Embed Size (px)

Citation preview

Bigdata Intelligence PlatformBICube 2

목차

I. Paradigm ShiftII. Machine LearningIII. Neural StreamIV. FinTechV. Fraud Detection SystemVI. Conclusions

Bigdata Intelligence PlatformBICube 3

목차

I. Paradigm ShiftII. Machine LearningIII. Neural StreamIV. FinTechV. Fraud Detection SystemVI. Conclusions

Bigdata Intelligence PlatformBICube 4

I. Paradigm Shift

Paradigm Shift

see the same information in an entirely different way.

Bigdata Intelligence PlatformBICube 5

I. Paradigm Shift

Banking is Broken !

Bigdata Intelligence PlatformBICube 6

I. Paradigm Shift

Bigdata Intelligence PlatformBICube 7

I. Paradigm Shift

수많은 직종은 향후 20년내에 로봇 및 자동화로 소멸-빌게이츠

2030년까지 20억개 이상의 일자리가 소멸-토마스 프레이

Bigdata Intelligence PlatformBICube 8

I. Paradigm Shift

과거의 인력거꾼보다 훨씬 많은 운전자와 직종이 생겨났다.

Bigdata Intelligence PlatformBICube 9

목차

I. Paradigm ShiftII. Machine LearningIII. Neural StreamIV. FinTechV. Fraud Detection SystemVI. Conclusions

Bigdata Intelligence PlatformBICube 10

II. Machine Learning

Data로 부터 출발....

• 기계(Machine) + Learning (학습)

• 기계(컴퓨터)에게 데이터를 이용하여 학습하는 방법을 가르치는 것. Teach computer how to learn from data

따라서 Data가 교재이다.

Bigdata Intelligence PlatformBICube 11

II. Machine Learning

Data

알고리즘 개발자

Model

Bigdata Intelligence PlatformBICube 12

II. Machine Learning

Machine Learning Model • 컴퓨터가 학습할 수 있도록 하는 알고리즘과 기술

• 문제를 해결하기위한 일련의 컴퓨터 프로세스.

• 정확한 미래를 예측하기 위한 컴퓨터 알고리즘.

• 컴퓨터가 스스로 학습하는 예측모형

(Training Data)

Learning Algorithms Predictive Model

실데이터(Actual Data)

Forecast Prediction ClassificationClusteringProactive

• Optical character recognition• Face detection• Spam filtering• Topic spotting• Spoken language understanding• Medical diagnosis• Customer segmentation• Fraud detection• Weather prediction

SupervisedUnsupervisedSemi-supervised

StructuredUnstructuredSemi-structured

Example Data

Bigdata Intelligence PlatformBICube 13

II. Machine Learning

기계학습(Machine Learning)의 종류

• Supervised learning : 지도학습• Data의 종류를 알고 있을 때(Category, Labeled)• ex: spam mail

• Unsupervised : 비지도학습• Data의 종류는 모르지만 패턴을 알고 싶을 때 • SNS, Twitter

• Semi-supervised learning : 지도학습 + 비지도학습• Reinforcement learning : 강화학습

• 잘못된 것을 다시 피드백• Evolutionary learning : 진화학습• Meta Learning : Landmark of data for classifier

Bigdata Intelligence PlatformBICube 14

ML Modeling

ML Deploy

ML Optimizer

New Data

Decision Making

Alert

ML Lifecycle

Anomaly Store

Hadoop DFS/NoSQl/Hive

II. Machine Learning

Bigdata Intelligence PlatformBICube 15

Batch

Delploy Flow

Validate Deploy/Active

Back-line Near-line On-line

모델 개발SVMlogisticregressionFDSAnomalyOptimization

모델 검증개발된 모델이 잘 적용되는지 검증

모델 적용검증된 모델이 실환경에적용하여 실행

New Data

II. Machine Learning

Bigdata Intelligence PlatformBICube 16

II. Machine Learning

Netwrok?

