Embed Size (px)

Citation preview

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 1/72

Introduction

The etymology of the word risk can be traced to the Latin word rescue

meaning risk at sea or that which cuts. Risk is associated with uncertainty

and reflected by way of charge on the fundamental/ basic i.e. in the case of

business it is the capital, which is the cushion that protects the liability

holders of an institution from any unexpected loss. In the process of

financial intermediation the gap of which becomes thinner and thinner

banks are exposed to severe competition and hence are competition to

encounter various types of financial and non-financial risks viz., credit,

interest rate, foreign exchange, liquidity, equity price, commodity price,

legal reputation, brand equity risks etc. These risks are interdependent and

events affecting and area of risk can have ramifications and penetrations

for a range of other categories of risks. Foremost thing is to understand the

risks run by the bank and to ensure that the risks are properly confronted,

effectively controlled and rightly managed.

A risk is any uncertainty about future event that threatens yours

organization’s ability to accomplish its mission. Business is a trade off

between risk and return. There can be no risk free or zero risk oriented

business. This is due to the fact that the concept of a project implies

effecting current investment, for a future activity and a future gain after

the project construction period can be dither ways. When such changes are

adverse, when there is time over run or cost escalation the investment in

the project comes to grief even before the project is completed. There con

be also be several unexpected developments both internal and from the

external environment that can render your project calculation go away

1

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 2/72

There van be minimum risk in a captive controlled economy, where high

tariff walls protect industry and banks by directed credit and directed

interest rates, and directed investments, but along with such minimum risk,

there would also be minimum growth of the economy. In India after total,

regulation for several decades, the economy witnesses around 3% average

growth. The Indian economy has now been freed of state

Management risk: When you invest in a mutual fund, you depend on the

fund's manager to make the right decisions regarding the fund's portfolio.

If the manager does not perform as well as you had hoped, you might not

make as much money on your investment as you expected.

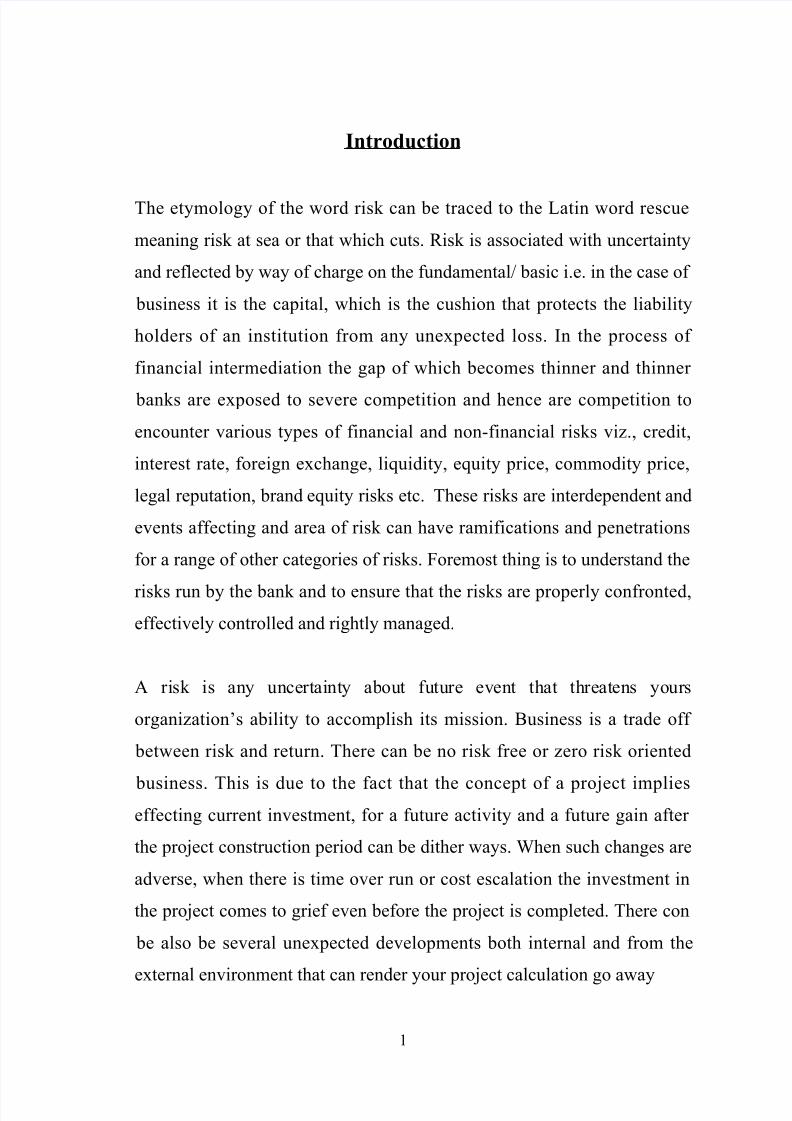

Risk:

2

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 3/72

Risk/Return Trade-Off: The most important relationship to understand is

the risk-return trade-off. Higher the risk greater the returns/loss and lower

the risk lesser the returns/loss.

Market Risk: Sometimes prices and yields of all securities rise and fall.

Broad outside influences affecting the market in general lead to this. This

is true, may it be big corporations or smaller mid-sized companies. This is

known as Market Risk. A Systematic Investment Plan (“SIP”) that works

on the concept of Rupee Cost Averaging (“RCA”) might help mitigate this

risk.

Credit Risk:

The debt servicing ability (may it be interest payments or repayment of

principal) of a company through its cash flows determines the Credit Risk

faced by you. This credit risk is measured by independent rating agencies

like CRISIL who rate companies and their paper. A ‘AAA’ rating is

considered the safest whereas a ‘D’ rating is considered poor credit

quality. A well-diversified portfolio might help mitigate this risk.

Interest risk:

In a free market economy interest rates are difficult if not impossible to

predict. Changes in interest rates affect the prices of bonds as well as

equities. If interest rates raise the prices of bonds fall and vice versa.

Equity might be negatively affected as well in a rising interest rate

environment. A well-diversified portfolio might help mitigate this risk.

3

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 4/72

Determinations of objectives:

It is very important for an organization to identify the objectives of the risk

management function. This includes the expectations that the organization

has from the risk manger. The efficiency of the risk management may be

seriously hampered if its objectives are not clearly specified. The clear

declination of objective helps in identification of the risk management

process as holistic approach rather than as isolated individual problems to

be dealt with. In order to ascertain the risk management objective of the

organization, it is very important to link the priorities, goals and on

objectives of risk management with that of the organization from various

exposures.

Post loss objectives

1. Survival of the organization

2. Perpetuity of the organizations operations

3. Steady flow of income’ earnings

4. Social obligation

Pre-loss objectives

1. Economy

2. Fulfillment of external obligations3. Reduction in anxiety

4. Social obligation

4

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 5/72

Identification of the objectives

Identification of the objectives of a risk management process

depends of the type of the organization. However, the guiding principle of

development of objectives for any organization remains the same; to save

the organization from the perceived risks.

Usually the organization develops a risk management policy, which

lays down the objectives of risk management. The top management of the

organization usually develops the policy for risk management. The

ultimate responsibility of the welfare of the organizations rests with the

top management because of which they lay down the important policy

decisions. However, the risk manager can provide valuable suggestions,

which will help the top management in arriving at well-developed policies.

SCOPE:

• My study about the risk management covers the following

Aspects

• Various types of risks in insurance sectors

• Need for risk management

• Managing various types of risk

5

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 6/72

METHODOLOGY AND DATA COLLECTION

PRIMARY SOURCE:

• I gathered information by interacting with employees at

Various levels in the insurance

SECONDARY SOURCE:

• I referred to risk management related books

• Material provided by ICICI prudential

6

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 7/72

ICICI PRUDENTIAL LIFE INSURANCE

ICICI prudential Life Insurance was established in the 2000 with a

commitment to expand and reshape the life insurance industry in India.

The company was amongst the first private sector insurance companies to

begin operations after receiving approval from Insurance Regulatory

Development Authority (IRDA)

Products

Insurance Solutions for Individuals

ICICI Prudential Life Insurance offers a range of innovative, customer-

centric products that meet the needs of customers at every life stage. Its

products can be enhanced with up to 4 riders, to create a customized

solution for each policyholder.

