Embed Size (px)

Citation preview

คณะพาณิชยศาสตร์และการบัญช ีมหาวิทยาลัยธรรมศาสตร ์

ปีที่ 34 ฉบับที่ 130 เมษายน-มิถุนายน 2554

59

Understanding the Event Study

Dr.Thitima Sitthipongpanich Assistant Professor of Department of Finance,

Faculty of Business Administration,

Dhurakij Pundit University

บทคัดย่อ ารศึกษาเหตุการณ์ (Event Study) เป็นวิธีวิจัย

ที่ใช้อย่างกว้างขวางสำหรับงานวิจัยทางด้าน

บริหารธุรกิจ การดำเนินงานวิจัยด้วยการศึกษา

เหตุการณ์มีส่วนเกี่ยวข้องถึงการระบุเหตุการณ์

ที่สนใจ การประมาณการณ์ผลตอบแทนส่วนเกิน และการ

ทดสอบความมีนัยสำคัญของเหตุการณ์ บทความนี้จะบรรยาย

ถึงการใช้วิธีวิจัยการศึกษาเหตุการณ์ ขั้นตอนการทำวิจัยด้วย

วิธีการศึกษาเหตุการณ์ และความแตกต่างของการใช้วิธีวิจัย

ดังกล่าว

vent studies are widely used in business

research. Conducting an event study

involves identifying an event of interest,

estimating abnormal stock returns relating

to the event and then testing the significance of the

event. This paper describes the application of event

study methodology, and reviews the practice and

variations of the method.

ABSTRACT

วารสารบริหารธุรกิจ 60

Understanding the Event Study

INTRODUCTION

An event study is an empirical analysis that

is normally used to measure the effect of an event on

stock prices (returns). Although the majority of

previous literature investigates stock prices, several

studies examine stock trading volume, or return

volatility. The event study is of importance because it

can be used to evaluate the impact of company

policies on firm value. The empirically conducted

study is based on the following assumptions.

• Under the market efficiency hypothesis, the

impact of an event will be instantly reflected in stock

prices. Therefore, the market reaction to the event

can be measured by stock returns over the study

time period.

• The event is unforeseen . Abnormal

(excess) stock returns indicate the market reaction to

the unanticipated event.

• During the event window, there are no

confounding effects, meaning that the effect of other

events is isolated.

This paper discusses the purposes of an

event study and provides examples of previous event

studies. The discussion includes an explanation of

the applications and procedures in conducting such a

study. The last part of the paper describes the

limitations of the event study method.

PURPOSES AND EXAMPLES OF EVENTS An event study is commonly developed to

attempt to measure whether an unanticipated event

could have an effect on stock prices and the

direction and magnitude any perceived effects might

have on those stock prices. The event study method

is applied in different research areas, such as

accounting and finance, management, marketing,

information technology, law and economics. Early

literature on event studies are include an investigation

of the impact of annual earnings announcement on

stock prices (Ball and Brown, 1968) and a study of

the announcement of stock splits on stock returns

(Fama et al., 1969).

Ball and Brown (1968) concluded that annual

accounting income data contains information that is

related to stock prices. They found that income

forecast errors, which are measured by the difference

between announced and expected accounting

earnings, have a positive impact on the abnormal

per formance index around the annual report

announcement date.

Fama et al (1969) also note that stock prices

appear to adjust to new information. Stock splits

generally occur following periods when stock prices

significantly increase relative to the market. They

found that, after a split announcement, stock prices

seem to quickly reflect all available information and

do not generate any abnormal returns. The results

demonstrate the efficiency of the capital market.

In th is paper , examples of events are

provided, including firm-specific events and economy-

wide events. The firm-specific events mainly involve a

change in or a new implementation of company

policy. Examples of firm-specific events used in

previous event studies are as follows.