• Neural Network : • 인간의 뇌 신경망에서 영감을 얻음• ex: Deep Learning

• Bayesian Netwrok• 노드들간의 확률적 의존성을 나타내는 그래프 모형 • 방향 비순환 그래프 (DAG: Directed Acyclic Graph)

• Markov Network• 결합분포확률 모형 • 비방향그래프

Bigdata Intelligence PlatformBICube 17

II. Machine Learning

Perceptron Deep Learning

x1

x3

x2

w3w2

w1

o

• Neural Network

Bigdata Intelligence PlatformBICube 18

II. Machine Learning

Markov Network Bayesian Netwrok

Bigdata Intelligence PlatformBICube 19

목차

I. Paradigm ShiftII. Machine LearningIII. Neural StreamIV. FinTechV. Fraud Detection SystemVI. Conclusions

Bigdata Intelligence PlatformBICube 20

• High throughput• Machine Learning• Power Computing

50billion Device

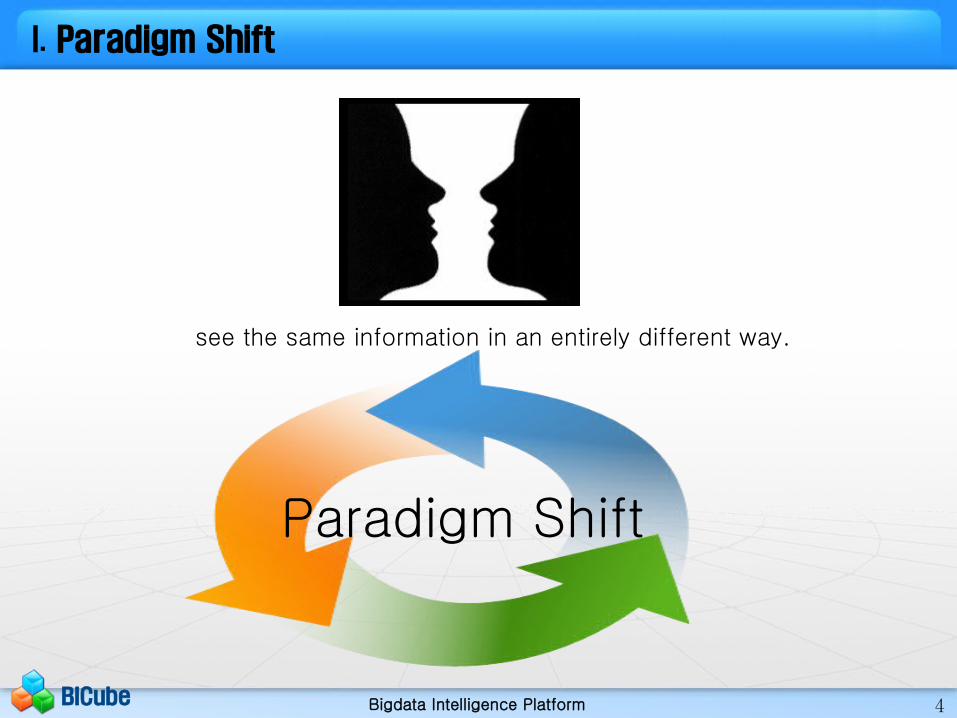

III. Neural Stream

Bigdata Intelligence PlatformBICube 21

Legacy CEP(Complex Event Processing)

CEPIII. Neural Stream

Bigdata Intelligence PlatformBICube 22

Complex Event ?Complex:복잡한 Event :A piece fo data in software system or in real world

금융거래 예시 :고객ID,IP주소,접속일자,접속시간,거래채널구분,거래종류,거래고유번호,출금은행명,출금계좌,출금계좌예금주명,출금계좌예금주명,보내는통장표시내용,입금은행코드,입금계좌,입금계좌예금주명,받는통장표시내용,거래금액,이체수수료,거래후잔액,거래일자,거래시간

Event Streaming Processing

CEPIII. Neural Stream

Bigdata Intelligence PlatformBICube 23

CEP System

복잡 다단한 연산을 수행하면서 많은 양의 데이터를 처리한다는 것은 사실상 물리적으로 불가하다.중앙집중형 폐쇄화된 CEP엔진으로 가능할까?

CEPIII. Neural Stream

Bigdata Intelligence PlatformBICube 24

Min, Max, Sum, Avg,Join 등으로 만족할 수 있을까?주식이 10% 떨어지고 3회 이상 5% 오른다는 패턴만으로 예측할 수 있을까?

