Embed Size (px)

Citation preview

Provided by Academy of Professional Accounting (APA)

Professional Accounting Education

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台

ACCA F3

Financial Accounting (FA)

财务会计 第十三讲

ACCA Lecturer: Carrie NI

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 2

D6: Intangible Non-Current Assets

Intangible assets

Research and development costs

Disclosure in financial statements

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 3

Intangible asset

Definition

An intangible non-current asset is an identifiable non-

monetary non-current asset without physical substance.

The following are examples of intangible assets:

Goodwill

Patents, licenses, trade markets, copyrights

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 4

Research and Development Cost

Research and development costs

Companies need to account for these costs and whilst the credit

entry may be recorded as a current liability, the question remains

as to where the debit entry should be shown.

The choices are:

a) To debit profit or loss with an expense, or

b) To debit the statement of financial position with an intangible

non-current asset.

An intangible non-current asset should only be recorded when the

entity is confident that the expenditure will generate future profit.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 5

Research and Development Cost

Definitions

Research is original and planned investigation

undertaken with the prospect of gaining new scientific or

technical knowledge and understanding.

Development is the application of research findings or

other knowledge to plan or design for the production of

new or substantially improved materials, devices,

products, processes, systems or services before the

start of commercial production or use.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 6

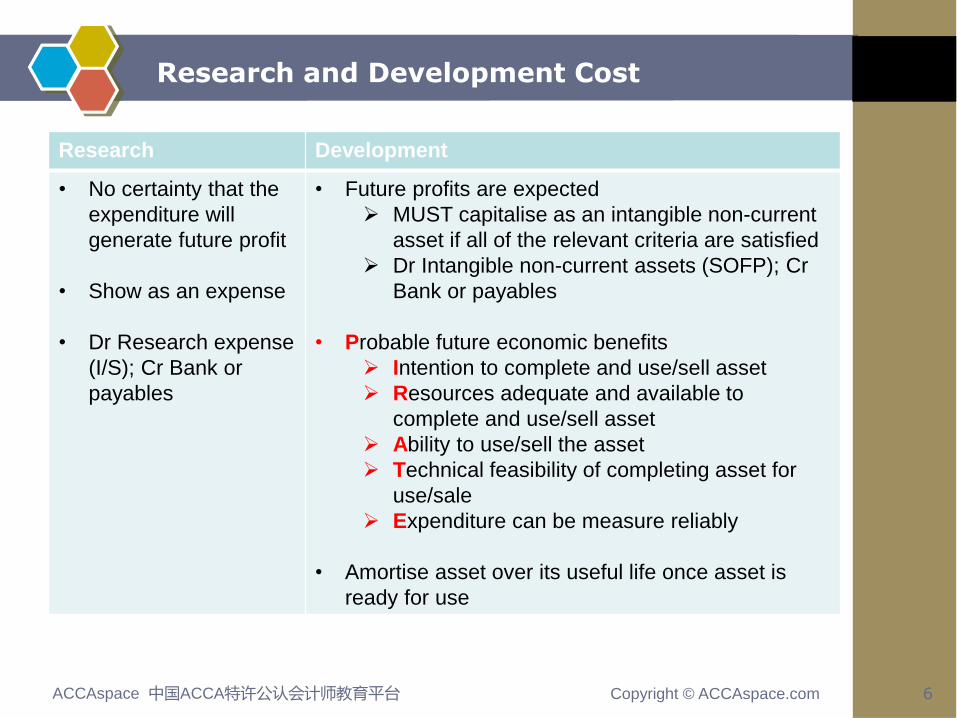

Research and Development Cost

Research Development

• No certainty that the

expenditure will

generate future profit

• Show as an expense

• Dr Research expense

(I/S); Cr Bank or

payables

• Future profits are expected

MUST capitalise as an intangible non-current

asset if all of the relevant criteria are satisfied

Dr Intangible non-current assets (SOFP); Cr

Bank or payables

• Probable future economic benefits

Intention to complete and use/sell asset

Resources adequate and available to

complete and use/sell asset

Ability to use/sell the asset

Technical feasibility of completing asset for

use/sale

Expenditure can be measure reliably

• Amortise asset over its useful life once asset is

ready for use

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 7

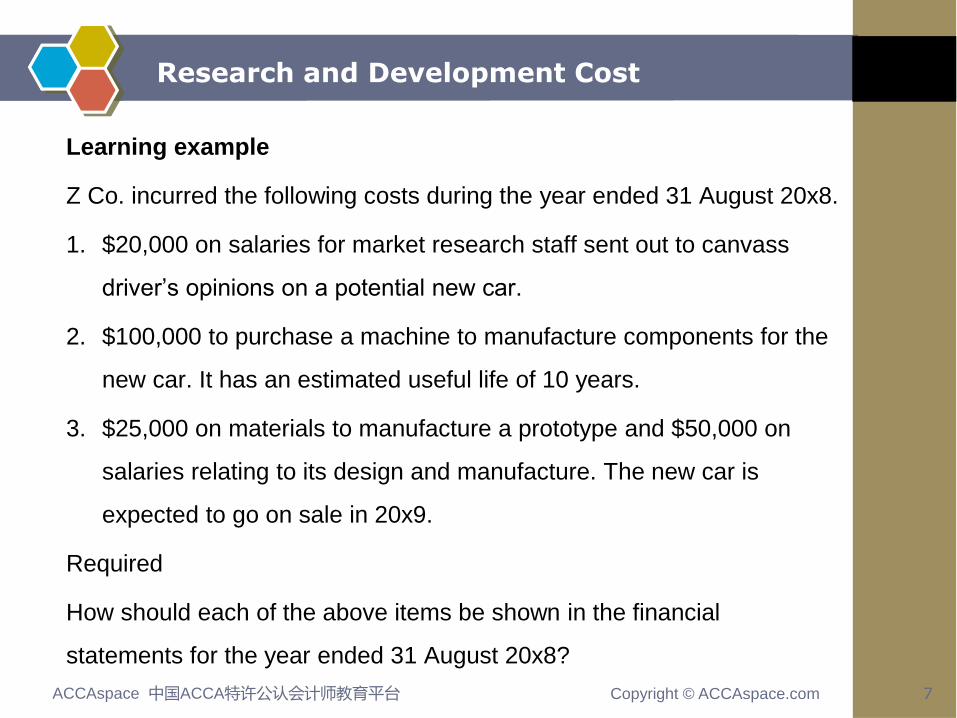

Research and Development Cost

Learning example

Z Co. incurred the following costs during the year ended 31 August 20x8.

1. $20,000 on salaries for market research staff sent out to canvass

driver’s opinions on a potential new car.

2. $100,000 to purchase a machine to manufacture components for the

new car. It has an estimated useful life of 10 years.

3. $25,000 on materials to manufacture a prototype and $50,000 on

salaries relating to its design and manufacture. The new car is

expected to go on sale in 20x9.

Required

How should each of the above items be shown in the financial

statements for the year ended 31 August 20x8?