Savings & Wealth Creation Solutions

Cash Plus is a transparent, feature-packed savings plan that offers3 level

of protection as well as liquidity options.

Save'n'Protect is a traditional endowment savings plan that offers life

protection along with adequate returns.

Cashbook is an anticipated endowment policy ideal for meeting milestone

expenses like a child's marriage, expenses for a child's higher education or

purchase of an asset. It is available for terms of 15 and years.

Lifetime Super & Lifetime Plus are unit-linked plans that offer

customers the flexibility and control to customize the policy to meet the

changing needs at different life stages. Each offers 4 fund options -

Preserver, Protector, Balancer and Maxi miser.

7

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 8/72

Lifeline Super is a single premium unit linked insurance Plan, which

combines life insurance cover with the opportunity to stay, invested in the

stock market.

Premier Life Gold is a limited premium-paying plan specially structured

for long-term wealth creation.

Invest Shield Life New is a unit linked plan that provides premium

guarantee on the invested premiums and ensures that the customer

receives only the benefits of fund appreciation without any of the risks of

depreciation.

Invest Shield Cashbook is a unit linked plan that provides premium

guarantee on the invested premiums along with flexible liquidity options.

Protection Solutions Lifeguard is a protection plan, which offers life

cover at low cost. It is available in 3 options - level term assurance, level

term assurance with return of premium & single premium.

Home Assure is a mortgage reducing term assurance plan designed

specifically to help customers cover their home loans in simple and cost-

effective manner.

Education insurance under the Smart Kid brand provides guaranteed

educational benefits to a child along with life insurance cover for the

parent who purchases the policy. Smart Kid plans are also available in

unit-linked form - both single premium and regular premium.

Retirement Solutions

Forever Life is a traditional retirement product that offers guaranteed

returns for the first 4 years and then declares bonuses annually.

8

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 9/72

Lifetime Super Pension is a regular premium unit linked pension plan

that helps one accumulate over the long term and offers an annuity option

(guaranteed income for life) at the time of retirement.

Life Link Super Pension is a single premium unit linked pension plan.

Immediate Annuity is a single premium annuity product that guarantees

income for life at the time of retirement. It offers the benefit of 5 payout

options.

Health Solutions

Health Assure and Health Assure Plus: Health Assure is a regular

premium plan which provides long term cover against 6 critical illnesses

by providing policyholder with financial assistance, irrespective of the

actual medical expenses. Health Assure Plus offers the added advantage of

an equivalent life insurance cover.

Cancer Care: is a regular premium plan that pays cash benefit on the

diagnosis as well as at different stages in the treatment of various cancer

conditions.

Diabetes Care: Diabetes Care is the first ever critical illness product

specially for individuals with Type 2 diabetes.

Group Insurance Solutions: ICICI Prudential also offers Group

Insurance Solutions for companies seeking to enhance benefits to their

employees.

Group Gratuity Plan: ICICI Pru's group gratuity plan helps employers

fund their statutory gratuity obligation in a scientific manner. The plan can

9

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 10/72

also be customized to structure schemes that can provide benefits beyond

the statutory obligations.

Group Superannuation Plan: ICICI Pru offers both defined contribution(DC) and defined benefit (DB) superannuation schemes to optimize

returns for the members of the trust and rationalize the cost. Members

have the option of choosing from various annuity options or opting for a

partial commutation of the annuity at the time of retirement.

Group Immediate Annuities: In addition to the annuities offered to

existing superannuation customers, we offer immediate annuities to

superannuation funds not managed by us.

Group Term Plan: ICICI Pru's flexible group term solution helps provide

affordable cover to members of a group. The cover could be uniform or

based on designation/rank or a multiple of salary. The benefit under the

policy is paid to the beneficiary nominated by the member on his/her

death.

Flexible Rider Options: ICICI Pru Life offers flexible riders, which can

be added to the basic policy at a marginal cost, depending on the specific

needs of the customer.

Accident & disability benefit: If death occurs as the result of an accident

during the term of the policy, the beneficiary receives an additional

amount equal to the rider sum assured under the policy. If the death occurs

while traveling in an authorized mass transport vehicle, the beneficiary

will be entitled to twice the sum assured as additional benefit.

Critical Illness Benefit: protects the insured against financial loss inthe

event of 9 specified critical illnesses. Benefits are payable to the insured

for medical expenses prior to death.

10

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 11/72

Income Benefit: This rider pays the 10% of the sum assured to the

nominee every year, till maturity, in the event of the death of the life

assured. It is available on SmartKid and Cash Plus.

Waiver of Premium: In case of total and permanent disability due to the

future premiums continue to be paid by the company till the time of

maturity.

This rider is available with Lifetime Super, Lifetime Super Pension and

Cash Plus.

Awards

India's Most Customer Responsive Insurance Company

Avaya Global Connect - Economic Times

Customer Responsiveness Awards

Most Trusted Private Life Insurer

The Economic Times - A C Nielsen Survey of Most Trusted Brands2003,

2004 and 2005

Prudence Customer Centricity Award 2004 & 2005

Prudential Corporation Asia

Outlook Money Awards 2003 & 2004

Best Life Insurer 2003

Silver Effie for Effectiveness of the ‘Retire from Work not life’

advertising campaign

11

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 12/72

ABOUT THE COMPANY

ICICI Prudential Life Insurance Company is a joint venture between ICICI

Bank, a premier financial powerhouse, and Prudential plc, a leading

international financial services group headquartered in the United

Kingdom. ICICI Prudential was amongst the first private sector insurance

companies to begin operations in December 2000 after receiving approval

from Insurance Regulatory Development Authority (IRDA).

ICICI Prudential capital stands at Rs. 18.15 billion with ICICI Bank and

Prudential plc holding 74% and 26% stake respectively. For the 10 months

ended January 31, 2007, the company garnered Rs 3,240 core of weighted

retail + group new business premiums and wrote over 1.3 million policies.

The company has assets held to the tune of over Rs. 14,000 core.

ICICI Prudential is also the only private life insurer in India to receive a

National Insurer Financial Strength rating of AAA (Ind) from Fitch

ratings. The AAA (Ind) rating is the highest rating, and is a clear assurance

of ICICI Prudential's ability to meet its obligations to customers at the

time of maturity or claims.

For the past six years, ICICI Prudential has retained its position as the No.

1 private life insurer in the country, with a wide range of flexible products

that meet the needs of the Indian customer at every step in life. To know

more about the company, please visit www.iciciprulife.com.

12

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 13/72

Distribution

ICICI Prudential has one of the largest distribution networks amongst

private life insurers in India. As of January 31, 2007 the company has over

540 offices across the country and over 200,000 advisors.

The company has over 20 bancassurnace partners, having tie-ups with

ICICI Bank, Federal Bank, South Indian Bank, Bank of India, Lord

Krishna Bank, Idukki District Co-operative Bank, Jalgaon Peoples Co-

operative Bank, Shamrao Vithal Co-op Bank, Ernakulam Bank and 9

Bank of India sponsored Regional Rural Banks (RRBs). It has also tied up

with NGOs MFIs and corporates for the distribution of rural policies.

ICICI Bank (NYSE:IBN) is India's second largest bank and largest

private sector bank with assets of Rs. 2958.32 billion as on December 31,

2006. ICICI Bank provides a broad spectrum of financial services to

individuals and companies. This includes mortgages, car and personal

loans, credit and debit cards, corporate and agricultural finance. The Bank

services a growing customer base through a multi-channel access network

which includes over 695 branches and extension counters, 3051 ATMs,

call centers and Internet banking.

13

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 14/72

MANAGEMENT

The ICICI Prudential Life Insurance Company Limited Board comprises

reputed people from the finance industry both from India and abroad.

Mr. K.V. Kamath, Chairman

Mr.BarryStowe

Mrs.KalpanaMorparia

Mrs.ChandaKochhar

Mr.RNarayanan

Mr.KekiDadiseth

Ms.ShikhaSharma,ManagingDirector

Mr.N.S.Kannan,ExecutiveDirector

Mr. Bhargav Dasgupta, Executive Director

14

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 15/72

RISK SPECTRUM

Risk is better understood in terms of and in relations to uncertainty.

Whatever we do there is an element of risk or uncertainty. Whatever we

do there is an element of risk or uncertainty attached to the outcome.

Certainty and uncertainty are two extremes on a continuum, and risk exists

some where between the two. The following paragraphs would help you

understand these concepts.

