Embed Size (px)

Citation preview

1

Structures For Acquiring Entities Federal & State

Tax Consequences

Tax Institute CPEFort Worth, TexasAugust 3, 2017

William H. HornbergerJackson Walker L.L.P.

2323 Ross Avenue, Suite 600Dallas, Texas 75201

214‐953‐[email protected]

Steven D. MooreJackson Walker L.L.P.

100 Congress Avenue, Suite 1100Austin, Texas 78701

512‐236‐[email protected]

2

JOINT & SEVERAL LIABILITYFOR MARGIN TAX PURPOSES

3

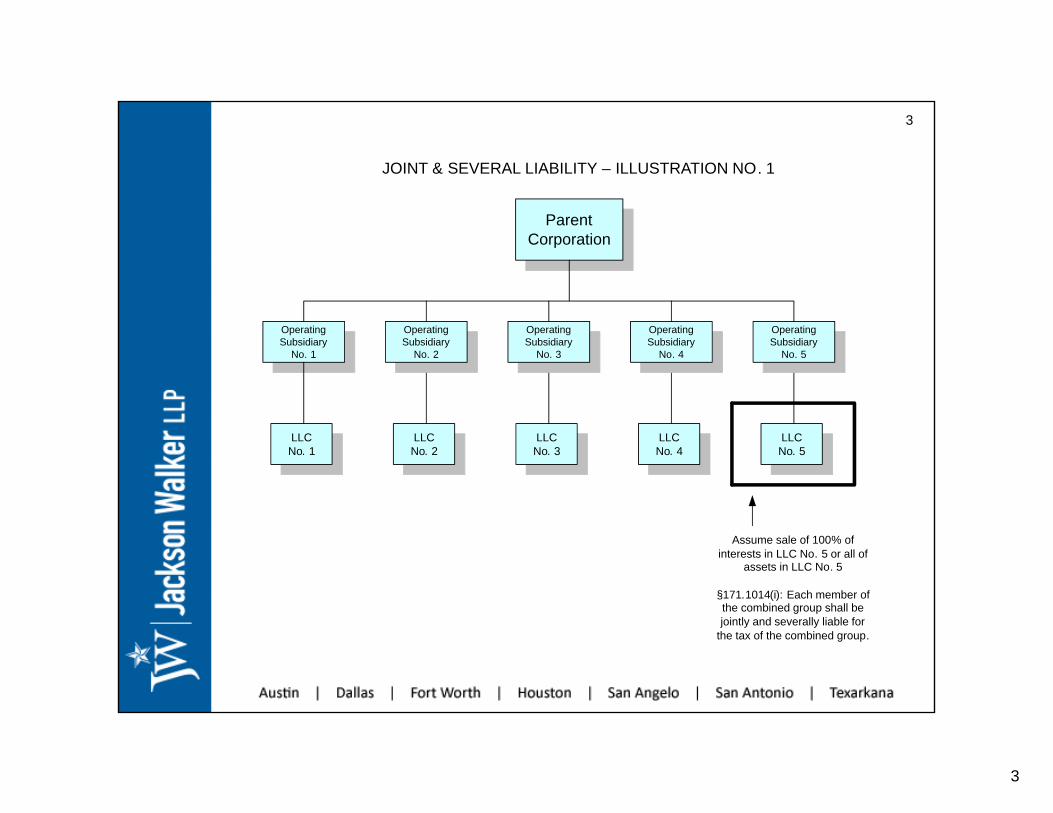

Parent Corporation

LLC No. 1

LLC No. 2

LLC No. 3

LLC No. 4

LLC No. 5

Operating Subsidiary

No. 1

Operating Subsidiary

No. 2

Operating Subsidiary

No. 3

Operating Subsidiary

No. 4

Operating Subsidiary

No. 5

JOINT & SEVERAL LIABILITY – ILLUSTRATION NO. 1

Assume sale of 100% of interests in LLC No. 5 or all of

assets in LLC No. 5

§171.1014(i): Each member of the combined group shall be jointly and severally liable for

the tax of the combined group.

3

4

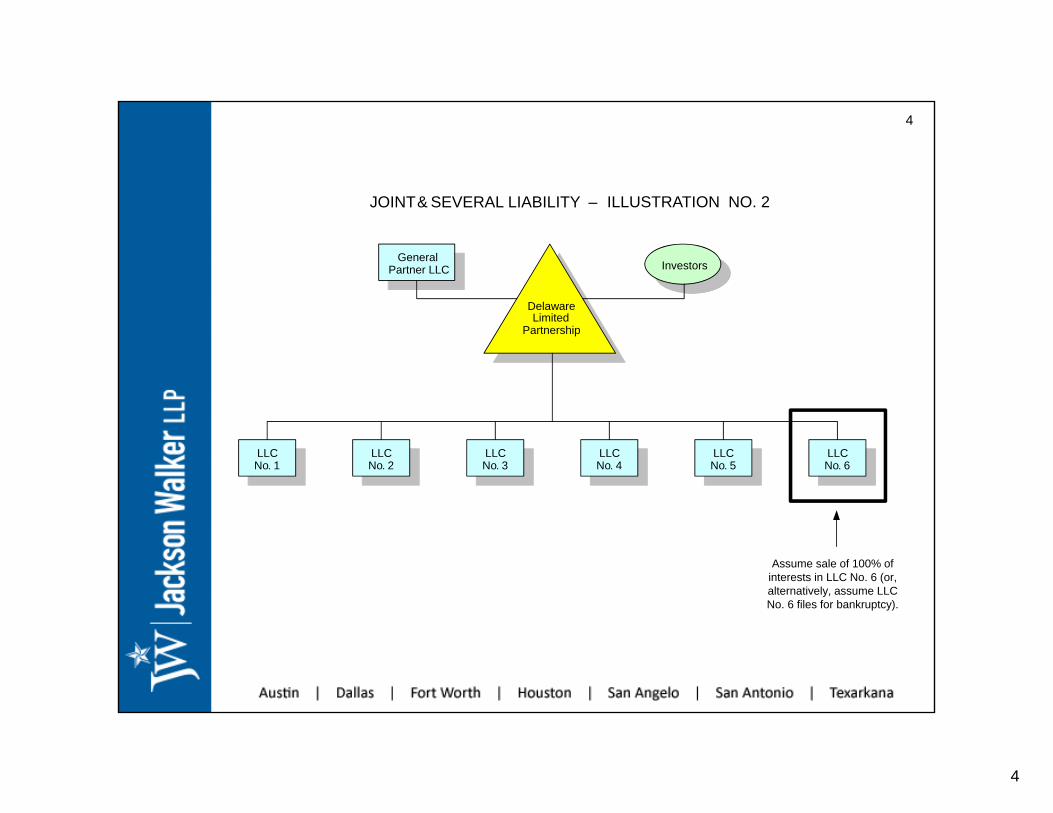

DelawareLimited

Partnership

General Partner LLC Investors

LLC No. 1

LLC No. 2

LLC No. 3

LLC No. 4

LLC No. 5

LLC No. 6

JOINT & SEVERAL LIABILITY – ILLUSTRATION NO. 2

Assume sale of 100% of interests in LLC No. 6 (or, alternatively, assume LLC No. 6 files for bankruptcy).

4

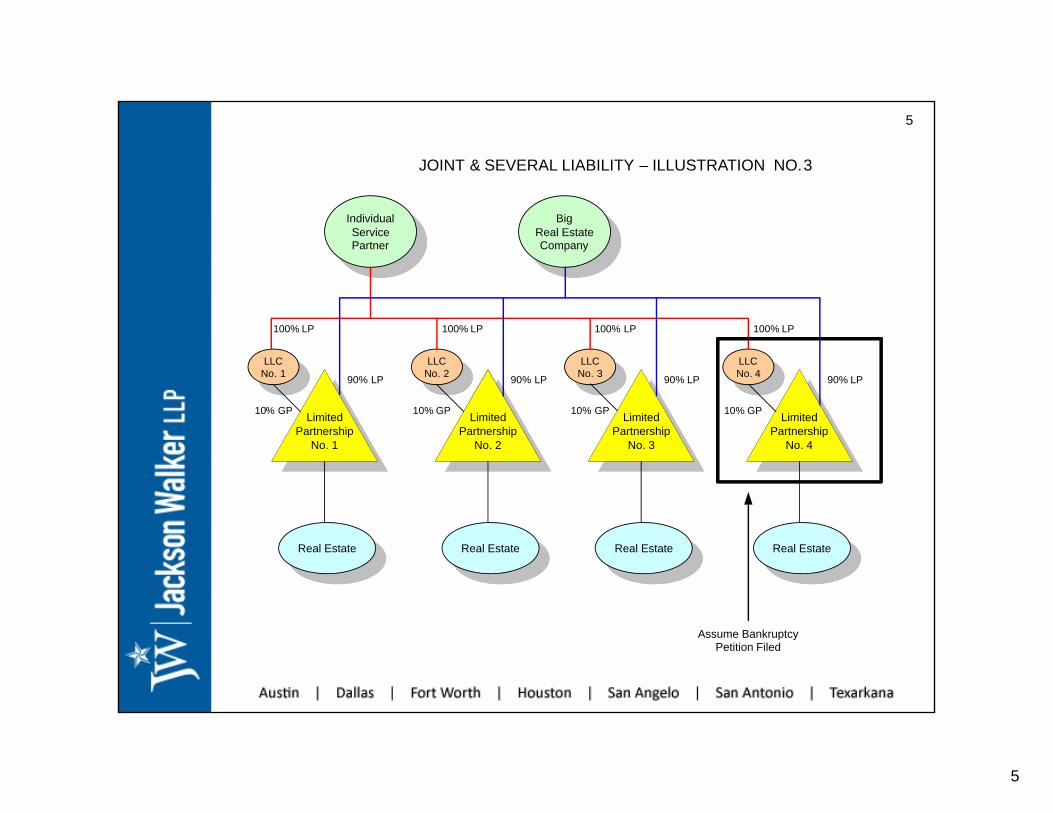

5

JOINT & SEVERAL LIABILITY – ILLUSTRATION NO.3

LimitedPartnership

No. 1

LimitedPartnership

No. 2

LimitedPartnership

No. 3

LimitedPartnership

No. 4

Real Estate Real Estate Real Estate Real Estate

Individual Service Partner

BigReal EstateCompany

LLCNo. 1

LLCNo. 2

LLCNo. 3

LLCNo. 490% LP 90% LP 90% LP 90% LP

10% GP 10% GP 10% GP 10% GP

Assume Bankruptcy Petition Filed

100% LP 100% LP 100% LP 100% LP

5

6

Selected Acquisition Structures

7

CORPORATIONS – SELECTED FORMS OF TAXABLE ACQUISITIONS

8

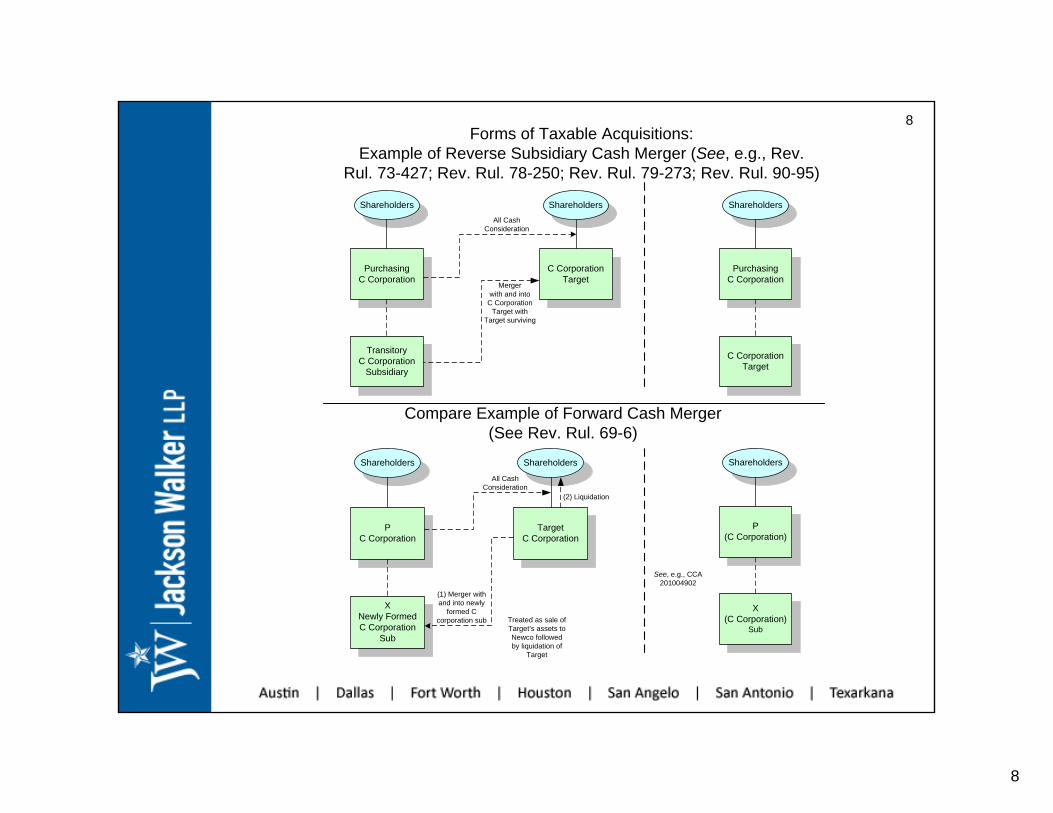

Forms of Taxable Acquisitions: Example of Reverse Subsidiary Cash Merger (See, e.g., Rev.

