Embed Size (px)

Citation preview

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 1/34

2011 Valuation Actuary Symposium

Sept. 12- 13, 2011

Session #39 PD: What’s New in Reserve Financing

for Life Insurance Products?

Scott Avitabile, Esq.

Robert Meehan, FIAAnn G. Perry

Moderator

Alan J. Routhenstein, FSA, MAAA

Primary Competency

Results-Oriented Solutions

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 2/34

1

What’s New in Reserve Financing

for Life Insurance Products?

Presented by: Scott D. Avitabile, Partner Dewey & LeBoeuf LLP

Session 39PD2011 Valuation Actuary Symposium

September 13, 2011

Dewey & LeBoeuf | 1

Table of Contents

I. Bank Funding Solutions to XXX/AXXX Reserves

II. Structure Overviews and Schematics

III. Regulatory Issues

IV. Limited Purpose Subsidiary

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 3/34

2

Dewey & LeBoeuf | 2

Bank Funding Solutions to XXX Reserves

Dewey & LeBoeuf | 3

Bank Funding Solutions to XXX/AXXX Reserves

Structured financial transaction designed to access bank funding toalleviate the reserve strain from Regulation XXX/AXXX reserverequirements on level premium term life and universal life insuranceproducts

Permits ceding insurer to retain economic benefits of experience on theceded policies

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 4/34

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 5/34

4

Dewey & LeBoeuf | 6

1. Ceding Insurer cedes its XXX/AXXX business toCaptive Re through a reinsurance contract

2. Captive Re issues Surplus Notes to the bank orbank issues letter of credit to Ceding Insurer

3. Captive Re accounts for Surplus Notes or Letter ofCredit as statutory capital

4. Captive Re deposits proceeds from Surplus Notesor the Letter of Credit equal to the reserves into theReserve Credit Trust or the Ceding Insurer holdsthe Letter of Credit as beneficiary

5. The Reserve Credit Trust is pledged to CedingInsurer, or Letter of Credit is held by CedingInsurer in each case to secure reinsurancereserve credit for the Ceding Insurer

6. Parent Company provides guaranty ofobligations of Captive Re

Capitve Re

Structure Schematic – Recourse Transaction

Ceding Insurer

Surplus Notes

Assets

Reinsurance

Contract

Reserve

Credit Trust

Parent

For the

Benefit of

LOC

Bank

LOC

Guaranty

LOC for the

Benefit of

Ceding Insurer

Dewey & LeBoeuf | 7

1. Ceding Insurer cedes its XXX/AXXX business toCaptive Re through a reinsurance contract

2. Captive Re issues Surplus Notes to the bank or

bank issues letter of credit to Ceding Insurer 3. Captive Re accounts for Surplus Notes or Letter of

Credit as statutory capital

4. Captive Re deposits proceeds from Surplus Notesor the Letter of Credit equal to the reserves into theReserve Credit Trust or the Ceding Insurer holdsthe Letter of Credit as beneficiary

5. The Reserve Credit Trust is pledged to CedingInsurer, or Letter of Credit is held by CedingInsurer in each case to secure reinsurancereserve credit for the Ceding Insurer

6. Obligation to reimburse the bank on a Letter ofCredit Draw is solely that of the Captive

Capitve Re

Structure Schematic – Non-Recourse Transaction

Ceding Insurer

Surplus Notes

Assets

Reinsurance

Contract

Reserve

Credit Trust

For the

Benefit of

LOC

Bank

LOC

LOC for the

Benefit of

Ceding Insurer

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 6/34

5

Dewey & LeBoeuf | 8

Regulatory Issues

Dewey & LeBoeuf | 9

Regulatory Issues

Formation of Special Purpose Captive Reinsurance Company

– Choice of domicile (South Carolina, Vermont, offshore)

Domiciliary Approvals

– Organization and licensure of captive

– Affiliate reinsurance arrangement

– Issuance of surplus notes

– Execution and delivery of related transaction documents

– Ongoing approval of payments on surplus notes

Reinsurance Arrangement

– Terms of reinsurance agreement between ceding insurer and captive must be approved byceding insurer's domiciliary state

– Reinsurance trust must be established and must comply with ceding insurer's domici liaryrequirements

– Investment guidelines must be established to manage funds inside and outside Reinsurancetrust

– Letter of Credit must comply with ceding insurer’s domiciliary requirements, although arecent trend in Non-recourse letter of credit transactions has been to uti lize “conditional”letters of credit, which do not necessari ly comply with such requirements

