Embed Size (px)

Citation preview

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

IG Execution and Client Trends

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

Execution Stats

•

•

•

•

•

•

•

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

ProOrder: Automated Trading and Backtesting

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

Client Trends

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014

Equities

FX

Futures

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

Client Sentiment

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

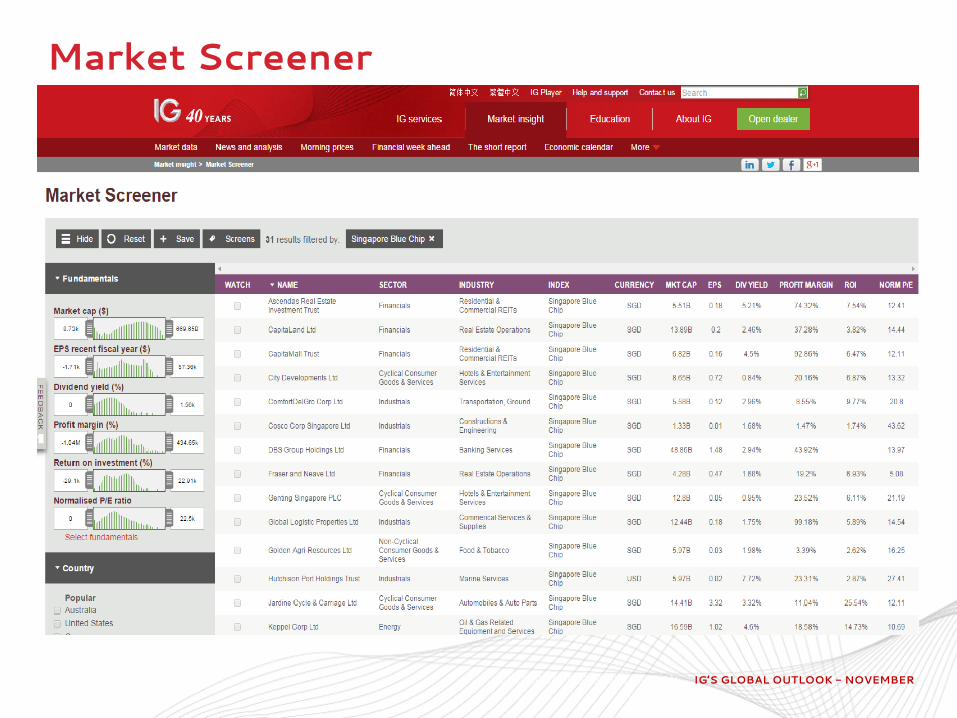

Market Screener

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

Chinese Opportunities

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SEARCHING SECTORS

RYAN HUANG

MARKET STRATEGIST

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

DISCLAIMER

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SECTOR ROTATION

WHICH INDUSTRIES BENEFIT?

-

-

-

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SECTOR ROTATION

WHICH INDUSTRIES BENEFIT?

ECONOMY

Recovery Expansion

EARLY MID LATE

Contraction

RECESSION

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SECTOR ROTATION

EARLY

• Activity rebounds! (GDP, IP, incomes)

• Credit

• Profit

• Policy still stimulative

• Inventories low: Sales improve

• Low interest rates, hints of economic improvement?

Consumer discretionary : Autos Financials : Real Estate, Banks Tech : Intel, Google, Microsoft, Apple Industrials : Boeing, Caterpillar and Lockheed

