.12.2015Gross Debt, EURm 2,302Gross Debt to Equity 32%Financial Leverage* 24%

Sampo Group, EURm Q4/2015 Q3/2015 Shareholders' Equity 11,411 10,876 Hybrid Bonds 10 10 Senior Debt 2,143 2,121Financial leverage 18.8% 19.5%

Sampo plc

38*= Debt/(Debt+Equity)

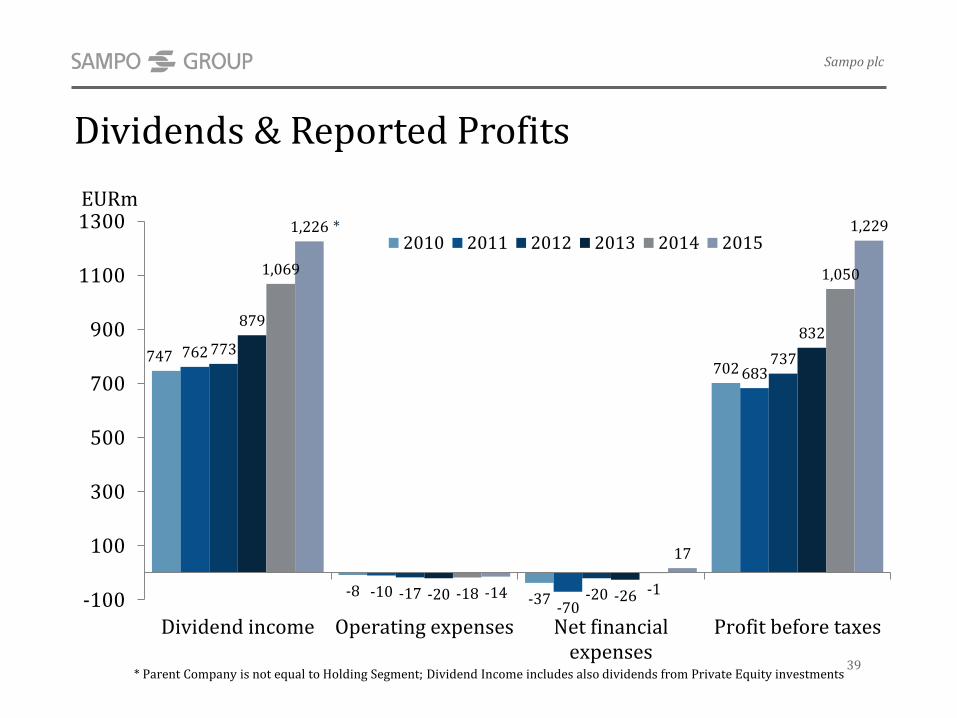

Dividends & Reported Profits

* Parent Company is not equal to Holding Segment; Dividend Income includes also dividends from Private Equity investments

747

-8 -37

702762

-10-70

683

773

-17 -20

737

879

-20 -26

832

1,069

-18 -1

1,050

1,226

-14

17

1,229

-100

100

300

500

700

900

1100

1300

Dividend income Operating expenses Net financialexpenses

Profit before taxes

2010 2011 2012 2013 2014 2015*

EURm

Sampo plc

39

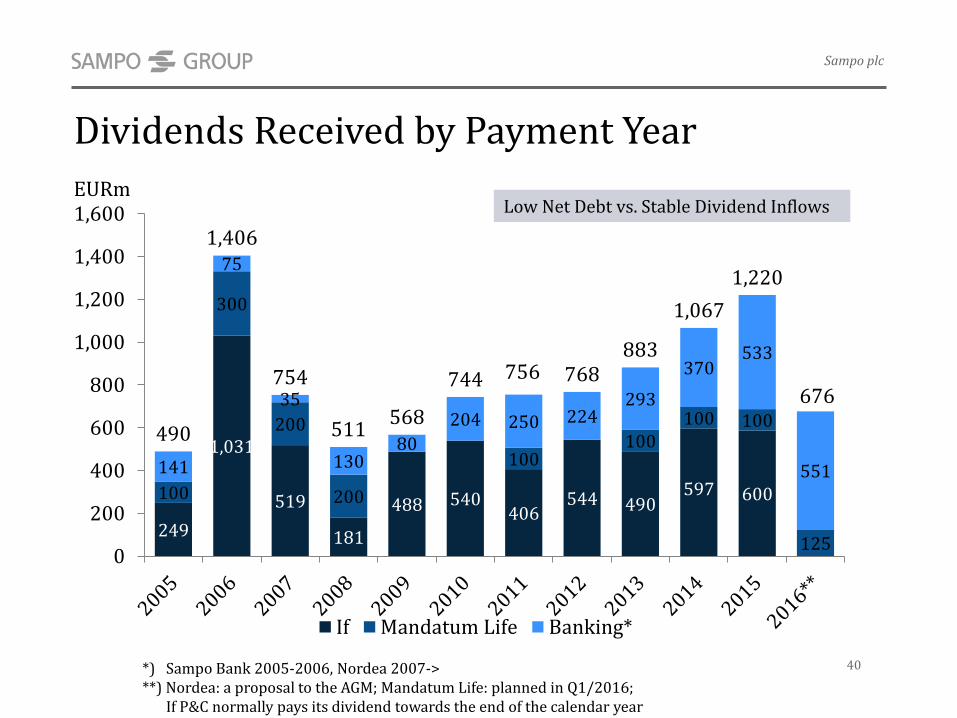

Dividends Received by Payment Year

EURm

249

1,031

519

181

488 540406

544 490597 600100

300

200

200

100100

100 100

125

141

75

35

13080

204 250 224293

370533

551

490

1,406

754

511568

744 756 768883

1,067

1,220

0

200

400

600

800

1,000

1,200

1,400

1,600

If Mandatum Life Banking*

Sampo plc

40

Low Net Debt vs. Stable Dividend Inflows

*) Sampo Bank 2005-2006, Nordea 2007->**) Nordea: a proposal to the AGM; Mandatum Life: planned in Q1/2016;

