CCXI’s ratings reflect the expected loss severity of senior notes, and the possibility of timely payment of invest and fully payment of principal on or before legal maturity. This report does not constitute a solicitation of an offer to buy any securities.

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

www.ccxi.com.cn

Volkswagen Finance

(China) Co., Ltd.

Asset Backed Notes Rating Report

for Driver China seven Auto Loan ABS

R

Report date

Sep. 18th

, 2017

Analysts

Xiaoyu Wang [email protected]

Kai Kang [email protected] Jingwen Yuan [email protected]

This report is for VWFC’s and investors' reference only. In case there is any divergence between this report and the Chinese version report, the Chinese report shall prevail.

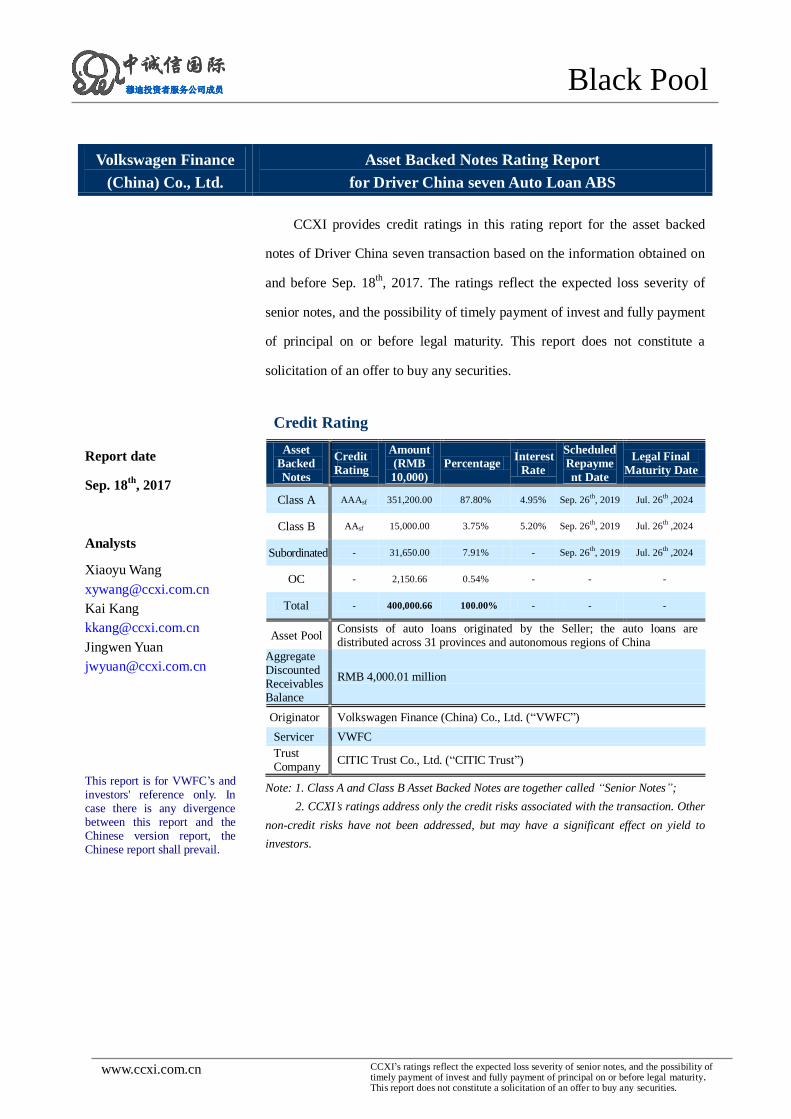

CCXI provides credit ratings in this rating report for the asset backed

notes of Driver China seven transaction based on the information obtained on

and before Sep. 18th

, 2017. The ratings reflect the expected loss severity of

senior notes, and the possibility of timely payment of invest and fully payment

of principal on or before legal maturity. This report does not constitute a

solicitation of an offer to buy any securities.

Credit Rating

Asset

Backed

Notes

Credit

Rating

Amount

(RMB

10,000)

Percentage Interest

Rate

Scheduled

Repayme

nt Date

Legal Final

Maturity Date

Class A AAAsf 351,200.00 87.80% 4.95% Sep. 26th

, 2019 Jul. 26th

,2024

Class B AAsf 15,000.00 3.75% 5.20% Sep. 26th

, 2019 Jul. 26th

,2024

Subordinated - 31,650.00 7.91% - Sep. 26th

, 2019 Jul. 26th

,2024

OC - 2,150.66 0.54% - - -

Total - 400,000.66 100.00% - - -

Asset Pool Consists of auto loans originated by the Seller; the auto loans are distributed across 31 provinces and autonomous regions of China

Aggregate Discounted Receivables Balance

RMB 4,000.01 million

Originator Volkswagen Finance (China) Co., Ltd. (“VWFC”)

Servicer VWFC

Trust Company

CITIC Trust Co., Ltd. (“CITIC Trust”)

Note: 1. Class A and Class B Asset Backed Notes are together called “Senior Notes”;

2. CCXI’s ratings address only the credit risks associated with the transaction. Other

non-credit risks have not been addressed, but may have a significant effect on yield to

investors.

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

2 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

Rating Opinion

Strengths

The payment of interest and principal adopts the senior/subordinate payment system. Class A

Notes benefit from 12.20% of credit enhancement provided by Class B Notes, Subordinated

Notes and Overcollateralisation; Class B Notes benefit from 8.45% of credit enhancement

provided by Subordinated Notes and Overcollateralisation.

The transaction benefits from 0.54% of credit enhancement provided by initial

Overcollateralisation.

Loans in the securitized portfolio are all auto loans originated by VWFC. Aggregate

outstanding discounted receivables balance is RMB 4,000,006,554.35. Total number of

borrowers in the pool is 67,402. Average outstanding discounted receivables balance per

borrower is RMB 59,345.52 and the maximum outstanding discounted receivables balance

from a single borrower is about RMB 2.26 million. The pool benefits from its granular

composition.

All loans in the pool are “Normal” category of loans based on CBRC’s five-grade loan

classification standard as of the Cut-off Date. The average seasoning of loans is 6.88 months

while the shortest is 2 months. The underlying assets are in good quality and their credit

performance is decent.

All the loans in the pool are fixed interest rate loans. The transaction is hence not subject to

interest risks.

The Originator and Servicer is VWFC, a wholly-owned subsidiary of Volkswagen Financial

Services (“VWFS”). Thanks to the extensive experience of VWFS in automobile finance

management and operations, VWFC is highly competitive in serving its dealers and

individual customers. Since establishment, the company has recorded high growth and

established strong risk control capabilities. As of December 31st, 2016, the NPL ratio of the

company was 0.14%. In addition, VWFS has gained securitization experience over the last 20

years with a good number of well performing ABS transactions in Germany, UK, France, the

Netherlands, Spain, Japan, Australia, Brazil and China. VWFS will provide strong support to

VWFC in this transaction.

This transaction is a static pool transaction. Hence there is no additional loss probability

arising from replenishing portfolio.

Concerns and Mitigants

Due to the limitation of business development and information systems, VWFC only

provides the historical data from Aug. 2010 onwards which is relatively short. Although part

of the historical data has experienced a complete life cycle, it does not reflect a complete

economic cycle. As such, the historical performance plays a limited role in forecasting the

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

3 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

future performance of the asset pool.

Mitigant: We made appropriate adjustments to the results of historical data analysis based on

macro-economic conditions, industrial developments and the business developments of the

Originator, in order to forecast the future credit performance of the asset pool. In our credit

analysis, we have fully factored in the limitation of historical data and the impact of future

economic movements on the asset pool.

The underlying assets are auto loans. According to relevant arrangement, the underlying

assets are transferred to the trust, but the mortgage registration will not be updated.

Meanwhile, among the assets in the pool, there are loans in relation to which the mortgage

has not been registered. As a result of the foregoing, the mortgage may not be upheld against

bona fide third party. This may impose certain negative impact on the trust interests.

Mitigant: In analyzing the recovery of default assets, we have considered the potential impact

of the lack of registration or re-registration for the security interest over collateral rights.

Before Foreclosure Event is triggered, and after the tax bore by trust company is paid, the

order of cash flow allocation is first to pay for the interest payable for Senior Notes, and then

pay for the principal of Senior Notes until the Targeted Overcollateralisation Amount is

reached, and the remaining cash flow is allocated to pay for the interest and principal of

Subordinated Notes until the outstanding principal amounts of Subordinated Notes after

repayment is no less than 5% of the then outstanding principal amount of the Notes. As such,

Subordinated Notes might receive principal payment before Senior Notes are fully paid down.

Under extreme situation (for example, extremely high prepayment rate scenario),

Subordinated Notes might be rapid paid, so the remain Subordinated Notes may not support

Senior Notes completely.

Mitigant: We have fully-factored in the impact of cash flow Order of Priority in relation to the

repayment of different classes of notes, and we have simulated the principal repayment and

potential loss of different classes of notes under different cash flow scenarios. We believe

Class A and Class B Notes could achieve AAAsf and AAsf rating respectively as stated in the

tranching in this report.

In the asset pool, there are two types of loans that allow borrowers to extend loan tenor when

they are due (Note that it is an option built in the original loan contract) except new car credit

and used car credit. Such loans account for 1.26% of the outstanding discounted receivables

balance of the asset pool as of Cut-Off Date. The uncertainties pertaining to the actual

maturity of such loans may affect the cash flow of the asset pool.

Mitigant: We have simulated different scenarios of cash flow Order of Priority when these

three types of loans are due, and fully-factored in the impact of tenor extension on the asset

pool.

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

4 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

Rating opinion and consideration

CCXI grants provisional ratings of AAAsf and AAsf to Class A Notes and Class B Notes under

the “Driver China seven Auto Loan ABS”.

