Embed Size (px)

Citation preview

This presentation has been prepared to help stakeholders understand the updated workplan for the projects in the Memorandum of Understanding between the FASB and IASB. The views expressed in this presentation are those of the presenter. Official positions of the IASB and the FASB are reached only after extensive due process and deliberations.

Leases Update

April 2011

April 2011

2

Russ Golden – FASB Member

Susan Cosper – FASB Technical Director

April 2011

3Agenda

• Outreach

• Changes made from the Exposure Draft

– Definition of a lease

– Variable payments

– Renewal options

– Short-term leases

– Finance/Other-than-finance leases

• Next steps

April 2011

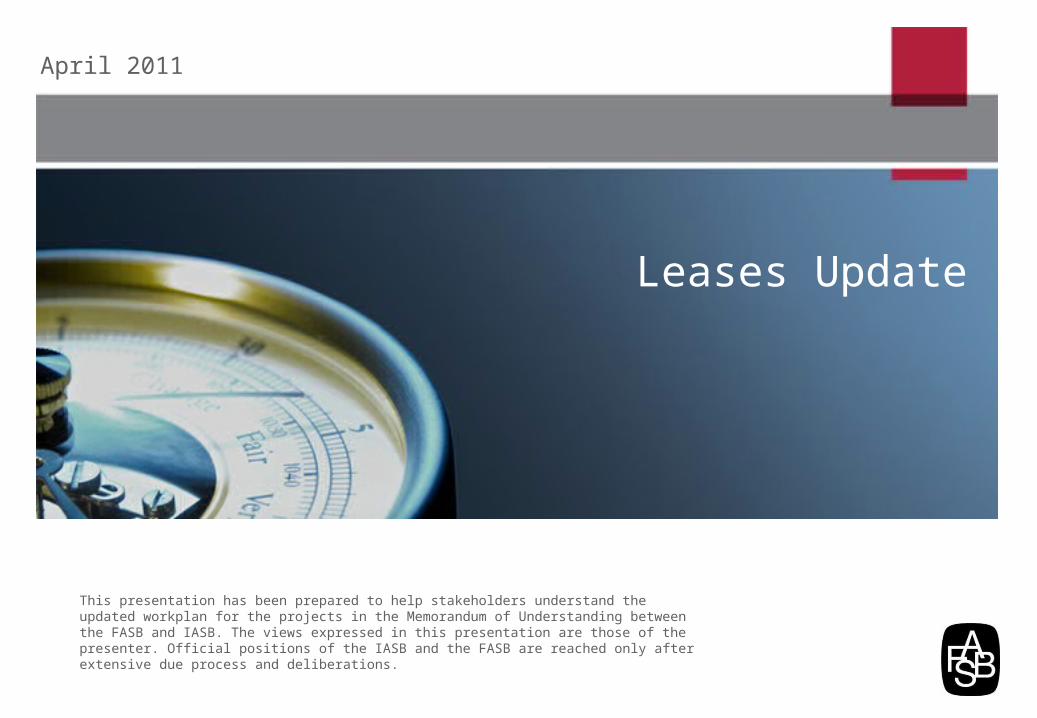

4Outreach – comment letter period

• Roundtables (7)

– London, Hong Kong, Chicago, Norwalk

• Preparer workshops (15)