• The announcement and completion of a

takeover bid/divestiture (Agrawal and Mandelker,

1990; Lys and Vincent, 1995; Gregory, 1997; Bruner,

1999)

• Initial public offering (Ritter, 1991; Loughran

and Ritter, 1995; Espenlaub et al., 2001)

• Seasoned equity offering (Loughran and

Ritter, 1995; Carlson et al., 2006)

• Earning management practices before IPO

and SEO (Teoh et al., 1998a; Teoh et al., 1998b)

คณะพาณิชยศาสตร์และการบัญช ีมหาวิทยาลัยธรรมศาสตร ์

ปีที่ 34 ฉบับที่ 130 เมษายน-มิถุนายน 2554

61

• Obtaining new bank loans or loan renewal

(Lummer and McConnell, 1989)

• Selecting an auditor and its reputation

(Weber et al., 2008)

• An appointment of a new CEO with

financial expertise (Defond et al., 2005)

• Top executive changes (Bonnier and

Bruner, 1989; Dahya et al., 1998)

• Sudden CEO vacancy (Lambertides, 2009)

• Compensation plan policy (DeFusco et al.,

1990; Yermack, 1997; Yeo et al., 1999)

• An internet name change (Mase, 2009)

• An advertising campaign (Kim and Morris,

2003; Choong et al., 2007)

• Football results of listed European clubs

(Benkraiem et al., 2009)

• IT investments (Roztocki and Weistroffer,

2009)

• Enterprise resource planning system (ERP)

implementation (Benco and Prather, 2008)

Economy-wide events are often used in large

sample event studies, which examine the effect of a

particular event on relevant firms. The following

studies are examples of economy-wide events.

• A new item of legislature (Schipper and

Thompson, 1983; Schumann, 1988)

• Sarbanes Oxley Act (Small et al., 2007)

• A financial crisis (Baek et al., 2004)

• The “9/11” terrorist attack in New York

(Homan, 2006)

