Embed Size (px)

Citation preview

SEB Nordic SeminarThreats and opportunities related to digitization

Powering Digital Payments

CFO Klaus Pedersen, 9 January 2017

Disclaimer

This presentation contains forward-looking statements. Forward-looking statements are statements (other than statements of historical fact) relating to future events and Nets’ anticipated or planned financial and operational performance. The words ‘may’, ‘will’, ‘will continue’, ‘should’, ‘expect’, ‘foresee’, ‘anticipate’, ‘believe’, ‘estimate’, ‘plan’, ‘predict’, ‘intend’ or variations of these words, including negatives thereof, as well as other statements regarding matters that are not historical fact or regarding future events or prospects, constitute forward-looking statements. Nets has based these forward-looking statements on its current viewswith respect to future events and financial performance. These views involve a number of risks and uncertainties, which couldcause actual results to differ materially from those predicted in the forward-looking statements and from the past performance of Nets. Although Nets believes that the estimates and projections reflected in the forward-looking statements are reasonable, theymay prove materially incorrect, and actual results may materially differ, e.g. as the result of risks related to the industry in general or Nets in particular, including those described in Nets Holding’s Annual Report 2015, Offering Circular of 13 September 2016and other information made available by Nets.

Factors that may affect future results include, but are not limited to, global and economic conditions, including currency exchange rate and interest rate fluctuations, delay or failure of projects related to research and/or development, unexpected contractbreaches or terminations, unplanned loss of patents, government-mandated or market-driven price decreases for Nets’ products, introduction of competing products, reliance on information technology, Nets’ ability to successfully market current and new products, exposure to product liability, litigation and investigations, regulatory developments, actual or perceived failure to adhere to ethical marketing practices, unexpected growth in costs and expenses, failure to recruit and retain the right employees, and failure to maintain a culture of compliance.

As a result, forward-looking statements should not be relied on as a prediction of actual results. Nets undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except to the extent required by law.

The Annual Report 2015 of Nets Holding A/S and the Offering Circular are available at www.nets.eu

Forward looking statements

2

Nets is at the Centre of Daily Life

in the Nordics…

Powering Digital Payments

of Danish households use Nets’ e-Bill

payments to pay utility bills in Denmark>90%

of Danish merchant payments authorised

& processed by Nets98%

of Norwegians access online/mobile banking

through the e-ID platform operated by Nets80%

of Norwegian e-merchant payments

authorised & processed by Nets>60%

Source Management estimates as of and for the year ended 31 December 20153

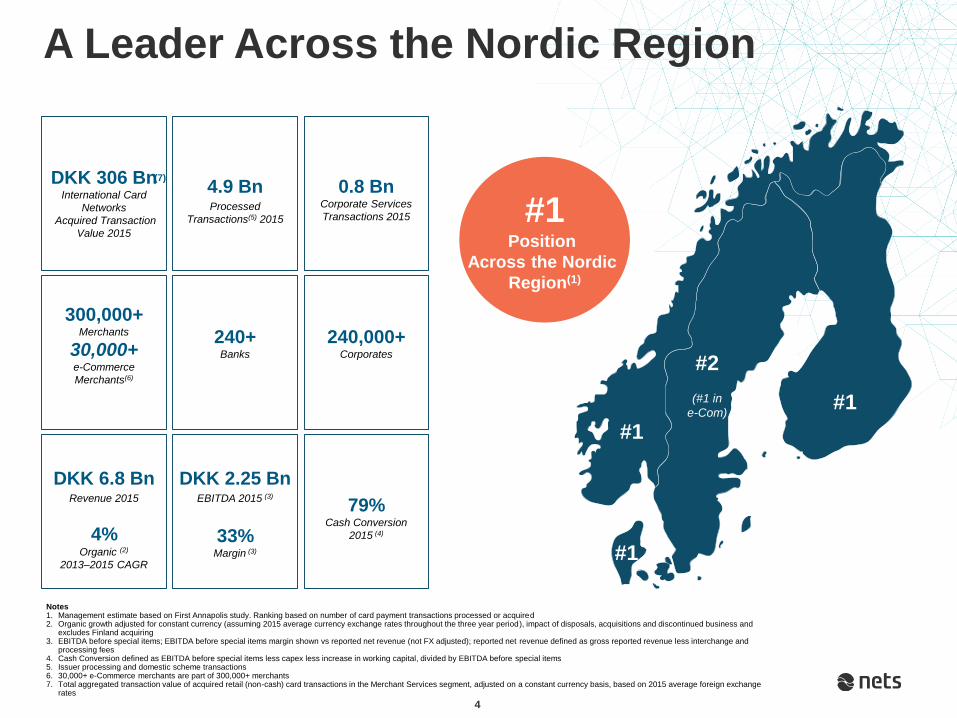

A Leader Across the Nordic Region

#1Position

Across the Nordic

Region(1)

DKK 306 BnInternational Card

Networks

Acquired Transaction

Value 2015

4.9 Bn Processed

Transactions(5) 2015

0.8 BnCorporate Services

Transactions 2015

DKK 6.8 BnRevenue 2015

4%Organic (2)

2013–2015 CAGR

79%Cash Conversion

2015 (4)

