Embed Size (px)

Citation preview

ARKANSAS DIVISION OF LEGISLATIVE AUDIT 172 State Capitol, Little Rock, AR 72201 Phone: 501-683-8600 Fax: 501-683-8605 www.arklegaudit.gov

Report ID: IRPA02811 Report Date: June 30, 2011

INTRODUCTION This report is issued to provide Legislative Joint Auditing Committee (LJAC) a summary of disposition reports provided by elected Prosecuting Attorneys of the State’s twenty-eight judicial districts. A map of judicial districts is provided on page 3. BACKGROUND Arkansas Code Annotated (Code) § 10-4-419, provided in Appendix A, requires the Legislative Auditor to notify applicable prosecuting attorneys of audit reports reflecting apparent unauthorized disbursements or unaccounted for funds or property by a public official or employee. The Legislative Auditor also refers apparent conflicts with various state ethics laws to the appropriate prosecuting attorney. Ark. Code Ann. § 10-4-419 stipulates prosecuting attorneys shall report to LJAC, by June 30 of each year, the status or disposition of any matter referred to them by the Legislative Auditor on behalf of LJAC. Further, Ark. Code Ann. § 21-2-708 directs LJAC to notify the Arkansas Governmental Bonding Board (Board) of audit reports reflecting apparent improper transactions for which a public official, officer, or employee may be liable. After a prosecutor has disposed of a matter referred by LJAC, the Board determines whether a loss is covered by Arkansas Self-Insured Fidelity Bond Program. In response to LJAC’s request to formalize interaction, relating to “white collar crime,” among Legislative Audit, Arkansas State Police, and Prosecuting Attorneys, the parties agreed to a Memorandum of Understanding, approved by LJAC on July 14, 2006, presented in Appendix B. OBJECTIVES Objectives in preparing this special report were to:

Compile responses from each Prosecuting Attorney concerning all matters referred them by the Legislative Auditor on behalf of LJAC;

Provide information of special interest to LJAC; and

Present disposition reports in a concise manner for LJAC.

Prosecuting Attorneys

Disposition of Matters Referred by Legislative Joint Auditing Committee January 1, 2010 through December 31, 2010

Special Report Legislative Joint Auditing Committee

October 14, 2011

2

SCOPE AND METHODOLOGY Disposition information submitted by Prosecuting Attorneys was compiled for the period January 1, 2010 through December 31, 2010. Matters referred to prosecuting attorneys prior to January 1, 2010, but unresolved as of the previous special report date of June 30, 2010 are also included in the report. To facilitate the reporting process, information related to referred matters was provided each Prosecutor. Relevant Code, federal and state circuit court orders, and audit related files were reviewed. In addition, Board approved bond payments from Arkansas Fidelity Bond Trust Fund are disclosed in this report. The methodology used in conducting this review was developed uniquely to address the stated objectives; therefore, this review was more limited in scope than an audit or attestation engagement performed in accordance with Government Auditing Standards issued by the Comptroller General of the United States. MATTERS REFERRED TO PROSECUTING ATTORNEYS Each audit report referred to the applicable Prosecutor is listed by judicial district on pages 8 through 68. Individual matters are briefly summarized with Bond Trust Fund payments included, if applicable, followed by the status or disposition provided by the appropriate Prosecuting Attorney. A summary of disposition of matters referred to Prosecuting Attorneys is presented in Exhibit I on pages 4 and 5. Also provided in Exhibit I are the dollar amounts, if applicable, disclosed in audit findings of matters referred. Of the 223 matters in which disposition reports were requested, the LJAC referred 153 matters to the State’s Prosecuting Attorneys during the period January 1, 2010 through December 31, 2010. The remaining 70 matters were referred, but not resolved, prior to 2010.

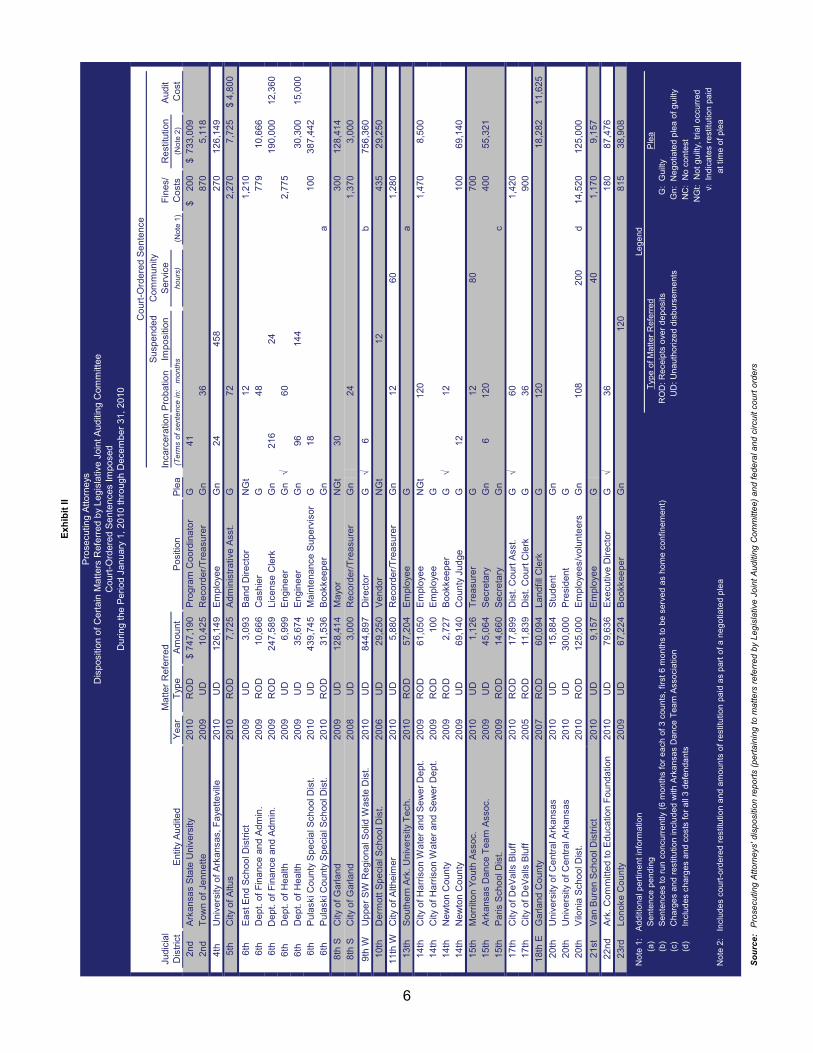

ITEMS OF SPECIAL INTEREST TO LJAC Prosecution Declined Of special interest to LJAC are instances in which the individual responsible for the improper transaction(s) reimbursed the public entity, but no charges were filed. The Second Judicial District Prosecuting Attorney did not pursue criminal charges in one matter for which repayment of $4,902 was made, by City of Keiser Recorder/Treasurer, for unauthorized compensation. Court-Ordered Sentences Imposed Court-ordered sentences imposed for cases in which a conviction was obtained is also of particular interest to LJAC. Criminal charges were filed in 40 of 223 matters referred to a Prosecutor. Five cases are pending in court, two cases were dismissed, and the remaining 33 cases, in which a conviction was obtained and sentence imposed, are listed, by judicial district, in Exhibit II on page 6. Information provided includes: Entity audited.

Type of matter referred.

Amount of improper transaction(s).

Position of employee or elected official against whom charges were filed.

Plea of defendant.

Court-ordered sentence. The terms of a defendant’s court-ordered sentence, also presented in Exhibit II on page 6, include: Time, in months, of incarceration, probation,

and suspended imposition of a sentence.

Hours of community service.

Fines, court costs, restitution, and audit costs. Defendants entered pleas of no contest or guilty in all but 4 of the 33 cases in which a conviction was obtained.

3

Source: Arkansas Judicial Directory

Arkansas Judicial Districts Counties Comprising Each District

Of the 33 cases in which a conviction was obtained, 27 were disposed of in state circuit courts and 6 were resolved in federal court.

Information relating to the matters referred to, and disposition of those matters by, the State’s

Prosecuting Attorneys are referenced below by judicial districts and the starting page numbers.

A map of counties comprising each judicial district is also presented.

