ΓΕΝΙΚΗ ΣΥΝΕΛΕΥΣΗ / ΗΜΕΡΙΔΑ ΕΣΒΕΠ

Τετάρτη 27 Μαρτίου 2013

ΑΠΟ… “ΠΛΗΘΩΡΙΣΜΟ” ΣΤΗΝ ΚΡΙΣΗΟΙ ΕΞΕΛΙΞΕΙΣ ΣΤΟ ΛΙΑΝΕΜΠΟΡΙΟ ΤΡΟΦΙΜΩΝ ΤΑ ΤΕΛΕΥΤΑΙΑ ΧΡΟΝΙΑ

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

2

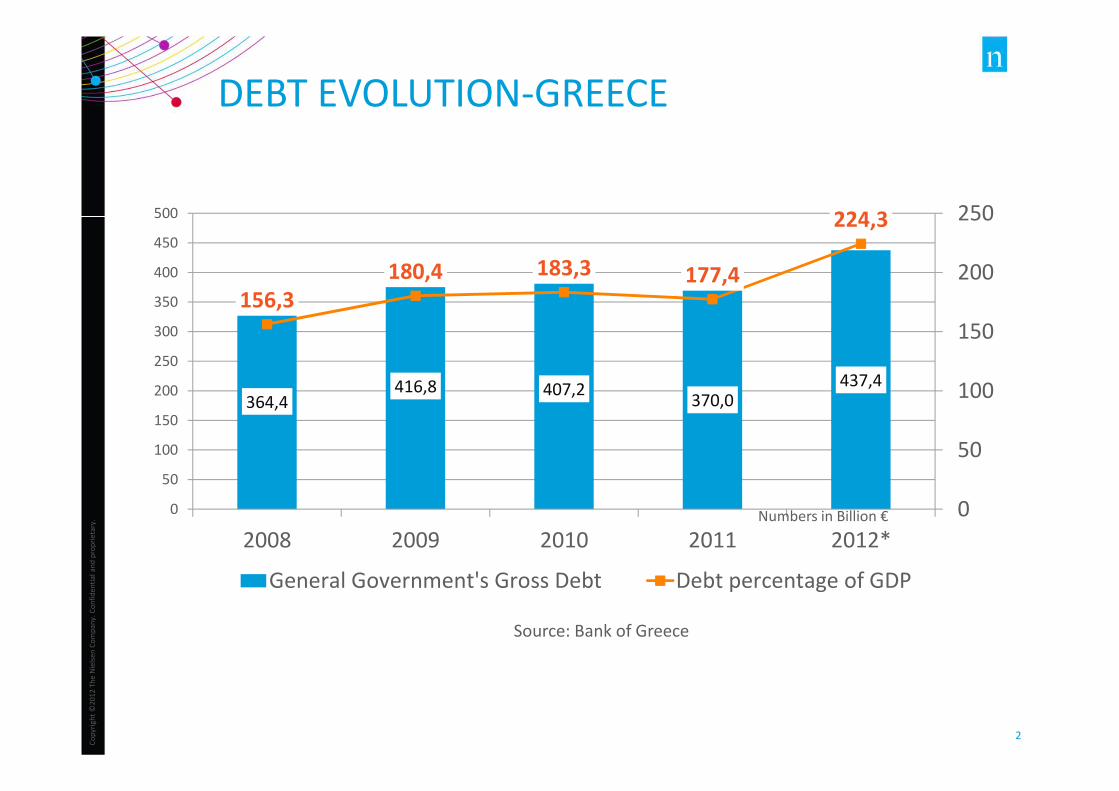

364,4416,8 407,2

370,0437,4

156,3

180,4 183,3 177,4

224,3

0

50

100

150

200

250

0

50

100

150

200

250

300

350

400

450

500

2008 2009 2010 2011 2012*

General Government's Gross Debt Debt percentage of GDP

DEBT EVOLUTION-GREECE

Numbers in Billion €

Source: Bank of Greece

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

3

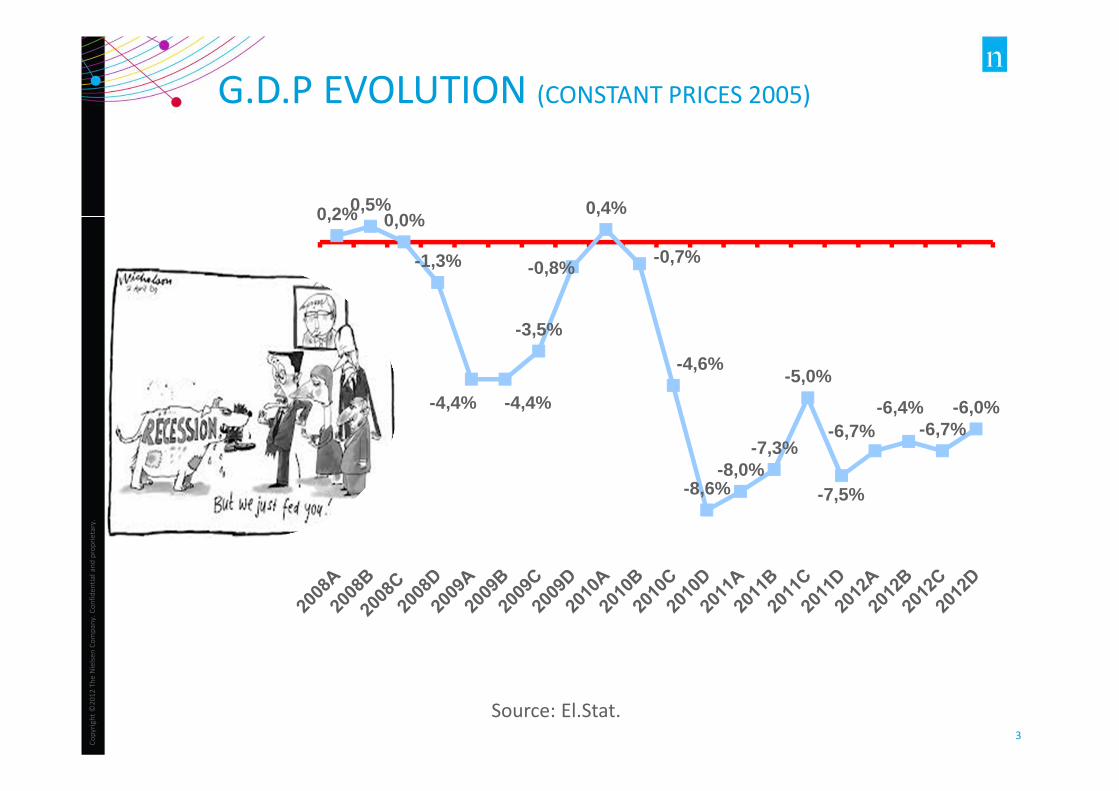

0,2%0,5%0,0%

-1,3%

-4,4% -4,4%

-3,5%

-0,8%

0,4%

-0,7%

-4,6%

-8,6%-8,0%

-7,3%

-5,0%

-7,5%

-6,7%-6,4%

-6,7%-6,0%

Source: El.Stat.

