Embed Size (px)

Citation preview

WELKOM

Nikolas Vandelanotte

#FIER! Vandelanotte 2015 – 2016 Cloud accountant award winner

PROGRAMMA

Björn Crul

LET’S MEET Colors speak louder than words.

Jonas “Je moet show verkopen als je

een bedrijf begint” Jonas Dhaenens

7 STARTUP INSIGHTS Wim Derkinderen

Claim back your time By Wim derkinderen

About Myself

• Master in Economics, Sales & Marketing

• Self employed since 2014

• Investing in Real Estate, Stock exchange market and Startups/Scale ups

• Spacechecker: Satellite tracking & Tracing of Trailers and containers

• Netlog: Social Network, mainly for youngsters

• Cardwise: Prepaid MasterCard Program Management

• Xpenditure: Cloud based Expense management platform

About Xpenditure

• Founded in 2011

• Our shareholders:

Boris Bogaert & Wim Derkinderen

Lorenz Bogaert & Toon Coppens - founders Netlog.com/Twoo.com

Jonas Dhaenens - Founder Combell

Luc Verelst - Founder Verelst real estate group, Eurinpro, Droia, AntiCancerfund,…

Bart Swanson - Former MD Amazon EU, Former CCO Badoo, Advisor Horizon Ventures

• Capital: 8 Mio Euro (new fundraise October 2015)

• Headcount: 48 FTE and counting…

• Offices in Mechelen (Belgium), London, Amsterdam, Cologne, New York and Sao Paulo

• > 80000 customers in 167 countries

A Global Reach, A Local Approach

Offices in Mechelen (Belgium), London,

Amsterdam, Cologne, New York and Sao

Paulo

Users in 160 countries and more

A Short Introduction

We redefine expense management for

businesses of all sizes

by introducing a fully digital, real time process.

No more expense notes!

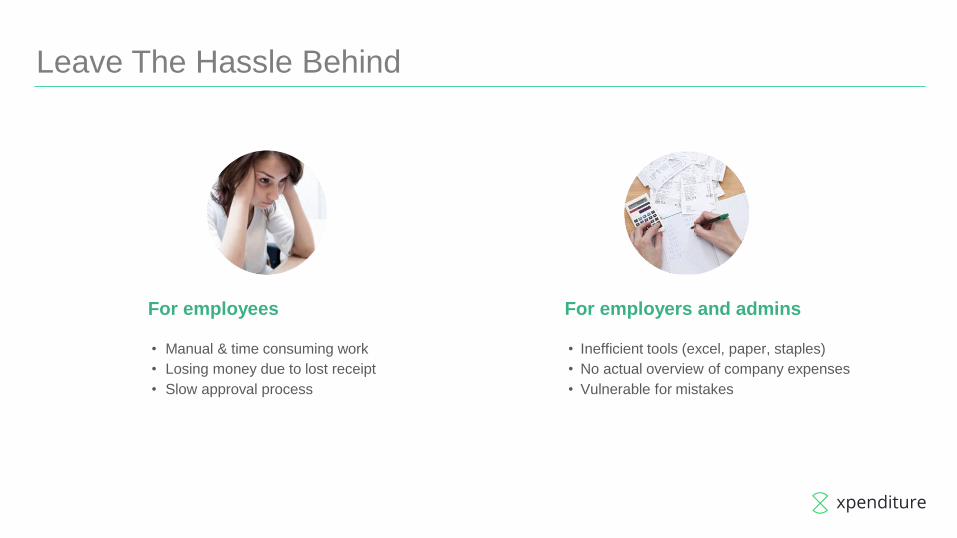

Leave The Hassle Behind

For employees

• Manual & time consuming work

• Losing money due to lost receipt

• Slow approval process

For employers and admins

• Inefficient tools (excel, paper, staples)

