Embed Size (px)

Citation preview

Prepared by Aon Benfield

A.M. Best Ratings Impact from the New Rating Methodology and Stochastic-based BCAR September 2017

1 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

Executive Summary

A.M. Best is expected to finalize new rating criteria by mid-October – This includes stochastic-based BCAR, Best’s Credit Rating Methodology (“BCRM”) and related

specialty criteria papers – Once the new criteria is adopted, all ratings will be based upon the new criteria immediately – In conjunction with the finalized criteria, A.M. Best is required to publically announce any ratings

that may be impacted as a result of the change in criteria – These ratings will be placed under review with positive, negative or developing implications; the

under review status will then be resolved over the ensuing six months

Aon Benfield proactively advising clients – We continue to be in close contact with clients likely to have rating pressure due to the new criteria – A limited number of companies may need to consider additional reinsurance purchase to bolster

capital adequacy to support their current rating prior to criteria being finalized • Unlikely to be a market moving event on its own

– Some ratings may be impacted by other components of Best’s Credit Rating Methodology (BCRM): operating performance, business profile, ERM, etc.

Feedback to A.M. Best contributed to numerous positive changes for clients – Such as eliminating of TVaR, change from aggregate to occurrence, reducing peak return period

from 1,000-yr to 250-yr, etc.

Please contact your Aon Benfield broker or Rating Agency Advisory Team members (slide 16) for any questions or assistance

2 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

Evolution of Stochastic-Based BCAR Criteria

Oct 2017

A.M. Best finalizes criteria; all rated

companies subject to new criteria as of finalization date

A.M. Best to release updated stochastic-based BCAR & BCRM

criteria

A.M. Best releases revised BCRM and issues remaining

draft criteria papers, including

terrorism and specialty insurance

companies

A.M. Best issues 13 draft criteria

papers, including new company formations and

specialty insurance

procedures

A.M. Best releases briefing discussing concern with high confidence intervals (99.8% & 99.9%); Aon Benfield’s Cat

Risk Tolerance Study highlights that 250-yr (99.6%) is the peak return period that most companies manage to

A.M. Best implements cat stress test on a post-tax basis to keep consistent

with other surplus adjustments

A.M. Best releases draft criteria outlining the new stochastic-based BCAR with 5 confidence intervals

(95% - 99.9%)

A.M. Best releases revised stochastic-based BCAR criteria removing the higher confidence

intervals and adding in the 99.6%; cat risk is added

within the covariance formula on a pre-tax basis

A.M. Best also issues first draft of Life/Health and Universal BCAR

models

End of public comment period for

revised draft stochastic-based

BCAR criteria; Aon Benfield provides feedback based upon client input

End of public comment period

for draft stochastic-based

BCAR criteria; Aon Benfield

provides feedback based

upon client input

A.M. Best announces stochastic-based BCAR

will use an updated formula (Available

Capital – Net Required Capital / Available

Capital)

Review & Preview

conference discusses developing

stochastic-based BCAR

methodology; Aggregate TVaR likely going to be used to measure

cat risk

Aon Benfield meets with A.M. Best to discuss concerns with using Aggregate TVaR to measure cat risk