Every action is followed by outcomes. Some action have single outcome,

while most action have a wide range of out come, consider the tossing of

coin. When we toss a fair coin there are two possible outcomes; it either

lands heads or tails. Similarly, six outcomes are possible when we throw a

dice. Profitability from a business activity is characterized by a range of

outcomes; from maximum loss to maximum profit

DEFINING RISK

Usually, the term ‘risk’ is used synonymously with insurance, which is not

correct. There is no universally accepted definition of risk.

In one sense, risk is defined as “a variation in the possible outcome”. In

another sense, risk is defined as “The degree of uncertainty associated

with apostle loss”.

The degree of risk is estimated based on the certainty level with which the

outcome of an activity can be forecast. The greater the accuracy withwhich the outcome can be predicated the lower is the risk.

Possibility of loss or injury: Peril.

Someone or something that creates or suggests a hazard.

The chance of loss or the perils to the subject matter of an insurance

contract; also the degree of probability of such loss.

A person or a thing that is a specified hazard to an insurer.

15

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 16/72

An insurance hazard from a specified cause or source.

Apart from the words ‘uncertainty’,’ certainty’, ‘risk’ other words such as

‘peril’ and ‘hazard’ are most frequently used in the field of risk and

insurance management quite often they are used interchangeably with risk.

It is better to understand the distinction between them before we start

using these words.

A peril is a cause of risk. Fire, earthquake, flood, criminal activities, etc.,

are examples of perils. Thus perils are causes of losses. Organizations and

individuals buy insurance policies and use other methods to protect their

assets from perils.

THE EFFECT OF RISK

As mentioned earlier risk results in gains or losses. If we invest in an

equality share we may gain or lose when we sell it at a later date. If a fire

accident occurs in a warehouse it will result in losses only. We are very

much concerned with negative impact of risk when we attempt to manage

it. ‘Loss’ is a state wherein someone is deprived of something he/she had.

It may refer to loss of money, memory, stock, or reputation. Loss as used

in the insurance, has limited meaning. It is defined as an undesired

unplanned reduction in economic value resulting from chance.

Those losses, which do not result from chance, are not covered as loss ininsurance. For instance, depreciation, expenditure, age, time, friction, etc,

are not insurable, as they do not occur from chance events. Some losses

are immediate in nature and result from insured peril. These are called

‘Direct losses’. If a fire reduces the building to ash, the building is a direct

loss. A direct loss leads to consequential or indirect losses, which are in

the from of increased expenses on account of construction of new

16

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 17/72

building. Other establishment expenses, etc. Such losses are termed as

‘indirect losses’.

CERTAINTY, RISK AND UCERTAINTY

The term ’certainty’ refers to the state where there is a little or no doubt

about the outcome of an event or action. Webster’s New Collegiate

dictionary defines certainty as ‘a state of being free from doubt’. Opposite

of certainty is uncertainty. Uncertainty results from the doubt or inability

to predict the future outcome of current actions. Thus, uncertainty crops up

when there is a doubt in the achievement of target or the desired

objectives. The potential variation in the outcome is called risk. In is a

certain other words, it is not possible to determine the outcome of an

action with certainty when there degree of risk. Let us look at the concept

of risk with the help of an example. Table 1.1 shows the outcome of two

bets. In one of them, the amount at risk is Re .1 and in the other, it is

Rs.100.

CLASSIFICATION OF RISK

Different risks require different methods and approaches to deal with

them.

Board Classification of pure Risks

Types of losses from pure Risks

Direct losses

Indirect losses

17

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 18/72

Direct losses

Damage to assets

Injury /illness to employees

Liability claims and defense cost

Indirect losses

Loss of normal profit

Higher cost of funds

Foregone InvestmentBankruptcy costs

Classification of Pure Risks

There are four broad categories of pure risk. They are

Property risk

Personal risk

Liability risk

Loss of income risk.

PROPERTY RISK

In this case there is a fear of loss of property because of some unforeseenevents. Property includes both movable and immovable assets.

18

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 19/72

PERSONAL RISK

It refers to the possibility of loss of income or assets as a result of the loss

of the ability; to earn income. This may result from untimely death of the

earning member, dependent old age, prolonged illness, disability or

unemployment.

LIABILITY RISK

Liability risk arises when there is a possibility of an unintentional damage

to other person or to his property because of negligence. However, the

chances of intentional harm are not ruled out in certain circumstances.

LOSS OF INCOME RISK

Loss of income risk is an indirect loss from a given risk. As discussed

under property risks, whenever there is a direct loss, it is followed by some

consequences that result in indirect loss.

Dynamic vs. Static Risk Static risk remains constant over an observed period of time. Risks remain

static because the environments in which they exist are static.

Dynamic risks arise from the changes that occur in an environment, which

may be economic, social, technological, and political. Change in the

environment creates risk and uncertainty about the future.

Fundamental vs. Particular Risks

Those risks, which affect a larger group, such as a society or an industry,

or a particular segment of an industry, are termed as fundamental risks.

For example, natural calamities such as flood, earthquake, drought,

epidemics, etc. affect the whole mass in the same manner irrespective of

caste, creed or religion or geographical boundaries..

19

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 20/72

ATTITUDE TOWARDS RISK

Attitude towards risk reflects the perception or a mental position with

regard to a fact or state, or it is a feeling or emotion towards a fact or a

situation. Individuals can be grouped into three different categories as per

their attitude towards risk. They are:

Those who are neutral/indifferent to risk,

Those who are willing to take up risks, and

Those who avoid risk.

HUMAN RESPONSE TO RISK

It is not possible for an individual or an organization to avoid risk. Every

organization is exposed to risks of various degrees in the course of

business. It is the duty of the risk manager of a company to analyze the

characteristics of risks to which the organization is exposed and develop

suitable strategies to minimize the same.

Mankind has developed various tools and techniques to safeguard itself

against the perceived risks and hazards since the dawn of civilization.

Though the procedures or methods adopted for the purpose might have

undergone a sea change, the objective remains the same. As the saying

goes, “Man proposes and God disposes”, the uncertainty of outcome of

any future event adds to the severity of risk in any situation. There is

always a certain degree of uncertainty involved in achievement of any task

regardless of the precautionary measures taken up. This is because any

system draws its strength from two sources viz. external and internal. It is

very important that for the smooth functioning ;of the organization both

the external and internal environments must be understood well.

20

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 21/72

MANAGEMENT OF RISK

In risk management, the term “management” refers to the efforts of an

individual or an organization for achieving the desired objective. For

example, a businessman would like to plan the production level as per the

demand of the market. Designing of the product shall be in accordance

with the needs of the consumers. Pricing of the product will take into

consideration the cost of production and competitor’s prices. Moreover the

businessman would like to instill confidence in consumers by offering

after sales service.

RISK MANAGEMENT STRATEGIES

Risk is all pervasive and there is no escape. Hence, human beings must

always find different ways in dealing with risks. Several methods can be

used in everyday life to handle both pure risk and speculative risks. They

are.

Risk avoidance

Risk reduction

Risk retention

Risk combination

Risk sharing

Risk hedging

Risk avoidance

This is the strongest method of dealing with risks. Risk avoidance results

in the total elimination of exposure to loss due to a specific risk. It

21

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 22/72

involves abandoning some activity and so losing the benefits associated

with it.

There are two ways by which risk can be avoided. In the first case the

person will not assume any risk, therefore, he will not do any project that

exposes him to risks. This is known as proactive evidence. In the second

case a person will try to abandon the exposure to loss assumed earlier, by

discontinuing the activity or winding up the project. This is called

abandonment avoidance.

Proactive avoidance is resorted into many situations.

Risk reduction

Risk reduction aims at decreasing the number of losses by reducing the

occurrence of loss through various measures. Risk may be reduced in two

ways namely loss prevention and loss control.

LOSS PREVENTION

It is the most desirable means of dealing with risks. Since the possibility of

loss is eliminated., risk is also completely eliminated. Safety programmers

like medical care, security guards etc. and other measures like fire

sprinkler systems, burglar alarms, are all examples of loss prevention

activities.

These measures intervene at various stages of the activity such as the perceived activity itself, its environment and the link between the activity

and its environment. It tries to.