If P&C normally pays its dividend towards the end of the calendar year

676

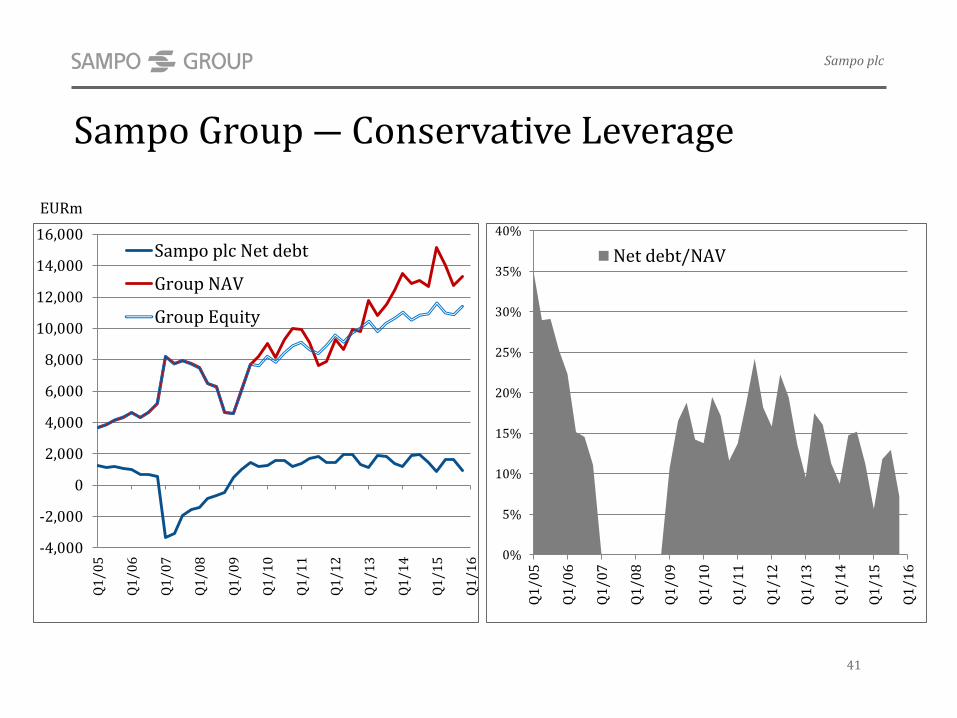

Sampo Group ― Conservative Leverage

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Q1

/05

Q1

/06

Q1

/07

Q1

/08

Q1

/09

Q1

/10

Q1

/11

Q1

/12

Q1

/13

Q1

/14

Q1

/15

Q1

/16

Sampo plc Net debt

Group NAV

Group Equity

41

Sampo plc

EURm

0%

5%

10%

15%

20%

25%

30%

35%

40%

Q1

/05

Q1

/06

Q1

/07

Q1

/08

Q1

/09

Q1

/10

Q1

/11

Q1

/12

Q1

/13

Q1

/14

Q1

/15

Q1

/16

Net debt/NAV

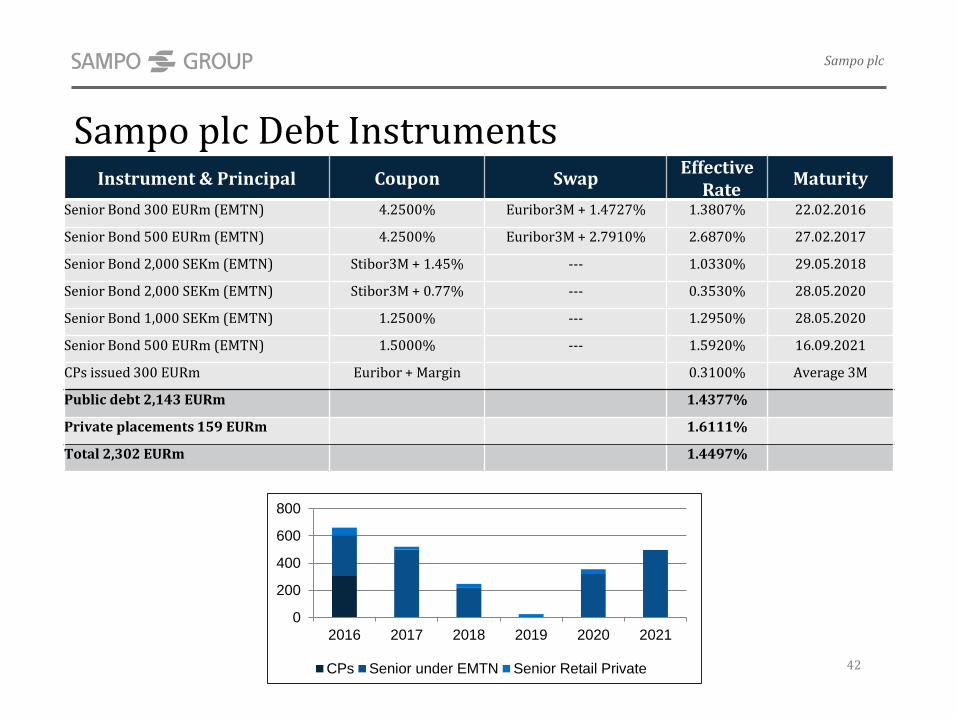

Sampo plc Debt Instruments

42

Sampo plc

EURm

Instrument & Principal Coupon SwapEffective

RateMaturity

Senior Bond 300 EURm (EMTN) 4.2500% Euribor3M + 1.4727% 1.3807% 22.02.2016

Senior Bond 500 EURm (EMTN) 4.2500% Euribor3M + 2.7910% 2.6870% 27.02.2017

Senior Bond 2,000 SEKm (EMTN) Stibor3M + 1.45% --- 1.0330% 29.05.2018

Senior Bond 2,000 SEKm (EMTN) Stibor3M + 0.77% --- 0.3530% 28.05.2020

Senior Bond 1,000 SEKm (EMTN) 1.2500% --- 1.2950% 28.05.2020

Senior Bond 500 EURm (EMTN) 1.5000% --- 1.5920% 16.09.2021

CPs issued 300 EURm Euribor + Margin 0.3100% Average 3M

Public debt 2,143 EURm 1.4377%

Private placements 159 EURm 1.6111%

Total 2,302 EURm 1.4497%

0

200

400

600

800

2016 2017 2018 2019 2020 2021

CPs Senior under EMTN Senior Retail Private

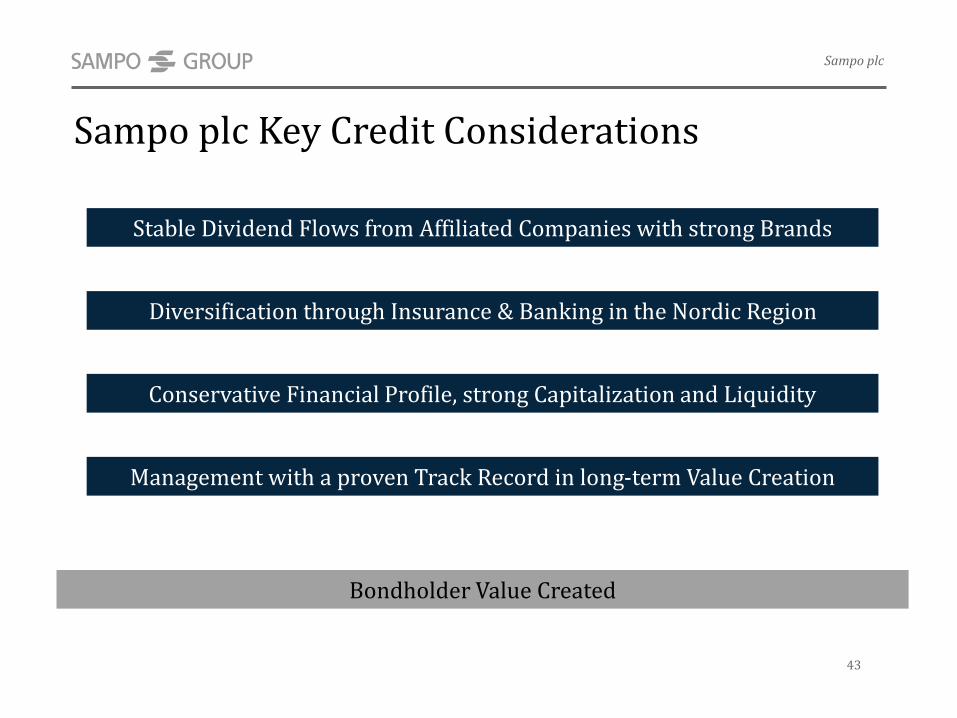

Sampo plc Key Credit Considerations

Diversification through Insurance & Banking in the Nordic Region

Management with a proven Track Record in long-term Value Creation

Conservative Financial Profile, strong Capitalization and Liquidity

Stable Dividend Flows from Affiliated Companies with strong Brands

Bondholder Value Created

Sampo plc

43

44

Appendix 44-57

45

Sampo Group’s Outlook for 2016

Appendix

• Sampo Group’s business areas are expected to report good operating results for 2016.

• However, the mark-to-market results are, particularly in life insurance, highly dependent on capital market developments. The continuing low interest rate level also creates a challenging environment for reinvestment in fixed income instruments.