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

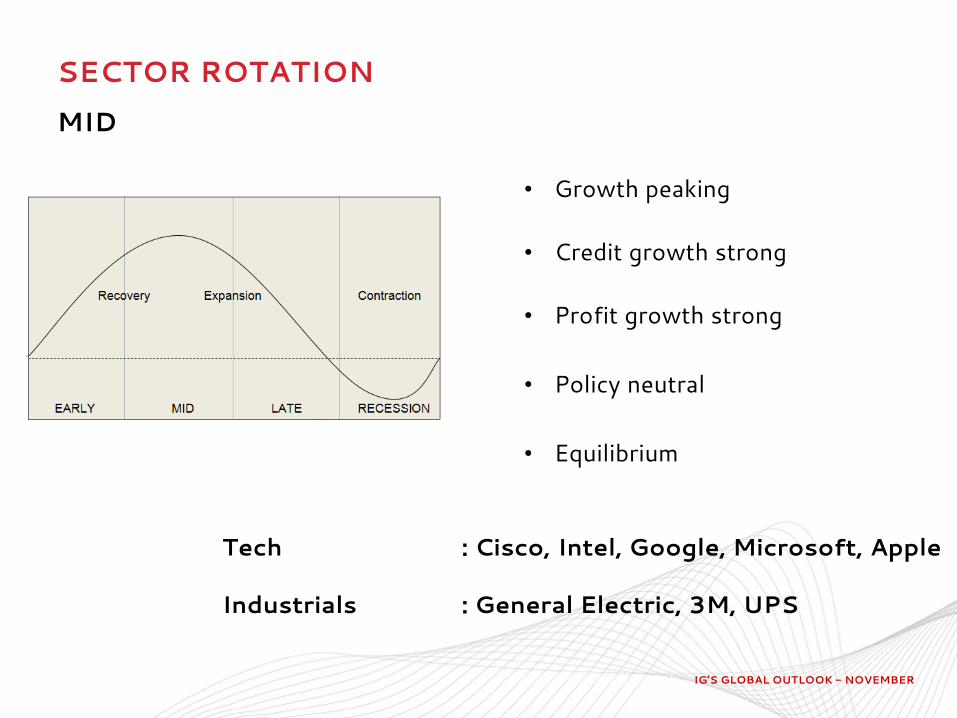

SECTOR ROTATION

MID

• Growth peaking

• Credit growth strong

• Profit growth strong

• Policy neutral

• Equilibrium

Tech : Cisco, Intel, Google, Microsoft, Apple Industrials : General Electric, 3M, UPS

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SECTOR ROTATION

LATE

• Growth moderating

• Credit tightens

• Earnings under pressure

• Overheating = Policy contraction

• Inventories grow, sales fall

Healthcare : GSK, Pfizer, Novartis, Roche Energy : Santos, Oil Search, Chesapeake, Peabody

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SECTOR ROTATION

RECESSION

• GDP flatlines

• Credit dries up

• Profits decline

• Policy eases

Consumer staples : Procter & Gamble, Unilever Healthcare : GSK, Pfizer, Roche, Gilead Utilities : Hyflux, American Electric Power

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SECTOR ROTATION

RELATIVE PERFORMANCE

(source: Fidelity Investments)