• Various outreach meetings – over 1500 organizations, over 200 meetings

• Preparer questionnaires – 250 lessors, 400 lessees

• Project webcasts and podcasts

April 2011

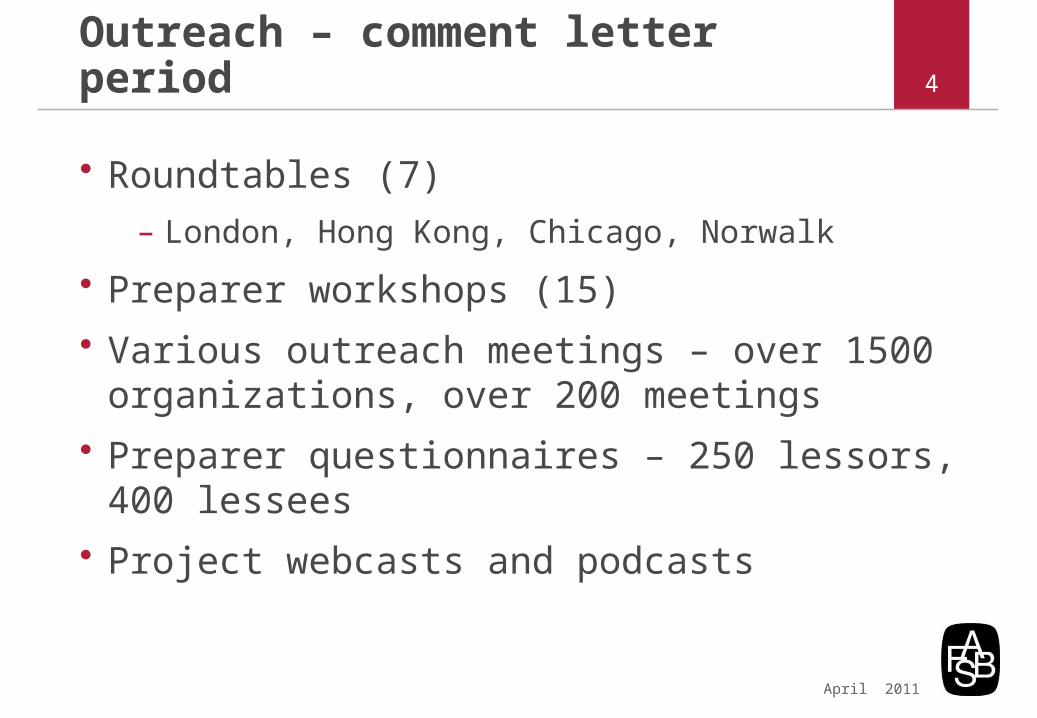

5Targeted outreach – March/April 2011

• Over 20 meetings, 70 representatives

– Users, preparers, standard-setting organizations, accounting firms and representatives of the leases joint working group

• Industries: retail and trade, power and utilities, oil and gas, life sciences, financial services, real estate, airlines, outsourcing, shipping, telecommunications and construction