Such provisional ratings are based on:

Robustness of the legal structure of the transaction and underlying assets;

Credit quality of the asset pool;

Credit support provided by the senior/subordinate mechanism;

Structural features of the transaction which include the Order of Priority, the switch of the

Order of Priority following Foreclosure Events, the pre-funded Cash Collateral Account and

Monthly Collateral Account, etc;

Credit profile of VWFC and its experience as a Servicer.

Monitoring

CCXI will monitor the ratings while Senior Notes are outstanding. On-going review will be

conducted on the performance of the underlying assets and the credit quality of the Servicer, the

Trustee and the Fund Custodian. CCXI will publish the tracking report every year before 31th

July from the second year of issuance, and provide prompt notice to the Trustee and publicly

announce any changes in the ratings on CCXI’s website.

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

5 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

Transaction Overview

Transaction summary

Trust company CITIC Trust

Type of structure Static cash flow auto loan ABS

Cut-off Date Aug. 31th ,2017

Closing Date Sep. 21th , 2017

Frequency of interest payment Monthly

Frequency of principal payment Monthly

Legal Maturity Date Jul. 26th,2024

Servicer VWFC

Account Bank China Construction Bank Corporation Beijing Branch (“CCB Beijing Branch”),

Originator VWFC

Lead Underwriter CITIC Securities Co., Ltd.

Joint Lead Underwriters Standard Chartered Bank (China) Limited / Bank of China Limited

Registry/Paying Agent China Central Depository and Clearing Co., ltd(“CCDC”)

Asset pool and characteristics of pooled assets (At Cut-off Date)1

Discounted Principal balance of the asset pool RMB 4,000,006,554.35

Initial loan size of the asset pool RMB 5,817,582,887.25

Number of borrowers 67,402

Number of loans 68,331

Highest principal balance of single loan RMB 2,257,877.05

Average outstanding discounted receivables balance of single loan RMB 58,538.68

Average outstanding discounted receivables balance of single borrower RMB 59,345.52

Lowest/highest interest rate of loans 0%2/15.72%

Weighted average interest rate of loans 1.85%

Shortest/longest tenor of loans 12 months/60 months

Shortest/longest remaining time to maturity of loans 6 months/58 months

Weighted average remaining time to maturity of loans 22.78 months

Age range of Borrowers 18~86

Geographic distribution of Borrowers borrowers widely distributed in 31 provinces and

autonomous regions of China

Weighted average initial collateralization rate 56.09%

Asset Backed Notes

Asset Backed Notes Proportion of amount Interest

Rate Credit Enhancement

Class A 87.80% 4.95% Class A Notes receive 12.20% of credit enhancement from Class B Notes, Subordinated Notes and Overcollateralisation

Class B 3.75% 5.20% Class B Notes receive 8.45% of credit enhancement from Subordinated Notes and Overcollateralisation

Subordinated Notes 7.91% - -

1 Weighted average data are weighted by outstanding discounted receivables balance 2 Some loans in the pool are loans with interest subsidy, with 0%

interest rate

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

6 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

Overcollateralisation 0.54% - -

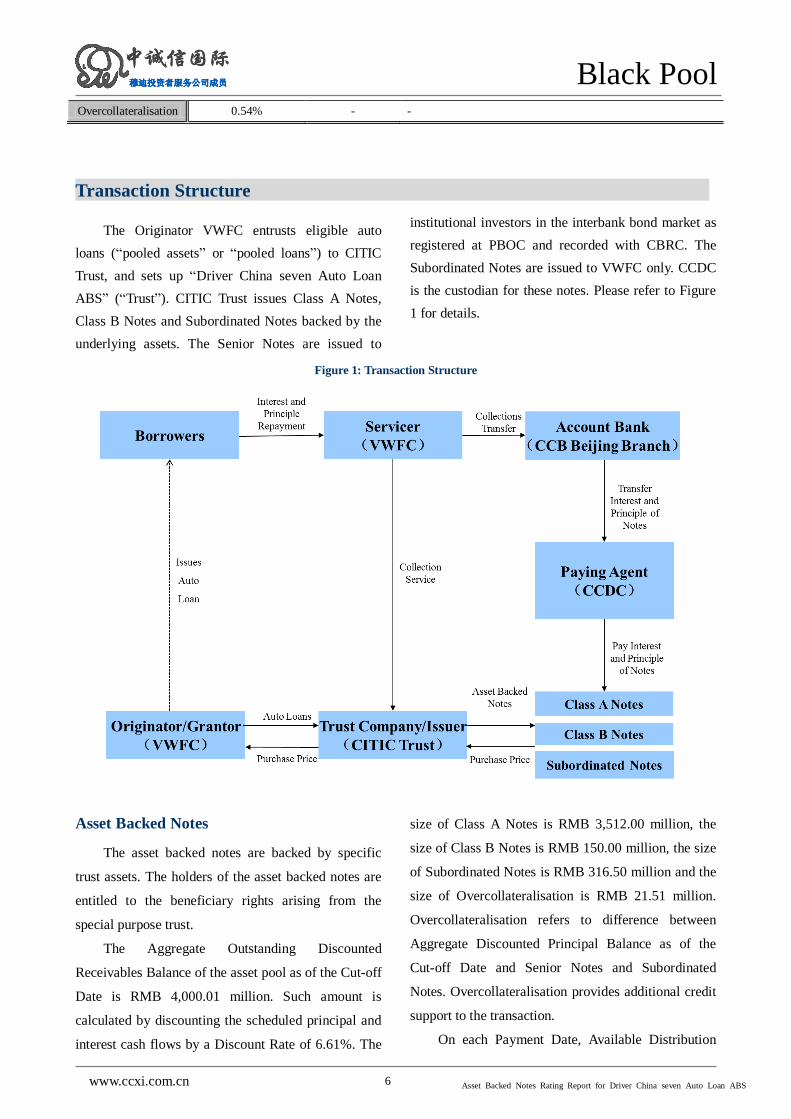

Transaction Structure

The Originator VWFC entrusts eligible auto

loans (“pooled assets” or “pooled loans”) to CITIC

Trust, and sets up “Driver China seven Auto Loan

ABS” (“Trust”). CITIC Trust issues Class A Notes,

Class B Notes and Subordinated Notes backed by the

underlying assets. The Senior Notes are issued to

institutional investors in the interbank bond market as

registered at PBOC and recorded with CBRC. The

Subordinated Notes are issued to VWFC only. CCDC

is the custodian for these notes. Please refer to Figure

1 for details.

Figure 1: Transaction Structure

Asset Backed Notes

The asset backed notes are backed by specific

trust assets. The holders of the asset backed notes are

entitled to the beneficiary rights arising from the

special purpose trust.

The Aggregate Outstanding Discounted

Receivables Balance of the asset pool as of the Cut-off

Date is RMB 4,000.01 million. Such amount is

calculated by discounting the scheduled principal and

interest cash flows by a Discount Rate of 6.61%. The

size of Class A Notes is RMB 3,512.00 million, the

size of Class B Notes is RMB 150.00 million, the size

of Subordinated Notes is RMB 316.50 million and the

size of Overcollateralisation is RMB 21.51 million.

Overcollateralisation refers to difference between

Aggregate Discounted Principal Balance as of the

Cut-off Date and Senior Notes and Subordinated

Notes. Overcollateralisation provides additional credit

support to the transaction.

On each Payment Date, Available Distribution

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

7 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

Amount is allocated according to the Order of Priority.

The cash flow is allocated according to the Order

of Priority. On each Payment Date, the Available

Distribution Amount which at a level equal to the

Specified Cash Collateral Account Balance will first

to replenish the Cash Collateral Account, then to

continuous be distributed follow the payment

mechanism (Please see Cash flow payment

mechanism for details).

Cash flow payment mechanism

On each Account Bank Transfer Date, the

Available Distribution Amount shall be distributed

according to the following Order of Priority:

Order of Priority before the occurrence of a

Foreclosure Event

Prior to the occurrence of a Foreclosure Event

(Please see Appendix 2 for details of Foreclosure

Event), on the preceding day to each Payment Date,

all or a portion of the Available Distribution Amount

shall be deposited to the Cash Collateral Account to

the extent needed to replenish and maintain the credit

balance of the Cash Collateral Account at a level equal

to the Specified Cash Collateral Account Balance and

any balance will, on each Payment Date, be

distributed according to the following Order of

Priority:

first, amounts payable by the Issuer in respect of

taxes (if any) in relation to the Trust;

second, the Servicer Fee payable to the Servicer;

third, on a pari passu basis, (1) the Trust

Company Fee and Expenses payable to the Trust

Company, (2) the Expenses payable to the Servicer (or

replacement Servicer), (3) the Custodian Fee and

Expenses payable to the Account Bank, (4) the Paying

Agent Fee and Expenses payable to the Paying Agent,

(5) the Rating Agencies Fee and Expenses payable to

the Rating Agencies, and (6) the Auditor Fee payable

to the Auditor;

fourth, amounts payable in respect of (1) interest

accrued during the immediately preceding Interest

Period plus (2) Interest Shortfalls (if any) on the Class

A Notes;

fifth, amounts payable in respect of (1) interest

accrued during the immediately preceding Interest

Period plus (2) Interest Shortfalls (if any) on the Class

B Notes;

sixth, to Class A Noteholders, an aggregate

amount equal to the Class A Principal Payment

Amount for such Payment Date which is equal to the

amount necessary to reduce the outstanding principal

amount of the Class A Notes to the Class A Targeted

Note Balance;

seventh, to Class B Noteholders, an aggregate

amount equal to the Class B Principal Payment

Amount for such Payment Date which is equal to the

amount necessary to reduce the outstanding principal

amount of the Class B Notes to the Class B Targeted

Note Balance;

eighth, amounts payable in respect of accrued

and unpaid interest on the Subordinated Notes

(including, without limitation, overdue interest);

ninth, (i) prior to the satisfaction of Clean-Up

Call Conditions or in the case that the Clean-Up Call

Conditions are satisfied but the Originator does not

exercise a Clean-Up Call, to the Subordinated

Noteholders for repayment of outstanding principal

amounts of Subordinated Notes on condition that the

outstanding principal amounts of Subordinated Notes

after repayment is no less than 5% of the then

outstanding principal amount of the Notes; or (ii) after

the satisfaction of Clean-Up Call Conditions and the

Originator choose to exercise a Clean-Up Call, to the

Subordinated Noteholders, for repayment of

outstanding principal amounts of Subordinated Notes

until it has been reduced to zero; and

tenth, to pay all remaining excess to the

Originator by way of final success fee.