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

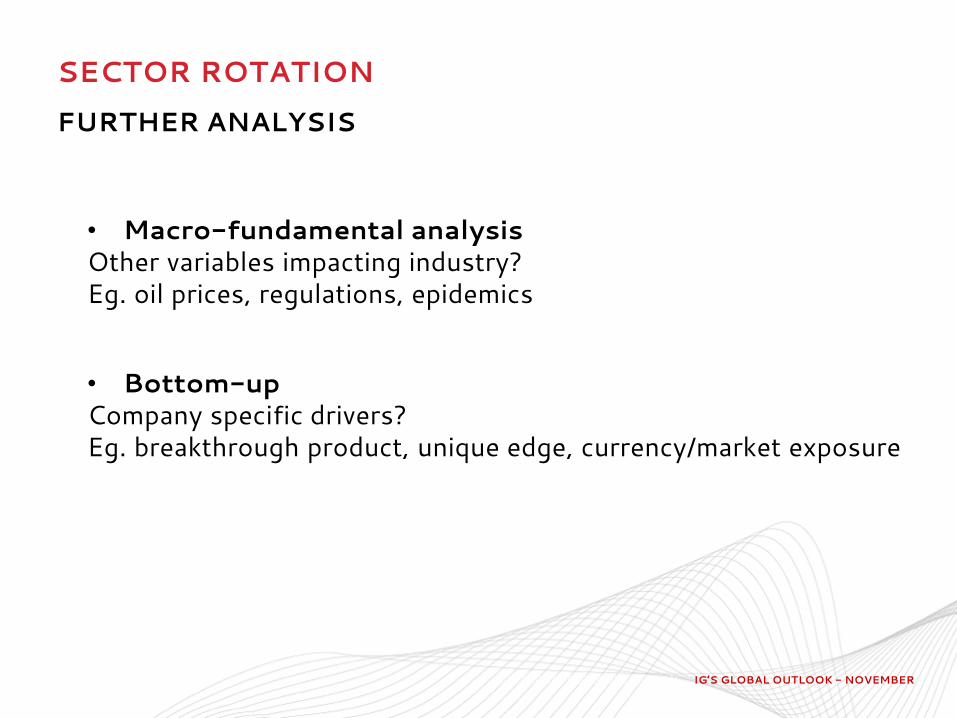

SECTOR ROTATION

FURTHER ANALYSIS

• Macro-fundamental analysis Other variables impacting industry? Eg. oil prices, regulations, epidemics • Bottom-up Company specific drivers? Eg. breakthrough product, unique edge, currency/market exposure