G.D.P EVOLUTION (CONSTANT PRICES 2005)

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

4

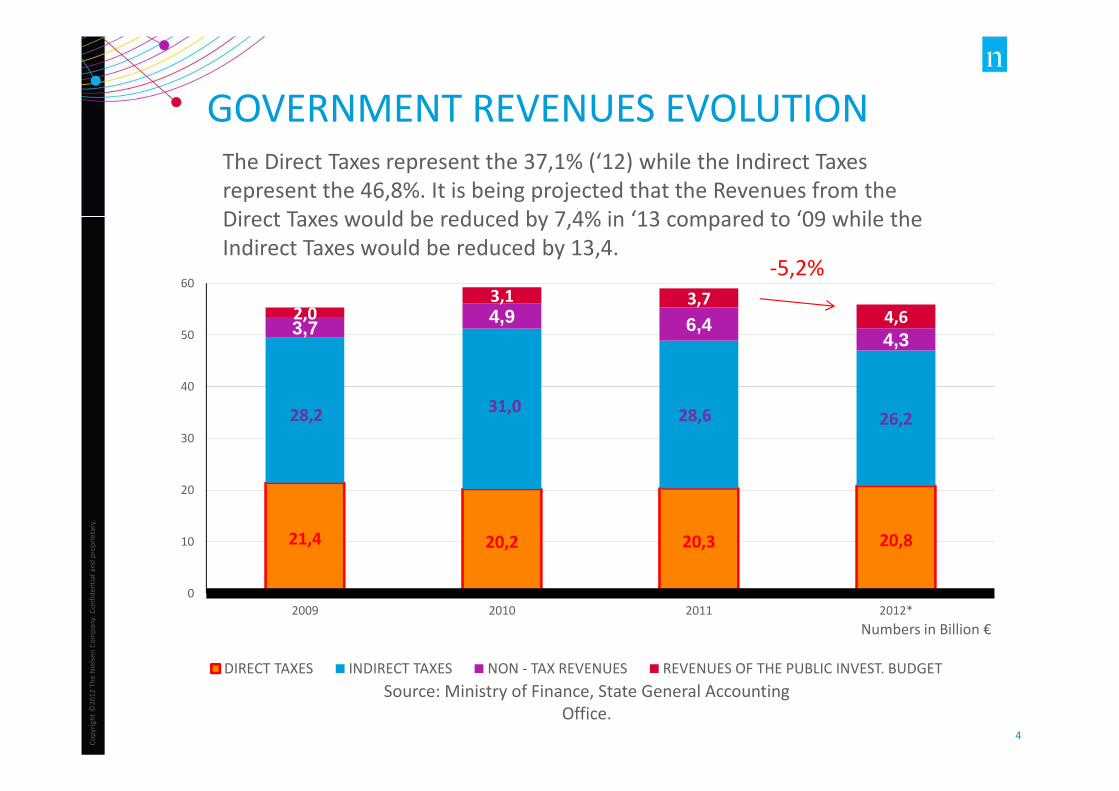

21,4 20,2 20,3 20,8

28,231,0

28,6 26,2

3,74,9 6,4

4,32,0

3,1 3,74,6

0

10

20

30

40

50

60

2009 2010 2011 2012*

DIRECT TAXES INDIRECT TAXES NON - TAX REVENUES REVENUES OF THE PUBLIC INVEST. BUDGET

Numbers in Billion €

Source: Ministry of Finance, State General Accounting

Office.

-5,2%

GOVERNMENT REVENUES EVOLUTIONThe Direct Taxes represent the 37,1% (‘12) while the Indirect Taxes

represent the 46,8%. It is being projected that the Revenues from the

Direct Taxes would be reduced by 7,4% in ‘13 compared to ‘09 while the

Indirect Taxes would be reduced by 13,4.

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

5

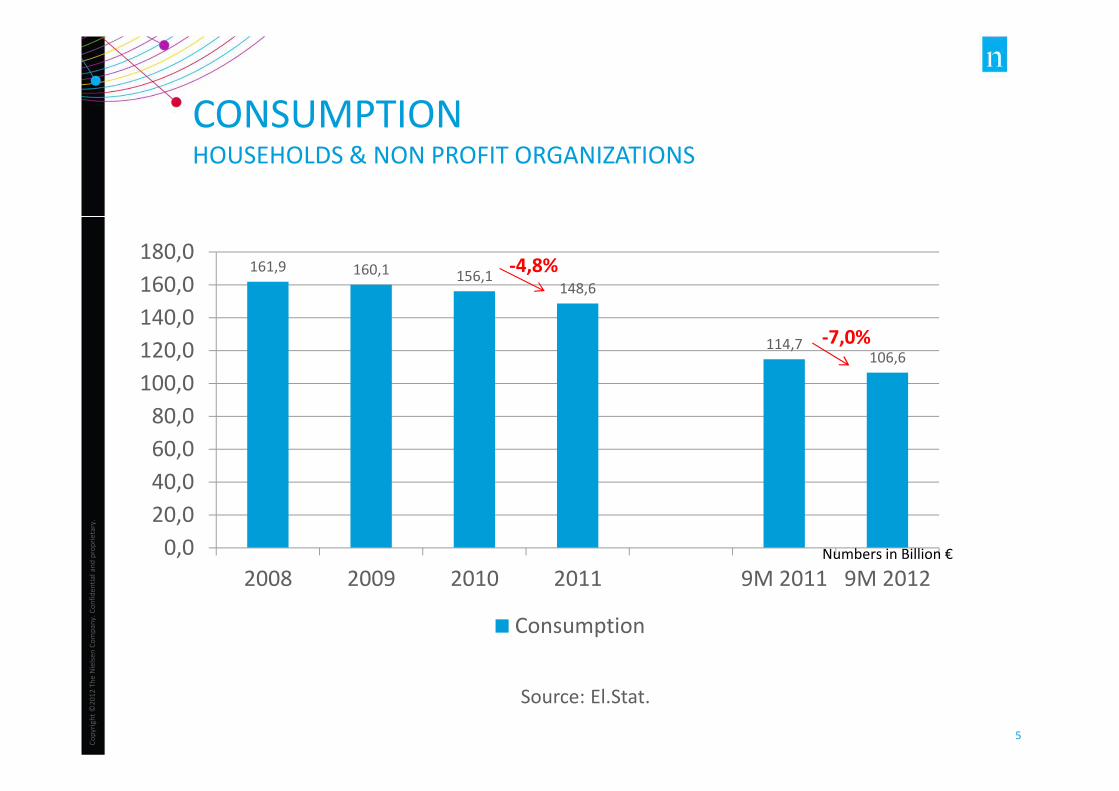

161,9 160,1 156,1148,6

114,7106,6

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

180,0

2008 2009 2010 2011 9M 2011 9M 2012

Consumption

Numbers in Billion €

CONSUMPTIONHOUSEHOLDS & NON PROFIT ORGANIZATIONS

Source: El.Stat.