LOSS CONTROL

Organizations buy insurance in order to protect themselves against a

perceived loss from a risk. This may be because of occurrence of a

certain event. At the same time the insurance company would like to

22

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 23/72

avoid occurrence of such event. For this purpose it would provide

various methods or incentives to the company to undertake safety

measures.

Risk retention

It is the most common method of dealing with risks. Individuals face

a number of risks some of which cannot be avoided, reduced or

transferred. Individuals and organizations retain such risks. Risk may

be retained knowingly or unknowingly. Transfer it or reduce it. When

the risk is perceived and no attempts are made to transfer it or reduce

it. When the risk is not perceived at all then it is retained

unknowingly. In such cases, the person retains the financial

consequences of the possible loss without realizing of doing so.

Risk transfer

If risk or effect of risk is borne by a party other than the one who is

primarily exposed to risk, it may be called risk transfer. For example, a

building contractor who does not expertise in interior decoration may hire

an interior decorator for the building. Thus the contractor has passed on

the risk of loss of reputation in the market because of the poor interior

decoration. Similarly if there is an expectation of increase in price of wood

and furniture material the contractor passes the contract to some other agency. In this way the perception and chances of occurrence of risk is

being transferred from one agency to the other. Thus it is different from

abandonment wherein the risk is totally eliminated by abandoning the

activity.

23

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 24/72

Risk sharing

Risk sharing is an arrangement to share losses. Risk is usually shared in a

number of forms. One conmen example is the corporation, where

investments of large number of persons are pooled and each bears only a

portion of risk that the enterprise may incur. Insurance is an other advice

of risk sharing where members of the group share risk.

Hedging

Corporation in which individual investors and organization place money

have exposure to fluctuations in all kind of financial prices like foreign

exchange rate, interest rates, commodity prices and equity prices. The

effect of changes in these prices on the earnings is huge. Hence

organization resort to hedging which reduces the risk evolved in holding

an investment’s

LOSS REDUCTION

The aim of the loss reduction into reduces the degree of loss incurred by

the occurrence of a particular event. Though it does not reduce the chances

of occurrence of the event. It reduces the impact of the loss caused by the

event. For example, the seat belt in a car does not reduce the chances of

accident but it reduces the extent of injury inflicted upon the person. So is

the case with wearing helmets, using parachutes, fire sprinkler system in a building etc. all these safety devices add to the reduction of loss rather

than the reduction of probability of occurrence of the event itself.

The hazard

The environment

The interaction

The outcome

24

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 25/72

The consequences

RISK MANAGEMENT ESSENTIALS

After reading this chapter, you will be conversant with

•

The nature of risk management• The evolution of risk management

• Risk in personal life

• Corporate/organizational risks

• The process of risk management

NATURE OF RISK MANAGEMENT

Risk management aims to at controlling the risk exposure of a firm. It is

a rational approach towards controlling the our risk to which an

organization or an individual is exposed to, risk management function

can be grouped with other management functions such as financial

management, human resources management, etc.

An over view of different risks will help us to understand the nature of

risk management organizations and individuals are exposed to a wide

arrays of risk in their day-to-day operations, such:

Fire risk

Risk of theft

Loss of customers

25

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 26/72

Delay in delivery of raw materials

Break down of machinery

Accidents

Bad debts

CORPORATE RISK MANAGEMENT

Private corporate sector adopted active risk management for a variety of

reasons. The risk management program of a corporate entity aims at

logical way to solve problems it perceives. These problems if not managed

properly, can result in heavy losses. The loss may be in term of money,

material, opportunities or human life.

The risk manager of a company develops plans for protecting against any

unfavorable events. He undertakes the risk management process, whish

starts from information, supervising the initiation and progress plans of

loss control measures, which are critical for the organization. He also

undertakes negotiation for the terms and conditions to cover the losses and

takes adequate steps for amicably setting them against the insurers.

The risk management process of an organization involves answering

questions like:

What are the various activities or circumstances, which can cause

loss to the organization?

What are the alternatives available to the organization to protect it

self against these activities and circumstances?

The first question aims at identifying the different potential risky activities

and the second one price to protect the organization against the

consequences of these activities. The risk management process as

26

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 27/72

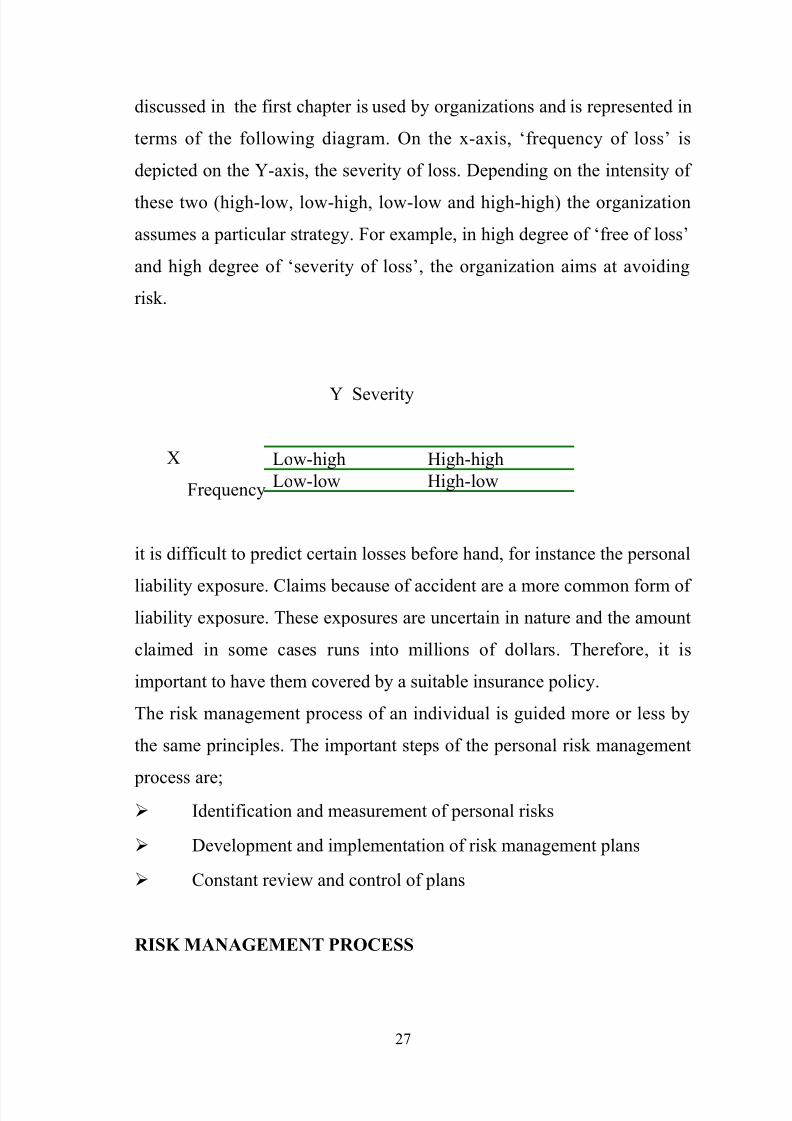

discussed in the first chapter is used by organizations and is represented in

terms of the following diagram. On the x-axis, ‘frequency of loss’ is

depicted on the Y-axis, the severity of loss. Depending on the intensity of

these two (high-low, low-high, low-low and high-high) the organization

assumes a particular strategy. For example, in high degree of ‘free of loss’

and high degree of ‘severity of loss’, the organization aims at avoiding

risk.

Y Severity

X

Frequency

it is difficult to predict certain losses before hand, for instance the personal

liability exposure. Claims because of accident are a more common form of

liability exposure. These exposures are uncertain in nature and the amount

claimed in some cases runs into millions of dollars. Therefore, it is

important to have them covered by a suitable insurance policy.

The risk management process of an individual is guided more or less by

the same principles. The important steps of the personal risk management

process are; Identification and measurement of personal risks

Development and implementation of risk management plans

Constant review and control of plans

RISK MANAGEMENT PROCESS

27

Low-high High-high

Low-low High-low

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 28/72

There are six distinct steps in risk management process, which are stated

below:

Evaluation of risk/exposures

Consideration and selection of risk management techniques

Implementation of decisions

Evaluation and review

Identification of risks

The second objective of the risk management process is to identify the

potential risks to which the organization can be exposed. Therefore, the

risk manager has to analyze various systems of the organization in detail

and identify the maximum possible risk exposure of the firm. The risk

manager usually undertakes a systematic study of identifying the potential

risks. A few other methods used in general are checklist, questionnaire,

flowchart, financial system analysis and close examination of company

operations. A brief description of the techniques applied by risk managers

to identify organizational risk is given below.