April 2011

6What we heard

• Complexity and cost

• Definition of a lease

• Estimation and judgment

– Variable payments, renewal options

• P/L pattern

• Lessor accounting

• Investment properties

April 2011

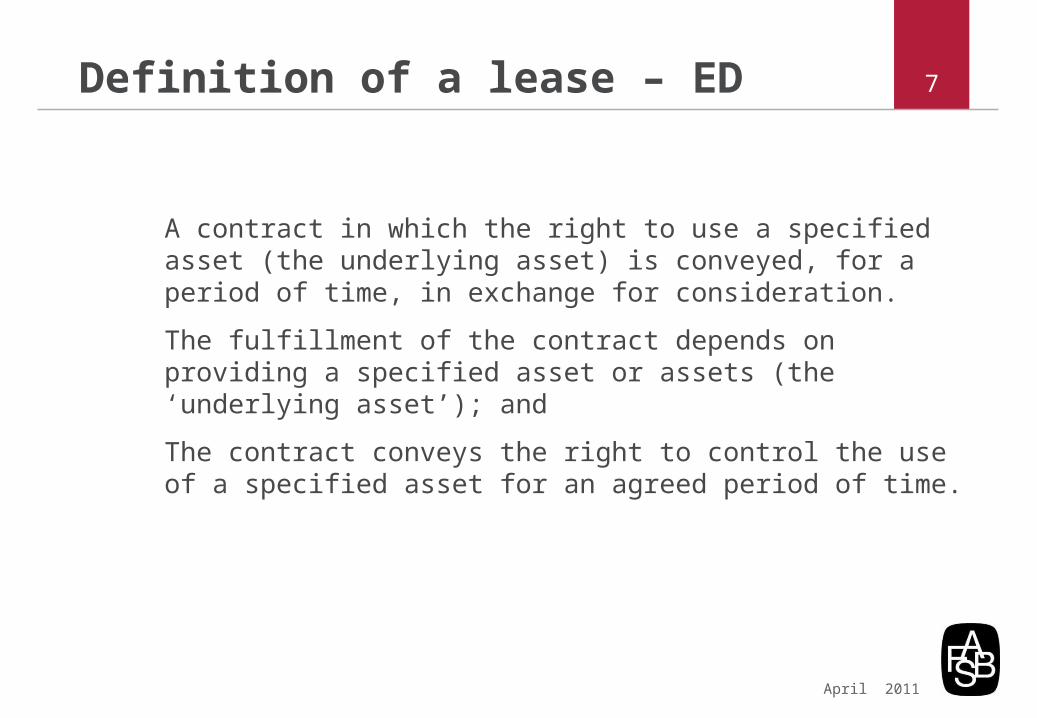

7Definition of a lease – ED

A contract in which the right to use a specified asset (the underlying asset) is conveyed, for a period of time, in exchange for consideration.

The fulfillment of the contract depends on providing a specified asset or assets (the ‘underlying asset’); and

The contract conveys the right to control the use of a specified asset for an agreed period of time.

April 2011

8

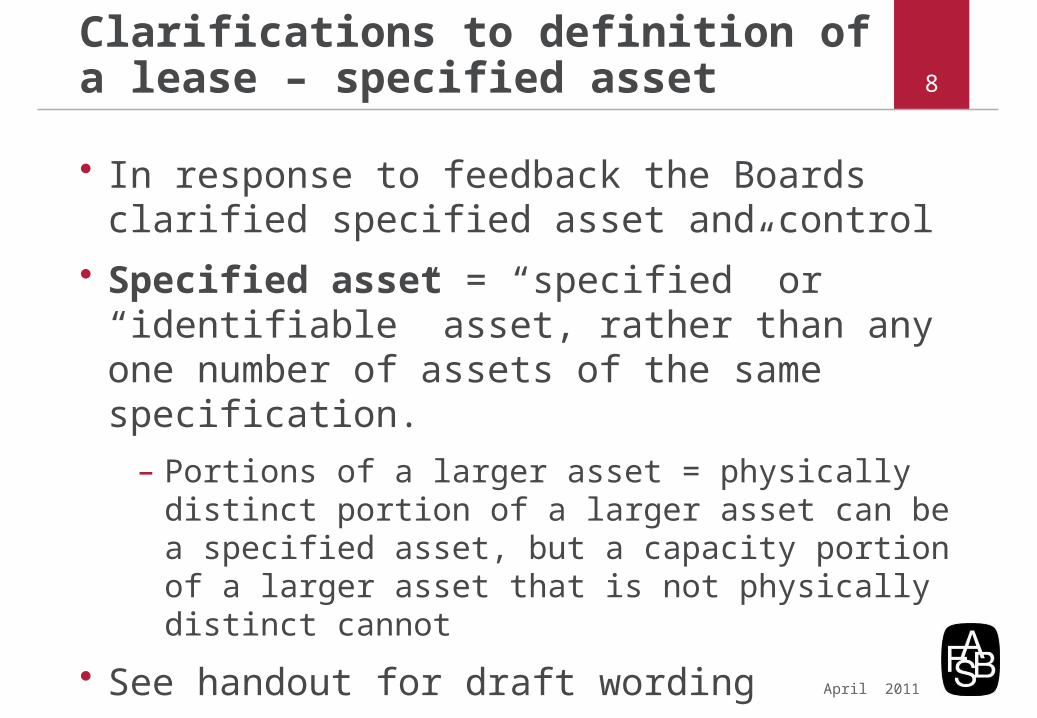

Clarifications to definition of a lease – specified asset

• In response to feedback the Boards clarified specified asset and control

• Specified asset = “specified” or “identifiable” asset, rather than any one number of assets of the same specification.

