Embed Size (px)

Citation preview

1

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])2016

Supreme audit institutions’ contribution to good governanceDomokos–Pulay–Pályi–Németh–Mészáros

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

S������ ����� ������������’ ������������ �� ���� ����������Domokos–Pulay–Pályi–Németh–Mészáros

1

2016

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

C����������� �� S��������� G��� G���������T�� C������������� S�����, M������� ��� I����������� �� ��� S���� A���� O����� �� H������

Domokos–Mészáros–Szakács

2

2016

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

C����������� �� ��� S���� A���� O����� �� H������ �� ��� Q������ �� ��� L����������Mészáros–Nagy–Domokos–Gergely–Posta–Fülöp

3

2016

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

1

A���� ��� ��� U���������� �� A������� Domokos–Renkó–Gál–Pálmai

4

2016

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

5

T����������� �� P����� F������ M��������� S���� A���� O����� �� H������ �� �� I������������ G�������� �� T�����������

Horváth–Németh–Domokos

2016

E����������� ��� C������ �� I�������� �� ��� H�������� P����� S�����Domokos–Pulay–Szatmári–Gergely–Szabó

6

2016

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

7

G������� B����� S������������� T�� R��� �� ��� S���� A���� O����� �� H������ �� P������� ��� E�������� �� ��� B�����

Domokos–Pulay–Pető–Pongrácz

2016

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

8

S��������� G��� G��������� �� A���� P�������Jakovác–Domokos–Németh

2016

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

V���� C������� ��� C�����������R������ �� O����������� ��� O�������� �� ��� S���� A���� O����� �� H������

Domokos–Pályi–Farkasinszki

9

2016

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

10

S��������� ��� E������������ �� G��������� E��������� ������� ��� ����������� ����������� �� SAI'� �����

Domokos–Németh–Jakovác

2016

Pillars of Good Governance – Focus on State Audit Office of Hungary as a Supreme Audit InstitutionStudy Series

"With its findings, recommendations and advice based on its audit experience, the State Audit Office of Hungary assists the National Assembly, its committees and the work of the audited entities, thus facilitating well-governed state operations." (Act on SAO, §1[4])

R������ �� P����� M���������C������������ �� S���� A���� O����� �� H������ �� ��������� C�������� G��������� �� S����-����� E����������

Domokos–Várpalotai–Jakovác–Németh–Makkai–Horváth

11

2016

Individual Studies:

Supreme audit institutions’ contribution

to good governance

KEYWORDS: good governance, UN, INTOSAI, OECD, indicators, supreme audit institutions,

audit, independence, legality, transparency, accountability, integrity, financial sustainability, effectiveness, efficiency, “Hungarian model”

PIllARS Of GOOD GOvERNANCE – fOCUS ON STATE AUDIT OffICE Of HUNGARY AS A SUPREmE AUDIT INSTITUTION

Study Series

4

S t u d y S e r I e S S t u d y S e r I e S

edItOr:

ErzsébEt NémEth PhD supervisory manager

AutHOrS:

LászLó Domokos president

GyuLa PuLay PhD supervisory manager

kataLiN PáLyi auditor counsellor

ErzsébEt NémEth PhD supervisory manager

LEiLa mészáros J.D. auditor counsellor

PublISHed by tHe StAte AudIt OffIce Of HungAry

ISbn 978-615-5222-11-5

PiLLars of GooD GovErNaNcE – focus oN statE auDit

officE of huNGary as a suPrEmE auDit iNstitutioN

tHe IndIvIduAl StudIeS Are AvAIlAble tHrOugH tHe webSIte Of SAO

At https://www.asz.hu/en/pillars-of-good-governance

S t u d y S e r I e S

5

S t u d y S e r I e S

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2 the concept of good governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2.1 good governance and the failure of the neo-liberal school . . . . . . . . . . . . . . . . . . . . . . . 7

2.2 good government . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

2.3 A new interpretation emerging from the reinforced role of the state . . . . . . . . . . . . . . 9

2.4 Principles proposed by international organisations . . . . . . . . . . . . . . . . . . . . . . . . . . . .10

2.5 the modern concept and theoretical model of good governance . . . . . . . . . . . . . . . .10

2.6 Measuring the performance of government . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

3 contribution of SAIs to good governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

3.1 resolutions of the united nations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

3.2 IntOSAI documents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

3.3 the Oecd’s approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

4 contribution of SAO to good governance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

4.1 the role of the State Audit Office in good governance – “the Hungarian model” . . .19

4.1.1 first level: foundations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

4.1.2 Second level: fundamental principles and goals . . . . . . . . . . . . . . . . . . . . . . . . . .20

4.1.3 third level: instruments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

4.1.4 fourth level: scope of influence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

4.1.5 fifth level: Outcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

4.2 fundamental principles of the “contribution of supreme audit institutions

to good governance” model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

4.2.1 High-quality lawmaking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

4.2.2 lawfulness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

4.2.3 Accountability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

4.2.4 transparency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

4.2.5 Integrity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

4.2.6 economic and financial sustainability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

4.2.7 leading by example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

4.2.8 effective and efficient financial management . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

4.3 A series of studies entitled “Pillars of good governance – focus on State Audit

Office of Hungary as a Supreme Audit Institution” . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

COntentS

6

S t u d y S e r I e S S t u d y S e r I e S

SUmmARY

in accordance with its institutional strategy, the mission of the state audit office of hungary

(sao) is to promote the transparency and regu-larity of public finances with its value creating audits performed on a solid professional basis, thus contributing to “good governance”. With regard to its evolution, good governance has emerged as a model promoting state interven-tion and state participation in stark contrast to the tenets of laissez-faire liberal and neo-liberal schools. by now, good governance has become a concept that can be described with a complex set of criteria against which the performance of individual economic policies and state organi-sations can be measured. the role of supreme audit institutions in supporting good govern-ance, however, has not been explained before by means of a similarly comprehensive model despite the prominent role sais play in the implementation of individual criteria through their audits. in consideration of its mandate and the duties enshrined in the new legislation, the state audit office of hungary has constructed a model to provide an overview and a classifica-tion of the contribution of supreme audit institu-tions to good governance. the hungarian model presents the basic conditions, principles, tools and scope of influence associated with the pro-motion of good governance.

IntrOduCtIOn

in accordance with its institutional strategy, the mission of the state audit office of hun-

gary (sao) is to promote the transparency and regularity of public finances with its value creat-ing audits performed on a solid professional ba-sis, thus contributing to “good governance”. as part of the research on good governance, there is a growing body of literature analysing the role and activity of supreme audit institutions in fos-tering good governance. Due to their independ-ence, knowledge base and audit mandate, state audit offices possess the credibility required for the representation of public interest and hence, obtaining public confidence, while providing significant information through their audit ac-tivity to be leveraged by those working on the implementation of government objectives. that notwithstanding, papers addressing the role and contribution of state audit offices to good gov-ernance at the systemic level are still scarce.

this study is intended to give a comprehen-sive insight into the role of the state audit of-fice of hungary in good governance for a broad range of academic and civil society audiences with an interest in public affairs. before elabo-rating on the topic, a general explanation is war-ranted with respect to the evolution of the con-cept of good governance and the background of its emergence. this study is intended to clarify the concept of good governance by reiterating the development of the ideas associated with the notion itself. it discusses the good governance research of authoritative international organisa-tions and defines the widely accepted and ex-tensively examined criteria of good governance. a separate section is dedicated to the latest in-ternational approach to the subject – prepared by the oEcD – as it relates to supreme audit institutions. finally, the contribution of supreme audit institutions to good governance is summa-rised in the sao’s own “hungarian model”.

