Embed Size (px)

Citation preview

The Changing World of PaymentsJoe Divanna, Demystifying Policy Making

9/28/2017 The Changing World of Payments 2

• Why regulate? – what is the point of regulation?

• Typically Regulation is forensic

• Can regulation be proactive?

• Can regulatory structures be fast-tracked?

Story Board

9/28/2017 The Changing World of Payments 33

I only have 5 min left and 42

slides to go…

Am I

excited?

I’m still hungry

Not in my

budgetThat will

never work

with our

banks

Typical Discussion on Regulatory Issues

9/28/2017 The Changing World of Payments 4

July 2016: “Trying to regulate the financial system is like trying to predict and control the global weather system.”

Economic Storms

Regulation is easy in rough times (bail out the water),

Hard in good times (its hard to sell buckets in smooth seas).

9/28/2017 The Changing World of Payments 6

Classical and Neo-Classical economists,

believe that an economy moves

naturally towards maximum economic

welfare and full employment when its

markets were allowed to operate freely.

Why Regulate?

Adam Smith

Jean-Baptiste Say

David Ricardo

John Stuart Mill

Thomas Robert Malthus

9/28/2017 The Changing World of Payments

John Maynard Keynes response to the Great Depression clearly showed that a macro-

economy would not always automatically or quickly self-correct.

The contrast between the Classical and Keynesian perspective is often expressed in

terms of the extent to which Adam Smith’s invisible hand works, or fails, to maximise

economic welfare.

Why Regulate?

not an evidence-

based model

9/28/2017 The Changing World of Payments 8

Those on the Classical side of the argument believes

the invisible hand works , while those on the Keynesian

side generally believe it does not, and that full

employment equilibrium is a special, rather than a

general case.

This Creates the Regulator’s Dilemma

How much regulation is needed and at what time?

9/28/2017 The Changing World of Payments

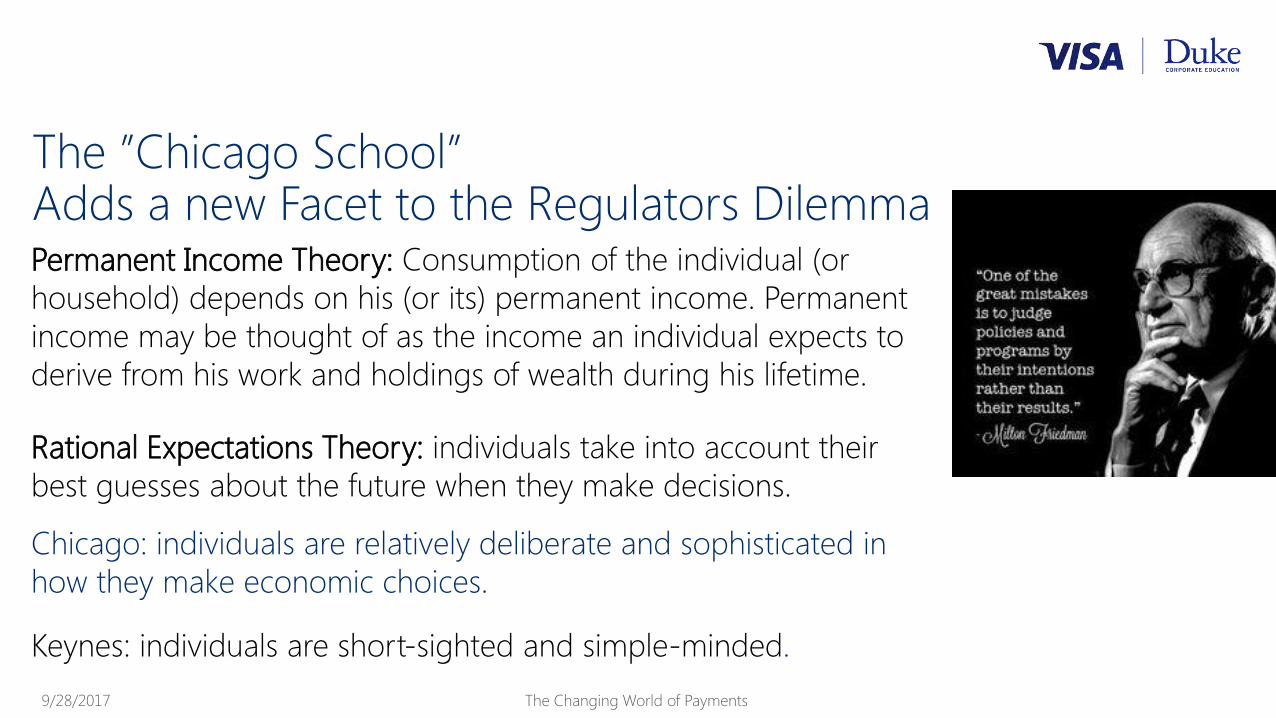

Permanent Income Theory: Consumption of the individual (or

household) depends on his (or its) permanent income. Permanent

income may be thought of as the income an individual expects to

derive from his work and holdings of wealth during his lifetime.

The ”Chicago School”Adds a new Facet to the Regulators Dilemma

Rational Expectations Theory: individuals take into account their

best guesses about the future when they make decisions.

Chicago: individuals are relatively deliberate and sophisticated in

how they make economic choices.

Keynes: individuals are short-sighted and simple-minded.

9/28/2017 The Changing World of Payments

Key Drivers in the connected economy

Non-FS PlayersTechnology giants, telcos,

NGOs

TechnologyTechnology is the key

enabler of the Internet and

fintech

ConsumerGrowing middle class and

millennial adoption

RegulationConducive regulatory

environment

AdoptionIncreasing adoption of

various forms of payment

modes

Mobile Penetration Exponentially increasing

mobile and smartphone

penetration

9/28/2017 The Changing World of Payments 11

The fundamental challenge facing policymakers is that the

costs and benefits of regulation are not shared equally across

all parts of society.

9/28/2017 The Changing World of Payments 12

Source: How to Run a Country: the burden of regulation by Richard Harries and Katy Sawyer, 2014

Regulatory Impacts

Regulatory Costs Regulatory Benefits

Direct Costs

Direct Compliance Costs

• Charges• Administrative Burden• Compliance Costs

Hassle Costs

• Corruption• Annoyance• Waiting time

Enforcement Costs

Monitoring Adjudication

Enforcement

Direct Benefits

Indirect Costs

Indirect Compliance CostsOther Indirect Costs

Substitution Efforts

Transaction Costs

Reduced• Efficiency• Competition• innovation

Wider Range of products/services

Monitoring

Health Safety

Environment

Indirect Benefits

Wider Macroeconomic

benefits

Other, non monetizable benefits

Indirect compliance

benefits

Ultimate Impacts

Well-beingHappiness

Life satisfactionEnvironmental

qualityGDP GrowthEmployment

Market Efficiency

Improved Information

Cost Savings

9/28/2017 The Changing World of Payments

What is the right balance for Payments Regulation?

