Embed Size (px)

Citation preview

1© 2011 The MathWorks, Inc.

信用リスクモデリング ケーススタディ

The MathWorks® Computational Finance Team

2

Time Table

Time Agenda

15:20 – 15:25 Introduction

15:25 – 15:50 決定木による格付モデル

15:50 – 16:00 休憩

16:00 – 16:15 遷移行列とデフォルト確率

16:15 – 16:35 信用リスクの解析

16:35 – 16:50 まとめ

3

利率

回収率

Market Data

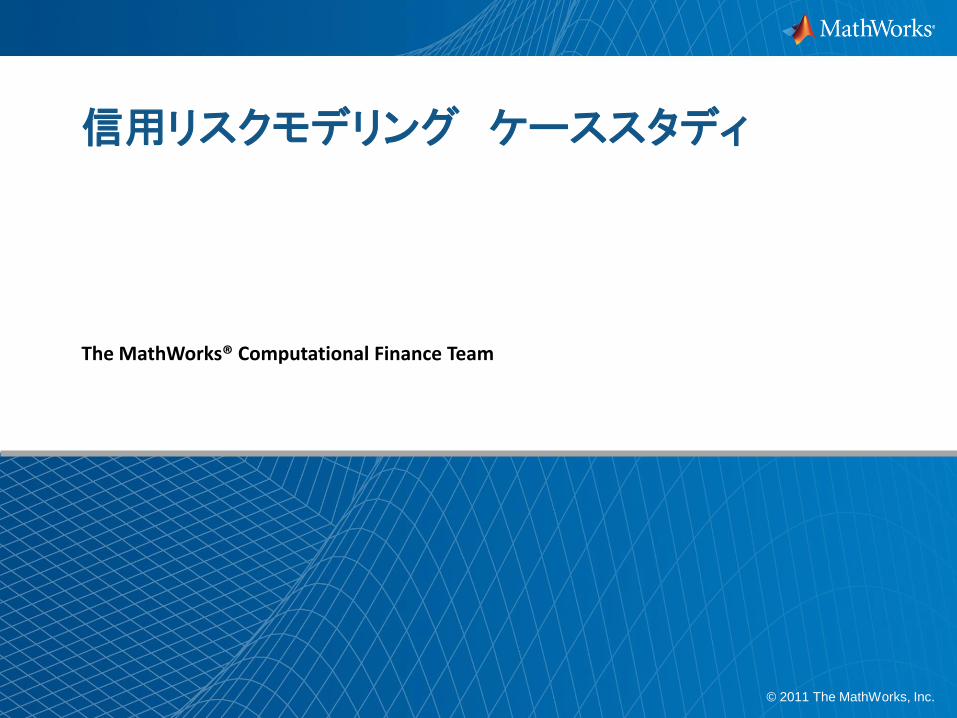

目標:信用リスクモデルのアプリケーション作成

Credit Value at Risk

信用VaR を算出するツールを開発しExcel のアプリケーションとして組み込む

Historical Data

Rating System

Portfolio Data

格付け

クーポン・レート

日付

業種

優先順位

Transition

Probabilities

4

要求課題

計算能力– 1,000 以上の債券銘柄

– 10,000 回のシミュレーション

コスト– 開発工数の削減

– 既存環境への適用

透明性– アルゴリズムの可読性

– 第三者への説明

5

Agenda

決定木による格付モデル

遷移行列とデフォルト確率

信用リスクの解析

まとめ

6

利率

回収率

Market Data

Task 1: Calibrating the rating system

Credit Value at Risk

過去のデータから格付分類モデルを作成

Historical Data

Rating System

Portfolio Data

格付け

クーポン・レート

日付

業種

優先順位

Transition

Probabilities

7

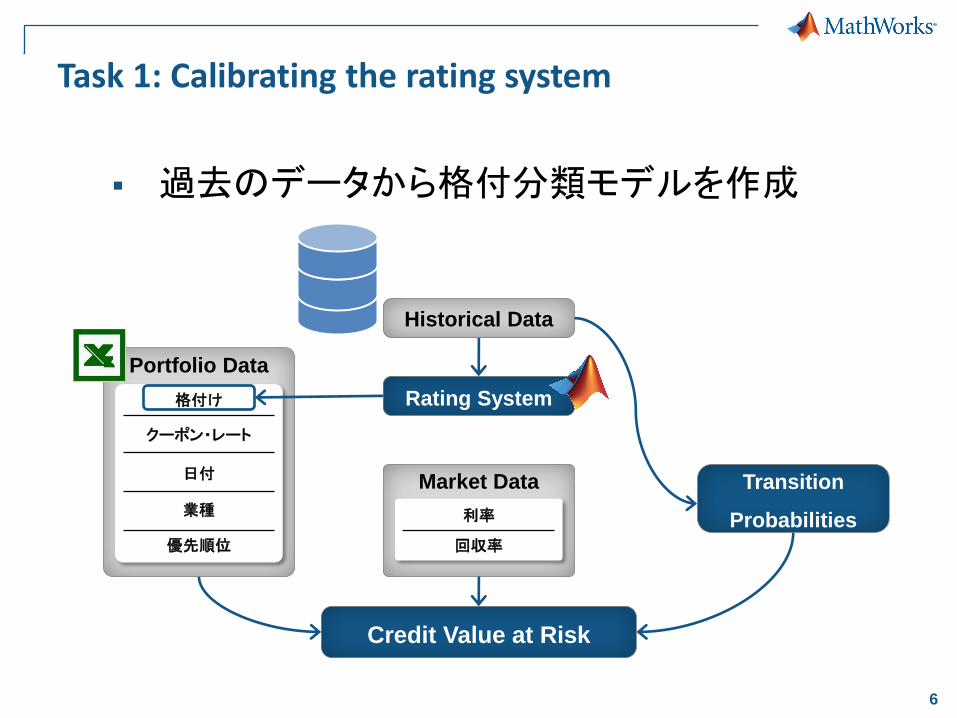

Calibrating the rating system

手順1. データのインポート: DB / Excel

