Embed Size (px)

Citation preview

World Cargo Symposium 2015

WCS 2015开幕式:

� The plenary session will have speeches conducted in English and Mandarin.

� Please pick up your interpretation device in the foyer by dropping off your ID.

� 中英双语,需要同声传译设备

� 请在回廊处凭有效证件领取同声传译设备

The WCS 2015 Opening Session:

Opening Plenary

Sponsored by

World Cargo Symposium 2015

Chairman’s Opening Remarks

� Glyn Hughes

� Global Head of Cargo, IATA

World Cargo Symposium 2015

Welcome Remarks

� Jiang Zhuoqing

� Vice Mayor of Shanghai

World Cargo Symposium 2015

Host Carrier Address

� Liu Shaoyong

� The Board Chairman, China Eastern

Innovation & Revitalization

Mr. Liu ShaoyongPresident

China Eastern Air Holding Company

The Future of Air Cargo in the Global Supply Chain

I. History and Current Situation of Air CargoII. Analysis of Stagnancy of Air Cargo Demand

III. Suggestion for Innovation and Transformation

Air Cargo Enjoys a Long History

First Air Freight in 1910

The PresentGlobal Air Cargo

Cargo Carryingin 1783

Air Cargo Faces Huge Challenges

(2007-2014) (2007-2014)

Innovation and Transformation� Innovation in Business Mind

� Transformation in Business Mode

consignor Agencies Airlines

Express

Delivery

Companies

consignee

Value Of Air Cargo

• Creating huge opportunities for employment, innovation and collaboration

• Transporting goods worth $6.4 trillion• Transforming lifestyle and work style

around the world

Potential for Industry Development� Informationization transforms business

ecosystem� Online shopping and cross-border

e-commerce emerges� Express delivery volume in China reaches

14 billions in 2014

I. History and Current Situation of Air Cargo

II. Analysis of Stagnancy of Air Cargo Demand

III. Suggestion for Innovation and Transformation

Bottlenecks for the Industry

Compared to rapid recovery of growth in

air passenger transport, air cargo

development clearly lacks momentum.

After the global financial crisis, global

economy faces slow recovery and the air cargo

industry encounters “engine shut-down”.

Analysis of Stagnancy of Air Cargo Demand

� Impact from macro-economy and policies

� Constraints from traditional business mode

� Impact from other transport modes

I. History and Current Situation of Air CargoII. Analysis of Stagnancy of Air Cargo Demand

III.. Suggestion for Innovation and Transformation

Reconstruction of Business Process

Through IT, outdated Through IT, outdated Through IT, outdated Through IT, outdated air cargo air cargo air cargo air cargo

process process process process can be modernized.can be modernized.can be modernized.can be modernized.

Revitalization of Business Ecosystem

Air cargo Air cargo Air cargo Air cargo industry industry industry industry is not is not is not is not isolated, isolated, isolated, isolated,

but a part of the modern logistics but a part of the modern logistics but a part of the modern logistics but a part of the modern logistics

chain.chain.chain.chain.

Cooperation Cooperation Cooperation Cooperation & win& win& win& win----win future.win future.win future.win future.

Improvement of Policy EnvironmentMuch remaining to be done Much remaining to be done Much remaining to be done Much remaining to be done

concerning the policy environment concerning the policy environment concerning the policy environment concerning the policy environment

of IATAof IATAof IATAof IATA, cargo associations, , cargo associations, , cargo associations, , cargo associations,

logistics associations and other logistics associations and other logistics associations and other logistics associations and other

market market market market competitors.competitors.competitors.competitors.

Thank you

World Cargo Symposium 2015

Shanghai: At the heart of today's air cargo industry

� Jing Yiming� President, Shanghai Airport Authority

World Cargo Symposium 2015

Keynote: Facilitating trade and smart regulations, working with the air cargo industry

