Embed Size (px)

Citation preview

The Role of Saving

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Benefits of Savings Savings means setting aside money for

future use. It allows you to accumulate money for

future purchases. Money in savings can earn an income.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Saving Basics Savings is the portion of current income

not spent on consumption. Savings accounts provide an easily

accessible place for people to store their money to meet daily living expenses and to have money for emergencies.

Financial experts recommend individuals keep a minimum of three to six months of salary in a savings account.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Savings Account Uses Daily Expenses Emergencies Future Purchases Future Investing

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Saving and Investing Saving is closely related to another

financial principle: investing. Saving – the main purpose is to set aside

money for some anticipated future need. Investing is committing money for the purpose

of making a profit over time. The objective is to make your money grow in the long run.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Saving vs. Investing Saving

The portion of current income not spent on consumption.

Place to store money for daily expenses and for emergencies.

Liquidity is how quickly and easily an asset can be converted into cash. In an emergency, cash needs to be easily accessible. Savings accounts are more liquid than investment accounts.

Generally yield a low interest rate, often barely meeting inflation.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Saving vs. Investing cont. Investing

The purchase of assets with the goal of increasing future income.

Develop and implement a savings plan before beginning an investment.

Investments are not liquid as savings. Rate of return, or annual return on the

investment, varies, but is usually higher.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Reasons People Should Save Emergencies – It is recommended individuals have a

minimum of three to six months of salary in savings accounts for emergencies. Examples of emergencies can include illness, losing a job, or immediate need to replace a large item such as a washing machine.

Recurring Expenses – Savings accounts can be used as a budgeting tool to manage monthly expenses.

Future Purchases – Money can be used to meet future goals such as a college education, new car, down payment on a home, or a new stereo.

Investing – After an individual has established a savings account, money should be invested monthly for future income.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Reasons People Should Save Financial Goals – pay for college, have a

family. Retirement – although it seems a long way

off, to live comfortably you have to start when you get a full time job.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Why People Don’t Save People are not having their current consumption

needs and wants met. People do not know how much they need to be saving

or investing for future goals. Money in savings accounts earns such poor interest

rates. It barely (if at all) keeps up with inflation. Investing usually gains higher interest rates.

Individuals justify not needing money for emergencies because they have credit easily available.

People feel they have adequate insurance and job security; therefore they do not need money for emergencies.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Developing a Savings Plan Track spending for one month to

determine where money is currently going.

Evaluate spending and determine where money can be saved.

Decide what you are saving for. Set a specific goal Decide what amount will be put into

savings per month, put decision into writing and stick to it!

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Develop a Spending Plan Break your long term goal into short temr

goals Save regualry and consistently Put your savings to work – keep in an

account that earns some interest. Be willing to make adjustments. If the

savings plan is not working evaluate why. Keep your savigns golas in mind.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Consider your budget The amount you save must be realistic,

leave enough money to pay your daily expenses.

Percent to go to savings will depend on your Discretionary income – the amount of available income after taxes and necessary spending for food, clothing and shelther

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

“Pay Yourself First” Put money away into a savings

account or investment BEFORE you pay other bills or use for spending.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

70-20-10 Rule Spend 70% of money you earn Save 20% of money you earn Invest 10% of money you earn

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Pay Yourself First (continued)

If you are self disciplined, you can deposit into savings when you cash a check

But…. Automatic transfers – Each month the bank will

transfer a specified amount from checking to savings

Direct deposit – employers can electronically deposit earnings in the employee’s bank account.

Payroll deductions – you tell employers an amount to deduct and put into a savings plan

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Earning by Savings When you open an account at a financial

institution, your money will begin to earn interest.

Savings accounts can differ in how often interest is paid or credited to you.