2. 線型回帰による単純な分類モデルを構築

3. ランダム・フォレストを適用した分類モデルを構築

4. 分類モデルをROC曲線/AUCにより評価

ID WC_TA RE_TA EBIT_TA MVE_BVTD S_TA Industry

60644 0.049 0.220 0.041 2.400 0.489 6

Ratings

AA

Rating System

AltmanのZ-スコアのための5つの財務指標

8

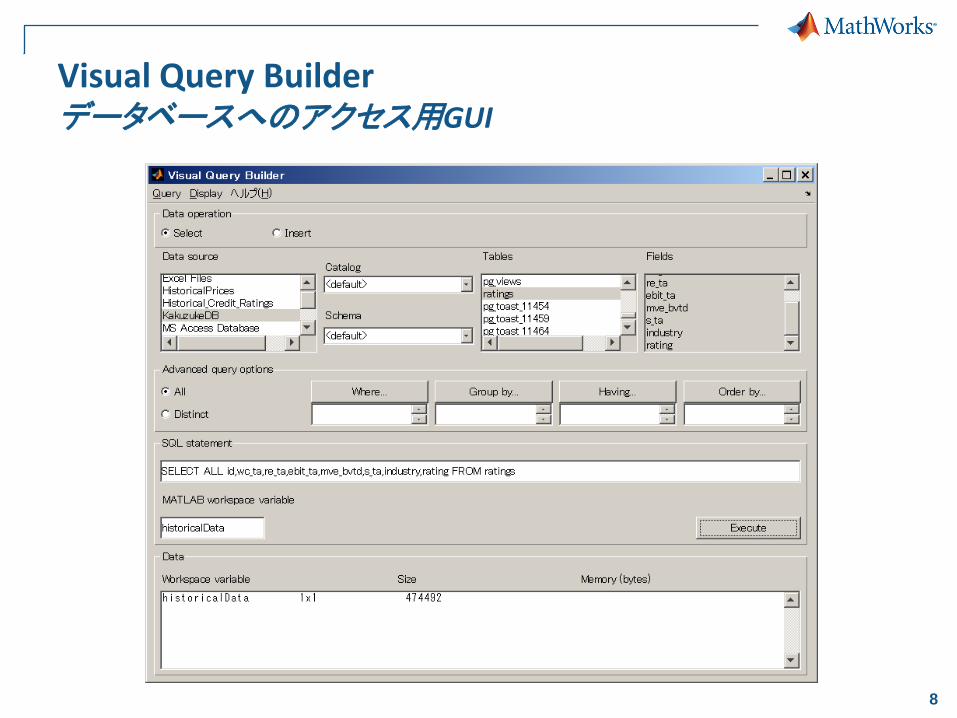

Visual Query Builderデータベースへのアクセス用GUI

9

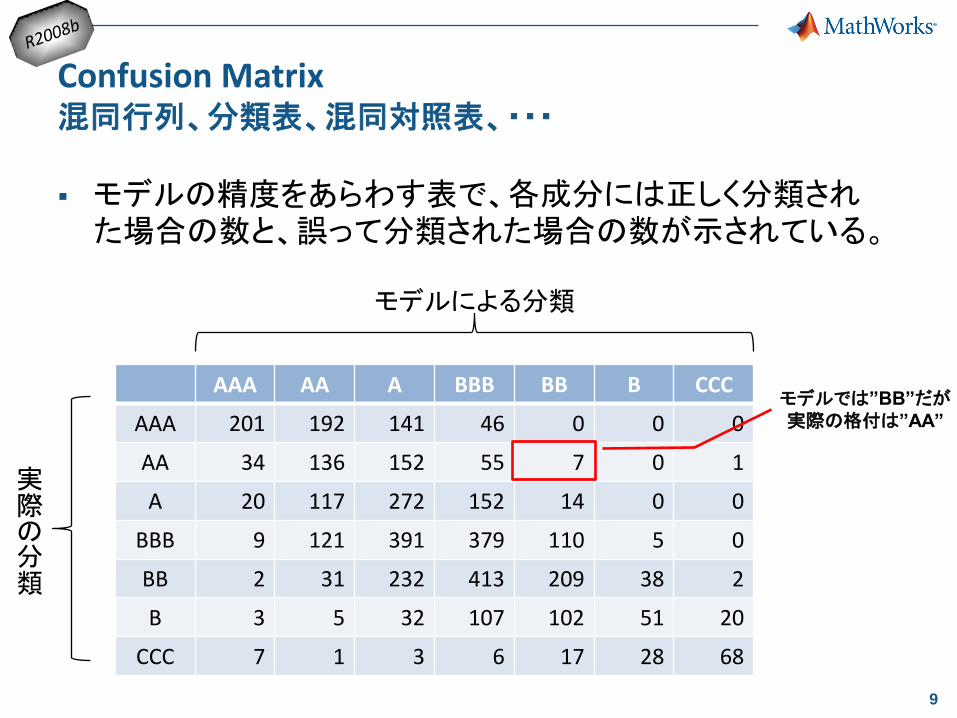

Confusion Matrix混同行列、分類表、混同対照表、・・・

モデルの精度をあらわす表で、各成分には正しく分類された場合の数と、誤って分類された場合の数が示されている。

AAA AA A BBB BB B CCC

AAA 201 192 141 46 0 0 0

AA 34 136 152 55 7 0 1

A 20 117 272 152 14 0 0

BBB 9 121 391 379 110 5 0

BB 2 31 232 413 209 38 2

B 3 5 32 107 102 51 20

CCC 7 1 3 6 17 28 68

実際の分類

モデルによる分類

モデルでは”BB”だが実際の格付は”AA”

10

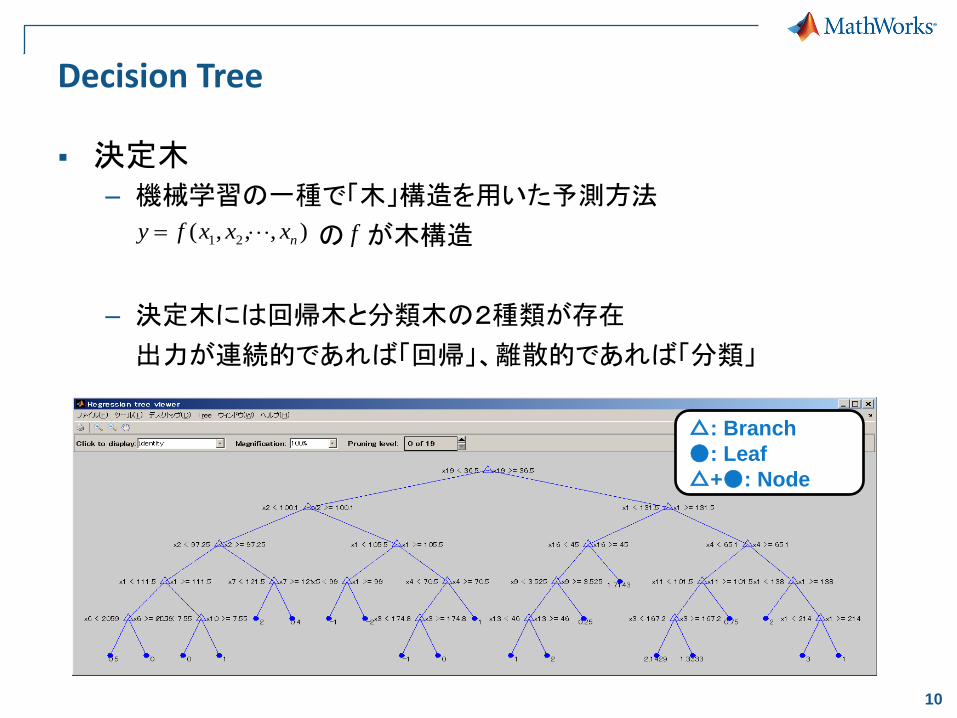

Decision Tree

決定木– 機械学習の一種で「木」構造を用いた予測方法

の が木構造

– 決定木には回帰木と分類木の2種類が存在

出力が連続的であれば「回帰」、離散的であれば「分類」

),,,( 21 nxxxfy f

△: Branch

●: Leaf

△+●: Node

11

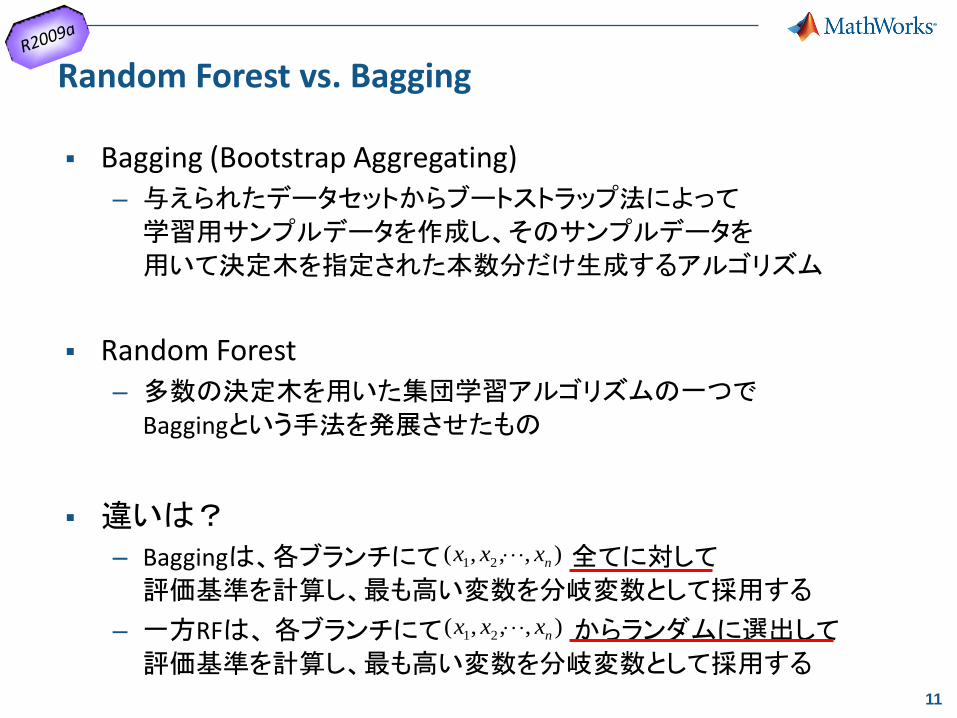

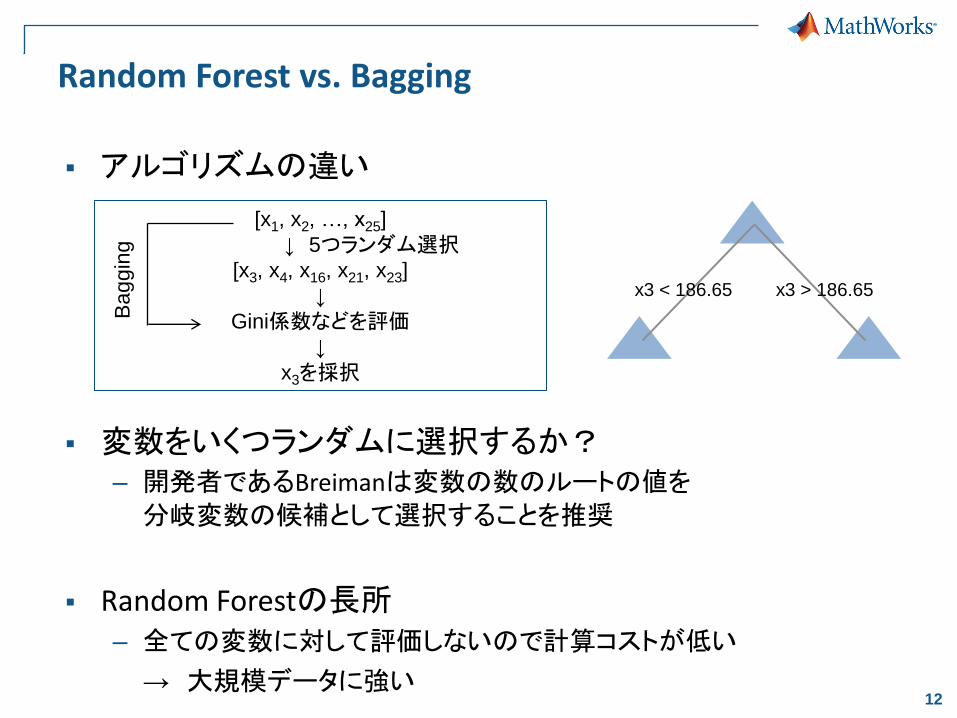

Random Forest vs. Bagging

Bagging (Bootstrap Aggregating)

