Embed Size (px)

Citation preview

1

For professional clients only

HSBC GIF Indian Equity PresentationSeptember 2011

2

HSBC Overview

HSBC Global Asset Management

The Investment Team & Emerging Markets Investment Resources

Investment Philosophy and Process

Risk management

Market overview

HSBC GIF Indian Equity Fund overview

Competitor analysis

Outlook

Appendix

Contents

HSBC Overview

4

HSBC overview

Emerging markets are at the heart of HSBC's corporate identity

HSBC’s roots were formed in China and India in the 19th century

HSBC Group has maintained a strong presence in global trade, particularly in India and China, the world's most dynamic emerging markets.

Headquartered in London, HSBC is one of the largest banking and financial services organisations in the world, with over 300,000 employees spanning

an international network of around 7,500 offices in the Asia-Pacific region, Europe, the Americas, the Middle East and Africa.

One of the largest global financial services networks with offices in 87 countries of which 54 are in emerging market countries

A unique local market knowledge, enhancing the portfolio management processes

Direct access to local companies and investment opportunities

Source: HSBC Holdings Plc, data as of 31st December 2010.

5

Mexico

Honduras

El Salvador Nicaragua

Costa Rica Panama

Colombia

PeruBrazil

ParaguayChile

ArgentinaUruguay

South Africa

Mauritius

Algeria

Libya Egypt

PolandCzech RepublicSlovakia

TurkeyLebanon

IsraelPalestine

Georgia

ArmeniaIraq

KuwaitBahrain, QatarUAE

OmanSaudi Arabia

Kazakhstan

Russia

PakistanChina Korea

India

MaldivesSri Lanka

Taiwan

Philippines

Indonesia

BruneiMalaysia

Singapore

Hong Kong

ThailandVietnam

Macau

Malta

HSBC Global Asset ManagementHSBC Holdings plc

Source: HSBC Global Asset Management, as of 31 December 2010

HSBC’s presence in emerging markets

HSBC Global Asset Management

7

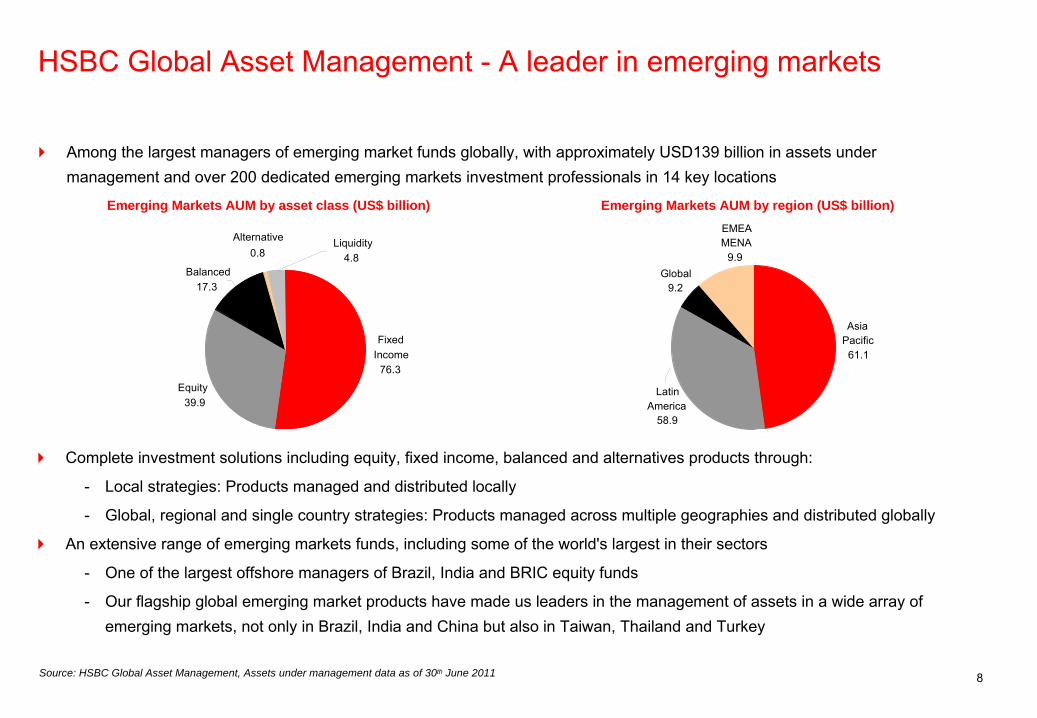

HSBC Global Asset Management

HSBC Global Asset Management is a leading global asset management firm managing assets totalling USD453.4 billion at the end of June 2011.

HSBC Global Asset Management offers clients around the world a diverse and full range of active and quantitative investment products including equity, fixed income, liquidity and alternative strategies.

Worldwide client base invested in both segregated accounts and pooled funds.

HSBC Global Asset Management is part of HSBC Holdings plc.

8

HSBC Global Asset Management -

A leader in emerging markets

Complete investment solutions including equity, fixed income, balanced and alternatives products through:

-

Local strategies: Products managed and distributed locally

-

Global, regional and single country strategies: Products managed

across multiple geographies and distributed globally

An extensive range of emerging markets funds, including some of the world's largest in their sectors

-

One of the largest offshore managers of Brazil, India and BRIC equity funds

-

Our flagship global emerging market products have made us leaders in the management of assets in a wide array of emerging markets, not only in Brazil, India and China but also in Taiwan, Thailand and Turkey

Emerging Markets AUM by region (US$ billion)

Source: HSBC Global Asset Management, Assets under management data as of 30th June 2011

Emerging Markets AUM by asset class (US$ billion)

Among the largest managers of emerging market funds globally, with approximately USD139 billion in assets under management and over 200 dedicated emerging markets investment professionals in 14 key locations

Latin America

58.9

Asia Pacific61.1

EMEAMENA

9.9Global

9.2

Equity39.9

Fixed Income

76.3

Balanced17.3

Alternative0.8

Liquidity4.8

The Investment Team & Emerging Markets Investment Resources

10

New YorkGEM Fixed Income8 Investmentprofessionals

Mexico CityMexican Fixed IncomeMexican EquityMexican Alternatives11 Investmentprofessionals

BogotaColombian Fixed IncomeColombian Equity5 Investmentprofessionals

Sao PauloBrazilian Fixed IncomeBrazilian EquityBrazilian AlternativesBrazilian Multimanager21 Investmentprofessionals

Buenos AiresArgentinian Fixed IncomeArgentinian Equity5 Investmentprofessionals

LondonGEM EquityGEM AlternativesGEM Multimanager13 Investmentprofessionals

ParisGEM Fixed IncomeGEM Equity (inc Amanah)9 Investmentprofessionals

IstanbulTurkish Fixed IncomeTurkish EquityTurkish Alternatives10 Investmentprofessionals

RiyadhSaudi Fixed Income (inc

Amanah)Saudi EquitySaudi Alternatives18 Investmentprofessionals

Mumbai Indian Fixed Income Indian Equity19 Investmentprofessionals

SingaporeSingaporean Equity7 Investmentprofessionals

Hong KongHong Kong Fixed IncomeHong Kong EquityHong Kong Alternatives37 Investmentprofessionals

Shanghai Jintrust Chinese Fixed

Income Jintrust Chinese EquityChinese M ultimanager17 Investmentprofessionals

TaipeiTaipei Fixed IncomeTaipei Equity23 Investmentprofessionals

19464

Emerging markets investment capabilities –

A portfolio of opportunities Strategies and locations

As of June 2011

11

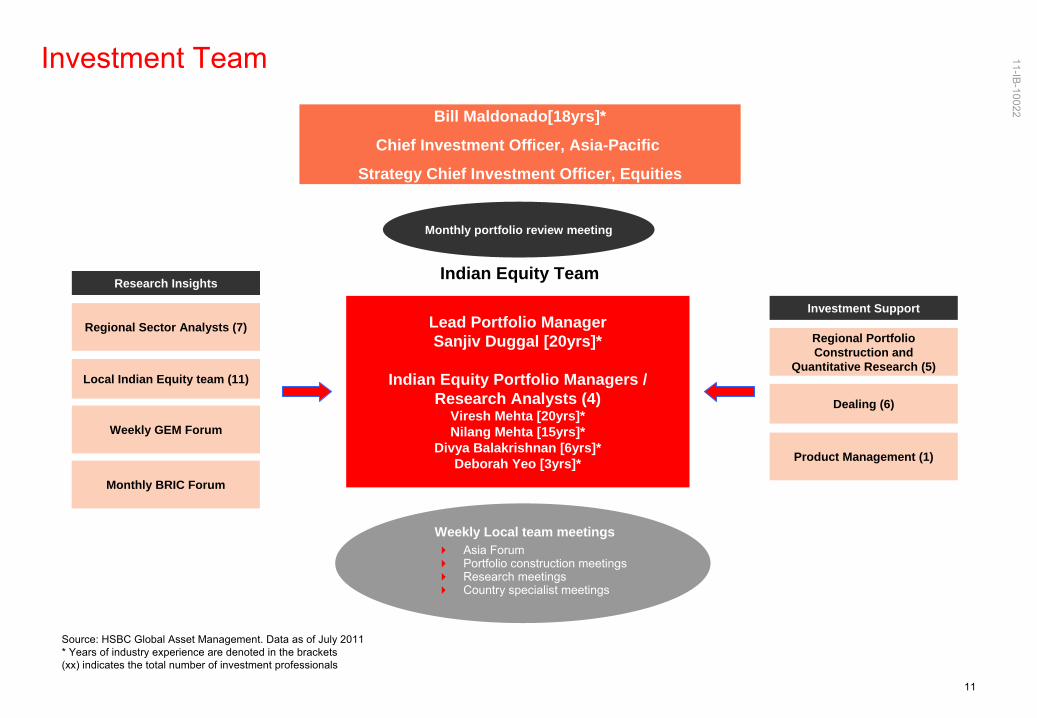

11-IB-10022

Investment Team

Source: HSBC Global Asset Management. Data as of July 2011* Years of industry experience are denoted in the brackets(xx) indicates the total number of investment professionals

Bill Maldonado[18yrs]*

Chief Investment Officer, Asia-Pacific

Strategy Chief Investment Officer, Equities

Weekly Local team meetings

Asia Forum Portfolio construction meetings Research meetings Country specialist meetings

Lead Portfolio ManagerSanjiv Duggal [20yrs]*

Indian Equity Portfolio Managers / Research Analysts (4)

Viresh Mehta [20yrs]*Nilang Mehta [15yrs]*

Divya Balakrishnan [6yrs]*Deborah Yeo [3yrs]*

Indian Equity Team

Monthly portfolio review meeting

Regional Portfolio Construction and

Quantitative Research (5)

Product Management (1)

Dealing (6)

Investment SupportRegional Sector Analysts (7)

Weekly GEM Forum

Local Indian Equity team (11)

Research Insights

Monthly BRIC Forum

12

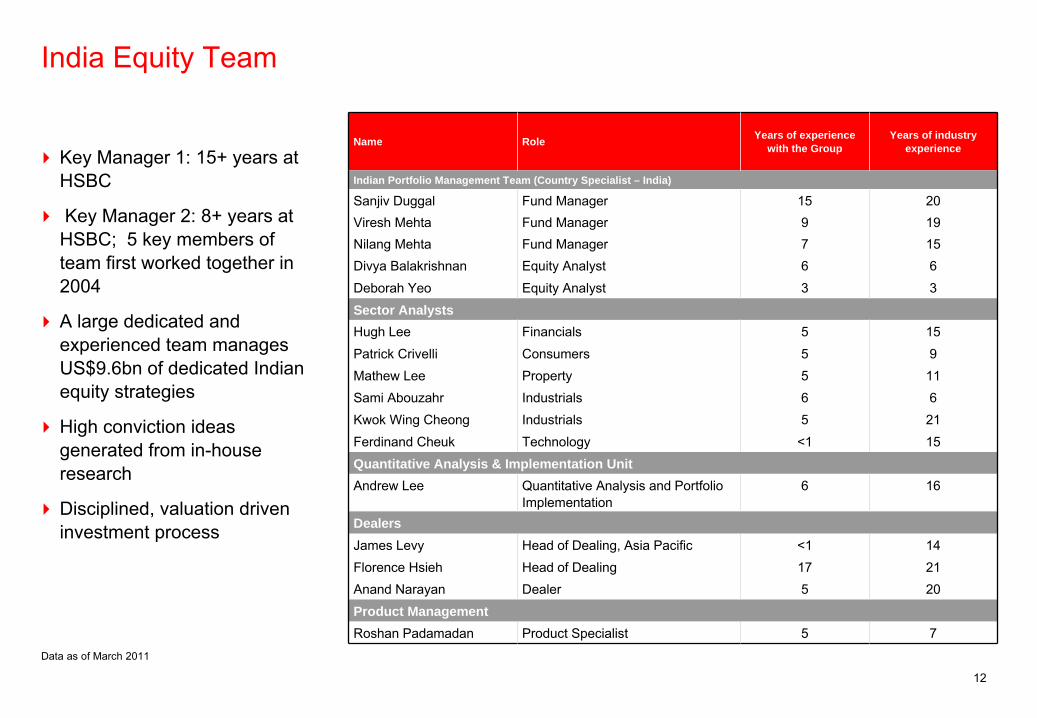

Key Manager 1: 15+ years at HSBC

Key Manager 2: 8+ years at HSBC; 5 key members of team first worked together in 2004

A large dedicated and experienced team manages US$9.6bn of dedicated Indian equity strategies

High conviction ideas generated from in-house research

Disciplined, valuation driven investment process

Data as of March 2011

Name Role Years of experience with the Group

Years of industry experience

Indian Portfolio Management Team (Country Specialist – India)

Sanjiv Duggal Fund Manager 15 20Viresh Mehta Fund Manager 9 19Nilang Mehta Fund Manager 7 15Divya Balakrishnan Equity Analyst 6 6Deborah Yeo Equity Analyst 3 3Sector AnalystsHugh Lee Financials 5 15Patrick Crivelli Consumers 5 9Mathew Lee Property 5 11Sami Abouzahr Industrials 6 6Kwok Wing Cheong Industrials 5 21Ferdinand Cheuk Technology <1 15Quantitative Analysis & Implementation UnitAndrew Lee Quantitative Analysis and Portfolio

Implementation6 16

DealersJames Levy Head of Dealing, Asia Pacific <1 14Florence Hsieh Head of Dealing 17 21Anand

Narayan Dealer 5 20Product ManagementRoshan

Padamadan Product Specialist 5 7

India Equity Team

13

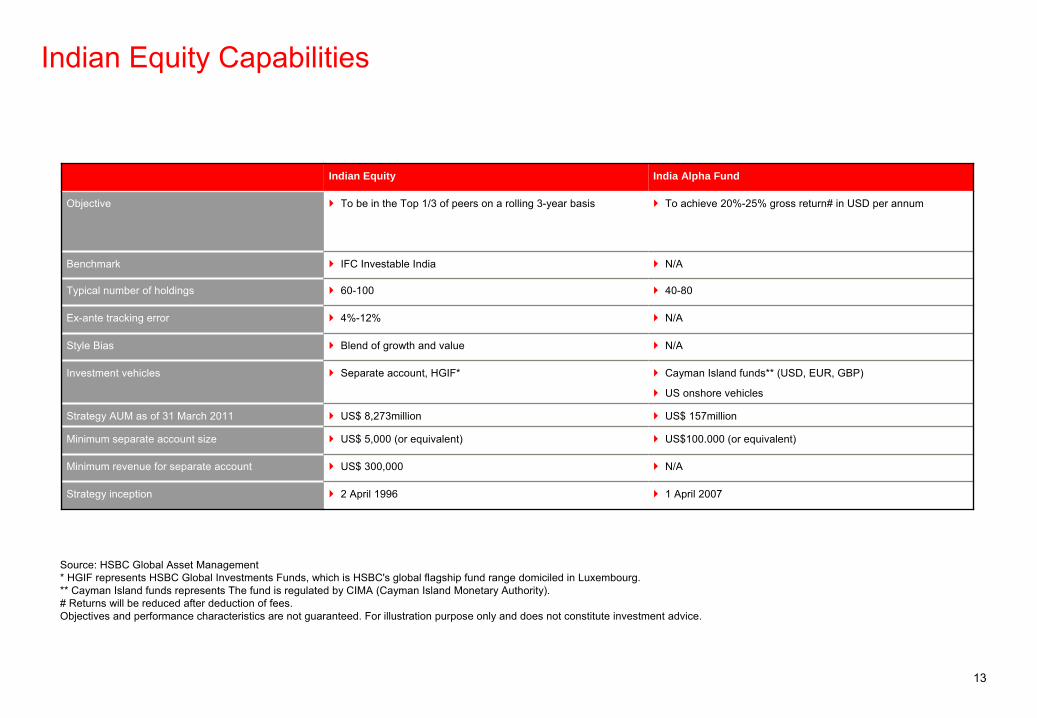

Indian Equity Capabilities

Indian Equity India Alpha Fund

Objective

To be in the Top 1/3 of peers on a rolling 3-year basis

To achieve 20%-25% gross return# in USD per annum

Benchmark

IFC Investable India

N/A

Typical number of holdings

60-100

40-80

Ex-ante tracking error

4%-12%

N/A

Style Bias

Blend of growth and value

N/A

Investment vehicles

Separate account, HGIF*

Cayman Island funds** (USD, EUR, GBP)

US onshore vehicles

Strategy AUM as of 31 March 2011

US$ 8,273million

US$ 157million

Minimum separate account size

US$ 5,000 (or equivalent)

US$100.000 (or equivalent)

Minimum revenue for separate account

US$ 300,000

N/A

Strategy inception

2 April 1996

1 April 2007

Source: HSBC Global Asset Management * HGIF represents HSBC Global Investments Funds, which is HSBC's

global flagship fund range domiciled in Luxembourg.** Cayman Island funds represents The fund is regulated by CIMA (Cayman Island Monetary Authority).# Returns will be reduced after deduction of fees.Objectives and performance characteristics are not guaranteed. For illustration purpose only and does not constitute investment advice.