-4,8%

-7,0%

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

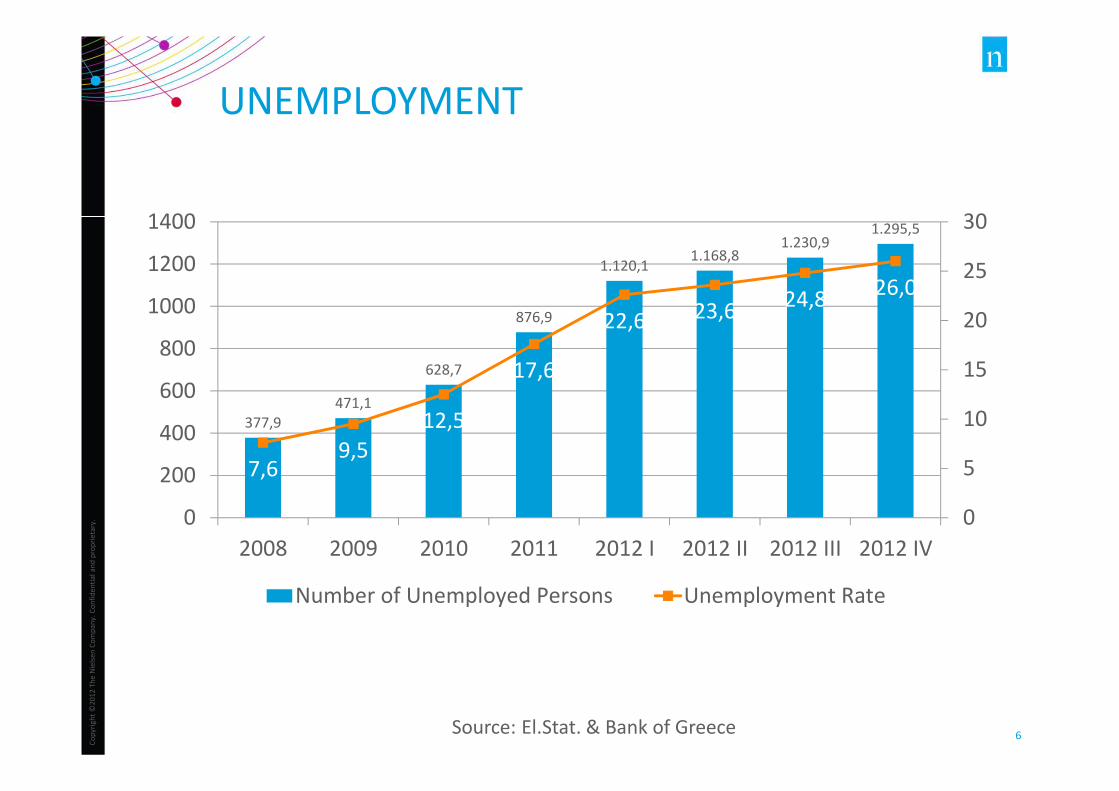

6

377,9

471,1

628,7

876,9

1.120,11.168,8

1.230,91.295,5

7,69,5

12,5

17,6

22,6 23,624,8

26,0

0

5

10

15

20

25

30

0

200

400

600

800

1000

1200

1400

2008 2009 2010 2011 2012 I 2012 II 2012 III 2012 IV

Number of Unemployed Persons Unemployment Rate

UNEMPLOYMENT

Source: El.Stat. & Bank of Greece

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

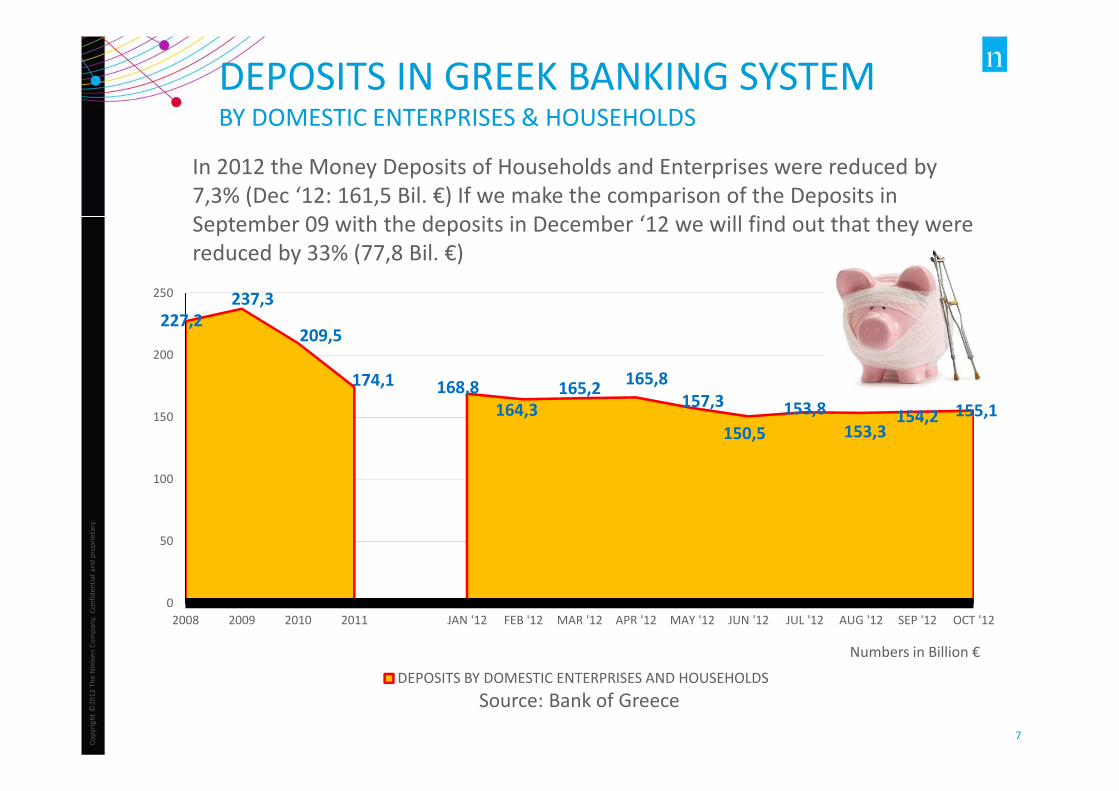

7

227,2

237,3

209,5

174,1 168,8

164,3

165,2165,8

157,3

150,5

153,8

153,3154,2 155,1

0

50

100

150

200

250

2008 2009 2010 2011 JAN '12 FEB '12 MAR '12 APR '12 MAY '12 JUN '12 JUL '12 AUG '12 SEP '12 OCT '12

DEPOSITS BY DOMESTIC ENTERPRISES AND HOUSEHOLDS

Numbers in Billion €

Source: Bank of Greece

DEPOSITS IN GREEK BANKING SYSTEMBY DOMESTIC ENTERPRISES & HOUSEHOLDS

In 2012 the Money Deposits of Households and Enterprises were reduced by

7,3% (Dec ‘12: 161,5 Bil. €) If we make the comparison of the Deposits in

September 09 with the deposits in December ‘12 we will find out that they were

reduced by 33% (77,8 Bil. €)