• The P&C insurance operations are expected to reach their long-term combined ratio target of below 95 per cent in 2016 by a margin.

• Nordea’s contribution to the Group’s profit is expected to be significant.

Principles of Investment Management

• Company specific needs form the basis for all investments

– Liabilities intensively analysed and modelled.

– Regulatory requirements.

• Strategy

– Absolute Return targets taking into account the liabilities and general business targets.

– Direct Investments into Nordic countries mainly, outside Nordics Funds mainly.

– No diversification for the sake of diversification.

• Centrally Managed

– Sampo plc Chief Investment Officer responsible for all investments, all portfolio managers have a direct reporting line to him.

– Common infrastructure for investment administration and reporting.

– Investment strategies coordinated and streamlined, no overlapping activities

to prevent Group wide concentrations.

46

Appendix

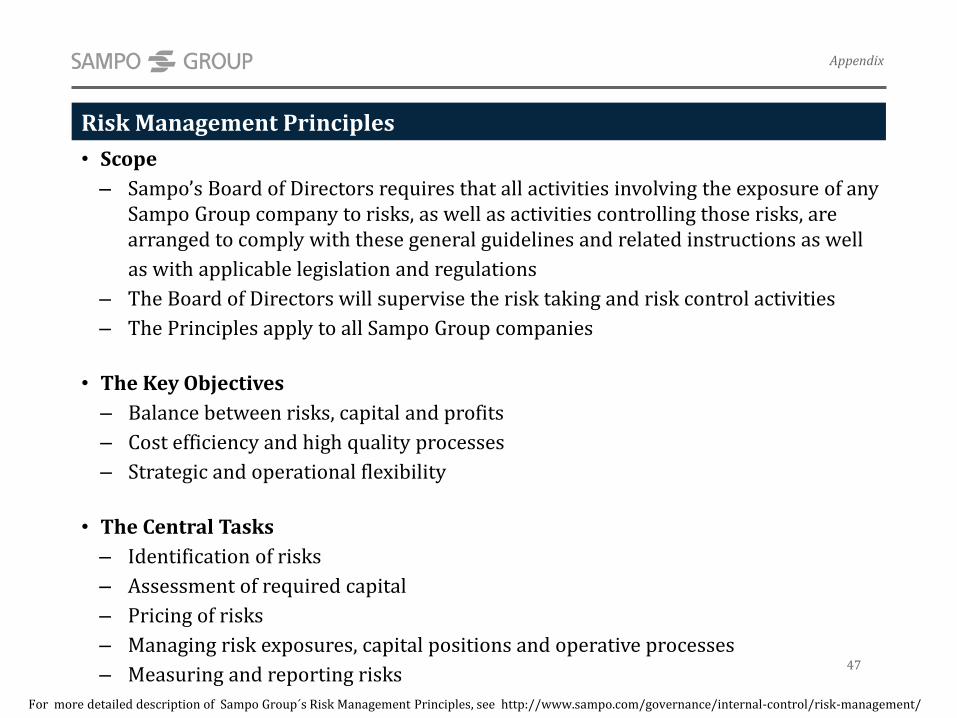

Risk Management Principles

• Scope

– Sampo’s Board of Directors requires that all activities involving the exposure of any Sampo Group company to risks, as well as activities controlling those risks, are arranged to comply with these general guidelines and related instructions as well

as with applicable legislation and regulations

– The Board of Directors will supervise the risk taking and risk control activities

– The Principles apply to all Sampo Group companies

• The Key Objectives

– Balance between risks, capital and profits

– Cost efficiency and high quality processes

– Strategic and operational flexibility

• The Central Tasks

– Identification of risks

– Assessment of required capital

– Pricing of risks

– Managing risk exposures, capital positions and operative processes

– Measuring and reporting risks47

Appendix

For more detailed description of Sampo Group´s Risk Management Principles, see http://www.sampo.com/governance/internal-control/risk-management/