S t u d y S e r I e S

7

S t u d y S e r I e S

2. THE CONCEPT Of gOOd gOvernAnCe

2.1 good governance and the failure of the neo-liberal school

the concept of good governance, in other

words governance as a process, is fre-quently linked to the economic and socio-political reforms recommended by the World bank and launched in the 1980s (World bank, 1983). these reforms reflected the theses of the New Public management movement that gained momentum at the end of the 1970s as a result of the global economic recession. first and foremost, disciples of the movement strived to release public management from ex-cessive red tape. With that in mind, proposed reforms included the widespread adaptation of the management techniques applied in the organisational models of business ventures (hajnal, 2004), while the need to change the principles of management was also recognised (Pulay, 2012). With respect to management – as a critical part of good governance – the report concluded that, amidst the increasingly complex socio-economic conditions of our times, public management is only capable of successfully navigating the state through the intricate patchwork of various interests by abandoning the belief in its own omnipotence and engaging in continuous consultation with key interest groups. this attitude implies that state organisations involve advocacy groups and non-governmental organisations in pre-decision processes in order to find broadly ac-ceptable trade-offs to resolve complex prob-lems (Pulay, 2012). however, this value and participation oriented approach is not without disadvantages or risks: it requires complete (or at the very least, more) openness on the part

of public administration, while citizens should be able – and want – to participate in making public policy decisions (torma, 2010).

Neo-liberal representatives of the same movement contrasted the bureaucratic domi-nance of the state with deregulation and the marketisation, privatisation and NGo-isation of most public services; in short, with dena-tionalisation. the World bank’s approach con-tains the traits that reduce state influence and role, which are also characteristic of the NPm movement. as such, in particular, the stimula-tion of deregulation and privatisation process-es desirable in state operation, based on which certain authors interpret good governance as a neo-liberal concept that limits the state to a ‘night-watch’ function in the narrowest sense and which allows for market mechanisms and the social coordination function of the private sector (G. fodor – stumpf, 2007). the gaining ground of the neo-liberal movement of good government led to the weakening of the state.

the 2008 economic crisis – as well as the 1997 financial crisis in asia – demonstrated that unregulated or poorly regulated markets can produce extraordinary costs and social losses (birdshall and fukuyama, 2011). main-taining the ideology of the minimal state leads to further disparities which, in turn, increase political polarisation and undermine citi-zen’s confidence in democratic arrangements (fukuyama, 2014). “the holy trinity of liber-alisation, deregulation and privatisation can be no longer sustained when american financial policy – a policy founded on the efficiency of self-regulating markets and responsible market behaviour – ends up depreciating the stock of the largest financial institutions and disrupting the functioning of the banking sector, leading to state bailouts and direct shareholder partici-pation” (Gál, 2010). in addition, the failure of development policies aimed at the convergence of indebted, crisis-ridden developing countries in the context of the Washington consensus also prompted the academic literature to urge

8

S t u d y S e r I e S S t u d y S e r I e S

the replacement of neo-liberalism as early as the turn of the millennium.

stiglitz, for instance, initiated the craft-ing of a “Post-Washington consensus” as a rivalrous public policy programme (stiglitz, 2001), focusing primarily on the citizens’ liv-ing standards, the promotion of equality and sustainable and democratic development. in-stead of advocating one-size-fits-all recipes and criteria, the Post-Washington consensus is meant to propose a framework of guidelines and angles (Pongrácz, 2015). this is yet an-other indication that the countries of the world are facing a paradigm shift and science is in search of new points of reference to replace the old ideology. it is a common trait of the new movements that, as an antithesis to the previous consensus of economic philosophy, they manifest a renewed appreciation of state involvement which, however, is not identi-cal with re-nationalisation. Debates between the new movements advocating a new type of state role are about the extent and area of state involvement and the relevant regulatory approach.

2.2 good government

intensified by the crisis phenomena, voices of social and environmental demands urging

for more state participation posed a new, dou-ble challenge for governments. indeed, in an attempt to flee from the high degree of uncer-tainty stemming from market risks, social and economic participants demanded the states to establish a predictable and stable economic environment. at the same time, besides alle-viating the repercussions of the crisis, govern-ments cannot relinquish the efforts expended to dynamise the economy and increase com-petitiveness with a view to achieving long-term economic objectives. consequently, the former neo-liberal trend was replaced by a narrative that emphasised the importance of

establishing/strengthening good governance (or, increasingly, good government), a market-regulating institutional environment and the relevant state functions, the provision of fun-damental rights and high-quality public serv-ices (scheiring, 2008).

the English language distinguishes be-tween the two ideological trends that have developed along good governance (good gov-ernance and good government). according to the good government concept, not only does the state have to put in place the conditions required for good governance, but it also needs to take on the responsibility of governance. in the case of social issues this means, for ex-ample, that it is the duty of the government to ensure that the distribution of resources is fair and facilitates the equal opportunity of disad-vantaged groups; in other words, it should not always allow decisions to be based on mar-ket allocation mechanisms or the agreement of interest groups as this would prevent pre-cisely the most vulnerable groups from hav-ing access to the goods they need (G. fodor and stumpf, 2007). the starting point of the good government trend is the expectation that the enforcement of public interest requires the state to ensure the fair allocation of economic and social resources based on solidarity and in consideration of the position of all stakehold-ers. consequently, the realisation of “good governance” requires an active, intelligent and strong state. in this respect, the good govern-ment trend exhibits similar characteristics to the Neo-Weberian state. the state, assigned with a reinforced role, is attempting to ensure access to public services at the best possible quality and price to consumer citizens, with the wide-scale participation of these citizens. the essence of the Neo-Weberian notion is that result-oriented governance that embodies unbiased professionalism, must be based on constitutionality and rule of law, thereby en-suring the enforcement of accountability and political responsibility (stumpf, 2009).

S t u d y S e r I e S

9

S t u d y S e r I e S

2.3 A new interpretation emerging from the reinforced role of the state

the global crisis enfolding in 2008 brought about a turning point in deciding the theo-

retical debate of the early 2000s. on the one hand, it proved that the lack of adequate regu-lation (excessively permissive financial regu-lation) may trigger devastating crises. on the other hand, it also demonstrated that in severe crises all economic participants expect the state to deliver the solution. as a result of the crisis, individual states had to take over tre-mendous burdens from defaulting banks and insolvent debtors. skyrocketing public debt, however, called for the radical curtailment of public expenditures which, in turn, spurred yet another recession. the resulting W-shaped cri-sis, therefore, underscored both the necessity and the limitations of state intervention.

under such circumstances, good govern-ance primarily requires a sustainable balance between the state’s role (including its explicit and implicit guarantees) and the financing pos-sibilities thereof. a noteworthy example of the solutions applied is the establishment of the banking union in the European union (par-ticularly in the euro area). besides regulating cross-border financial services at the level of the union, this arrangement relieves member states (and their taxpayers) from bearing the burdens of bank bailouts. accordingly, instead of the respective budgets of nation states, the problems of bankrupt banks will be addressed in the future by resolution funds set up from the contributions of banks. the hungarian Na-tional assembly also established a resolution fund and entrusted the state audit office of hungary with the audit of its financial man-agement.

another noteworthy element of the Eu regulation is the strengthening of fiscal disci-

pline, including the establishment of a reliable accounting system, the definition of various debt rules, and the setting up of independent fiscal agencies (fiscal councils). it should be noted that hungary had enshrined the debt rule in the fundamental Law of hungary even be-fore the relevant Eu directive came into force, along with the institution of the fiscal council which, unprecedentedly, was bestowed with veto powers. a member of the hungarian fis-cal council is the President of the state audit office of hungary – the institution which con-tinuously keeps an eye on the state’s central budget through providing an opinion of the budget appropriation bill and auditing the final accounts of the budget.

the third important element of crisis man-agement is the more active role of monetary policy in crisis management and in the subse-quent stimulation of the economy and provision of support to the economic policy. this is not a novelty in the usa where monetary policy has been aimed at fostering employment from the start. in the European union, however, it can be viewed as a rejection of the previous ortho-doxy that both the European central bank and most national banks of non-euro area member states pursue a monetary policy of quantita-tive easing. the change also has a philosophi-cal significance in that monetary policy was meant to offset overspending fiscal policies in the past. by contrast, monetary policy today works in partnership with a balance-oriented fiscal policy on establishing the conditions for sustainable economic growth.

the processes observed in recent decades (especially economic and financial crisis phe-nomena) have inevitably called attention to the fact – which all national governments need to face sooner or later – that governments will have no more money available in the future than they have today to address social, eco-nomic and welfare problems and to operate the state apparatus. consequently, they will have to rely on sparse financial resources to

10

S t u d y S e r I e S S t u d y S e r I e S

ensure, in line with socio-economic expecta-tions, the provision of more and higher-quality public services while establishing a stable and sustainable economy and efficient state opera-tion. Good governance theories so far have not placed much emphasis on the necessity of an adequate economic policy, even though finan-cial and economic sustainability is a factor not to be overlooked. indeed, even if compliance with the abovementioned principles of good governance is ensured, a lax fiscal policy may render the economy defenceless and vulner-able to potentially unfavourable global trends even in the face of monetary tightening and strict inflation targeting.

it is easy to see that good governance is not a theoretical fiction which should be pursued under all circumstances. Quite the contrary; the ideal of good governance should always be aligned with changing circumstances.

