BeijingBostonChennaiChicagoLondonLos AngelesMelbourneMilanMumbaiMunichNew Delhi

New YorkParisSan FranciscoSão PauloSeoulShanghaiSingaporeSydneyTokyoWroclaw

Ending the Payer-Provider Cold War:Working together to produce value

Linde Finsrud WilsonL.E.K. ConsultingNew York, New [email protected]

May 7, 2015

2 Footer

Whether we like it or not, the reality is the payer-provider world is radically changing Increases in the number of covered

individuals

Employer-sponsored coverage eroding

Consumers bearing increased responsibility for healthcare

Focus on value

- Movement from fee-for-service to fee-for-value

Providers becoming payers and payers becoming providers

Disruptors who are adept at lower cost and higher quality enter the market

3 Footer

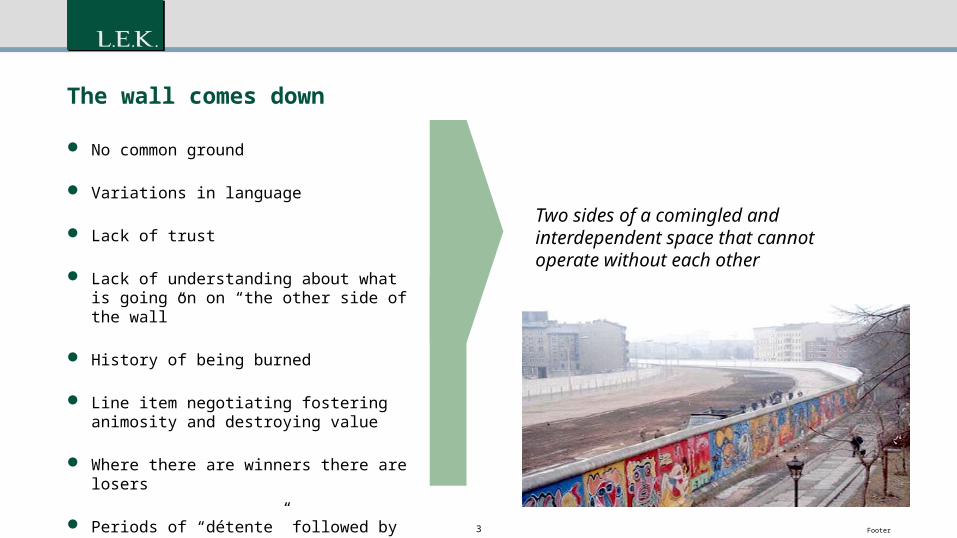

The wall comes down

No common ground

Variations in language

Lack of trust

Lack of understanding about what is going on on “the other side of the wall”

History of being burned

Line item negotiating fostering animosity and destroying value

Where there are winners there are losers

Periods of “détente” followed by surprise attacks

Two sides of a comingled and interdependent space that cannot operate without each other

4 FooterSource: L.E.K. research and analysis

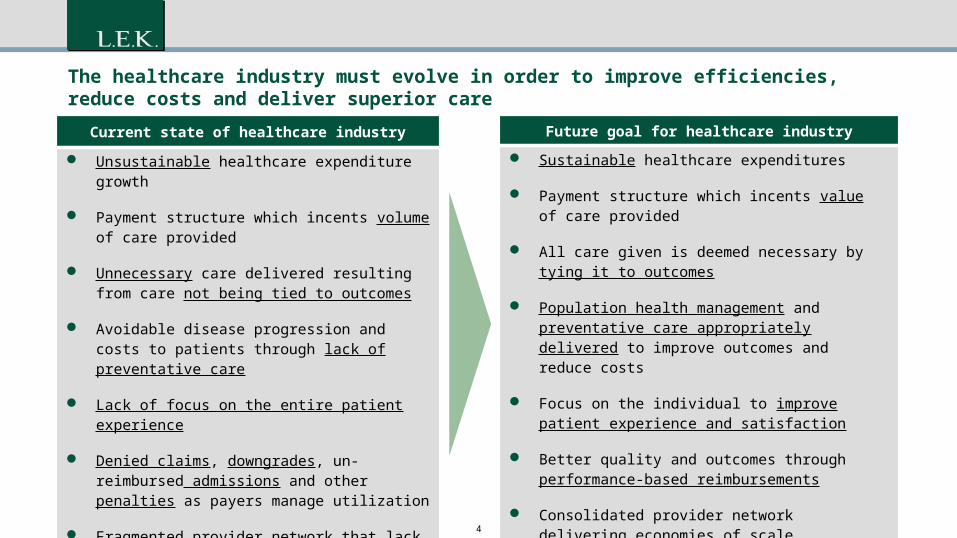

Current state of healthcare industry

Unsustainable healthcare expenditure growth

Payment structure which incents volume of care provided

Unnecessary care delivered resulting from care not being tied to outcomes

Avoidable disease progression and costs to patients through lack of preventative care

Lack of focus on the entire patient experience

Denied claims, downgrades, un-reimbursed admissions and other penalties as payers manage utilization

Fragmented provider network that lack economies of scale

Future goal for healthcare industry Sustainable healthcare expenditures

Payment structure which incents value of care provided

All care given is deemed necessary by tying it to outcomes

Population health management and preventative care appropriately delivered to improve outcomes and reduce costs

Focus on the individual to improve patient experience and satisfaction

Better quality and outcomes through performance-based reimbursements

Consolidated provider network delivering economies of scale

The healthcare industry must evolve in order to improve efficiencies, reduce costs and deliver superior care

