RTEP Program

Administration Report and Presentation - May 22nd, 2013

AdvantageHOPE- Hope's Economic Development Agency | (604) 860 0930 | [email protected]

Revitalization Tax Exemption Program

Administration Report

District of Hope

Committee of the Whole Meeting

May 22nd, 2013

Contents:

Administration Report (8 pages)

Revitalization Tax Exemptions - a primer on the Provisions in the Community Charter (8 pages)

DRAFT Bylaw Package including

o RTEP Information Sheet (1 page)

o RTEP Process Flow Chart (1 page)

o DRAFT Bylaw 1337, 2013 (7 pages)

o RTEP Application Form (2 pages)

o RTEP Agreement (8 pages)

o RTEP Certificate (2 pages)

Administration Report Hope Business & Development Society

Advantage HOPE

AdvantageHOPE | Administration Report | RTEP Program | Page 1 of 8

Date: May 22, 2013 Topic: Revitalization Tax Exemption Program (RTEP)

Author: Tyler Mattheis, Executive Director Related

Documents

1) Revitalization Tax Exemptions, A Primer on the Provisions in the Community Charter (January 2008)

2) DRAFT Bylaw 1337 Package (Draft as of May 21st, 2013)

Background ................................................................................................................................................... 1

Current Community Economic Development Status ....................................................... 2

Official Community Plan ................................................................................................................................... 2

Examples from Neighbouring Municipalities ........................................................................ 2

Key Benefits to a Hope RTEP Program ...................................................................................... 3

DRAFT BYLAW 1337, 2013 .................................................................................................................. 4

Information Sources .......................................................................................................................................... 4

Continued Points of Discussion ........................................................................................................................ 5

1. Investment Thresholds ......................................................................................................................... 5

2. Length of Benefit .................................................................................................................................. 6

3. Scale / Amount of Benefit .................................................................................................................... 6

4. Level of BC Assessment Support ......................................................................................................... 7

Conclusion ..................................................................................................................................................... 8

Background

Since becoming operational in the spring of 2011, the Hope Business and Development Society has worked to establish itself in the District of Hope as a reliable, viable, and productive economic development office.

A continued challenge is moving from converting the work we have done in communications, relationship building, and information gathering to actual investment, building, and local jobs. AdvantageHOPE is not a financial institution or a government body, and therefore does not have the ability to offer financial or tax incentives of any sort - our role is set as a communicator and marketer at this time.

To that end, it is often apparent that potential investors are looking for specific monetary incentives in the form of tax breaks or surety to help them make a decision to invest in Hope.

Administration Report Hope Business & Development Society

Advantage HOPE

AdvantageHOPE | Administration Report | RTEP Program | Page 2 of 8

Many competing jurisdictions offer such programs, often built upon specific goals laid out in their official community plans, downtown revitalization plans, or similar documents.

A synopsis of RTEP's in municipalities around Hope is available in a previous report to the AdvantageHOPE Board. In 2006, a draft bylaw for Hope was created to take advantage of the provisions of the Community Charter, however that effort was not pursued.

It is AdvantageHOPE's opinion that an RTEP for Hope, combined with and propelled by a strong brand, will spur investment in targeted areas of our community.

Current Community Economic Development Status

Official Community Plan

In sections 6.3 - Commercial Land Uses, and 6.4 - Industrial Land Uses, of the Official Community Plan, many policies are stated to encourage various forms of development deemed important to the community. Many of the objectives of the OCP are re-iterated in the Economic Development Plan, yet many of the objectives have not yet been achieved.

The reasons for the lack of achievement are many - global economic events, competition from neighbouring municipalities, and a small land base are some of them. There have been instances of interested corporations from 2004 to the current year investigating Hope due to our natural advantages, but have not gone beyond the investigative stage due to the reasons above, but also due to physical constraints such as flood hazard, geotechnical hazard, lack of servicing, or simply an inability to come to an agreement with the land-owner.

Examples from Neighbouring Municipalities

RTEP's are a staple of neighbouring municipalities, and are used for a variety of purposes. The Province of BC has provided a backgrounder on the RTEP entitled Revitalization Tax Exemptions, A Primer on the Provisions in the Community Charter (January 2008), for more information.

Our neighbours (and competitors) have wielded this tool to encourage activity such as: - Commercial Development; - Downtown Beautification; - Industrial Growth; - Density Developments; - Green Development; - Airport Development; - Waterfront Development; and - General economic revitalization.

Administration Report Hope Business & Development Society

Advantage HOPE

AdvantageHOPE | Administration Report | RTEP Program | Page 3 of 8

The incentives vary in terms of: - Incentive Duration ......................3 to 10 years (10 years maximum allowed) - Program Term .............................5 years to indefinitely - Exemption Amount ....................10% of increased assessed value to 100% of municipal

taxes - Minimum Construction Value .....No minimum to $10M - Applicable Area ...........................By Zone, OCP designation, BC

Assessment Designation or Specific Mapped Area

Key Benefits to a Hope RTEP Program

The following key benefits are the primary reason for AdvantageHOPE's advocacy for the adoption of an RTEP program

1. No lost tax revenue a. An RTEP program is designed to inspire developers and businesses to

embark on development and re-development projects that they would not have considered in the absence of this program.

2. More development, construction, and business start-ups a. An RTEP program is expected to create greater economic activity in the

District of Hope 3. Increased long-term revenue to the District of Hope

a. Once the RTEP certificate expires on any Parcel, the assessed value and subsequent tax revenue will be greater, positively impacting the future financial status of the District

4. Collaboration with Provincial Agencies a. With a well designed bylaw, and collaboration with BC Assessment and

other provincial agencies, AdvantageHOPE expects Hope's RTEP program to minimally impact staff resources

5. Competitiveness with Neighbouring Municipalities a. With Chilliwack, Abbotsford, and Merritt all using this tool, Hope is

currently at a competitive disadvantage 6. Inspires development to comply with all regulations

a. Benefit is dependent on compliance with all zoning and other regulations, therefore compelling new development to conform to design standards prescribed by the zoning bylaw and OCP

b. More visually appealing and visionary developments are likely to ensue 7. Scalability

a. Council may in the future decide to use this tool to incentify other activities such as

i. Residential Development, or ii. Brownfield Development

Administration Report Hope Business & Development Society

Advantage HOPE

AdvantageHOPE | Administration Report | RTEP Program | Page 4 of 8

DRAFT BYLAW 1337, 2013

Information Sources

The draft bylaw has been crafted with input from four main sources.

1) The Province of BC a. Community Charter b. Revitalization Tax Exemptions, A Primer on the Provisions in the Community

Charter (January 2008)

2) Existing programs in other municipalities. Ten municipalities with over 20 different bylaws were reviewed.

a. The main contributors to the final Draft Bylaw 1337 were the City of Chilliwack, the District of Logan Lake, and the City of Abbotsford

b. Advice and input from other Economic Development Officers and Planning officials was sought from the District of Logan Lake, the City of Chilliwack, and the District of Maple Ridge

3) AdvantageHOPE RTEP Task Force a. This Advisory Task Force has met twice, and been consulted by email on multiple

occasions. Members include: i. Gordon Younie, AdvantageHOPE Board Member

ii. Laurie French, AdvantageHOPE Board Member iii. Peter Robb, District Councillor / AdvantageHOPE Board Member iv. Scott Medlock, District Councillor / AdvantageHOPE Board Member v. Gerry Dyble, District Councillor

vi. Johanna Coughlin, Former District of Hope Director of Finance vii. Kent McKinnon, AdvantageHOPE Resource Panel Member

viii. Rob Pellegrino, local realtor and businessman

4) District of Hope Staff a. Several formal and informal meetings have occurred with District of Hope Staff

to ensure the RTEP process is designed effectively to maximize community benefit and process clarity while minimizing staff administrative time required.

b. Two distinct areas are proposed as part of Hope's RTEP, both being tied to the District of Hope's zoning bylaw. Close linkages were identified as being critical to simplicity and future congruency: if adopted as proposed, an RTEP bylaw would change in lockstep with any future zoning bylaw changes.

Administration Report Hope Business & Development Society

Advantage HOPE

AdvantageHOPE | Administration Report | RTEP Program | Page 5 of 8

Continued Points of Discussion

Bylaw 1337 has been crafted to take into account many views and objectives of the community. In addition to work remaining to ensure that the process will work well and that the document works well with partner agencies such as BC Assessment and Land Titles Office, the following items are key to the substance of the Bylaw and remain topics of discussion for District Staff and the RTEP task force. We therefore ask for Council's input and direction on these topics.

A strong desire of the Task Force was to ensure that the Downtown Core had access to a greater benefit than other commercial areas, in congruence with direction from the OCP and the Economic Development Plan. However, there is also a strong desire to ensure the program is simple to both administer and explain to clients. Therefore, it is desirable that either the investment thresholds or the length of benefit be designed to better benefit that area. With that in mind, following are discussion points that remain unresolved.

1. Investment Thresholds

a. View 1 - Low Thresholds to encourage many applications

i. For example, $20,000 minimum for renovations or façade improvements, $200,000 minimum for new construction

1. Positive a. Likely to benefit existing Property Owners b. Greater uptake, more applications

2. Negative

a. Small investments generate very modest benefits under the program, possibly making the work required to apply for and administer the program costly when compared to the economic benefit to the community

b. Greater amounts of Staff Time may take focus away from larger projects

c. Since only one RTEP program can be active on any one property at one time, a small investment in the short term may prevent a larger investment from qualifying in the future

b. View 2 - High Thresholds to encourage greater investment and offer greater benefits

Administration Report Hope Business & Development Society

Advantage HOPE

AdvantageHOPE | Administration Report | RTEP Program | Page 6 of 8

i. For example, $50,000 or $75,000 minimum for renovations or façade improvements, $300,000 or $400,000 minimum for new construction

1. Positive a. Likely to attract both investment from local investors and

investment from new residents. b. Fewer applications (less staff time) yet potentially greater

community economic impact

2. Negative a. Less likely to benefit Property Owners wishing to engage in

small façade improvements

c. QUESTION: What is Council's general view on Investment Thresholds in both the Downtown Revitalization Area and the Industrial Commercial Revitalization Area?

2. Length of Benefit

a. Current DRAFT Bylaw

i. 7 year program for Commercial - Industrial, first two years with a 100% exemption from the Increased Assessment

ii. 10 year program for Downtown, first two years with a 100% exemption from the Increased Assessment

b. QUESTION: What is Council's general view on Length of Benefit in both the Downtown Revitalization Area and the Industrial Commercial Revitalization Area?

3. Scale / Amount of Benefit

a. View 1 - Give a 100% exemption on the Increased Assessed Value for 1 to 3 years, then gradually decrease the exemption over a period of years

i. Positive 1. Excellent up front incentive 2. Excellent support for developers

Administration Report Hope Business & Development Society

Advantage HOPE

AdvantageHOPE | Administration Report | RTEP Program | Page 7 of 8

3. Property Owner is not faced with a single substantial rise in taxes at the program end

4. Proven design - many municipalities use this model (usually larger than Hope)

ii. Negative 1. Greater likelihood of errors or backlog due to the necessity of

calculations every year 2. Greater complexity

b. View 2 - Give a larger exemption for either the full duration of the incentive

period, or only 1 graduation (to 50% for instance)

i. Positive 1. Simple Design

a. Easier to explain 2. Simpler to Administer

b. Less staff time 3. Possible to have a similar net benefit to the client over a shorter

program time 4. Seems to be more prevalent among smaller communities

ii. Negative

1. Property owner faced with a single substantial rise in taxes at the program end

c. QUESTION: What is Council's general view on Scale of Benefit in both the Downtown Revitalization Area and the Industrial Commercial Revitalization Area?

