Embed Size (px)

Citation preview

Review of Measures to Reduce Costs in the Private Health Insurance Market 2014

Independent Report to the Minister for Health and Health Insurance Council

October 2014

1 | P a g e

TABLE OF CONTENTS

Acknowledgements……………………………………………………… page 4

Chapter 1 Introduction…………………………………………………. page 5

Chapter 2 Analysis of Claims Cost Data - Health Insurance Authority page 9

2. 1 Introduction …………………………………………………….. page 9

2.2 Recent Irish Claims Cost Experience……………………………… page 9

2.3 Impact of Ageing………………………………………………….. page 13

2.4 Analysis of Claims Data Submitted by Insurers…………………….. page 19

Chapter 3 Summary of Submissions Received………………………… page 26

Introduction………………………………………………………………. page 26

3.1 Summary of HSE Submission…………………………………….. page 26

3.2 Summary of IHAI Submission (non-psychiatric elements)……….. page 28

3.3 Summary of Insurance Ireland Submission………………………. page 30

3.4 Summary of IHCA Submission ………..………………………… page 35

3.5 Summary of Society of Actuaries in Ireland Submission………… page 37

3.6 Summary of Submissions from Saint John of God Hospital,

St. Patrick’s Mental Health Services and IHAI on Industry

Approach to Private Psychiatry…………………………………….. page 38

Chapter 4 Chairman’s Observations and Recommendations ………… page 41

Introduction………………………………………………………………… page 41

4.1 Key Recommendations Phase 1 Interim Report…………………… page 41

4.2 Data to Analyse Trends in Industry………………………………. page 42

4.3 Private Health Insurance Claims Cost Analysis……………………. page 44

4.4 Care Setting and Resources………………………………………… page 46

4.5 Age Structure……………………………………………………… page 47

4.6 Clinical Audit and Utilisation Management………………………. page 48

2 | P a g e

4.7 Industry Approach to Private Psychiatry…………………………… page 49

4.8 Fraud, Waste & Abuse……………………………………………… page 50

4.9 Chronic Disease Management……………………………………… page 50

4.10 Claims Processing………………………………………………….. page 50

4.11 Admission & Discharge Processes…………………………………. page 51

4.12 Private A&E……………………………………………………….. page 52

Chapter 5 Conclusion.……………………………………………………… page 53

Appendix 1 Status Report on Recommendations made in Phase 1 Report page 55

Appendix 2 HIA Claims Cost Data………………………………………… page 62

3 | P a g e

ACKNOWLEDGEMENTS

I would like to acknowledge the support and co-operation I received from all participants in this review – the health insurers, the Health Insurance Authority, and the Department of Health.

Chair, Review GroupOctober 2014

4 | P a g e

Chapter 1 Introduction

1.1 Introduction

On 27 June 2013, I was appointed by the Minister for Health to Chair a Review Group under the auspices of the Consultative Forum on Health Insurance, to work with the insurance companies and the Department of Health to effect real cost reductions in the private health insurance market. The work of the Group has been conducted in two phases, with the first phase report published on 26 December 2013.

The Phase 1 report sets out the context, establishment, membership and terms of reference for both phases of the Groups’ work. The report also outlines the legislative provisions for private health insurance in Ireland, the objectives of both phases of the review and the approach and methodology followed. (Membership and Terms of Reference for the Group are reproduced at 1.2 below for reference).

On completion of Phase 1 of the review, I reported to the Minister for Health and the Health Insurance Council, and following Ministerial approval, the Group moved to Phase 2 of its review.

Work on Phase 2 has now been completed and I have reported to the Minister and the Health Insurance Council, with the results of this work now presented in this report. In particular, Phase 2 of the process focused on the compilation and analysis by the Health Insurance Authority (HIA) of claims data to assess the cost drivers for health insurance, the effects of medical technology and innovations on costs, and claims processing issues. As with Phase 1, a number of plenary meetings were held, and I also engaged in a series of bi-lateral meetings with health insurers and relevant stakeholders. I also received a number of submissions from relevant stakeholders which were examined and considered under the Phase 2 Review. A summary of these submissions is contained in Chapter 3 of this report. (Full text of the submissions is available to view on the Department of Health’s web-site at .http://www.health.gov.ie.

1.2 Membership and Terms of Reference

Membership of the Review Group is comprised of representatives of the four commercial health insurers – Aviva Health Insurance, GloHealth, Laya Healthcare and VHI Healthcare, the Department of Health and the Health Insurance Authority. The Secretariat is provided by the Department of Health.

The following Terms of Reference were agreed by the Group for Phase 1 and Phase 2 of the review process:

5 | P a g e

The Minister for Health and the four commercial private health insurers have agreed to a process to effect real cost reduction/cost management in the Irish private health insurance market to ensure its long term sustainability.

The Review Group will be chaired by Mr. Pat McLoughlin. The Review Group will also comprise representatives from the Department of Health and the HIA and will be mindful of the need to respect competition law in its deliberations. All parties will be represented by two persons. As appropriate, the Chairman may meet other stakeholders for their input in order to complete the review.

The purpose/objective of the Review Group is to consider/identify effective industry-wide cost reduction/cost management strategies for the private health insurance market (scope to include but not limited to public hospitals, private hospitals and consultants). It is envisaged that this will be a two stage process as follows:

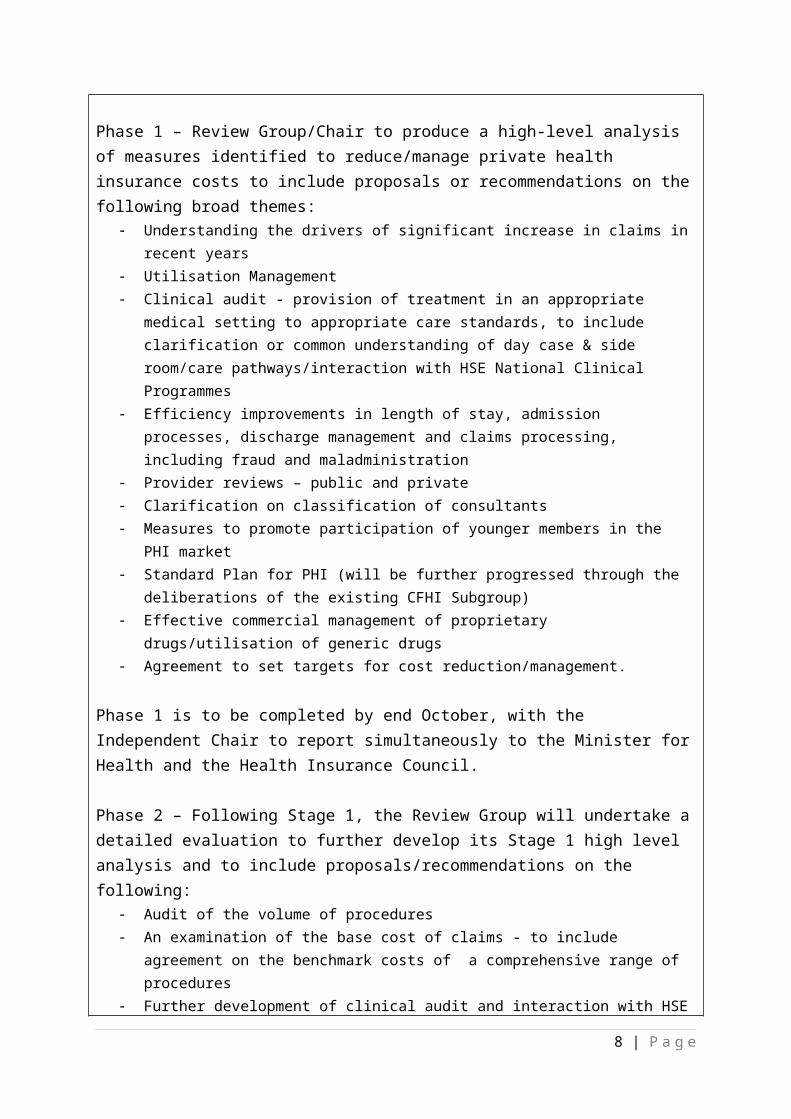

Phase 1 – Review Group/Chair to produce a high-level analysis of measures identified to reduce/manage private health insurance costs to include proposals or recommendations on the following broad themes:

Understanding the drivers of significant increase in claims in recent years Utilisation Management Clinical audit - provision of treatment in an appropriate medical setting to appropriate care

standards, to include clarification or common understanding of day case & side room/care pathways/interaction with HSE National Clinical Programmes

Efficiency improvements in length of stay, admission processes, discharge management and claims processing, including fraud and maladministration

Provider reviews – public and private Clarification on classification of consultants Measures to promote participation of younger members in the PHI market Standard Plan for PHI (will be further progressed through the deliberations of the existing

CFHI Subgroup) Effective commercial management of proprietary drugs/utilisation of generic drugs Agreement to set targets for cost reduction/management.

Phase 1 is to be completed by end October, with the Independent Chair to report simultaneously to the Minister for Health and the Health Insurance Council.

Phase 2 – Following Stage 1, the Review Group will undertake a detailed evaluation to further develop its Stage 1 high level analysis and to include proposals/recommendations on the following:

Audit of the volume of procedures An examination of the base cost of claims - to include agreement on the benchmark costs of

a comprehensive range of procedures Further development of clinical audit and interaction with HSE Clinical Programmes Measures to introduce procedure-based payments in public hospitals and clarity on what is

6 | P a g e

chargeable, including negotiation of rates and rewards for efficiency and outcomes Measures to curb year-on year increases in claims through wider/more targeted use of claims

management tools Consideration of possible ways to lessen the impact of medical technology /innovation on

PHI costs, i.e. through cost effectiveness analysis. This will include the development of initiatives to manage procurement

Legislative measures that might be required to address cost reductions Agreement on measures to promote participation of younger members in the market, e.g.

discounts on premiums for 23-29yr olds ; introduction of LCR (will be further progressed through the deliberations of the existing CFHI Subgroup)

Industry approach to private A&Es Industry approach to private psychiatry Ways to clarify certain processes and structures which influence charges to private health

insurers, e.g. consultant classifications, consultant charges for private patients, determination of public/private patient status at admission, completeness of claims information from public hospitals

Further efficiency improvements in relation to length of stay, admission & discharge procedures and claims processing

Increased utilisation of appropriate Primary Care settings.