– 与えられたデータセットからブートストラップ法によって

学習用サンプルデータを作成し、そのサンプルデータを

用いて決定木を指定された本数分だけ生成するアルゴリズム

Random Forest

– 多数の決定木を用いた集団学習アルゴリズムの一つで

Baggingという手法を発展させたもの

違いは?– Baggingは、各ブランチにて 全てに対して

評価基準を計算し、最も高い変数を分岐変数として採用する

– 一方RFは、各ブランチにて からランダムに選出して

評価基準を計算し、最も高い変数を分岐変数として採用する

),,,( 21 nxxx

),,,( 21 nxxx

12

Random Forest vs. Bagging

アルゴリズムの違い

変数をいくつランダムに選択するか?– 開発者であるBreimanは変数の数のルートの値を

分岐変数の候補として選択することを推奨

Random Forestの長所– 全ての変数に対して評価しないので計算コストが低い

→ 大規模データに強い

x3 < 186.65 x3 > 186.65

[x1, x2, …, x25]

↓ 5つランダム選択[x3, x4, x16, x21, x23]

↓

Gini係数などを評価↓

x3を採択

Bagg

ing

13

ROC曲線: Receiver Operating Characteristic Curve受信者動作特性曲線

ROC曲線: 分類の精度を表すグラフ– 赤枠で囲まれるような表を考え、閾値「11」を

設けます。この時、11以上を陽性(Positive)、

11未満を陰性(Negative)といい、5個のFのう

ち1個がPositive側に含まれることから偽陽

性率は0.2で、10個のTのうち5個がPositive

側に属するので真陽性率は0.5となります。

– 関数「perfcurve」はFalse/True Positive Rate

やAUC (Area under the curve)を計算する

スコア ラベル(分類)

偽陽性率(False Positive)

真陽性率(True Positive)

16 T 0 0.1

15 T 0 0.2

14 F 0.2 0.2

13 T 0.2 0.3

12 T 0.2 0.4

11 T 0.2 0.5

10 F 0.4 0.5

9 T 0.4 0.6

8 T 0.4 0.7

8 T 0.4 0.8

8 T 0.4 0.9

8 F 0.6 0.9

7 F 0.8 0.9

6 T 0.8 1

5 F 1 1

Threshold= 11

14

ROC曲線とAUC

>> [x, y, t, auc] = perfcurve(labels, scores, 'T‘);

>> plot(x,y);

>> xlabel(‘False Positive Rate’); ylabel('True Positive Rate');

>> text(0.5, 0.3, ['AUC = ', num2str(auc)], 'EdgeColor', 'k');

>> title('ROC曲線');