Savers

Spenders

Bank’s Value Proposition

Bank’s Business Model

9/28/2017 The Changing World of Payments

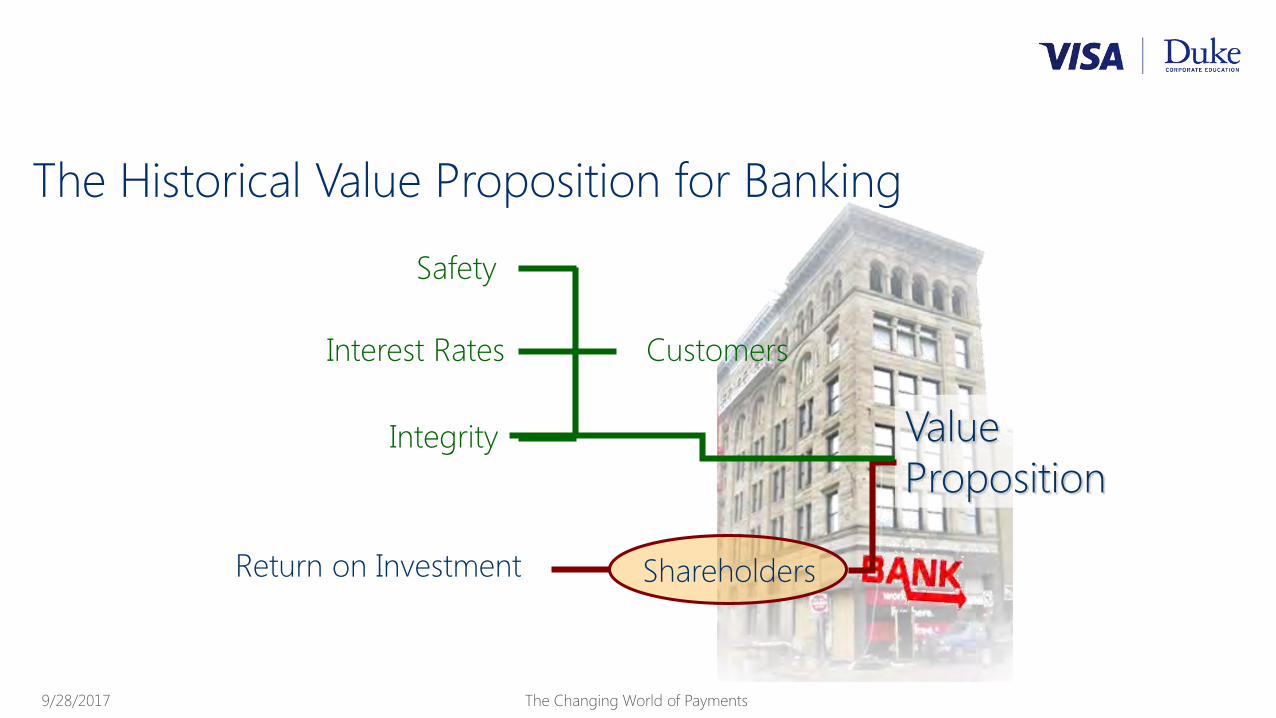

The Historical Value Proposition for Banking

Value

Proposition

Shareholders

Safety

Interest Rates

Integrity

Return on Investment

Customers

9/28/2017 The Changing World of Payments

21st Century Bank’s Value Proposition

Value

Proposition

Customers

Shareholders

Convenience

Level of

customer intimacy

Ease of use

Cost

Security

Fidelity

Corporate

values

Telephone banking

ProfitabilityGrowthCommunity standing

Treated like an account

Feel like an individual not a number

Customisation andpersonalisation of servicesLow cost High Quality

Branch(Access)

ATM(1st generation)

Expanded Hours

ATM(2nd generation)

Remote locationsExtended

reach

Internet(With linkedServices)Extendedbreath ofServices

Branch ofthe future(Advisory)Extendsdepth ofService

Physically safe Deposits insured

Accuracy of information Discretion Secrecy

Morals Ethics CommunityNationalism(keeping the profits in the country)

9/28/2017 The Changing World of Payments

Emerging 20th Century Bank’s Value Proposition

convenience

(availability/time

)

Value

Proposition

perceived value

(standardization/

customization)

value for money

(price/cost)+ +=

Short-term goal: increase shareholder value

Long-term strategy: demonstrate value to customers

9/28/2017 The Changing World of Payments

Just as Banks have Value Propositions so do Regulatory Frameworks?

Regulatory

Value

Proposition

Improve Financial System Efficiency

Protect Consumers/Investors

Facilitate growth

Balance risk in society

Provide the framework for a stronger and more productive economy

Protect the vulnerable from harm

Uphold the rights of consumers

Promote a level playing field for businesses

Spur Competition

Safeguarding the stability of the financial system

9/28/2017 The Changing World of Payments

Regulate the Business Models

1. Operator CentricOperator acts as the acquirer, payment network and

issuers

2. Bank CentricFinancial institutions own payment systems; cards

payments

3. CollaborativeCollaboration between banks and operators

4. Peer to Peer3rd party company that links customers, merchants

and bankers.

9/28/2017 The Changing World of Payments 19

9/28/2017 The Changing World of Payments 20

Retail Payments Value Chain

Web Hosting & Shopping Carts Value Added Services Gateways

• Expand sales of eCommerce

solutions by developing additional

plugins to major carts & VARs

• Develop new referral partnerships

• Incentivize acquired merchants to

sign-up for merchant services

• Enhanced gateway functionality and achieve market parity pricing

• Partner with or acquire unique functionality and customer sets

Expand into new merchant segments by integrating new features:

• Advanced Fraud Screening• Alternative Payments• Recurring Billing w/Profile Mgt.• B2C eCommerce Module• eCommerce in-a-box

Customer InternetPaymentGateway Acquirer

Issuer

eCommerceEco System

Merchant Website & Shopping Cart

Value Add Services (ex. Fraud)