4. Level of BC Assessment Support

Also to be determined is the amount of support and/or participation that BC Assessment plays in this process. Greater levels of support from BC Assessment would alleviate the potential of greater administrative costs to the District of Hope and reduce the workload impact of the above options.

Administration Report Hope Business & Development Society

Advantage HOPE

AdvantageHOPE | Administration Report | RTEP Program | Page 8 of 8

Conclusion

AdvantageHOPE looks forward to continued collaboration with the District of Hope Staff and Council, and looks forward to a completed Bylaw ready for 1st reading in June or July.

It is expected that the Hope RTEP program will be ready for its first applicants on January 1st, 2014.

Sincerely,

22/05/2013

XTyler Mattheis

Executive Director, AdvantageHOPE

Revitalization Tax Exemptions

A Primer on the Provisions in the Community Charter

January 2008

_____________________________________________________________________________________________ Revitalization Tax Exemptions: A Primer on the Provisions in the Community Charter Page 2

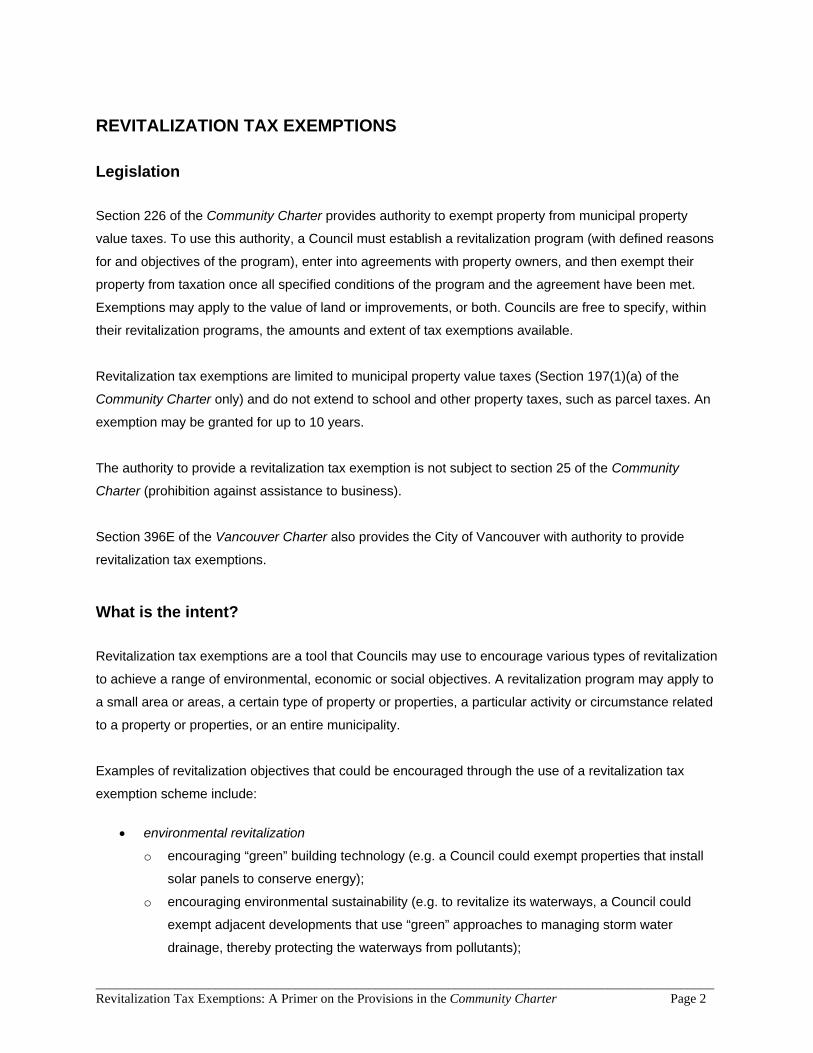

REVITALIZATION TAX EXEMPTIONS Legislation Section 226 of the Community Charter provides authority to exempt property from municipal property

value taxes. To use this authority, a Council must establish a revitalization program (with defined reasons

for and objectives of the program), enter into agreements with property owners, and then exempt their

property from taxation once all specified conditions of the program and the agreement have been met.

Exemptions may apply to the value of land or improvements, or both. Councils are free to specify, within

their revitalization programs, the amounts and extent of tax exemptions available.

Revitalization tax exemptions are limited to municipal property value taxes (Section 197(1)(a) of the

Community Charter only) and do not extend to school and other property taxes, such as parcel taxes. An

exemption may be granted for up to 10 years.

The authority to provide a revitalization tax exemption is not subject to section 25 of the Community

Charter (prohibition against assistance to business).

Section 396E of the Vancouver Charter also provides the City of Vancouver with authority to provide

revitalization tax exemptions.

What is the intent? Revitalization tax exemptions are a tool that Councils may use to encourage various types of revitalization

to achieve a range of environmental, economic or social objectives. A revitalization program may apply to

a small area or areas, a certain type of property or properties, a particular activity or circumstance related

to a property or properties, or an entire municipality.

Examples of revitalization objectives that could be encouraged through the use of a revitalization tax

exemption scheme include:

• environmental revitalization

o encouraging “green” building technology (e.g. a Council could exempt properties that install

solar panels to conserve energy);

o encouraging environmental sustainability (e.g. to revitalize its waterways, a Council could

exempt adjacent developments that use “green” approaches to managing storm water

drainage, thereby protecting the waterways from pollutants);

_____________________________________________________________________________________________ Revitalization Tax Exemptions: A Primer on the Provisions in the Community Charter Page 3

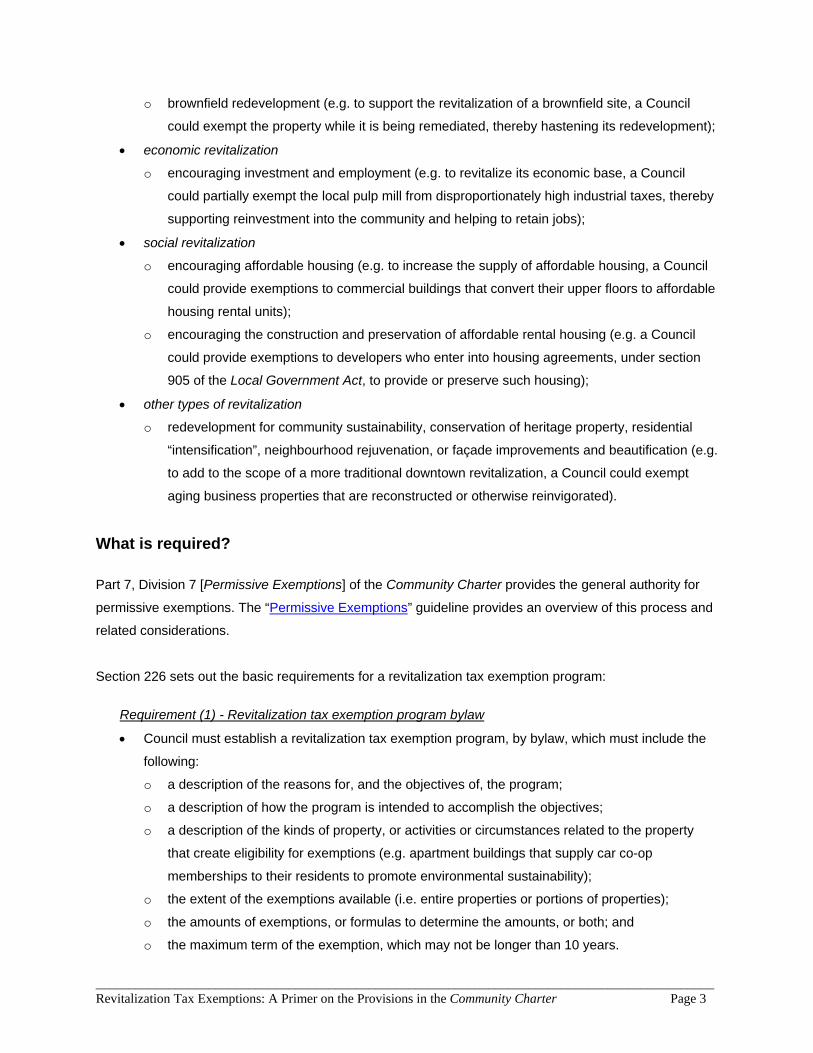

o brownfield redevelopment (e.g. to support the revitalization of a brownfield site, a Council

could exempt the property while it is being remediated, thereby hastening its redevelopment);

• economic revitalization

o encouraging investment and employment (e.g. to revitalize its economic base, a Council

could partially exempt the local pulp mill from disproportionately high industrial taxes, thereby

supporting reinvestment into the community and helping to retain jobs);

• social revitalization

o encouraging affordable housing (e.g. to increase the supply of affordable housing, a Council

could provide exemptions to commercial buildings that convert their upper floors to affordable

housing rental units);

o encouraging the construction and preservation of affordable rental housing (e.g. a Council

could provide exemptions to developers who enter into housing agreements, under section

905 of the Local Government Act, to provide or preserve such housing);

• other types of revitalization

o redevelopment for community sustainability, conservation of heritage property, residential

“intensification”, neighbourhood rejuvenation, or façade improvements and beautification (e.g.

to add to the scope of a more traditional downtown revitalization, a Council could exempt

aging business properties that are reconstructed or otherwise reinvigorated).

What is required? Part 7, Division 7 [Permissive Exemptions] of the Community Charter provides the general authority for

permissive exemptions. The “Permissive Exemptions” guideline provides an overview of this process and

related considerations.

Section 226 sets out the basic requirements for a revitalization tax exemption program:

Requirement (1) - Revitalization tax exemption program bylaw

• Council must establish a revitalization tax exemption program, by bylaw, which must include the

following:

o a description of the reasons for, and the objectives of, the program;

o a description of how the program is intended to accomplish the objectives;

o a description of the kinds of property, or activities or circumstances related to the property

that create eligibility for exemptions (e.g. apartment buildings that supply car co-op

memberships to their residents to promote environmental sustainability);

o the extent of the exemptions available (i.e. entire properties or portions of properties);

o the amounts of exemptions, or formulas to determine the amounts, or both; and

o the maximum term of the exemption, which may not be longer than 10 years.

_____________________________________________________________________________________________ Revitalization Tax Exemptions: A Primer on the Provisions in the Community Charter Page 4

• Council may also include in its revitalization program bylaw:

o the requirements that must be met before an exemption certificate may be issued;

o conditions that must be included in the exemption certificate;

o provisions for a recapture amount that must be paid if the conditions specified in the

certificate are not met.

• A revitalization program bylaw may be different, for different:

o areas of the municipality;

o property classes;

o classes of land and improvements, or both, as established by the bylaw;

o activities and circumstances related to a property or its uses, as established by the bylaw,

and;

o uses as established by zoning bylaw.