• No actual overview of company expenses

• Vulnerable for mistakes

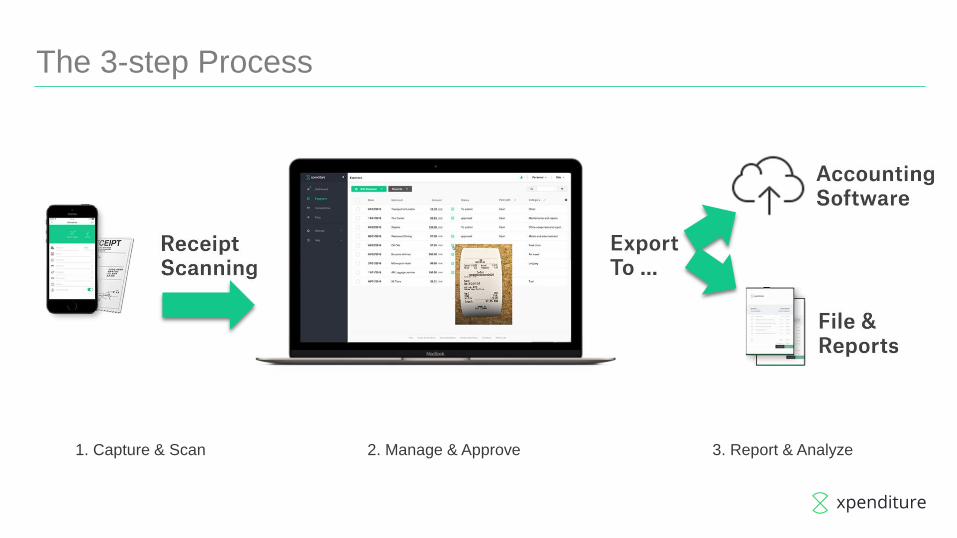

A Game Changing Process

The 3-step Process

1. Capture & Scan 2. Manage & Approve 3. Report & Analyze

Capture &

scan receipts

Extract date, merchant,

amount & currency

Reports

Statistics

Analysis

Input & matching

Integrate with ERP or accounting software

or default .csv / .xml How?

Via mobile phone

Via scanner or webcam

Via e-mail

credit card

transactions

And many others....

Manage Approve Control

A Three Step Process

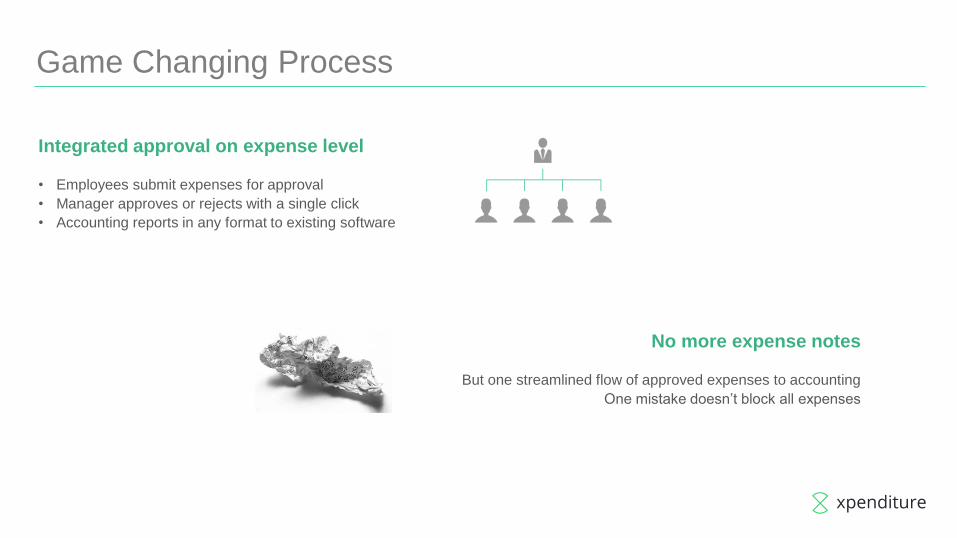

Game Changing Process

Integrated approval on expense level

• Employees submit expenses for approval

• Manager approves or rejects with a single click

• Accounting reports in any format to existing software

No more expense notes

But one streamlined flow of approved expenses to accounting

One mistake doesn’t block all expenses

Security and Data Storage

All expenses and receipts are stored safely and secured

on Xpenditure servers in EU (Combell)

All data stays accessible and searchable for at least 10 years

for analysis and control

Digital receipt in Xpenditure is accepted as exhibit by authorities

no more paper archive

Power warranty & graceful exit

data export in pdf or xml or long-term storage offering

Why Choose Xpenditure?

Receipt & Statement scanning

•Xpenditure automatically extracts date, merchant, amount and currency

•Automatic conversion of exchange rates

•Matching with Credit Card statements

Approval on expense level

•Xpenditure checks with company policy and potential duplicates

•One streamlined flow of approved expenses

•Only rejected expenses go back to employee for review

Easy setup and no local implementation

•Xpenditure is configured in hours instead of months

•Test period with power guarantee

No more paperwork or archive

•Digital flow from expense to accountancy

Global Customers Trust Us

About SaaS

“Software that is owned, delivered and managed remotely by one or more providers. The provider delivers software based on one set of common code and data definitions that is consumed in a one-to-many model by all contracted customers at any time on a pay-for-use basis or as a subscription based on use metrics.”