AUC: ROC曲線とx軸が囲む領域の面積で、AUCが1に近いほど分類の精度が高いことを意味する

15

CAP曲線Cumulative Accuracy Profile

格付

x以下でデフォルトした会社の割合

格付 x 以下に属する会社の割合0

1

1

D

Dx

k

k

N

Nx

k

k

x

N

kD

D

: 格付の低いほうから並べた順序付きランク

: 会社の総数

: 格付 k でデフォルトした会社の数

: デフォルトした会社の総数

kN :格付 k に属する会社の数

理想的な予測精度

ランダムな予測精度

16

ARAccuracy Ratio

以下のように囲まれる面積の比で定義される値で、1に近いほど分類モデルの精度が良いことを示す

AR =

の面積

の面積

17

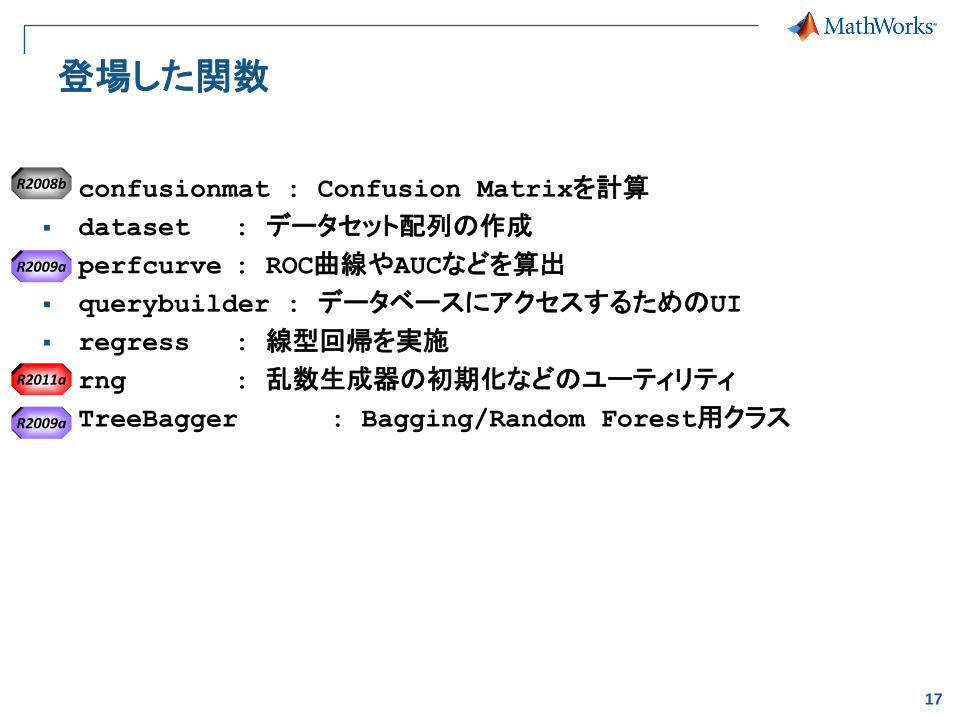

登場した関数

confusionmat : Confusion Matrixを計算

dataset : データセット配列の作成

perfcurve : ROC曲線やAUCなどを算出

querybuilder : データベースにアクセスするためのUI

regress : 線型回帰を実施

rng : 乱数生成器の初期化などのユーティリティ

TreeBagger : Bagging/Random Forest用クラス

R2011a

R2008b

R2009a

R2009a

18

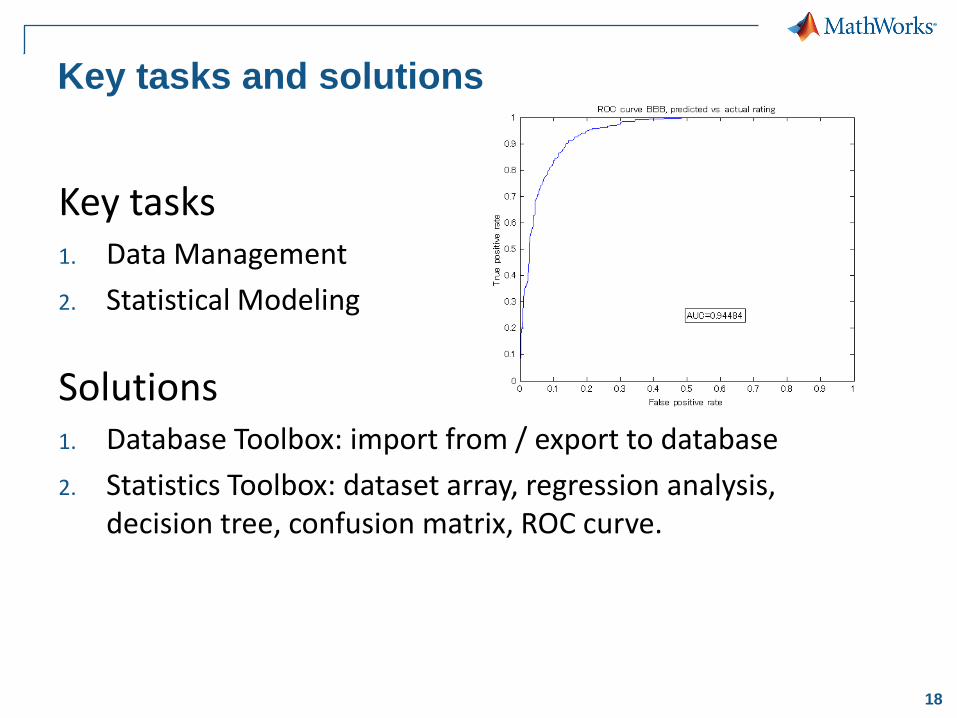

Key tasks1. Data Management

2. Statistical Modeling

Solutions1. Database Toolbox: import from / export to database

2. Statistics Toolbox: dataset array, regression analysis, decision tree, confusion matrix, ROC curve.

Key tasks and solutions

19

Agenda

決定木による格付モデル

遷移行列とデフォルト確率

信用リスクの解析

まとめ

20

利率

回収率

Market Data

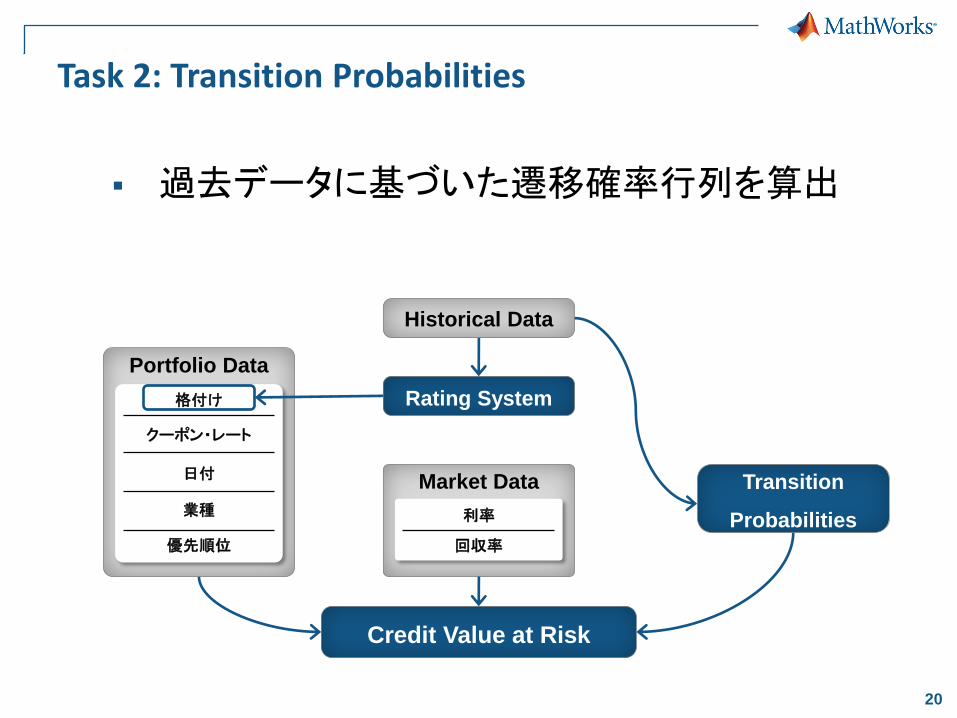

Task 2: Transition Probabilities

Credit Value at Risk

過去データに基づいた遷移確率行列を算出

Historical Data

Rating System

Portfolio Data

格付け

クーポン・レート

日付

業種

優先順位

Transition

Probabilities

21

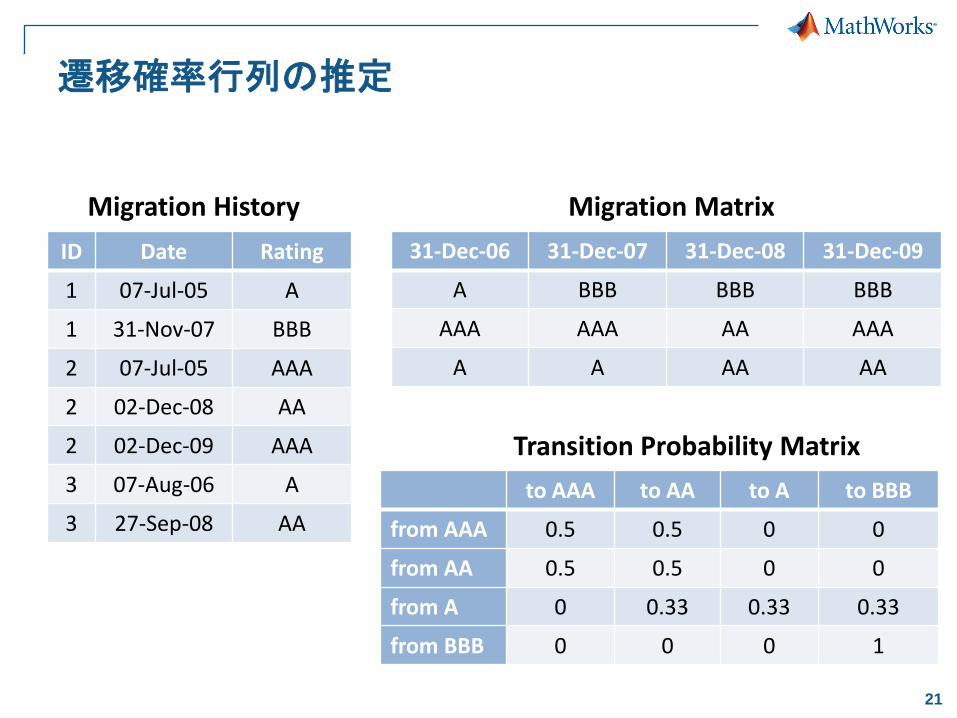

31-Dec-06 31-Dec-07 31-Dec-08 31-Dec-09

A BBB BBB BBB

AAA AAA AA AAA

A A AA AA

Migration Matrix

Transition Probability Matrix

ID Date Rating

1 07-Jul-05 A

1 31-Nov-07 BBB

2 07-Jul-05 AAA

2 02-Dec-08 AA

2 02-Dec-09 AAA

3 07-Aug-06 A

3 27-Sep-08 AA

Migration History

to AAA to AA to A to BBB

from AAA 0.5 0.5 0 0

from AA 0.5 0.5 0 0

from A 0 0.33 0.33 0.33

from BBB 0 0 0 1

遷移確率行列の推定

22

93.68%

2.44%

0.14%

0.03%

0.03%

0.00%

0.00%

0.00%

5.55%

92.60%

4.18%

0.23%

0.12%

0.00%

0.00%

0.00%

0.59%

4.03%

91.02%

7.49%

0.73%

0.11%

0.00%

0.00%

0.18%

0.73%

3.90%

87.86%

8.27%

0.82%

0.37%

0.00%

0.00%

0.15%

0.60%

3.78%

86.74%

9.64%

1.84%

0.00%

0.00%

0.00%

0.08%

0.39%

3.28%

85.37%

6.24%

0.00%

0.00%

0.00%

0.00%

0.06%

0.18%

2.41%

81.88%

0.00%

0.00%

0.06%

0.08%

0.16%

0.64%

1.64%

9.67%

100.00%

AAA AA A BBB BB B CCC D

AAA

AA

A

BBB

BB

B

CCC

D

手順1. テキストデータのインポートと時系列データの作成

2. Migration Matrixの生成

3. 遷移確率行列の算出と可視化

4. デフォルト確率の計算

遷移確率行列の推定

23

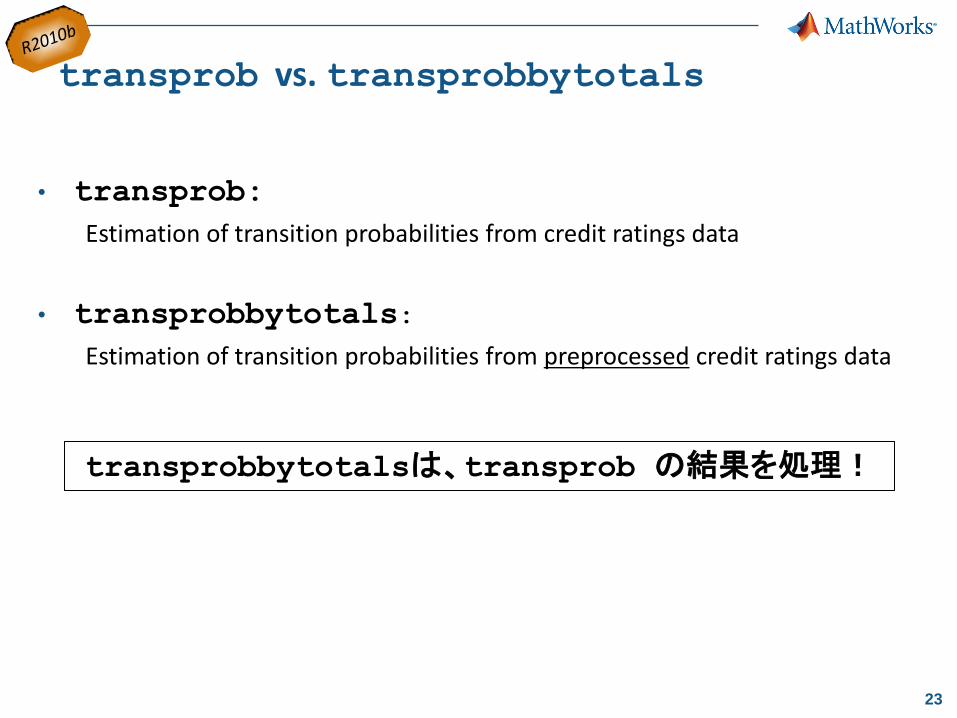

transprob vs. transprobbytotals

• transprob:

Estimation of transition probabilities from credit ratings data

• transprobbytotals:

Estimation of transition probabilities from preprocessed credit ratings data

transprobbytotalsは、transprob の結果を処理!