� Kunio Mikuriya� Secretary General, World Customs Organization

World Cargo Symposium 2015

The State of the Industry

� Tony Tyler

� Director General and CEO IATA

World Cargo Symposium 2015

Chairman’s Remarks

� Glyn Hughes

� Global Head of Cargo, IATA

World Cargo Symposium 2015

COFFEE BREAKSponsored by

In Exhibition

World Cargo Symposium 2015

Cyclical Gains but challenges & risks remain

� Julie Perovic� Senior Economist, IATA

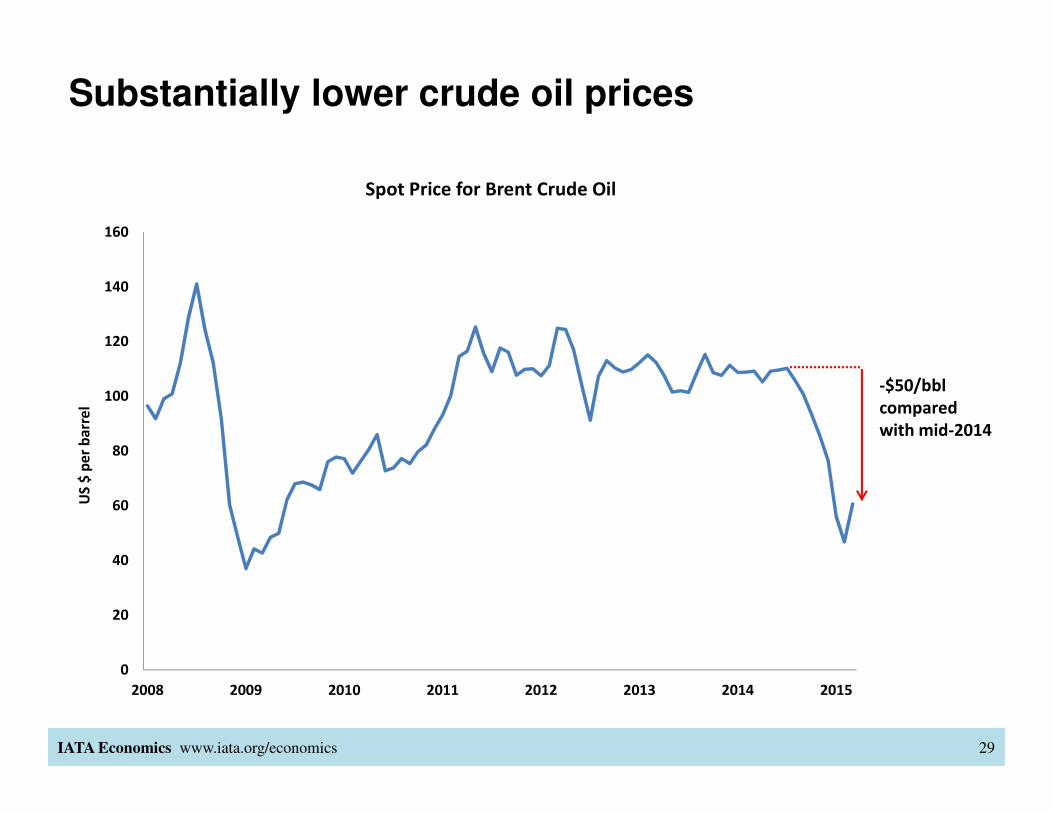

Substantially lower crude oil prices

IATA Economics www.iata.org/economics 29

0

20

40

60

80

100

120

140

160

2008 2009 2010 2011 2012 2013 2014 2015

US

$ p

er

ba

rre

l

Spot Price for Brent Crude Oil

-$50/bbl

compared

with mid-2014

Is that good or bad for the world economy?

IATA Economics www.iata.org/economics 30

Source: Schroders, Oxford Economics

And for the airline industry?