In fact, SaaS is a leased software maintained by its creator and not hosted on your premises.

SaaS apps run in the cloud and are changing the world of technology

SaaS

The ideal SaaS Startup ?

Product = Core of the business

Salesforce automates your sales processes

Xpenditure manages employee expenses

ZenDesk builds customer support system

Cost & Value proposition = Straightforward

Very clear pricing models

No surprises

Direct ROI

Finances its own growth

The company benefits from

- negative working capital

- shorter time-to-market

- Upfront payments

70% of the Xpenditure customers pay yearly

subscriptions upfront.

Sales Model = Internationally focused

Go international from day 1 (website

#languages)

Focus on max. 5 key countries

Recoup customer acquisition cost (CAC)

Do not do freemium – difficult to convert

The ideal SaaS Startup ?

Market leader potential

Becoming market leader / operating in a segment with

little viable competition.

Offer something which is unique and try to become

market leader in your segment.

7 insights on how

to become a

successful

SaaS startup

1. Build a service that your customers love

Users love your application because it solves an immediate problem (e.g. Xpenditure)

and they are referring new customers by showing of.

Services must be of high quality

– they are used to quality web services e.g. Google

SaaS businesses have to delight their customers &

meet their expectations day after day to keep them renewing their contracts.

2. Sell a best of breed service, not a product

A SaaS company should operate more like a service business than a product business.

Focus to become leader in best of breed solution and be open towards other systems.

Deliver service packs and not consultancy. Most SaaS companies are not designed for that.

Always think pragmatic in terms of services and features.

Innovate by growing and experimenting with your customers. E.g. Netflix,…

3. Customer service needs to be outstanding

Happy customers are your best sales force.

Customer satisfaction is critical in keeping churn low and increasing revenues.

React fast towards inquiries and incoming leads (minutes) and over deliver where possible.

Subscription businesses have to look for cross-sell and up-sell opportunities to get

customers “addicted” to their services.

SaaS Companies have to interact on continuous basis and make their customers happy

to create demand for their services.

4. Use the SaaS ‘API eco system’

SaaS companies have to find ways to generate leads without spending a lot on marketing

and advertisement.

Integrate with other major apps to create immediate added value for the customer,

partner and yourself.

Eg. At Xpenditure we see conversion ratios of higher then 20% via accounting packages

Start to integrate the API of high reach partners and create your own API for others later

(Xpenditure featured on Dropbox integrations).

5. Keep simplicity and usability in mind

Don’t step in the we can “customize everything trap”.

Once you have an innovative product customers expect you solve the most crazy things.

Focus on the real need: Only if you hear the same question more than 20 times,

start building it (and then… do it fast).

Be flexible and work in short development sprints.

Do user testing on usability via online services & your existing customers

Always keep UI simple.

6. Switching software is BIG for big companies

Fear of change is the biggest reason not selling your SaaS service as fast as you would expect.

Try to avoid the big RFP’s

– they think in a traditional way and existing market leaders will use that sentiment.

Convince bigger companies to buy a POC first (not for free but prove your solution)

and give warranties on your service. Money back guaranty if POC was not successful.

Bigger companies expect at least high touch sales (phone & email) and in Europe field sales.

7. Partnerships are great but need time

SaaS companies need partnerships but don’t expect wonders from it.

It creates trust & confidence

Be a real added value to the partner or it’s a waste of time.

Look for a balanced deal and this does not always mean extra revenues, but also lead creation.

Study the Sales Learning Curve Invest in success

Smart online Marketing is a must Your customers know how the web works

Use more aggressive online marketing tactics

Check the 6 C’s of Cloud Finance These metrics indicate the health of the business, churn rate and revenues.

The 6C’s are:

What you should remember

Customer Life Time Value (CLTV),

Customer Acquisition Cost (CAC),

Churn,

CMRR Pipeline (Cpipe),

Cash Flow,

Committed Monthly Recurring Revenue (CMRR)

Saas has unseen potential to grow your startup.

But keep in mind that every successful SaaS company faced

following phases to be innovative and market leader in his segment:

Experiment (also with potential and existing customers on new upcoming features)

Learn from failure (by opening test features for specific groups)

Patience & Persistence (it takes time & don’t give up)

Conclusion

BREAK-OUT Kies uw corner

Pieter Capiau

Frank Maene

Veerle Cool Anneleen Wydooghe

LEGAL CORNER FINANCE CORNER HR CORNER

BREAK-OUT Kies uw corner

Frank Maene

FINANCE CORNER

INVESTOR READINESS RELEVANT ASPECTS FOR A TECHNOLOGY VENTURE

• How to raise funding?