• Before adopting it, Council must consider the revitalization tax exemption program bylaw in

conjunction with the objectives and policies as set out under section 165(3.1)(c) [use of

permissive tax exemptions] of the Community Charter. The intent is that Council consider the

municipality’s overall objectives and policies in relation to permissive tax exemptions, when

exercising its revitalization tax exemption powers.

• Council must also, prior to adopting the revitalization tax exemption program bylaw, fulfill the

general requirements for public notice as set out under section 94 of the Community Charter

(section 94 specifies, for example, the requirement for notices to be publicly posted, and

published in a newspaper for two consecutive weeks). Section 227 [notice of permissive tax

exemptions] sets out the specific notice requirements in relation to a revitalization tax exemption

program bylaw. A revitalization tax exemption program bylaw notice must include a general

description of:

o the reasons for, and objectives of, the program;

o how the program is intended to accomplish the objectives;

o the kinds of property, or activities or circumstances that are eligible for an exemption; and

o the extent, amounts and maximum terms of tax exemptions that may be provided.

Requirement (2) - Agreement with property owner

• Once a revitalization tax exemption program bylaw has been adopted, Council may enter into an

agreement with the owner of a property regarding the provision of a revitalization tax exemption.

The agreement between the municipality and the property owner may outline requirements that

must be met before an exemption certificate is issued, and any other conditions on which the tax

exemption will be provided.

_____________________________________________________________________________________________ Revitalization Tax Exemptions: A Primer on the Provisions in the Community Charter Page 5

• The agreement with the property owner provides Council with an opportunity to build on the

program bylaw by enabling Council to provide a more specific level of detail regarding the

conditions of an exemption as they relate to a particular property. Essentially, the agreement is

intended to take the program bylaw to another level of specificity.

Requirement (3) - Tax exemption certificate

• Once all of the requirements established in the bylaw and in the agreement have been met, a

revitalization tax exemption certificate must be issued for the property that is the subject of the

agreement. This certificate must be issued no later than October 31 in the year before the tax

exemption takes effect.

• As soon as practicable, a copy of the certificate must be provided to the assessor. This ensures

that any tax exemptions related to a property are taken into account by

BC Assessment during the calculation of the taxable value of a property.

What to consider? Council is not obliged to establish a revitalization tax exemption program. This is a tool that Council may

use at its discretion. In addition to the requirement to consider its objectives and policies in relation to the

use of permissive tax exemptions (as set out under section 165(3.1)(c) of the Community Charter),

Council may wish to consider some additional factors in the design of any revitalization tax exemption

program, such as:

• What may be the immediate and long-term implications of the exemption program on:

o the community - what are the municipality’s objectives for the environmental, economic and

social well-being of the community, and how might the exemption program help fulfill such

objectives?

o the municipality - what will such an exemption program cost the municipality in terms of lost

tax revenue, overhead to manage the program, and other costs (such as any costs

associated with servicing a new development)?

o the municipality’s larger operating environment - is the exemption program consistent with the

BC/Alberta Trade, Investment and Labour Mobility Agreement under which investment

distorting subsidies are prohibited?

• What is the “right” amount of tax relief to encourage the desired level of revitalization under an

exemption program?

• Is this type of revitalization likely to occur without any tax incentives in place?

• What other benefits might occur as a result of the exemption program (e.g. a tax exemption that

partially exempts the local pulp mill from disproportionately high industrial taxes might support

reinvestment into the community while helping to retain jobs)?

_____________________________________________________________________________________________ Revitalization Tax Exemptions: A Primer on the Provisions in the Community Charter Page 6

• Tax shift. How will the program impact the property taxes of other properties in the same

assessment class, and the taxes of properties in other classes of assessment?

• Can Council clearly explain its intentions to the public and demonstrate how the program

supports municipal purposes? And what does the community think about the proposal?

Frequently Asked Questions Aren’t municipalities required to designate an area to provide revitalization tax exemptions? Not anymore. Amendments to section 226 of the Community Charter (via Bill 35, the Miscellaneous

Statues Amendment Act (No.2) 2007) came into effect on May 31, 2007. These amendments broadened

the revitalization tax exemption tool in a number of ways, including by eliminating the requirement to

designate an area for revitalization purposes. The new broadened tax exemption tool is a much more

flexible and adaptable tool that can be used by Council to meet any type of revitalization need.

What will happen to revitalization tax exemption program bylaws and their corresponding agreements and certificates that were in place before the broadened revitalization tax exemption tool came into effect on May 31, 2007? Transitional provisions (under Bill 35) ensure that all existing revitalization tax exemption program bylaws,

and their corresponding agreements and certificates that were in place before the tool was broadened,

can continue. However, if a municipality chooses to amend its revitalization program bylaw (to, for

example, expand the scope of the types of property that could be exempted), it must comply with the

requirements under the new, broadened section 226.

What does the legislation mean in section 226(5)(b) when it says that a program may be different for “different classes of property” and “different classes of land or improvements or both”? This means that Council may use any criteria to identify the property that will be eligible for tax relief. For

example, a class of property might include all the homes that were built before a certain date, or all the

buildings that front on certain streets, whereas a class of land may include all contaminated brownfield

sites within the municipality. These distinctions are designed to provide Council with the greatest flexibility

to determine how best to provide a tax exemption.

What is the difference between “activities” and “circumstances” as specified under section 226(5)(b)(iv) of the legislation? Under the legislation, a Council could choose to exempt property based on certain types of activities

related to a property (such as the distribution of a free bicycle to each resident living in a condominium

_____________________________________________________________________________________________ Revitalization Tax Exemptions: A Primer on the Provisions in the Community Charter Page 7

building as an incentive to reduce vehicle use), or it could choose to exempt certain circumstances

related to a property (such as the presence of solar panels on a property that are helping to reduce the

burden on the community’s energy grid). Essentially, activities require property owners to do something to

receive an exemption (such as remediate a brownfield site), and circumstances require that there be

particular conditions or factors related to the property in place that the municipality is interested in

promoting (such as whether properties are LEED certified or not). This distinction enables municipalities

to apply tax exemptions in the most flexible manner, to meet their individual revitalization needs.

Can a revitalization tax exemption be transferred to a new property owner? This is a decision for Council. The legislation specifies that a tax exemption certificate must be issued “for

the property” once all the conditions in the bylaw and the agreement have been met. So the tax

exemption applies to the property. However, section 226(6) permits Council to enter an agreement with a

property owner respecting the provision of a section 226 tax exemption “and the conditions on which it is

made”. One such condition might be that the exemption no longer applies if the property changes

ownership.

What’s the difference between a section 225 exemption for heritage property and using section 226 to exempt heritage property? A Council may decide to use either section 225 or section 226 as a way to encourage heritage

preservation within the municipality.

If they wish to use section 225, the property must be “eligible heritage property” that meets one of the

conditions in section 225(2)(b). For these purposes, heritage property is defined in the Local Government

Act. In contrast, section 226 provides a way to encourage investment in property with heritage

characteristics without using a formal designation process.

A heritage tax exemption exempts property from all property value taxes – provincial and municipal –

while a section 226 exemption only applies to the municipal portion. Another important difference is that

section 225 does not provide a time limit on heritage exemptions, while section 226 limits the benefit to 10

years. In addition, a heritage exemption bylaw requires the approval of two-thirds of all Council members;

a section 226 exemption bylaw requires a simple majority vote. Both section 225 and 226 permit Council

to impose conditions under which the tax exemption is granted.

_____________________________________________________________________________________________ Revitalization Tax Exemptions: A Primer on the Provisions in the Community Charter Page 8

What is the BC/Alberta Trade, Investment and Labour Mobility Agreement (TILMA) and why do municipalities need to consider it when providing revitalization tax exemptions? TILMA is an inter-provincial trade agreement between B.C. and Alberta that is designed to help eliminate

barriers to trade and to enhance the competitiveness and stability of both provinces. The agreement

came into force on April 1, 2007.

Although local governments are not parties to the agreement, their measures, including any legislation,

regulation, standard, directive, requirement, guideline, policy or program (such as a revitalization tax

exemption program), are subject to TILMA. More specifically, Article 12 of the agreement prohibits both

the provinces of B.C. and Alberta, as well as their local governments, from providing unfair, investment

distorting business subsidies. This means that any revitalization tax exemption provided by a Council

must be compliant with Article 12 of the agreement.

Although TILMA prohibits investment distorting business subsidies, it does not prohibit Council from

promoting the environmental, economic and social well-being of their communities. Councils are free to

use the tax exemption tool in a number of ways to promote various forms of community revitalization, so

long as they use the tool in a non-discriminatory, non-distorting manner and in a manner that does not

result in investment-distorting subsidies to business.

For more information: Contact the Local Government Infrastructure and Finance Branch Address: Local Government Infrastructure & Finance Division

Ministry of Community Services 4th Floor, 800 Johnson Street PO Box 9838 Stn Prov Govt Victoria, BC V8W 9T1

Phone: 250 387-4060 (in Victoria) Toll Free: Call 604-660-2421 (in Vancouver) or 1-800-663-7867 (elsewhere in B.C.) and

request a transfer to 250 387-4060 in Victoria

Email: [email protected] Website: http://www.cserv.gov.bc.ca/lgd/infra/index.htm

District of Hope

DRAFT Hope Revitalization Tax Exemption Bylaw (RTEP)

Package

DRAFT Bylaw Package - As of May 21st, 2013

1) DRAFT Package Contents:

a) RTEP Information Sheet (1 page)

b) RTEP Process Flow Chart (1 page)

c) Revitalization Tax Exemption Bylaw No. 1337, 2013 (7 pages)

d) RTEP Application Form (2 pages)

e) RTEP Agreement (8 pages)

f) RTEP Certificate (2 pages)