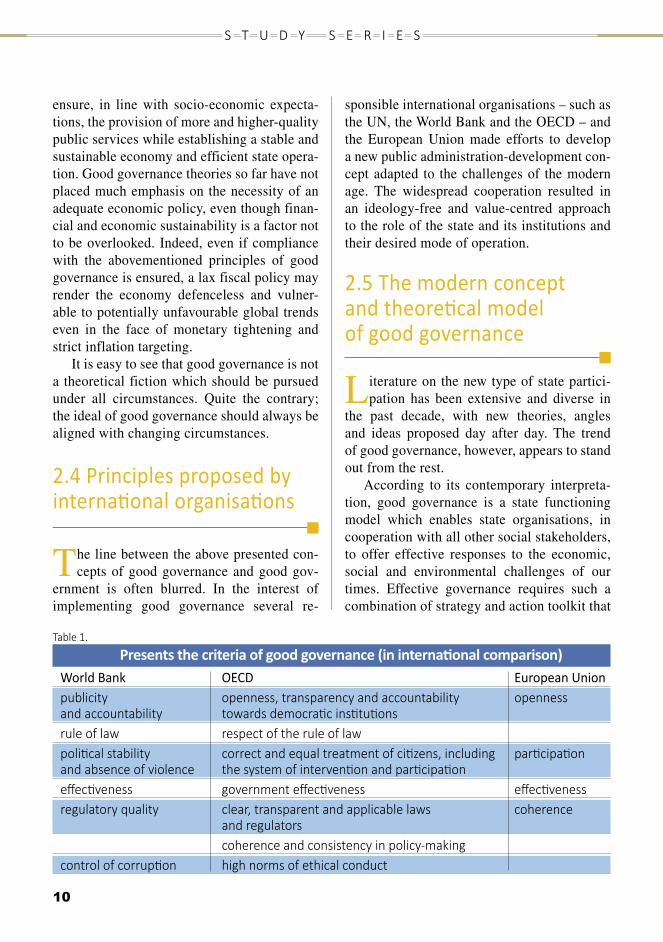

2.4 Principles proposed by international organisations

the line between the above presented con-cepts of good governance and good gov-

ernment is often blurred. in the interest of implementing good governance several re-

sponsible international organisations – such as the uN, the World bank and the oEcD – and the European union made efforts to develop a new public administration-development con-cept adapted to the challenges of the modern age. the widespread cooperation resulted in an ideology-free and value-centred approach to the role of the state and its institutions and their desired mode of operation.

2.5 the modern concept and theoretical model of good governance

Literature on the new type of state partici-pation has been extensive and diverse in

the past decade, with new theories, angles and ideas proposed day after day. the trend of good governance, however, appears to stand out from the rest.

according to its contemporary interpreta-tion, good governance is a state functioning model which enables state organisations, in cooperation with all other social stakeholders, to offer effective responses to the economic, social and environmental challenges of our times. Effective governance requires such a combination of strategy and action toolkit that

table 1.

Presents the criteria of good governance (in international comparison)World Bank OeCd european unionpublicity openness, transparency and accountability opennessand accountability towards democratic institutions rule of law respect of the rule of law political stability correct and equal treatment of citizens, including participationand absence of violence the system of intervention and participation effectiveness government effectiveness effectivenessregulatory quality clear, transparent and applicable laws coherence and regulators coherence and consistency in policy-making control of corruption high norms of ethical conduct

S t u d y S e r I e S

11

S t u d y S e r I e S

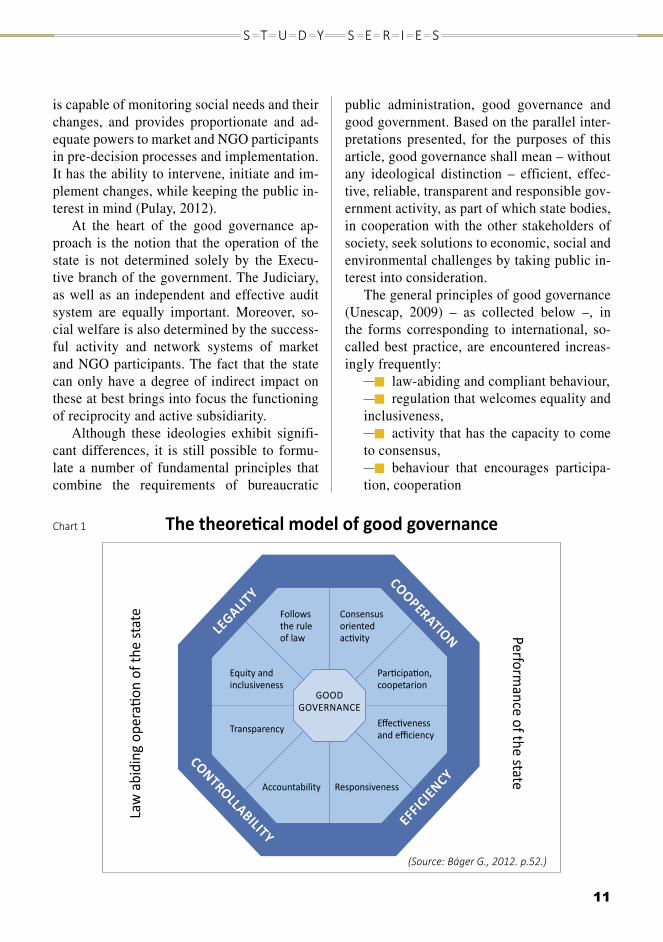

is capable of monitoring social needs and their changes, and provides proportionate and ad-equate powers to market and NGo participants in pre-decision processes and implementation. it has the ability to intervene, initiate and im-plement changes, while keeping the public in-terest in mind (Pulay, 2012).

at the heart of the good governance ap-proach is the notion that the operation of the state is not determined solely by the Execu-tive branch of the government. the Judiciary, as well as an independent and effective audit system are equally important. moreover, so-cial welfare is also determined by the success-ful activity and network systems of market and NGo participants. the fact that the state can only have a degree of indirect impact on these at best brings into focus the functioning of reciprocity and active subsidiarity.

although these ideologies exhibit signifi-cant differences, it is still possible to formu-late a number of fundamental principles that combine the requirements of bureaucratic

public administration, good governance and good government. based on the parallel inter-pretations presented, for the purposes of this article, good governance shall mean – without any ideological distinction – efficient, effec-tive, reliable, transparent and responsible gov-ernment activity, as part of which state bodies, in cooperation with the other stakeholders of society, seek solutions to economic, social and environmental challenges by taking public in-terest into consideration.

the general principles of good governance (unescap, 2009) – as collected below –, in the forms corresponding to international, so-called best practice, are encountered increas-ingly frequently:

law-abiding and compliant behaviour,regulation that welcomes equality and

inclusiveness,activity that has the capacity to come

to consensus, behaviour that encourages participa-

tion, cooperation

The theoretical model of good governance

(Source: Báger G., 2012. p.52.)

chart 1

law

abi

ding

ope

ratio

n of

the

stat

ePerform

ance of the state

LegaLit

y

follows the rule of law

Accountability responsiveness

equity and inclusiveness

transparency Effectiveness and efficiency

Participation, coopetarion

Consensus oriented activity

efficiency

cooperation

controLLabiLity

gOOd gOvernAnCe

12

S t u d y S e r I e S S t u d y S e r I e S

efficient and effective financial man-agement,

responsive operation, accountable activity, transparent operation.

in the theoretical model of good govern-ance (see chart 1), these general principles are structured according to the dimensions of

legality, controllability, cooperation and ef-fectiveness and form the interpretation frame-work of the regular operation and performance of the state organisation (according to báger, 2012, based on unescap, 2009). it should be noted that báger’s translation mentions “ex-pedient and effective” financial management, but the uN document uses the terms “effective and efficient”.