Judicial District Page Judicial District Page

First 8 Twelfth 42Second 13 Thirteenth 43Third 20 Fourteenth 46Fourth 22 Fifteenth 50Fifth 23 Sixteenth 52Sixth 24 Seventeenth 53Seventh 31 Eighteenth East 55Eighth North 32 Eighteenth West 56Eighth South 34 Nineteenth East 57Ninth East 36 Nineteenth West 58Ninth West 37 Twentieth 59Tenth 38 Twenty-first 65Eleventh East 39 Twenty-second 66Eleventh West 40 Twenty-third 67

4

Number ofMatters Charges Acquitted/ Insufficient Under

Judicial Referred Filed Conviction Pending Dismissed Prosecution Evidence Ethics ReviewDistrict (Note 1) (a+b+c) a b c Declined (Note 2) Violation (Note 3)

1st 23 2 2 8 4 9$9,249 $103,592 $48,433 $367,664

2nd 38 43 2 1 1 14 6 14

$743,434 $24,112 $4,902 130,587 32,840 138,607

3rd 11 0 3 7 1244,199 40,591 5,607

4th 1 1 1126,149

5th 1 1 17,725

6th 37 7 7 12 2 16775,302 441,997 1,999 219,476

7th 3 1 1 2

202,113 1,118

8th N 3 0 2 111,345 2,270

8th S 6 2 2 3 1131,414 37,549

9th E 3 0 1 21,170 18,756

9th W 2 1 1 1 844,897 812

10th 5 1 1 2 229,250 338 596

11th E 1 1 10,151

11th W 3 1 1 25,880 25,055

12th 2 1 11,000 4,000

13th 14 1 1 8 557,204 187,119 25,210

14th 12 4 4 3 3 281,707 94,840 15,684 5,026

15th 7 3 3 4 60,850 3,535

16th 4 1 1 230,225 43,134

Exhibit I

Prosecuting AttorneysSummary of Disposition Reports of Matters Referred by Legislative Joint Auditing Committee

For the Period January 1, 2010 through December 31,2010

Case Results Charges Not Filed

5

Number ofMatters Charges Acquitted/ Insufficient Under

Judicial Referred Filed Conviction Pending Dismissed Prosecution Evidence Ethics ReviewDistrict (Note 1) (a+b+c) a b c Declined (Note 2) Violation (Note 3)

17th 9 3 2 1 1 3 2$11,839 $869 $1,122 $19,395 $998

18th E 3 1 1 1 160,094 1,100 15,248

18th W 1 1 9,560

19th E 0

19th W 1 13,090

20th 17 5 3 2 6 6540,884 14,267 131,611 176,887

21st 4 1 1 39,157 40,250

22nd 7 1 1 679,636 18,787

23rd 5 1 1 2 267,224 2,588 1,428

Matters Charges Acquitted/ Insufficient Under

Referred Filed Conviction Pending Dismissed Prosecution Evidence Ethics Review(Note 1) (a+b+c) a b c Declined (Note 2) Violation (Note 3)

Totals 223 40 33 5 2 1 82 42 58

$3,575,442 $241,361 $9,249 $4,902 $1,446,730 $251,602 $1,018,257

Note 1: Includes matters referred in previous years

Note 2: Prosecutor indicated evidence was not sufficient to sustain a criminal case

Note 3: Matter is under review by a law enforcement agency

Note 4: Dollar amounts reflect, in most instances referred amount, if applicable

Totals (Note 4)

Source: Prosecuting Attorneys' disposition reports

Exhibit I

Prosecuting AttorneysSummary of Disposition Reports of Matters Referred by Legislative Joint Auditing Committee

For the Period January 1, 2010 through December 31,2010

Case Results Charges Not Filed

6

Judi

cia

lIn

carc

erat

ion

Pro

batio

nS

usp

end

ed

Imp

ositi

onC

omm

unity

S

ervi

ceF

ines

/R

est

itutio

nA

udit

Dis

tric

tE

ntity

Au

dite

dY

ear

Typ

eA

mou

ntP

ositi

onP

lea

hour

s)(N

ote

1)C

osts

(Not

e 2)

Co

st2n

dA

rkan

sas

Sta

te U

nive

rsity

2010

RO

D74

7,19

0$

P

rogr

am C

oord

ina

tor

G41

200

$

733

,009

$

2nd

Tow

n o

f Je

nnet

te20

09U

D1

0,42

5

Re

cord

er/T

rea

sure

rG

n3

687

0

5

,118

4th

Uni

vers

ity o

f A

rkan

sas,

Fay

ette

ville

2010

UD

126,

149

Em

ploy

eeG

n24

458

270

126

,149

5th

City

of

Altu

s20

10R

OD

7,72

5

Adm

inis

trat

ive

Ass

t.G

72

2,2

70

7,7

25

4,80

0$

6th

Eas

t End

Sch

ool D

istr

ict

2009

UD

3,09

3

Ban

d D

irect

orN

Gt

12

1,2

10

6th

Dep

t. o

f F

ina

nce

and

Ad

min

.20

09R

OD

10,

666

C

ash

ier

G4

877

9

10

,666

6t

h D

ept.

of

Fin

anc

e an

d A

dmin

. 20

09R

OD

247,

589

Lic

ense

Cle

rkG

n21

624

190

,000

12,3

60

6th

Dep

t. o

f H

ealth

2009

UD

6,99

9

Eng

inee

rG

n√

60

2,7

75

6th

Dep

t. o

f H

ealth

2009

UD

35,

674

E

ngin

eer

Gn

9614

430

,300

15,0

00

6th

Pul

aski

Cou

nty

Spe

cia

l Sch

ool D

ist.

2010

UD

439,

745

Mai

nte

nanc

e S

upe

rvis

orG

1810

0

38

7,4

42

6t

hP

ulas

ki C

ount

y S

peci

al S

choo

l Dis

t.20

10R

OD

31,

536

B

ookk

eepe

rG

na

8th

SC

ity o

f G

arla

nd

2009

UD

128,

414

May

or

NG

t30

300

128

,414

8th

SC

ity o

f G

arla

nd

2008

UD

3,00

0

Re

cord

er/T

rea

sure

rG

n2

41

,370

3

,000

9th

WU

ppe

r S

W R

egi

ona

l Sol

id W

aste

Dis

t.20

10U

D84

4,89

7

D

irec

tor

G√

6b

756

,360

10th

Der

mot

t Spe

cial

Sch

ool D

ist.

2006

UD

29,

250

V

endo

rN

Gt

1243

5

29

,250

11th

WC

ity o

f A

lthei

mer

2010

UD

5,88

0

Re

cord

er/T

rea

sure

rG

n1

26

01

,280

13th

Sou

ther

n A

rk.

Uni

vers

ity T

ech.

2010

RO

D5

7,20

4

Em

ploy

eeG

a

14th

City

of

Ha

rris

on W

ate

r an

d S

ew

er

De

pt.

2009

RO

D6

1,05

0

Em

ploy

eeN

Gt

120

1,4

70

8,5

00

14th

City

of

Ha

rris

on W

ate

r an

d S

ew

er

De

pt.

2009

RO

D10

0

E

mpl

oyee

G14

thN

ewto

n C

oun

ty20

09R

OD

2,72

7

Boo

kkee

per

G√

12

14th

New

ton

Cou

nty

2009

UD

69,

140

C

oun

ty J

udge

G12

100

69,1

40

15th

Mo

rrilt

on

Yo

uth

Ass

oc.

2010

UD

1,12

6

Tre

asu

rer

G1

28

070

0

15

thA

rkan

sas

Dan

ce T

eam

Ass

oc.

2009

UD

45,

064

S

ecre

tary

Gn

61

2040

0

55

,321

15th

Par

is S

choo

l Dis

t.20

09R

OD

14,

660

S

ecre

tary

Gn

c

17th

City

of

De

Va

lls B

luff

2010

RO

D1

7,89

9

Dis

t. C

ourt

Ass

t.G

√6

01

,420

17

thC

ity o

f D

eV

alls

Blu

ff20

05R

OD

11,

839

D

ist.

Cou

rt C

lerk

G3

690

0

18t

h E

Ga

rland

Cou

nty

2007

RO

D6

0,09

4

Lan

dfill

Cle

rkG

120

18,2

82

11

,625

20t h

Uni

vers

ity o

f C

ent

ral A

rka

nsas

2010

UD

15,

884

S

tud

ent

Gn

20

thU

nive

rsity

of

Ce

ntra

l Ark

ans

as20

10U

D30

0,00

0

P

resi

den

tG

20th

Vilo

nia

Sch

ool D

ist.

