Embed Size (px)

Citation preview

Annual Report for

AmBalanced31 July 2019

AmBalanced

TRUST DIRECTORY

Manager AmFunds Management Berhad

9th&10th Floor, Bangunan AmBank Group 55 Jalan Raja Chulan 50200 Kuala Lumpur

Board of Directors Jeyaratnam A/L Tamotharam Pillai

Dato’ Mustafa Bin Mohd Nor Tai Terk Lin

Sum Leng Kuang Seohan Soo

Goh Wee Peng

Investment Committee Sum Leng Kuang

Tai Terk Lin Dato’ Mustafa Bin Mohd Nor

Zainal Abidin Bin Mohd Kassim Goh Wee Peng

Trustee HSBC (Malaysia) Trustee Berhad

Auditors and Reporting Accountants Ernst & Young

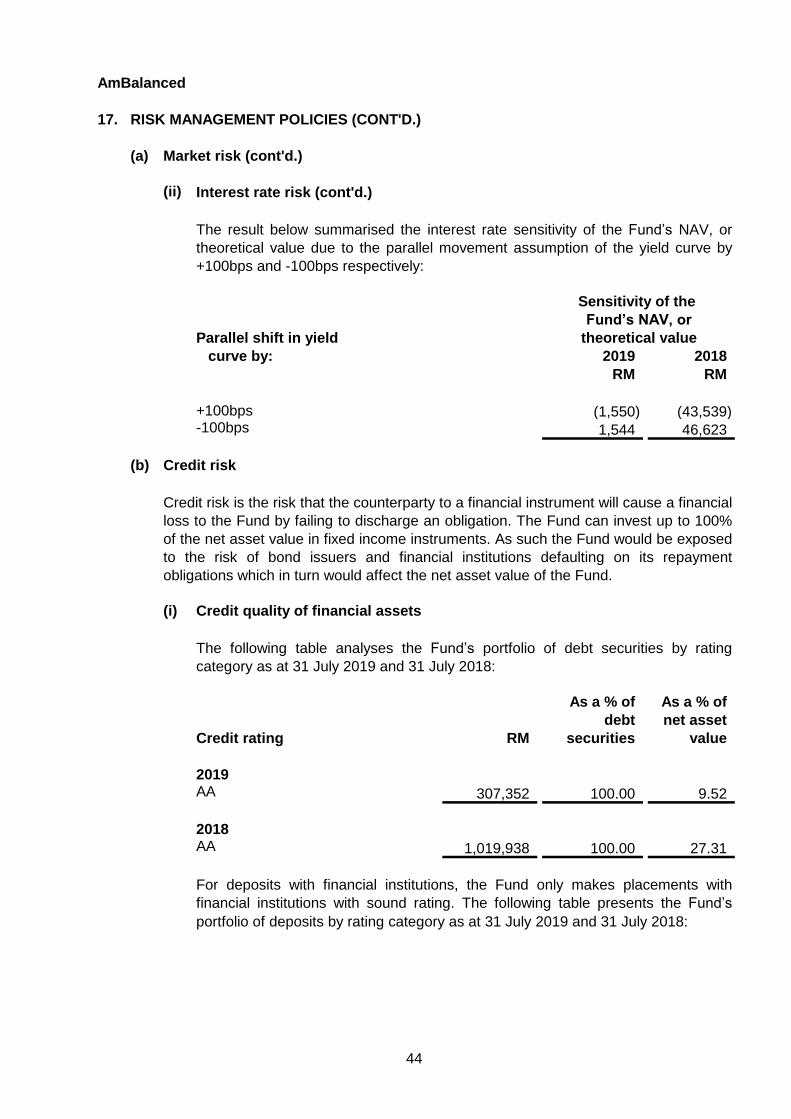

Taxation Adviser Deloitte Tax Services Sdn Bhd

AmBalanced

CONTENTS

1 Manager’s Report

10 Independent Auditor’s Report to the Unitholders

14 Statement of Financial Position

15 Statement of Comprehensive Income

16 Statement of Changes in Equity

17 Statement of Cash Flows

18 Notes to the Financial Statements

48 Statement by the Manager

49 Trustee’s Report

50 Directory

1

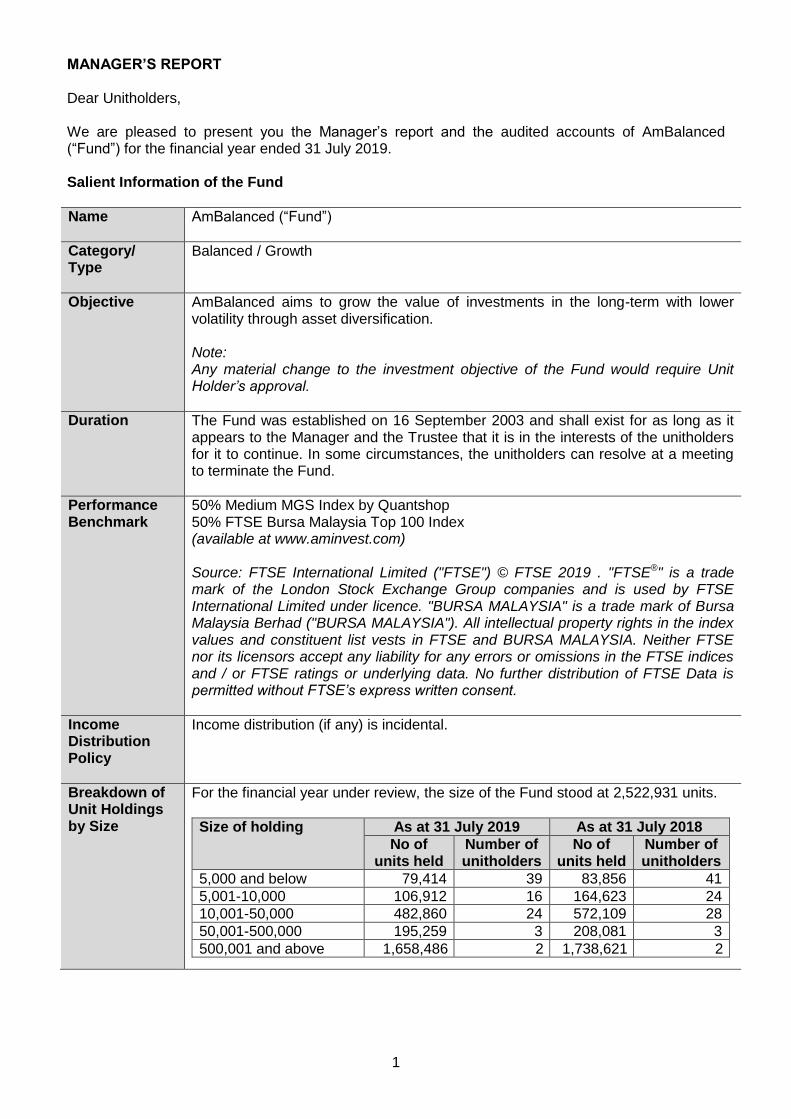

MANAGER’S REPORT

Dear Unitholders,

We are pleased to present you the Manager’s report and the audited accounts of AmBalanced (“Fund”) for the financial year ended 31 July 2019.

Salient Information of the Fund

Name AmBalanced (“Fund”)

Category/ Type

Balanced / Growth

Objective AmBalanced aims to grow the value of investments in the long-term with lower volatility through asset diversification.

Note: Any material change to the investment objective of the Fund would require Unit Holder’s approval.

Duration The Fund was established on 16 September 2003 and shall exist for as long as it appears to the Manager and the Trustee that it is in the interests of the unitholders for it to continue. In some circumstances, the unitholders can resolve at a meeting to terminate the Fund.

Performance Benchmark

50% Medium MGS Index by Quantshop 50% FTSE Bursa Malaysia Top 100 Index (available at www.aminvest.com)

Source: FTSE International Limited ("FTSE") © FTSE 2019 . "FTSE®" is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under licence. "BURSA MALAYSIA" is a trade mark of Bursa Malaysia Berhad ("BURSA MALAYSIA"). All intellectual property rights in the index values and constituent list vests in FTSE and BURSA MALAYSIA. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and / or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent.

Income Distribution Policy

Income distribution (if any) is incidental.

Breakdown of Unit Holdings by Size

For the financial year under review, the size of the Fund stood at 2,522,931 units.

Size of holding As at 31 July 2019 As at 31 July 2018

No of units held

Number of unitholders

No of units held

Number of unitholders

5,000 and below 79,414 39 83,856 41

5,001-10,000 106,912 16 164,623 24

10,001-50,000 482,860 24 572,109 28

50,001-500,000 195,259 3 208,081 3

500,001 and above 1,658,486 2 1,738,621 2

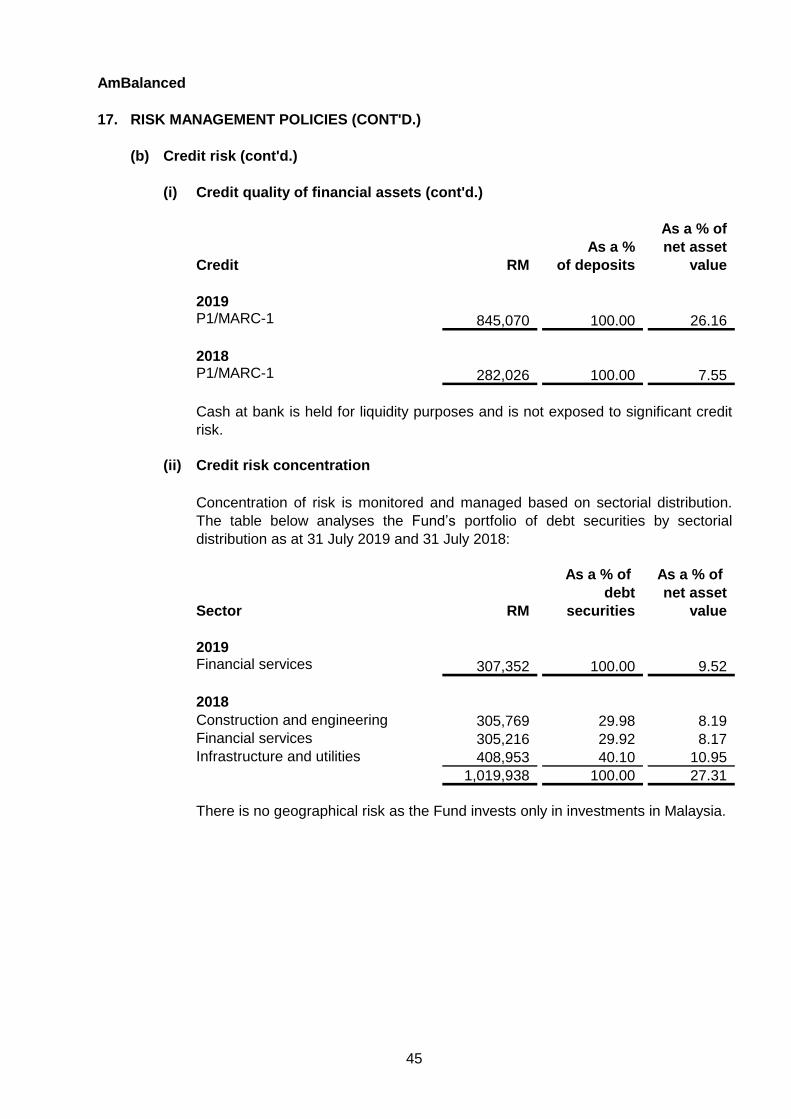

2

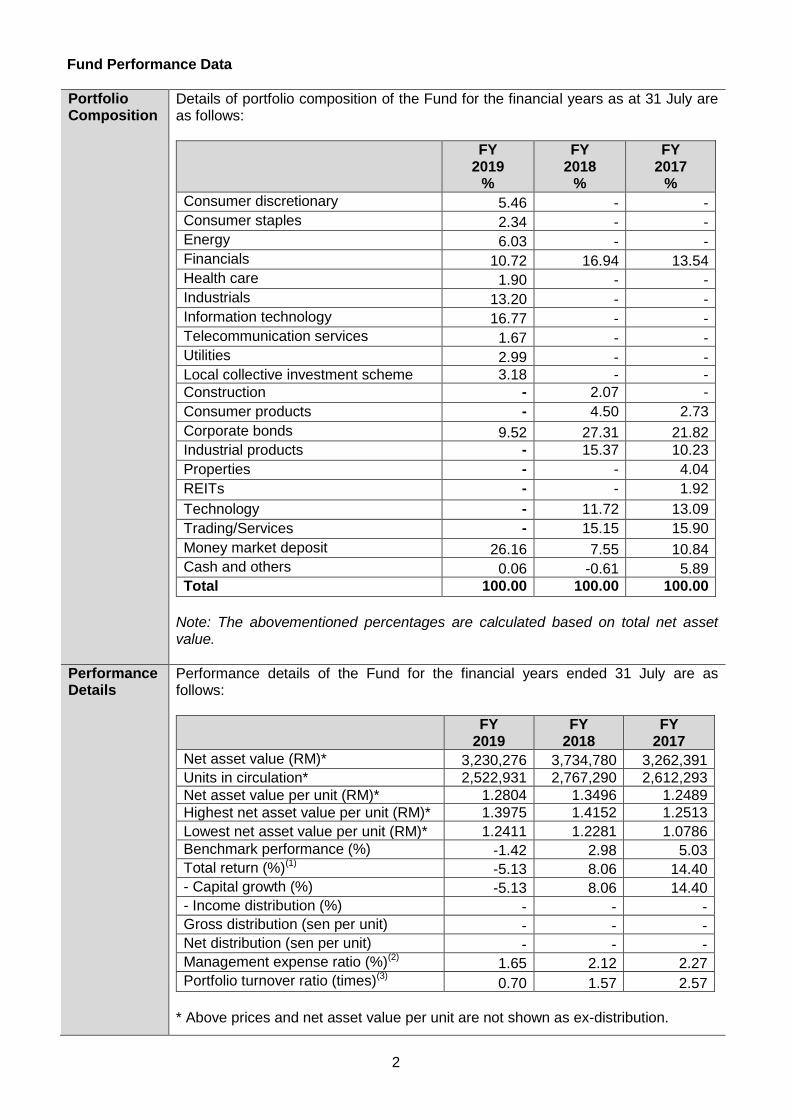

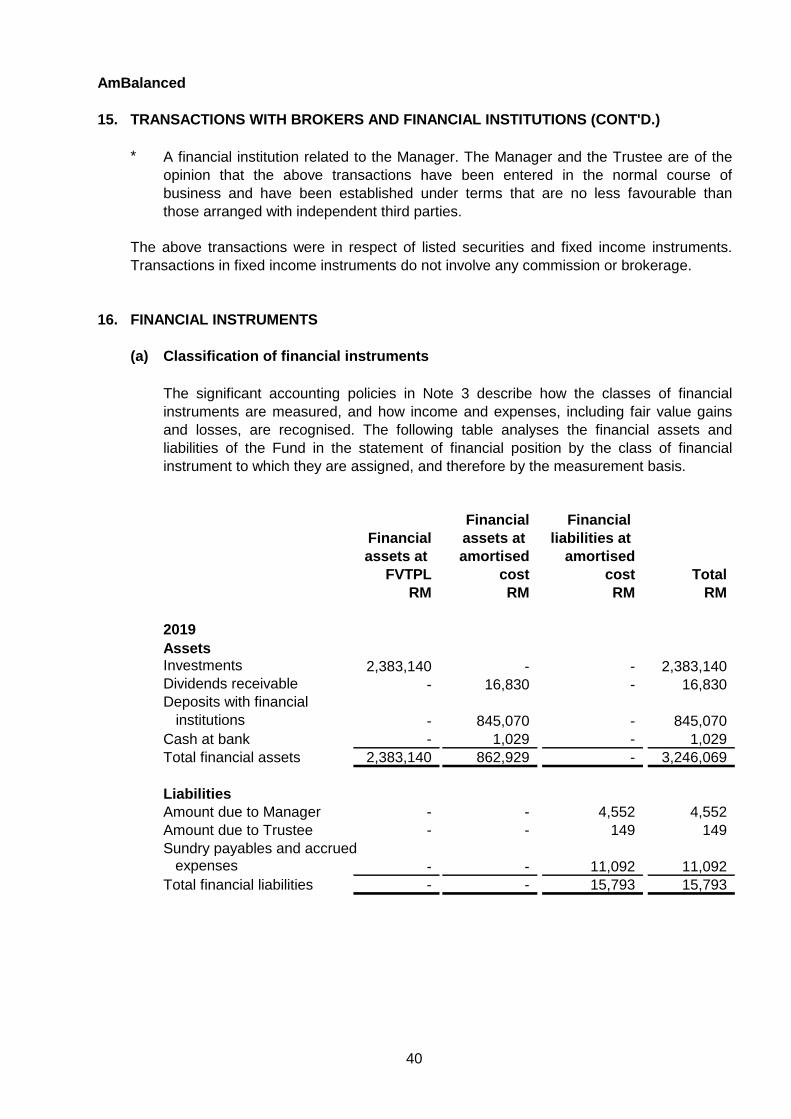

Fund Performance Data

Portfolio Composition

Details of portfolio composition of the Fund for the financial years as at 31 July are as follows:

FY 2019

%

FY 2018

%

FY 2017

%

Consumer discretionary 5.46 - -

Consumer staples 2.34 - -

Energy 6.03 - -

Financials 10.72 16.94 13.54

Health care 1.90 - -

Industrials 13.20 - -

Information technology 16.77 - -

Telecommunication services 1.67 - -

Utilities 2.99 - -

Local collective investment scheme 3.18 - -

Construction - 2.07 -

Consumer products - 4.50 2.73

Corporate bonds 9.52 27.31 21.82

Industrial products - 15.37 10.23

Properties - - 4.04

REITs - - 1.92

Technology - 11.72 13.09

Trading/Services - 15.15 15.90

Money market deposit 26.16 7.55 10.84

Cash and others 0.06 -0.61 5.89

Total 100.00 100.00 100.00

Note: The abovementioned percentages are calculated based on total net asset value.

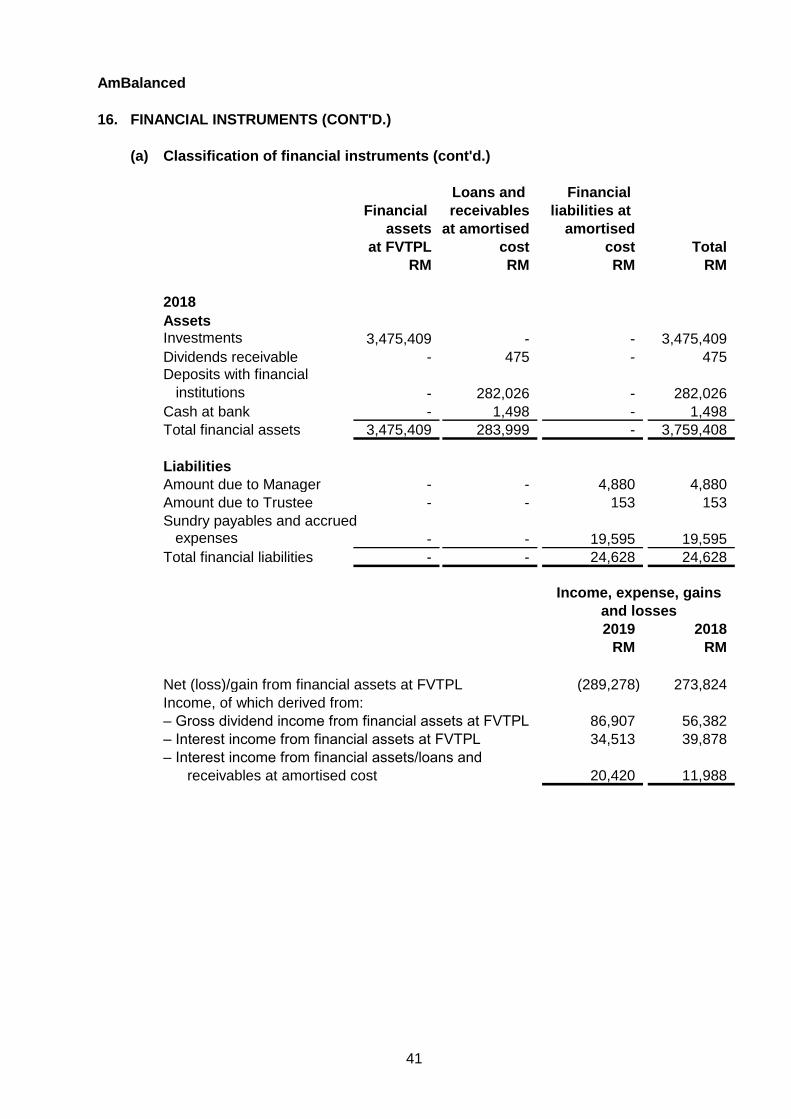

Performance Details

Performance details of the Fund for the financial years ended 31 July are as follows:

FY 2019

FY 2018

FY 2017

Net asset value (RM)* 3,230,276 3,734,780 3,262,391

Units in circulation* 2,522,931 2,767,290 2,612,293

Net asset value per unit (RM)* 1.2804 1.3496 1.2489

Highest net asset value per unit (RM)* 1.3975 1.4152 1.2513

Lowest net asset value per unit (RM)* 1.2411 1.2281 1.0786

Benchmark performance (%) -1.42 2.98 5.03

Total return (%)(1) -5.13 8.06 14.40

- Capital growth (%) -5.13 8.06 14.40

- Income distribution (%) - - -

Gross distribution (sen per unit) - - -

Net distribution (sen per unit) - - -

Management expense ratio (%)(2) 1.65 2.12 2.27

Portfolio turnover ratio (times)(3) 0.70 1.57 2.57

* Above prices and net asset value per unit are not shown as ex-distribution.

3

Note: (1) Total return is the annualised return of the Fund for the respective financial

years computed based on the net asset value per unit and net of all fees.(2) Management expense ratio (“MER”) is calculated based on the total fees and

expenses incurred by the Fund divided by the average fund size calculated on adaily basis. The MER decreased by 0.47% as compared to 2.12% per annumfor the financial year ended 31 July 2018 mainly due to decrease in expenses.

(3) Portfolio turnover ratio (“PTR”) is calculated based on the average of the totalacquisitions and total disposals of investment securities of the Fund divided bythe average fund size calculated on a daily basis. The PTR decreased by 0.87times (55.4%) as compared to 1.57 times for the financial year ended 31 July2018 mainly due to decrease in investing activities.

Average Total Return (as at 31 July 2019)

AmBalanced(a) %

50% FBM Top100 & 50% MMGS(b)

%

One year -5.13 -1.42

Three years 5.46 2.16

Five years 2.15 1.18

Ten years 6.19 4.09

Annual Total Return

Financial Years Ended (31 July) AmBalanced(a)

%

50% FBM Top 100 & 50% MMGS(b)

%

2019 -5.13 -1.42

2018 8.06 2.98

2017 14.40 5.03

2016 -1.71 2.06

2015 -3.51 -2.28

(a) Source: Novagni Analytics and Advisory Sdn Bhd.(b) 50% FTSE Bursa Malaysia Top 100 Index (FBM Top 100) and 50% Medium

MMGS Index (available at www.aminvest.com)

The Fund performance is calculated based on the net asset value per unit of the Fund. Average total return of the Fund and its benchmark for a period is computed based on the absolute return for that period annualised over one year.

Note: Past performance is not necessarily indicative of future performance and that unit prices and investment returns may go down, as well as up.

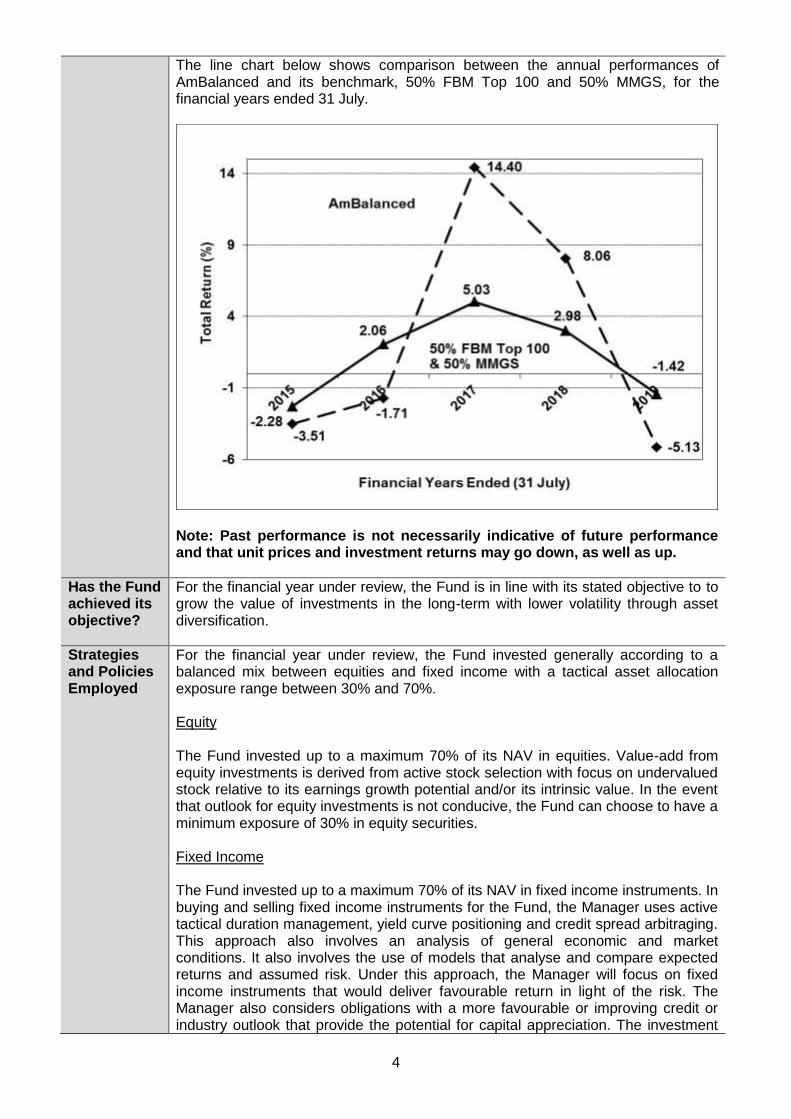

Fund Performance

For the financial year under review, the Fund registered a negative return of 5.13% which was entirely capital in nature.

Thus, the Fund’s negative return of 5.13% has underperformed the benchmark’s negative return of 1.42% by 3.17%.

As compared with the financial year ended 31 July 2018, the net asset value (“NAV”) per unit of the Fund decreased by 5.13% from RM1.3496 to RM1.2804 while units in circulation have decreased by 8.83% from 2,767,290 units to 2,522,931 units.

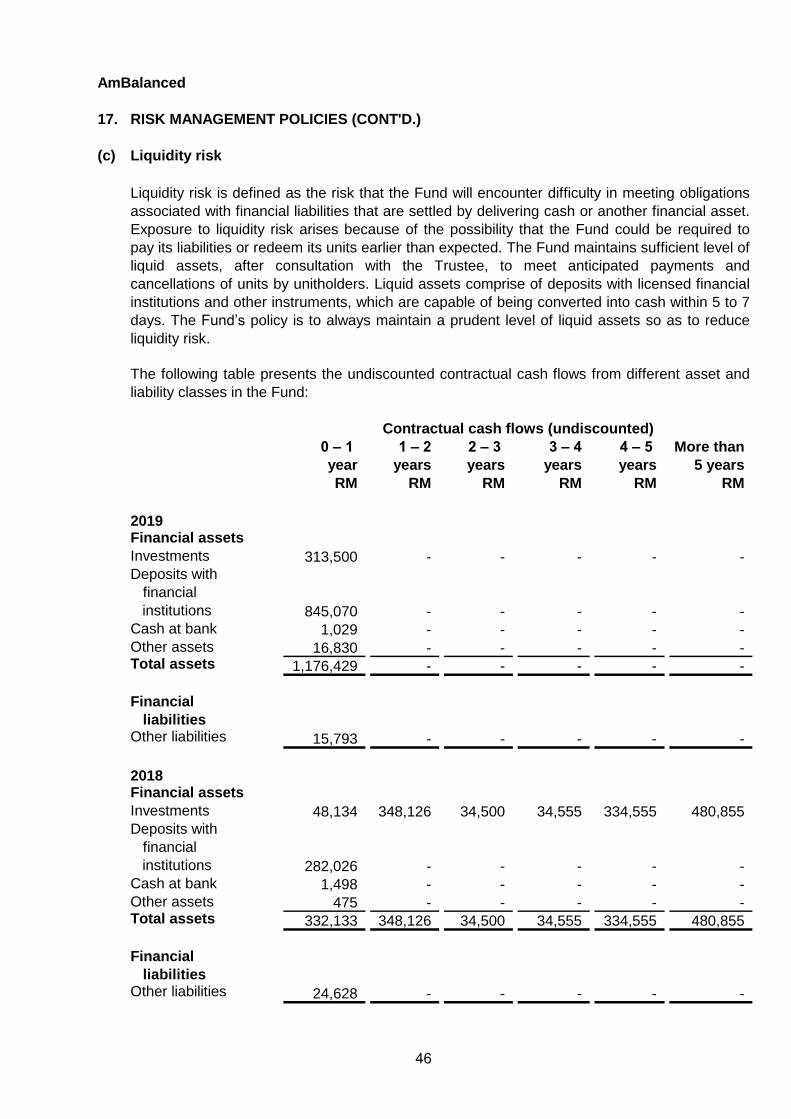

4

The line chart below shows comparison between the annual performances of AmBalanced and its benchmark, 50% FBM Top 100 and 50% MMGS, for the financial years ended 31 July.

Note: Past performance is not necessarily indicative of future performance and that unit prices and investment returns may go down, as well as up.

Has the Fund achieved its objective?

For the financial year under review, the Fund is in line with its stated objective to to grow the value of investments in the long-term with lower volatility through asset diversification.

Strategies and Policies Employed

For the financial year under review, the Fund invested generally according to a balanced mix between equities and fixed income with a tactical asset allocation exposure range between 30% and 70%.

Equity

The Fund invested up to a maximum 70% of its NAV in equities. Value-add from equity investments is derived from active stock selection with focus on undervalued stock relative to its earnings growth potential and/or its intrinsic value. In the event that outlook for equity investments is not conducive, the Fund can choose to have a minimum exposure of 30% in equity securities.