Rul. 73-427; Rev. Rul. 78-250; Rev. Rul. 79-273; Rev. Rul. 90-95)

Purchasing C Corporation

Shareholders

C Corporation Target

Transitory C Corporation

Subsidiary

ShareholdersAll Cash

Consideration

Mergerwith and into

C CorporationTarget with

Target surviving

PC Corporation

Shareholders

TargetC Corporation

XNewly FormedC Corporation

Sub

Shareholders

All Cash Consideration

(1) Merger with and into newly

formed C corporation sub

Compare Example of Forward Cash Merger (See Rev. Rul. 69-6)

Purchasing C Corporation

Shareholders

C Corporation Target

(2) Liquidation

Treated as sale of Target’s assets to Newco followed by liquidation of

Target

P(C Corporation)

Shareholders

X(C Corporation)

Sub

See, e.g., CCA 201004902

8

9

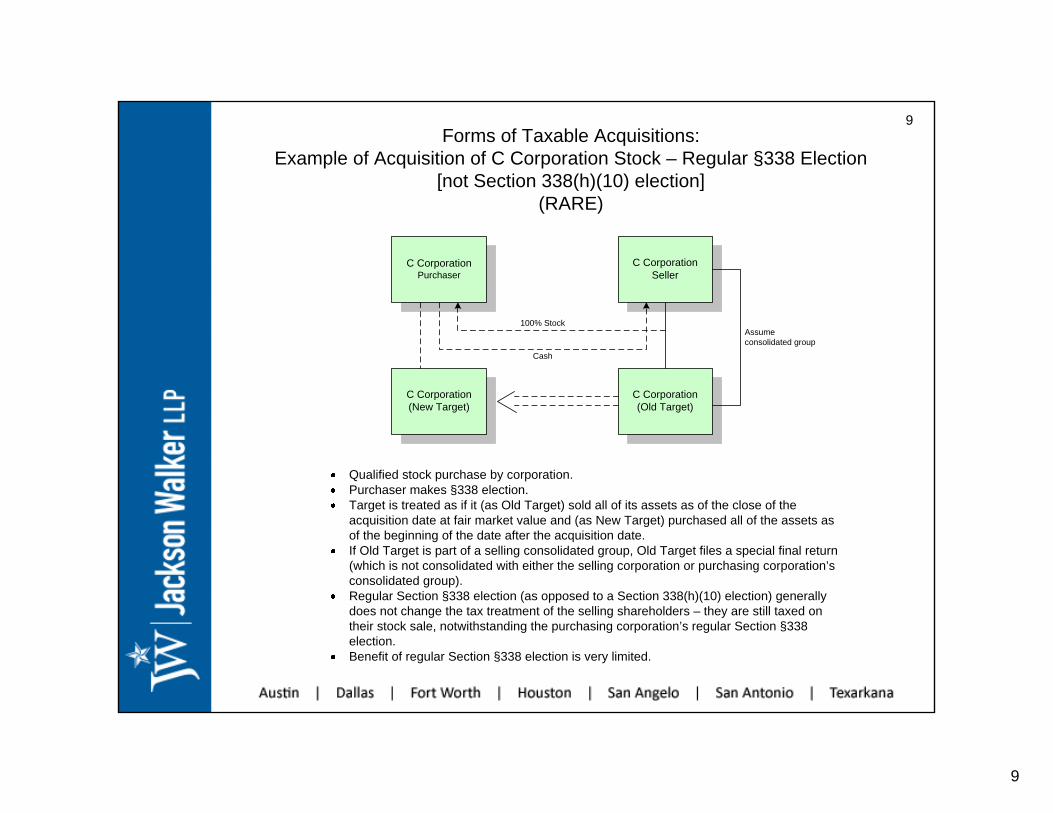

Forms of Taxable Acquisitions: Example of Acquisition of C Corporation Stock – Regular §338 Election

[not Section 338(h)(10) election](RARE)

C CorporationPurchaser

C Corporation (Old Target)

C Corporation Seller

Cash

100% Stock

C Corporation (New Target)

Qualified stock purchase by corporation.Purchaser makes §338 election.Target is treated as if it (as Old Target) sold all of its assets as of the close of the acquisition date at fair market value and (as New Target) purchased all of the assets as of the beginning of the date after the acquisition date.If Old Target is part of a selling consolidated group, Old Target files a special final return (which is not consolidated with either the selling corporation or purchasing corporation’s consolidated group).Regular Section §338 election (as opposed to a Section 338(h)(10) election) generally does not change the tax treatment of the selling shareholders – they are still taxed on their stock sale, notwithstanding the purchasing corporation’s regular Section §338 election. Benefit of regular Section §338 election is very limited.

Assume consolidated group

9

10

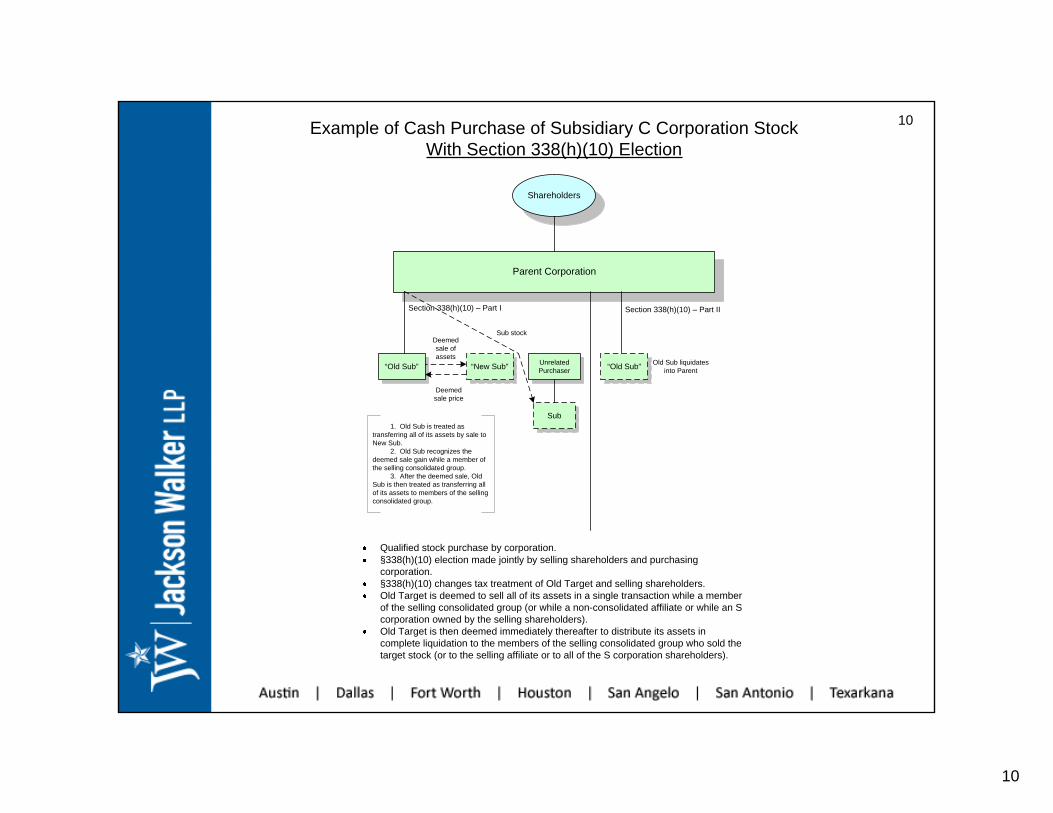

Parent Corporation

Shareholders

Example of Cash Purchase of Subsidiary C Corporation StockWith Section 338(h)(10) Election

Sub

“Old Sub” Unrelated Purchaser“New Sub”

Deemed sale price

Deemed sale of assets

Section 338(h)(10) – Part I

“Old Sub”

Section 338(h)(10) – Part II

Old Sub liquidates into Parent

Sub stock

1. Old Sub is treated as transferring all of its assets by sale to New Sub.

2. Old Sub recognizes the deemed sale gain while a member of the selling consolidated group.

3. After the deemed sale, Old Sub is then treated as transferring all of its assets to members of the selling consolidated group.

Qualified stock purchase by corporation.§338(h)(10) election made jointly by selling shareholders and purchasing corporation.§338(h)(10) changes tax treatment of Old Target and selling shareholders.Old Target is deemed to sell all of its assets in a single transaction while a member of the selling consolidated group (or while a non-consolidated affiliate or while an S corporation owned by the selling shareholders).Old Target is then deemed immediately thereafter to distribute its assets in complete liquidation to the members of the selling consolidated group who sold the target stock (or to the selling affiliate or to all of the S corporation shareholders).

10

11

CORPORATIONS – SELECTED FORMS OF TAX‐FREE ACQUISITIONS

12

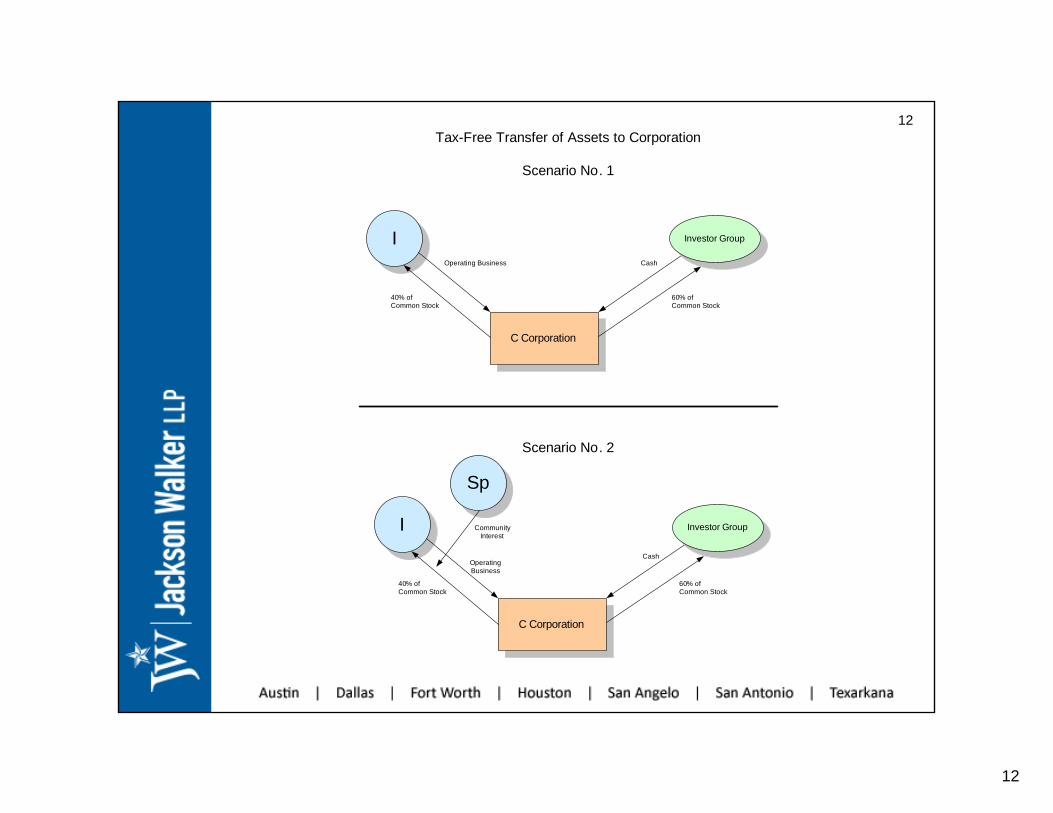

I

Tax-Free Transfer of Assets to Corporation

Scenario No. 1

C Corporation

60% of Common Stock

Operating Business Cash

Scenario No. 2

40% of Common Stock

I

C Corporation

60% of Common Stock

Operating Business

Cash

40% of Common Stock

Investor Group

Investor Group

Sp

CommunityInterest

12

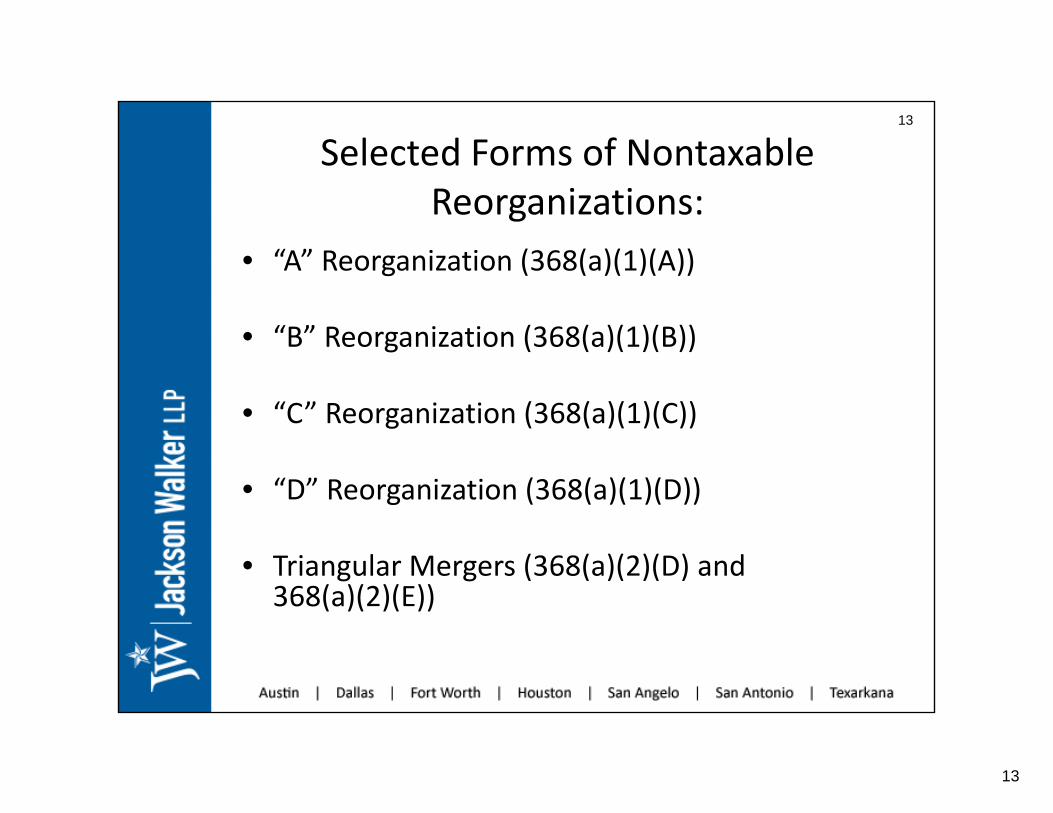

13

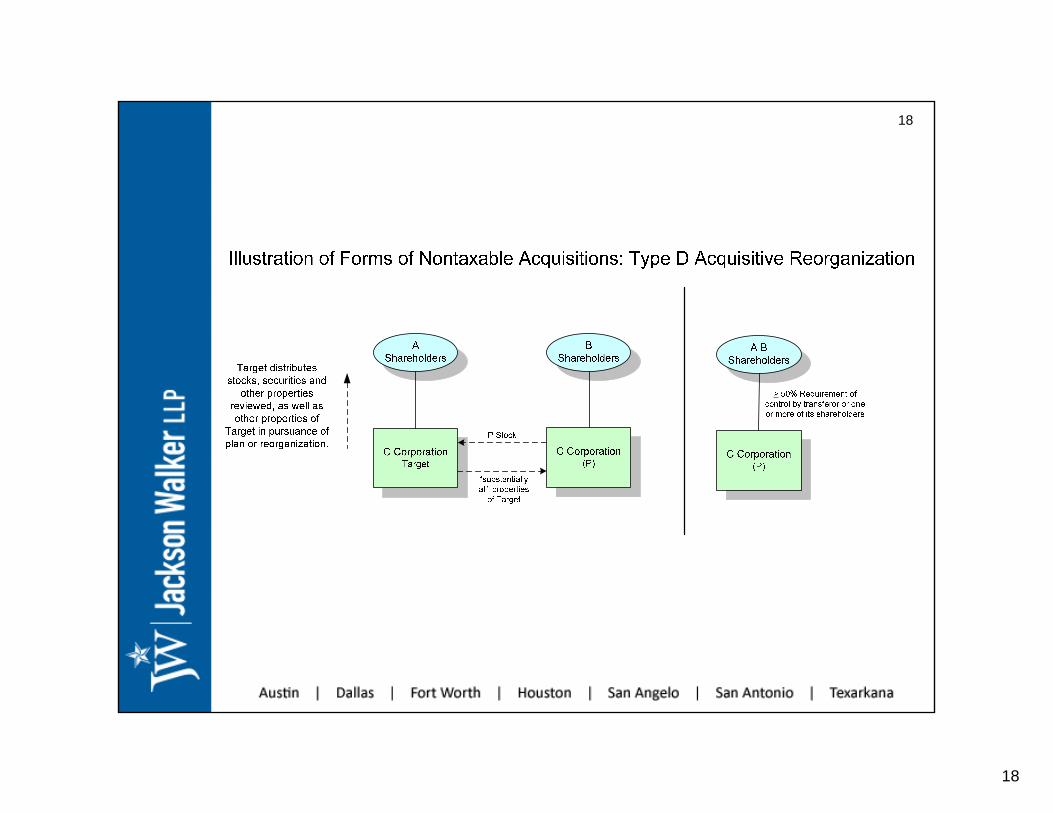

Selected Forms of Nontaxable Reorganizations:

• “A” Reorganization (368(a)(1)(A))

• “B” Reorganization (368(a)(1)(B))

• “C” Reorganization (368(a)(1)(C))

• “D” Reorganization (368(a)(1)(D))

