Embed Size (px)

Citation preview

The Governance Role of AccountingInformation

Pingyang Gao

Chicago Booth

SWUFE Workshop

July 1, 2016

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 1 / 1

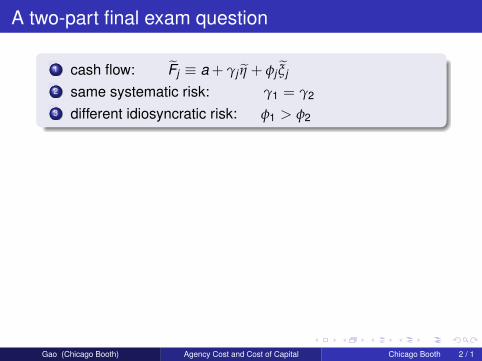

A two-part final exam question

1 cash flow: Fj ≡ a + γj η + φj ξj

2 same systematic risk: γ1 = γ2

3 different idiosyncratic risk: φ1 > φ2

Q1: which has a higher cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Q2: which has a higher implied cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 2 / 1

A two-part final exam question

1 cash flow: Fj ≡ a + γj η + φj ξj

2 same systematic risk: γ1 = γ2

3 different idiosyncratic risk: φ1 > φ2

Q1: which has a higher cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Q2: which has a higher implied cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 2 / 1

A two-part final exam question

1 cash flow: Fj ≡ a + γj η + φj ξj

2 same systematic risk: γ1 = γ2

3 different idiosyncratic risk: φ1 > φ2

Q1: which has a higher cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Q2: which has a higher implied cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 2 / 1

A two-part final exam question

1 cash flow: Fj ≡ a + γj η + φj ξj

2 same systematic risk: γ1 = γ2

3 different idiosyncratic risk: φ1 > φ2

Q1: which has a higher cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Q2: which has a higher implied cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 2 / 1

A two-part final exam question

1 cash flow: Fj ≡ a + γj η + φj ξj

2 same systematic risk: γ1 = γ2

3 different idiosyncratic risk: φ1 > φ2

Q1: which has a higher cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Q2: which has a higher implied cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 2 / 1

A two-part final exam question

1 cash flow: Fj ≡ a + γj η + φj ξj

2 same systematic risk: γ1 = γ2

3 different idiosyncratic risk: φ1 > φ2

Q1: which has a higher cost of capital?a ∆1 = ∆2 correct without moral hazard

b ∆1 > ∆2

Q2: which has a higher implied cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 2 / 1

A two-part final exam question

1 cash flow: Fj ≡ a + γj η + φj ξj

2 same systematic risk: γ1 = γ2

3 different idiosyncratic risk: φ1 > φ2

Q1: which has a higher cost of capital?a ∆1 = ∆2 correct without moral hazard

b ∆1 > ∆2 correct with moral hazard

Q2: which has a higher implied cost of capital?a ∆1 = ∆2

b ∆1 > ∆2

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 2 / 1

A two-part final exam question

1 cash flow: Fj ≡ a + γj η + φj ξj

2 same systematic risk: γ1 = γ2

3 different idiosyncratic risk: φ1 > φ2

Q1: which has a higher cost of capital?a ∆1 = ∆2 correct without moral hazard

b ∆1 > ∆2 correct with moral hazard

Q2: which has a higher implied cost of capital?a ∆1 = ∆2 correct regardless of moral hazard

b ∆1 > ∆2

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 2 / 1

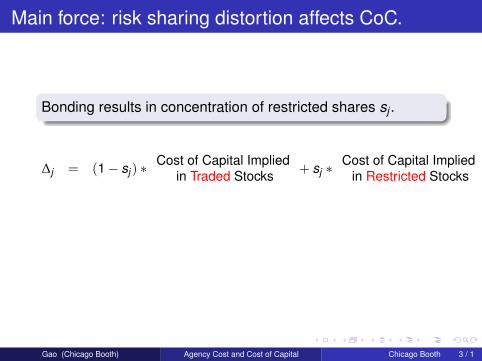

Main force: risk sharing distortion affects CoC.

Bonding results in concentration of restricted shares sj .

∆j

= (1− sj ) ∗Cost of Capital Implied

in Traded Stocks + sj ∗Cost of Capital Implied

in Restricted Stocks= Invisible

=Firm j’s

CAPM Beta ×Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+Risk Premium ofIdiosyncratic Risk

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 3 / 1

Main force: risk sharing distortion affects CoC.

Bonding results in concentration of restricted shares sj .

∆j = (1− sj ) ∗Cost of Capital Implied

in Traded Stocks + sj ∗Cost of Capital Implied

in Restricted Stocks

= Invisible

=Firm j’s

CAPM Beta ×Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+Risk Premium ofIdiosyncratic Risk

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 3 / 1

Main force: risk sharing distortion affects CoC.

Bonding results in concentration of restricted shares sj .

∆j = (1− sj ) ∗Cost of Capital Implied

in Traded Stocks + sj ∗Cost of Capital Implied

in Restricted Stocks

= Invisible

=Firm j’s

CAPM Beta ×Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+Risk Premium ofIdiosyncratic Risk

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 3 / 1

Main force: risk sharing distortion affects CoC.

Bonding results in concentration of restricted shares sj .