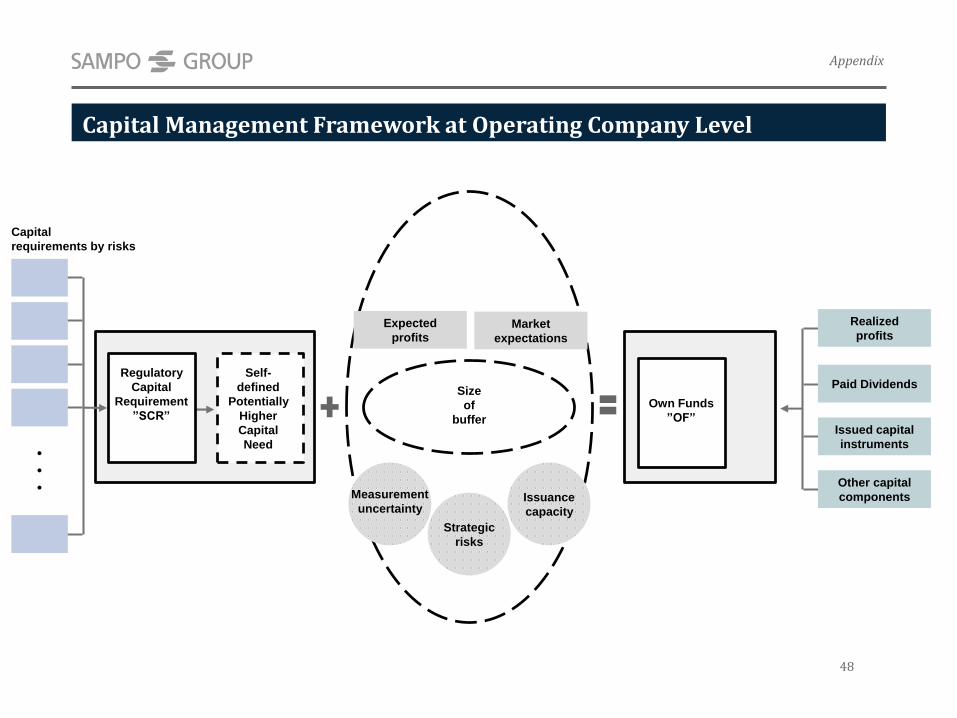

Capital Management Framework at Operating Company Level

48

Appendix

Own Funds

”OF”

•

••

Capital

requirements by risks

Self-

defined

Potentially

Higher

Capital

Need

Regulatory

Capital

Requirement

”SCR”

Measurement

uncertainty

Strategic

risks

Issuance

capacity

Expected

profits

Realized

profits

Paid Dividends

Issued capital

instruments

Other capital

components

Market

expectations

Size

of

buffer

Capital Management Framework at Group Level

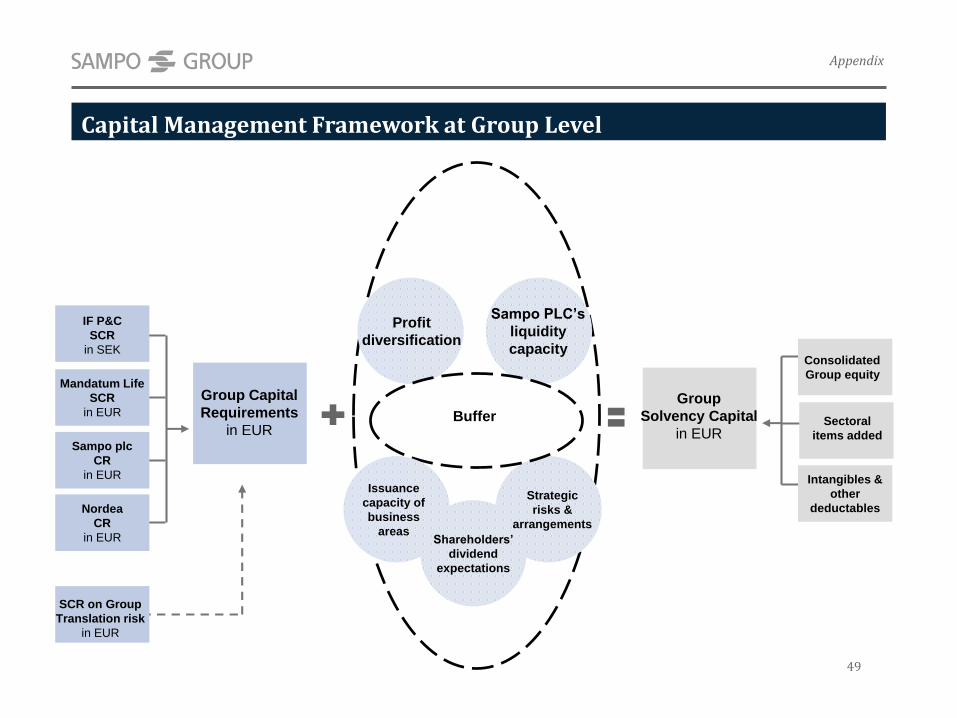

49

Appendix

Group Capital

Requirements

in EUR

Group

Solvency Capital

in EUR

IF P&C

SCR

in SEK

Mandatum Life

SCR

in EUR

Sampo plc

CR

in EUR

Nordea

CR

in EUR

SCR on Group

Translation risk

in EUR

Buffer

Issuance

capacity of

business

areas

Strategic

risks &

arrangements

Profit

diversification

Shareholders’