– Portions of a larger asset = physically distinct portion of a larger asset can be a specified asset, but a capacity portion of a larger asset that is not physically distinct cannot

• See handout for draft wording

April 2011

9

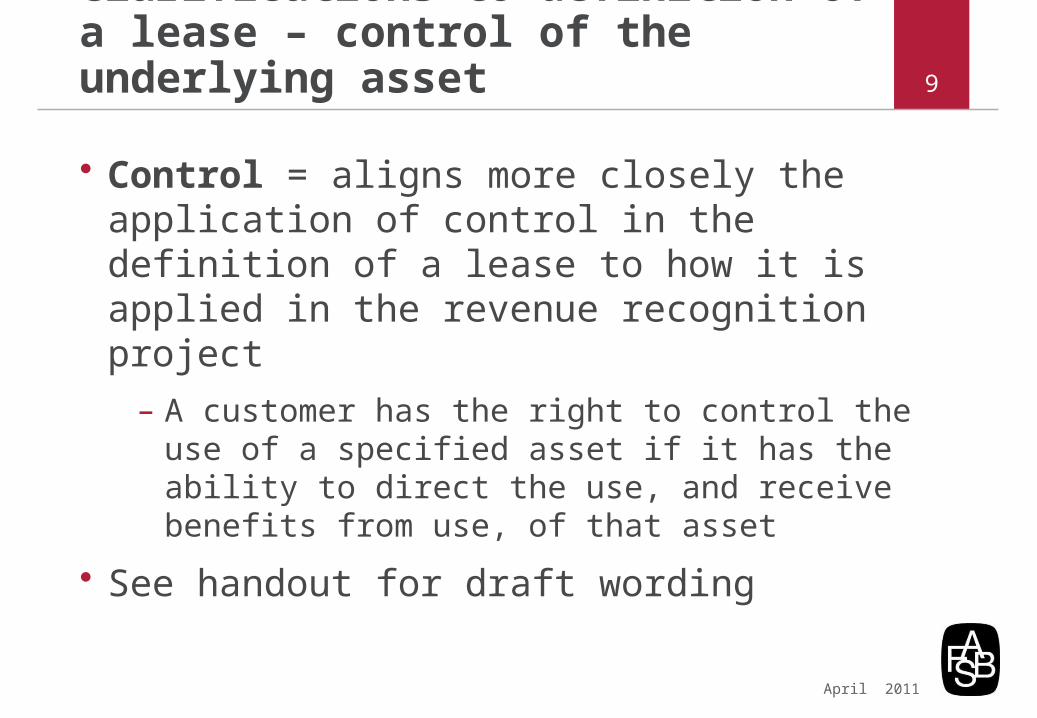

Clarifications to definition of a lease – control of the underlying asset

• Control = aligns more closely the application of control in the definition of a lease to how it is applied in the revenue recognition project

– A customer has the right to control the use of a specified asset if it has the ability to direct the use, and receive benefits from use, of that asset