∆j = (1− sj ) ∗Cost of Capital Implied

in Traded Stocks + sj ∗Cost of Capital Implied

in Restricted Stocks

= Invisible

=Firm j’s

CAPM Beta ×Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+Risk Premium ofIdiosyncratic Risk

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 3 / 1

Intuition for the wedge

1 Restricted stocks are issued to the manager as bonding.

2 Concentrated idiosyncratic risk is useful for incentives butcostly to the firm.

3 Systematic risk is filtered out for incentives and optimallyshared in the market.

4 Implied CoC from traded shares v.s. the true financingcost to the firm.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 4 / 1

Intuition for the wedge

1 Restricted stocks are issued to the manager as bonding.

2 Concentrated idiosyncratic risk is useful for incentives butcostly to the firm.

3 Systematic risk is filtered out for incentives and optimallyshared in the market.

4 Implied CoC from traded shares v.s. the true financingcost to the firm.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 4 / 1

Intuition for the wedge

1 Restricted stocks are issued to the manager as bonding.

2 Concentrated idiosyncratic risk is useful for incentives butcostly to the firm.

3 Systematic risk is filtered out for incentives and optimallyshared in the market.

4 Implied CoC from traded shares v.s. the true financingcost to the firm.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 4 / 1

Intuition for the wedge

1 Restricted stocks are issued to the manager as bonding.

2 Concentrated idiosyncratic risk is useful for incentives butcostly to the firm.

3 Systematic risk is filtered out for incentives and optimallyshared in the market.

4 Implied CoC from traded shares v.s. the true financingcost to the firm.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 4 / 1

Main results

1 Idio info reduces use of restricted shares and CoC.2 Implied CoC systematically bias downward the true CoC.3 Economy level idio info quality can increase CoC.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 5 / 1

The model

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 6 / 1

A general equilibrium model with three sub-problems

Moral hazard and optimal compensation contract withineach firm

Personal portfolio management of both managers andinvestorsInvestors’ project selection decisions for each firm

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 7 / 1

A general equilibrium model with three sub-problems

Moral hazard and optimal compensation contract withineach firmPersonal portfolio management of both managers andinvestors

Investors’ project selection decisions for each firm

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 7 / 1

A general equilibrium model with three sub-problems

Moral hazard and optimal compensation contract withineach firmPersonal portfolio management of both managers andinvestorsInvestors’ project selection decisions for each firm

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 7 / 1

The timeline

1 Each investor is endowed with a project, hires a managerwith a compensation package, sells the project, andinvests

2 Each manager receives a contract, chooses an effort, andinvests

3 Projects pay off and all consume.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 8 / 1

The timeline

1 Each investor is endowed with a project, hires a managerwith a compensation package, sells the project, andinvests

2 Each manager receives a contract, chooses an effort, andinvests

3 Projects pay off and all consume.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 8 / 1

The timeline

1 Each investor is endowed with a project, hires a managerwith a compensation package, sells the project, andinvests

2 Each manager receives a contract, chooses an effort, andinvests

3 Projects pay off and all consume.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 8 / 1

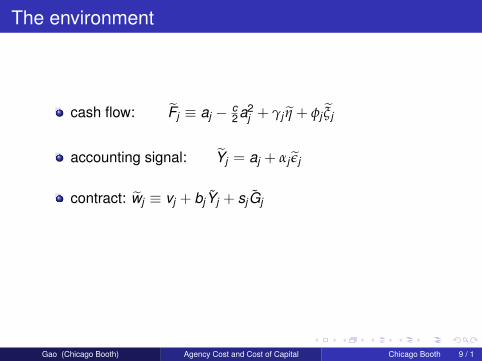

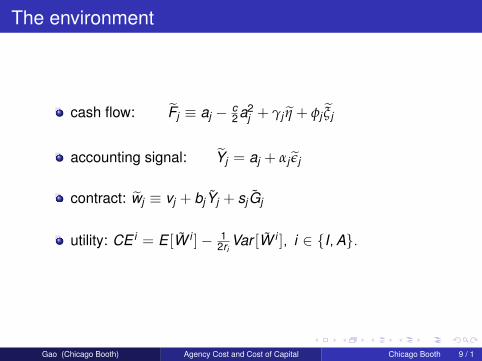

The environment

cash flow: Fj ≡ aj − c2a2

j + γj η + φj ξj

accounting signal: Yj = aj + αj εj

contract: wj ≡ vj + bj Yj + sjGj

utility: CE i = E [W i ]− 12ri

Var [W i ], i ∈ I,A.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 9 / 1

The environment

cash flow: Fj ≡ aj − c2a2

j + γj η + φj ξj

accounting signal: Yj = aj + αj εj

contract: wj ≡ vj + bj Yj + sjGj

utility: CE i = E [W i ]− 12ri

Var [W i ], i ∈ I,A.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 9 / 1

The environment

cash flow: Fj ≡ aj − c2a2

j + γj η + φj ξj

accounting signal: Yj = aj + αj εj

contract: wj ≡ vj + bj Yj + sjGj

utility: CE i = E [W i ]− 12ri

Var [W i ], i ∈ I,A.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 9 / 1

The environment

cash flow: Fj ≡ aj − c2a2

j + γj η + φj ξj

accounting signal: Yj = aj + αj εj

contract: wj ≡ vj + bj Yj + sjGj

utility: CE i = E [W i ]− 12ri

Var [W i ], i ∈ I,A.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 9 / 1

Problem 1: moral hazard

The manager chooses an effort.

wj = vj︸︷︷︸Base

Salary

+ bj Yj︸︷︷︸Earnings-based

Bonus

+ sj (Fj − bj Yj )︸ ︷︷ ︸Restricted

Stocks

− c2

a2j︸︷︷︸

EffortCost

+ zj (∫

i∈Ω(1− si )(Fi − bi Yi )di − p)︸ ︷︷ ︸

MarketPortfolio

= (bj + (1− bj )sj )aj −c2

a2j + vj + (E [M ]− p)

= Invisible

+ bj (1− sj )αj ε j︸ ︷︷ ︸Idiosyncratic

Measurement error

+ sj φj ξj︸ ︷︷ ︸Idiosyncratic

Cash Flow Risk

+ (sj γj + zj (Avg[γ]− Avg[rs ]))η︸ ︷︷ ︸Systematic

Cash Flow Risk

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 10 / 1

Problem 1: moral hazard

The manager chooses an effort.