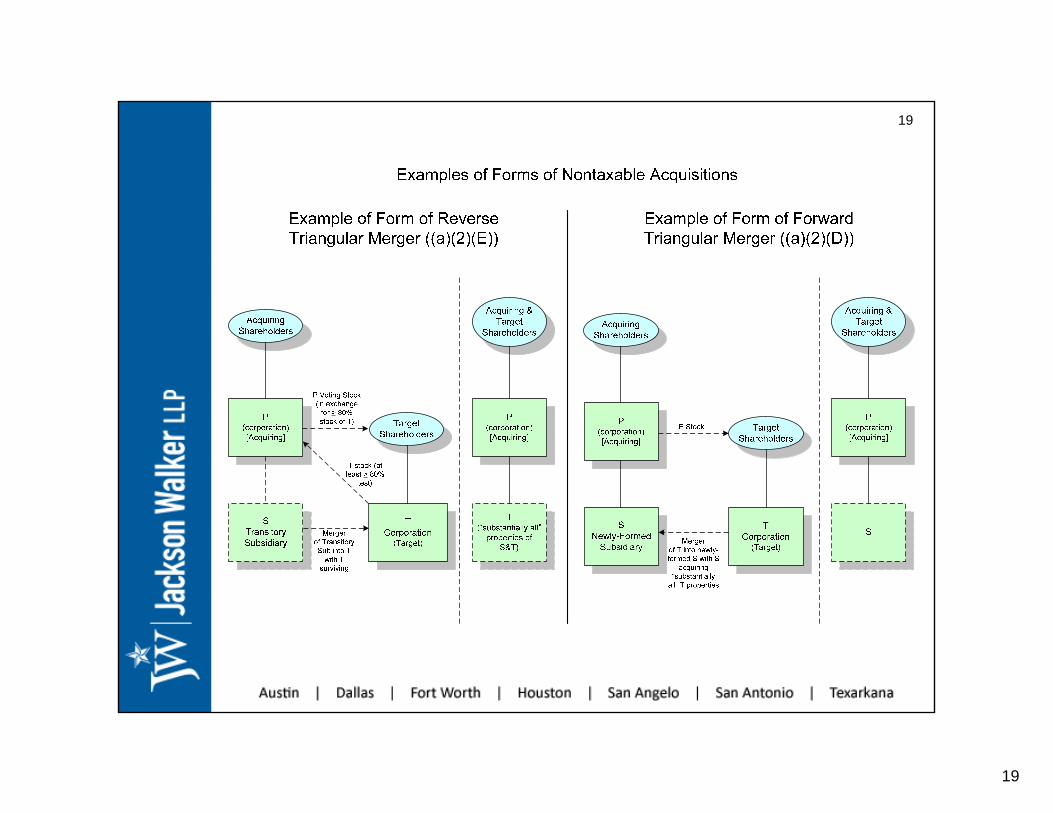

• Triangular Mergers (368(a)(2)(D) and 368(a)(2)(E))

13

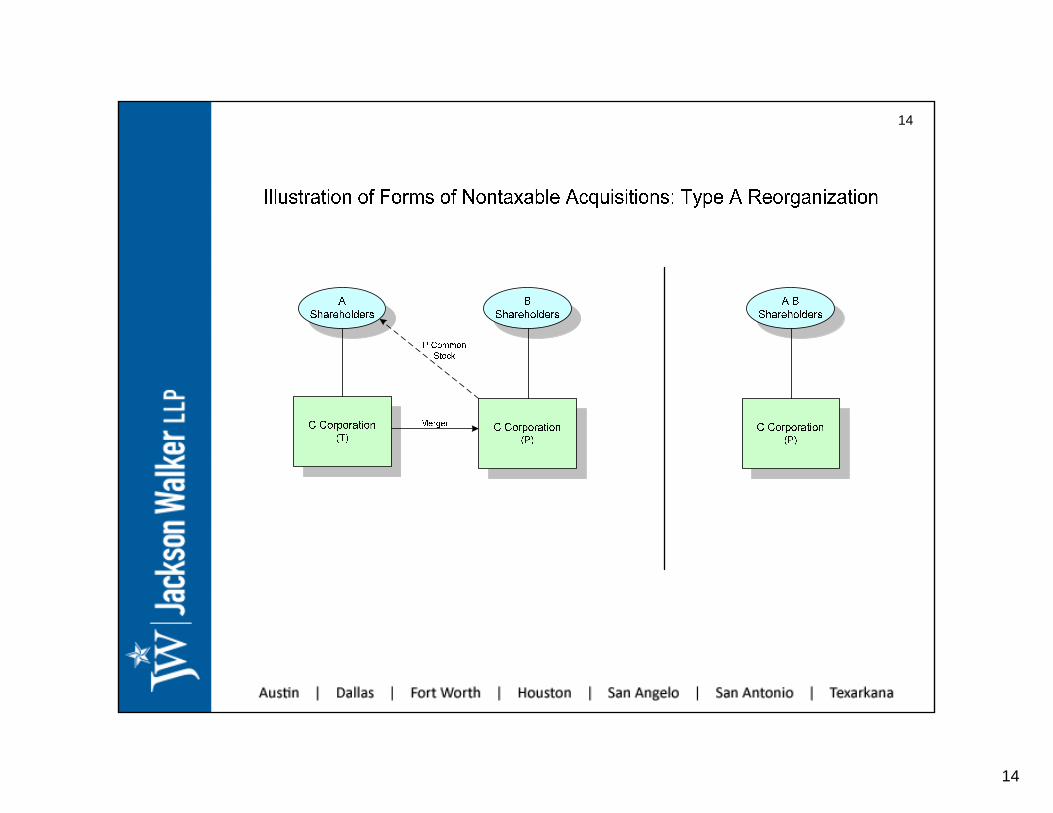

14

14

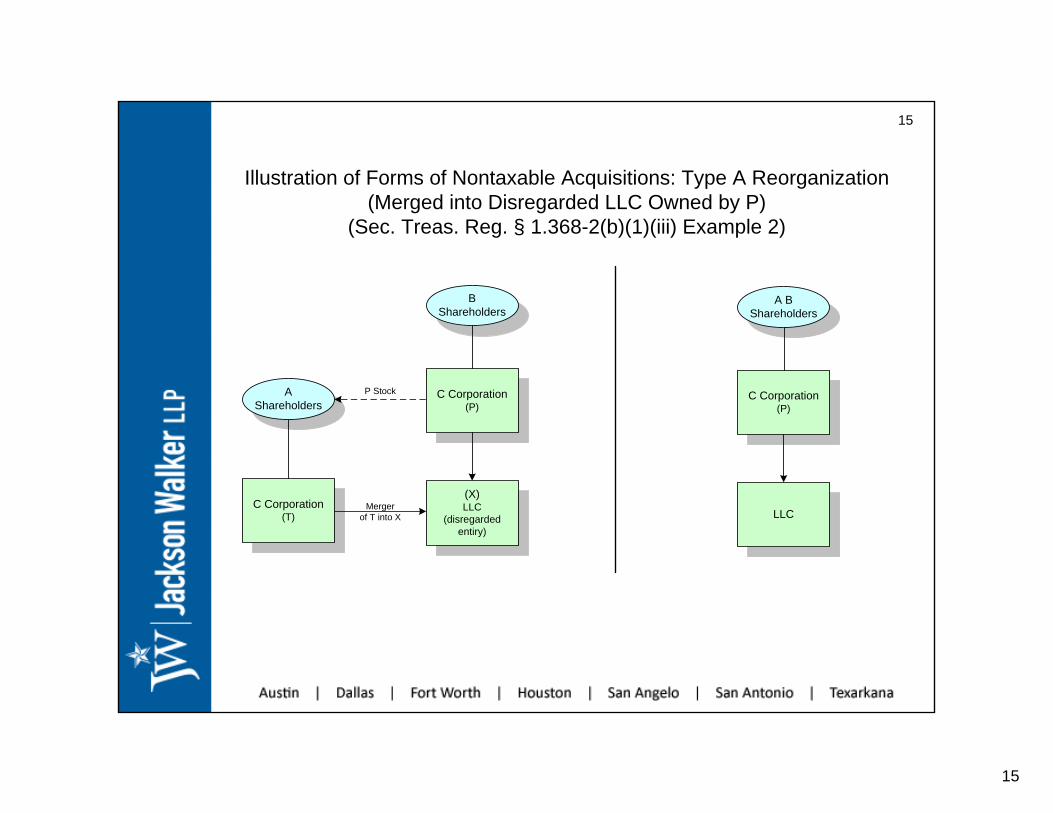

15

Illustration of Forms of Nontaxable Acquisitions: Type A Reorganization (Merged into Disregarded LLC Owned by P)

(Sec. Treas. Reg. § 1.368-2(b)(1)(iii) Example 2)

C Corporation(T)

C Corporation(P)

AShareholders

BShareholders

Mergerof T into X

P Stock

(X)LLC

(disregarded entiry)

C Corporation(P)

A BShareholders

LLC

15

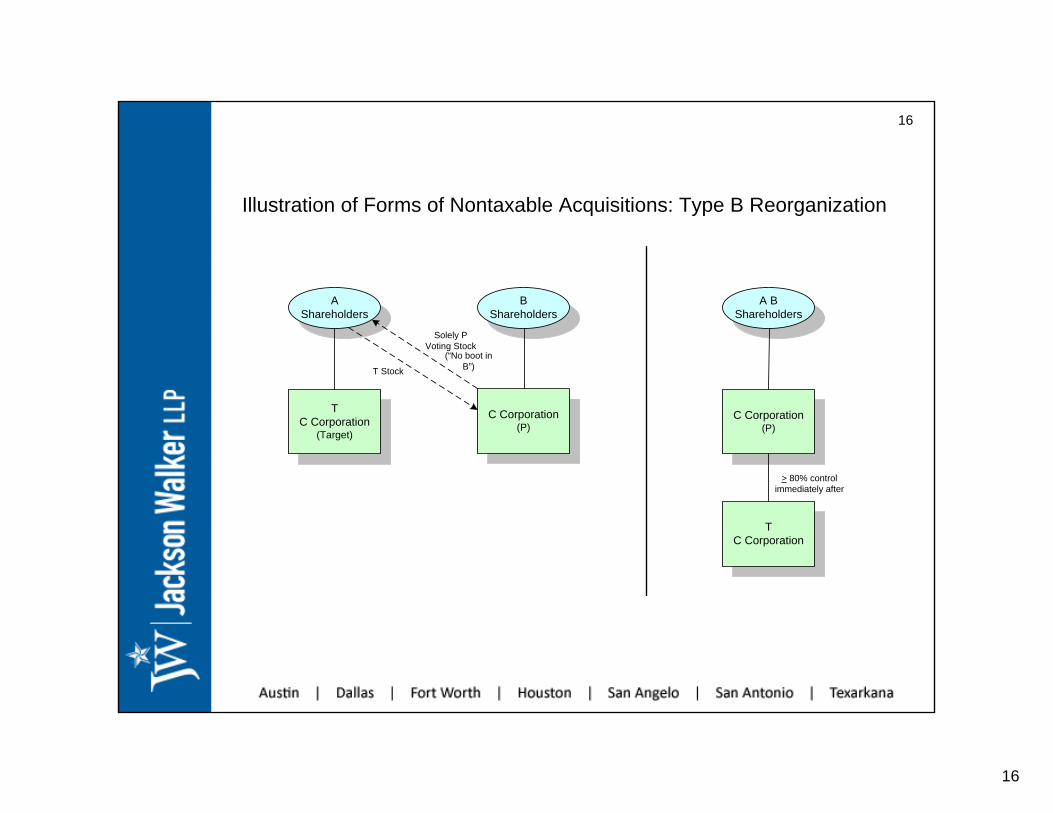

16

Illustration of Forms of Nontaxable Acquisitions: Type B Reorganization

TC Corporation

(Target)

C Corporation(P)

AShareholders

BShareholders

T Stock

Solely P Voting Stock

C Corporation(P)

A BShareholders

(“No boot in B”)

TC Corporation

> 80% control immediately after

16

17

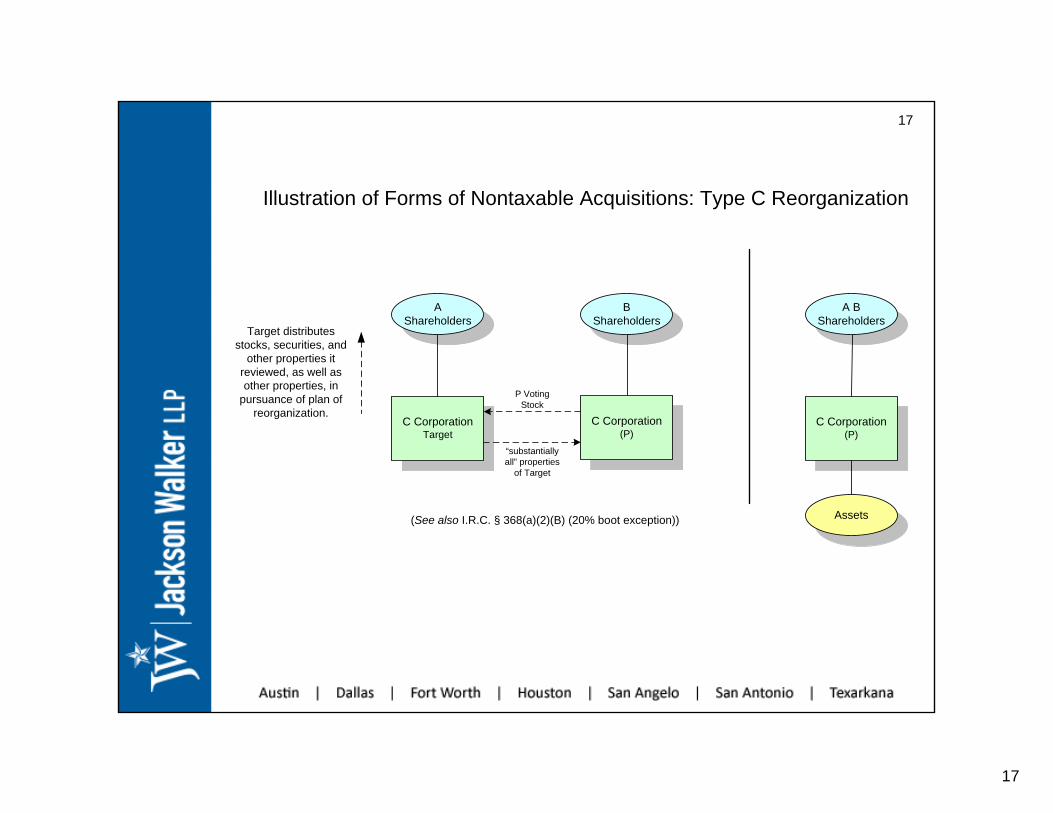

Illustration of Forms of Nontaxable Acquisitions: Type C Reorganization

C CorporationTarget

C Corporation(P)

AShareholders

BShareholders

“substantially all” properties

of Target

P Voting Stock

C Corporation(P)

A BShareholders

Assets(See also I.R.C. § 368(a)(2)(B) (20% boot exception))

Target distributes stocks, securities, and

other properties it reviewed, as well as other properties, in

pursuance of plan of reorganization.