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 7/34

6

Dewey & LeBoeuf | 10

Regulatory Issues

Order of Draws on Letters of Credit

Conditions to Draws on Letters of Credit

Primary/Joint Liability of the Captive Reinsurer

Pledge of Assets of the Captive or the Cedant

Physical Segregation of Funds Withheld

Mark-to-Model Collateral Posting

Permitted Practices

– Letters of Credit as Capital of the Captive

– Trust Assets as Capital of the Captive

Parental Guarantees as Capital of the Captive

Dewey & LeBoeuf | 11

Limited Purpose Subsidiary Laws

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 8/34

7

Dewey & LeBoeuf | 12

Limited Purpose Subsidiary

Limited Purpose Subsidiary Laws adopted in Iowa (12/22/10), Georgia(7/1/11), Indiana (4/6/11) and Texas (6/17/11). All are very similar andbased on the original Iowa model

An LPS is similar to a captive insurance company in most ways, and isorganized via an application, which includes, among other items, aplan of operation, pro forma financial statements and a model of theproposed book of business to be reinsured, the same as would berequired to form a special purpose financial captive in Vermont orSouth Carolina

An LPS must be wholly-owned by the organizing life insurer

An LPS is required to maintain a minimum amount of capital ($2.5million in Iowa, plus any additional amount of capital as prescribed bythe Commissioner)

Dewey & LeBoeuf | 13

Limited Purpose Subsidiary (cont’d)

An LPS may:

i. Reinsure life risks of a parent or affiliate (except in Georgia, where itmay reinsurer only the risks of the direct parent)

ii. Issue debt securities (like surplus notes) and access financial marketsto support its capital

iii. Count as admitted assets on its statutory financial statementsproceeds from a securitization, letters of credit, parental guaranties andother assets approved by the state insurance department

iv. Retrocede its risks to third-party reinsurers if permitted by theCommissioner

v. Pay dividends to its parent so long as its prescribed minimum capitaland surplus amounts are not breached

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 9/34

8

Dewey & LeBoeuf | 14

Limited Purpose Subsidiary (cont’d)

The statutory right to count letters of credit and parental guaranties ascapital is a major development in the ability to finance Triple X reserves

The laws expressly provide that a debt security issued by an LPS willnot be considered an insurance product and that investors holding suchsecurities will not be deemed to be engaging in the business ofinsurance, which clarifies a long-running concern in the insurance-linked securities market

Dewey & LeBoeuf | 15

Offices Worldwide

Dewey & LeBoeuf LLP

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 10/34

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 11/34

2

Bank Loan:Payback - Guaranteed

Cost - Credit Rating

Monetization:

Payback - Secured Cost - <Full Sale

RBC Support:Payback - Heavily Secured

Cost - Credit Rating+/-

Trust Preferred:Payback - Unsecured

Cost - Credit Rating++

Debt Issuance:Payback - Unsecured

Cost - Credit Rating +

XXX Securitization:Payback-Heavily Secured

Cost - Min Size of 250M

collateral need

Surplus Note:Payback - Contingent on

Regulatory Approval

Cost - Credit Rating

Surplus Relief:Payback - Secured

Cost - Credit Rating+

DEBT EQUITY

Coinsurance:Payback - Underwritten

cash flows

Cost - Full Sale +/-

Equity Issue:Payback - Unsecured

Cost - Full Sale

Financial Solutions LandscapeExamples

Mortality Hedge:Payback - Extremely Secured

Cost - <<Credit Rating

Reserve Financing2

Reserve Financing

• Modified coinsurance or coinsurance structure on newlywritten business

New Business CashFinancing

• Often modified coinsurance or funds withheld coinsurancewhere assets reside with original cedant

Inforce Block CashFinancing

• Structured reinsurance using both coinsurance and modifiedcoinsurance or yearly renewable term (YRT) to reduce /eliminate cash transfer at inception

New Business Non-cash Financing

• Often referred to as “Surplus Relief” or “EV Securitizations”.Takes many forms st ructurally but in most cases accelerates aportion of the future statutory cash flow

Inforce Block Non-cashFinancing

• Modified coinsurance or funds held coinsurance generallyplaced without an explicit up-front ceding commissionSolvency Capital Relief

• Bank structured financing combined with reinsuranceprotections in a tax-advantaged solution for the cedingcompany