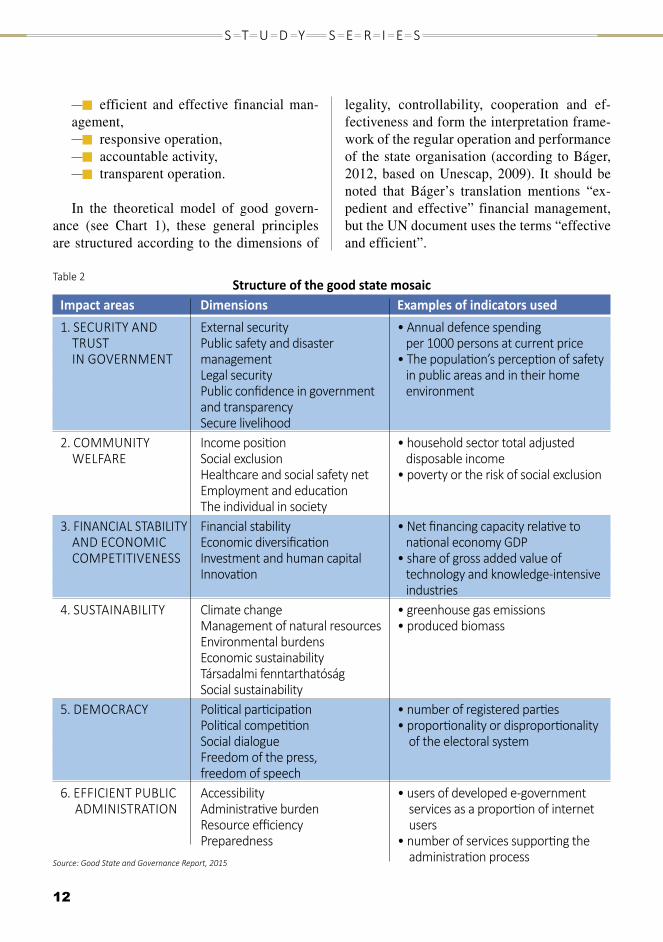

table 2Structure of the good state mosaic

Impact areas Dimensions Examples of indicators used1. SecurIty And external security • Annual defence spending truSt Public safety and disaster per 1000 persons at current price In gOvernMent management • the population’s perception of safety legal security in public areas and in their home Public confidence in government environment and transparency Secure livelihood2. cOMMunIty Income position • household sector total adjusted welfAre Social exclusion disposable income Healthcare and social safety net • poverty or the risk of social exclusion employment and education the individual in society 3. fInAncIAl StAbIlIty financial stability • net financing capacity relative to And ecOnOMIc economic diversification national economy gdP cOMPetItIveneSS Investment and human capital • share of gross added value of Innovation technology and knowledge-intensive industries4. SuStAInAbIlIty climate change • greenhouse gas emissions Management of natural resources • produced biomass environmental burdens economic sustainability társadalmi fenntarthatóság Social sustainability5. deMOcrAcy Political participation • number of registered parties Political competition • proportionality or disproportionality Social dialogue of the electoral system freedom of the press, freedom of speech 6. effIcIent PublIc Accessibility • users of developed e-government AdMInIStrAtIOn Administrative burden services as a proportion of internet resource efficiency users Preparedness • number of services supporting the administration processSource: Good State and Governance Report, 2015

S t u d y S e r I e S

13

S t u d y S e r I e S

2.6 measuring the performance of government

Numerous international economic, financial

and development policy organisations have developed, along the basic principles of good governance, indicators and indicator systems aimed at measuring the goodness of the state and the performance of the government. among the assessment and evaluation methods used in hungary, the JáX and the Good state mosaic developed by the Good state and Governance research institute, operating within the institute of the science of the state and Governance of the National university of Public service, merits mention. the approximately four hundred gov-ernance indicators registered worldwide (as a function of the objectives to be accomplished by and the requirements set against them) set out to measure the enforcement of public good and the implementation of good governance along vary-ing impact areas and dimensions. accordingly, the various indicator systems focus on different aspects of governance during measurement and assessment.

the differentiation of evaluation methods can in part be traced back to the fact that the issue of the enforcement and measurability of the content of value abstractions embodying public good have generated heated value de-bates. the value concepts linked to the enforce-ment of public good as the ultimate objective of state operation generate relatively pure catego-ries. such as compliance with laws and statutes, equality, impartiality, proportionality, rule of law, proceedings within a reasonable time, par-ticipation, respect of privacy, transparency, or in the approach of bovaird and Löffler (2003), social participation, transparency, accountabil-ity, equality , ethics, fairness (fair proceedings), competitiveness, efficiency, sustainability, rule of law. however, the evaluation of content val-ues, such as the input and output side is not so obvious, as from the perspective of the enforce-

ment of the effects of public good (output), a number of government instruments (input) may be classified as” “good” (kis, 2014).

the most frequently used indicators and in-dicator systems, which serve to ‘describe’ the enforcement of value abstractions, do not di-rectly assess the goodness and quality of gov-ernance, but rather through the measurement of social, economic and environmental impacts generated by governance. Well-known interna-tional examples include, but are not limited to the following:

WGi indicators (World bank, 2015) society at a Glance and Government at

a Glance indicators (oEcD, 2014a) indicator systems of the European com-

mission World competitiveness ranking (imD,

2015)hungarian examples, such as the JáX or

the Good state mosaic, focus primarily on the strengths and weaknesses of governance capaci-ties determining state operation and similarly to international practice assessment is conducted through the impacts achieved. the JáX and the Good state mosaic are based on the impact ar-eas detailed in table 2 as well as the system of value-based indicators characterising these areas along varying dimensions (báger et al., 2014).

14

S t u d y S e r I e S S t u d y S e r I e S

3. COntrIButIOn Of SAIS tO gOOd gOvernAnCe

by virtue of their task, supreme audit insti-tutions play a key role in supporting good

governance in the casual sense. state audit of-fices contribute to good governance primarily by auditing public spending and by communi-cating audit results.

as the movement of good governance gained popularity, a growing number of au-thoritative international organisations incorpo-rated the concept of good governance into their documents, and some institutions also defined and expressed the most important aspects of the role of supreme audit institutions in good governance.

3.1 Resolutions of the United Nations

the first resolution of the united Nations adopted on the role of supreme audit in-

stitutions was published in 2011 under the title “Promoting the efficiency, accountability, ef-fectiveness and transparency of public admin-istration by strengthening supreme audit insti-tutions” (united Nations, 2011). Point 5 of the resolution states that good governance is to be promoted by ensuring efficiency, account-ability, effectiveness and transparency through strengthened supreme audit institutions. With this statement the uN resolution clearly de-fined the role of supreme audit institutions in the efforts to achieve the objectives of good governance. a new resolution adopted in 2014 (united Nations, 2014) added that good gov-ernance was to be promoted at all levels by ensuring efficiency, accountability, effective-ness and transparency through strengthened supreme audit institutions, including, as ap-

propriate, the improvement of public account-ing systems.