dividend

expectations

Consolidated

Group equity

Sectoral

items added

Intangibles &

other

deductables

Sampo PLC’s

liquidity

capacity

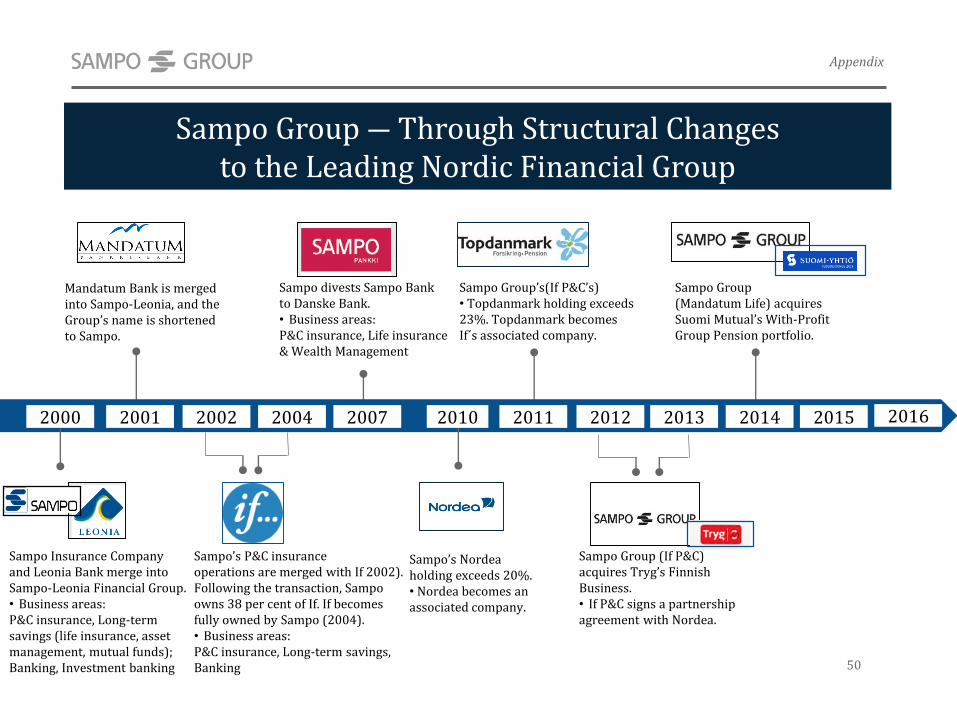

Sampo’s P&C insurance operations are merged with If 2002). Following the transaction, Sampoowns 38 per cent of If. If becomes fully owned by Sampo (2004).• Business areas:P&C insurance, Long-term savings,Banking

Sampo Insurance Companyand Leonia Bank merge into Sampo-Leonia Financial Group. • Business areas: P&C insurance, Long-term savings (life insurance, asset management, mutual funds); Banking, Investment banking

Mandatum Bank is merged into Sampo-Leonia, and the Group’s name is shortenedto Sampo.

Sampo divests Sampo Bank to Danske Bank.• Business areas: P&C insurance, Life insurance & Wealth Management

Sampo’s Nordea holding exceeds 20%. • Nordea becomes an associated company.

20072004200220012000 2010 2011

Sampo Group’s(If P&Cʼs) • Topdanmark holding exceeds 23%. Topdanmark becomes If´s associated company.

2012

Sampo Group (If P&C)acquires Tryg’s FinnishBusiness.• If P&C signs a partnership agreement with Nordea.

Sampo Group ― Through Structural Changes to the Leading Nordic Financial Group

2013 2014

Sampo Group(Mandatum Life) acquires Suomi Mutualʼs With-ProfitGroup Pension portfolio.

2015

Appendix

50

2016

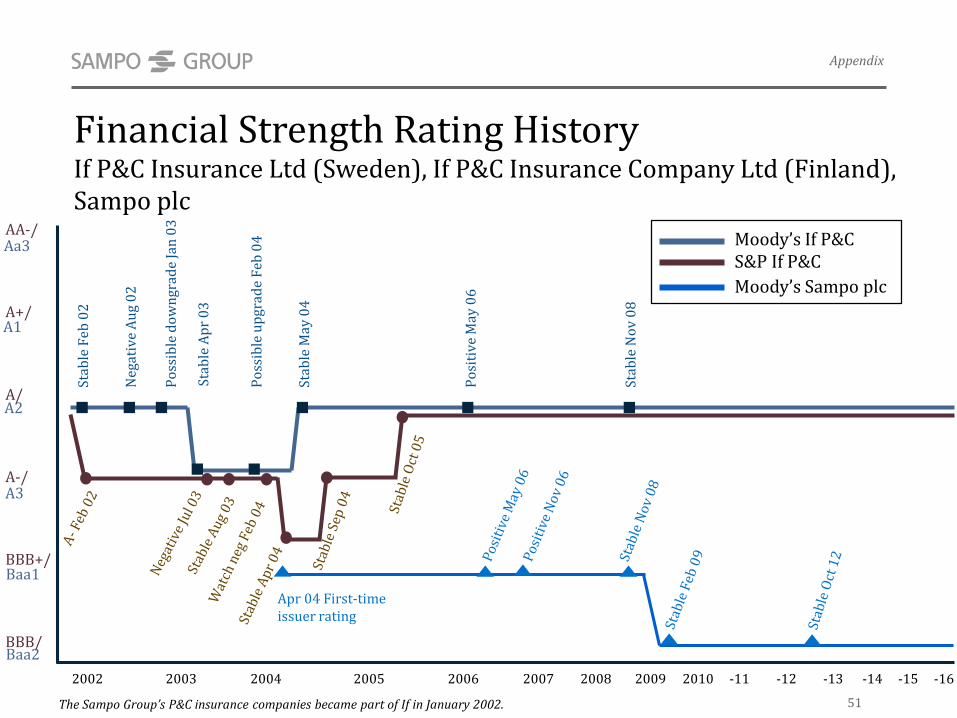

Financial Strength Rating HistoryIf P&C Insurance Ltd (Sweden), If P&C Insurance Company Ltd (Finland),Sampo plc

The Sampo Groupʼs P&C insurance companies became part of If in January 2002.