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

8 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

Cash flow payment adjustment before the occurrence

of a Foreclosure Event

Before the occurrence of a Foreclosure Event, the

repayment of principal for Senior Notes each time

shall be made until the aggregate principal amount of

the notes reduced to its targeted balance. If the

Aggregate Principal Balance as at the end of the

preceding Monthly Period is less than 10 percent of

the Aggregate Cut-off Date Discounted Receivables

Balance or if a Servicer Replacement Event occurs,

the targeted balance of Senior Notes is zero.

Otherwise, the targeted balance of Senior A Notes is

an amount equal to the excess of the Aggregate

Discounted Receivables Balance as at the end of the

preceding Monthly Period over the Targeted

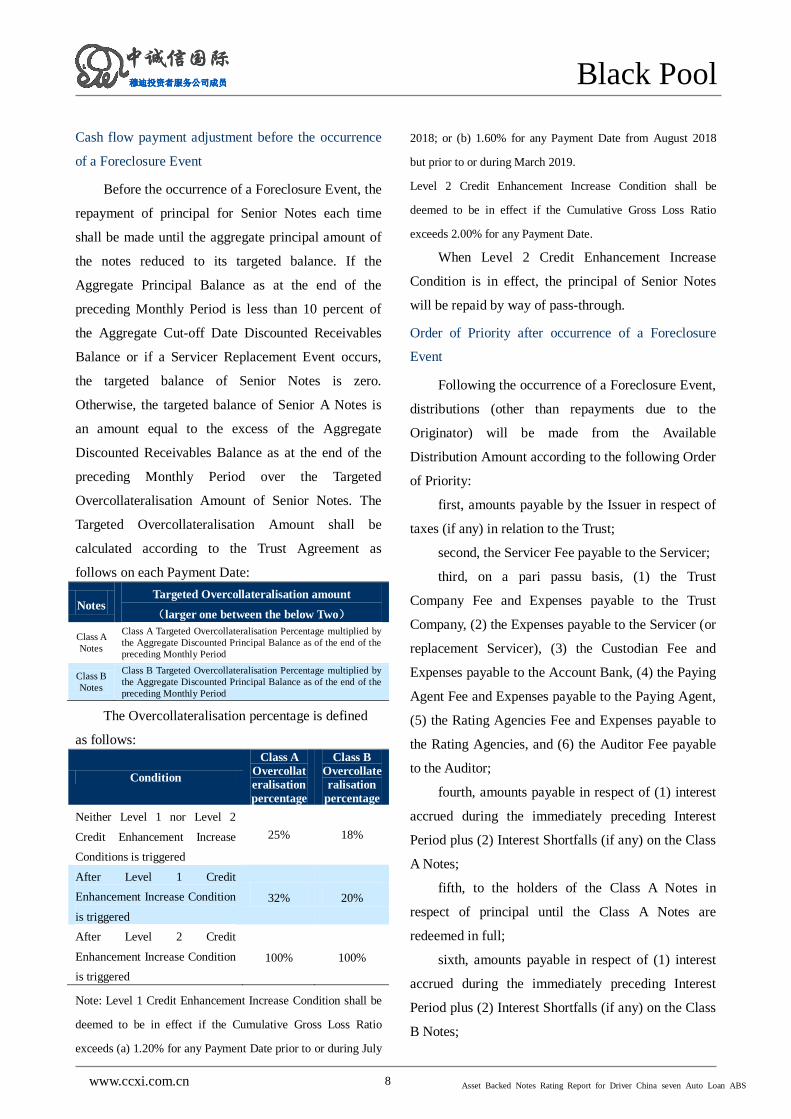

Overcollateralisation Amount of Senior Notes. The

Targeted Overcollateralisation Amount shall be

calculated according to the Trust Agreement as

follows on each Payment Date:

Notes Targeted Overcollateralisation amount

(larger one between the below Two)

Class A

Notes

Class A Targeted Overcollateralisation Percentage multiplied by

the Aggregate Discounted Principal Balance as of the end of the

preceding Monthly Period

Class B

Notes

Class B Targeted Overcollateralisation Percentage multiplied by

the Aggregate Discounted Principal Balance as of the end of the

preceding Monthly Period

The Overcollateralisation percentage is defined

as follows:

Condition

Class A

Overcollat

eralisation

percentage

Class B

Overcollate

ralisation

percentage

Neither Level 1 nor Level 2

Credit Enhancement Increase

Conditions is triggered

25% 18%

After Level 1 Credit

Enhancement Increase Condition

is triggered

32% 20%

After Level 2 Credit

Enhancement Increase Condition

is triggered

100% 100%

Note: Level 1 Credit Enhancement Increase Condition shall be

deemed to be in effect if the Cumulative Gross Loss Ratio

exceeds (a) 1.20% for any Payment Date prior to or during July

2018; or (b) 1.60% for any Payment Date from August 2018

but prior to or during March 2019.

Level 2 Credit Enhancement Increase Condition shall be

deemed to be in effect if the Cumulative Gross Loss Ratio

exceeds 2.00% for any Payment Date.

When Level 2 Credit Enhancement Increase

Condition is in effect, the principal of Senior Notes

will be repaid by way of pass-through.

Order of Priority after occurrence of a Foreclosure

Event

Following the occurrence of a Foreclosure Event,

distributions (other than repayments due to the

Originator) will be made from the Available

Distribution Amount according to the following Order

of Priority:

first, amounts payable by the Issuer in respect of

taxes (if any) in relation to the Trust;

second, the Servicer Fee payable to the Servicer;

third, on a pari passu basis, (1) the Trust

Company Fee and Expenses payable to the Trust

Company, (2) the Expenses payable to the Servicer (or

replacement Servicer), (3) the Custodian Fee and

Expenses payable to the Account Bank, (4) the Paying

Agent Fee and Expenses payable to the Paying Agent,

(5) the Rating Agencies Fee and Expenses payable to

the Rating Agencies, and (6) the Auditor Fee payable

to the Auditor;

fourth, amounts payable in respect of (1) interest

accrued during the immediately preceding Interest

Period plus (2) Interest Shortfalls (if any) on the Class

A Notes;

fifth, to the holders of the Class A Notes in

respect of principal until the Class A Notes are

redeemed in full;

sixth, amounts payable in respect of (1) interest

accrued during the immediately preceding Interest

Period plus (2) Interest Shortfalls (if any) on the Class

B Notes;

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

9 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

seventh, to the holders of the Class B Notes in

respect of principal until the Class B Notes are

redeemed in full;

eighth, amounts payable in respect of accrued

and unpaid interest on the Subordinated Notes

(including, without limitation, overdue interest);

ninth, (i) prior to the satisfaction of Clean-Up

Call Conditions or in the case that the Clean-Up Call

Conditions are satisfied but the Originator does not

exercise the Clean-Up Call, to the Subordinated

Noteholders for repayment of outstanding principal

amounts of Subordinated Notes on condition that the

outstanding principal amounts of Subordinated Notes

after repayment is no less than 5% of the then

outstanding principal amount of the Notes; or (ii) after

the satisfaction of Clean-Up Call Conditions and the

Originator choose to exercise the Clean-Up Call, to

the Subordinated Noteholders, for repayment of

outstanding principal amounts of Subordinated Notes

until it has been reduced to zero; and

tenth, to pay all remaining excess to the

Originator by way of final success fee.

Fund transfer

According to the transaction arrangement,

VWFC will act as the Servicer. After the sale of assets

to the trust, the Borrowers of the loans in the pool will

still make repayment to VWFC, and VWFC will

consolidate these Collections and make a single

deposit of such monthly Collections into the

Distribution Account no later than the sixth Business

Day before each Payment Date. The Account Bank

will make payment of various taxes, expenses and

compensation to relevant institutions according to the

instruction of the trust company, and transfer the

payable interest and principal of notes to CCDC,

which will make payment of the principal and interest.

If VWFC’s long term credit rating is lower than A, it

shall, on the second business day of each month,

transfer the collections obtained between the 16th

calendar day and the last day of the previous monthly

period (Monthly Collections Part 2) to the Distribution

Account; and, on the second business day after the

15th calendar day of each month, transfer the

collections from the first 15 calendar days of the

monthly period (Monthly Collections Part 1) to the

Distribution Account, and meanwhile, the Monthly

Collateral Account shall apply. In addition, following

the occurrence of a Servicer Replacement Event,

Borrowers and/or Security Providers relevant to the

Borrowers will be requested to make repayment

directly to Trust Company.

Monthly Collateral Account

To mitigate the commingling risks due to the

deterioration of financial or credit profile of the

Servicer, the transaction sets up a Monthly Collateral

Account, and the funding source for this account is the

Servicer. If the Servicer’s long term credit rating falls

below A, it shall make Monthly Collateral payments

to the Monthly Collateral Account twice a month. The

Monthly Collateral Account is an account maintained

in the name of the Trust with the Account Bank.