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 8

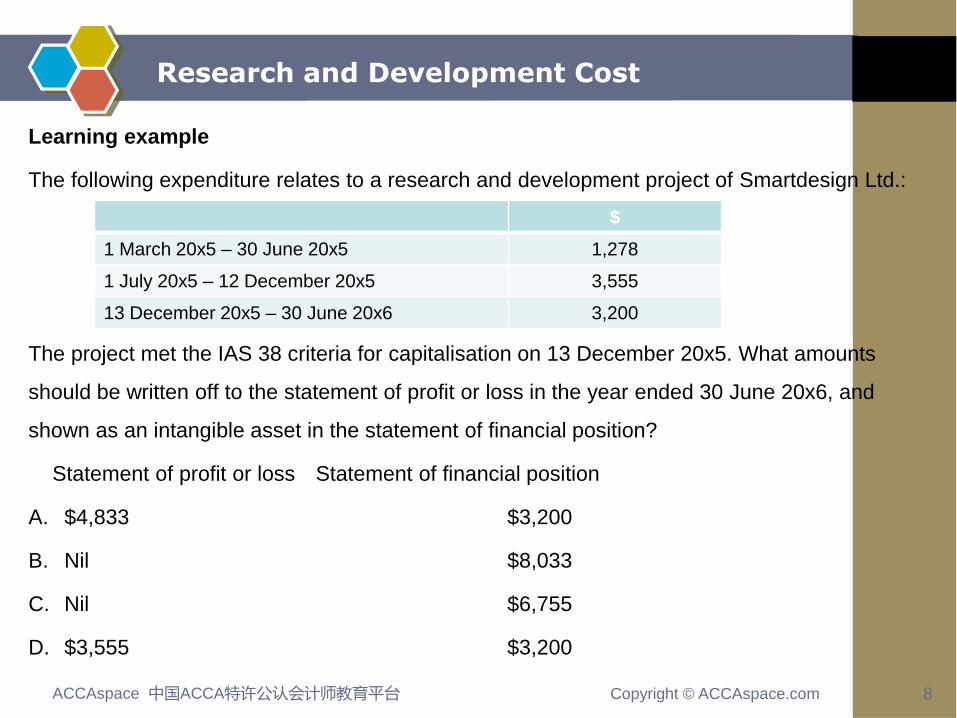

Research and Development Cost

Learning example

The following expenditure relates to a research and development project of Smartdesign Ltd.:

The project met the IAS 38 criteria for capitalisation on 13 December 20x5. What amounts

should be written off to the statement of profit or loss in the year ended 30 June 20x6, and

shown as an intangible asset in the statement of financial position?

Statement of profit or loss Statement of financial position

A. $4,833 $3,200

B. Nil $8,033

C. Nil $6,755

D. $3,555 $3,200

$

1 March 20x5 – 30 June 20x5 1,278

1 July 20x5 – 12 December 20x5 3,555

13 December 20x5 – 30 June 20x6 3,200

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 9

Research and Development Cost

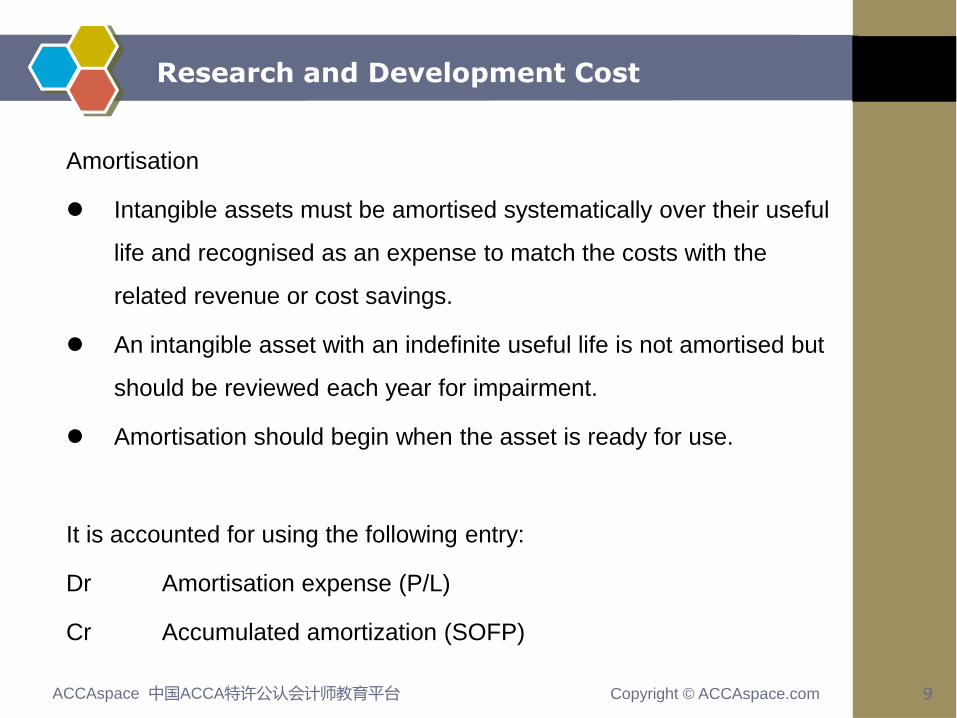

Amortisation

Intangible assets must be amortised systematically over their useful

life and recognised as an expense to match the costs with the

related revenue or cost savings.

An intangible asset with an indefinite useful life is not amortised but

should be reviewed each year for impairment.

Amortisation should begin when the asset is ready for use.

