Embed Size (px)

Citation preview

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 1/11

Chapter2-1

C H A P T E R 2

CONCEPTUAL FRAMEWORK FOR

FINANCIAL REPORTING

Intermediate Accounting

IFRS Edition

Presented by;

Ratna candra sari

Email:[email protected]

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 2/11

Chapter2-2

1. Describe the usefulness of a conceptual framework.

2. Describe efforts to construct a conceptual framework.

3. Understand the objective of financial reporting.

4. Identify the qualitative characteristics of accounting information.

5. Define the basic elements of financial statements.

6. Describe the basic assumptions of accounting.

7. Explain the application of the basic principles of accounting.

8. Describe the impact that constraints have on reporting

accounting information.

Learning Objectives

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 3/11

Chapter2-3

Need for a Conceptual Framework

Rule-making should build on and relate to an

established body of concepts.

Enables IASB to issue more useful and consistentpronouncements over time.

Conceptual Framework

LO 1 Describe the usefulness of a conceptual framework.

Conceptual Framework establishes the concepts

that underlie financial reporting.

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 4/11

Chapter2-4

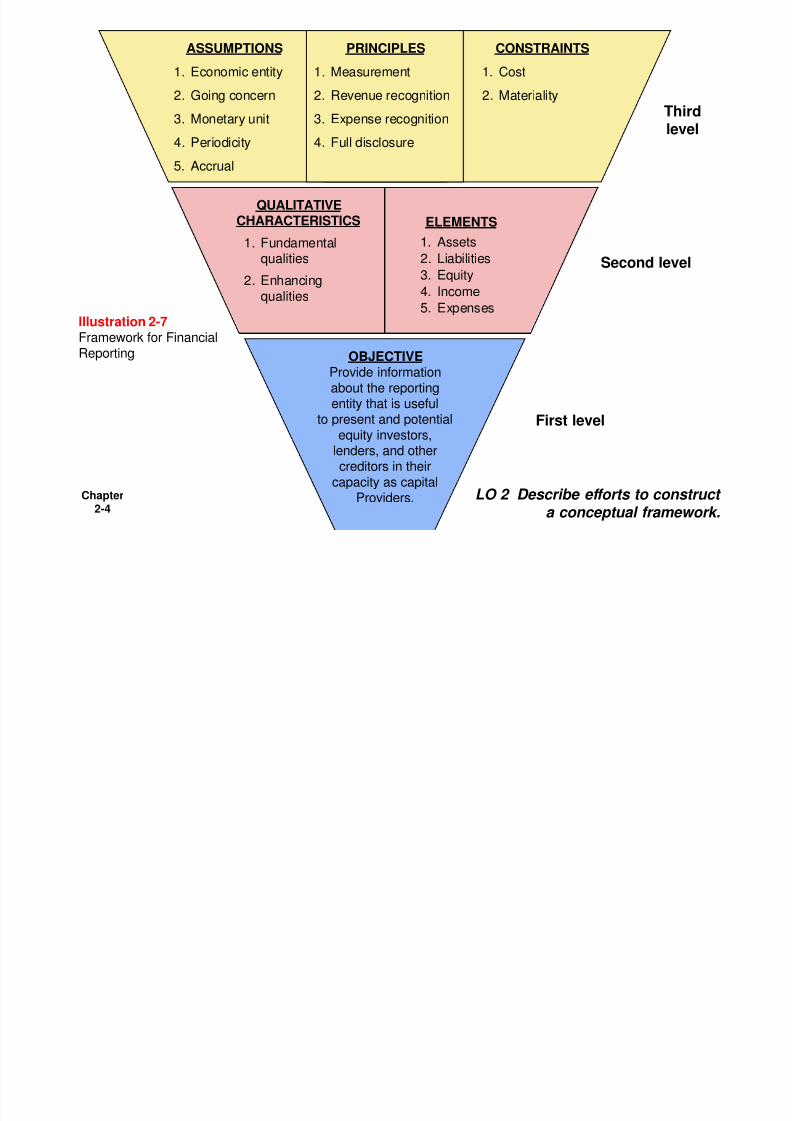

LO 2 Describe efforts to constructa conceptual framework.

ASSUMPTIONS

1. Economic entity

2. Going concern3. Monetary unit

4. Periodicity

5. Accrual

PRINCIPLES

1. Measurement

2. Revenue recognition3. Expense recognition

4. Full disclosure

CONSTRAINTS

1. Cost

2. Materiality

OBJECTIVEProvide information

about the reportingentity that is useful

to present and potentialequity investors,

lenders, and othercreditors in their

capacity as capitalProviders.