A.M. Best announces use of

an all perils occurrence VaR

net PML to measure cat risk

in new stochastic-based BCAR

model webinar

March 2015

April 2015

May 2015

Oct 2015

March 2016

May 2016

June 2016

Nov 2016

March 2017

April 2017

June / July 2017

Aon Benfield provides

feedback on specialty

criteria papers

3 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

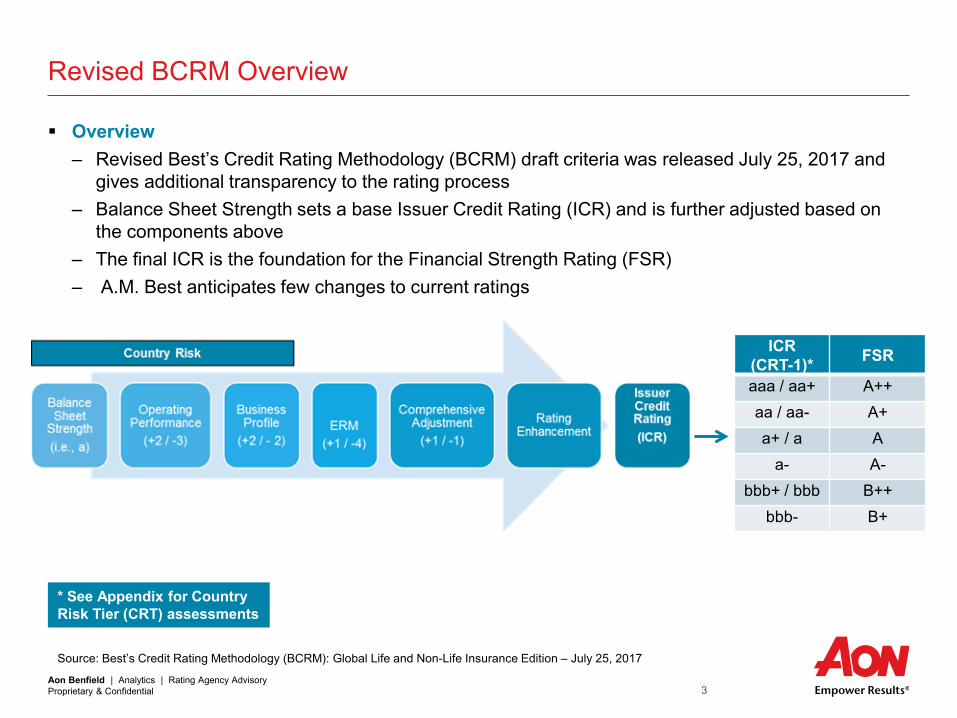

Revised BCRM Overview

Overview – Revised Best’s Credit Rating Methodology (BCRM) draft criteria was released July 25, 2017 and

gives additional transparency to the rating process – Balance Sheet Strength sets a base Issuer Credit Rating (ICR) and is further adjusted based on

the components above – The final ICR is the foundation for the Financial Strength Rating (FSR) – A.M. Best anticipates few changes to current ratings

ICR (CRT-1)* FSR

aaa / aa+ A++ aa / aa- A+ a+ / a A

a- A- bbb+ / bbb B++

bbb- B+

Source: Best’s Credit Rating Methodology (BCRM): Global Life and Non-Life Insurance Edition – July 25, 2017

* See Appendix for Country Risk Tier (CRT) assessments

4 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

How to interpret stochastic-based BCAR results? – The highest FSR a company can achieve from BCAR alone is an “A” – In order to achieve a rating above an “A” a company must demonstrate superior attributes

concerning the other risk components (e.g. operating performance, business profile, ERM, etc.)

Balance Sheet Strength

Notching from other components to achieve

FSR rating > A

Additional balance sheet strength considerations – Stress tests – Quality of reinsurance and appropriateness of reinsurance program – Financial and operating leverage – Liquidity – Quality of capital – Internal capital models