DKK 2.25 BnEBITDA 2015 (3)

33%Margin (3)

300,000+Merchants

30,000+e-Commerce

Merchants(6)

240+Banks

240,000+Corporates

Notes1. Management estimate based on First Annapolis study. Ranking based on number of card payment transactions processed or acquired2. Organic growth adjusted for constant currency (assuming 2015 average currency exchange rates throughout the three year period), impact of disposals, acquisitions and discontinued business and

excludes Finland acquiring3. EBITDA before special items; EBITDA before special items margin shown vs reported net revenue (not FX adjusted); reported net revenue defined as gross reported revenue less interchange and

processing fees4. Cash Conversion defined as EBITDA before special items less capex less increase in working capital, divided by EBITDA before special items5. Issuer processing and domestic scheme transactions6. 30,000+ e-Commerce merchants are part of 300,000+ merchants7. Total aggregated transaction value of acquired retail (non-cash) card transactions in the Merchant Services segment, adjusted on a constant currency basis, based on 2015 average foreign exchange

rates

#1

#1

#1

#2

(#1 in

e-Com)

(7)

4

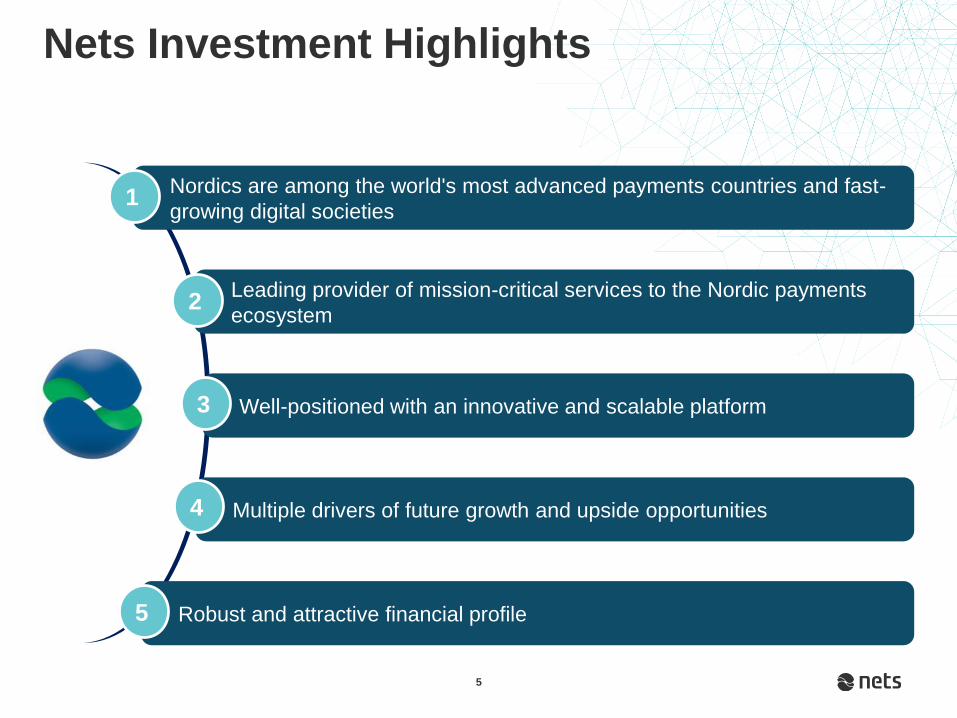

Nets Investment Highlights

Nordics are among the world's most advanced payments countries and fast-

growing digital societies1

Leading provider of mission-critical services to the Nordic payments

ecosystem2

Well-positioned with an innovative and scalable platform3

Multiple drivers of future growth and upside opportunities4

Robust and attractive financial profile5

5

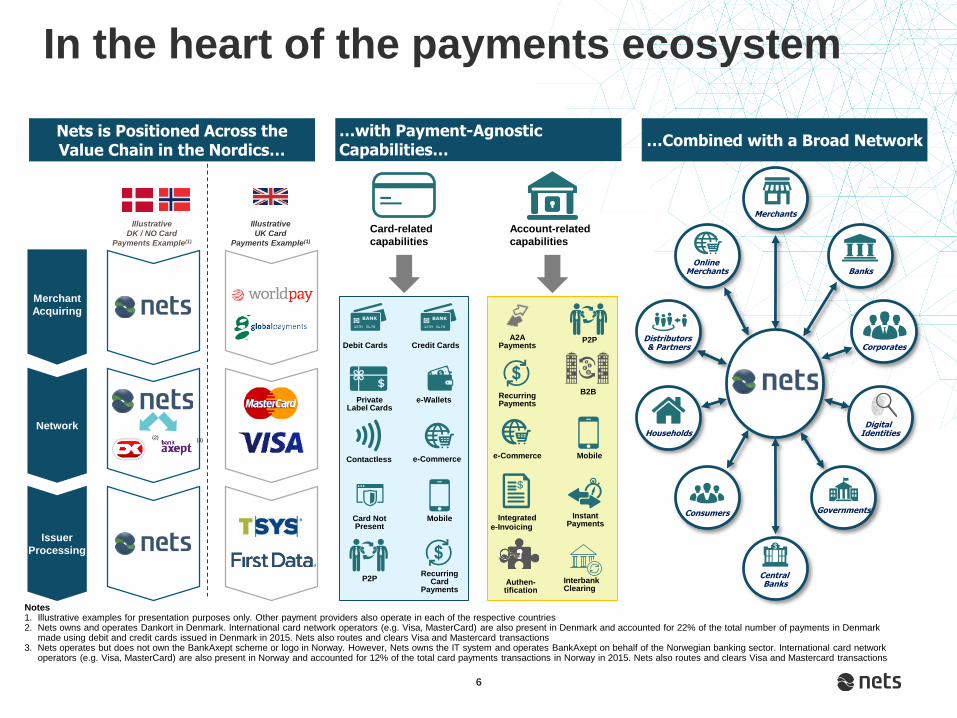

In the heart of the payments ecosystem

…Combined with a Broad Network Nets is Positioned Across the Value Chain in the Nordics…

Merchant

Acquiring

Network

Issuer

Processing

Illustrative

UK Card

Payments Example(1)

Illustrative

DK / NO Card

Payments Example(1)

Merchants

Online Merchants Banks

Consumers Governments

Central Banks

HouseholdsDigital

Identities

CorporatesDistributors & Partners

(3)(2)