24

Open exchange for the MATLAB and Simulink user community

662,000 visits per month

File Exchange– Upload/download access to free files including

MATLAB code, Simulink models, and documents

– Ability to rate files, comment, and ask questions

– More than 9,000 contributed files, 400 submissions per month, 25,500 downloads per day

Newsgroup– Web forum for technical discussions about MATLAB

and Simulink

– 200 posts per day

Blogs– Frequent posts from key MathWorks developers

who design and build the products

– Open conversation at blogs.mathworks.com

Based on February 2009 data

MATLAB Central

25

登場した関数

cfdates : キャッシュフロー日付の作成

fillts : Financial Time Series Objectの欠損データ補完

fints : Financial Time Series Objectを作成

intersect : 2つの集合の共通部分を抽出 (A∩B)

ordinal : オーディナル配列の作成

parfor : forループの並列版

transprob : 格付データから遷移確率行列を推定

transprobbytotals :前処理済み格付データから遷移確率行列を推定

R2008a

R2010b

R2010b

26

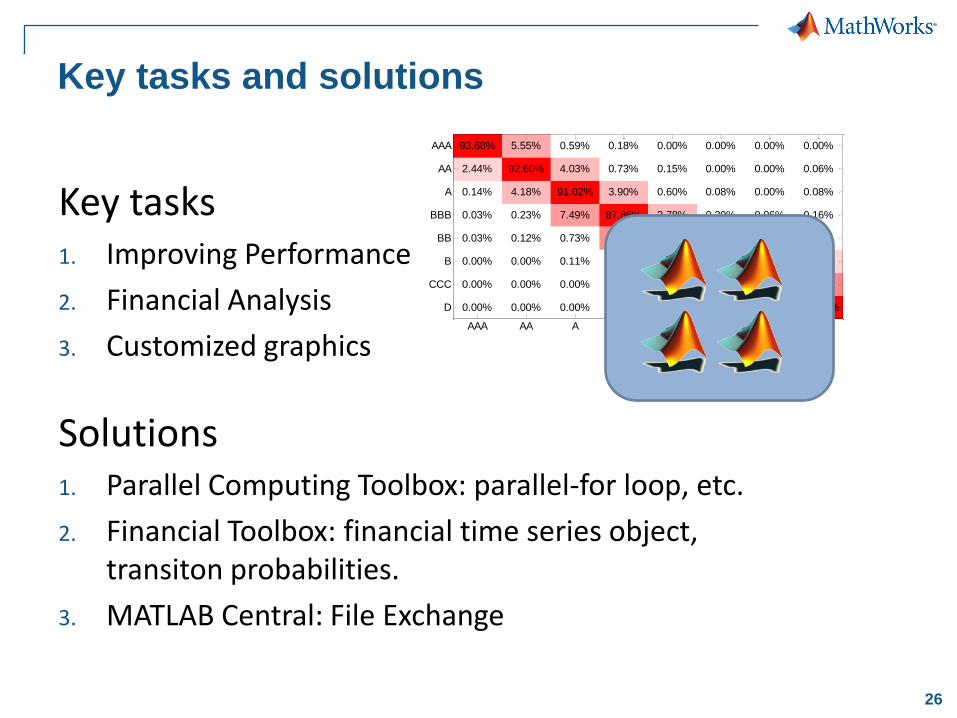

Key tasks1. Improving Performance

2. Financial Analysis

3. Customized graphics

Solutions1. Parallel Computing Toolbox: parallel-for loop, etc.