Investment Philosophy and Process

15

11-IB-10022

Investment Philosophy

We believe that the Indian equity market is inefficient, and that it can stay inefficient for some time

The Indian market is sentiment and rumour/noise driven in the short term

The Indian market can be volatile due to the large options and futures markets

The above factors coupled with momentum can cause severe market distortions at sector and stock levels

Inherent value will be recognised by the market over time, eliminating mis-pricing, thus allowing us to deliver superior returns

Business cycle investing gives a blend of value and/or growth sectors

We are not swayed by rumour, noise and momentum and focus on implementing our investment process in a disciplined manner to exploit the above inefficiencies

We do not believe in overpaying for good companies

16

11-IB-10022

Stock Analysis

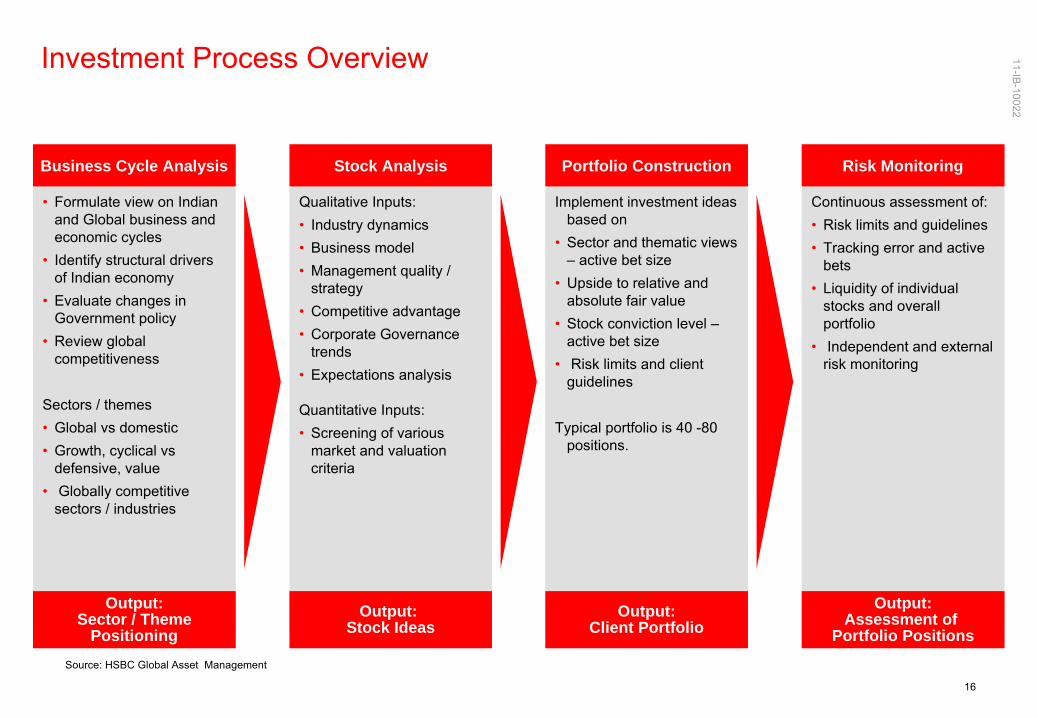

Continuous assessment of:•

Risk limits and guidelines•

Tracking error and active bets

•

Liquidity of individual stocks and overall portfolio

•

Independent and external risk monitoring

Implement investment ideas based on

•

Sector and thematic views –

active bet size•

Upside to relative and absolute fair value

•

Stock conviction level –

active bet size

•

Risk limits and client guidelines

Typical portfolio is 40 -80 positions.

•

Formulate view on Indian and Global business and economic cycles

•

Identify structural drivers of Indian economy

•

Evaluate changes in Government policy

•

Review global competitiveness

Sectors / themes•

Global vs domestic•

Growth, cyclical vs defensive, value

•

Globally competitive sectors / industries

Qualitative Inputs:•

Industry dynamics •

Business model•

Management quality / strategy

•

Competitive advantage •

Corporate Governance trends

•

Expectations analysis

Quantitative Inputs:•

Screening of various market and valuation criteria

Risk MonitoringPortfolio Construction

Output: Sector / Theme

PositioningOutput:

Stock IdeasOutput:

Client PortfolioOutput:

Assessment of Portfolio Positions

Business Cycle Analysis

Source: HSBC Global Asset Management

Investment Process Overview

11-IB-10022

17

Evaluate the Indian and global business cycle and determine cyclical directions–

Focus on inflection points

Identify structural drivers of the Indian economy–

Changes in government policy, for example, privatisation in 2001

& 2002

–

Demographics

Review global competitiveness of Indian sectors–

Software services, generic pharmaceuticals, metals, refining, manufacturing

Evaluate the sectors and themes that will benefit from the above

assessment

Review sector / theme valuations

Source: HSBC Global Asset Management

Investment Process -

Business Cycle Analysis (1) Formulate sector & thematic positioning

11-IB-10022

18

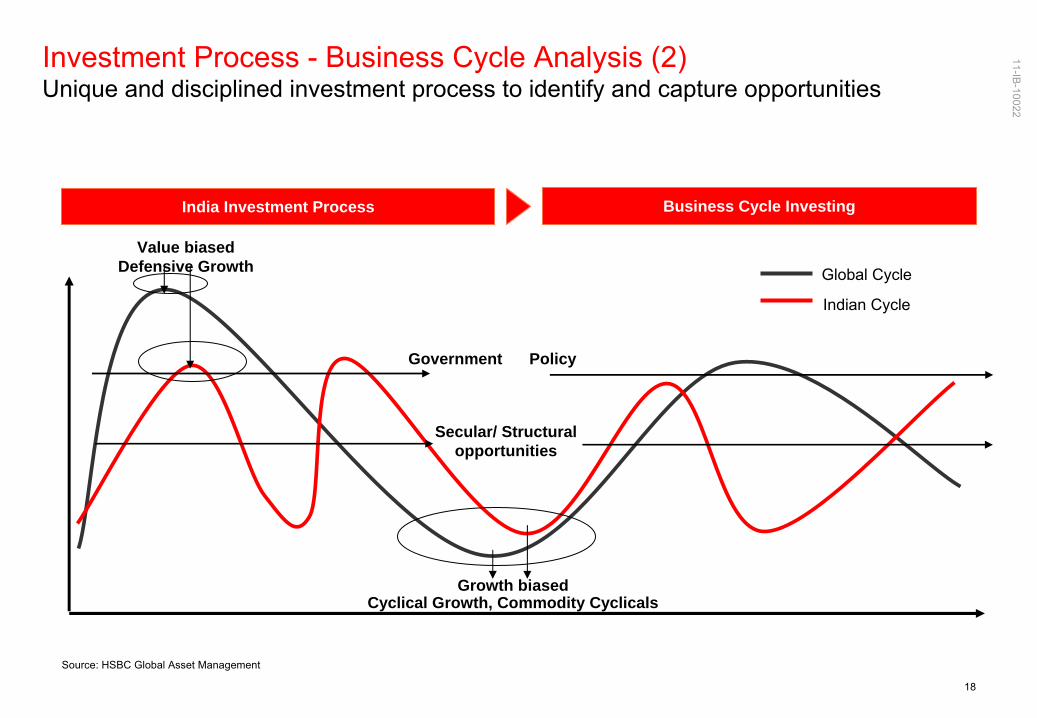

Indian Cycle

Global Cycle

Growth biasedCyclical Growth, Commodity Cyclicals

Government Policy

Secular/ Structural opportunities

Value biasedDefensive Growth

India Investment Process Business Cycle Investing

Investment Process -

Business Cycle Analysis (2) Unique and disciplined investment process to identify and capture opportunities

Source: HSBC Global Asset Management

11-IB-10022

19

The in-depth Stock Analysis combines qualitative and quantitative analysis

The qualitative analysis is based on individual assessment of:

–

Industry dynamics

–

Business model

–

Management quality / strategy

–

Competitive advantage within sector

–

Return on / use of capital

–

Cash flow generation, earnings growth

–

Corporate Governance trends

–

Expectations analysis

Quantitative input:

–

Screen for liquidity and market capitalisation

–

Screen for relative and absolute valuations

Source: HSBC Global Asset Management

Investment Process -

Stock Analysis (1) In-depth analysis of stocks

20

11-IB-10022

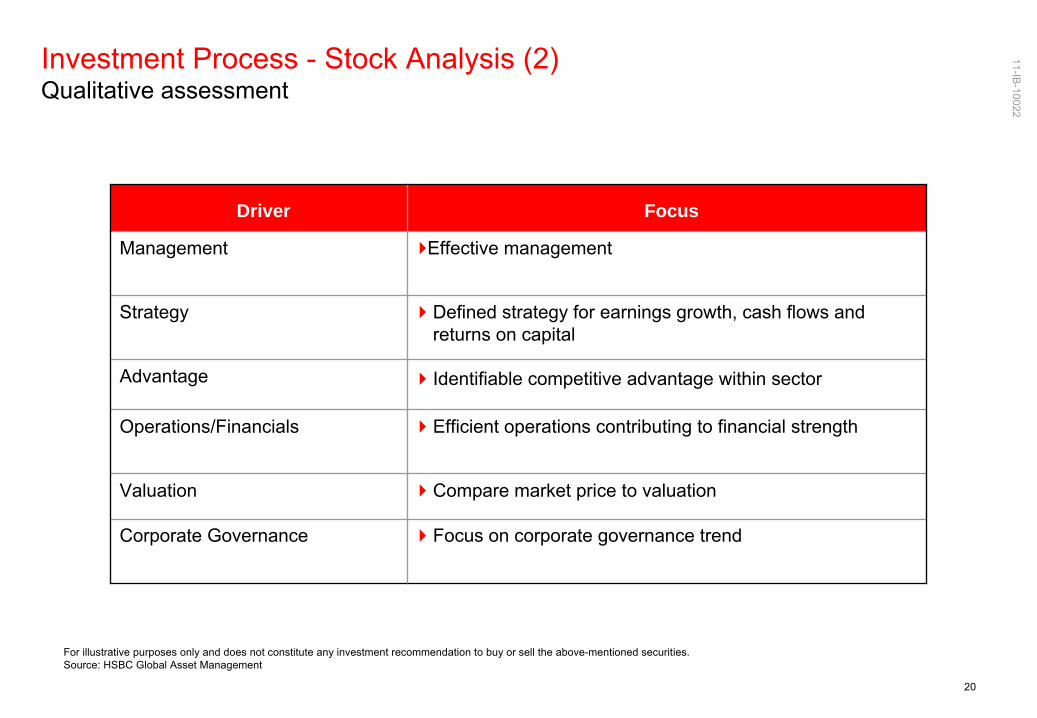

Investment Process -

Stock Analysis (2) Qualitative assessment

For illustrative purposes only and does not constitute any investment recommendation to buy or sell the above-mentioned securities.

Source: HSBC Global Asset Management

Driver Focus

Management Effective management

Strategy

Defined strategy for earnings growth, cash flows and returns on capital

Advantage

Identifiable competitive advantage within sector

Operations/Financials

Efficient operations contributing to financial strength

Valuation

Compare market price to valuation

Corporate Governance

Focus on corporate governance trend

11-IB-10022

21

Implement investment ideas based on

–

Sector and thematic views –

active bet size

–

Upside to relative and absolute fair value

–

Stock conviction level –

active bet size

–

Risk limits and client guidelines

Typical portfolio is 40-80 stocks

Source: HSBC Global Asset Management

Investment Process Construct optimal long portfolio within defined trading limits

11-IB-10022

22

The portfolio is monitored by independent risk monitoring teams

External risk monitoring is overseen by an independent Risk Management department within HSBC Global Asset Management

The team continuously monitors the following:

–

That the portfolio is in line with Risk Limits and Client Guidelines

–

Tracking error of portfolio

–

Contribution from sectors and stocks to total risk

–

Underlying liquidity of individual holding to ensure sufficient liquidity for the portfolio

Source: HSBC Global Asset Management

Investment Process Monitor portfolio positions and adjust if necessary

Risk Management

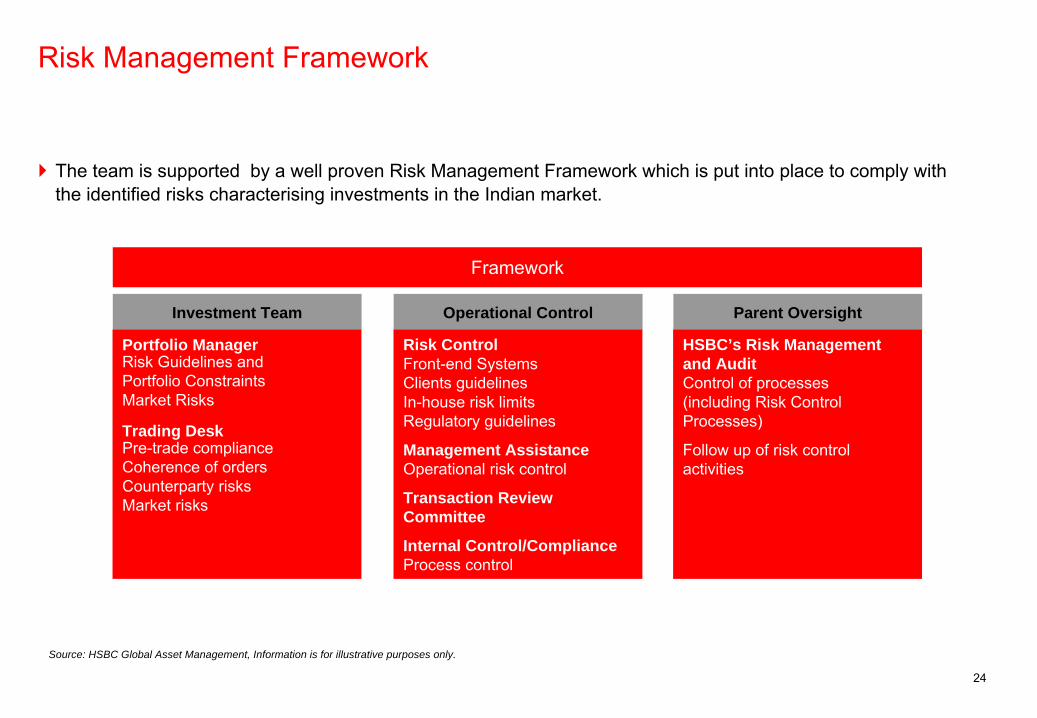

24

Framework

Investment Team Operational Control Parent Oversight

Portfolio Manager Risk Guidelines and Portfolio Constraints Market Risks

Trading Desk Pre-trade compliance

Coherence of orders

Counterparty risks

Market risks

Risk Control Front-end Systems

Clients guidelines

In-house risk limits

Regulatory guidelines

Management Assistance Operational risk control

Transaction Review Committee

Internal Control/Compliance Process control

HSBC’s Risk Management and Audit Control of processes (including Risk Control Processes)

Follow up of risk control activities

The team is supported by a well proven Risk Management Framework which is put into place to comply with the identified risks characterising investments in the Indian market.

Source: HSBC Global Asset Management, Information is for illustrative purposes only.

Risk Management Framework

25

11-IB-10022

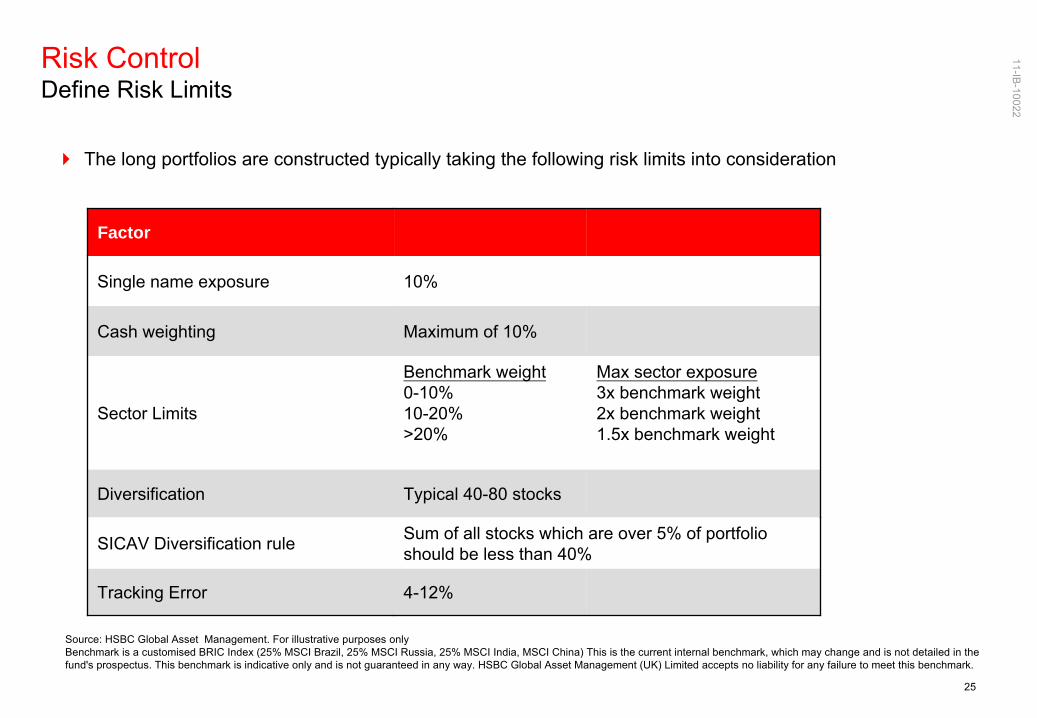

The long portfolios are constructed typically taking the following risk limits into consideration

Source: HSBC Global Asset Management. For illustrative purposes

onlyBenchmark is a customised BRIC Index (25% MSCI Brazil, 25% MSCI Russia, 25% MSCI India, MSCI China) This is the current internal

benchmark, which may change and is not detailed in the fund's prospectus. This benchmark is indicative only and is not guaranteed in any way. HSBC Global Asset Management (UK) Limited

accepts no liability for any failure to meet this benchmark.