CEP

Need more Algorithoms and more ML puzzle

III. Neural Stream

Bigdata Intelligence PlatformBICube 25

Near Real-time

Seconds 수준의 지연(latency) 시간 보장

Real-time

Real Real-time

Milliseconds 수준의 지연(latency) 시간 보장

Microseconds 수준의 지연(latency) 시간 보장 (16ms)

리얼타임 스트리밍의 종류

III. Neural Stream

Bigdata Intelligence PlatformBICube 26

Giga Internet

Neural Streaming

External Neural Streaming

Beacon

Routing

Internal Neural Cluster

Neural Cluster

CEP

III. Neural Stream

Bigdata Intelligence PlatformBICube 27

BIP

Sharing Neural Streaming

ML

Neural

Cortex

Cortex Streaming

Cortex Streaming

Cortex Streaming

III. Neural Stream

Bigdata Intelligence PlatformBICube 28

Neural Streaming

Beacon Neural Cluster

Modeling

Deploy Neurons (ML model)

BIP

CEP

Share Cortex Streaming

III. Neural Stream

Bigdata Intelligence PlatformBICube 29

Neural Learning – Multi Model

III. Neural Stream

Bigdata Intelligence PlatformBICube 30

I. Paradigm ShiftII. Machine LearningIII. Neural StreamIV. FinTechV. Fraud Detection SystemVI. Conclusions

목차

Bigdata Intelligence PlatformBICube 31

정보기술을 활용하여 구조·제공방식·기법 면에서 새로운 형태의 금융서비스를 제공하는 것을 의미

IV. FinTech

Bigdata Intelligence PlatformBICube 32

IV. FinTech

Bigdata Intelligence PlatformBICube 33

IV. FinTech

Bigdata Intelligence PlatformBICube 34

IV. FinTech

Bigdata Intelligence PlatformBICube 35

기업명 사업 내용

스트라이프 (Stripe.com)

자사의 앱 프로그래밍 인터페이스를 앱에 삽입 한 회원에게 글로벌 고객을 대상으로 한 지급결 제와 7일 안에 대금을 지급해 주는 서비스 제공

전 세계 139개국 통화와 비트코인, 알리페이 등으로도 결제 가능

어펌 (Affirm.com)

회원이 온라인쇼핑몰에서 물건을 구매할 때, 신용카드가 아닌 본인의 신용으로 할부 구매할 수 있도록 해주는 결제 서비스 제공 회원의 공개된 데이터를 분석해 단 몇 초 만 에 신용도를 평가한 후, 회원의 적정 할부 수수료

를 산정하여 부과

빌가드 (Billguard.com)

자사가 개발한 예측 알고리즘을 활용하여 신용카드 청구서 상 오청구 또는 수수료 과다 인출 등의 징후를 포착하여 회원에게 알려주는 서비스 제공 모바일앱으로 회원의 신용카드와 은행 계좌를 통합 관리 가능

온덱 (OnDeck.com)

100% 온라인 기반으로 대출 신청서 제출에 10분, 신청 익일에 지정 계좌로 자금을 입금해주는 대출 서비스 제공 자체 개발한 신용평가 알고리즘이 대출 신청자의 금융기관 거래내용, 현금 흐름, SNS 상 평판 등을 고려해 몇 분 만에 신용 평가 및 대출 여부 심사

자료: 우리금융경영연구소

IV. FinTech

Bigdata Intelligence PlatformBICube 36

IV. FinTech

Bigdata Intelligence PlatformBICube 37

Accenture

IV. FinTech

Bigdata Intelligence PlatformBICube 38

Accenture

IV. FinTech

Bigdata Intelligence PlatformBICube 39

IV. FinTech

Bigdata Intelligence PlatformBICube 40

IV. FinTech

Bigdata Intelligence PlatformBICube 41

FinTech의 주요 시장

• 해외 송금수수료 시장• 신용카드 수수료 시장-약480 억 달러• 양면 시장(Two-side markets)• 카드 소지자와 가맹점• 구글 뱅크(Bank as a Platform-2007 영국)• 알고리즘 뱅크• M-Money• E-Money -without banks

IV. FinTech

Bigdata Intelligence PlatformBICube 42

알고리즘 금융 서비스의 성장

IV. FinTech

Bigdata Intelligence PlatformBICube 43

Two-side markets

IV. FinTech

Bigdata Intelligence PlatformBICube 44

애플 페이(Apple Pay)