Total Pages in the Package (including this cover): 22

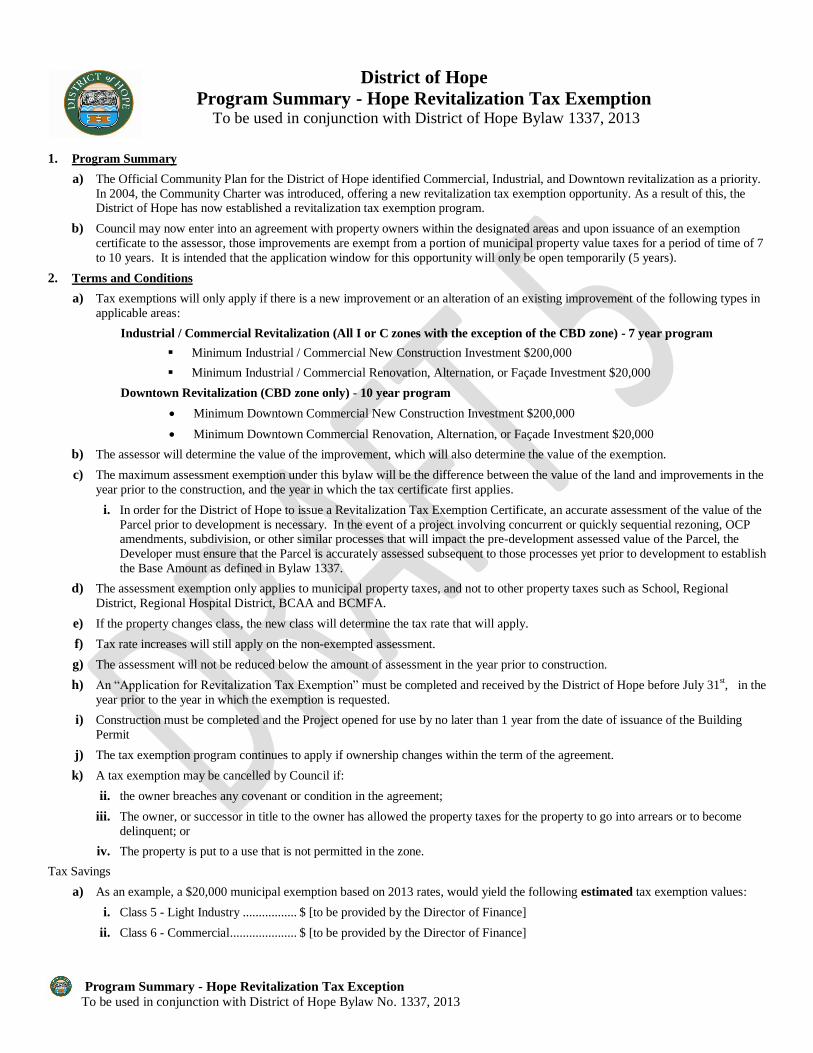

Program Summary - Hope Revitalization Tax Exception

To be used in conjunction with District of Hope Bylaw No. 1337, 2013

District of Hope

Program Summary - Hope Revitalization Tax Exemption To be used in conjunction with District of Hope Bylaw 1337, 2013

1. Program Summary

a) The Official Community Plan for the District of Hope identified Commercial, Industrial, and Downtown revitalization as a priority.

In 2004, the Community Charter was introduced, offering a new revitalization tax exemption opportunity. As a result of this, the District of Hope has now established a revitalization tax exemption program.

b) Council may now enter into an agreement with property owners within the designated areas and upon issuance of an exemption

certificate to the assessor, those improvements are exempt from a portion of municipal property value taxes for a period of time of 7

to 10 years. It is intended that the application window for this opportunity will only be open temporarily (5 years).

2. Terms and Conditions

a) Tax exemptions will only apply if there is a new improvement or an alteration of an existing improvement of the following types in

applicable areas:

Industrial / Commercial Revitalization (All I or C zones with the exception of the CBD zone) - 7 year program

Minimum Industrial / Commercial New Construction Investment $200,000

Minimum Industrial / Commercial Renovation, Alternation, or Façade Investment $20,000

Downtown Revitalization (CBD zone only) - 10 year program

Minimum Downtown Commercial New Construction Investment $200,000

Minimum Downtown Commercial Renovation, Alternation, or Façade Investment $20,000

b) The assessor will determine the value of the improvement, which will also determine the value of the exemption.

c) The maximum assessment exemption under this bylaw will be the difference between the value of the land and improvements in the

year prior to the construction, and the year in which the tax certificate first applies.

i. In order for the District of Hope to issue a Revitalization Tax Exemption Certificate, an accurate assessment of the value of the

Parcel prior to development is necessary. In the event of a project involving concurrent or quickly sequential rezoning, OCP amendments, subdivision, or other similar processes that will impact the pre-development assessed value of the Parcel, the

Developer must ensure that the Parcel is accurately assessed subsequent to those processes yet prior to development to establish

the Base Amount as defined in Bylaw 1337.

d) The assessment exemption only applies to municipal property taxes, and not to other property taxes such as School, Regional

District, Regional Hospital District, BCAA and BCMFA.

e) If the property changes class, the new class will determine the tax rate that will apply.

f) Tax rate increases will still apply on the non-exempted assessment.

g) The assessment will not be reduced below the amount of assessment in the year prior to construction.

h) An “Application for Revitalization Tax Exemption” must be completed and received by the District of Hope before July 31st, in the

year prior to the year in which the exemption is requested.

i) Construction must be completed and the Project opened for use by no later than 1 year from the date of issuance of the Building

Permit

j) The tax exemption program continues to apply if ownership changes within the term of the agreement.

k) A tax exemption may be cancelled by Council if:

ii. the owner breaches any covenant or condition in the agreement;

iii. The owner, or successor in title to the owner has allowed the property taxes for the property to go into arrears or to become

delinquent; or

iv. The property is put to a use that is not permitted in the zone.

Tax Savings

a) As an example, a $20,000 municipal exemption based on 2013 rates, would yield the following estimated tax exemption values:

i. Class 5 - Light Industry ................. $ [to be provided by the Director of Finance]

ii. Class 6 - Commercial ..................... $ [to be provided by the Director of Finance]

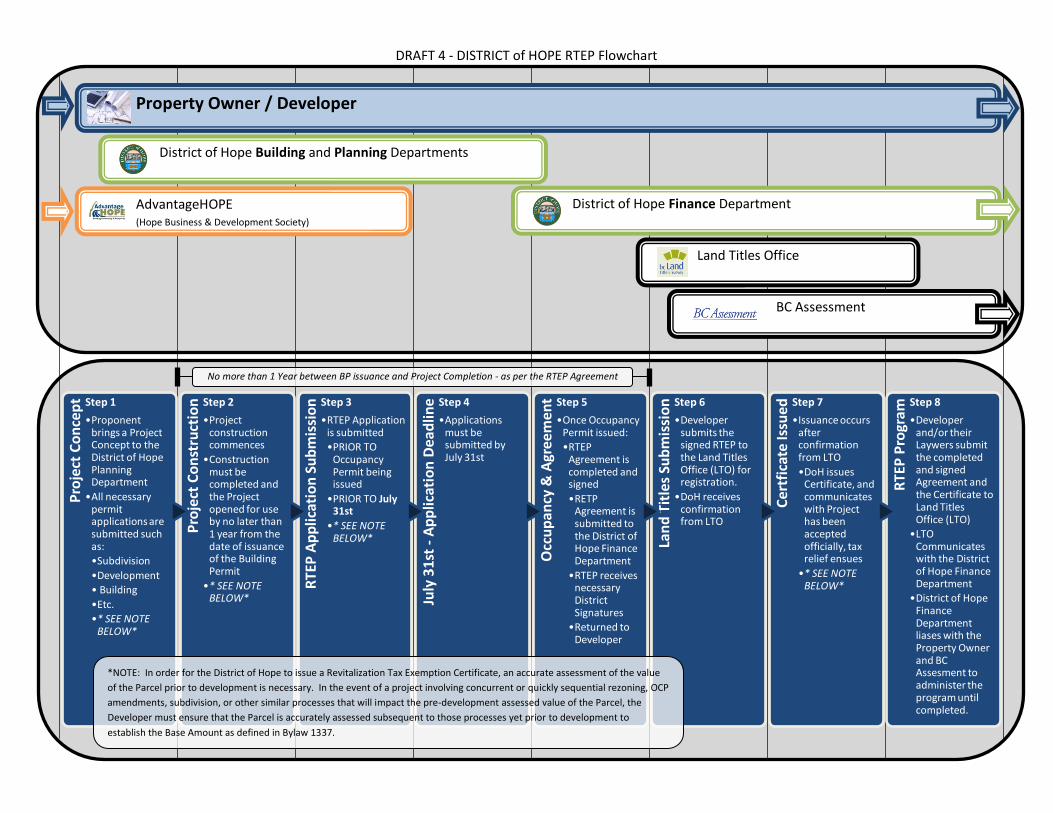

DRAFT 4 - DISTRICT of HOPE RTEP Flowchart

Property Owner / Developer

District of Hope Building and Planning Departments

District of Hope Finance Department

Land Titles Office

BC Assessment

AdvantageHOPE (Hope Business & Development Society)

Pro

ject

Co

nce

pt Step 1

•Proponent brings a Project Concept to the District of Hope Planning Department

•All necessary permit applications are submitted such as:

•Subdivision

•Development

• Building

•Etc.

•* SEE NOTE BELOW*

Pro

ject

Co

nst

ruct

ion

Step 2

•Project construction commences

•Construction must be completed and the Project opened for use by no later than 1 year from the date of issuance of the Building Permit

•* SEE NOTE BELOW*

RTE

P A

pp

licat

ion

Su

bm

issi

on

Step 3

•RTEP Application is submitted

•PRIOR TO Occupancy Permit being issued

•PRIOR TO July 31st

•* SEE NOTE BELOW*

July

31s

t -

Ap

plic

atio

n D

ead

line

Step 4

•Applications must be submitted by July 31st

Occ

up

ancy

& A

gree

men

t Step 5

•Once Occupancy Permit issued:

•RTEP Agreement is completed and signed

•RETP Agreement is submitted to the District of Hope Finance Department

•RTEP receives necessary District Signatures

•Returned to Developer

Lan

d T

itle

s Su

bm

issi

on

Step 6

•Developer submits the signed RTEP to the Land Titles Office (LTO) for registration.

•DoH receives confirmation from LTO

Cer

tfic

ate

Issu

ed

Step 7

•Issuance occurs after confirmation from LTO

•DoH issues Certificate, and communicates with Project has been accepted officially, tax relief ensues

•* SEE NOTE BELOW*

RTE

P P

rogr

am

Step 8

•Developer and/or their Laywers submit the completed and signed Agreement and the Certificate to Land Titles Office (LTO)

•LTO Communicates with the District of Hope Finance Department

•District of Hope Finance Department liases with the Property Owner and BC Assesment to administer the program until completed.

*NOTE: In order for the District of Hope to issue a Revitalization Tax Exemption Certificate, an accurate assessment of the value

of the Parcel prior to development is necessary. In the event of a project involving concurrent or quickly sequential rezoning, OCP

amendments, subdivision, or other similar processes that will impact the pre-development assessed value of the Parcel, the

Developer must ensure that the Parcel is accurately assessed subsequent to those processes yet prior to development to

establish the Base Amount as defined in Bylaw 1337.

No more than 1 Year between BP issuance and Project Completion - as per the RTEP Agreement

THE DISTRICT OF HOPE BYLAW NO. 1337, 2013

A Bylaw to establish a Revitalization Tax Exemption Program.

WHEREAS under Section 226 of the Community Charter, Council may, by bylaw, establish a Revitalization

Tax Exemption Program (RTEP);

AND WHEREAS Council wishes to establish a Revitalization Tax Exemption Program for specific

designated areas;

AND WHEREAS Council wishes to partner with the Hope Business and Development Society (Doing

Business As AdvantageHOPE) to promote economic development in our community;

AND WHEREAS the Community Charter provides that a revitalization tax exemption bylaw may only be

adopted after notice of the proposed bylaw has been given in accordance with Section 227 of the Community

Charter and council has given this notice;

NOW THEREFORE the Council of the District of Hope, in open meeting assembled, enacts as follows:

1) TITLE

This Bylaw may be cited for all purposes as the “District of Hope Revitalization Tax Exemption Bylaw

1337, 2013”.