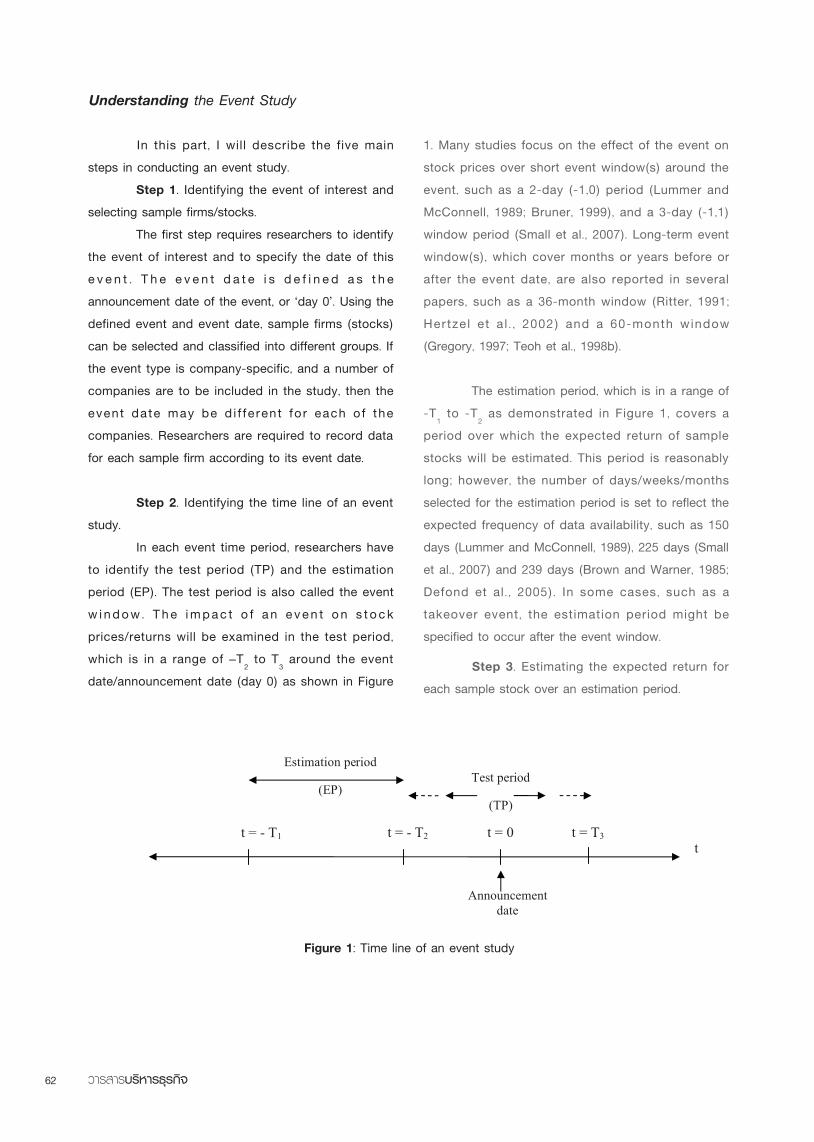

RESEARCH DES IGN AND PROCEDURES OF AN EVENT STUDY

Event studies can be designed in different

ways to reflect specific purposes and research

questions. The event study can be used in both

clinical studies and large sample studies. A clinical

study investigates the effect of an event on stock

prices of a single company, such as an analysis of

the market reaction to a takeover announcement;

where the study focuses on the acquiring firm and/or

on the target firm (Lys and Vincent, 1995; Bruner,

1999). Large sample studies examine the impact of

an event on prices of different sample stocks.

Examples of this type of event study include the

effect of company policy implementation in a large

sample of listed firms, such as a stock split, a top

management compensation policy, or a director

appointment policy (Fama et al., 1969; Yermack,

1997; Defond et al., 2005).

In addition to the effect of an event on stock

returns, researchers have examined the impact of an

event on stock volatility (DeFusco et al., 1990; Engle

and Ng, 1993; Jayaraman and Shastri, 1993), on

stock trading volume (Benkraiem et al . , 2009;

Karafiath, 2009), or on accounting performance

(Barber and Lyon, 1996). Furthermore, not only

company stocks, but also other types of securities

can be considered in the event study. Prior research

using event studies has analyzed effects on company

bonds , whe r e abno rma l bond r e t u r n s c an

d emon s t r a t e t h e ma r k e t imp a c t o f e v e n t

announcements (Gugler et al., 2004; Asquith and

Wizman, 1990; DeFusco et al., 1990; Steiner and

Heinke, 2001).

When designing an event study, the length of

the event periods and the expected availability of

data will be considered in determining the return

frequency. Choices of return frequency can be daily,

weekly, monthly, or annually. Daily and monthly

returns are commonly found in previous literature.

Daily data is often used for short-term event studies

(Lummer and McConnell, 1989; Small et al., 2007),

whilst monthly data is normally chosen for long-term

studies (Ritter, 1991; Teoh et al., 1998b).

คณะพาณิชยศาสตร์และการบัญช ีมหาวิทยาลัยธรรมศาสตร ์

ปีที่ 34 ฉบับที่ 130 เมษายน-มิถุนายน 2554

63

The expected return, , is used as the

benchmark return in the normal situation to compare

with the actual return during the event window(s).

The benchmark return represents the return that is

not related to the event of interest. There are choices

of model to estimate expected returns.

3.1) Mean-adjusted return

The mean return is the average return over

the estimation period. Each stock can use the

average return during the estimation period as its

own expected return (Brown and Warner, 1985;

Lambertides, 2009).

3.2) Market-adjusted return

The expected return is the market return

at the same period of time, assuming that all

stocks, on average, generate the same rate of return

(Ritter, 1991; Bruner, 1999; Teoh et al., 1998b; Weber

et al., 2008). Using the market-adjusted return method

does not require an estimation period.

3.3) Market-model-adjusted return

The expected return is computed based on a

single factor market model. The parameters of the

market model, i.e. and , are estimated using

Ordinary Least Square (OLS) regression over the

estimation period. This method is used to control the

relation between stock returns and market returns, or

allows for the variation in risk associated with a

selected stock. The market-model-adjusted return is

commonly found as an expected return in previous

event studies (Bonnier and Bruner, 1989; Lummer and

McConnell, 1989; Schipper and Thompson, 1983;

Homan, 2006; Small et al., 2007).

3.4) CAPM-adjusted return

Using the Capital Asset Pricing Model

(CAPM), the expected return is the outcome of the

risk-free rate return plus market risk premium

(Espenlaub et al., 2001). of the model measures

the risk of stock (i), assuming that an investor

requires higher return to compensate for higher risk.

3.5) Reference portfolios

The expected return in this method is the

return of the reference portfol io. The portfol io

comprises stocks based on the criteria of size, the

book-to-market ratio, or both size and the book-to-

market ratio. To calculate this benchmark expected

return , the est imat ion per iod is not required.