ORIENTATION

It is important for the risk managers to have clear understanding of the

various processes of the organization and orient their thinking towards

these processes. They should have in depth knowledge about the aims and

objectives of the organization as well as specific characteristic of the

organization, which distinguishes it from other. The past documents of the

organization will provide data about the history and scope of the

organization.

RISK ANALYSIS QUESTIONNAIRE

28

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 29/72

The risk analysis questionnaire is very much helpful in identifying the

possible risk of a particular department. A structured questionnaire is to be

prepared for a particular department keeping in mind its activities, past

performance and personnel. The questionnaire is to be distributed among

the employees. Thus, by analyzing the response from the questionnaire,

one can identify the different potential risks to which that particular

department risks to both insurable and uninsurable risks.

CHECKLIST OF EXPOSURES

In this case, a list of those activities is prepared which may prove risky to

the organization. Though the list is not exhaustive, it covers the major

potential risky activities. The list of such activities depends basically on

the business of the organization, its priorities, sizes, location, etc. the

checklist, along with other risk identification methods, helps in identifying

the potential risk to which the organization may be exposed to.

INSURANCE POLICY CHECKLIST

These checklists are usually available with the insurance companies. They

are also periodically published in the insurance related journals or

magazines. These checklists provide insight about the type of insurance

that particular insurance that a particular industry may need. Thus the job

of a risk manager is to identify the best-suited checklist emphasizes mostlyonly on the insurable risks and very little focus is given on non-insurable

pure risks.

FLOW CHARTS

Flow charts are usually system specific. These concentrate on specific

events, which may be potentially risky to the organization, are depicted in

a structural manner and each of these activities is analyzed. The most

29

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 30/72

important objective of the flow chart is that the risk manger becomes

though roughly acquainted with the technicalities of the company. This is

turn help in the determination of specific risk, which may be potential and

hazardous to the organization.

ANALYSIS OF FINANCIAL SYSTEM

The financial systems of a company include the balance sheet, profit and

loss account, cash flow statement, auditors, report, report of the

chairperson, etc. the balance sheet analysis helps in identifying, for

example, the overlooked assets or contingent liabilities. Similarly, the

profit and loss statement identifies those areas of business which the risk

manager to have thorough knowledge of the source and utilization of

funds of a company. Because, ultimately the effort of risk manager is

going to be reflected in these statements. The risk manager must also

gather as much information as he can from the notes to the accounts and

reports of the auditors and the chairperson.

INSPECTION

Inspection of premises and departments of the company gives practicalknowledge to the risk manager about particular process followed. It is very

helpful in getting clear understanding of the operations. The concerned

officials of the company provide immediate information about the

subsystem. Different activities and the potential risks involved are clearly

mentioned at the time of inspection. Thus the risk manager has little

chance of overlooking a particular risky activity.

30

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 31/72

COMBINATION APPROACH

This the most suitable and justified approach for identification of risk. In

the approach, all the above-mentioned methods are used in different

degrees of intensity for identification of the potential exposure. This is a

multipronged strategy where as every possible care is being taken to

identify the risks. It covers the gap left by the above methods. Thus, this

method eliminates (to the possible extent) the involuntary retention of risk

within the organization.

EVALUATION OF RISK

After identification of different risks from all the possible angles, it is

important to evaluate each of them. What would be the degree of loss

(both in quantitative and qualitative terms)? What is the probability of the

carryout with its occurrence of these activities? There may be a few risks,

which need immediate attention, and others, which demand to loss or even

bankruptcy to the organization, rank equally. And it is not possible to align

these into separate categories. If a firm becomes bankrupt because of

earthquake or legal liability or financial liability or heavy fire, the final

outcome of all these risks in the same and that is bankruptcy. Therefore,

instead of assigning some numerical or alphabetical value such as 1,2,3…

or A, B, C…one should attempt to group them into different categories.

These may be:

Critical categories

Important categories

Unimportant categories

CRITICAL CATEGORIES

31

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 32/72

These include those risks, which are left exposed, would result into heavy

loss to the company. These risks mostly lead to bankruptcy of the

company. For example, flood, earthquake, volcano eruption, legal battles,

loss in exports, etc.

IMPORTANT RISKS

This category includes those risks, which would become detrimental to the

survival f the company. Though the company may not become bankrupt, it

has to borrow funds from the market in order to business. For example,

popularly because of the fact that reduction of risk exposure is a more

economic approach theft or fire to go down, lockout, strike, bomb blast in

the premises, etc.

UNIMPORTANT RISK

These are the risks, which though disadvantageous to the company, can

meet the loss from its existing recourses. Foe example, injury to a worker,

delay in receipt of material, temporary power failure, etc.

In order to classify the various exposures , it id=s important to ascertain

the degree of financial loss and the extent to which the company can

absorb such loss. Moreover, it is also important to ascertain the extent to

which the company can meet the uninsured part of the loss without

resorting to borrowing from the market. It is difficult to standardize the

risks into the above-mentioned three categories for different types of organization. However, this is an important guideline, which will help the

organization in prioritizing their respective exposures.

RISK AVOIDANCE

In this case, the entity does not accept the risk even for a momentary

period. Thus, the entity retains from undertaking any risky activity. A

person who is afraid of meeting with an accident of while driving does not

drive. Similarly, a company, which is afraid of some chemical leakage,

32

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 33/72

may not undertake production of such goods. Thus the entity identifies to

avoids the potential various risks

RISK REDUCTION

In this case all activities undertaken by the entity to reduce the risk

exposure are included so that the organization can decrease the frequency,

severity and unpredictability of loss. This method gained than

underwriting an insurance policy. This results in giving more emphasis to

development of such procedures and approaches, which will decrease the

occurrence, or severity of the losses.

RISK RETENTION

When an organization fails to avoid or reduce or transfer the risk, then if=t

retains the risk with itself. It may be voluntary retention or involuntary

retention. Lastly, it maybe funded retention or unfounded retention. In

case of funded retention, the firm sets a side some property may be in a

liquid or semi liquid form for the retained risk. This depends on the cash

position of the firm. In case of unfunded risk, the risk is left exposedRISK TRANSFER

In this case, the risk is transferred through agreements, contracts, surety

bonds or insurance. Purchase of insurance is the most prevalent practice

amongst the businessmen. In addition to insurance there are other risk

transfer techniques, which will be discussed in chapter V.

33

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 34/72

MEASUREMENT OF RISK IDENTIFICATION AND

EVALUATION

After reading this chapter, you will be conversant with:

• Various sources of risk

• The exposure to risk

• How risk can be identified

• How to analyze hazards and losses

• How risk can be evaluated

• The uses of budgets and other quantitative methods

IDENTIFICATION OF RISK

Risk is a process of identifying risk and uncertainties systematically and

continuously. Identification of risk is a crucial step in the process of risk

management for both individuals as well as organizations. The process

leads to the development of information on various sources of risk,

hazards, risk, factors, perils and various exposures to loss, since some of

these words are new we will give their meaning in brief.

34

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 35/72

Sources of risk are the sources from which hazards, perils and risk factors

develop.

Hazard is a condition in the environment that creates or increases the

chance of loss or its severity.

Peril is a cause of loss.

Exposure to loss means properties, situations or persons facing the

possibility of loss.

SOURCES OF RISK

Hazards, perils, risk factors emanate from different sources. a ;riot’ may

arise from a social environment. A governments decision to grant or

withdraw subsidy given to farmers on fertilizers arise from political

environment create different risks to organizations and individuals.

Though the sources of environment can be classified on different bases,

we have tried to use a general classification. Given below are the sources

of risk.

Physical environment

It is one of the primary sources or risk. It is important for two reasons it is

all pervasive or is a general risk and it is unavoidable. Perhaps this one

environment, which is common to both individuals and organizations.Each organization should study the prevailing physical environments in

terms of climatic conditions, possibility of flood or eruption of volcanoes

among others.

Technological environment

35

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 36/72

Today technological rules every walk of life. Organizations use

technology in the process of production. Individuals use technology to

increase their output, decrease the defects, to make their life easier.