2) TABLE OF CONTENTS

1) TITLE ................................................................................................................................................................... 1

2) TABLE OF CONTENTS ....................................................................................................................................... 1

3) DEFINITIONS ...................................................................................................................................................... 2

4) REVITALIZATION TAX EXEMPTION PROGRAM OBJECTIVES .................................................................. 2

5) REVITALIZATION TAX EXEMPTION PROGRAM ELIGIBILITY................................................................... 3

i) Commercial - Industrial Revitalization Tax Exemption ...................................................................................... 3

ii) Downtown Revitalization Tax Exemption.......................................................................................................... 4

6) EXTENT OF REVITALIZATION TAX EXEMPTION ........................................................................................ 5

7) REVITALIZATION TAX EXEMPTION PROGRAM APPLICATION ................................................................ 5

8) TAX EXEMPTION CERTIFICATE...................................................................................................................... 6

9) REVITALIZATION TAX EXEMPTION CERTIFICATE CANCELLATION ...................................................... 6

10) RECAPTURE OF EXEMPTED TAXES ........................................................................................................... 6

11) SEVERABILITY .............................................................................................................................................. 7

12) DESIGNATED MUNICIPAL OFFICER .......................................................................................................... 7

13) EFFECTIVE DATE .......................................................................................................................................... 7

3) DEFINITIONS

In this bylaw:

“Agreement” means a revitalization tax exemption agreement between the owner of a Parcel and the

District, in a format provided by the District of Hope;

"Base Amount" means an assessed value of land and improvements used to calculate municipal property

tax payable on a parcel located in the Revitalization Area during the Base Amount Year;

"Base Amount Year" means the calendar year before the construction of the Project;

"District" means the District of Hope;

"Full Assessment" means the amount of municipal property tax that would be payable in respect of a

Parcel in the Revitalization Tax Exemption Areas after the calendar year during which an Agreement is

made, as if the Agreement had never been made;

“Investment Threshold(s)” means the amount of capital investment required to be eligible to apply for

the Revitalization Tax Exemption Program;

"Increased Assessed Value" means the difference, as per values determined by the British Columbia

Assessment Authority, in the assessed value of a Parcel between:

(a) the Base Amount Year; and,

(b) the year in which the Tax Exemption Certificate is issued

“Parcel” has the same meaning as in the Schedule (Definition and Rules of Interpretation) to the

Community Charter;

“Project” means a revitalization project on a Parcel involving the construction of a new improvement or

alteration of an existing improvement;

“Revitalization Tax Exemption Areas” means areas that have been designated and defined in this

bylaw;

“Revitalization Tax Exemption Program Application” means an application to the District of Hope

for a Revitalization Tax Exemption according to this bylaw;

"Significant Development" means development that requires a capital investment that meets the

minimum requirements as described in Section 5: REVITALIZATION TAX EXEMPTION PROGRAM

ELIGIBILITY;

“Tax Exemption” means a revitalization tax exemption pursuant to a Tax Exemption Certificate;

“Tax Exemption Certificate” means a revitalization tax exemption certificate issued by the District

pursuant to this Bylaw and pursuant to the provisions of section 226 of the Community Charter.

4) REVITALIZATION TAX EXEMPTION PROGRAM OBJECTIVES

Pursuant to Section 226 of the Community Charter, the District of Hope Council hereby establishes a

Revitalization Tax Exemption Program as follows:

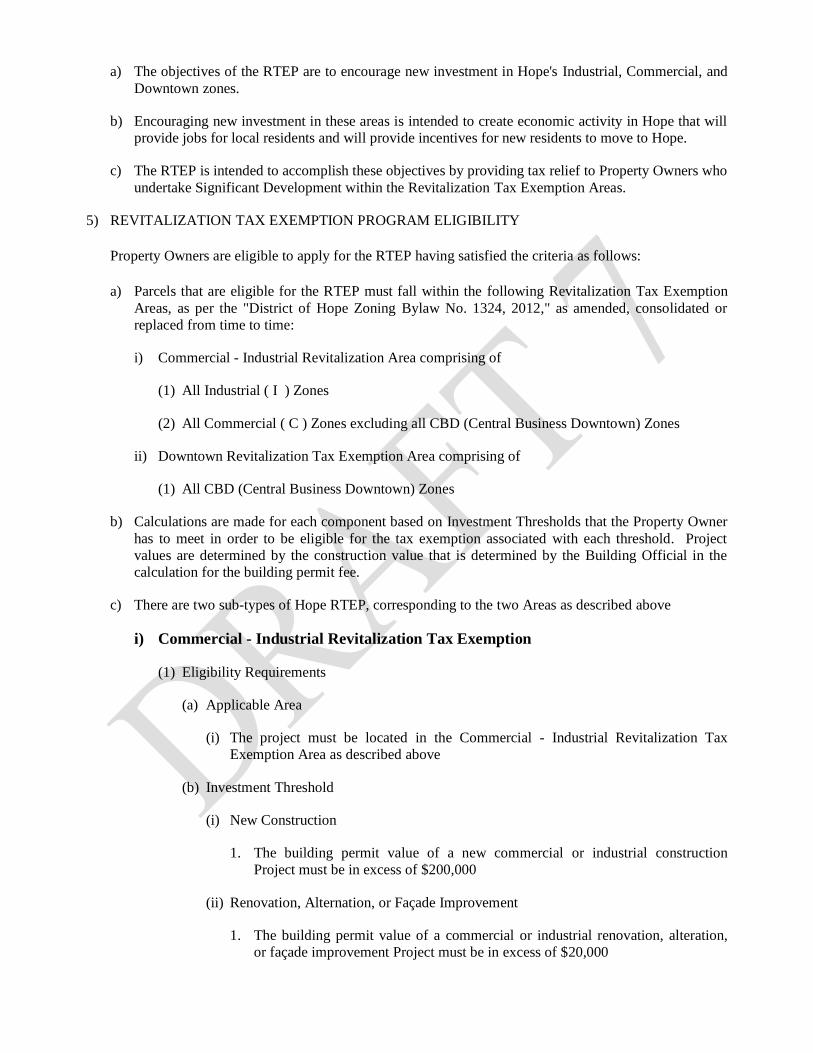

a) The objectives of the RTEP are to encourage new investment in Hope's Industrial, Commercial, and

Downtown zones.

b) Encouraging new investment in these areas is intended to create economic activity in Hope that will

provide jobs for local residents and will provide incentives for new residents to move to Hope.

c) The RTEP is intended to accomplish these objectives by providing tax relief to Property Owners who

undertake Significant Development within the Revitalization Tax Exemption Areas.

5) REVITALIZATION TAX EXEMPTION PROGRAM ELIGIBILITY

Property Owners are eligible to apply for the RTEP having satisfied the criteria as follows:

a) Parcels that are eligible for the RTEP must fall within the following Revitalization Tax Exemption

Areas, as per the "District of Hope Zoning Bylaw No. 1324, 2012," as amended, consolidated or

replaced from time to time:

i) Commercial - Industrial Revitalization Area comprising of

(1) All Industrial ( I ) Zones

(2) All Commercial ( C ) Zones excluding all CBD (Central Business Downtown) Zones

ii) Downtown Revitalization Tax Exemption Area comprising of

(1) All CBD (Central Business Downtown) Zones

b) Calculations are made for each component based on Investment Thresholds that the Property Owner

has to meet in order to be eligible for the tax exemption associated with each threshold. Project

values are determined by the construction value that is determined by the Building Official in the

calculation for the building permit fee.

c) There are two sub-types of Hope RTEP, corresponding to the two Areas as described above

i) Commercial - Industrial Revitalization Tax Exemption

(1) Eligibility Requirements

(a) Applicable Area

(i) The project must be located in the Commercial - Industrial Revitalization Tax

Exemption Area as described above

(b) Investment Threshold

(i) New Construction

1. The building permit value of a new commercial or industrial construction

Project must be in excess of $200,000

(ii) Renovation, Alternation, or Façade Improvement

1. The building permit value of a commercial or industrial renovation, alteration,

or façade improvement Project must be in excess of $20,000

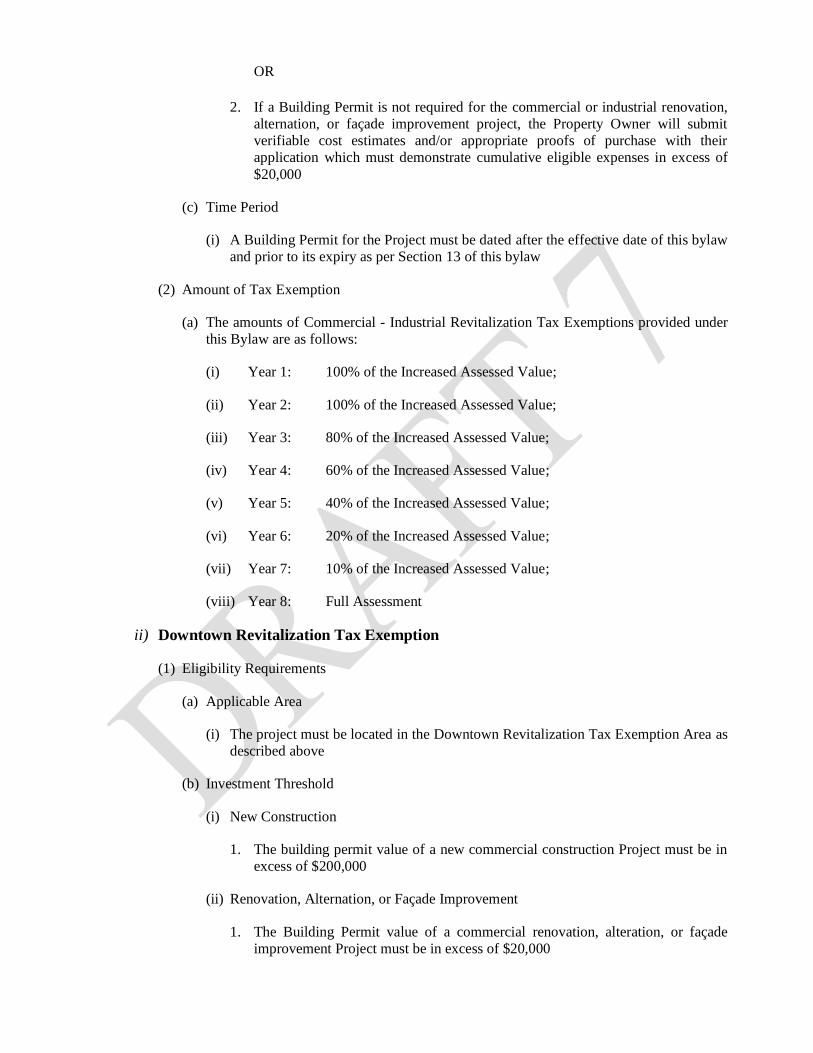

OR

2. If a Building Permit is not required for the commercial or industrial renovation,

alternation, or façade improvement project, the Property Owner will submit

verifiable cost estimates and/or appropriate proofs of purchase with their

application which must demonstrate cumulative eligible expenses in excess of

$20,000

(c) Time Period

(i) A Building Permit for the Project must be dated after the effective date of this bylaw