Adaptive Strategic Thinking to Policy MakingCard Payments Value Chain

9/28/2017 The Changing World of Payments 21

Pure Acquiring

Transaction

capture

mechanism /

payment

gateways,

provided by

merchant

acquirers or

third parties

Card Issuer

Card HolderMerchant

Merchant Acquirer

In-house

gateway

services

Third

party

gateway

Gateway

ISV/VAR

Card

Scheme

Adaptive Strategic Thinking to Policy Making

9/28/2017 The Changing World of Payments 22

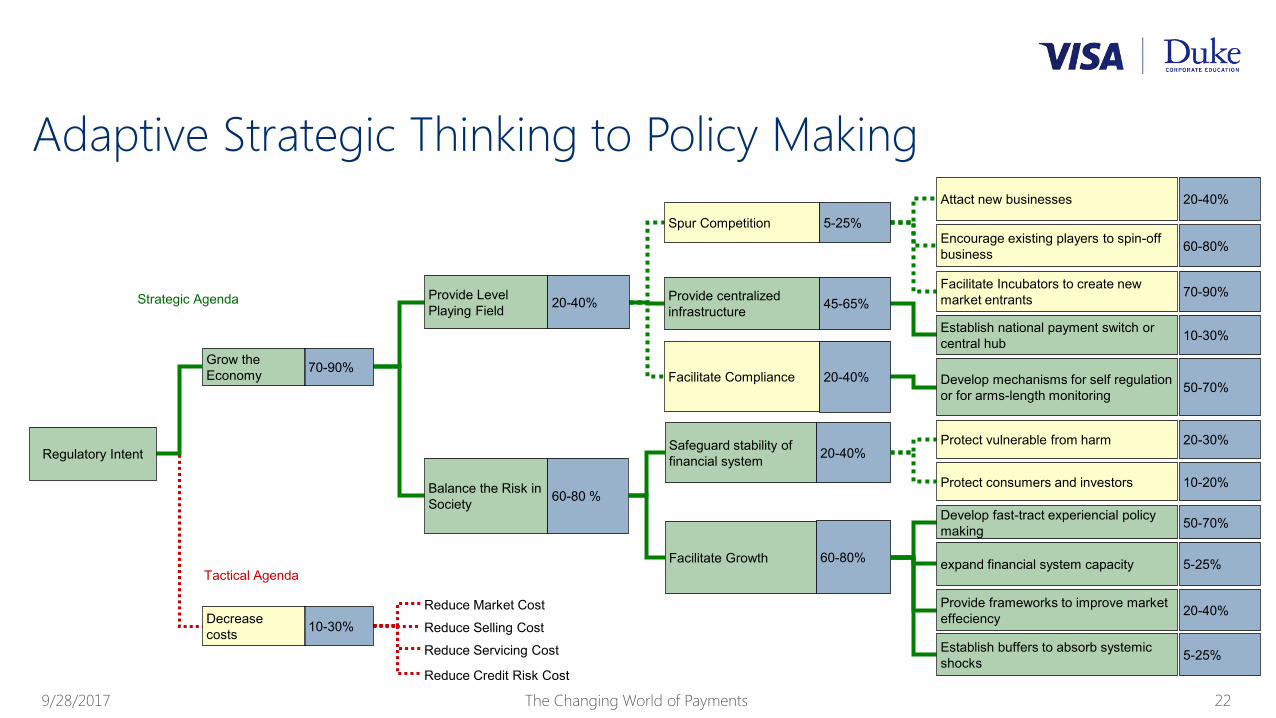

Safeguard stability of financial system 20-40%

Facilitate Growth 60-80%

Attact new businesses 20-40%

Encourage existing players to spin-off business 60-80%

Facilitate Incubators to create new market entrants 70-90%

Establish national payment switch or central hub 10-30%

Develop mechanisms for self regulation or for arms-length monitoring 50-70%

Develop fast-tract experiencial policy making 50-70%

expand financial system capacity 5-25%

Provide frameworks to improve market effeciency 20-40%

Establish buffers to absorb systemic shocks 5-25%

Protect vulnerable from harm 20-30%

Reduce Market Cost

Reduce Selling Cost

Reduce Servicing Cost

Reduce Credit Risk Cost

Balance the Risk in Society 60-80 %

Facilitate Compliance 20-40%

Provide centralized infrastructure 45-65%

Spur Competition 5-25%

Decreasecosts 10-30%

Grow the Economy 70-90%

Protect consumers and investors 10-20%

Regulatory Intent

Provide Level Playing Field 20-40%

Tactical Agenda

Strategic Agenda

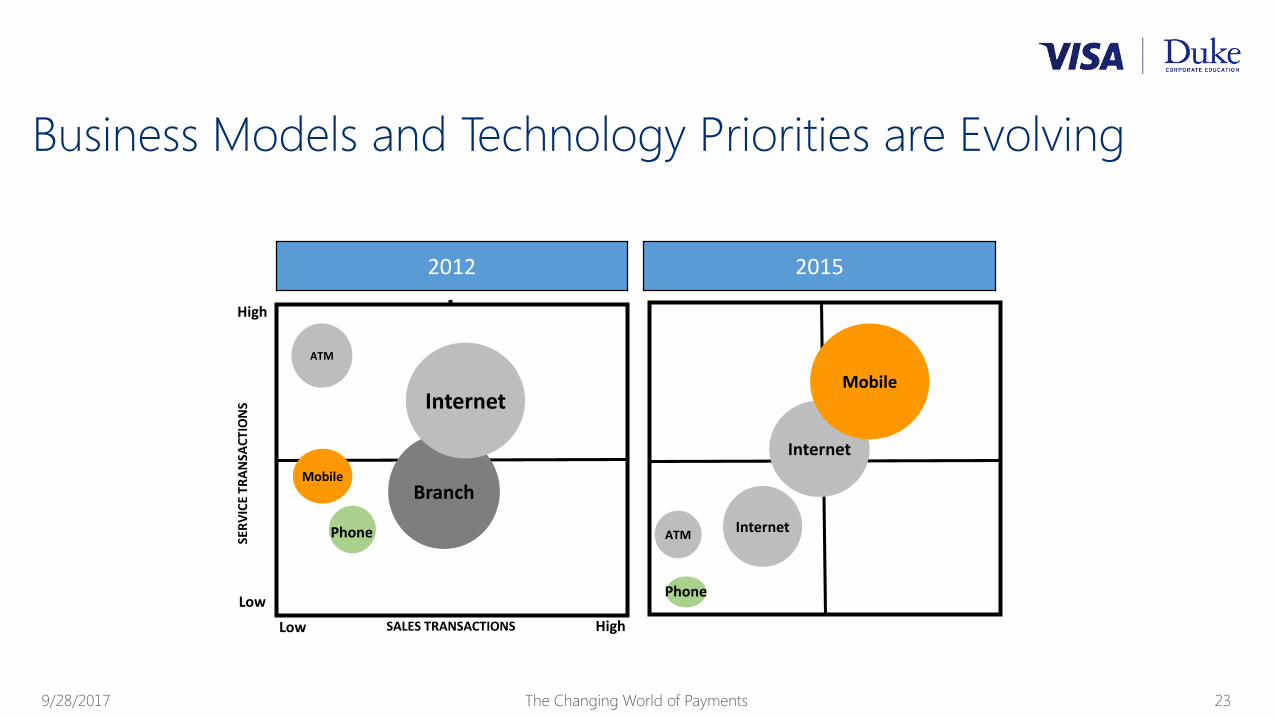

Business Models and Technology Priorities are Evolving

9/28/2017 The Changing World of Payments 23

ATM

ATMInternetPhone

Phone

2012 2015

Internet

Mobile

Branch

InternetMobile

High

High

Low

Low SALES TRANSACTIONS

SER

VIC

E TR

AN

SAC

TIO

NS

9/28/2017 The Changing World of Payments 24

Regulatory Challenge: Technology is Changing the Rules

From domestic supplier to

international distributor in 3

days, with no banks involved.