Description Proposed BCAR

ICR (CRT-1) * FSR

Strongest >25 at 99.6 a+ / a A

Very Strong >10 at 99.6 a / a- A / A-

Strong >0 at 99.5 a- / bbb+ A- / B++

Adequate >0 at 99 bbb+ / bbb / bbb- B++ / B+

Weak >0 at 95 bb+ / bb / bb- B / B-

Very Weak <0 at 95 b+ and below C++ and below

Final ICR Final FSR

aaa / aa+ A++

aa / aa- A+

a+ / a A

* See Appendix for Country Risk Tier (CRT) assessments

5 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

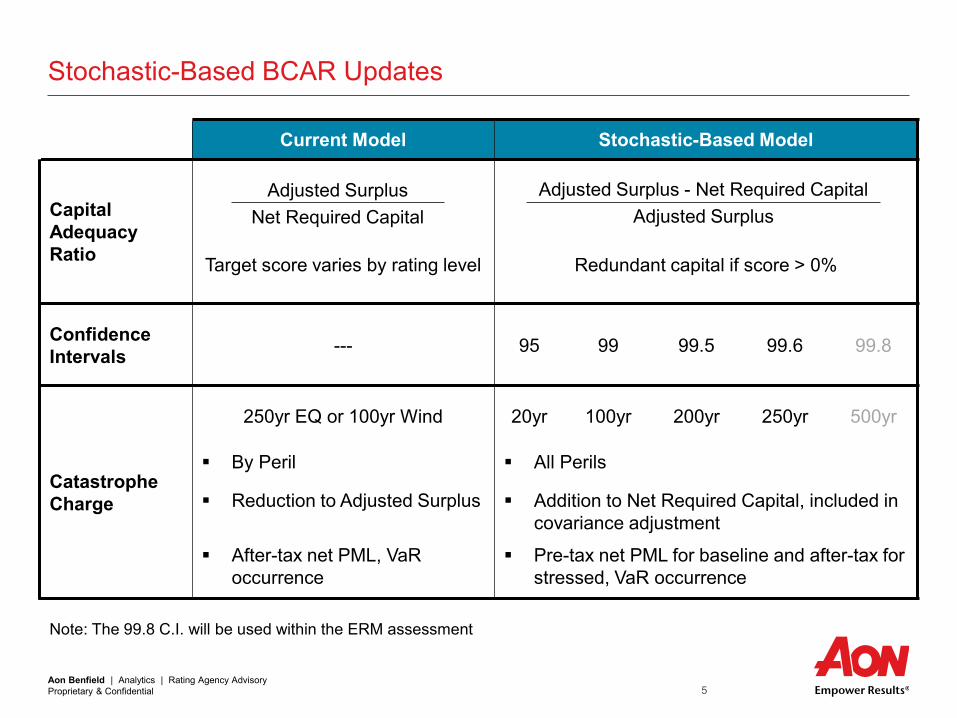

Stochastic-Based BCAR Updates

Current Model Stochastic-Based Model

Capital Adequacy Ratio

Target score varies by rating level

Redundant capital if score > 0%

Confidence Intervals --- 95 99 99.5 99.6 99.8

Catastrophe Charge

250yr EQ or 100yr Wind 20yr 100yr 200yr 250yr 500yr

By Peril All Perils

Reduction to Adjusted Surplus Addition to Net Required Capital, included in covariance adjustment

After-tax net PML, VaR occurrence

Pre-tax net PML for baseline and after-tax for stressed, VaR occurrence

Note: The 99.8 C.I. will be used within the ERM assessment

Adjusted Surplus Net Required Capital

Adjusted Surplus - Net Required Capital Adjusted Surplus

6 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

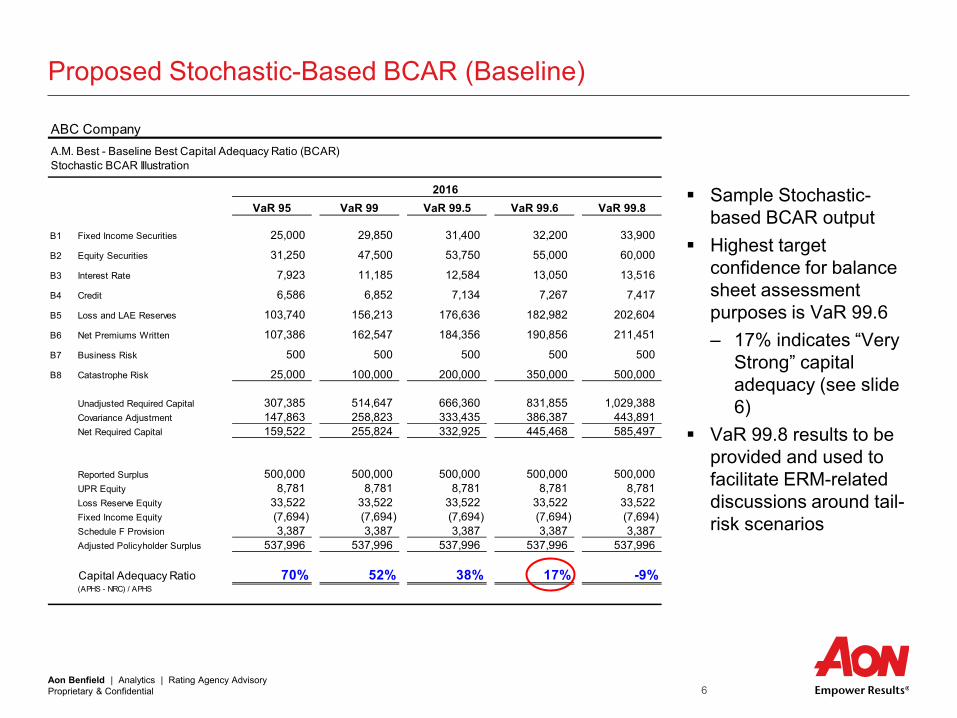

ABC CompanyA.M. Best - Baseline Best Capital Adequacy Ratio (BCAR)Stochastic BCAR Illustration

VaR 95 VaR 99 VaR 99.5 VaR 99.6 VaR 99.8

B1 Fixed Income Securities 25,000 29,850 31,400 32,200 33,900

B2 Equity Securities 31,250 47,500 53,750 55,000 60,000

B3 Interest Rate 7,923 11,185 12,584 13,050 13,516

B4 Credit 6,586 6,852 7,134 7,267 7,417

B5 Loss and LAE Reserves 103,740 156,213 176,636 182,982 202,604

B6 Net Premiums Written 107,386 162,547 184,356 190,856 211,451

B7 Business Risk 500 500 500 500 500

B8 Catastrophe Risk 25,000 100,000 200,000 350,000 500,000

Unadjusted Required Capital 307,385 514,647 666,360 831,855 1,029,388 Covariance Adjustment 147,863 258,823 333,435 386,387 443,891 Net Required Capital 159,522 255,824 332,925 445,468 585,497

Reported Surplus 500,000 500,000 500,000 500,000 500,000 UPR Equity 8,781 8,781 8,781 8,781 8,781 Loss Reserve Equity 33,522 33,522 33,522 33,522 33,522 Fixed Income Equity (7,694) (7,694) (7,694) (7,694) (7,694) Schedule F Provision 3,387 3,387 3,387 3,387 3,387 Adjusted Policyholder Surplus 537,996 537,996 537,996 537,996 537,996