3.2 IntOSAI documents

according to the strategic Plan (iNtosai, 2010) of the international organisation

of supreme audit institutions (iNtosai), the vision of the organisation is to promote good governance by enabling sais to help their re-spective governments improve performance, enhance transparency, ensure accountability, maintain credibility, fight corruption, promote public trust, and foster the efficient and effec-tive receipt and use of public resources for the benefit of their peoples. this vision is reflected in several documents approved at the beijing congress in 2013. both the fundamental Prin-ciples of Public sector auditing (issai 100) and the fundamental Principles of compliance auditing (issai 400) reflect the view that su-preme audit institutions should contribute to good governance at the highest level with the best possible utilisation. they emphasise the role of state audit offices in objective evalua-tion (issai 100) and in identifying weakness-es, instances of non-compliance, irregularities and inadequacies (issai 400). in addition, compliance audit helps facilitate good govern-ance in the public sector by detecting risks of fraud.

the commitment of iNtosai to supporting good governance is also demonstrated by the publication of iNtosai Gov (Guidance for Good Governance). this term covers several documents that have been published by iNto-sai for administrative authorities as guidelines in such areas as internal controls and account-ing principles. these guidelines are also appli-cable to the activity and control of state audit offices.

at the same time, the primary task of iNto-sai is to assist and enhance the work of state audit offices, in the context of which the organ-

S t u d y S e r I e S

15

S t u d y S e r I e S

isation primarily issues guidelines focused on the good governance of supreme audit institu-tions. Examples include the document entitled “Principles of transparency and accountability” (issai 20) adopted at the Johannesburg con-gress in 2010 – which specifically discusses the criteria of transparency and accountability as two significant pillars of the good govern-ance of state audit offices – and the document entitled “value and benefits of supreme audit institutions – making a difference to the lives of citizens” (issai 12). according to the lat-ter document, in addition to creating added value by disseminating appropriate responses to new social and environmental challenges in the public sector, supreme audit institutions – as the third line of defence in audit – should appear as a model organisation for all audited entities (leading by example).

3.3 the OeCd’s approach

the oEcD has prepared the most exhaus-tive, most thorough, yet not entirely com-

prehensive analysis of the role taken by state audit offices in good governance (oEcD, 2014b). Entitled “Partners for good govern-ance: mapping the role of supreme audit in-stitutions”, the oEcD analysis (hereinafter: oEcD analysis) emphasised that it was not intended to address the full spectrum of the factors required to achieve good governance. instead, the study purposefully selected key ar-eas and the relevant government activities for their importance to developing and delivering policies and programmes that benefit citizens. the analysis provided an illustration of how supreme audit institutions can support good governance in these selected areas, assuming that it would serve as a basis for understand-ing how it may be replicated in other areas of governance.

the objective of the oEcD analysis was to provide helpful ideas for state audit offices’

engagement in supporting good governance by analysing the activity of 11 state audit offices and the European court of auditors in the key areas along with the relevant government ac-tivities, and to allow the Executive and Legisla-tive branches as well as state audit offices of all countries to consider and evaluate the practices

presented. the approach of the oEcD analysis was to define public governance in general and good governance in particular, before identify-ing the key public areas that need to function well in order to successfully practice the good governance suggested by the definition. the study then proceeded to assign government activities to each key area for setting up its analytical framework. it identified human re-source management, rule-making and govern-ment-wide coherence as the key functions of good governance. the key functions are based on, and thus require the optimal functioning, of four government activities: sound budget-ary processes, good regulatory programmes,

16

S t u d y S e r I e S S t u d y S e r I e S

strategically agile centres of Government and effective internal control processes. Public policy-making, as a whole, relies on these four government activities.

sound budgetary governance ensures integ-rity, efficiency and economy in the use of pub-lic resources, while the audits of budget plan-ning and execution are traditionally the tasks of state audit offices. by contrast, auditing the soundness of regulatory policy is not among the traditional duties of supreme audit institutions; however, a growing number of state audit of-fices are making efforts worldwide to support the better functioning of the regulatory area in their country and to help their legislature in es-tablishing a coherent regulatory environment. the oEcD analysis points out that state audit offices do not have dedicated tasks with respect to the support of agile centres of Government; their undertakings in this regard tend to be ad hoc and limited. however, state audit offices can provide valuable input by offering an as-sessment of the programmes and policies im-plemented in the context of government activi-ties. finally, the analysis emphasises the critical role of state audit offices in setting up efficient and effective internal control systems.

the oEcD also worked out the methods through which state audit offices can support these four different types of government ac-tivities: for the most part, they are audits ap-propriately focused on organisations in charge and their relevant activities. state audit offices can foster good governance by ensuring ac-countability through independent audits on the one hand, and by evaluating programmes and policies through compliance and performance audits on the other hand. the oEcD analysis stresses that state audit offices produce reliable and robust reports upon which the Executive and Legislative branches can base their deci-sions.

it notes that in selecting the method of sup-porting good governance, state audit offices should consider the constitutional situation of

individual institutions; their role in the legal framework; their relationship with the legisla-ture; the reporting obligation of the institution; and finally, the existence of other institutions vested with the same task or similar duties. at the same time, it underscores that state audit offices are uniquely placed to support public confidence in the government and foster good governance. trust in public institutions hinges upon the extent to which their policies and pro-grammes serve the public interest, and state au-dit offices, by virtue of their independence, can evaluate this objectively.

S t u d y S e r I e S

17

S t u d y S e r I e S

4. COntrIButIOn Of SAO tO gOOd gOvernAnCe

in defining the role of the state audit office of hungary in good governance, the most appro-

priate starting point is the fundamental Law of hungary. Pursuant to article 43 (1) of the funda-mental Law: the state audit office shall be the organ of the National assembly responsible for financial and economic audit. acting within its functions laid down in an act, the state audit of-fice shall audit the implementation of the central budget, the management of public finances, the use of funds from public finances and the man-agement of national assets. the state audit office shall carry out its audits according to the criteria of lawfulness, expediency and efficiency”.

in view of the tasks bestowed upon it by the fundamental Law, we should examine the con-tents of the fundamental Law with respect to the central budget, public finances and the manage-ment of national assets. article N) of the funda-mental Law lays down the following principles:

„(1) hungary shall observe the principle of balanced, transparent and sustainable budget management.(2) the National assembly and the Govern-ment shall have primary responsibility for the observance of the principle referred to in Para-graph (1).(3) in performing their duties, the constitu-tional court, courts, local governments and other state organs shall be obliged to respect the principle referred to in Paragraph (1)”.in keeping with the principles, in the fun-

damental Law a separate chapter is dedicated to public finances, the first element of which is the debt rule: the reversal of hungary’s indebted-ness. as article 36 (4)–(5) states: “the National assembly may not adopt an act on the central budget as a result of which state debt would ex-ceed half of the Gross Domestic Product. as long

as state debt exceeds half of the Gross Domestic Product, the National assembly may only adopt an act on the central budget which provides for state debt reduction in proportion to the Gross Domestic Product”. the fundamental Law es-tablished the fiscal council as the guardian of the debt rule. besides the chairman of the fiscal council appointed by the President of the repub-lic of hungary, the three-member fiscal coun-cil is composed of the Governor of the National bank of hungary and the President of the state audit office.