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

8

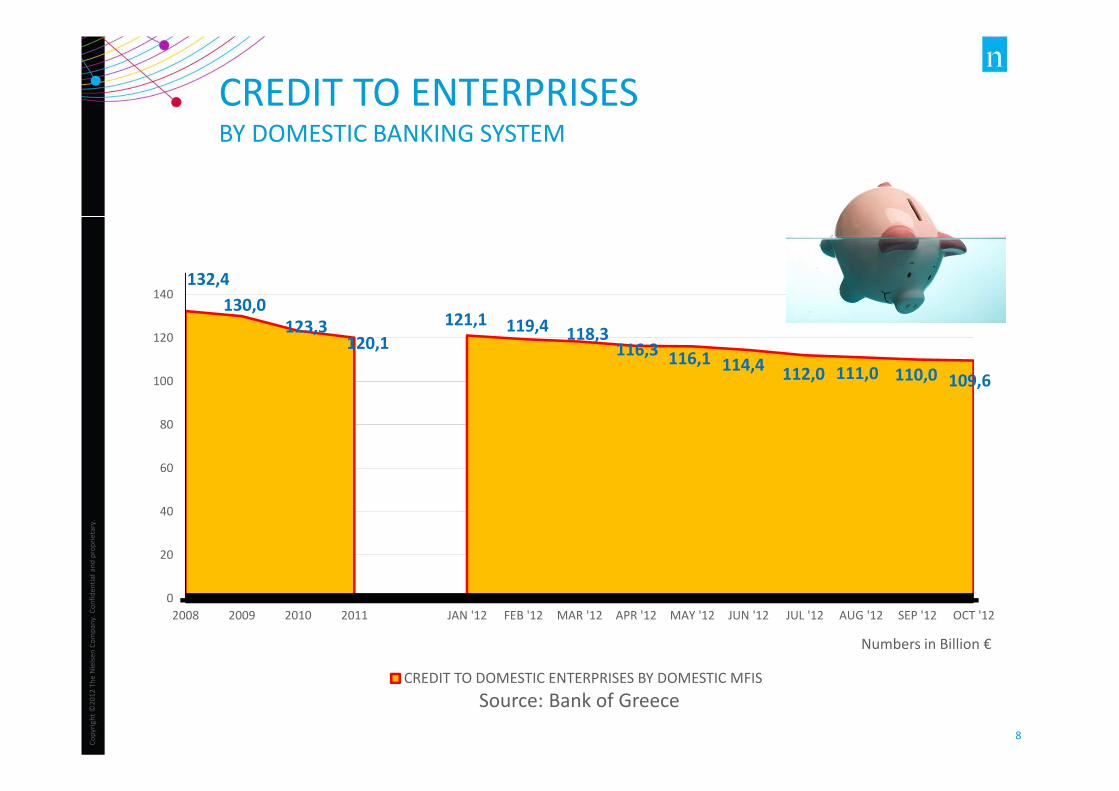

132,4

130,0

123,3120,1

121,1 119,4 118,3116,3

116,1 114,4112,0 111,0 110,0 109,6

0

20

40

60

80

100

120

140

2008 2009 2010 2011 JAN '12 FEB '12 MAR '12 APR '12 MAY '12 JUN '12 JUL '12 AUG '12 SEP '12 OCT '12

CREDIT TO DOMESTIC ENTERPRISES BY DOMESTIC MFIS

Numbers in Billion €

CREDIT TO ENTERPRISES BY DOMESTIC BANKING SYSTEM

Source: Bank of Greece

CONSUMER CONFIDENCE

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

10

Πηγή: Nielsen Global Consumer Confidence Survey

100

8682

7370

57

43 46

35374141

514845

57

7279

3Q

2006

1Q

2007

3Q

2007

1Q

2008

3Q

2008

1Q

2009

3Q

2009

1Q

2010

3Q

2010

4Q

2010

1Q

2011

2Q

2011

3Q

2011

4Q

2011

1Q

2012

2Q

2012

3Q

2012

4Q

2012

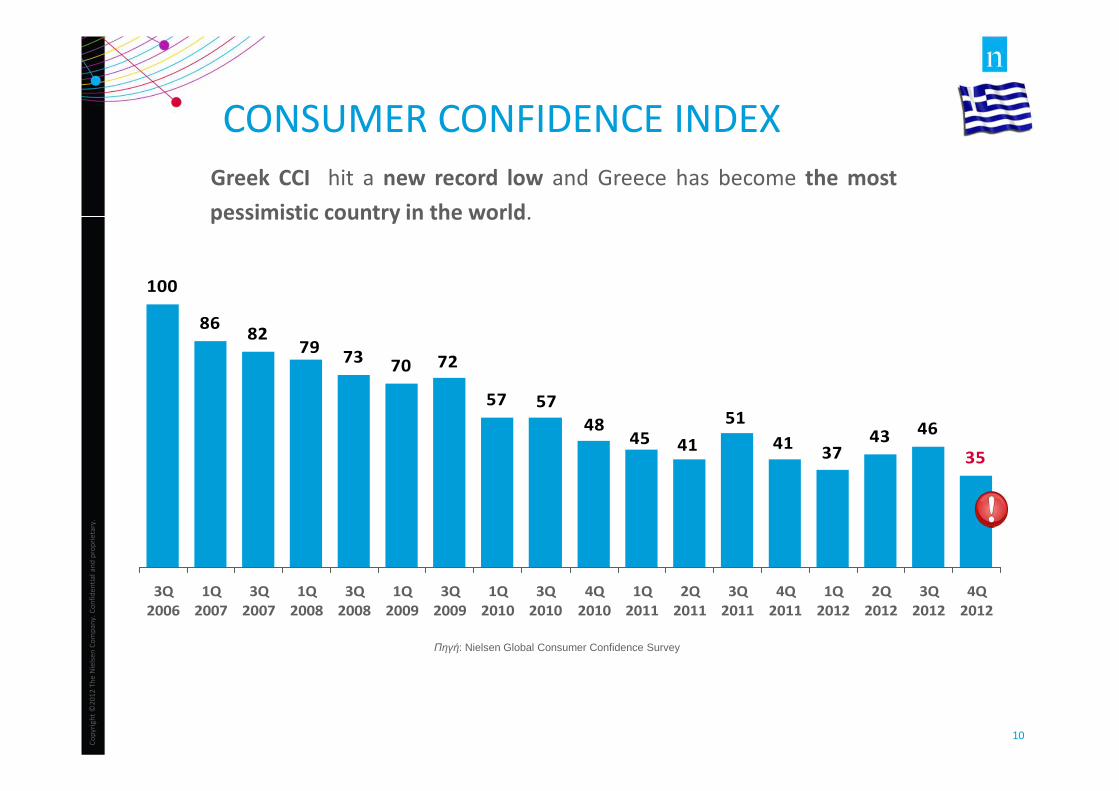

CONSUMER CONFIDENCE INDEX

Greek CCI hit a new record low and Greece has become the most

pessimistic country in the world.

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

11

Source: Q4 , 2012 Nielsen Global Consumer Confidence Survey

71

5141 37

43 4635

717372717474737570 7683

78 78 78

41

79

73 70 72

57 5748 45

Q12008

Q32008

Q12009

Q32009

Q12010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Europe Greece

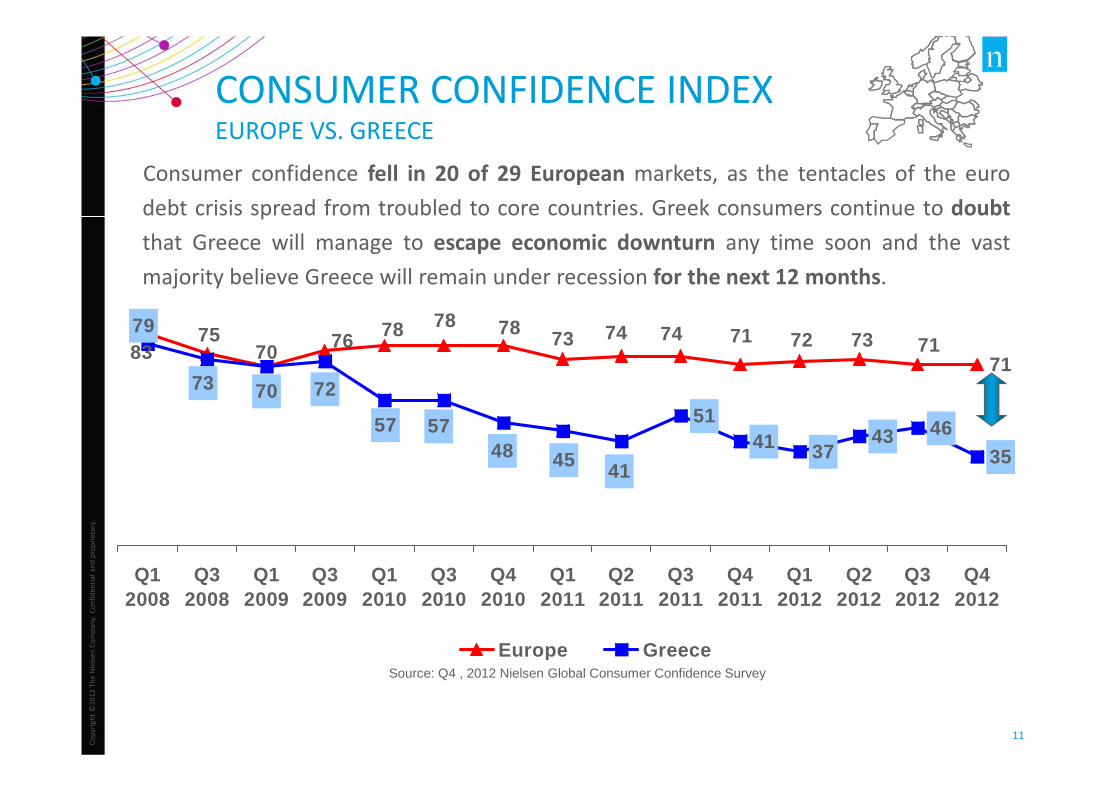

CONSUMER CONFIDENCE INDEX EUROPE VS. GREECE

Consumer confidence fell in 20 of 29 European markets, as the tentacles of the euro

debt crisis spread from troubled to core countries. Greek consumers continue to doubt

that Greece will manage to escape economic downturn any time soon and the vast

majority believe Greece will remain under recession for the next 12 months.