IATA Economics www.iata.org/economics 31

Source: IATA, McKinsey, Platts

0

20

40

60

80

100

120

140

160

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Jet

fue

l pri

ce,

US$

/ba

rre

l

RO

IC,

% o

f in

vest

ed

ca

pit

al

Airline industry ROIC and jet fuel prices

ROIC

Jet fuel price

A strong economic upturn would really help

IATA Economics www.iata.org/economics 32

Source: IATA, McKinsey, IHS Global Insight

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Air

lin

es

RO

IC,

% in

vest

ed

ca

pit

al

Wo

rld

GD

P g

row

th,

%

Airline industry ROIC and world GDP growth

Airlines ROIC

World GDP

growth

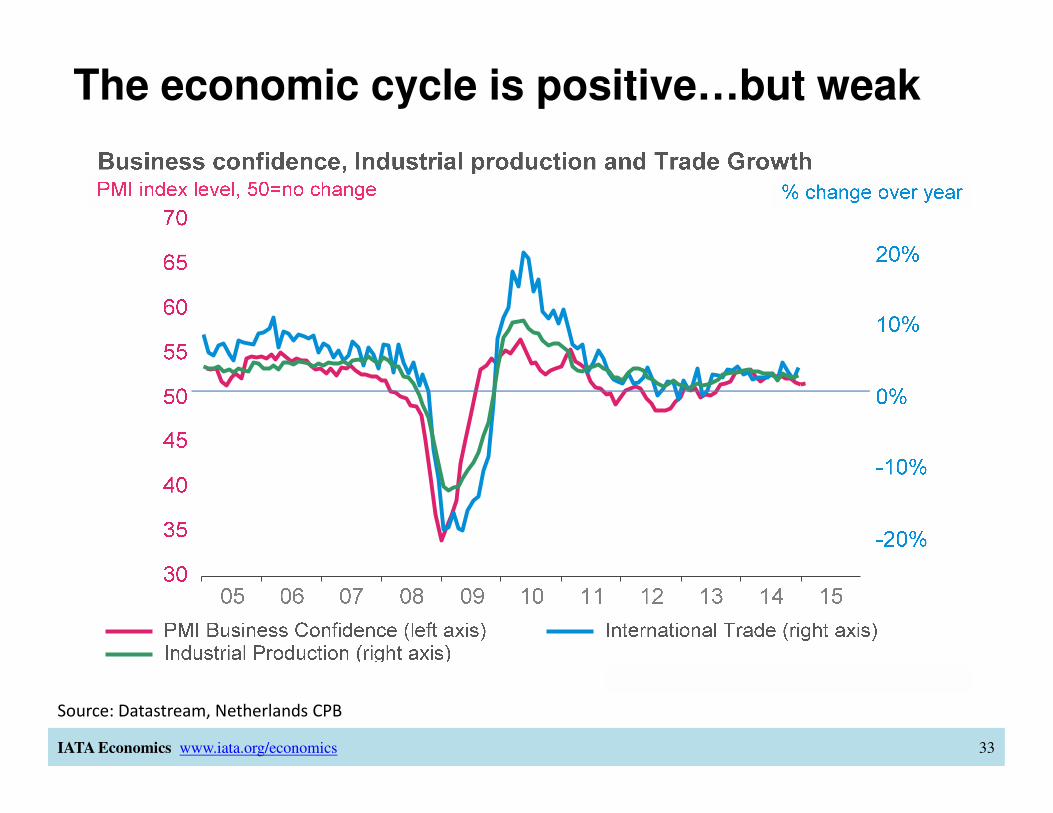

The economic cycle is positive…but weak

IATA Economics www.iata.org/economics 33

Source: Datastream, Netherlands CPB

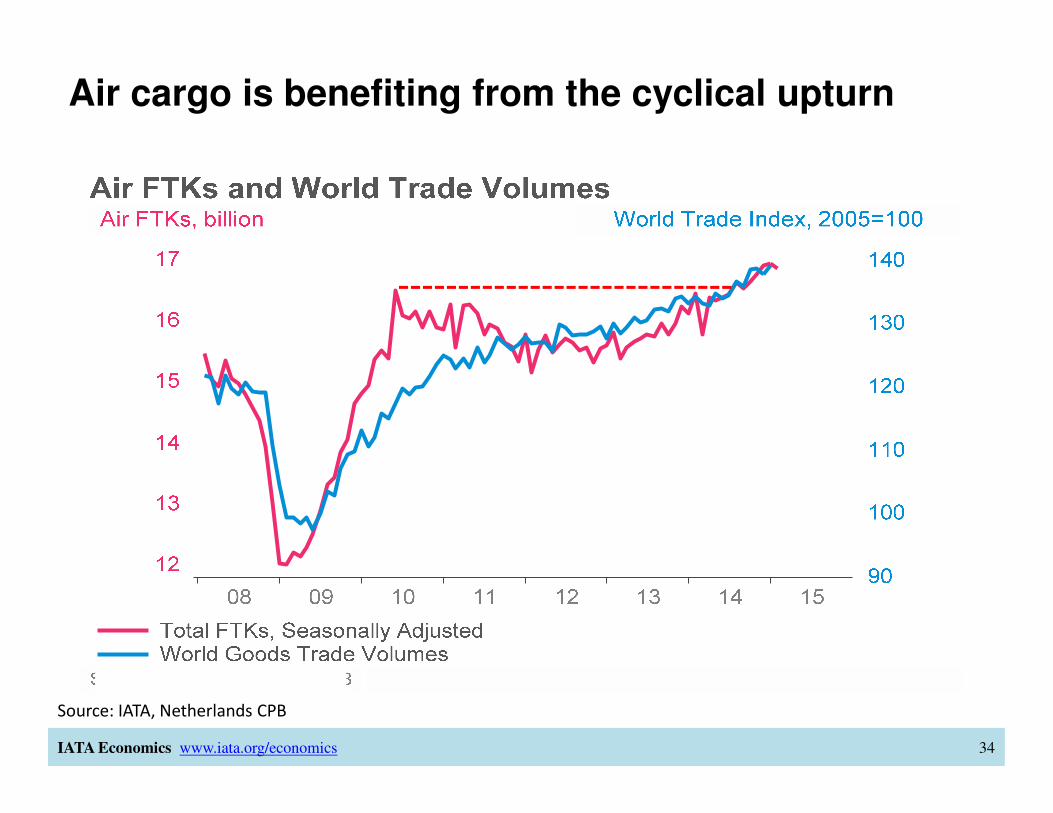

Air cargo is benefiting from the cyclical upturn

IATA Economics www.iata.org/economics 34

Source: IATA, Netherlands CPB

But performance by airline region is uneven

IATA Economics www.iata.org/economics 35

Source: IATA

80

90

100

110

120

130

140

150

160

170

2010 2011 2012 2013 2014 2015

Indexe

d t

o 1

00 in

May

2010

FTKs by region of airline registration

Middle East(+60%)

Africa

EuropeLatin America

Asia-Pacific(-8%)