Phase 2 is to be completed within six months, with the Chair to report simultaneously to the Minister for Health and the Health Insurance Council.

Secretariat to the Review Group will be provided by the Department of Health.

1.3 Updated Figures

Since publication of the Phase 1 report the HIA has collated data for 2013, based on Information Returns submitted by health insurers for July to December 2013; this data is referenced in the Phase 2 report. The HIA has also collated data for the first quarter of 2014.

At the end of June 2014 there were 2,017,087 people insured with inpatient health insurance plans, or 43.9% of the population. This compares with 2,058,239 at the end of June 2013 and represents a reduction in the number of insured people of almost 41,000 over the previous 12 months. The market peaked in 2008 with 2,297,000 people insured at that time.

In 2013, Irish open membership private health insurers paid claims of €1,783m which represents a 4% decrease compared to 2012 levels of €1,856m. Between 2004 and 2008, there was an increase of 6.7% in the average claim per insured person. Between 2008 and 2012, there was an increase of 12.6% per insured person. The average cost of claims paid (prescribed benefit) per insured person fell by 2% between 2012 and 2013. The HIA notes

7 | P a g e

that while a reduction in the average claims costs per person is positive, it is based on data for claims paid and so is impacted by speed of claims payments. Further data will be required in order to determine whether reduced claims paid in 2013 is part of a change in trend.

8 | P a g e

Chapter 2 Analysis of Claims Cost Data - Health Insurance Authority

2.1 Introduction

Early in my work, we agreed that it would be important to assess the drivers behind the growth in private health insurance costs. As part of this analysis, the Health Insurance Authority submitted a paper on health insurance claims costs to the Department of Health and the Consultative Forum on Health Insurance, in July 2013.

That paper discussed the Irish experience in relation to health insurance claims costs and examined general methods used to control private health insurance claims costs, in principle and in practice, drawing on examples from other jurisdictions.

Subsequently it was agreed under the Consultative Forum that insurers would submit further data on claims costs broken down by procedure to the Health Insurance Authority and that the Authority would analyse that data.

This Chapter updates the analyses included in the July 2013 paper and adds an analysis of the data referred to above.

This data supports the indications in earlier analyses that claims costs increases between 2007 and 2012 arose mainly in relation to increased activity in private hospitals and that this increased activity is not driven primarily by demographic factors.

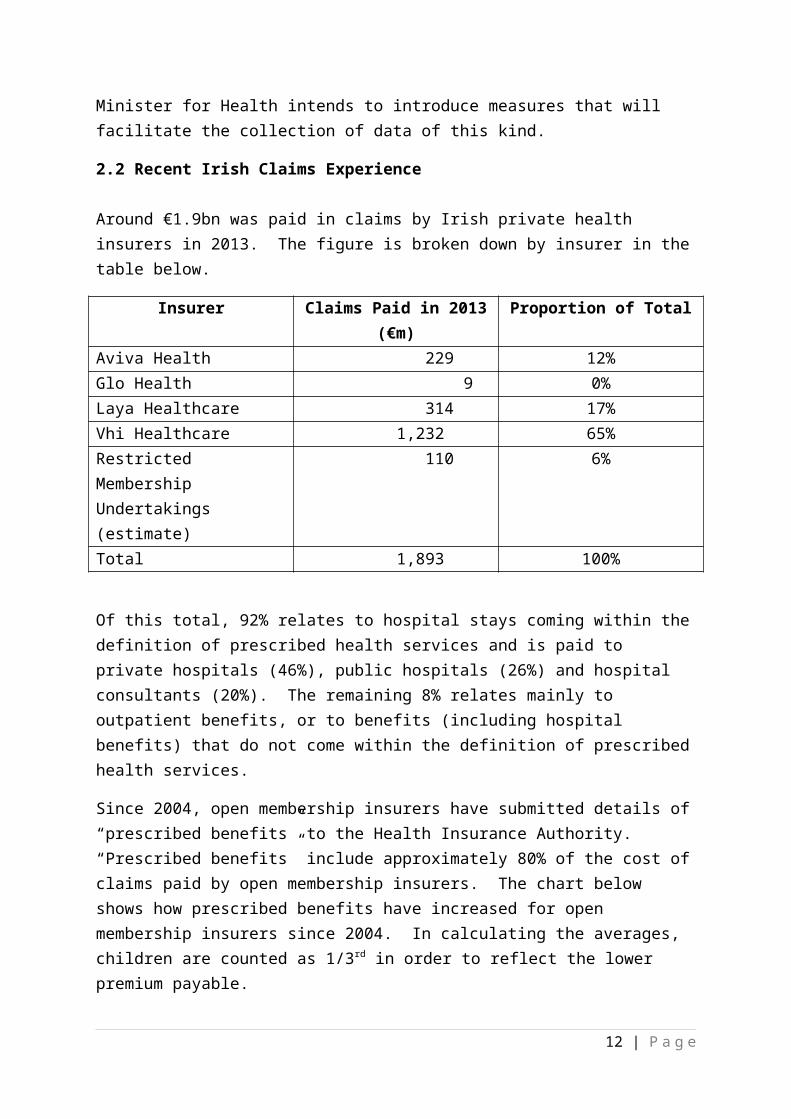

It is not possible to fully determine the impact that changed casemix has on claims costs from the data available because the data does not provide information on diagnosis. In order to conduct such an analysis, it would be necessary for insurers to collect and submit data on diagnosis in a consistent way. This is not currently happening but the Minister for Health intends to introduce measures that will facilitate the collection of data of this kind.

2.2 Recent Irish Claims Experience

Around €1.9bn was paid in claims by Irish private health insurers in 2013. The figure is broken down by insurer in the table below.

Insurer Claims Paid in 2013 (€m) Proportion of TotalAviva Health 229 12%Glo Health 9 0%Laya Healthcare 314 17%Vhi Healthcare 1,232 65%Restricted Membership Undertakings (estimate)

110 6%

Total 1,893 100%

9 | P a g e

Of this total, 92% relates to hospital stays coming within the definition of prescribed health services and is paid to private hospitals (46%), public hospitals (26%) and hospital consultants (20%). The remaining 8% relates mainly to outpatient benefits, or to benefits (including hospital benefits) that do not come within the definition of prescribed health services.

Since 2004, open membership insurers have submitted details of “prescribed benefits” to the Health Insurance Authority. “Prescribed benefits” include approximately 80% of the cost of claims paid by open membership insurers. The chart below shows how prescribed benefits have increased for open membership insurers since 2004. In calculating the averages, children are counted as 1/3rd in order to reflect the lower premium payable.

In the four years between 2004 and 2008, the average claim per insured person (measured by market prescribed benefit) increased by 6.7% p.a. on average. During this period, the consumer price index grew by an average of 3.9% p.a.

In the four years between 2008 and 2012, the average prescribed benefit per insured person grew by 12.6% p.a. During this period, the consumer price index fell by an average of 0.3% p.a.

In 2013, the average prescribed benefit per insured person fell by 2.2%, the first time this figure decreased since the Authority started receiving this data.

Increased Utilisation

10 | P a g e

The trend in recent years in the average number of treatment days per insured person is shown in the following chart. Again, children are counted as 1/3rd in order to reflect the lower premium payable.

Between 2004 and 2008 the average number of treatment days per insured person fell by 12%. Between 2008 and 2012 the average number of treatment days per insured person increased by 45%. It can be seen, therefore, that the increase in average claim per member between 2008 and 2012 (61%) largely results from increased usage of hospital services, with the utilisation measure increasing by (45%). The remainder of the increase results from increased cost per utilisation (11%).

In 2013, the average number of hospital treatment days per insured person fell by 3%, indicating that the reduction in average claims cost per insured person in 2013 was driven by reduced utilisation.

