Embed Size (px)

Citation preview

Partono Arif 2014

A Knowledge audit should be the first step in any Knowledge Management initiative.

KMA assesses what knowledge assets are possessed by an organization, by knowing it the organization can find the effective method of storage and dissemination (Liebowitz, 2000).

KM audit provides evidence-based information about current knowledge status (knowledge health).

As a basis to set up new knowledge management program.

KM Teaching Group - Universitas TELKOM09/12/2014 2

Partono Arif 2014

A knowledge audit, is a qualitative evaluation.

KM audit will look at;

What knowledge are the organization’s needs?

What knowledge assets or resources does the organization has and where are they kept?

What gaps exist in its knowledge?

How does knowledge flow around the organization?

What blockages are there to that flow (to what extent do its people, processes and technology currently support or hamper the effective flow of knowledge?

09/12/2014 KM Teaching Group - Universitas TELKOM 3

Partono Arif 2014

KMA

The process to identify every knowledge,

Produced by an organization,

Who produce and use it,

How frequent is the knowledge used, and

Where is the knowledge stored.

Once the as is” portrait of the organization has been completed through information gathering and the knowledge audit, a gap analysis can be performed

KM Teaching Group - Universitas TELKOM09/12/2014 4

Partono Arif 2014

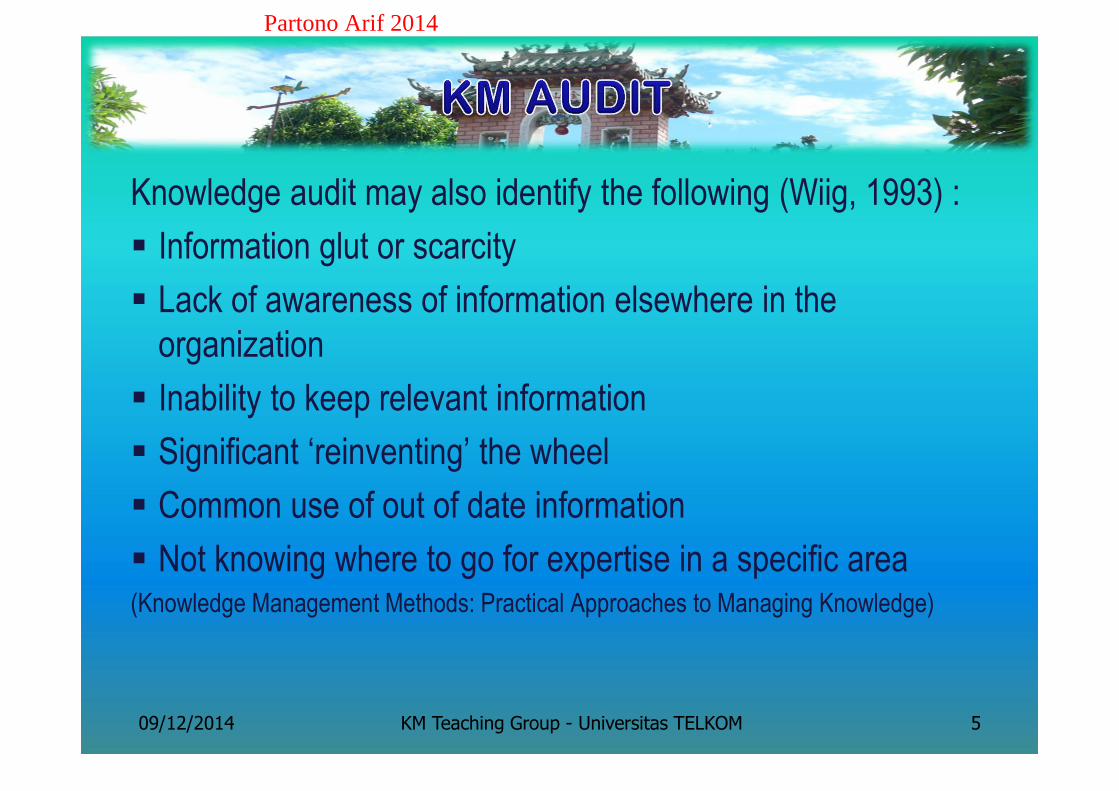

Knowledge audit may also identify the following (Wiig, 1993) :

Information glut or scarcity

Lack of awareness of information elsewhere in the organization

Inability to keep relevant information

Significant ‘reinventing’ the wheel

Common use of out of date information

Not knowing where to go for expertise in a specific area(Knowledge Management Methods: Practical Approaches to Managing Knowledge)