Specifically, the Servicer should transfer the Monthly

Collateral Part 2 to the Monthly Collateral Account on

the second Business Day following the fifteenth

calendar day of each Monthly Period for the purpose

of securing the Issuer's claim with respect to the

Monthly Collections Part 2, and maintain the Monthly

Collateral Part 2 as collateral on the Monthly

Collateral Account until the Monthly Collections Part

2 have been paid. The Servicer should transfer the

Monthly Collateral Part 1 to the Monthly Collateral

Account on the second Business Day of each Monthly

Period for the purpose of securing the Issuer's claim

with respect to the Monthly Collections Part 1, and

maintain the Monthly Collateral Part 1 as collateral on

the Monthly Collateral Account until the Monthly

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

10 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

Collections Part 1 have been paid.

Cash Collateral Account

The transaction sets up the Cash Collateral

Account, and the initial source of funding for the

account is from VWFC for the occurrence of Servicer

Utilisation Event. On the Issue Date, an amount equal

to 1.20% of the Aggregate Cut-Off Date Discounted

Receivables Balance will be deposited into the Cash

Collateral Account as the Initial Cash Collateral

Amount by VWFC. On each Payment Date, the Cash

Collateral Account shouldn’t be less than the

Specified Cash Collateral Account Balance, which

shall be the greater of (a) 1.2 per cent. of the

Aggregate Discounted Receivables Balance as of the

end of the Monthly Period, and (b) the lesser of (i)

RMB 40,000,000.00 and (ii) the aggregate outstanding

principal amount of the Class A Notes and Class B

Notes as of the end of the Monthly Period.

Upon the occurrence of a Servicer Utilisation

Event and while it is continuing, on each Payment

Date the General Cash Collateral Amount shall be

used to cover (a) any shortfalls in the amounts payable

under first through fifth items according to the Order

of Priority before the occurrence of a Foreclosure

Event above, or first through seventh items according

to the Order of Priority after the occurrence of a

Foreclosure Event above; and (b) on the Legal

Maturity Date or as soon as no more Receivables are

outstanding, any amounts payable under sixth though

eleventh items of the Order of Priority before the

occurrence of a Foreclosure Event above, or eighth

though tenth items according to the Order of Priority

after the occurrence of a Foreclosure Event above.

In addition, the Originator as Servicer is

entitled to utilise the Cash Collateral Amount for

the purposes of the Clean-Up Call in accordance

with the terms of Trust Agreement. Upon payment

of all amounts payable under the Notes and upon

fulfillment of all claims of all Transaction Creditors,

the Originator shall be entitled to the sums

remaining in the Cash Collateral Account together

with the interest accrued thereon.

Credit Enhancement

According to the senior/subordinate payment

system based on the Order of Priority, the Class A

Notes receive 12.20% credit enhancement from the

Class B Notes, Subordinated Notes and

Overcollateralisation; the Class B Notes receive 8.45%

credit enhancement from the Subordinated Notes and

Overcollateralisation.

Risk and Mitigants

Commingling risk related to the Servicer

If the financial or credit profile of the Servicer

deteriorates, the Collections may be commingled with

other funds of the Servicer, hence causing losses to the

Trust assets.

According to the arrangement of the transaction,

after receiving the Collections, the Servicer shall

make a single deposit of such monthly Collections

into the Distribution Account no later than the sixth

Business Day before each Payment Date. If VWFC’s

long term credit rating is lower than A, the payment

frequency shall be adjusted, and the Monthly

Collateral Account shall apply. When the Servicer is

replaced, Borrowers and/or Security Providers will be

requested to make payment directly to the Trust. In

addition, on each Payment Date the General Cash

Collateral Amount shall be used to (a) cover any

shortfalls in the amounts payable under (1) through

(5) items according to the Order of Priority before

the occurrence of a Foreclosure Event above, or (1)

through (7) items according to the Order of Priority

after the occurrence of a Foreclosure Event above;

and (b) on the Legal Repayment Date or as soon as

no more Loan Receivables are outstanding, any

amounts payable under (6) though (10) items of

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

11 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

Order of Priority after the occurrence of a

Foreclosure Event above, or (8) through (10) items

according to the Order of Priority after the occurrence

of a Foreclosure Event above.

Considering the good credit quality of VWFC as

the Servicer, Monthly Collateral Account and Cash

Collateral Account mechanism, we believe the

commingling risk related to the Servicer is minimal.

Lack of Back-up Servicer

The transaction does not designate a backup

Servicer at closing, but according to the Transaction

Documents, if the credit rating of VWFC falls below

A, it shall designate a back-up Servicer acceptable to

the Trust Company and send written notice to the

Trust Company. Upon the occurrence of a Servicer

Replacement Event, the Issuer shall be entitled to

dismiss the Servicer by written notification and to

appoint a replacement Servicer (which may be the

back-up Servicer designated by VWFC or such other

Servicer as the Issuer may appoint at its discretion).

Based on our assessment on VWFC (see the following

section of “Servicer”) and its current credit profile, we

believe the possibility of VWFC being dismissed is

low. Meanwhile, according to the Servicing

Agreement, if VWFC is dismissed, it shall execute

transfer plans properly. We believe the lack of back-up

Servicer at the beginning of the transaction have very

limited negative impact on the target rating of the

notes.

Expense risk

According to the Order of Priority, before the

repayment of interest for Senior Notes on each

payment date, the expenses of various participants and

intermediaries shall be paid first, and there is no upper

limit for such expenses. Specifically, the expenses

include Rights Perfection Notice expense, fund

transfer expense and litigation expense incurred by

Trust Company. Due to the uncertainties of such

expenses, it may have negative impact on the

repayment of interest and principal of Senior Notes.

Based on the quality of the underlying assets, the

credit profiles of the Servicer and the Trust Company

and by referring to international practice, CCXI has

fully considered the possible scenarios of relevant

expenses and have carried out stress test. We believe

the negative impact on the credit rating of senior notes

raised by the lack of upper limit for the expense is

very limited.

Liquidity risk

Liquidity risks will occur when the Collections

are not enough to pay for the interest of Senior Notes

and the various kinds of taxes, fees and expenses

before the repayment of interest for Senior Notes.

We measure liquidity risk by the possibility of

interest default. Considering the quality of the

underlying assets, the transaction arrangement and the

distribution of principal and interest repayment, the

possibility of interest default is within the range

required by the rating of Senior Notes based on our

simulation.

Meanwhile, a Servicer replacement will bring

risks to the trust. During the period of replacing the

Servicer, it is necessary to pay for the replacement and

take-over fees and the fees for the Rights Perfection

Notice. According to the arrangement of the

transaction, the trust asset will bear the notice costs.

Meanwhile, the replacing Servicer shall agree to

indemnify and hold harmless the Issuer from all

procedures, claims, obligations and liabilities as well

as all related costs, fees, damages claims and

expenditures which it may incur, arising out of, in

connection with or based upon any negligence, breach

of contractual duties or any other omission or action

of the dismissed Servicer. Considering the good credit

quality of VWFC, we believe the possibility for it to

be discharged is small, and meanwhile, the Cash

Collateral Account will mitigate the risk to some

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

12 www.ccxi.com.cn

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

extent.

Overall, we believe the good credit quality of the

Assets in the pool, the distribution pattern of the

principal and interest collection and the high

credibility of VWFC have effectively mitigated the

liquidity risk of the transaction. During the life of the

Senior Notes, we will monitor the asset quality of the

pool and the credit profile of VWFC, and will make

adjustments accordingly if any deterioration of asset

quality or credit profile leads to higher liquidity risk

which affects the credit rating of the Senior Notes.

Risk related to collateral rights registration

The underlying assets are auto loans. According

to relevant arrangement, the underlying assets are

transferred to the trust, but the mortgage registration

will not be updated. Meanwhile, among the assets in

the pool, there are loans in relation to which the

mortgage has not been registered. As a result of the

foregoing, the mortgage may not be upheld against

bona fide third party. This may impose certain

negative impact on the trust interests.

In analyzing the recovery of default assets, we

have considered the potential impact of the lack of

registration or re-registration for the security interest

over collateral rights.

Transaction related laws and regulations

The transaction is governed by P.R.C. Trust Law,

P.R.C. Contract Law, P.R.C. Property Rights Law,

P.R.C. Security Law, P.R.C. Bankruptcy Law, Credit

Asset Securitization Pilot Policy, Credit Asset

Securitization Policy for Financial Institutions, Notice

Issued by Ministry of Finance and State

Administration of Taxation on the Tax Policy for

Credit Asset Securitization, Notice on Further

Expansion of Credit Asset Securitization Pilot and

other relevant laws and regulations.

According to King & Wood Mallesons, all the

participants of the transaction are well qualified; the

proposed ABS is not against any mandatory legal or

regulatory requirements; the form of the Transaction

Documents in relation to the issuance is in line with

relevant laws and regulations and the content is not

against any mandatory legal or regulatory

requirements; the transaction does not require any

approval, consent, authorization or agreement from

any government authority except the approval from

CBRC and PBOC; once the trust enters into effect,

there is bankruptcy segregation between the trust asset

and the other property of the Issuer or the property of

the Trust Company.

CCXI’s consideration of the legal status of the

transaction is based on the above laws and regulations,

and we will keep watching any updates thereafter, if

any.