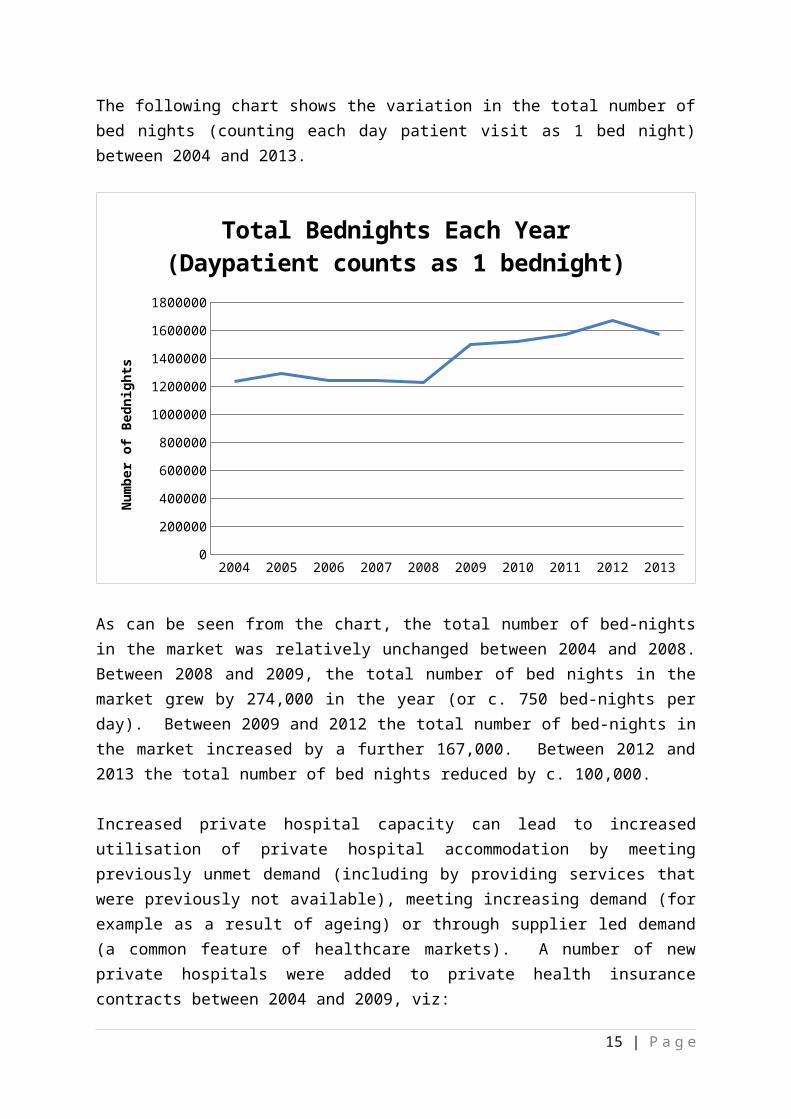

The following chart shows the variation in the total number of bed nights (counting each day patient visit as 1 bed night) between 2004 and 2013.

11 | P a g e

2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

Total Bednights Each Year(Daypatient counts as 1 bednight)

Num

ber o

f Bed

nigh

ts

As can be seen from the chart, the total number of bed-nights in the market was relatively unchanged between 2004 and 2008. Between 2008 and 2009, the total number of bed nights in the market grew by 274,000 in the year (or c. 750 bed-nights per day). Between 2009 and 2012 the total number of bed-nights in the market increased by a further 167,000. Between 2012 and 2013 the total number of bed nights reduced by c. 100,000.

Increased private hospital capacity can lead to increased utilisation of private hospital accommodation by meeting previously unmet demand (including by providing services that were previously not available), meeting increasing demand (for example as a result of ageing) or through supplier led demand (a common feature of healthcare markets). A number of new private hospitals were added to private health insurance contracts between 2004 and 2009, viz:

The Galway Clinic, covered by private health insurance since 2004, 146 beds The Hermitage Medical Clinic, covered since 2007, 101 beds The Whitfield Clinic, covered since 2007, 64 beds (inpatient and day patient) The Beacon Clinic, covered since 2008, “capacity for 214 beds” The Santry Sports Clinic, covered since 2008, 62 beds (inpatient and day patient)

(Sources: Insurance policy documents, www.galwayclinic.com, www.hermitageclinic.ie, www.waterfordchamber.com, www.beaconhospital.ie, www.sportssurgeryclinic.com )

From 2010, the total number of private hospital beds continued to increase, viz;

12 | P a g e

The Blackrock Clinic main extension opened in October 2010 increasing by 50 inpatient bed capacity to 170 and providing for an expanded 30 bed day surgery unit, as well as a new A&E department.

St Vincent’s Private Hospital moved to a new building, which opened in November 2010 with 236 inpatient beds (previously 164) and additionally, an expanded day case/day surgery facility with 54 beds (previously 36).

Mater Private Cork opened in January 2013 with 75 beds with business from the old Shanakiel Hospital (44 beds) transferring to it.(Sources: www.svph.ie, www.blackrock-clinic.ie, www.materprivate.ie, www.irishexaminer.com )

The substantial change in the role of the National Treatment Purchase Fund has almost eliminated demand for private hospital stays from publicly funded patients and made additional capacity available for use in private hospitals by insurance funded private patients.

It can be seen that there has been a very substantial increase in private hospital capacity. The Acute Hospital Bed Capacity Review: A Preferred Health System in Ireland to 2020, published by the HSE in 2007, stated that in May 2007, there were 1,654 private hospital in-patient beds and 272 day case bed/places. This was in addition to 2,227 designated inpatient and 229 day case private beds in public hospitals and not counting 200 beds in smaller private clinics. The report also stated that “It is conservatively estimated that there is a surplus of 130 private patient beds in Ireland. This increases to 900 with those currently in plan.”

2.3 Impact of Ageing

The health insurance market has been ageing since the Authority commenced receiving data on the age structure of the market in 2003. The rate of ageing increased substantially when the insured population began to decline.

The ageing of the private health insurance market is a result of the following:

Ageing of the general population. Increased private health insurance penetration amongst older people. Reduced private health insurance uptake amongst younger people.

Ageing of the General Population

The age structure of the Irish population in the last three censuses is set out in the following table, along with the age structure in the 2013 population estimate produced by the Central Statistics Office (CSO).

Age Structure of the Irish Population in the Last Three Censuses and in 2013 Estimate

13 | P a g e

Age Group 2002 2006 2011 2013 (Est)0-19 29.1% 27.2% 27.5% 27.9%20-29 16.4% 16.9% 14.3% 12.6%30-39 15.2% 15.8% 16.5% 16.4%40-49 13.3% 13.6% 13.9% 14.3%50-59 10.9% 11.1% 11.3% 11.6%60-69 7.3% 7.7% 8.6% 9.0%70-79 5.2% 5.0% 5.1% 5.3%80+ 2.6% 2.7% 2.8% 2.9%

It can be seen that the general population aged somewhat between 2002 and 2013, with the proportion of the population aged over 60 increasing from 15.1% to 17.2%. Most of this ageing took place between 2006 and 2013, during which the proportion of the population aged over 60 increased from 15.3% to 17.2%. In particular, the fastest increase in the proportion of the population aged over 60 took place between 2011 and 2013 when the proportion increased from 16.4% to 17.2%. The CSO is projecting that the rate of ageing of the population will continue, with the proportion over the age of 60 exceeding 20% of the population by 2021.

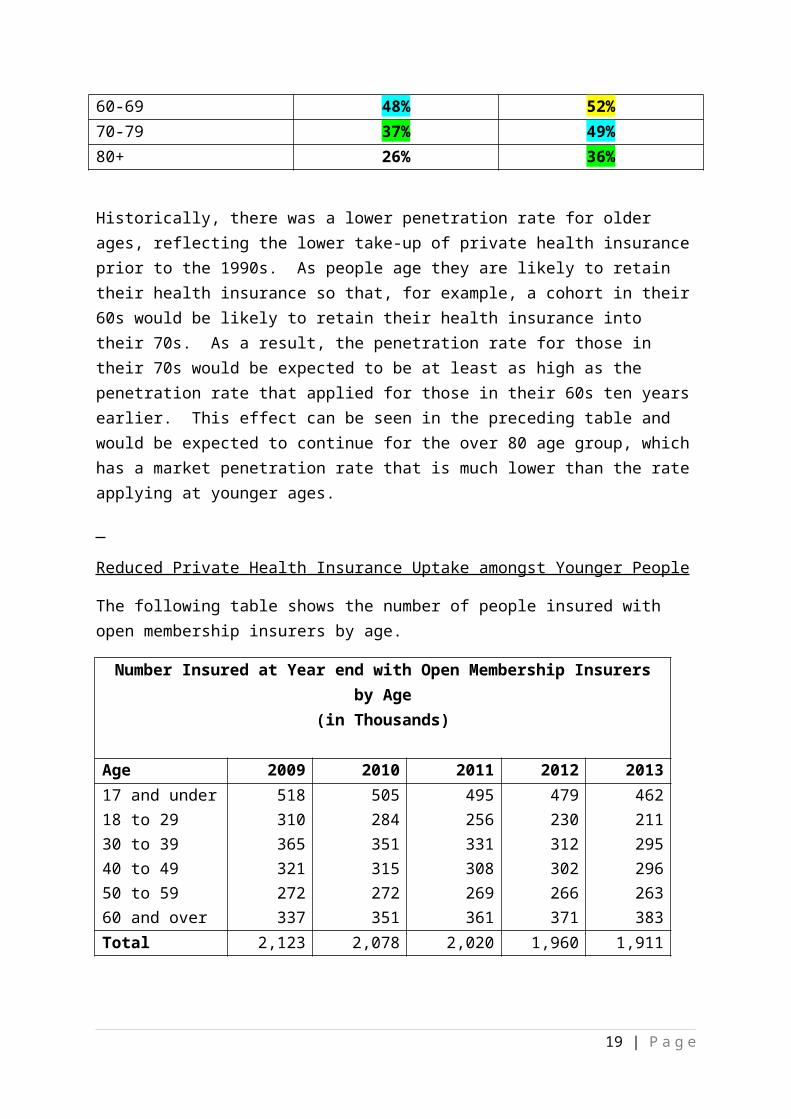

Increased Private Health Insurance Penetration amongst Older People

The market penetration rates of open membership insurers (i.e. the proportions of the population insured with an open membership insurer) over the age of 50 in the second half of 2003 and in the second half of 2013 are set out in the following table.

Open Membership Insurer Penetration RatesAge Group 2003 2013

50-59 52% 49%60-69 48% 52%70-79 37% 49%80+ 26% 36%

Historically, there was a lower penetration rate for older ages, reflecting the lower take-up of private health insurance prior to the 1990s. As people age they are likely to retain their health insurance so that, for example, a cohort in their 60s would be likely to retain their health insurance into their 70s. As a result, the penetration rate for those in their 70s would be expected to be at least as high as the penetration rate that applied for those in their 60s ten years earlier. This effect can be seen in the preceding table and would be expected to continue for the over 80 age group, which has a market penetration rate that is much lower than the rate applying at younger ages.

14 | P a g e

Reduced Private Health Insurance Uptake amongst Younger People

The following table shows the number of people insured with open membership insurers by age.