09/12/2014 KM Teaching Group - Universitas TELKOM 5

Partono Arif 2014

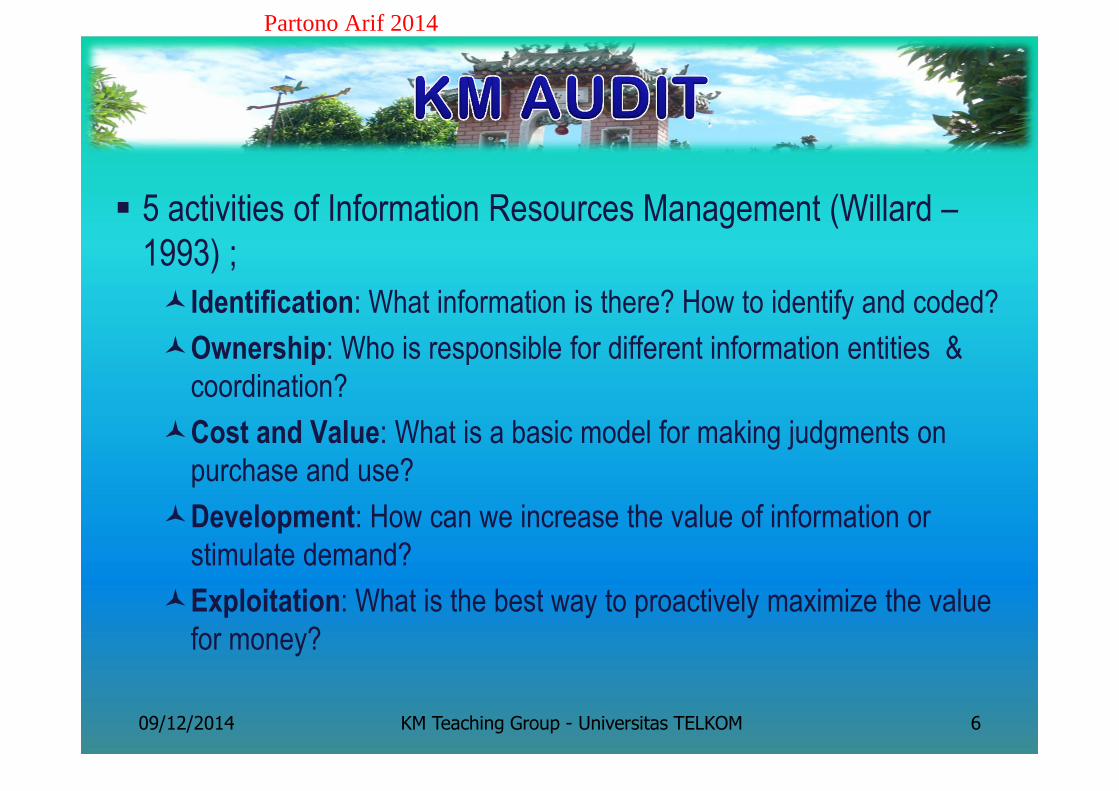

5 activities of Information Resources Management (Willard –1993) ;

Identification: What information is there? How to identify and coded?

Ownership: Who is responsible for different information entities & coordination?

Cost and Value: What is a basic model for making judgments on purchase and use?

Development: How can we increase the value of information or stimulate demand?

Exploitation: What is the best way to proactively maximize the value for money?

KM Teaching Group - Universitas TELKOM09/12/2014 6

Partono Arif 2014

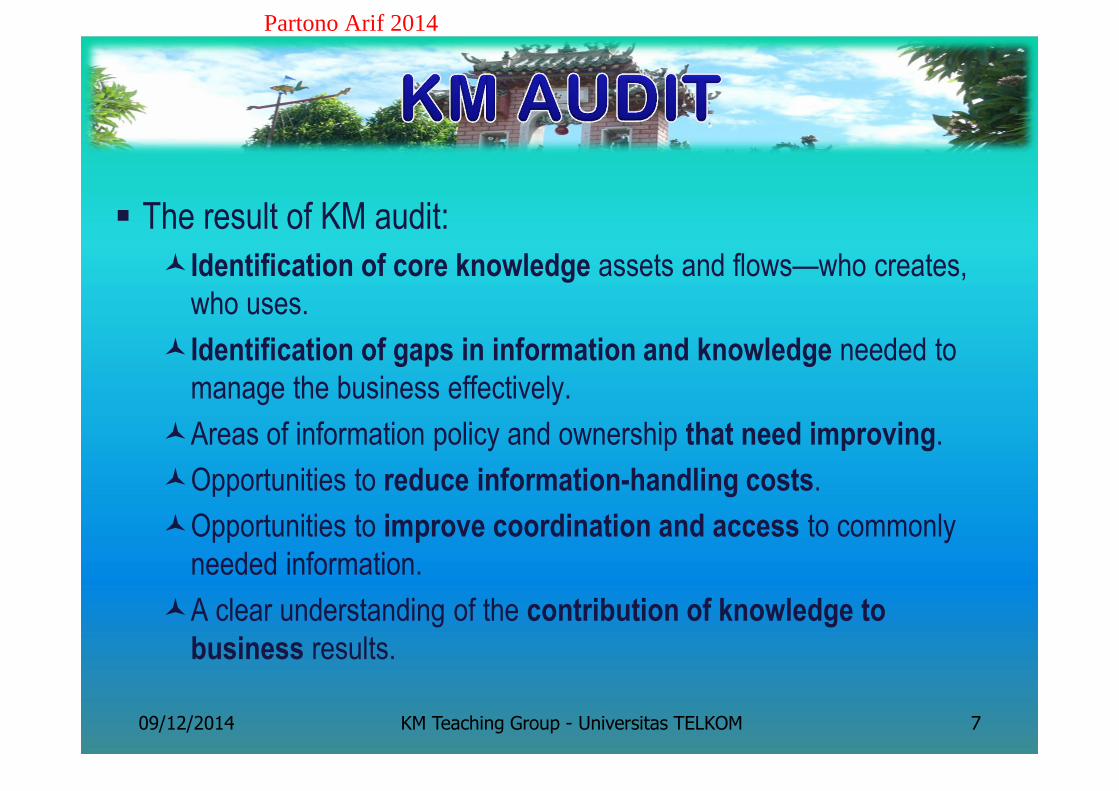

The result of KM audit:

Identification of core knowledge assets and flows—who creates, who uses.