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

13

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

Asset pool and pooled assets

Overview of asset pool

Qualification of Purchased Loan Receivables (key

criteria)

1. The Purchased Loan Receivables are “normal”

loans according to CBRC’s “5-category” loan

classification method;

2. None of the Purchased Loan Receivables is

overdue as of the Cut-off Date;

3. Each of the Purchased Loan Receivables will

mature no earlier than six months and no later

than fifty-eight months after the Cut-off Date;

4. On the Cut-off Date, at least two contractual

instalments (which include interest payments)

have been paid in respect of each of the

Purchased Loan Receivables;

5. Each Loan Contract under which the relevant

Loan Receivables arise provides for a

mortgage of the relevant Financed Object;

6. The total outstanding amount of Purchased

Loan Receivables entrusted hereunder

pursuant to the Loan Contracts with one and

the same Borrower does not exceed RMB

4,000,000 in respect of any single Borrower;

7. All Financed Objects are insured with the

Originator named as the first loss payee

during the first year of the term of the

relevant loan;

8. Each Purchased Loan Receivable requires

substantially equal monthly payments to be

made within 60 months of the date of

origination of each Loan Contract and may

also provide for a final balloon payment;

9. The Purchased Loan Receivables are free of

defences, whether peremptory or otherwise,

for the agreed term of the Loan Contracts as

well as free of rights of third parties;

10. The Purchased Loan Receivables are

assignable;

11. The Loan Contracts shall be governed by the

laws of China;

12. The maximum delinquent days of each

Purchased Receivable is no more than 60

days.

Loan profile in the pool

According to the above criteria, the loans of

the asset pool have the following characteristics:

Nature of loans: auto loans

Discounted Receivables balance of loan

contract of single borrower (“Discounted

Balance” or “ODRB”): RMB 4,905.09~

RMB 2.26 million;

Loan interest rate is 0%~15.72% on the

Cut-off Date, and all loans of the asset pool

are fixed rate loans;

Five-category loan classification: “Normal”

loans according to CBRC’s five-category

loan classification.

Asset pool overview as the Cut-Off Date3

Number of contracts 68,331

Number of borrowers 67,402

Total outstanding discounted receivables balance

RMB 4,000,006,554.35

Average outstanding discounted receivables balance of single contract

RMB 58,538.68

Average outstanding discounted receivables balance of single borrower

RMB 59,345.52

Weighted average loan interest rate

1.85%

Loan Tenor 12~60 months

Weighted average loan tenor

29.66 months

Seasoning4 2~54 months

Weighted average seasoning

6.88 months

3 Weighted average data is weighted by outstanding discounted

receivables balance (ODRB). 4 Seasoning is the months that the loan is already repaid as loans are

monthly repaid

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

14

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

Remaining term5 6~58 months

Weighted average remaining term

22.78 months

Characteristics of the asset pool

Interest rate distribution

The lowest interest rate in the portfolio is

0.00% and the highest is 15.72%. The weighted

average interest rate is 1.85%. Below is the

interest rate distribution of the portfolio.

Interest rate

ODRB as a

percentage in

total

Number of

loans as a

percentage

in total

<=3% 66.60% 78.79%

3%~6%(inclusive) 28.62% 16.43%

6%~9%(inclusive) 3.08% 2.98%

9%~12%(inclusive) 1.62% 1.72%

>12% 0.08% 0.08%

Total 100.00% 100.00%

CBRC Category

The assets of the asset pool are individual

auto loans and corporate auto loans. All of the

loans are “Normal” loans according to CBRC’s

five-category loan classification method, and

there was no overdue or default case as at Cut-Off

Day. The amount of loans with co-borrower

accounts for 26.07% of the total outstanding

discounted receivables balance (ODRB) of the

asset pool.

ODRB

The largest ODRB of single loan is RMB

2.26 million, and the smallest is RMB 4,905.09,

with the average being RMB 58,538.68. The 20

largest ODRB loans account for 0.44% of the total

outstanding discounted receivables balance of the

asset pool. The ODRB of single loan and its

proportion in total ODRB of the asset pool are as

follows:

5 Remaining term is the months that the left loan needs to be repaid

according to contract.

ODRB of single loan

ODRB as a

percentage

in total

Number of

loans as a

percentage in

total

<=RMB50,000 32.47% 54.72%

RMB50,000~100,000 (inclusive)

40.67% 35.05%

RMB100,000~150,000 (inclusive)

13.55% 6.72%

RMB150,000~200,000

(inclusive) 5.40% 1.84%

>RMB200,000 7.91% 1.67%

Total 100.00% 100.00%

Original Term of the loans

The shortest original term of the loans is

12.00 months, and the longest is 60.00 months,

with the weighted average original term being

29.66 months. The specific distribution of original

term is as follows:

Original term of loans

(in month)

ODRB as a

percentage

in total

Number of

Loans as a

percentage

in total

<=12months 0.85% 0.83%

12~24 months (inclusive) 51.21% 58.60%

24~36 months (inclusive) 47.50% 40.30%

36~48 months (inclusive) 0.26% 0.12%

>48 months 0.18% 0.15%

Total 100.00% 100.00%

Remaining Term of the loans

The shortest remaining term of the loans is 6

months, and the longest is 58 months, with the

weighted average remaining term being 22.78

months. As of the Cut-Off Date, there was no case

of delinquency or default. The specific

distribution of remaining term is as follows:

Remaining term of loans

(in month)

ODRB as a

percentage in

total

Number of

Loans as a

percentage in

total

<=6months 0.38% 1.00%

6~12 months (inclusive) 6.64% 11.50%

12~18 months (inclusive) 21.44% 25.93%

18~24 months (inclusive) 32.73% 32.04%

>24 months 38.81% 29.53%

Total 100.00% 100.00%

Seasoning of the loans

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

15

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

The shortest seasoning is 2 month and the

longest is 54 months; the weighted average is 6.88

months. Please refer to the following figure for

details:

Seasoning

ODRB as a

percentage in

total

Number of

Loans as a

percentage in

total

<=6 months 56.64% 46.95%

6~12 months (inclusive) 32.30% 36.40%

12~18 months (inclusive) 7.68% 12.33%

18~24 months (inclusive) 2.54% 2.85%

>24 months 0.84% 1.47%

Total 100.00% 100.00%

Characteristics of Borrowers

Geographic distribution of Borrowers

The loans are distributed across 31 provinces,

autonomous regions and municipalities in China.

No province accounts for more than 10% of total

ODRB of the asset pool. The asset pool is well

diversified in terms of geographic distribution.

The following are the top 10 provinces with

highest ODRB.

Regions

ODRB as a

percentage

in total

Number of

Loans as a

percentage

in total

Shandong Province 8.59% 9.44%

Guangdong Province 7.29% 6.56%

Hebei Province 6.43% 7.26%

Sichuan Province 6.07% 6.26%

Jiangsu Province 6.04% 5.88%

Zhejiang Province 5.97% 5.93%

Henan Province 5.54% 5.52%

Hubei Province 4.92% 4.86%

Jilin Province 4.67% 4.74%

Beijing City 4.17% 3.38%

Nature of Borrowers

As at the Cut-Off Date, the youngest

individual Borrower is 18 years old, and the

oldest is 86 years old. Please refer to the

following figure for detailed age distribution.

Borrower age

distribution

ODRB as a

percentage in

Number of

Loans as a

total percentage in

total

<=30 37.88% 40.57%

30~40 (inclusive) 34.37% 33.72%

40~50 (inclusive) 20.74% 19.26%

>50 7.01% 6.45%

Total 100.00% 100.00%

Characteristics of collaterals

There are 68,331 automobiles as implied by

the loans in the pool, out of which 67,876 are new

vehicles and 455 are second-hand vehicles. VW

(VW imported are excluded) accounts for 81.39%

of the total, and Audi accounts for 10.83%. VW’s

production technology is decent and the usable

life of vehicles is relatively long.

The range of the initial collateralization rate

is from 6.00% to 80.00%, and the weighted

average initial collateralization rate is 56.09%. As

the weighted average contract term of the loans is

29.66 months, far below vehicles’ normal life.

Therefore, the real collateralization rate is even

lower, and this provides a buffer against the

decline of collateral value.

Collateralization

rate distribution

ODRB as a

percentage in

total

Number as a

percentage to

total

<50% 25.30% 29.76%

50%~60% (incl. 50%)

33.88% 37.57%

60%~70% (incl. 60%)

15.88% 14.30%

>=70% 24.94% 18.37%

Total 100.00% 100.00%

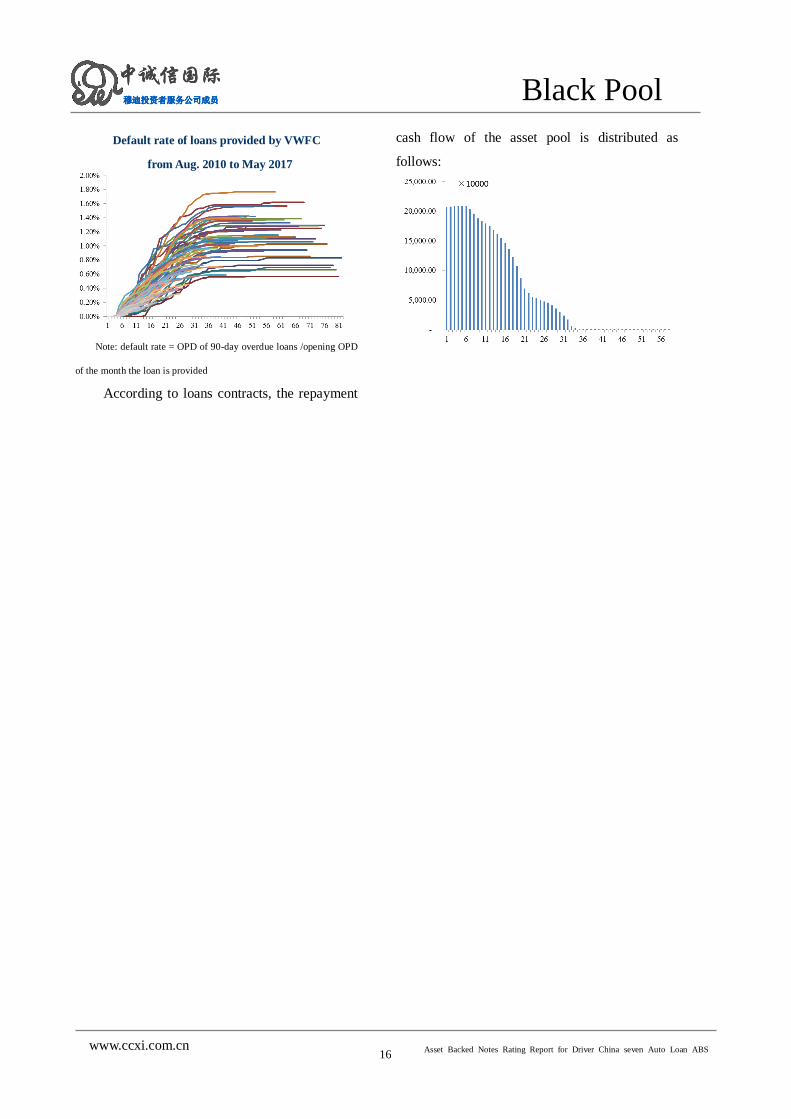

Credit quality

Based on the static asset pool historical data

as provided by the Originator, the figure below

shows the default rate (as of May 2017) of the

loans provided by VWFC from Aug. 2010 to May

2017:

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

16

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

Default rate of loans provided by VWFC

from Aug. 2010 to May 2017

Note: default rate = OPD of 90-day overdue loans /opening OPD

of the month the loan is provided

According to loans contracts, the repayment

cash flow of the asset pool is distributed as

follows:

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

17

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

Credit analysis approach

CCXI has built ABS cash flow analytic model

and rating model, which are more suitable to

evaluate the economic environment in China.

CCXI’s approach of computing the expected

loss of auto-loan ABS is based on the analysis of

historical data of static and dynamic pools with

concerning macroeconomic conditions, industrial

trends and features of the assets in the pool, and to

calculate the loss rate and loss volatility of the

pooled assets and obtain the loss probability density

function (assuming auto-loan loss rate is in

lognormal distribution). Based on the function, we

simulate the cash flow (interest and principal) to be

generated by the asset pool at various payment

periods (i.e. cash flow time distribution), and

arrange for simulated cash flow distribution based

on various security payment structure and

mechanism, in order to get the expected loss of

various classes of notes (i.e. required level of credit

enhancement). In the stress test based on target

ratings, we simulate scenarios of loss rate increase,

loss volatility increase, loss time distribution

adjustment and spread decline, etc., in order to

adjust the required credit enhancement level for

various classes of notes. Meanwhile, we also take

into account the impact of structural features of the

trade (e.g. prior/secondary payment, principal

transfer, etc.) and the experience of Servicers on the

credit enhancement level.

To obtain the loss probability distribution,

CCXI first derives the parameters from the data of

overdue loans(i.e. exceed 90 days) of the static pool

between 2010.08 and 2017.05 provided by issuer,

and then adjusts the parameters based on the

features of the asset pool, the macro economy, the

trend of industries and so forth. The following

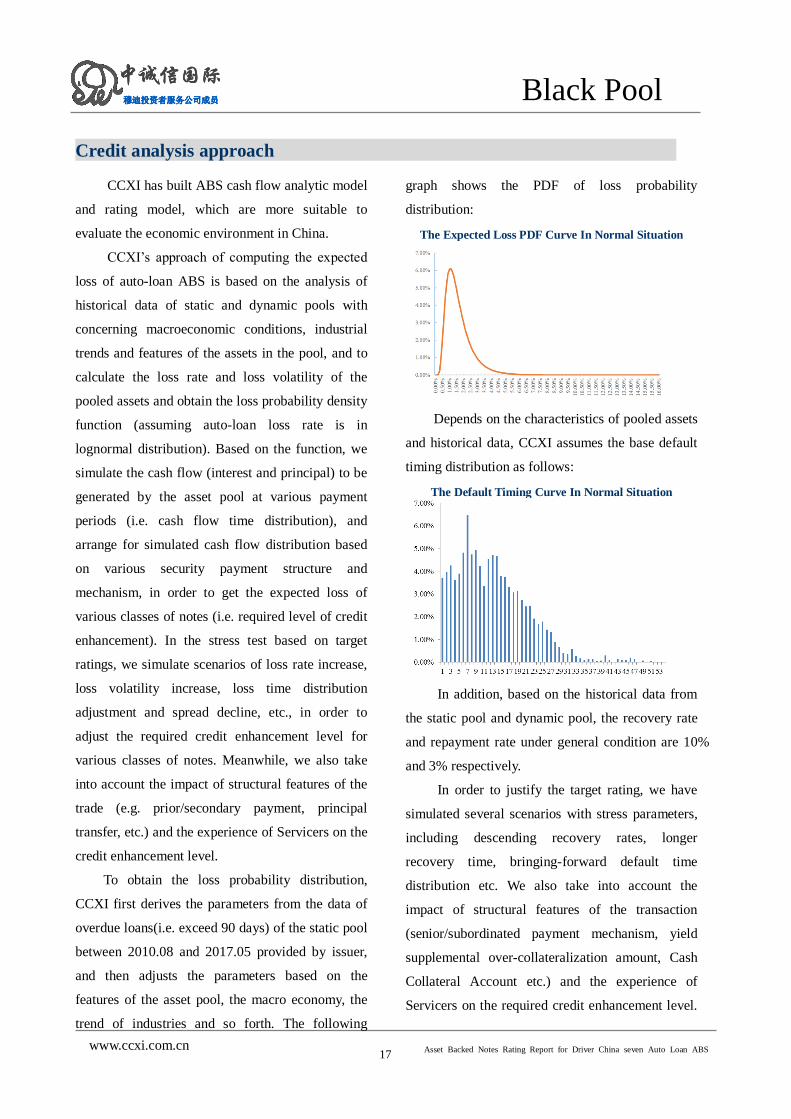

graph shows the PDF of loss probability

distribution:

The Expected Loss PDF Curve In Normal Situation

Depends on the characteristics of pooled assets

and historical data, CCXI assumes the base default

timing distribution as follows:

The Default Timing Curve In Normal Situation

In addition, based on the historical data from

the static pool and dynamic pool, the recovery rate

and repayment rate under general condition are 10%

and 3% respectively.

In order to justify the target rating, we have

simulated several scenarios with stress parameters,

including descending recovery rates, longer

recovery time, bringing-forward default time

distribution etc. We also take into account the

impact of structural features of the transaction

(senior/subordinated payment mechanism, yield

supplemental over-collateralization amount, Cash

Collateral Account etc.) and the experience of

Servicers on the required credit enhancement level.

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

18

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

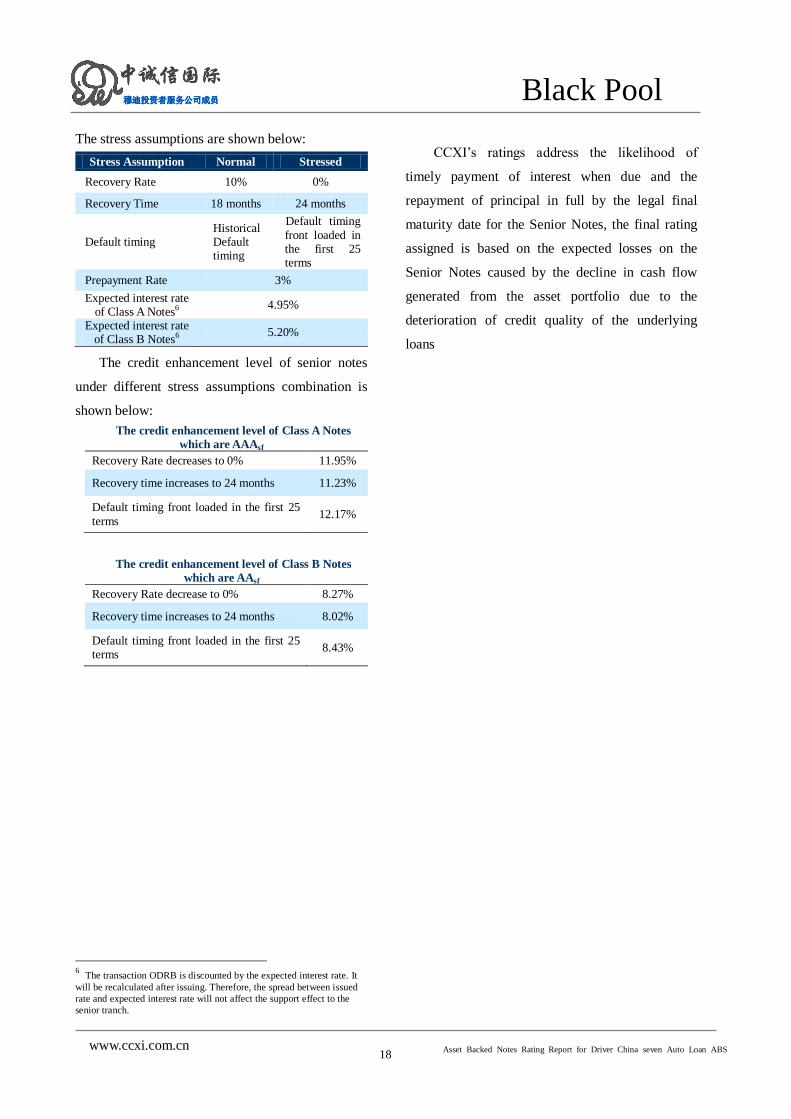

The stress assumptions are shown below:

Stress Assumption Normal Stressed

Recovery Rate 10% 0%

Recovery Time 18 months 24 months

Default timing Historical Default timing

Default timing

front loaded in the first 25 terms

Prepayment Rate 3%

Expected interest rate of Class A Notes6

4.95%

Expected interest rate of Class B Notes6

5.20%

The credit enhancement level of senior notes

under different stress assumptions combination is

shown below:

The credit enhancement level of Class A Notes

which are AAAsf

Recovery Rate decreases to 0% 11.95%

Recovery time increases to 24 months 11.23%

Default timing front loaded in the first 25

terms 12.17%

The credit enhancement level of Class B Notes

which are AAsf

Recovery Rate decrease to 0% 8.27%

Recovery time increases to 24 months 8.02%

Default timing front loaded in the first 25 terms

8.43%

6 The transaction ODRB is discounted by the expected interest rate. It

will be recalculated after issuing. Therefore, the spread between issued

rate and expected interest rate will not affect the support effect to the

senior tranch.