2. Financial Toolbox: financial time series object, transiton probabilities.

3. MATLAB Central: File Exchange

Key tasks and solutions

93.68%

2.44%

0.14%

0.03%

0.03%

0.00%

0.00%

0.00%

5.55%

92.60%

4.18%

0.23%

0.12%

0.00%

0.00%

0.00%

0.59%

4.03%

91.02%

7.49%

0.73%

0.11%

0.00%

0.00%

0.18%

0.73%

3.90%

87.86%

8.27%

0.82%

0.37%

0.00%

0.00%

0.15%

0.60%

3.78%

86.74%

9.64%

1.84%

0.00%

0.00%

0.00%

0.08%

0.39%

3.28%

85.37%

6.24%

0.00%

0.00%

0.00%

0.00%

0.06%

0.18%

2.41%

81.88%

0.00%

0.00%

0.06%

0.08%

0.16%

0.64%

1.64%

9.67%

100.00%

AAA AA A BBB BB B CCC D

AAA

AA

A

BBB

BB

B

CCC

D

27

Agenda

決定木による格付モデル

遷移行列とデフォルト確率

信用リスクの解析

まとめ

28

利率

回収率

Market Data

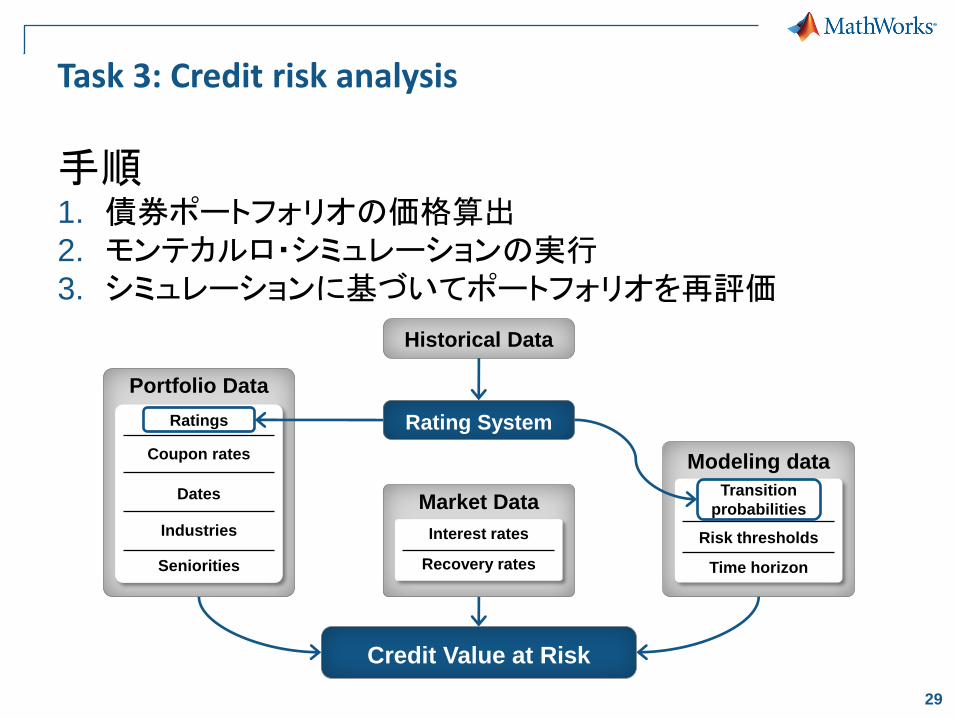

Task 3: Credit Risk Analysis

Credit Value at Risk

債券ポートフォリオの信用VaRを計算

Historical Data

Rating System

Portfolio Data

格付け

クーポン・レート

日付

業種

優先順位

Transition

Probabilities

29

Task 3: Credit risk analysis

手順1. 債券ポートフォリオの価格算出2. モンテカルロ・シミュレーションの実行3. シミュレーションに基づいてポートフォリオを再評価

Interest rates

Recovery rates

Market Data

Portfolio Data

Ratings

Coupon rates

Dates

Industries

Seniorities

Transition

probabilities

Time horizon

Modeling data

Risk thresholds

Credit Value at Risk

Historical Data

Rating System

30

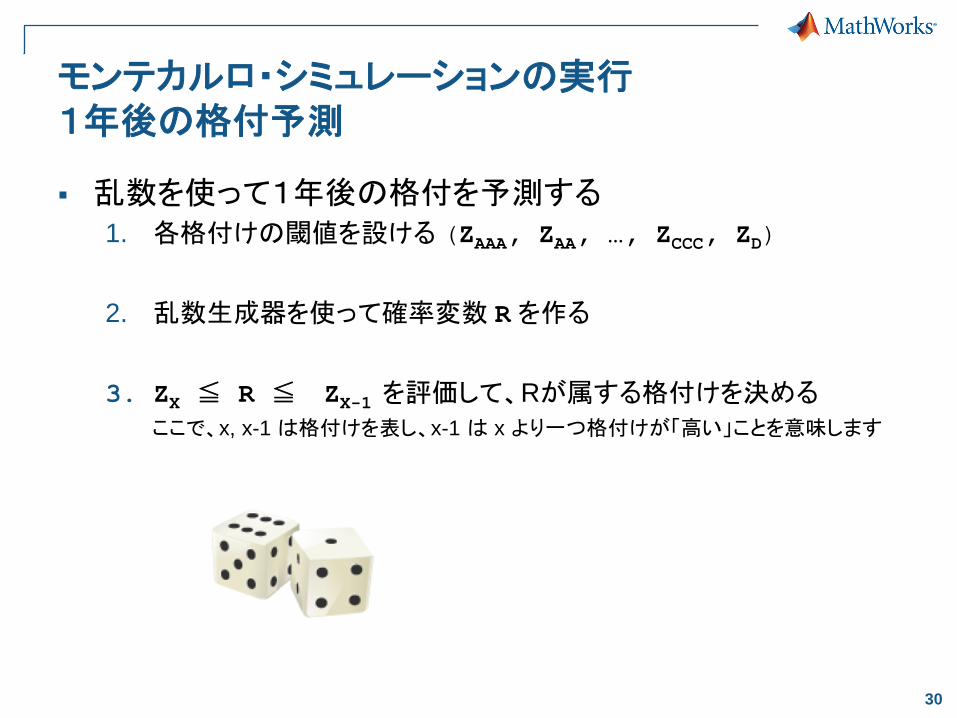

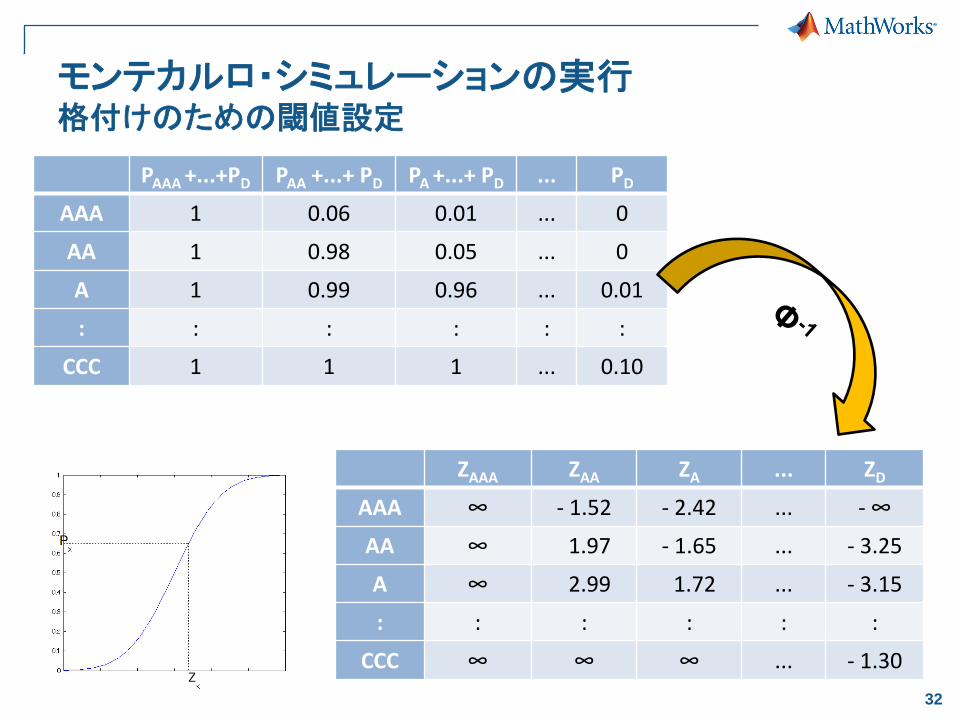

モンテカルロ・シミュレーションの実行1年後の格付予測

乱数を使って1年後の格付を予測する1. 各格付けの閾値を設ける (ZAAA, ZAA, …, ZCCC, ZD)

2. 乱数生成器を使って確率変数 R を作る

3. ZX ≦ R ≦ ZX-1 を評価して、Rが属する格付けを決める

ここで、x, x-1 は格付けを表し、x-1 は x より一つ格付けが「高い」ことを意味します

31

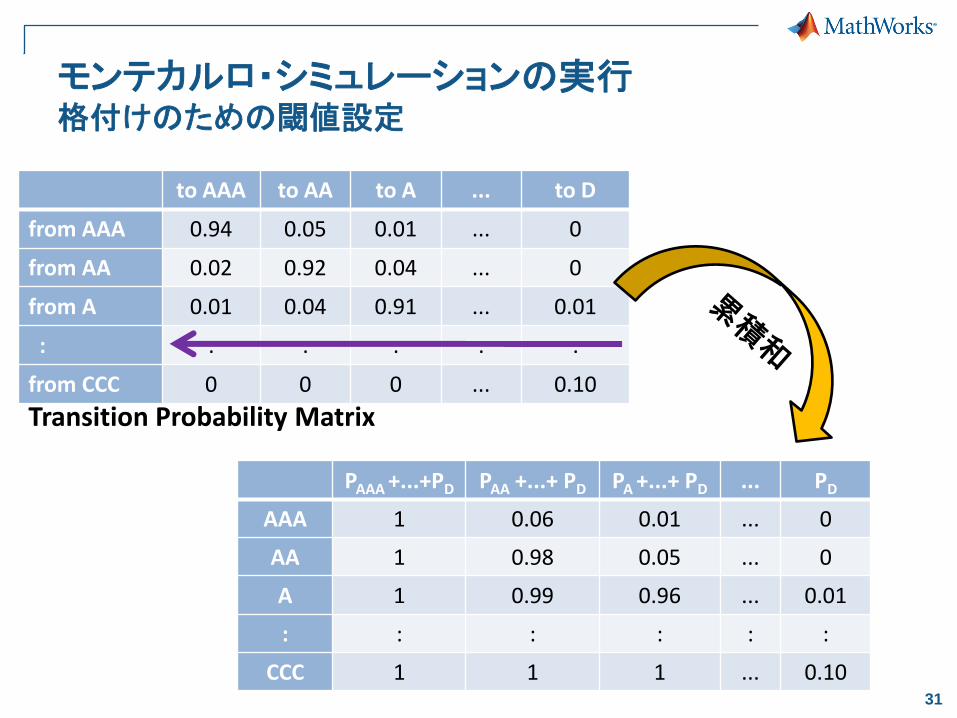

モンテカルロ・シミュレーションの実行格付けのための閾値設定

to AAA to AA to A ... to D

from AAA 0.94 0.05 0.01 ... 0

from AA 0.02 0.92 0.04 ... 0

from A 0.01 0.04 0.91 ... 0.01

: : : : : :

from CCC 0 0 0 ... 0.10

Transition Probability Matrix

PAAA +...+PD PAA +...+ PD PA +...+ PD ... PD

AAA 1 0.06 0.01 ... 0

AA 1 0.98 0.05 ... 0

A 1 0.99 0.96 ... 0.01

: : : : : :

CCC 1 1 1 ... 0.10

32

モンテカルロ・シミュレーションの実行格付けのための閾値設定

PAAA +...+PD PAA +...+ PD PA +...+ PD ... PD

AAA 1 0.06 0.01 ... 0

AA 1 0.98 0.05 ... 0

A 1 0.99 0.96 ... 0.01

: : : : : :

CCC 1 1 1 ... 0.10

ZAAA ZAA ZA ... ZD

AAA ∞ - 1.52 - 2.42 ... - ∞

AA ∞ 1.97 - 1.65 ... - 3.25

A ∞ 2.99 1.72 ... - 3.15

: : : : : :