Identification of gaps in information and knowledge needed to manage the business effectively.

Areas of information policy and ownership that need improving.

Opportunities to reduce information-handling costs.

Opportunities to improve coordination and access to commonly needed information.

A clear understanding of the contribution of knowledge to business results.

KM Teaching Group - Universitas TELKOM09/12/2014 7

Partono Arif 2014

The difference between the organization’s existing and desired KM state is analyzed to identify the enablers and barriers to KM implementation

Gap analysis should consider these points ;

What are the major differences between the current and desired KM

Recent situation of the organization?

List barriers to KM implementation (e.g., culture where “knowledge is power” or where individual possession of knowledge is consistently rewarded).

List KM leverage points or enablers (e.g., existing initiatives that could be built upon)

KM Teaching Group - Universitas TELKOM09/12/2014 8

Partono Arif 2014

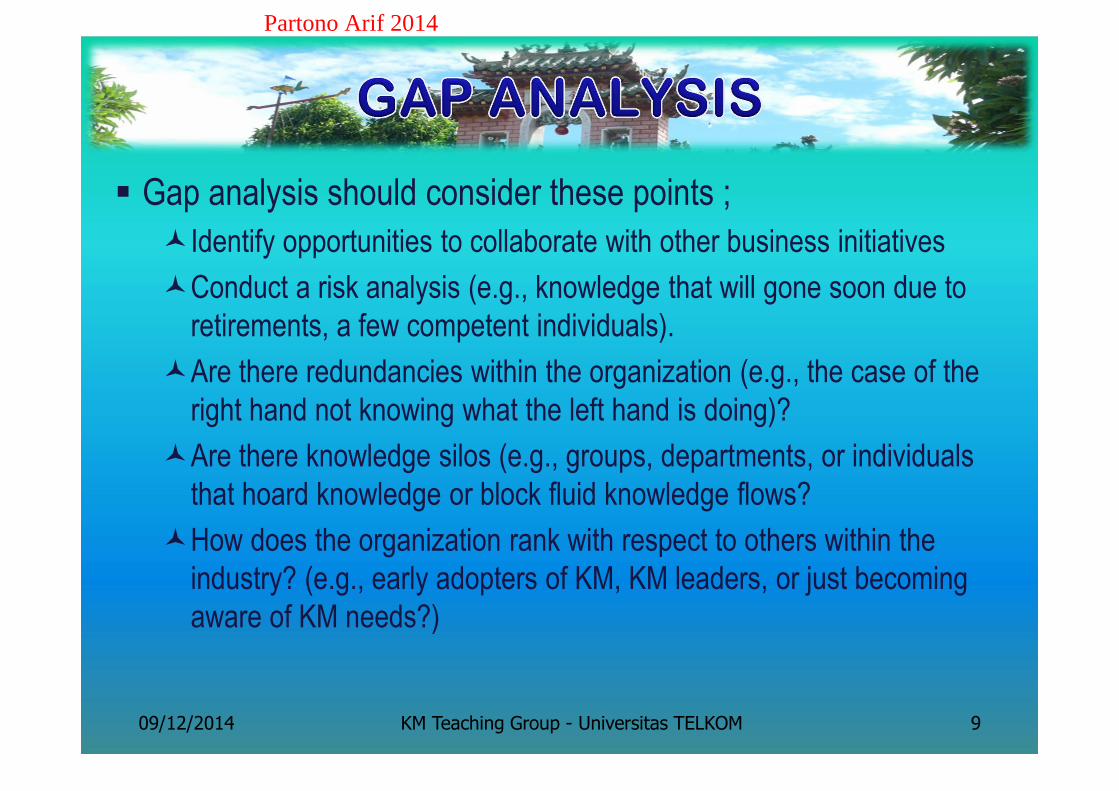

Gap analysis should consider these points ;

Identify opportunities to collaborate with other business initiatives

Conduct a risk analysis (e.g., knowledge that will gone soon due to retirements, a few competent individuals).

Are there redundancies within the organization (e.g., the case of the right hand not knowing what the left hand is doing)?

Are there knowledge silos (e.g., groups, departments, or individuals that hoard knowledge or block fluid knowledge flows?

How does the organization rank with respect to others within the industry? (e.g., early adopters of KM, KM leaders, or just becoming aware of KM needs?)

KM Teaching Group - Universitas TELKOM09/12/2014 9

Partono Arif 2014

This result can be used to list and prioritize KM objectives to be addressed by the organization.

The priorities should be determined by a consensus of the organization’s key stakeholders.

The result will be a KM strategy in form of document which used as road map to implement KM within the organization.

KM Teaching Group - Universitas TELKOM09/12/2014 10

Partono Arif 2014

KM Teaching Group - Universitas TELKOM09/12/2014 11

Assembly Hall, Hoi AnVietnam, 2012

Partono Arif 2014

Intellectual assets are intellectual materials that have been formalized, captured, and leveraged to produce higher value for the firm

Intellectual asset classified as ;

Body of tacit and explicit knowledge about a task, person, or organization.