CCXI’s ratings address the likelihood of

timely payment of interest when due and the

repayment of principal in full by the legal final

maturity date for the Senior Notes, the final rating

assigned is based on the expected losses on the

Senior Notes caused by the decline in cash flow

generated from the asset portfolio due to the

deterioration of credit quality of the underlying

loans

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

19

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

Important participants

Originator/ Servicer

Volkswagen Finance China Co,. Ltd (“VWFC” or

the Company) was established on August 30, 2004

as a fully-funded subsidiary of Volkswagen

Financial Services AG (“VWFS”). As a non-bank

financial institution subject to the jurisdiction of

CBRC, the company had RMB 0.5bn as its initial

registered capital. During 4 times increase the

registered capital, As of end of 2016, the registered

capital of company had reached RMB 4bn. The

business scope of VWFC includes extending

automobile loans to residents and institutions

permanently or temporarily residing in China (e.g.

taxi companies and driving schools); providing

purchase loans to automobile dealers etc.

With the growth of VW automobiles in

Chinese market, the company’s auto finance

business has been growing rapidly. VWFC has

cooperated closely with Shanghai Volkswagen,

Faw-Volkswagen and Volkswagen Group Import

(China) Co., Ltd (VGIC), etc., and has applied

services for VW, Audi, Skoda, Porsche, Scania,

Seat, Bentley, Lamborghini and Man etc. major

brands. At the end of June 2016, VWFC’s retail

business has covered 310 cities in China, and with

cooperation relation with 2,786 auto dealers; its

corporate business has covered 114 cities and

applied loan services for 549 dealers. VWFC’s

total assets increased to RMB 48.54bn, the total

amount of loans and advances is RMB 43.27bn,

and the owner's equity is RMB 6.67bn. During the

first half of 2016, the operating revenue totaled

RMB 0.92bn. Meanwhile, VWFC has controlled

its risk strictly, at the end of 2016, the

non-performing loan ratio of VWFC is 0.14%.

The Company rolled out retail business in

2004, providing loan services to consumers,

including both individuals and institutes. The

business has been growing quickly since launched.

As of end of 2016, the penetration rate of the

company in retail loan market reached 13.5%.

In terms of product structure, the retail

business is divided into new car credit and used car

credit; and new car credit are further divided into

several sub-categories (i.e. classic loan, balloon

credit, exquisite easy loan, enjoyable balance loan

and used car classic loan) to meet different needs

of consumers. There is a steady increase in the

retail business of VWFC during the past 3 years.

As of end of 2016, the number of retail loan

contracts reached 850 thousand, increasing 32%

from last year, and the number of new contracts in

2016 was 528 thousand. As of end of 2016, the

balance of loans for retail business reached RMB

40.53bn, increasing 24% from last year.

Due to a policy restriction, the Company only

has one office in China at the moment which is the

head office in Beijing. The head office has set up

the Board of Directors, but without shareholder

meetings or a Board of Supervisors. The Board of

Director is responsible for all business-related

decision making and supervision. The Board of

Management and other managers are responsible

for the day-to-day operation management. The

business units of the Company are divided into

Front, Middle and Back offices. Front Office

includes Retail Sales, Wholesale Sales, Marketing

& Communication, Business Strategy & Product

Development, Treasury Front Office, Government

Relationship and Brand Relationship & Corporate

Strategy department; Middle Office includes

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

20

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

Customer Care, Retail Sales Care and Operation

Planning & Excellence; Back Office includes Risk

Management, Wholesale Back Office, Accounting

& Treasury Back Office, HR & Administration,

Controlling, Purchasing department, IT & Project

Management departments and Legal &

Compliance. Specifically, Risk Management

Department is responsible for drafting and

maintenance of risk management policies and the

collections of overdue retail loans and asset

preservation; and the Retail Sales Care Department

is responsible for underwriting loans.

The Company has been strengthening risk

management since establishment, and has set up a

risk management framework comprised of decision

making system, execution system, supervision

system. Specifically, the decision-making body is

the Board of Directors; the execution system is

comprised of various business units led by Risk

Management Department; and the supervision

system is comprised of Legal & Compliance

Department and Internal Audit Department. The

Risk Management department is further divided

into three working groups, respectively taking

charge of risk assessment, overdue loan collection,

and wholesale stock management. The risk

assessment team is responsible for providing

procedures and policies regarding risk related

issues, supervision and quality assurance of credit

business related policies, guidelines and

procedures, risk analysis, assessment and

controlling, risk cost analysis and internal and

external risk reporting and conduct of risk reviews.

The Company has established a complete set of

risk management policies and procedures,

including Credit Application Guideline (Retail),

Field Visit Guideline, Retail Loan Origination

Guideline, Client Management Guideline, Credit

Authorization – Loan Business, Risk Management

Principle, and Asset Provision Guideline, etc.

For credit risk management, the company has

established a standard loan business process

centering on retail business. A customer will first

signs a credit application materials and gives

personal documents to the car dealer, and the

information will be sent to VWFC via on-line IT

tool; and the scoring system will generate a credit

score to the applications. Based on score results,

the application will be automatically accepted

/rejected or enter manual decision process. By the

end 0f 2016, about 50% applications are

automatically approved, and 3% are automatically

rejected. Applications which enter manual decision

process will receive a comprehensive credit

assessment by credit officers, including client

stability (working stability, living stability and

family information), repayment capacity, credit

behavior, living status, and income and expense

information. When necessary, the credit officers

will require additional document or field visit, in

order to make a final decision. The credit team is

divided into five levels based on their working

experience, and has different approval limits. It is

effective to control the credit risk of VWFC. The

whole underwriting process generally takes only

2.5 hours.

The Customer Care Department will provide

loan servicing. Before the repayment date, the

hotline team will send a SMS to remind clients

about the repayment date and the amount, in order

to reduce overdue cases. The collection team of

Risk Management Department is responsible for

collecting overdue installments: Reminding text

message and warming letter will be sent to clients

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

21

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

whose loan installments are overdue less than or

equal to 5 days. Not only Reminding text message

and warming letter will be sent to clients, but also

Intensive-collection text message and call will be

made to clients whose loans are overdue by 6~30

days. Collections via call will be conducted for

loans which are overdue more than 30 days but

less than 60 days, and loans overdue more than 60

days will be intensive-collections and terminate a

contract while overdue 90 days. Loans overdure 95

days will be outsourced for collections or

transferred to Legal department.

The IT & Project Management Department is

responsible for information management. There are

six working teams respectively taking charge of

infrastructure, project management, system

development, IT compliance, application

management system and IT service desk. The

Company allocates much budget for IT operations.

Currently VWFC invested in Data Center

Capabilities (primary and 2nd

location) within

China to be fully compliant and to provide

performed /reliable IT services for the market

China.

CCXI believes VWFC is one of industry

peers in terms of its expertise and efficiency of

underwriting by relying on a set of well-

established application management system and

techniques, which reduces the inconsistency of

human judgment.

After an on-site due diligence, CCXI believes

VWFC has good credibility, and its business

process, risk control and information systems can

properly satisfy the needs of loan servicing in this

transaction.

Trust Company

CITIC Trust was established from CITIC

Industrial Trust Investment, a fully-funded

subsidiary of CITIC Group set up on March 5,

1988. In 2002, it was restructured into CITIC Trust

Investment Co., Ltd, and in 2007, its name was

changed to CITIC Trust Co., Ltd. Through twice

capital increase in 2005 and 2006, CITIC Trust has

had RMB1.2bn of registered capital, and the

shareholders are CITIC Group and CITIC East

China. As of end-2015, the balance of trust asset

totaled RMB 1,763.95bn. During the whole year of

2016, operating revenue of CITIC Trust was RMB

5.82bn, and net profit was RMB 3.12bn.

CITIC Trust has obtained business licenses as

a special purpose trust company in ABS

transactions, enterprise annuity fund legal entity

trust company and account manager, qualified

domestic institutional investor (QDII) as well as

national social security fund trust company. The

scope of business includes trust business,

traditional business and other business. Trust

business includes investment, financing and

management businesses; and traditional business

includes short term loans, financial product

investment, and long term equity investment, etc.

As of end-2016, the amount of collective trust

plans reached RMB 373.56bn, and the amount of

single trust projects was RMB 597.10bn.

In terms of risk management, CITIC Trust has

established fire walls and risk control frameworks

according to CBRC requirement. It issued Risk

Management Handbook in 2011 to improve the

risk management system, internal control process

and management systems.

In terms of IT construction, CITIC Trust has

set up two server rooms for production systems

and one server room for disaster recovery through

ten years of efforts from 2002, which can properly

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

22

穆迪投资者服务公司成员穆迪投资者服务公司成员

www.ccxi.com.cn

Black Pool

meet the demand of information processing and

security.