AA-/

A+/

A/

A-/

BBB+/

BBB/

Moodyʼs If P&CS&P If P&C

2002 2003 2004 2005 2006 2007 2008 2009 2010 -11 -12 -13 -14 -15 -16

Po

ssib

le d

ow

ngr

ade

Jan

03

Stab

le F

eb 0

2

Neg

ativ

e A

ug

02

Stab

le A

pr

03

Po

ssib

le u

pgr

ade

Feb

04

Stab

le M

ay 0

4

Po

siti

ve M

ay 0

6

Stab

le N

ov

08

51

Moodyʼs Sampo plc

Apr 04 First-time issuer rating

Appendix

Aa3

A1

A2

A3

Baa1

Baa2

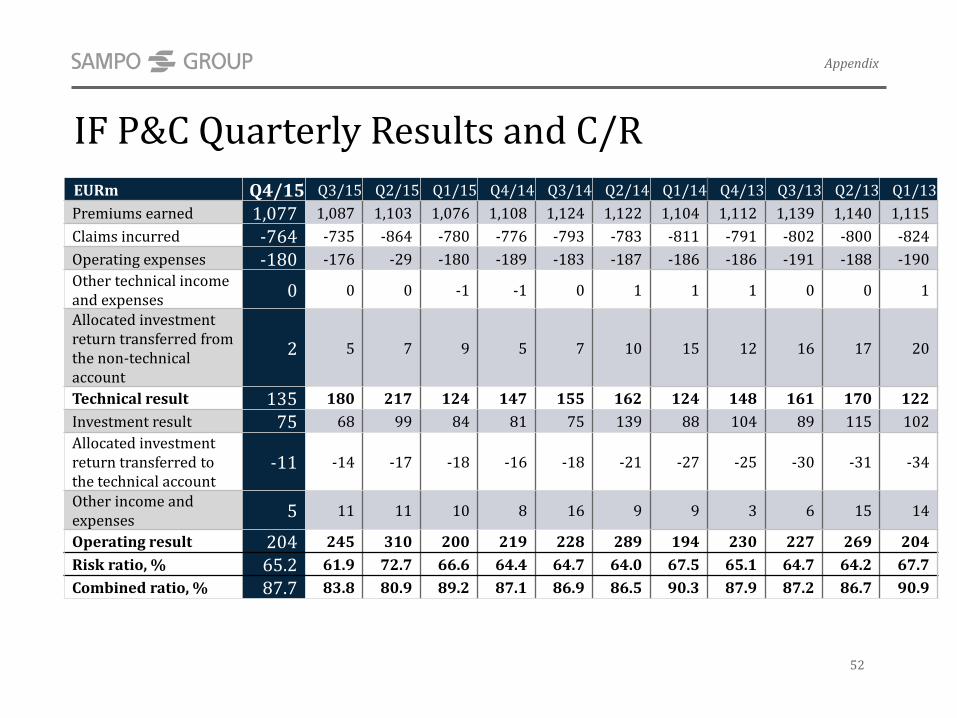

IF P&C Quarterly Results and C/R

EURm Q4/15 Q3/15 Q2/15 Q1/15 Q4/14 Q3/14 Q2/14 Q1/14 Q4/13 Q3/13 Q2/13 Q1/13

Premiums earned 1,077 1,087 1,103 1,076 1,108 1,124 1,122 1,104 1,112 1,139 1,140 1,115

Claims incurred -764 -735 -864 -780 -776 -793 -783 -811 -791 -802 -800 -824

Operating expenses -180 -176 -29 -180 -189 -183 -187 -186 -186 -191 -188 -190

Other technical income and expenses

0 0 0 -1 -1 0 1 1 1 0 0 1

Allocated investment return transferred from the non-technical account

2 5 7 9 5 7 10 15 12 16 17 20

Technical result 135 180 217 124 147 155 162 124 148 161 170 122

Investment result 75 68 99 84 81 75 139 88 104 89 115 102

Allocated investment return transferred tothe technical account

-11 -14 -17 -18 -16 -18 -21 -27 -25 -30 -31 -34

Other income and expenses

5 11 11 10 8 16 9 9 3 6 15 14

Operating result 204 245 310 200 219 228 289 194 230 227 269 204

Risk ratio, % 65.2 61.9 72.7 66.6 64.4 64.7 64.0 67.5 65.1 64.7 64.2 67.7

Combined ratio, % 87.7 83.8 80.9 89.2 87.1 86.9 86.5 90.3 87.9 87.2 86.7 90.9

Appendix

52

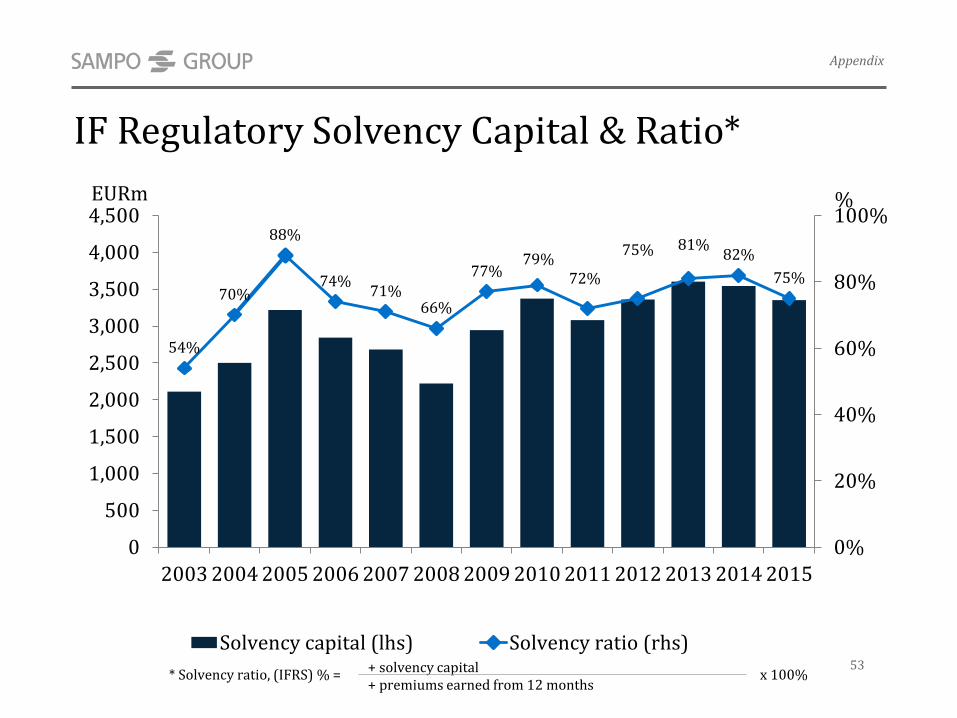

IF Regulatory Solvency Capital & Ratio*

54%

70%

88%

74%71%

66%

77%79%

72%

75% 81%82%

75%

0%

20%

40%

60%

80%

100%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

%EURm

Solvency capital (lhs) Solvency ratio (rhs)