North America

2010 peak level

And only some trade lanes seeing strong growth

IATA Economics www.iata.org/economics 36

Source: IATA

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2010 2011 2012 2013 2014

% c

ha

nge

ove

r ye

ar

International Freight growth by major routes

Europe - Far East

North Atlantic

North & Mid Pacific

Asset utilization has been improving

IATA Economics www.iata.org/economics 37

Source: IATA, Boeing, all data seasonally adjusted by IATA

37%

39%

41%

43%

45%

47%

49%

51%

53%

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

2008 2010 2011 2012 2013 2014

% a

vail

ab

le f

reig

ht

ton

ne c

ap

acit

y

Avera

ge d

ail

y h

ou

rs f

low

n

Freight Load Factor

Freight aircraft utilization

Freight load factor and freighter aircraft utilization

But lots of new capacity is still arriving

IATA Economics www.iata.org/economics 38

Source: IATA, Ascend

0

2000

4000

6000

8000

10000

12000

14000

1980 1985 1990 1995 2000 2005 2010 2015

Ton

nes

Additional cargo capacity from new aircraft

Pax fleet belly capacity

Freighter fleet capacity

Yields continue to decline

IATA Economics www.iata.org/economics 39

Source: IATA CASS

1.8

1.9

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2010 2011 2012 2013 2014

US

$ p

er

kil

o

Global average cargo yield, including surcharges

Air cargo is likely to get cheaper

IATA Economics www.iata.org/economics 40

Source: IATA CASS

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

2.7

20

40

60

80

100

120

140

2010 2011 2012 2013 2014 2015

US

$ p

er

ba

rre

l

Brent crude oil prices and global cargo rates

US$

pe

rki

lo

Global cargo rates

Brent crude oil prices

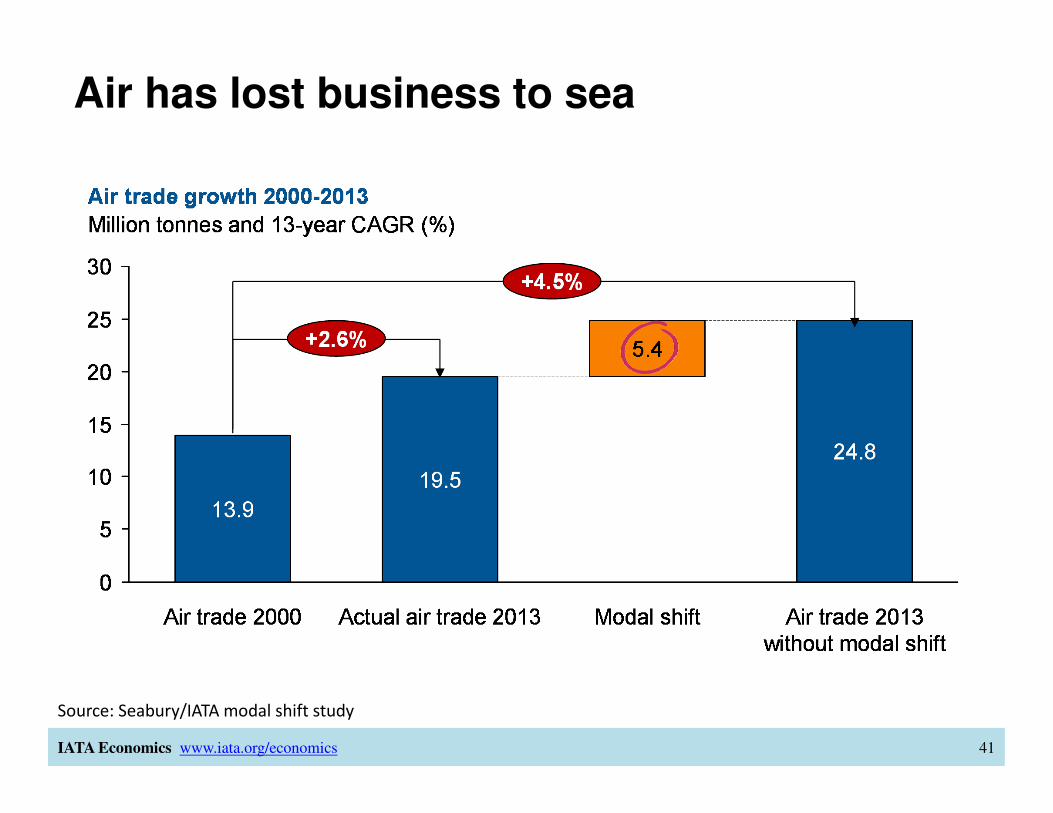

Air has lost business to sea

IATA Economics www.iata.org/economics 41

Source: Seabury/IATA modal shift study

But air cargo’s trade share stable recently

IATA Economics www.iata.org/economics 42

Source: Seabury/IATA modal shift study

0.7

0.8

0.9

1.0

1.1

1995 2000 2005 2010

Ind

ex

rati

o,

eq

ua

l to

1 i

n 2

00

5

FTKs / international trade

-1.5% a year

The recent problem is trade weakness

IATA Economics www.iata.org/economics 43

Source: IATA, Netherlands CPB

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

1995 2000 2005 2010

% c

ha

ng

e o

ver

yea

r

Growth of international trade and industrial production

Expected

international

trade growth

International

trade growth

Domestic industrial

production growth

A serious challenge to the future of air cargo

IATA Economics www.iata.org/economics 44

Source: IATA, Netherlands CPB

Growing trade protectionism is a threat

IATA Economics www.iata.org/economics 45

Source: World Trade Organization, Global Trade Alert, B20

The economic backdrop is improving

IATA Economics www.iata.org/economics 46

Source: EIU

0

1

2

3

4

5

6

US Japan Euro Area ASPACexcl Japan

LatinAmerica

MiddleEast North

Africa

Sub-SaharanAfrica

World

% c

han

ge o

ver

yea

r

Forecasts for GDP growth

2014

2015

But risks are still skewed toward the downside

IATA Economics www.iata.org/economics 47

Source: Schroders

Stagflationary

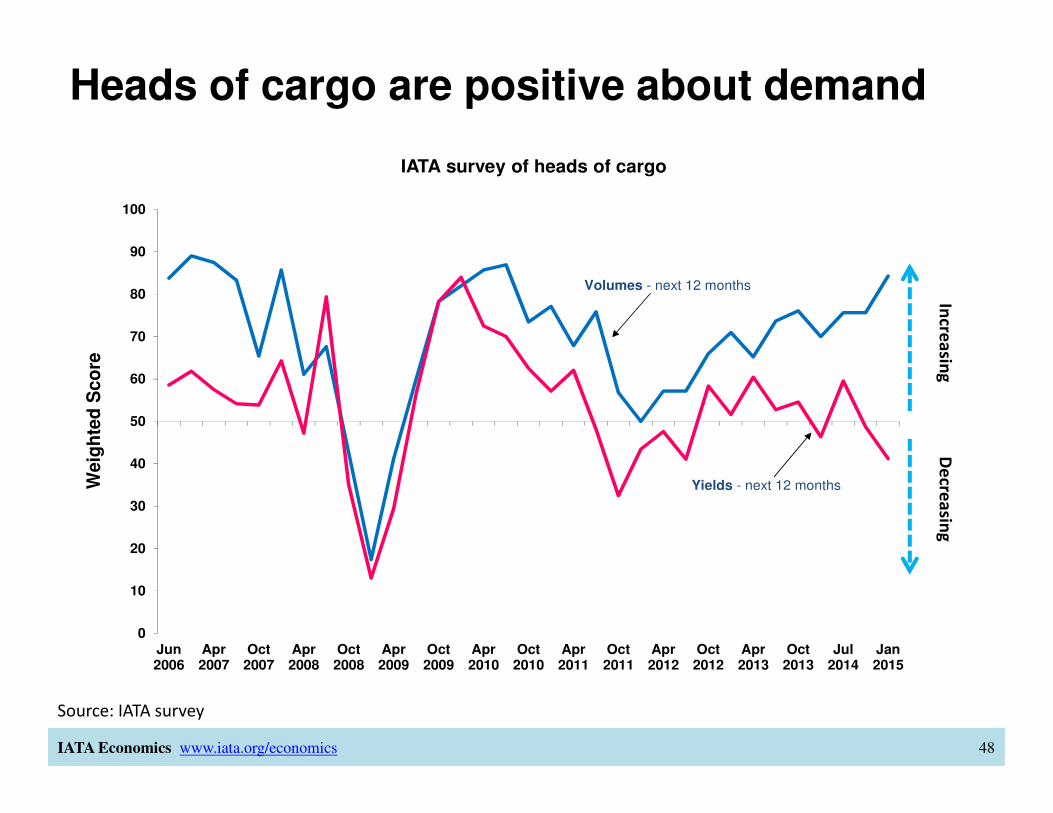

Heads of cargo are positive about demand

IATA Economics www.iata.org/economics 48

Source: IATA survey

0

10

20

30

40

50

60

70

80

90

100

Jun2006

Apr2007

Oct2007

Apr2008

Oct2008

Apr2009

Oct2009

Apr2010

Oct2010

Apr2011

Oct2011

Apr2012

Oct2012

Apr2013

Oct2013

Jul2014

Jan2015

We

igh

ted

Sc

ore

IATA survey of heads of cargo

Volumes - next 12 months

Yields - next 12 months

Incre

asin

gD

ecre

asin

g

World Cargo Symposium 2015

Glyn HughesGlobal Head of Cargo, IATA

The year in review: Did we deliver on promises made?

24.9%e-AWB penetration

World Cargo Symposium 2015

Pharma

Dangerous Goods

SimplifyingCargo Governance

World Cargo Symposium 2015

ModernizingAgency Program

World Cargo Symposium 2015

Enhanced

ULDguidelines

CO2reporting

IATA & UPUMemorandum of Understanding

CSD & e-CSD

Secure freight

ACI

EU ACC3

World Cargo Symposium 2015

Transforming the air cargo industry

MatrixFacility capabilities

World Cargo Symposium 2015

World Cargo Symposium 2015

Executive Round Table: Instruments for global and regional development

� Moderator: � Andrew Herdman, Director General AAPA

� Executives:� Tony Tyler, IATA DG and CEO

� Kunio Mikuriya, Secretary General WCO

� Xiaozhun Yi, Deputy Director General WTO

World Cargo Symposium 2015

NETWORKING LUNCHSponsored by

In Exhibition

World Cargo Symposium 2015

Improving Air Cargo:The Customer’s View

� Moderator: � Tom Windmuller, IATA SVP Airport, Passenger, Cargo and

Security (APCS)

� Shippers� Robert Mellin, Head of Distribution Logistics, Ericsson

� Alex Xu, Associate Supply Chain Director, Lilly Suzhou Pharmaceutical Co., Ltd

� Chris Welsh, Secretary General, Global Shippers Forum

World Cargo Symposium 2015

IATA 2015 global shippers survey

� Short online questionnaire

� 336 answers received in 6 weeks

� Part of IATA’s overall transformation strategy

� Good feedback for airlines

� We know because we asked!