17

18

18

19

19

20

PARTNERSHIPS – SELECTED FORMS OF TAXABLE ACQUISITIONS

21

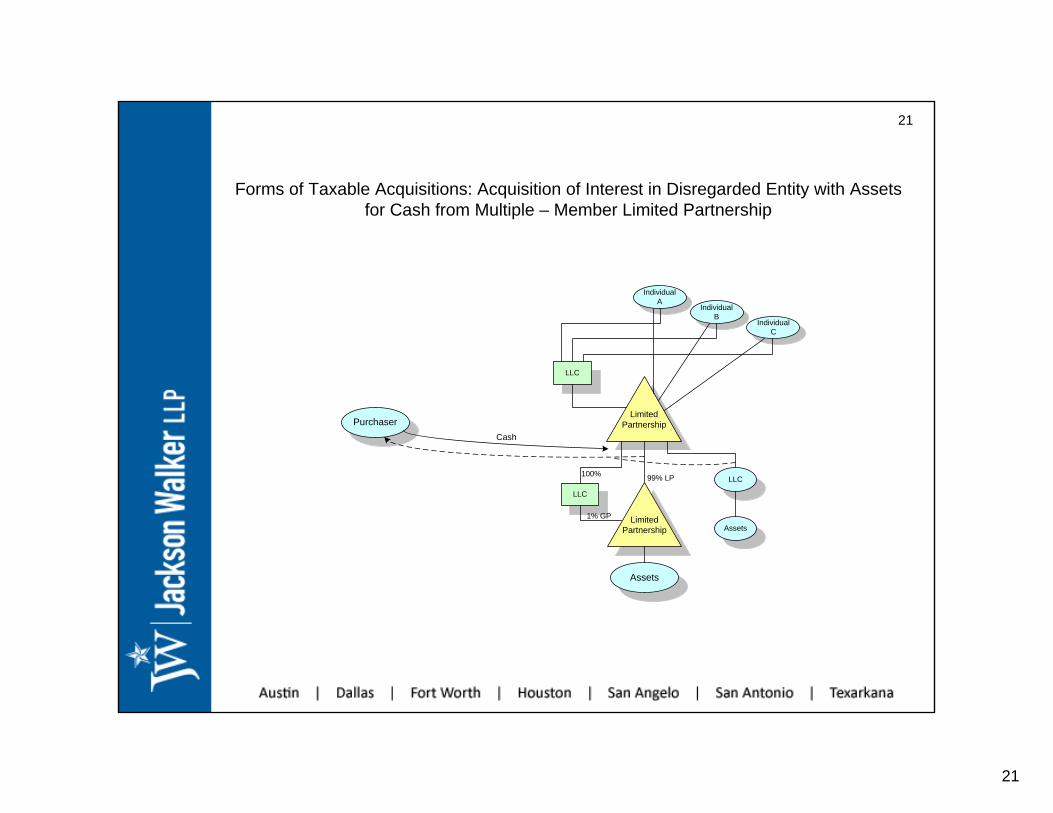

Forms of Taxable Acquisitions: Acquisition of Interest in Disregarded Entity with Assets for Cash from Multiple – Member Limited Partnership

LimitedPartnershipPurchaser

LLC

IndividualA

IndividualB

IndividualC

Cash

LimitedPartnership

Assets

LLC

LLC

Assets

99% LP100%

1% GP

21

22

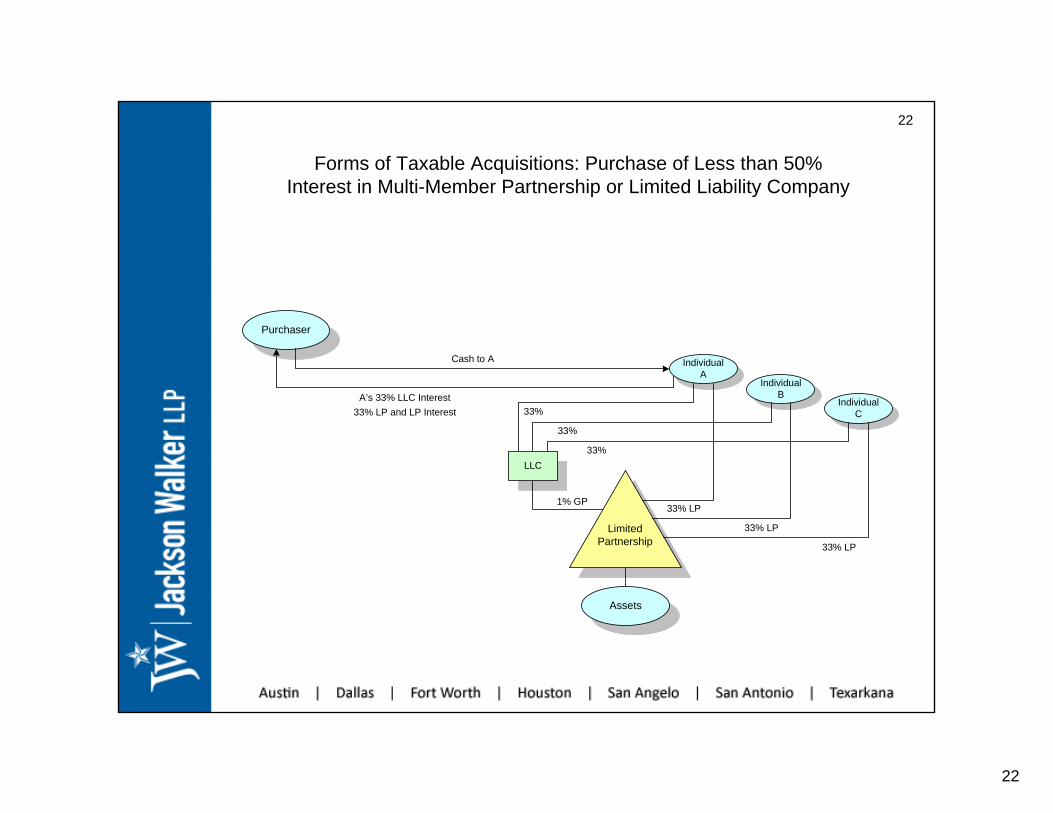

Forms of Taxable Acquisitions: Purchase of Less than 50% Interest in Multi-Member Partnership or Limited Liability Company

LimitedPartnership

Purchaser

LLC

IndividualA

IndividualB

IndividualC

Assets

33% LP

33% LP

33% LP1% GP

33%

33%

33%

33% LP and LP InterestA’s 33% LLC Interest

Cash to A

22

23

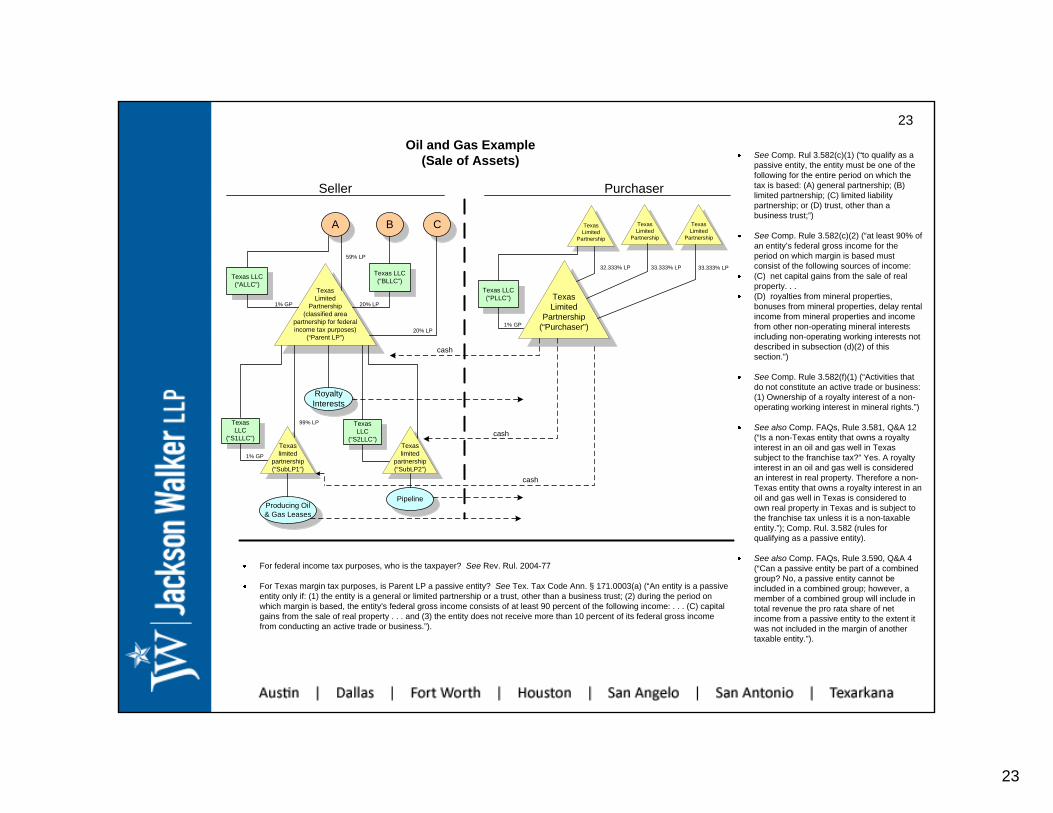

TexasLimited

Partnership(classified area

partnership for federal income tax purposes)

(“Parent LP”)

Texas LLC(“ALLC”)

Texas LLC(“BLLC”)

Texas LLC

(“S1LLC”)

Texas LLC

(“S2LLC”)Texaslimited

partnership(“SubLP1”)

Texaslimited

partnership(“SubLP2”)

PipelineProducing Oil & Gas Leases

Royalty Interests

BA

TexasLimited

Partnership(“Purchaser”)

TexasLimited

Partnership

TexasLimited

Partnership

TexasLimited

Partnership

Texas LLC(“PLLC”)

59% LP

20% LP1% GP

1% GP

99% LP

1% GP

32.333% LP 33.333% LP 33.333% LP

cash

For federal income tax purposes, who is the taxpayer? See Rev. Rul. 2004-77

For Texas margin tax purposes, is Parent LP a passive entity? See Tex. Tax Code Ann. § 171.0003(a) (“An entity is a passive entity only if: (1) the entity is a general or limited partnership or a trust, other than a business trust; (2) during the period on which margin is based, the entity's federal gross income consists of at least 90 percent of the following income: . . . (C) capital gains from the sale of real property . . . and (3) the entity does not receive more than 10 percent of its federal gross income from conducting an active trade or business.”).

Seller Purchaser

Oil and Gas Example(Sale of Assets)

C

20% LP

See Comp. Rul 3.582(c)(1) (“to qualify as a passive entity, the entity must be one of the following for the entire period on which the tax is based: (A) general partnership; (B) limited partnership; (C) limited liability partnership; or (D) trust, other than a business trust;”)

See Comp. Rule 3.582(c)(2) (“at least 90% of an entity’s federal gross income for the period on which margin is based must consist of the following sources of income:(C) net capital gains from the sale of real property. . .(D) royalties from mineral properties, bonuses from mineral properties, delay rental income from mineral properties and income from other non-operating mineral interests including non-operating working interests not described in subsection (d)(2) of this section.”)

See Comp. Rule 3.582(f)(1) (“Activities that do not constitute an active trade or business: (1) Ownership of a royalty interest of a non-operating working interest in mineral rights.”)

See also Comp. FAQs, Rule 3.581, Q&A 12 (“Is a non-Texas entity that owns a royalty interest in an oil and gas well in Texas subject to the franchise tax?” Yes. A royalty interest in an oil and gas well is considered an interest in real property. Therefore a non-Texas entity that owns a royalty interest in an oil and gas well in Texas is considered to own real property in Texas and is subject to the franchise tax unless it is a non-taxable entity.”); Comp. Rul. 3.582 (rules for qualifying as a passive entity).

See also Comp. FAQs, Rule 3.590, Q&A 4 (“Can a passive entity be part of a combined group? No, a passive entity cannot be included in a combined group; however, a member of a combined group will include in total revenue the pro rata share of net income from a passive entity to the extent it was not included in the margin of another taxable entity.”).

cash

cash

23

24

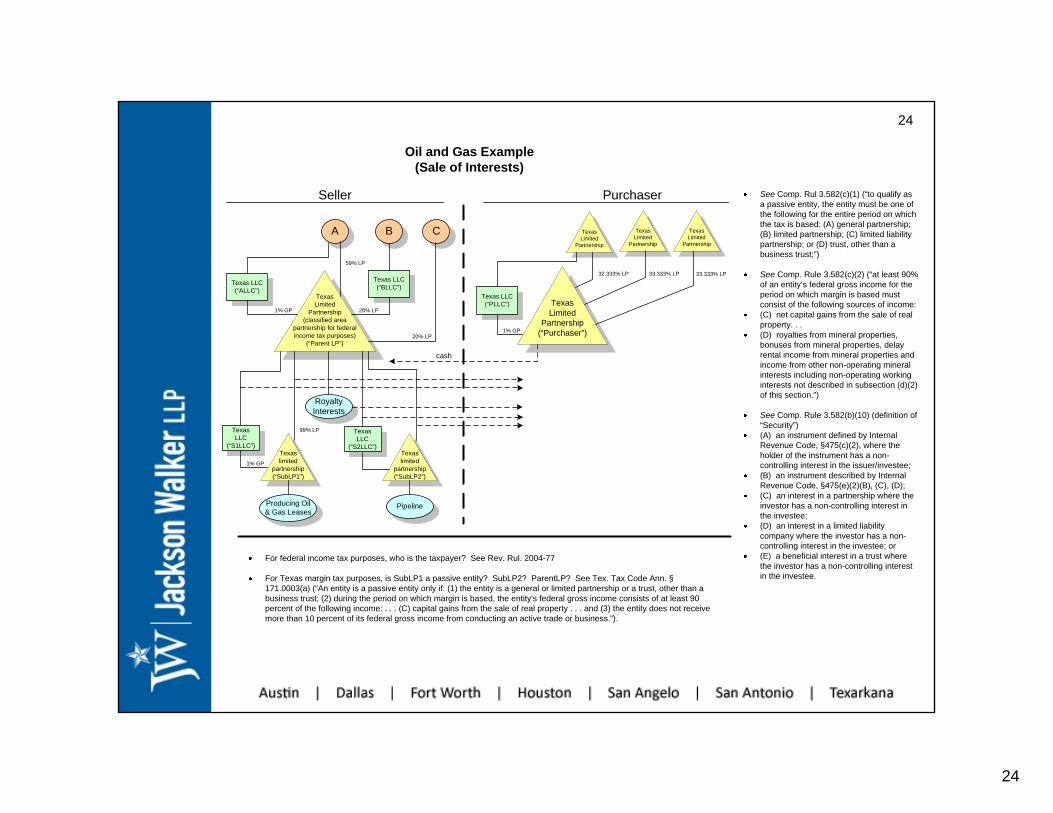

TexasLimited

Partnership(classified area

partnership for federal income tax purposes)

(“Parent LP”)

Texas LLC(“ALLC”)

Texas LLC(“BLLC”)

BA

TexasLimited

Partnership(“Purchaser”)

TexasLimited

Partnership

TexasLimited

Partnership

TexasLimited

Partnership

Texas LLC(“PLLC”)

59% LP

20% LP1% GP

1% GP

32.333% LP 33.333% LP 33.333% LP

cash

For federal income tax purposes, who is the taxpayer? See Rev. Rul. 2004-77

For Texas margin tax purposes, is SubLP1 a passive entity? SubLP2? ParentLP? See Tex. Tax Code Ann. § 171.0003(a) (“An entity is a passive entity only if: (1) the entity is a general or limited partnership or a trust, other than a business trust; (2) during the period on which margin is based, the entity's federal gross income consists of at least 90 percent of the following income: . . . (C) capital gains from the sale of real property . . . and (3) the entity does not receive more than 10 percent of its federal gross income from conducting an active trade or business.”).