The interest rate stated if the annual rate, Accounts differ in how the interest

calculation is made Simple vs. compound interest

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

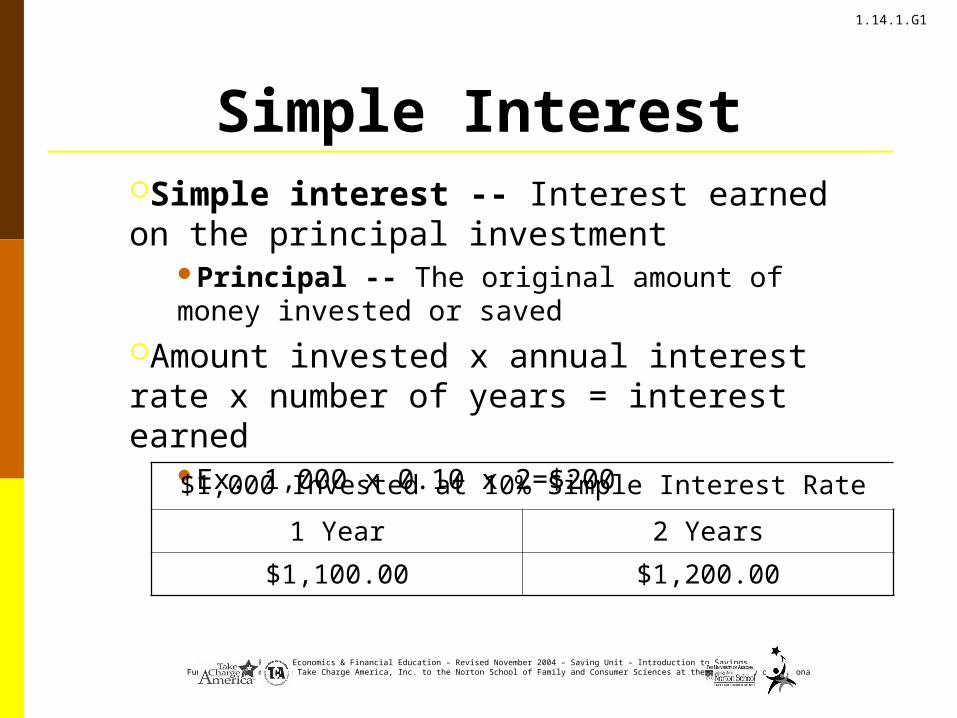

Simple InterestSimple interest -- Interest earned on the principal investment

Principal -- The original amount of money invested or saved

Amount invested x annual interest rate x number of years = interest earned

Ex. 1,000 x 0.10 x 2=$200

$1,000 Invested at 10% Simple Interest Rate

1 Year 2 Years

$1,100.00 $1,200.00

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

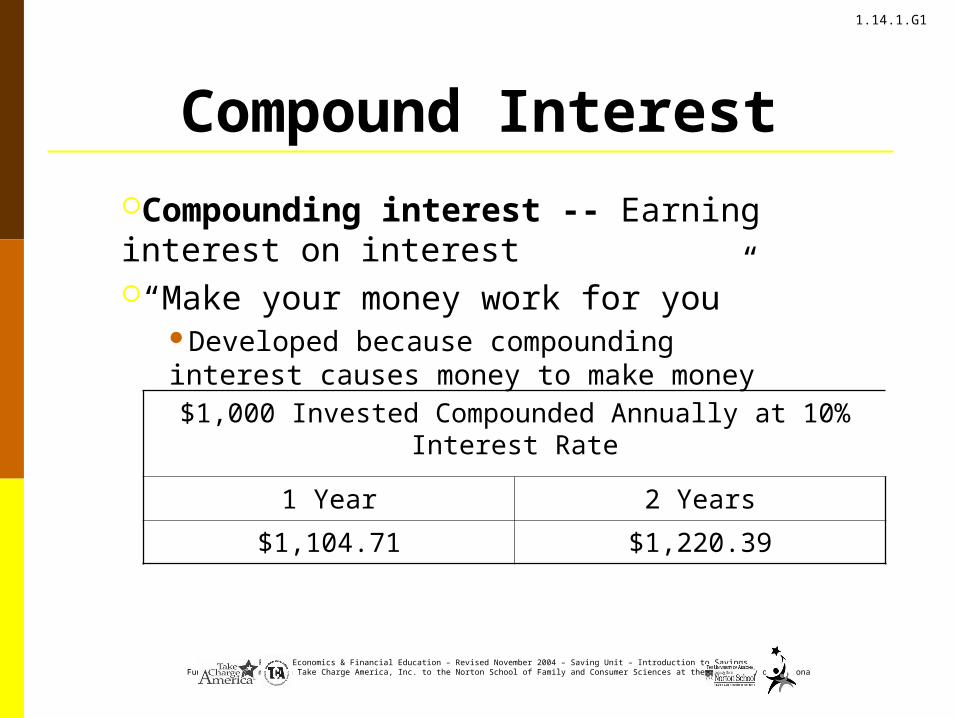

Compound InterestCompounding interest -- Earning interest on interest“Make your money work for you”

Developed because compounding interest causes money to make money

$1,000 Invested Compounded Annually at 10% Interest Rate

1 Year 2 Years

$1,104.71 $1,220.39

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Annual Percentage Yield APY – tells you the actual annual rate at

which interest is earned, including the effects of compounding.