최초로 신용카드, 체크카드 등을 등록-불편

카드를 등록하면서 부여되는 '기기계정번호(Device Account Number)'를 저장

근거리무선통신(NFC) 기능을 활성화한 상태에서 가맹점 내 단말기에 아이폰을 갖다대고, 손가락의 지문을 통해 본인인증

결제가 이뤄지는 순간에만 생성되는 일회용 비밀번호인 '동적보안코드(dynamic security code)'와 연동해 결제

아이튠즈 유료 사용자 2억명에 대한 카드결제정보를 보유

애플페이는 아이폰6, 아이폰6 플러스, 애플워치와 같은 최신 애플 기기 사용자들만 쓸 수 있는데다가 가맹점 수 또한 페이팔에 비해 턱없이 부족

IV. FinTech

Bigdata Intelligence PlatformBICube 45

IV. FinTech

The Kreditech Group uses big data, complex algorithms and automated workflows to serve a simple mission: “Better banking for everyone”. Based on 20,000 dynamic data points, the unique technology is capable of scoring everyone worldwide, including the 4bn individuals without credit score.

Deploying the technology makes physical contact and paper exchange redundant. Funds can be paid out within seconds to a credit card, bank account or NFC wallet, 24/7.

Bigdata Intelligence PlatformBICube 46

아프리카 케냐의 이동통신사인 사파리콤(Safaricom)이 영국의 보다폰(Vodafone)과 함께 2007년 도입

http://slownews.kr/32306

IV. FinTech

Bigdata Intelligence PlatformBICube 47

은행 계좌 없이 돈을 이체할 수 있는 서비스-엠 페사

페이스북 메신저, 왓츠앱, 카카오톡, 라인 등이 준비하고 있는 모바일 메신저 기반 지불 서비스(payment service)는 페이팔(PayPal)의 작동 원리와 유사이 모든 서비스는 특정 은행 계좌 또는 신용카드 계좌와 연결

돈을 내고 ‘모바일 가상 화폐’를 받는다. 이를 ‘엠-머니(M-Money)’라 부른다. 엠-머니는 문자메시지와 PIN(Personal Identification number)을 동시에 이용해 타인의 휴대폰으로 이체 가능하며, 엠-머니로 위의 그림처럼 오프라인 매장에서 지불 수단으로 이용할 수 있다. 필요에 따라 사파리콤 대리점을 방문하여 엠-머니를 실제 화폐로 쉽게 교환할 수 있다.

IV. FinTech

Bigdata Intelligence PlatformBICube 48

I. Paradigm ShiftII. Machine LearningIII. Neural StreamIV. FinTechV. Fraud Detection SystemVI. Conclusions

목차

Bigdata Intelligence PlatformBICube 49

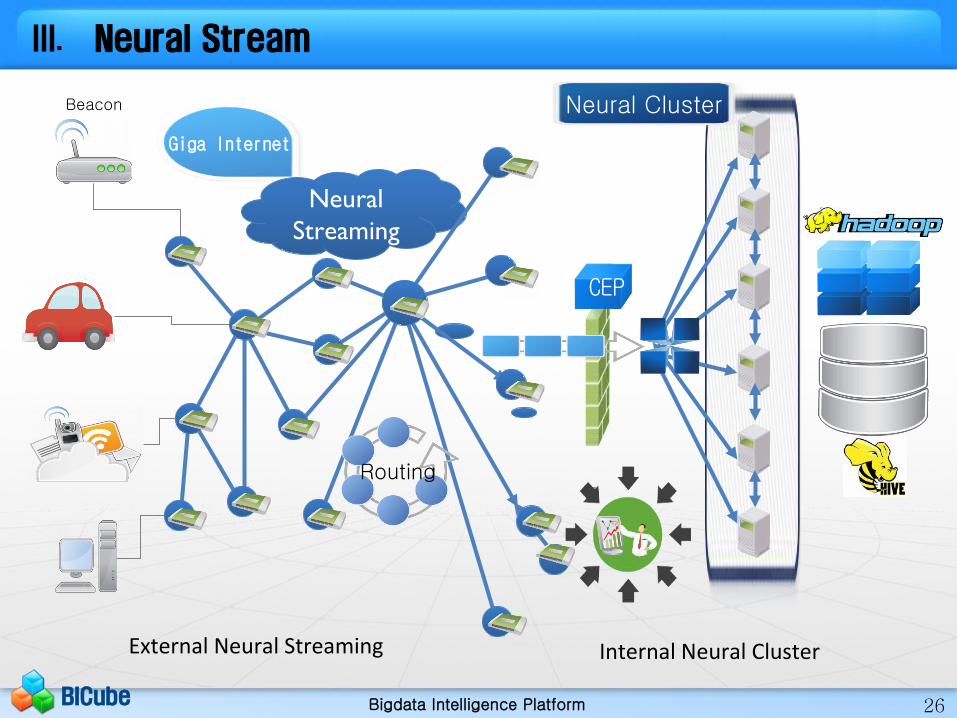

V. Fraud Detection System

이상금융거래탐지 시스템이란

전자금융거래 이용자 전자 금융거래 정보를 분석하여 이용자의 거래 이상유무를 분석,차단하는 시스템.