2010

RO

D12

5,00

0

E

mpl

oyee

s/vo

lunt

eer

sG

n1

082

00d

14,5

20

125

,000

21s

tV

an B

uren

Sch

ool D

istr

ict

2010

UD

9,15

7

Em

ploy

eeG

40

1,1

70

9,1

57

22nd

Ark

. Com

mitt

ed to

Edu

catio

n F

oun

datio

n20

10U

D7

9,63

6

Exe

cutiv

e D

irec

tor

G√

36

180

87,4

76

23r

dLo

nok

e C

oun

ty20

09U

D6

7,22

4

Boo

kkee

per

Gn

120

81

5

38

,908

No

te 1

: A

dd

itio

na

l per

tine

nt i

nfo

rma

tion

(a)

S

en

ten

ce p

en

din

g(b

)

Se

nte

nce

s to

ru

n c

on

curr

en

tly (

6 m

onth

s fo

r e

ach

of 3

cou

nts,

fir

st 6

mo

nth

s to

be

se

rve

d a

s h

om

e c

on

fine

me

nt)

RO

D:

Rec

eip

ts o

ver

de

po

sits

G

: G

uilt

y(c

)

Ch

arg

es

an

d r

estit

utio

n in

clu

de

d w

ith A

rka

nsa

s D

an

ce T

eam

Ass

oci

atio

n

UD

: U

na

uth

ori

zed

dis

bu

rse

me

nts

Gn

: N

eg

otia

ted

ple

a o

f g

uilt

y(d

)In

clu

des

ch

arg

es

an

d c

ost

s fo

r a

ll 3

de

fen

da

nts

NC

: N

o co

nte

stN

Gt:

Not

gui

lty,

tria

l occ

urr

ed

√: I

ndic

ate

s re

stitu

tion

pa

id

No

te 2

: In

clu

de

s co

urt

-ord

ere

d r

estit

utio

n a

nd

am

ou

nts

of r

est

itutio

n p

aid

as

par

t o

f a n

eg

otia

ted

ple

a

a

t tim

e o

f ple

a

So

urc

e:

Pro

secu

ting

Att

orn

eys

' dis

po

sitio

n r

ep

ort

s (p

ert

ain

ing

to

ma

tters

re

ferr

ed

by

Le

gis

lativ

e J

oin

t A

ud

itin

g C

om

mitt

ee

) a

nd

fed

era

l an

d c

ircu

it co

urt

ord

ers

Ma

tter

Ref

erre

d(T

erm

s of

sen

tenc

e in

:

mon

ths

Lege

ndT

ype

of M

atte

r R

efe

rre

dP

lea

Cou

rt-O

rder

ed S

ente

nce

Exh

ibit

II

Pro

secu

ting

Atto

rney

sD

isp

ositi

on o

f C

ert

ain

Mat

ters

Ref

err

ed b

y L

egis

lativ

e Jo

int A

uditi

ng

Com

mitt

ee

Cou

rt-O

rder

ed

Sen

tenc

es Im

pose

dD

urin

g th

e P

erio

d Ja

nuar

y 1,

201

0 th

roug

h D

ece

mbe

r 31

, 20

10

7

THIS PAGE INTENTIONALLY LEFT BLANK

8

Judicial District Population: 93,718 Fletcher Long, Jr. Circuit Judges: 5 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Lee County

City of Marianna (Audit Period: 1/1/09 - 12/31/09):

2010 $1,692 salary advances to Clerk/Treasurer.

Status per Prosecuting Attorney: Noted the salary advances to the City Clerk/Treasurer and the reimbursement for the same. No action is required.

City of Marianna (Audit Period: 1/1/08 - 12/31/08):

2010 $8,000 undocumented disbursements to paving contractor.

Status per Prosecuting Attorney: Prosecuting Attorney contacted the Mayor’s Office to inquire about the $8,000 payment made to a contractor beyond the contract terms without supporting documentation. The City provided him a letter dated October 5, 2010, from the contractor and a receipt to the contractor from the City reflecting repayment to the City of the aforesaid $8,000.

Phillips County

Barton-Lexa School District (Audit Period: 7/1/08 - 6/30/09):

2010 $5,183 improper disbursements to, or on behalf of, Superintendent for unused sick leave in apparent conflict with District policy ($5,100) and items purchased which did not have a District purpose ($83). Of this amount, $63 has been reimbursed.

Status per Prosecuting Attorney: The dispute regarding the $5,100 for unused sick leave which Mr. Vent caused to be paid himself seems to revolve around whether Vent was authorized to receive this $5,100 because he had given due notice of his retirement, or whether he was entitled to receive the money only upon separation from service as well as retirement. The resolution of this dispute falls back on the district policy which states “retiring teachers will be paid for unused sick leave.” Obviously, Mr. Vent was retiring. The practice of the district, however, was to pay employees for unused sick leave only upon actual separation from service to the district. Mr. Vent has not been formally separated from service. This is a conflict that will have to be resolved by a court, and I cannot say that the payment to Mr. Vent involves a violation of the criminal law. Case is closed until additional facts are provided.

First Judicial District Cross, Lee, Monroe, Phillips, St. Francis, and Woodruff Counties

9

1st Judicial District (continued)

Phillips County

Barton-Lexa School District (Audit Period: 7/1/08 - 6/30/09) (continued):

2010 $1,400 unauthorized compensation to District Treasurer ($700) and Superintendent’s Secretary ($700).

Status per Prosecuting Attorney: From the language of Legislative Audit’s letter to the Prosecuting Attorney, there is no question that the District Treasurer and the Superintendent’s secretary performed the service in question. The shortcoming is that the additional service was not approved by the board, and the board did not request a deviation from the ethics law. I do not think this will occur again, and do not intend to take any further action on it. Case is closed.

$3,044 conflict of interest disbursements to a Board member’s spouse.

Status per Prosecuting Attorney: I think that this matter has rectified itself and I do not believe that it will be reoccurring. Apparently the services were genuinely rendered and were necessary. Case is closed.

City of Helena-West Helena (Audit Period: 1/1/08 - 12/31/09):

2010 $20,424 improper disbursements to Mayor ($1,955), Treasurer ($2,413), former Alderman ($79), employees ($13,401), and vendors and other organizations ($2,576).

$3,666 Mayor’s checks for reimbursement of improper disbursements were returned by bank for insufficient funds and remain uncollected.

$68,797 paid to various hotels, restaurants, businesses, organizations, and individuals without adequate documentation or documented business purpose.

$543 improper disbursements for parties.

$180,215 disbursements paid by debit card rather than prenumbered checks, in conflict with state law, and majority of debit card activity was not recorded in City’s ledger.

$10,491 improper disbursements for videotaping City Council meetings and copying videos after the City Council voted to discontinue paying video-related expenditures.

$2,000 improper disbursements for donations to two organizations.

$23,005 undeposited bond and fine receipts. Sarah Angel, Bond and Fine Clerk, admitted misappropriating funds for personal use.

$58,523 conflict of interest disbursements to employees ($5,620), employee-owned businesses ($26,970), business owned by City Inspector ($18,933), and City Clerk’s son ($7,000).

Status per Prosecuting Attorney: The matter of the 1/1/08 – 12/31/09 audit is under active investigation by the Arkansas State Police. The matter was given to an investigator after a conference between Prosecutor, Legislative Audit personnel, and Arkansas State Police Special Agent. As soon as the results of the investigation are submitted, Prosecutor will report that fact to Legislative Audit as well as any intentions in regard to the matter.

Matters Reported by Legislative Joint Auditing Committee

10

1st Judicial District (continued)

Phillips County (continued)

City of Helena-West Helena (Audit Period: 1/1/07 - 6/30/09):

2009 City was not in compliance with Ark. Code Ann. §§ 14-59-101 to -118 regarding proper accounting procedures for municipalities as noted below:

Cash receipt and disbursement journals were not properly maintained.

Monthly bank statements were not presented to City Council. Six-month financial statements were not prepared nor published. Accounting records were not auditable at engagement start date.

Status per Prosecuting Attorney: The Treasurer lost his bid for re-election and since his most serious sanction is for his failure to keep the records charges in this case was removal from office, it was deemed to moot and the case dismissed.

Helena-West Helena School District (Audit Period: 7/1/08 - 6/30/09):

2010 $34,781 improper disbursements to Superintendent ($735), Interim Business Manager ($236), five Board members ($1,058), and 100 employees ($32,752). Disbursements consisted of items not documented for a public purpose, travel advances not subsequently documented, alcoholic beverages, and expenses incurred for personal excursions of Board members while attending a National School Boards Association conference.

$52,536 undocumented disbursements to restaurants and other businesses while personnel were in business travel status. Note: Arkansas Department of Education took control of the District on June 20, 2011. Status per Prosecuting Attorney: It seems Superintendent Willie C. Williams’ plan of corrective action appropriately addresses the negative findings by Legislative Audit. It is my opinion that no further action is required by my office. Case is closed.

Helena-West Helena School District (Audit Period: 7/1/05 - 6/30/06):

2007 $1,458 unauthorized salary disbursements to former Superintendent Shirley T. J. Graham.

Status per Prosecuting Attorney: The case against Shirley Graham has been dismissed as they were unable to locate a witness in the State of New York who could testify as to her non-attendance at the conference for which she claimed expenses. Furthermore, one of these school district cases was tried to a jury and the jury returned a unanimous verdict of acquittal after about 45 minutes deliberation. I did not anticipate and do not anticipate that there would be any different result as to the other school district officials, and therefore, did not see the sense in wasting the time and money of Circuit Court personnel to futilely try a defendant who will be acquitted.

Matters Reported by Legislative Joint Auditing Committee

11

1st Judicial District (continued)

Phillips County (continued)

Helena-West Helena School District (Audit Period: 7/1/04 - 8/31/05):

2005 $7,791 unauthorized salary disbursements to Shirley T. J. Graham, former Superintendent.

Status per Prosecuting Attorney: Same response as page 10.