ELEMENTS

1. Assets

2. Liabilities

3. Equity

4. Income5. Expenses

Illustration 2-7Framework for FinancialReporting

First level

Second level

Thirdlevel

QUALITATIVECHARACTERISTICS

1. Fundamentalqualities

2. Enhancing

qualities

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 5/11

Chapter2-5

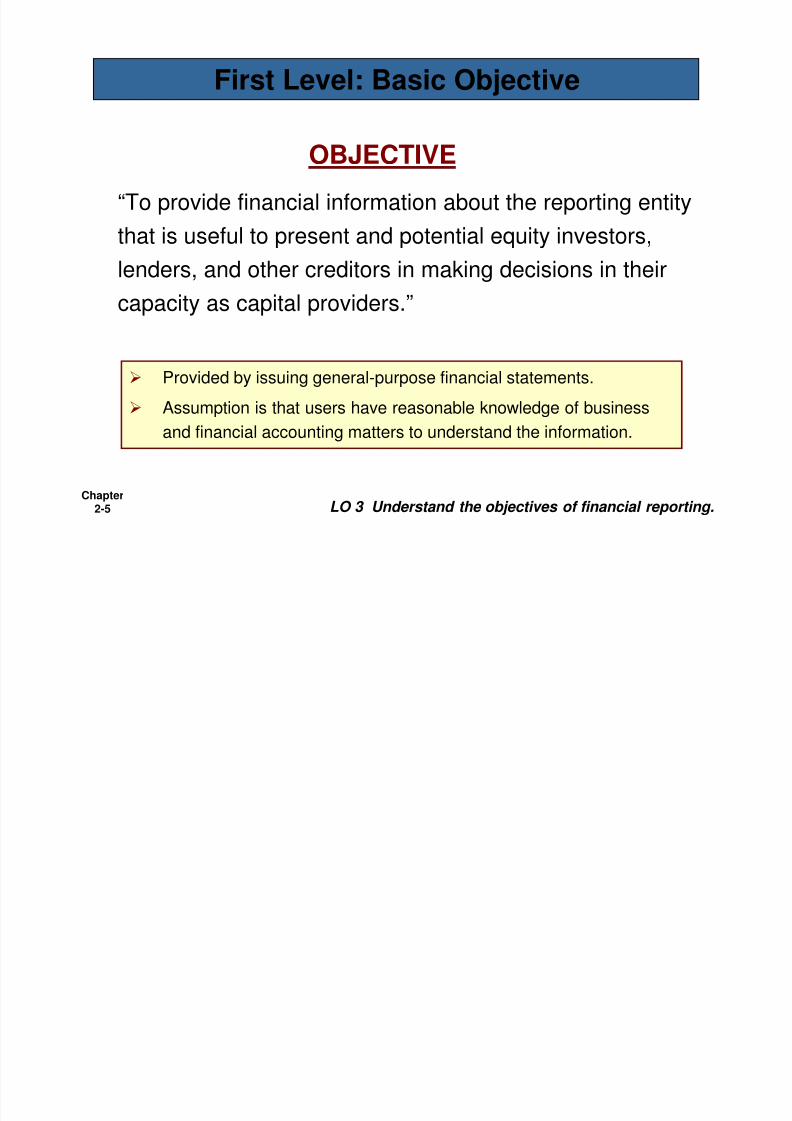

“To provide financial information about the reporting entity

that is useful to present and potential equity investors,

lenders, and other creditors in making decisions in their

capacity as capital providers.”

First Level: Basic Objective

LO 3 Understand the objectives of financial reporting.

OBJECTIVE

Provided by issuing general-purpose financial statements.

Assumption is that users have reasonable knowledge of business

and financial accounting matters to understand the information.

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 6/11

Chapter2-6

IASB identified the Qualitative Characteristics of

accounting information that distinguish better (more

useful) information from inferior (less useful)

information for decision-making purposes.

Second Level: Fundamental Concepts

LO 4 Identify the qualitative characteristics of accounting information.