and prior to its expiry as per Section 13 of this bylaw

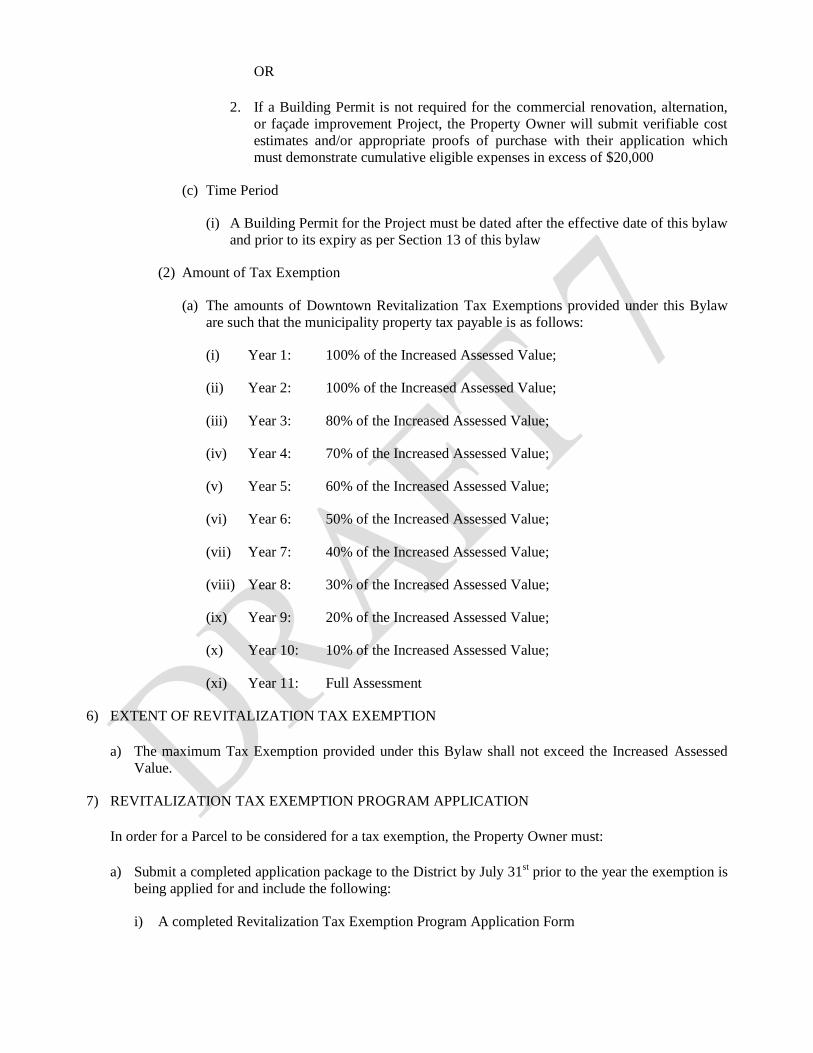

(2) Amount of Tax Exemption

(a) The amounts of Commercial - Industrial Revitalization Tax Exemptions provided under

this Bylaw are as follows:

(i) Year 1: 100% of the Increased Assessed Value;

(ii) Year 2: 100% of the Increased Assessed Value;

(iii) Year 3: 80% of the Increased Assessed Value;

(iv) Year 4: 60% of the Increased Assessed Value;

(v) Year 5: 40% of the Increased Assessed Value;

(vi) Year 6: 20% of the Increased Assessed Value;

(vii) Year 7: 10% of the Increased Assessed Value;

(viii) Year 8: Full Assessment

ii) Downtown Revitalization Tax Exemption

(1) Eligibility Requirements

(a) Applicable Area

(i) The project must be located in the Downtown Revitalization Tax Exemption Area as

described above

(b) Investment Threshold

(i) New Construction

1. The building permit value of a new commercial construction Project must be in

excess of $200,000

(ii) Renovation, Alternation, or Façade Improvement

1. The Building Permit value of a commercial renovation, alteration, or façade

improvement Project must be in excess of $20,000

OR

2. If a Building Permit is not required for the commercial renovation, alternation,

or façade improvement Project, the Property Owner will submit verifiable cost

estimates and/or appropriate proofs of purchase with their application which

must demonstrate cumulative eligible expenses in excess of $20,000

(c) Time Period

(i) A Building Permit for the Project must be dated after the effective date of this bylaw

and prior to its expiry as per Section 13 of this bylaw

(2) Amount of Tax Exemption

(a) The amounts of Downtown Revitalization Tax Exemptions provided under this Bylaw

are such that the municipality property tax payable is as follows:

(i) Year 1: 100% of the Increased Assessed Value;

(ii) Year 2: 100% of the Increased Assessed Value;

(iii) Year 3: 80% of the Increased Assessed Value;

(iv) Year 4: 70% of the Increased Assessed Value;

(v) Year 5: 60% of the Increased Assessed Value;

(vi) Year 6: 50% of the Increased Assessed Value;

(vii) Year 7: 40% of the Increased Assessed Value;

(viii) Year 8: 30% of the Increased Assessed Value;

(ix) Year 9: 20% of the Increased Assessed Value;

(x) Year 10: 10% of the Increased Assessed Value;

(xi) Year 11: Full Assessment

6) EXTENT OF REVITALIZATION TAX EXEMPTION

a) The maximum Tax Exemption provided under this Bylaw shall not exceed the Increased Assessed

Value.

7) REVITALIZATION TAX EXEMPTION PROGRAM APPLICATION

In order for a Parcel to be considered for a tax exemption, the Property Owner must:

a) Submit a completed application package to the District by July 31st prior to the year the exemption is

being applied for and include the following:

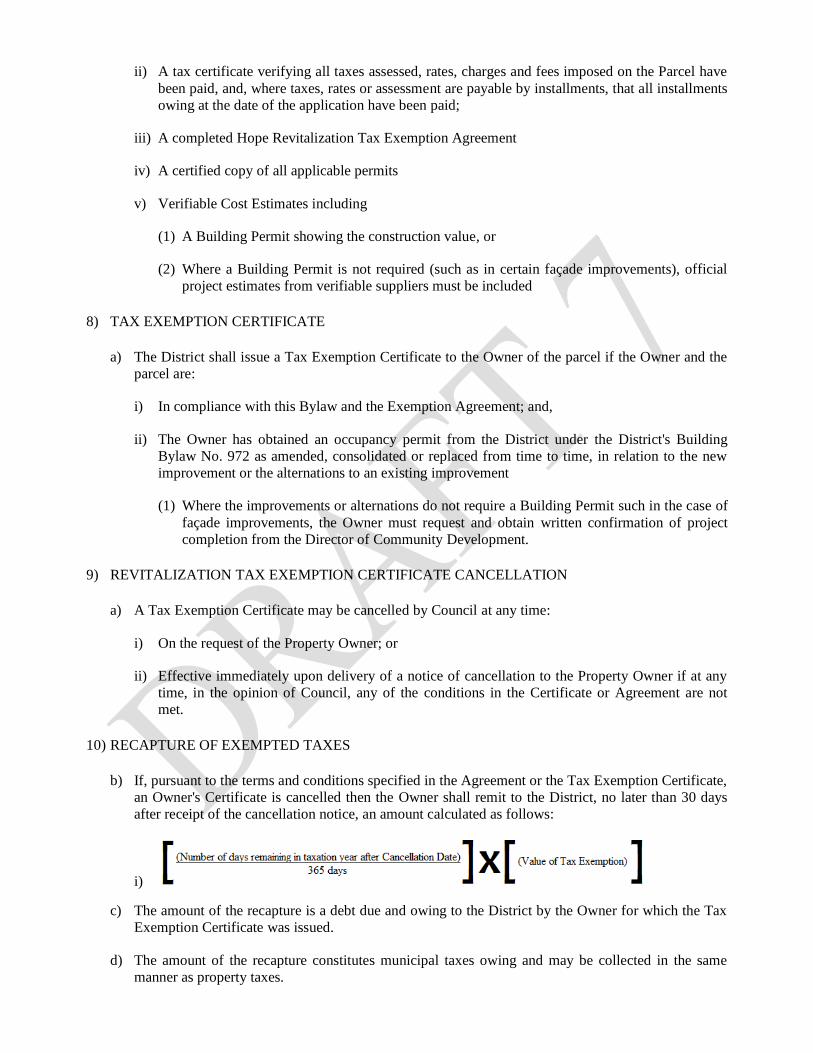

i) A completed Revitalization Tax Exemption Program Application Form

ii) A tax certificate verifying all taxes assessed, rates, charges and fees imposed on the Parcel have

been paid, and, where taxes, rates or assessment are payable by installments, that all installments

owing at the date of the application have been paid;

iii) A completed Hope Revitalization Tax Exemption Agreement

iv) A certified copy of all applicable permits

v) Verifiable Cost Estimates including

(1) A Building Permit showing the construction value, or

(2) Where a Building Permit is not required (such as in certain façade improvements), official

project estimates from verifiable suppliers must be included

8) TAX EXEMPTION CERTIFICATE

a) The District shall issue a Tax Exemption Certificate to the Owner of the parcel if the Owner and the

parcel are:

i) In compliance with this Bylaw and the Exemption Agreement; and,

ii) The Owner has obtained an occupancy permit from the District under the District's Building

Bylaw No. 972 as amended, consolidated or replaced from time to time, in relation to the new

improvement or the alternations to an existing improvement

(1) Where the improvements or alternations do not require a Building Permit such in the case of

façade improvements, the Owner must request and obtain written confirmation of project

completion from the Director of Community Development.

9) REVITALIZATION TAX EXEMPTION CERTIFICATE CANCELLATION

a) A Tax Exemption Certificate may be cancelled by Council at any time:

i) On the request of the Property Owner; or

ii) Effective immediately upon delivery of a notice of cancellation to the Property Owner if at any

time, in the opinion of Council, any of the conditions in the Certificate or Agreement are not

met.

10) RECAPTURE OF EXEMPTED TAXES

b) If, pursuant to the terms and conditions specified in the Agreement or the Tax Exemption Certificate,

an Owner's Certificate is cancelled then the Owner shall remit to the District, no later than 30 days

after receipt of the cancellation notice, an amount calculated as follows:

i)

c) The amount of the recapture is a debt due and owing to the District by the Owner for which the Tax

Exemption Certificate was issued.

d) The amount of the recapture constitutes municipal taxes owing and may be collected in the same

manner as property taxes.

11) SEVERABILITY

a) The provisions of this Bylaw are severable, and if, for any reason, any subdivision, part, section,

subsection, clause, or sub-clause, or other words in this Bylaw are, for any reason, found to be

invalid or unenforceable by the decision of a Court of competent jurisdiction, then that decision shall

no affect the validity of the remaining portions of this Bylaw.

12) DESIGNATED MUNICIPAL OFFICER

a) The Director of Finance for the District is the designated municipal officer for the purpose of section

226 (13) in the Community Charter.

13) EFFECTIVE DATE

a) This bylaw will take effect on September 30th, 2013 and is valid until September 30th, 2018.

Read a first time by the Municipal Council this ___ day of ____, 2013.

Read a second time by the Municipal Council this ___ day of ____, 2013.

Read a third time by the Municipal Council this ___ day of ____, 2013.

Adopted by the Municipal Council of the Municipality of Hope this ___ day of ______, 2013.