Capital Adequacy Ratio 70% 52% 38% 17% -9%(APHS - NRC) / APHS

2016

Proposed Stochastic-Based BCAR (Baseline)

Sample Stochastic-based BCAR output

Highest target confidence for balance sheet assessment purposes is VaR 99.6 – 17% indicates “Very

Strong” capital adequacy (see slide 6)

VaR 99.8 results to be provided and used to facilitate ERM-related discussions around tail-risk scenarios

7 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

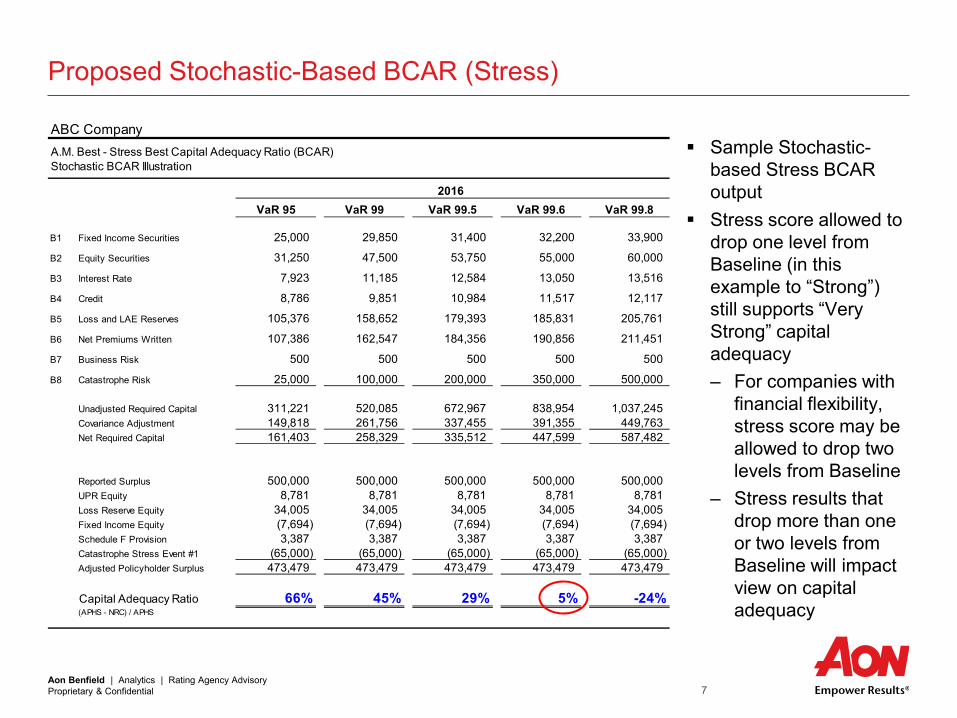

ABC CompanyA.M. Best - Stress Best Capital Adequacy Ratio (BCAR)Stochastic BCAR Illustration

VaR 95 VaR 99 VaR 99.5 VaR 99.6 VaR 99.8

B1 Fixed Income Securities 25,000 29,850 31,400 32,200 33,900

B2 Equity Securities 31,250 47,500 53,750 55,000 60,000

B3 Interest Rate 7,923 11,185 12,584 13,050 13,516

B4 Credit 8,786 9,851 10,984 11,517 12,117

B5 Loss and LAE Reserves 105,376 158,652 179,393 185,831 205,761

B6 Net Premiums Written 107,386 162,547 184,356 190,856 211,451

B7 Business Risk 500 500 500 500 500

B8 Catastrophe Risk 25,000 100,000 200,000 350,000 500,000

Unadjusted Required Capital 311,221 520,085 672,967 838,954 1,037,245 Covariance Adjustment 149,818 261,756 337,455 391,355 449,763 Net Required Capital 161,403 258,329 335,512 447,599 587,482

Reported Surplus 500,000 500,000 500,000 500,000 500,000 UPR Equity 8,781 8,781 8,781 8,781 8,781 Loss Reserve Equity 34,005 34,005 34,005 34,005 34,005 Fixed Income Equity (7,694) (7,694) (7,694) (7,694) (7,694) Schedule F Provision 3,387 3,387 3,387 3,387 3,387 Catastrophe Stress Event #1 (65,000) (65,000) (65,000) (65,000) (65,000) Adjusted Policyholder Surplus 473,479 473,479 473,479 473,479 473,479

Capital Adequacy Ratio 66% 45% 29% 5% -24%(APHS - NRC) / APHS

2016

Proposed Stochastic-Based BCAR (Stress)

Sample Stochastic-based Stress BCAR output

Stress score allowed to drop one level from Baseline (in this example to “Strong”) still supports “Very Strong” capital adequacy – For companies with

financial flexibility, stress score may be allowed to drop two levels from Baseline