Hybrid Reinsurance

3

Structured ReinsuranceTransaction Types

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 12/34

3

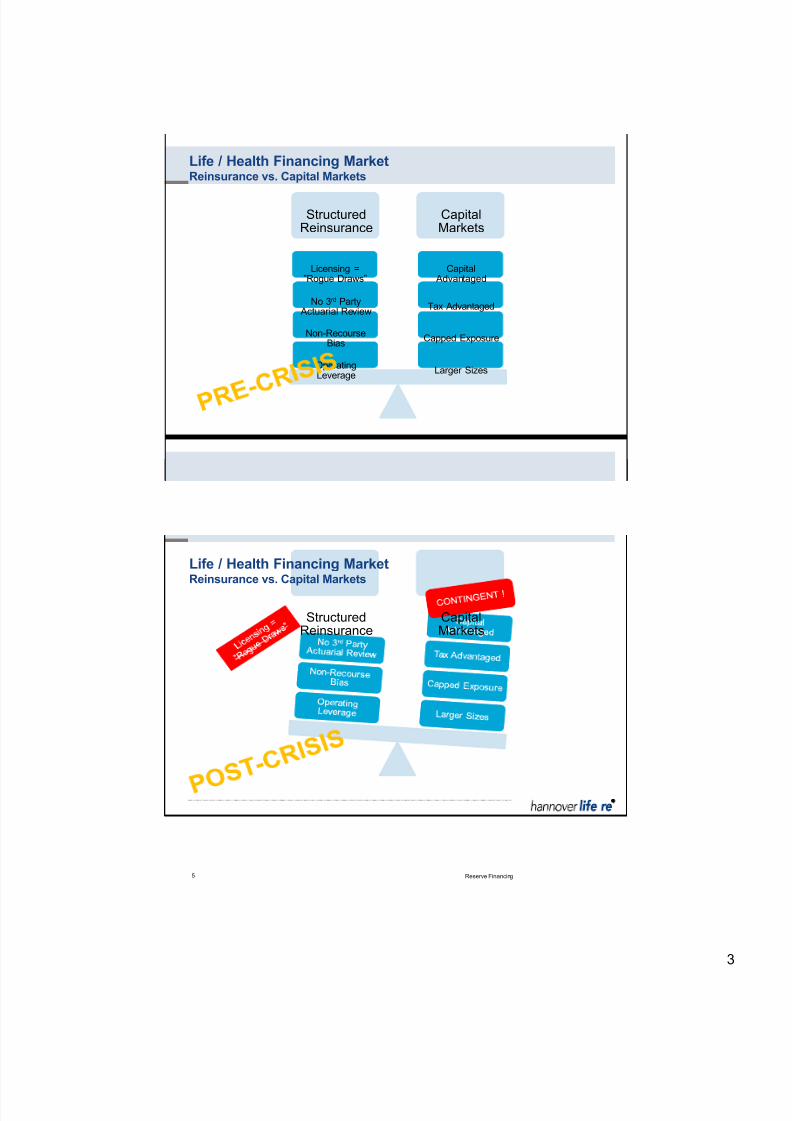

Reserve Financing

StructuredReinsurance

CapitalMarkets

Larger Sizes

Capped Exposure

Tax Advantaged

Capital Advantaged

OperatingLeverage

Non-RecourseBias

No 3rd Party Actuarial Review

Licensing =”Rogue Draws”