World Cargo Symposium 2015

Do survey respondents ship by air?

Yes 316 94%

No 20 6%

Total 336 100%

World Cargo Symposium 2015

How satisfied are airfreight customers?

Average score for the 316 customers using air

How satisfied are you with the air cargo services that you have used in the last 12 months?

(1 = not satisfied at all -- 10 = extremely satisfied)

7.08very unhappy

customers7%

World Cargo Symposium 2015

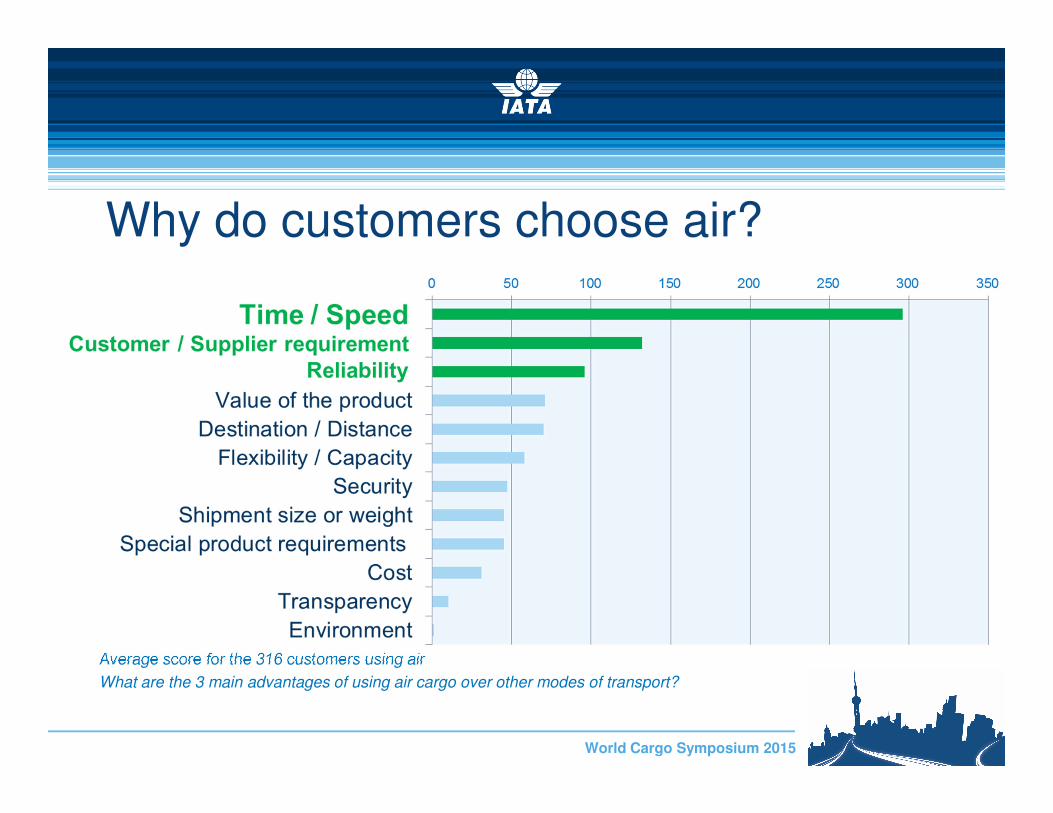

Why do customers choose air?

Average score for the 316 customers using air

What are the 3 main advantages of using air cargo over other modes of transport?

World Cargo Symposium 2015

What’s wrong with air cargo?

Air cargo represents less than

0.5% of our shipments but

around 2% of time and effort

spent – Too complex! Cargo not flying as booked,

offloads common, partial shipments

– Lack of transparency!

Replies to inquiries for simple

things like rates can take days!

& Poor websites to handle

transactions on my own – Poor customer service, very old-fashion!

Long lead times compared to

cost – Value proposition is weak!

It's a pain to pick up and drop off

cargo – Painful experience!

[Time & temperature sensitive]

products not handled very well in

airports – Lack of quality!

To much repetitive data entry for

necessary documentation –Inefficient processes!

When something goes wrong it

takes time to get information – Lack of visibility & real-time information!

World Cargo Symposium 2015

Is air freight competitive w/ other modes?

Equally 130 41%

More 70 22%

Less 125 36%

No response 1 <1%

World Cargo Symposium 2015

Is air cargo innovative?

Equally 148 47%

More 106 33%

Less 61 19%

No response 1 <1%

World Cargo Symposium 2015

Improving Air Cargo:The Customer’s View

� Moderator: � Tom Windmuller, IATA SVP Airport, Passenger, Cargo and

Security (APCS)