Number Insured at Year end with Open Membership Insurers by Age(in Thousands)

Age 2009 2010 2011 2012 201317 and under 518 505 495 479 46218 to 29 310 284 256 230 21130 to 39 365 351 331 312 29540 to 49 321 315 308 302 29650 to 59 272 272 269 266 26360 and over 337 351 361 371 383Total 2,123 2,078 2,020 1,960 1,911

It can be seen that the insured population in younger adult age groups is declining at a rapid rate. In particular, the 18-29 age group has declined 32% in four years (or 9% p.a.). The 30-39 age group has also declined rapidly, by 19% in four years or by 5% p.a.

It is noted that one reason for the decline in the number insured in the 20-29 age cohort is that this age cohort has declined significantly in the population in recent years, partly due to emigration but also partly due to the ageing of those born in the “baby boom” of the late seventies / early eighties. The number of people born in Ireland in 1990 (who are now aged 23) was 54,000, almost 30% lower than the 74,000 people born in 1980. While the insured population in the 18 to 29 age group declined by 32% between 2009 and 2013, the general population in the 20 – 29 age group declined by 23%.

On the other hand, the reduction between 2009 and 2013 of the insured populations between the ages of 30 and 39 and between the ages of 40 and 49 have occurred in spite of increases in the general population in these age groups over the same period.

Ireland: population in younger adult age cohorts (Source: CSO)2009 2010 2011 2012 2013

20-29 755 707.9 661.5 618.9 578.830-39 730.8 740.9 756.5 756.6 751.340-49 612.3 622.7 633.4 643.8 654.9All ages 4,533.4 4,554.8 4,574.9 4,585.0 4,593.120-29 -6.2% -6.6% -6.4% -6.5%30-39 1.4% 2.1% 0.0% -0.7%40-49 1.7% 1.7% 1.6% 1.7%

15 | P a g e

Market Penetration by Age

As at the end of 2013, the market penetration rate for open membership insurers is c. 42% (45% when restricted membership undertakings and those serving waiting periods are included). The following chart illustrates how market penetration rates vary by age for open membership insurers and how the rates of penetration have changed in recent years:

0-17 18-29 30-39 40-49 50-59 60-69 70-79 80+0%

10%

20%

30%

40%

50%

60%

Market Penetration Rates by Age Group - 2009 and 2013

End 2009End 2013

It can be seen that between 2009 and 2013, the penetration rate fell for all age groups up to age 70 and increased for older age groups. As discussed earlier, the increase in penetration rates at older age groups is entirely predictable and, while the penetration rate for those in their seventies is now close to the market peak, over the next 10 years the penetration rate for those over age 80 is likely to continue to increase from 36% to much closer to 49% (the penetration rate currently applying in the 70-79 age group).

Amongst the younger age groups, even though the 18-29 age group has experienced the greatest decline in insured persons, the greatest decline in penetration rates has occurred in the 30-39 age group (a decline of 13 percentage points vs a 6 percentage point decline in the 18-29 age group).

In 2011, the Information Returns Regulations were amended to provide that insurers would submit data to the Authority by year of age, enabling analysis of penetration rates by year of age (rather than age group) from 2011 on. The following chart shows how penetration rates vary by year of age at the end of 2013.

16 | P a g e

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 840%

10%

20%

30%

40%

50%

60%

Health Insurance Market Penetration by Age - end 2013

The chart shows that, apart from infants (for whom there is no charge prior to the first renewal date), the market penetration rate is below the market average (42%) for all ages under age 35 and is above average for all ages from 35 up to age 82. It would be expected in a voluntary community rated market for penetration rates at younger ages to be significantly lower than penetration rates at older ages and this is the case here. However, it is only between the ages of 22 and 31 (and above age 83) that the penetration rate drops below 35%. As noted earlier, the lower penetration rate for people in their 20s is not a new feature of the market.

Looking more closely at the dip in penetration rates for young adults, it can be seen that the penetration rate remains relatively high (at 38%) up to age 20 after which it drops quickly. It reaches a low point of 25% at age 25 after which it rises (again quickly) achieving the market average penetration rate of 42% by age 35.

Financial Impact of Ageing

The ageing of the insured population currently contributes approximately 3.1% p.a. to claims inflation. This compares with an ageing impact of approximately 1.3% when the market was growing up to 2008. Approximately half of the current ageing impact of 3.1% relates to the ageing of the general population and increased penetration rates in older ages. The other half of the ageing impact (c. 1.6%) relates to reduced market penetration rates at younger ages.

17 | P a g e

Summary of Analysis of Ageing

The preceding analysis shows that there are three causes for the ageing of the insured population:

The ageing of the general population. The portion of this factor that relates to increasing longevity and reduced fertility rates was almost inevitable and is likely to continue. A significant factor in recent years has also been the emigration of young adults. This ageing of the general population has particularly impacted on the 18-29 age group. Over the last four years, the impact on claims costs of the ageing of the general population is estimated to have been approximately 0.8% p.a.

An increase in penetration rates amongst older people. This factor was almost inevitable as age groups with higher penetration rates get older. It will continue for the next ten years as the penetration rates of those aged over 80 will increase from 36% to c. 50% in line with the penetration rate currently applying in the 70-79 age group. However, the effect of this factor over the next ten years would be expected to be lower than in the last ten years because the penetration rate in the 70-79 age group is already close to the peak. Over the last four years, the impact of this factor is estimated to have been approximately 0.6% p.a.

Reduced penetration rates at younger adult lives. There has been a very large reduction in the penetration rate in the 30-39 age group (of 13 percentage points) and smaller, but still large, reductions in the penetration rates in the 40-49 and 18-29 age groups (of 9 and 6 percentage points respectively). Over the last four years, the impact of this factor is estimated to have been approximately 1.6% p.a.

18 | P a g e

2.4 Analysis of Claims Data broken down by Procedure

Data Received

The four open membership insurers provided the Health Insurance Authority with data on claims paid broken down by year of admission, age, gender and hospital type. VHI Healthcare and Laya Healthcare provided the data for every year from 2007 to 2012 inclusive. Aviva Health provided the data for every year from 2009 to 2012 inclusive. GloHealth commenced operations in 2012 and, accordingly, do not have data for prior years. The insurers also provided the data for their most costly procedures (in terms of total costs).

An important factor to bear in mind when considering the data submitted is that data on casemix was not provided and, accordingly, it is not possible to allow for the impact of changes in casemix. This is especially important when considering changes in total costs but also has an impact when considering costs for individual procedures (e.g. there could be changes in the casemixes in public or private hospitals for those receiving chemotherapy which would not be apparent in this data). In order to allow fully for casemix changes it would be necessary for data to be coded by diagnosis in a consistent way across the market and submitted using a central system, such as the Hospital Inpatient Enquiry (HIPE) system. It is noted that, in the context of both universal health insurance and the enhancement of the risk equalisation system, the Minister for Health intends to introduce measures that will facilitate data collection of this kind. Analysis of Increase in Total Costs

The total cost for hospital admissions in 2007 was €1,089m1, while the total cost in the data for hospital admissions in 2012 was €1,646m.

The figure for 2007 is 103% of the figure included in information returns to the Authority for claims paid in respect of inpatient/day patient hospital episodes in the year 2007. This is in the range of what would be expected in view of the fact that the information returns data relates to claims paid in the year rather than admissions in the year.

The figure for 2012 is 96% of the figure included in information returns to the Authority for claims paid in respect of inpatient/day patient hospital episodes in that year. Accordingly, based on data in information returns, it would be expected that the ultimate cost of claims in respect of 2012 admissions would be higher than the amount included in the data provided. Some claims relating to 2012 admissions, which will ultimately be paid, would not have been included in the data provided to the Authority because they would not yet have been paid on the cut-off date for compiling the data. Based on discussions with insurers, it is understood that c. 5% of 2012 claims were outstanding when the data was submitted.

1 This figure does not include data for AVIVA Health / VIVAS Health, but information returns indicate the amount would be small in the context of the analysis.

19 | P a g e

Between 2007 and 2012, the total cost of claims included in the data submitted increased by €557m (or 51% of the total cost in 2007).

It is important to note that, consistent with the analysis of the impact of ageing earlier in this document, the increase in costs has not been driven primarily by demographic factors, which the data indicates only contributed 6% to the increase in total costs (the combined effect of a 5% reduction in market size and an 11% age related increase).

Claims relating to private hospitals accounted for €450m of the increase (or 81% of the total increase), while claims relating to public hospitals accounted for €106m (or 19% of the total increase).

Put another way, the total cost of claims relating to private hospitals grew by 72% from €622m to €1,072m during the period, while the total cost of claims relating to public hospitals grew by 23% from €467m to €573m.

The data indicates that the increase in costs in private hospitals has been driven by increased activity, with the number of admissions in private hospitals almost doubling (increase of 98%) in the period. The increase in total costs in private hospitals has been mitigated by a reduction of 13% in average cost per admission.

Conversely, the much lower increase in total cost relating to public hospital claims has been driven by an increase in the average cost per admission (36% increase). The number of public hospital admissions for which insurers paid claims reduced by 10% in the period.

Overall there has been an increase of 40% in the number of insurance related admissions between 2007 and 2012 and the average cost of claims related to these admissions has increased by 8%.

The increase in activity is coincident with an increase in the supply of private hospital services. In the five year period insurance related hospital admissions in private hospitals increased from 241,000 admissions in 2007 to 477,000 admissions in 2012. In the same period insurance related admissions in public hospitals reduced from 281,000 to 253,000.