Xiamen City, Fujian Province, CHINA

Cambridge, UK

9/28/2017 The Changing World of Payments 25

$99 13.56MHz ISO14443A & NFC Type 2 NTAG216 RFID

chipset

A Regulatory Dilema:

Payment Chip in His Arm

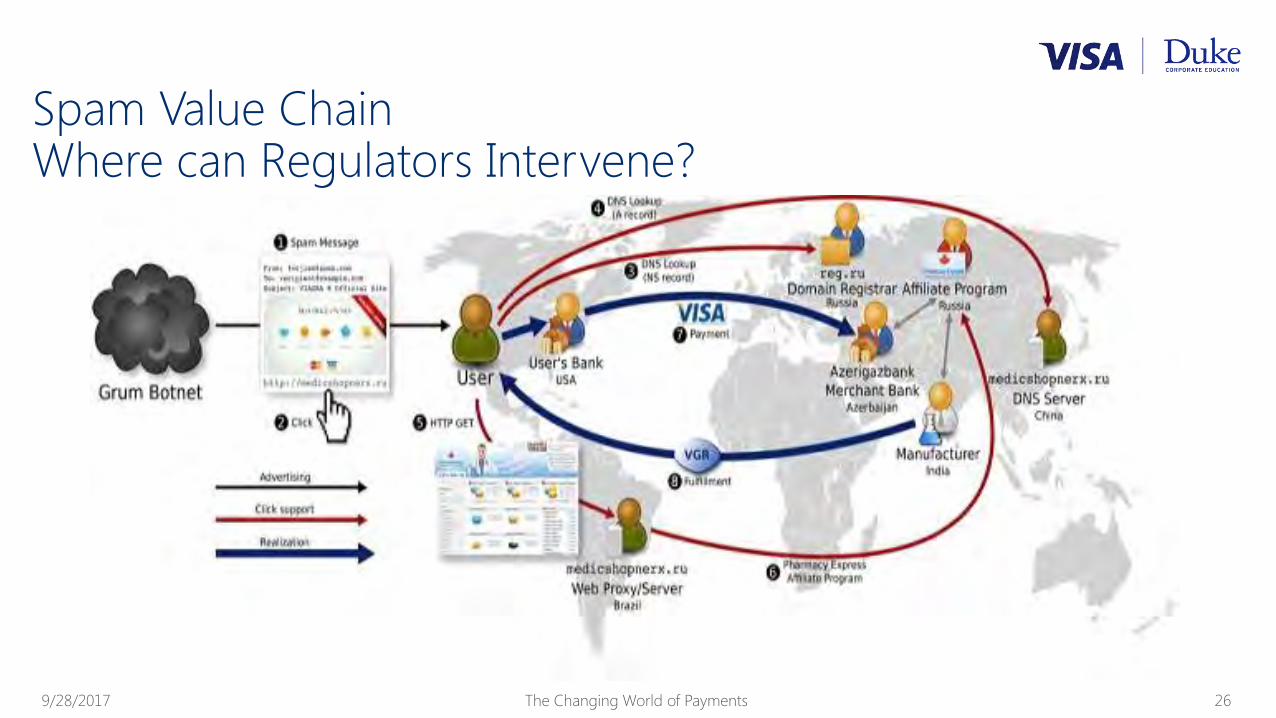

Spam Value ChainWhere can Regulators Intervene?

9/28/2017 The Changing World of Payments 26

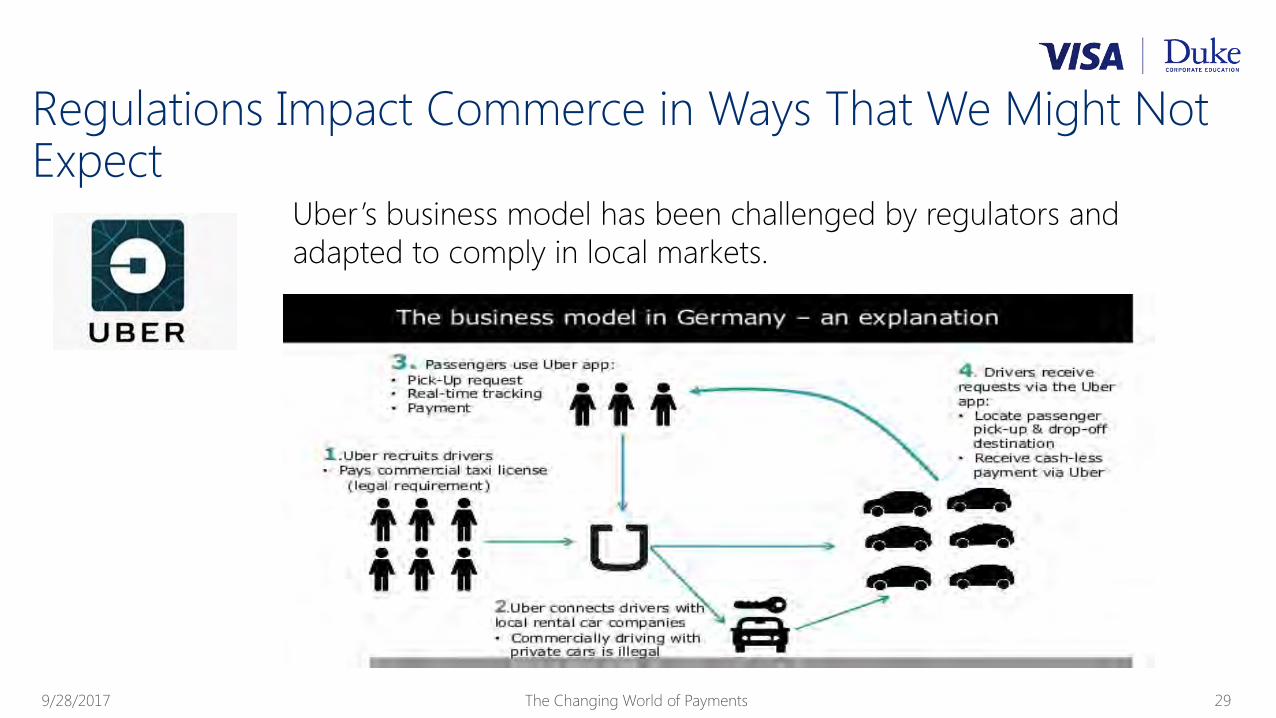

Regulations Impact Commerce in Ways That We Might Not Expect

9/28/2017 The Changing World of Payments 27

Margins in retail are notoriously

small. Best Buy has a profit margin of

~3% as does Wal-Mart. So having a

10% price advantage means that

Amazon could have had lower

prices (including tax) and still have a

higher profit.

In the beginning, Amazon.com didn’t need to collect

sales tax because of a gap in interstate regulation.

Regulations Impact Commerce in Ways That We Might Not Expect

9/28/2017 The Changing World of Payments 28

Uber disrupted a highly regulated market and again, undercut on price.

• In 2009 a license to operating a taxi in Chicago was $150k-$200k.

• Regulators set limits on how many cabs could operate and prices

charged.

• This meant that there was money to be made in driving a cab which

drove up the value of medallions.