Fixed Income

The Fund invested up to a maximum 70% of its NAV in fixed income instruments. In buying and selling fixed income instruments for the Fund, the Manager uses active tactical duration management, yield curve positioning and credit spread arbitraging. This approach also involves an analysis of general economic and market conditions. It also involves the use of models that analyse and compare expected returns and assumed risk. Under this approach, the Manager will focus on fixed income instruments that would deliver favourable return in light of the risk. The Manager also considers obligations with a more favourable or improving credit or industry outlook that provide the potential for capital appreciation. The investment

5

management team may adopt an active trading stance, and will not consider portfolio turnover as a limiting factor in ensuring that the Fund meets its investment objective.

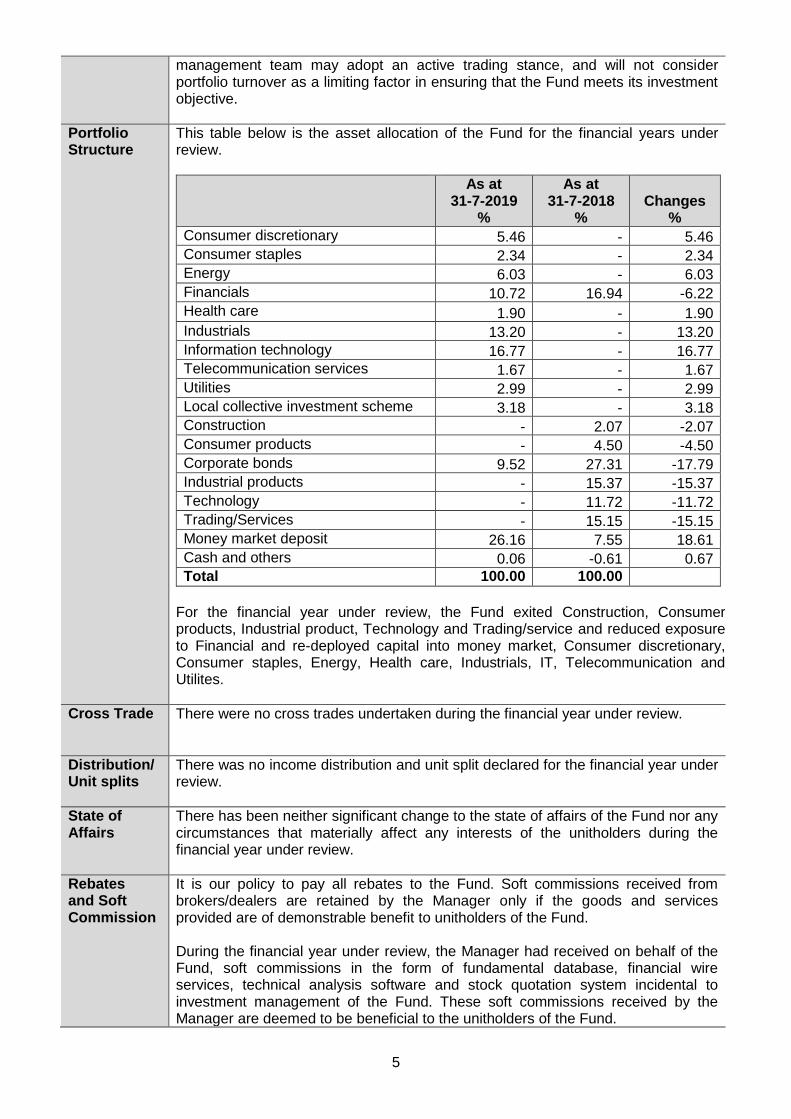

Portfolio Structure

This table below is the asset allocation of the Fund for the financial years under review.

As at 31-7-2019

%

As at 31-7-2018

%

Changes

%

Consumer discretionary 5.46 - 5.46

Consumer staples 2.34 - 2.34

Energy 6.03 - 6.03

Financials 10.72 16.94 -6.22

Health care 1.90 - 1.90

Industrials 13.20 - 13.20

Information technology 16.77 - 16.77

Telecommunication services 1.67 - 1.67

Utilities 2.99 - 2.99

Local collective investment scheme 3.18 - 3.18

Construction - 2.07 -2.07

Consumer products - 4.50 -4.50

Corporate bonds 9.52 27.31 -17.79

Industrial products - 15.37 -15.37

Technology - 11.72 -11.72

Trading/Services - 15.15 -15.15

Money market deposit 26.16 7.55 18.61

Cash and others 0.06 -0.61 0.67

Total 100.00 100.00

For the financial year under review, the Fund exited Construction, Consumer products, Industrial product, Technology and Trading/service and reduced exposure to Financial and re-deployed capital into money market, Consumer discretionary, Consumer staples, Energy, Health care, Industrials, IT, Telecommunication and Utilites.

Cross Trade

There were no cross trades undertaken during the financial year under review.

Distribution/ Unit splits

There was no income distribution and unit split declared for the financial year under review.

State of Affairs

There has been neither significant change to the state of affairs of the Fund nor any circumstances that materially affect any interests of the unitholders during the financial year under review.

Rebates and Soft Commission

It is our policy to pay all rebates to the Fund. Soft commissions received from brokers/dealers are retained by the Manager only if the goods and services provided are of demonstrable benefit to unitholders of the Fund. During the financial year under review, the Manager had received on behalf of the Fund, soft commissions in the form of fundamental database, financial wire services, technical analysis software and stock quotation system incidental to investment management of the Fund. These soft commissions received by the Manager are deemed to be beneficial to the unitholders of the Fund.

6

Market Review

The KLCI is up 2% m.o.m. Although KLCI seemed strong, it was not broad-based. FBM Mid 70 Index and FBM Small Cap Index actually declined 2.5% and 2.2% m.o.m respectively. KLCI’s outperformance was driven mainly by the Finance sector, up 3.1% m.o.m. Construction and Properties were the worst performing sector, declined 5.8% and 4.7% m.o.m respectively. Sentiment for Construction sector turned bearish after Prime Minister (PM) Mahathir announced the cancellation of the East Coast Rail Link project after his visit to Beijing. He further highlighted that fixing the country’s finances remains the key priority of the government. Government’s finance was weakened especially after Finance Minister Lim revealed that total tax refund (GST and income tax) owed by Government amounted to MYR35.4b. Foreigners net selling dropped to near zero in August 2018 (July: - MYR1.7b). Year To Date (YTD) foreign outflow was unchanged at MYR8.5b. For the month of September, KLCI was down 4.7% m.o.m, in tandem with the global equity market rout. This was mainly driven by US Treasury 10Y yields surging to 3.18% in early October. Bursa Malaysia Small Cap Index was worst hit down by 11.4%% m.o.m, followed by FBM70 that tumbled 9.3% m.o.m. Sector wise, construction and telecommunication were the worst performing sectors, declined by 15.9% and 14.2% m.o.m. respectively. In October, foreign outflows resumed with MYR1.5b outflow. The KLCI was down 1.6% m.o.m. Bursa Malaysia Small Cap Index was worst hit, down by 4.4% m.o.m. Sector wise, energy, plantation and technologies were the worst performing sectors, declined by 12.8%, 6.8% and 6.8% m.o.m respectively. In November, foreign outflows slowed down to MYR700m, bringing YTD foreign outflows to MYR10.7b. The oil and gas sector was affected by the sold down as Brent crude oil price tumbled 22% m.o.m to close at USD59/bbl. The plantation sector was also down as Crude Palm Oil (CPO) price plunged 12.8% m.o.m. to MYR1,762/mt. Technology stocks were sold down in tandem with the drop in Apple share price arising from the concern of lower than expected iPhone sales. Genting Malaysia was hit by the unexpected steep 10% increase in casino duties to 35% during the 2019 Budget announcement. The KLCI was up 0.6% m.o.m, bucking the global equities downtrend. Global market was in a bearish mode, as most were in fear of the yield curve inversion, a critical indicator of an imminent recession and a steep market correction. The United States (US) 10Y-2Y yield curve has narrowed to its lowest since June 2007. The arrest of Huawei CFO, Meng Wanzhou, threw more doubt into whether the US-China trade dispute can be resolved, after a promising start with the 90-day truce. Also, there was concern on prolonged US government shutdown. Outside of blue chip universe, the Malaysian market was weak as shown by FBM70 Index and Bursa Malaysia Small Cap Index which tumbled 3.4% and 7.1% m.o.m respectively. Sector wise, technologies and energy were the worst performing sectors, declined by 8.3% and 8.0% m.o.m respectively. The KLCI was down 0.4% m.o.m, despite strong performance of global equities where Dow Jones surged 7.2% m.o.m. In line with the risk-on sentiment, investors dumped blue chips in exchange for the mid and small cap stocks. Hence, the FBM70 and FBM Small Cap gained 5.7% and 7.2% m.o.m. respectively. Global market was rather bullish as for now since the US Federal signalled it is putting further interest rate rises on hold “in light of global economic and financial developments and muted inflation pressures”. The Federal also pledged flexibility on the path for reducing its balance sheet. This marked a reversal, barely a month ago, from December 2018, when the Federal signalled that "some further gradual increases" were coming. As a consequence of change in US rate hike expectation, US dollar (USD) weakened and Malaysia Ringgit (MYR) strengthened 0.9% m.o.m. to MYR4.10 to the dollar. US-China trade talk had some setbacks when US

7

Commerce Secretary Wilbur Ross says the US-China are “miles and miles” apart from coming to a broader trade deal before the 1 March deadline. On top of that, US Federal prosecutors went after Huawei for financial fraud and allegedly stealing trade secrets. The KLCI was up 1.4% m.o.m, in line with strong performance of Dow Jones. Global market was rather bullish as President Trump extends China tariff deadline to raise tariffs on Chinese goods beyond 1 March, citing substantial progress in the latest round of trade talks. Malaysia’s 4Q18 corporate reporting season was disappointing; with only 45% of companies under Maybank research universe met expectation, down from 48% in the preceding quarter. KLCI earnings growth ended 2018 with -2.5% y.o.y. Maybank research cut 2019 earnings growth to 6.1% from 7.8% y.o.y. previously. The KLCI was down 3.8% m.o.m. The big cap led by the banks dragged the KLCI down. FBM70 and FBMSC performed much better, went up by 1.9% and 1.3% m.o.m. respectively. US 10-Year Treasury yield collapsed 31bps in the month of March to close at 2.41%, which caused an inverted yield curve versus the US 3-Month Treasury bill yield which closed at 2.42%. The Federal funds futures are now discounting a 25bp cut this year and another 25bp rate cut in 2020. Besides pausing the rate hike, the US Federal also announced a schedule for ending balance sheet contraction. As a consequence, the Federal balance sheet contraction will end at the end of September at USD3.70T, or 6.8% below the current level of USD3.97T. The rate collapse came about following the release of weak February manufacturing Purchasing Managers' Index (PMI) numbers from major economies of the world. European and Japan’s PMI was particularly weak dipping below 50, signaling contraction in economic activities. The KLCI was down marginally by -0.1% m.o.m. The mid and small cap as represented by FBM70 and FBMSC performed much better, gone up by 2.6% and 7.2% m.o.m. respectively. MYR was weakened against USD by 1.3% m.o.m. to close at 4.13. Two major news that drove the MYR weakness were: 1) FTSE Russell announced that Malaysia’s “market accessibility level’ has been

put on watch list, with the next review in September 2019. If Malaysia’s classification drops 1 level, it will be removed from FTSE World Government Bond Index. Malaysia weighting in the index is estimated at 0.39% or USD7-8b which is 20% of foreign holdings in Malaysia Government Securities (MGS); and

2) An International Rating Agency views the Malaysian Government's financial aid

of MYR6.2b (USD1.5b or 0.4% of Gross Domestic Product (GDP)) to Federal Land Development Authority (Felda) is a credit negative.

The KLCI was up 0.5% m.o.m bucking the downtrend of global market where the Dow Jones fell 6.7% m.o.m The mid and small cap as represented by FBM70 and FBMSC performed much worse, down by 2.3% and 7.9% m.o.m respectively. On the back of deterioration in global economic outlook from trade wars, US 10-year treasury yield plunged 38bps to close at 2.12%, resulted in inverted yield curve against the 3-month Treasury bill. The US 10Y-3m yield gap had widened to 20bps, compared to 2-3bps in the past few months, signaling weaker growth and possible recession ahead. Back to Malaysia, the recent concluded 1Q19 corporate results were mixed. According to CGSCIMB, revision ratio (% of outperformers vs. underperformers) deteriorated to 0.32x in 1Q19 vs. 0.46x in 4Q18. KLCI earnings growth was cut to -3% from +5% previously for 2019. The KLCI was up 1.3% m.o.m, in line with the strong performance of the Dow Jones, which was up 7.2% m.o.m. The mid and small cap as represented by

8

FBM70 and FBMSC performed even better, up by 2.5% and 3.6% m.o.m respectively. Investors turned bullish by the assurance offered by Federal Chairman Powell, that the Federal “will act as appropriate to sustain the expansion” if the trade situation deteriorates. Subsequently, in the June United States (US) Federal Open Market Committee (FOMC) meeting, the Federal held interest rates steady but sent a clear signal that it will likely cut rates this year as uncertainty on the growth outlook has increased and inflationary pressure has been muted. The result is that money markets are now discounting up to 4 Federal rate cuts in one year’s time to 1.5% from current 2.5%. US 10-year treasury yield declined 12bps to 2.01%, the lowest level since 2016. This sparked the sell-off in the US dollar, where the Dollar Index went down 1.7% m.o.m and the related break out in the Gold price, up 8% m.o.m to US1,410/oz. On top of that, market was greeted by another positive news at the G20 summit, where US President Trump and China President Xi, have agreed to a temporary truce to restart the trade talk. US no longer imposes new tariffs on Chinese products, but the US maintains the current tariff level of 25% of the US250b. US allows Huawei to continue to trade with US companies and purchase products of US companies in a field that does not threaten US national security. The KLCI was down -2.2% m.o.m. The mid and small cap as represented by FBM70 and FBMSC were more resilient, down by -0.7% and up by +4.2% m.o.m respectively. As widely expected by the market, on 31 Jul 2019, US Federal cut interest rate by 25bps, for the first time in a decade, bringing Federal rate down to 2.00-2.25% range. Federal Chairman Powell explained that the cut was an insurance cut as concerns intensified over global growth, tariffs and low inflation but stopped short of signaling the beginning of rate cut cycle. The statement was less dovish than market and President Trump’s expectation thus the Dow fell -1.23% on that day. 10Y US treasury yield hardly moved and stayed at 2.03% on the day of rate cut, signaling that market is still expecting further rate cut.