The impact on total claims cost of average cost and activity in public and private hospitals is summarised in the table below:

20 | P a g e

Table: Impact on total claims cost of changes in activity levels and average cost per admission in public and private hospitals

Activity Average Cost Total

Public Hospitals -€ 55m € 162m € 106m

Private Hospitals € 571m -€ 121m € 450m

Total € 516m € 41m € 557m

The average cost per 2012 admission is similar in public and private hospitals (c. €2,250), although there are significant differences in casemix (e.g. public hospitals account for 35% of total claims but only 25% of claims for which data by procedure was provided) and the average length of stay in public hospitals is much longer than in private hospitals (3.2 days versus 2.2 days).

Data broken down by Procedure

Insurers were asked to provide data on their top 30 (by total cost) inpatient and day patient procedures. Accordingly the data provided excludes medical cases. The data broken down by procedure includes 37% of the total claims cost for 2012.

Analysis of this data shows similar results to the analysis of the total claims cost.

Specifically:

Total cost of these procedures increased by €194m or 46%. This increase related mainly to private hospitals, where the increase in cost was

€176m or 62%. The increase related mainly to an increase in activity (increase of 32%) rather than to

average cost per admission (increase of 11%). Looking at public and private hospitals separately it can be seen that the number of

related admissions in private hospitals increased by 63%, while the average cost per admission reduced by 13%. With respect to public hospitals, the number of related admissions reduced by 11%, while the average cost of these admissions increased by 28%.

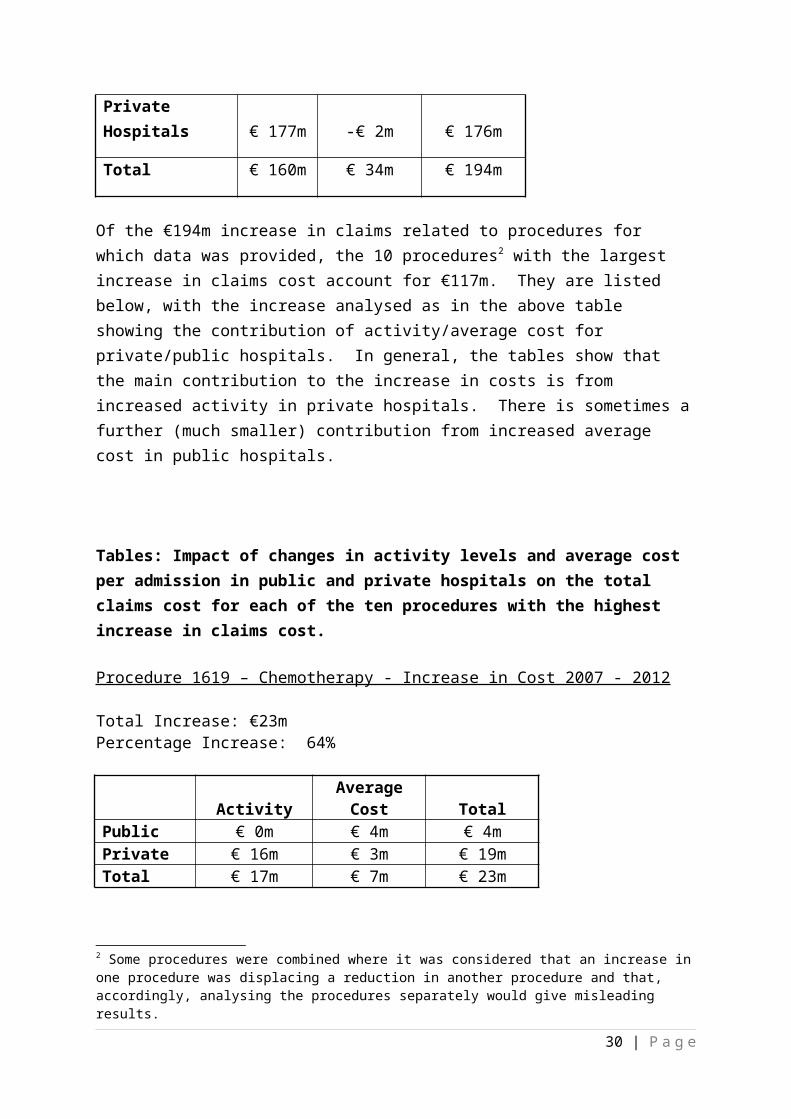

The impact on total claims cost for procedures for which data was provided of average cost and activity in public and private hospitals is summarised in the table below:

21 | P a g e

Table: Impact of changes in activity levels and average cost per admission in public and private hospitals on the total claims cost of procedures for which data was provided

ActivityAverage

Cost Total

Public Hospitals -€ 17m € 36m € 19m

Private Hospitals € 177m -€ 2m € 176m

Total € 160m € 34m € 194m

Of the €194m increase in claims related to procedures for which data was provided, the 10 procedures2 with the largest increase in claims cost account for €117m. They are listed below, with the increase analysed as in the above table showing the contribution of activity/average cost for private/public hospitals. In general, the tables show that the main contribution to the increase in costs is from increased activity in private hospitals. There is sometimes a further (much smaller) contribution from increased average cost in public hospitals.

Tables: Impact of changes in activity levels and average cost per admission in public and private hospitals on the total claims cost for each of the ten procedures with the highest increase in claims cost.

Procedure 1619 – Chemotherapy - Increase in Cost 2007 - 2012

Total Increase: €23mPercentage Increase: 64%

Activity Average Cost TotalPublic € 0m € 4m € 4mPrivate € 16m € 3m € 19mTotal € 17m € 7m € 23m

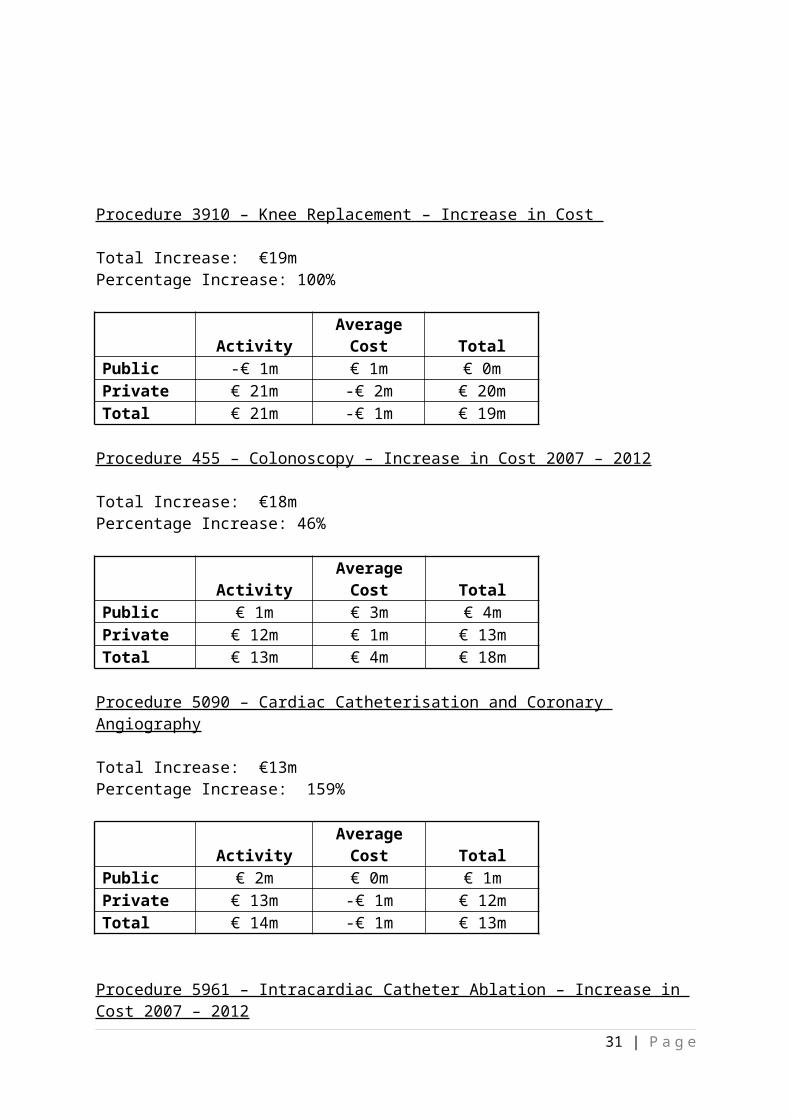

Procedure 3910 – Knee Replacement – Increase in Cost

2 Some procedures were combined where it was considered that an increase in one procedure was displacing a reduction in another procedure and that, accordingly, analysing the procedures separately would give misleading results.

22 | P a g e

Total Increase: €19mPercentage Increase: 100%

Activity Average Cost TotalPublic -€ 1m € 1m € 0mPrivate € 21m -€ 2m € 20mTotal € 21m -€ 1m € 19m

Procedure 455 – Colonoscopy – Increase in Cost 2007 – 2012

Total Increase: €18mPercentage Increase: 46%

Activity Average Cost TotalPublic € 1m € 3m € 4mPrivate € 12m € 1m € 13mTotal € 13m € 4m € 18m

Procedure 5090 – Cardiac Catheterisation and Coronary Angiography

Total Increase: €13mPercentage Increase: 159%

Activity Average Cost TotalPublic € 2m € 0m € 1mPrivate € 13m -€ 1m € 12mTotal € 14m -€ 1m € 13m

Procedure 5961 – Intracardiac Catheter Ablation – Increase in Cost 2007 – 2012

Total Increase: €11mPercentage Increase: 226%

Activity Average Cost TotalPublic € 0m € 0m € 0mPrivate € 10m € 1m € 11mTotal € 10m € 1m € 11m

Procedures 3660 and 3666 – Hip Replacement – Increase in Cost 2007 - 2012

23 | P a g e

Total Increase: €10mPercentage Increase: 31%

Activity Average Cost TotalPublic -€ 3m € 1m -€ 2mPrivate € 14m -€ 2m € 12mTotal € 11m -€ 2m € 10m

Procedure 2802 – Cataracts – Increase in Cost 2007 to 2012

Total Increase: €6mPercentage Increase: 31%

Activity Average Cost TotalPublic -€ 1m € 0m -€ 1mPrivate € 14m -€ 6m € 8mTotal € 12m -€ 6m € 6m

Procedures 3821 and 3822 Knee Cartilage – Increase in Cost 2007 to 2012

Total Increase: €6mPercentage Increase: 65%

Activity Average Cost TotalPublic € 0m € 0m € 0mPrivate € 6m € 0m € 6mTotal € 5m € 0m € 6m

Procedure 194 Upper GI Endoscopy – Increase in Cost 2007 to 2012

Total Increase: €6mPercentage Increase: 38%

Activity Average Cost TotalPublic € 0m € 3m € 2mPrivate € 4m € 0m € 4mTotal € 3m € 3m € 6m

Procedure 2190 – Caesarean Delivery – Increase in Cost 2007 to 2012

24 | P a g e

Total Increase: €5mPercentage Increase: 17%

Activity Average Cost TotalPublic -€ 6m € 12m € 5mPrivate -€ 1m € 1m € 0mTotal -€ 7m € 12m € 5m

Note: References to “activity” in the above tables and throughout this document relate only to activity in respect of which insurance claims were paid and references to cost are references to the cost of claims paid by the insurers.