With respect to the execution of the budget, the fundamental Law sets high requirements for the Government: “the Government shall be obliged to execute the central budget in a lawful and expedient manner, with efficient management of public funds and by ensuring transparency”.

article 38 (1) of the fundamental law de-clares the property of the state and of local gov-ernments to be national assets. the management and protection of national assets shall aim at serv-ing public interest, meeting common needs and preserving natural resources, as well as at taking into account the needs of future generations.

of the provisions listed above, it is important to underline the need for balanced and sustainable budget management. the primary responsibility in this regard rests with the National assembly and the Government. it is an important shift of emphasis compared to the previous constitution, that the role of the constitutional court in this re-gard is not to ensure checks and balances, but it is that of an institution that respects the country’s endeavour to have a balanced and sustainable budget. it should be understood that this shift is backed by the obvious truth that the enforcement of rights is constrained by the possibilities of the economy. Even so, the fiscal policy of the Na-tional assembly and the Government was not left without checks and balances: the fiscal council was set up to safeguard this constitutional require-ment, with veto powers regarding compliance with the debt rule. having said that, the responsi-bilities of the fiscal council, apart from the right

18

S t u d y S e r I e S S t u d y S e r I e S

to veto, are relatively limited. contrary to similar institutions in other countries, the fiscal council does not develop budget scenarios as an alterna-tive to that of the Government, because, as the fundamental Law states, “as an organ supporting the legislative activity of the National assembly, the fiscal council shall examine the feasibility of the central budget”.

it is an enlightening exercise to compare the constitutional tasks of the state audit office with the responsibilities of the Government with re-spect to the execution of the budget. indeed, the adjectives used by the fundamental Law are the same: lawful, expedient, efficient. the same ad-jectives are cited in Paragraph (5) of the funda-mental Law’s article on national assets, which states: “business organisations owned by the state or local governments shall manage their af-fairs in a manner determined in an act, autono-mously and responsibly according to the require-ments of lawfulness, expediency and efficiency”. consequently, the state audit office contributes to good governance primarily by auditing fiscal management and the management of public as-sets from the perspective of lawfulness, expedi-ency and efficiency, and prepares audit-related re-ports with special emphasis on these dimensions.

it should be recognised, however, that adher-ence to the debt rule – which has become the cen-tral element of public finance regulations – not only depends on the reduction of public debt, but also on GDP growth. the dynamics of the hun-garian economy, in turn, largely depends on the competitiveness of hungarian enterprises and the quality of work of hungarian employees. in es-sence, the fundamental Law emphasises the same notion in article m) which states, as a principle, that “the economy of hungary shall be based on work which creates value, and on freedom of en-terprise”, and that “hungary shall ensure the con-ditions of fair economic competition. hungary shall act against any abuse of a dominant posi-tion, and shall protect the rights of consumers”. according to the fundamental Law, the hungari-an economy is a competitive economy, where fair

competition among businesses and value gener-ating work constitute the basis of the economy’s competitiveness. at the same time, the public finance system redistributes around a half of the income generated across the hungarian economy. the required expropriation and spending mecha-nisms, in turn, have a significant impact on the functioning of the economy. therefore, the role of the sao in relation to good governance neces-sarily includes the priority audit of the tax system and the various funding schemes.

it is also noteworthy that the regulation ap-plicable to the National bank of hungary (mNb, the organisation responsible for monetary policy) has been also included in the chapter on Public finances in the fundamental Law, and that the governor of the mNb is member of the fiscal council ex officio. both solutions indicate the importance of harmony between fiscal policy and monetary policy. if compliance with the debt rule is at the heart of fiscal policy, then monetary policy will not need to deploy strict instruments in order to contain fiscal overspending; in fact, it can apply economic stimuluses even while main-taining price stability. obviously, in the case of a small, open economy, this ambition cannot be separated from developments in international money markets. in any event, the period elapsed since the adoption of the fundamental Law has demonstrated that both the deficit of the govern-ment sector and the inflation rate could be kept below 3 per cent simultaneously in case of a har-mony between fiscal policy and monetary policy. a well-run state cannot exist without an inde-pendent institution inspecting the use of public funds. as was shown in Point 2, an academic and professional consensus is emerging with specific emphasis on the role and contribution of state au-dit offices to the implementation of good govern-ance. at the same time, no systemic overviews or models have been published so far with regard to the basic conditions, principles, criteria, methods and scopes of influence associated with supreme audit institutions as they fulfil their role in facili-tating good governance. consequently, national

S t u d y S e r I e S

19

S t u d y S e r I e S

state audit offices work out individually, in line with their respective mandates, the way in which they contribute to good governance.

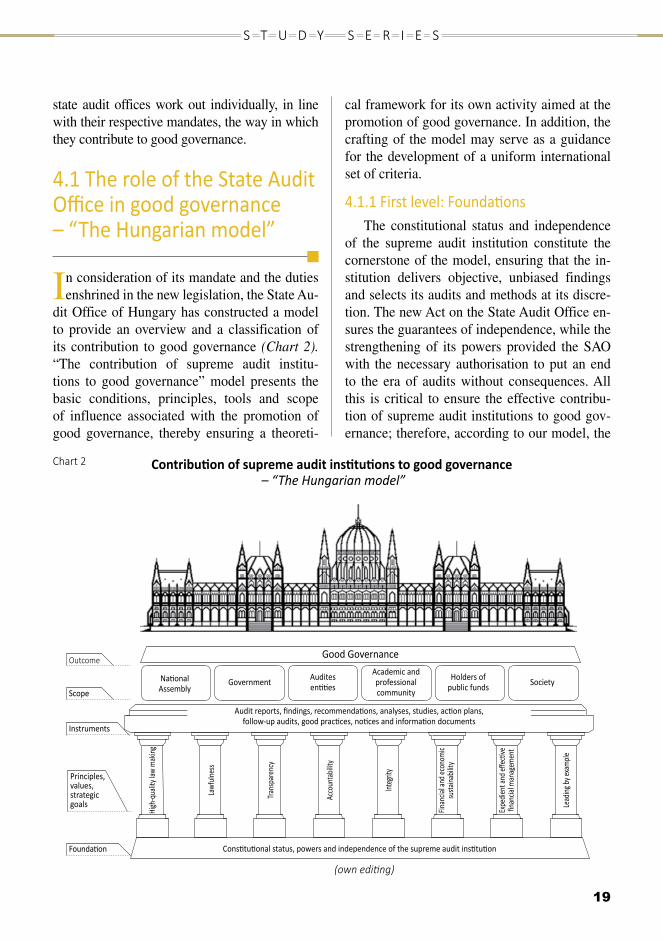

4.1 the role of the State Audit Office in good governance – “The Hungarian model”

in consideration of its mandate and the duties enshrined in the new legislation, the state au-

dit office of hungary has constructed a model to provide an overview and a classification of its contribution to good governance (Chart 2). “the contribution of supreme audit institu-tions to good governance” model presents the basic conditions, principles, tools and scope of influence associated with the promotion of good governance, thereby ensuring a theoreti-

cal framework for its own activity aimed at the promotion of good governance. in addition, the crafting of the model may serve as a guidance for the development of a uniform international set of criteria.

4.1.1 first level: foundationsthe constitutional status and independence

of the supreme audit institution constitute the cornerstone of the model, ensuring that the in-stitution delivers objective, unbiased findings and selects its audits and methods at its discre-tion. the new act on the state audit office en-sures the guarantees of independence, while the strengthening of its powers provided the sao with the necessary authorisation to put an end to the era of audits without consequences. all this is critical to ensure the effective contribu-tion of supreme audit institutions to good gov-ernance; therefore, according to our model, the

good governance

National Assembly

Outcome

Scope

Principles, values, strategic goals

Instruments

foundation

government

High

-qua

lity l

aw m

aking

Lead

ing by

exam

ple

Expe

dient

and e

ffecti

ve

finan

cial m

anag

emen

t

Lawf

ulnes

s

trans

pare

ncy

Acco

unta

bility

Integ

rity

finan

cial a

nd ec

onom

ic su

staina

bility

Society

Audit reports, findings, recommendations, analyses, studies, action plans, follow-up audits, good practices, notices and information documents

Audites entities

Academic and professional community

Holders of public funds

Constitutional status, powers and independence of the supreme audit institution

Contribution of supreme audit institutions to good governance – “The Hungarian model”

chart 2

(own editing)

20

S t u d y S e r I e S S t u d y S e r I e S

legal standing, powers and independence of supreme audit institutions form the foundation upon which their good governance promoting activity is based.

4.1.2 Second level: fundamental principles and goals

moreover, the hungarian model determines the fundamental principles and strategic goals that serve as a compass for supreme audit insti-tutions in supporting good governance, whether it is about the definition of objectives, the selec-tion of audited entities, the planning of individ-ual tasks or the evaluation of the results. these are the principles in consideration of which su-preme audit institutions undertake a role in fa-cilitating good governance.

Pillars for supreme audit institutions in sup-porting good governance according to the hun-garian model:

high-quality lawmaking;lawfulness;accountability;transparency;integrity;economic and financial sustainability;a model organisation;effective and efficient financial man-

agement.the enforcement of these principles is one

of the strategic goals of the sao, permeating its entire activity.