Notes1. Illustrative examples for presentation purposes only. Other payment providers also operate in each of the respective countries 2. Nets owns and operates Dankort in Denmark. International card network operators (e.g. Visa, MasterCard) are also present in Denmark and accounted for 22% of the total number of payments in Denmark

made using debit and credit cards issued in Denmark in 2015. Nets also routes and clears Visa and Mastercard transactions3. Nets operates but does not own the BankAxept scheme or logo in Norway. However, Nets owns the IT system and operates BankAxept on behalf of the Norwegian banking sector. International card network

operators (e.g. Visa, MasterCard) are also present in Norway and accounted for 12% of the total card payments transactions in Norway in 2015. Nets also routes and clears Visa and Mastercard transactions

Card-related

capabilities

Mobile

Credit Cards

Recurring Card

Payments

e-Wallets

e-Commerce

Card Not Present

Debit Cards

P2P

Private Label Cards

Contactless

Account-related

capabilities

Mobile

P2P

Interbank Clearing

B2B

e-Commerce

Recurring Payments

Integratede-Invoicing

$

Instant Payments

Authen-tification

…with Payment-Agnostic Capabilities…

A2A Payments

6

Scale Across the Nordic Region

Source The Nilson Report 2015, Company data

4.2

2.0

0.4 0.2

0.0

1.5

3.0

4.5

Acquired Nordic Transactions 2014 (Bn) (2)

Scale Achieved – Acquiring Example

(3)

Significant Scale Advantages (illustrative) (4)

Country Position

#1

#1

#2

#1

(#1 in e-Com)

Local Position(1)

Denmark

Norway

Sweden

Finland

Source Company estimates

Cost Per-Transaction

Number of Transactions

c.50%

Volumes x 4

Merchant Acquiring Curve

Notes1. All rankings are based on number of card payment transactions processed or acquired2. Captive (in-house) volumes highlighted in grey3. Nets volumes include processed Dankort and BankAxept transactions of 2.5 Bn and acquired international transactions of 1.7 Bn4. c.50% lower cost as a result of movement from c.0.5 Bn to 2 Bn acquiring transactions