• See handout for draft wording

April 2011

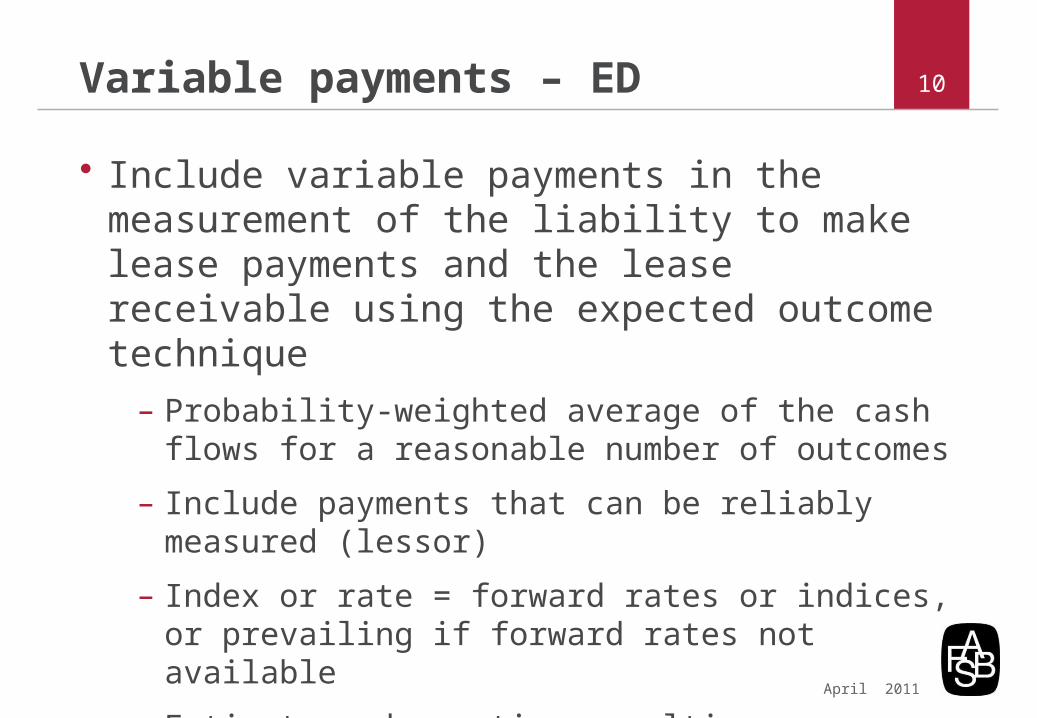

10Variable payments – ED

• Include variable payments in the measurement of the liability to make lease payments and the lease receivable using the expected outcome technique

– Probability-weighted average of the cash flows for a reasonable number of outcomes

– Include payments that can be reliably measured (lessor)

– Index or rate = forward rates or indices, or prevailing if forward rates not available

– Estimate under option penalties

April 2011

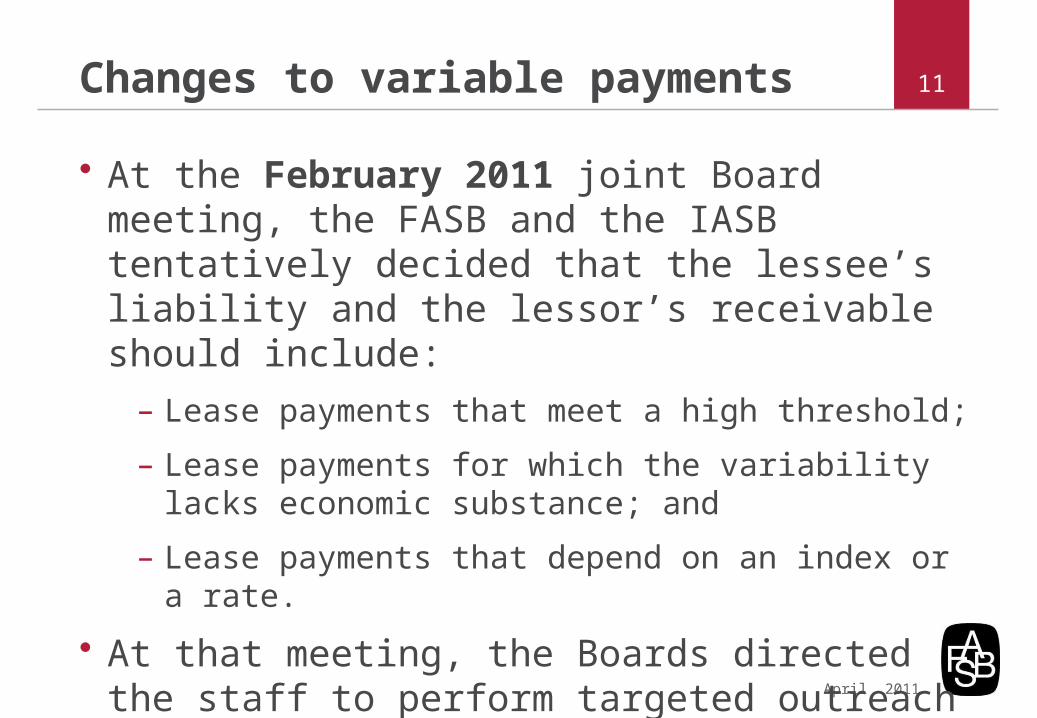

11Changes to variable payments

• At the February 2011 joint Board meeting, the FASB and the IASB tentatively decided that the lessee’s liability and the lessor’s receivable should include:

– Lease payments that meet a high threshold;

– Lease payments for which the variability lacks economic substance; and

– Lease payments that depend on an index or a rate.