Qualitative Characteristics of Accounting

Information

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 7/11

Chapter2-7

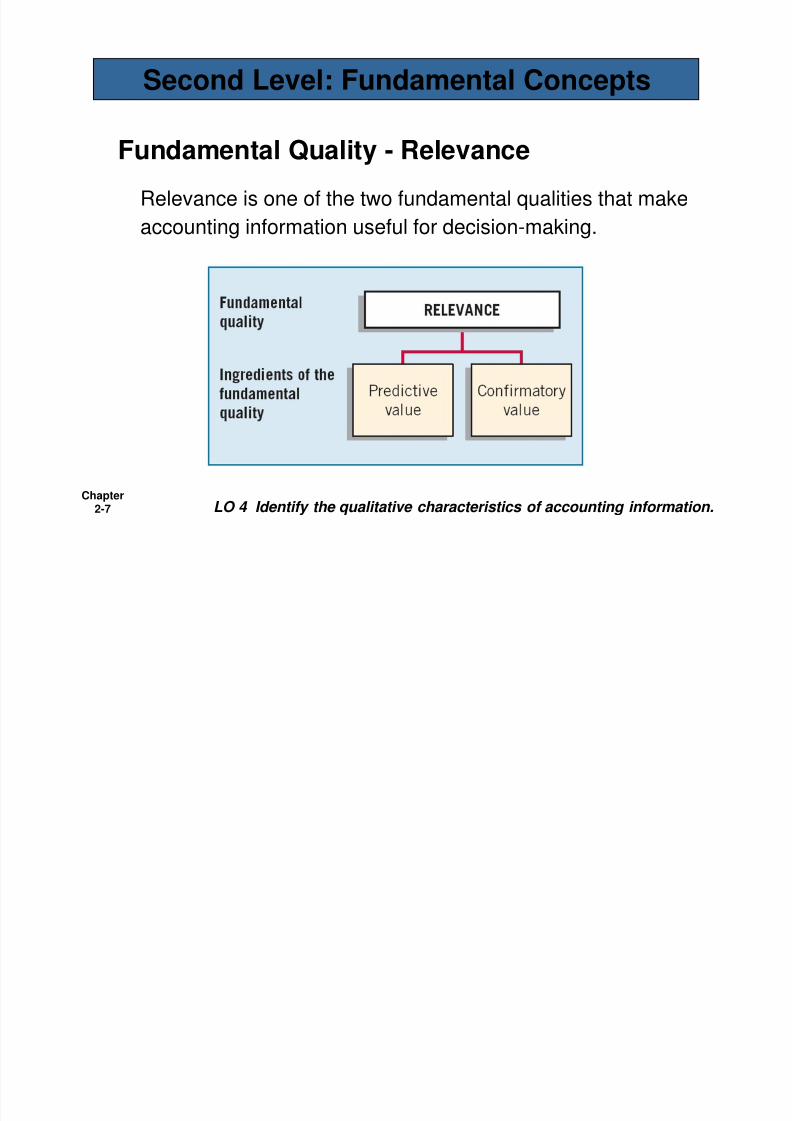

Fundamental Quality - Relevance

Relevance is one of the two fundamental qualities that makeaccounting information useful for decision-making.

Second Level: Fundamental Concepts

LO 4 Identify the qualitative characteristics of accounting information.