It is accounted for using the following entry:

Dr Amortisation expense (P/L)

Cr Accumulated amortization (SOFP)

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 10

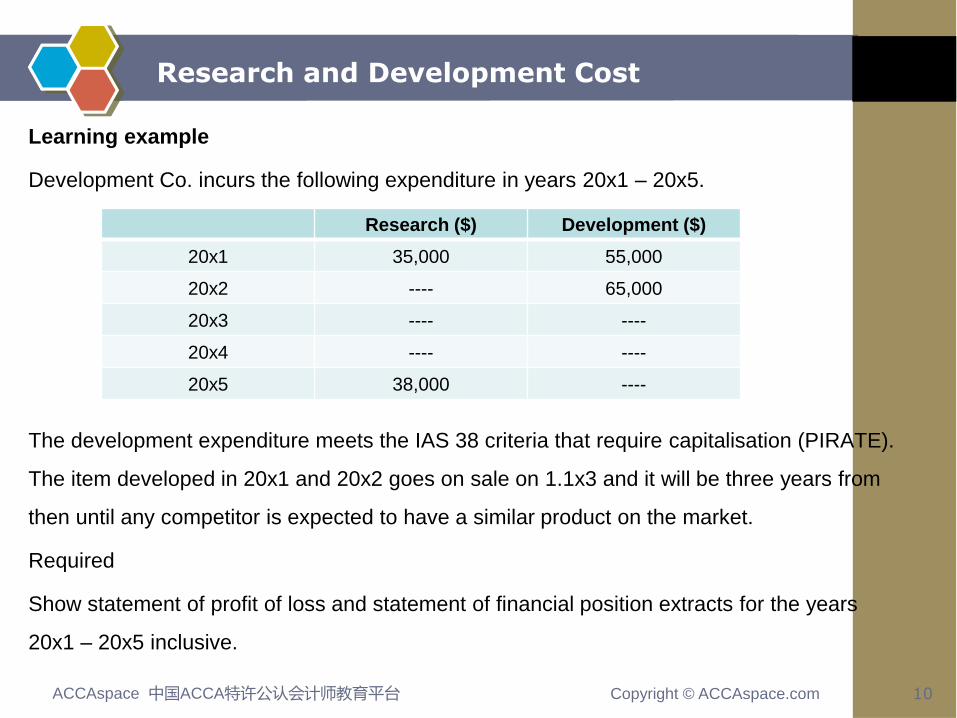

Research and Development Cost

Learning example

Development Co. incurs the following expenditure in years 20x1 – 20x5.

The development expenditure meets the IAS 38 criteria that require capitalisation (PIRATE).

The item developed in 20x1 and 20x2 goes on sale on 1.1x3 and it will be three years from

then until any competitor is expected to have a similar product on the market.

Required

Show statement of profit of loss and statement of financial position extracts for the years

20x1 – 20x5 inclusive.

Research ($) Development ($)