wj = vj︸︷︷︸Base

Salary

+ bj Yj︸︷︷︸Earnings-based

Bonus

+ sj (Fj − bj Yj )︸ ︷︷ ︸Restricted

Stocks

− c2

a2j︸︷︷︸

EffortCost

+ zj (∫

i∈Ω(1− si )(Fi − bi Yi )di − p)︸ ︷︷ ︸

MarketPortfolio

= (bj + (1− bj )sj )aj −c2

a2j + vj + (E [M ]− p)

= Invisible

+ bj (1− sj )αj ε j︸ ︷︷ ︸Idiosyncratic

Measurement error

+ sj φj ξj︸ ︷︷ ︸Idiosyncratic

Cash Flow Risk

+ (sj γj + zj (Avg[γ]− Avg[rs ]))η︸ ︷︷ ︸Systematic

Cash Flow Risk

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 10 / 1

Problem 1: moral hazard

The manager chooses an effort.

wj = vj︸︷︷︸Base

Salary

+ bj Yj︸︷︷︸Earnings-based

Bonus

+ sj (Fj − bj Yj )︸ ︷︷ ︸Restricted

Stocks

− c2

a2j︸︷︷︸

EffortCost

+ zj (∫

i∈Ω(1− si )(Fi − bi Yi )di − p)︸ ︷︷ ︸

MarketPortfolio

= (bj + (1− bj )sj )aj −c2

a2j + vj + (E [M ]− p)

= Invisible

+ bj (1− sj )αj ε j︸ ︷︷ ︸Idiosyncratic

Measurement error

+ sj φj ξj︸ ︷︷ ︸Idiosyncratic

Cash Flow Risk

+ (sj γj + zj (Avg[γ]− Avg[rs ]))η︸ ︷︷ ︸Systematic

Cash Flow Risk

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 10 / 1

Problem 1: moral hazard

The manager chooses an effort.

wj = vj︸︷︷︸Base

Salary

+ bj Yj︸︷︷︸Earnings-based

Bonus

+ sj (Fj − bj Yj )︸ ︷︷ ︸Restricted

Stocks

− c2

a2j︸︷︷︸

EffortCost

+ zj (∫

i∈Ω(1− si )(Fi − bi Yi )di − p)︸ ︷︷ ︸

MarketPortfolio

= (bj + (1− bj )sj )aj −c2

a2j + vj + (E [M ]− p)

= Invisible

+ bj (1− sj )αj ε j︸ ︷︷ ︸Idiosyncratic

Measurement error

+ sj φj ξj︸ ︷︷ ︸Idiosyncratic

Cash Flow Risk

+ (sj γj + zj (Avg[γ]− Avg[rs ]))η︸ ︷︷ ︸Systematic

Cash Flow Risk

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 10 / 1

Solution to Moral Hazard

Incentive Compatible:

bj + sj (1− bj )︸ ︷︷ ︸Marginal Benefit

of Effort

− aj c︸︷︷︸Marginal Cost

of Effort

= 0

Individual Rationality:

vj = w0 +c2

aj2 − (sj + (1− sj )bj )aj︸ ︷︷ ︸

Reimbursement forDirect Cost

+Avg[γ]ρE + ρA

sj γj︸ ︷︷ ︸Compensation forSystematic Risk

+s2

j φ2j + (1− sj )

2b2j α2

j

2ρA︸ ︷︷ ︸Compensation forIdiosyncratic Risk

Manager’s portfolio decision

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 11 / 1

Solution to Moral Hazard

Incentive Compatible:

bj + sj (1− bj )︸ ︷︷ ︸Marginal Benefit

of Effort

− aj c︸︷︷︸Marginal Cost

of Effort

= 0

Individual Rationality:

vj = w0 +c2

aj2 − (sj + (1− sj )bj )aj︸ ︷︷ ︸

Reimbursement forDirect Cost

+Avg[γ]ρE + ρA

sj γj︸ ︷︷ ︸Compensation forSystematic Risk

+s2

j φ2j + (1− sj )

2b2j α2

j

2ρA︸ ︷︷ ︸Compensation forIdiosyncratic Risk

Manager’s portfolio decision

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 11 / 1

Solution to Moral Hazard

Incentive Compatible:

bj + sj (1− bj )︸ ︷︷ ︸Marginal Benefit

of Effort

− aj c︸︷︷︸Marginal Cost

of Effort

= 0

Individual Rationality:

vj = w0 +c2

aj2 − (sj + (1− sj )bj )aj︸ ︷︷ ︸

Reimbursement forDirect Cost

+Avg[γ]ρE + ρA

sj γj︸ ︷︷ ︸Compensation forSystematic Risk

+s2

j φ2j + (1− sj )

2b2j α2

j

2ρA︸ ︷︷ ︸Compensation forIdiosyncratic Risk

Manager’s portfolio decision

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 11 / 1

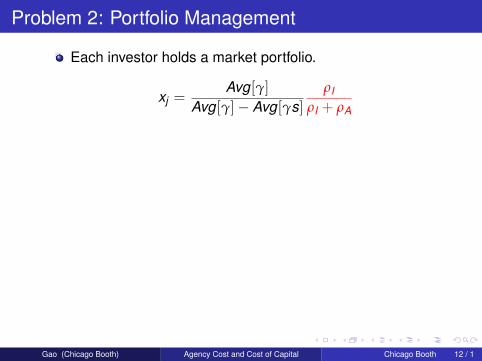

Problem 2: Portfolio Management

Each investor holds a market portfolio.

xj =Avg[γ]

Avg[γ]− Avg[γs]ρI

ρI + ρA

Manager holds a market portfolio plus restricted shares.The systematic risk in her compensation is hedged away.The idiosyncratic risk in her compensation is not.

zj =Avg[γ]

Avg[γ]− Avg[γs]ρA

ρI + ρA− Avg[γ]

Avg[γ]− Avg[γs]γjsj

Avg[γ]

Price of traded shares pays only for systematic risk.

pj = (1− bj)aj −Avg[γ]ρI + ρA

γj

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 12 / 1

Problem 2: Portfolio Management

Each investor holds a market portfolio.

xj =Avg[γ]