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

12

27

21

17

5

6

4

6

5

2

3

1

1

17

17

9

16

6

7

4

2

4

2

4

3

7

4

5

5

6

10

21

12

11

26

38

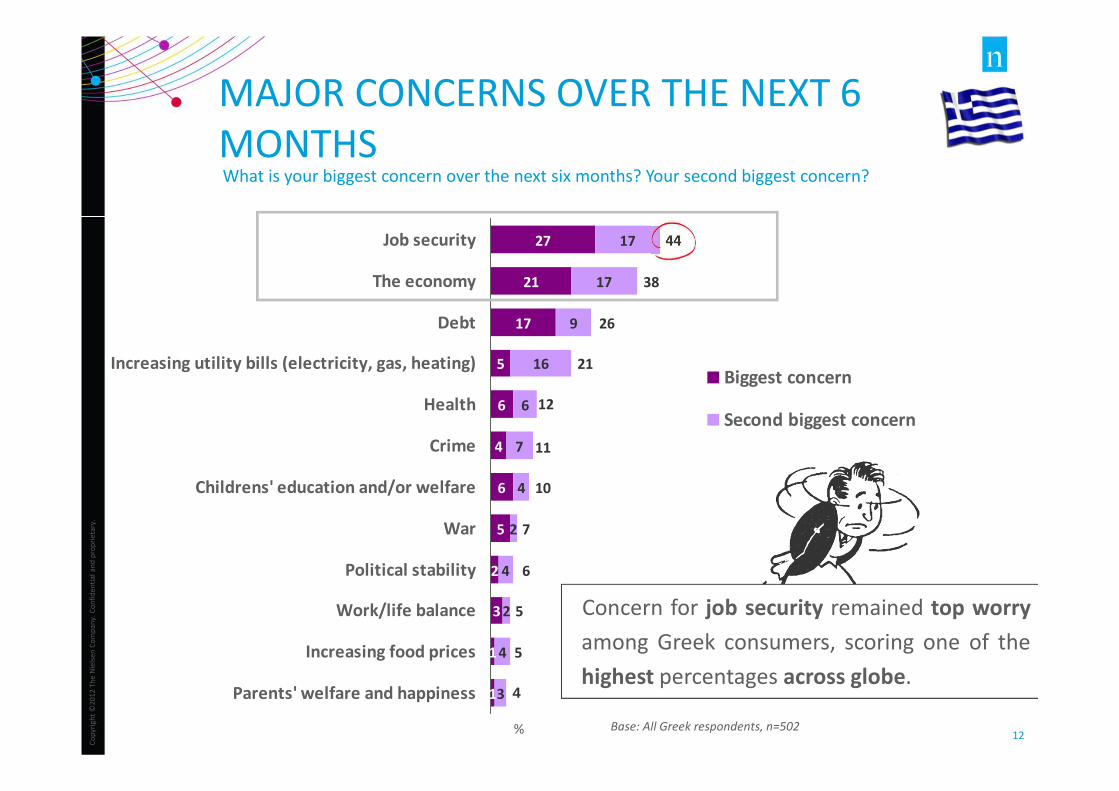

44Job security

The economy

Debt

Increasing utility bills (electricity, gas, heating)

Health

Crime

Childrens' education and/or welfare

War

Political stability

Work/life balance

Increasing food prices

Parents' welfare and happiness

Biggest concern

Second biggest concern

MAJOR CONCERNS OVER THE NEXT 6

MONTHS

Base: All Greek respondents, n=502%

What is your biggest concern over the next six months? Your second biggest concern?

Concern for job security remained top worry

among Greek consumers, scoring one of the

highest percentages across globe.

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

13

UTILIZATION OF SPARE CASH

31%

22%

14%

10%

9%

9%

7%

3%

2%

41%

34%

20%

20%

13%

15%

16%

9%

4%

5%

34%

34%

25%

25%

16%

28%

21%

13%

5%

5%

25%

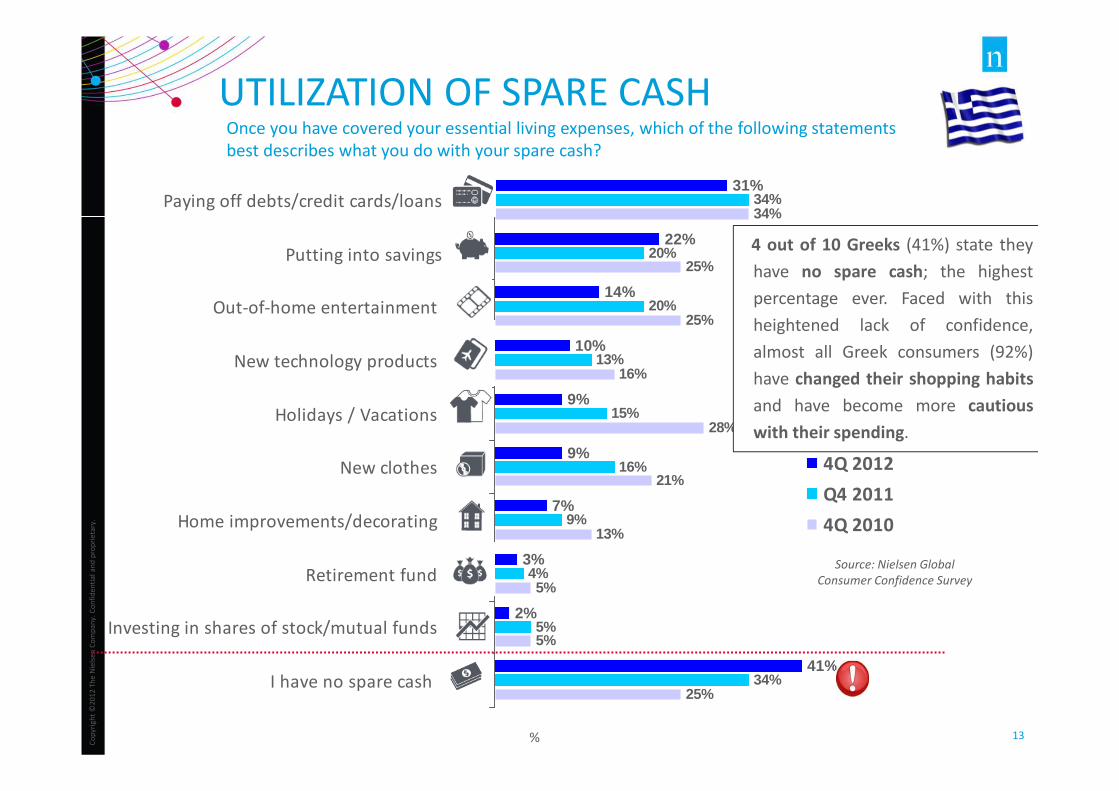

Paying off debts/credit cards/loans

Putting into savings

Out-of-home entertainment

New technology products

Holidays / Vacations

New clothes

Home improvements/decorating

Retirement fund

Investing in shares of stock/mutual funds

I have no spare cash

4Q 2012

Q4 2011

4Q 2010

Source: Nielsen Global

Consumer Confidence Survey

%

Once you have covered your essential living expenses, which of the following statements

best describes what you do with your spare cash?

4 out of 10 Greeks (41%) state they

have no spare cash; the highest

percentage ever. Faced with this

heightened lack of confidence,

almost all Greek consumers (92%)

have changed their shopping habits

and have become more cautious

with their spending.

