Embed Size (px)

Citation preview

Telecommunications and Natural Gas Industry

Telecommunications• Voice (landline, wireless)• Video (cable, satellite)• Data (cable, wireless)• Convergence– Technology• Analog -> digital

– The Internet• Data -> VoIP, Video

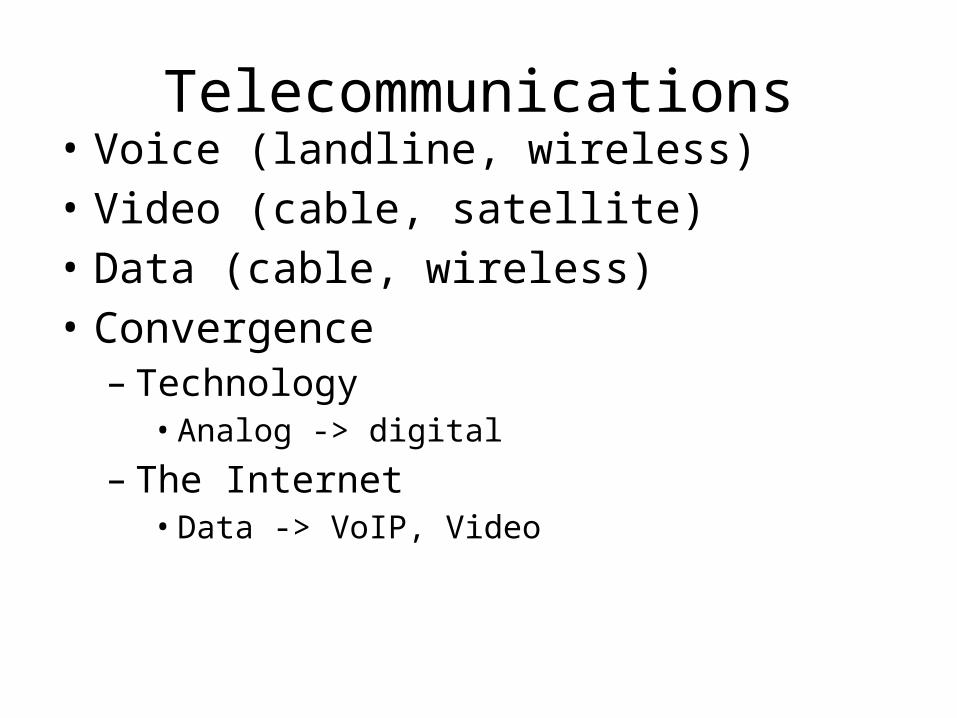

Changes• Telecommunications Act 1996– Opened more competition– FCC does not regulate nascent technologies

• Standard Products– Landline voice– High speed internet– TV/entertainment– Wireless voice/data

• Oligopoly – AT&T– Verizon

Landlines

• Mostly AT&T• Competition increases and creates distinction

of local & long distance• Market forces cause local & long distance to

no longer have a distinction

Long Distance Voice Market

• During 70s the FCC allowed other companies(MCI, Sprint) to compete with AT&T.

• http://www.youtube.com/watch?v=LCfSNdbUCXw• http://www.youtube.com/watch?v=NVAk8o7uCoU

• Competition lead to decreased prices– Transition from Public Switched Telephone Network (PSTN)

to private data networks and the Internet– Cellphones

• AT&T was still regulated until 1995.

Local Voice Market

• AT&T split into regions.• Local companies did not face competition until later than

long distance• Competitive Access Providers and Alternative Local

Transport Companies – create competition by charging lower prices for connection to