Babs

Source First Annapolis

7

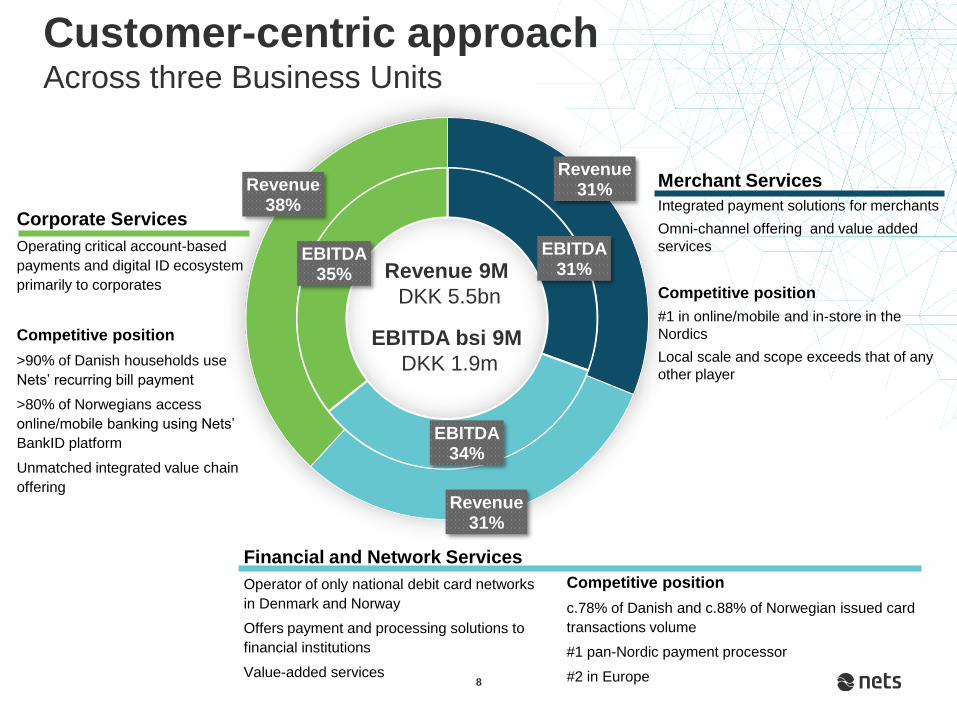

Customer-centric approachAcross three Business Units

8

EBITDA31%

EBITDA34%

EBITDA35%

Revenue31%

Revenue31%

Revenue38%

Merchant Services

Integrated payment solutions for merchants

Omni-channel offering and value added

services

Competitive position

#1 in online/mobile and in-store in the

Nordics

Local scale and scope exceeds that of any

other player

Revenue 9M

DKK 5.5bn

EBITDA bsi 9M

DKK 1.9m

Competitive position

c.78% of Danish and c.88% of Norwegian issued card

transactions volume

#1 pan-Nordic payment processor

#2 in Europe

Corporate Services

Operating critical account-based

payments and digital ID ecosystem

primarily to corporates

Competitive position

>90% of Danish households use

Nets’ recurring bill payment

>80% of Norwegians access

online/mobile banking using Nets’

BankID platform

Unmatched integrated value chain

offering

Financial and Network Services

Operator of only national debit card networks

in Denmark and Norway

Offers payment and processing solutions to

financial institutions

Value-added services

14%

28%

Significant potential to gain

volume in Sweden from bank

acquirers

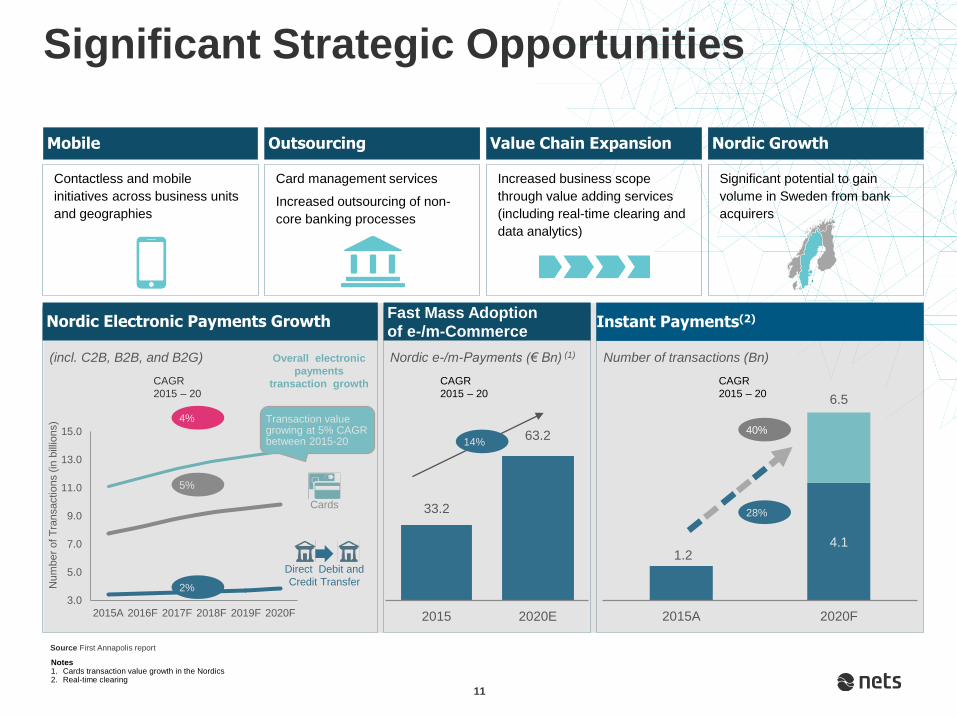

3.0

5.0

7.0

9.0

11.0

13.0

15.0

2015A 2016F 2017F 2018F 2019F 2020F

Num

ber

of T

ransactio

ns (

in b

illio

ns)

Notes1. Cards transaction value growth in the Nordics2. Real-time clearing

Mobile

Source First Annapolis report

Significant Strategic Opportunities

Outsourcing Value Chain Expansion Nordic Growth

Contactless and mobile

initiatives across business units

and geographies

Card management services

Increased outsourcing of non-

core banking processes

Increased business scope

through value adding services

(including real-time clearing and

data analytics)

4.11.2

6.5

2015A 2020F

Number of transactions (Bn)(incl. C2B, B2B, and B2G)

CAGR

2015 – 20

2%

4%

5%

Overall electronic

payments

transaction growth

Cards

Direct Debit and

Credit Transfer

Transaction value growing at 5% CAGR between 2015-20

33.2

63.2

2015 2020E

Nordic e-/m-Payments (€ Bn) (1)

Nordic Electronic Payments Growth Instant Payments(2)