– Stress results that drop more than one or two levels from Baseline will impact view on capital adequacy

8 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

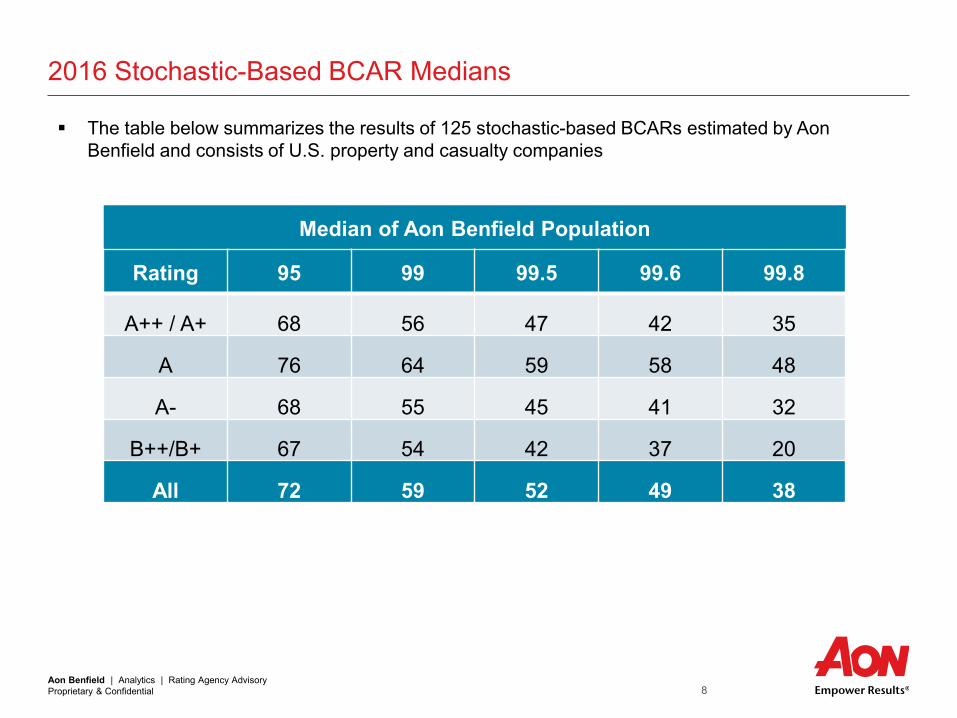

2016 Stochastic-Based BCAR Medians

The table below summarizes the results of 125 stochastic-based BCARs estimated by Aon Benfield and consists of U.S. property and casualty companies

Median of Aon Benfield Population

Rating 95 99 99.5 99.6 99.8

A++ / A+ 68 56 47 42 35

A 76 64 59 58 48

A- 68 55 45 41 32

B++/B+ 67 54 42 37 20

All 72 59 52 49 38

9 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

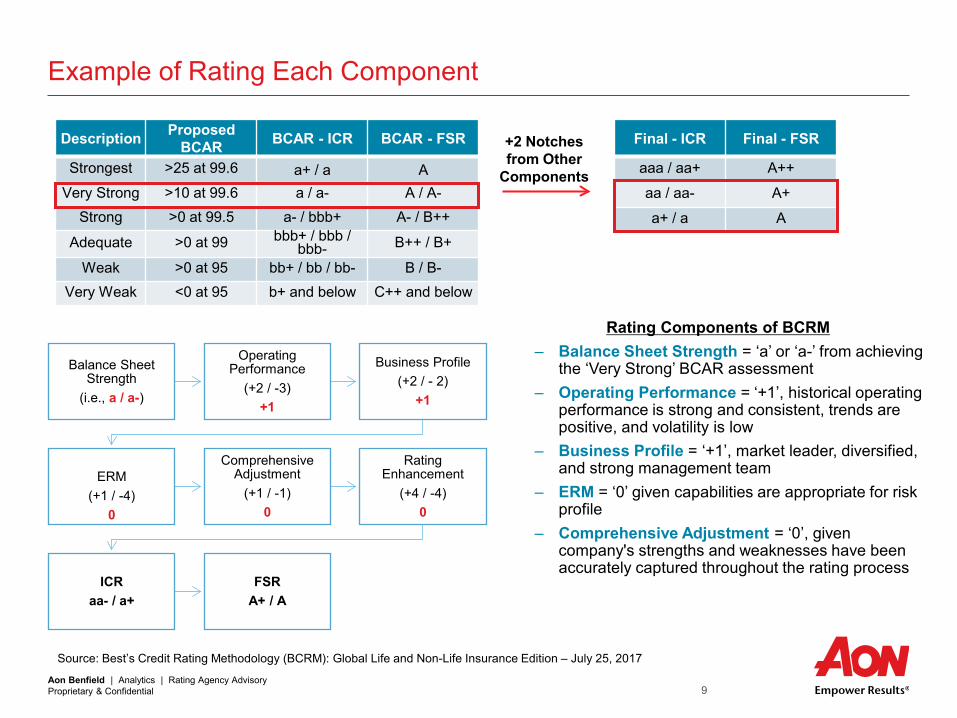

Example of Rating Each Component

Balance Sheet Strength

(i.e., a / a-)