– How to prepare your company for fundraising?

– The search for unicorns – (sky)high valuation vs investor protection – How to structure relationships between stakeholders?

• Trends in technology M&A

• Importance of (legal) organization during the growth cycle • Annex – Cresco representative transactions

PROGRAM

• Research has shown that the way VC providers ensure funding for the expansion of companies is increasingly done on the basis of emerging global standards and best practices

• Actual relationship between VC firms and entrepreneurs will depend on, i.a.:

– Experience and reputation of the management/entrepreneur and state of the market – The attractiveness of the portfolio company as an investment opportunity (e.g. global expansion in promising

economies) – The stage of the company’s development (idea, start-up, emerging to more established)

• Exit horizon is typically set between 7 to 10 years (equal to the expected duration of the fund)

• There is a big difference in the nature of investment depending on its stage (seed, growth, expansion, etc..)

RAISING CAPITAL

• VC investment process 1. Agree preliminary valuation with VC

• Valuation with VC will be based on company’s past results (if available), its current level of performance and the present value of expected future profits if it obtains new capital for growth

• At this stage an elaborate “pre” due diligence exercise will already take place to assist in the determination of the value

2. Agree on amount of funding • Parties to agree on amount of funding and required return on investment • Minimizing investment risk can be accomplished by the use of staged financing whereby the funds are

invested in tranches with different expected returns per tranche, depending on performance • Win-win situation for entrepreneur and the venture capital fund

3. Execution of letter of intent or term sheet with basic business terms 4. Performance of extensive due diligence 5. Execution of definitive agreements and closing

RAISING CAPITAL

• Valuation and milestones – Pre-money valuation: used to determine the price per share to be paid by

investors in the investment round • PPS is obtained by dividing such valuation by all shares and any options outstanding prior to the round

– Post-money valuation: refers to the valuation of the company immediately following closing (and including the proceeds)

– Often a VC will invest in tranches, subject to various technical and/or commercial milestones being met

– Such milestones need to be carefully thought through to avoid later conflicts of interests between founders, company and investors.

RAISING CAPITAL

• USD 1 billion+ valuations - the search for the next unicorn – Little awareness amongst entrepeneurs that these sky high valuations go hand in hand

with very onerous equity instruments – Many instruments are akin to subordinated debt but offering significant downside and

upside protection to investor – Entrepreneur required to realize exits at valuations up to 4x the valuation applied to VC

to neutralize effect of liquidation preference

• Bootstrapping, valuation, staged financing and milestones – Bootstrapping and staged financing minimizes venture capital dilution – Often an investor will propose to invest in tranches subject to milestones being met –

potential for conflicts of interests between founders, company and investors.

VALUATION VS PROTECTION

VALUATION VS PROTECTION

• Liquidation preference and deemed liquidation

– Right of investor to receive certain amount of proceeds upon liquidation or exit before any other shareholder

– Preference amount may be equal to the amount invested or a multiple of it, such as: • non-participating preferred: if exit below post-money valuation, investors receive their funds back with remaining proceeds

distributed to the other shareholders; • capped non-participating preferred: investors first receive a multiple on their investment but do not share pro rata (unless

they convert) • participating preferred: investors receive their funds back and then share pro rata in remaining proceeds with the other

shareholders

– Size and structure of preference reflects the risk inherent in a round (the higher the risk, the higher the required return) and diverging views between founders and investors

– Right also applies upon merger, acquisition, change of control, consolidation, asset sale or IPO