Factor

Single name exposure 10%

Cash weighting Maximum of 10%

Sector Limits

Benchmark weight0-10%10-20%>20%

Max sector exposure3x benchmark weight2x benchmark weight1.5x benchmark weight

Diversification Typical 40-80 stocks

SICAV Diversification rule Sum of all stocks which are over 5% of portfolio should be less than 40%

Tracking Error 4-12%

Risk Control Define Risk Limits

26

11-IB-10022

Sell Discipline

Portfolio managers adhere to a strict sell discipline that may be triggered by any of the following:

–

A change in our sector and thematic views driven by our investment process–

A fundamental deterioration in a stock–

Adverse changes in management and strategy–

Corporate governance deterioration–

Price target being reached (absolute or relative) and with no further appreciation expected–

Better opportunities arising in other sectors or stocks within the same sector

This discipline is based on our investment philosophy that the market will eventually recognise inherent value

27

11-IB-10022

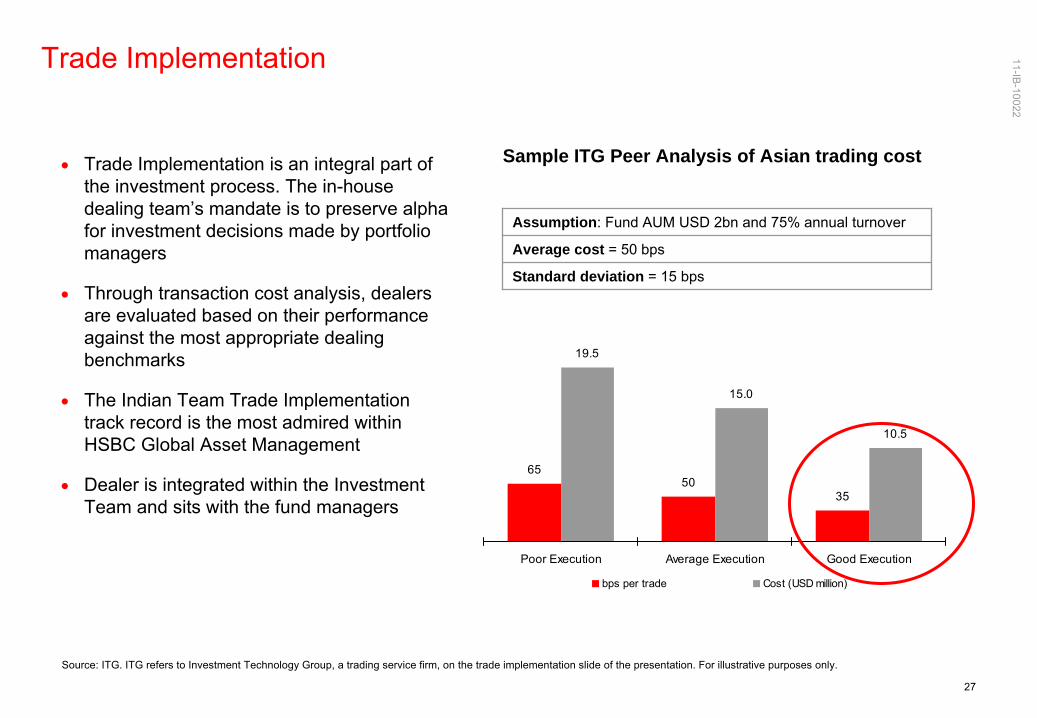

Trade Implementation

Trade Implementation is an integral part of the investment process. The in-house dealing team’s mandate is to preserve alpha for investment decisions made by portfolio managers

Through transaction cost analysis, dealers are evaluated based on their performance against the most appropriate dealing benchmarks

The Indian Team Trade Implementation track record is the most admired within HSBC Global Asset Management

Dealer is integrated within the Investment Team and sits with the fund managers

Sample ITG Peer Analysis of Asian trading cost

Assumption: Fund AUM USD 2bn and 75% annual turnover

Average cost = 50 bps

Standard deviation = 15 bps

6550

35

10.5

15.0

19.5

Poor Execution Average Execution Good Execution

bps per trade Cost (USD million)

Source: ITG. ITG refers to Investment Technology Group, a trading service firm, on the trade implementation slide of the presentation. For illustrative purposes only.

28

11-IB-10022

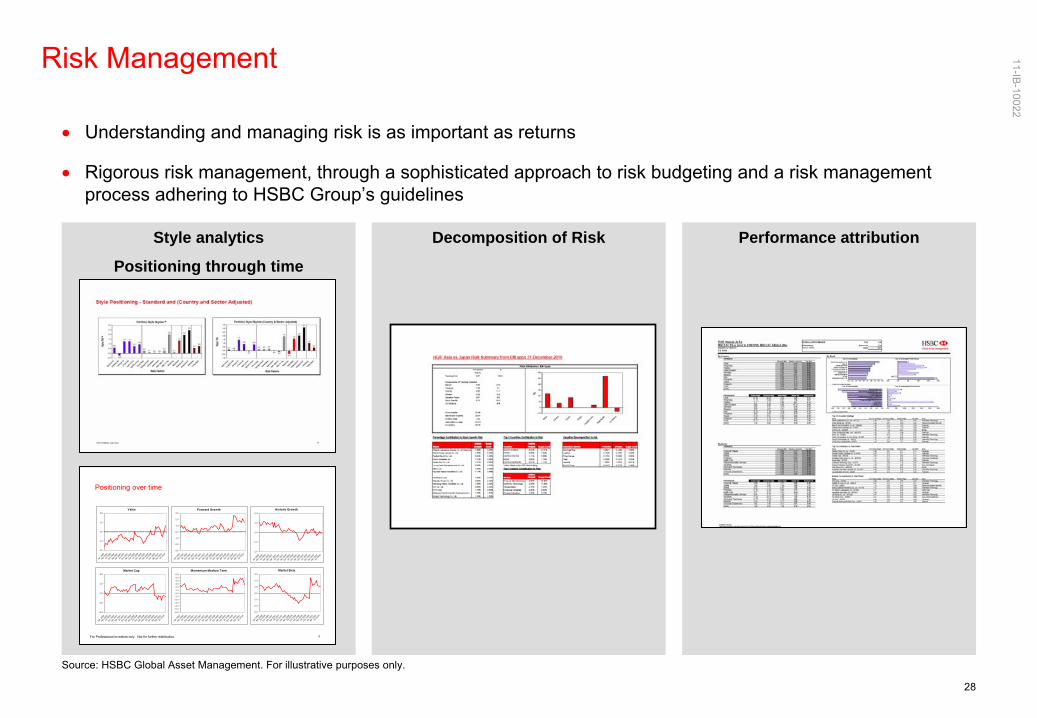

Risk Management

Source: HSBC Global Asset Management. For illustrative purposes only.

Understanding and managing risk is as important as returns

Rigorous risk management, through a sophisticated approach to risk budgeting and a risk management process adhering to HSBC Group’s guidelines

•A

•B

•C

•D

Performance attributionDecomposition of RiskStyle analytics

Positioning through time

8For Professional Investors only. Not for further distribution.

Positioning over time

Value

-2.0

-1.0

0.0

1.0

2.0

Jan

2006

Apr 20

06Ju

l 200

6Oct

2006

Jan

2007

Apr 20

07Ju

l 200

7Oct

2007

Jan

2008

Apr 20

08Ju

l 200

8Oct

2008

Jan

2009

Apr 20

09Ju

l 200

9Oct

2009

Jan

2010

Apr 20

10Ju

l 201

0

Forward Growth

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Jan 2

006

Apr 20

06Ju

l 200

6Oct

2006

Jan 2

007

Apr 20

07Ju

l 200

7Oct

2007

Jan 2

008

Apr 20

08Ju

l 200

8Oct

2008

Jan 2

009

Apr 2

009

Jul 2

009

Oct 20

09Ja

n 201

0Apr

2010

Jul 2

010

Historic Growth

-2.0

-1.0

0.0

1.0

2.0

Jan

2006

Apr 20

06Ju

l 200

6Oct

2006

Jan

2007

Apr 20

07Ju

l 200

7Oct

2007

Jan

2008

Apr 20

08Ju

l 200

8Oct

2008

Jan

2009

Apr 20

09Ju

l 200

9Oct

2009

Jan

2010

Apr 20

10Ju

l 201

0

Market Cap

-2.0

-1.0

0.0

1.0

2.0

Jan 2

006

Apr 20

06Ju

l 200

6Oct

2006

Jan 2

007

Apr 20

07Ju

l 200

7Oct

2007

Jan 2

008

Apr 20

08Ju

l 200

8Oct

2008

Jan 2

009

Apr 2

009

Jul 2

009

Oct 20

09Ja

n 201

0Apr

2010

Jul 2

010

Momentum Medium Term

-6.0

-5.0-4.0-3.0-2.0

-1.00.01.0

2.03.04.05.0

6.0

Jan 2

006

Apr 20

06Ju

l 200

6Oct

2006

Jan 2

007

Apr 2

007

Jul 2

007

Oct 20

07Ja

n 200

8Ap

r 200

8Ju

l 200

8Oct

2008

Jan 2

009

Apr 2

009

Jul 2

009

Oct 20

09Ja

n 201

0Apr

2010

Jul 2

010

Market Beta

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Jan

2006

Apr 20

06Ju

l 200

6Oct

2006

Jan

2007

Apr 20

07Ju

l 200

7Oct

2007

Jan

2008

Apr 20

08Ju

l 200

8Oct

2008

Jan

2009

Apr 2

009

Jul 2

009

Oct 20

09Ja

n 20

10Ap

r 201

0Ju

l 201

0

29

11-IB-10022

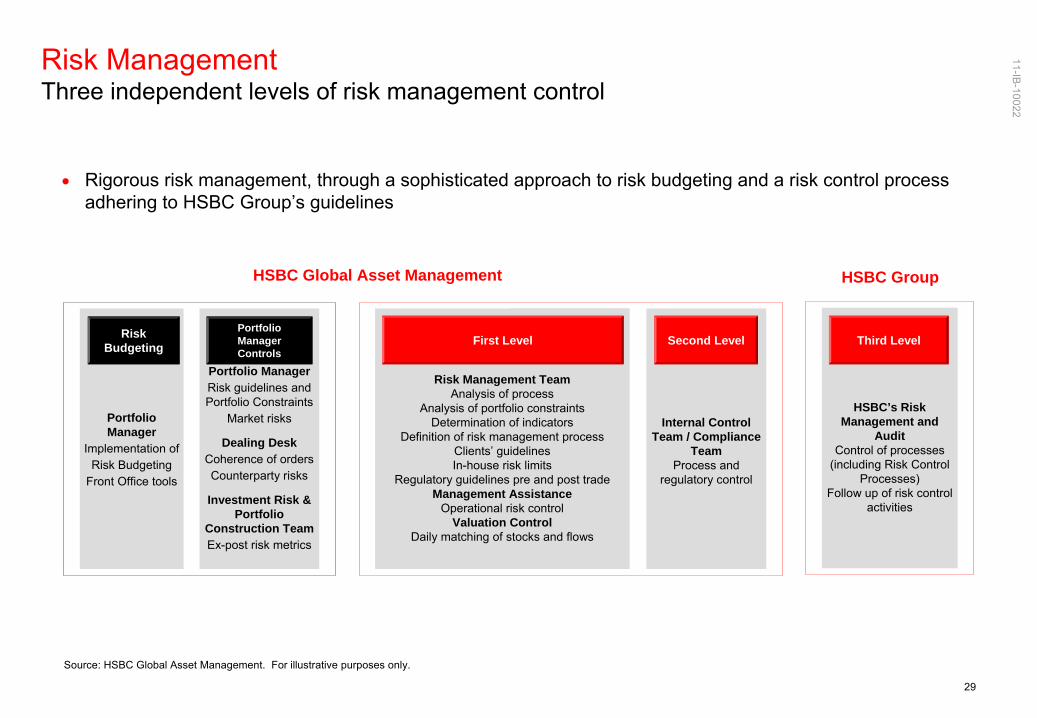

Risk Management Three independent levels of risk management control

Source: HSBC Global Asset Management. For illustrative purposes

only.

Rigorous risk management, through a sophisticated approach to risk budgeting and a risk control process adhering to HSBC Group’s guidelines

HSBC Global Asset Management HSBC Group

Portfolio Manager

Implementation ofRisk Budgeting

Front Office tools

Risk Control TeamClients’

guidelinesIn-house risk limits

Regulatory guidelines pre and

post trade

Management Assistance

Operational risk control

Valuation ControlDaily matching of stocks and flows

Internal Control Team / Compliance

TeamProcess and

regulatory control

HSBC’s Risk Management and

AuditControl of processes

(including Risk Control Processes)

Follow up of risk control activities

Portfolio ManagerRisk guidelines and Portfolio Constraints

Market risks

Dealing DeskCoherence of ordersCounterparty risks

Investment Risk & Portfolio

Construction TeamEx-post risk metrics

Risk Budgeting

Portfolio Manager Controls

Second Level

Risk Management TeamAnalysis of process

Analysis of portfolio constraintsDetermination of indicators

Definition of risk management processClients’

guidelinesIn-house risk limits

Regulatory guidelines pre and post tradeManagement Assistance

Operational risk controlValuation Control

Daily matching of stocks and flows

First Level Third Level

Market Overview

31

Vision 2020•

Over 7% CAGR in GDP in this decade•

To remain amongst fastest growing large economies•

Nominal economy to treble in size

Favourable demographics•

India's population expected to cross China‘s by 2025 •

One of the largest labour pools plus one of the largest consumer

markets•

Rising income and aspirational levels

Improving infrastructure to support growth

Vibrant democracy ensures long-term political stability

Corruption peaking? Improving governance at State level

* For information only and does not have any regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this document.

India = a must-have allocation for growth portfolios *

32

Valuations close to 10-year average

Source: FactSet, MSCI, Morgan Stanley, Bloomberg dated as of June 30, 2011. For illustrative purposes only and does not constitute any investment recommendation to buy or sell in the above-mentioned sectors/index. Opinions expressed herein are subject to change without notice.

Consensus forecasts for EPS growth: FY12: 19% FY13: 17%

(Source: IBES, June 30, 2011)

8

11

14

17

20

23

26

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

5 Yr Avg(16.3)

10 Yr Avg(14.4)

MSCI India 12M Fwd PE, 1995-2011MSCI India Fwd PE

June 2011 (14.5)

Nov-98

Feb 00

Sep 01 Apr 03

Dec 03

Nov 08

Dec 07

33

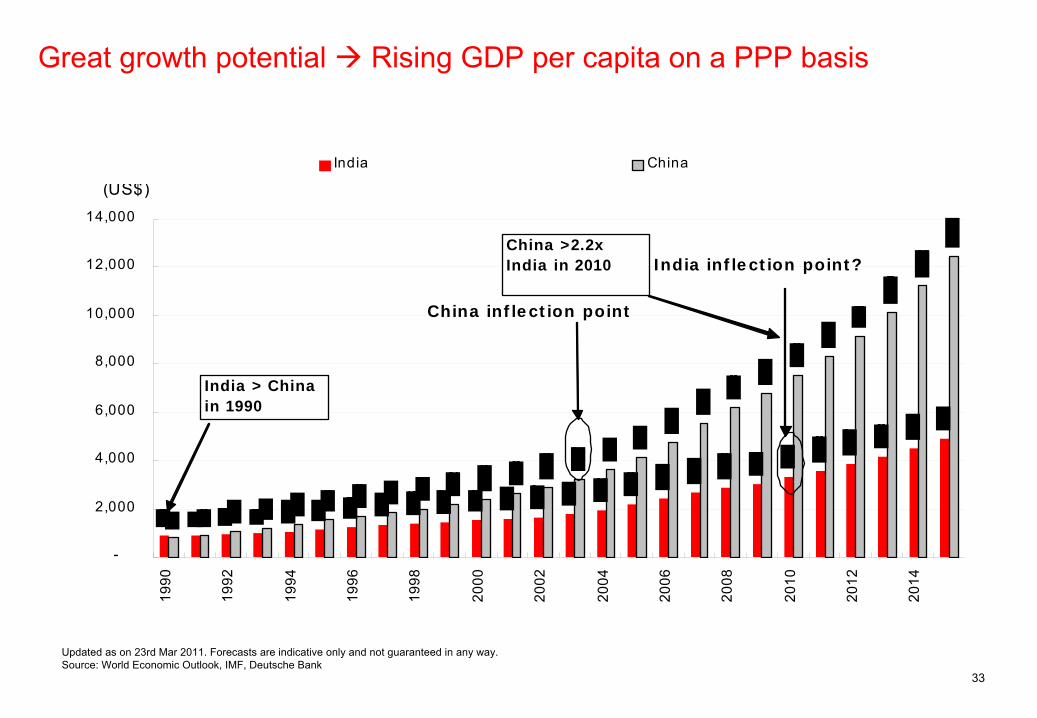

Great growth potential Rising GDP per capita on a PPP basis

Updated as on 23rd Mar 2011. Forecasts are indicative only and not guaranteed in any way.Source: World Economic Outlook, IMF, Deutsche Bank

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

India China

China inf le ct ion point

(US$)

India inf le ct ion point ?