With simple interest, the APY is the same as the state interest rate.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Three Factors Affecting the Time Value Calculations

TimeAmount investedInterest rate

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Time

The earlier an individual invests, the more time their investment has to compound interest and increase in value

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

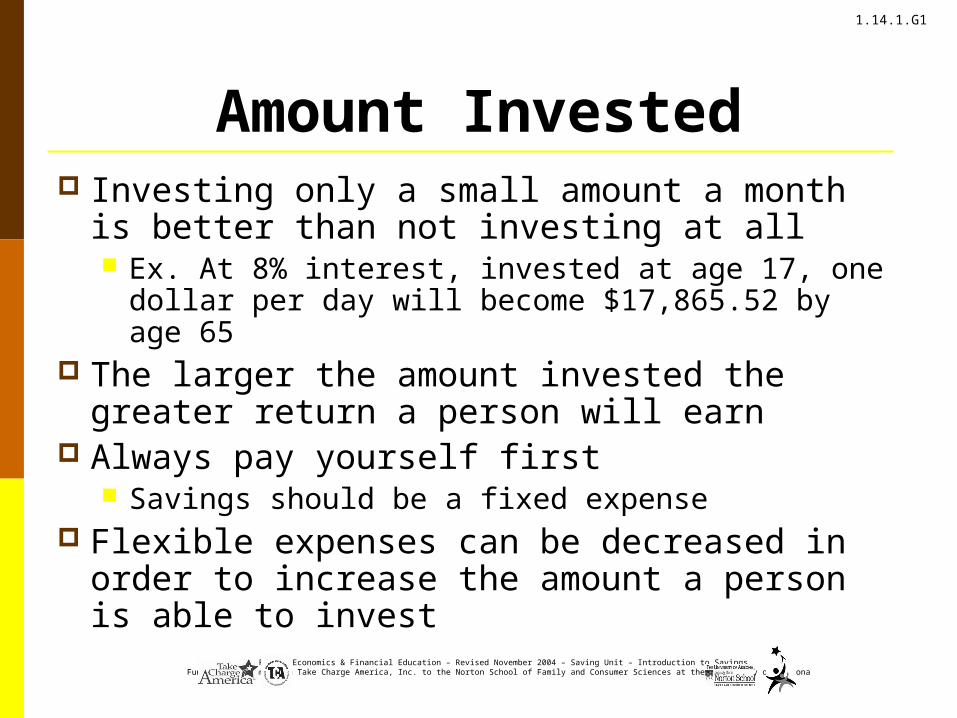

Amount Invested Investing only a small amount a month is

better than not investing at all Ex. At 8% interest, invested at age 17, one dollar

per day will become $17,865.52 by age 65 The larger the amount invested the greater