Researchers generally rank all firms into different

groups by a particular characteristic; for example, into

ten size-different groups. Then an average return for

al l stocks in each group is calculated as the

expected return of a reference portfolio. Examples of

event studies using this method are Ritter (1991) and

Barber & Lyon (1997)1.

3.6) Matched firm approach

Similar to the reference portfolio method, the

expected return is assumed to be the same as the

return of matched stocks during the test period. The

matching process will be done on the basis of

relevant risk characteristics and the matched stocks

not being exposed to the event of interest. The

common matching characteristics are size (i.e. equity

market value), the book-to-market ratio, and the

combinat ion of both. For example, using size

characteristics, the abnormal return of an event stock

is the difference between its actual return and the

portfolio return of matched stocks in the same range

of equity market value (Ritter, 1991; Loughran and

1Reference portfolio: by size (Ritter, 1991; Barber & Lyon, 1997), by book-to-market ratio (Barber & Lyon, 1997), by size and book-

to-market ratio (Barber & Lyon, 1997).

วารสารบริหารธุรกิจ 64

Understanding the Event Study

Ritter, 1995; Barber and Lyon, 1997). Several authors

have reported the use of combined size and book-to-

market matching (Barber and Lyon, 1997; Teoh et al.,

1998a; Hertzel et al., 2002; Carlson et al., 2006).

3.7) Fama-French three factor model

This method is an extension of the CAPM-

adjusted return, combining more risk factors, i.e. a

market excess return factor, a factor for

size (small minus big, SMB) and a factor for book-to-

market-equity ratio (high minus low, HML) (Fama and

French, 1993). SMB is the difference between

average returns of small stock portfolios and those of

big stock portfolios. HML is the difference in average

returns between high and low book-to-market stock

portfolios. This method uses monthly returns over a

long period of time. It can be implemented as in the

CAPM and is widely used in previous work (Barber

and Lyon, 1997; Loughran and Ritter, 1995; Teoh et

al., 1998b; Hertzel et al., 2002; Dutta and Jog, 2009).

Step 4. Computing abnormal (or excess)

returns.

An abnormal return for an individual stock is

the difference between the actual return on time (t) in

the event window and the expected return of an

individual stock.

To calculate the cumulative abnormal return

(CAR) for an individual stock, the abnormal return of

each stock is aggregated over the event window

(-T2 to T3).

The buy-and-hold abnormal return (BHAR)

for an individual stock is the difference between the

buy-and-hold return of a sample firm and that of the

benchmark expected return, assuming that an

investor buys a stock and holds it until the end of the

event period (Ritter, 1991;Teoh et al., 1998a; Hertzel

et al., 2002).

The average abnormal return for all sample

stocks on time (t) can be calculated as follows.

Step 5. Testing the significance of abnormal

(excess) returns.

To test the significance of abnormal returns,

most event studies use a parametric test of t-

statistics (e.g. Brown and Warner, 1985; Barber and

Lyon, 1997); however, non-parametric tests, such as a

sign test, or a rank test (e.g. Benco and Prather,

2008; Benkraiem et al., 2009), can be applied to

confirm the results2.

For an individual firm (i), whether or not the

abnormal return is different from zero can be tested

by t-statistics as follows.

Across firms, the following formulae give

parametr ic test stat is t ics , which are used to

investigate if the average cumulative, or buy-and-hold

abnormal returns are equal to zero.

2Parametric tests have some specific assumptions, such as normal distribution of returns; while non-parametric tests allow for any

distribution of data.

คณะพาณิชยศาสตร์และการบัญช ีมหาวิทยาลัยธรรมศาสตร ์

ปีที่ 34 ฉบับที่ 130 เมษายน-มิถุนายน 2554

65

LIMITATIONS OF THE EVENT STUDY

The event study is a simple research method

which allows uncomplicated interpretation of results.

The method has been commonly used by researchers

to examine how events can affect both gains and

losses in company value as perceived by the market.

I t is a lso used to measure the market-based

performance in terms of abnormal stock returns in

s i tuat ions where researchers ant ic ipate that

inaccuracies in financial statements may give an

inaccurate measure of company performance.

Although the event study methodology is useful in

several ways, there are some major limitations.