India > China in 1990

China >2.2x India in 2010

3434

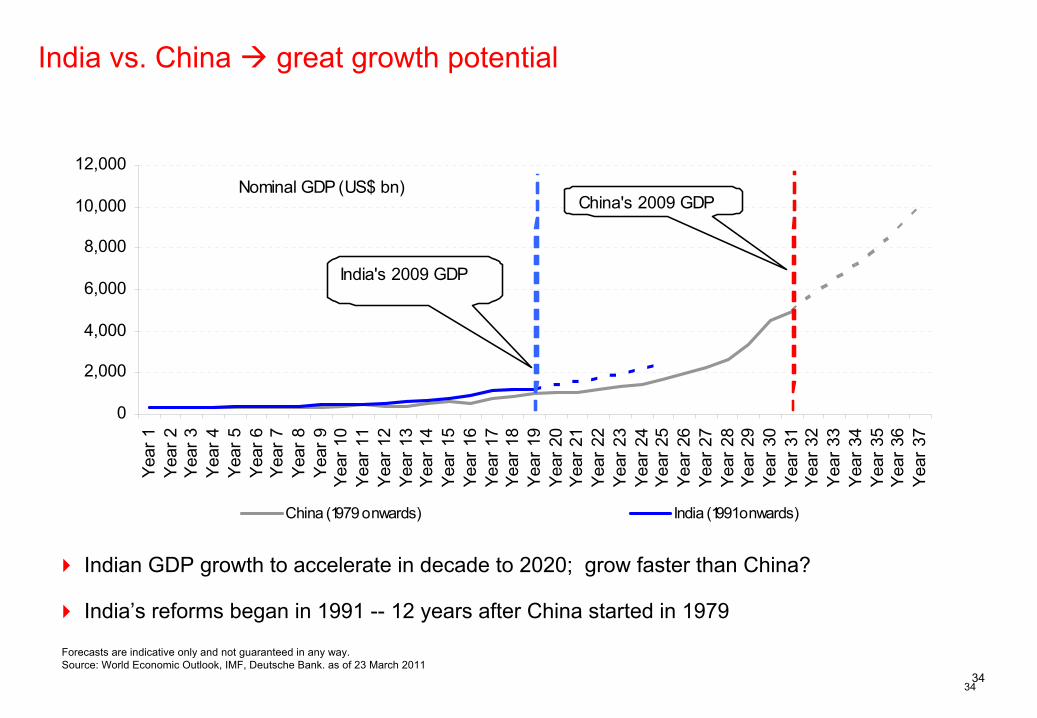

India vs. China great growth potential

Forecasts are indicative only and not guaranteed in any way.Source: World Economic Outlook, IMF, Deutsche Bank. as of 23 March 2011

Indian GDP growth to accelerate in decade to 2020; grow faster than China?

India’s reforms began in 1991 --

12 years after China started in 1979

Nominal GDP (US$ bn)

0

2,000

4,000

6,000

8,000

10,000

12,000Ye

ar 1

Year

2Ye

ar 3

Year

4Ye

ar 5

Year

6Ye

ar 7

Year

8Ye

ar 9

Year

10

Year

11

Year

12

Year

13

Year

14

Year

15

Year

16

Year

17

Year

18

Year

19

Year

20

Year

21

Year

22

Year

23

Year

24

Year

25

Year

26

Year

27

Year

28

Year

29

Year

30

Year

31

Year

32

Year

33

Year

34

Year

35

Year

36

Year

37

China (1979 onwards) India (1991 onwards)

China's 2009 GDP

India's 2009 GDP

35

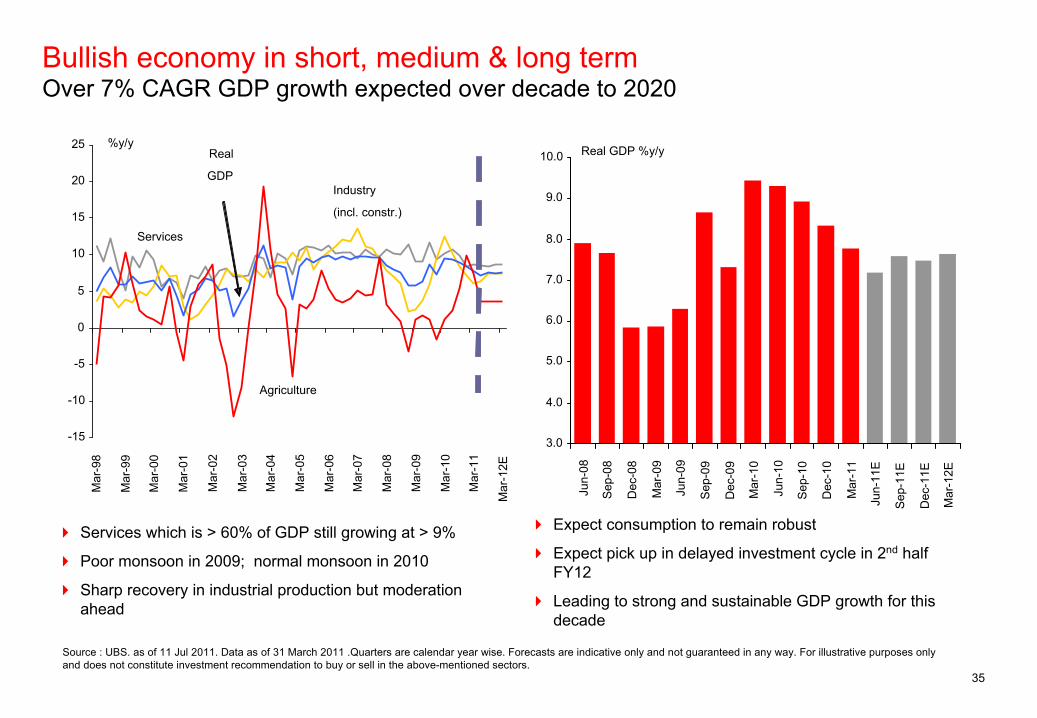

Bullish economy in short, medium & long term Over 7% CAGR GDP growth expected over decade to 2020

Source : UBS. as of 11 Jul 2011. Data as of 31 March 2011 .Quarters are calendar year wise. Forecasts are indicative only and not guaranteed in any way. For illustrative purposes only and does not constitute investment recommendation to buy or sell

in the above-mentioned sectors.

Services which is > 60% of GDP still growing at > 9%

Poor monsoon in 2009; normal monsoon in 2010

Sharp recovery in industrial production but moderation ahead

Expect consumption to remain robust

Expect pick up in delayed investment cycle in 2nd

half FY12

Leading to strong and sustainable GDP growth for this decade

Real GDP %y/y

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11E

Sep-

11E

Dec

-11E

Mar

-12E

%y/y

-15

-10

-5

0

5

10

15

20

25

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12E

Agriculture

Industry

(incl. constr.)

Services

Real

GDP

36

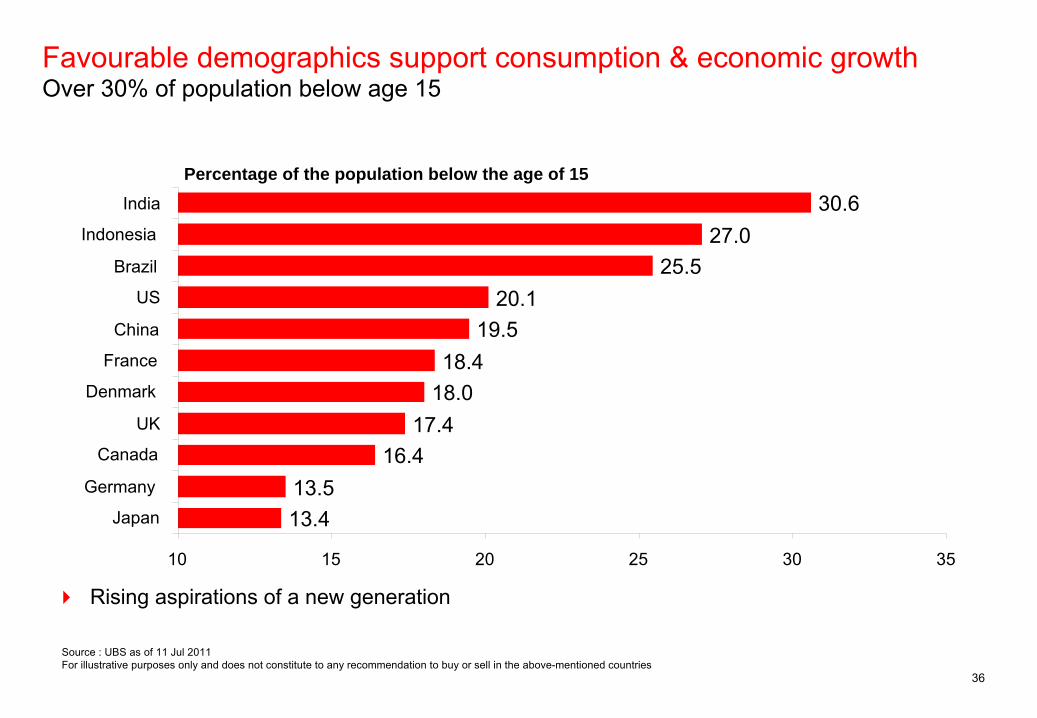

Favourable demographics support consumption & economic growth Over 30% of population below age 15

Source : UBS as of 11 Jul 2011For illustrative purposes only and does not constitute to any recommendation to buy or sell in the above-mentioned countries

Rising aspirations of a new generation

Percentage of the population below the age of 15

13.413.5

16.417.4

18.018.4

19.520.1

25.527.0

30.6

10 15 20 25 30 35

Japan

Germany

Canada

UK

Denmark

France

China

US

Brazil

Indonesia

India

HSBC GIF Indian Equity Fund -

Overview

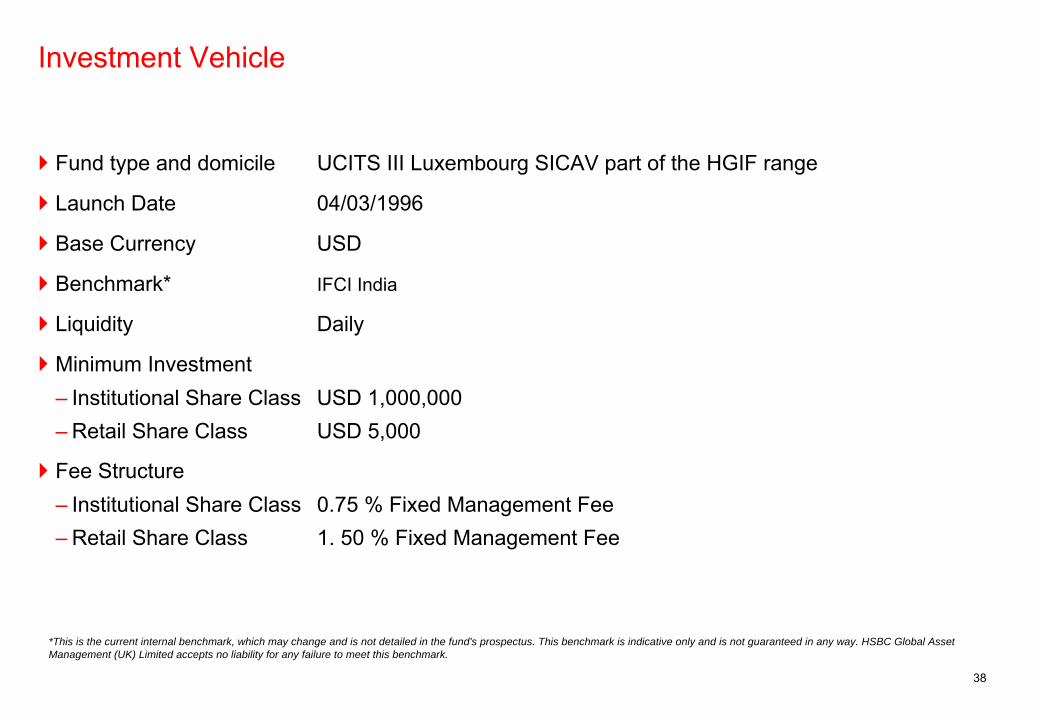

38

Fund type and domicile

UCITS III Luxembourg SICAV part of the HGIF range

Launch Date

04/03/1996

Base Currency

USD

Benchmark*

IFCI India

Liquidity

Daily

Minimum Investment –

Institutional Share Class

USD 1,000,000 –

Retail Share Class

USD 5,000

Fee Structure–

Institutional Share Class 0.75 % Fixed Management Fee–

Retail Share Class

1. 50 % Fixed Management Fee

Investment Vehicle

*This is the current internal benchmark, which may change and is not detailed in the fund's prospectus. This benchmark is indicative only and is not guaranteed in any way. HSBC Global Asset Management (UK) Limited accepts no liability for any failure to meet this benchmark.

39

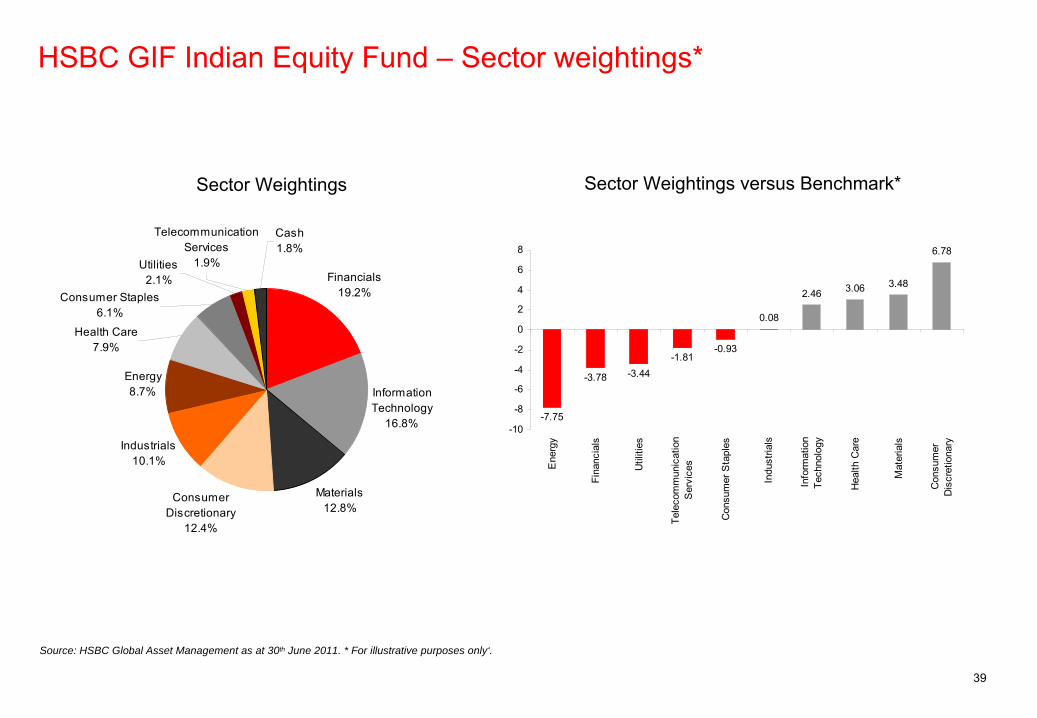

Sector Weightings versus Benchmark*Sector Weightings

HSBC GIF Indian Equity Fund – Sector weightings*

Source: HSBC Global Asset Management as at 30th June 2011. * For illustrative purposes only‘.