4

Life / Health Financing MarketReinsurance vs. Capital Markets

StructuredReinsurance

CapitalMarkets

Reserve Financing5

Life / Health Financing MarketReinsurance vs. Capital Markets

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 13/34

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 14/34

5

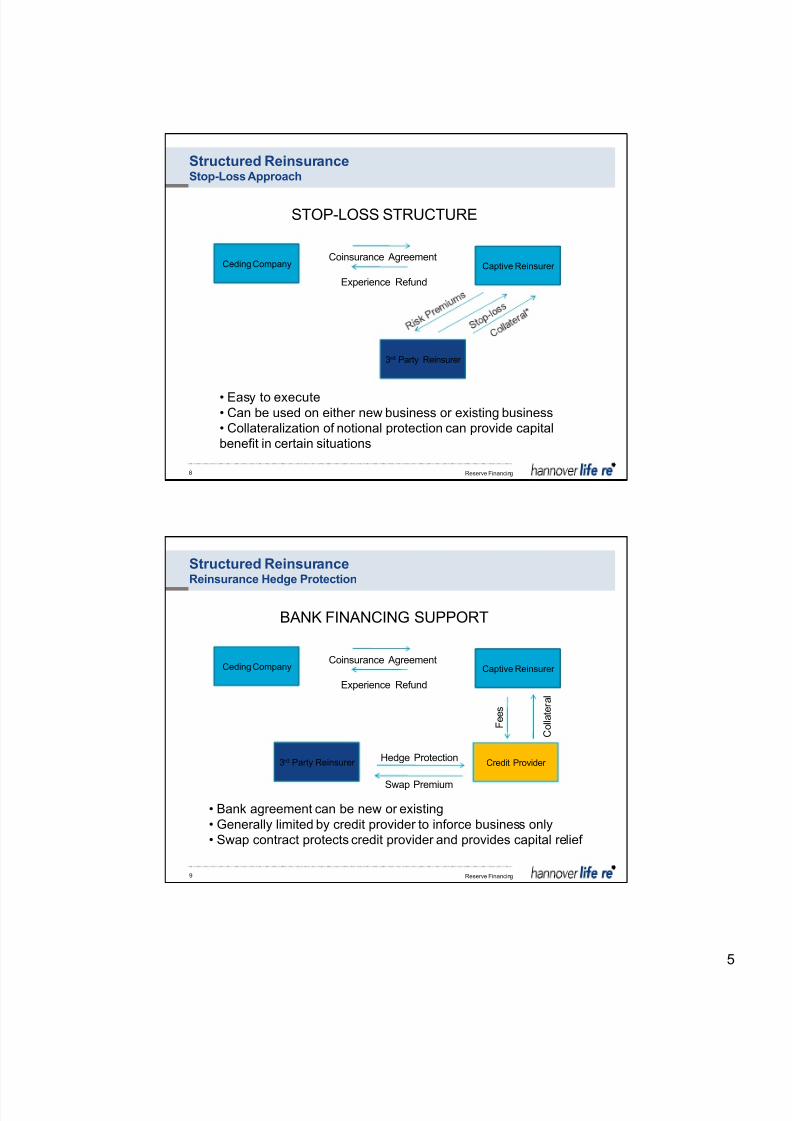

Reserve Financing

Ceding Company

3rd Party Reinsurer

STOP-LOSS STRUCTURE

Coinsurance Agreement

• Easy to execute• Can be used on either new business or existing business

• Collateralization of notional protection can provide capital

benefit in certain situations

Experience Refund

Captive Reinsurer

Structured ReinsuranceStop-Loss Approach

8

Reserve Financing

Ceding Company

3rd Party Reinsurer

BANK FINANCING SUPPORT

Coinsurance Agreement

• Bank agreement can be new or existing

• Generally limited by credit provider to inforce business only

• Swap contract protects credit provider and provides capital relief

Experience Refund

Captive Reinsurer

C o l l a t e r a l

F e e s

Credit Provider

Swap Premium

Hedge Protection

Structured ReinsuranceReinsurance Hedge Protection

9

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 15/34

6

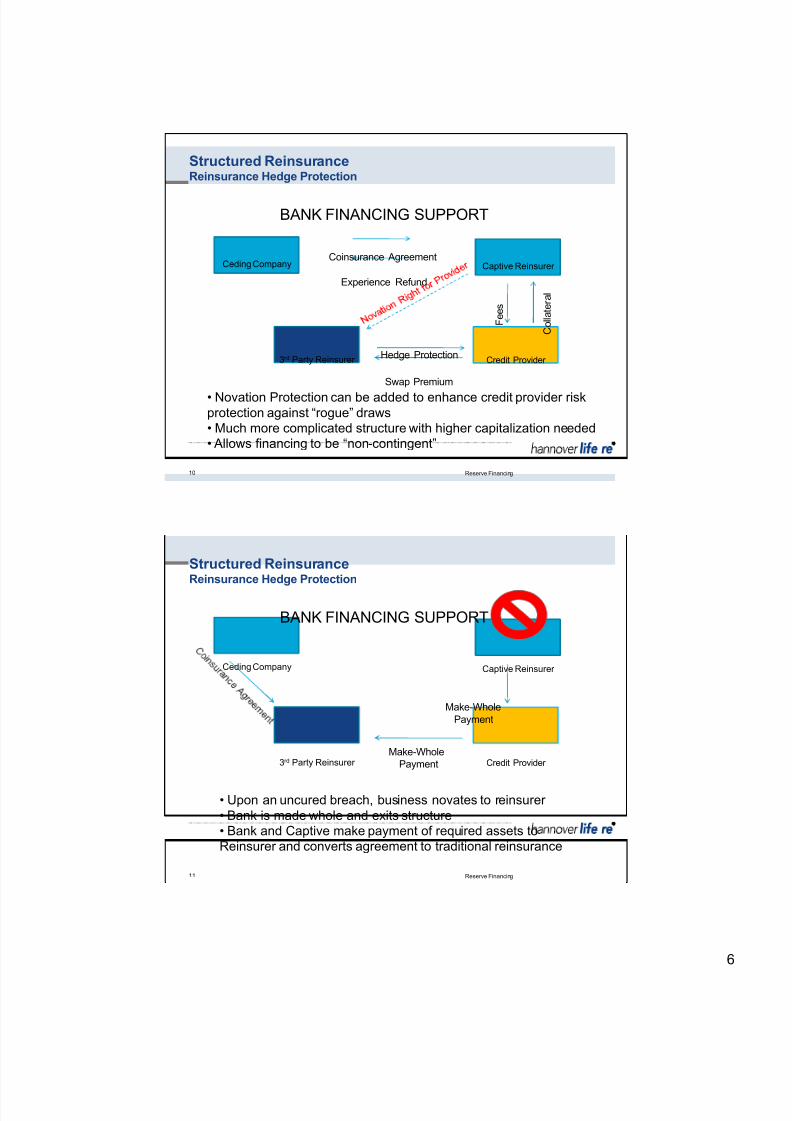

Reserve Financing

Ceding Company

3rd Party Reinsurer

BANK FINANCING SUPPORT

Coinsurance Agreement

• Novation Protection can be added to enhance credit provider riskprotection against “rogue” draws

• Much more complicated structure with higher capitalization needed

• Allows financing to be “non-contingent”

Experience Refund

Captive Reinsurer

C o l l a t e r a l

F e e s

Credit Provider

Swap Premium

Hedge Protection

Structured ReinsuranceReinsurance Hedge Protection

10

Reserve Financing

Ceding Company

3rd Party Reinsurer

BANK FINANCING SUPPORT

• Upon an uncured breach, business novates to reinsurer

• Bank is made whole and exits structure

• Bank and Captive make payment of required assets to

Reinsurer and converts agreement to traditional reinsurance

Captive Reinsurer

Make-Whole

Payment

Credit Provider Make-Whole

Payment

Structured ReinsuranceReinsurance Hedge Protection

11