• Uber enters and skips that whole business and just offers rides for a

fee. Bypassing regulatory costs prices could be lower.

Regulations Impact Commerce in Ways That We Might Not Expect

9/28/2017 The Changing World of Payments 29

Uber’s business model has been challenged by regulators and

adapted to comply in local markets.

9/28/2017 The Changing World of Payments 30

Now Banks are Collaborating to Form Payment Ecosystems

9/28/2017 The Changing World of Payments 31

Fast Track:a system of light touch scrutiny for deregulatory and low-cost regulatory measures.

9/28/2017 The Changing World of Payments 32

A fast track system is intended to :-

• Speed up the implementation

• Strengthen proportionality and reduce the burdens on

Departments by focusing appraisal and scrutiny on

regulatory measures with the most significant impacts

• Promote self regulation

• Collaboration based to adjust as conditions change

Challenges for Payments Regulation Today

9/28/2017 The Changing World of Payments 33

Constant changes in technology, society and

demographics is rapidly altering the financial

markets, which requires more complex

monitoring.

An increasing number of policy and regulatory

stakeholders are focusing in payments creating new

levels of uncertainty.

The rate and pace of change is

compromising the effectiveness of existing

legislation and regulatory structures.

Currently, the view of regulators is to encourage innovation in fintech by restrained supervision, this is the ethos of the ‘Sandbox’ similar to technology incubators

9/28/2017 The Changing World of Payments 34

Some countries view a Sandbox as a non-intervention environment until the

initiative has scale and other view it as ongoing light monitoring.

Regulators help innovation when they:

• act pragmatically in the application of

rules (to remove the dogma of

compliance),

• observe/ monitor closely the innovators

through Sandboxes

• have a thorough understanding of the

areas through running Sandboxes

• are able to act decisively to level the

playing field or pass an Act to allow the

equivalent infrastructure to be built.

Attributes Regulators are considering:

• Payment services often are the entry point into

using formal financial services

• Poor regulation is one of the major obstacles to

financial inclusion.

• Lack of good infrastructure slows implementation

• Weak institutions and poor cooperation restricts

capacity

• Unstable economic and political conditions reduce

innovation and adoption.

9/28/2017 The Changing World of Payments 35

28.9.2017 г. The Changing World of Payments 35

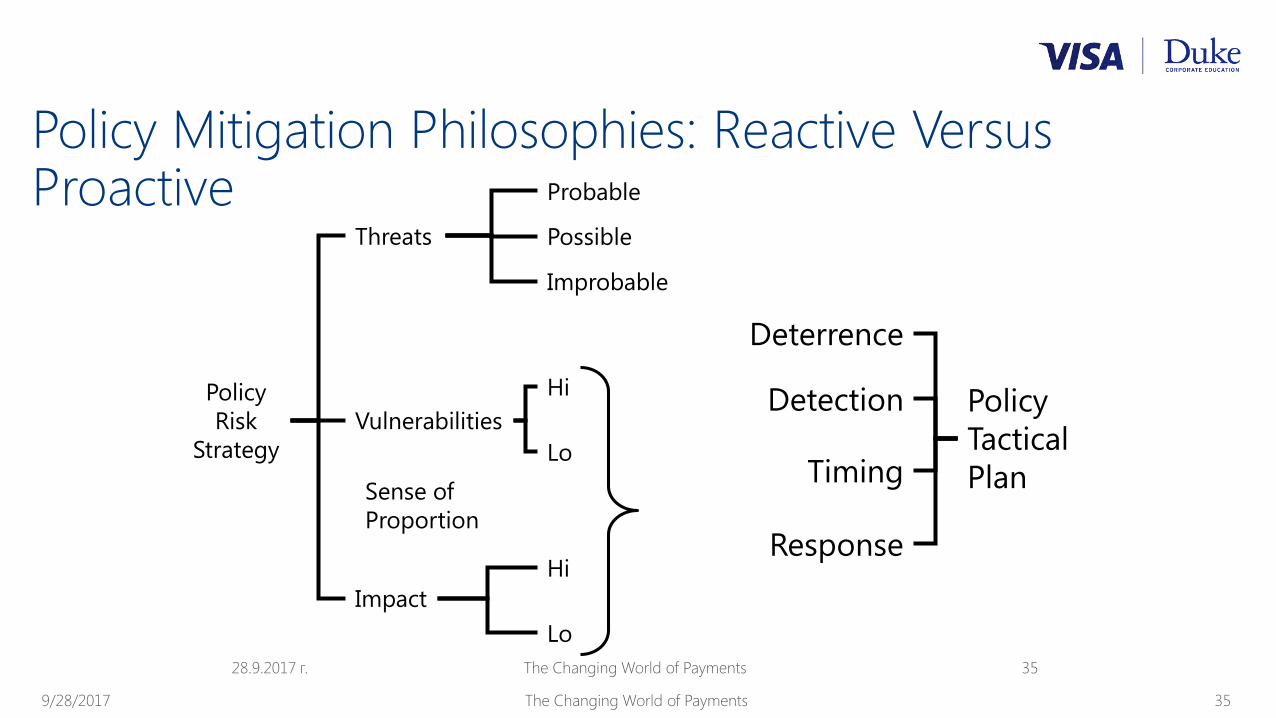

Policy

Risk

Strategy

Threats

Vulnerabilities

Impact

Probable

Improbable

Possible

Hi

Lo

Hi

Lo

Sense of

Proportion

Deterrence

Detection

Timing

Response

Policy

Tactical

Plan

Policy Mitigation Philosophies: Reactive Versus Proactive

Policy Mitigation Philosophies:Reactive Versus Proactive

9/28/2017 The Changing World of Payments 36

Interoperability as a market solution

In Tanzania, interoperability in the mobile-payments market

emerged as a market solution through an industry-wide

process facilitated by the International Finance Corporation

(IFC) who acted as an impartial broker between participants.

The regulator’s stated preference was for the market to reach

interoperability on its own.

Airtel, Tigo, and Zantel became interoperable on September

2014. Vodacom joined in early 2016.

Policy Philosophies: Reactive Versus Proactive

9/28/2017 The Changing World of Payments 37

Partial interoperability through ex-post regulation

In Kenya, business incentives created by an ex post regulatory

approach led to partial interoperability.

M-Pesa operated on a trial basis for 7 years which lead to the

National Payments Systems Act.

Safaricom’s M-Pesa, the leading mobile money service, lacks full

interoperability with services offered by other operators.

Kenyan authorities were concerned about the high-level of agent

exclusivity (before July 2014, 96 percent of agents were serving one

provider exclusively).

In July 2014, Safaricom opened up its M-Pesa network of 85,000

agents to competitors just before the Competition Authority of

Kenya ordered it to do so.