Bigdata Intelligence PlatformBICube 50

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 51

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 52

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 53

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 54

1.고객ID(S10) 2.IP주소(S20) 3.접속일자(S8) 4.접속시간(S10)5.고객ID(S10) 6.거래채널구분(S20) 7.거래종류(S20) 8.거래고유번호(S10)9.출금은행명(S20) 10.출금계좌(S20) 11.출금계좌예금주명(S20) 12.출금계좌예금주명(S20) 13.보내는통장표시내용(S50) 14.입금은행코드(S3) 15.입금계좌(S20) 16.입금계좌예금주명(S20) 17.받는통장표시내용(S50) 18.거래금액(N20) 19.이체수수료(N20)20.거래후잔액(N20) 21.거래일자(S8) 22.거래시간(S10)

1.000167,2.153.167.89.7,3,20140418,4.04:20:34,5.000167,6.인터넷뱅킹7.즉시이체,로그인/잔액조회,이체잔액조회8.0000000002,9.xx은행,10.123-45-678915,11.이순신67,12.이순신67,13.송금합니다.,14.신한은행,15.144-23141-2477,16.김길동167,17.(이순신67)님께서 입금하셨습니다.,18.9708000,19.1000,20.31401000,21.20140418,22.00:04:40 -예시-

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 55

모니터링단계/모드에 따른 기능

• 배치타임(bach/non-realtime) 모니터링 기능- 저장된 로그 파일에 대한 매뉴얼 혹은 자동화된 모니터링 모드- 저장된 트랜잭션을 사후에 세부적으로 검토 가능하나 즉각적인 탐지 대응은 어려움

• 리얼타임(real time) 모니터링기능- 웹서버 필터를 사용하여 실시간으로 모든 트랜잭션을 모니터링 하는 모드- 응용프로그램에 대한 수정을 필요로 하지 않음

• 어플리케이션 기능을 이용 하는 리얼타임 모니터링 기능- 어플리케이션에 모니터링 기능을 통합 하여 웹 트랜잭션을 모니터링 하는 모드- 어플리케이션 자체를 수정해야하는 요구사항을 가짐

• 외부 어플리 케이션 기반 리얼타임 모니터링 기능- 외부 어플리케이션을 이용해 모든 웹 트랜잭션을 모니터링 하는 모드- 이 방식은 웹 필터와 모니터링 모듈이 순차적으로 작동하기 때문에 어플리 케이션의 성능에 영향을 미칠 수 있음

• 다중채널 데이터 수집 모니터링 기능- 다른 채널로부터의 트랜잭션데이터를 통합하여 부정행위를 모니터링하고 탐지하는 모드

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 56

모니터링단계/대상에 따른 기능

•데이터베이스- 특정 사용자와 관련된 데이터베이스 트랜잭션을 모니터링 하는 기능

•데이터/콘텐츠- 데이터 패턴 규칙 에 따라 부적절한 콘텐츠나 데이터의 사용을 모니터링하는 기능

•서비스- 특정 서비스의 비즈니스 룰 에 따라 해당 어플리케이션 서비스 및 접근 채널에서 의심되는 사용자 활동을 모니터링 기능

•네트워크- 특정 사용자와 연관된 어플리케이션들의 비정상적인 네트워크 트래픽 을 모니터링하는 기능- 네트워크 이외에 파일 시스템, 콘텐츠, 데이터베이스까지 포괄하여 모니터링하지 못함

•보안이벤트- 다양한 보안 모니터링 장치 에 의해 인프라에서 어플리케이션까지 광범위한 범위 로부터의 보안 이벤트를 모니터링 하 는 기능

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 57

탐지단계

•트랜잭션 캡처- 사용자가 처음 액세스 한 이후에 각 사용자의 행위 프로파일을 자동적으로 생성하고 트랜잭션으로부터 이상행위 속성을 추출하여 매핑하는 기능