Greatest risk all of us face from ever changing technology is the risk of

obsolescence. A technological breakthrough renders some old technology

useless or economically infeasible, which is called obsolescence. The four-

stroke technology in motorbikes has made the two stroke engines

obsolescent.

However, the risk of technological failures is also high, when we depend

too much on technology.

Social Environment

It broadly covers the customs, habits, and level of education, tastes and

standard of living of the people in the society. Today’s social environment

is influenced to a major extent to the technological environment. With

rapid progress in technology and economic liberalization, the physical

boundaries between people of various nations are blurring.

Political environment

Political environment consists of the ideology of the government, by-laws

and regulations, regulatory authorities and other agencies, which

command the activities of the individuals as well as the organizations.Changes in the above factors may affect the interest of individuals and

corporations t5hus creating new risks. Any change in the fiscal policy may

affect an industry either positively or negatively.

Some countries like India, US, UK have a democratic government, while

china and Cuba still follow the old communist ideology which does not

favor opening of the economy to international business.

Economic environment

36

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 37/72

Economic environment of a country comprises the national income,

money supply, inflation, consumption and savings habits of the public,

capital markets, export and import policies, government expenditure and

nature of investment. Any change in income level, consumption pattern

habits influence the demand-supply conditions of goods and services as

well as the growth of an industry.

Legal environment

Law is usually evolved on the basis of the established habits and thoughts

of people. It performs the following functions;

It ensures stability and security in society.

It clearly sets the limits on the actions of individuals and

organization.

It establishes the rule of law by ensuring fairer justice.

Operational environment

Business organizations produce and sell some products or services. They

employ some technology and people; use a place and other resources in

the process of production. By nature of product or service some

organizations are exposed to risk. For instance, a coal mining business

exposes the company to accidents in the field. Air carrier business is

exposed to aviation risks. A cinema theatre is exposed to the risk of riots.

State transport buses are exposed to the risk of fire from public.

Cognitive environment

Cognitive environment consists of ability to understand, see, measure and

assess a given situation. The thinking process, risk perception and theassessment of risk are prone to errors. In every stage of human life, the

37

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 38/72

possibility of committing an error cannot be ruled out. The chances of

error in judgment and the ability to assess risk vary from person to person.

Since person in various positions populates an organization, the

organization as an entity may be penalized for the mistakes committed by

any of its employees. Cognitive risk arise due to human errors such as

error in perception., error in assessment and error in perception, error in

assessment and error in judgment about a given environment, hazard or

peril.

EXPOSURES TO RISK

Usually in any business enterprise, people only bother to manage risks

when the organization is directly exposed it them. These exposures create

hazardous conditions, which in turn influence the acts of perils. So one of

the important parts of risk identification is to find out the exposures well in

advance to avoid direct exposures to loss. Broadly speaking, any

organization is exposed to risk. But the nature of exposure needs to be

categorized for an easier evaluation of the negative financial impact.

Based on the nature, exposure can be classified into three categories;

property exposures, liability exposures and human resource exposures.

Property exposures

Property can be of two types; real and personal.

Real property may be defined as the land and whatever is growing on it,

or erected on it or affixed to it.

38

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 39/72

Personal property is anything that is subject to owner ship that another

real property. According to another classification, property may be divided

into physical assets (consisting of land, buildings, plant and machinery),

financial assets (comprising of investments in stocks, bonds, government

securities and cash on hand) and intangible assets (like goodwill,

intellectual properties).

These are exposed to different types of hazards or risk factors depending

up on their nature. Physical property may be damaged, destroyed, stolen of

may suffer a loss of value. The physical property exposure leads to direct

losses (the property itself is lost) or indirect losses (the loss of property,

such as plant, results in business discontinuity and income loss.

Liability exposures

The legal environment in a given country determines the liability

exposures. These exposures are pure risks. Under a given law, rights can

be enforced while the obligations have to be fulfilled. Every organization

is exposed to the risk of losses due to the failure in fulfilling the legally

imposed obligations. Civil and criminal law describe the duties and

responsibilities a citizen is expected to follow. On certain activities,

statutory limitations are imposed through state and union legislations.

Statutory authorities impose rules and directives to establish the standards

of care.

Human resources exposures

People are the prime movers of any organization. The employees of a

company are exposed to several risks. Due to this risk the organizations as

well as the employees suffer the loss. Human resources of a company are

exposed to poor as well as speculative risk. A company may have to

sustain the following types of human resources exposures.

39

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 40/72

A person may meet with an accident and suffer physical injury while

working. It may result in temporary or permanent disability or even death.

Either of the above outcome forces the company as well as the injured to

sustain loss. This is a pure risk.

FRAMEWORK FOR POTENTIAL RISK IDENTIFICATION

A formal procedure is needed to identify the risks in a systematic way,

without which formulation of strategies for managing will difficult. If a

risk manager does not identify the losses or gains to which an organization

is an exposed to, he would find it too difficult to handle when the

undiscovered risks confront the organization.

Systematic procedures must be evolved to developed a framework all the

risks, pure as well as speculative. The identification process must

continuously monetarily internal and the external environment to capture

the information on various risks, since the risk identification is not a one-

time affair or an episodic event.

A well-developed framework results in a comprehensive checklist that

captures all the risks. When the checklist of risk is developed, the manager

needs to evaluate to which of these risks the organization is exposed so

that effective measures can be taken to control the risks.

LOSS EXPOSURE CHECK LISTA detailed understanding of the events that cause loss will help in the

preparation of a risk check list a check list of potential losses can be

prepared from the insurance survey and loss analysis questionnaires.

Insurance survey questionnaires eliciting information of exposures that are

insurable whereas the loss in a analysis questionnaires generally deal with

all pure risks. The questionnaires published by American management

association (AMA), international risk management institute and risk and

40

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 41/72

insurance management society (RIMS) are often referred by many.

AMA’s risk analysis guide provides a checklist of (a) the possible assets

and (b) possible exposures. Further, the exposures are categorized in to

direct, indirect and third party exposures. Such checklist may not be fully

useful as they fail to cover some risks usual to a given organization and

they failed to cover speculative risks.

PROPERTY EXPOSURES

Tangible assets: building, plant, stocks, vehicles, and vessels.

Intangible assets: patents copyrights, trademarks, and goodwill

Liability exposure: liabilities for failure of products, process, and

compensation claims etc.

Human resource exposures

Key personal resignation, accidents etc.

Application of checklist

A checklist is very helpful to an organization to frame the potential risk

identification systems how ever; a standard checklist has drawbacks,which are given below .

It may fail to consider the risks, which are unusual and uniquely

related to a particular organization or situation .

It does not focus on the speculative risk properly, as is done in the

traditional risk practices.

It does not include all risk exhaustively.

41

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 42/72

The first in Appling the checklist is to have a look at the seven

sources of risks, mention in the sections. The risk management can

briefly describe each of the sources. Some experts suggest a slightly

different approach. They say that a careful analysis must be made of

not only the external environment but also internal exposures. As

for this organization they consider the arising from (a) customer or

client, (b) suppliers, (c) competitors, (d) regulators

FINANCIAL STAMENT ANALYSIS

Trading account profit and loss account and balance sheet are refer to as

financial statement. The risks applicable to a given organization can be

identified from the check list the advocates of this method argue that it is

possible to identify the property, liability and personal exposures from a

careful study and detailed analysis of the organizations financial

statements

Using this method a detailed study of each account is made to determine

what risks it create. The risks identified will be reported under eachaccount title. Merits of this method are:

It is objective and reliable as the results are based on readily

available figures

The result can be presented in a clear and concise form

It translates risks identification in to financial terminology which

is more acceptable to the managers, accountants, bankers, creditors andshareholders