St. Francis County

Palestine-Wheatley School District (Audit Period: 7/1/08 - 6/30/09):

2010 $43,964 conflict of interest disbursements to Superintendent’s spouse ($42,844) and District Treasurer’s spouse ($1,120) without Board resolution or Department of Education approval.

Status per Prosecuting Attorney: The Prosecuting Attorney has spoken to the present Superintendent of the Palestine-Wheatley School District and has been told that the Palestine-Wheatley School Board of Directors had approved the contract for the speech therapy services rendered by the Superintendent’s spouse. Prosecuting Attorney has advised the Superintendent that it will be necessary for the School Board of Directors to pass a specific resolution approving retroactively the services and specifying the reason why it was necessary to purchase those services from the Superintendent’s spouse.

Prosecuting Attorney also spoke to the Superintendent about payment of services for $1,120 to the District Treasurer’s spouse. The District had a structure that was destroyed by fire and it was necessary to remove the slab from the school premises. The school district contracted with the Treasurer’s spouse for these services because it was important to get the job done immediately. Prosecuting Attorney was told that no one else was available to perform the services for a price equal to or less than that paid to the District Treasurer’s spouse. The Board of Directors is also to pass a resolution retroactively approving this expenditure and recognizing the facts as set out in this paragraph.

Assuming that the Board of Directors takes the action specified in this letter, and assuming that they properly notify the State Board of Education as to their actions in regard to the speech therapy services, then Prosecutor sees no further need for any action in regard to these matters. Case is closed.

Matters Reported by Legislative Joint Auditing Committee

12

1st Judicial District (continued)

Woodruff County

Town of Widener (Audit Period: 1/1/05 - 12/31/07):

2008 $5,404 alleged fuel theft that was not reported to an applicable law enforcement agency.

$625 unauthorized disbursements to Mayor. Fully reimbursed.

$800 improper compensation to employee for work performed on private property using Town equipment during normal working hours. Status per Prosecuting Attorney: There will be no further developments in relation to the theft charge until and unless a suspected culprit is developed and Prosecutor doubts this will happen at this late date. The matters relating to the Mayor and the Mayor’s employee are ethics matters and there will no action taken in regard to that.

Note: No matters were reported in Cross and Monroe Counties.

Matters Reported by Legislative Joint Auditing Committee

13

Scott Ellington (Current) Judicial District Population: 276,581 Michael Walden (2010) Circuit Judges: 11 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Clay County

Town of Datto (Audit Period: 1/1/08 - 12/31/09):

2010 $576 conflict of interest disbursements to Mayor without an authorizing ordinance.

Status per Prosecuting Attorney: Ethics matter currently under review.

City of St. Francis (Audit Period: 1/1/08 - 12/31/09):

2010 $911 conflict of interest disbursements to Mayor ($610), Mayor’s spouse ($206), and Recorder/Treasurer ($95) without an authorizing ordinance.

Status per Prosecuting Attorney: Authorizing ordinance received from City of St. Francis approving payment. This matter is concluded and satisfactorily resolved.

Craighead County

Arkansas State University - Childhood Development Associate Program (CDA) (Audit Period: 8/7/02 - 8/7/09):

2010 $747,190 misappropriated fees. CDA Program Coordinator Virginia

DeMaine identified as responsible individual. Bond Trust Fund reimbursed losses totaling $249,000.

Status per Prosecuting Attorney: DeMaine pled guilty to mail fraud and money laundering in federal court and was sentenced to 41 months imprisonment on each count, to run concurrently. Upon release from prison, DeMaine will be on supervised release for three years. Restitution of $733,009 was also ordered.

Arkansas State University System (Audit Period: 7/1/09 - 6/30/10):

2010 $84,034 unauthorized payments for unused sick leave to non-classified employees upon their retirement from the University.

Status per Prosecuting Attorney: Arkansas State Legislature has taken corrective measure by passing Senate Bill 354 which amends Ark. Code Ann. § 21-4-505, which addresses this issue. Case is closed.

Second Judicial District Clay, Craighead, Crittenden, Greene, Mississippi, and Poinsett Counties

14

2nd Judicial District (continued)

Matters Reported by Legislative Joint Auditing Committee

Craighead County (continued)

City of Caraway (Audit Period: 1/1/08 - 12/31/09):

2010 $2,350 improper disbursements for donations to private entities.

Status per Prosecuting Attorney: Correspondence received from Mayor advising that the city sponsored activities for educational purposes. The use of the word “donation” was not appropriate and the city believes that contributing to the education of its people benefits the city and its population. No further action to be taken.

Craighead County (Audit Period: 1/1/08 - 12/31/08):

2010 $5,578 jail commissary fund receipts not deposited. Of this amount, $1,500 was reimbursed. Sheriff’s Office Manager, who resigned from employment, was custodian of these funds.

Status per Prosecuting Attorney: Prosecutor declined to file a criminal charge in the matter. Due to the failure to segregate duties and the lack of internal controls in this matter, Prosecuting Attorney does not feel pursuing this matter in criminal court could be justified. Many persons may well have access to these funds, with many of those being jail inmates. Success at jury trial with the State’s burden of proof would be extremely difficult at best.

Crittenden County

Town of Anthonyville (Audit Period: 1/1/07 - 12/31/08): 2010 $1,343 undocumented reimbursements to Mayor ($986) and

Recorder/Treasurer ($357).

$8,539 undocumented credit card payments.

$992 improper disbursements for purchases not for Town purposes.

$341 improper disbursements for flowers and partial payment of funeral expenses.

Status per Prosecuting Attorney: City ordinance approving payments of $8,539 to the Mayor and Recorder/Treasurer. There was also language stating the city would repay the street account for expenditures not street related, but $1,684 was not addressed. Because the city has been put on notice regarding disbursements for flowers and undocumented reimbursements and because of the age of this infraction, this matter will be closed with no further action taken.

15

2nd Judicial District (continued)

Matters Reported by Legislative Joint Auditing Committee

Crittenden County (continued)

City of Gilmore (Audit Period: 1/1/05 - 1/7/09):

2009 $797 improper expenditure for a holiday meal for City officials/employees and their family members.

$1,440 unauthorized compensation to Payroll Clerk Cathy Moore.

$17,548 disbursement for purchase of a building the Mayor acquired for nonbusiness purpose. Subsequently, the Mayor reimbursed $13,994, leaving a balance of $3,554 due the City.

$1,300 conflict of interest disbursements to an alderman for labor costs without an authorizing ordinance.

The Council established, by ordinance, a police court in 1993. Section 19 of Amendment No. 80 to the Arkansas Constitution removed the constitutional basis for police court jurisdiction effective January 1, 2005. However, the Court continued to function until October 2006. Police citations are adjudicated in the Marion District Court. The Judge was compensated $15,600 during the period January 1, 2005 through March 1, 2008, of which $6,800 was paid after the Court ceased to operate in October 2006.

Status per Prosecuting Attorney: Letter was sent to Mayor instructing him to take immediate action to correct the problem and provide proof of such correction. The Mayor has made no response. As of August 2011, no additional correspondence received from the City of Gilmore. The matter justifies further investigation by local law enforcement. The matter is considered pending at this time, subject to said investigation.

Town of Jennette (Audit Period: 1/1/07 - 12/31/08):

2009 $2,865 conflict of interest disbursements to Council member’s son for mowing ($1,980) and Mayor for contract labor ($885) without an authorizing ordinance.

$40,126 undocumented disbursements for 2008 ($29,275) and 2007 ($10,851).

$2,010 undocumented reimbursements to Recorder/Treasurer ($1,120) and Mayor ($890).

$9,360 inadequately documented vehicle mileage reimbursement to Mayor in 2007. Travel reimbursement forms included mileage for 22 weekend days.

$3,158 inadequately documented vehicle mileage reimbursement to the Recorder/Treasurer in 2007. Travel reimbursement forms included mileage for four trips to the same location on the same weekend day.

$20,009 undocumented vehicle mileage expense reimbursements to the Mayor ($13,862) and Recorder/Treasurer ($6,147) in 2008.

Status per Prosecuting Attorney: These matters are the subject of an ongoing Arkansas State Police investigation. Recorder/Treasurer resigned from office and did not run for re-election. Theft of property charges were filed against Recorder/Treasurer, who pled guilty. Restitution of $5,118 was ordered, in monthly installments of $167 and probation of 36 monthly. The Mayor did not run for re-election.

16

2nd Judicial District (continued)

Matters Reported by Legislative Joint Auditing Committee

Crittenden County (continued)

Town of Jennette (Audit Period: 1/1/07 - 12/31/08) (continued):

Status per Prosecuting Attorney (continued): Mayor was charged and a criminal case is pending in Crittenden County Circuit Court.

Town of Jennette (Audit Period: 1/1/06 - 12/31/06):

2008 $1,472 undocumented and conflict of interest disbursements to Mayor

($1,320), Recorder/Treasurer ($50), and a Council member ($102).

$22,615 undocumented disbursements to a home project contractor ($17,956) and various other individuals/vendors ($4,659).