VALUATION VS PROTECTION

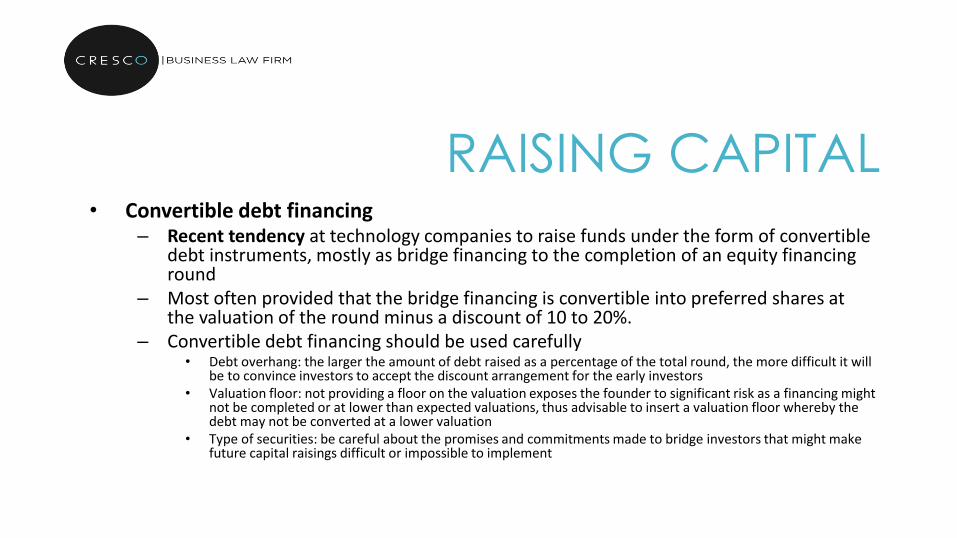

• Convertible debt financing – Recent tendency at technology companies to raise funds under the form of convertible

debt instruments, mostly as bridge financing to the completion of an equity financing round

– Most often provided that the bridge financing is convertible into preferred shares at the valuation of the round minus a discount of 10 to 20%.

– Convertible debt financing should be used carefully • Debt overhang: the larger the amount of debt raised as a percentage of the total round, the more difficult it will

be to convince investors to accept the discount arrangement for the early investors • Valuation floor: not providing a floor on the valuation exposes the founder to significant risk as a financing might

not be completed or at lower than expected valuations, thus advisable to insert a valuation floor whereby the debt may not be converted at a lower valuation

• Type of securities: be careful about the promises and commitments made to bridge investors that might make future capital raisings difficult or impossible to implement

RAISING CAPITAL

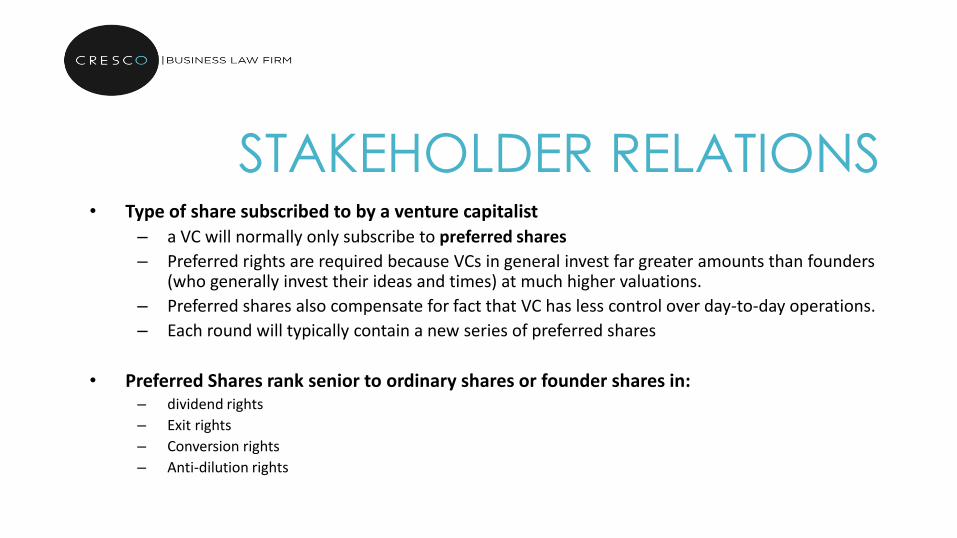

• Type of share subscribed to by a venture capitalist – a VC will normally only subscribe to preferred shares

– Preferred rights are required because VCs in general invest far greater amounts than founders (who generally invest their ideas and times) at much higher valuations.

– Preferred shares also compensate for fact that VC has less control over day-to-day operations.

– Each round will typically contain a new series of preferred shares

• Preferred Shares rank senior to ordinary shares or founder shares in: – dividend rights

– Exit rights

– Conversion rights

– Anti-dilution rights

STAKEHOLDER RELATIONS

• Conversion rights

– VCs are typically entitled to convert the preferred shares into ordinary shares at any time, on a 1:1 basis

– Conversion ratio is adjusted to take account of any reorganisation of the capital structure as a form of anti-dilution protection

– Automatic conversion into ordinary shares often required in the event of IPO at a certain valuation and minimum net proceeds

STAKEHOLDER RELATIONS

• Anti-dilution rights (or price protection)

– VCs almost always require anti-dilution protection against new investments at a valuation lower than their pre-money valuation (down round)

– VCs will receive new shares for no or minimal cost to compensate the dilutive effect of the issuance of cheaper shares

• Full ratchet: ensures that the % ownership of VC is kept at same level or same value in down rounds

• Weighted average ratchet: level of protection depends on several factors, including the number of shares outstanding at the time of the down round, the size of the dilutive offering and the dilutive price