5 Footer

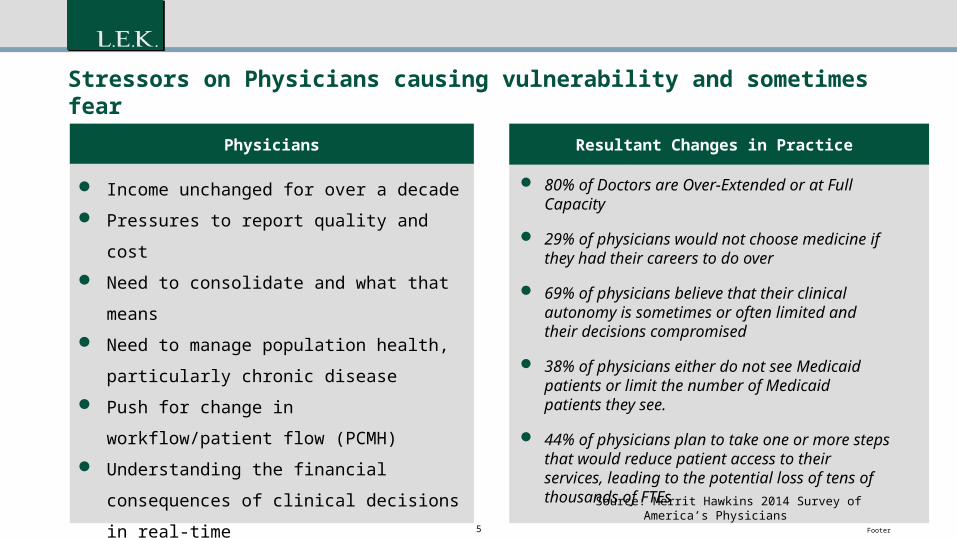

Stressors on Physicians causing vulnerability and sometimes fear

80% of Doctors are Over-Extended or at Full Capacity

29% of physicians would not choose medicine if they had their careers to do over

69% of physicians believe that their clinical autonomy is sometimes or often limited and their decisions compromised

38% of physicians either do not see Medicaid patients or limit the number of Medicaid patients they see.

44% of physicians plan to take one or more steps that would reduce patient access to their services, leading to the potential loss of tens of thousands of FTEs

Source: Merrit Hawkins 2014 Survey of America’s Physicians

Physicians

Income unchanged for over a decade

Pressures to report quality and cost

Need to consolidate and what that means

Need to manage population health, particularly

chronic disease

Push for change in workflow/patient flow

(PCMH)

Understanding the financial consequences of

clinical decisions in real-time

Getting up to speed on multiple IT systems

combined with manual processes

Resultant Changes in Practice

6 Footer

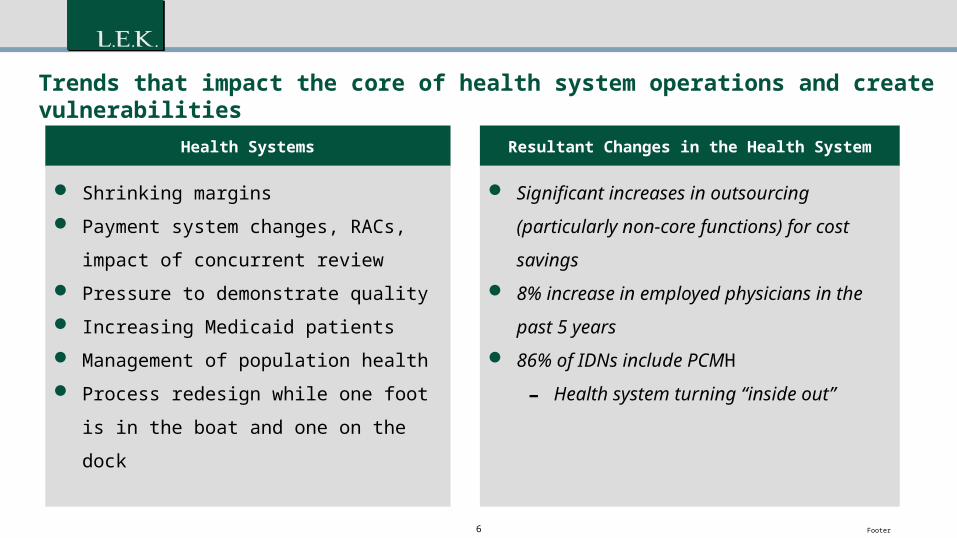

Trends that impact the core of health system operations and create vulnerabilities

Health Systems

Shrinking margins

Payment system changes, RACs, impact of

concurrent review

Pressure to demonstrate quality

Increasing Medicaid patients

Management of population health

Process redesign while one foot is in the

boat and one on the dock

Resultant Changes in the Health System

Significant increases in outsourcing

(particularly non-core functions) for cost

savings 8% increase in employed physicians in the

past 5 years 86% of IDNs include PCMH

- Health system turning “inside out”