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

MACRO ANALYSIS

OIL Sharpest decline in recent years Down over 30% since June, 4-year lows

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

MACRO ANALYSIS

OIL

• lower input costs, good for biz

• lower expenses, household budgets grow

Winners • Retail, and F&B

• Airlines

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

MACRO ANALYSIS

OIL

Losers • BP earnings were hit by lower oil prices

• Woodside, Santos and Oil Search, SembCorp Marine

What next: to cut or not to cut? OPEC meeting on 27 November in Vienna

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

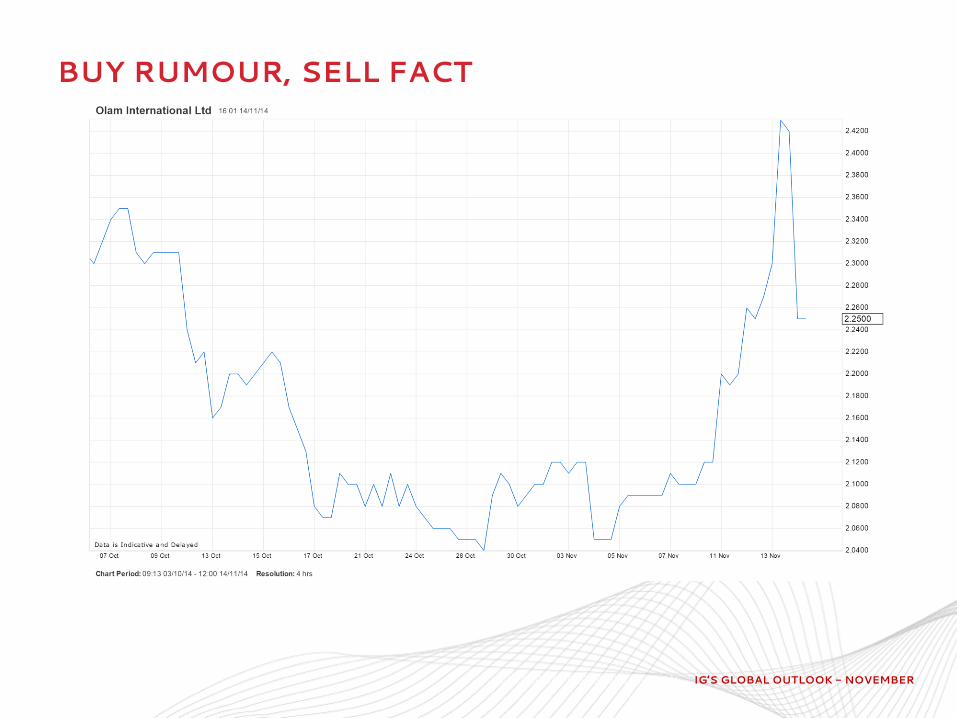

BUY RUMOUR, SELL FACT

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

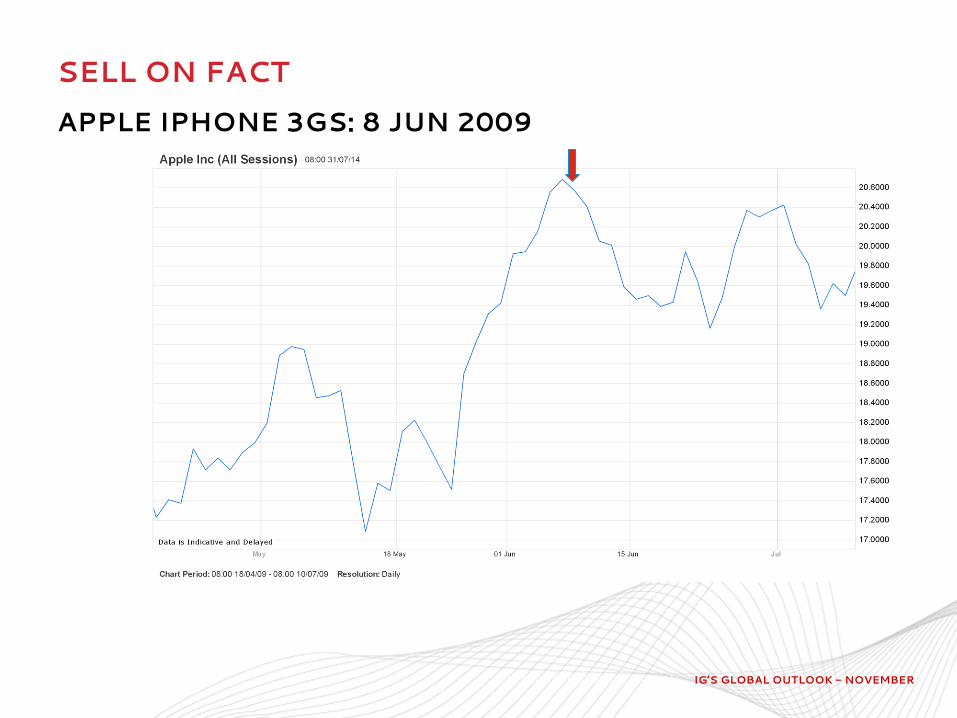

SELL ON FACT

APPLE IPHONE 5: 12, 19 SEP 2012

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SELL ON FACT

APPLE IPHONE 4: 7, 24 JUN 2010

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SELL ON FACT

APPLE IPHONE 3GS: 8 JUN 2009

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

IPHONE LAUNCH IMPACT

Product % change on

announcement

Pullback within a week

iPhone 6, 6 Plus -0.38% (Sept 9, 2014) NA

iPhone 5S, 5C -2.28% (Sept 10, 2013) -5.4%

iPhone 5 +1.39% (Sept 12, 2012) NA

iPhone 4S -0.56% (Oct 4,2011) -0.72%

iPhone 4 -1.96% (Jun 7, 2010) -3%

iPhone 3GS -0.57% (Jun 8, 2009) -5.3%

iPhone 3G -2.17% (Jun 9, 2008) -5.1%

iPhone +8.3% (Jan 9, 2007) NA

(Source: IG)