9/28/2017 The Changing World of Payments 38

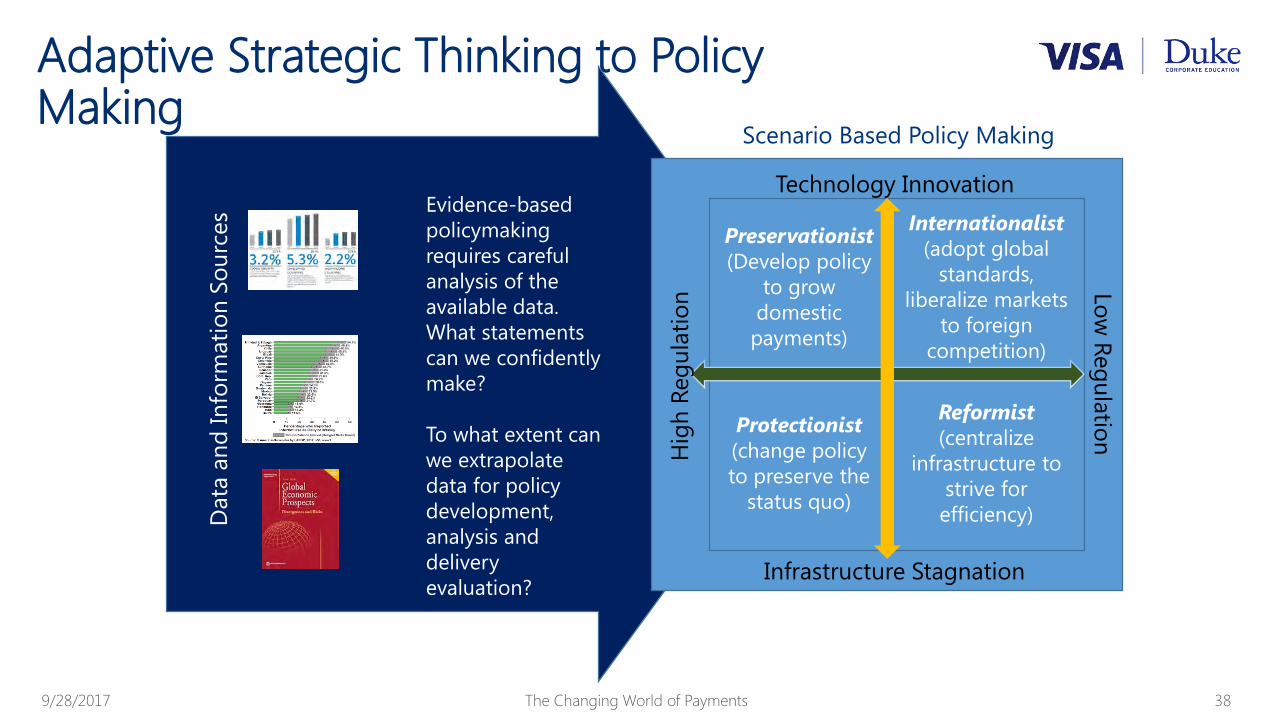

Adaptive Strategic Thinking to Policy Making

Evidence-based

policymaking

requires careful

analysis of the

available data.

What statements

can we confidently

make?

To what extent can

we extrapolate

data for policy

development,

analysis and

delivery

evaluation?

Data

an

d In

form

ati

on

So

urc

es

Preservationist

(Develop policy

to grow

domestic

payments)

Internationalist

(adopt global

standards,

liberalize markets

to foreign

competition)

Protectionist

(change policy

to preserve the

status quo)

Reformist

(centralize

infrastructure to

strive for

efficiency)

Technology Innovation

Infrastructure Stagnation

Hig

h R

eg

ula

tio

n

Lo

w R

eg

ula

tion

Scenario Based Policy Making

The Changing World of PaymentsJoe Divanna, Payments Industry: Global & Regional Trends

Storyboard

Global Trends

• Political, economic and financial

Regional Trends

• Social, demographic and traditional

• How do they apply to the local markets

9/28/2017 The Changing World of Payments 2

Global trends that Regulators should have seen on their radar

9/28/2017 The Changing World of Payments 3

Emerging Markets

Consumer and Demographics

Developments in Competitors

Technology Advances

Macroeconomic Directions

9/28/2017 The Changing World of Payments 4

CHANGE IN WORLD ECONOMIC ORDERHas the Americanization of the World Ended?

CHANGES IN ECONOMIC ACTIVITYWill emerging economies surpass service economies?

CHANGES IN NATIONAL POLICIES AND REGULATIONIs free market capitalism an answer or a question?

CHANGES IN AGGREGATE CONSUMER BEHAVIORWill global consumerism initiate a

global battle for natural resources?