•이상행위 패턴 갱신- 네트워크로부터 이상 행위 데이터를 자동적으로 갱신하는 기능 - 이상 행위 데이터는 규칙에 벗어나는 트랜잭션 위치정보, 블랙리스트 단말 정보 등을 포함함

•사전 정의 규칙 지원- 이상행위 탐지 시스템이 사전에 정의한 탐지 규칙에 기반하여 동작하는 기능- 부가적으로 신규 규칙을 생성, 수정,삭제하는 기능을 포함하며, 다른 조직과 규칙을 공유 가능할 수 있음

•실시간 룰 처리 기능- 사용자/세션의 위협 스코어와 세부적인 위협 통지를 실시간으로 생성할 수 있는 기능- 사용자의 행위를 일정시간이상 프로파일하여 비정상적인 사용자 행위, 블랙/화이트 리스트, 이상 행위 데이터, 정상 위치데이터 등을 이용하는 기능- 본 기능을 통하여 특정 위협 수준 이상의 경우 대응 및 차단 행위로 연계할 수 있음

•관리 도구 지원- 관리도구는 알려진 이상 징후 상태, 활동현황, 새로운 이상 징후에 대해 관리자 인터페이스를 제공하고 e메일과 웹서비스 통지를 포함하는 통지 메커니즘 설정을 지원

•사후 트랜잭션 분석- 사후 이상징후 분석을 위해 관련 모든 데이터를 저장하고 수집하는 기능으로 일정기간 동안 모든 사용자의 거래 데이터를 포함- 부정방지시스템은 각 사용자의 행위 프로파일을 사용하여 세션, 사용자,시간에 따라 각 트랜잭션의 사후 분석을위하여 분류 및 수집 저장함

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 58

•포렌식 분석 기능- 패턴에 따라 트랜잭션 데이터의 세부 내용을 분석하고 추출 검색하는 기능으로 실시간 탐지 룰을 위한 신규 부정 패턴을 식별하는 것을 지원

•사용자 행위 프로파일 및 학습 기능- 행위 프로파일은 정상적인 사용자의 행위로부터 벗어나는 사용자 행위에 대하여 위협 여부를 결정하기 위한 근거로 활용- 모든 개별 사용자에 대하여 처음 접속 시점부터 일정기간 동안 정상 행위 패턴의 프로파일을 생성하는 기능

•지능적인 이상행위 패턴 탐지- 모든 부정거래가 개별적인 데이터 필드와 네트워크 응용 로그를 통해서만 탐지될 수 없음- 데이터 간의 연관성 분석과 평가를 위하여 지능적인 탐지 알고리즘 및 기능이 필요

•특정 서비스의 이상행위 패턴 탐지 패턴- 알려진 부정 패턴 및 서비스 의존적인 부정 패턴에 일치하는 트랜잭션의 패턴을 찾기 위한 규칙을 정의하는 기능- 서비스의 비즈니스 로직에 따라 의심되는 트랜잭션의 특정 순서나 상태를 찾는 기능

•다중 채널 위협 평가- 부정탐지시스템은 주어진 응용, 채널 이외에 전화, 웹, 대면 거래 등의 다중채널, 및 신용거래, 직불거래 등의 다중 서비스 간에 부정행위를 탐지하는 기능- 부정탐지 시스템은 응용뿐만 아니라 시스템, 네트워크로부터의 부정행위와 연계하여 평가하는 기능

•자동 위협 분석 및 수준 평가- 보안 위협을 자동적으로 인식하고 평가하여 설정하는 기능

탐지단계

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 59

• 추가적인 사용자 인증 및 검증- 고수준의 보안을 요구하는 응용 혹은 부정 징후가 탐지된 접근에서 사용자에게 추가적인 인증 을 요구하는 기능- 사용자에게 사전에 정의된 정보나 인증 정보를 요청하거나, 추가적인 인증을위해 별도의 채널 인증 등을 요청 하는기능

• 부정행위 통지 및 경고- 의심된 행위가 탐지되었을 때 자동적으로 혹은 매뉴얼 하게 경고를 관리자에게 통지 하는 기능- 경고는 트랜잭션의 속성 행위 내용이 세부적으로 포함 되며, e메일, 페이저 등을 통해 전달

• 사용자 계정 차단- 의심되는 행위가 탐지되었을 때 사용자 계정에 접속 차단 을 적용하는 기능

차단단계

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 60

6 개월 동안 거래가 없다가 공인인증서를 재발급하고 3 건 이상의 거래를 한다.