Financials19.2%

Information Technology

16.8%

Materials12.8%

Consumer Discretionary

12.4%

Industrials10.1%

Energy8.7%

Utilities2.1%

Consumer Staples6.1%

Health Care7.9%

Cash1.8%

Telecommunication Services

1.9%

-7.75

-3.78 -3.44-1.81

-0.93

0.08

2.46 3.06 3.48

6.78

-10

-8

-6

-4

-2

0

2

4

6

8

Ene

rgy

Fina

ncia

ls

Util

ities

Tele

com

mun

icat

ion

Ser

vice

s

Con

sum

er S

tapl

es

Indu

stria

ls

Info

rmat

ion

Tech

nolo

gy

Hea

lth C

are

Mat

eria

ls

Con

sum

erD

iscr

etio

nary

40

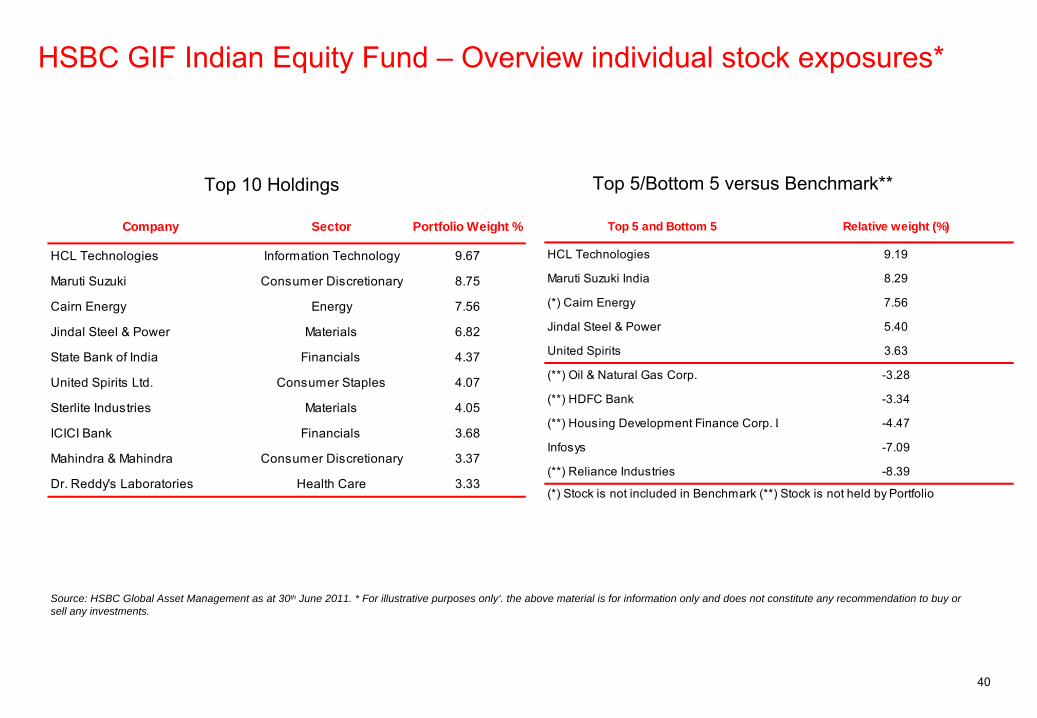

Source: HSBC Global Asset Management as at 30th June 2011. * For illustrative purposes only‘. the above material is for information only and does not constitute any recommendation to buy or sell any investments.

HSBC GIF Indian Equity Fund – Overview individual stock exposures*

Top 5/Bottom 5 versus Benchmark**Top 10 Holdings

Company Sector Portfolio Weight %

HCL Technologies Information Technology 9.67

Maruti Suzuki Consumer Discretionary 8.75

Cairn Energy Energy 7.56

Jindal Steel & Power Materials 6.82

State Bank of India Financials 4.37

United Spirits Ltd. Consumer Staples 4.07

Sterlite Industries Materials 4.05

ICICI Bank Financials 3.68

Mahindra & Mahindra Consumer Discretionary 3.37

Dr. Reddy's Laboratories Health Care 3.33

Top 5 and Bottom 5 Relative weight (%)

HCL Technologies 9.19

Maruti Suzuki India 8.29

(*) Cairn Energy 7.56

Jindal Steel & Power 5.40

United Spirits 3.63

(**) Oil & Natural Gas Corp. -3.28

(**) HDFC Bank -3.34

(**) Housing Development Finance Corp. L -4.47

Infosys -7.09

(**) Reliance Industries -8.39

(*) Stock is not included in Benchmark (**) Stock is not held by Portfolio

41

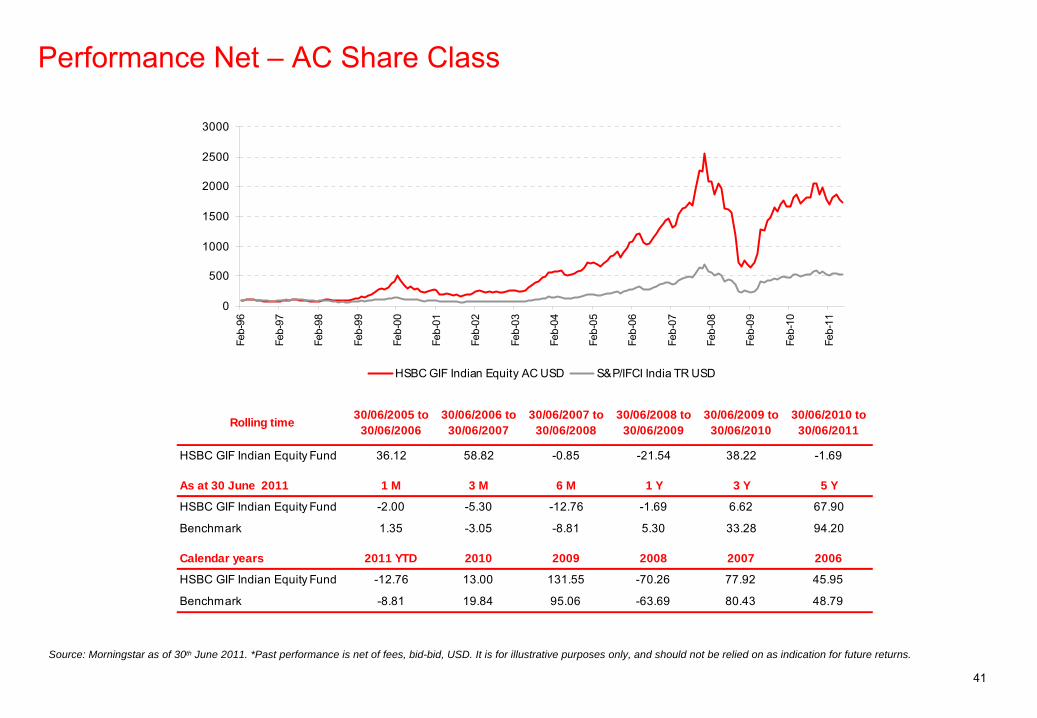

Source: Morningstar as of 30th June 2011. *Past performance is net of fees, bid-bid, USD. It is for illustrative purposes only, and should not be relied on as indication for future returns.

Performance Net –

AC Share Class

0

500

1000

1500

2000

2500

3000

Feb-

96

Feb-

97

Feb-

98

Feb-

99

Feb-

00

Feb-

01

Feb-

02

Feb-

03

Feb-

04

Feb-

05

Feb-

06

Feb-

07

Feb-

08

Feb-

09

Feb-

10

Feb-

11

HSBC GIF Indian Equity AC USD S&P/IFCI India TR USD

Rolling time 30/06/2005 to 30/06/2006

30/06/2006 to 30/06/2007

30/06/2007 to 30/06/2008

30/06/2008 to 30/06/2009

30/06/2009 to 30/06/2010

30/06/2010 to 30/06/2011

HSBC GIF Indian Equity Fund 36.12 58.82 -0.85 -21.54 38.22 -1.69

As at 30 June 2011 1 M 3 M 6 M 1 Y 3 Y 5 Y

HSBC GIF Indian Equity Fund -2.00 -5.30 -12.76 -1.69 6.62 67.90

Benchmark 1.35 -3.05 -8.81 5.30 33.28 94.20

Calendar years 2011 YTD 2010 2009 2008 2007 2006

HSBC GIF Indian Equity Fund -12.76 13.00 131.55 -70.26 77.92 45.95

Benchmark -8.81 19.84 95.06 -63.69 80.43 48.79

42

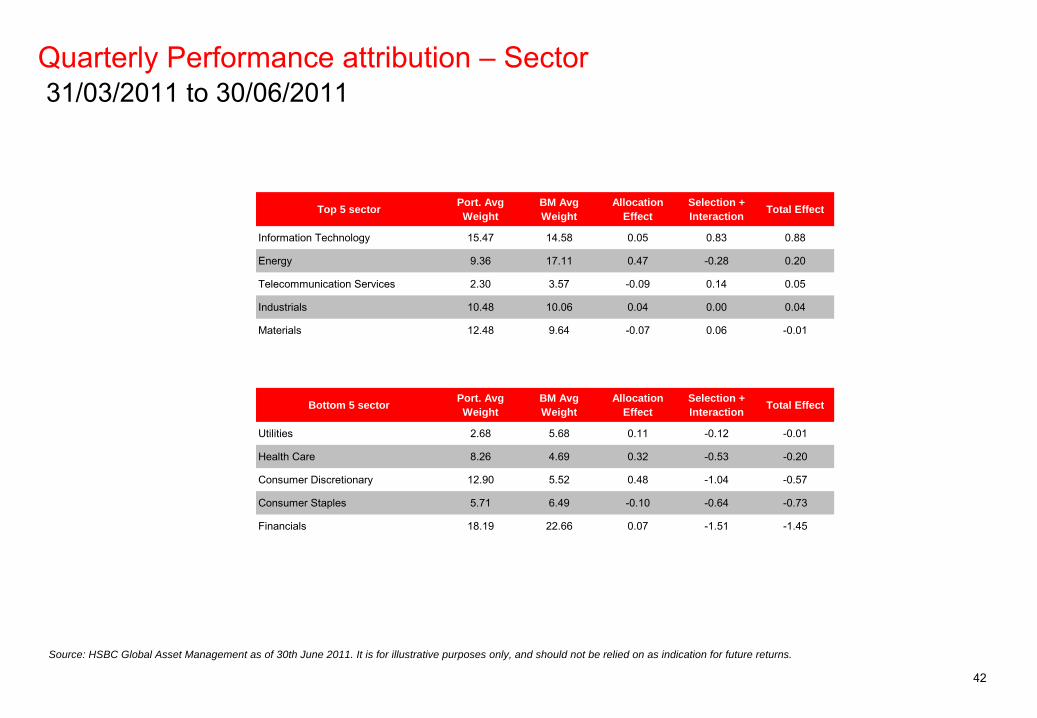

Quarterly Performance attribution – Sector31/03/2011 to 30/06/2011

Source: HSBC Global Asset Management as of 30th June 2011. It is for illustrative purposes only, and should not be relied on as indication for future returns.

Top 5 sector Port. Avg Weight

BM Avg Weight

Allocation Effect

Selection + Interaction Total Effect

Information Technology 15.47 14.58 0.05 0.83 0.88

Energy 9.36 17.11 0.47 -0.28 0.20

Telecommunication Services 2.30 3.57 -0.09 0.14 0.05

Industrials 10.48 10.06 0.04 0.00 0.04

Materials 12.48 9.64 -0.07 0.06 -0.01

Bottom 5 sector Port. Avg Weight

BM Avg Weight

Allocation Effect

Selection + Interaction Total Effect

Utilities 2.68 5.68 0.11 -0.12 -0.01

Health Care 8.26 4.69 0.32 -0.53 -0.20

Consumer Discretionary 12.90 5.52 0.48 -1.04 -0.57

Consumer Staples 5.71 6.49 -0.10 -0.64 -0.73

Financials 18.19 22.66 0.07 -1.51 -1.45

43

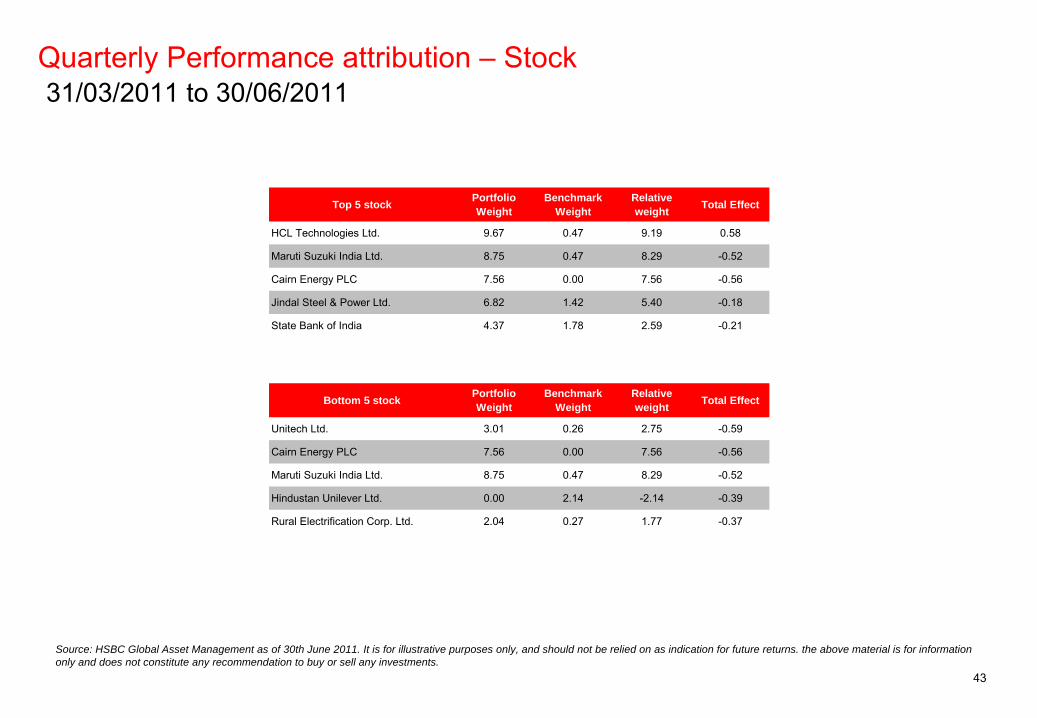

Source: HSBC Global Asset Management as of 30th June 2011. It is for illustrative purposes only, and should not be relied on as indication for future returns. the above material is for information only and does not constitute any recommendation to buy or sell any investments.

Quarterly Performance attribution – Stock31/03/2011 to 30/06/2011

Top 5 stock Portfolio Weight

Benchmark Weight

Relative weight Total Effect

HCL Technologies Ltd. 9.67 0.47 9.19 0.58

Maruti Suzuki India Ltd. 8.75 0.47 8.29 -0.52

Cairn Energy PLC 7.56 0.00 7.56 -0.56

Jindal Steel & Power Ltd. 6.82 1.42 5.40 -0.18

State Bank of India 4.37 1.78 2.59 -0.21

Bottom 5 stock Portfolio Weight

Benchmark Weight

Relative weight Total Effect

Unitech Ltd. 3.01 0.26 2.75 -0.59

Cairn Energy PLC 7.56 0.00 7.56 -0.56

Maruti Suzuki India Ltd. 8.75 0.47 8.29 -0.52

Hindustan Unilever Ltd. 0.00 2.14 -2.14 -0.39

Rural Electrification Corp. Ltd. 2.04 0.27 1.77 -0.37

Competitor Analysis

45

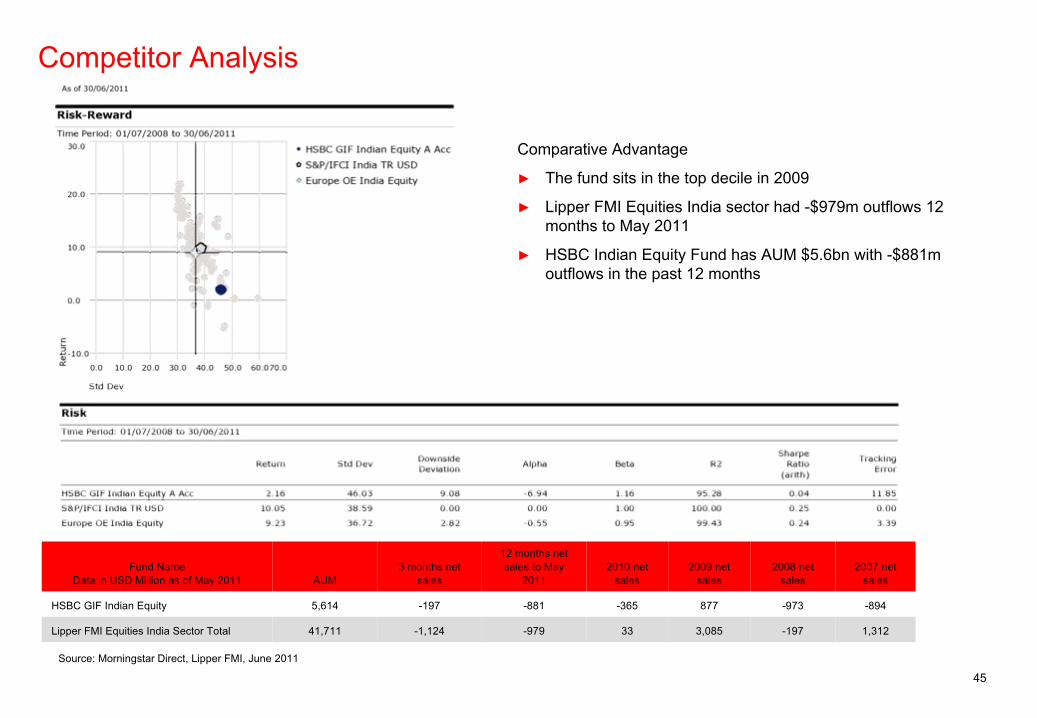

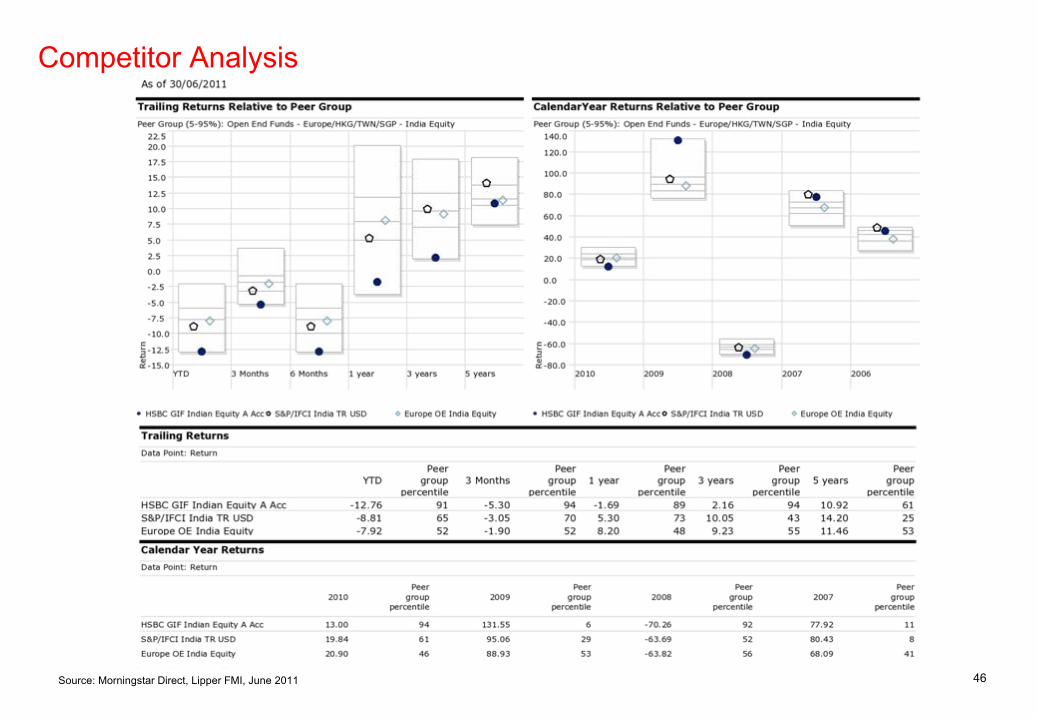

Competitor Analysis

Fund Name Data in USD Million as of May 2011 AUM

3 months net sales

12 months net sales to May

20112010 net

sales 2009 net

sales2008 net

sales2007 net

sales

HSBC GIF Indian Equity 5,614 -197 -881 -365 877 -973 -894

Lipper FMI Equities India Sector Total 41,711 -1,124 -979 33 3,085 -197 1,312

Source: Morningstar Direct, Lipper FMI, June 2011

Comparative Advantage

►

The fund sits in the top decile

in 2009

►

Lipper FMI Equities India sector had -$979m outflows 12 months to May 2011

►

HSBC Indian Equity Fund has AUM $5.6bn with -$881m outflows in the past 12 months