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 16/34

7

u Longer tenors (durations)• 12+ years for XXX

• 20 years for AXXX

u AXXX• No-lapse guarantee “rider” approach

• Traditional coinsurance

u New business financing• Reinsurance support to credit providers allowing for inclusion of new

business into existing XXX/AXXX facilities

u Will funded solutions come back?• Rate environment issues

• Spreads• Market l iquidity

u Reinsurers / Banks / ILS Funds• Value added = f(size, tenor, risk appetite)

Reserve Financing

On the Horizon ... What’s New?Discussion Topics

12

Thank you!

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 17/34

1

EVALUATING OPERATING DEBT

USED BY LIFE INSURANCECOMPANIES

SEPTEMBER 13, 2011ANN PERRY, VICE PRESIDENT – SENIOR CREDIT OFFICER

2011 Valuation Actuary Symposium

Session 39PD

2EVALUATING OPERATING DEBT , SEPT EMBER-2011

Agenda

1. Operating Debt Framework - Criteria

2. Financing XXX/AXXX Reserves

3. Letters of Credit

4. Financial Metrics

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 18/34

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 19/34

3

5EVALUATING OPERATING DEBT , SEPT EMBER-2011

Asset Liability Management

» Assets and liabilities well matched

»Duration mismatch limited to +/- 6 months

»More cash matched as maturity approaches

»Minimal refinance risk/ pricing step-up risk small(<100bp)

6EVALUATING OPERATING DEBT , SEPT EMBER-2011

FINANCING XXX/AXXX RESERVES2

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 20/34

4

7EVALUATING OPERATING DEBT , SEPT EMBER-2011

Financing XXX/AXXX Reserves

» Term of debt should be matched to trust assets

» The term of debt may be less than peak level and/or runoff ofreserves

» Longer term financing solution may be required when debtmatures

» If debt matures within 3 years analysis includes stress scenarios

– Impact on capital adequacy and financial flexibility

– Reserves back onto ceding company’s balance sheet

8EVALUATING OPERATING DEBT , SEPT EMBER-2011

Asset Quality

» Asset risk must be low

– Investment grade with average A3

– Well diversified - no material concentration in any sector

» No security >1% of assets (excluding Aaa-rated governmentsecurities)