The capital resources (human, structural, and relational) that augment this body of knowledge.

09/12/2014 KM Teaching Group - Universitas TELKOM 12

Partono Arif 2014

3 categories of knowledge assets (p. 267)

Human Capital brainpower that left after 5 pm

Structural Capital brainpower that stay after 5 pm (procedures, system, software, policies, patent)

Customer Capital relationship value (current & future)

09/12/2014 KM Teaching Group - Universitas TELKOM 13

Partono Arif 2014

Organization can take inventories of the IC/IA, or even sell them (training, consultancies)

Example of IA inventories (ideas);

Product formulas

Business plan

Marketing strategies

Vendor terms

Employee information

Product composition

New services process

SWOT analysis

09/12/2014 KM Teaching Group - Universitas TELKOM 14

Partono Arif 2014

4 dimensions of business that form Skandia Navigator model

Financial focus, represented in monetary terms.

Customer focus, a financial and nonfinancial measure of the value of customer capital.

Process focus, address the effective use of technology within organization

Renewal and development focus, attempts to capture the innovative capabilities of the organization.

All related to human capital

09/12/2014 KM Teaching Group - Universitas TELKOM 15

Partono Arif 2014

3 popular approach for measuring KM are ;

Benchmarking

Balance scorecard

House of quality

09/12/2014 KM Teaching Group - Universitas TELKOM 16

Partono Arif 2014

Comparison with key leader in the industry to identify any best practices that can be applied in other organization

Avoiding wheel reinventing, by looking at what has worked and what has not worked for other companies operating in comparable environments or industrial sectors

Lack of sufficient value & flexibility in the future, leads to other measurement tools and techniques to measure the effectiveness of KM

09/12/2014 KM Teaching Group - Universitas TELKOM 17

Partono Arif 2014

Originated from Xerox in 1970’s, when they learn the logistic model of LL Bean (p. 272)

Learn from the best to become one

Internal – comparison against other unit

External – comparison with other companies/industries

3 types of benchmarking (read p. 273)

Industry group measurement

Best practices studies

Cooperative / collaborative benchmarking

Competitive benchmarking

09/12/2014 KM Teaching Group - Universitas TELKOM 18

Partono Arif 2014

Industry group measurement

Measurement of various aspects of the operation and compare to similar industry measurements.

Best practices studies

Studies and lists of what works best.

Useful to benchmarking research, but they are not useful as metrics.

What works best for an organization in its specific environment may not work the same way in another environment.

Book, consulting, research

09/12/2014 KM Teaching Group - Universitas TELKOM 19

Partono Arif 2014

Cooperative benchmarking

the measurement of key production functions of inputs, outputs, and outcomes with the aim of improving them.

Performed with the assistance of the entity being studied (the benchmark “partner”).

The entity selected as a benchmark must be the one that has “best practices” in the area of interest or has won a major national or international quality award.

Collaborative benchmarking

Both entities study each other and work together to improve.

09/12/2014 KM Teaching Group - Universitas TELKOM 20

Partono Arif 2014

Competitive benchmarking

The study and measurement of a competitor without its cooperation for the purposes of process or product quality improvement.

A version of competitive benchmarking is the commisioning of a third party to study a group of competitors and share the results.

The third party consultant is might knows what data belong to which entity.

09/12/2014 KM Teaching Group - Universitas TELKOM 21

Partono Arif 2014

The key steps ;

1. Determine what to benchmark: which knowledge processes, products, services? Why? With what scope?

2. Form a benchmarking team.

3. Select a benchmarking short list—which companies will you be benchmarking against?

4. Collect and analyze data.

5. Determine what changes should be made as a result of the metrics obtained

6. Repeat when an appropriate amount of time has lapse to measure progress

09/12/2014 KM Teaching Group - Universitas TELKOM 22

Partono Arif 2014

The potential benefit ;

Overall productivity of knowledge investments.

Service quality.

Customer satisfaction and the operational level of customer service.

Time to market in relation to other competitors.

Costs, profits, and margins.

Distribution.

Relationships and relationship management.

09/12/2014 KM Teaching Group - Universitas TELKOM 23

Partono Arif 2014

A measurement and management system that enable organization to clarify its vision & strategy, then translate them into action

Provides feedback on both the internal business processes and external outcomes in order to continuously improve strategic performance and results.