Seller Purchaser

Oil and Gas Example(Sale of Interests)

C

20% LP

See Comp. Rul 3.582(c)(1) (“to qualify as a passive entity, the entity must be one of the following for the entire period on which the tax is based: (A) general partnership; (B) limited partnership; (C) limited liability partnership; or (D) trust, other than a business trust;”)

See Comp. Rule 3.582(c)(2) (“at least 90% of an entity’s federal gross income for the period on which margin is based must consist of the following sources of income:(C) net capital gains from the sale of real property. . .(D) royalties from mineral properties, bonuses from mineral properties, delay rental income from mineral properties and income from other non-operating mineral interests including non-operating working interests not described in subsection (d)(2) of this section.”)

See Comp. Rule 3.582(b)(10) (definition of “Security”)(A) an instrument defined by Internal Revenue Code, §475(c)(2), where the holder of the instrument has a non-controlling interest in the issuer/investee;(B) an instrument described by Internal Revenue Code, §475(e)(2)(B), (C), (D);(C) an interest in a partnership where the investor has a non-controlling interest in the investee;(D) an interest in a limited liability company where the investor has a non-controlling interest in the investee; or(E) a beneficial interest in a trust where the investor has a non-controlling interest in the investee.

Texas LLC

(“S1LLC”)

Texas LLC

(“S2LLC”)Texaslimited

partnership(“SubLP1”)

Texaslimited

partnership(“SubLP2”)