According to the arrangement of this

transaction, Trust Company authorizes VWFC to

manage the asset of the pool and the collections of

the repayment based on “Service Contract”. Trust

Company authorizes Bank of China to manage

trust fund according to Account Agreement. The

key work of CITIC Trust is to handle day-to-day

trust related affairs, and supervise the performance

of duties of various parties. We believe CITIC

Trust as the Trust Company for the transaction can

properly provide the required service of trust asset

management and trust related affair handling.

Account Bank

In the transaction, China Construction Bank

Corporation Beijing Branch (“CCB Beijing”) acts

as account bank to custody funds. The bank, which

was founded in September 2004, is one of the four

largest commercial banks in China, and it has

about 10.15% of the market share of the banking

system. In October 2005 and September 2007,

CCB has successively listed in the Hong Kong

stock exchange and the Shanghai Stock Exchange,

respectively. By the end of 2016, the total amount

of the capital stock of CCB is 250.01bn, and its

largest shareholder is the Central Huijin

Investment Co., Ltd holds 57.31% of the shares.

CCB’s branches have covered provinces and

cities nationwide in China, and the number of

branches has ranked among the leading banks in

the bank system in China. By the end of 2016,

there are 14,956 commercial institutions in

domestic market and 29 commercial branches

located in other regions and nations. Meanwhile,

CCB has 369,482 staff.

As of the end of 2016, CCB held total assets

of RMB 20,963.71bn, include the loans and net

advances RMB 11,488.36bn; the liabilities of CCB

is RMB 19,374.05bn, include client deposit RMB

15,402.92bn; stockholder's equity is RMB

1,589.65bn; capital adequacy ratio is 14.94%, tier

1 capital ratio is 13.15% and core tier one capital

ratio is 12.98%; non-performing loan ratio is

1.52%, provision for coverage is 150.36%.

Operating revenue for 2016 was RMB 605.09bn

and net profit was RMB 232.39 bn.

In terms of Credit risk, recently, the Bank

actively responded to the complex and volatile

economic situation, continuously optimised credit

policies and credit systems, focusing on the

overcapacity industry, make the screening criteria

standards details, continuously the quota

management and reduce the government financing

platform loans. In addition, CCB reinforced the

fundamental management on pre-lending

evaluations, business structure, storage assets and

creating new products to reduce the concentration

of credit risks.

In terms of liquidity Risk Management,

According to both the regulatory requirements and

the principle of prudence, CCB has formulated

related management policies. CCB measures the

liquidity Risk by liquidity factors analysis,

remaining maturity date analysis and cash flow

analysis of non-discounted contracts. Moreover,

the bank would measure the influence of liquidity

risk by predicting the cash flow in next year in

different scenarios.

According to our credit assessment, we believe

CCB can properly provide the required service as

the Account Bank for the transaction.

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

23

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

www.ccxi.com.cn

Appendix 1

Development and competitive dynamics

of automobile industry

The automobile industry has become an

essential pillar industry in China’s national economic

development. Automobile industry is moving into

high gear in the 21st century, crystallizing into

multiple-categories and a full range of competed

vehicles and parts production. China auto industry

now has upgraded degree of industrial concentration

and improving technical standards up to the level of a

major global producer.

In 2016, China’s automobile industry has shown

a rapid growth, and the production and sales volume

are 28.12mn and 28.03mn, respectively, up to 14.46%

and 13.65% increase on a year-on-year basis (YoY).

The growth rate is 11.21 percentage points and 8.97

percentage points higher than last year respectively.

The production and sales volume of passenger

vehicles are 24.42mn and 24.38mn, respectively, up

to 15.50% and 14.93% increase YoY, higher than that

in 2015. As the effect of the reducing vehicles tax

policy, the sales volume of passenger vehicles within

1.6 liters displacement engine is 17.61mn, grew

21.40% than last year. The small liters engine

passenger vehicles sales volume is 72.20% of the

total passenger vehicles sales volume, and up to 3.60%

increase YoY. Between January and March of 2017,

the production and sales of vehicles are 7.13mn and

7.00mn, up to 7.99% and 7.02% increasing YoY

respectively, the growth rate has decreased 5.26

percentage points and 6.15 percentage points

comparing to them of the same time of 2015. As the

impact of the reducing tax of small liter displacement

vehicles policy expired at the end of 2016 and

subsidies to new energy vehicles will reduce in 2017,

the vehicles market has taken up the segment of the

potential demands, and may have negative

impact in 2017.

Sales Volume of China’s Automobile Industry

The growth of the domestic economy, the

deepening of urbanization and the

improvement of the living standard of residents

are the main factors of the growth of China's

automobile industry, and the large number of

population and the low car inventory provide

large space for China's automobile industry.

The car inventory of 1,000 person in USA is

797, which at the same time, the car inventory

of 1,000 person in China was only 125, about

15% of that in USA.

With the rapid development of China’s

automobile industry, the car inventory has

increased to 194mn at the end of 2016, and the

car inventory of 1,000 person has passed to 140,

up to 12.79% increase comparing to 2015. As

of the differences between different provinces,

the development of automobile industry in

different provinces is not the same. According

to the car inventory at the end of 2016, some

cities’ car inventory of 1,000 person has further

exceeded the average of the nation, and some

cities are far behind. There are 46 cities which

their car inventory has passed 1mn, and there

are 18 cities which are Beijing, Chengdu,

Shenzhen, Chongqing, Shanghai, Suzhou,

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

24

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

www.ccxi.com.cn

Tianjin, Zhengzhou, Xi’an, Hangzhou, Guangzhou,

Wuhan, Shijiazhuang, Nanjing, Qingdao, Dongguan,

Ningbo, foshan, their car inventory has passed 2mn.

In medium and long term, the first demand of

automobile from third and fourth-tier cities with large

population and the replacing demand of automobile

from first and second-tier cities will certain high

growth of China’s automobile market.

Overall, the reducing tax of small liter

displacement vehicles policy in 2016 had improved

the passenger vehicles market, along with the cars

market. In 2017, as the policy expired, the car market

growth rate may experience a slight drop.

Developments of automobile finance

companies

As an integral part of the modern automobile

sales chain, automobile financial companies are

improving the sales of manufacturers, promoting the

consumption of cars and the cost recovery of

manufacturers. Meanwhile, automobile financial

companies also gain loads of profits from providing

professional financial services. During the

development of automobile financial industry, they

play a positive role in improving the profit structure

of automobile industrial chain and enhancing the

capabilities of manufacturers in comprehensive

service and competition, as well as promoting the

sustained and stable development of automobile

industry.

Automobile financial industry has developed for

almost 100 years in overseas market, while in China

it is still an emerging industry. According to China’s

commitment for WTO entry, the CBRC issued the

Policy on the Management of Automobile Finance

Companies and the Details on the Execution of the

Policy on the Management of Automobile Finance

Companies in October and November 2003, which

opened China’s automobile consumer credit

market to overseas entities and allowed

qualified foreign institutions to set up

automobile finance companies in China. As the

domestic consumer finance markets are

immature at that time, the above policies were

prudent. The policies give many limitations to

automobile financial companies, in particular,

they only allowed automobile financial

companies to raise fund through shareholder

deposits or borrowing from banks, which

restricted the funding channel and curbed the

growth of business. Meanwhile, despite of

international practice, the policies did not allow

automobile leasing to be part of the business

for automobile finance companies.

To promote healthy growth and complete

supervision of the automobile financial industry,

the CBRC issued the new version of Policy on

the Management of Automobile Finance

Companies in December 2007. The Policy

entered force on January 24, 2008, which lifted

the control over the funding channels of

automobile financial companies by allowing

them to issue bond to obtain long term fund

and alleviate the mismatch of assets and

liabilities, and it allowed for inter-peer

borrowing/lending to increase short term

financing capabilities. Meanwhile, it also

allowed automobile financial companies to

engage in leasing business, which creates a

new profit growth engine and makes it possible

for automobile financial companies to establish

three core businesses of retail loans, wholesale

loans and financing leasing based on

international practice. In addition, the new

Policy increased the threshold on the economic

strength of fund providers, stressing on their

Asset Backed Notes Rating Report for Driver China seven Auto Loan ABS

25

穆迪投资者服务公司成员穆迪投资者服务公司成员 Black Pool

www.ccxi.com.cn

management experiences, and raised higher

requirement on the risk management framework of

automobile finance companies. In 2014, PBOC and

CBRC issued an announcement (Document No.:

Other[2014]8) to further standardize financial-bond

issurance of automobile finance companies. The

announcement also relaxed the requirements of bond

issuance, which contribute to financing of automobile

financial companies.

At the end of 2016, 25 companies have been

established, including SAIC-GMAC Automotive

Finance Co.,Ltd., Toyota Motor Finance (China) Co.,

Ltd., etc. According to automobile financial industry

report published by CHINA BANKING

ASSOCIATION-AFC Association Standing

Committee, as of end 2015, the total equity of all

automobile companies raise to 419 billion, which is

23.12% higher than the number in 2014.

Automobile Financial Companies approved to be

established by-2016 Q4

Company name Establishment

SAIC-GMAC Automotive Finance

Co.,Ltd. Aug, 2004

Volkswagen Finance (China) Co., Ltd.

Aug, 2004

Toyota Motor Finance (China) Co., Ltd.

Jan, 2005

Ford Automotive Finance (China) Limited

May, 2005

Mercedes-Benz Auto Finance Ltd. Nov, 2005

Dongfeng Peugeot Citroen Auto Finance Co., Ltd.

Aug, 2006

Volvo Automotive Finance (China) Limited

Aug, 2006

Dongfeng Nissan Auto Finance Co., Ltd.

Oct, 2007

FCA Automotive Finance Co., Ltd.

Dec, 2007