Status per Prosecuting Attorney: See response on page 15.

Town of Jericho (Audit Period: 1/1/09 - 12/31/09):

2010 $18,389 inadequately documented disbursements to, or endorsed by, Mayor ($15,142) and to Police Chief ($3,247).

Status per Prosecuting Attorney: The Town of Jericho is the subject of an ongoing Arkansas State Police investigation. No charging decision has been made as yet.

Town of Jericho (Audit Period: 1/1/07 - 12/31/08):

2009 $16,545 inadequately documented disbursements of which $3,923 was

paid to the Mayor and $950 to the Police Chief.

Status per Prosecuting Attorney: The Town of Jericho is the subject of an ongoing Arkansas State Police investigation. No charging decision has been made as yet.

Town of Jericho (Audit Period: 1/1/06 - 9/5/07):

2008 $12,692 unauthorized compensation payments to elected officials

($9,300) and undocumented disbursements ($3,392) to elected officials and other vendors/individuals. Payments made to Mayor ($5,250), Recorder/Treasurer ($2,200), Council members ($3,975), Fire Chief ($225), other vendor/individuals ($642), and cash ($400).

Status per Prosecuting Attorney: The Town of Jericho was investigated and after review of the criminal investigation, a determination was made by previous prosecuting attorney not to prosecute the Mayor.

17

2nd Judicial District (continued)

Matters Reported by Legislative Joint Auditing Committee

Crittenden County (continued)

Town of Sunset (Audit Period: 1/1/07 - 12/31/08):

2009 Violations of certain fiscal responsibility and management laws as defined and applied to municipalities by Ark. Code Ann. § 14-77-102(2)(B).

Status per Prosecuting Attorney: The City of Sunset passed an ordinance allowing the employment of family members, and the mayor reimbursed the city for health premiums not withheld from his pay. By receiving letter from Legislative Audit, the City was put on notice that donations to individuals and churches are not appropriate.

City of Turrell (Audit Period: 1/1/07 - 12/31/08):

2009 $2,235 unauthorized compensation to Court Clerk ($960) and

Bookkeeper ($1,275) without an authorizing ordinance.

$1,775 unauthorized bonuses to Mayor ($500), Bookkeeper ($375), and eight other employees ($900) without Council approval. The Council voted not to retroactively approve the bonuses. Subsequently, the Council adopted motion for employees to repay bonuses to City, but no payments have been received.

$3,627 improper credit card charges for fuel placed in personal vehicles of Mayor ($1,745), Bookkeeper ($1,313), and Court Clerk ($569).

Status per Prosecuting Attorney: The City of Turrell is the subject of an ongoing Arkansas State Police investigation. The investigation resulted in the Prosecuting Attorney’s Office pursuing legal action to have the Mayor removed from office for nonfeasance. However, the mayor resigned from office. Because of the acrimonious relationship between the former mayor and the former city council, the previous prosecuting attorney, with assistance from deputy prosecutor, determined that no criminal charges should be filed in this case.

18

2nd Judicial District (continued)

Matters Reported by Legislative Joint Auditing Committee

Greene County

Greene County Technical School District (Audit Period: 7/1/08 - 6/30/09):

2010 $4,534 child care program fees not deposited. A District management investigation was inconclusive as to custodian. Subsequently, $3,724 was recovered from parents who replaced checks that were not deposited.

Status per Prosecuting Attorney: Prior Prosecuting Attorney determined that the funds were lost, or that no determination could be made regarding the loss of the remaining uncollected funds, therefore no further action would be taken unless a suspect surfaces.

City of Oak Grove Heights (Audit Period: 1/1/07 - 12/31/08):

2010 $1,880 conflict of interest disbursements to Marshal without an authorizing ordinance.

Status per Prosecuting Attorney: The City of Oak Grove Heights passed an ordinance authorizing the payment. No further action will be taken.

Mississippi County

Armorel School District (Audit Period: 7/1/08 - 6/30/09):

2010 $2,547 improper disbursements to three classified employees, each with a 260 day contract, for overtime. The employees received overtime compensation for holidays, snow days, and Christmas and Spring breaks.

Status per Prosecuting Attorney: Prior Prosecuting Attorney forwarded Legislative Audit correspondence to Armorel School District thereby putting the school district on notice that such payments were not appropriate. The file was then closed because collection of the stated payments from employees’ wages would likely occur and no criminal wrong doing was apparent. No further action will be taken.

Town of Etowah (Audit Period: 1/1/08 - 12/31/08):

2010 $4,487 conflict of interest disbursements to Mayor’s mother without an authorizing ordinance.

Status per Prosecuting Attorney: The Town of Etowah passed an ordinance approving the employment of family members of city officials. No further action will be taken.

City of Keiser (Audit Period: 1/1/08 - 12/31/09):

2010 $4,902 unauthorized compensation to Recorder/Treasurer who prepared the payroll.

Status per Prosecuting Attorney: The City of Keiser was reimbursed the amount of $4,902 by the Recorder/Treasurer. Prior Prosecuting Attorney decided not to file charges against the recorder/treasurer since full restitution was made.

19

2nd Judicial District (continued)

Matters Reported by Legislative Joint Auditing Committee

Poinsett County

City of Fisher (Audit Period: 1/1/07 - 12/31/08):

2010 $21,536 conflict of interest disbursements to Recorder/Treasurer without an authorizing ordinance.

Status per Prosecuting Attorney: City of Fisher responded to Legislative Audit finding regarding payment to the Recorder/Treasurer. In the City’s response the mayor provided a copy of an ordinance passed in 2005 which city officials believe approved payments of this nature. This matter will remain under review for further determinations to be made if necessary.

City of Lepanto (Audit Period: 1/1/08 - 12/31/09):

2010 $1,043 improper credit card charges for fuel purchased and placed in Mayor’s personal vehicle.

$603 conflict of interest disbursements to Police Chief without an auth-orizing ordinance.

Status per Prosecuting Attorney: This matter is pending and warrants further investigation.

City of Trumann (Audit Period: 1/1/08 - 12/31/09):

2010 $3,450 conflict of interest disbursements to Clerk/Treasurer’s husband without an authorizing ordinance.

Status per Prosecuting Attorney: The City of Trumann passed an ordinance authorizing the disbursements.

Weiner School District (Audit Period: 7/1/08 - 6/30/09): 2010 $22,698 undocumented credit card charges.

Note: Wiener School District was annexed on July 1, 2010 by the Harrisburg School District.

Status per Prosecuting Attorney: This remains pending and warrants further investigation.

20

Judicial District Population: 70,645 Henry H. Boyce Circuit Judges: 3 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Jackson County City of Campbell Station (Audit Period: 1/1/07 - 12/31/09):

2010 $16,800 conflict of interest disbursements to Council member’s spouse without an authorizing ordinance.

Status per Prosecuting Attorney: Although the procedures to authorize these payments may have been statutorily improper, this office does not consider there to be any criminal intent underlying this matter. This matter is considered closed.

Lawrence County Lawrence County (Audit Period: 1/1/08 - 12/31/08):

2010 $226,770 inadequately documented disbursements to an independent contractor in 2009, 2008, and 2007. During 2008, this individual worked 302 days of which 50 were on weekends or holidays primarily providing courthouse maintenance and janitorial services. Based on Internal Revenue Service guidelines, an employer-employee relationship may exist between the County and independent contractor.

Status per Prosecuting Attorney: Deputy Prosecuting Attorney assigned to case determined that no criminal laws had been broken and no further action is needed. This matter is considered closed.

Town of Portia (Audit Period: 1/1/07 - 12/31/09):

2010 $2,400 conflict of interest disbursement to Mayor’s son-in-law without an authorizing ordinance.

Status per Prosecuting Attorney: Although the procedures to authorize these payments may have been statutorily improper, this office does not consider there to be any criminal intent underlying this matter. This matter is considered closed.

Town of Powhattan (Audit Period: 1/1/07 - 12/31/09):

2010 $9,168 conflict of interest disbursements to elected officials without an authorizing ordinance.

Status per Prosecuting Attorney: Although the procedures to authorize these payments may have been statutorily improper, this office does not consider there to be any criminal intent underlying this matter. This matter is considered closed.

Third Judicial District Jackson, Lawrence, Randolph, and Sharp Counties

21

3rd Judicial District (continued)

Matters Reported by Legislative Joint Auditing Committee

Randolph County Town of O’Kean (Audit Period: 1/1/07 - 12/31/09):

2010 $3,107 conflict of interest disbursements to elected officials and/or immediate family members without an authorizing ordinance.

Status per Prosecuting Attorney: Although the procedures to authorize these payments may have been statutorily improper, this office does not consider there to be any criminal intent underlying this matter.

Ravenden Springs Volunteer Fire Department (Audit Period: 1/1/07 - 10/31/09):

2010 $12,029 undocumented disbursements. These included checks issued to “cash” ($2,850), Pulaski Bank ($300), former Fire Department Secretary ($450), Fire Department Chief ($20), and various vendors ($8,409).