PipelineProducing Oil & Gas Leases

Royalty Interests

1% GP

99% LP

24

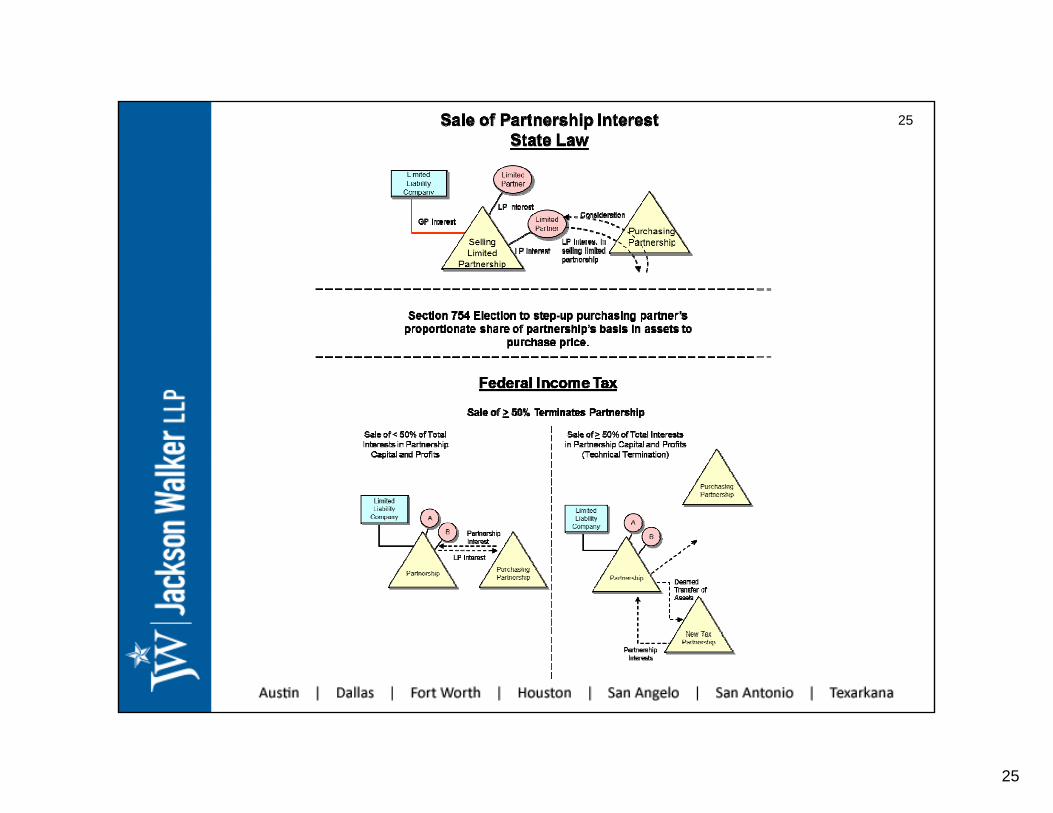

25

25

26

PARTNERSHIPS – SELECTED FORMS OF TAX‐FREE ACQUISITION

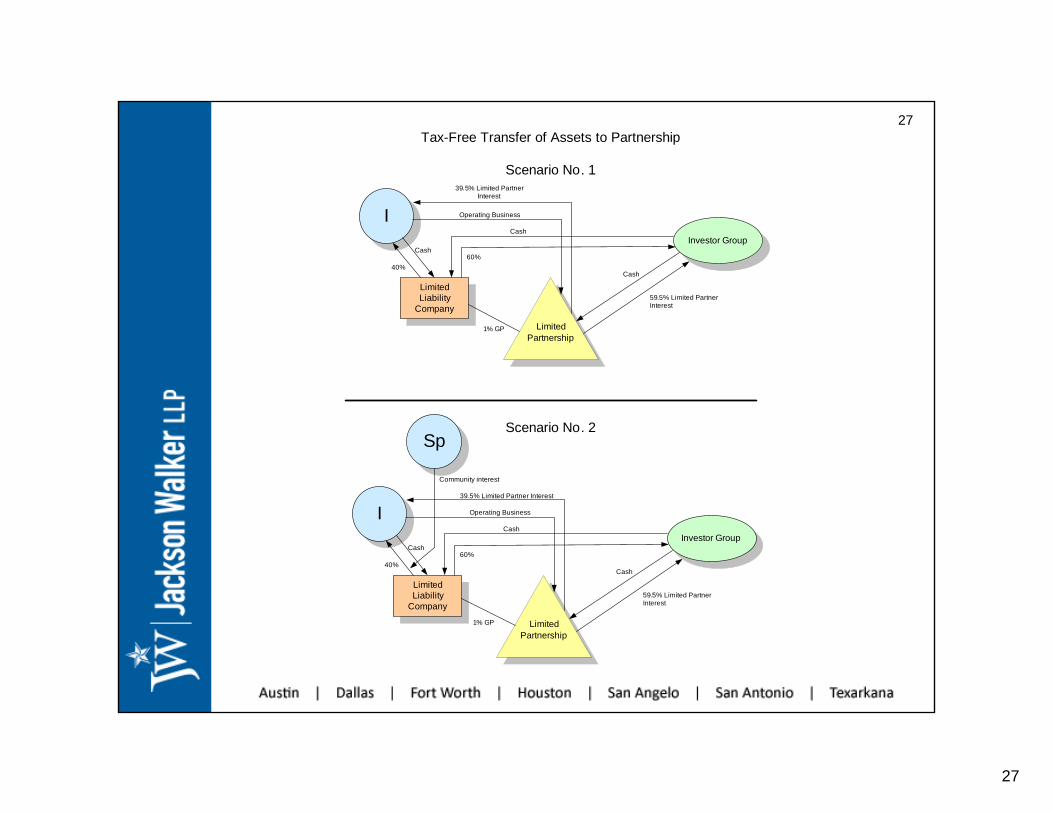

27

I

Tax-Free Transfer of Assets to Partnership

Scenario No. 1

LimitedPartnership

Limited Liability

Company59.5% Limited Partner Interest

39.5% Limited Partner Interest

Operating Business

Cash

Cash

Cash40%

60%

Scenario No. 2

Investor Group

I

LimitedPartnership

Limited Liability

Company59.5% Limited Partner Interest

39.5% Limited Partner Interest

Operating Business

Cash

Cash

Cash40%

60%

Investor Group

1% GP

Sp

Community interest

1% GP

27

28

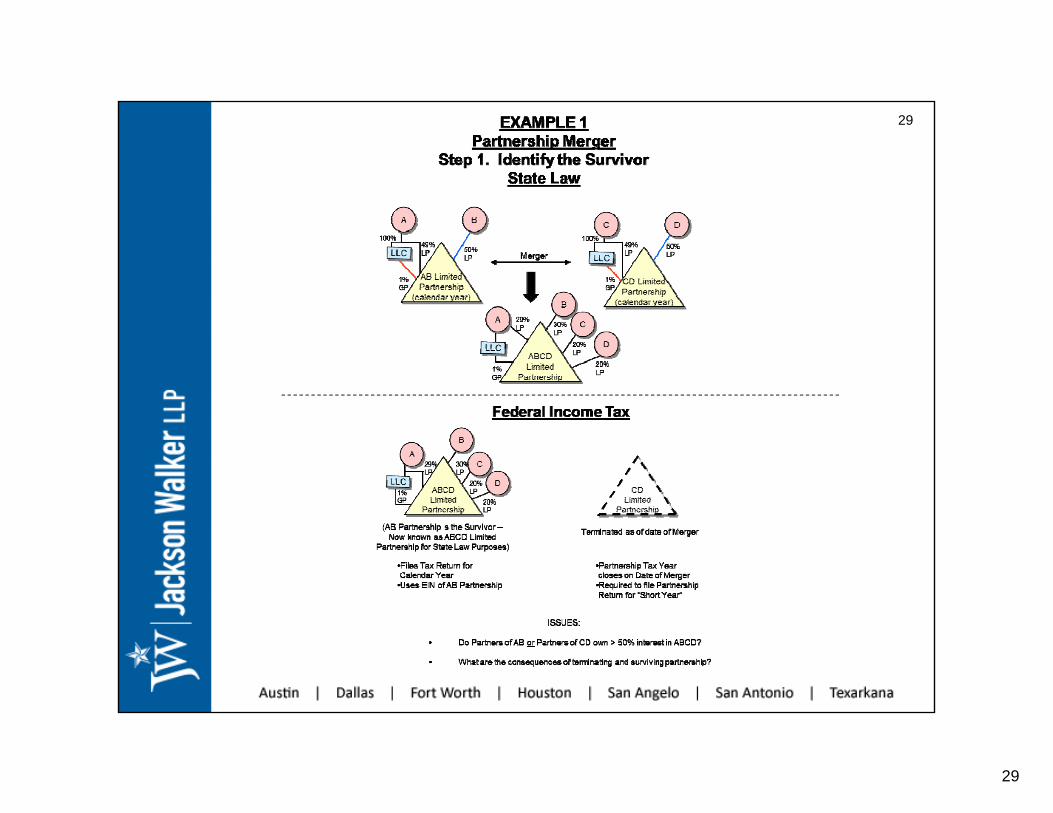

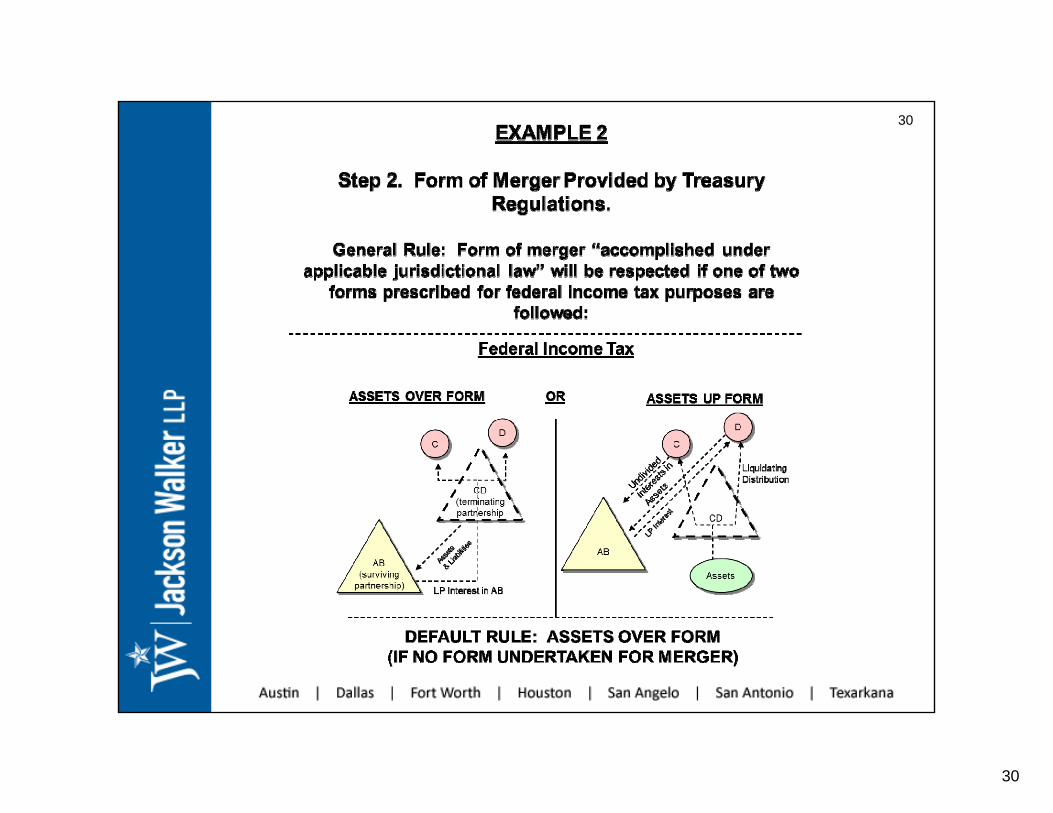

PARTNERSHIP MERGER REGULATIONS

29

29

30

30

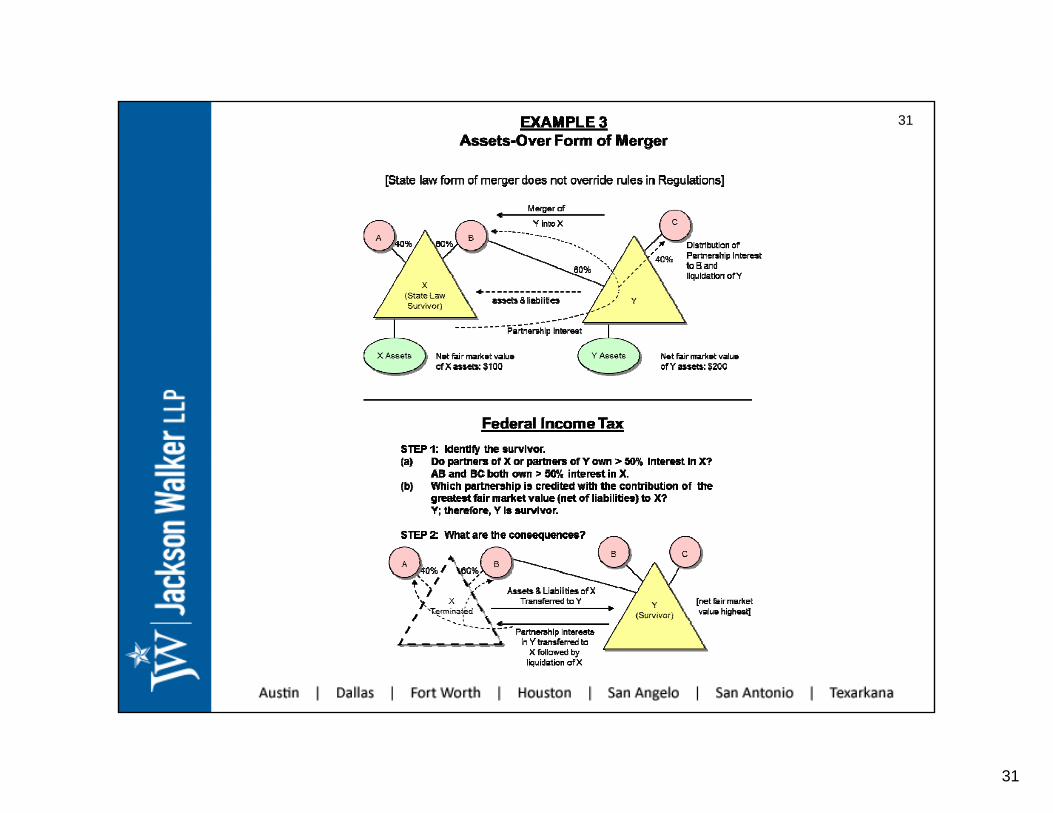

31

31

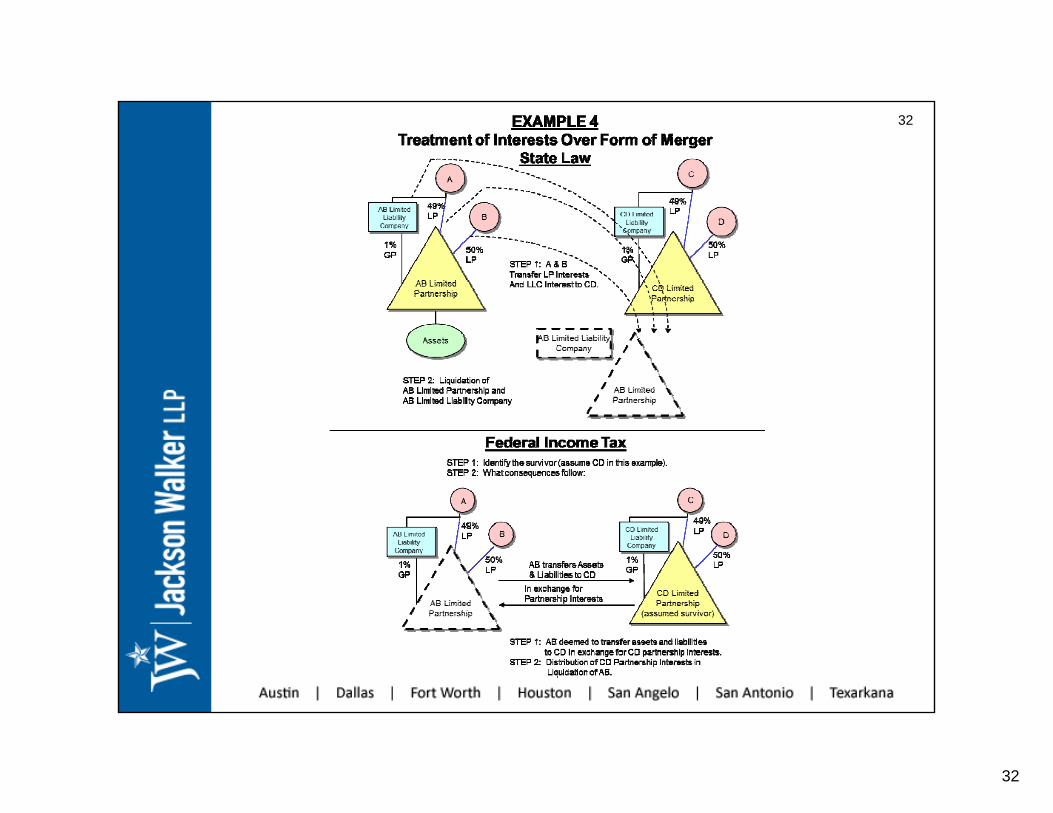

32

32

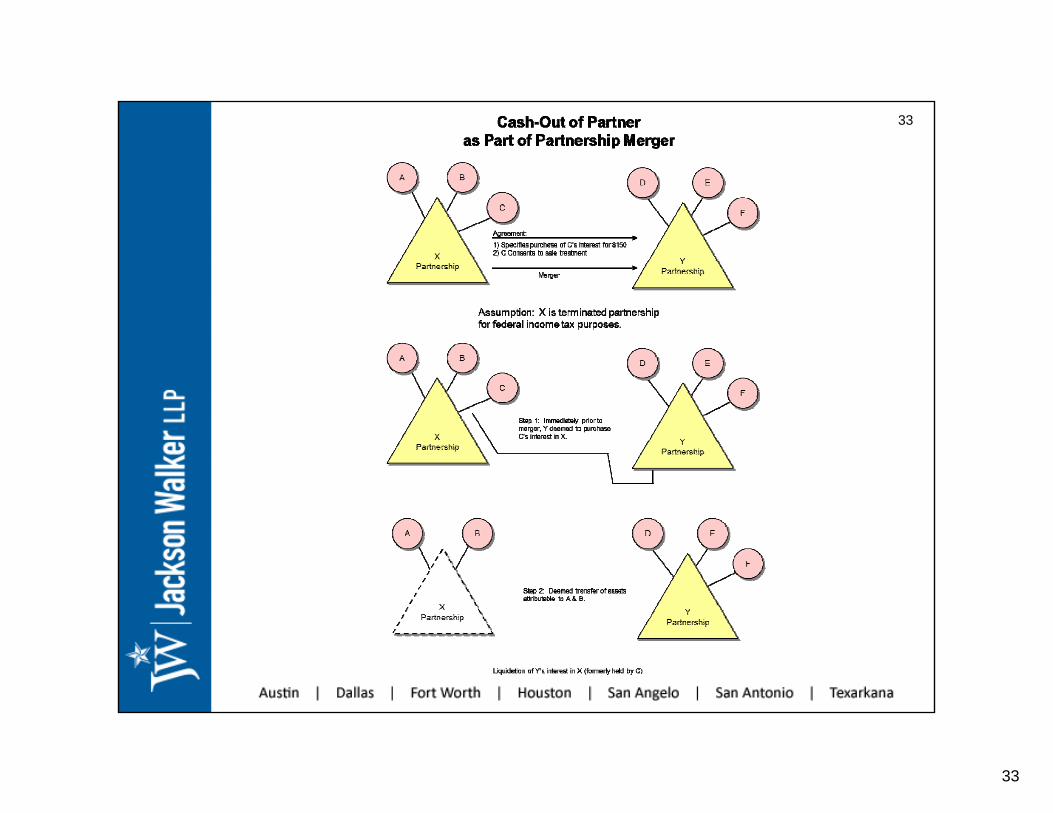

33

33

34

Partnership Division Regulations

• Identify:– Prior Partnership– Resulting Partnership– Divided Partnership– Recipient Partnership

34

35

Partnership Division Regulations

• In the division of a partnership into two or more partnership, the resulting partnerships (other than any resulting partnership the members of which had an interest of 50‐percent or less in the capital and profits of the prior partnership) are considered a continuation of the prior partnership. Any other resulting partnership is not considered a continuation of the prior partnership but is considered a new partnership.

• If none of the members of the resulting partnership owned an interest of more than 50‐percent in the capital and profits of the prior partnership, the prior partnership is terminated.

• Where members of a partnership that has been divided do not become members of a resulting partnership that is considered a continuation of the prior partnership, such partner’s interest is considered liquidated as of the date of the division.

35

36

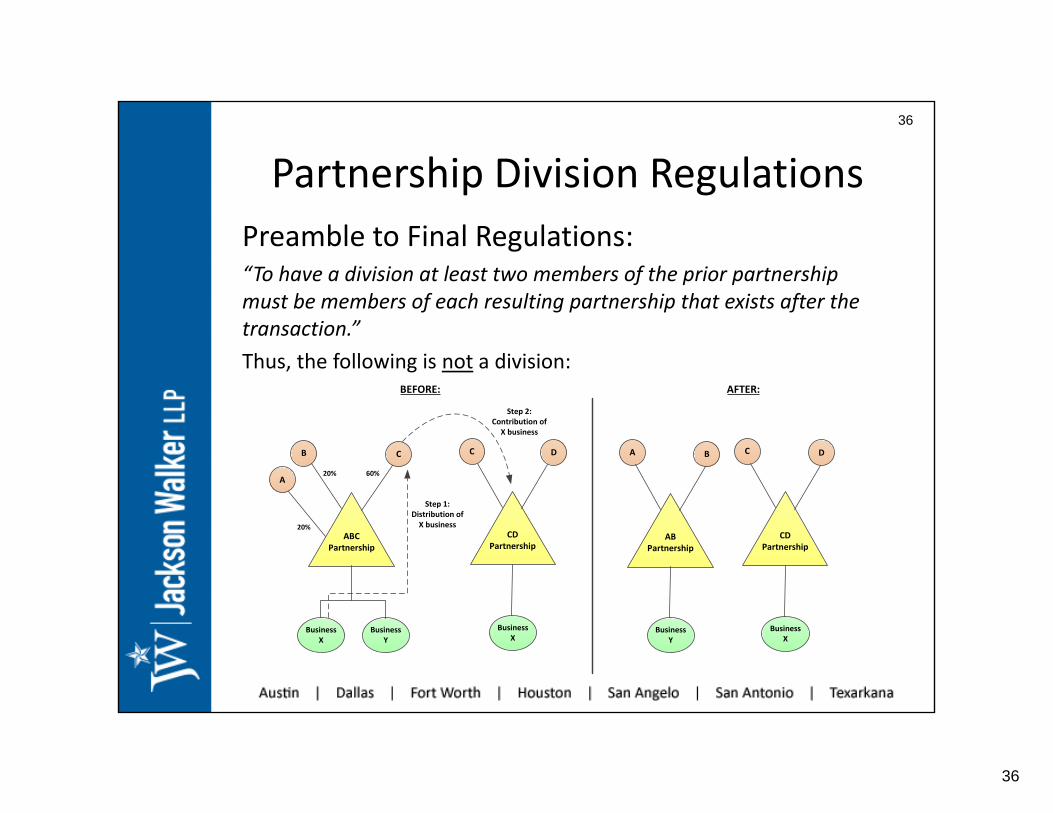

Partnership Division RegulationsPreamble to Final Regulations:“To have a division at least two members of the prior partnership must be members of each resulting partnership that exists after the transaction.”Thus, the following is not a division:

ABCPartnership

BusinessX

BusinessY

A

B C

20%

20% 60%

Step 1: Distribution of X business

CDPartnership

BusinessX

C D

Step 2: Contribution of

X business

ABPartnership

BusinessY

A B

CDPartnership

BusinessX

C D

AFTER:BEFORE:

36

37

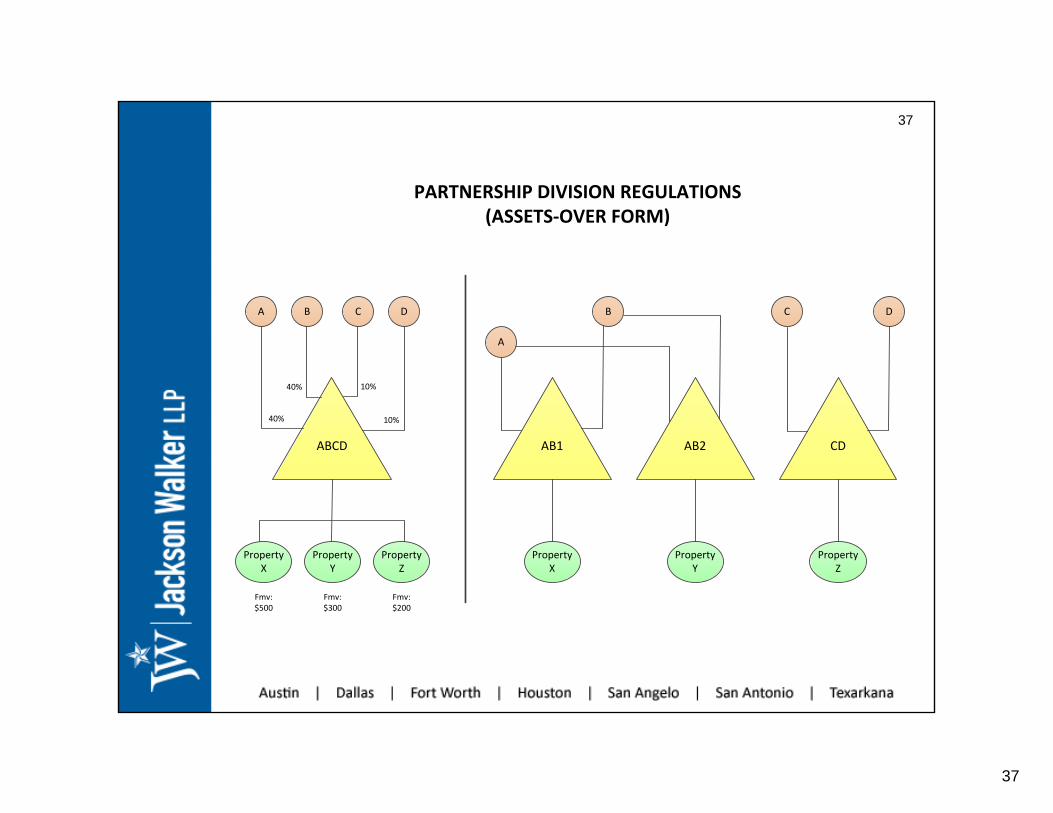

ABCD

PropertyX

PropertyY

PropertyZ

A B C D

40%

40% 10%

10%

AB1 AB2 CD

PropertyX

PropertyY

PropertyZ

A

B C D

PARTNERSHIP DIVISION REGULATIONS(ASSETS‐OVER FORM)

Fmv: $500

Fmv: $300

Fmv: $200

37

38

Multi‐State Considerations

39

COMMOM M&A SALT CONSIDERATIONS

40

Premise – Representation 1

“Seller is qualified to do business in each state in which either the ownership or use of the properties owned or used by it or the nature of the activities conducted by it require such qualification.”

Common Sources: Loan CovenantAsset Purchase AgreementOpinion Letter

40

41

Premise – Representation 2

“Seller has filed or caused to be filed all tax returns that are or were required to be filed pursuant to applicable law.”

Common Sources: Asset Purchase Agreement

41

42

Sources of Scrutiny

• Secretary of State oversight• State Revenue Department oversight• Contractual requirements• GAAP and financial audit oversight

42

43

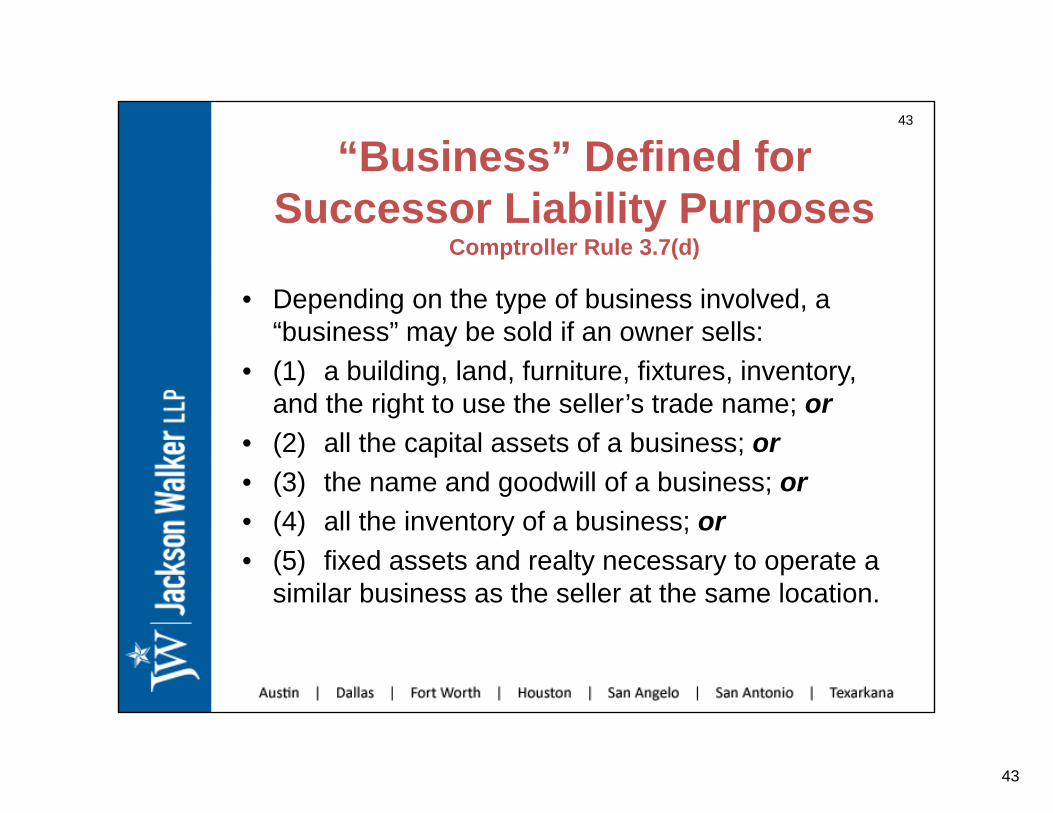

“Business” Defined forSuccessor Liability Purposes

Comptroller Rule 3.7(d)

• Depending on the type of business involved, a “business” may be sold if an owner sells:

• (1) a building, land, furniture, fixtures, inventory, and the right to use the seller’s trade name; or

• (2) all the capital assets of a business; or• (3) the name and goodwill of a business; or• (4) all the inventory of a business; or• (5) fixed assets and realty necessary to operate a

similar business as the seller at the same location.