7 Footer

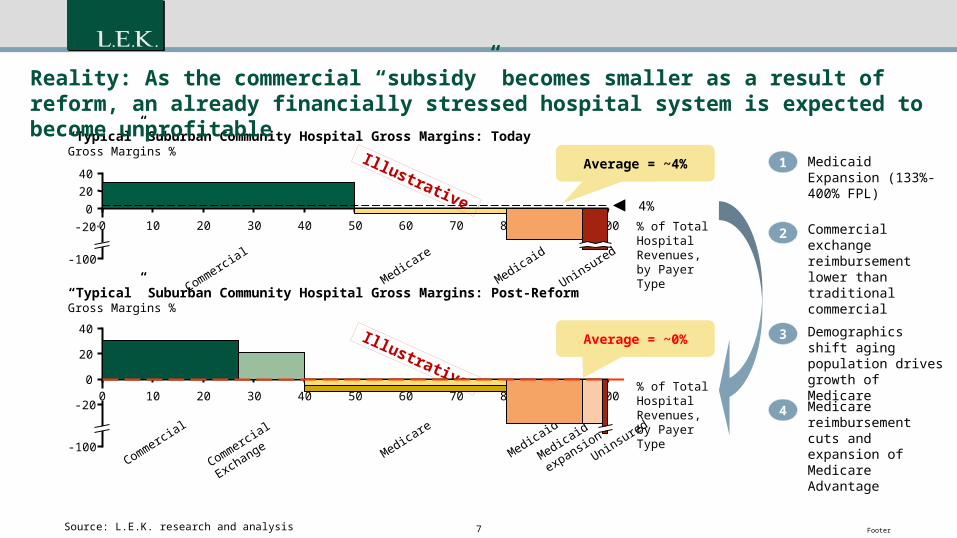

403020100 100

4020

0-20

-100

9080706050

“Typical” Suburban Community Hospital Gross Margins: TodayGross Margins %

4%

Commercial

Medicare

Medicaid

Uninsured

% of Total Hospital Revenues,by Payer Type

Average = ~4%

Average = ~0%

Commercial

Exchange Medicare

Medicaid

Medicaid

expansionUninsured

Commercial

% of Total Hospital Revenues,by Payer Type

Reality: As the commercial “subsidy” becomes smaller as a result of reform, an already financially stressed hospital system is expected to become unprofitable

Source: L.E.K. research and analysis

1

2

3

4

Medicaid Expansion (133%-400% FPL)

Commercial exchange reimbursement lower than traditional commercial

Demographics shift aging population drives growth of Medicare

Medicare reimbursement cuts and expansion of Medicare Advantage

Illustrative

Illustrative

40

20

0

-20

-100

1009080706050403020100

“Typical” Suburban Community Hospital Gross Margins: Post-ReformGross Margins %

8 Footer

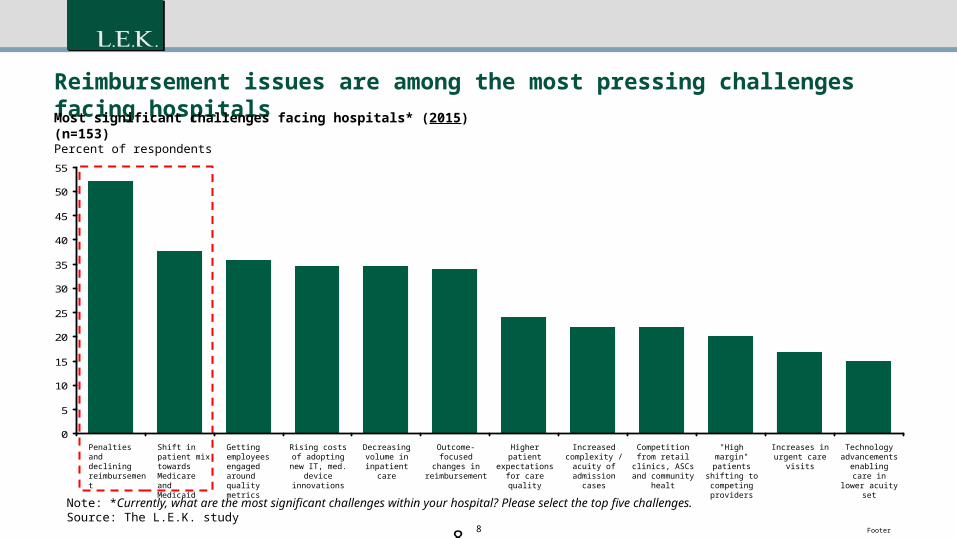

Reimbursement issues are among the most pressing challenges facing hospitals

Note: *Currently, what are the most significant challenges within your hospital? Please select the top five challenges.Source: The L.E.K. study

0

5

10

15

20

25

30

35

40

45

50

55

Rising costs of adopting new IT,

med. device innovations

Decreasing volume in

inpatient care

Outcome-focused changes in

reimbursement

Higher patient expectations for

care quality

Increased complexity /

acuity of admission cases

Competition from retail clinics, ASCs

and community healt

"High margin" patients shifting

to competing providers

Increases in urgent care visits

Technology advancements

enabling care in lower acuity set

Getting employees engaged around quality metrics

Shift in patient mix towards Medicare and Medicaid

Penalties and declining reimbursement

Most significant challenges facing hospitals* (2015) (n=153)Percent of respondents

8

9 Footer

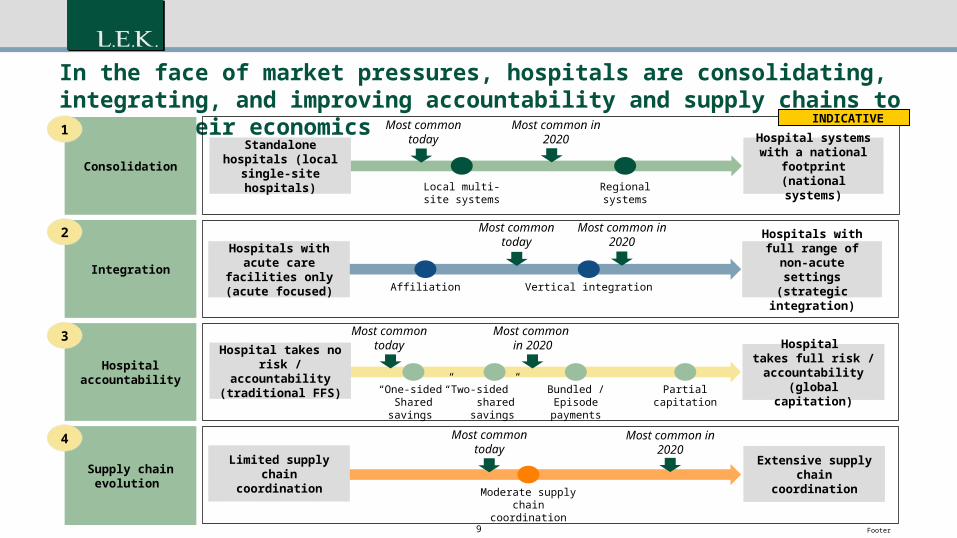

In the face of market pressures, hospitals are consolidating, integrating, and improving accountability and supply chains to improve their economics