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

14

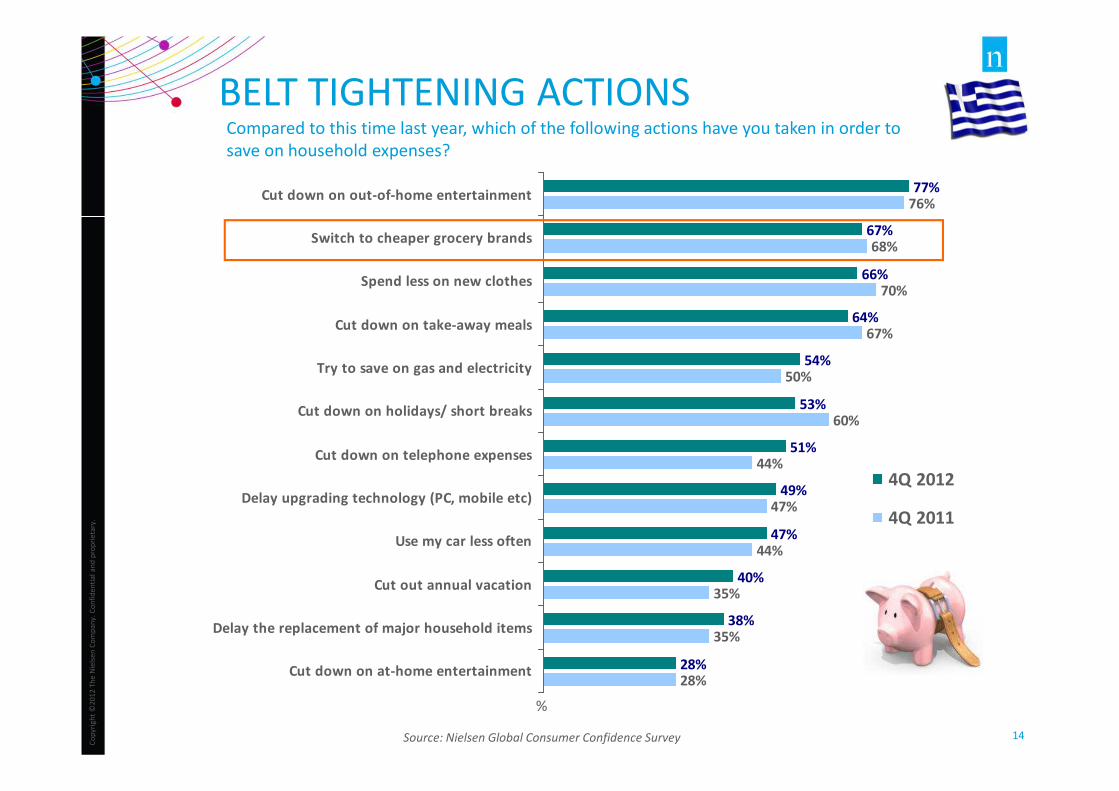

BELT TIGHTENING ACTIONS

77%

67%

66%

64%

54%

53%

51%

49%

47%

40%

38%

28%

76%

68%

70%

67%

50%

60%

44%

47%

44%

35%

35%

28%

Cut down on out-of-home entertainment

Switch to cheaper grocery brands

Spend less on new clothes

Cut down on take-away meals

Try to save on gas and electricity

Cut down on holidays/ short breaks

Cut down on telephone expenses

Delay upgrading technology (PC, mobile etc)

Use my car less often

Cut out annual vacation

Delay the replacement of major household items

Cut down on at-home entertainment

4Q 2012

4Q 2011

Source: Nielsen Global Consumer Confidence Survey

%

Compared to this time last year, which of the following actions have you taken in order to

save on household expenses?

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

15

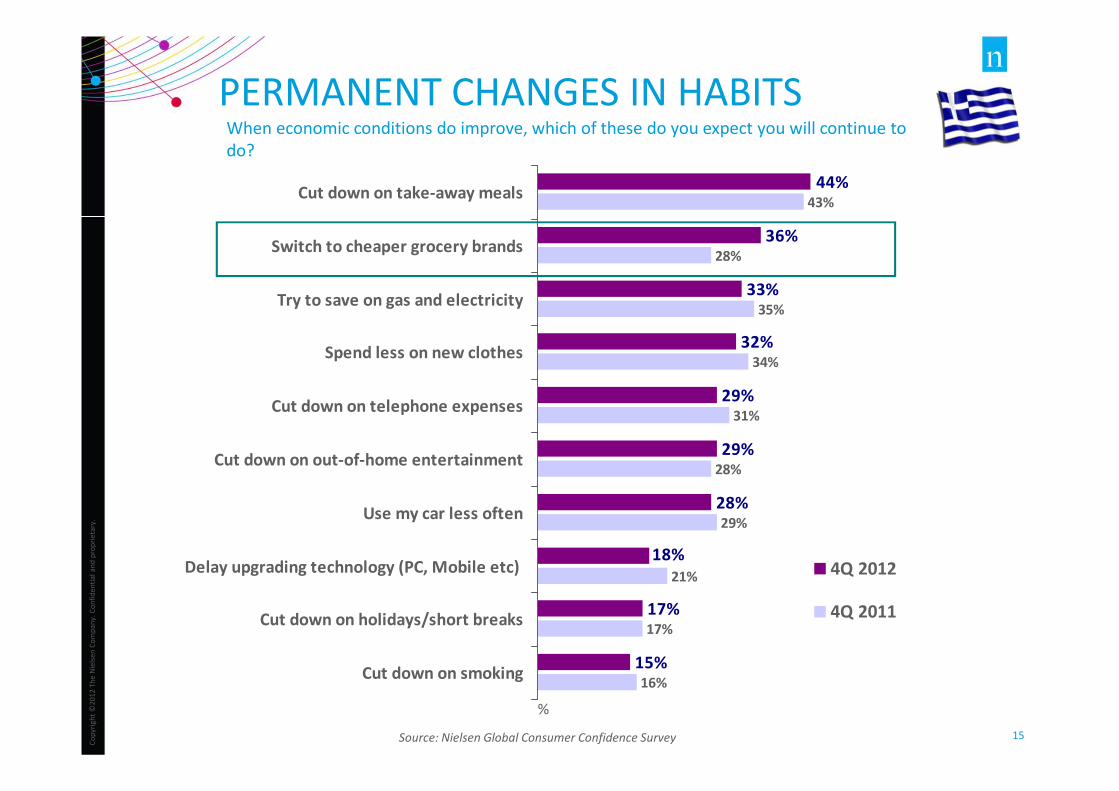

PERMANENT CHANGES IN HABITSWhen economic conditions do improve, which of these do you expect you will continue to

do?

36%

33%

32%

29%

29%

28%

17%

15%

43%

28%

35%

34%

31%

28%

29%

21%

17%

16%

44%

18%

Cut down on take-away meals

Switch to cheaper grocery brands

Try to save on gas and electricity

Spend less on new clothes

Cut down on telephone expenses

Cut down on out-of-home entertainment

Use my car less often

Delay upgrading technology (PC, Mobile etc)

Cut down on holidays/short breaks

Cut down on smoking

4Q 2012

4Q 2011

Source: Nielsen Global Consumer Confidence Survey

%

RETAIL MARKET & GROWTH REPORTER

ANALYSIS

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

17

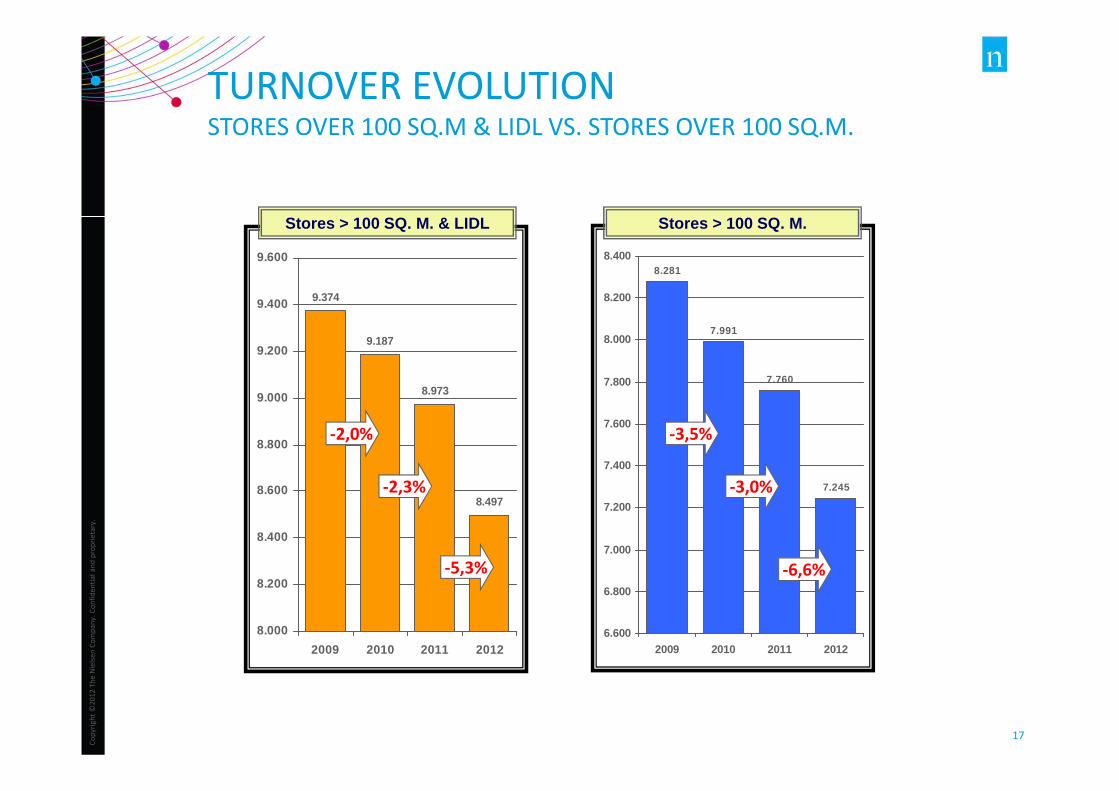

8.281

7.991

7.760

7.245

6.600

6.800

7.000

7.200

7.400

7.600

7.800

8.000

8.200

8.400

2009 2010 2011 2012

TURNOVER EVOLUTIONSTORES OVER 100 SQ.M & LIDL VS. STORES OVER 100 SQ.M.