___________________________ ________________________________

Mayor Director of Corporate Services

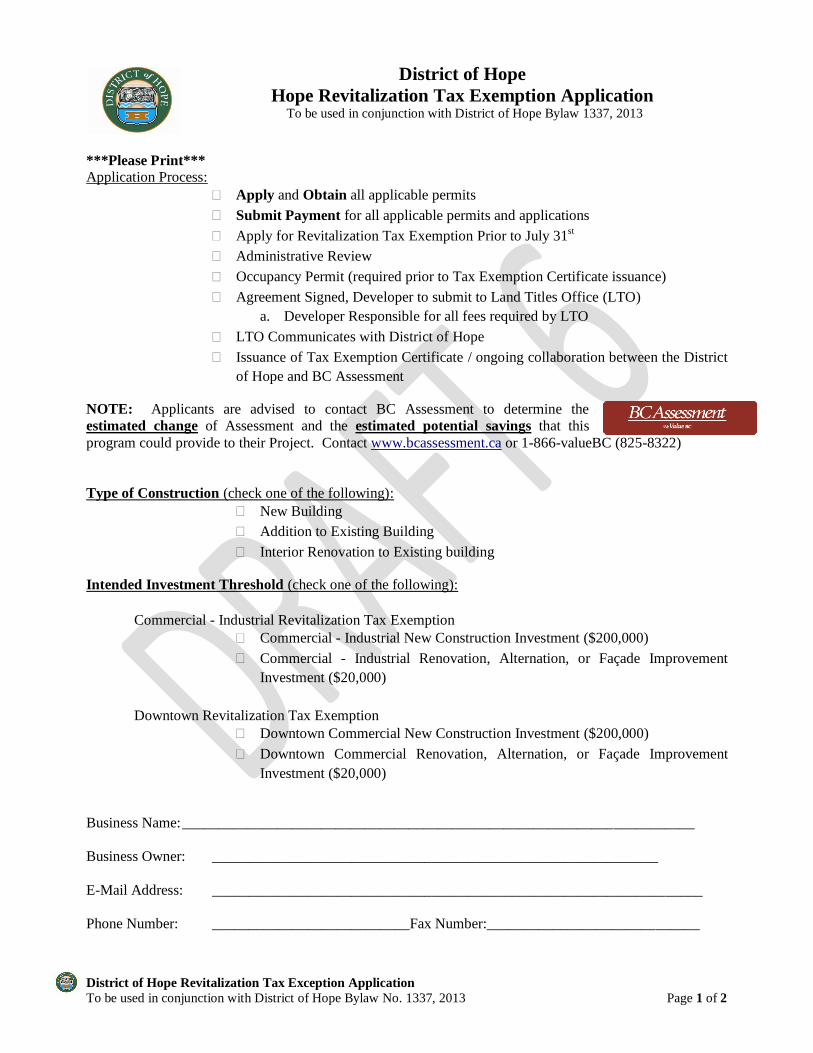

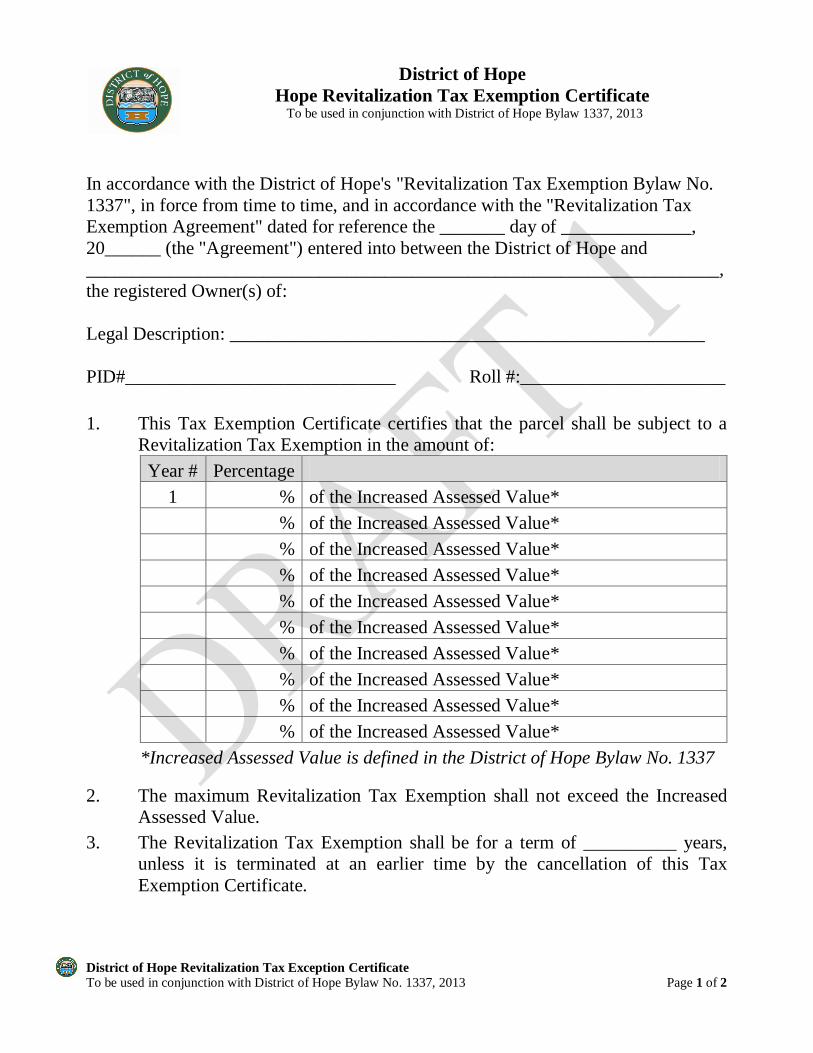

District of Hope Revitalization Tax Exception Application

To be used in conjunction with District of Hope Bylaw No. 1337, 2013 Page 1 of 2

District of Hope

Hope Revitalization Tax Exemption Application To be used in conjunction with District of Hope Bylaw 1337, 2013

***Please Print***

Application Process:

Apply and Obtain all applicable permits

Submit Payment for all applicable permits and applications

Apply for Revitalization Tax Exemption Prior to July 31st

Administrative Review

Occupancy Permit (required prior to Tax Exemption Certificate issuance)

Agreement Signed, Developer to submit to Land Titles Office (LTO)

a. Developer Responsible for all fees required by LTO

LTO Communicates with District of Hope

Issuance of Tax Exemption Certificate / ongoing collaboration between the District

of Hope and BC Assessment

NOTE: Applicants are advised to contact BC Assessment to determine the

estimated change of Assessment and the estimated potential savings that this

program could provide to their Project. Contact www.bcassessment.ca or 1-866-valueBC (825-8322)

Type of Construction (check one of the following):

New Building

Addition to Existing Building

Interior Renovation to Existing building

Intended Investment Threshold (check one of the following):

Commercial - Industrial Revitalization Tax Exemption

Commercial - Industrial New Construction Investment ($200,000)

Commercial - Industrial Renovation, Alternation, or Façade Improvement

Investment ($20,000)

Downtown Revitalization Tax Exemption

Downtown Commercial New Construction Investment ($200,000)

Downtown Commercial Renovation, Alternation, or Façade Improvement

Investment ($20,000)

Business Name: ______________________________________________________________________

Business Owner: _____________________________________________________________

E-Mail Address: ___________________________________________________________________

Phone Number: ___________________________Fax Number:_____________________________

District of Hope Revitalization Tax Exception Application

To be used in conjunction with District of Hope Bylaw No. 1337, 2013 Page 2 of 2

Mailing Address: ___________________________________________________________________

___________________________________________________________________

Business License Number:__________Building Permit Number: ________________________________

Legal Description: ___________________________________________________________________

PID#______________________________________ Roll #:___________________________

Civic Address of Construction:___________________________________________________________

Building Permit Number: _______________________________________________________________

Building Permit Estimated Project Value:__________________________________________________

Start Date: ______________________________Completion Date:______________________________

Description of Improvements:

Attach all of the following items to this application

Drawings, photos, and site plans of the project

Black and White Renderings of the Project (required for Land Titles Office)

Written Description of the Project

Written Description of the Community Benefit and/or Contribution that will

result from this project

Nature of Business: ___________________________________________________________________

Estimated New Jobs to be Created:_______________________________________________________

Intended first year of tax exemption: 20____

If any of the above information needs to be treated as confidential, please indicate reasons:

___________________________________________________________________________________

___________________________________________________________________________________

___________________________________________________________________________________

Declaration of Applicant

I (We), ______________________________ solemnly declare that all the above statements contained within

the Application are true, and I make this solemn declaration conscientiously believing it to be true, knowing

that it is the same force and effect as if made under oath, and by virtue of : The Canada Evidence Act.”

Dated: ___________________________________

Signature: ________________________________

District of Hope Revitalization Tax Exception Agreement

To be used in conjunction with District of Hope Bylaw No. 1337, 2013 Page 1 of 8

District of Hope

Hope Revitalization Tax Exemption Agreement To be used in conjunction with District of Hope Bylaw 1337, 2013

THIS AGREEMENT dated for reference the _____day of ________, 20_____

BETWEEN:

(Name):__________________________________________________________

(Address):________________________________________________________

(the “Property Owner”)

AND:

Corporation of the District of Hope

325 Wallace Street

Hope, BC

V0X 1L0

(the “District”)

TABLE OF CONTENTS

TABLE OF CONTENTS ............................................................................................................................................... 1

GIVEN THAT: .............................................................................................................................................................. 2

TERMS AND CONDITIONS ........................................................................................................................................ 2

1) PROPERTY OWNER OBLIGATIONS ............................................................................................................. 2

2) DISTRICT'S RIGHTS AND POWERS .............................................................................................................. 3

3) COVENANTS ................................................................................................................................................... 3

4) REPRESENTATIONS AND WARRANTIES ................................................................................................... 3

5) CONDITIONS ................................................................................................................................................... 4

6) STRATIFICATION ........................................................................................................................................... 4

7) NO REFUND..................................................................................................................................................... 5

8) NO ASSIGNEMENT ......................................................................................................................................... 5

9) SEVERANCE .................................................................................................................................................... 5

10) INTERPRETATION .......................................................................................................................................... 5

11) NO RIGHT OF ACTION ................................................................................................................................... 5

12) REFERENCES .................................................................................................................................................. 5

13) NOTICES .......................................................................................................................................................... 5

14) AMENDENT AND WAIVER ........................................................................................................................... 6

15) GENERAL PROVISIONS ................................................................................................................................. 6

16) SIGNATURES................................................................................................................................................... 8