» 10 largest securities not > 5% of total assets

– Liquid – 144a or publicly traded

– Stable cash flows – Minimal market volatility

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 21/34

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 22/34

6

11EVALUATING OPERATING DEBT , SEPT EMBER-2011

Collateral Posting

» If collateral posting required, debt may not be eligible foroperating debt treatment

» Evaluations made at transaction inception

» CDS spread triggers problematic

» Collateral posting requirements incorporated intocompany’s liquidity analysis

12EVALUATING OPERATING DEBT , SEPT EMBER-2011

Other Considerations

»Operating debt must be issued closely (within 6months) to acquisition of associated assets

»Policyholder obligations not generally classified asdebt

»Recourse transactions only (analyticallydetermined)

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 23/34

7

13EVALUATING OPERATING DEBT , SEPT EMBER-2011

LETTERS OF CREDIT3

14EVALUATING OPERATING DEBT , SEPT EMBER-2011

Letters of Credit

»LOCs funding capital are treated as financial debt

However,…

»LOCs associated with remote risks (includingXXX/AXXX) analyzed for liquidity and capitaladequacy – not leverage and coverage

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 24/34

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 25/34

9

17EVALUATING OPERATING DEBT , SEPT EMBER-2011

7 WORLD TRADE CENTER250 GREENWICH STREETNEW YORK, NY 10007

18EVALUATING OPERATING DEBT , SEPT EMBER-2011

© 2011 Moody’s Investors Service, Inc. and/or its licensors and affiliates (collectively, “MOODY’S” ). All rights reserved.

CREDIT RATINGS ARE MOODY'S INVESTORS SERVICE , INC.'S (“MIS”) CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDITCOMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MIS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIALOBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK,INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS ARE NOT STATEMENTS OF CURRENT ORHISTORICAL FACT. CREDIT RATINGS DO NOT CONSTITUTE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS ARE NOT RECOMMENDATI ONS TOPURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. CREDIT RATINGS DO NOT COMMENT ON THE SUITABILI TY OF AN INVESTMENT FOR ANY PARTICULARINVESTOR. MIS ISSUES ITS CREDIT RATINGS WI TH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR W ILL MAKE ITS OWN STUDY AND EVALUATIONOF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BECOPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FORSUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WI THOUTMOODY’S PRIOR WRITTEN CONSENT. All information contai ned herein is obtained by MOODY’S fr om sources believed by it to be accurate and reliable. Because of the possibilityof human or mechanical error as well as other factors, however, all infor mation contained herei n is provided “AS IS” without warranty of any kind. Except as expressly statedotherwise, MOODY’S has not verified, audited or validated independently any information rec eived in the rating process, nor will it do so. Under no circumstances shall MOODY’Shave any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting f rom, or relating to, any error (negligent or otherwise) or other circ umstanceor contingency within or outside the control of MOODY’S or any of its directors, offic ers, employees or agents in connection with the procur ement, collection, compilati on, analysis,interpretation, c ommunication, publicati on or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever(including without limitation, lost profits ), even if MOODY’S is advised in advance of the possibility of suc h damages, resulting fr om the use of or inability to use, any such information.The ratings, financial reporting analysis , projections, and other observations, if any, constituting part of the information contained herei n are, and must be construed solely as,statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Eac h user of the information contained herein must make its own studyand evaluation of each security it may consider purchasing, holding or selling. NO W ARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS,MERCHANTABILITY OR FI TNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION I S GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned cr edit rating agency subsidiary of Moody’s Corporation (“MCO”) , hereby discloses that most issuers of debt securities (including cor porate and municipal bonds,debentures, notes and c ommercial paper) and prefer red stock rated by MIS have, prior to assignment of any rating, agr eed to pay to MIS for appraisal and rating services rendered

by it fees ranging from $1,500 to approximately $2,500, 000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes.Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reportedto the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Shareholder Relations —Corpor ate Governance — Directorand Shareholder Affiliation Policy.”

Any publication into Australia of this document is by MOODY’S aff iliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657, which holds Australian Financial ServicesLicense no. 336969. This document i s intended to be provided only to “wholesale clients” within the meaning of sec tion 761G of the Corporations Ac t 2001. By continuing to accessthis document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor theentity you represent will directly or indirectly disseminate this document or its contents to “retail clients”within the meaning of section 761G of the Corporations Act 2001.

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 26/34

1 September 21, 2011 [Enter presentation title in footer] Copyright © 2007

What’s New in Reserve Financing

for Life Insurance Products?