42

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 43/72

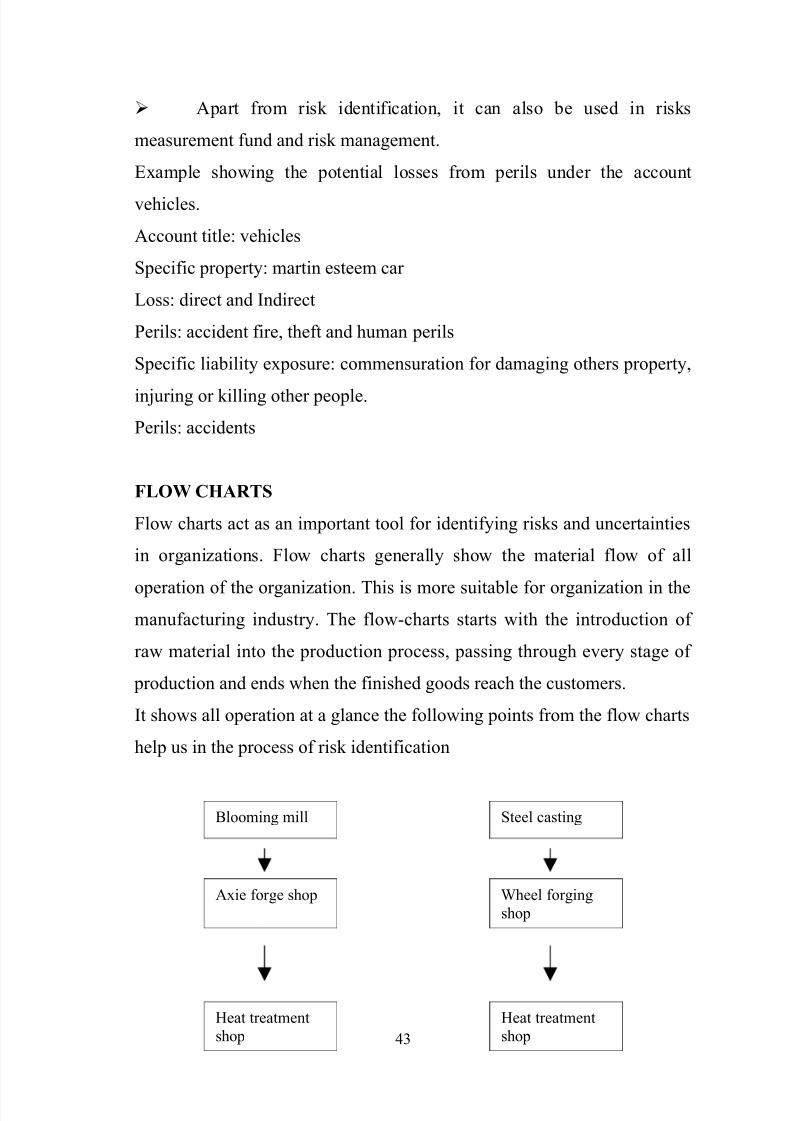

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 44/72

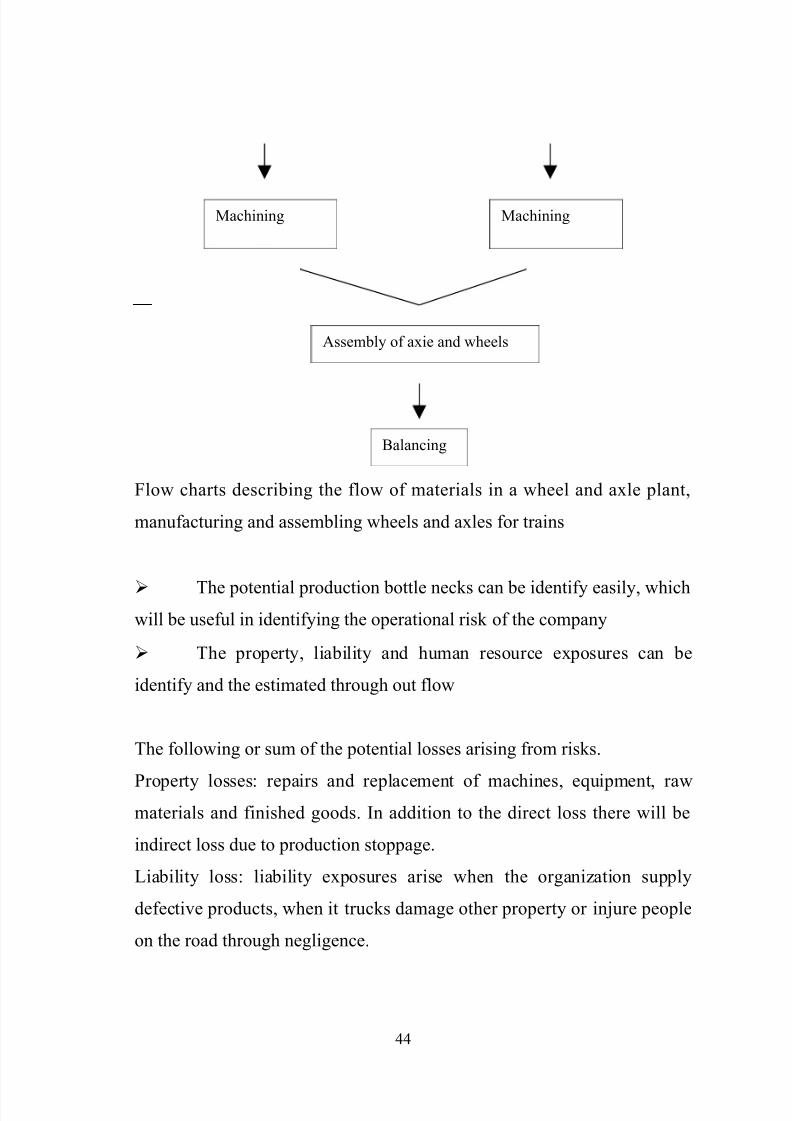

Flow charts describing the flow of materials in a wheel and axle plant,

manufacturing and assembling wheels and axles for trains

The potential production bottle necks can be identify easily, which

will be useful in identifying the operational risk of the company

The property, liability and human resource exposures can be

identify and the estimated through out flow

The following or sum of the potential losses arising from risks.

Property losses: repairs and replacement of machines, equipment, rawmaterials and finished goods. In addition to the direct loss there will be

indirect loss due to production stoppage.

Liability loss: liability exposures arise when the organization supply

defective products, when it trucks damage other property or injure people

on the road through negligence.

44

Machining Machining

Assembly of axie and wheels

Balancing

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 45/72

Human resource exposure: loss arising from the death of key employ, loss

to the families of employee due to the death, retirement, accident, or poor

health.

INPUT-OUTPUT ANALASYS

Input-output analysis is based on the flow of goods and services in the

economy where the output of one organization or entity becomes the input

for another organization. In an organization the output of one department

is assumed to be the input for another department. It is applicable mostly

to process industry or assembly line production processes, or wherever

interdependencies exist between organization units.

The difference between the value of input and output of eachdepartment is considered to be value addition in the given department.

With the help value additions data, we can determine the contribution

from each department to the profits of the organization and the

interdependencies between them. Input-output analysis highlights the

departments whose output is critical.

45

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 46/72

Risk Chain Methods

It can be termed as a loss and hazard analysis tool. the relationship

between hazards and losses is analytically examined. This approach

performs a detailed analysis of the environmental influence on the hazrd,

result of the influence and its long-tern effects.the events in the chain will

be discussed in the chapters ahead.however,they are listed below as a

foretaste:

The hazard,

The environment,

The interaction,

The outcome, and

The consequence,

RISK EVALUATION

Risk identification involves the perception of risk and analyzing its

possible outcomes, while risk evaluation

Helps an organization to find out the possible

CONSEQUENCES OF RISK IN MONETARY TERMS.

To develop a benchmark based on the importance of the risk to

the organization.

To apply this yardstick to all the risks identified.

The consequences of risk may lead to direct and indirect losses, which

may have some adverse financial impact on the company. Risk evaluation

46

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 47/72

begins with the risk identification and its outcomes; Risk identification is

the initial step in the process of risk evaluation or assessment.

RISK CLAIMS & RISK ANALYSE

INTRODUCTION

A claims is the demand that the insurer should redeem the promise made

in the contract. The insurer has then to perform his part of the contract i.e.settle the claim, after satisfying himself that all the condition and

requirements for settlement of claim have been complied. In particular he

should check.

• Whether an insured event has taken place?

• What are the obligations assumed under the contract, which are

required to be performed? These may be payment of bonus, payment of sum assured in installments, waiver of future premiums, etc

47

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 48/72

MATURITY CLAIMS

Under endowment type of policies, the SA is to be paid when the term of

the policy is over. The date on which the term is complete, is the date of

maturity and the settlement of the SA on that date, is the maturity claim.

The amount payable on maturity is the SA, less any debts like loan and

interest or outstanding premium. To this bonuses, if any would be added,

if it is a with profit policy.