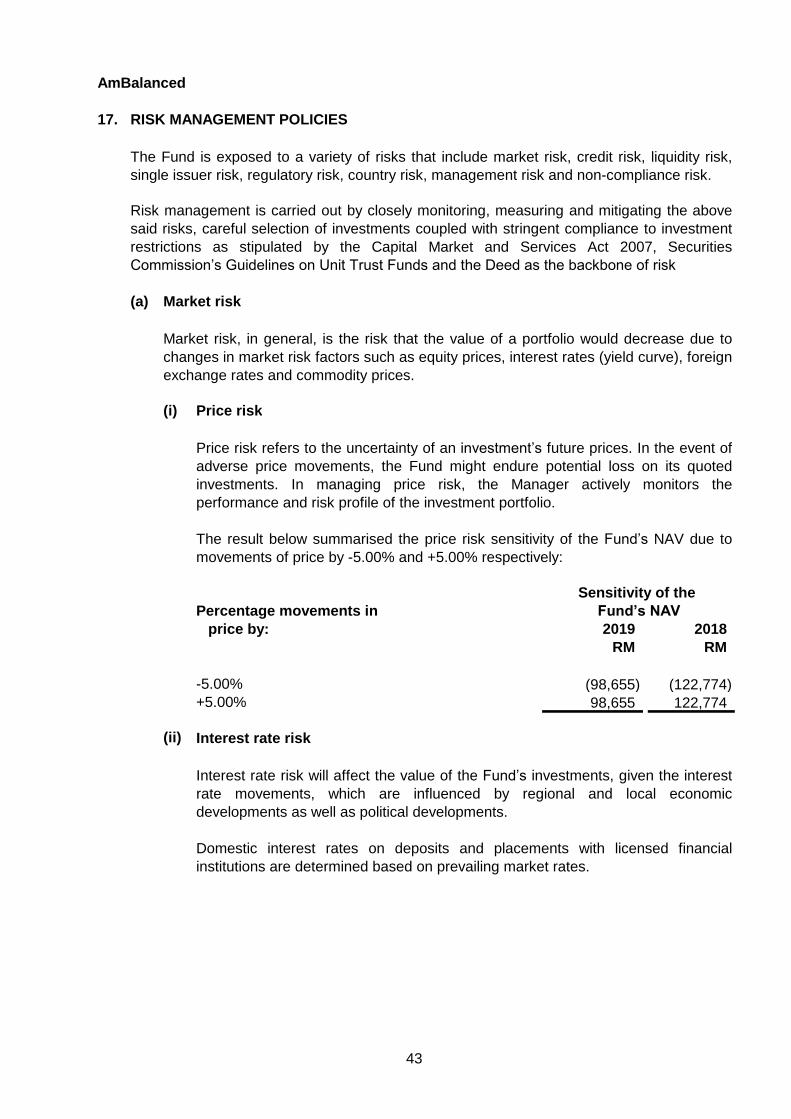

Market Outlook

In August, global market remained volatile as they were impacted by the ongoing external turmoil whilst the imposition of a fresh round of tariffs by both US-China have further worsen the sentiment. Although global central banks have rolled out their accommodative monetary policy to support the market, investors remained concerned about a potential full-blown trade war. This will continue to linger in the mind of all investors around the globe until it is resolved. Locally, market was not spared from the weak sentiment. It was precipitated by the recent uninspiring 2Q19 corporates’ report cards. Despite being the worst performing market in the region YTD, foreign funds continued to flow out from our equity market. We believe it is best to remain defensive to ride through this difficult period. As we remain defensive, we continue to prefer sectors such as consumer (non-discretionary), oil & gas players involved in maintenance, exporters such as gloves, construction players which are focusing on government’s effort in reviving some shelved projects (as the sector has the highest multiplier effect of 2x) and REITs. We have dropped financial as our preferred sector due to the weakening loans growth outlook and a possibility of interest rate cut in the near term.

9

Additional Information

The following information was updated: 1. Jeyaratnam A/L Tamotharam Pillai was appointed as an Independent Non-

Executive Chairman for AmFunds Management Berhad with effect from 1st April 2019.

Kuala Lumpur, Malaysia AmFunds Management Berhad 17 September 2019

Independent auditors’ report to the unitholders of

AmBalanced

Report on the audit of the financial statements

Opinion

Basis for opinion

Independence and other ethical responsibilities

Information other than the financial statements and auditors’ report thereon

We have audited the financial statements of AmBalanced (“the Fund”), which comprise the statement of financial position as at 31 July 2019, the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies, as set out on pages 14 to 47.

In our opinion, the accompanying financial statements give a true and fair view of the financial position of the Fund as at 31 July 2019 and of its financial performance and cash flows for the year then ended in accordance with Malaysian Financial Reporting Standards and International Financial Reporting Standards.

We conducted our audit in accordance with approved standards on auditing in Malaysia and International Standards on Auditing. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

We are independent of the Fund in accordance with the By-Laws (on Professional Ethics, Conduct and Practice) of the Malaysian Institute of Accountants (“By-Laws”) and the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants (“IESBA Code”), and we have fulfilled our other ethical responsibilities in accordance with the By-Laws and the IESBA Code.

The Manager is responsible for the other information. The other information comprises the Annual Report, but does not include the financial statements of the Fund and our auditors’ report thereon. The Annual Report is expected to be made available to us after the date of this auditors’ report.

Our opinion on the financial statements of the Fund does not cover the other information and we do not and will not express any form of assurance conclusion thereon.

10

Independent auditors’ report to the unitholders of

AmBalanced (cont'd.)

Information other than the financial statements and auditors’ report thereon (cont'd.)

Responsibilities of the Manager and the Trustees for the financial statements

Auditor’s responsibilities for the audit of the financial statements

In connection with our audit of the financial statements of the Fund, our responsibility is to read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the financial statements of the Fund or our knowledge obtained in the audit or otherwise appears to be materially misstated.

When we read the Annual Report, if we conclude that there is a material misstatement therein, we are required to communicate the matter to the Manager and Trustee of the Fund and take appropriate action to seek to have the uncorrected material misstatement appropriately brought to the attention of users for whom the auditors’ report is prepared.

The Manager is responsible for the preparation of the financial statements of the Fund that give a true and fair view in accordance with Malaysian Financial Reporting Standards and International Financial Reporting Standards. The Manager is also responsible for such internal control as the Manager determines is necessary to enable the preparation of financial statements of the Fund that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements of the Fund, the Manager is responsible for assessing the Fund’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the Manager either intends to liquidate the Fund or to cease operations, or has no realistic alternative to do so.

The Trustee is responsible for ensuring that the Manager maintains proper accounting and other records as are necessary to enable true and fair presentation of these financial statements.

Our objectives are to obtain reasonable assurance about whether the financial statements of the Fund, as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance approved standards on auditing in Malaysia and International Standards on Auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

11

Independent auditors’ report to the unitholders of

AmBalanced (cont'd.)

Auditor’s responsibilities for the audit of the financial statements (cont'd.)

As part of an audit in accordance with the approved standards on auditing in Malaysia and International Standards on Auditing, we exercise professional judgment and maintain professional skepticism throughout the planning and performance of the audit. We also:

ª Identify and assess the risks of material misstatement of the financial statements of the Fund, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

ª Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control.

ª Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the Manager.

ª Conclude on the appropriateness of the Manager’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Fund’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditors’ report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors’ report. However, future events or conditions may cause the Fund to cease to continue as a going concern.

ª Evaluate the overall presentation, structure and content of the financial statements of the Fund, including the disclosures, and whether the financial statements of the Fund represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with the Manager regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

12

Independent auditors’ report to the unitholders of

AmBalanced (cont'd.)

Other matters

Ernst & Young Lee Pei Yin

AF: 0039 No. 03189/05/2021 J

Chartered Accountants Chartered Accountant

Kuala Lumpur, Malaysia

17 September 2019

This report is made solely to the unitholders of the Fund, as a body, in accordance with the Guidelines on Unit Trust Funds issued by Securities Commission Malaysia and for no other purpose. We do not assume responsibility to any other person for the content of this report.

13

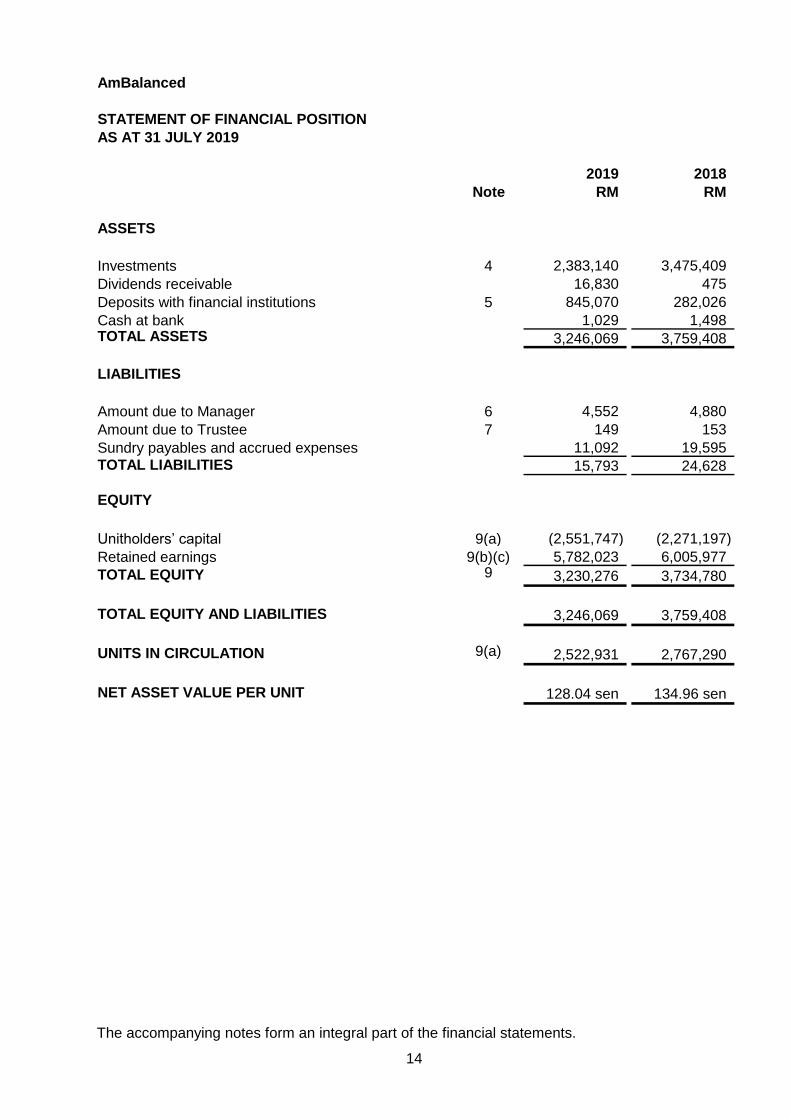

AmBalanced

STATEMENT OF FINANCIAL POSITION

AS AT 31 JULY 2019

2019 2018

Note RM RM

ASSETS

Investments 4 2,383,140 3,475,409

Dividends receivable 16,830 475

Deposits with financial institutions 5 845,070 282,026

Cash at bank 1,029 1,498 TOTAL ASSETS 3,246,069 3,759,408

LIABILITIES

Amount due to Manager 6 4,552 4,880

Amount due to Trustee 7 149 153

Sundry payables and accrued expenses 11,092 19,595

TOTAL LIABILITIES 15,793 24,628

EQUITY

Unitholders’ capital 9(a) (2,551,747) (2,271,197)

Retained earnings 9(b)(c) 5,782,023 6,005,977

TOTAL EQUITY 9 3,230,276 3,734,780

TOTAL EQUITY AND LIABILITIES 3,246,069 3,759,408

UNITS IN CIRCULATION 9(a) 2,522,931 2,767,290

NET ASSET VALUE PER UNIT 128.04 sen 134.96 sen

The accompanying notes form an integral part of the financial statements.

14

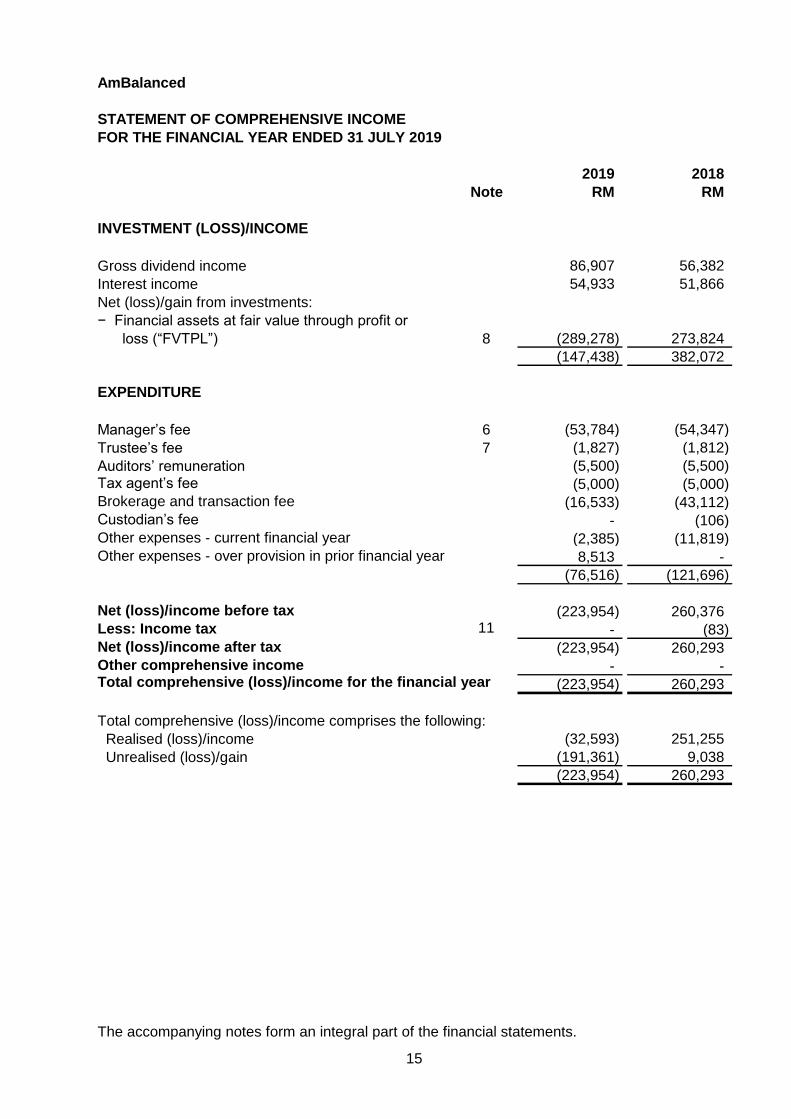

AmBalanced

STATEMENT OF COMPREHENSIVE INCOME

FOR THE FINANCIAL YEAR ENDED 31 JULY 2019

2019 2018

Note RM RM

INVESTMENT (LOSS)/INCOME

Gross dividend income 86,907 56,382

Interest income 54,933 51,866

Net (loss)/gain from investments:

− Financial assets at fair value through profit or

loss (“FVTPL”) 8 (289,278) 273,824

(147,438) 382,072

EXPENDITURE

Manager’s fee 6 (53,784) (54,347)

Trustee’s fee 7 (1,827) (1,812)

Auditors’ remuneration (5,500) (5,500)

Tax agent’s fee (5,000) (5,000)

Brokerage and transaction fee (16,533) (43,112)

Custodian’s fee - (106)

Other expenses - current financial year (2,385) (11,819)

Other expenses - over provision in prior financial year 8,513 -

(76,516) (121,696)

Net (loss)/income before tax (223,954) 260,376

Less: Income tax 11 - (83)

Net (loss)/income after tax (223,954) 260,293

Other comprehensive income - - Total comprehensive (loss)/income for the financial year (223,954) 260,293

Total comprehensive (loss)/income comprises the following:

Realised (loss)/income (32,593) 251,255

Unrealised (loss)/gain (191,361) 9,038

(223,954) 260,293

The accompanying notes form an integral part of the financial statements.