� Shippers� Robert Mellin, Head of Distribution Logistics, Ericsson

� Alex Xu, Associate Supply Chain Director, Lilly Suzhou Pharmaceutical Co., Ltd

� Chris Welsh, Secretary General, Global Shippers Forum

World Cargo Symposium 2015

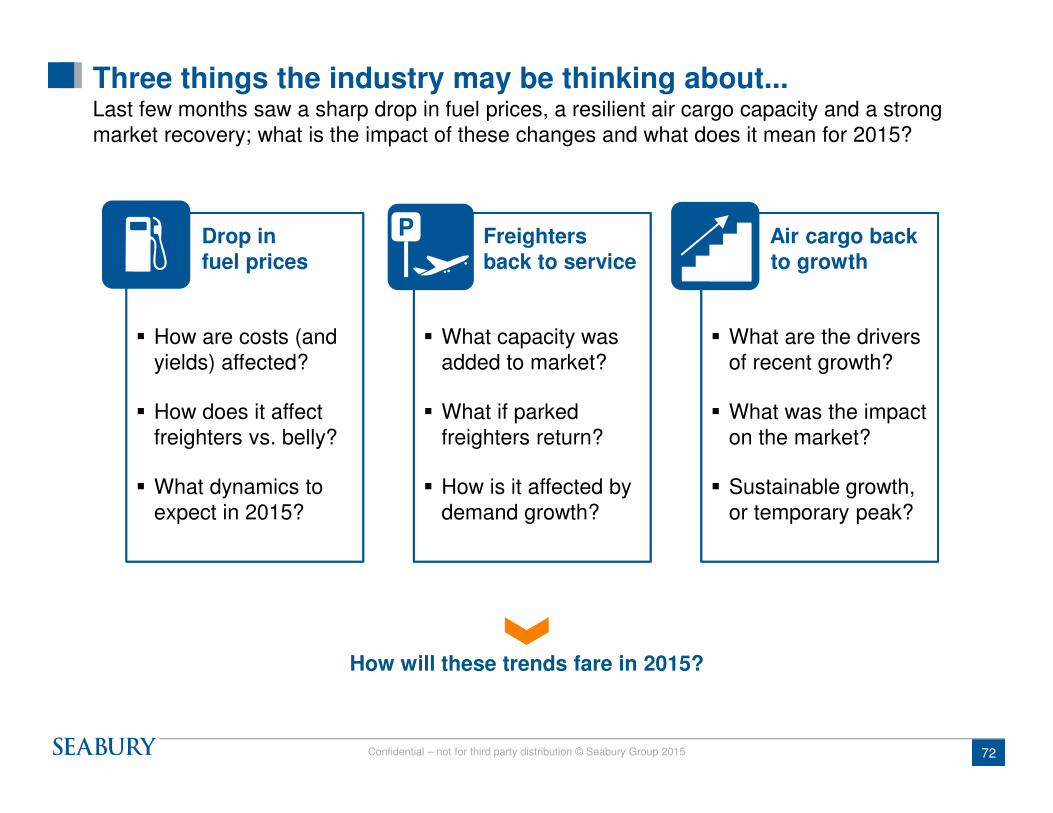

Air Cargo 2015: What is the impact of key recent trends to the air cargo industry?

� Marco Bloemen

� Senior Vice President Seabury Group

Confidential – not for third party distribution © Seabury Group 2015

Air Cargo 2015: Recent trends and impact on air cargo industry

More insights, better decisions...

10.Mar.15

72Confidential – not for third party distribution © Seabury Group 2015

Air cargo backto growth

� What are the drivers of recent growth?

� What was the impact on the market?

� Sustainable growth, or temporary peak?

Freightersback to service

� What capacity was added to market?

� What if parked freighters return?

� How is it affected by demand growth?

Drop in fuel prices

� How are costs (and yields) affected?

� How does it affect freighters vs. belly?

� What dynamics to expect in 2015?

Three things the industry may be thinking about...Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong market recovery; what is the impact of these changes and what does it mean for 2015?

P

How will these trends fare in 2015?

73Confidential – not for third party distribution © Seabury Group 2015

Air cargo backto growth

� What are the drivers of recent growth?

� What was the impact on the market?

� Sustainable growth, or temporary peak?

Freightersback to service

� What capacity was added to market?

� What if parked freighters return?

� How is it affected by demand growth?

Drop in fuel prices

� How are costs (and yields) affected?

� How does it affect freighters vs. belly?

� What dynamics to expect in 2015?

Three things the industry may be thinking about...Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong market recovery; what is the impact of these changes and what does it mean for 2015?

P

How will these trends fare in 2015?

74Confidential – not for third party distribution © Seabury Group 2015

110

80

70

100

90

60

50

Oct-2014

Jan-2015

Jul-2014

Apr-2014

Jan-2014

Oct-2013

Jul-2013

Apr-2013

Jan-2013

What to predict for 2015?Predictions for fuel price drop for the full year 2015 vary; as usual with fuel, several scenarios are plausible; yields are far less volatile and have historically shown lesser variations

Global yields vs. jet fuel price1

Index (fuel Jan 2014 = 100; yield Q1’ 14= 100)

1) Jet fuel is U.S. Gulf Coast Kerosene-Type Jet Fuel Spot Price FOB (Dollars per Gallon); Source: U.S. Energy Information Administration; IATA (December 2014 forecast); IATA e-Chartbook: IATA’s forecast of jet kerosene prices from December 2014; IEA’s forecast of Brent crude oil prices from its market report 2015; Seabury Analysis

IATA predicts jet fuel price to drop 14%, IEA forecasts a 45% decrease in crude oil prices

Jet fuel

Gross yield (quarterly)

75Confidential – not for third party distribution © Seabury Group 2015

Drop in fuel price will stimulate freighter contributionFreighter contribution may have largely benefited from recent drop in fuel prices; even though yield will have suffered a drop, it is likely to be largely offset by fuel cost saving

Impact of fuel and yield changes on freighter contribution$M, per year, per aircraft

Note: evaluates illustrative Europe – Asia rotation on 747-400F, at average utilization of 10.1BH/day, average load factor of 85%, average gross yield of $2.05/kg in 2014, annual revenue of ~$67M per year; cost include: aircraft leasing cost; crew cost; maintenance cost; fuel burn; navigation; landing; handling. Fuel cost assumes $2.70/gal in 2014. Illustrative contribution, actual contribution will depend on several factorsSource: industry benchmark cost; Seabury analysis

Gross yield downside

-5%

Fuel costsaving -30%

+7.7

Freighter contribution

(2015)

Freighter contribution

(2014)

-3.4

11.1

0.9

8.6

Illustrative example:

operating 1x 747-400F

three times a week on

Europe – Asia rotation

Significant change in contribution of

$ 7.7 Million per year per freighter

Change in fuel price largely offsets drop in yields

76Confidential – not for third party distribution © Seabury Group 2015

Several fuel vs. yield scenarios are positive for freightersEven though fuel price is “difficult” to forecast, expected full year 2015 drop is most likely greater than the anticipated change in yield

Impact of fuel & yield changes, on freighter contributionChange in contribution ($M, per year, per aircraft)

Note: evaluates illustrative Europe – Asia rotation on 747-400F, at average utilization of 10.1BH/day, average load factor of 85%, average gross yield of $2.05/kg in 2014, annual revenue of ~$67M per year; cost include: aircraft leasing cost; crew cost; maintenance cost; fuel burn; navigation; landing; handling. Fuel cost assumes $2.70/gal in 2014. Illustrative contribution, actual contribution will depend on several factorsSource: industry benchmark cost; Seabury analysis

$ 0 M $ -3.4 M $ -6.7 M $ -10.1 M $ -13.5 M

$ 3.7 M $ 0.3 M $ -3 M $ -6.4 M $ -9.8 M

$ 7.4 M $ 4 M $ 0.7 M $ -2.7 M $ -6.1 M

$ 11.1 M $ 7.7 M $ 4.3 M $ 1 M $ -2.4 M

$ 14.8 M $ 11.4 M $ 8 M $ 4.7 M $ 1.3 M

$ 18.5 M $ 15.1 M $ 11.7 M $ 8.4 M $ 5 M

0

-10%

-20%

-30%

-40%

-50%

0 -5% -10% -15% -20%

Change in fuel cost (%)