9.374

9.187

8.973

8.497

8.000

8.200

8.400

8.600

8.800

9.000

9.200

9.400

9.600

2009 2010 2011 2012

-2,3%

-5,3%

-3,0%

-6,6%

Stores > 100 SQ. M. & LIDL Stores > 100 SQ. M.

-2,0% -3,5%

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

18

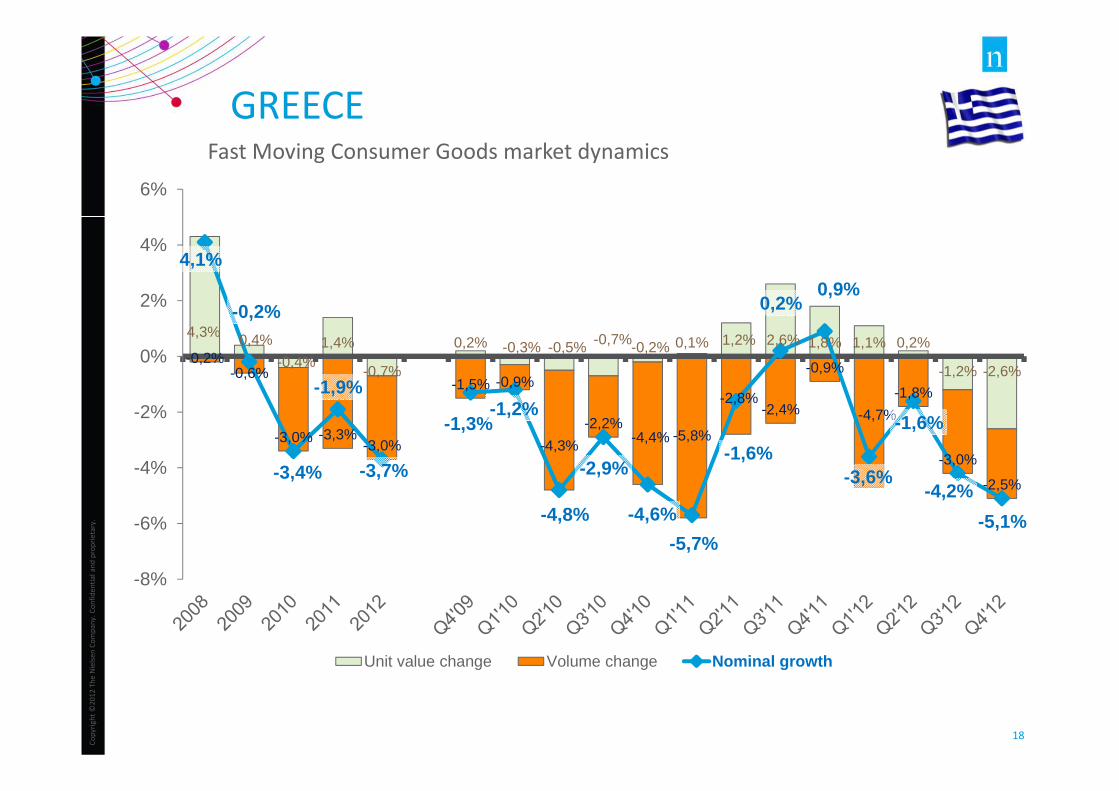

GREECEFast Moving Consumer Goods market dynamics

4,3% 0,4%

-0,4%1,4%

-0,7%

0,2% -0,3% -0,5% -0,7%-0,2% 0,1% 1,2% 2,6% 1,8% 1,1% 0,2%

-1,2% -2,6%-0,2%

-0,6%

-3,0% -3,3%-3,0%

-1,5% -0,9%

-4,3%

-2,2%-4,4% -5,8%

-2,8%-2,4%

-0,9%

-4,7%

-1,8%

-3,0%

-2,5%

4,1%

-0,2%

-3,4%

-1,9%

-3,7%

-1,3%-1,2%

-4,8%

-2,9%

-4,6%

-5,7%

-1,6%

0,2%0,9%

-3,6%

-1,6%

-4,2%

-5,1%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Unit value change Volume change Nominal growth

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

19

GROWTH RATES PER COUNTRY 2012Fast Moving Consumer Goods market dynamics

-3,7%

-0,6%

0,1% 0,8% 0,9%

1,1%

1,7% 2,0% 2,2% 2,4% 2,5% 2,5% 2,6%3,3% 3,4%

3,9% 4,0%

5,4%5,9%

6,7%

10,8%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

Unit value change Volume change Nominal growth

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

20

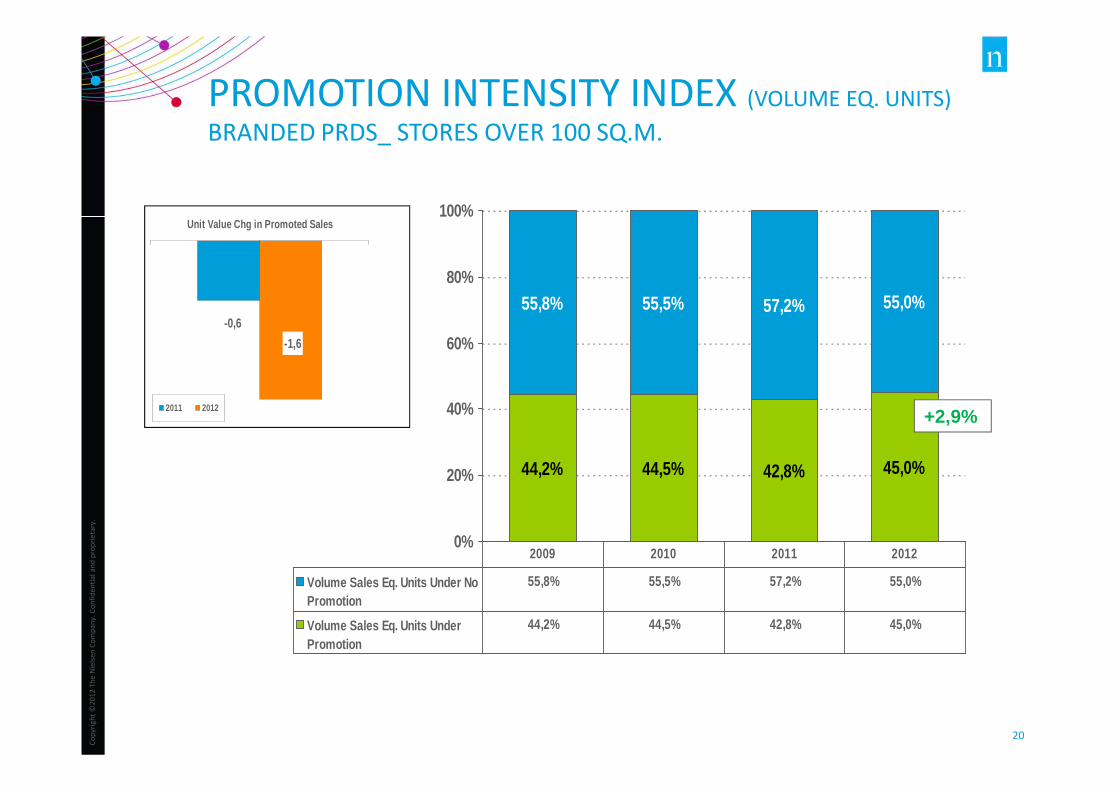

PROMOTION INTENSITY INDEX (VOLUME EQ. UNITS)

BRANDED PRDS_ STORES OVER 100 SQ.M.