Action on maturity claims is initiated by the insurer, based on the records

showing the policies that will mature every month. the insurer normally

send advance intimation to the insured. The insurer has to satisfy that

• There are no assignments

• The identity of the policyholder is proved.

• The age stands admitted

• The premiums are all paid (this is not required for a paid-up policy)

• The original policy is handed in

• The discharge voucher is duly complete.

The insurer is expected to make payment on the maturity date. Post-dated

cheques are normally sent a few days in advance of the maturity date,

provided the discharge form is received duly signed.

SURVIVAL BENEFIT PAYMENTS

A survival benefit is paid during the currency of the policy, before the date

of maturity. The procedure will be similar to payment of maturity claims.

Action will be initiated by the insurer and post dated cheques will be sent

in advance

48

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 49/72

If the policy is reported to be lost, insurers are unlikely to settle on the

basis of an indemnity, as may done in the case of a maturity claim. The

reason is that when a maturity claim is paid, no further obligations remain

under the policy. but, the policy does not cease to exist after the survival

benefits.

If the life assured dies after the date when the survival benefit was due,

but before it is settled, the survival benefit will not be paid to the nominee.

The death claim will be paid to the nominee.

DEATH CLAIM

The procedures in settling a death claim are more complex than in the case

of maturity claims. This is mainly because, the facts relating to death have

to be studied and the identities of claimants have to be established.

The death claim action beings with an intimation being received in the

insurer’s office. The intimation may be sent by the nominee, assignee

relative of the life assured, the employee, agent or development officer.

This intimation may have very little information other than the police

number, the name of the life assured and the data of death.

The following will be necessary before a death claim can be settled

• Policy document

• Deeds of assignments / reassignments

CLAIM CONCESSION

There are situation when, though the policy has lapsed and nothing is

payable, yet the insurer pays the death claim. For example, assume that in

a 30 years old. Endowment policy, 30th annual premium is not paid and the

policy is in a state of lapse in the last year. If the life assured dies a few

49

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 50/72

weeks before maturity, it would be wrong to say that the death claim is not

payable. There is practically no risk in the last year.

The L.I.C pays claims in full in the following circumstances, after

deducting the outstanding premiums with interest. In both the cases, the

policy could have been revived by just paying the arrears of premium and

no proof of good health would have been necessary.

• After there years, if the death claims arises within six months from the

date of lapse.

• After five years, if the death claims arises within twelve months from

the date of lapse.

In cases where premiums are being advanced from surrender value, the

claim amount will be payable in full.

PERSUMPTION OF DEATH

Proof of death is essential. A death certificate issued by the municipal

office or similar local body is the acceptable proof of death. A certificate

of burial or cremation can also be obtained. Statements from witness to the

last rites will be supporting evidence. In the case of accidents, air crashesor an seas, or natural calamities, the bodies may not be found. In such

cases, insurers rely on statements from the carriers or other authorities

with relevant information. In case of defense personnel, a certificate from

the commanding officer of the unit is to be obtained. If a court of enquiry

is ordered, its findings should be obtained.

PRECAUTIONS

50

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 51/72

As per the Indian lunacy Act, if a person is mentally deranged, a court of

law is required to appoint a person to act as a guardian to manage the

properties of the lunatic. Where the assured or the person to sign the

discharge form. If the person to sign the discharge is known to be a

lunatic, only such a guardian can sign the discharge form. If the person has

recovered from the mental disorder, a medical certificate to that effect,

would be necessary.

If the life assured is reported to have died before the maturity date, the

claim has to be treated as a death claim and processed accordingly. But if

the assured is reported to have died after the date of maturity but be fore

the receipt is discharged, the claim is to be treated as a maturity claim and

paid to the legal heirs. Death certificate and evidence of title would be

necessary.

Payments of claim amount to non-residents are governed by the foreign

exchange control regulations.

ACCIDENT AND DISABILITY BENEFITS

These benefits are conditional on conclusive evidence, that all the

eligibility conditions are satisfied and that the exclusions do not apply.

The conditions are that

The accident must be caused by outward, violent means, not self

inflicted

The death must be result of injuries caused by that accident

The death must occur within 120 days or such other period as may

be specified

The exclusions may be

51

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 52/72

Intentional self-injury, attempted suicide, insanity, immorality,

intoxication

Accident while engaged in civil aviation or aeronautics, other than

as

assenger

Injuries resulting from riots, civil commotion etc

IRDA REGULATIONS

The IRDA Regulations stipulate that

The insurer should ask for all the requirements in the case of a death

claim at one time and not piecemeal

The decision to admit or to repudiate should be made within 30 days

of receipt of papers

If an investigation is necessary, it should be completed within 6

months

Interest at 2% over the bank rate, will be payable for delays in

settling the death claims

Interest at the savings Bank rate will be paid if the insurer is ready

to pay but the claimants are not ready to collect.

RISK ANALYSER

You thought you and your childhood friend had the same likes and

dislikes, preferences and prejudices because you grew up together.

Ever wondered why he continues to put his money in bank fixed

deposit while you thrive on playing the stock markets? Its all about

how different your risk profiles are…

52

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 53/72

Your risk profile is essentially determined by objective factors (age,

income level, number of dependence, security of your job) and

subjective factors(risk behavior intrinsic to each individual’s

psychology).

The risk analyzer takes you through a series of scientifically design

multiple choose questions to understand risk taking capacity and

behavior and there by arrive assessment of your risk profile.

1. Your age:

• Under – 30

• 30– 40

• 41 – 50

• 51 – 60

• 60 or over

•

2. Your current annual take-home income is:

• Under Rs. 100,000

• Between Rs. 100,000 and Re.200, 000

• Between Rs. 200,000 and Re.500, 000

• Between Rs. 500,000 and Re.10, 00,000

• Over Rs. 10,00,000

1 The number of years you have until retirement is:

• 3years or less

• to 5 years

• to 10years

53

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 54/72

• 1-3 years

• More than 3 years

2 Your present job or business is :

• Is not dependable

• Is relatively secure

• Is secure

• Doesn’t matters you already have enough wealth

• Doesn’t matter as you can easily find an equally good new

job/career

3 What is your expectation of how your future earnings would be:

• It would far outpace inflation

• It would be some what ahead of inflation

• It would keep pace with inflation

• It may not be able to keep pace with inflation

4 How would you describe your self as a risk-taker?

• Careless

• Willing to take risks for higher return

• Can take calculate risks

•How risk taking capability

• Extremely averse to risk

5 How good is your knowledge of finance?

• I’m an expert in the field of finance

• I’m proficient in finance

• I don’t know much about finance but I keep myself up date about

the development through newspapers, journals, TV, etc.

54

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 55/72

• Limited to knowing things like how the stock market or certain

select script is/are moving

• I’m totally zero as far as knowledge of finance is concerned

6 If you lose your job or stop working today, how long do you think

Your savings can support you?

• Less than 3 months

– 6 months

• months to 1 year

• 1 – 3 years

• More than 3 years

7 If you had Rs.50, 000 to invest, which of the following choices would

you make?

• Put the money in bank fixed deposits and bonds

• Invest the money in mutual funds

• Invest the money in shares

• Invest in a combination of the above with higher proportion

of bank FDs and bonds

• Invest in a combination of the above with higher proportio of mutual

funds and shares

10 you have a market tip on the price appreciation of a certain scrip, you :

• Immediately invest in the scrip

• Invest if feel that the source of tip an experienced /expert market

player

• Give some enquiry and analysis and then decide

• Want to invest but are generally unable to take a decision in such

cases

• Don’t relay on such tip are totally ignore it

55

8/8/2019 venky project2

http://slidepdf.com/reader/full/venky-project2 56/72

1 You are on a TV game show and you rs 10000. you have a choice

to keep the money or risk it to win a higher amount. You:

• Are happy with the rs 10000 that we earned

• Risk the rs 10000 on a 50% chance of winning rs 30000

• Risk the rs 10000 on a 25% chance of winning rs 75000

• Risk the rs 10000 on a 10% chance of winning 100000

2 Which one of the following best describes your feeling

immediately after making an investment, you:

•Aren’t bothered –its just another for you

•Are satisfied and contained with the decision

•Are very sure whether you made the right decision

•Are worried

•Generally regret your decision

3 The stock market has dropped 25% and a share that you won also