Local multi-site systems

Regional systems

Affiliation Vertical integration

Consolidation

Integration

Most common in 2020

Most common today

Most common today

Most common in 2020

Standalone hospitals (local single-site

hospitals)

Hospital systems with a national

footprint (national systems)

Hospitals with acute care facilities only

(acute focused)

Hospitals with full range of non-acute settings (strategic

integration)

“Two-sided” sharedsavings

Bundled /Episode

payments

“One-sided”Sharedsavings

Hospital accountability

Supply chain evolution

Partialcapitation

Most common today

Most common today

Most common in 2020

Moderate supply chain coordination

Most common in 2020

Hospital takes no risk / accountability (traditional FFS)

Hospital takes full risk /

accountability (global capitation)

Limited supply chain coordination

Extensive supply chain coordination

1

2

3

4

INDICATIVE

10 Footer10

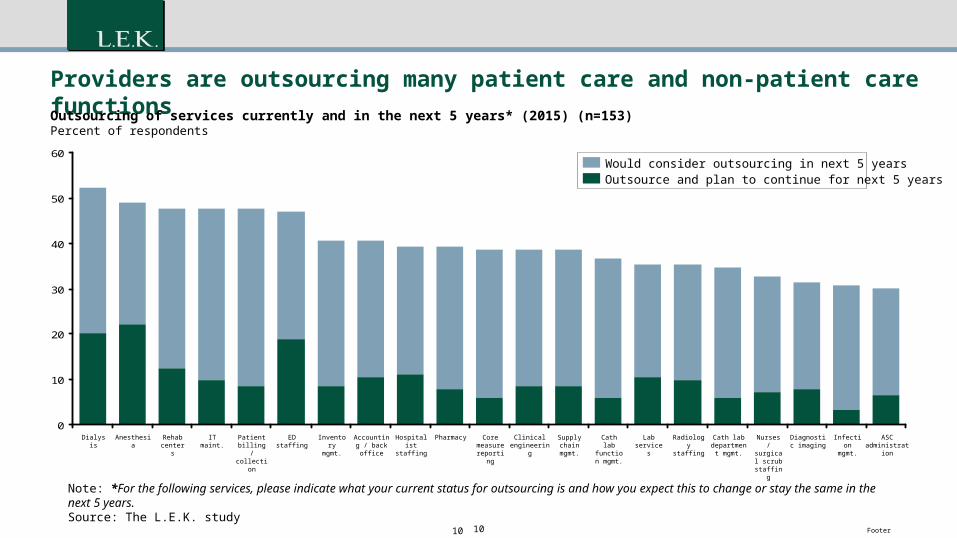

Providers are outsourcing many patient care and non-patient care functions

Note: *For the following services, please indicate what your current status for outsourcing is and how you expect this to change or stay the same in the next 5 years. Source: The L.E.K. study

0

10

20

30

40

50

60

Core measure reporting

Clinical engineering

Supply chain mgmt.

Cath lab function mgmt.

Lab services

Radiology staffing

PharmacyHospitalist staffing

Accounting / back office

Inventory mgmt.

ED staffingPatient billing /

collection

IT maint. Nurses / surgical scrub

staffing

Diagnostic imaging

Infection mgmt.

ASC administration

Cath lab department

mgmt.

Outsourcing of services currently and in the next 5 years* (2015) (n=153)Percent of respondents

Dialysis Anesthesia Rehab centers

Would consider outsourcing in next 5 yearsOutsource and plan to continue for next 5 years

11 Footer

Payers are being hit as well

Payers

Scaling many new and innovative reimbursement

models and new populations-”new game begins

before the old one ends”

Managing the gap between funding and medical

costs within a changing regulatory environment

Reducing administrative costs

Understanding the idiosyncrasies of the provider

environment

Impacting care decisions before care is delivered

Efficient change to operations to facilitate the “new

world”

Inspiring providers to move from traditional model

Provider market consolidation and contract modeling

Resultant Changes in Payers

98% of payers involved in some type of value-based

care risk model In the shorter term, payers are more focused on cost

containment than on outcomes-based approaches to

containing costs.

(Source: E&Y Progressions 2014) Trust between health systems and payers is at an all