Session 39PD

2011 Valuation Actuary Symposium

Presented by

Alan Routhenstein, FSA, MAAA

September 13, 2011

2

First, let’s meet the panelists …

Ann Perry, Vice President – Senior Credit Officer

Moody’s Investor Service

Scott Avitabile, Esq, Partner

Dewey & LeBoeuf LLP

Rob Meehan, FIA, VP, Pricing - Financial Solutions

Hannover Life Re

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 27/34

2 September 21, 2011 [Enter presentation title in footer] Copyright © 2007

3

Our organizational plan for this session is:

1. Consulting Actuary Perspective (Alan)

2. Rating Agency Perspective (Ann)

3. Law Firm Perspective (Scott)

4. Reinsurer Perspective (Rob)

5. Questions & Answers (Audience)

4

Consulting Actuary Perspective

§Why do many insurers and reinsurers use reserve financing?

§ Financing transactions publicized in the last 18 months

§Common forms of life reserve f inancing transactions

§Recent developments in life reserve f inancing

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 28/34

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 29/34

4 September 21, 2011 [Enter presentation title in footer] Copyright © 2007

7

Consulting Actuary Perspective

§Why do many insurers and reinsurers use reserve financing?

§ Financing transactions publicized in the last 18 months

§Common forms of life reserve f inancing transactions

§Recent developments in life reserve f inancing

8

At least 13 reserve or EV financing deals have

been disclosed in the last 18 months

Disclosure

or Announce-

ment Date

Protection Buyer or

Insurance Group

Issuer of Financing

Disclosed Description

of Subject Business

Disclosed

Maturity of

Transaction LOC Funding

Unclear or

Other

Forms of

Collateral

Lead Financing

Provider or Risk

Taker

6/6/2011 Atlanticlux unit linked life EV 10y EUR 60 PartnerRe

5/24/2011 Lincoln XXX 12y $925 Credit Suisse

4/19/2011 Ohio National XXX & AXXX 20y $250 sr. debt investors

4/6/2011 Old Mutual XXX &/or AXXX N / A N / A Nomura

3/30/2011 MetLife XXX & AXXX 10y $350 Credit Agricole

1/24/2011 ING XXX 8y $615 CS, HLR

12/21/2010 RGA XXX 10y ext to 20y $300 Nomura

12/10/2010 Protective XXX 12y $790 UBS

7/13/2010 Aviva XXX & AXXX "long term" $325 Credit Agricole

6/15/2010 Lincoln AXXX 30y $500 sr. debt investors

5/4/2010 Mutual of Omaha XXX 7y $150 Credit Agricole

4/29/2010 Protective XXX 8y $610 UBS

3/1/2010 Hannover Re life & health 30y $500 Deutsche Bank

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 30/34

5 September 21, 2011 [Enter presentation title in footer] Copyright © 2007

9

Consulting Actuary Perspective

§Why do many insurers and reinsurers use reserve financing?