Operating Performance

(+2 / -3) +1

Business Profile (+2 / - 2)

+1

ERM

(+1 / -4) 0

Comprehensive Adjustment

(+1 / -1) 0

Rating Enhancement

(+4 / -4) 0

ICR aa- / a+

FSR A+ / A

Description Proposed BCAR BCAR - ICR BCAR - FSR

Strongest >25 at 99.6 a+ / a A Very Strong >10 at 99.6 a / a- A / A-

Strong >0 at 99.5 a- / bbb+ A- / B++

Adequate >0 at 99 bbb+ / bbb / bbb- B++ / B+

Weak >0 at 95 bb+ / bb / bb- B / B- Very Weak <0 at 95 b+ and below C++ and below

Rating Components of BCRM – Balance Sheet Strength = ‘a’ or ‘a-’ from achieving

the ‘Very Strong’ BCAR assessment – Operating Performance = ‘+1’, historical operating

performance is strong and consistent, trends are positive, and volatility is low

– Business Profile = ‘+1’, market leader, diversified, and strong management team

– ERM = ‘0’ given capabilities are appropriate for risk profile

– Comprehensive Adjustment = ‘0’, given company's strengths and weaknesses have been accurately captured throughout the rating process

Final - ICR Final - FSR

aaa / aa+ A++ aa / aa- A+ a+ / a A

Source: Best’s Credit Rating Methodology (BCRM): Global Life and Non-Life Insurance Edition – July 25, 2017

+2 Notches from Other

Components

10 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

Appendix – Other BCRM components Operating Performance Business Profile Enterprise Risk Management (ERM) Other Adjustments Country Risk

11 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

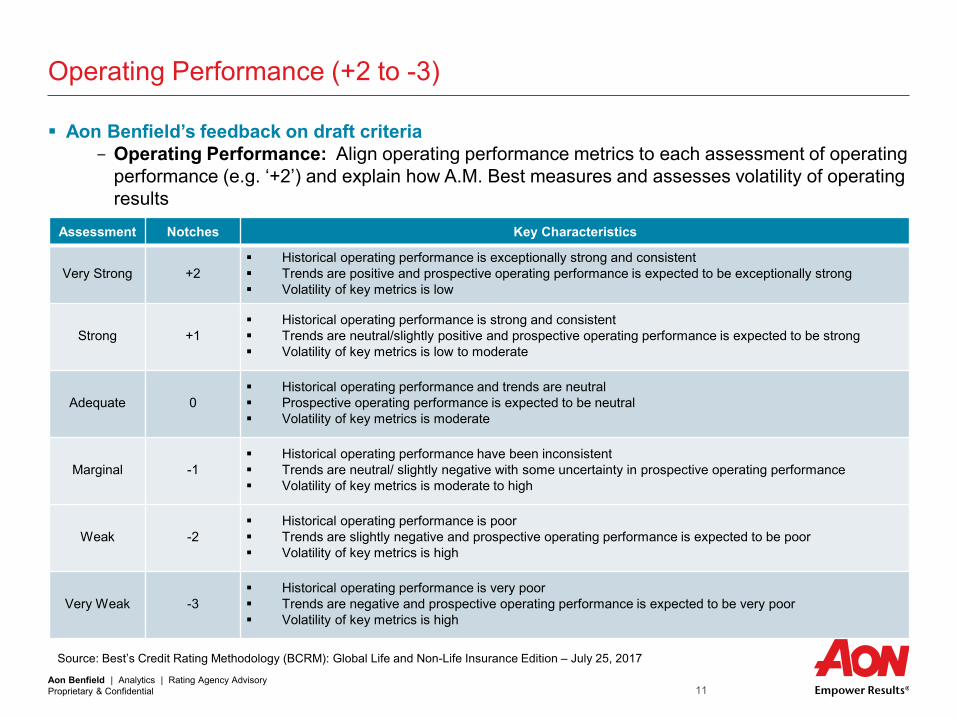

Operating Performance (+2 to -3)

Aon Benfield’s feedback on draft criteria - Operating Performance: Align operating performance metrics to each assessment of operating

performance (e.g. ‘+2’) and explain how A.M. Best measures and assesses volatility of operating results

Source: Best’s Credit Rating Methodology (BCRM): Global Life and Non-Life Insurance Edition – July 25, 2017