time low-narrow networks, tiered networks,

implantation of population health workers rather than

collaborating Vast majority of 5 star MA plans are provider-

sponsored causing stress with payers

12 Footer

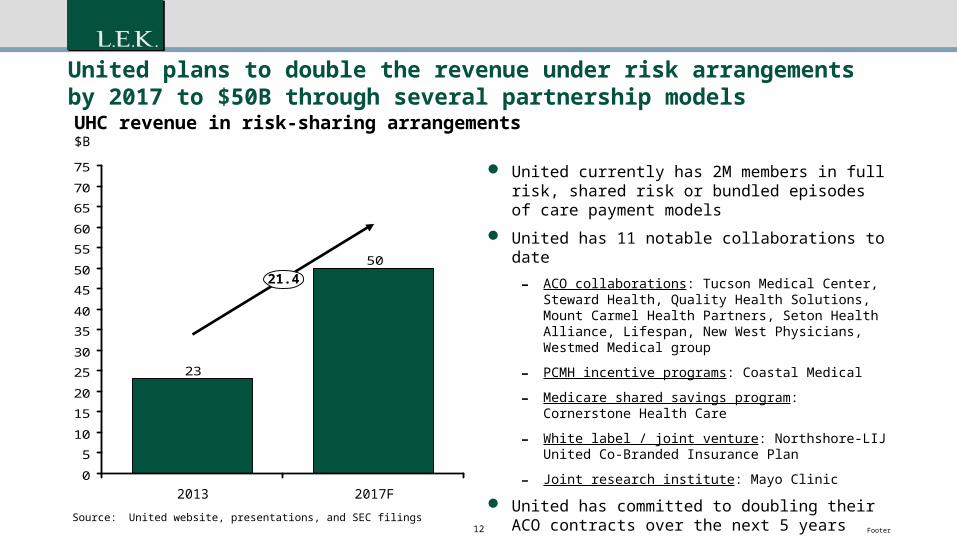

United plans to double the revenue under risk arrangements by 2017 to $50B through several partnership models

United currently has 2M members in full risk, shared risk or bundled episodes of care payment models

United has 11 notable collaborations to date

- ACO collaborations: Tucson Medical Center, Steward Health, Quality Health Solutions, Mount Carmel Health Partners, Seton Health Alliance, Lifespan, New West Physicians, Westmed Medical group

- PCMH incentive programs: Coastal Medical

- Medicare shared savings program: Cornerstone Health Care

- White label / joint venture: Northshore-LIJ United Co-Branded Insurance Plan

- Joint research institute: Mayo Clinic

United has committed to doubling their ACO contracts over the next 5 years

50

23

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

UHC revenue in risk-sharing arrangements$B

21.4

2017F2013

Source: United website, presentations, and SEC filings

13 Footer

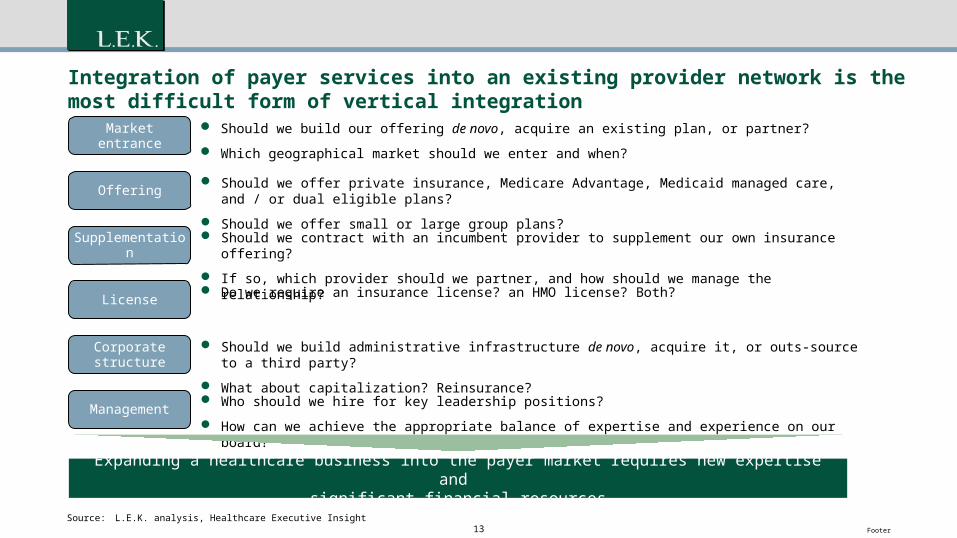

Integration of payer services into an existing provider network is the most difficult form of vertical integration

Source: L.E.K. analysis, Healthcare Executive Insight

Supplementation

Corporate structure

License

Management

Market entrance

Offering Should we offer private insurance, Medicare Advantage, Medicaid managed care, and / or dual eligible

plans?

Should we offer small or large group plans? Should we contract with an incumbent provider to supplement our own insurance offering?

If so, which provider should we partner, and how should we manage the relationship?

Do we require an insurance license? an HMO license? Both?

Should we build administrative infrastructure de novo, acquire it, or outs-source to a third party?

What about capitalization? Reinsurance?

Who should we hire for key leadership positions?

How can we achieve the appropriate balance of expertise and experience on our board?

Should we build our offering de novo, acquire an existing plan, or partner?

Which geographical market should we enter and when?

Expanding a healthcare business into the payer market requires new expertise and significant financial resources

14 Footer

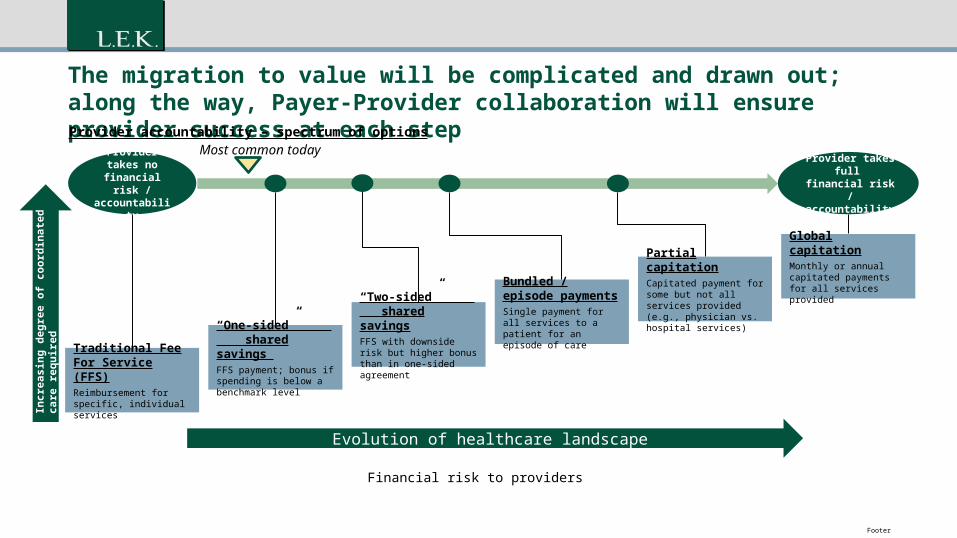

The migration to value will be complicated and drawn out; along the way, Payer-Provider collaboration will ensure provider success at each step