STAKEHOLDER RELATIONS

• Preferred dividend rights

– Investors negotiate a preferential, cumulative dividend, usually fixed at a percentage of the purchase price paid for each share

– No dividends may be paid to any other shareholders until the preferred dividend is paid

– Capitalised dividends usually form part of the liquidation preference (with potentially severe consequences, depending on the timing of an exit)

– Upon conversion of preferred shares into ordinary shares, dividends are also converted into common shares

STAKEHOLDER RELATIONS

• Founder shares – Founders and senior management are key to the investment decision and must remain

in place to execute their business plan – Often provided that if they leave the company within a certain period of time, they are

required to offer to sell their shares back – Price paid depends upon reasons for departure:

• Good leaver: may be at fair market value • Bad leaver: may be a nominal price or nothing

– Shares may also be made subject to a vesting schedule to ensure retention • Vesting means that person must remain engaged by the company for a certain period of time (except if through

no fault of the relevant person) • Vesting can also be tied to performance targets • Vesting can be accelerated upon change of control

STAKEHOLDER RELATIONS

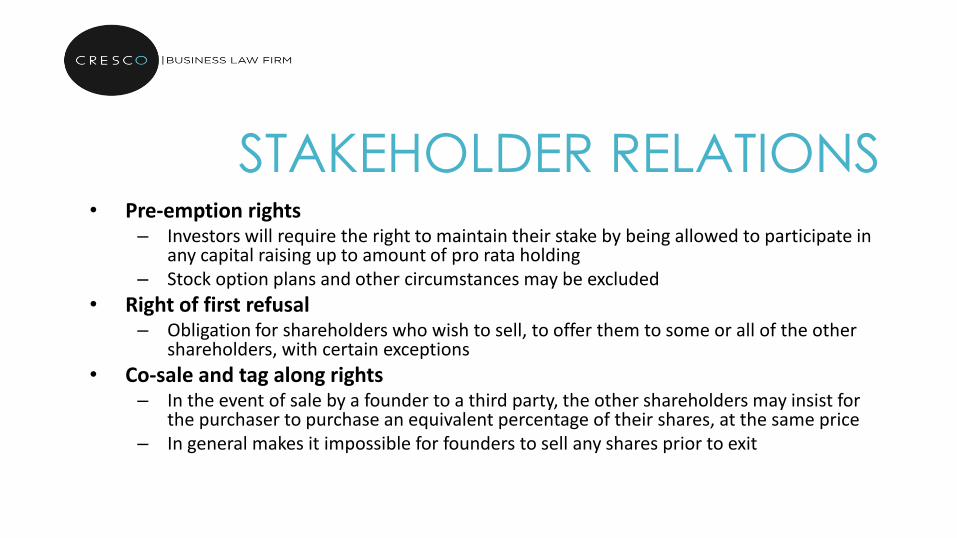

• Pre-emption rights – Investors will require the right to maintain their stake by being allowed to participate in

any capital raising up to amount of pro rata holding – Stock option plans and other circumstances may be excluded

• Right of first refusal – Obligation for shareholders who wish to sell, to offer them to some or all of the other

shareholders, with certain exceptions

• Co-sale and tag along rights – In the event of sale by a founder to a third party, the other shareholders may insist for

the purchaser to purchase an equivalent percentage of their shares, at the same price – In general makes it impossible for founders to sell any shares prior to exit

STAKEHOLDER RELATIONS

• Drag along rights

– A drag along creates an obligation on all shareholders to sell their shares if a certain percentage votes to sell to that purchaser

– Often provided that regardless of required majority, VC has a veto right on a sale and that liquidation preference applies

• Exit rights

– In view of 5 to 7 year investment horizon, VCs often negotiate forced exit rights

– VC entitled to find buyer for 100% of the capital and force the other shareholders to sell