15

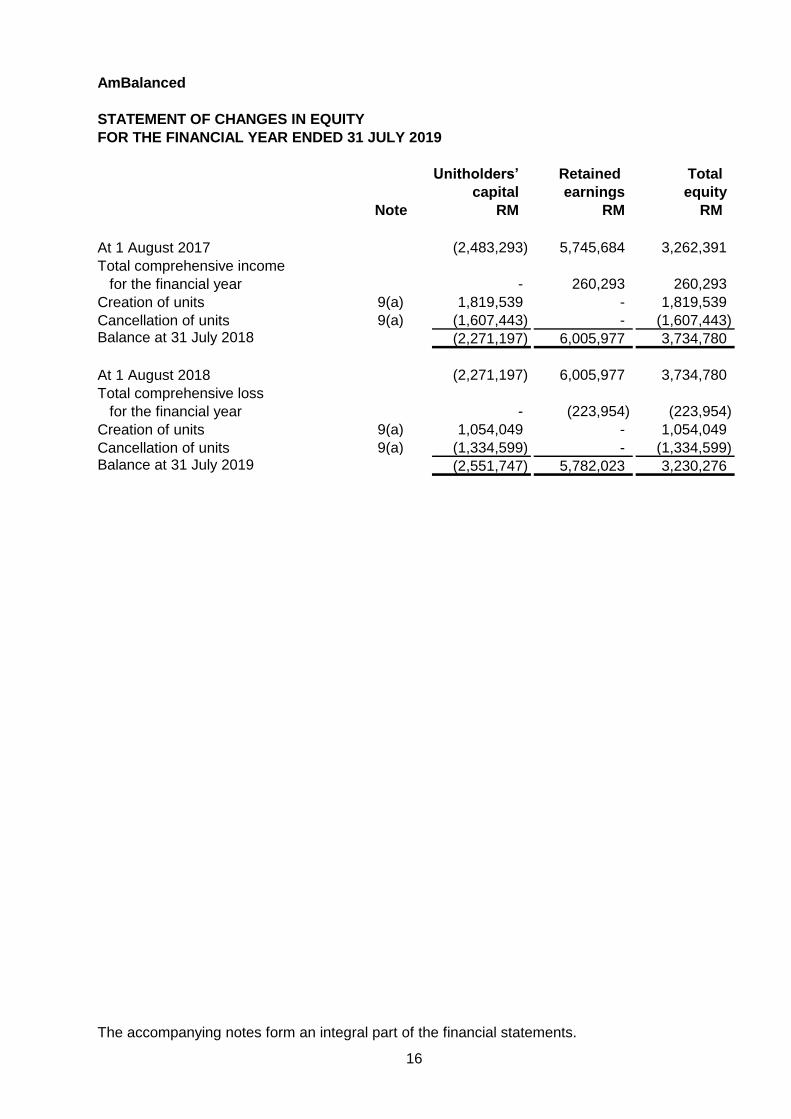

AmBalanced

STATEMENT OF CHANGES IN EQUITY

FOR THE FINANCIAL YEAR ENDED 31 JULY 2019

Unitholders’ Retained Total

capital earnings equity

Note RM RM RM

At 1 August 2017 (2,483,293) 5,745,684 3,262,391

Total comprehensive income

for the financial year - 260,293 260,293

Creation of units 9(a) 1,819,539 - 1,819,539

Cancellation of units 9(a) (1,607,443) - (1,607,443) Balance at 31 July 2018 (2,271,197) 6,005,977 3,734,780

At 1 August 2018 (2,271,197) 6,005,977 3,734,780

Total comprehensive loss

for the financial year - (223,954) (223,954)

Creation of units 9(a) 1,054,049 - 1,054,049

Cancellation of units 9(a) (1,334,599) - (1,334,599) Balance at 31 July 2019 (2,551,747) 5,782,023 3,230,276

The accompanying notes form an integral part of the financial statements.

16

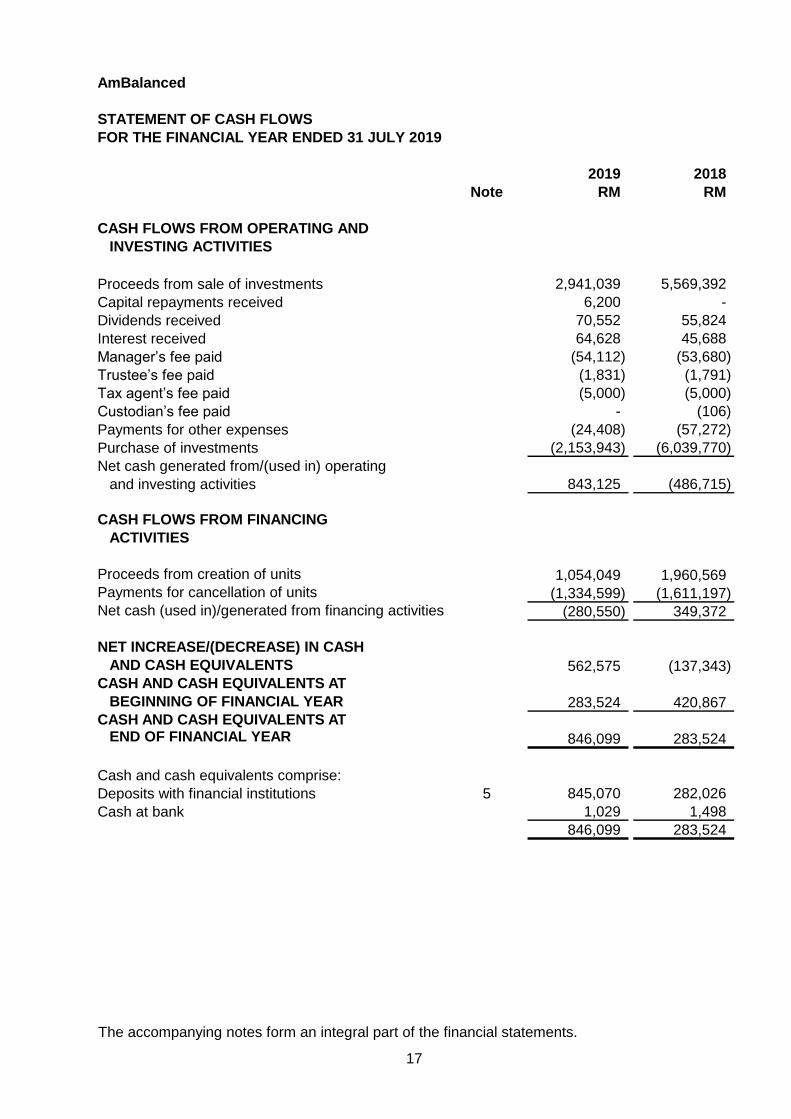

AmBalanced

STATEMENT OF CASH FLOWS

FOR THE FINANCIAL YEAR ENDED 31 JULY 2019

2019 2018

Note RM RM

CASH FLOWS FROM OPERATING AND

INVESTING ACTIVITIES

Proceeds from sale of investments 2,941,039 5,569,392

Capital repayments received 6,200 -

Dividends received 70,552 55,824

Interest received 64,628 45,688

Manager’s fee paid (54,112) (53,680)

Trustee’s fee paid (1,831) (1,791)

Tax agent’s fee paid (5,000) (5,000)

Custodian’s fee paid - (106)

Payments for other expenses (24,408) (57,272)

Purchase of investments (2,153,943) (6,039,770)

Net cash generated from/(used in) operating

and investing activities 843,125 (486,715)

CASH FLOWS FROM FINANCING

ACTIVITIES

Proceeds from creation of units 1,054,049 1,960,569

Payments for cancellation of units (1,334,599) (1,611,197)

Net cash (used in)/generated from financing activities (280,550) 349,372

NET INCREASE/(DECREASE) IN CASH

AND CASH EQUIVALENTS 562,575 (137,343)

CASH AND CASH EQUIVALENTS AT

BEGINNING OF FINANCIAL YEAR 283,524 420,867

CASH AND CASH EQUIVALENTS AT END OF FINANCIAL YEAR 846,099 283,524

Cash and cash equivalents comprise:

Deposits with financial institutions 5 845,070 282,026

Cash at bank 1,029 1,498

846,099 283,524

The accompanying notes form an integral part of the financial statements.

17

AmBalanced

NOTES TO THE FINANCIAL STATEMENTS

FOR THE FINANCIAL YEAR ENDED 31 JULY 2019

1. GENERAL INFORMATION

2. BASIS OF PREPARATION OF FINANCIAL STATEMENTS

Adoption of new standards

MFRS 9 Financial Instruments

MFRS 15 Revenue From Contracts With Customers

MFRS 9 Financial Instruments

AmBalanced (“the Fund”) was established pursuant to a Deed dated 11 September 2003 as

amended by Deeds Supplemental thereto (“the Deed”), between AmFunds Management

Berhad as the Manager, HSBC (Malaysia) Trustee Berhad as the Trustee and all unitholders.

The Fund was set up with the objective of growing the value of investments in longer term

with lower volatility through asset diversification. As provided in the Deed, the “accrual period”

or the financial year shall end on 31 July and the units in the Fund were first offered for sale

on 16 September 2003.

The financial statements of the Fund have been prepared in accordance with Malaysian

Financial Reporting Standards (“MFRS”) as issued by the Malaysian Accounting Standards

Board (“MASB”) and are in compliance with International Financial Reporting Standards.

The financial statements of the Fund have been prepared under the historical cost

convention, unless otherwise stated in the accounting policies.

The accounting policies adopted are consistent with those of the previous financial year

except for the adoption of the following new standards which became effective for the first

time on 1 August 2018:

MFRS 9 replaces the provisions of MFRS 139 Financial Instruments: Recognition and

Measurement that relate to the recognition, classification and measurement, as well as

derecognition of financial instruments, impairment of financial assets and hedge accounting.

As permitted by the transitional provision of MFRS 9, comparative information has not been

restated. The impact arising from the adoption of MFRS 9 is as follows:

The adoption of these new standards did not have any material impact on the financial

statements of the Fund except for those arising from the adoption of MFRS 9 as disclosed

below. Other than the adoption of new accounting policies for financial instruments as

disclosed below, the Fund did not change its accounting policies or make retrospective

adjustments as a result of adopting the new standards.

The financial statements were authorised for issue by the Chief Executive Officer of the

Manager on 17 September 2019.

18

AmBalanced

2. BASIS OF PREPARATION OF FINANCIAL STATEMENTS (CONT'D.)

MFRS 9 Financial Instruments (cont'd.)

(i) Classification and measurement

(ii) Impairment

The loan loss impairment methodology is fundamentally changed under MFRS 9 as it

replaces MFRS 139’s incurred loss approach with a forward-looking expected credit loss

(“ECL”) approach. The impairment requirements based on ECL approach is applicable

for debt financial assets not held at FVTPL. The allowance for expected losses are

determined based on the expected credit losses associated with the probability of default

(“PD”) in the next twelve months unless there has been a significant increase in credit

risk since origination, in which case, the allowance is based on the probability of default

over the lifetime of the asset.

There was no ECL impact on the Fund’s financial assets at amortised cost upon the

adoption of MFRS 9 on 1 August 2018 or during the current financial year.

MFRS 9 requires all financial assets, other than equity instruments and derivatives, to be

classified on the basis of two criteria, namely the entity’s business model for managing

the assets, as well as the instruments’ contractual cash flow characteristics. Financial

assets are measured at amortised cost if they are held within a business model whose

objective is to hold financial assets in order to collect contractual cash flows that are

solely payments of principal and interest. If the financial assets are held within a

business model whose objective is achieved by both selling financial assets and

collecting contractual cash flows that are solely payments of principal and interest, the

assets are measured at fair value through other comprehensive income (“FVOCI”). Any

financial assets that are not measured at amortised cost or FVOCI are measured at fair

value through profit or loss (“FVTPL”). Instruments that qualify for amortised cost or

FVOCI may be irrevocably designated as FVTPL, if doing so eliminates or significantly

reduces a measurement or recognition inconsistency. Equity instruments are normally

measured at FVTPL; nevertheless entities are allowed to irrevocably designate equity

instruments that are not held for trading as FVOCI, with no subsequent reclassification

of gains or losses to the statement of profit or loss.

Upon the adoption of MFRS 9 on 1 August 2018, all the Fund’s equity investments,

collective investment schemes and debt securities continue to be measured at FVTPL.

There is no impact on the Fund’s accounting for financial liabilities, as the new

requirements only affect the accounting for financial liabilities that are designated at

FVTPL and the Fund does not have any such liabilities.

The Fund has established a policy to perform an assessment at the end of each

reporting period of whether credit risk has increased significantly since initial recognition

by considering the change in the risk of default occurring over the remaining life of the

financial instrument. To calculate ECL, the Fund has estimated the risk of a default

occurring on the financial instrument during its expected life. ECLs are estimated based

on the present value of all cash shortfalls over the remaining expected life of the

financial asset, i.e. the difference between the contractual cash flows that are due to the

Fund under the contract and the cash flows that the Fund expect to receive, discounted

at the effective interest rate of the financial asset.

19

AmBalanced

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

3.1 Income recognition

(i) Dividend/Distribution income

(ii) Interest income

(iii) Gain or loss on disposal of investments

3.2 Income tax

3.3 Functional and presentation currency

Dividend/distribution income is recognised when the Fund’s right to receive payment is

established.

Income is recognised to the extent that it is probable that the economic benefits will flow to

the Fund and the income can be reliably measured. Income is measured at the fair value of

consideration received or receivable.

For all interest-bearing financial assets, interest income is calculated using the effective

interest method. Effective interest rate is the rate that exactly discounts estimated future

cash payments or receipts through the expected life of the financial instrument or a

shorter period, where appropriate, to the net carrying amount of the financial asset. The

calculation takes into account all contractual terms of the financial instrument and

includes any fees or incremental costs that are directly attributable to the instrument and

are an integral part of the effective interest rate, but not future credit losses.

Once the recorded value of a financial asset or a group of similar financial assets has

been reduced due to an impairment loss, interest income continues to be recognised

using the rate of interest used to discount the future cash flows for the purpose of

measuring the impairment loss.

On disposal of investments, the net realised gain or loss on disposal is measured as the

difference between the net disposal proceeds and the carrying amount of the

investments. The net realised gain or loss is recognised in profit or loss.

Current tax assets and liabilities are measured at the amount expected to be recovered from

or paid to the tax authorities. The tax rates and tax laws used to compute the amount are

those that are enacted or substantively enacted at the reporting date.

Current taxes are recognised in profit or loss except to the extent that the tax relates to items

recognised outside profit or loss, either in other comprehensive income or directly in equity.

Functional currency is the currency of the primary economic environment in which the Fund

operates that most faithfully represents the economic effects of the underlying transactions.

The functional currency of the Fund is Ringgit Malaysia which reflects the currency in which

the Fund competes for funds, issues and redeems units. The Fund has also adopted Ringgit

Malaysia as its presentation currency.

20

AmBalanced

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

3.4 Statement of cash flows

3.5 Distribution

3.6 Unitholders’ capital

3.7 Financial assets – initial recognition and measurement

(i) Initial recognition

(ii) Initial measurement

(iii) “Day 1” profit or loss

Cash equivalents are short-term, highly liquid investments that are readily convertible to cash

with insignificant risk of changes in value.

The unitholders’ capital of the Fund meets the definition of puttable instruments and is

classified as equity instruments under MFRS 132 Financial Instruments: Presentation (“MFRS

132”).

Financial assets and financial liabilities are recognised when the Fund becomes a party

to the contractual provisions of the instrument. Regular way purchases and sales of

financial assets are recognised using trade date accounting or settlement date

accounting. The method used is applied consistently for all purchases and sales of

financial assets that belong to the same category of financial assets.

All financial assets are recognised initially at fair value plus, in the case of financial

assets not recorded at fair value through profit or loss, transaction costs that are

attributable to the acquisition of the financial asset. All financial liabilities are recognised

initially at fair value and, in the case of financial liabilities not recorded at fair value

through profit or loss, net of directly attributable transaction costs.