Chapter 3 Summary of Submissions Received

25 | P a g e

Introduction

As part of Phase 2 of the Review of Measures to Reduce Costs in the Private Health Insurance Market, submissions were invited from interested parties by 14 April 2014. Seven submissions were received from the following parties.

Health Service Executive (HSE) The Independent Hospitals Association of Ireland ( IHAI) Insurance Ireland Irish Hospital Consultants Association (IHCA) Saint John of God Hospital St. Patrick’s Mental Health Services Society of Actuaries in Ireland (SAI)

A summary of all submissions received is provided below. As the submissions from the IHAI, Saint John of God Hospital and St. Patrick’s Mental Health Services focused in particular on responding to Chapter 7 of the Phase 1 report entitled ‘Industry Approach to Private Psychiatry’, a collective summary of those submissions is provided at 3.6 below.

3.1 Summary of HSE Submission

The HSE submission states that the Phase I report contains a number of recommendations that have significant implications for the HSE and it makes the following observations on the report:

The HSE is in broad agreement with the thrust of the report. The private health insurance market generates approximately €500m per annum for the public hospital system.

The HSE is in broad agreement with recommendations 1 to 7 of the report and are willing to work with the private health insurers on these issues.

Regarding the recommendations around claims processing, the HSE are striving to improve internal debt management processes including the continued roll out of the Claimsure electronic claims management system.

The issue around claims outstanding needs to be addressed through negotiations on Terms of Business between the HSE and health insurers.

The recommendation in Chapter 11 that a person confirms details of their treatment upon discharge has been introduced by the private health insurers by way of patient signatures at discharge and is the most problematic issue for the HSE and Voluntary hospitals (further details below).

26 | P a g e

The submission also lists ongoing issues between the HSE hospitals and private health insurers as follows:

Outstanding Claims – The HSE states that claims pended by private health insurers are increasing and that there is a lack of detail provided by insurers on the reasons why claims are pended or not paid.

Terms of Business Agreement – The absence of such an agreement between the HSE and private health insurers is an impediment to both parties.

Insurance Company Procedures – The HSE say there is a lack of clarity regarding what is covered by private health insurance policies and no arbitration method for any claims which are in dispute.

Insurers not paying for certain Day Case Procedures – Private health insurers have taken a strict interpretation of the word ‘bed’ and have refused payment when other treatment facilities, trollies or therapy chairs are used. The HSE position is that it is obliged to bill for inpatient services availed of and the accommodation resource is not relevant. The HSE see a need for clarity on what constitutes a day case versus an outpatient procedure.

New Consultant Appointees – Delays in private health insurers recognising new consultant appointees means that hospital claims cannot be processed.

Requests for More Information – Private health insurers are requesting more medical information on low value claims which delays payment.

Claim Code Indicator – Private health insurers have changed codes for some medical procedures which consultants appear to have been notified of but not hospitals, thereby delaying action on these claims.

Medical report for Orthopaedic Claims – Orthopaedic claims will not be paid unless accompanied by a medical report which is causing huge delays in payments.

Nominated contact person in Private Health Insurers – All hospitals identify the lack of a direct point of contact with private health insurers as a significant problem.

Road Traffic Accidents – One private health insurer is currently requesting an undertaking from patients that if their claim is successful the insurer will recover 100% of what they paid to the hospital, even though most RTA cases settle on a percentage basis.

Decoupling – The HSE propose that the statutory charge for inpatient services be decoupled from the primary and secondary Consultant’s bill.

Seeking Patient Signature on Discharge:

27 | P a g e

The main issue between the HSE and private health insurers is the new request from private health insurers seeking patient signatures on discharge, before a public hospital claim is processed

The same requirement has not been made of private hospitals

The HSE states that public hospitals currently do not have the IT systems or manpower resources available to comply with this new requirement (this is supported in the submission by a description of the impact of this new procedure on Beaumont Hospital).

There was no prior consultation by private health insurers with the HSE on this new requirement.

The HSE is open to finding a rational workable solution and are investigating how that can be achieved through the HSE Claimsure system.

The introduction of the Health (Amendment) Act 2013, which made provision for the charging of all private patients using public hospital beds, has led to some problems in the working relationship between the HSE and private health insurers. Both the HSE and insurers have engaged on these issues facilitated by Pat McLoughlin and Michael Horan of Insurance Ireland. The purpose of the engagement is to improve the working relationship between the parties.

Conclusion:

The HSE fully supports streamlining private income processes to enable faster billing and faster payment and are willing to work with private health insurers to maximise the benefit of any proposed changes to both parties.

Progress has been made to date, apart from the issue of signing on discharge, in engagements between the HSE and private health insurers. The HSE is confident that most issues between the parties can be resolved.

3.2 Summary of IHAI Submission (Non-Psychiatric Elements)

The IHAI submission noted the following points:

The important contribution made by the independent hospital sector in the provision of acute and mental health services nationally, through the 20 hospitals operated by its members, treating in the region of 400,000 patients annually.

The importance of private health insurance to the independent hospital sector, which is the main source of income for the sector. IHAI therefore welcomes measures which will ensure the long-term sustainability of the private health insurance market.

IHAI member hospitals contract on an individual basis with each health insurance provider, with such contracts negotiated annually. This is in contrast to the

28 | P a g e

arrangements between insurers and public hospitals where the rate for the provision of care is set by the Minister for Health.

The impact of recent national initiatives in the private health insurance market, including the State-driven measures affecting affordability for consumers, the charging of private patients occupying a public hospital bed, the increases by the private health insurance companies referencing the Health (Amendment) Act 2013 as a key driver for increases and the knock-on effect of consumers cancelling or downgrading their cover on increasing numbers of patients seeking treatment in public hospitals.

IHAI reiterated its support for initiatives which seek to address the affordability of private health insurance for citizens, providing them with the option of seeking independent hospital care.

The IHAI submission also responded to particular points made in the Phase 1 report including:

Cost of Claims

IHAI argues that while claims costs have increased between 2008 and 2012, it does not follow that this has been driven by an increase in the cost of services provided by its members and that through contract negotiation, prices paid by health insurers to providers have been reduced significantly in recent years.

Increased bed capacity in private hospitals arose as a direct result of State schemes which incentivised provision of additional facilities; there was also demand for these facilities due to the National Treatment Purchase Fund, under which over 20,000 public patients were treated annually.

Care Settings and Use of Resources:

While in the main private hospitals are reimbursed on a per-procedure basis, per diem rates apply in a number of instances, particularly for mental health services.

The tariff to be developed for DRG based charging under Money Follows the Patient (MFTP) should reflect the full economic cost of providing the service.

Age Structure of the Market:

IHAI support the introduction of lifetime community rating to incentivise younger people to join the private health insurance market; it also wants measures to be introduced to discourage people from taking out private health insurance cover for the first time in later life.

29 | P a g e

Clinical Audit and Utilisation Management:

IHAI states that look back audits and utilisation reviews are now a permanent feature of interaction between private hospitals and insurers and are reflected in contracts. The review proposed in the Phase 1 report should include ensuring that those undertaking such reviews are appropriately qualified.

Claims Processing:

IHAI state that the number of days taken by insurers to settle claims is increasing significantly with more claims being pended/queried. The majority of IHAI hospitals are currently using, or moving towards a ‘claims scanning’ system. However, despite engagement with the main private health insurance providers no agreement has been reached on the introduction of an E-Claims system, with the main issue relating to a significant increase in data requirements from insurers (106 data fields in current claim form and insurers want this increased to 164). Only one IHAI member has decided to move forward to pilot an E-Claims system.

3.3 Summary of Insurance Ireland Submission

The Insurance Ireland submission deals with Billing Audit, Fraud, Psychiatric Benefit, the submission from HSE, the submission from IHAI and other issues as follows:

Billing Audit:

Health insurers are carrying out greater claims scrutiny in order to contain costs, verify appropriate care and encourage efficiencies in the healthcare system. Claim enquiries are usually resolved directly with the healthcare provider, but if a satisfactory resolution cannot be reached, a full billing audit process may be invoked. The objective of a billing audit is to verify that a valid claim was submitted, that the treatment provided was necessary, adequate and effective and that the charges are appropriate and accurate. The multi-insurer group have also defined a dataset to facilitate electronic claiming in Ireland.

Fraud:

The term malpractice/fraud is wide ranging including inappropriate charging, i.e. incorrect billing for accommodation type, treatment not performed, up-coding etc. and supplying incorrect medical information, i.e. incorrect onset dates, wrong medical necessity information and questionable medical necessity for extended length of stay.