CCC ∞ ∞ ∞ ... - 1.30

33

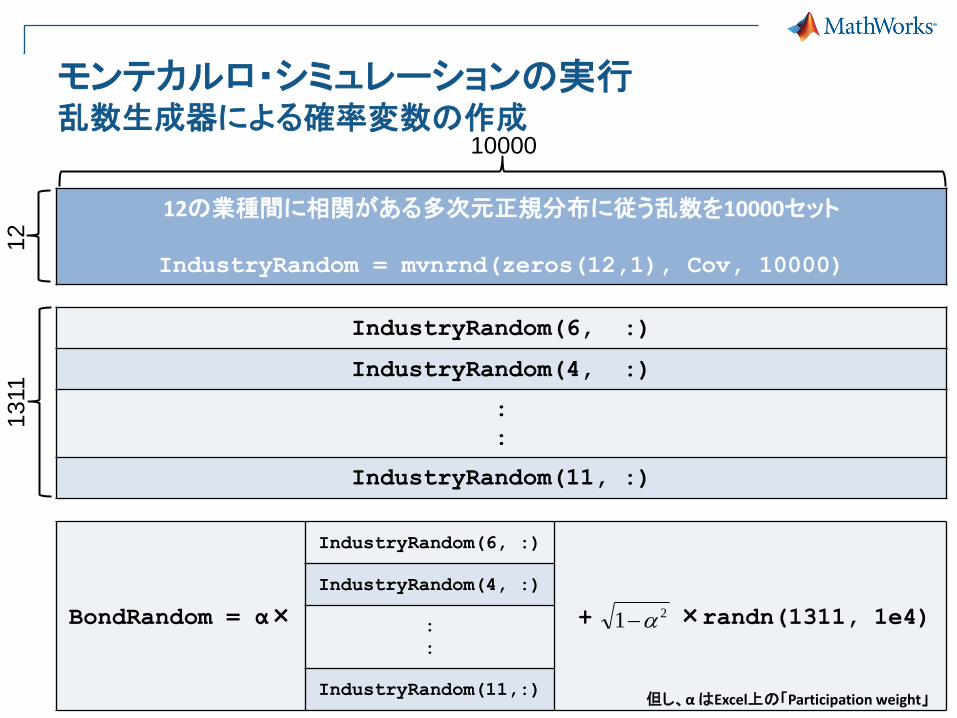

モンテカルロ・シミュレーションの実行乱数生成器による確率変数の作成

IndustryRandom(6, :)

IndustryRandom(4, :)

:

:

IndustryRandom(11, :)

12の業種間に相関がある多次元正規分布に従う乱数を10000セット

IndustryRandom = mvnrnd(zeros(12,1), Cov, 10000)

10000

12

1311

BondRandom = α×

IndustryRandom(6, :)

+ ×randn(1311, 1e4)

IndustryRandom(4, :)

:

:

IndustryRandom(11,:)

21

但し、α はExcel上の「Participation weight」

34

モンテカルロ・シミュレーションの実行確率変数がどの格付けに属するか評価

ZX ≦ BondRandom(n, :) ≦ ZX-1 を評価

• たとえば、n番目の債権がAAで先に作成した閾値ベクトルが

ZAAA ZAA ZA ZBBB ... ZCCC ZD

AA ∞ 1.97 - 1.65 -2.34 ... -3.24 -3.25

で、乱数により生成した BondRandom(n, :) のある成分の値が「-0.2735」とすると

ZA ≦ -0.2735 ≦ ZAA

という関係より、シミュレーションの結果は”ZAA “と判定される。

35

シミュレーションに基づいてポートフォリオを再評価

シミュレーションの結果、格付が「D」判定になった場合はSeniority (優先順位)に応じて、Β分布に従う乱数により回収率をシミュレーション

(デフォルト時の価格) = (額面価格) × ( に従う乱数)),( ba

但し、

2

2232

2

232

2

b

a

36

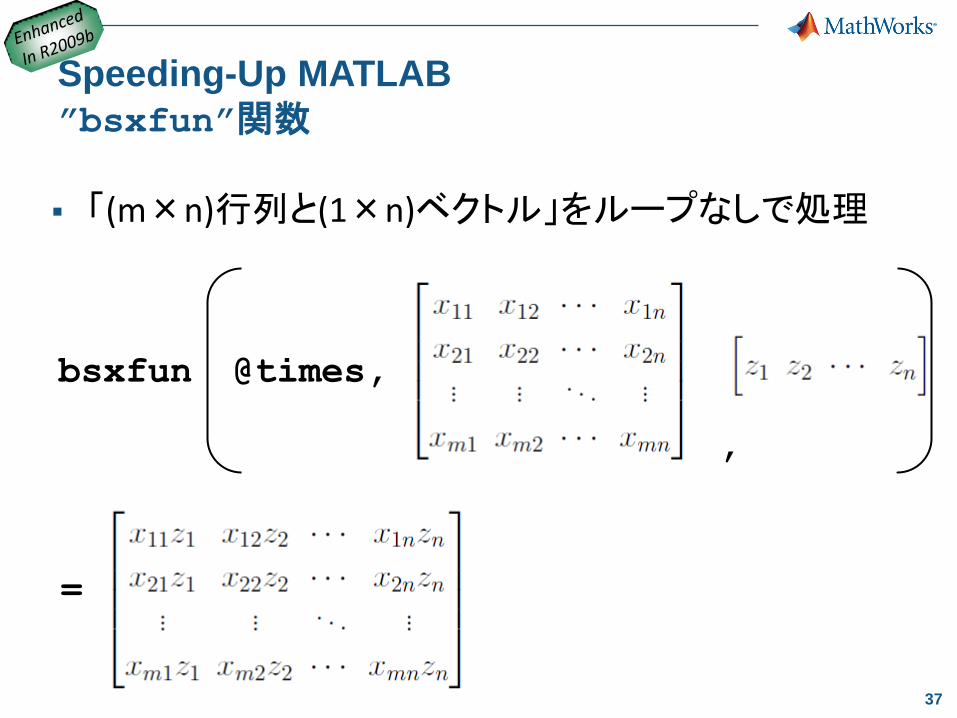

Speeding-Up MATLAB

”bsxfun”関数

「(m×n)行列と(m×1)ベクトル」をループなしで処理

bsxfun @plus,

,

=

37

Speeding-Up MATLAB

”bsxfun”関数

「(m×n)行列と(1×n)ベクトル」をループなしで処理

=

bsxfun @times,

,

38

登場した関数

betarnd : Β分布に従う乱数生成

bsxfun : 行列とベクトルを要素ごとに演算

prbyzero : ゼロ・クーポン・イールドカーブから債券価格を算出

mvnrnd : 多次元正規分布に従う乱数生成

norminv : 正規分布の逆関数

prctile : パーセンタイル値の計算

R2009b

39

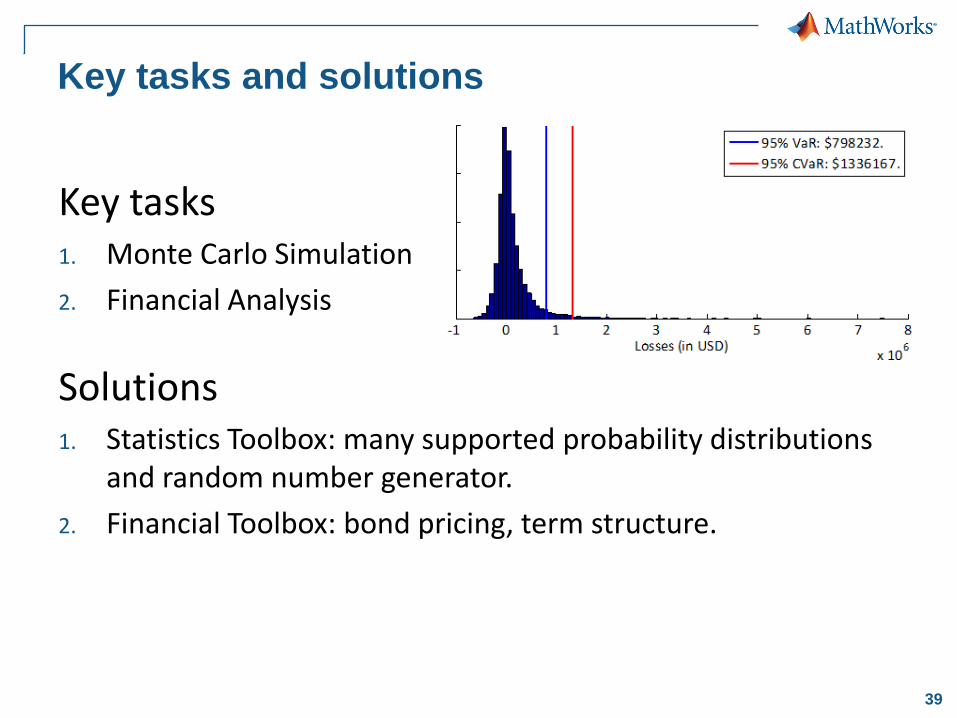

Key tasks1. Monte Carlo Simulation

2. Financial Analysis

Solutions1. Statistics Toolbox: many supported probability distributions

and random number generator.