4.1.3 Third level: instrumentsthe next level of the model “contribution of

supreme audit institutions to good governance” enumerates the tools on which supreme audit in-stitutions can rely in their effort to support good governance. state audit offices exercise their in-fluence by issuing reports, findings, recommen-dations, analyses and studies; by requesting and evaluating action plans; by follow-up audits; by sharing good practices and audit experience; by notices and administrative indications; by the preparation of information documents; by pub-

lishing opinions; and by active social and pro-fessional communication.

4.1.4 fourth level: scope of influenceat the fourth level, the model illustrates the

ways in which state audit offices exercise their influence on institutional, professional and social groups by leveraging the tools available to them in order to support a well-managed state.

With a view to establishing and enhancing high-quality lawmaking lawfulness, integrity, leading by example, transparency, economic and financial stability, accountability and effective and efficient financial management, supreme au-dit institutions exercise their influence on:

the National assembly and the Govern-ment;

the audited entities;all organisations that use public funds

and hence, are in a position to utilise the audit findings and recommendations of state audit offices;

academic and professional audiences; and

society at large, in particular, the com-munity of taxpaying citizens.

4.1.5 fifth level: Outcomeaccording to the “contribution of supreme

audit institutions to good governance” model, the outcome is good governance itself. the purpose of our activity is to ensure high-quality lawmak-ing, strengthen lawfulness, spread integrity-based operations, promote the good practices of the su-preme audit institution, improve the transparency of public spending, strengthen economic and fi-nancial sustainability and stability, increase audit coverage and accountability, and implement ex-pedient and effective financial management. We can only consider our work effective if a measur-able step forward has been made in respect of the above aspects.

the basic values of the model designed to support a well-run state permeate the entire activity of the sao and form the benchmark

S t u d y S e r I e S

21

S t u d y S e r I e S

against which we measure the effectiveness of our activity and define areas for improvement. our objective is to increase the transparency and efficiency of the use of public funds, foster the more efficient functioning of the institutions and systems providing public services, and ensure that our audits and analyses generate positive changes that will improve the everyday life of citizens.

4.2 fundamental principles of the “Contribution of supreme audit institutions to good governance” model

4.2.1 High-quality lawmakingin order to ensure high-quality lawmaking

the legislature is expected to protect basic demo-cratic values, while legislation is expected to ful-fil the criteria of clarity, coherence, justice and efficiency. it is the duty of supreme audit institu-tions to support the legislative work of the Na-tional assembly through their audit activity and audit experience. as a result, their advisory and opinion-forming function is gradually becoming more prominent.

one of the principal uses of public sector audits and analyses is to support the legislative activity of the National assembly. as a matter of fact, state audit offices can achieve the greatest and most lasting impact through legislation; con-sequently, their findings, experiences and recom-mendations all serve to make certain that laws adopted are as well-founded as possible. their goal is to ensure the incorporation of the experi-ences of public sector audits into legislation at the preparatory stage.

through their audits, state audit offices not only measure practices against legislation but also gather experiences, by virtue of their opera-tion, about legal standards. the audits not only

contribute to rendering the operation and finan-cial management of the audited institutions more compliant and more transparent, but, by identi-fying systemic problems, they can considerably contribute to ensuring that the legislator ap-proaches the transformation of complex public finance areas in the appropriate manner and at the appropriate place.

4.2.2 Lawfulnesssupreme audit institutions serve the desired

law-abiding and compliant behaviour, lawful-ness and legal compliance – and hence, good governance – by their audits, audit findings and recommendations, by requesting and evaluating action plans for the restoration of regular opera-tions and by the follow-up audits designed to verify their implementation.

through the measures taken in response to audit findings, the utility of audits lies in the regular, effective and efficient operation of the audited entities.

it is the legal and moral obligation of all play-ers in the public sector – be it an organisation or an office employee – to reinforce the legally transparent rule of law. the functioning of a con-stitutional state, in turn, is based on compliant behaviour. the guarantee of the sustainability of regularity, however, lies in the fact that the regular utilisation of public funds is not simply a form of behaviour enforced by audit activity, but it is primarily based on the voluntary legal compliance of the stakeholders arising from their commitment to regularity. therefore, the advisory activity of state audit offices is critical in facilitating the legally compliant operation of public organisations.

4.2.3 Accountabilityall players of the public sector embody the

state through their actions and, depending on their activities, they (may) make decisions about the use of public funds and about the future of others. as such, public service is a profession that carries great responsibility, where the guarantees

22

S t u d y S e r I e S S t u d y S e r I e S

of responsibility and accountability related to the given activity must be ensured.

accountability means that persons, organi-sations and the community take responsibility for their use of public funds and the financial management of national assets, and can be held accountable for their use of the public resources entrusted to them. the principle of accountabil-ity can only be enforced if the relevant compe-tences and responsibilities can be identified, and the processes related to public funds are regu-lated, transparent and easy to monitor.

state audit offices enforce accountability by way of their audits; however, since most saos are not authorities, they do not have direct sanc-tioning powers with respect to the irregularities detected. they assist in the enforcement of ac-countability by calling the attention of the au-thorities that are entitled to impose sanctions regarding detected infringement.

4.2.4 transparencythe foundation of democracy and accounta-

bility is that citizens know what happens to their money, who uses the public assets entrusted to them and how. Ensuring the transparency of the use of public funds is a priority task of state au-dit offices. supreme audit institutions take part in the attitude-changing mission of ensuring that the use of public funds is also supported by so-cial control and the power of publicity. the pub-lication of reports guarantees the transparency of public spending and as such, it is a part of the information provided about the spending of tax-payers’ money. full publicity could facilitate the accountability of persons and organisations us-ing public funds towards social, political or eco-nomic participants and contribute to eliminating incorrect practices.

the transparency of public spending can be ensured in various ways: the beneficiary organi-sations of budget subsidies ensure the transpar-ency of their own financial transactions and the use of public funds, and submit regular reports on their activities and public spending. supreme

audit institutions play a critical role in estab-lishing transparency: by virtue of their legal power and competence and through their audits, they are in a position to explore the practice of public spending and the financial management of public assets. they publish their findings in easy-to-understand, publicly available reports. in view of the objectivity of state audit offices, their distance from the government and their constitu-tional status that ensures their independence, cit-izens have every reason to trust the credibility of audit reports and the information provided. Due to the objectivity, publicity and clarity of their reports, the opinion of state audit offices serves as a point of reference for citizens in formulating their own opinions.

4.2.5 Integritythe fight against corruption is a matter of

strategic significance for all nations. its effec-tiveness may greatly influence not only the per-ception of a particular country, but also various economic processes and the development of the national economy. in the spirit of the fight against corruption, some supreme audit institu-tions undertake the mission of supporting the integrity-based management of the public sec-tor and the auditing of integrity controls, while their ultimate goal is to facilitate a change in the administrative culture and to establish integrity-based institutional operation in the public sector. by identifying integrity risks, by auditing the coverage and functioning of integrity controls and by promoting integrity awareness, state audit offices perform a preventive function in the fight against corruption.

4.2.6 Economic and financial sustainabilityone of the most important tasks of a well-run

state is to ensure financial and economic stability and sustainability to its institutions and citizens. surging deficits and financial and debt crises are powerful reminders of the fact that sustainability is a core objective in the economic sense, and a core task in the governmental sense. supreme

S t u d y S e r I e S

23

S t u d y S e r I e S

audit institutions play a prominent supporting role in the implementation of this goal.

financial decisions have long-term conse-quences and therefore, financial planning and plan-driven operations are important. supreme audit institutions provide assistance to elected representatives and the government in this regard. traditionally, they are responsible for auditing the execution of the annual budget, and in some countries providing an opinion on the budget ap-propriation bill is also counted among the tasks of state audit offices. financial planning and execu-tion can also be assessed at institutional level dur-ing individual audits, whereby state audit offices might discover systemic problems or specific op-erational deficiencies that require intervention.

based on these considerations, the hungarian model also includes the fundamental principle of economic and financial sustainability as a road that leads to stability. in our view, promoting the healthy financial standing of the state is one of the most important values added in the context of the supreme audit institutions’ promotion of good governance. Without financial equilibrium the state does not have the resources that could be harnessed for the welfare of citizens.