Macr

oeco

no

mic

Direct

ions

9/28/2017 The Changing World of Payments 5

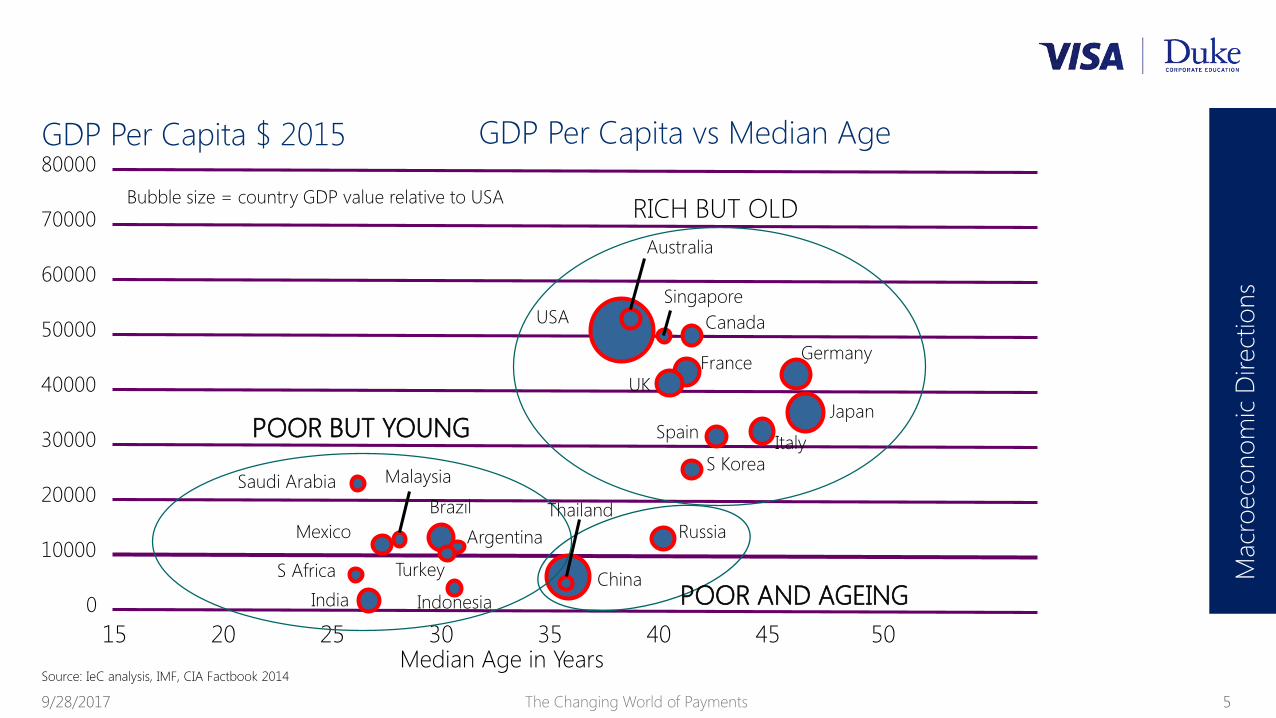

GDP Per Capita vs Median Age 80000

70000

60000

50000

40000

30000

20000

10000

0

Australia

Germany

Canada

Japan

USA

FranceUK

ItalySpain

S Korea

Russia

China

Saudi Arabia

Mexico

Brazil

Argentina

Turkey

Indonesia

S Africa

India

Bubble size = country GDP value relative to USA

GDP Per Capita $ 2015

15 20 25 30 35 40 45 50Median Age in Years

POOR BUT YOUNG

RICH BUT OLD

POOR AND AGEING

Singapore

Malaysia

Thailand

Macr

oeco

no

mic

Direct

ions

Source: IeC analysis, IMF, CIA Factbook 2014

9/28/2017 The Changing World of Payments 6

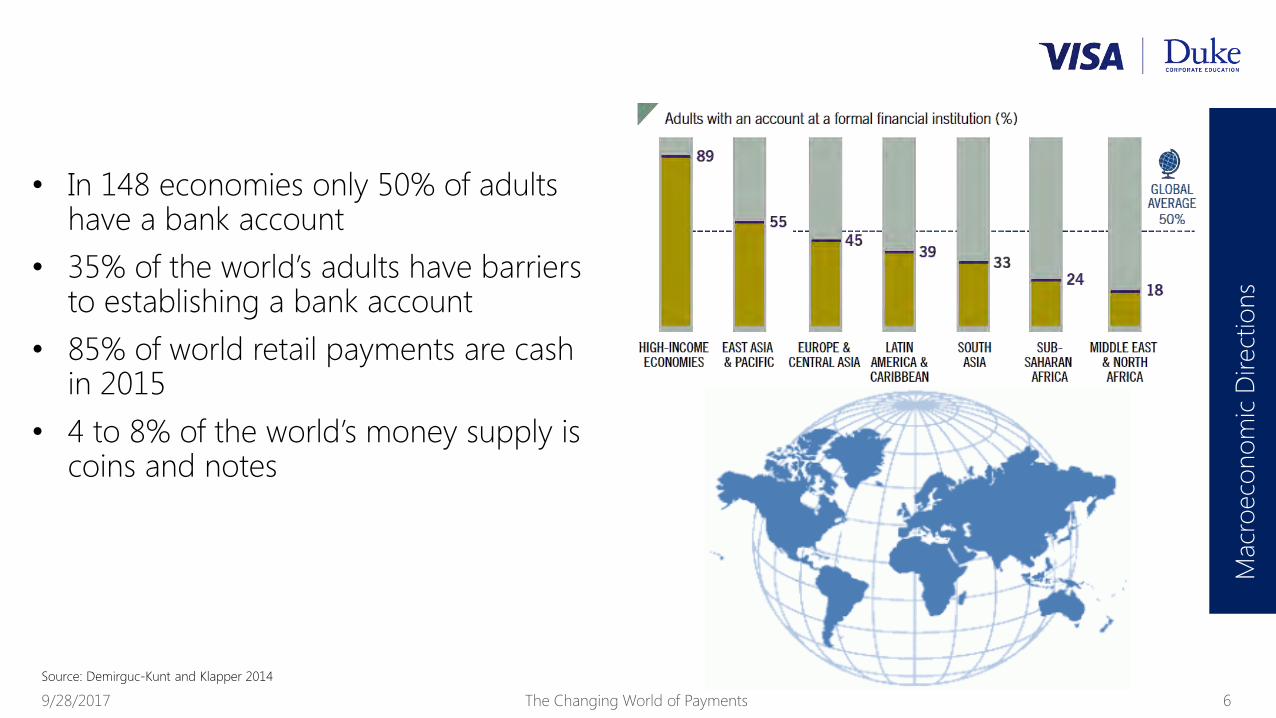

• In 148 economies only 50% of adults have a bank account

• 35% of the world’s adults have barriers to establishing a bank account

• 85% of world retail payments are cash in 2015

• 4 to 8% of the world’s money supply is coins and notes

Macr

oeco

no

mic

Direct

ions

Source: Demirguc-Kunt and Klapper 2014

9/28/2017 The Changing World of Payments 7

Em

erg

ing

Mark

ets

Source: UN Habitat 2015

9/28/2017 The Changing World of Payments 8

Interpreting Trends:Gauging Economic Growth

Tower Cranes TrafficTourism

Em

erg

ing

Mark

ets

9/28/2017 The Changing World of Payments 9

Interpreting Trends:Gauging Economic Growth

Em

erg

ing

Mark

ets

Many Choices

Checkers

Eco Marche

Leader Price

Lulu Hypermarket

Metro

Park 'n' Shop

Pick n Pay

Shoprite

Spar

Woolworths

Fewer Choices

Is my life getting

better using this

bank?

Commissions, charges

and fees how is this

making me wealthy?

I don’t understand, I deposit

my money so they can lend it

out to other people to make

a profit. They pay me very

little interest and I have to

pay fee for this privilege?