Change in gross yield (%)

Unless yields drop stronger than -5%, fuel price drop should translate to substantial cost savings

77Confidential – not for third party distribution © Seabury Group 2015

Belly contribution is substantially larger than contribution in freighter operations, in part due to a significantly lower fuel cost component

Change in incremental belly contributionUSD/kg

Change in freighter contributionUSD/kg

Note: evaluates illustrative Europe – Asia rotation on 747-400F, at average utilization of 10.1BH/day, average load factor of 85%, average gross yield of $2.05/kg in 2014, annual revenue of ~$67M per year; Using ACMI cost (aircraft leasing-; crew-; maintenance- and insurance cost), fuel burn and other Direct Operating Cost (navigation-; landing- and handling cost). Fuel cost assumes $2.70/gal in 2014. Illustrative contribution, actual contribution will depend on several factors. Source: industry benchmark cost; Seabury analysis

Other DOC

Fuel (incremental)

Contribution

2015 scenario

1.95

8%

1.30(67%)

2014 average

2.05

12%

1.33(65%)

Average yield 1%

Contribution

1.95

40%

13%

2.05

55%

Fuel cost

Other DOC

ACMI

2015 scenario2014 average

2015 scenario assumes:-5% on yields

-30% on fuel cost

Recent fuel price drops generates much more contribution for freighters, compared to belly operators

Fuel impact is more positive for freighters than for bellies

78Confidential – not for third party distribution © Seabury Group 2015

Air cargo backto growth

� What are the drivers of recent growth?

� What was the impact on the market?

� Sustainable growth, or temporary peak?

Freightersback to service

� What capacity was added to market?

� What if parked freighters return?

� How is it affected by demand growth?

Drop in fuel prices

� How are costs (and yields) affected?

� How does it affect freighters vs. belly?

� What dynamics to expect in 2015?

Three things the industry may be thinking about...Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong market recovery; what is the impact of these changes and what does it mean for 2015?

How will these trends fare in 2015?

P

79Confidential – not for third party distribution © Seabury Group 2015

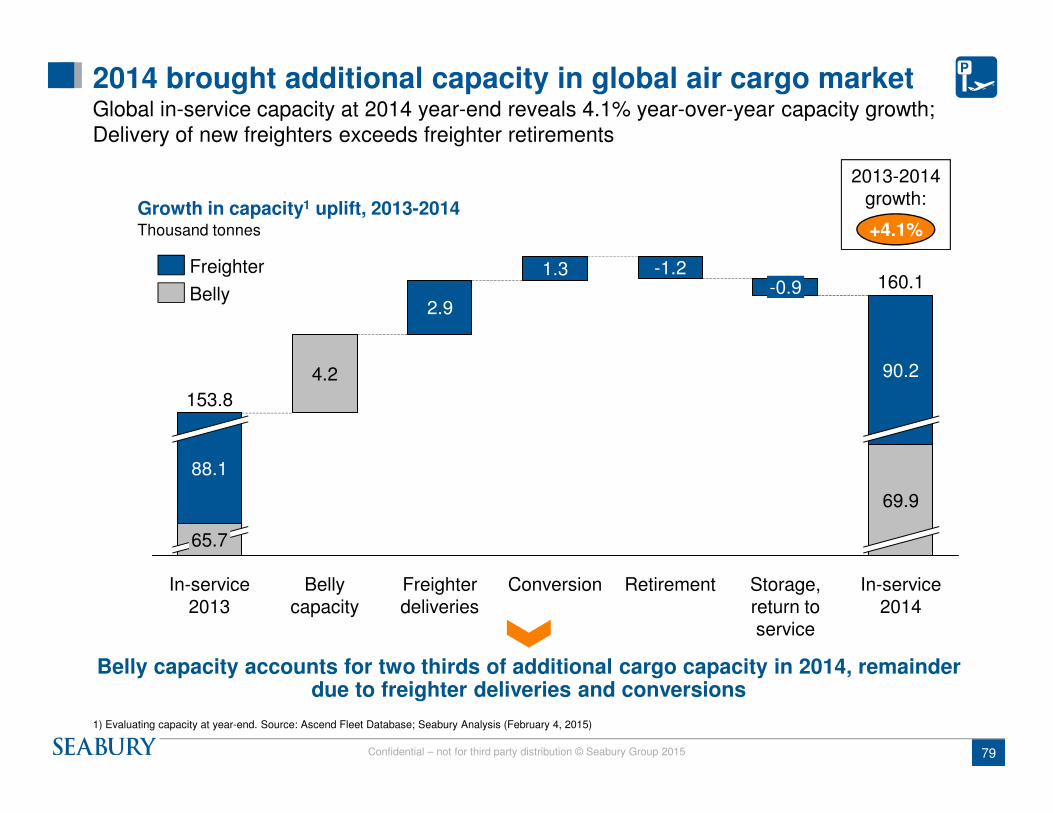

Growth in capacity1 uplift, 2013-2014

2014 brought additional capacity in global air cargo marketGlobal in-service capacity at 2014 year-end reveals 4.1% year-over-year capacity growth; Delivery of new freighters exceeds freighter retirements

Thousand tonnes

1) Evaluating capacity at year-end. Source: Ascend Fleet Database; Seabury Analysis (February 4, 2015)

2013-2014 growth:

+4.1%

P

Belly capacity accounts for two thirds of additional cargo capacity in 2014, remainder due to freighter deliveries and conversions

90.2

69.9

-0.9 160.1

2.9

Bellycapacity

4.2

Freighterdeliveries

1.3

Conversion In-service 2014

Storage, return to service

88.1

65.7

153.8

In-service 2013

-1.2

Retirement

Belly

Freighter

80Confidential – not for third party distribution © Seabury Group 2015

Roughly 110 large wide body freighters are currently parked16x 747-400F are parked and could potentially return to service, if favourable market conditions persist; 92 other older large aircraft are also parked

Size of large freighter fleet, February 2015# aircraft

1) Fleet age of aircraft in serviceSource: Ascend Fleet Database (February 4, 2015); Seabury analysis

3327

32

747-200F747-400P2F

MD11F767F

4

747-400F

16

777FA330F747-8F

2

What will a more favourable fuel and market outlook do to the parked freighter fleet?