Provider takes full financial risk / accountability

Provider takes no financial risk / accountability

Provider accountability – spectrum of optionsMost common today

Incr

easi

ng d

egre

e of

coo

rdin

ated

car

e re

quire

d

Traditional Fee For Service (FFS)Reimbursement for specific, individual services

“Two-sided” shared savingsFFS with downside risk but higher bonus than in one-sided agreement

“One-sided” shared savings FFS payment; bonus if spending is below a benchmark level

Bundled / episode paymentsSingle payment for all services to a patient for an episode of care

Partial capitationCapitated payment for some but not all services provided (e.g., physician vs. hospital services)

Global capitationMonthly or annual capitated payments for all services provided

14

Financial risk to providers

Evolution of healthcare landscape

15 Footer

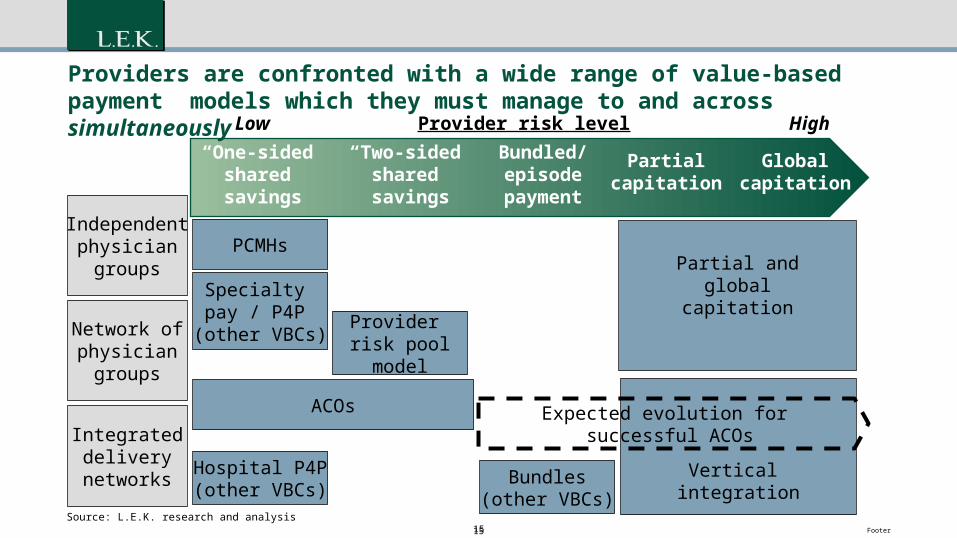

Vertical integration

“One-sided”shared savings

“Two-sided”shared savings

Bundled/episodepayment

Partialcapitation

Globalcapitation

Provider risk level HighLow

Independentphysician

groups

Network ofphysician

groups

Integrateddelivery

networks

PCMHs

Specialty pay / P4P

(other VBCs)Provider risk poolmodel

Hospital P4P(other VBCs)

ACOs

Bundles(other VBCs)

Partial andglobal

capitation

Source: L.E.K. research and analysis

Providers are confronted with a wide range of value-based payment models which they must manage to and across simultaneously

Expected evolution for successful ACOs

15

16 Footer

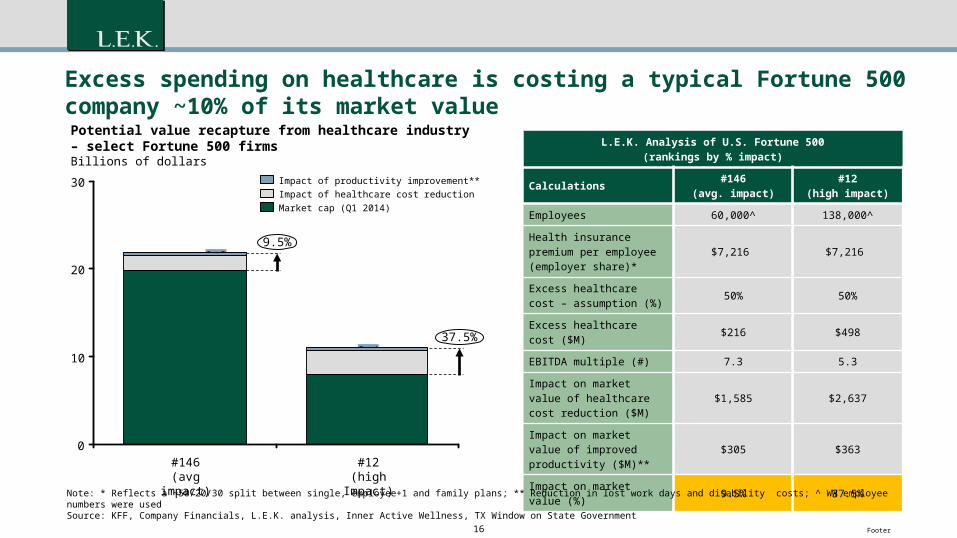

Excess spending on healthcare is costing a typical Fortune 500 company ~10% of its market value