Under the auspices of Insurance Ireland each of the four health insurers will appoint

members from their organisations to represent them on Insurance Ireland’s Anti -

30 | P a g e

Fraud Forum. This Forum will address fraud, abuse and inefficiencies in the Irish health care system, encompassing public and private hospitals, consultants, GPs and medical accounts service agents. Draft terms of reference have been discussed and are being prepared. Some elements will be implemented straight away such as a whistleblower phone line. Independently each of the four insurers are making their own respective investments in personnel and IT system infrastructure to alert and future proof them from provider fraud into the future.

Psychiatric Benefit:

Insurance Ireland state that private psychiatric treatment in Ireland is currently underdeveloped and under-funded particularly in the areas of a) the provision of private psychiatric institutions outside the Dublin area and b) the provision of private community care at national level. It notes the increasing focus at European and national level on addressing mental health problems including the significant increase in alcohol and drug abuse.

In its submission, Insurance Ireland note that mental health services in the private sector are almost entirely Dublin-based and exclusively inpatient and lengths of stay are significantly longer in the private sector than the public sector. It notes that internationally it is accepted that there should be parity between physical and mental care. There may be an opportunity for insurers and private providers to take the initiative in support of the development of community mental health services while also improving in patient services.

The submission outlines in further detail the current system of mental healthcare in Ireland, governance, government policy (A Vision for Change) and future trends. It also gives an overview of the infrastructure of the public system, inpatient care, and the underlying principles and structure of outpatient/community-based care, and the private providers of mental healthcare in Ireland.

An international comparison by Insurance Ireland of resources available in other countries shows the proportion of the health budget allocated to mental health for Ireland as lower than France, the Netherlands, Germany and Australia.

The submission notes that the development of community-based services varies between the public and private systems, and states that careful consideration must be given when deciding on the insurance approach to community-based care – there are distinct differences between the public and private systems.

An integrated mental health service would require collaboration between private insurers and providers to develop community based mental health teams, day hospitals/day centres, and outpatient clinics.

31 | P a g e

The submission concludes that treating patients in day care/outpatient settings where appropriate usually has a lower unit cost than inpatient care due to lower per diem rates. Outpatient benefit is only paid through outpatient schemes but can be quite limited with significant co-payments applying. While the provision of community services in the private sector would broaden the range of treatment options available and would add to quality of care, it has the potential to increase costs overall given the investment requirement.

The insurers fully concur with the views from St. Patrick’s Hospital that the demand for high quality mental health services is increasing due to demographic and other factors. The submission states that a focus on quality based outcome measures supported by an adequate and properly resourced integrated care model based on best practice, is the only way to increase the cost effectiveness of services as demand continues to rise. The insurers also welcome the position of St. Patrick’s Hospital and St. John of God Hospital to working towards the mutual goal of excellence in Mental Health Care for patients within that system and state it will also be necessary to recognise and make explicit the constraints prescribed by funding challenges for insurers and providers in the development of such a model.

Response to HSE Submission:

Insurance Ireland welcomes the acknowledgement by the HSE that the private health insurance market represents a significant component of income received, however health insurers question the figure for outstanding debt put forward by the HSE. The submission states that all private health insurers receive notifications from public hospitals on outstanding debt which include payments that have already been paid or claims that have been rejected. Insurers consider a rejected claim as on outstanding debt between the hospital and the patient rather than the hospital and the insurer.

Claims Outstanding:

Insurance Ireland maintain there are a number of contributing factors to the HSE contention that outstanding claims have increased, citing a deterioration in the level of information provided by the HSE, failure to submit properly completed claim forms and a heightened level of claims scrutiny and clinical audit by insurers. Insurers also note that public hospitals take significantly longer to submit claims than private hospitals.

Terms of Business Agreement:

32 | P a g e

Private health insurers would welcome the opportunity to negotiate individual contracts with public hospitals similar to the contractual arrangements it enters into with private hospitals.

Insurance Company Procedures:

The HSE contention that there is a lack of clarity with regard to health insurance company procedures is rejected by Insurance Ireland as all insurers publicly publish their tables of cover and policy handbooks and this information is also held by the HIA. This submission also rejects that there is no arbitration provision for claims in dispute, stating the payment or otherwise of a claim is an insurance matter. It notes that the insurer has no liability for rejected claims and that private hospitals and consultants pursue monies owed from patients where a claim is rejected.

Insurers not paying for certain Day Case Procedures:

Insurers disagree with the HSE that the accommodation resource is not relevant in determining whether to charge private patients and state they have never covered services provided on a trolley, chair or other facility.

Seeking Patient Signature on Discharge:

Health insurers insist this requirement is an imperative since the introduction of new charging structures in public hospitals as of 1 January 2014. Agreement has been reached with the HSE on a form to be signed by all patients on admission from 1 June 2014 and it has been agreed that discussions will continue with HSE towards signature on discharge within 6 months.

New Consultant Appointees:

Health insurers are seeking receipt from the HSE of centralised information on all consultant changes and appointments, across all categories, in order to avoid delays in consultant recognition by insurers.

Requests for More Information:

Insurers acknowledge they are carrying out more claims scrutiny which requires further medical information and accept that Patient Accounts Departments should be advised when this information is sought.

33 | P a g e

Claim Code Indicator/Incorrect Codes:

Insurers note that hospitals should be notified in addition to consultants when changes in procedures occur.

Medical Reports for Orthopaedic Claims:

Health insurers are only obliged to pay claims for medically necessary treatments and require medical reports is order to assess claims properly.

Nominated Contact Person for Private Insurers:

Health insurers will ensure that all hospitals are provided with a contact point for queries.

Road Traffic Accidents:

Health insurers are legally entitled to recoup costs incurred by virtue of a third party.

Other Issues:

Insurance Ireland reiterates its position regarding the implementation of charges under the Health (Amendment) Act 2013.

Response to IHAI Submission:

Insurance Ireland agrees with the IHAI on the important role that private hospitals play within the health system and emphasises the interdependence between health insurers and private hospitals. They also support the IHAI view that insurers should be able to negotiate competitively with public hospitals in the same way as with private hospitals.

Cost Drivers in Private Hospitals:

While insurance Ireland accepts that the costs of private hospital beds has reduced over the period 2008 to 2012, it notes that the overall cost of private hospital care has increased due to the effects of changes in technology (costs of drugs and implants, changes in surgical techniques) and increases in utilisation.

Chronic Disease Management:

Insurance Ireland welcome support for measures to deal with chronic disease and its management.

34 | P a g e

Claims Processing:

Insurance Ireland accepts that private hospitals have a lower lead time from discharge to submission in the settlement of claims compared to public hospitals, but do not believe there has been an increase in the number of days taken to settle private claims in recent times. The introduction of an electronic claims process would significantly reduce the time taken to settle claims and a number of private providers are piloting e-claims.

Other Issues for Insurance Ireland:

The submission refers to the decision in Budget 2014 to curtail tax relief on premiums and states this has had a significant negative impact on the health insurance market. It refers to problems with the affordability of private health insurance and that it wishes to work constructively with the Government to ensure the benefits of a vibrant private health insurance sector are delivered to the maximum extent possible and in a way that achieves Universal Health Insurance. It welcomes the recent announcement by the Minister for Health regarding the introduction of lifetime community rating in 2015 and discounting for members up to age 25 in an effort to halt the exodus from the health insurance market.

3.4 Summary of IHCA Submission

The IHCA represents medical and dental hospital consultants in Ireland and is of the view that a number of significant issues need to be taken into account in assessing the sustainable provision of private health care in the future. Its submission sets out IHCA concerns, submissions and comments on the Phase 1 report’s conclusions and recommendations:

Representation on the Review Group:

IHCA highlights that the Review Group does not include representation from the IHCA which represents circa 85% of hospital consultants; IHCA believes the Review Group should have included representatives of all key stakeholders and is concerned that the “sectional and limited representation” on the Review Group will fail to ensure a comprehensive and balanced assessment of the issues.

Low Number of Hospital Consultants:

IHCA is concerned the Phase 1 report has overlooked the relatively low number of hospital consultants per capita in Ireland compared with other developed countries, which it sees as one of the significant challenges impacting on the provision of care to patients.

35 | P a g e

IHCA states Ireland has around two thirds the number of hospital consultants recommended by the Hanly report a decade ago and that demand for care has since grown substantially due to an ageing population. There are also difficulties in attracting and retaining the calibre and number of consultants needed due to significant reductions in income and increases in the cost of practising.

Costs:

IHCA argues that the chapter dealing with costs in the Phase 1 report does not fully assess a number of underlying costs such as the increases in per diem charges for private beds in public hospitals and the significant reductions in private procedure fees paid to consultants.

Cost of Clinical Indemnification: Reductions in procedure fees payable to consultants contrasts sharply with cost increases incurred by consultants for clinical indemnification, which depending on the specialty, has increased by 49% and 67% since 2008, with increases of between 25% and 33% in 2013.

The Medical Protection Society (MPS), the main provider of clinical indemnification in Ireland has confirmed that the costs of medical claims has increased by 42% in the past year which will lead to a corresponding average increase to clinical indemnification charges. IHCA state this represents a serious threat to the sustainability of care for patients in private hospitals, especially as the public system does not have the capacity to absorb additional patients.

Insurance payments to consultants: Reported levels of payments are based on gross revenue and do not reflect practice costs such as clinical indemnification, staff, rooms, general and other insurance, billing and other variable overhead costs. These costs have increased substantially in the past six years while procedure fees have been reduced, leading to a significant decline in private practice income.

Specific Points on Phase 1 Report Include:

The reference to consultant classifications needs to take account of the provisions included in consultant contracts which provide for consultants to treat private patients.

Hospital consultants had designed and implemented new clinical programmes to deliver improved models of care which have reduced lengths of stay and improved admission and discharge procedures.