Avg[γ]− Avg[γs]ρI

ρI + ρA

Manager holds a market portfolio plus restricted shares.The systematic risk in her compensation is hedged away.The idiosyncratic risk in her compensation is not.

zj =Avg[γ]

Avg[γ]− Avg[γs]ρA

ρI + ρA− Avg[γ]

Avg[γ]− Avg[γs]γjsj

Avg[γ]

Price of traded shares pays only for systematic risk.

pj = (1− bj)aj −Avg[γ]ρI + ρA

γj

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 12 / 1

Problem 2: Portfolio Management

Each investor holds a market portfolio.

xj =Avg[γ]

Avg[γ]− Avg[γs]ρI

ρI + ρA

Manager holds a market portfolio plus restricted shares.The systematic risk in her compensation is hedged away.The idiosyncratic risk in her compensation is not.

zj =Avg[γ]

Avg[γ]− Avg[γs]ρA

ρI + ρA− Avg[γ]

Avg[γ]− Avg[γs]γjsj

Avg[γ]

Price of traded shares pays only for systematic risk.

pj = (1− bj)aj −Avg[γ]ρI + ρA

γj

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 12 / 1

Problem 2: Portfolio Management

Each investor holds a market portfolio.

xj =Avg[γ]

Avg[γ]− Avg[γs]ρI

ρI + ρA

Manager holds a market portfolio plus restricted shares.The systematic risk in her compensation is hedged away.The idiosyncratic risk in her compensation is not.

zj =Avg[γ]

Avg[γ]− Avg[γs]ρA

ρI + ρA− Avg[γ]

Avg[γ]− Avg[γs]γjsj

Avg[γ]

Price of traded shares pays only for systematic risk.

pj = (1− bj)aj −Avg[γ]ρI + ρA

γj

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 12 / 1

Problem 2: Portfolio Management

Each investor holds a market portfolio.

xj =Avg[γ]

Avg[γ]− Avg[γs]ρI

ρI + ρA

Manager holds a market portfolio plus restricted shares.The systematic risk in her compensation is hedged away.The idiosyncratic risk in her compensation is not.

zj =Avg[γ]

Avg[γ]− Avg[γs]ρA

ρI + ρA− Avg[γ]

Avg[γ]− Avg[γs]γjsj

Avg[γ]

Price of traded shares pays only for systematic risk.

pj = (1− bj)aj −Avg[γ]ρI + ρA

γj

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 12 / 1

Problem 3: optimal contract and financing decisions

The NPV rule for financing: (1− sj)pj − vj − k0

The optimal compensation contract decision:

L(bj , sj , µ) = aj −c2

a2j −

Avg[γ]ρI + ρA

γj −(bj(1− sj))

2α2j + s2

j φ2j

2ρA

+invisible

+2µ(bj + (1− bj)sj − ajc)

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 13 / 1

Problem 3: optimal contract and financing decisions

The NPV rule for financing: (1− sj)pj − vj − k0

The optimal compensation contract decision:

L(bj , sj , µ) = aj −c2

a2j −

Avg[γ]ρI + ρA

γj −(bj(1− sj))

2α2j + s2

j φ2j

2ρA

+invisible

+2µ(bj + (1− bj)sj − ajc)

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 13 / 1

Problem 3: optimal contract and financing decisions

The NPV rule for financing: (1− sj)pj − vj − k0

The optimal compensation contract decision:

L(bj , sj , µ) = aj −c2

a2j −

Avg[γ]ρI + ρA

γj −(bj(1− sj))

2α2j + s2

j φ2j

2ρA

+invisible

+2µ(bj + (1− bj)sj − ajc)

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 13 / 1

Problem 3: optimal contract and financing decisions

The NPV rule for financing: (1− sj)pj − vj − k0

The optimal compensation contract decision:

L(bj , sj , µ) = aj −c2

a2j −

Avg[γ]ρI + ρA

γj −(bj(1− sj))

2α2j + s2

j φ2j

2ρA

+invisible

+2µ(bj + (1− bj)sj − ajc)

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 13 / 1

The main results

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 14 / 1

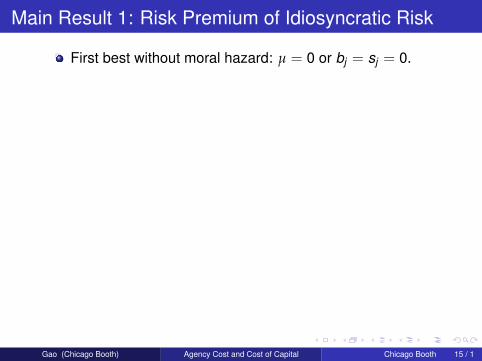

Main Result 1: Risk Premium of Idiosyncratic Risk

First best without moral hazard: µ = 0 or bj = sj = 0.

Second best with moral hazard: µ > 0 or bj > 0, sj > 0.

Implication for cost of capital:

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

Risk premium of the idiosyncratic risk is the shadow priceof moral hazard constraint.

Aj ≡ µ =12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 15 / 1

Main Result 1: Risk Premium of Idiosyncratic Risk

First best without moral hazard: µ = 0 or bj = sj = 0.

Second best with moral hazard: µ > 0 or bj > 0, sj > 0.

Implication for cost of capital:

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

Risk premium of the idiosyncratic risk is the shadow priceof moral hazard constraint.

Aj ≡ µ =12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 15 / 1

Main Result 1: Risk Premium of Idiosyncratic Risk

First best without moral hazard: µ = 0 or bj = sj = 0.

Second best with moral hazard: µ > 0 or bj > 0, sj > 0.

Implication for cost of capital:

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

Risk premium of the idiosyncratic risk is the shadow priceof moral hazard constraint.

Aj ≡ µ =12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 15 / 1

Main Result 1: Risk Premium of Idiosyncratic Risk

First best without moral hazard: µ = 0 or bj = sj = 0.

Second best with moral hazard: µ > 0 or bj > 0, sj > 0.