CAGR

2015 – 20

CAGR

2015 – 20

40%

Fast Mass Adoption of e-/m-Commerce

11

Notes1. Third-party payment provider

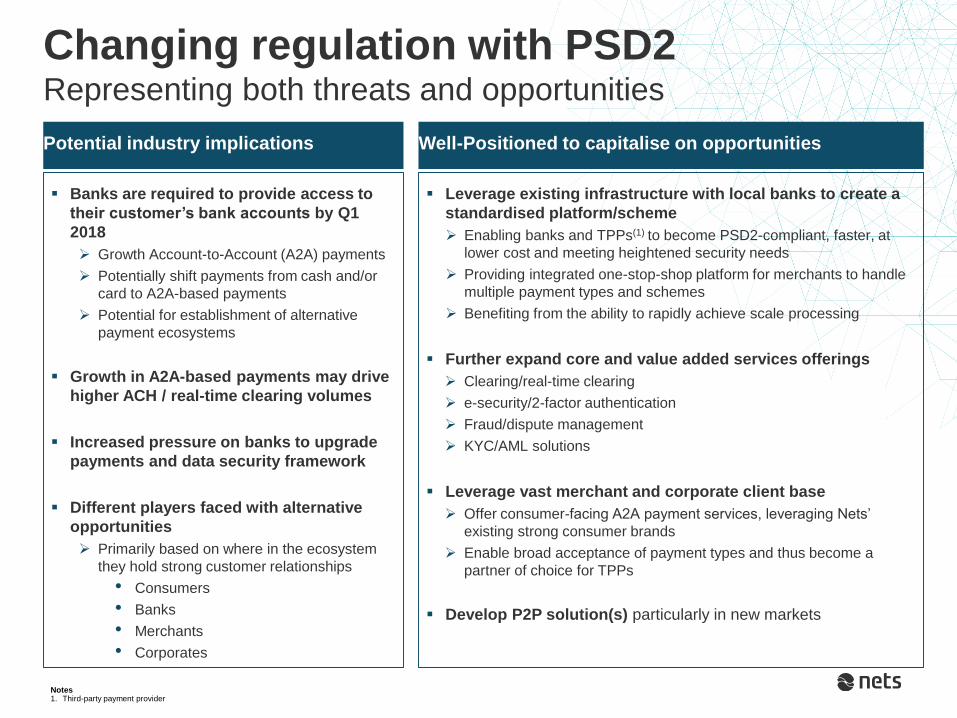

Well-Positioned to capitalise on opportunities Potential industry implications

Banks are required to provide access to

their customer’s bank accounts by Q1

2018

Growth Account-to-Account (A2A) payments

Potentially shift payments from cash and/or

card to A2A-based payments

Potential for establishment of alternative

payment ecosystems

Growth in A2A-based payments may drive

higher ACH / real-time clearing volumes

Increased pressure on banks to upgrade

payments and data security framework

Different players faced with alternative

opportunities

Primarily based on where in the ecosystem

they hold strong customer relationships

• Consumers

• Banks

• Merchants

• Corporates

Leverage existing infrastructure with local banks to create a

standardised platform/scheme

Enabling banks and TPPs(1) to become PSD2-compliant, faster, at

lower cost and meeting heightened security needs

Providing integrated one-stop-shop platform for merchants to handle

multiple payment types and schemes

Benefiting from the ability to rapidly achieve scale processing

Further expand core and value added services offerings

Clearing/real-time clearing

e-security/2-factor authentication

Fraud/dispute management

KYC/AML solutions

Leverage vast merchant and corporate client base

Offer consumer-facing A2A payment services, leveraging Nets’

existing strong consumer brands

Enable broad acceptance of payment types and thus become a

partner of choice for TPPs

Develop P2P solution(s) particularly in new markets

Changing regulation with PSD2Representing both threats and opportunities

Mobile Dankort launching in Q1 2017

•Mobile Dankort is a result of a close

cooperation between Dankort merchants,

banks and Nets

•Strong support from terminal vendors

•Several large retailers recently signed on

the platform to accept mobile payments

•Simple payment experience and strong

merchant support

•Acceptance by NFC, QR and Bluetooth

Mobile Dankort offers low cost and scale to merchants and is user friendly and secure

Contactless Dankort is important to establish the user experience in mobile Dankort

2016 2017

11

0.0% 0.0% 0.1% 0.3%0.6%

0.9%1.5%

2.2%

3.1%

4.0%

4.9%

6.2%

7.1%

8.8%

10.7%

12.2%

14.0%

1 11 119312 558 869 1,210 1,848

2,8023,767

4,8116,030 6,681

8,2469,846

11,392

13,318

Dankort CL trans Share of trans. in chip term.