44,2% 44,5% 42,8% 45,0%

55,8% 55,5% 57,2% 55,0%

0%

20%

40%

60%

80%

100%

Volume Sales Eq. Units Under NoPromotion

55,8% 55,5% 57,2% 55,0%

Volume Sales Eq. Units UnderPromotion

44,2% 44,5% 42,8% 45,0%

2009 2010 2011 2012

+2,9%

-0,6

-1,6

Unit Value Chg in Promoted Sales

2011 2012

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

21

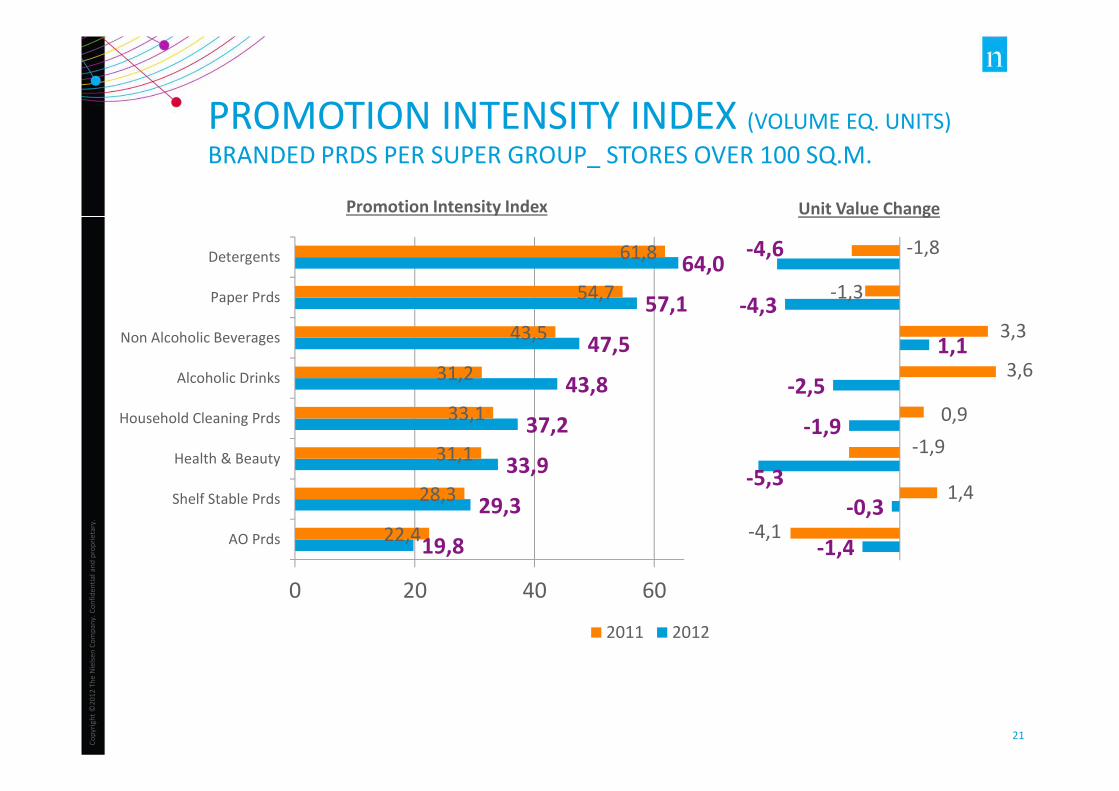

19,8

29,3

33,9

37,2

43,8

47,5

57,1

64,0

22,4

28,3

31,1

33,1

31,2

43,5

54,7

61,8

0 20 40 60

AO Prds

Shelf Stable Prds

Health & Beauty

Household Cleaning Prds

Alcoholic Drinks

Non Alcoholic Beverages

Paper Prds

Detergents

2011 2012

-1,4

-0,3

-5,3

-1,9

-2,5

1,1

-4,3

-4,6

-4,1

1,4

-1,9

0,9

3,6

3,3

-1,3

-1,8

PROMOTION INTENSITY INDEX (VOLUME EQ. UNITS)

BRANDED PRDS PER SUPER GROUP_ STORES OVER 100 SQ.M.

Unit Value ChangePromotion Intensity Index

Co

py

rig

ht

©2

01

2 T

he

Nie

lse

n C

om

pa

ny

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry.

22

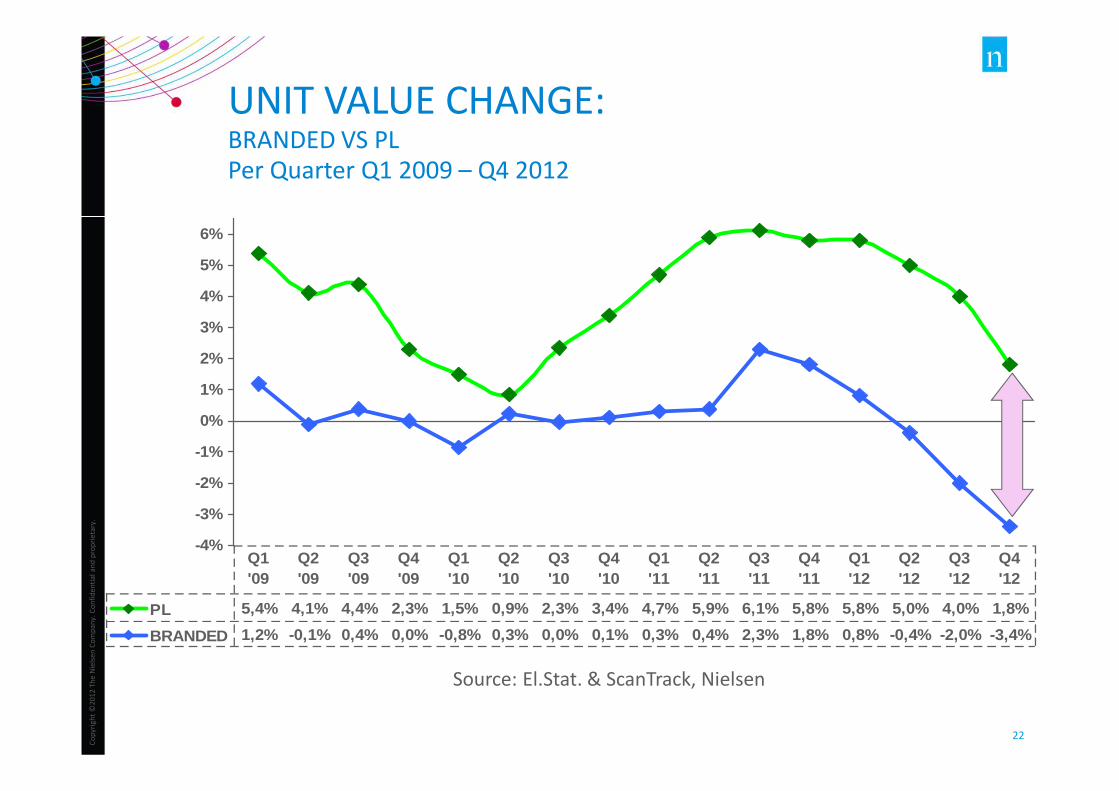

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

PL 5,4% 4,1% 4,4% 2,3% 1,5% 0,9% 2,3% 3,4% 4,7% 5,9% 6,1% 5,8% 5,8% 5,0% 4,0% 1,8%

BRANDED 1,2% -0,1% 0,4% 0,0% -0,8% 0,3% 0,0% 0,1% 0,3% 0,4% 2,3% 1,8% 0,8% -0,4% -2,0% -3,4%

Q1 '09

Q2 '09

Q3 '09

Q4 '09

Q1 '10

Q2 '10

Q3 '10

Q4 '10

Q1 '11

Q2 '11

Q3 '11

Q4 '11

Q1 '12

Q2 '12

Q3 '12

Q4 '12

Source: El.Stat. & ScanTrack, Nielsen

UNIT VALUE CHANGE: BRANDED VS PL

Per Quarter Q1 2009 – Q4 2012

THANK YOU!

For more information please contact:

Alexandros Floros

Retailer Services Manager

Nielsen Greece, Bulgaria, Cyprus

� +210 9500516

Recommended