Implication for cost of capital:

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

Risk premium of the idiosyncratic risk is the shadow priceof moral hazard constraint.

Aj ≡ µ =12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 15 / 1

Main Result 1: Risk Premium of Idiosyncratic Risk

First best without moral hazard: µ = 0 or bj = sj = 0.

Second best with moral hazard: µ > 0 or bj > 0, sj > 0.

Implication for cost of capital:

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

Risk premium of the idiosyncratic risk is the shadow priceof moral hazard constraint.

Aj ≡ µ =12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 15 / 1

Generalizablity of Result 1

Moral hazard is one example of frictions that leads toconcentration of idiosyncratic risk. Other examples:

Adverse selection: Leland and Pyle (1977)

Blockholding and institutional holding

Debt financing

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 16 / 1

Generalizablity of Result 1

Moral hazard is one example of frictions that leads toconcentration of idiosyncratic risk. Other examples:

Adverse selection: Leland and Pyle (1977)

Blockholding and institutional holding

Debt financing

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 16 / 1

Generalizablity of Result 1

Moral hazard is one example of frictions that leads toconcentration of idiosyncratic risk. Other examples:

Adverse selection: Leland and Pyle (1977)

Blockholding and institutional holding

Debt financing

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 16 / 1

Generalizablity of Result 1

Moral hazard is one example of frictions that leads toconcentration of idiosyncratic risk. Other examples:

Adverse selection: Leland and Pyle (1977)

Blockholding and institutional holding

Debt financing

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 16 / 1

Implication 1: Biased Proxy of Cost of Capital

∆j

= (1− sj ) ∗Cost of Capital Implied

in Traded Stocks + sj ∗Cost of Capital Implied

in Restricted Stocks= Invisible

=Firm j’s

CAPM Beta ×Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+Risk Premium ofIdiosyncratic Risk

=γj

Avg[γ]Avg2[γ]

ρI + ρA+

12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 17 / 1

Implication 1: Biased Proxy of Cost of Capital

∆j = (1− sj ) ∗Cost of Capital Implied

in Traded Stocks + sj ∗Cost of Capital Implied

in Restricted Stocks

= Invisible

=Firm j’s

CAPM Beta ×Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+Risk Premium ofIdiosyncratic Risk

=γj

Avg[γ]Avg2[γ]

ρI + ρA+

12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 17 / 1

Implication 1: Biased Proxy of Cost of Capital

∆j = (1− sj ) ∗Cost of Capital Implied

in Traded Stocks + sj ∗Cost of Capital Implied

in Restricted Stocks

= Invisible

=Firm j’s

CAPM Beta ×Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+Risk Premium ofIdiosyncratic Risk

=γj

Avg[γ]Avg2[γ]

ρI + ρA+

12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 17 / 1

Implication 1: Biased Proxy of Cost of Capital

∆j = (1− sj ) ∗Cost of Capital Implied

in Traded Stocks + sj ∗Cost of Capital Implied

in Restricted Stocks

= Invisible

=Firm j’s

CAPM Beta ×Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+Risk Premium ofIdiosyncratic Risk

=γj

Avg[γ]Avg2[γ]

ρI + ρA+

12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 17 / 1

Implication 1: Biased Proxy of Cost of Capital

∆j = (1− sj ) ∗Cost of Capital Implied

in Traded Stocks + sj ∗Cost of Capital Implied

in Restricted Stocks

= Invisible

=Firm j’s

CAPM Beta ×Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+Risk Premium ofIdiosyncratic Risk

=γj

Avg[γ]Avg2[γ]

ρI + ρA+

12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 17 / 1

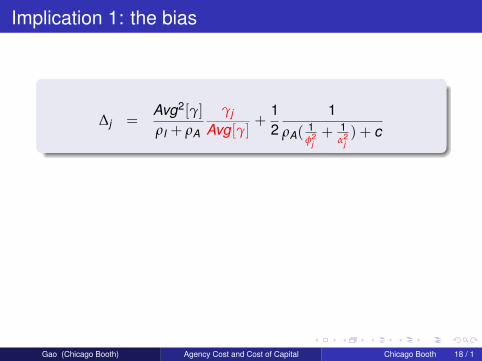

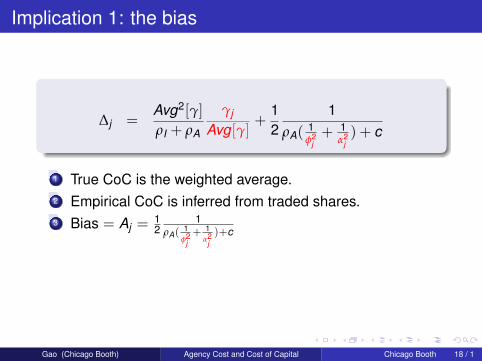

Implication 1: the bias

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

1 True CoC is the weighted average.2 Empirical CoC is inferred from traded shares.3 Bias = Aj =

12

1ρA(

1φ2

j+ 1

α2j)+c

4 All the effects of idiosyncratic risk on CoC are filtered outby the biased proxy of CoC.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 18 / 1

Implication 1: the bias

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

1 True CoC is the weighted average.

2 Empirical CoC is inferred from traded shares.3 Bias = Aj =

12

1ρA(

1φ2

j+ 1

α2j)+c

4 All the effects of idiosyncratic risk on CoC are filtered outby the biased proxy of CoC.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 18 / 1

Implication 1: the bias

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

1 True CoC is the weighted average.2 Empirical CoC is inferred from traded shares.

3 Bias = Aj =12

1ρA(

1φ2

j+ 1

α2j)+c

4 All the effects of idiosyncratic risk on CoC are filtered outby the biased proxy of CoC.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 18 / 1

Implication 1: the bias

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

1 True CoC is the weighted average.2 Empirical CoC is inferred from traded shares.3 Bias = Aj =

12

1ρA(

1φ2

j+ 1

α2j)+c

4 All the effects of idiosyncratic risk on CoC are filtered outby the biased proxy of CoC.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 18 / 1