return a person will earn Always pay yourself first

Savings should be a fixed expense Flexible expenses can be decreased in

order to increase the amount a person is able to invest

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

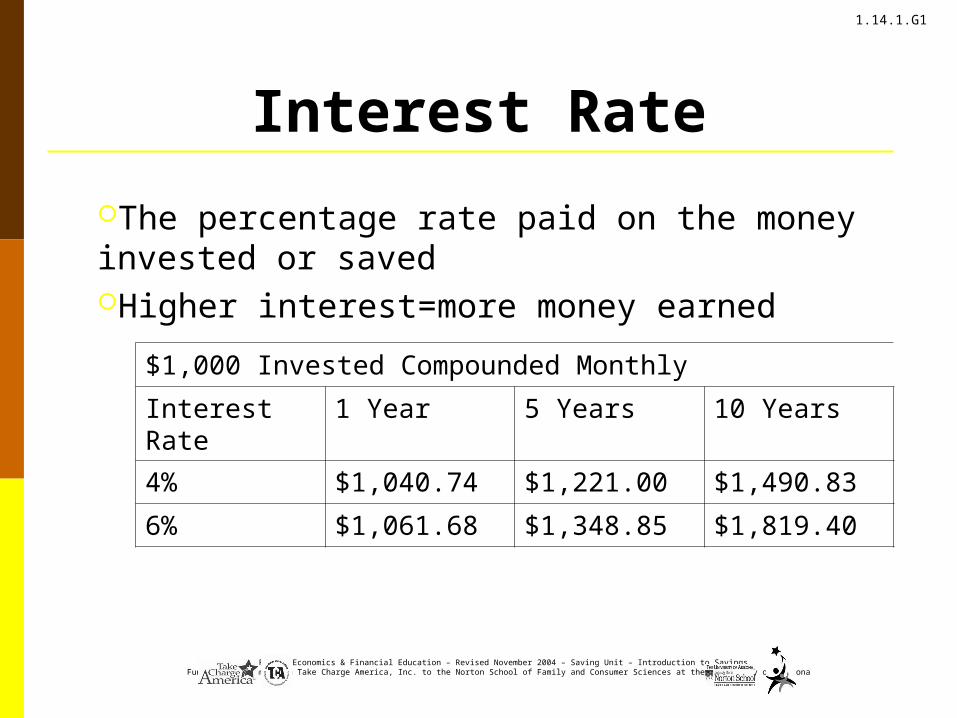

Interest Rate

The percentage rate paid on the money invested or savedHigher interest=more money earned

$1,000 Invested Compounded Monthly

Interest Rate

1 Year 5 Years 10 Years

4% $1,040.74 $1,221.00 $1,490.83

6% $1,061.68 $1,348.85 $1,819.40

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Long term effects of Compounding

The effects of compound interest increase greatly over time.

Long term effects of Interest Rates

Higher interest rates mean greater earning in the long run.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

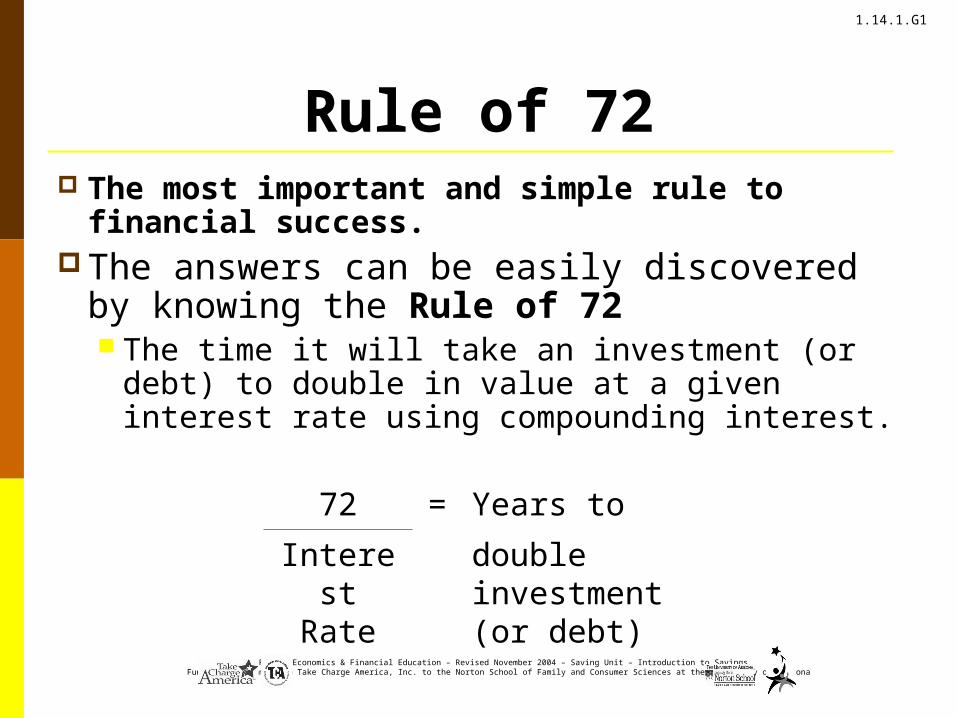

Rule of 72 The most important and simple rule to

financial success. The answers can be easily discovered by

knowing the Rule of 72 The time it will take an investment (or debt)

to double in value at a given interest rate using compounding interest.