First of all, the assumptions used in event

s t ud y me t hodo l og y a r e no t v a l i d i n s ome

circumstances. Due to market inefficiency observed

stock prices may not fully and immediately reflect all

information. Furthermore, events might be anticipated

in some situations, whilst unforeseen coexisting

events could also have an effect on the sample

stocks, which could lead to biased stock returns.

Therefore, abnormal returns are not entirely the result

of market reaction to the specific event of interest.

Secondly, variations in estimation and test

periods are commonly found in event studies. Precise

estimation periods are not easy to determine. The

length of the estimation period is subject to a

tradeoff between improved estimation accuracy and

potential parameter shifts. Moreover, the estimation

period is difficult to control for other confounding

effects if researchers select long test periods, or long

event windows.

Thirdly, the choice of model to estimate

expected returns will have a bearing on the results in

the magnitude and the significance of abnormal

returns. For example, using the average return

method is simple, but it produces upwardly, or

downwardly biased abnormal returns in bull and bear

markets, respectively. Ritter (1991) also documents

that using different market indices to calculate

market-adjusted returns can show differences in long-

term performance results. More importantly, if the

expected return is incorrectly estimated, other factors

that are not properly controlled could lead to biased

information in the event study results.

Fourthly, not all stocks trade every day. Thin

trading over the estimation and test period is a

problem in event studies. For example, stock and

market returns might not be available on the selected

days throughout the estimation period if researchers

apply the market model or Fama-French three factor

model.

Fifthly, calendar time clustering of events is a

problem of cross-sectional dependence if test

per iods, or event dates of sample stocks are

clustered in the same calendar time period (Brown

and Warner, 1980). When the test periods of those

stocks overlap in calendar time, the problem of

cross-correlation in abnormal returns could exist.

However, in traditional large sample studies, the event

of interest is assumed to be isolated from other

ef fects . Calendar t ime is not expected to be

problematic because the effects of other events are

supposed to be cancelled out across the large

sample of firms.

วารสารบริหารธุรกิจ 66

Understanding the Event Study

Bibliography

AGRAWAL, A. & MANDELKER, G.

N . ( 1 9 9 0 ) L a r g e

Shareholders and the

Monitoring of Managers:

The Case of Antitakeover

Charter Amendments.

Journal of Financial &

Quantitative Analysis, 25,

143-161.

ASQUITH, P. & WIZMAN, T. A.

( 1 9 9 0 ) E v e n t r i s k ,

c o v e n a n t s , a n d

bondholder returns in

l e v e r a g e d b u y o u t s .

Jou rna l o f F i n anc i a l

Economics, 27, 195-213.

BAEK, J. S., KANG, J. K. & SUH

P A R K , K . ( 2 0 0 4 )

Corporate governance

and firm value: evidence

from the Korean financial

crisis. Journal of Financial

Economics, 71, 265-313.

BALL, R. & BROWN, P. (1968) An

Empirical Evaluation of

A c c o u n t i n g I n c ome

Numbers . Jou rna l o f

Accounting Research, 6,

159-178

BARBER, B. M. & LYON, J. D.

( 1 9 9 6 ) D e t e c t i n g

a b no rma l o p e r a t i n g

p e r f o r m a n c e : T h e

emp i r i ca l power and

spec i f i ca t i on o f t es t

s ta t i s t i cs . Journa l o f

Financial Economics, 41,

359-399.

BARBER, B. M. & LYON, J. D.

(1997) Detecting long-run

abnormal stock returns:

The empirical power and

spec i f i ca t i on o f t es t

s ta t i s t i cs . Journa l o f

Financial Economics, 43,

341-372.

BENCO, D. & PRATHER, L. (2008)

Ma r k e t R e a c t i o n t o

Announcements to Invest

i n E R P S y s t e m s .

Qua r t e r l y Jou rna l o f

Finance and Accounting,

47, 145-169.

BENKRAIEM, R., LOUHICHI, W. &

MARQUES, P . (2009)

M a r k e t r e a c t i o n t o

s p o r t i n g r e s u l t s .

Management Decision ,

47, 100-109.

BONNIER, K.-A. & BRUNER, R. F.

(1989) An analys is of

stock price reaction to

management change in

distressed firms. Journal

o f A c c o u n t i n g a n d

Economics, 11, 95-106.

BROWN, S. J. & WARNER, J. B.