Implication 1: the bias

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ 1

α2j) + c

1 True CoC is the weighted average.2 Empirical CoC is inferred from traded shares.3 Bias = Aj =

12

1ρA(

1φ2

j+ 1

α2j)+c

4 All the effects of idiosyncratic risk on CoC are filtered outby the biased proxy of CoC.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 18 / 1

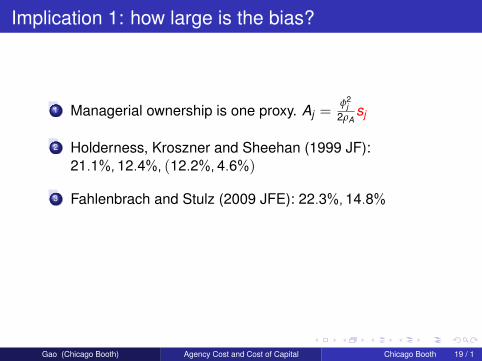

Implication 1: how large is the bias?

1 Managerial ownership is one proxy. Aj =φ2

j2ρA

sj

2 Holderness, Kroszner and Sheehan (1999 JF):21.1%,12.4%, (12.2%,4.6%)

3 Fahlenbrach and Stulz (2009 JFE): 22.3%,14.8%

4 Other solutions that lead to concentration of idiosyncraticrisk: Leland and Pyle (1977), blockholders, debt financing

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 19 / 1

Implication 1: how large is the bias?

1 Managerial ownership is one proxy. Aj =φ2

j2ρA

sj

2 Holderness, Kroszner and Sheehan (1999 JF):21.1%,12.4%, (12.2%,4.6%)

3 Fahlenbrach and Stulz (2009 JFE): 22.3%,14.8%

4 Other solutions that lead to concentration of idiosyncraticrisk: Leland and Pyle (1977), blockholders, debt financing

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 19 / 1

Implication 1: how large is the bias?

1 Managerial ownership is one proxy. Aj =φ2

j2ρA

sj

2 Holderness, Kroszner and Sheehan (1999 JF):21.1%,12.4%, (12.2%,4.6%)

3 Fahlenbrach and Stulz (2009 JFE): 22.3%,14.8%

4 Other solutions that lead to concentration of idiosyncraticrisk: Leland and Pyle (1977), blockholders, debt financing

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 19 / 1

Implication 1: how large is the bias?

1 Managerial ownership is one proxy. Aj =φ2

j2ρA

sj

2 Holderness, Kroszner and Sheehan (1999 JF):21.1%,12.4%, (12.2%,4.6%)

3 Fahlenbrach and Stulz (2009 JFE): 22.3%,14.8%

4 Other solutions that lead to concentration of idiosyncraticrisk: Leland and Pyle (1977), blockholders, debt financing

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 19 / 1

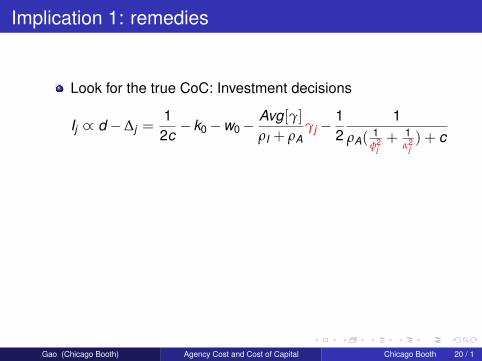

Implication 1: remedies

Look for the true CoC: Investment decisions

Ij ∝ d −∆j =12c− k0−w0−

Avg[γ]ρI + ρA

γj −12

1ρA(

1φ2

j+ 1

α2j) + c

Determinants of the bias:

Aj =12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 20 / 1

Implication 1: remedies

Look for the true CoC: Investment decisions

Ij ∝ d −∆j =12c− k0−w0−

Avg[γ]ρI + ρA

γj −12

1ρA(

1φ2

j+ 1

α2j) + c

Determinants of the bias:

Aj =12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 20 / 1

The general equilibrium effects

αj ≡ λj α + δj

firm level quality: δj

economy level quality: α

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 21 / 1

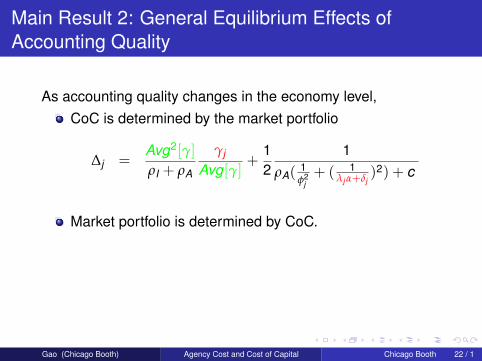

Main Result 2: General Equilibrium Effects ofAccounting Quality

As accounting quality changes in the economy level,

CoC is determined by the market portfolio

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ ( 1

λj α+δj)2) + c

Market portfolio is determined by CoC.

Avg[γ] =∫

∆i<dγidi

CoC could increase or decrease and firms differ.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 22 / 1

Main Result 2: General Equilibrium Effects ofAccounting Quality

As accounting quality changes in the economy level,CoC is determined by the market portfolio

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ ( 1

λj α+δj)2) + c

Market portfolio is determined by CoC.

Avg[γ] =∫

∆i<dγidi

CoC could increase or decrease and firms differ.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 22 / 1

Main Result 2: General Equilibrium Effects ofAccounting Quality

As accounting quality changes in the economy level,CoC is determined by the market portfolio

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ ( 1

λj α+δj)2) + c

Market portfolio is determined by CoC.

Avg[γ] =∫

∆i<dγidi

CoC could increase or decrease and firms differ.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 22 / 1

Main Result 2: General Equilibrium Effects ofAccounting Quality

As accounting quality changes in the economy level,CoC is determined by the market portfolio

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ ( 1

λj α+δj)2) + c

Market portfolio is determined by CoC.