46

Competitor Analysis

Source: Morningstar Direct, Lipper FMI, June 2011

Outlook

48

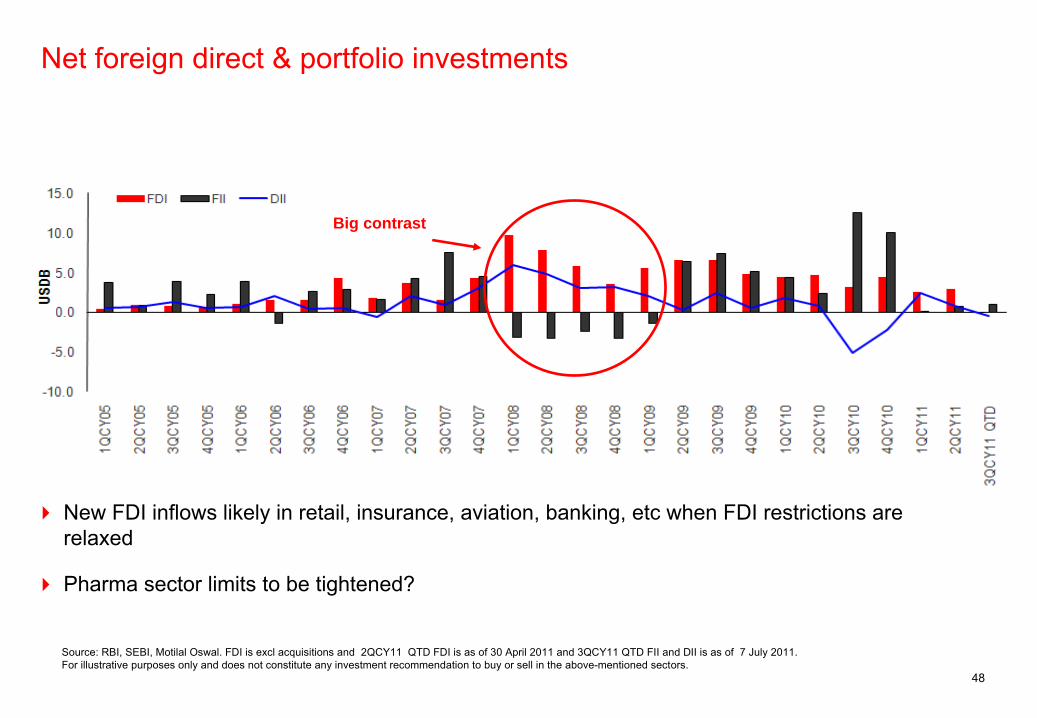

Net foreign direct & portfolio investments

Source: RBI, SEBI, Motilal Oswal. FDI is excl acquisitions and 2QCY11 QTD FDI is as of 30 April 2011 and 3QCY11 QTD FII and DII is as of 7 July 2011.

For illustrative purposes only and does not constitute any investment recommendation to buy or sell in the above-mentioned sectors.

Big contrast

New FDI inflows likely in retail, insurance, aviation, banking, etc when FDI restrictions are relaxed

Pharma sector limits to be tightened?

49

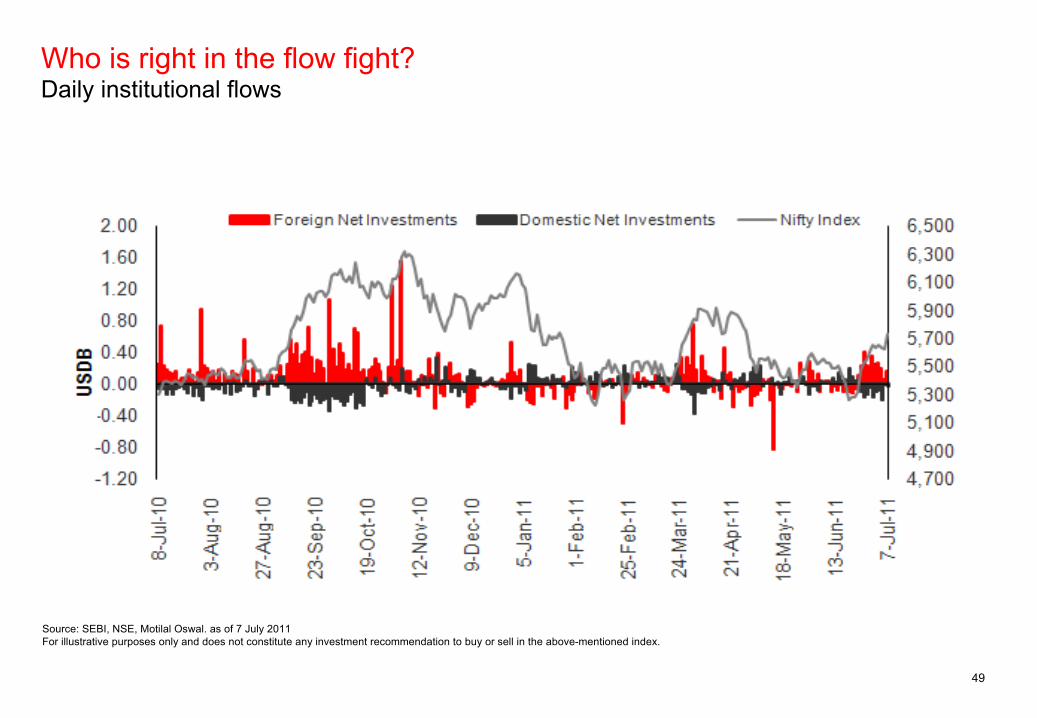

Source: SEBI, NSE, Motilal Oswal. as of 7 July 2011For illustrative purposes only and does not constitute any investment recommendation to buy or sell in the above-mentioned index.

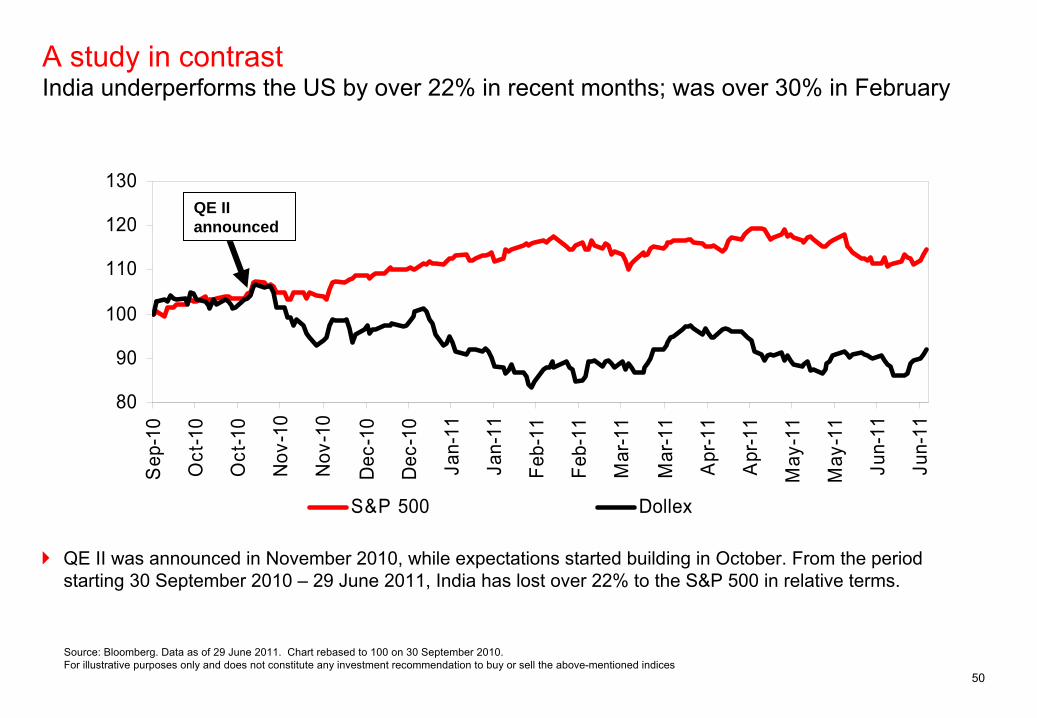

Who is right in the flow fight? Daily institutional flows

50

80

90

100

110

120

130S

ep-1

0

Oct

-10

Oct

-10

Nov

-10

Nov

-10

Dec

-10

Dec

-10

Jan-

11

Jan-

11

Feb-

11

Feb-

11

Mar

-11

Mar

-11

Apr

-11

Apr

-11

May

-11

May

-11

Jun-

11

Jun-

11

S&P 500 Dollex

Source: Bloomberg. Data as of 29 June 2011. Chart rebased to 100 on 30 September 2010.For illustrative purposes only and does not constitute any investment recommendation to buy or sell the above-mentioned indices

QE II was announced in November 2010, while expectations started

building in October. From the period starting 30 September 2010 –

29 June 2011, India has lost over 22% to the S&P 500 in relative terms.

A study in contrast India underperforms the US by over 22% in recent months; was over 30% in February

QE II announced

51

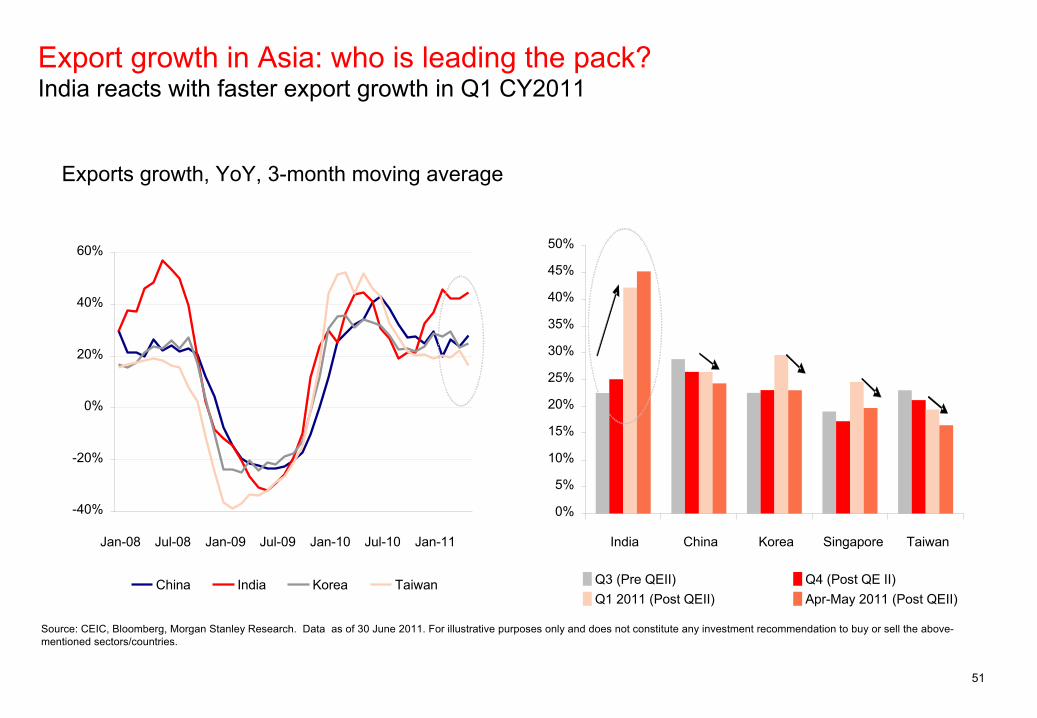

Export growth in Asia: who is leading the pack? India reacts with faster export growth in Q1 CY2011

Source: CEIC, Bloomberg, Morgan Stanley Research. Data as of 30 June 2011. For illustrative purposes only and does not constitute any investment recommendation to buy or sell the above-

mentioned sectors/countries.

Exports growth, YoY, 3-month moving average

-40%

-20%

0%

20%

40%

60%

Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11

China India Korea Taiwan

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

India China Korea Singapore Taiwan

Q3 (Pre QEII) Q4 (Post QE II)Q1 2011 (Post QEII) Apr-May 2011 (Post QEII)

52

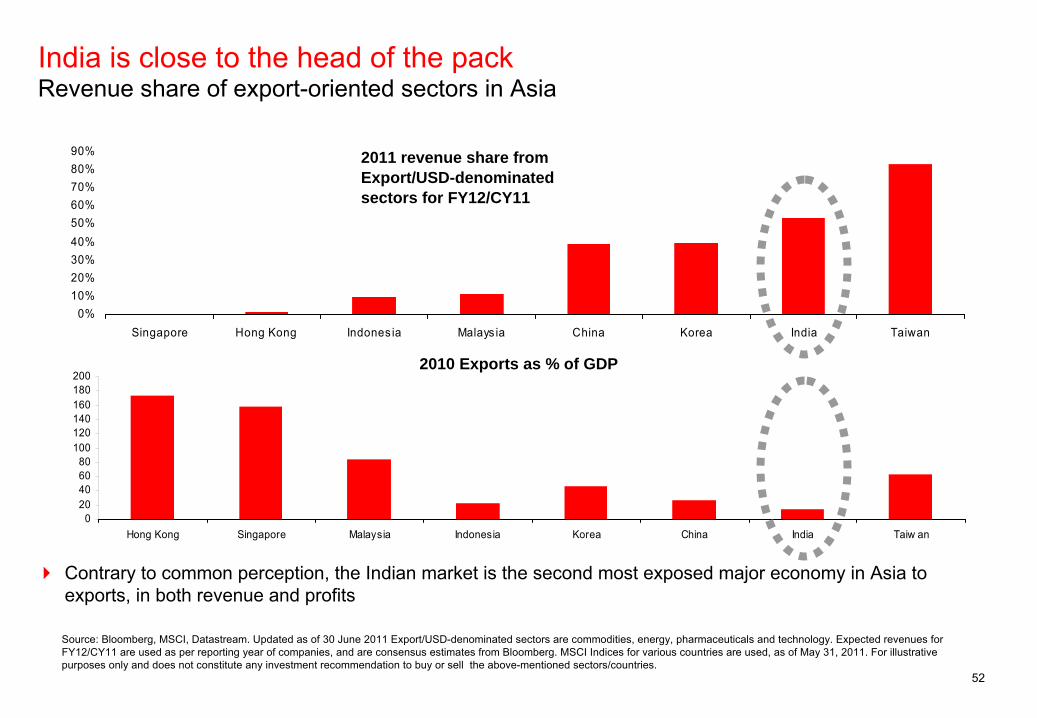

0%10%20%30%40%50%60%70%80%90%

Singapore Hong Kong Indones ia Malays ia China Korea India Taiwan

020406080

100120140160180200

Hong Kong Singapore Malaysia Indonesia Korea China India Taiw an

Source: Bloomberg, MSCI, Datastream. Updated as of 30 June 2011 Export/USD-denominated sectors are commodities, energy, pharmaceuticals and

technology. Expected revenues for FY12/CY11 are used as per reporting year of companies, and are consensus estimates from Bloomberg. MSCI Indices for various countries are used, as of May 31, 2011. For illustrative purposes only and does not constitute any investment recommendation to buy or sell the above-mentioned sectors/countries.