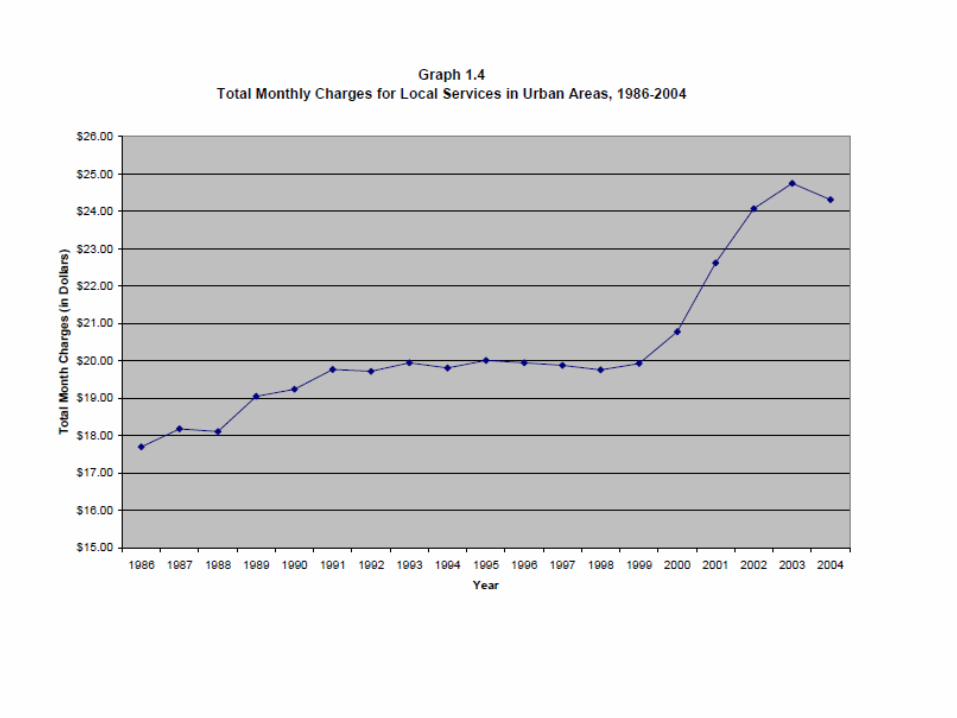

long distance providers• Barrier for competition was the number switch• Rates have increase, because of the shift from per

minute costs to per-line charges (number of users per line)

Public policies• Universal service – having a network available

to everyone– Long distance was priced above MC– Local priced below its MC

• Local rates increased but long distanced increased faster

• E-rate => lower subsidized rates for education– Voice– Internet

• Subsidy to lower rates for rural customers

Public policies

• Intercarrier compensation – long distance had to compensate local telephone networks.

• Traffic-sensitive (variable) vs. non-traffic-sensitive (fixed)

• SLC set to low => access charges too high• FCC created the Presubscribed Interexchange Carrier

Charge (PICC), local companies charge long distance companies.

• Long distance companies added PICC to new customers rather than the per-minute charges.

Public policies• Reciprocal Compensation – payments for

terminating local traffic.– CLECs would accept local traffic from long distance

companies and pass it on to ILEC as local.– Pressure to lower access costs and make

reciprocal compensation higher.– The Internet. • Example ISP customer of CLEC and internet user

customer of ILEC => lots of money for CLEC• VoIP is even more complicated• Reform in the works

Wireless Voice

• Cellular provider licenses– Landline company– Merit hearings and lotteries

• Large demand• FCC auctions permits• Spectrum cap removal created mergers• Cingular(27), Verizon(24), Sprint-Nextel (12), T-

Mobile (10)

Wireless Spectrum Auction

• US auctioned off additional spectrum that was occupied by local television stations.– Verizon– AT&T– Frontline Wireless– Google

Wireless Networks• Regional Carriers and Roaming Charges• Nationwide carrier and growth in wireless

subscribers & usage

• Pricing– AT&T Digital One Rate in 1998– Long distance landline calls decreased– Mobile-to-mobile pricing.– Contracting for service => contracting for phones– Family plans

Wireless Technology

• 2G networks– Time Division Multiple Access – Cingular and T-mobile– Code division Multiple Access – Verizon, AT&T and

Sprint

– Costly to switch technologies

• 1XRTT – adds more channels– Verizon

Video/Cable TV

• VHF and UHF channels for over-the-air broadcast (now carried over cable and satellite)

• 98.8% of homes are passed by cable• Was one-way, but is becoming two-way• Broadcast begins a slow death• Cable Act of 1992- gave broadcasters the right

to forbid retransmission without consent.