STAKEHOLDER RELATIONS

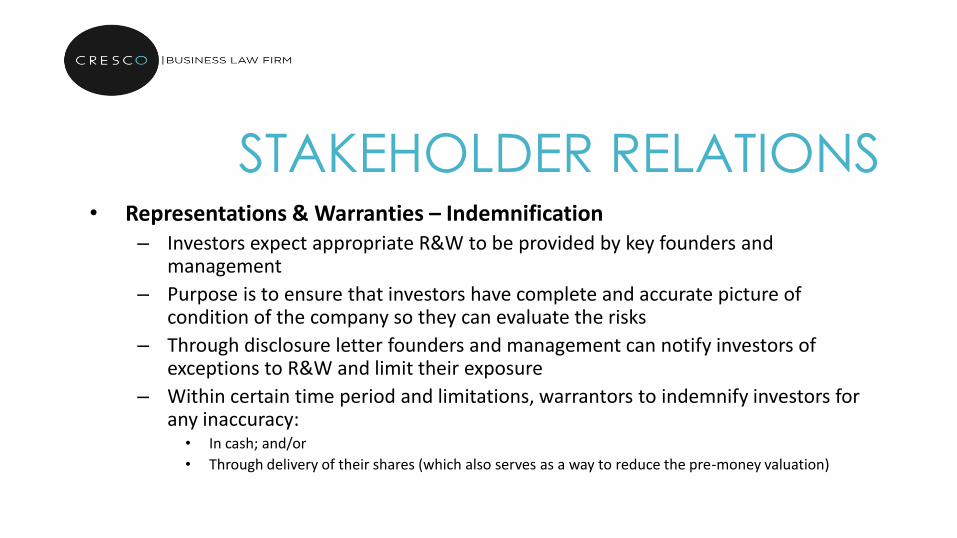

• Representations & Warranties – Indemnification – Investors expect appropriate R&W to be provided by key founders and

management

– Purpose is to ensure that investors have complete and accurate picture of condition of the company so they can evaluate the risks

– Through disclosure letter founders and management can notify investors of exceptions to R&W and limit their exposure

– Within certain time period and limitations, warrantors to indemnify investors for any inaccuracy:

• In cash; and/or

• Through delivery of their shares (which also serves as a way to reduce the pre-money valuation)

STAKEHOLDER RELATIONS

• Protective provisions and consent rights – Investors expect rights to nominate board members which will have veto rights for

certain significant board decisions

– Investors expect certain rights to block shareholder resolutions on significant shareholder matters

• Information rights – Investors are required (by their investors) to monitor the condition of their investment,

which is why they negotiate rights to receive: • annual budgets;

• Unaudited monthly statements

• Unaudited quarterly statements

• Any other important information concerning the company

STAKEHOLDER RELATIONS

• Relationships between Board of Directors and management – The Board of Directors sets the general policy and supervises the management – The ounders/management runs the company on a daily basis and reports to the board of

directors – Decision making by management is subject to veto and information rights imposed by

external investors

• Negative control rights – It is important to note that VC’s generally do not wish to run a start-up and actively manage it – VC’s will normally only exercise their veto rights when in total disagreement with

management – Veto right is “passive” to the extent that it confers the right to say “no” rather than actively

manage the company

STAKEHOLDER RELATIONS

• IP Assignment and non-compete agreements

– Investors will demand all founders, executive and employees to assign their IP rights to the company

– This is also valid for employees of an academic institution working for a spin-off of such institution

– Founders and senior management will also be required to execute non-compete agreements

• Investment is based largely on value of technology and management experience

• Leaving to a competitor to do the same, could significantly affect the value of the company

STAKEHOLDER RELATIONS

• Employee share option plan

– A percentage of shares of the company must be reserved for share option grants to employees and management of the company

– To provide an incentive for such persons to share in the financial rewards resultign from the success of the company

– 10-20% is customary for technoloy companies and should be held steady, taking into account each capital raising

– Typically stock option plan is not for founders and other management with significant shareholdings

STAKEHOLDER RELATIONS

• Very strong focus on IPR in Technology Venture Capital M&A

– Unique and exclusive nature of IPR (patents, copyrights, trade secrets) attracts a significant valuation premium

– Extreme focus on legal, technical and commercial aspects of IP portfolio

• Issues with IPR ownership lead to significant issues in Venture Capital and M&A transactions:

– Making you hostage to investor’s buyer’s requirement to obtain IP assignments from third parties or to have them agree to modifications to existing agreements

– Leading to substantial valuation reduction

– Leading to buyer to walk away if problems cannot be solved

TRENDS IN TECHNOLOGY VENTURE CAPITAL AND M&A

• Technology Venture Capitalists and purchasers demand the following:

– Very detailed historical overview on source code development and ownership

– Open source contamination issues are very high on the agenda – specialized code scanning firms are engaged by buyers

– Foreign corrupt practices and export compliance issues surrounding encryption technology

– Higher indemnification caps and claim periods for IPR warranties

– “Clean” third party infringement warranties are demanded, amounting to an IPR insurance

TRENDS IN TECHNOLOGY VENTURE CAPITAL AND M&A

• Development of IP portfolio – Obtain and secure IP rights:

• Define core technology (product roadmap) vs. customer specific technology • Patents vs. trade secrets

– Maintain IP rights • Pay registration fees, renewal fees • Set out guidelines with respect to the development, use and confidentiality of your IP portfolio • Keep in touch with the market and monitor relevant sector:

– Is a certain technology already available on the market? – Is there a need for such technology on the market? – Are there market shifts or changes to be anticipated?