72 = Years to

Interest Rate

double investment (or debt)

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

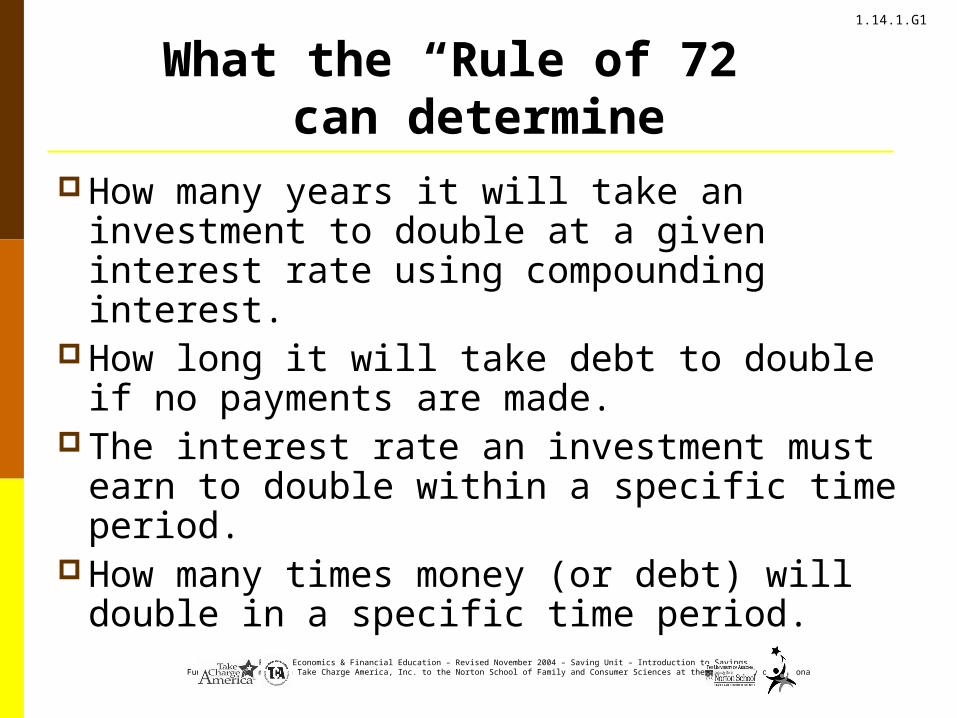

What the “Rule of 72” can determine

How many years it will take an investment to double at a given interest rate using compounding interest.

How long it will take debt to double if no payments are made.

The interest rate an investment must earn to double within a specific time period.

How many times money (or debt) will double in a specific time period.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

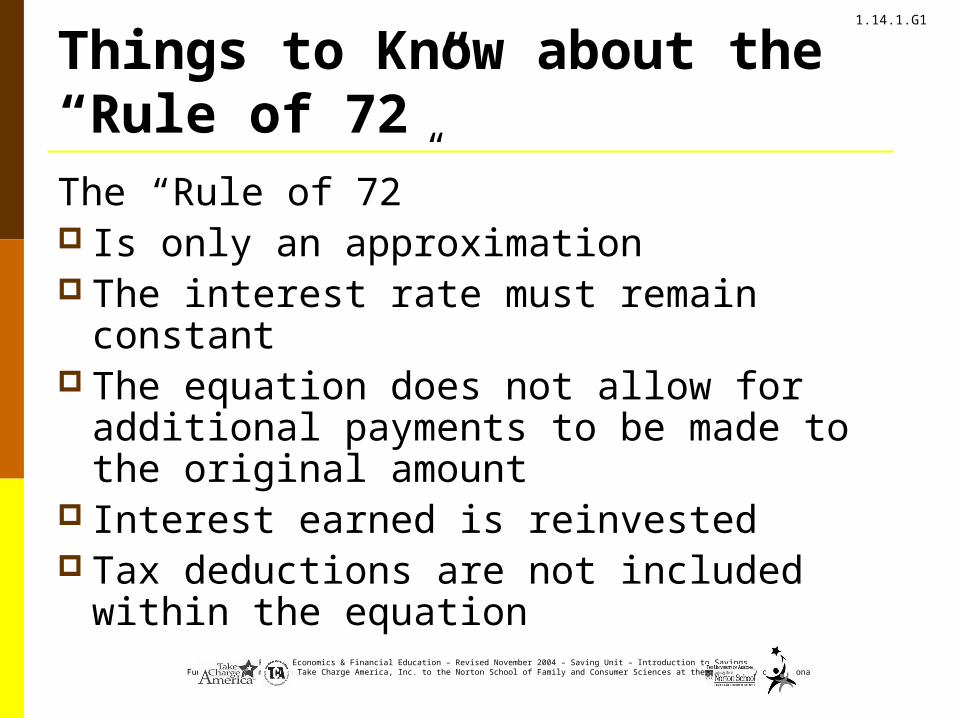

Things to Know about the “Rule of 72”The “Rule of 72” Is only an approximation The interest rate must remain constant The equation does not allow for