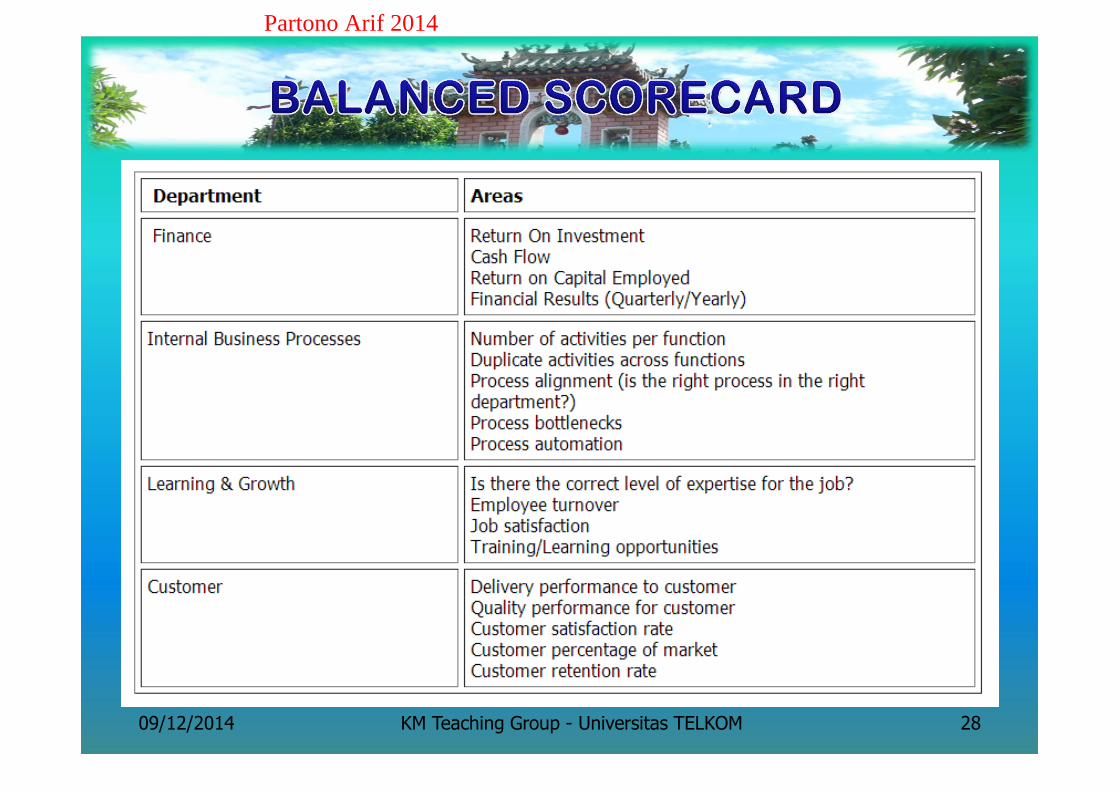

A conceptual framework for translating an organization’s vision into a set of performance indicators distributed among four dimensions – Financial, Customer, Internal Business Process, Learning & Growth

See p. 275 for the illustration of BSC

09/12/2014 KM Teaching Group - Universitas TELKOM 24

Partono Arif 2014

09/12/2014 KM Teaching Group - Universitas TELKOM 25

Partono Arif 2014

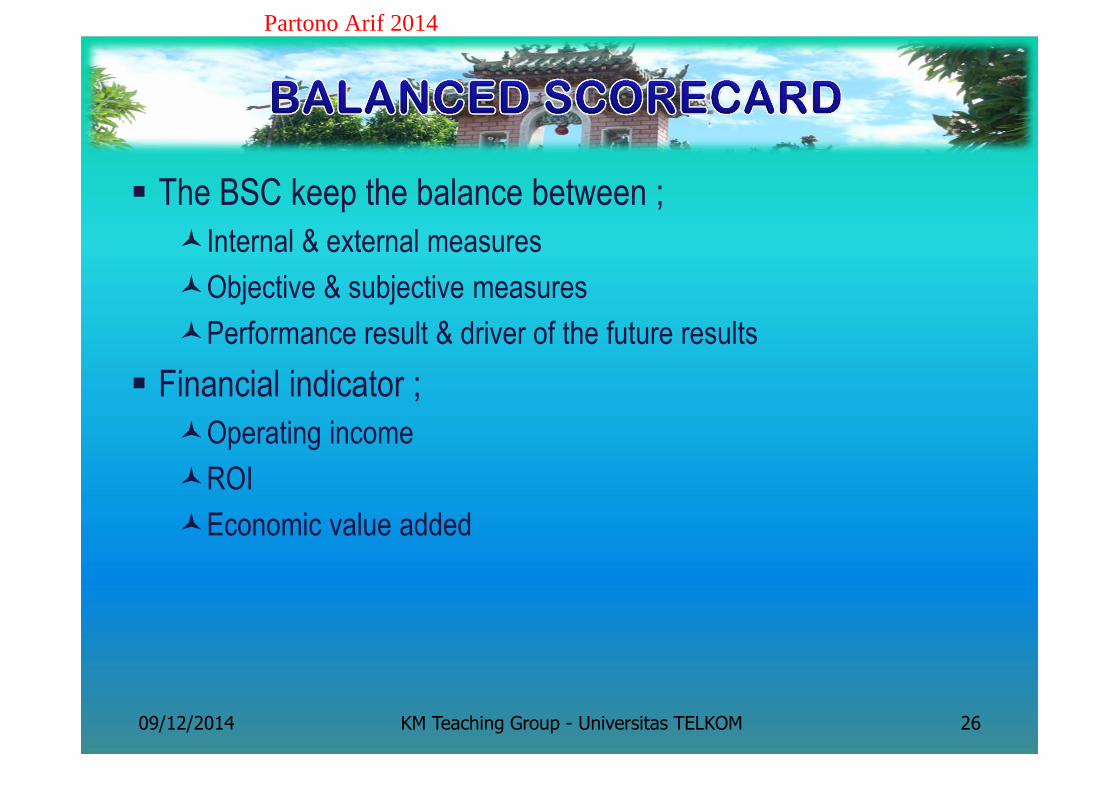

The BSC keep the balance between ;

Internal & external measures

Objective & subjective measures

Performance result & driver of the future results

Financial indicator ;