At initial measurement, if the transaction price differs from the fair value, the Fund

immediately recognises the difference between the transaction price and fair value (a

“Day 1” profit or loss) in profit or loss provided that fair value is evidenced by a quoted

price in an active market for an identical asset or liability (i.e. Level 1 input) or based on

a valuation technique that uses only data from observable markets. In all other cases,

the difference between the transaction price and model value is recognised in profit or

loss on a systematic and rational basis that reflects the nature of the instrument over its

tenure.

Distributions are at the discretion of the Fund. A distribution to the Fund’s unitholders is

accounted for as a deduction from realised reserves. A proposed distribution is recognised as

a liability in the period in which it is approved.

The Fund adopts the direct method in the preparation of the statement of cash flows.

21

AmBalanced

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

3.8

(i) Debt instruments

Business model

Cash flow characteristics

(ii) Equity instruments and collective investment schemes

Financial assets – classification and subsequent measurement

The classification and subsequent measurement of debt instruments held by the Fund

are determined based on their business model and cash flow characteristics.

The business model reflects how the Fund manages the financial assets in order to

generate cash flows. That is, whether the Fund’s objective is solely to collect the

contractual cash flows from the assets, or is to collect both the contractual cash flows

and cash flows arising from the sale of assets. If neither of these is applicable (e.g. the

financial assets are held for trading purposes), then the financial assets are classified as

part of “other” business model. Factors considered by the Fund in determining the

business model for a portfolio of assets include past experience on how the cash flows

for these assets were collected, how the asset’s performance is evaluated and reported

to key management personnel, and how risks are assessed and managed.

Where the business model is to hold the financial assets to collect contractual cash

flows, or to collect contractual cash flows and sell, the Fund assesses whether the

financial assets’ contractual cash flows represent solely payment of principal and interest

(“SPPI”). In making this assessment, the Fund considers whether the contractual cash

flows are consistent with a basic lending arrangement, i.e. interest includes only

consideration for time value of money, credit risk, other basic lending risks and a profit

margin that is consistent with a basic lending arrangement. Financial assets with

embedded derivatives are considered in their entirety when determining whether their

cash flows are SPPI.

The Fund subsequently measures its investments in equity investments and collective

investment schemes at FVTPL. Dividends/distribution earned whilst holding the

investments are recognised in profit or loss when the right to the payment has been

established. Gains and losses on the investments, realised and unrealised, are included

in profit or loss.

22

AmBalanced

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

3.9 Financial instruments under MFRS 9

(i) Classification and measurement

The Fund may classify its financial assets under the following categories:

Financial assets at amortised cost

Financial assets at FVOCI

Financial assets at FVTPL

A financial asset is measured at amortised cost if it is held within a business model

whose objective is to hold financial assets in order to collect contractual cash flows and

its contractual terms give rise on specified dates to cash flows that are solely payments

of principal and interest on the principal amount outstanding. The Fund includes in this

category deposits with financial institutions, cash at banks, amounts due from

brokers/financial institutions, amount due from the Manager and other receivables.

The classification of financial assets depends on the Fund’s business model of

managing the financial assets in order to generate cash flows (“business model test”)

and the contractual cash flow characteristics of the financial instruments (“SPPI test”).

The business model test determines whether cash flows will result from collecting

contractual cash flows, selling the financial assets, or both and the assessment is

performed on a portfolio basis. The SPPI test determines whether the contractual cash

flows are solely for payments of principal and interest and the assessment is performed

on a financial instrument basis.

A financial asset is measured at fair value through other comprehensive income

(“FVOCI”) if its business model is both to hold the asset to collect contractual cash flows

and to sell the financial asset. In addition, the contractual terms of the financial assets

give rise on specified dates to cash flows that are solely payments of principal and

interest on the outstanding principal.

These investments are initially recorded at fair value and transaction costs are expensed

in the profit or loss. Subsequent to initial recognition, these investments are remeasured

at fair value. All fair value adjustments are initially recognised through OCI. Debt

instruments at FVOCI are subject to impairment assessment.

Any financial assets that are not measured at amortised cost or FVOCI are measured at

fair value to profit or loss (“FVTPL”). Subsequent to initial recognition, financial assets at

FVTPL are measured at fair value. Changes in the fair value of those financial

instruments are recorded in “Net gain or loss on financial assets at FVTPL”. Interest

earned and dividend revenue elements of such instruments are recorded separately in

“Interest income” and “Dividend income” respectively. Exchange differences on financial

assets at FVTPL are not recognised separately in profit or loss but are included in net

gain or net loss on changes in fair value of financial assets at FVTPL.

23

AmBalanced

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

3.9 Financial instruments under MFRS 9 (cont'd.)

(i) Classification and measurement (cont'd.)

Financial assets at FVTPL (cont'd.)

3.10

3.11 Derecognition of financial instruments

(i) Derecognition of financial asset

- the rights to receive cash flows from the asset have expired, or

-

- the Fund has transferred substantially all the risks and rewards of the asset, or

-

(ii) Derecognition of financial liability

Financial liabilities issued by the Fund are classified as financial liabilities at amortised cost,

where the substance of the contractual arrangement results in the Fund having an obligation

either to deliver cash or another financial asset to the holder. After initial measurement,

financial liabilities are subsequently measured at amortised cost using the effective interest

method. Amortised cost is calculated by taking into account any discount or premium on

acquisition and fees or costs that are an integral part of the effective interest rate.

A financial asset (or, where applicable a part of a financial asset or part of a group of

similar financial assets) is derecognised when:

Instruments that qualify for amortised cost or FVOCI may be irrevocably designated as

FVTPL, if doing so eliminates or significantly reduces a measurement or recognition

inconsistency. Equity instruments are normally measured at FVTPL, nevertheless, the

Fund is allowed to irrevocably designate equity instruments that are not held for trading

as FVOCI, with no subsequent reclassification of gains or losses to profit or loss.

Financial liabilities – classification and subsequent measurement

the Fund has transferred its rights to receive cash flows from the asset or has

assumed an obligation to pay the received cash flows in full without material delay

to a third party under a “pass-through” arrangement; and either:

the Fund has neither transferred nor retained substantially all the risks and

rewards of the asset, but has transferred control of the asset.

A financial liability is derecognised when the obligation under the liability is discharged,

cancelled or expired. Gains and losses are recognised in profit or loss when the liabilities

are recognised, and through the amortisation process.

24

AmBalanced

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

3.12 Financial instruments – expected credit losses

-

-

-

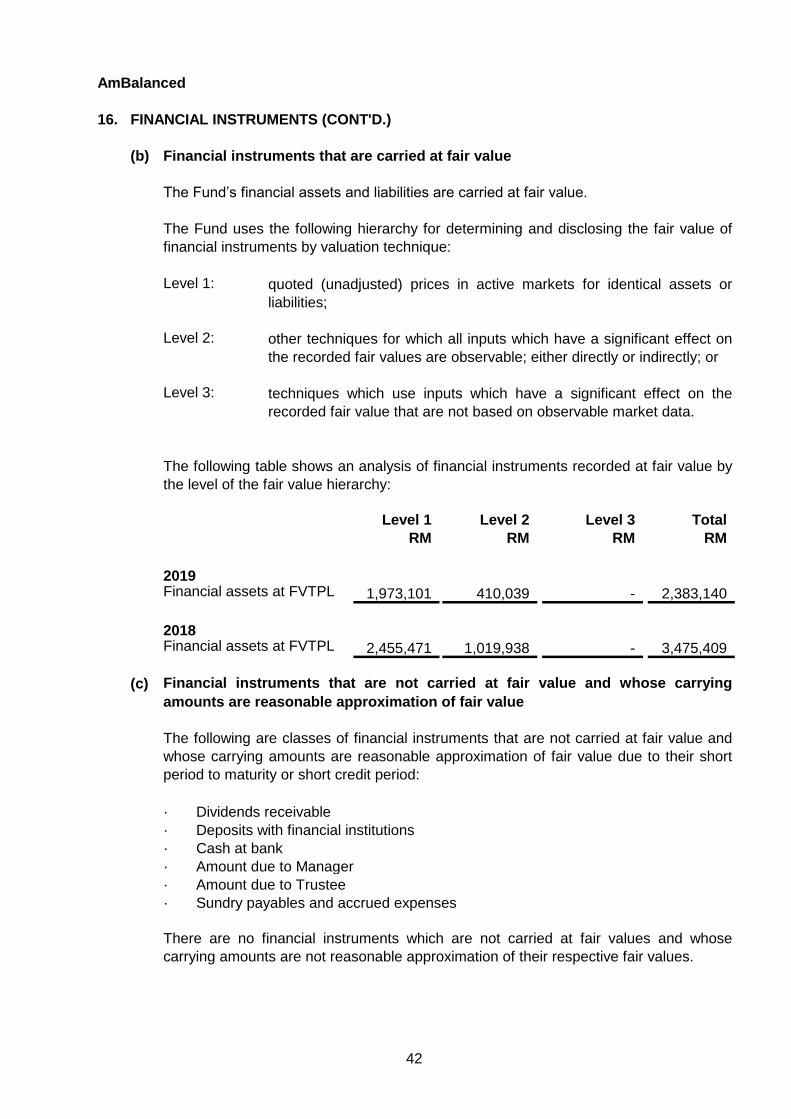

3.13 Determination of fair value

3.14 Classification of realised and unrealised gains and losses

the time value of money; and

reasonable and supportable information that is available without undue cost or effort at

the reporting date about past events, current conditions and forecasts of future

economic conditions.

Financial assets together with the associated allowance are written off when it has exhausted

all practical recovery efforts and there is no realistic prospect of future recovery. The Fund

may also write-off financial assets that are still subject to enforcement activity when there is

no reasonable expectation of full recovery. If a write-off is later recovered, the recovery is

credited to profit or loss.

The Fund assesses on a forward-looking basis the expected credit losses (“ECL”) associated

with its financial assets at amortised cost. The Fund recognises a loss allowance for such

losses at each reporting date. The measurement of ECL reflects:

an unbiased and probability-weighted amount that is determined by evaluating a range

of possible outcomes;

The ECL in respect of financial assets at amortised cost, if any, is recognised in profit or loss.

For investments in local quoted securities, market value is determined based on the closing

price quoted on Bursa Malaysia Berhad. For the investment in collective investment scheme,

fair value is determined based on the closing net asset value per unit of the collective

investment scheme. For investments in local unquoted fixed income securities, fair value is

determined based on the indicative prices from Bond Pricing Agency Malaysia Sdn Bhd plus

accrued interest, which includes the accretion of discount and amortisation of premium.

Adjusted cost of investments relates to the purchase cost plus accrued interest, adjusted for

amortisation of premium and accretion of discount, if any, calculated over the period from the

date of acquisition to the date of maturity of the respective securities as approved by the

Manager and the Trustee. The difference between cost and fair value is treated as unrealised

gain or loss and is recognised in profit or loss. Unrealised gains or losses recognised in profit

or loss are not distributable in nature.

Unrealised gains and losses comprise changes in the fair value of financial instruments for

the period and from reversal of prior period’s unrealised gains and losses for financial

instruments which were realised (i.e. sold, redeemed or matured) during the reporting period.

Realised gains and losses on disposals of financial instruments are classified at fair value

through profit or loss and are calculated using weighted average method. They represent the

difference between an instrument’s initial carrying amount and disposal amount.

25

AmBalanced

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D.)

3.15 Significant accounting estimates and judgments

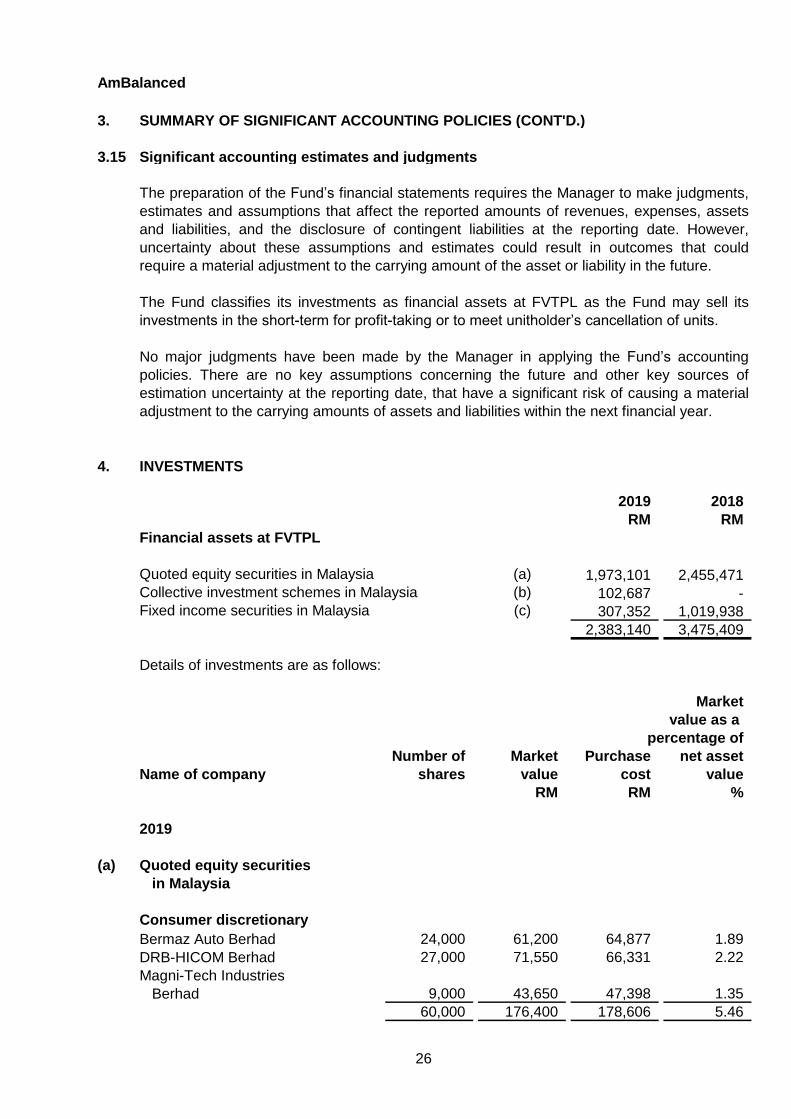

4. INVESTMENTS

2019 2018

RM RM

Financial assets at FVTPL

Quoted equity securities in Malaysia (a) 1,973,101 2,455,471

Collective investment schemes in Malaysia (b) 102,687 -

Fixed income securities in Malaysia (c) 307,352 1,019,938

2,383,140 3,475,409

Details of investments are as follows:

Market

value as a

percentage of

Number of Market Purchase net asset

Name of company shares value cost value

RM RM %

2019

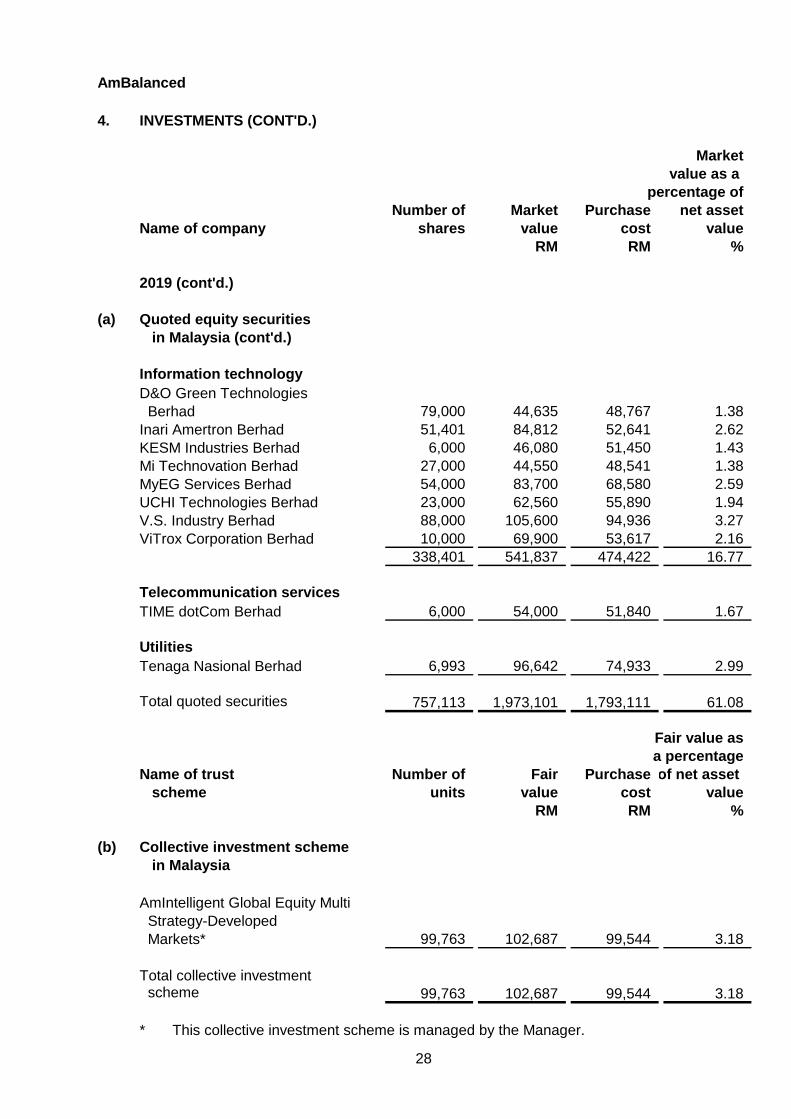

(a) Quoted equity securities

in Malaysia

Consumer discretionary

Bermaz Auto Berhad 24,000 61,200 64,877 1.89

DRB-HICOM Berhad 27,000 71,550 66,331 2.22

Magni-Tech Industries

Berhad 9,000 43,650 47,398 1.35

60,000 176,400 178,606 5.46

No major judgments have been made by the Manager in applying the Fund’s accounting

policies. There are no key assumptions concerning the future and other key sources of

estimation uncertainty at the reporting date, that have a significant risk of causing a material

adjustment to the carrying amounts of assets and liabilities within the next financial year.

The preparation of the Fund’s financial statements requires the Manager to make judgments,

estimates and assumptions that affect the reported amounts of revenues, expenses, assets

and liabilities, and the disclosure of contingent liabilities at the reporting date. However,

uncertainty about these assumptions and estimates could result in outcomes that could

require a material adjustment to the carrying amount of the asset or liability in the future.

The Fund classifies its investments as financial assets at FVTPL as the Fund may sell its

investments in the short-term for profit-taking or to meet unitholder’s cancellation of units.

26

AmBalanced

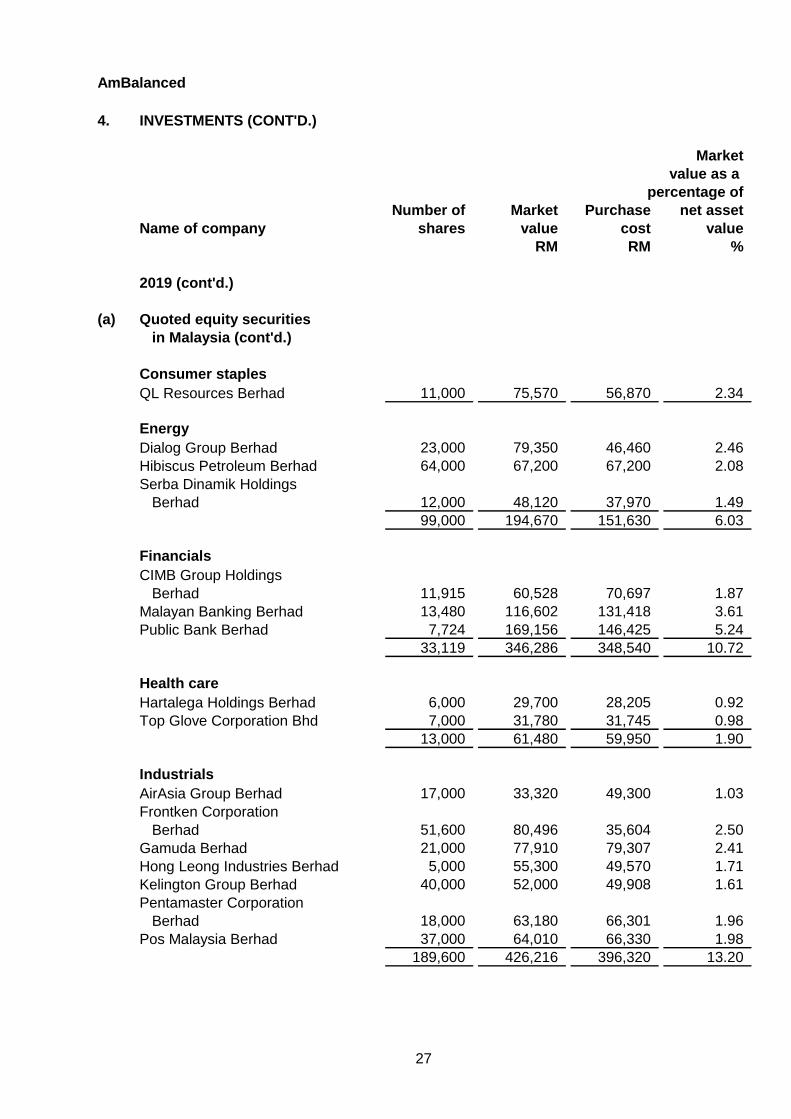

4. INVESTMENTS (CONT'D.)

Market

value as a

percentage of

Number of Market Purchase net asset

Name of company shares value cost value

RM RM %

2019 (cont'd.)

(a) Quoted equity securities

in Malaysia (cont'd.)

Consumer staples

QL Resources Berhad 11,000 75,570 56,870 2.34

Energy

Dialog Group Berhad 23,000 79,350 46,460 2.46

Hibiscus Petroleum Berhad 64,000 67,200 67,200 2.08

Serba Dinamik Holdings

Berhad 12,000 48,120 37,970 1.49

99,000 194,670 151,630 6.03

Financials

CIMB Group Holdings

Berhad 11,915 60,528 70,697 1.87

Malayan Banking Berhad 13,480 116,602 131,418 3.61

Public Bank Berhad 7,724 169,156 146,425 5.24

33,119 346,286 348,540 10.72

Health care

Hartalega Holdings Berhad 6,000 29,700 28,205 0.92

Top Glove Corporation Bhd 7,000 31,780 31,745 0.98

13,000 61,480 59,950 1.90

Industrials

AirAsia Group Berhad 17,000 33,320 49,300 1.03

Frontken Corporation

Berhad 51,600 80,496 35,604 2.50

Gamuda Berhad 21,000 77,910 79,307 2.41

Hong Leong Industries Berhad 5,000 55,300 49,570 1.71

Kelington Group Berhad 40,000 52,000 49,908 1.61

Pentamaster Corporation

Berhad 18,000 63,180 66,301 1.96

Pos Malaysia Berhad 37,000 64,010 66,330 1.98

189,600 426,216 396,320 13.20

27

AmBalanced

4. INVESTMENTS (CONT'D.)

Market

value as a

percentage of

Number of Market Purchase net asset

Name of company shares value cost value

RM RM %

2019 (cont'd.)

(a) Quoted equity securities

in Malaysia (cont'd.)

Information technology

D&O Green Technologies

Berhad 79,000 44,635 48,767 1.38

Inari Amertron Berhad 51,401 84,812 52,641 2.62

KESM Industries Berhad 6,000 46,080 51,450 1.43

Mi Technovation Berhad 27,000 44,550 48,541 1.38

MyEG Services Berhad 54,000 83,700 68,580 2.59

UCHI Technologies Berhad 23,000 62,560 55,890 1.94

V.S. Industry Berhad 88,000 105,600 94,936 3.27

ViTrox Corporation Berhad 10,000 69,900 53,617 2.16

338,401 541,837 474,422 16.77

Telecommunication services

TIME dotCom Berhad 6,000 54,000 51,840 1.67

Utilities

Tenaga Nasional Berhad 6,993 96,642 74,933 2.99

Total quoted securities 757,113 1,973,101 1,793,111 61.08

Fair value as

a percentage

Name of trust Number of Fair Purchase of net asset

scheme units value cost value

RM RM %

(b) Collective investment scheme

in Malaysia

AmIntelligent Global Equity Multi

Strategy-Developed

Markets* 99,763 102,687 99,544 3.18

Total collective investment scheme 99,763 102,687 99,544 3.18

* This collective investment scheme is managed by the Manager.

28

AmBalanced

4. INVESTMENTS (CONT'D.)

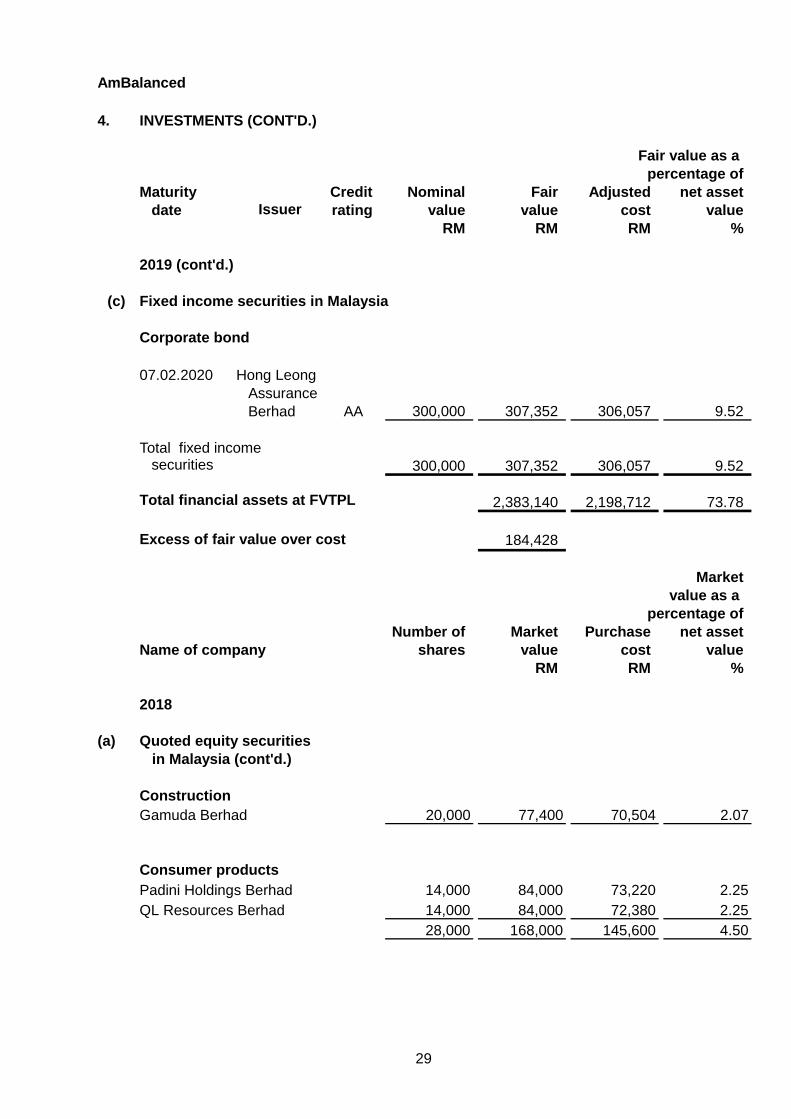

Fair value as a

percentage of

Maturity Credit Nominal Fair Adjusted net asset

date Issuer rating value value cost value

RM RM RM %

2019 (cont'd.)

(c) Fixed income securities in Malaysia

Corporate bond

07.02.2020 Hong Leong

Assurance

Berhad AA 300,000 307,352 306,057 9.52

Total fixed incomesecurities 300,000 307,352 306,057 9.52

Total financial assets at FVTPL 2,383,140 2,198,712 73.78

Excess of fair value over cost 184,428

Market

value as a

percentage of

Number of Market Purchase net asset

Name of company shares value cost value

RM RM %

2018

(a) Quoted equity securities

in Malaysia (cont'd.)

Construction

Gamuda Berhad 20,000 77,400 70,504 2.07

Consumer products

Padini Holdings Berhad 14,000 84,000 73,220 2.25

QL Resources Berhad 14,000 84,000 72,380 2.25

28,000 168,000 145,600 4.50

29

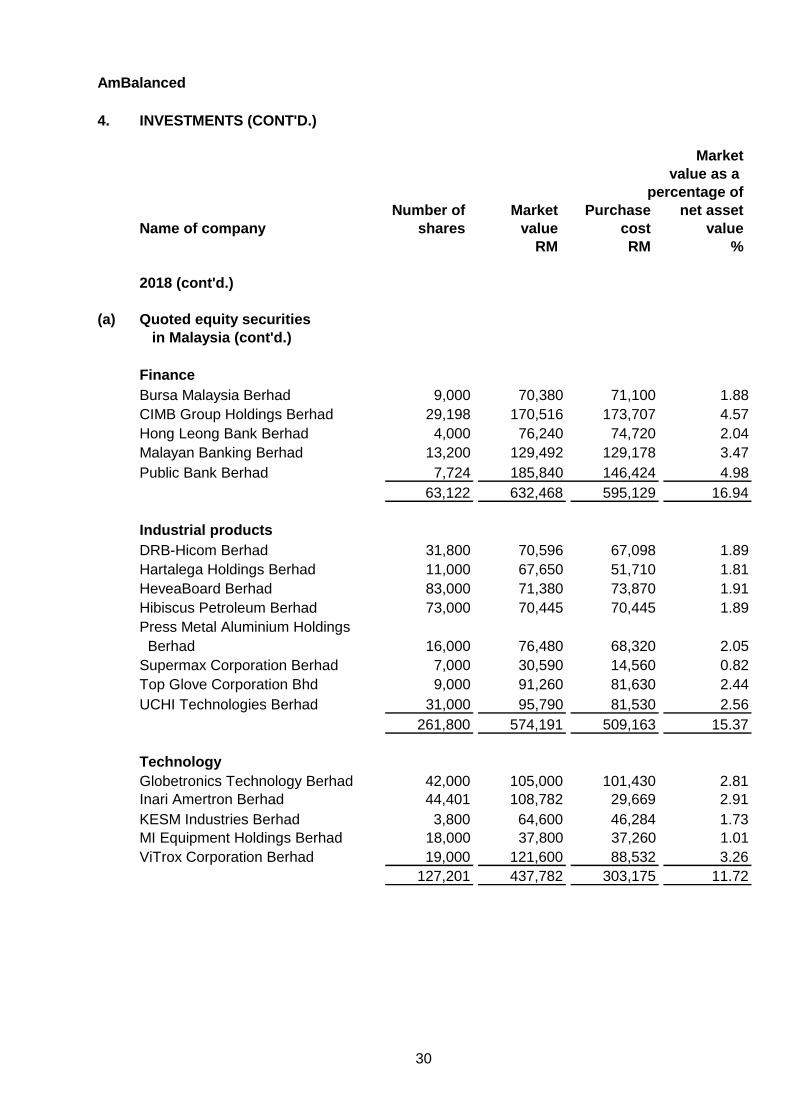

AmBalanced

4. INVESTMENTS (CONT'D.)

Market

value as a

percentage of

Number of Market Purchase net asset

Name of company shares value cost value

RM RM %

2018 (cont'd.)