L.E.K. Analysis of U.S. Fortune 500(rankings by % impact)

Calculations #146(avg. impact)

#12(high impact)

Employees 60,000^ 138,000^

Health insurance premium per employee (employer share)*

$7,216 $7,216

Excess healthcare cost – assumption (%) 50% 50%

Excess healthcare cost ($M) $216 $498

EBITDA multiple (#) 7.3 5.3

Impact on market value of healthcare cost reduction ($M)

$1,585 $2,637

Impact on market value of improved productivity ($M)** $305 $363

Impact on market value (%) 9.5% 37.5%

Note: * Reflects a ~50/20/30 split between single, employee+1 and family plans; ** Reduction in lost work days and disability costs; ^ WW employee numbers were usedSource: KFF, Company Financials, L.E.K. analysis, Inner Active Wellness, TX Window on State Government

30

20

10

0

9.5%

Potential value recapture from healthcare industry– select Fortune 500 firmsBillions of dollars

37.5%

#12(high Impact)

8.0

2.60.4

#146(avg impact)

19.9

1.60.3

Market cap (Q1 2014)Impact of healthcare cost reductionImpact of productivity improvement**

17 Footer

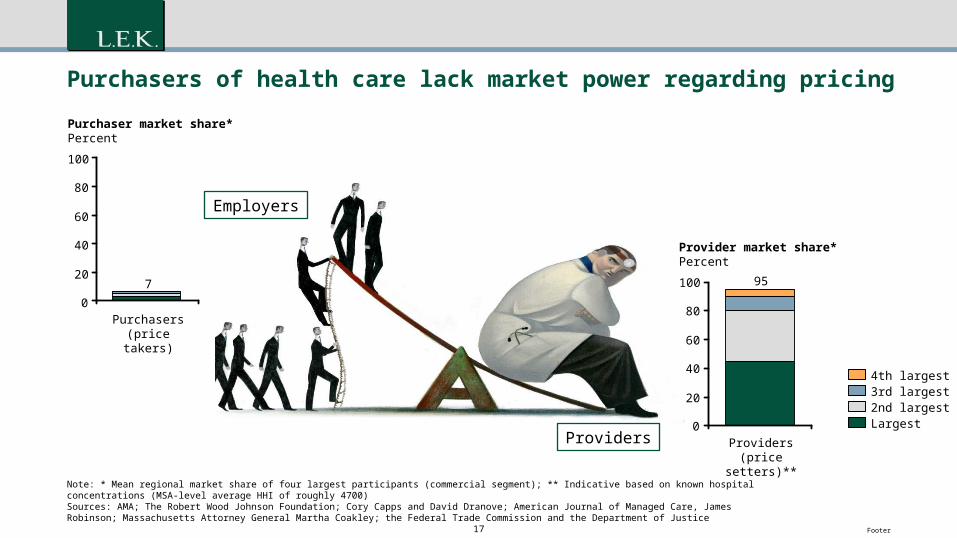

Purchasers of health care lack market power regarding pricing

Note: * Mean regional market share of four largest participants (commercial segment); ** Indicative based on known hospital concentrations (MSA-level average HHI of roughly 4700)Sources: AMA; The Robert Wood Johnson Foundation; Cory Capps and David Dranove; American Journal of Managed Care, James Robinson; Massachusetts Attorney General Martha Coakley; the Federal Trade Commission and the Department of Justice

100

80

60

40

20

0

Purchaser market share*Percent

Purchasers (price takers)

7 100

80

60

40

20

0

Provider market share*Percent

Providers (price setters)**

95

2nd largest

4th largest3rd largest

Largest

Employers

Providers

18 Footer

The demand for value by employers has placed pressure on payers and providers to

collaborate….but years of often double digit price

increases has impacted patience and patients.

The collaborative imperative is now.

19 Footer

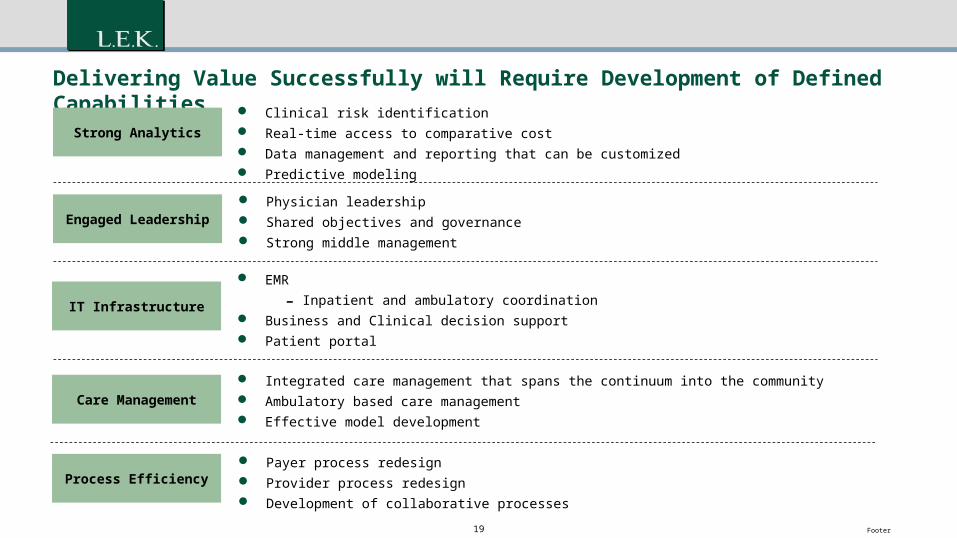

Delivering Value Successfully will Require Development of Defined Capabilities

Strong Analytics

Engaged Leadership

IT Infrastructure

Care Management

Clinical risk identification Real-time access to comparative cost Data management and reporting that can be customized Predictive modeling