Assessment Notches Key Characteristics

Very Strong +2 Historical operating performance is exceptionally strong and consistent Trends are positive and prospective operating performance is expected to be exceptionally strong Volatility of key metrics is low

Strong +1 Historical operating performance is strong and consistent Trends are neutral/slightly positive and prospective operating performance is expected to be strong Volatility of key metrics is low to moderate

Adequate 0 Historical operating performance and trends are neutral Prospective operating performance is expected to be neutral Volatility of key metrics is moderate

Marginal -1 Historical operating performance have been inconsistent Trends are neutral/ slightly negative with some uncertainty in prospective operating performance Volatility of key metrics is moderate to high

Weak -2 Historical operating performance is poor Trends are slightly negative and prospective operating performance is expected to be poor Volatility of key metrics is high

Very Weak -3 Historical operating performance is very poor Trends are negative and prospective operating performance is expected to be very poor Volatility of key metrics is high

12 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

Business Profile (+2 to -2)

Source: Best’s Credit Rating Methodology (BCRM): Global Life and Non-Life Insurance Edition – July 25, 2017

Aon Benfield’s feedback on draft criteria - Business Profile: Provide additional guidance on how results from the sub-assessments of

business profile fit into the overall business profile assessment

Assessment Notches Key Characteristics

Very Favorable +2

Market leadership position is unquestionable, demonstrated, and defensible with high brand recognition Distribution is seen as a competitive advantage; Business lines are non-correlated and generally lower risk Management capabilities and data management are very strong

Favorable +1

Market leader with strong business trends Good control over distribution Diversified operations in key markets that have high to moderate barriers to entry with low competition Strong management team that is able to meet projections and utilize data effectively

Neutral 0

Not a market leader, but is viewed as competitive in chosen markets Some concentration and/or limited control of distribution Moderate product risk but limited severity and frequency of loss Use of technology is evolving and its business spread of risk is adequate

Limited -1

Lack of diversification in geographic and/or product lines Control over distribution is limited and undifferentiated Faces high/increasing competition with low barriers to entry and elevated product risk Management is unable to utilize data effectively or consistently in

business decisions

Very Limited -2 Faces high competition and low barriers to entry High concentration in commodity or higher-risk products with very limited geographic diversity Weak data management; Country risk may factor into its elevated business profile risks

13 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

Enterprise Risk Management (+1 to -4)

Source: AM Best Review Preview Conference, 2017

Assessment Notches Key Characteristics of ERM

Very Strong +1 ERM framework is sophisticated, time/stress-tested and embedded across the enterprise. Risk management capabilities are excellent and are suitable for the risk profile of the company

Adequate 0 ERM framework is well-developed and is adequate given size and complexity of its operations. Risk management capabilities are good and are adequate for the risk profile of the company

Marginal -1 ERM framework is developing; certain key elements of the framework are not yet in place or have proven inadequate given the complexity of its operations. Some risk management capabilities are not aligned with the risk profile of the company

Weak -2 ERM framework is emerging and management is still developing formal risk protocols. Risk management capabilities are insufficient given the risk profile of the company

Very Weak -3 to -4 There is limited evidence of a formal ERM framework in place. Risk management capabilities contain severe deficiencies relative to risk profile of the company

Aon Benfield’s Risk Impact Worksheet Tool

14 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

Other Adjustments

The rating enhancement impacts non-lead rating units

The comprehensive adjustment allows flexibility in adjusting the ICR for special cases

Source: Best’s Credit Rating Methodology (BCRM): Global Life and Non-Life Insurance Edition – July 25, 2017

Assessment Notches Key Characteristics

Positive +1 The company has uncommon strengths that exceed what has been captured throughout the rating process.

None 0 The company's strengths and weaknesses have been accurately captured throughout the rating process.

Negative -1 The company has uncommon weaknesses that exceed what has been captured throughout the rating process.

Enhancement Notches Key Characteristics

Typical Lift +1 to +4 The non-lead rating unit either receives explicit support from the broader organization or is deemed materially important within the broader organization as demonstrated by its level of integration.

Neutral 0 The non-lead rating unit does not have explicit support from the broader organization and is not considered materially important within the organization.

Typical Drag -1 to -4 The non-lead rating unit is negatively impacted by its association with the weaker affiliates of the broader organization.