District of Hope Revitalization Tax Exception Agreement

To be used in conjunction with District of Hope Bylaw No. 1337, 2013 Page 2 of 8

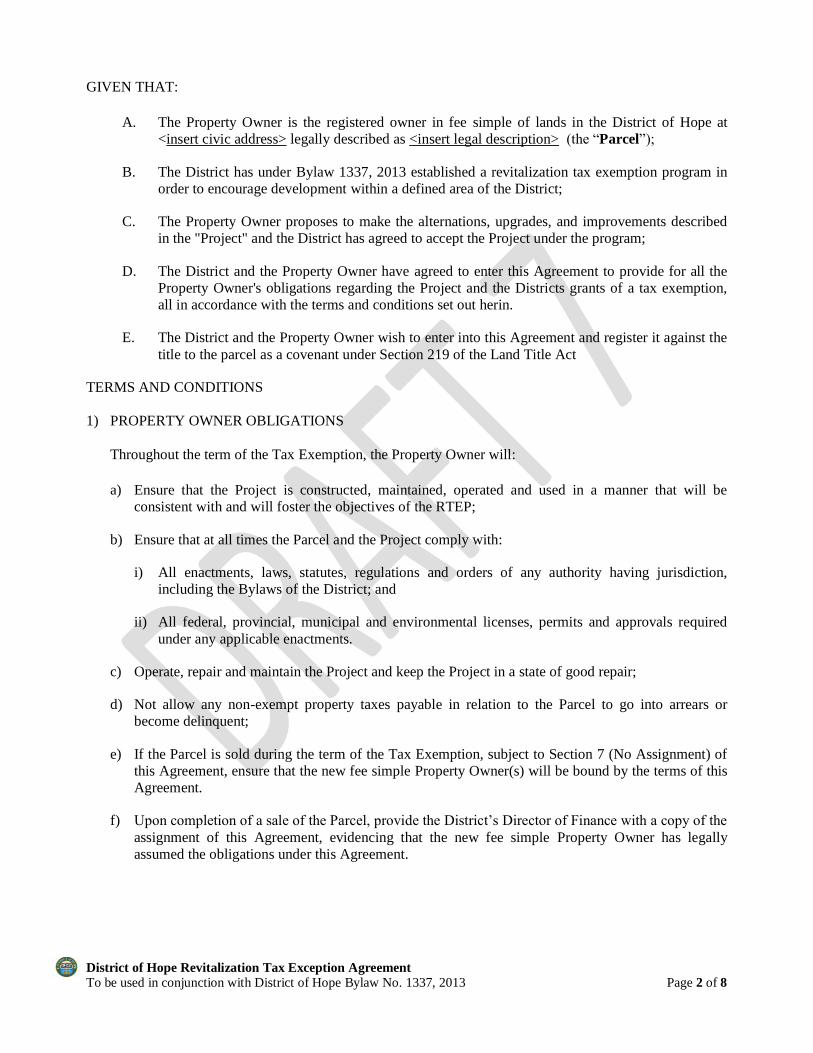

GIVEN THAT:

A. The Property Owner is the registered owner in fee simple of lands in the District of Hope at

<insert civic address> legally described as <insert legal description> (the “Parcel”);

B. The District has under Bylaw 1337, 2013 established a revitalization tax exemption program in

order to encourage development within a defined area of the District;

C. The Property Owner proposes to make the alternations, upgrades, and improvements described

in the "Project" and the District has agreed to accept the Project under the program;

D. The District and the Property Owner have agreed to enter this Agreement to provide for all the

Property Owner's obligations regarding the Project and the Districts grants of a tax exemption,

all in accordance with the terms and conditions set out herin.

E. The District and the Property Owner wish to enter into this Agreement and register it against the

title to the parcel as a covenant under Section 219 of the Land Title Act

TERMS AND CONDITIONS

1) PROPERTY OWNER OBLIGATIONS

Throughout the term of the Tax Exemption, the Property Owner will:

a) Ensure that the Project is constructed, maintained, operated and used in a manner that will be

consistent with and will foster the objectives of the RTEP;

b) Ensure that at all times the Parcel and the Project comply with:

i) All enactments, laws, statutes, regulations and orders of any authority having jurisdiction,

including the Bylaws of the District; and

ii) All federal, provincial, municipal and environmental licenses, permits and approvals required

under any applicable enactments.

c) Operate, repair and maintain the Project and keep the Project in a state of good repair;

d) Not allow any non-exempt property taxes payable in relation to the Parcel to go into arrears or

become delinquent;

e) If the Parcel is sold during the term of the Tax Exemption, subject to Section 7 (No Assignment) of

this Agreement, ensure that the new fee simple Property Owner(s) will be bound by the terms of this

Agreement.

f) Upon completion of a sale of the Parcel, provide the District’s Director of Finance with a copy of the

assignment of this Agreement, evidencing that the new fee simple Property Owner has legally

assumed the obligations under this Agreement.

District of Hope Revitalization Tax Exception Agreement

To be used in conjunction with District of Hope Bylaw No. 1337, 2013 Page 3 of 8

2) DISTRICT'S RIGHTS AND POWERS

a) Nothing contained or implied in this Agreement shall prejudice or affect the District's rights and

powers in the exercise of its functions, or its rights and powers under any public and private statues,

Bylaws, orders, or regulations, to the extent that they are applicable to the parcel, all of which may

be fully and effectively exercised in relation to the parcel as if this Agreement had not been executed

and delivered by the Property Owner.

3) COVENANTS

a) Property Owner covenants and agrees to use their best efforts to do, or cause to be done, at the

expense of the Property Owner, all acts reasonably necessary to grant priority to this Agreement as a

covenant over all charges and encumbrances that may have been registered against the title to the

parcel in the office of the Land Title Survey and Authority of British Columbia, save and except

those specifically approved in writing by the District or in favour of the District.

b) The covenants set forth in this Agreement shall charge the parcel pursuant to Section 219 of the Land

Title Act and shall be covenants, the burden of which shall run with the parcel and bind the parcel

and every part or parts thereof, and every part to which the parcel may be divided or subdivided,

whether by subdivision plan, strata plan or otherwise.

c) The covenants set forth in the Agreement shall not terminate if and when a purchaser becomes a

Property Owner in fee simple of the parcel, or any portion thereof, but shall charge the whole of

interest of such purchaser and shall continue to run with the parcel and bind the parcel and all future

owners for the time being of the parcel or any portion thereof, except the Property Owner will be

entitled to a partial discharge of this Agreement with respect to any subdivided parcel on acceptance

of the works and on compliance by the Property Owner with all requirements under this Agreement

with respect to the subdivided portion of the parcel.

d) It is further expressly agreed that the benefit of all covenants made by the Property Owner shall

accrue solely to the District and this Agreement may only be modified by Agreement between the

District and the Property Owner, or discharged by the District pursuant to the provisions of Section

219 of the Land Title Act and this Agreement. All of the costs of the preparation, execution and

registration of any amendments or discharges shall be borne by the Property Owner.

4) REPRESENTATIONS AND WARRANTIES

a) The Property Owner represents and warrants to the District that:

i) all necessary corporate actions and proceedings have been taken by the Property Owner to

authorize its entry into and performance of this Agreement;

ii) upon execution and delivery on behalf of the Property Owner, this Agreement constitutes a valid

and binding contractual obligation of the Property Owner;

iii) neither the execution and delivery, nor the performance of this Agreement, shall breach any

other Agreement or obligation, or cause the Property Owner to be in default of any other

Agreement or obligation, respecting the parcel; and,

iv) the Property Owner has the corporate capacity and authority to enter into and perform this

Agreement.

District of Hope Revitalization Tax Exception Agreement

To be used in conjunction with District of Hope Bylaw No. 1337, 2013 Page 4 of 8

5) CONDITIONS

The following conditions must be fulfilled before the District will issue a Property Tax Exemption

Certificate to the Property Owner:

a) The Property Owner will obtain a Building Permit prior to construction if required for the Project,

and obtain an Occupancy Permit from the Building Official for the Project and submit a completed

Revitalization tax Exemption Program Application with all relevant attachments on or before July

31st in the year the Property Owner applies for the Tax Exemption under the Bylaw;

i) If a Building Permit is not required for the commercial or industrial renovation, alternation, or

façade improvement project, the Property Owner will submit verifiable cost estimates and/or

appropriate proofs of purchase with their application

b) The Property Owner shall complete or cause to be completed construction of the Project in a good

and workmanlike fashion and in strict accordance with the building permit and the plans and

specifications attached hereto as a part of a completed Hope Revitalization Tax Exemption Program

Application and the Project must be officially opened for use by no later than one (1) year from the

date of issuance of the building permit.

c) The completed Project will not deviate significantly from plans supplied to District staff at the time

of application with compliance determined solely by the District’s Director of Community

Development.

d) The Property Owner will provide the District with the following:

i) A copy of the Projects Building Permit certifying the total contract price for the work including

all subcontracts or the value of construction as determined by the Building Official;

ii) A certificate verifying taxes assessed, rates, charges and fees imposed on the Parcel have been

paid, and, where taxes, rates or assessments are payable by installments, that all installments

owing at the date of application have been paid; and

iii) All applicable fees as required under District of Hope bylaws

e) At any time, if the Property Owner breaches or does not fully satisfy any of the obligations and

conditions in the Certificate or this Agreement, the District will provide notice of cancellation to the

Property Owner.

6) STRATIFICATION

If the Property Owner stratifies the Parcel under the Strata Parcel Act the Tax Exemption shall be

prorated among the strata lots in accordance with the unit entitlement of each strata lot for:

a) The current and each subsequent tax year during the term of this Agreement if the strata plan is

accepted for registration at the Land title Office before May 1 in the year of stratification; or

b) For the next calendar year and each subsequent tax year during the term of this Agreement if the

strata plan is accepted for registration at the Land Title Office after May 1 in the year of

stratification.

District of Hope Revitalization Tax Exception Agreement

To be used in conjunction with District of Hope Bylaw No. 1337, 2013 Page 5 of 8

provided that the Property Owner has assigned this Agreement to the strata corporation as required under

Section 1(e) of this Agreement.

7) NO REFUND

a) For greater certainty, under no circumstances will the Property Owner be entitled under or pursuant

to this Agreement to the revitalization tax exemption program to any cash credit, any carry forward

tax exemption credit or any refund for any property taxes paid.

8) NO ASSIGNEMENT

a) The Property Owner may not assign its interest in this Agreement except to a subsequent Property

Owner in fee simple of the Property.

9) SEVERANCE

a) If any portion of this Agreement is held invalid by a court of competent jurisdiction, the invalid

portion shall be severed and the decision that it is invalid shall not affect the validity of the

remainder of this Agreement.

10) INTERPRETATION

a) Wherever the singular or masculine is used in this Agreement, the same shall be construed as

meaning the plural, the feminine or body corporate where the context or the parties thereto so

required.

11) NO RIGHT OF ACTION

a) The Property Owner will have no cause of action for any losses incurred if this Agreement is found,

for any reason, to be illegal, invalid or unenforceable by a court of competent jurisdiction and in the

event of the finding of such illegality, invalidity or unenforceability, the Property Owner will be

obligated to pay all municipal Parcel taxes which would otherwise have been payable by the

Property Owner during the Term.

12) REFERENCES

a) Every reference to each party is deemed to include the heirs, executors, administrators, personal

representatives, successors, assigns, servants, employees, agents, contractors, officers, licensees and

invitees of such party, wherever the context so requires or allows.

13) NOTICES

a) Any notice or other communication required or contemplated to be given or made by any provision

of the Agreement shall be given or made in writing and delivered personally (and if so shall be

deemed received when delivered) or mailed by prepaid registered mail in any Canada Post Office

(and if so shall be deemed delivered on the sixth business day following such mailing except that, in

the event of interruption of mail service notice shall be deemed to be delivered only when actually

received by the party to whom it is addressed), so long as notice is addressed as follows:

i) To the Property Owner at the address given in this Agreement,

ii) And to the District at the address given in this Agreement

District of Hope Revitalization Tax Exception Agreement

To be used in conjunction with District of Hope Bylaw No. 1337, 2013 Page 6 of 8