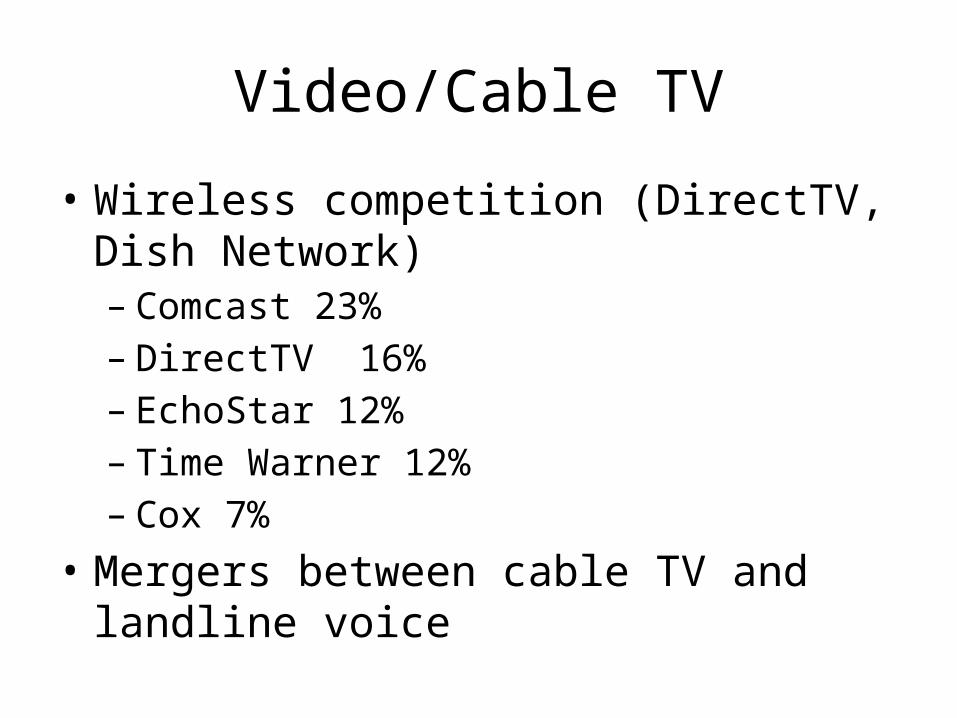

Video/Cable TV

• Wireless competition (DirectTV, Dish Network)– Comcast 23%– DirectTV 16%– EchoStar 12%– Time Warner 12%– Cox 7%

• Mergers between cable TV and landline voice

Cable TV

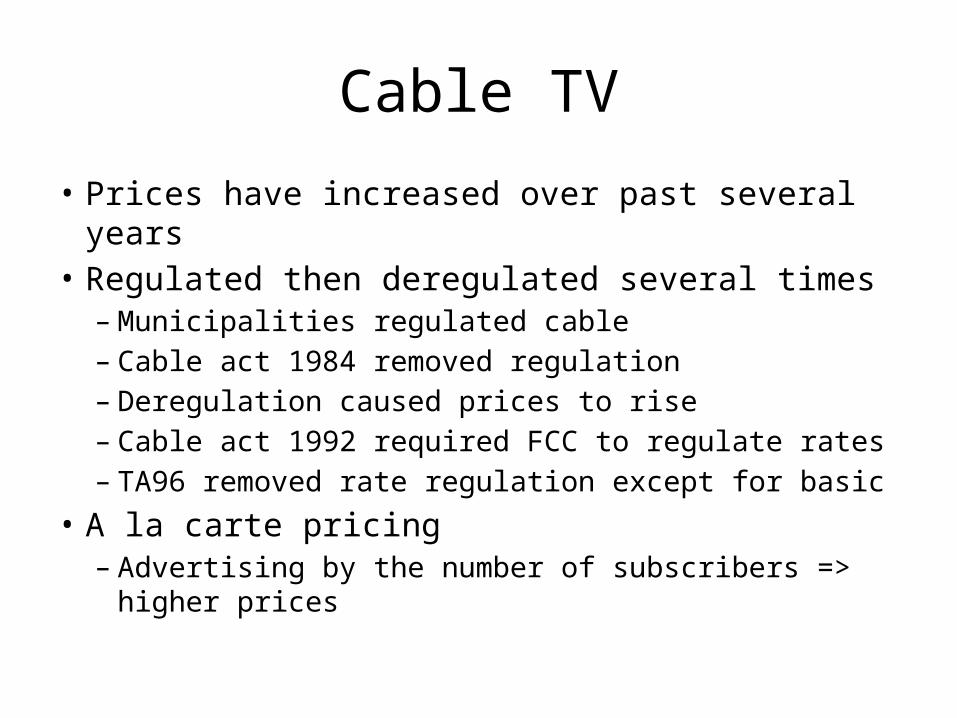

• Prices have increased over past several years• Regulated then deregulated several times– Municipalities regulated cable– Cable act 1984 removed regulation– Deregulation caused prices to rise– Cable act 1992 required FCC to regulate rates– TA96 removed rate regulation except for basic