(1980) Measuring security

p r i c e p e r f o rm a n c e .

Jou rna l o f F i n anc i a l

Economics, 8, 205-258.

BROWN, S. J. & WARNER, J. B.

(1985) Using daily stock

re tu rns : The Case o f

Event Studies. Journal of

Financial Economics, 14,

3-31.

BRUNER, R. F. (1999) An analysis

of value destruction and

recovery in the alliance

and proposed merger of

V o l v o a n d R e n a u l t .

Jou rna l o f F i n anc i a l

Economics, 51, 125-166.

CARLSON, M. , F ISHER, A . &

GIAMMARINO, R. O. N.

( 2 0 0 6 ) C o r p o r a t e

Investment and Asset

P r i c e D y n a m i c s :

Imp l ica t ions fo r SEO

Event Studies and Long-

Run Performance. Journal

of F inance , 61 , 1009-

1034.

CHOONG, P. , F ILBECK, G. &

TOMPKINS, D. (2007)

Advertising Strategy and

Returns on Advertising: A

Market Value Approach.

The Business Review ,

Cambridge, 8, 17-23.

DAHYA , J . , LON IE , A . A . &

POWER, D. M. (1998)

Ownersh ip St ructure ,

คณะพาณิชยศาสตร์และการบัญช ีมหาวิทยาลัยธรรมศาสตร ์

ปีที่ 34 ฉบับที่ 130 เมษายน-มิถุนายน 2554

67

Firm Performance and

Top Executive Change:

An Analysis of UK Firms.

Jou r n a l o f Bus i n e s s

Finance & Accounting ,

25, 1089-1118.

DEFOND, M. L., HANN, R. N. &

HU, X. (2005) Does the

Market Value Financial

E x p e r t i s e o n A u d i t

Committees of Boards of

Di rectors? Journal of

Accounting Research, 43,

153-193.

DEFUSCO, R. A., JOHNSON, R. R.

& ZORN, T. S. (1990) The

Effect of Executive Stock

O p t i o n P l a n s o n

S t o c k h o l d e r s a n d

Bondholders. Journal of

Finance, 45, 617-627.

DUTTA, S. & JOG, V. (2009) The

long-term performance of

acquir ing f i rms: A re-

e x a m i n a t i o n o f a n

anoma l y . J ou r n a l o f

Banking & Finance , 33,

1400-1412.

ENGLE, R. F. & NG, V. K. (1993)

Measuring and Testing

the Impact of News on

Vo la t i l i t y . Jou rna l o f

Finance, 48, 1749-1778.

ESPENLAUB, S., GOERGEN, M. &

KHURSHED, A. (2001)

IPO Lock-in Agreements

in the UK. Journa l of

Bu s i n e s s F i n a n c e &

Accounting , 28, 1235-

1278.

FAMA, E. F., FISHER, L., JENSEN,

M. C. & ROLL, R. (1969)

The Adjustment of Stock

P r i c e s t o N e w

Information. International

Economic Review, 10, 1-

21.

FAMA, E. F. & FRENCH, K. R.

( 1993 ) Common r i s k

factors in the returns on

s t o c k s a n d b o n d s .

Jou rna l o f F i n anc i a l

Economics, 33, 3-56.

G R E G O R Y , A . ( 1 9 9 7 ) A n

Examination of the Long

Run Performance of UK

Acquiring Firms. Journal

of Business Finance &

Accounting, 24, 971-1002.

GUGLER, K., MUELLER, D. C. &

YURTOGLU, B. B. (2004)

Marginal q , Tobin’s q,

C a s h F l o w , a n d

Investment . Southern

Economic Journal , 70,

512-531.

HERTZEL , M. , LEMMON, M. ,

LINCK, J. S. & REES, L.

( 2 0 0 2 ) L o n g - R u n

Performance following

Private Placements of

E q u i t y . J o u r n a l o f

Finance, 57, 2595-2617.

HOMAN, A. C. (2006) The Impact

of 9/11 on Financial Risk,

Volatility and Returns of

Marine Firms. Maritime

Economics & Logistics, 8,

387-401.

JAYARAMAN, N. & SHASTRI, K.