2. Financial Toolbox: bond pricing, term structure.

Key tasks and solutions

40

Agenda

決定木による格付モデル

遷移行列とデフォルト確率

信用リスクの解析

まとめ

41

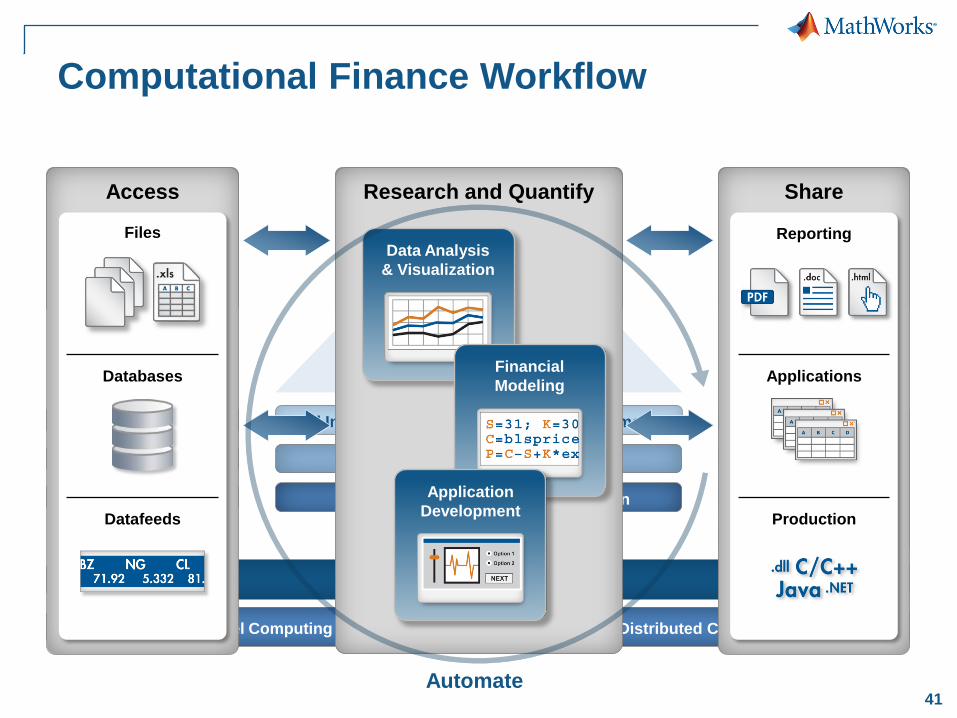

Computational Finance Workflow

Financial

Statistics Optimization

Fixed Income Financial Derivatives Econometrics

MATLAB

Parallel Computing MATLAB Distributed Computing Server

Files

Databases

Datafeeds

Access

Reporting

Applications

Production

Share

Data Analysis and Visualization

Financial Modeling

Application Development

Research and Quantify

Datafeed

Database

Spreadsheet Link EX

Builder NE

Builder EX

Builder JA

MATLAB Compiler

Rep

ort G

en

era

tor

Research and Quantify

Data Analysis

& Visualization

Financial

Modeling

Application

Development

Reporting

Applications

Production

Share

Automate

Files

Databases

Datafeeds

Access

42

標準モジュール生成と配布Excel VBAへの組込み

43

MATLABデスクトップ

End User

1

2

Toolboxes

標準モジュールの配布フロー

3

4

.dll

MATLAB Builder™ EX

MATLAB Compiler

MATLAB® Compiler™

44

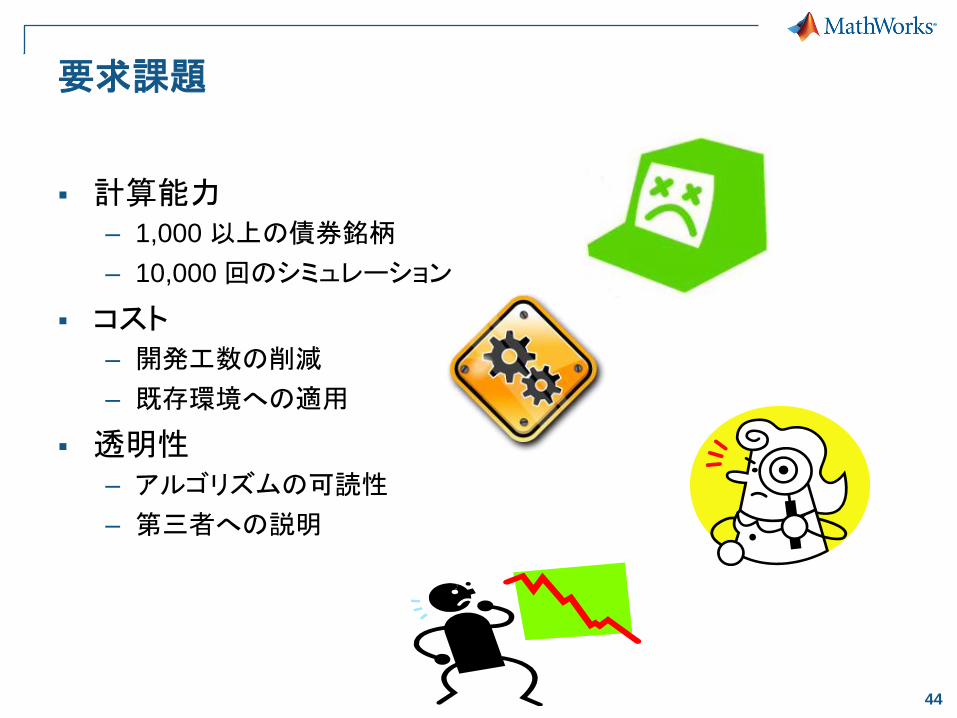

要求課題

計算能力– 1,000 以上の債券銘柄

– 10,000 回のシミュレーション

コスト– 開発工数の削減

– 既存環境への適用

透明性– アルゴリズムの可読性

– 第三者への説明

45

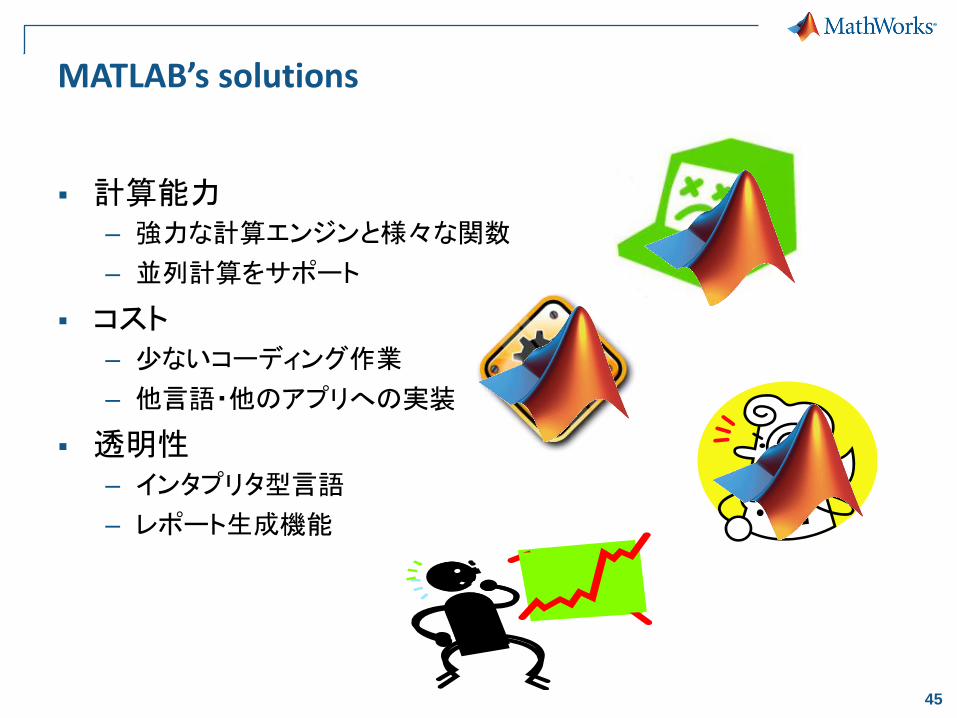

MATLAB’s solutions

計算能力– 強力な計算エンジンと様々な関数

– 並列計算をサポート

コスト– 少ないコーディング作業

– 他言語・他のアプリへの実装

透明性– インタプリタ型言語

– レポート生成機能

46

トレーニング サービス

投資 効果 トレーニング サービス 定期 トレーニング;

東京、名古屋、大阪にて定期開催

基礎コース(11)、応用コース(11)、

専門コース(4)を ご提供

オンサイト トレーニング; お客様サイトにて開催

ご要望に応じて3つのレベルでカリキュラムのカスタマイズが可能

投資対効果の最大化

47

Support and Community

48

Connections Program

More than 300 add-on products and services that

complement and extend MathWorks products:

Specialized third-party toolboxes for MATLAB

Interfaces to third-party software and hardware products

Specialized training courses and consulting services

System integrators and suppliers that incorporate

MathWorks products

49

Book Program

Controls Signal Processing Image Processing Biosciences Communications Mechanical Engineering

Mathematics Aerospace Engineering Environmental Sciences Chemistry Finance Electronics

More than 1,000 books for educational and professional use, in 26 languages

50

Technical Support

Resources

Over 100 support engineers

– All with MS degrees (EE, ME, CS)

– Local support in North America,

Europe, and Asia

Comprehensive, product-specific Web

support resources

High customer satisfaction

95% of calls answered

within three minutes

70% of issues resolved

within 24 hours

80% of customers surveyed

rate satisfaction at 80-100%