Avg[γ] =∫

∆i<dγidi

CoC could increase or decrease and firms differ.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 22 / 1

Main Result 2: General Equilibrium Effects ofAccounting Quality

As accounting quality changes in the economy level,CoC is determined by the market portfolio

∆j =Avg2[γ]

ρI + ρA

γj

Avg[γ]+

12

1ρA(

1φ2

j+ ( 1

λj α+δj)2) + c

Market portfolio is determined by CoC.

Avg[γ] =∫

∆i<dγidi

CoC could increase or decrease and firms differ.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 22 / 1

Proposition

As the quality of accounting information at the economy-levelimproves (α becomes smaller), for an individual firm:

1 the quality of its accounting information improves;2 the risk premium for its idiosyncratic risk decreases

(∂Aj∂α > 0);

3 the risk premium for its systematic risk (weakly) increases(

γjrI+rA

∂Γ∂α < 0); and

4 the risk premium it pays to finance its project could eitherincrease or decrease, depending on its sensitivity to theeconomy-level factor α and its relative exposure tosystematic and idiosyncratic risk. That is, ∂∆j

∂α > 0 if andonly if − γj

rI+rA

∂Γ∂α <

λj2

∂Aj∂αj

.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 23 / 1

An Example of the General Equilibrium Effect

1 Type 1: λ1 = 0 and γ1 > 0

2 Type 2: λ2 = 0 and γ2 = 3γ1

3 Type 3: λ3 > 0 is large and γ3 = 2γ1

Assumption: 4 γ21

ρI+ρA< d < 9

2γ2

1ρI+ρA

If α=0, Avg[γ] = γ1+2γ12 , None of Type 2 is financed:

∆2 =32 γ1

ρI+ρA∗ (3γ1) > d ;

If α =1, Avg[γ] = γ1, Some of Type 2 are financed:∆2 = γ1

ρI+ρA∗ (3γ1) < d ;

The first and second best cases do not subsume each other.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 24 / 1

An Example of the General Equilibrium Effect

1 Type 1: λ1 = 0 and γ1 > 0

2 Type 2: λ2 = 0 and γ2 = 3γ1

3 Type 3: λ3 > 0 is large and γ3 = 2γ1

Assumption: 4 γ21

ρI+ρA< d < 9

2γ2

1ρI+ρA

If α=0, Avg[γ] = γ1+2γ12 , None of Type 2 is financed:

∆2 =32 γ1

ρI+ρA∗ (3γ1) > d ;

If α =1, Avg[γ] = γ1, Some of Type 2 are financed:∆2 = γ1

ρI+ρA∗ (3γ1) < d ;

The first and second best cases do not subsume each other.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 24 / 1

An Example of the General Equilibrium Effect

1 Type 1: λ1 = 0 and γ1 > 0

2 Type 2: λ2 = 0 and γ2 = 3γ1

3 Type 3: λ3 > 0 is large and γ3 = 2γ1

Assumption: 4 γ21

ρI+ρA< d < 9

2γ2

1ρI+ρA

If α=0, Avg[γ] = γ1+2γ12 , None of Type 2 is financed:

∆2 =32 γ1

ρI+ρA∗ (3γ1) > d ;

If α =1, Avg[γ] = γ1, Some of Type 2 are financed:∆2 = γ1

ρI+ρA∗ (3γ1) < d ;

The first and second best cases do not subsume each other.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 24 / 1

An Example of the General Equilibrium Effect

1 Type 1: λ1 = 0 and γ1 > 0

2 Type 2: λ2 = 0 and γ2 = 3γ1

3 Type 3: λ3 > 0 is large and γ3 = 2γ1

Assumption: 4 γ21

ρI+ρA< d < 9

2γ2

1ρI+ρA

If α=0, Avg[γ] = γ1+2γ12 , None of Type 2 is financed:

∆2 =32 γ1

ρI+ρA∗ (3γ1) > d ;

If α =1, Avg[γ] = γ1, Some of Type 2 are financed:∆2 = γ1

ρI+ρA∗ (3γ1) < d ;

The first and second best cases do not subsume each other.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 24 / 1

An Example of the General Equilibrium Effect

1 Type 1: λ1 = 0 and γ1 > 0

2 Type 2: λ2 = 0 and γ2 = 3γ1

3 Type 3: λ3 > 0 is large and γ3 = 2γ1

Assumption: 4 γ21

ρI+ρA< d < 9

2γ2

1ρI+ρA

If α=0, Avg[γ] = γ1+2γ12 , None of Type 2 is financed:

∆2 =32 γ1

ρI+ρA∗ (3γ1) > d ;

If α =1, Avg[γ] = γ1, Some of Type 2 are financed:∆2 = γ1

ρI+ρA∗ (3γ1) < d ;

The first and second best cases do not subsume each other.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 24 / 1

An Example of the General Equilibrium Effect

1 Type 1: λ1 = 0 and γ1 > 0

2 Type 2: λ2 = 0 and γ2 = 3γ1

3 Type 3: λ3 > 0 is large and γ3 = 2γ1

Assumption: 4 γ21

ρI+ρA< d < 9

2γ2

1ρI+ρA

If α=0, Avg[γ] = γ1+2γ12 , None of Type 2 is financed:

∆2 =32 γ1

ρI+ρA∗ (3γ1) > d ;

If α =1, Avg[γ] = γ1, Some of Type 2 are financed:∆2 = γ1

ρI+ρA∗ (3γ1) < d ;

The first and second best cases do not subsume each other.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 24 / 1

An Example of the General Equilibrium Effect

1 Type 1: λ1 = 0 and γ1 > 0

2 Type 2: λ2 = 0 and γ2 = 3γ1

3 Type 3: λ3 > 0 is large and γ3 = 2γ1

Assumption: 4 γ21

ρI+ρA< d < 9

2γ2

1ρI+ρA

If α=0, Avg[γ] = γ1+2γ12 , None of Type 2 is financed:

∆2 =32 γ1

ρI+ρA∗ (3γ1) > d ;

If α =1, Avg[γ] = γ1, Some of Type 2 are financed:∆2 = γ1

ρI+ρA∗ (3γ1) < d ;

The first and second best cases do not subsume each other.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 24 / 1

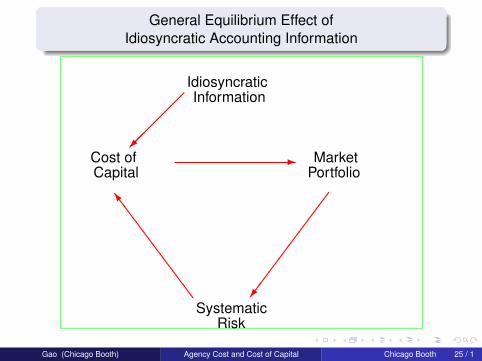

General Equilibrium Effect ofIdiosyncratic Accounting Information

SystematicRisk

SSSSSSSSo

Cost ofCapital

- MarketPortfolio

/

IdiosyncraticInformation

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 25 / 1

General Equilibrium Effect ofIdiosyncratic Accounting Information

SystematicRisk

SSSSSSSSo

Cost ofCapital

- MarketPortfolio

/

IdiosyncraticInformation

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 25 / 1

General Equilibrium Effect ofIdiosyncratic Accounting Information

SystematicRisk

SSSSSSSSo

Cost ofCapital

- MarketPortfolio

/

IdiosyncraticInformation

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 25 / 1

General Equilibrium Effect ofIdiosyncratic Accounting Information

SystematicRisk

SSSSSSSSo

Cost ofCapital

- MarketPortfolio

/

IdiosyncraticInformation

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 25 / 1

General Equilibrium Effect ofIdiosyncratic Accounting Information

SystematicRisk

SSSSSSSSo

Cost ofCapital

- MarketPortfolio

/

IdiosyncraticInformation

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 25 / 1

General Equilibrium Effect ofIdiosyncratic Accounting Information

SystematicRisk

SSSSSSSSo

Cost ofCapital

- MarketPortfolio

/

IdiosyncraticInformation

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 25 / 1

General Equilibrium Effect ofIdiosyncratic Accounting Information

SystematicRisk

SSSSSSSSo

Cost ofCapital

- MarketPortfolio

/

IdiosyncraticInformation

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 25 / 1

Implication 2: Accounting Quality is a "Factor"!

∆j =γj

Avg[γ]︸ ︷︷ ︸Firm j’s

CAPM Beta

× Avg2[γ]

ρI + ρA︸ ︷︷ ︸Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+ Aj︸︷︷︸Risk Premium ofIdiosyncratic Risk

Aj =12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 26 / 1

Implication 2: Accounting Quality is a "Factor"!

∆j =γj

Avg[γ]︸ ︷︷ ︸Firm j’s

CAPM Beta

× Avg2[γ]

ρI + ρA︸ ︷︷ ︸Risk Premium of

the Market Portfolio︸ ︷︷ ︸CAPM Cost of Capital

+ Aj︸︷︷︸Risk Premium ofIdiosyncratic Risk

Aj =12

1ρA(

1φ2

j+ 1

α2j) + c

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 26 / 1

Implication 3: Testing Effects of Accounting Standardsand Disclosure Regulation

Higher accounting quality for all does not lead to lower CoC forall!

The GE effect, or the externality through market portfolio, hasdistributional consequences.

As accounting quality in the economy-level increases,risk premium of the idiosyncratic risk decreases

risk premium of the market portfolio and beta could eitherincrease or decrease

overall effect on CoC is not clear

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 27 / 1

Implication 3: Testing Effects of Accounting Standardsand Disclosure Regulation

Higher accounting quality for all does not lead to lower CoC forall!

The GE effect, or the externality through market portfolio, hasdistributional consequences.

As accounting quality in the economy-level increases,risk premium of the idiosyncratic risk decreases

risk premium of the market portfolio and beta could eitherincrease or decrease

overall effect on CoC is not clear

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 27 / 1

Implication 3: Testing Effects of Accounting Standardsand Disclosure Regulation

Higher accounting quality for all does not lead to lower CoC forall!

The GE effect, or the externality through market portfolio, hasdistributional consequences.

As accounting quality in the economy-level increases,risk premium of the idiosyncratic risk decreases

risk premium of the market portfolio and beta could eitherincrease or decrease

overall effect on CoC is not clear

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 27 / 1

Implication 3: Testing Effects of Accounting Standardsand Disclosure Regulation

Higher accounting quality for all does not lead to lower CoC forall!

The GE effect, or the externality through market portfolio, hasdistributional consequences.

As accounting quality in the economy-level increases,risk premium of the idiosyncratic risk decreases

risk premium of the market portfolio and beta could eitherincrease or decrease

overall effect on CoC is not clear

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 27 / 1

Implication 3: Testing Effects of Accounting Standardsand Disclosure Regulation

Higher accounting quality for all does not lead to lower CoC forall!

The GE effect, or the externality through market portfolio, hasdistributional consequences.

As accounting quality in the economy-level increases,risk premium of the idiosyncratic risk decreases

risk premium of the market portfolio and beta could eitherincrease or decrease

overall effect on CoC is not clear

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 27 / 1

Take-aways

Idiosyncratic accounting information reduces CoC.

Implied CoC biases downward the true CoC.

Economy-wide accounting quality change hascomplicated general equilibrium effect.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 28 / 1

Take-aways

Idiosyncratic accounting information reduces CoC.

Implied CoC biases downward the true CoC.

Economy-wide accounting quality change hascomplicated general equilibrium effect.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 28 / 1

Take-aways

Idiosyncratic accounting information reduces CoC.

Implied CoC biases downward the true CoC.

Economy-wide accounting quality change hascomplicated general equilibrium effect.

Gao (Chicago Booth) Agency Cost and Cost of Capital Chicago Booth 28 / 1