Operating income

ROI

Economic value added

09/12/2014 KM Teaching Group - Universitas TELKOM 26

Partono Arif 2014

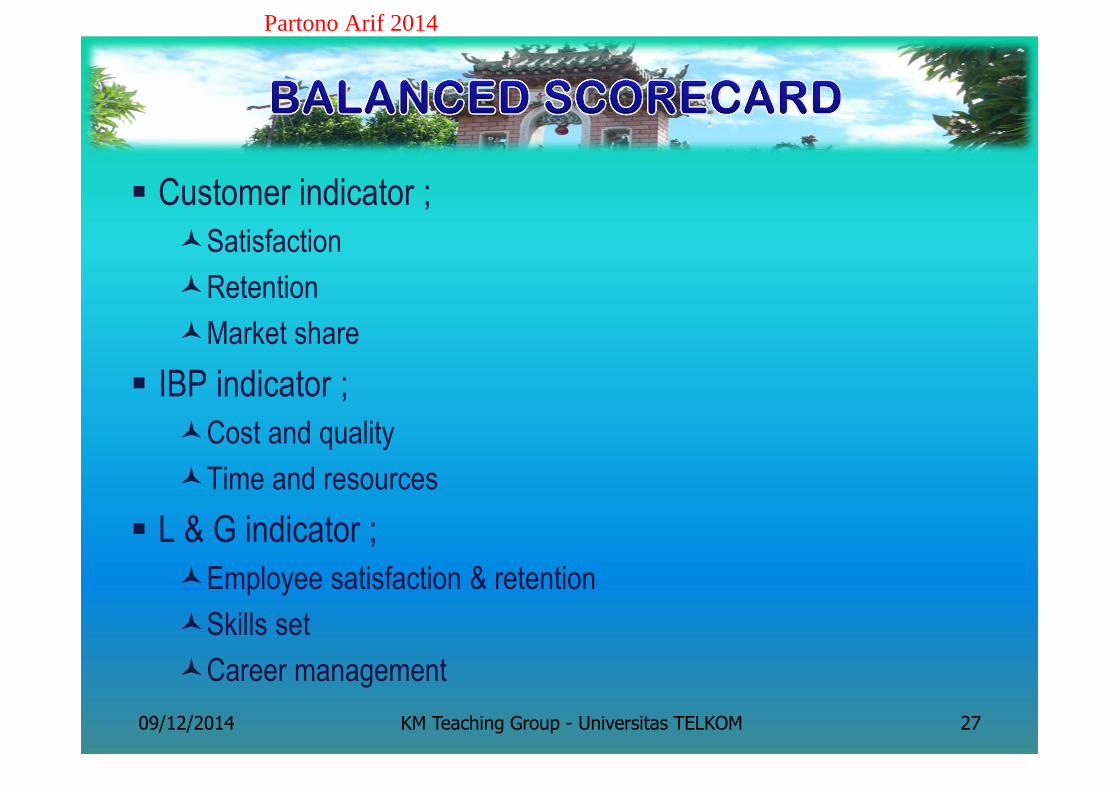

Customer indicator ;

Satisfaction

Retention

Market share

IBP indicator ;

Cost and quality

Time and resources

L & G indicator ;