• At that meeting, the Boards directed the staff to perform targeted outreach on those tentative decisions.

April 2011

12Changes to variable payments

• In response to targeted outreach in March and April the Boards tentatively decided:

– The measurement of the lessee’s liability and the lessor’s receivable should not include variable lease payments that meet a high threshold.

– The measurement of the lessee’s liability and the lessor’s receivable should include lease payments that are in-substance fixed lease payments but are structured as variable lease payments in form.

– The Boards will discuss lease payments that depend on an index or a rate, including reassessment, at a future meeting.

April 2011

13Renewal Options

• ED: longest possible term that is more likely than not to occur

• Changes:

– Options to extend or terminate when there is a significant economic incentive to extend, or not to terminate the lease

– Reassess only when there is a significant change in relevant factors

April 2011

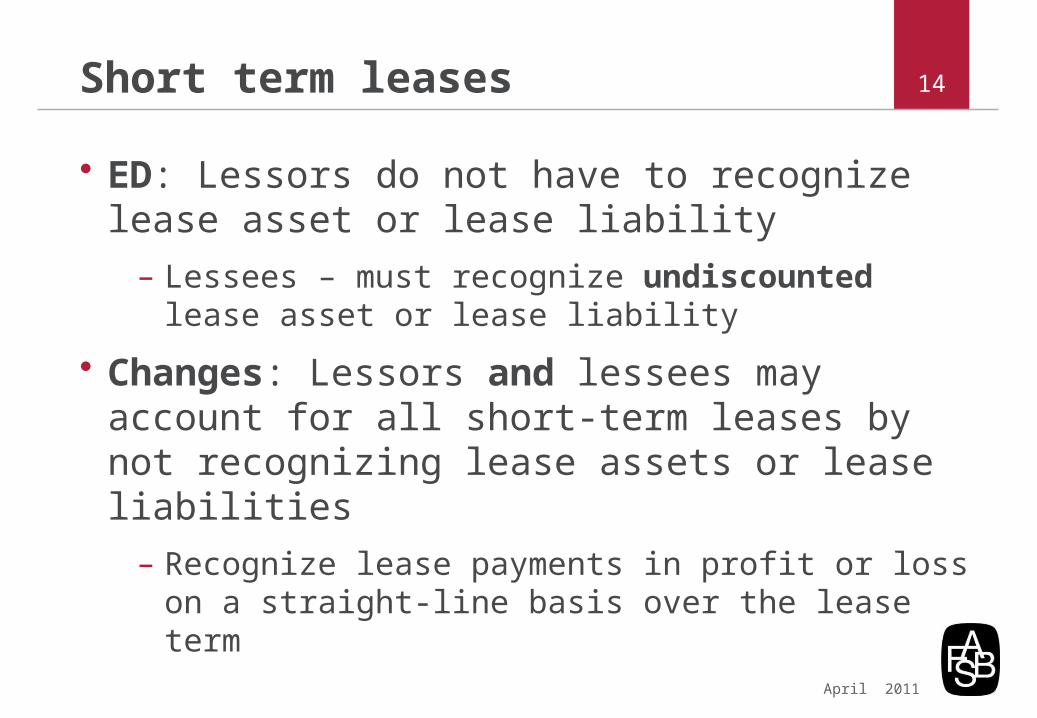

14Short term leases

• ED: Lessors do not have to recognize lease asset or lease liability

– Lessees – must recognize undiscounted lease asset or lease liability

• Changes: Lessors and lessees may account for all short-term leases by not recognizing lease assets or lease liabilities

– Recognize lease payments in profit or loss on a straight-line basis over the lease term