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 8/11

Chapter2-8

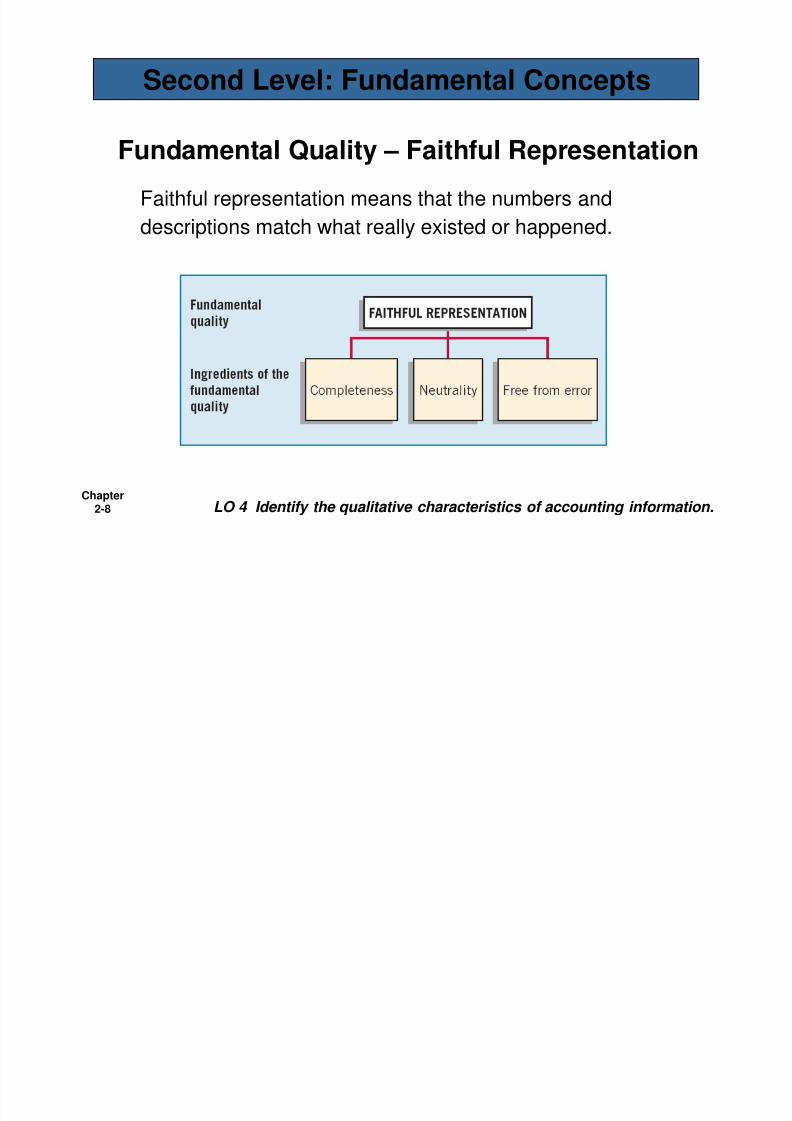

Fundamental Quality – Faithful Representation

Faithful representation means that the numbers anddescriptions match what really existed or happened.

Second Level: Fundamental Concepts

LO 4 Identify the qualitative characteristics of accounting information.

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 9/11

Chapter2-9

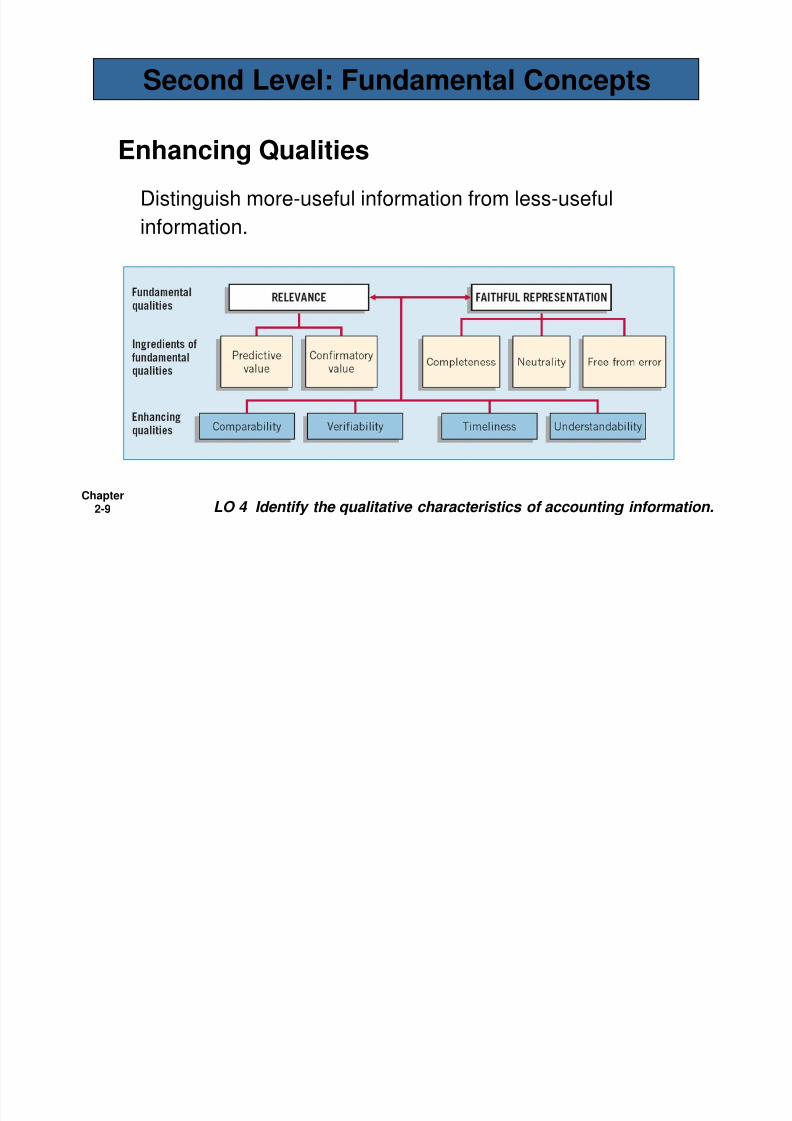

Enhancing Qualities

Distinguish more-useful information from less-usefulinformation.