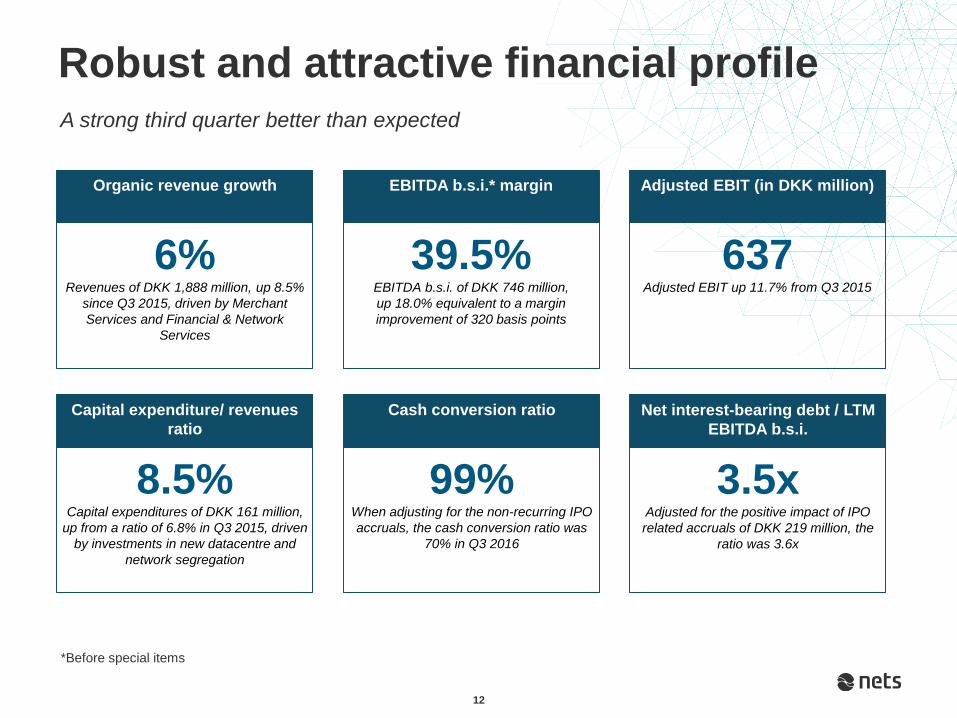

A strong third quarter better than expected

Robust and attractive financial profile

6%Revenues of DKK 1,888 million, up 8.5%

since Q3 2015, driven by Merchant

Services and Financial & Network

Services

Organic revenue growth

39.5%EBITDA b.s.i. of DKK 746 million,

up 18.0% equivalent to a margin

improvement of 320 basis points

EBITDA b.s.i.* margin

8.5%Capital expenditures of DKK 161 million,

up from a ratio of 6.8% in Q3 2015, driven

by investments in new datacentre and

network segregation

Capital expenditure/ revenues

ratio

637 Adjusted EBIT up 11.7% from Q3 2015

Adjusted EBIT (in DKK million)

3.5xAdjusted for the positive impact of IPO

related accruals of DKK 219 million, the

ratio was 3.6x

Net interest-bearing debt / LTM

EBITDA b.s.i.

99%When adjusting for the non-recurring IPO

accruals, the cash conversion ratio was

70% in Q3 2016

Cash conversion ratio

12

*Before special items

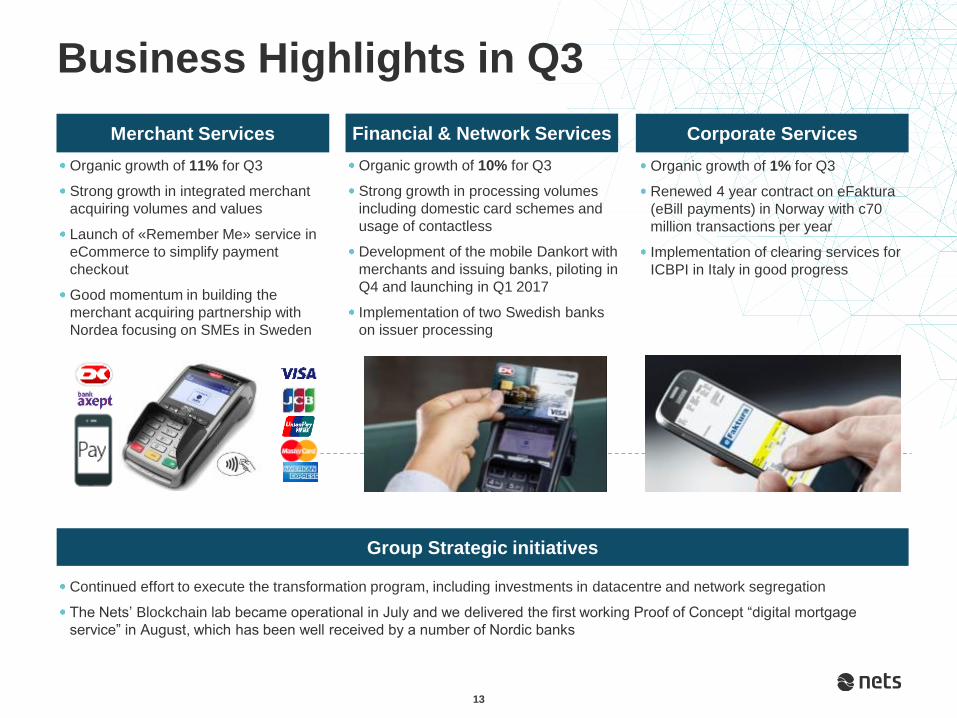

Merchant Services

Business Highlights in Q3

Organic growth of 11% for Q3

Strong growth in integrated merchant

acquiring volumes and values

Launch of «Remember Me» service in

eCommerce to simplify payment

checkout

Good momentum in building the

merchant acquiring partnership with

Nordea focusing on SMEs in Sweden

Group Strategic initiatives

Organic growth of 10% for Q3

Strong growth in processing volumes

including domestic card schemes and

usage of contactless

Development of the mobile Dankort with

merchants and issuing banks, piloting in

Q4 and launching in Q1 2017

Implementation of two Swedish banks

on issuer processing

Continued effort to execute the transformation program, including investments in datacentre and network segregation