April 2011

15Lessee model – ED

• Lessee

– Right-of-use model

– Initial measurement

• Liability = PV of the estimated future lease payments over the lease term

• ROU asset = liability plus any initial direct costs

– Subsequent measurement

• Amortization expense on ROU asset

• Interest expense on the liability using the interest method to recognize liability at amortized cost

April 2011

16Lessor: performance obligation – ED

• Performance obligation approach – lessor exposed to significant risks or benefits associated with the underlying asset

– Initial measurement

• Lease receivable = PV of estimated lease payments plus any initial direct costs

• Performance obligation

– Subsequent measurement

• Systematic and rational approach to amortize to lease income

• Recognize interest income using the interest method

April 2011

17Lessor: derecognition model – ED

• Derecognition approach – lessor not exposed to significant risks or benefits of the underlying asset

• Initial measurement

– Lease receivable = PV of estimated lease payments plus any initial direct costs

– Residual asset

– Derecognize the underlying asset

• Subsequent measurement

– Amortize the receivable and recognize interest income using the interest method

April 2011

18Two types of leases

• In response to feedback, the Boards discussed two models for both lessees and lessors at the April 13th Board Meeting

• Boards decided that there should be two accounting approaches for leases for both lessees and lessors

– Tentatively termed ‘other-than-finance’ and ‘finance’ leases

– Existing guidance in IAS 17 should be used to make that distinction for both lessees and lessors – see handout for draft wording

April 2011

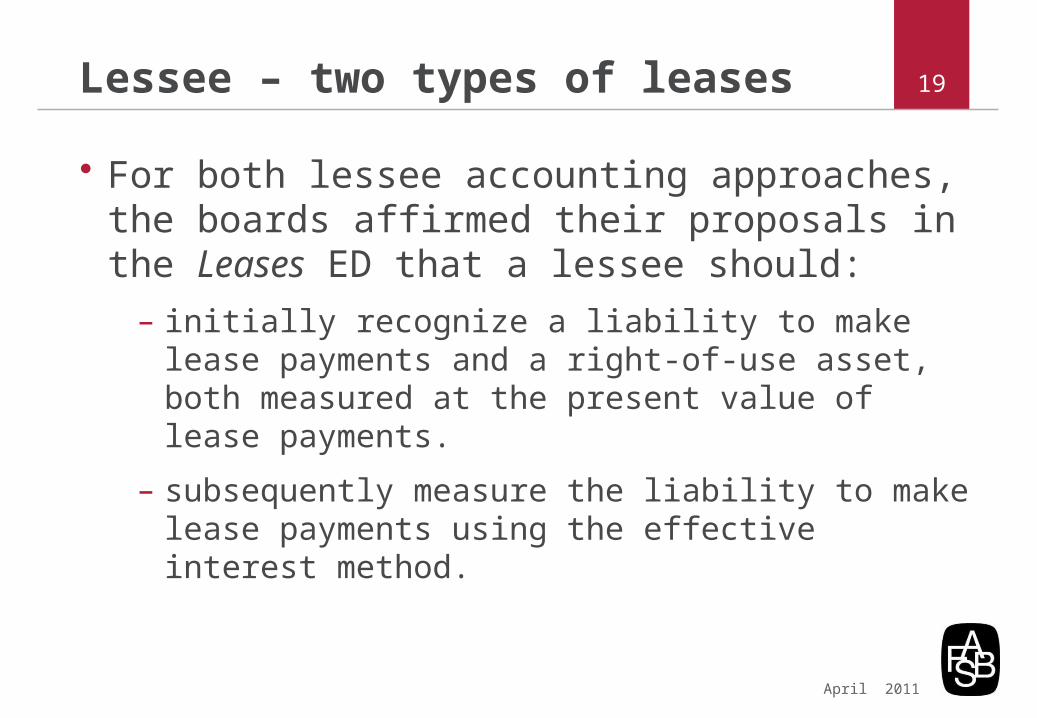

19Lessee – two types of leases

• For both lessee accounting approaches, the boards affirmed their proposals in the Leases ED that a lessee should:

– initially recognize a liability to make lease payments and a right-of-use asset, both measured at the present value of lease payments.