Second Level: Fundamental Concepts

LO 4 Identify the qualitative characteristics of accounting information.

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 10/11

Chapter2-10

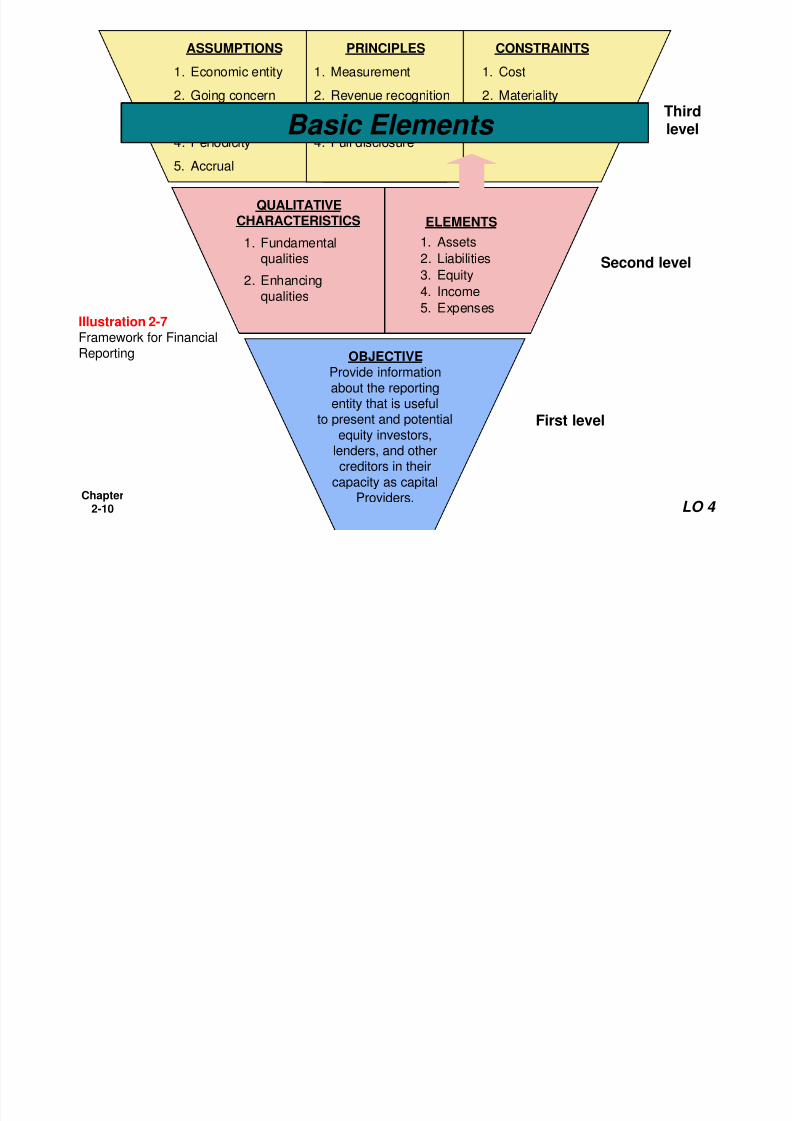

ASSUMPTIONS

1. Economic entity

2. Going concern3. Monetary unit

4. Periodicity

5. Accrual

PRINCIPLES

1. Measurement

2. Revenue recognition3. Expense recognition

4. Full disclosure

CONSTRAINTS

1. Cost

2. Materiality

OBJECTIVEProvide information

about the reportingentity that is usefulto present and potential

equity investors,lenders, and othercreditors in their

capacity as capitalProviders.

ELEMENTS

1. Assets

2. Liabilities

3. Equity

4. Income5. Expenses

Illustration 2-7Framework for FinancialReporting

First level

Second level

Thirdlevel

QUALITATIVECHARACTERISTICS

1. Fundamentalqualities

2. Enhancing

qualities

Basic Elements

LO 4

7/26/2019 AKM Ch02 Ifrs

http://slidepdf.com/reader/full/akm-ch02-ifrs 11/11

Chapter2-11

Second Level: Basic Elements

LO 5 Define the basic elements of financial statements.