Contrary to common perception, the Indian market is the second most exposed major economy in Asia to exports, in both revenue and profits

2011 revenue share from Export/USD-denominated sectors for FY12/CY11

2010 Exports as % of GDP

India is close to the head of the pack Revenue share of export-oriented sectors in Asia

53

Source: CLSA Asia-Pacific Markets as 28th February 2011. *Unique Identification Authority (India)

Fiscal deficit for FY12 targeted at 4.6% (FY11 estimated at 5.2%)

Fiscal deficit targeted to be brought down to 3.5% by FY14

Assumed nominal GDP growth of 14% appears conservative

Moderate tax rates and simplify system, introduce Direct Taxes Code and Goods and Services Tax

Focus on infrastructure and manufacturing

Reforms to continue

Liberalise

FDI policy

Guidelines on new banking licenses to be issued

Continue divestment

Roll out of UID*

Direct transfer of cash subsidies

FY12 Union Budget –

The Inclusive Growth Mantra

54

Inflation –

a concern being addressed

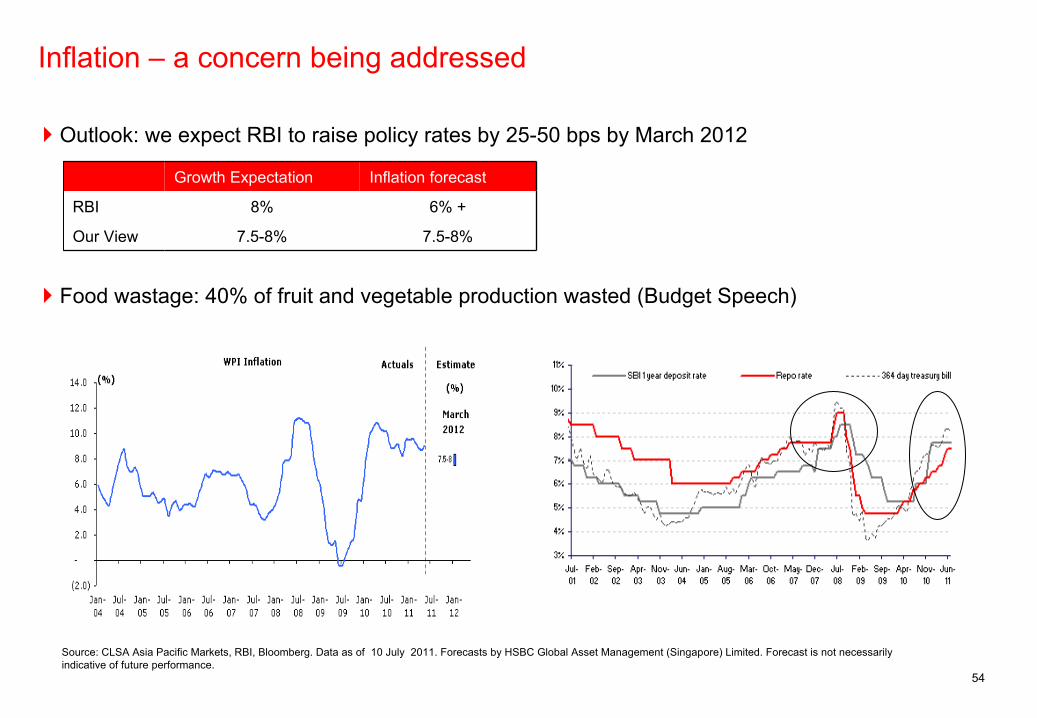

Outlook: we expect RBI to raise policy rates by 25-50 bps by March 2012

Food wastage: 40% of fruit and vegetable production wasted (Budget Speech)

Source: CLSA Asia Pacific Markets, RBI, Bloomberg. Data as of 10 July 2011. Forecasts by HSBC Global Asset Management (Singapore) Limited. Forecast is not necessarily indicative of future performance.

Growth Expectation Inflation forecast

RBI 8% 6% +

Our View 7.5-8% 7.5-8%

55Source: CLSA Asia-Pacific Markets as 30 April 2011

Multiple corruption / bribery issues affected market sentiment in recent months

2G Telecom ‘scandal’

from early 2008

New Delhi Commonwealth Games

Raids on financial institutions in 4th

quarter 2010

Food, fertiliser

and fuel subsidy losses

Leakage to be reduced substantially by Unique Identification (UID) numbers

UID Benefits Increase Financial inclusion

At least 50% of adult Indians have no bank account

Subsidy reduction and targeting of benefits

Over US$200bn of subsidies to be given over next five years. Cash transfers -

more efficient

Tracking transactions

Better tax administration

Corruption

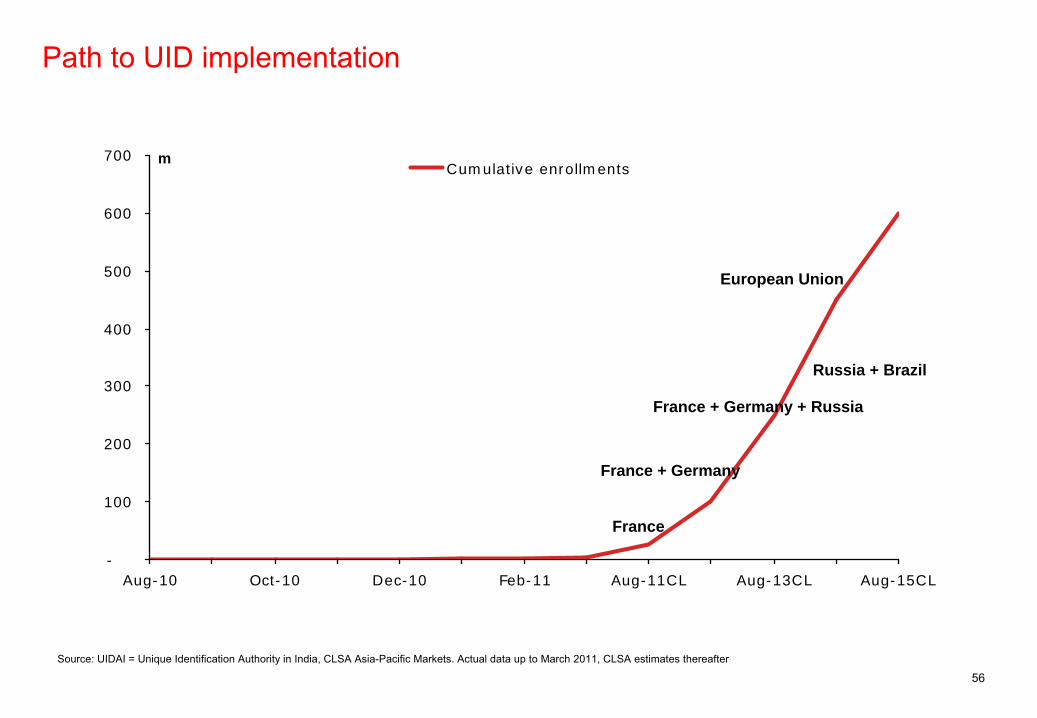

56Source: UIDAI = Unique Identification Authority in India, CLSA Asia-Pacific Markets. Actual data up to March 2011, CLSA estimates thereafter

-

100

200

300

400

500

600

700

Aug-10 Oct-10 Dec-10 Feb-11 Aug-11CL Aug-13CL Aug-15CL

mCumulative enrollments

France

France + Germany

European Union

France + Germany + Russia

Russia + Brazil

Path to UID implementation

57

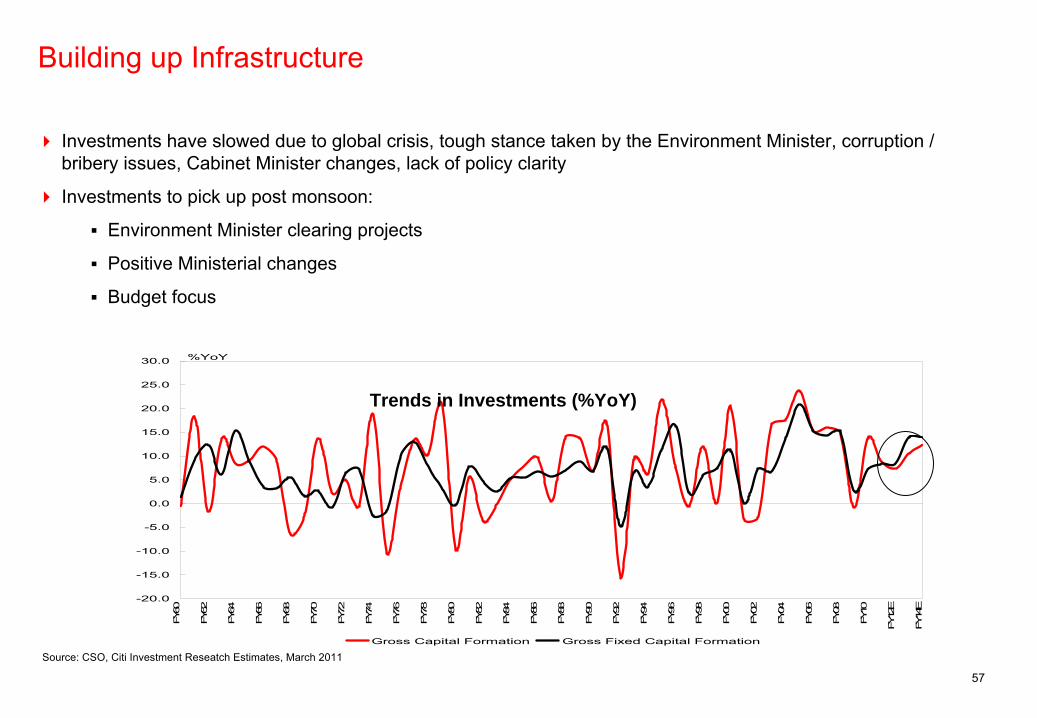

Building up Infrastructure

Source: CSO, Citi Investment Reseatch

Estimates, March 2011

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

FY60

FY62

FY64

FY66

FY68

FY70

FY72

FY74

FY76

FY78

FY80

FY82

FY84

FY86

FY88

FY90

FY92

FY94

FY96

FY98

FY00

FY02

FY04

FY06

FY08

FY10

FY12

E

FY14

E

Gross Capital Formation Gross Fixed Capital Formation

%YoY

Investments have slowed due to global crisis, tough stance taken

by the Environment Minister, corruption / bribery issues, Cabinet Minister changes, lack of policy clarity

Investments to pick up post monsoon:

Environment Minister clearing projects

Positive Ministerial changes

Budget focus

Trends in Investments (%YoY)

58

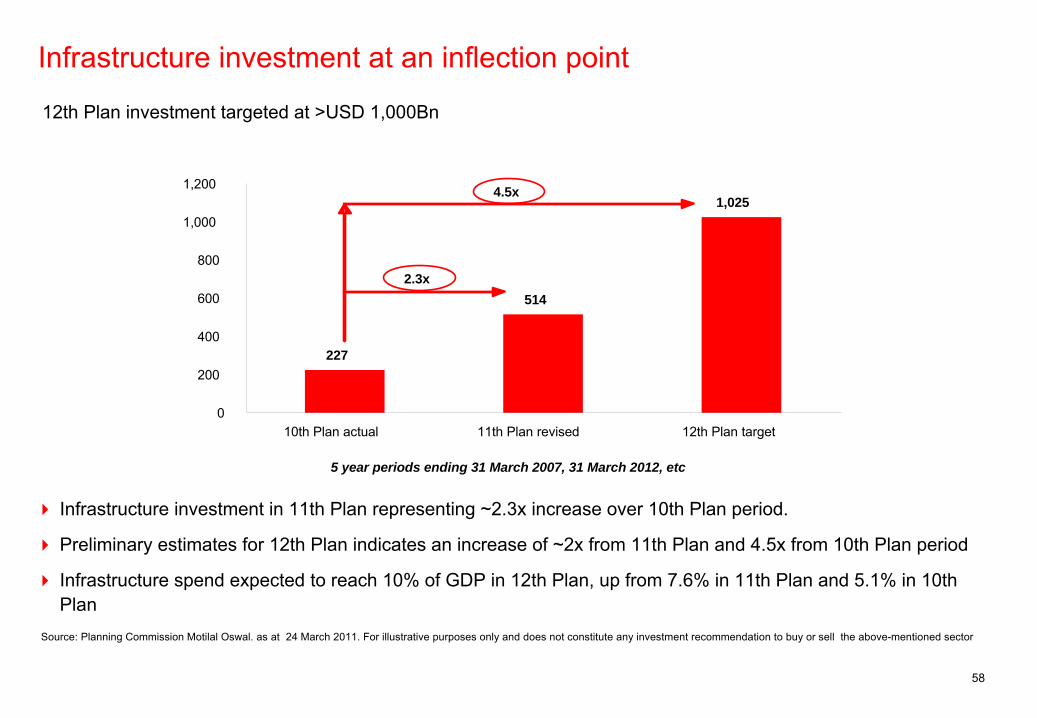

Infrastructure investment at an inflection point

12th Plan investment targeted at >USD 1,000Bn

Infrastructure investment in 11th Plan representing ~2.3x increase over 10th Plan period.

Preliminary estimates for 12th Plan indicates an increase of ~2x

from 11th Plan and 4.5x from 10th Plan period

Infrastructure spend expected to reach 10% of GDP in 12th Plan, up from 7.6% in 11th Plan and 5.1% in 10th Plan

Source: Planning Commission Motilal

Oswal. as at 24 March 2011. For illustrative purposes only and

does not constitute any investment recommendation to buy or sell the above-mentioned sector

227

514

1,025

0

200

400

600

800

1,000

1,200

10th Plan actual 11th Plan revised 12th Plan target

2.3x

4.5x

5 year periods ending 31 March 2007, 31 March 2012, etc

59

1.5

31.3

64.470.4

77.3

88.7

108.2

0

20

40

60

80

100

120

Germany Australia USA UK Brazil France India

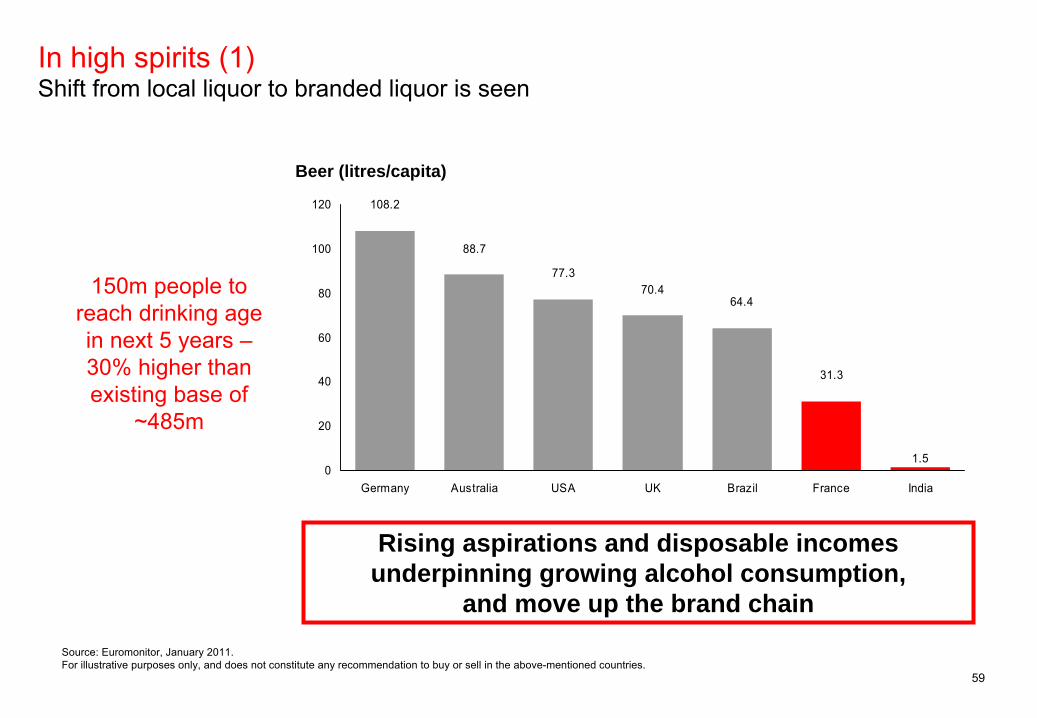

In high spirits (1) Shift from local liquor to branded liquor is seen

150m people to reach drinking age in next 5 years –

30% higher than existing base of

~485m

Source: Euromonitor, January 2011.For illustrative purposes only, and does not constitute any recommendation to buy or sell in the above-mentioned countries.