additional payments to be made to the original amount

Interest earned is reinvested Tax deductions are not included within

the equation

Savings Option

To get the most out you your savings,you

need to keep your money where it will

earn interest.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

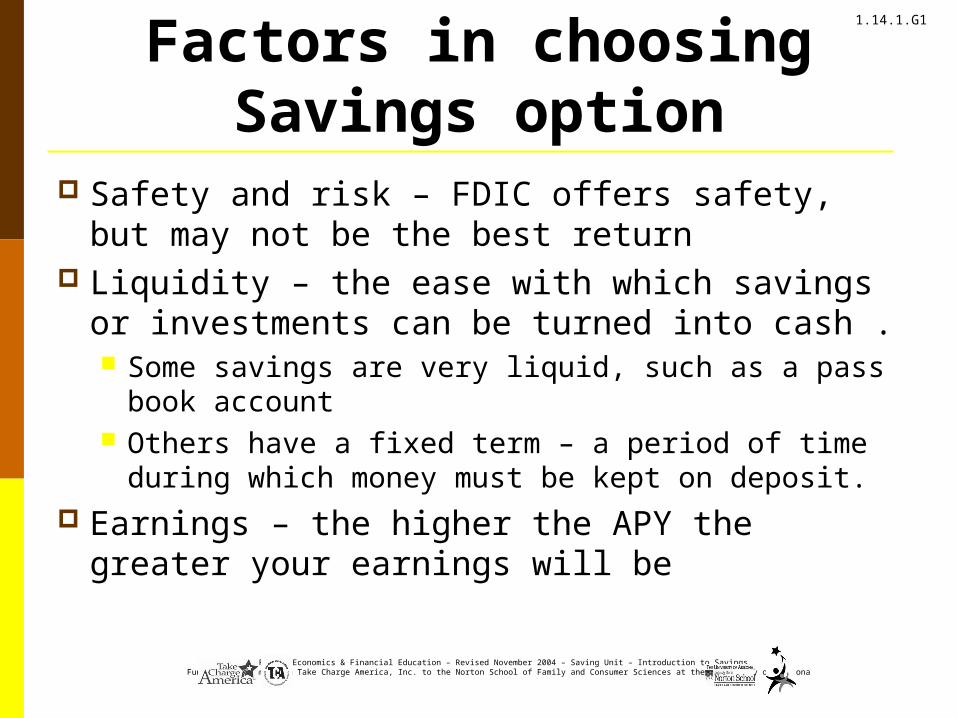

Factors in choosing Savings option

Safety and risk – FDIC offers safety, but may not be the best return

Liquidity – the ease with which savings or investments can be turned into cash . Some savings are very liquid, such as a pass

book account Others have a fixed term – a period of time

during which money must be kept on deposit. Earnings – the higher the APY the greater

your earnings will be

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Factors in choosing Savings option (continued)

Taxes – in most cases you must pay income taxes on the interest you earn from a savings account. Although some offer tax advantages.

Restrictions – depending on the type of savings product you choose, you may have to comply with some restrictions

Fee and service charges

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Basic Savings Options Savings Account

Account to hold money not spent on consumption.

Money may be accessed or transferred between accounts through:

Automated teller machines; Telephones; Internet.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Savings Account continued

Features may include: Allows for frequent deposits or

withdrawals; Easily accessible; Money storage for emergencies or daily

living; Available at depository institutions; May require a minimum balance or have

a limited number of withdrawals.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Money Market Deposit Account

Money Market Deposit Account A government insured account offered at

most depository institutions. Have a minimum balance requirement with

tiered interest rates. The amount of interest earned depends on

the account balance. For example: a balance of $10,000

will earn a higher interest rate than a balance of $2,500.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Continued Features of may include:

Minimum amount required to open the account, often $1,000;

Usually limited to three to six transactions each month;

If the average monthly balance falls below a specified amount, the entire account will earn a lower interest rate.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Certificate of Deposit Certificate of Deposit (CD)

An insured, interest earning savings instrument with restricted access to the funds.