In Service

Storage

Firm order

Option/LOI

Fleetage1

3 3 4 13 21 2919 23

P

Younger aircraft types Older aircraft types

81Confidential – not for third party distribution © Seabury Group 2015

What if parked capacity would return?With 16x 747-400F currently parked, capacity may increase by ~1% if these are all brought back to service; the older and less likely to return capacity may add as much as ~6.8% in total

In-service capacity uplift: what if parked capacity would return?Thousand tonnes and % increase

Source: Ascend Fleet Database (February 4, 2015); Seabury analysis

What-if capacity uplift

171.0

Belly

Freighter

33x 747-200F

3.3

32x MD11F27x 747-400P2F

5.4

16x 747-400F4x 767F

1.8

2x 747-8F

0.2

In-servicecapacity 2014

160.1

Belly

Freighter

+1.1%

What freighter capacity would return to service?

+3.4% +2.1%

P

0.2%

Returns to service may have limited impact, even if all parked 747-400F’s are brought back to service

+6.8%

Younger aircraft types Older aircraft types

Total %

82Confidential – not for third party distribution © Seabury Group 2015

Parked capacity fluctuates with market growthPeriods of negative air trade growth have led to increased parked freighter share

Parked freighter capacity, quarterly, 2001-2014% parked capacity vs. in-service capacity (weight)

Source: Ascend fleet database (February 2015); Seabury Global Trade Database

6%

8%

10%

12%

14%

16%

18%

20%

-30%

-20%

-10%

0%

10%

20%

30%

40%

201020092008 2011 20132012 20142001 20062005 200720042002 2003

Share of parked capacity (left axis)

Air trade growth (right axis)

Air trade growth, YoY (%)

Recent parked freighter share hovers around 14%

83Confidential – not for third party distribution © Seabury Group 2015

Drop in fuel prices

� How are costs (and yields) affected?

� How does it affect freighters vs. belly?

� What dynamics to expect in 2015?

Three things the industry may be thinking about...Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong market recovery; what is the impact of these changes and what does it mean for 2015?

How will these trends fare in 2015?

Air cargo backto growth

� What are the drivers of recent growth?

� What was the impact on the market?

� Sustainable growth, or temporary peak?

Freightersback to service

� What capacity was added to market?

� What if parked freighters return?

� How is it affected by demand growth?

P

84Confidential – not for third party distribution © Seabury Group 2015

Thank you China’s exports...China’s exports were behind nearly four out of every seven tonnes of additional air cargo in 2014; other Asian exports and European exports round up the rest of the growth

Breakdown of 2013-2014 air cargo growthThousand tonnes

Note: Estimating UN comtrade for 2014. Source: Seabury Global Trade Database, World Monthly dataset (March 3rd, 2015)

Middle East & S. Asia

21,631

Europe

158

Air cargo 2013

China Air cargo 2014

398

OtherLatin America

North America

20,868

OtherAsia

Exporting region

High-tech contributes to 40% of China

incremental air tonnes

China provides 52% of global incremental

air tonnes

85Confidential – not for third party distribution © Seabury Group 2015

...and North America’s importsWhile China and the rest of Asia have catalyzed exports, imports from North America have increased, from either China, Europe or Asia Pacific

Incremental air cargo 2013-2014, top changesThousand tonnes

Note: Estimating UN comtrade for 2014. Source: Seabury Global Trade Database (March 3rd, 2015)

Europe to North America

77

China to Middle East & South Asia

77

China to North America

161

North America to Europe

46

China to Europe

49

China to Other Asia

59

Other Asia to North America

70

North American imports

Other

US west coast port strike has triggered strong growth in Asia to North America air trade

86Confidential – not for third party distribution © Seabury Group 2015

Zhengzhou’s Foxconn factory drives China’s mobiles exportsExports of mobile phones gradually shifted to Zhengzhou (Foxconn) now manufacturing ~50% of the new iPhones, while the remainder likely originates from Shanghai (Pegatron)

China’s air exports of mobile phonesThousand tonnes

Source: Seabury Trade Database China Monthly (March 9th, 2015)

JA MMFJDNOSAJJM OA SJJ DNAMFJDNOSAJJMAMFJDNOSAJJMAMFJ

2011 2012 2013 2014

iPhone 5iPhone

5C & 5S

Others

Shanghai

Zhengzhou

Beijing

What will be the impact of next iPhone launch?

iPhone 4SiPhone 5C 8GBLaunch of: iPhone 6

‘15

87Confidential – not for third party distribution © Seabury Group 2015

Fashion

Each dot is a zip code, size represents amount of air weight traded in 2013-2014

High Tech

Consumer goods

Automotive Capital equipment

Industrial consumables

China shipper data provides new insightsData on individual shippers captures trends to/from regions within China

Note: Using trade (import and export) by air. Source: Seabury Global Trade Database, China shipper dataset (February 23, 2015)

High granularity in shipper data helps to understand the heartbeat of China growth

88Confidential – not for third party distribution © Seabury Group 2015

Air cargo backto growth

� What are the drivers of recent growth?

� What was the impact on the market?

� Sustainable growth, or temporary peak?

Freightersback to service

� What capacity was added to market?

� What if parked freighters return?

� How is it affected by demand growth?

Drop in fuel prices

� How are costs (and yields) affected?

� How does it affect freighters vs. belly?

� What dynamics to expect in 2015?

Three things the industry may be thinking about...Last few months saw a sharp drop in fuel prices, a resilient air cargo capacity and a strong market recovery; what is the impact of these changes and what does it mean for 2015?

P

World Cargo Symposium 2015

Matching Supply and DemandMeeting customer expectations – a panel discussion

� Moderator: � Enno Osinga, Senior Vice President, Cargo Amsterdam Schiphol

Airport & Vice Chair TIACA

� Panelists� Oliver Evans, Chief Cargo Officer Swiss World Cargo

� James Woodrow, Director Cargo Cathay Pacific Airways

� Michael Steen, CCO and EVP Atlas Air

World Cargo Symposium 2015

Chairman’s Closing Remarks

� Glyn Hughes

� Global Head of Cargo, IATA

World Cargo Symposium 2015

COFFEE BREAKIn Exhibition

World Cargo Symposium 2015

Thank you

For more information

� Visit our websitewww.iata.org/cargo

� Subscribe to Cargo Trackerwww.iata.org/optin

� Follow us on Twitter http://twitter.com/iata