Rising aspirations and disposable incomes underpinning growing alcohol consumption,

and move up the brand chain

Beer (litres/capita)

60

1.7

6.3

2.9

5.25.45.7

7.1

012345678

Brazil France Germany USA UK Australia India

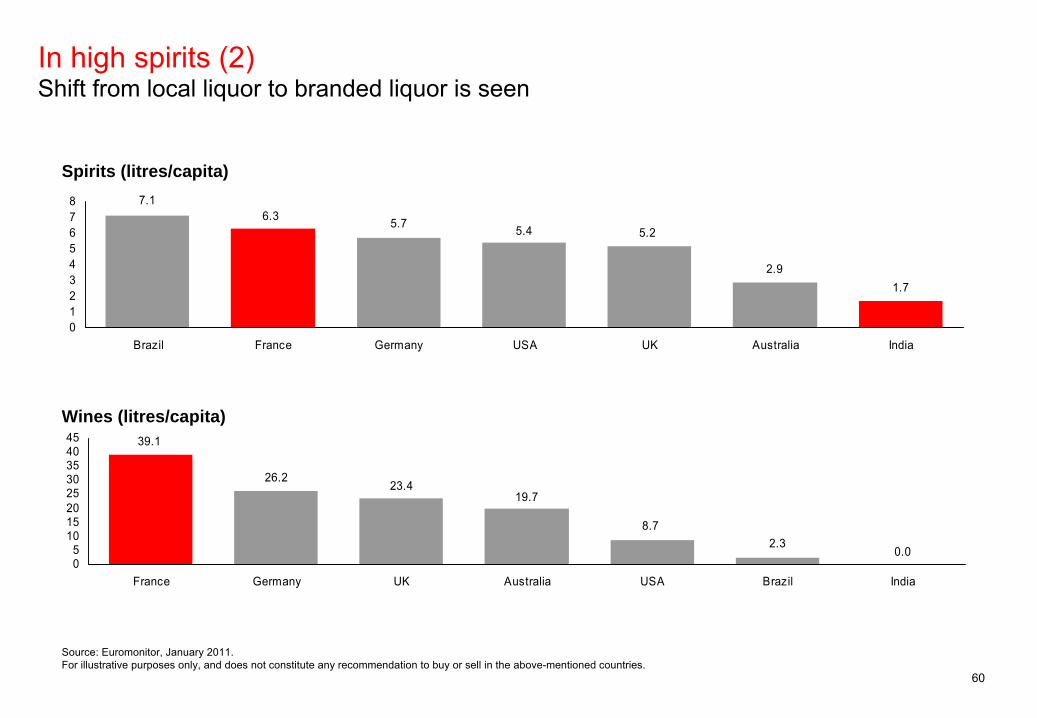

In high spirits (2) Shift from local liquor to branded liquor is seen

Spirits (litres/capita)

39.1

0.02.3

8.7

19.723.4

26.2

05

1015202530354045

France Germany UK Australia USA Brazil India

Wines (litres/capita)

Source: Euromonitor, January 2011.For illustrative purposes only, and does not constitute any recommendation to buy or sell in the above-mentioned countries.

61

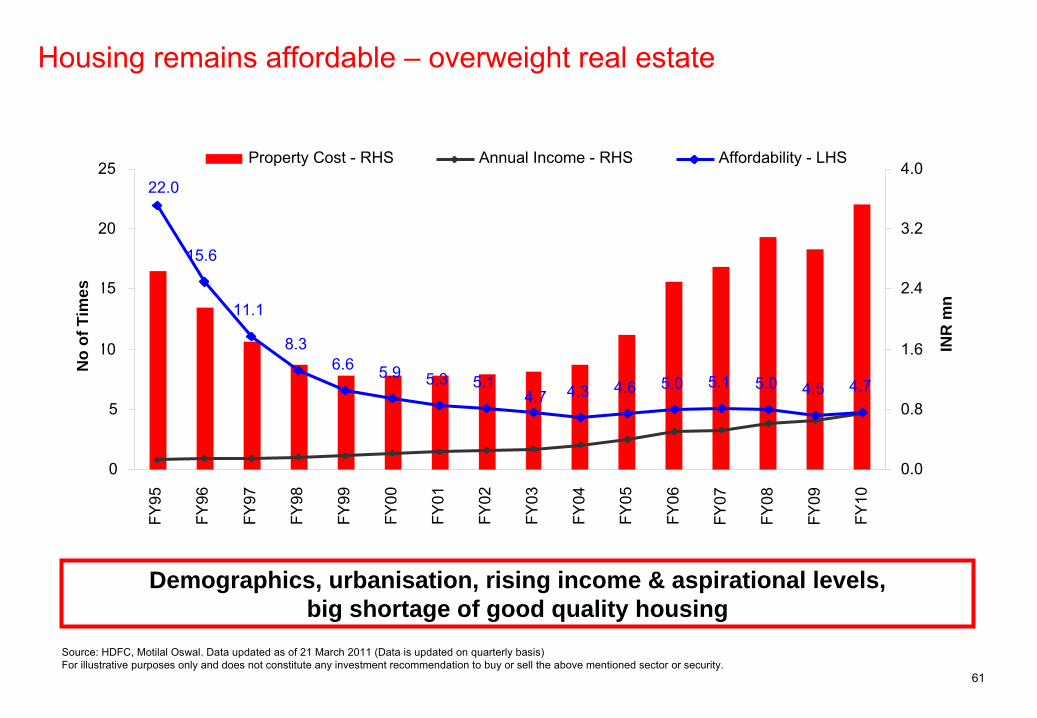

Housing remains affordable –

overweight real estate

Demographics, urbanisation, rising income & aspirational levels, big shortage of good quality housing

Source: HDFC, Motilal Oswal. Data updated as of 21 March 2011 (Data is updated on quarterly basis)For illustrative purposes only and does not constitute any investment recommendation to buy or sell the above mentioned sector or security.

15.6

11.1

8.36.6 5.9 5.3 5.1 4.3 4.6 5.0 5.1 5.0 4.5 4.7

4.7

22.0

0

5

10

15

20

25FY

95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

0.0

0.8

1.6

2.4

3.2

4.0Property Cost -

RHS Annual Income -

RHS Affordability -

LHS

No

of T

imes

INR

mn

62

Investment spend delayed due to government inaction and tight monetary policy

Consumption to remain bouyant; near normal monsoon forecast

Corruption issue has peaked –

UID scheme will reduce subsidy losses

Closely monitor government action on policy and reforms

Monitor trends in crude oil

Monitor relative and absolute market valuations

Conclusion

For illustrative purposes only and does not constitute investment recommendation to buy or sell in the above-mentioned sectors and commodities.

Appendix

64

Sanjiv Duggal – Fund Manager

Sanjiv

joined HSBC in April 1996 and is responsible for the management

of Indian equities. With over 16 years of investment experience, Sanjiv

has been involved in running the flagship HSBC GIF Indian Equity Fund since he joined. Prior to joining HSBC, Sanjiv

worked for the Hill Samuel Group where he spent nearly five years, initially in internal audit and latterly as an Emerging Markets fund manager.

Sanjiv

is a fully qualified Chartered Accountant.

Viresh Mehta – Fund Manager

Viresh

is a fund manager in the Indian equity team and has been working in the industry since 1992. Viresh

was recruited to HSBC Global Asset Management India in 2002 by Sanjiv. He relocated to Singapore in 2006. Prior to joining the firm in 2002, Viresh

was the head of dealing and sales trading with UBS Warburg Securities, India. He has also had prior experience in servicing institutional investors at Prabhudas

Lilladher

Limited and DSP Financial Consultants Limited. He holds a Bachelor’s degree in Engineering and an MMS in Finance, both from University of Bombay.

Nilang Mehta – Fund Manager Nilang

was recruited to HSBC Global Asset Management India in 2004 by Sanjiv. He relocated to Singapore in August 2009. He has been in the financial industry since 1996, starting out as a Senior Auditor. He holds a Masters degree in Commerce from University of Mumbai and is also

a fully qualified Chartered Accountant and a CFA charter holder.

5 team members who worked together at HSBC Global Asset Management (India) Limited. As at 31 March 2011

Investment team continuity over 14+ years 5 key people who first worked together in 2004

65

Divya Balakrishnan – Investment Analyst

Divya

is assisting the fund management team in researching sectors and stocks for their portfolio. She joined HSBC Singapore in July 2005 as a Management Associate, prior to joining Asset Management in Dec 2007. She holds a Bachelor's degree in Electrical Engineering from the National University of Singapore and is currently a Level 3 CFA candidate.

Deborah Yeo – Investment Analyst

Deborah is assisting the fund management team in researching sectors and stocks for their portfolio. She has been with HSBC since October 2008. She started her career with HSBC in London where she was on the global graduate programme supporting the GEM Equity team, Wholesale and

the Institutional Sales team on her rotations. She relocated to Singapore in 2010. She holds a MSc Finance degree from Tanaka Business School, Imperial College London, a Bachelor’s degree in Electrical Engineering from the National University of Singapore and is currently a Level 2 CFA candidate.

Anand Narayan – Dealer

Anand

is the Dealer for the team and is based in Singapore. Anand

was recruited to HSBC Global Asset Management India in August 2004 by Sanjiv. He relocated to Singapore in October 2008. Anand

worked at HSBC Asset Management in India earlier with Sanjiv, Viresh, Nilang

and Nancy. He has worked in this industry since 1991. He holds a Master’s Degree in Financial Management from Narsee

Monjee

Institute of Management Studies (Mumbai), and a Bachelor’s degree in Commerce from the University of Mumbai.

5 team members who worked together at HSBC Global Asset Management (India) Limited. As at 31 March 2011

Investment team continuity over 14+ years 5 key people who first worked together in 2004

66

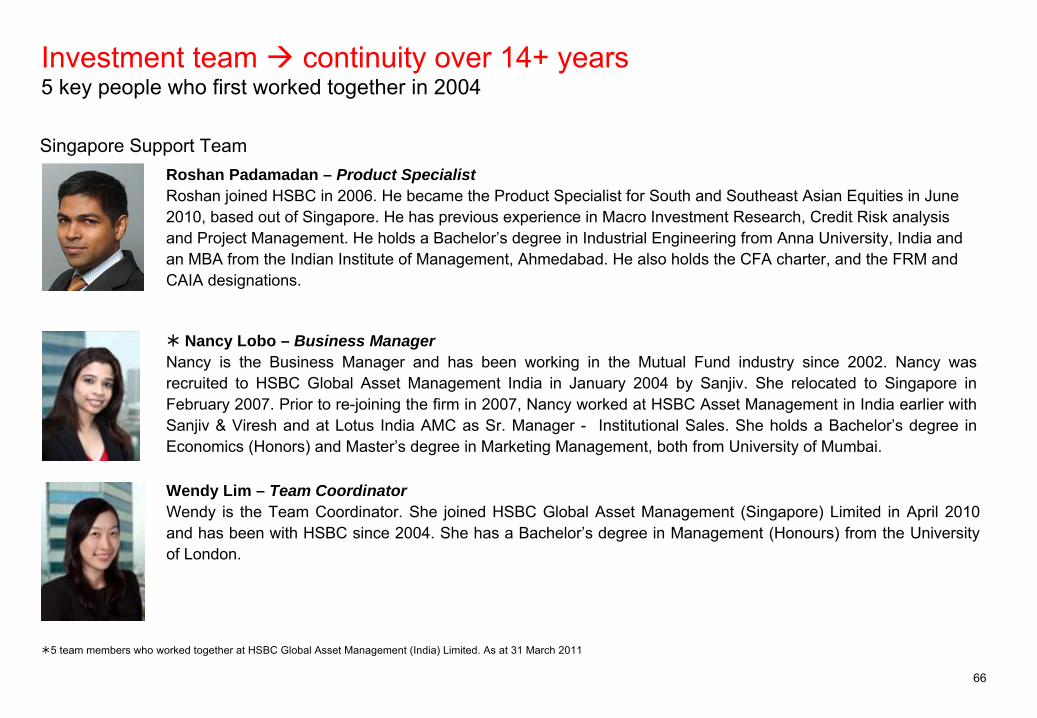

Nancy Lobo – Business ManagerNancy is the Business Manager and has been working in the Mutual

Fund industry since 2002. Nancy was recruited to HSBC Global Asset Management India in January 2004 by Sanjiv. She relocated to Singapore in February 2007.

Prior to re-joining the firm in 2007, Nancy worked at HSBC Asset Management in India earlier with Sanjiv

& Viresh

and at Lotus India AMC as Sr. Manager -

Institutional Sales. She holds a Bachelor’s degree in Economics (Honors) and Master’s degree in Marketing Management, both from University of Mumbai.

Singapore Support Team

Wendy Lim – Team CoordinatorWendy is the Team Coordinator. She joined HSBC Global Asset Management (Singapore) Limited in April 2010 and has been with HSBC since 2004. She has a Bachelor’s degree in Management (Honours) from the University of London.

Roshan Padamadan – Product Specialist Roshan

joined HSBC in 2006. He became the Product Specialist for South

and Southeast Asian Equities in June 2010, based out of Singapore. He has previous experience in Macro Investment Research, Credit Risk analysis and Project Management. He holds a Bachelor’s degree in Industrial Engineering from Anna University, India and an MBA from the Indian Institute of Management, Ahmedabad. He also holds the CFA charter, and the FRM and CAIA designations.

5 team members who worked together at HSBC Global Asset Management (India) Limited. As at 31 March 2011

Investment team continuity over 14+ years 5 key people who first worked together in 2004

67

This presentation is intended for Professional Clients only and should not be distributed to or relied upon by Retail Clients. The contents of this presentation are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. The material contained herein is for information only and does not constitute investment advice or a recommendation to any reader of this material to buy or sell investments. HSBC Global Asset Management (UK) Limited has based this presentation on information obtained from sources it believes to be reliable but which it has not independently verified. HSBC Global Asset Management (UK) Limited and HSBC Group accept no responsibility as to its accuracy or completeness. This presentation is intended for discussion only and shall not be capable of creating any contractual or other legal obligations on the part of HSBC Global Asset Management (UK) Limited or any other HSBC Group company. Care has been taken to

ensure the accuracy of this presentation but HSBC Global Asset Management (UK) Limited accepts no responsibility for any errors or omissions contained therein. This presentation and any issues or disputes arising out of or in connection with it (whether such disputes are contractual or non-contractual in nature, such as claims in tort, for breach of statute or regulation or otherwise) shall be governed by and construed in accordance with English law.The views expressed above were held at the time of preparation and are subject to change without notice.Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Global Asset Management (UK) Limited accepts no liability for any failure to meet such forecast, projection or target.The value of investments and any income from them can go down as

well as up and investors may not get back the amount originally

invested. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up.HSBC GIF Indian Equity Fund is a sub-fund of the HSBC Global Investment Funds, a Luxembourg domiciled

SICAV. UK based investors in HSBC Global Investment Funds are advised that they may not be afforded some of the protections conveyed by the provisions of the Financial Services and Markets Act 2000. HSBC Global Investment Funds is recognised in the United Kingdom by the Financial Services Authority under section 264 of the Act. The shares in HSBC Global Investment Funds have not been and will not be offered for sale or sold in the United States of America, its territories or possessions and all areas subject to its jurisdiction, or to United States Persons. All applications are made on the basis of the current HSBC Global Investment Funds Prospectus, simplified prospectus and most recent annual and semi-annual reports, which can be obtained upon request free of charge from HSBC Global Asset Management (UK) Limited, 8 Canada Square, Canary Wharf, London, E14 5HQ. UK, or the local distributors. Investors and potential investors should read and note the risk warnings in the prospectus and relevant simplified prospectus. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in established

markets. Economies in Emerging Markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the

countries with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries in which they trade.Brokerage commissions, custodial services and other costs relating to investment in Emerging Markets generally are more expensive than those relating to investment in more developed markets. Lack of adequate custodial systems in some markets may prevent investment in a given country or may require a

sub-fund to accept greater custodial risks in order to invest, although the Custodian will endeavour to minimise such risks through the appointment of correspondents that are

international, reputable and creditworthy financial institutions. In addition, such markets have different settlement and clearance procedures. In certain markets there have been times when settlements have been unable to keep pace with the volume of securities transactions, making it difficult to conduct such transactions. The inability of a sub-fund to make intended securities purchases due to settlement problems could cause the sub-fund to miss attractive investment opportunities. Inability to dispose of a portfolio security caused by settlement problems could result either in losses to a sub-fund due to subsequent declines in value of the portfolio security or, if a sub-fund has entered into a contract to sell the security, could result in potential liability to the purchaser.

Important information

68

MSCI Index – The MSCI information may only be used for your internal use, may

not be reproduced or redisseminated

in any form and may not be used to create any financial instruments or products or any indices. The MSCI information is provided on an ‘as is’

basis and the user of this information assumes the entire risk of any use it may make or permit to be made of this information. Neither MSCI, any of its affiliates or any other person involved in or related to compiling, computing or creating the MSCI information (collectively, the ‘MSCI Parties’) makes any express or implied warranties or representations with respect to such information or the results to be obtained by the use thereof, and the MSCI Parties hereby expressly disclaim all warranties (including, without limitation, all warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential or any other damages (including, without limitation, lost profits) even if notified of, or if it might otherwise have anticipated, the possibility of such damagesThe risk also exists that an emergency situation may arise in one or more developing markets as a result of which trading of securities may cease or may be substantially curtailed and prices for a sub-fund’s securities in such markets may not be readily available.Investors should note that changes in the political climate in Emerging Markets may result in significant shifts in the attitude

to the taxation of foreign investors. Such changes may result in changes to legislation, the interpretation

of legislation, or the granting of foreign investors the benefit of tax exemptions or international tax treaties. The effect of such changes can be retrospective and can (if they occur) have an adverse impact on the investment return of shareholders in any sub-fund so affected.This sub-fund invests predominantly in one geographic area; therefore any

decline in the economy of this area may affect the prices and value of the underlying assets. Stockmarket

investments should be viewed as a medium to long term investment and should be held for at least five years. Any performance information shown refers to the past and should not be seen as an indication of future returns.To help improve our service and in the interests of security we may record and/or monitor your communication with us.HSBC Global Asset Management (UK) Limited provides information to Institutions, Professional Advisers and their clients on the investment products and services of the HSBC Group. This presentation is approved for issue in the UK by HSBC Global

Asset Management (UK) Limited, who are authorised and regulated

by the Financial Services Authority. www.assetmanagement.hsbc.com/ukCopyright ©

HSBC Global Asset Management (UK) Limited 2011. All rights reserved. 20869/082011/FP11-1558

Important information (cont’d)