Status per Prosecuting Attorney: Deputy Prosecuting Attorney assigned to case declined to prosecute based upon questionable proof of criminal responsibility as well as the satisfaction by the board of directors of the fire department with regard to restitution which had been made by a former employee. This matter is considered closed.

Sharp County

City of Cherokee Village (Audit Period: 1/1/07 - 12/31/09):

2010 $11,800 conflict of interest disbursement to a business partially owned by a city employee without an authorizing ordinance.

Status per Prosecuting Attorney: Deputy Prosecuting Attorney assigned to the case determined that no criminal activity had occurred. This matter is considered closed.

Twin Rivers School District (Audit Period: 7/1/08 - 6/30/09): 2010 $5,607 undocumented credit card charges.

$12,116 conflict of interest disbursements to a company owned by an employee’s brother without Board resolution or Department of Education approval.

Status per Prosecuting Attorney: This matter has been referred to the Arkansas State Police Criminal Investigation Division. This matter is pending per State Police report.

Town of Williford (Audit Period: 1/1/07 - 12/31/09):

2010 $2,000 conflict of interest disbursements to an individual serving as an Alderman during 2009 and 2008 and Mayor during 2007 without an authorizing ordinance.

$5,400 undocumented payments to Recorder/Treasurer.

Status per Prosecuting Attorney: Although the procedures to authorize these payments may have been statutorily improper, this office does not consider there to be any criminal intent underlying this matter.

22

Judicial District Population: 218,782 John Threet Circuit Judges: 6 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Washington County

University of Arkansas, Fayetteville (Audit Period: 7/1/09 - 6/30/10):

2010 $126,149 unauthorized, non-University related purchases by Jami Coker, an employee. Coker pled guilty to theft of property, fraudulent use of a credit card, and forgery in the second degree. Restitution of $126,149 was ordered. Bond Trust Fund reimbursed losses totaling $125,149.

Status per Prosecuting Attorney: Coker pled guilty to Theft of Property, Fraudulent Use of a Credit Card, and Forgery in the Second Degree. Coker was sentenced, with each count to run consecutively, to a total of 482 months, with 458 months suspended imposition of sentence, and the remaining 24 months to be served in the Regional Punishment Facility. Restitution of $126,149 was ordered to be made in monthly payments of $275 beginning 90 days after release from the Regional Punishment Facility.

Note: No matters were reported in Madison County.

Fourth Judicial District Madison and Washington Counties

23

Judicial District Population: 105,419 David Gibbons Circuit Judges: 4 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Franklin County

City of Altus – Police Department (Audit Period: 3/1/09 - 7/27/10):

2010 $7,725 bond and fine funds were not deposited. Administrative Assistant Madelyn Hill, who resigned employment, was custodian of these funds. Bond Trust Fund reimbursed losses totaling $6,725.

Status per Prosecuting Attorney: Hill pled guilty to Theft of Property, Class B Felony, and was sentenced to 72 months probation. Hill was ordered to pay restitution of $ 12,525 of which $7,725 was to be paid to the City by no later than July 31, 201. Monthly installments are to be made to Legislative Audit to cover $4,800 in investigative expenses. In addition, Hill was ordered to pay costs plus a fine of $1,850.

Note: No matters were reported in Johnson and Pope Counties.

Fifth Judicial District Franklin, Johnson, and Pope Counties

24

Judicial District Population: 393,193 Larry Jegley Circuit Judges: 17 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Perry County

East End School District (Audit Period: 7/1/07 - 6/30/08):

2009 $3,093 improper transactions. Band instrument rental fees and fundraising sales deposited in two non-District bank accounts ($1,983), undocumented credit card charges ($40), and unauthorized, undocumented cash withdrawals ($1,070) by David Yarbrough. Yarbrough paid band invoices totaling $400, leaving $2,693 owed the District. Bond Trust Fund reimbursed losses totaling $1,693.

Status per Prosecuting Attorney: Former band director David Yarbrough was found guilty by jury of Theft of Property, Class C Felony, and sentenced to 12 months probation. Yarbrough was also ordered to pay fines and costs totaling $1,190.

Town of Fourche (Audit Period: 1/1/09 - 12/31/09):

2010 $724 conflict of interest disbursement to Mayor’s and

Recorder/Treasurer’s son without an authorizing ordinance.

Status per Prosecuting Attorney: No charges filed. Perryville School District (Audit Period: 7/1/07 - 6/30/08):

2009 $1,275 conflict of interest disbursements to a business owned by a

District employee without board resolution.

Status per Prosecuting Attorney: No charges filed. Pulaski County

City of Alexander (Audit Period: 1/1/08 - 12/31/09):

2010 $17,748 unauthorized compensation to Police Chief ($6,639), Assistant Police Chief ($5,772), and Fire Chief ($5,337).

Terms of a lease-purchase agreement (Agreement) for the purchase of two police cars are a loan of $44,700 with an annual interest rate of 6.25% to be repaid by a monthly payment of $977 for 5 years. The total lease price is $58,669 of which $13,969 represents interest. The Lessor-provided amortization schedule indicated a loan amount of $48,528, or $3,828 more than the Agreement, with an annual interest rate of 8%.

Sixth Judicial District Perry and Pulaski Counties

25

6th Judicial District (continued)

Pulaski County (continued)

City of Alexander (Audit Period: 1/1/08 - 12/31/09) (continued):

2010 Terms of the Agreement for the purchase of a fire truck are a loan of $50,000, no stated interest, to be repaid by a monthly payment of $884 for 7 years. The total lease price is $74,325 of which $24,325 represents interest. The Lessor-provided amortization schedule indicated a loan amount of $52,859, or $2,859 more than the Agreement, with an annual interest rate of 9.5%.

Terms of the prior year Agreement for the refinancing of six existing lease purchases are a loan of $350,000 with an annual interest rate of 9.9% to be repaid by a monthly payment of $4,971 for 14 years. The total lease price is $835,099 of which $485,099 represents interest. The Lessor-provided amortization schedule indicated a loan amount of $435,975, or $85,975 more than the Agreement, with an annual interest rate of 9% to be repaid over a 12 year period. The City continued making monthly payments on this loan during 2009 and 2008.

The Agreement does not comply with Ark. Const. amend. 78 which indicates municipalities may incur short-term financing obligations having a term not to exceed five years.

Status per Prosecuting Attorney: No criminal charges filed.

City of Alexander (Audit Period: 1/1/07 - 6/30/08):

2009 A lease-purchase agreement (Agreement) was executed to refinance six existing lease-purchase agreements with First Government Lease Company (Lessor). Terms of the Agreement are a loan of $350,000 with an annual interest rate of 9.9% to be repaid by a monthly payment of $4,971 for 14 years. The total lease price is $835,099 of which $485,099 represents interest. The Lessor-provided amortization schedule indicated a loan amount of $435,975, or $85,975 more than the Agreement, with an annual interest rate of 9% to be repaid over a 12 year period.

The Agreement does not comply with Ark. Const. amend. 78 which indicates municipalities may incur short-term financing obligations having a term not to exceed five years.

As a condition of the refinancing Agreement, the Lessor paid the existing lease agreements totaling $305,250, leaving a balance of $44,750 due the City. Of this amount, the Lessor paid only $31,650 in December 2007, leaving $13,100 due the City. Subsequently, on June 30, 2009, the Lessor paid $11,558 which leaves $1,542 due the City.

Status per Prosecuting Attorney: No criminal charges filed.

Matters Reported by Legislative Joint Auditing Committee

26

6th Judicial District (continued)

Pulaski County (continued)

Arkansas Department of Finance and Administration - Employee Benefits Division (EBD) (Audit Period: 7/1/06 - 6/30/07):

2008 Concerns regarding two professional/technical service contracts issued

to PDB Enterprises, Inc. and Pearce Enterprise, Inc.

Status per Prosecuting Attorney: No criminal charges filed.

Arkansas Department of Finance and Administration - Little Rock Revenue Central Office (Audit Period: 7/15/04 - 10/2/08):

2009 $247,589 misappropriated personalized license plate fees. Special

License Clerk Karen Brewer identified as custodian and her employment was terminated. Bond Trust Fund reimbursed losses totaling $249,000.

$10,666 misappropriated sales tax and vehicle title registration fees. Central Office Cashier Kenyatta Withers identified as custodian and her employment was terminated. Bond Trust Fund reimbursed losses totaling $9,666.

Status per Prosecuting Attorney: Brewer pled guilty to one count of Theft of Property, Class B Felony, was sentenced to 216 months incarceration, 24 months suspended imposition of sentence, and ordered to pay restitution of $190,000. Restitution to be paid in monthly installments of $1,000 to begin 30 days after release. Withers was charged with Forgery in the First Degree and Theft of Property, pled guilty, was sentenced to 48 months probation and ordered to pay restitution of $10,666 with monthly installments of $175 starting June 25, 2011.