* Solvency ratio, (IFRS) % =+ solvency capital+ premiums earned from 12 months

x 100%53

Appendix

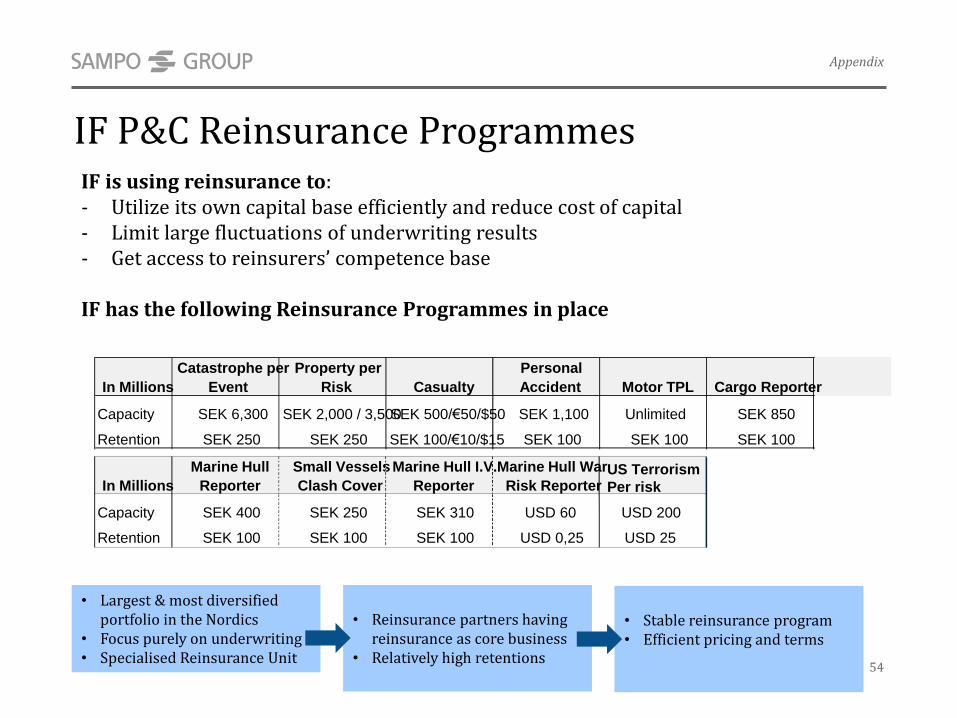

IF P&C Reinsurance ProgrammesIF is using reinsurance to:- Utilize its own capital base efficiently and reduce cost of capital- Limit large fluctuations of underwriting results- Get access to reinsurers’ competence base

IF has the following Reinsurance Programmes in place

• Largest & most diversifiedportfolio in the Nordics

• Focus purely on underwriting• Specialised Reinsurance Unit

• Reinsurance partners having reinsurance as core business

• Relatively high retentions

• Stable reinsurance program • Efficient pricing and terms

Appendix

In Millions

Marine Hull

Reporter

Small Vessels

Clash Cover

Marine Hull I.V.

Reporter

Marine Hull War

Risk ReporterUS Terrorism

Per risk

Capacity SEK 400 SEK 250 SEK 310 USD 60 USD 200

Retention SEK 100 SEK 100 SEK 100 USD 0,25 USD 25

In Millions

Catastrophe per

Event

Property per

Risk Casualty

Personal

Accident Motor TPL Cargo Reporter

Capacity SEK 6,300 SEK 2,000 / 3,500SEK 500/€50/$50 SEK 1,100 Unlimited SEK 850

Retention SEK 250 SEK 250 SEK 100/€10/$15 SEK 100 SEK 100 SEK 100

54

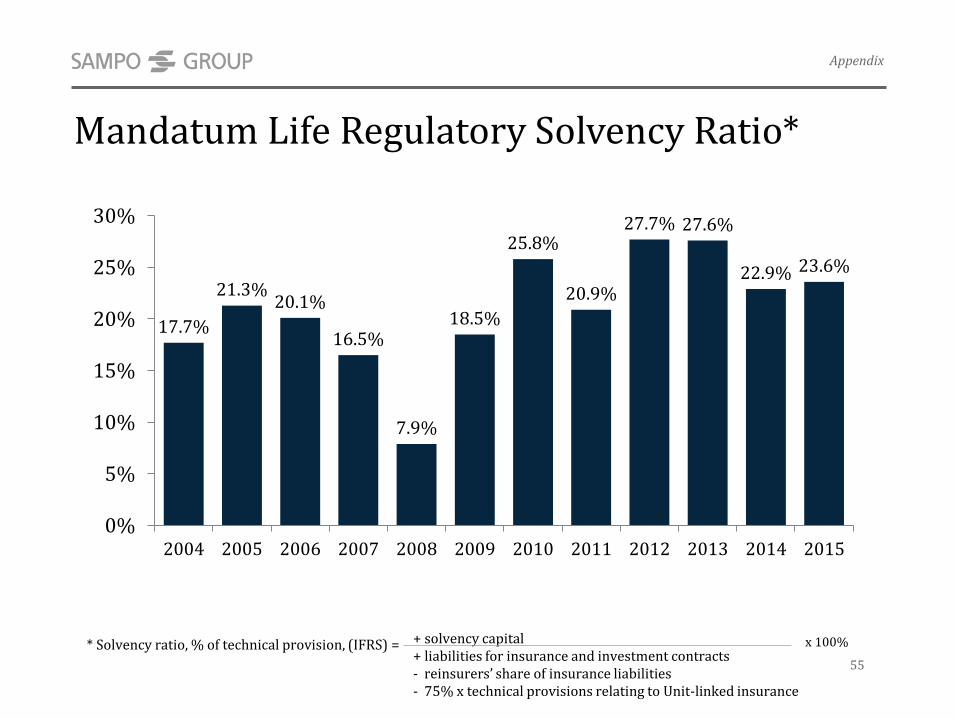

Mandatum Life Regulatory Solvency Ratio*

* Solvency ratio, % of technical provision, (IFRS) = + solvency capital+ liabilities for insurance and investment contracts- reinsurers’ share of insurance liabilities- 75% x technical provisions relating to Unit-linked insurance