3회이상거래?

이체No

Alert

6개월간이체거래?

공인인증서재발급?거래시작

No

Yes

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 61

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 62

V. Fraud Detection System

An overview of anomaly detection, 성균관대 이지형

Bigdata Intelligence PlatformBICube 63

V. Fraud Detection System

An overview of anomaly detection, 성균관대 이지형

Bigdata Intelligence PlatformBICube 64

V. Fraud Detection System

An overview of anomaly detection, 성균관대 이지형

Bigdata Intelligence PlatformBICube 65

V. Fraud Detection System

An overview of anomaly detection, 성균관대 이지형

Bigdata Intelligence PlatformBICube 66

V. Fraud Detection System

An overview of anomaly detection, 성균관대 이지형

Bigdata Intelligence PlatformBICube 67

Artificial Immune Systems

V. Fraud Detection System

Bigdata Intelligence PlatformBICube 68

V. Fraud Detection System

Credit Card Fraud Detection with Artificial Immune System

Bigdata Intelligence PlatformBICube 69

목차

I. Paradigm ShiftII. Machine LearningIII. Neural StreamIV. FinTechV. Fraud Detection SystemVI. Conclusions

Bigdata Intelligence PlatformBICube 70

한국 금융권의 이른바 신용 리스크(credit risk / creditworthiness) 점검 능력은 바닥 수준이다. 이유는 ‘(제3자) 보증’ 또는 ‘담보’ 때문

공인인증서와 액티브엑스의 금융 쇄국정책

강정수

핀테크 한국의 현실

VI. Conclusions

Bigdata Intelligence PlatformBICube 71

Classical rule-based approach

• Always “too late”: • New fraud pattern is “invented” by criminals • Cardholders lose money and complain • Banks investigate complains and try to understand the new pattern • A new rule is implemented a few weeks later • Expensive to build (knowledge intensive) • Difficult to maintain: • Many rules • The situation is dynamically changing, so frequently

• rules have to be added, modified, or removed …

VI. Conclusions

Bigdata Intelligence PlatformBICube 72

A perfect fraud detection system:• “Tuned” to every cardholder or bank account:each cardholder or bank account treated individually• Adaptive:evolve with slow/small changes in cardholder behavior• Fast (real-time)• High accuracy

A system based on profiles • Every cardholder gets a vector of parameters that describe his/her behavior: an “average-behavior” profile• The system constantly compares this “long-term” profile with the recent behavior of cardholder• Transactions that do not fit into cardholder’s profile are flagged as suspicious (or are blocked)• Profiles are updated with every single transaction, so the system constantly adopts to (slow and small) changes in cardholders’ behavior

VI. Conclusions

Bigdata Intelligence PlatformBICube 73

Challenge: real-time detection!

• Monitor in real time all POS/ATM transactions• Detect unusual patterns and block compromised cards as quickly as possible• Ideally: block compromised cards before fraud is discovered!• A big question: can we do it ???• Some numbers: • 3,000,000,000 transactions per year

• up to 15,000,000 transactions per day• up to 400 transactions per second (peak hours)• 100,000,000 cards

VI. Conclusions

Bigdata Intelligence PlatformBICube 74

Speed is the key !!!• Maintain a sliding buffer of the last billion transactions in RAM (fast memory)• Organize the transactions in such a way that some queries could be executed very fast• Develop some clever algorithms that operate on this data structure• Will it work??? Yes, it will !!! Yes, it does …• many transactions - billions - algorithms must be efficient• mixed variable types (generally not text, image)• large number of variables• incomprehensible variables, irrelevant variables• different misclassification costs• many ways of committing fraud• unbalanced class sizes (c. 0.1% transactions fraudulent)• delay in labelling• mislabelled classes• random transaction arrival times• (reactive) population drift

VI. Conclusions

Bigdata Intelligence PlatformBICube 75

Agent

TimeReducer

Daily

Weekly

Monthly

TwoMonth

ThreeMonth

FourMonth

FiveMonth

SixMonth

SevenMonth

EightMonth

NineMonth

TenMonth

TwoWeek

ThreeWeekTwoDay

ThreeDay

FourDay

FiveDay

SixDay

FourWeek

MetaParserTimeStore

Long Transaction Memory

BlackList

SeccueCode

POSEntry

VI. Conclusions

Bigdata Intelligence PlatformBICube 76

VI. Conclusions