43

44

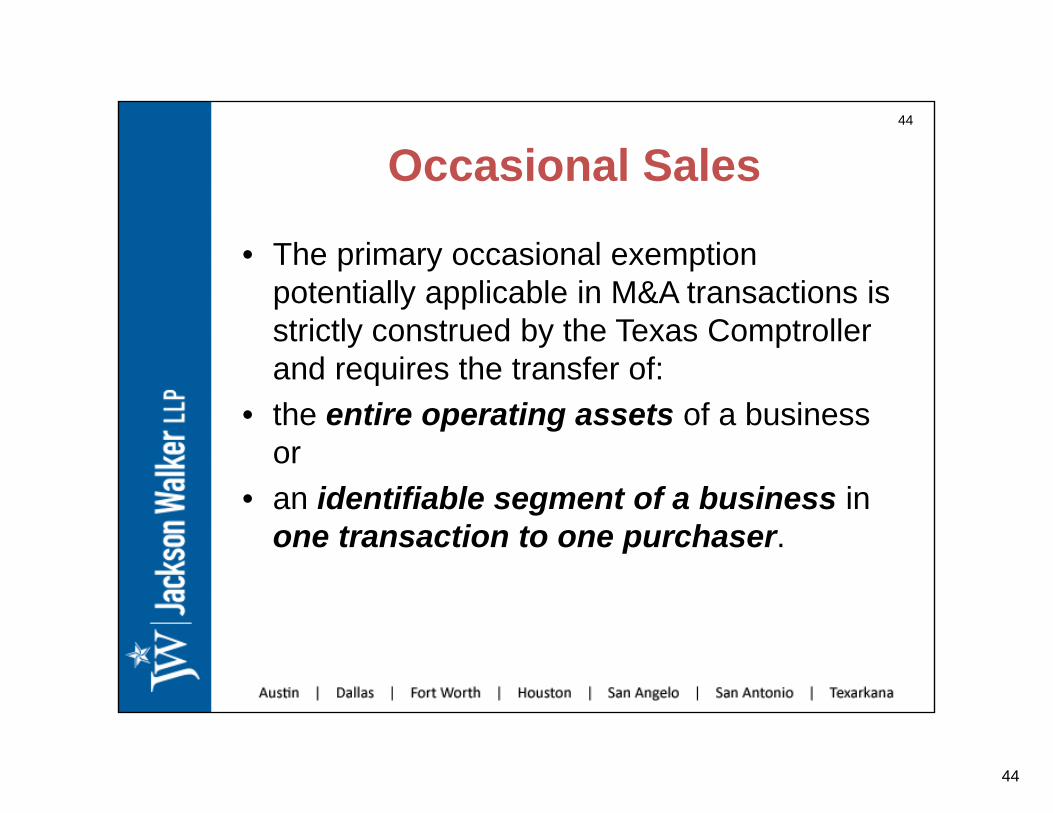

Occasional Sales

• The primary occasional exemption potentially applicable in M&A transactions is strictly construed by the Texas Comptroller and requires the transfer of:

• the entire operating assets of a business or

• an identifiable segment of a business in one transaction to one purchaser.

44

45

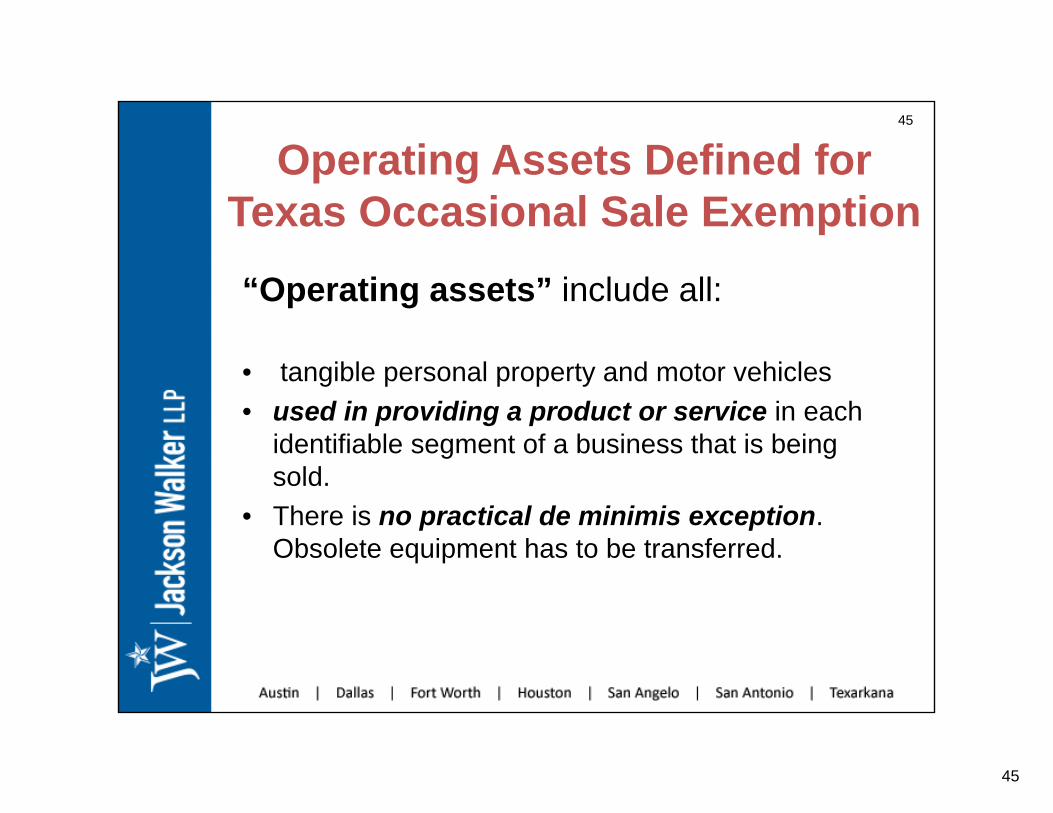

Operating Assets Defined for Texas Occasional Sale Exemption“Operating assets” include all:

• tangible personal property and motor vehicles • used in providing a product or service in each

identifiable segment of a business that is being sold.

• There is no practical de minimis exception. Obsolete equipment has to be transferred.

45

46

Motor Vehicles

• Licensed motor vehicles can be “operating assets” that if not transferred destroy the occasional sale exemption.

• But, even if they are transferred in an exempt occasional sale they will almost always be subject to the Texas motor vehicle tax.

46

47

Franchise Tax Apportionment

• Need to understand “location of payor” rule• If there is gain on the sale of a business, the

seller care where the gain is “apportioned” for purposes of the Texas franchise tax.

• In an asset sale gain on the sale of minerals, real estate, or tangible personal property is apportioned based on the physical location of the property

47

48

Location of Payor

• Gain on the sale of intangible (i.e., LLC membership interests, stock, or goodwill is apportioned based on the Texas Comptroller’s “location of payor” rules.

• The location of payor of an LLC or Corp. is the “legal domicile” of the payor = charter state.

• The location of payor of an partnership is the principal place of business of the partnership.

48

49

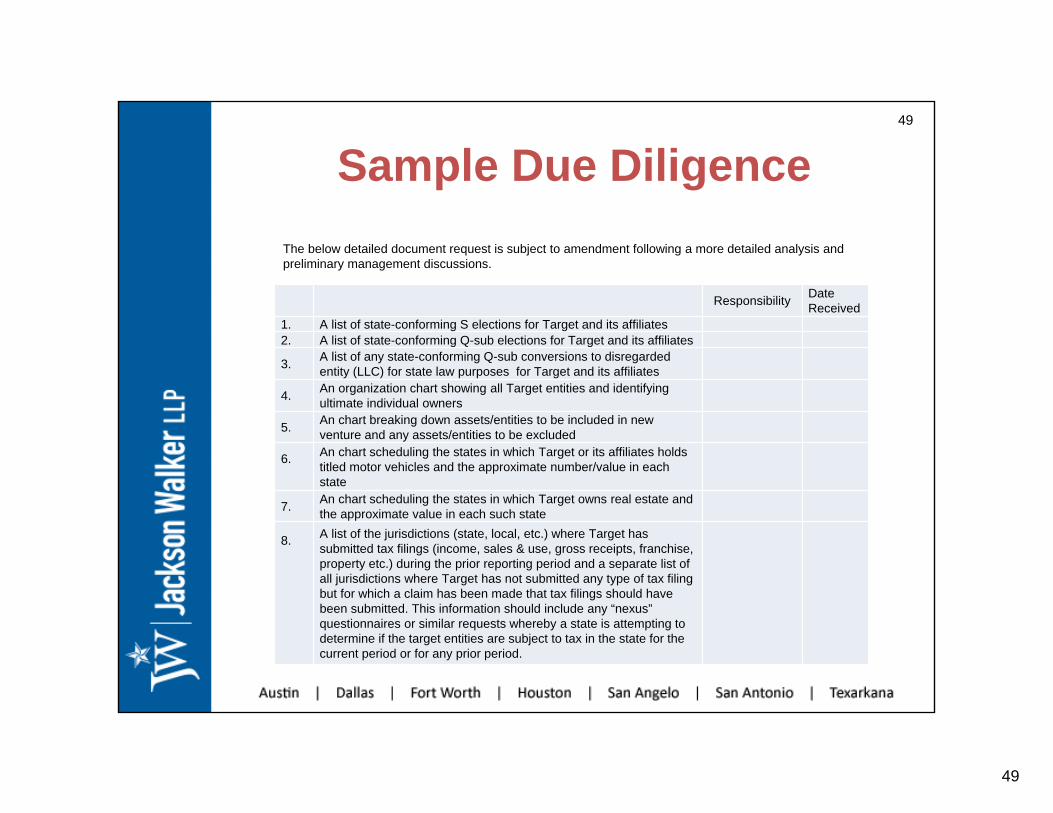

Sample Due DiligenceThe below detailed document request is subject to amendment following a more detailed analysis and preliminary management discussions.

Responsibility Date Received

1. A list of state-conforming S elections for Target and its affiliates2. A list of state-conforming Q-sub elections for Target and its affiliates

3. A list of any state-conforming Q-sub conversions to disregarded entity (LLC) for state law purposes for Target and its affiliates

4. An organization chart showing all Target entities and identifying ultimate individual owners

5. An chart breaking down assets/entities to be included in new venture and any assets/entities to be excluded

6. An chart scheduling the states in which Target or its affiliates holds titled motor vehicles and the approximate number/value in each state

7. An chart scheduling the states in which Target owns real estate and the approximate value in each such state

8. A list of the jurisdictions (state, local, etc.) where Target has submitted tax filings (income, sales & use, gross receipts, franchise, property etc.) during the prior reporting period and a separate list of all jurisdictions where Target has not submitted any type of tax filing but for which a claim has been made that tax filings should have been submitted. This information should include any “nexus” questionnaires or similar requests whereby a state is attempting to determine if the target entities are subject to tax in the state for the current period or for any prior period.

49

50

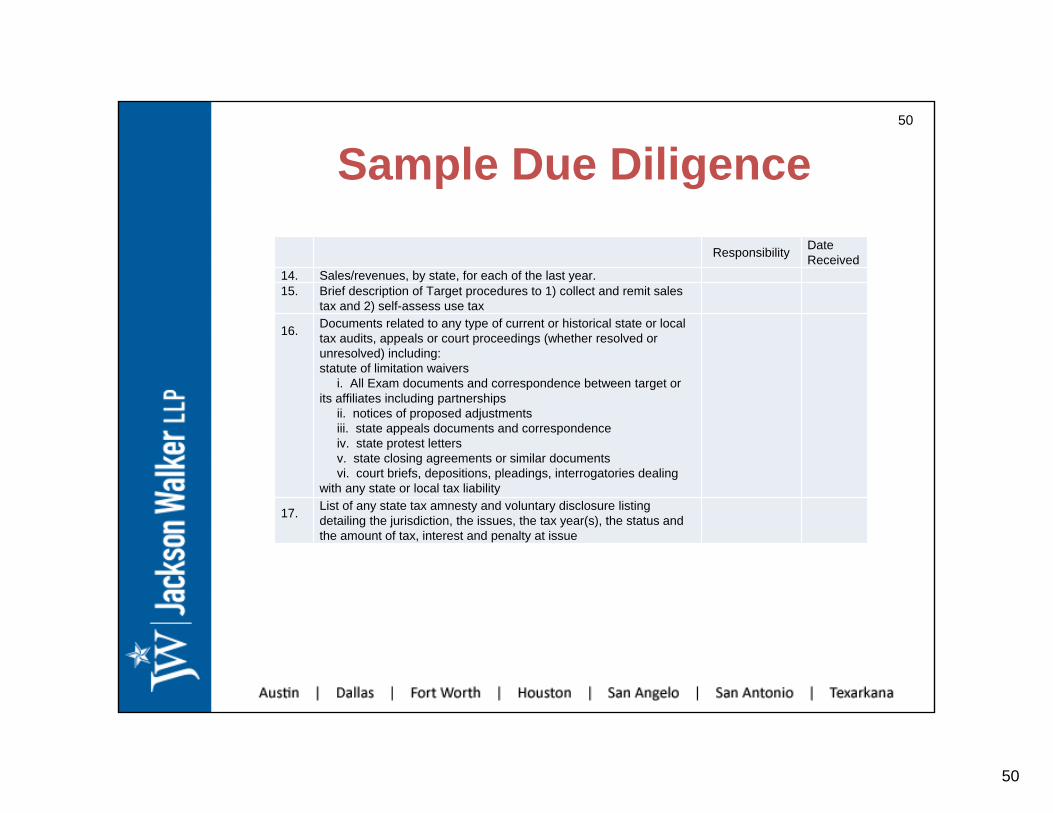

Sample Due DiligenceResponsibility Date

Received14. Sales/revenues, by state, for each of the last year.15. Brief description of Target procedures to 1) collect and remit sales

tax and 2) self-assess use tax

16. Documents related to any type of current or historical state or local tax audits, appeals or court proceedings (whether resolved or unresolved) including:statute of limitation waivers

i. All Exam documents and correspondence between target or its affiliates including partnerships

ii. notices of proposed adjustmentsiii. state appeals documents and correspondence iv. state protest lettersv. state closing agreements or similar documentsvi. court briefs, depositions, pleadings, interrogatories dealing

with any state or local tax liability

17. List of any state tax amnesty and voluntary disclosure listing detailing the jurisdiction, the issues, the tax year(s), the status and the amount of tax, interest and penalty at issue

50

51

Real Estate Transfer Tax / Conduit Entities

Some states impose real estate transfer tax on the transfer of an LLC interest.