x 100%

17.7%

21.3%20.1%

16.5%

7.9%

18.5%

25.8%

20.9%

27.7% 27.6%

22.9% 23.6%

0%

5%

10%

15%

20%

25%

30%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

55

Appendix

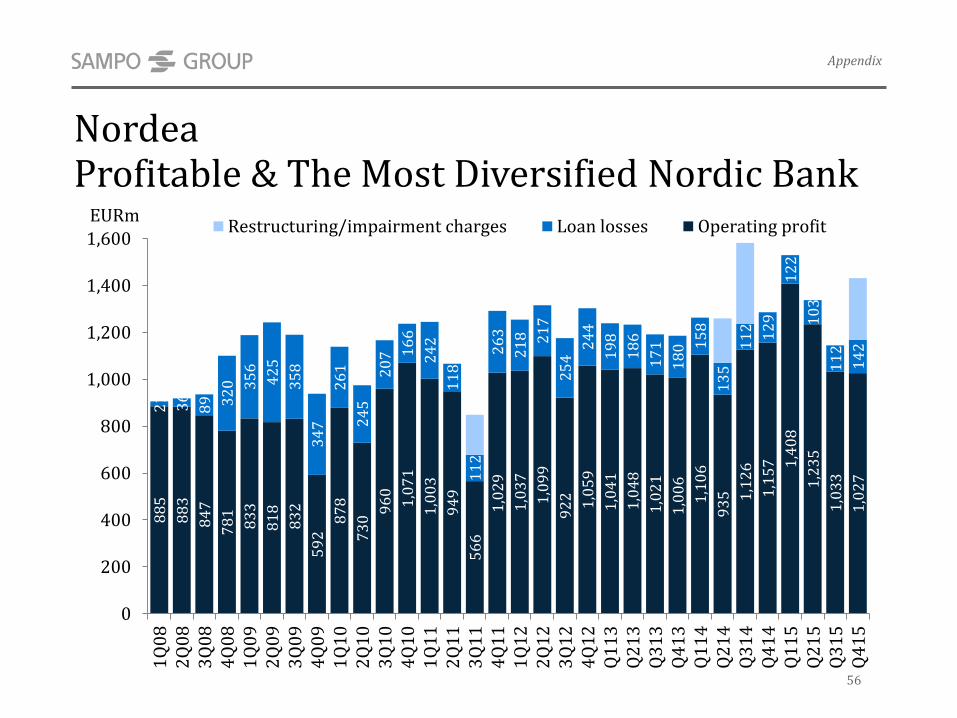

NordeaProfitable & The Most Diversified Nordic Bank

88

5

88

3

84

7

78

1

83

3

81

8

83

2

59

2

87

8

73

0

96

0

1,0

71

1,0

03

94

9

56

6

1,0

29

1,0

37

1,0

99

92

2 1,0

59

1,0

41

1,0

48

1,0

21

1,0

06

1,1

06

93

5 1,1

26

1,1

57 1

,40

8

1,2

35

1,0

33

1,0

27

21 36

89 3

20 3

56

42

5

35

8

34

7

26

1

24

5

20

7 16

6

24

2

11

8

11

2

26

3

21

8 21

7

25

4

24

4

19

8

18

6

17

1

18

0 15

8

13

5

11

2

12

9

12

2

10

3

11

2

14

2

0

200

400

600

800

1,000

1,200

1,400

1,600

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

Q1

13

Q2

13

Q3

13

Q4

13

Q1

14

Q2

14

Q3

14

Q4

14

Q1

15

Q2

15

Q3

15

Q4

15

EURmRestructuring/impairment charges Loan losses Operating profit

56

Appendix

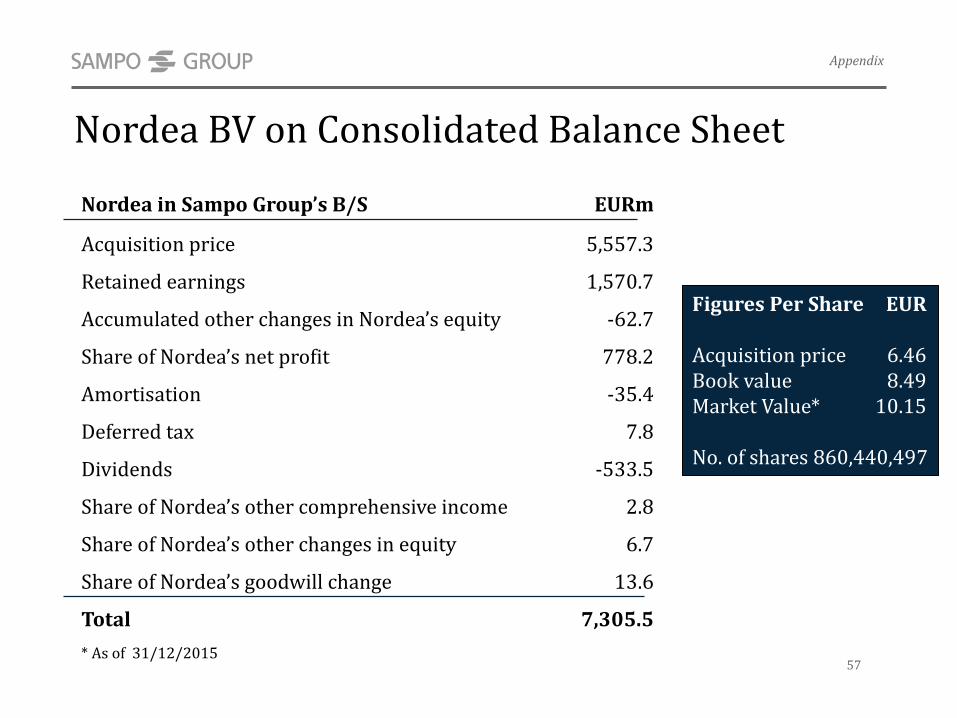

Nordea BV on Consolidated Balance Sheet

Figures Per Share EUR

Acquisition price 6.46Book value 8.49Market Value* 10.15

No. of shares 860,440,497

* As of 31/12/2015

Nordea in Sampo Group’s B/S EURm

Acquisition price 5,557.3

Retained earnings 1,570.7

Accumulated other changes in Nordea’s equity -62.7

Share of Nordea’s net profit 778.2

Amortisation -35.4

Deferred tax 7.8

Dividends -533.5

Share of Nordea’s other comprehensive income 2.8

Share of Nordea’s other changes in equity 6.7

Share of Nordea’s goodwill change 13.6

Total 7,305.5

Appendix

57