Arkansas Department of Health (Audit Period: 6/1/03 - 8/20/08):

2009 $42,673 improper travel expense reimbursements to employees Craig

Burger ($35,674) and Mark McIntosh ($6,999). In addition, travel expense reimbursements of $9,101 remain questioned as to authenticity. Burger and McIntosh were determined to have submitted falsified travel expense documentation and their employment was subsequently terminated.

Status per Prosecuting Attorney: On August 8, 2011, Craig Burger was sentenced in Pulaski County Circuit Court to 8 years in Arkansas Department of Correction plus 12 years suspended and restitution of $30,300 to Arkansas Department of Health and $15,000 to Legislative Audit for investigative cost. Restitution set at $400 per month after release. Mark McIntosh was charged with one count of Theft of Property, pled guilty, and ordered to 60 months probation and 50 hours of community service. Full restitution was paid prior to conviction.

Matters Reported by Legislative Joint Auditing Committee

27

6th Judicial District (continued)

Pulaski County (continued)

Arkansas Livestock Show Association (Audit Period: 1/1/09 - 12/31/09):

2010 $5,169 undocumented credit card purchases. Subsequent to the report date, the Association provided adequate documentation for $544 of the undocumented purchases, leaving $4,625 as undocumented.

Status per Prosecuting Attorney: No criminal charges filed.

Arkansas State Land Department (Audit Period: 7/1/08 - 6/30/09):

2010 Land Commissioner Mark Wilcox’s spouse was involved in an accident while driving a state-owned vehicle for nonbusiness purposes on September 6, 2008. Although no damages were reported to the state-owned vehicle, the Agency paid $995 to repair damage to the other vehicle. Subsequently, Wilcox reimbursed $995 to the Agency on August 11, 2010.

…..

$4,558 undeposited receipts. Arkansas State Police and Little Rock Police Department both declined to pursue the matter due to inconclusive evidence, low dollar amount, and the possible suspect no longer employed by the Agency.

Status per Prosecuting Attorney: No criminal charges filed.

Brothas and Sistas, Inc. (Audit Period: 4/1/09 - 3/31/10):

2010 $6,132 undocumented expenditures.

Status per Prosecuting Attorney: No criminal charges filed.

Matters Reported by Legislative Joint Auditing Committee

28

6th Judicial District (continued)

Pulaski County (continued)

Lottery Commission (Audit Period: 7/1/09 - 6/30/10):

2010 $3,470 travel reimbursement requests submitted by Executive Director lacked proper approval by a designated travel supervisor.

$16,189 travel payments/reimbursements in conflict with state laws and travel regulations. Hotel expenses were paid above the federal per diem rate without prior authorization by the Agency’s Executive Director ($9,616); charges to the travel credit card not supported by adequate documentation, the documentation did not match the amount charged, nor appear to be an original ($1,872); documentation to support travel credit card statements/TR-1 reimbursements for airline ticket purchases were screen prints from an airline/travel booking website printed prior to an actual flight confirmation ($2,814); travel expenses paid on behalf of, or reimbursed to, the Vice President of Gaming, for which a business purpose was not adequately documented ($1,423); and other reimbursements in conflict with various state laws and travel regulations including receipts not matching the dates listed on travel reimbursement forms, excess mileage reimbursement, exceeding federal per diem rate for meals incurred during overnight travel, reimbursement for meals without overnight travel, and reimbursement for tips above the 15% allowed by state law ($464).

$6,296 improper retroactive payments to two employees.

Travel regulation R1-19-903 states mileage shall be computed and reimbursed using map mileage. Auditor was unable to adequately test marketing sales representatives’ travel due to insufficient documentation. Information provided on employees’ travel reimbursement forms was vague and/or incomplete limiting the Agency’s ability to properly review the supporting documentation prior to payment. In addition, auditor was unable to verify miles traveled in order to recalculate mileage reimbursement for accuracy. Travel reimbursements for marketing sales representatives totaled $198,983, including one employee who was reimbursed $18,858 for 44,900 miles driven during a ten month period.

Ark. Code Ann. § 23-115-206 (a) (1) requires the Commission to establish effective internal controls. To effectively establish internal controls, management should communicate policy and procedures to all staff. Management did not communicate the policy and procedures for the accrual and use of compensatory time to exempt staff until August 3, 2010 for time purportedly earned between July 1 and November 30, 2009. Subsequent to the issuance of the formal policy, numerous changes were made by management including a suspension of compensatory time usage. In addition, management was unable to properly account for the potential compensatory time resulting in ten different versions of compensatory time being submitted for audit. Due to the numerous changes made to the compensatory time policy, at the end of audit fieldwork, it remains unclear what the Agency had established as policy. Status per Prosecuting Attorney: Under review.

Matters Reported by Legislative Joint Auditing Committee

29

6th Judicial District (continued)

Pulaski County (continued)

Martin Luther King, Jr. Commission (Audit Period: 7/1/07 - 6/30/08):

2009 $88,650 undocumented expenditures. Subsequently, the Agency

obtained invoices totaling $65,997 from various vendors. Analysis of one invoice from the Peabody Hotel in Little Rock revealed two Commission employees who reside in Little Rock had hotel charges of $1,325 and ten other individuals had hotel charges of $2,760 for which the Agency was unable to provide an explanation or justification.

Status per Prosecuting Attorney: No criminal charges filed.

Pulaski County Special School District (Audit Period: 3/1/04 - 2/19/10):

2010 $439,745 misappropriated funds by Mechanical Systems Supervisor James Diemer. Bond Trust Fund reimbursed losses totaling $249,000.

$72,918 unauthorized salary compensation to Superintendent which was subsequently reimbursed to the District.

$25,039 paid to Superintendent as salary/benefits overpayments ($17,203) and as reimbursement for, or charged on District credit card, unallowable, undocumented expenses ($7,836).

$3,677 cash advances to Board members for unallowable and questioned travel expenses.

$2,391 credit card purchases for which a business purpose could not be determined ($1,815) and finance and late payment charges ($576).

$11,975 overpayment to a vendor in November 2006 was not fully reimbursed until May 28, 2009.

$969 questioned purchases paid with Federal grants funds for women’s undergarments at Dillard’s ($311), athletic apparel at Lady Foot Locker ($464), and athletic shoes at Finish Line ($194).

$31,536 Jacksonville High School Activity Fund collections not deposited in bank account. Bookkeeper Rosalind Taylor was charged with theft of property. Note: Arkansas Department of Education took control of the District on June 20, 2011. Status per Prosecuting Attorney: Diemer pled guilty to Theft of Property from a Government Entity which Received Federal Funds, Class C Felony, in Federal Court. Diemer was sentenced to 18 months imprisonment and upon release will be on supervised release for 3 years. Restitution of $387,442 was ordered. During imprisonment, Diemer will pay as restitution 50%, per month, of all funds that are available to him. Upon release restitution payments will be reduced to 10%, per month, of gross monthly income.

Civil charges have been filed by the District against former Superintendent James Sharpe seeking damages of $25,039.

Matters Reported by Legislative Joint Auditing Committee

30

6th Judicial District (continued)

Pulaski County (continued)

Pulaski County Special School District (Audit Period: 3/1/04 - 2/19/10) (continued):

Status per Prosecuting Attorney (continued): Rosalind Taylor, former bookkeeper at Jacksonville High School pled guilty to theft of property is schedule to be sentenced November 8, 2011.

Remaining issues are under review.

Pulaski County Special School District (Audit Period: 3/1/09 - 11/30/10): 2010 $23,919 unallowable expenses paid to, or on behalf of, Superintendent.

$1,360 unallowable expenses paid to, or on behalf of, Board members.

$6,223 improper disbursements to employee for moving expenses not included in employment contract ($5,899) and unallowed expenses ($324).

$1,974 improper disbursements to a consultant for mileage reimbursements not included in contract.

$9,741 salary overpayments to three employees.

$1,799 improper reimbursements to Grant Writer for supplies not for District use ($1,564), questioned mileage reimbursements ($65), and duplicated mileage reimbursement ($170).

Status per Prosecuting Attorney: Under review.

City of Sherwood (Audit Period: 1/1/07 - 12/31/07):

2009 $219,913 improper transfer of funds from City’s bank account to several non-City bank accounts via unauthorized use of the Clerk/Treasurer’s electronic access (user name and password) to the bank account. The City has recovered $53,635 and received $50,000 from their insurance company. $7,165 improper transaction. City contributed funds to a nonprofit corporation.

Status per Prosecuting Attorney: No criminal charges filed.

Matters Reported by Legislative Joint Auditing Committee

31

Judicial District Population: 50,776 Eddy R. Easley Circuit Judges: 2 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Grant County Grant County (Audit Period: 1/1/08 - 12/31/09):

2010 $1,118 reimbursement to Juvenile Probation Officer for purchases that appear not for public purposes.