20x1 35,000 55,000

20x2 ---- 65,000

20x3 ---- ----

20x4 ---- ----

20x5 38,000 ----

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 11

Research and Development Cost

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 12

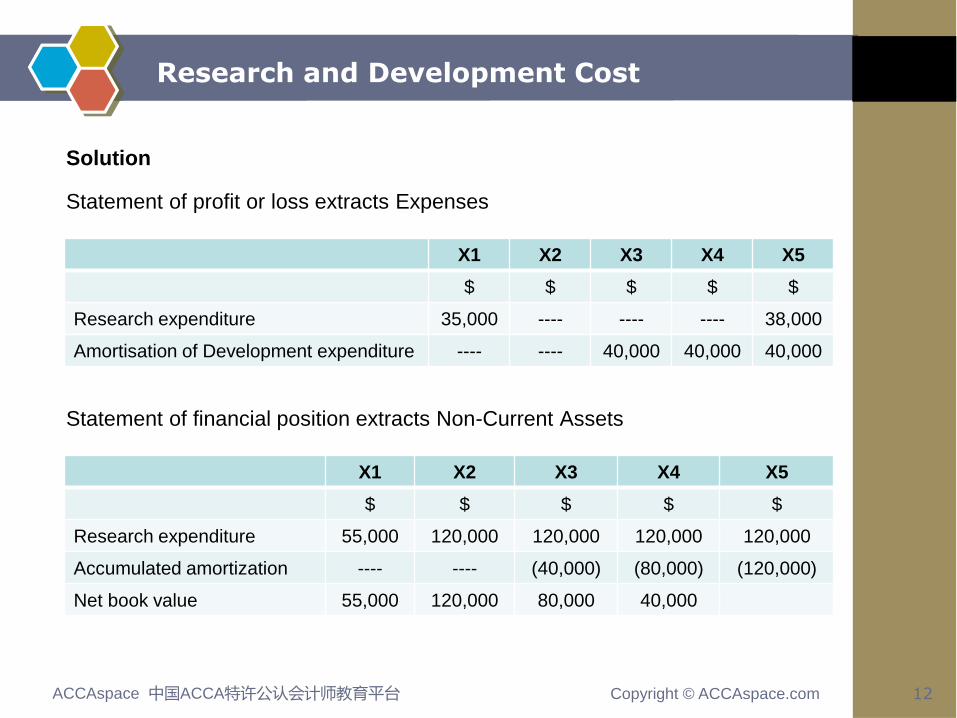

Research and Development Cost

Solution

Statement of profit or loss extracts Expenses

Statement of financial position extracts Non-Current Assets

X1 X2 X3 X4 X5

$ $ $ $ $

Research expenditure 35,000 ---- ---- ---- 38,000

Amortisation of Development expenditure ---- ---- 40,000 40,000 40,000

X1 X2 X3 X4 X5

$ $ $ $ $

Research expenditure 55,000 120,000 120,000 120,000 120,000

Accumulated amortization ---- ---- (40,000) (80,000) (120,000)

Net book value 55,000 120,000 80,000 40,000

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 13

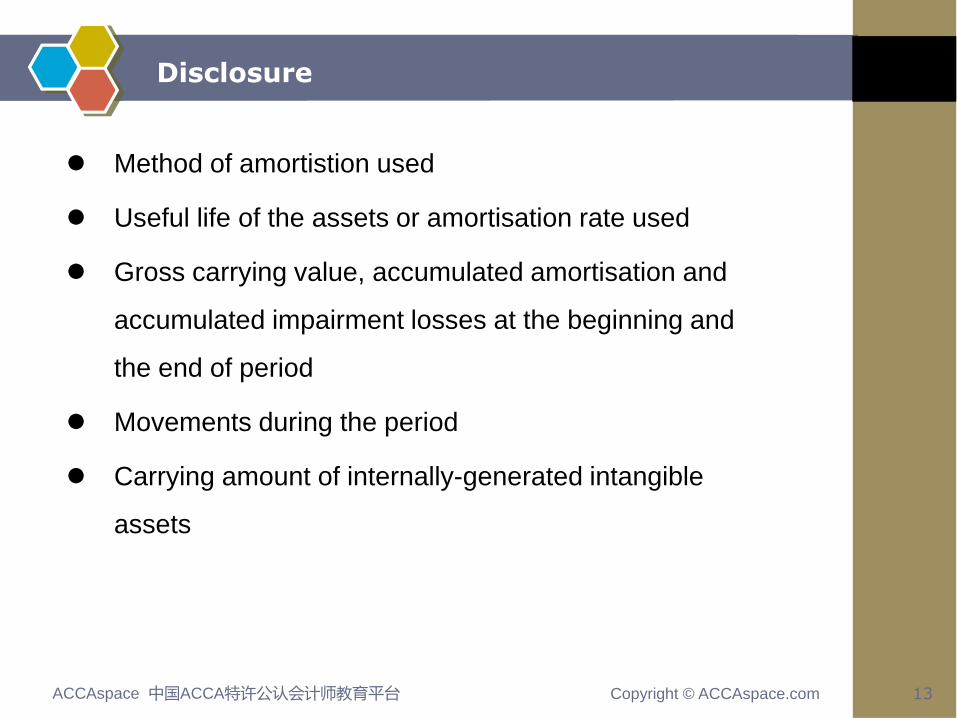

Disclosure

Method of amortistion used

Useful life of the assets or amortisation rate used

Gross carrying value, accumulated amortisation and

accumulated impairment losses at the beginning and

the end of period

Movements during the period

Carrying amount of internally-generated intangible

assets

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 14

Summary

Provided by Academy of Professional Accounting (APA)

Professional Accounting Education