– subsequently measure the liability to make lease payments using the effective interest method.

April 2011

20Lessee – finance lease

• For finance leases, a lessee should, consistent with the proposals in the exposure draft:

– amortize the right-of-use asset on a systematic basis that reflects the pattern of consumption of the expected future economic benefits in accordance with IAS 38 Intangible Assets and Topic 350 Intangibles—Goodwill and Other.

– present amortization of the right-of-use asset and interest expense on the liability to make lease payments separately from other amortization and interest expense, either in profit or loss or in the notes.

April 2011

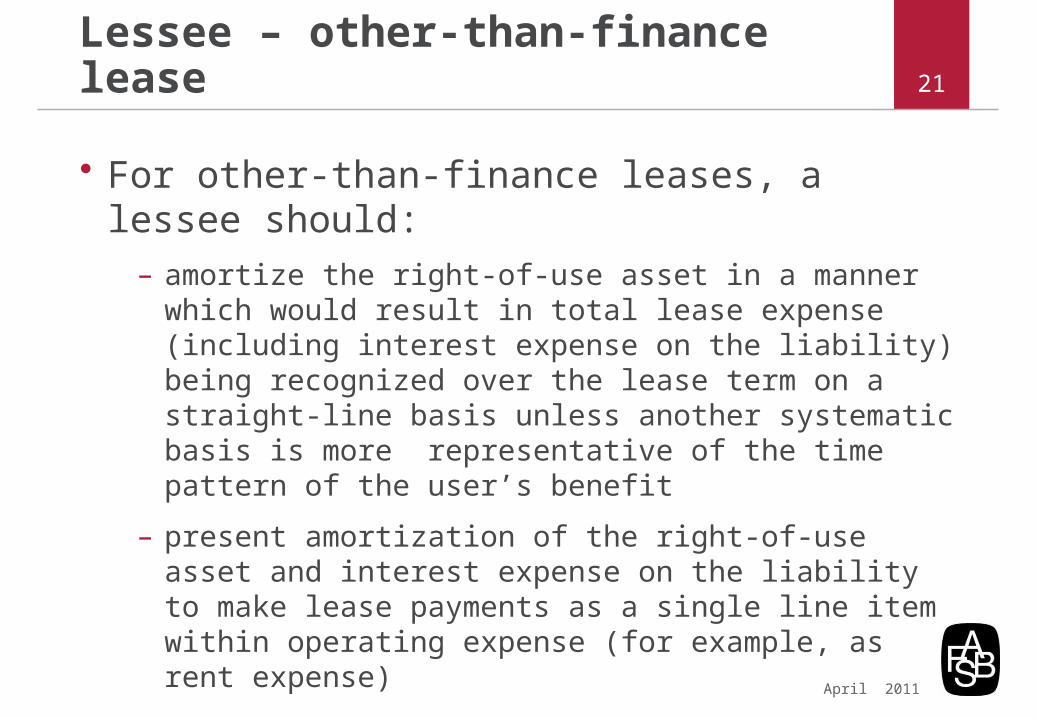

21Lessee – other-than-finance lease

• For other-than-finance leases, a lessee should:– amortize the right-of-use asset in a manner which would

result in total lease expense (including interest expense on the liability) being recognized over the lease term on a straight-line basis unless another systematic basis is more representative of the time pattern of the user’s benefit

– present amortization of the right-of-use asset and interest expense on the liability to make lease payments as a single line item within operating expense (for example, as rent expense)

April 2011

22Lessor model

• Next Board Meeting to decide the approaches for lessor accounting

April 2011

23Next steps

• Continue redeliberations – technical decisions

• Public consultation document

– Draft language – see handout

• Timing

April 2011

24Contact information

• Russ Golden – [email protected]

• Susan Cosper – [email protected]

• Danielle Zeyher – [email protected]

• Grace Hinchman – [email protected]

April 2011

25

QUESTIONS