Status per Prosecuting Attorney: The Juvenile Probation Officer used court funds in the amount of $377 and $741 in 2009 and 2008 respectively to buy Christmas gifts for under privileged children in Grant County. She is now aware that these types of expenditures are not allowable and will not expend court funds in the future for such purposes. No criminal charges were filed because of the absence of criminal intent.

Hot Spring County Arkansas Department of Parks and Tourism – DeGray Lake Resort State Park

(Audit Period: 7/1/04 - 11/30/08):

2010 $202,113 misappropriated park revenue. Parks Administration Support Coordinator and bookkeeper Carla Beatty was custodian of the funds.

Status per Prosecuting Attorney: Carla Beatty has been charged in Hot Spring County Circuit Court (30CR-11-099-1) with one count of Theft of Property and five counts of Attempt to Evade or Defeat Tax. The amount of the alleged theft is $202,113. The matter is pending.

Town of Friendship (Audit Period: 1/1/07 - 12/31/08):

2009 Fines and costs revenue for the years 2008 and 2007 totaled $76,742 and $109,264 which represented 56% and 71%, respectively, of the Town’s expenditures, less capital expenditures, transfers, and debt service in the preceding year.

Status per Prosecuting Attorney: The number of tickets issued decreased substantially from the year ended December 31, 2007 to the year ended December 31, 2008. Mayor and Chief of Police advised that subsequent to the audit period, a plan was implemented by Friendship to insure that it is in compliance with the “Arkansas Speed Trap Law.” Prosecuting Attorney has requested that this matter be addressed by Legislative Audit during the audit of Friendship for the year 2010.

Note: As of report date, the 2010 audit is in progress.

Seventh Judicial District Grant and Hot Spring Counties

32

Christi McQueen (Current) Judicial District Population: 31,606 Ashley Parker (2010) Circuit Judges: 2 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Hempstead County Hope School District (Audit Period: 7/1/08 - 6/30/09):

2010 $2,270 unauthorized compensation to Payroll Clerk/Custodian. Of this amount, $185 has been reimbursed.

Status per Prosecuting Attorney: This matter was referred to the prosecutor’s office on March 25, 2010. The unauthorized compensation to the payroll clerk/custodian, Danita Thomas, who prepared her own overtime calculations, was $2,270, of which $185 has been reimbursed, leaving an amount due of $2,085. In a settlement agreement, the Hope School Board elected not to proceed against Ms. Thomas for further reimbursement and Ms. Thomas agreed to resign her positions. Prosecutor has made several contacts with Ms. Thomas’ attorney, Marcia Barnes, who has since sent documents, with more forthcoming, which she believes are pertinent to the issue of criminal liability. The investigation of this matter is still pending.

Town of Oakhaven (Audit Period: 1/1/08 - 12/31/09):

2010 $3,120 conflict of interest disbursements to Mayor’s spouse, who was appointed Recorder/Treasurer on December 8, 2008 ($1,870), and Mayor ($1,250) without an authorizing ordinance.

Status per Prosecuting Attorney: This matter was referred to the prosecutor’s office on October 1, 2010. There were two unauthorized disbursements, specifically, $1,870 to the Mayor’s spouse and $1,250 to the Mayor. The Mayor, Summer Bright, informed prosecutor that her husband had been paid to work for the town before she took office and he continued to do similar work after she assumed office. Mayor Bright provided prosecutor a copy of minutes of the January 6, 2011, town meeting which reflected a motion and a second, with unanimous approval, “to continue to allow the Bright family to do contract labor for the town.” The minutes indicated the town would meet with Legislative Audit to ensure compliance with audit. Prosecutor determined that the unauthorized disbursement was an ethics matter. No further action will be taken.

Eighth Judicial District-North Hempstead and Nevada Counties

33

8th Judicial District (continued)

Hempstead County (continued)

Town of Patmos (Audit Period: 1/1/08 - 12/31/09):

2010 $8,225 conflict of interest disbursement to Recorder/Treasurer’s son without an authorizing ordinance.

Status per Prosecuting Attorney: This matter was referred to the prosecutor’s office on September 3, 2010. The Recorder/Treasurer’s son was paid $8,225 for labor without an authorizing ordinance. Prosecutor interviewed the Mayor/Recorder/Treasurer, Elizabeth Peters, and reviewed Ordinance No. 1-2010, dated September 13, 2010, which she provided. The ordinance provides as follows: “That Randy Peters be appointed the grounds keeper and general maintenance provider of all of the properties of the Town of Patmos…” Prosecutor determined that the unauthorized disbursement was an ethics matter. No further action will be taken.

Note: No matters were reported in Nevada County.

Matters Reported by Legislative Joint Auditing Committee

34

Carlton Jones (Current) Judicial District Population: 51,107 Brent Haltom (2010) Circuit Judges: 3 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Lafayette County Lafayette County (Audit Period: 1/1/08 - 12/31/09): 2010 $1,451 unallowable disbursements from the Sheriff’s Inmate Account.

Status per Prosecuting Attorney: Sherriff’s office has repaid funds to Lafayette County and Prosecutor is satisfied with steps taken by Sherriff’s office to resolve the finding.

Miller County Fouke School District (Audit Period: 7/1/08 - 6/30/09):

2010 $2,052 conflict of interest disbursements to a business owned by a District employee without Board resolution.

Status per Prosecuting Attorney: After discussion with Superintendent Tommy Tyler, the previous Prosecuting Attorney was satisfied the proper steps were taken to address the findings of the audit.

City of Garland (Audit Period: 1/1/07 - 7/31/09):

2009 $3,000 unearned payroll advances to Recorder/Treasurer Janice Hanson.

Status per Prosecuting Attorney: The discrepancies alleged on the part of Janice Hanson while she was recorder/treasurer are the subject of a criminal action. In Case# CR 2009-464-1, State of Arkansas vs. Janice Hanson, the defendant is charged with one (1) count of Theft of Property over $1,500, a Class “C” Felony. Hanson was ordered to pay restitution of $3,000 in lieu of 24 months probation.

$86,042 for two lease-purchase agreements executed by the Mayor for three used police squad cars and a 1979 GMC tanker and other fire equipment. Neither of the lease agreements were approved by the City Council nor has the City made any payments. A default judgment for $4,319 plus court costs was awarded the lease company and the City paid $5,466, but the potential liability the City may encumber due to the leases is unclear. The GMC tanker was sighted, but the vehicles and other fire equipment related to the lease-purchase agreements could not be located.

$10,098 outstanding account balance with a wireless telephone service provider. Account was cancelled by the vendor.

Status per Prosecuting Attorney: See response on page 35.

Eighth Judicial District-South Lafayette and Miller Counties

35

8th Judicial District-South (continued)

Miller County (continued)

City of Garland (Audit Period: 1/1/04 - 7/31/07):

2008 $48,800 undocumented disbursements to Mayor Yvonne Dockery ($6,400) (Note 1), Preston Lemay ($9,000), and two former City employees Lee Morris Cullins ($14,000) and David Johnson ($19,400).

$1,959 undocumented travel reimbursements to Mayor Yvonne Dockery ($681), Recorder/Treasurer Janice Hanson ($1,149), and former Recorder/Treasurer Lateta Briggs ($129).

$4,900 undocumented disbursements to a vendor.

$1,667 water and sewer receipts over deposits.

$7,747 unauthorized credits to water and sewer customer accounts of City employees and elected officials.

Bond Trust Fund reimbursed losses totaling $132,074.

Status per Prosecuting Attorney: Ms. Dockery was prosecuted in the United States District Court for the Western District of Arkansas for her conduct while in office. In Case # 4:09 CR 40021-001, Ms. Dockery, was found guilty on July 23, 2010, of three (3) counts of mail fraud in violation of 18 U.S.C section 1341. Those convictions are in relation to the thefts she committed from Garland City and are reflected in your audits. For these convictions, Ms. Dockery was sentenced to thirty (30) months imprisonment and ordered to make restitution in the amount of $128,414.

Miller County (Audit Period: 1/1/08 - 12/31/08):

2010 $26,000 unauthorized disbursements for malpractice insurance policy deductibles not within terms of contract executed between the County and a doctor to provide medical services for County inmates.

Status per Prosecuting Attorney: Miller County’s expenditure of $26,000 for malpractice insurance policy deductibles was ratified by the Quorum Court on December 15, 2008.

Matters Reported by Legislative Joint Auditing Committee

36

Judicial District Population: 22,995 C. A. Blake Batson Circuit Judge: 1 Prosecuting Attorney

Matters Reported by Legislative Joint Auditing Committee

Clark County

Arkadelphia School District (Audit Period: 7/1/08 - 6/30/09):

2010 $11,439 conflict of interest disbursements to a nonprofit organization for which a District employee also served as the organization’s Executive Director without Board resolution or Department of Education approval.

Status per Prosecuting Attorney: Approval was granted from Arkansas Department of Education on August 10, 2010. No criminal conduct to prosecute.

City of Gurdon (Audit Period: 1/1/07 - 12/31/09):