The New Customer Centric KPI’s

9/28/2017 The Changing World of Payments 10

Co

nsu

mer

and

Dem

og

rap

hic

s

9/28/2017 The Changing World of Payments 11

iPod People

Co

nsu

mer

and

Dem

og

rap

hic

s

9/28/2017 The Changing World of Payments 12

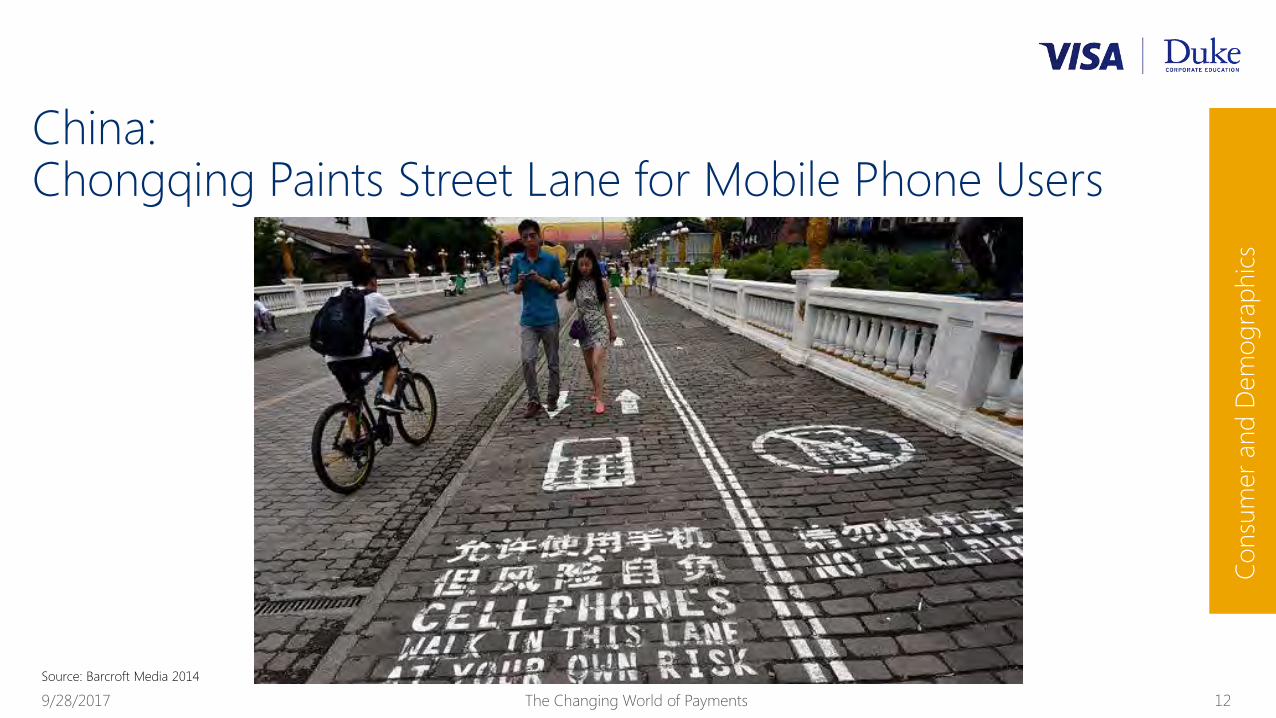

China:Chongqing Paints Street Lane for Mobile Phone Users

Co

nsu

mer

and

Dem

og

rap

hic

s

Source: Barcroft Media 2014

9/28/2017 The Changing World of Payments 13

Millennials

Co

nsu

mer

and

Dem

og

rap

hic

s

Source: Commonwealth Bank,

2016

9/28/2017 The Changing World of Payments 14

Facebook, London, August 1935

Co

nsu

mer

and

Dem

og

rap

hic

s

Source: Modern Mechanix, 1935

9/28/2017 The Changing World of Payments 15

New Financial Behaviours

Co

nsu

mer

and

Dem

og

rap

hic

s

Source: Maybank, 2016

9/28/2017 The Changing World of Payments 16

Five General Observations• Regulators have been late to react to social economic

changes and innovations in banking

• Customers in many markets demand more services and

are becoming fee conscience

• The higher your social/economic standing the less cash

you carry in proportion to your wealth

• The less money you have, the more debt you

accumulate

• An increasing number of factors that determine a bank’s

performance are beyond the bank’s direct control

Co

nsu

mer

and

Dem

og

rap

hic

s

21st Century Financial Services

9/28/2017 The Changing World of Payments 17

Top 10 Cross Border Payment Systems in Asia

Deve

lop

ments

in C

om

petito

rs

Source: trulioo.com, 2016

9/28/2017 The Changing World of Payments 18

Deve

lop

ments

in C

om

petito

rs

Source: Skrill.com, 2016

9/28/2017 The Changing World of Payments 19

Deve

lop

ments

in C

om

petito

rsIn most of Africa it has not been

financially viable for banks to

offer last-mile services.

African Fintech is not disrupting anything

Source: World Bank, 2011

9/28/2017 The Changing World of Payments 20

Deve

lop

ments

in C

om

petito

rs

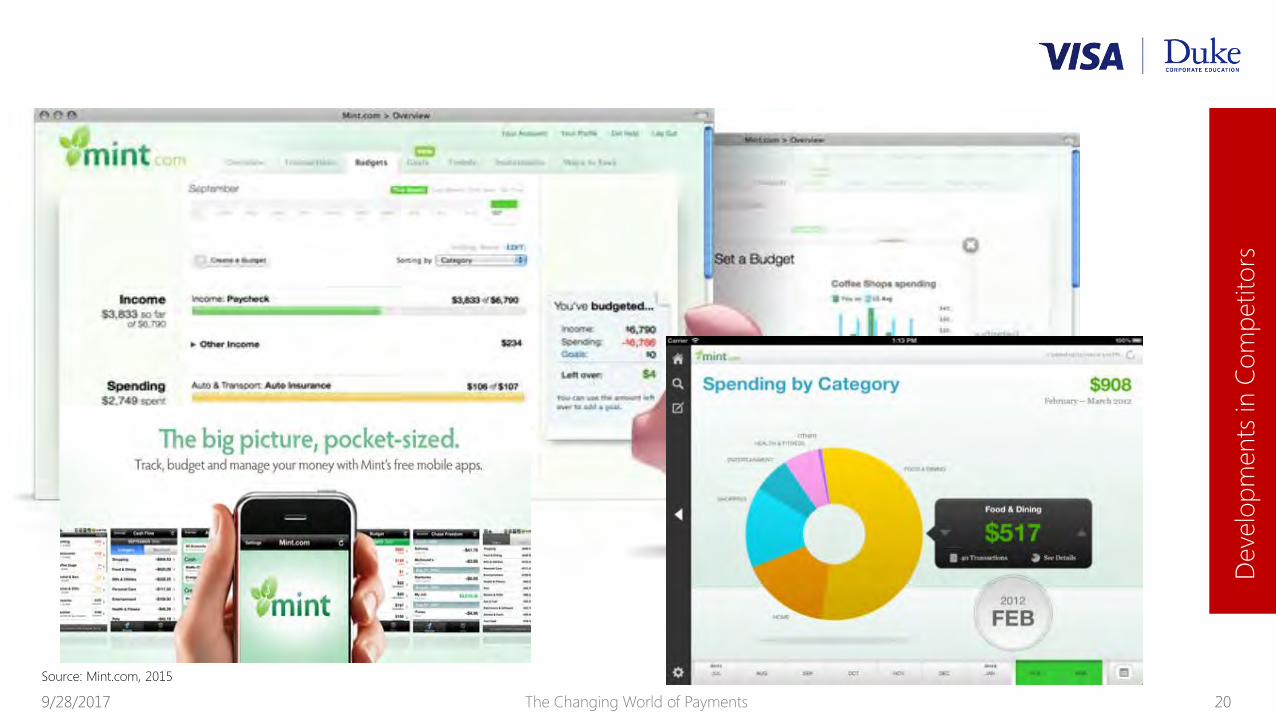

Source: Mint.com, 2015

9/28/2017 The Changing World of Payments 21

Deve

lop

ments

in C

om

petito

rs

Source: Digital money forum, 2015

9/28/2017 The Changing World of Payments 22

Tech

no

log

y A

dva

nce

s

Source: UBank, 2015

9/28/2017 The Changing World of Payments 23

Tech

no

log

y A

dva

nce

s

Source: Citibank, 2016

9/28/2017 The Changing World of Payments 24

Tech

no

log

y A

dva

nce

s

Source: Citibank, 2016