For example (not an exhaustive list):

South Carolina has a conduit ruling for transfers of interests in single member LLCs that are disregarded for federal income tax purposes. See SC revenue ruling 15-3. The current South Carolina real estate transfer tax rate is $1.85 for every $500 of the transferred property's value (e.g., a $10 million property would incur a tax of $37,000).

Connecticut applies real estate transfer tax to direct or indirect transfers of greater than 50% interest.

California has some local jurisdictions including San Francisco and Los Angeles County that impose real estate transfer taxes on certain transfers of entity interests.

Florida imposes a .7% tax on the consideration paid for the transfer of an interest in real estate (i.e. a deed). Florida also imposes a .35% tax on the amount of indebtedness secured by a mortgage. Therefore, the total tax rate is potentially 1.05%.

Florida extends its real estate transfer tax to sales of “conduit entities” defined as follows:

“Conduit entity” means a legal entity to which real property is conveyed without full consideration by a grantor who owns a direct or indirect interest in the entity, or a successor entity. Fla. Stat. § 201.02.

The conduit entity tax applies when real property is conveyed to a conduit entity and all or a portion of the grantor's direct or indirect ownership interest in the conduit entity is subsequently transferred for consideration within 3 years of such conveyance.

51

52

Case Study 4

Economic Nexus: The Next Wave States are asserting income tax nexus in

spite of 86-272 when businesses have economic presence from:

1) intellectual property2) material sales (E.g., California if >

$547K in annual sales or 25% of sales)3) other standards

52

53

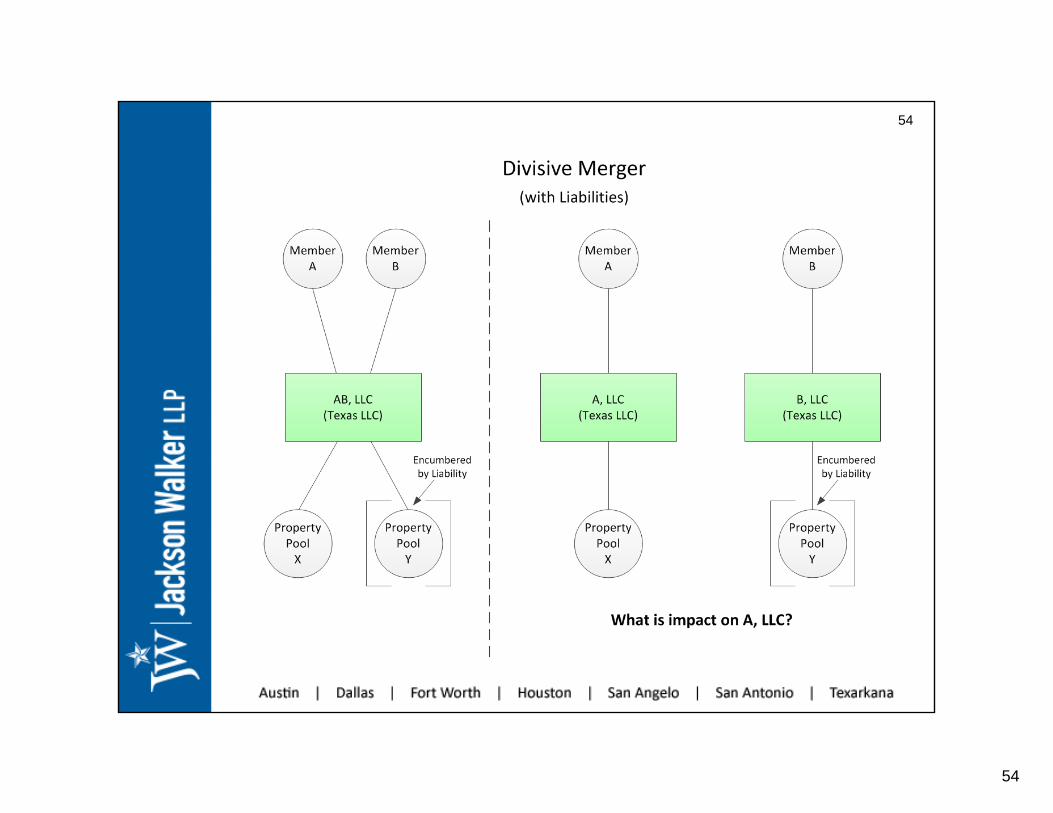

53

54

54

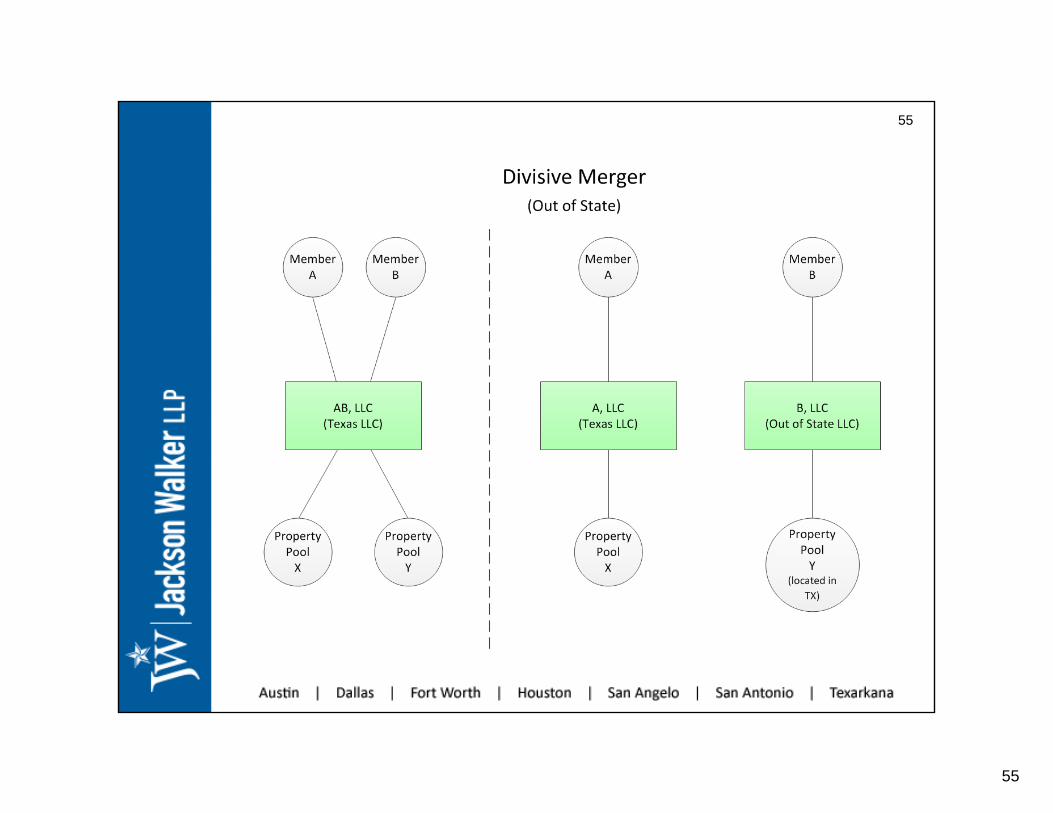

55

55

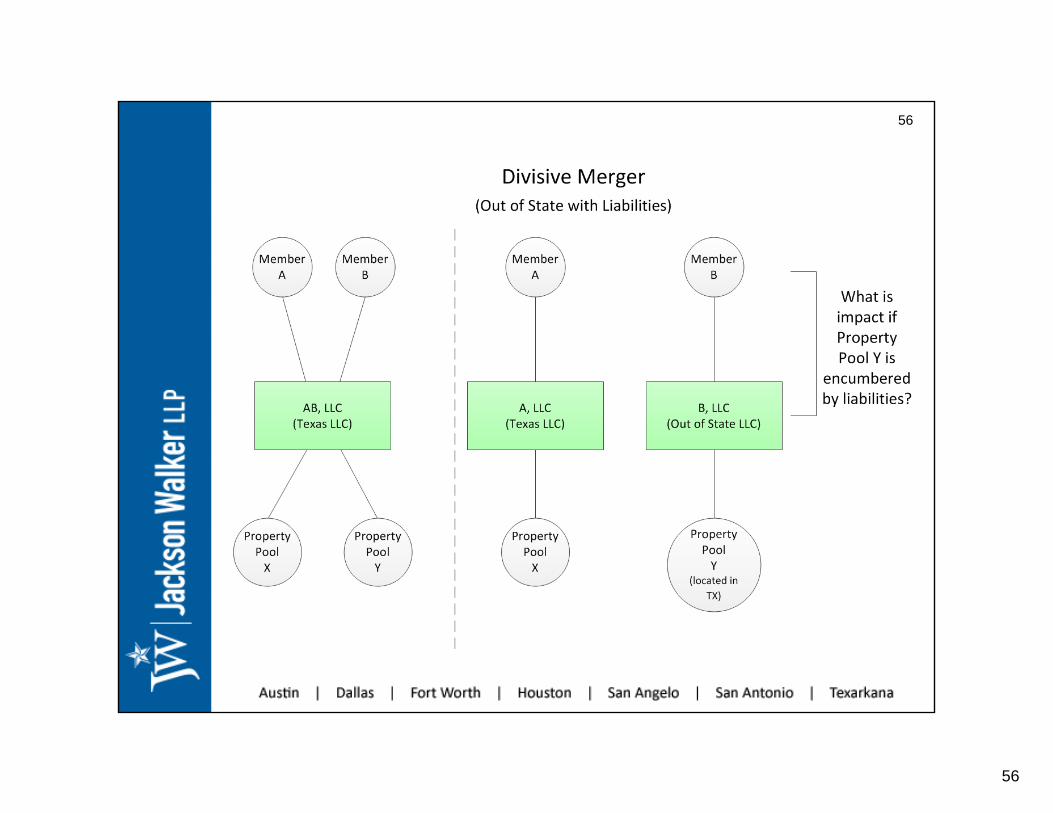

56

56

57

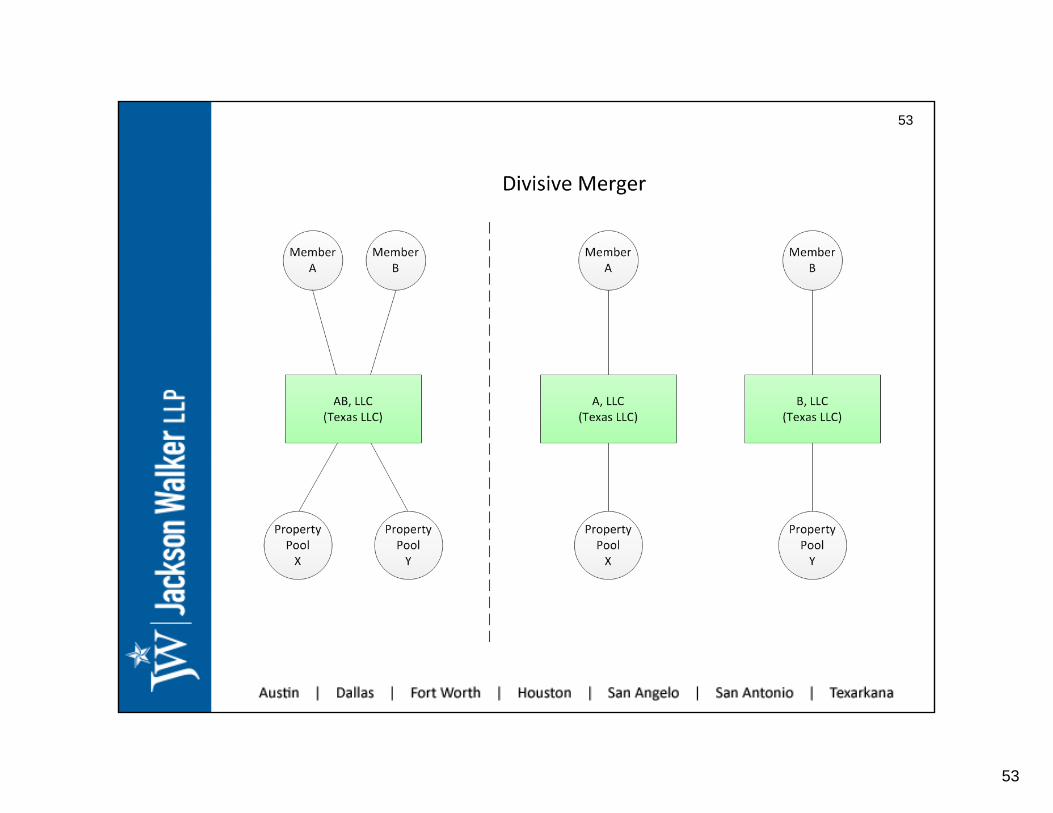

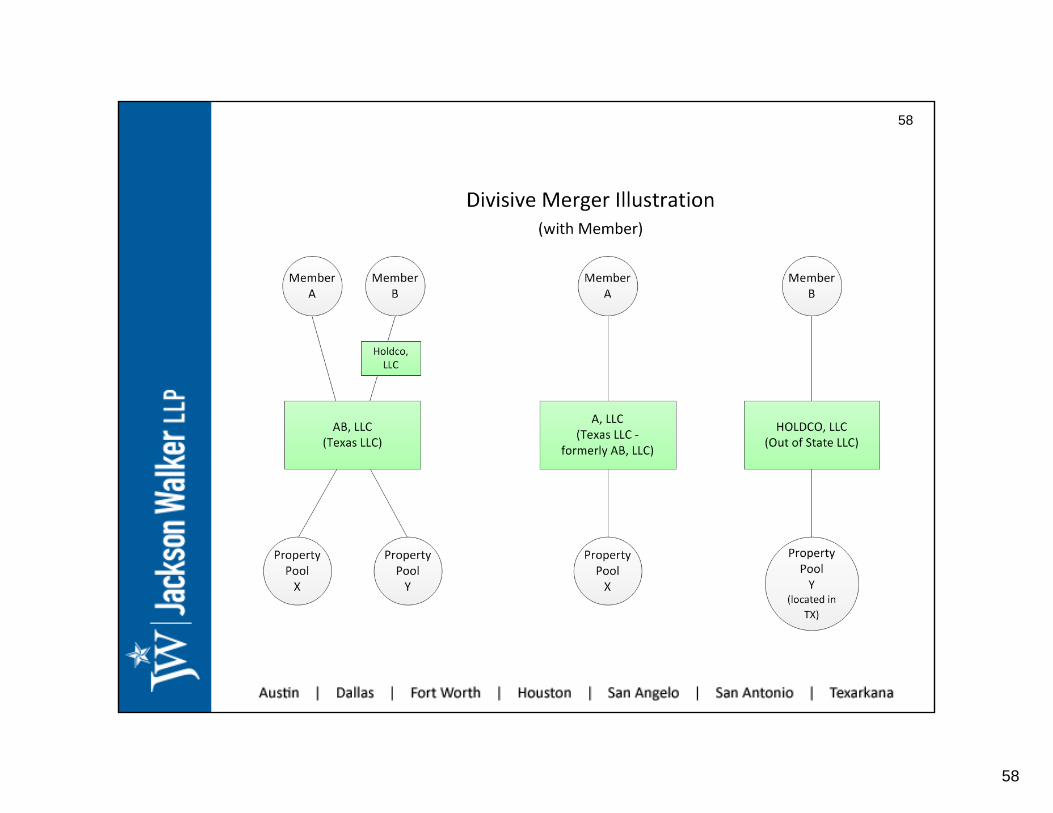

SELECTED DIVISIVE MERGER ILLUSTRATIONS

58

58