Employee satisfaction & retention

Skills set

Career management

09/12/2014 KM Teaching Group - Universitas TELKOM 27

Partono Arif 2014

09/12/2014 KM Teaching Group - Universitas TELKOM 28

Partono Arif 2014

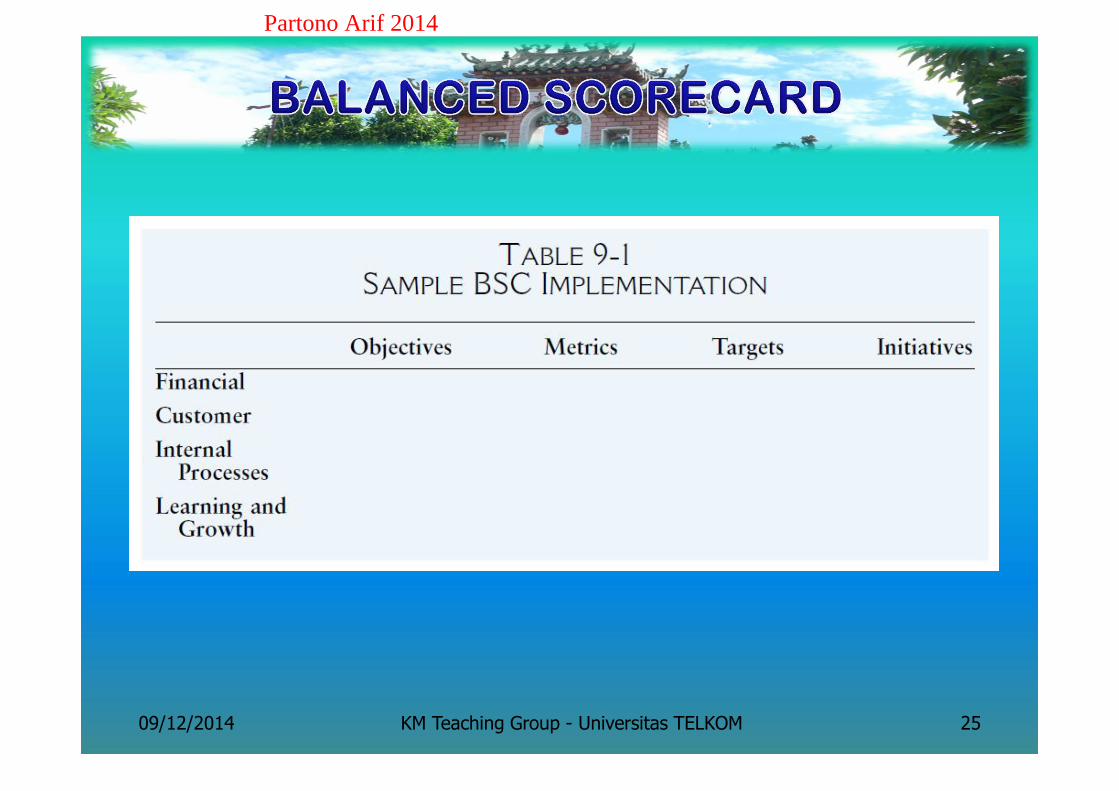

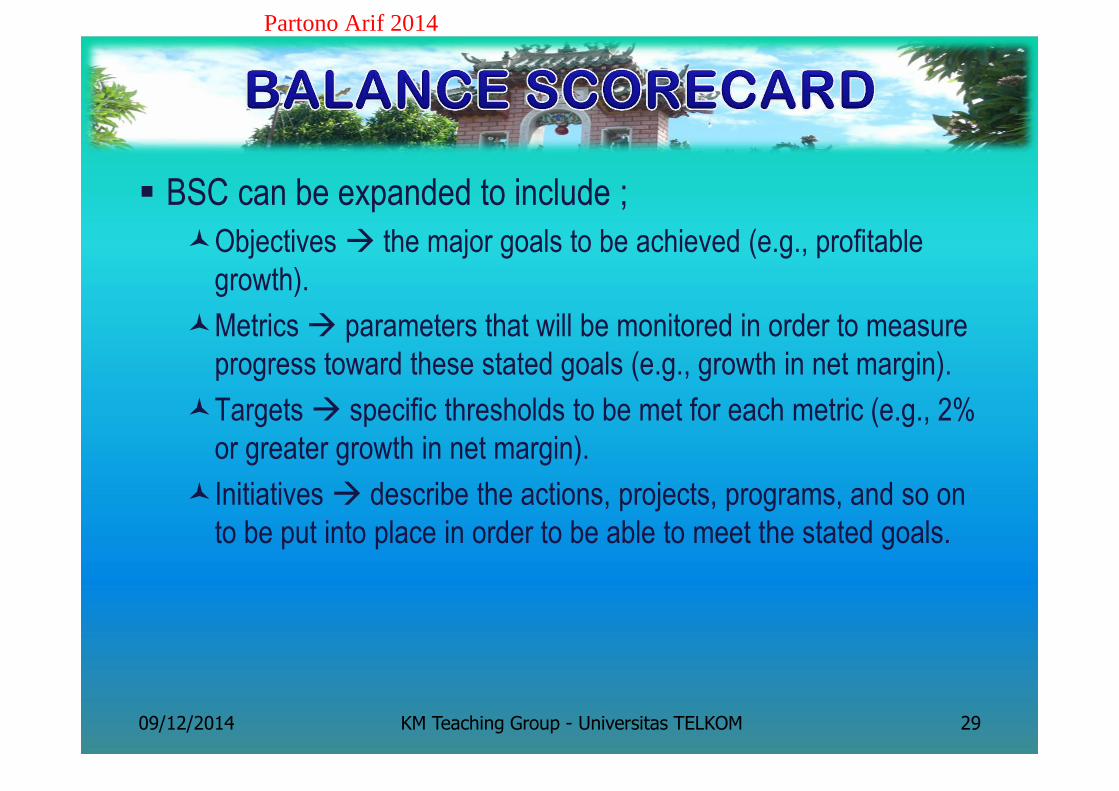

BSC can be expanded to include ;

Objectives the major goals to be achieved (e.g., profitable growth).

Metrics parameters that will be monitored in order to measure progress toward these stated goals (e.g., growth in net margin).

Targets specific thresholds to be met for each metric (e.g., 2% or greater growth in net margin).

Initiatives describe the actions, projects, programs, and so on to be put into place in order to be able to meet the stated goals.