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

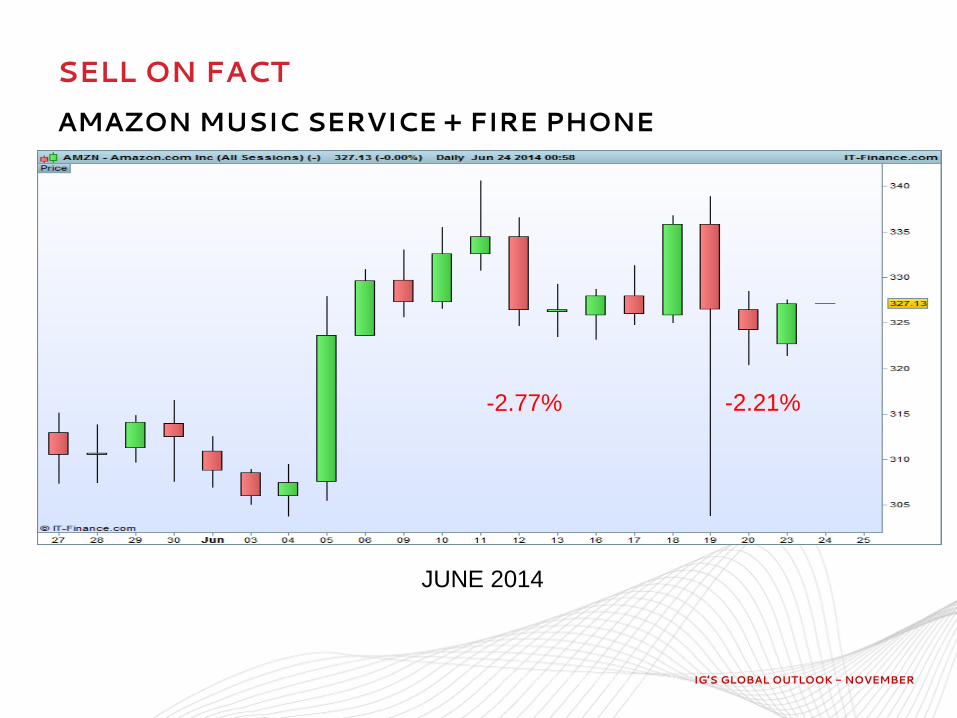

DIGGING FOR TECH

AMAZON

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

SELL ON FACT

AMAZON MUSIC SERVICE + FIRE PHONE

-2.77% -2.21%

JUNE 2014

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

GLOBAL MARKETS OUTLOOK November 2014

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

DISCLAIMER

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

US MARKET STILL TRENDING HIGHER

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

GOLD FIND BUYERS BELOW $1180

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

THE RACE FOR THE BOTTOM

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

BUY JAPAN

• US$ 180 billion of outflows • An extra ¥30 trillion in JGB

purchases

• Buying ETFs pegged to the JPX Nikkei

• Bank of Yokohama (8332) • Mitsubishi Estate (8802) • Sumitomo Electric • Nomura (8604) • MAZDA motors (7261)

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

USD/JPY – LOOKING STRONG

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

GBP/JPY – LOOKING STRONG

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

EUR/USD – EYEING KEY SUPPORT

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

WHY IG?

LARGEST CFD ASSET CLASS OFFERING

• Singapore shares – over 300 incl. flexibility using Direct Market Access (DMA)

• International shares – over 6000

• ETFs

• FX, over 60 pairs

• Stock Index CFDs, over 20 countries

• 24-hour trading is available for major indices

• Gold, Silver, Oil, Soft commodities

IG’S GLOBAL OUTLOOK LUNCEON IG’S GLOBAL OUTLOOK - NOVEMBER

Low transaction costs

• 0.10% commission for Singapore shares, 0.25% for HK shares, 2 cents / share for US market

• No commission for FX, commodities and indices – just highly competitive dealing spreads

Low capital requirement

Margin starts from :

• 10% for Share CFDs

• 2% for Forex CFDs

• 5% for Index CFDs

IS IG SUITABLE FOR YOU?

LARGEST CFD ASSET CLASS OFFERING