The Nets’ Blockchain lab became operational in July and we delivered the first working Proof of Concept “digital mortgage

service” in August, which has been well received by a number of Nordic banks

Organic growth of 1% for Q3

Renewed 4 year contract on eFaktura

(eBill payments) in Norway with c70

million transactions per year

Implementation of clearing services for

ICBPI in Italy in good progress

Financial & Network Services Corporate Services

13

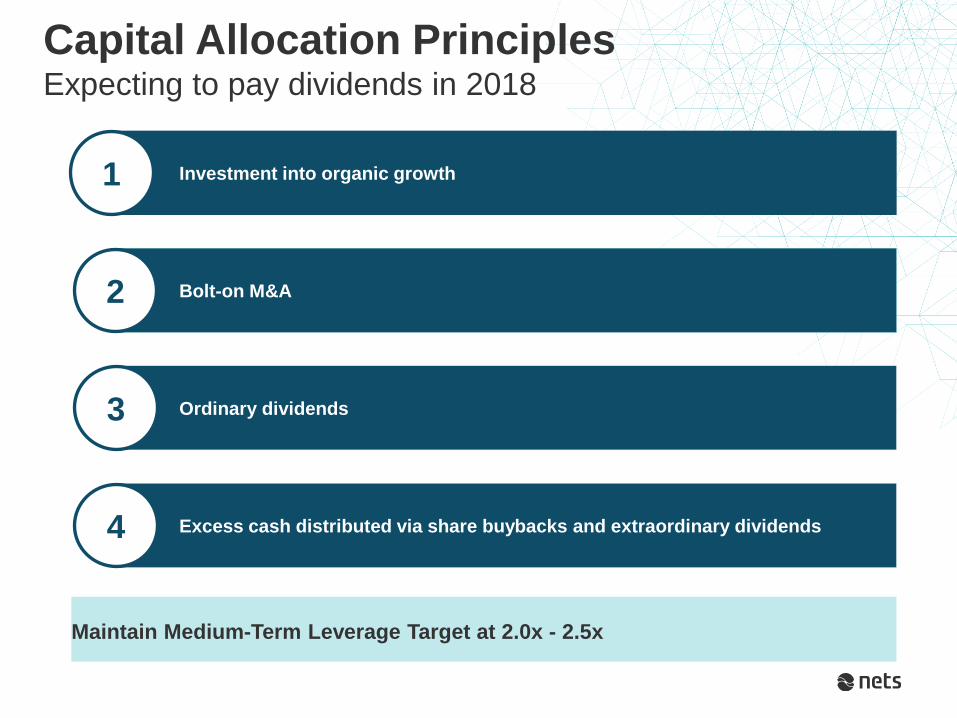

Capital Allocation PrinciplesExpecting to pay dividends in 2018

Investment into organic growth1

Ordinary dividends3

Excess cash distributed via share buybacks and extraordinary dividends4

Bolt-on M&A2

Maintain Medium-Term Leverage Target at 2.0x - 2.5x

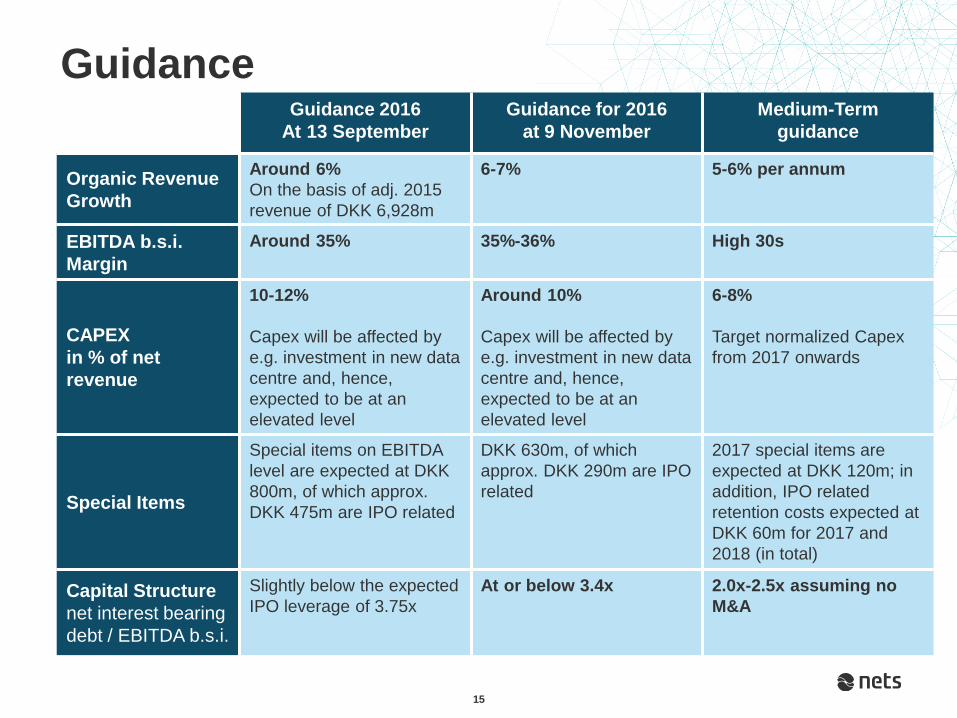

Guidance

15

Guidance 2016

At 13 September

Guidance for 2016

at 9 November

Medium-Term

guidance

Organic Revenue

Growth

Around 6%

On the basis of adj. 2015

revenue of DKK 6,928m

6-7% 5-6% per annum

EBITDA b.s.i.