Physician leadership Shared objectives and governance Strong middle management

EMR

- Inpatient and ambulatory coordination Business and Clinical decision support Patient portal

Integrated care management that spans the continuum into the community Ambulatory based care management Effective model development

Process Efficiency Payer process redesign Provider process redesign Development of collaborative processes

20 Footer

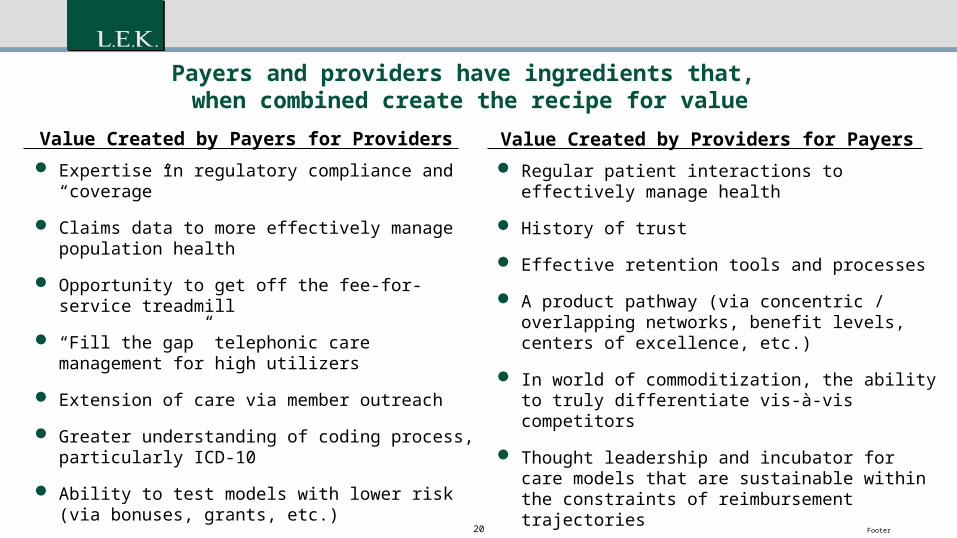

Payers and providers have ingredients that, when combined create the recipe for value

Expertise in regulatory compliance and “coverage”

Claims data to more effectively manage population health

Opportunity to get off the fee-for-service treadmill

“Fill the gap” telephonic care management for high utilizers

Extension of care via member outreach

Greater understanding of coding process, particularly ICD-10

Ability to test models with lower risk (via bonuses, grants, etc.)

Value Created by Payers for Providers Value Created by Providers for Payers Regular patient interactions to effectively manage

health

History of trust

Effective retention tools and processes

A product pathway (via concentric / overlapping networks, benefit levels, centers of excellence, etc.)

In world of commoditization, the ability to truly differentiate vis-à-vis competitors

Thought leadership and incubator for care models that are sustainable within the constraints of reimbursement trajectories

Face-to-face care management through PCMH rather than telephonic

21 Footer

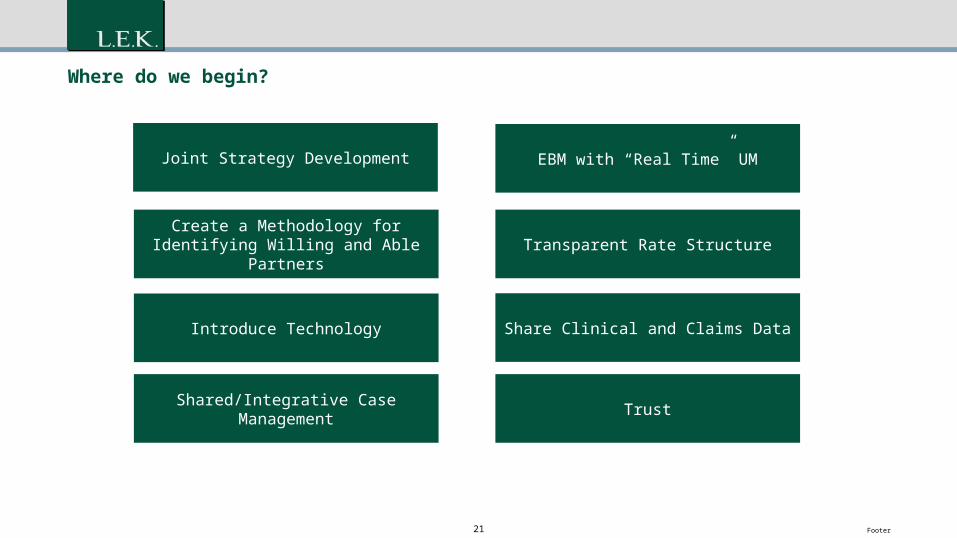

Where do we begin?

EBM with “Real Time” UM

Transparent Rate Structure

Share Clinical and Claims Data

Create a Methodology for Identifying Willing and Able Partners

Joint Strategy Development

Introduce Technology

Shared/Integrative Case Management Trust

22 Footer

Care Coordination

Provider Payer

23 Footer

Disrupter-what happens if payers and providers don’t collaborate?

Optimization of a business model for the needs of a relatively unattractive or small segment

Leverage an enabling technology that allows preservation or enhancement of cost or quality advantages

Design it so Incumbent competitors are unable to respond effectively due to legacy costs and a continuing need to serve their existing customer segments

24 Footer

Background and objectives

Disruptors

Payers

Providers become payers pushing payers to

become providers

Employers align for market power

Providers

Disruption to most profitable or core services

Hearing set on Highmark plan to put $175 million in Allegheny Health

Recommended