• Competitor analysis – What are your competitors doing?

– Defend IP rights: • Cease and desist letters • Litigation or settlement

IP IMPORTANCE

• Secure IP chain of title

– In the relation with employees – In the relation with external developers used by the emerging company to develop, create

the product, prototype, website, …

• IP awareness training

– Ensure a minimum level of IP awareness training for all staff to avoid employees compromising valuable IP

• Set out publication standards with regard to new inventions or innovations • Obeying contracting guidelines • Implement standards of use

IP IMPORTANCE

Protect valuable corporate assets that enable business to pursue significant revenue streams

– Develop a clear IP monetization strategy

– Develop contracting guidelines to support the monetization strategy

– Always avoid transferring IP ownership to third parties as it leads to: • lost opportunity to resell or sublicense IP to other customers

• additional costs in future business since business cannot copy or reuse the transferred IP rights

– Do not be afraid to form alliances and licensing deals to supplement the resources and to be able to exploit markets at an early stage in the growth cycle.

IP MONETIZATION

General contracting guidelines: some do’s and don’ts

– Limitation of liability: exclusion of any liability for indirect and consequential damages

as well as putting liability caps on sales of products and services

III. Most favoured customer clauses: to be avoided: restrict a business’ discretion to price its products and services and are likely to result in adverse impact on revenue forecasts set forth in financial model

IV. Non-compete: you should never agree to any contractual restrictions on your ability to freely conduct business

IP MONETIZATION

OFFICES

Lange Kievitstraat 118-120

2018 Antwerp

Belgium

CONTACT

+ 32 479 24 49 24

+32 497 86 94 77

BREAK-OUT Kies uw corner

Veerle Cool Anneleen Wydooghe

HR CORNER

Retentie

van X, Y tot … Z

Veerle Cool

Anneleen Wydooghe

22/04/2016 65

• 4 generaties op de werkvloer:

– Babyboom generatie (1940 – 1955) • (bijna) pensioen

– X generatie (1955 – 1980) • nadruk op kwaliteit, duurzaamheid, evenwicht werk / privé

– Y generatie (1980 – 1994) • nadruk op authenticiteit, creativiteit, flexibel werken, …

– Z generatie (1994 - …) • ??? • zapgeneratie

1. X, Y, Z ….

22/04/2016 66

• Hoe jonger, hoe … (studie van Acerta)

– meer zin in nieuwe projecten en uitdagingen – meer gericht op persoonlijke ontwikkeling – centraler het werk staat, maar … van 9 to 5 – groepsgerichter – meer ze veranderen van werkgever – groter de vraag naar duidelijke doelstellingen

22/04/2016 67

• Betekenis

– Retentie = het aan boord houden van goede,

waardevolle medewerkers die bijdragen tot het succes van de onderneming

– Causaal verband tussen ‘engagement’ en ‘verloopintentie’

2. Retentie

22/04/2016 68

• Creëren van engagement

– Kwaliteit van het werk / jobinhoud – Work / life balance – Inspiratie en waarden – Ontwikkelingsperspectieven – Faciliterende omgeving – Beloning

22/04/2016 69

• Opzetten van retentiebeleid:

– inzetten op alle dimensies!

– hét retentiebeleid bestaat niet!

• durf medewerkerstevredenheid bevragen, in kaart brengen en speel hierop in!

22/04/2016 70

• Loon als één van de 6 dimensies Nood aan dynamisch loonbeleid aangepast op noden medewerkers

– Cafetariaplannen – Green mobility pack – Variabele verloningssystemen – Stimuleren creativiteit en innovatie

22/04/2016 71

15 MINUTEN FISCALTEIT Over een aantal bijzondere bomen…

Dries Torreele

15 MINUTEN FISCALTEIT

15 MINUTEN FISCALTEIT

15 MINUTEN FISCALTEIT

15 MINUTEN FISCALTEIT

0 - 15.360: 50%

15.360 - 30.710: 25%

> 30.710 EUR: 0%

15 MINUTEN FISCALTEIT

15 MINUTEN FISCALTEIT

15 MINUTEN FISCALTEIT

15 MINUTEN FISCALTEIT

internationaltax.vandelanotte.be

Eric kenis

WRAP-UP Met een hoek af…

Eric Kenis

TIME TO CONNECT Meet our ambassadors

THANKS. OOK AAN ONZE SPONSORS

More than accountants

Find out why

DOWNLOAD

SLIDES

HIER