(1993) The effects of the

a n n o u n c e m e n t s o f

dividend increases on

stock return volatility: the

e v i d e n c e f r o m t h e

options market. Journal

of Business Finance &

Accounting, 20, 673-685.

KARAFIATH, I. (2009) Detecting

cumu la t i ve abnorma l

volume: a comparison of

event study methods.

App l i e d E c o n om i c s

Letters, 16, 797-802.

KIM, J. & MORRIS, J. D. (2003)

The effect of advertising

on the market value of

firms: Empirical evidence

from the Super Bowl ads.

Journa l o f Target ing ,

M e a s u r e m e n t a n d

Analysis for Marketing ,

12, 53-65.

LAMBERTIDES, N. (2009) Sudden

CEO vacancy and the

l o n g - r u n e c o n om i c

c o n s e q u e n c e s .

Managerial Finance, 35,

วารสารบริหารธุรกิจ 68

Understanding the Event Study

645-661.

LOUGHRAN, T. & RITTER, J. R.

(1995) The New Issues

P u z z l e . J o u r n a l o f

Finance, 50, 23-51.

LUMMER, S. L. & MCCONNELL,

J . J . ( 1 9 89 ) F u r t h e r

Evidence on the Bank

Lending Process and the

Capital-Market Response

t o B a n k L o a n

Agreements. Journal of

Financial Economics, 25,

99-122.

LYS, T. & VINCENT, L. (1995) An

a n a l y s i s o f v a l u e

dest ruct ion in AT&T’s

a cqu i s i t i o n o f NCR .

Jou rna l o f F i n anc i a l

Economics, 39, 353-378.

MASE, B. (2009) The impact of

n a m e c h a n g e s o n

c o m p a n y v a l u e .

Managerial Finance, 35,

316-324.

RITTER, J. R. (1991) The Long-

Run Pe r f o rmance o f

Initial Public Offerings.

J o u r n a l o f F i n a n c e ,

46, 3-27.

ROZTOCKI, N. & WEISTROFFER,

H. (2009) Informat ion

Technology Investments:

Does Ac t i v i t y Based

Cos t ing mat te r? The

Journa l o f Compute r

Information Systems, 50,

31-41.

SCHIPPER, K. & THOMPSON, R.

E. X. (1983) The Impact

o f M e r g e r - R e l a t e d

R e g u l a t i o n s o n t h e

Shareholders of Acquiring

F i r m s . J o u r n a l o f

Accounting Research, 21,

184-221.

SCHUMANN, L . (1988) State

Regulation of Takeovers

and Shareholder Wealth:

The Case of New York’s

1985 Takeover Statutes.

The Rand Journa l o f

Economics, 19, 557-567.

SMALL, K., IONICI, O. & ZHU, H.

(2007) Size Does Matter:

An Examination of the

Econom ic Impac t o f

Sarbanes-Oxley. Review

of Business, 27, 47-55.

STEINER, M. & HEINKE, V. G.

( 2 0 0 1 ) E v e n t s t u d y

concerning international

bond pr ice ef fects of

cred i t ra t ing act ions .

International Journal of

Finance & Economics, 6,

139-157.

TEOH, S. H., WELCH, I. & WONG,

T. J. (1998a) Earnings

management and the

l o n g - r u n m a r k e t

performance of in i t ia l

public offerings. Journal

of F inance , 53 , 1935-

1974.

TEOH, S. H., WELCH, I. & WONG,

T. J. (1998b) Earnings

management and the

underper fo rmance o f

s e a s o n e d e q u i t y

o f f e r i ngs . Jou rna l o f

Financial Economics, 50,

63-99.

WEBER, J., WILLENBORG, M. &

ZHANG, J. (2008) Does

A u d i t o r R e p u t a t i o n

Mat te r? The Case o f

KPMG Ge rmany and

ComROAD AG. Journal

of Accounting Research,

46, 941-972.

YEO, G. H. H., CHEN, S., HO, K.

W . & LEE , C . ( 1999 )

E f f ec t s o f execu t i v e

share option plans on

shareholder wealth and

firm performance: The

Singapore evidence. The

Financial Review, 34, 1-

20.

YERMACK , D . ( 1997 ) Good

T i m i n g : C EO S t o c k

Op t i o n Awa r d s a n d

C o m p a n y N e w s

Announcements. Journal

of Finance, 52, 449-476.