§ Financing transactions publicized in the last 18 months

§Common forms of life reserve f inancing transactions

§Recent developments in life reserve f inancing

10

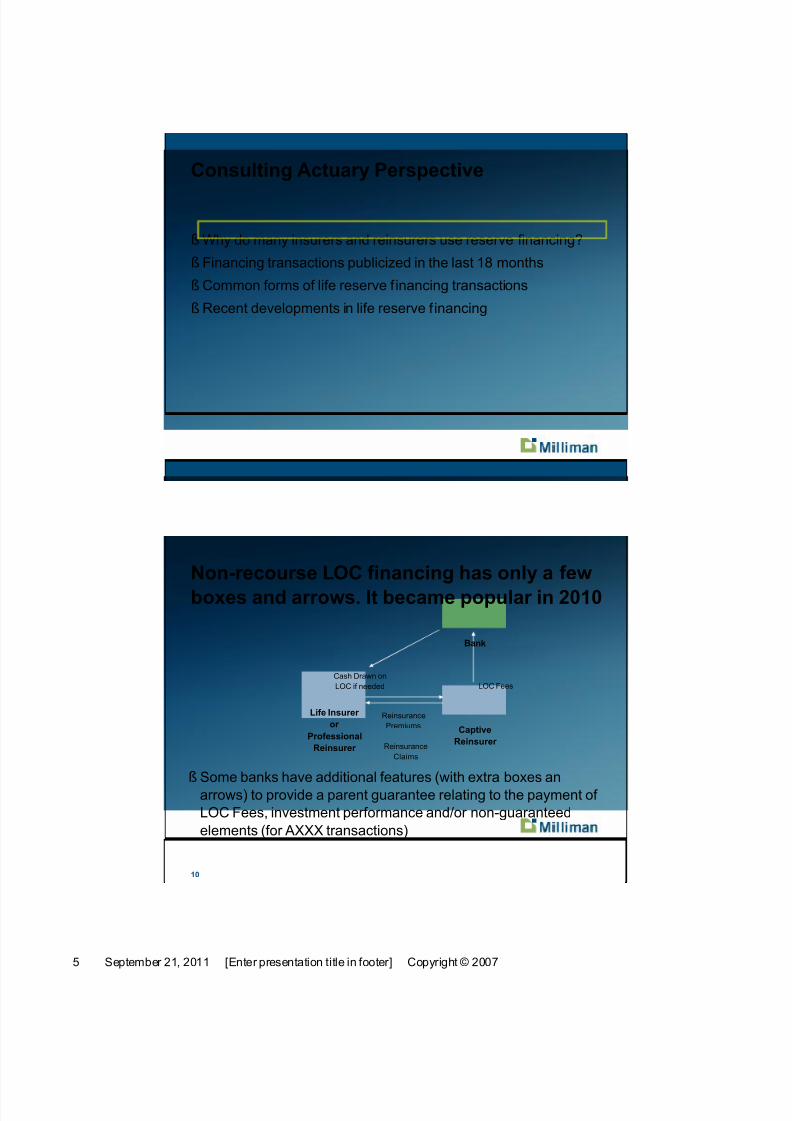

Non-recourse LOC financing has only a few

boxes and arrows. It became popular in 2010

§Some banks have additional features (with extra boxes an

arrows) to provide a parent guarantee relating to the payment of

LOC Fees, investment performance and/or non-guaranteed

elements (for AXXX transactions)

Bank

Captive

Reinsurer

Reinsurance

Premiums

Reinsurance

Claims

Life Insurer

or

Professional

Reinsurer

LOC Fees

Cash Drawn on

LOC if needed

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 31/34

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 32/34

7 September 21, 2011 [Enter presentation title in footer] Copyright © 2007

13

A recourse funded solution is usually

guaranteed by the holding company

§ In a diagram

for a non-

recourse

funded

solution, the

Holding

Company box

and arrowwould be

deleted

Surplus Note

Investor(s)

Captive

Reinsurer

Reinsurance

Premiums

Reinsurance

Claims

Surplus Note

proceeds

Reserve

Credit Trust

Ceding

company is

beneficiary

Life Insurer

or

Professional

Reinsurer

Holding

company

Guarantee

Surplus Note interest

& principal

Surplus Note

proceeds

Investment

income

14

A wrapped funded solution usually involves

an SPV and a financial guarantor

SPV

Captive

Reinsurer

Reinsurance

Premiums

Reinsurance

Claims

`

Surplus

Note

proceeds

Reserve

Credit Trust

Ceding

company is

beneficiary

Life Insurer

or

Professional

Reinsurer

Financial

Guarantor

Guarantee

of interest

& principal

Surplus

Note

interest &

principal

Surplus Note

proceeds

Investment

income

Debt

Investor(s)

Debt interest & principal

Pro-

ceeds

Guarantor

Fee

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 33/34

8 September 21, 2011 [Enter presentation title in footer] Copyright © 2007

15

Consulting Actuary Perspective

§Why do many insurers and reinsurers use reserve financing?

§ Financing transactions publicized in the last 18 months

§Common forms of life reserve f inancing transactions

§Recent developments in life reserve f inancing

16

We have seen key rating agency & regulatory

developments over the last 18 months

§Moody’s issued operating debt guidance in May 2011.

§ Fitch issued Insurance-Linked Securities (“ILS”) criteria in

August 2011.

§Dodd-Frank Act is a 2010 federal statute that restricts

extra-territorial state reinsurance regulation.

§ Limited Purpose Subsidiary (“LPS”) laws in IA, IN, GA and TX

permit a parent guarantee as a form of financing.

8/11/2019 2011-orlando-valact-39 (1)

http://slidepdf.com/reader/full/2011-orlando-valact-39-1 34/34

17

There have been of other ILS market

developments over the last 18 months

§Mutual insurers: Mutual of Omaha became the first mutual for

which LOC financing has been publicized.

§ Financing providers: More banks offer solutions. Some banks

prefer non-recourse solutions. More banks offer AXXX LOCs.

§Other forms of collateral: Many LOCs have provisions that don’t

meet the strict NAIC definition of LOC. Other innovative

structures are being marketed.

§Reinsurer participation: Professional reinsurers are involved in

many non-recourse transactions.