Margin

Around 35% 35%-36% High 30s

CAPEX

in % of net

revenue

10-12%

Capex will be affected by

e.g. investment in new data

centre and, hence,

expected to be at an

elevated level

Around 10%

Capex will be affected by

e.g. investment in new data

centre and, hence,

expected to be at an

elevated level

6-8%

Target normalized Capex

from 2017 onwards

Special Items

Special items on EBITDA

level are expected at DKK

800m, of which approx.

DKK 475m are IPO related

DKK 630m, of which

approx. DKK 290m are IPO

related

2017 special items are

expected at DKK 120m; in

addition, IPO related

retention costs expected at

DKK 60m for 2017 and

2018 (in total)

Capital Structure

net interest bearing

debt / EBITDA b.s.i.

Slightly below the expected

IPO leverage of 3.75x

At or below 3.4x 2.0x-2.5x assuming no

M&A

Back-up

16

17

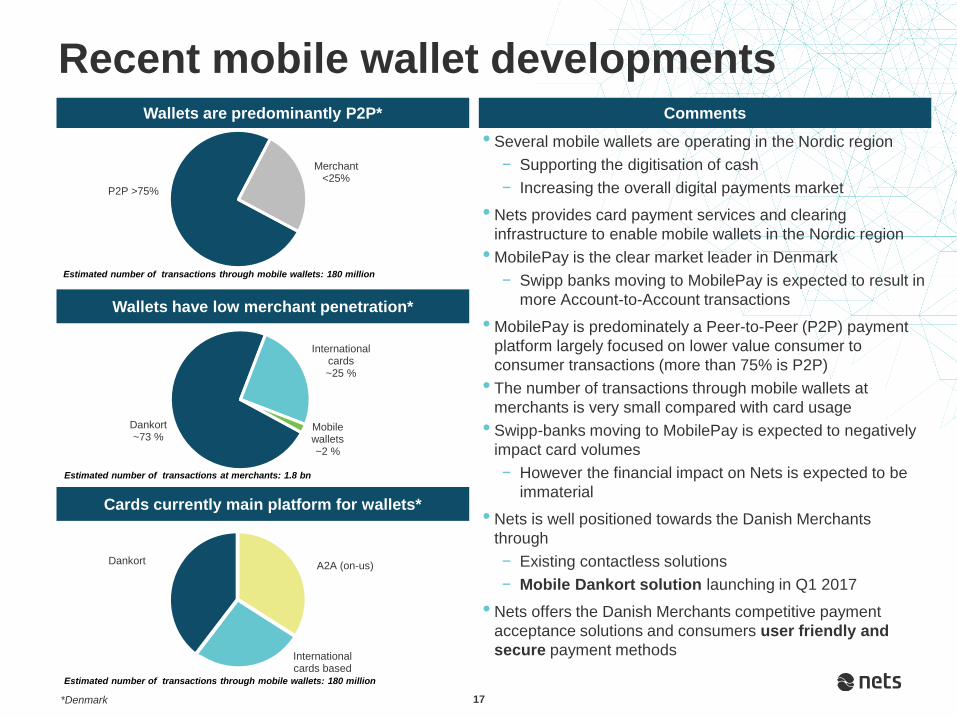

Recent mobile wallet developmentsComments

Dankort~73 %

International cards~25 %

Mobile wallets~2 %

P2P >75%

Merchant <25%

A2A (on-us) Dankort

International cards based

• Several mobile wallets are operating in the Nordic region

− Supporting the digitisation of cash

− Increasing the overall digital payments market

• Nets provides card payment services and clearing

infrastructure to enable mobile wallets in the Nordic region

• MobilePay is the clear market leader in Denmark

− Swipp banks moving to MobilePay is expected to result in

more Account-to-Account transactions

• MobilePay is predominately a Peer-to-Peer (P2P) payment

platform largely focused on lower value consumer to

consumer transactions (more than 75% is P2P)

• The number of transactions through mobile wallets at

merchants is very small compared with card usage

• Swipp-banks moving to MobilePay is expected to negatively

impact card volumes

− However the financial impact on Nets is expected to be

immaterial

• Nets is well positioned towards the Danish Merchants

through

− Existing contactless solutions

− Mobile Dankort solution launching in Q1 2017

• Nets offers the Danish Merchants competitive payment

acceptance solutions and consumers user friendly and

secure payment methods

Wallets have low merchant penetration*

Wallets are predominantly P2P*

Cards currently main platform for wallets*

*Denmark

Estimated number of transactions through mobile wallets: 180 million

Estimated number of transactions at merchants: 1.8 bn

Estimated number of transactions through mobile wallets: 180 million