09/12/2014 KM Teaching Group - Universitas TELKOM 29

Partono Arif 2014

09/12/2014 KM Teaching Group - Universitas TELKOM 30

Partono Arif 2014

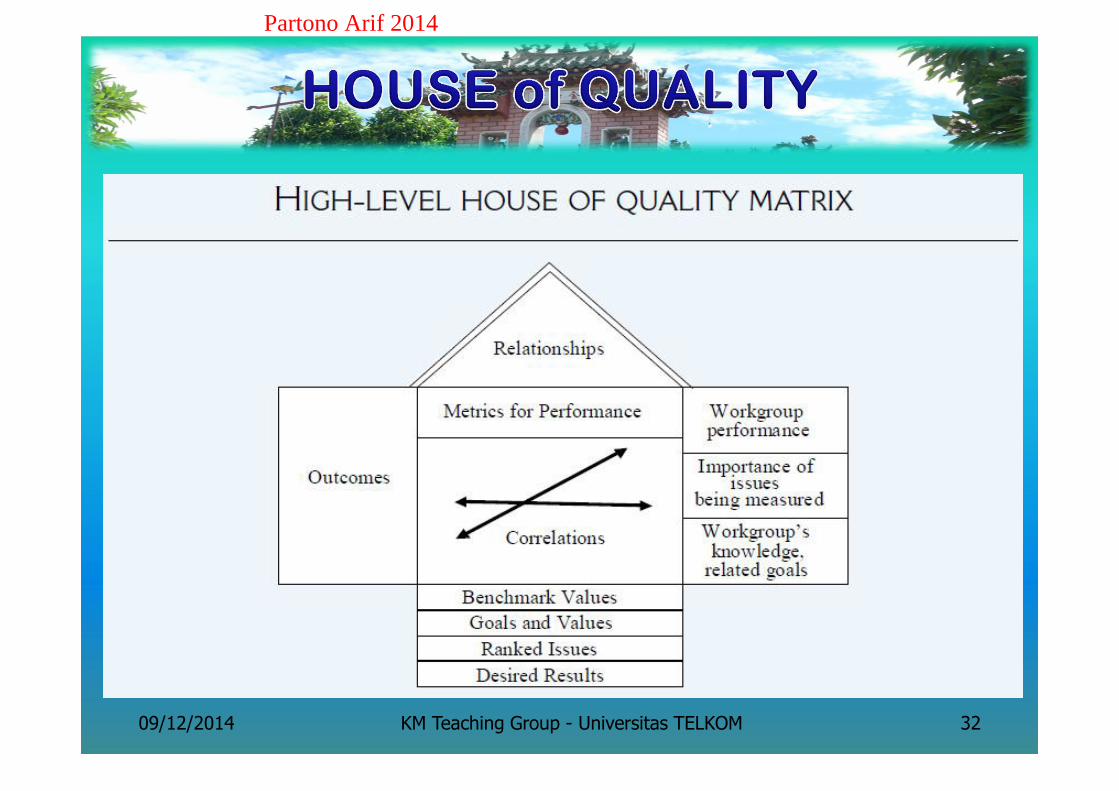

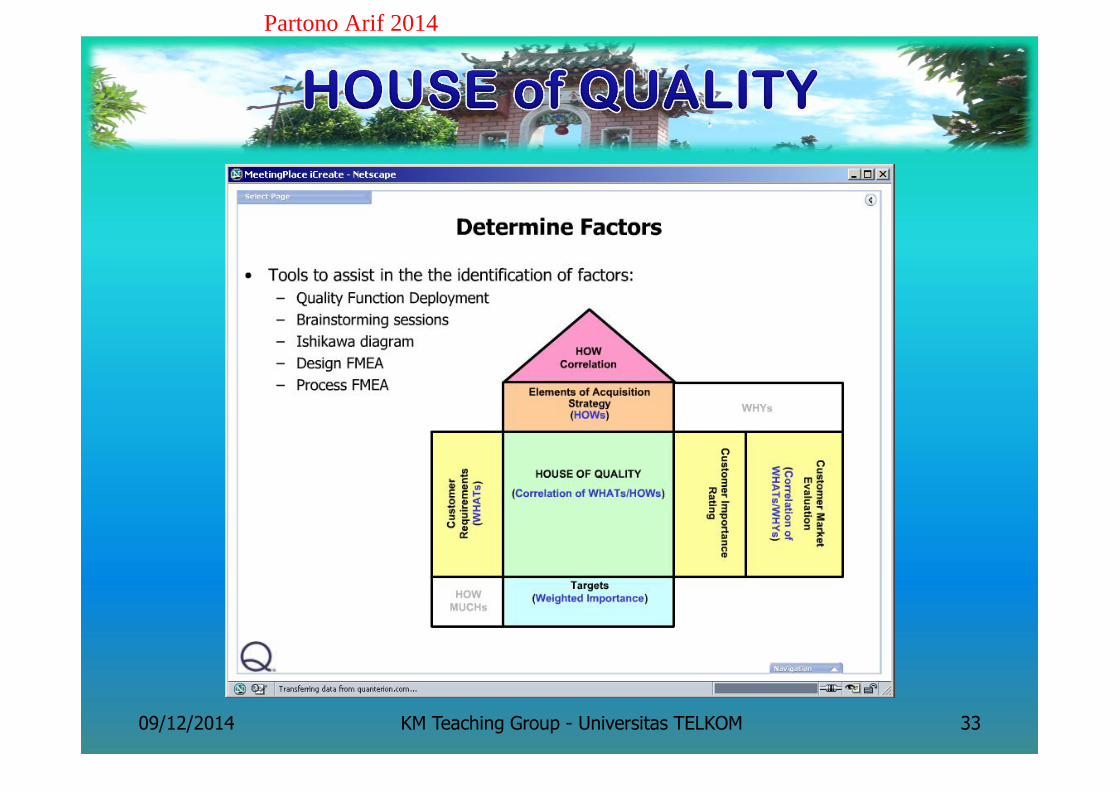

Develop to show the connection between true quality, quality characteristics, & process characteristic

09/12/2014 KM Teaching Group - Universitas TELKOM 31

Partono Arif 2014

09/12/2014 KM Teaching Group - Universitas TELKOM 32

Partono Arif 2014

09/12/2014 KM Teaching Group - Universitas TELKOM 33

Partono Arif 2014