Found in depository institutions accepting deposits for a certain length of time.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

CD continued Features of may include:

Range from seven days to eight years in length;

Minimum deposits range from $100-$100,000; If funds are withdrawn before the expiration

date, penalties are assessed; Low risk and no fees; Interest rates vary depending upon specified

time length. The longer the length, the higher the interest rate.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Savings BondsSavings Bond Discount bond purchased for 50% of the face

value from the U.S. Government.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

Savings Bond Continued Features of may include:

Many different types available; Can be purchased for $25.00 - $10,000.00;

A $100.00 bond would be purchased for $50.00. When the bond matures to $100.00, it can be redeemed.

Interest earned on a bond is tax exempt until redeemed.

No taxes are due on interest earned. It will be tax exempt when redeemed if used for

college expenses.

© Family Economics & Financial Education – Revised November 2004 – Saving Unit – Introduction to SavingsFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences at the University of Arizona

1.14.1.G1

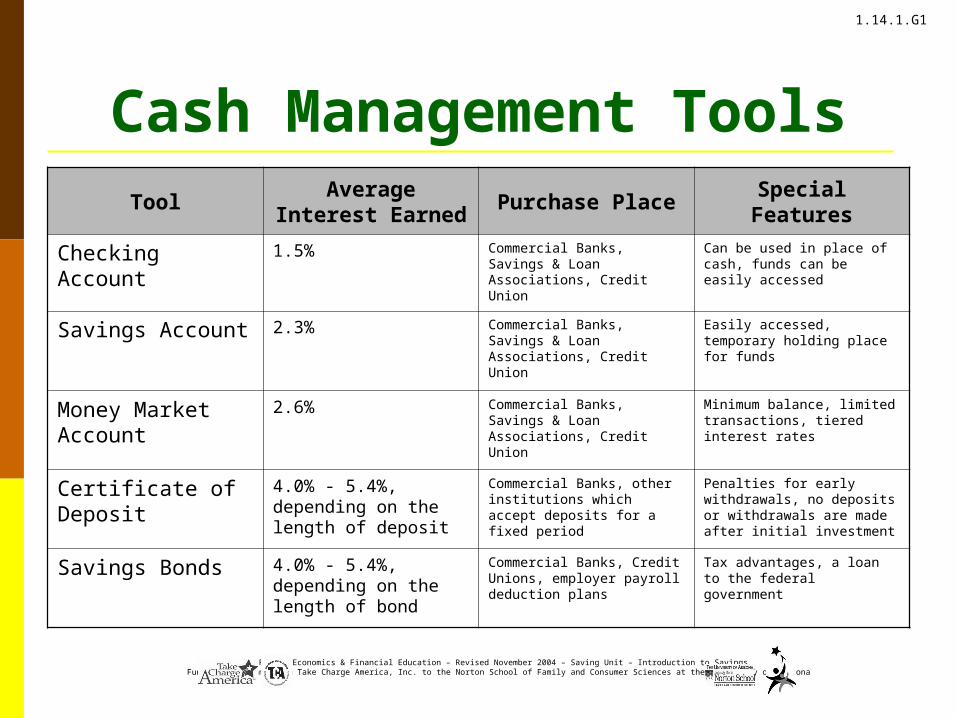

Cash Management ToolsTool

Average Interest Earned

Purchase PlaceSpecial

Features

Checking Account 1.5% Commercial Banks, Savings & Loan Associations, Credit Union

Can be used in place of cash, funds can be easily accessed

Savings Account 2.3% Commercial Banks, Savings & Loan Associations, Credit Union

Easily accessed, temporary holding place for funds

Money Market Account

2.6% Commercial Banks, Savings & Loan Associations, Credit Union

Minimum balance, limited transactions, tiered interest rates

Certificate of Deposit

4.0% - 5.4%, depending on the length of deposit

Commercial Banks, other institutions which accept deposits for a fixed period

Penalties for early withdrawals, no deposits or withdrawals are made after initial investment

Savings Bonds 4.0% - 5.4%, depending on the length of bond

Commercial Banks, Credit Unions, employer payroll deduction plans

Tax advantages, a loan to the federal government