4.2.7 Leading by examplein addition to ensuring the accountability, in-

tegrity and transparency of public finances and disseminating appropriate responses to new so-cial and environmental challenges in the public sector, the international recommendation for su-preme audit institutions1 (issai 12) includes the requirement of serving as a model organisation for all audited entities. a prominent element of the issai 12 standard states that “the operation of a public organisation should be exemplary at the level of its day-to-day operations”.

supreme economic and financial audit in-stitutions can only be credible advocates and representatives of transparency, accountability, effectiveness and efficiency if they lead by ex-

ample in implementing these values. the exem-plary behaviour of state audit offices in the fair, effective and goal-oriented use of public funds and public assets is the token of strengthening the good reputation of the state audit office and thus, the confidence of citizens.

4.2.8 Effective and efficient financial management

in light of globalisation processes and eco-nomic trends, players of the public sector have a growing obligation to comply with social expec-tations about the effectiveness and efficiency of the public sector, which should also be ensured in the operation of the public sector and in the provision of public services. During their au-dits, supreme audit institutions strive to assess the financial management of public sector par-ticipants from the perspective of effectiveness and efficiency as well, and to contribute to the implementation of good governance by offering specific recommendations.

through the provision of feedback, each indi-vidual audit contributes to eliminating deficien-cies, as well as inadequate practices and opera-tion; however, performance audits can make an even more substantial contribution to improving the performance and efficiency of the public sec-tor by exploring and promptly quantifying errors that can be expressed in monetary terms.

4.3 A series of studies entitled “Pillars of Good governance – focus on State Audit Office of Hungary as a Supreme Audit Institution”

aligned to the challenges of a changing world, the ideas influencing the state and

constitutional institutions – including the work

1ISSAI 12: Value and Benefits of Supreme Audit Institutions – making a difference to the lives of citizens

24

S t u d y S e r I e S S t u d y S e r I e S

of state audit offices –, as well as theoretical approaches to the role of the sao have gone through a considerable transformation. it was in the context of this renewal that the hungarian act on the sao was amended. the legislation represented an important step forward, which warrants the publication of a series of studies dedicated to discussing the role of the state au-dit office in a timely and academically sound manner. the collection of studies exploring the role of supreme audit institutions in good gov-ernance is rightfully considered a groundbreak-ing work that fills and important gap in the lit-erature.

it follows from the fundamental Law, the legal status and tasks of public institutions and the values of public service, that each individ-ual public institution and budgetary institution needs to clarify the core issues that justified its establishment and determine its relationship to the state, to the Government and to the citizens.

among the activities of state audit offices, the promotion of good governance has gained an increasingly important role, which also de-termines the themes evolving in the context of international knowledge transfer. the hungar-ian society also expects the state audit office of hungary to take an increasingly prominent role in facilitating good governance, as reflected in the renewed provisions of the 2011 act on the sao.

it can be stated that in recent years, each ac-tivity of the state audit office of hungary has been permeated by an approach facilitating good governance, exerting an influence on a wide ar-ray of factors, such as audits and their utilisation, the increasingly important role of analyses and studies, or the sao’s activities aimed at foster-ing the integrity of the public sector. in addition, as a model institution, we consider the criteria of efficiency, accountability and effectiveness in our efforts to develop our organisation and our employees.

the series of studies presents the role of supreme audit institutions in the promotion of

good governance in an international compari-son, defines the criteria, principles, require-ments, instruments and scopes of influence of good governance, and gives an account of the way in which the requirements on the support of good governance were fulfilled at the state audit office of hungary. individual items of the series of studies are published both in hungar-ian and in English in the form of working pa-pers, and are made available electronically on the dedicated online platform.

our series of studies is one of the most im-portant intellectual products of the past five years. as a model organisation, our goal is to share “good practices” both in hungary and abroad, whereby we not only aim to support good governance, but also to shape attitudes about the state and public life and to improve public thinking.

S t u d y S e r I e S

25

S t u d y S e r I e S

LIterAtureAcademic publications, other research results:1. Báger, G. (2012): Korrupció (Corruption). Akadémia Kiadó2. Báger et al. (2014): A Jó Állam mérhetősége (The measurability of the Good State and

Governance. National University of Public Service, Budapest3. Birdshall, N. – Fukuyama, F. (2011): The Post-Washington Consensus: Development After the

Crisis. foreign Affairs, vol. 90, No. 2, pp. 50–524. Bovaird, T. – Löffler, E. (2003): Evaluating the Quality of Governance: Indicators, models and

methodologies. International Review of Administrative Sciences, vol. 69, pp. 313–3285. Fukuyama, F. (2014): American Power is Waning Because Washington Won’t Stop Quarreling.

New Republican, march 10. Online: http://www.newrepublic.com/article/116953/american-power-decline-due-partisanship-washington

6. Gál, Z. (2010): Pénzügyi piacok globális térben (financial markets in the Global Space). Akadémia Kiadó, Budapest, pp. 661–662

7. G. Fodor, G. – Stumpf, I. (2007): A jó kormányzás két értelme avagy a demokratikus kormányzás programja és feltételei (The two meanings of “good governance” – or the programme and conditions of democratic governance). Századvég Working Papers 6. Századvég Alapítvány, Budapest

8. Hajnal, Gy. (2004): Igazgatási kultúra és New Public management reformok egy összehasonlító esettanulmány tükrében (Administrative culture and New Public management reforms in a comparative case study). Ph.D. Dissertation, Budapest University of Economic Sciences and Public Administration, pp. 8–11. Online: http://phd.lib.uni-corvinus.hu/174/1/hajnal_gyorgy.pdf

9. Kis, N. (2014): A kormányzás minőségének értékdilemmái (value dilemmas of governance quality). In: Kaiser, T. (ed.): Hatékony közszolgálat és jó közigazgatás – nemzetközi és európai dimenziók (Efficient public service and good public administration - International and European dimensions). Budapest, nuPS

10. Pongrácz, A. (2015): vissza a jövőbe, avagy variációs lehetőségek a XXI. századi állam- és társadalomépítésre (Back to the future or variations for state and society building in the 21st century). Diskurzus, vol. v, No. 1, pp. 53–61

11. Pulay, Gy. (2009): A közigazgatás feladatai a versenyképes tudásgazdaság kiépítésében (The tasks of public administration in building a competitive knowledge-based economy). In: Halm, T. and vadász, J. (eds.): A modern állam feladatai (The tasks of the modern state). Budapest

12. Pulay, Gy. (2012): A jó kormányzás és a közpolitika-alkotás magyarországon (Good Governance and Public Policy-making in Hungary). Public finance Quarterly Online). Online:http://www.penzugyiszemle.hu/vitaforum/a-jo-kormanyzas-es-a-kozpolitika-alkotas-folyamata

13. Stiglitz, J. (2001): more Instruments and Broader Goals: moving Toward the Post-Washington Consensus. In: Chang and Ha-Joon (eds.): The Rebel Within: Joseph Stiglitz and the World Bank. Wimbledon Publishing Company, London pp. 17–56

14. Stumpf, I. (2009): Szakmai alapú közigazgatás – A neoweberiánus állam (Professional Public Administration. The Neo-Weberian State). In: Halm, T. and vadász, J. (eds.): A modern állam feladatai (The tasks of the modern state). Hungarian Economic Association and the Economic and Social Council. Budapest

26

S t u d y S e r I e S

Recommendations, resolutions and documents published by international and domestic organisations:15. Commission of the European Communities (2001): European governance – A white paper. In: Official

Journal C287, 10/12/2001, pp. 0001–002916. Communication from the Commission on Impact Assessment. COm (2002) 276 and Impact

Assessment Guidelines SEC (2005) 79117. Council of Europe (2007): Recommendation Cm/REC (2007) 7 of the Committee of ministers to