• A la carte pricing– Advertising by the number of subscribers => higher

prices

Cable TV

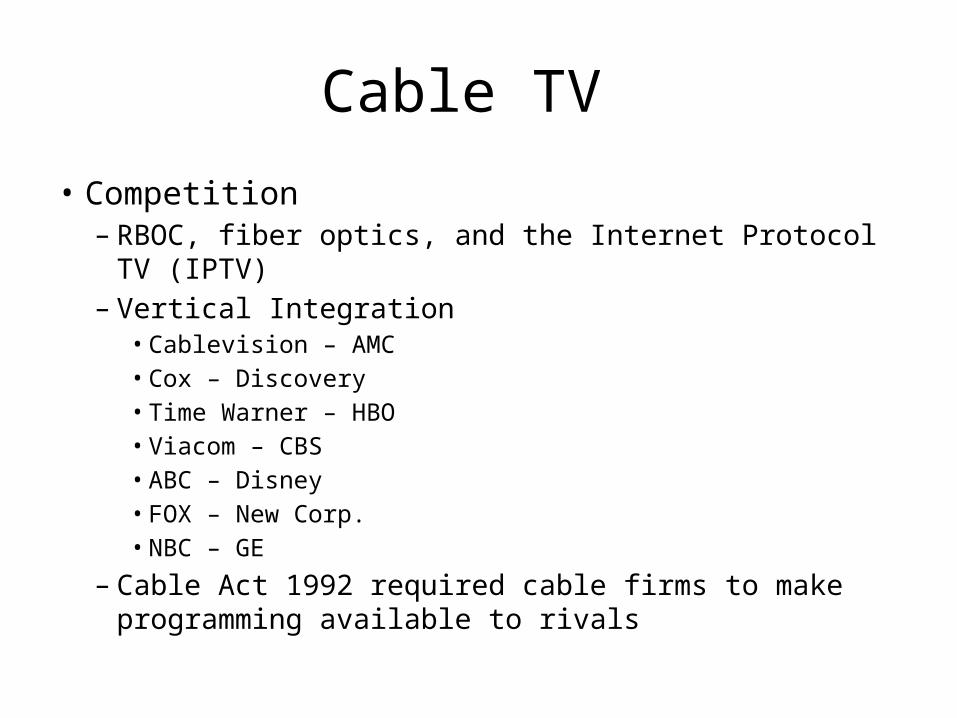

• Competition– RBOC, fiber optics, and the Internet Protocol TV (IPTV)– Vertical Integration

• Cablevision – AMC• Cox – Discovery• Time Warner – HBO• Viacom – CBS• ABC – Disney• FOX – New Corp.• NBC – GE

– Cable Act 1992 required cable firms to make programming available to rivals

Data

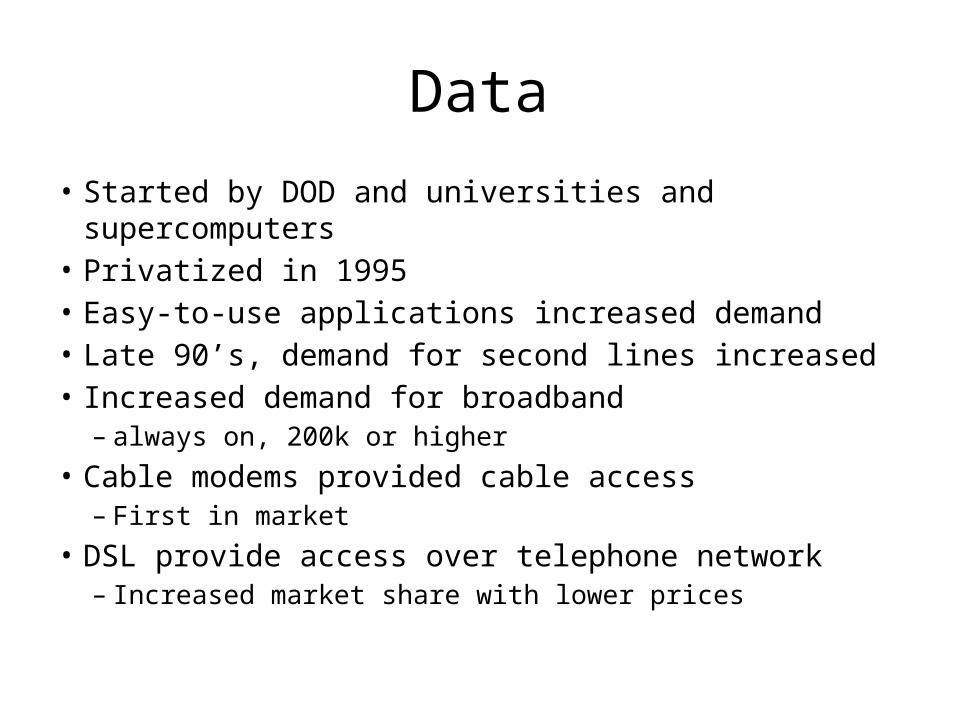

• Started by DOD and universities and supercomputers • Privatized in 1995• Easy-to-use applications increased demand• Late 90’s, demand for second lines increased• Increased demand for broadband

– always on, 200k or higher• Cable modems provided cable access

– First in market• DSL provide access over telephone network

– Increased market share with lower prices

Wireless competition and concerns• Cities and local governments building networks– Subsidies from taxpayers create unlevel playing field

• Net neutrality– Can’t charge for content, only access– Example, charge Google for sending data in a ‘faster

lane’– Criticism: paying twice for access

• 3G networks provide broadband speeds for wireless networks

Telecommunications, Conclusion

• Industry segments have begun to cross-over• Large multiple-market firms will continue to

increase market share• Government involvement in industry – assigning property rights of spectrum use– Regulating rates– Regulating access