The scale of the impact on health insurance premium increases of the reduction in income tax relief in the last budget should be quantified and reported.

36 | P a g e

The recommendation in relation to utilisation reviews should be discussed with the IHCA to ensure appropriate care is given to patients.

Private health insurers should have discussions with the IHCA on their proposals to develop an integrated care model for chronic disease management.

IHCA would welcome engagement with public hospitals on the improvement of debtor management performance; lack of support staff and systems in public hospitals are having an adverse impact on consultants submitting claims.

Insurers, hospitals and consultants should discuss development of a claims payment system to reduce payment delays and the administrative burden of dealing with pended, queried and returned claims.

IHCA should be consulted on proposals to develop discharge procedures.

3.5 Summary of Society of Actuaries in Ireland (SAI) Submission:

The SAI is the professional body representing the actuarial profession in Ireland. Its submission provides the SAI’s views on aspects of the Phase 1 report most relevant to actuarial consideration:

Age Structure of the Market:

SAI see the changing age structure of the market as potentially the most significant and most difficult issue to address. In a voluntary community rated market it will be difficult to slow the cycle of price increases which will potentially lead to younger healthier people leaving or not joining the private health insurance market, which in turn could lead to further price increases.

While ageing in the general population is a challenge for health services, ageing in the private health insurance market is significantly exacerbated as younger healthier people choose to exit the market. This contributes to a higher average age within the private health insurance market, making it likely that those leaving the market, across all age bands, are healthier, which in turn would have a further impact in terms of increasing average claims.

SAI notes some parallels between the private health insurance market and the difficulties faced in the pensions sector and suggests that an urgent examination of projections of the private health market in different scenarios will be important in devising policies to protect the sustainability of the private health insurance market.

37 | P a g e

Isolate the Impact of Ageing:

SAI recommend that the Phase 2 report isolates the impact of ageing on claims inflation as this will allow a better understanding of the extent to which non-demographic factors are impacting on claims inflation, and an enhanced understanding of the potential impact on inflation of measures designed to improve the age mix of the market.

SAI supports the Phase 1 recommendation that health insurers provide data to the HIA in relation to the top 30 procedures since 2008 which should enable the HIA to analyse the extent to which utilisation and unit costs for these procedures have varied over time. This will in turn help the review to understand the influence of factors such as cost per procedure and the relative impact of increased private bed capacity, high costs drugs and increased charges by public hospitals.

Measures to Encourage Younger People to Join the Market:

SAI agrees with the introduction of lifetime community rating as a means to incentivise younger people to enter or stay in the PHI market and with the recommendation that the Minister consider measures to encourage younger people to enter the market. In terms of health insurers extending student rates to age 23, SAI comments that student members attract a full adult risk equalisation levy.

3.6 Summary of Submissions from Saint John of God Hospital, St. Patrick’s Mental Health Services and IHAI on Industry Approach to Private Psychiatry

The submissions from IHAI, Saint John of God Hospital and St. Patrick’s Mental Health Services, all made the following points in response to Chapter 7 of the Phase 1 report:

Claims for psychiatric care are a small percentage of the overall claims paid out by health insurers.

All take issue with the comment that private patients are poorly served by a model of care which lacks a comprehensive and integrated approach by insurers and providers.

That international comparisons should be treated with caution, in particular lengths of stay comparisons between Ireland, Germany, Australia and South Africa – such comparisons are seen as not accurate or appropriate as these countries have a more developed model of community-based mental health services.

All disagree that there is a lack of clinical guidelines and point to adherence to the Mental Health Commission’s Code of Practice on Admission, Transfer and Discharge

38 | P a g e

from Approved Centres. Decisions regarding a person’s requirement for inpatient treatment are regulated by that Code and only occur after assessment by a specialist medical practitioner. The private health insurance industry should have no part to play in this process.

All would welcome increased collaboration and negotiation with health insurers to develop mental health services in line with best international practice.

Other points made include the following:

Absence of Community Based Infrastructure in the Mental Health Sector:

St. Patrick’s disagrees that there is such an absence and highlights the network of community based Dean Clinics it has established over the last seven years, with some support from the health insurance sector. It states that St. Patrick’s has moved towards a ‘Bundled Care’ model of service delivery and that if health insurers fully supported this model more services would be established in more regions around the country, resulting in better mental health for the insured and better value for the private health insurance industry.

St. Patrick’s states that it has engaged in ongoing annual negotiations with health insurance providers to move towards a more integrated model of care.

St. John of God Hospital makes that point that the HSE and the Department of Health have a role to play in the provision of community-based services. They also argue that in some cases private health insurers have been slow to, or have refused to cover, outpatient and day services for some specialist programmes such as addiction aftercare and eating disorder recovery.

Increases in Private Health Insurance Costs:

St. John of God Hospital points out that while health insurance premiums have increased steadily, the per diem rates it receives have been subject to price decreases and freezes since 2010. It also points out that private health insurers operate maximum revenue limits thereby controlling their annual spend with the hospital, and that consultant psychiatrists are not remunerated separately to the per diem rate.

Demand for high quality mental health services is increasing and it is only by focusing on quality based outcomes, supported by an adequate and properly resourced

39 | P a g e

integrated care model based on best practice, that any attempt can be made to increase the cost effectiveness of services for which there is increasing demand.

IHAI is concerned regarding the comments that private providers have not met the best international practice of an integrated private mental health service. IHAI responds that all IHAI member hospitals are regulated by the MHC and no comment regarding patients being poorly served has been made by the MHC to any member hospital. Similarly, insurers, which set out the terms annually for reimbursement to independent providers, have not expressed such concerns.

IHAI also refer to the Vision for Change Strategy for mental health services and that despite its members fully engaging with the strategy and bringing forward proposals to enhance implementation of Vision for Change through Public: Private Collaboration, none of the proposals it made were progressed.

40 | P a g e

Chapter 4 Chairman’s Observations and Recommendations

Introduction

In my interim Phase 1 report, issued in December 2013, I identified critical trends that raised serious concerns about the stability of a sustainable community rated private health insurance market. These were as follows:

250,000 persons had dropped out of the private health insurance market in the previous 5 years.

The increases in premiums ranged from 7.3% in 2011 to 12.1% in 2012.

The average cost of claims paid per insured person increased by 12.6 % per annum between 2008 and 2012.

The age structure of the market saw a significant ageing of the insured population. In 2003 13.3% of the insured population was aged over 60 and this had increased to 19% of the insured population by the second half of 2012.

The number of beds in private hospitals increased from 2,695 in 2008 to approximately 3,200 in 2011, an increase of 18.7%.

There was an increase of 33% in public consultants from 2005 to 2012.

4.1 Key Recommendations in the Phase 1 Interim Report

In the Phase 1 interim report, I recommended a series of actions which would:

help understand the dynamics of the market attract younger members into the market introduce a level playing pitch between public and private providers take collective actions as insurers to address key issues, and introduce best business practices in aspects of claims management.

Following the publication of the report, I received requests for meetings from interested parties, all of whom I met. The meetings involved the following:

Irish Hospital Consultants Association Independent Hospitals Association of Ireland Private Mental Health Providers Health Insurance Authority Insurance Ireland Each Health Insurer Senior HSE Management

41 | P a g e

St John of God Hospital, Dublin.

I invited submissions from all the parties I met and advised them in the interest of openness and transparency that I would publish their submissions in this report. These submissions were considered by the Review Group, but I would point out that the recommendations in this report are based on my own conclusions following all the meetings and submissions received. I have also included a table in Appendix 1 outlining the current position on each of the recommendations in the Phase 1 interim report. The following are my conclusions and recommendations in relation to the key issues identified in the interim report and addressed in Phase 2.

4.2 Data to Analyse Trends in the Industry

During Phase 1, the following issues were identified as potential contributors to the growth in claims:

An increase in the ageing of the population Higher use of insurance by membership Increased bed capacity in the private hospitals Increased use of high cost drugs and implants Shift of activity from public hospitals to high tech hospitals Increased claims for depression and mental health conditions Increased public bed charges for private patients.

During Phase 1, good progress was made in designing a template to analyse in detail the drivers behind rising costs in the industry. However, this issue became a difficulty again in Phase 2 and is the main cause of the delay in finalising this review. In particular:

There were difficulties in ensuring that the data requests were being interpreted similarly by each insurer.

Health insurers required a written confirmation from me that the Health Insurance Authority (HIA) would only use the data for the purpose of this review.

The completion of the data return took considerably longer than originally envisaged and agreed with the insurers.

The HIA needed to have a number of bi-lateral discussions with the insurers regarding the data provided.

Due to difficulties in extracting meaningful and comparable data on medical procedures, it was agreed ultimately to focus on surgical procedures.

42 | P a g e

Following a review of the first draft of claims cost data from HIA it was clear that further clarification of data with insurers would be required and this was done.

HIAs final paper ‘Private Health Insurance Claims Cost Analysis’ June 2014 is included in its entirety in Chapter 2 of this report.

Conclusions

In view of the trends in the industry over the past five years and the fact that €2 billion is being reimbursed it was surprising to note that:

Data of the type agreed in the template was not being collected by the HIA on an ongoing basis.

Insurers were not insisting on a common coding system across public and private providers to ensure they could understand the complexity of medical and surgical discharges.

The HIA and insurers held different views on whether the HIA was authorised to compile and analyse certain data.

Phase 2 Recommendations

In view of these conclusions, I recommend a number of steps to improve the availability and usefulness of data for the purpose of analysing and controlling costs:

The HIA should agree with the Department of Health the data set required to give the Minister the necessary analysis of industry trends, and/or additional legislative powers that the HIA may require to collect such information.

The HSE should work closely with the HIA to extract HIPE data on medical cases, so that the HIA can further analyse the causes of growth in medical admission costs.