15 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

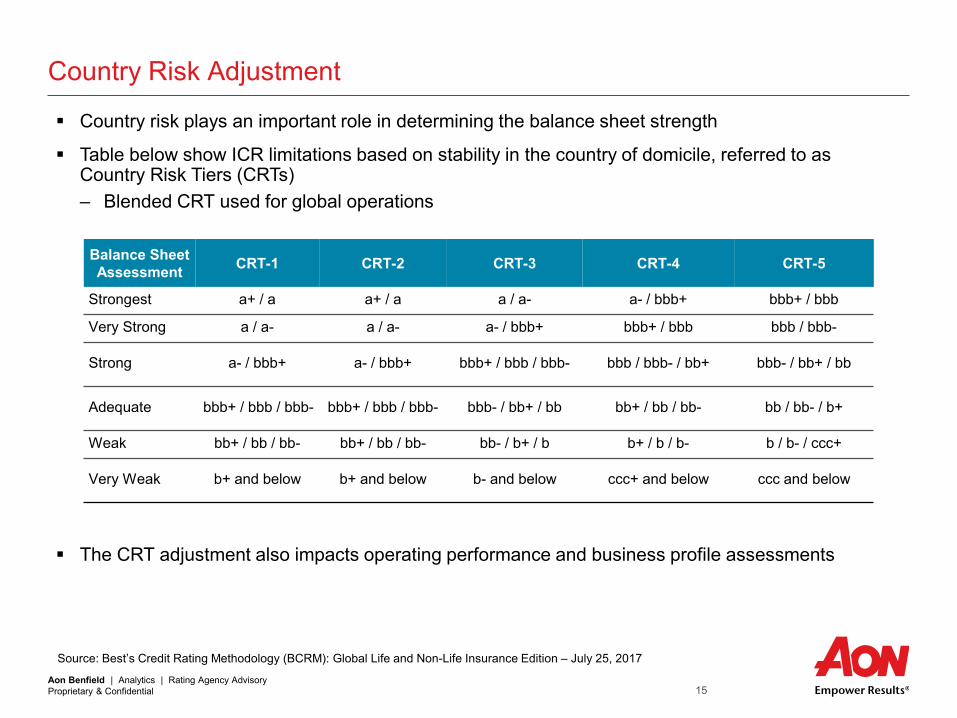

Country risk plays an important role in determining the balance sheet strength

Table below show ICR limitations based on stability in the country of domicile, referred to as Country Risk Tiers (CRTs) – Blended CRT used for global operations

The CRT adjustment also impacts operating performance and business profile assessments

Country Risk Adjustment

Balance Sheet Assessment CRT-1 CRT-2 CRT-3 CRT-4 CRT-5

Strongest a+ / a a+ / a a / a- a- / bbb+ bbb+ / bbb

Very Strong a / a- a / a- a- / bbb+ bbb+ / bbb bbb / bbb-

Strong a- / bbb+ a- / bbb+ bbb+ / bbb / bbb- bbb / bbb- / bb+ bbb- / bb+ / bb

Adequate bbb+ / bbb / bbb- bbb+ / bbb / bbb- bbb- / bb+ / bb bb+ / bb / bb- bb / bb- / b+

Weak bb+ / bb / bb- bb+ / bb / bb- bb- / b+ / b b+ / b / b- b / b- / ccc+

Very Weak b+ and below b+ and below b- and below ccc+ and below ccc and below

Source: Best’s Credit Rating Methodology (BCRM): Global Life and Non-Life Insurance Edition – July 25, 2017

16 Aon Benfield | Analytics | Rating Agency Advisory Proprietary & Confidential

Contact List

Pat Matthews Head of Rating Agency Advisory +1.215.751.1591 [email protected]

Kathleen Armstrong Managing Director, Americas +1.513.562.4508 [email protected]

Aon Benfield, a division of Aon plc (NYSE: AON), is the world‘s leading reinsurance intermediary and full-service capital advisor. We empower our clients to better understand, manage and transfer risk through innovative solutions and personalized access to all forms of global reinsurance capital across treaty, facultative and capital markets. As a trusted advocate, we deliver local reach to the world‘s markets, an unparalleled investment in innovative analytics, including catastrophe management, actuarial and rating agency advisory. Through our professionals’ expertise and experience, we advise clients in making optimal capital choices that will empower results and improve operational effectiveness for their business. With more than 80 offices in 50 countries, our worldwide client base has access to the broadest portfolio of integrated capital solutions and services. To learn how Aon Benfield helps empower results, please visit aonbenfield.com.

© Aon Benfield 2017. All rights reserved. This document is intended for general information purposes only and should not be construed as advice or opinions on any specific facts or circumstances. This analysis is based upon information from sources we consider to be reliable, however Aon Benfield does not warrant the accuracy of the data herein. The content of this document is made available on an “as is” basis, without warranty of any kind. Aon Benfield disclaims any legal liability to any person or organization for loss or damage caused by or resulting from any reliance placed on that content. Members of the Aon Benfield Analytics team will be pleased to consult on any specific situations and to provide further information regarding the matters discussed herein.

Sifang Zhang APAC Head of Rating Agency Advisory +852.2861.6493 [email protected]

Kelly Superczynski Head of EMEA Analytics +44 (0) 20 7086 2175 [email protected]

Raymond Lui Canada and Caribbean Rating Agency Advisory +1.416.598.7320 [email protected]