(a) Quoted equity securities

in Malaysia (cont'd.)

Finance

Bursa Malaysia Berhad 9,000 70,380 71,100 1.88

CIMB Group Holdings Berhad 29,198 170,516 173,707 4.57

Hong Leong Bank Berhad 4,000 76,240 74,720 2.04

Malayan Banking Berhad 13,200 129,492 129,178 3.47

Public Bank Berhad 7,724 185,840 146,424 4.98

63,122 632,468 595,129 16.94

Industrial products

DRB-Hicom Berhad 31,800 70,596 67,098 1.89

Hartalega Holdings Berhad 11,000 67,650 51,710 1.81

HeveaBoard Berhad 83,000 71,380 73,870 1.91

Hibiscus Petroleum Berhad 73,000 70,445 70,445 1.89

Press Metal Aluminium Holdings

Berhad 16,000 76,480 68,320 2.05

Supermax Corporation Berhad 7,000 30,590 14,560 0.82

Top Glove Corporation Bhd 9,000 91,260 81,630 2.44

UCHI Technologies Berhad 31,000 95,790 81,530 2.56

261,800 574,191 509,163 15.37

Technology

Globetronics Technology Berhad 42,000 105,000 101,430 2.81

Inari Amertron Berhad 44,401 108,782 29,669 2.91

KESM Industries Berhad 3,800 64,600 46,284 1.73

MI Equipment Holdings Berhad 18,000 37,800 37,260 1.01

ViTrox Corporation Berhad 19,000 121,600 88,532 3.26

127,201 437,782 303,175 11.72

30

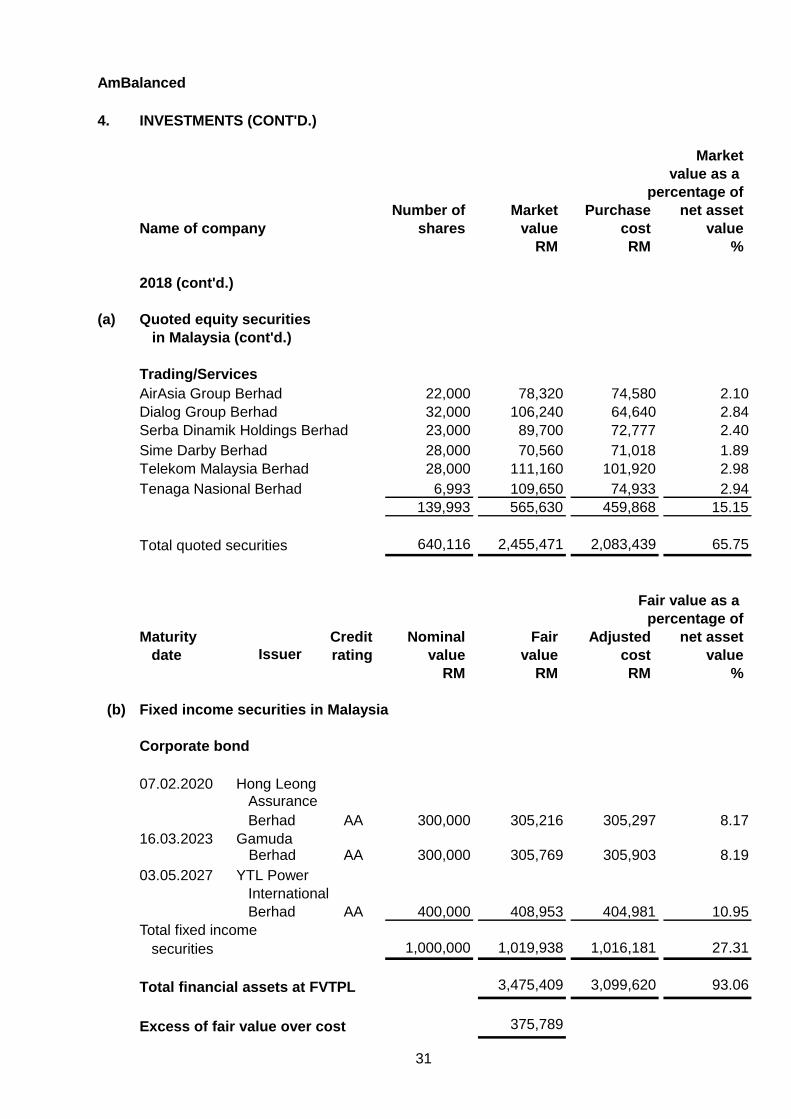

AmBalanced

4. INVESTMENTS (CONT'D.)

Market

value as a

percentage of

Number of Market Purchase net asset

Name of company shares value cost value

RM RM %

2018 (cont'd.)

(a) Quoted equity securities

in Malaysia (cont'd.)

Trading/Services

AirAsia Group Berhad 22,000 78,320 74,580 2.10

Dialog Group Berhad 32,000 106,240 64,640 2.84

Serba Dinamik Holdings Berhad 23,000 89,700 72,777 2.40

Sime Darby Berhad 28,000 70,560 71,018 1.89

Telekom Malaysia Berhad 28,000 111,160 101,920 2.98

Tenaga Nasional Berhad 6,993 109,650 74,933 2.94

139,993 565,630 459,868 15.15

Total quoted securities 640,116 2,455,471 2,083,439 65.75

Fair value as a

percentage of

Maturity Credit Nominal Fair Adjusted net asset

date Issuer rating value value cost value

RM RM RM %

(b) Fixed income securities in Malaysia

Corporate bond

07.02.2020 Hong Leong

Assurance

Berhad AA 300,000 305,216 305,297 8.17

16.03.2023 Gamuda Berhad AA 300,000 305,769 305,903 8.19

03.05.2027 YTL Power

International

Berhad AA 400,000 408,953 404,981 10.95

Total fixed income

securities 1,000,000 1,019,938 1,016,181 27.31

Total financial assets at FVTPL 3,475,409 3,099,620 93.06

Excess of fair value over cost 375,789

31

AmBalanced

4. INVESTMENTS (CONT'D.)

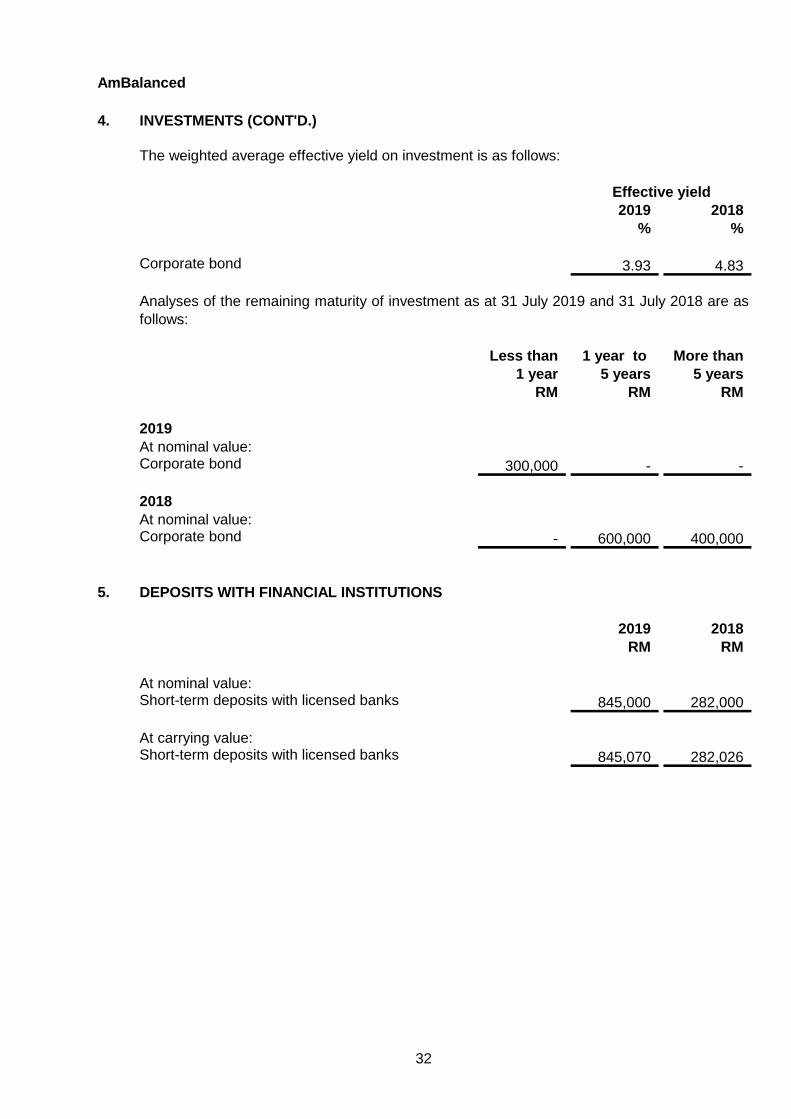

The weighted average effective yield on investment is as follows:

2019 2018

% %

Corporate bond 3.93 4.83

Less than 1 year to More than

1 year 5 years 5 years

RM RM RM

At nominal value:Corporate bond 300,000 - -

At nominal value:Corporate bond - 600,000 400,000

5. DEPOSITS WITH FINANCIAL INSTITUTIONS

2019 2018

RM RM

At nominal value:Short-term deposits with licensed banks 845,000 282,000

At carrying value:Short-term deposits with licensed banks 845,070 282,026

Effective yield

Analyses of the remaining maturity of investment as at 31 July 2019 and 31 July 2018 are as

follows:

2018

2019

32

AmBalanced

5. DEPOSITS WITH FINANCIAL INSTITUTIONS (CONT'D.)

Details of deposits with financial institutions are as follows:

Carrying

value as a

percentage of

Maturity Nominal Carrying Purchase net asset

date Bank value value cost value

RM RM RM %

2019

Short-term deposits with licensed banks

Malayan Banking

Berhad 433,000 433,035 433,000 13.41

Public Bank

Berhad 412,000 412,035 412,000 12.75

845,000 845,070 845,000 26.16

2018

Short-term deposit with a licensed bank

Public Bank

Berhad 282,000 282,026 282,000 7.55

Weighted average effective

2019 2018 2019 2018

% % Day Day

Short-term deposits withlicensed banks 3.02 3.35 1 1

6. AMOUNT DUE TO MANAGER

Manager’s fee is at a rate of 1.50% (2018: 1.50%) per annum on the net asset value of the

Fund, calculated on a daily basis.

01.08.2018

The weighted average effective interest rate and average remaining maturity of short-term

deposits are as follows:

interest rate Remaining maturity

01.08.2018

01.08.2018

The normal credit period in the previous and current financial years for creation and

redemption of units is three business days.

The normal credit period in the previous and current financial years for Manager’s fee payable

is one month.

33

AmBalanced

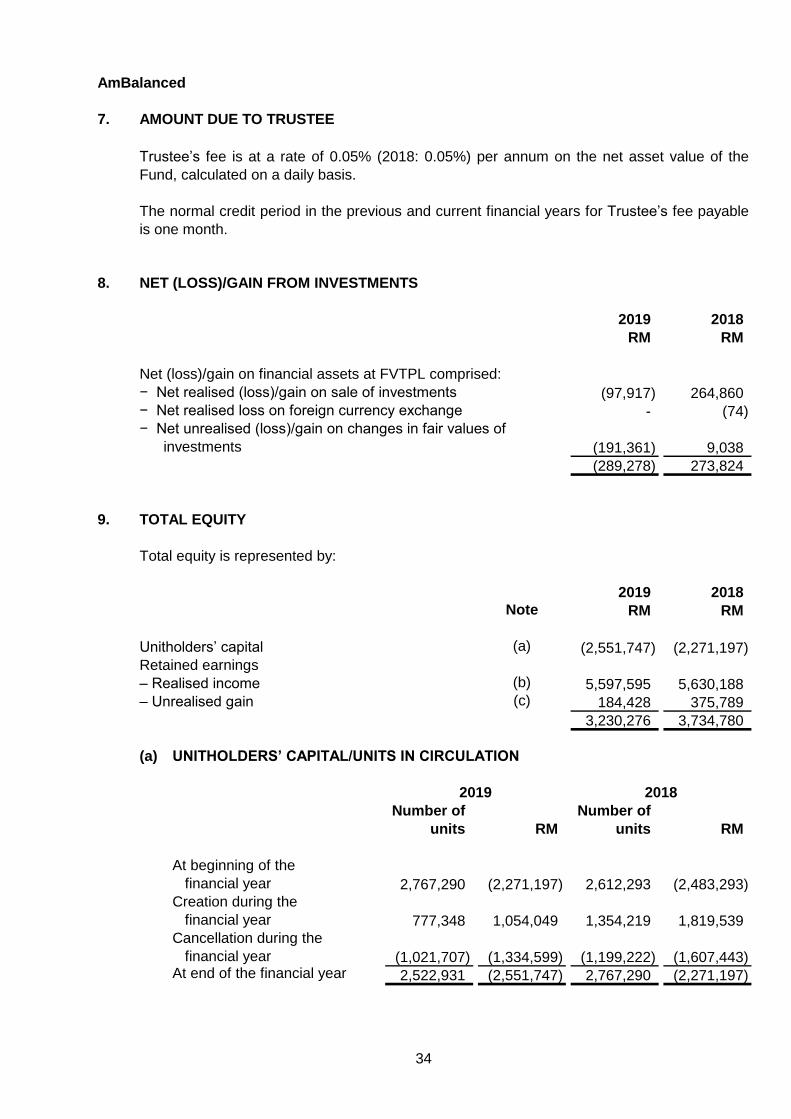

7. AMOUNT DUE TO TRUSTEE

8. NET (LOSS)/GAIN FROM INVESTMENTS

2019 2018

RM RM

Net (loss)/gain on financial assets at FVTPL comprised:

− Net realised (loss)/gain on sale of investments (97,917) 264,860

− Net realised loss on foreign currency exchange - (74)

− Net unrealised (loss)/gain on changes in fair values of

investments (191,361) 9,038

(289,278) 273,824

9. TOTAL EQUITY

Total equity is represented by:

2019 2018

Note RM RM

Unitholders’ capital (a) (2,551,747) (2,271,197)

Retained earnings

– Realised income (b) 5,597,595 5,630,188

– Unrealised gain (c) 184,428 375,789

3,230,276 3,734,780

(a) UNITHOLDERS’ CAPITAL/UNITS IN CIRCULATION

Number of Number of

units RM units RM

At beginning of the

financial year 2,767,290 (2,271,197) 2,612,293 (2,483,293)

Creation during the

financial year 777,348 1,054,049 1,354,219 1,819,539

Cancellation during the

financial year (1,021,707) (1,334,599) (1,199,222) (1,607,443) At end of the financial year 2,522,931 (2,551,747) 2,767,290 (2,271,197)

2018

The normal credit period in the previous and current financial years for Trustee’s fee payable

is one month.

Trustee’s fee is at a rate of 0.05% (2018: 0.05%) per annum on the net asset value of the

Fund, calculated on a daily basis.

2019

34

AmBalanced

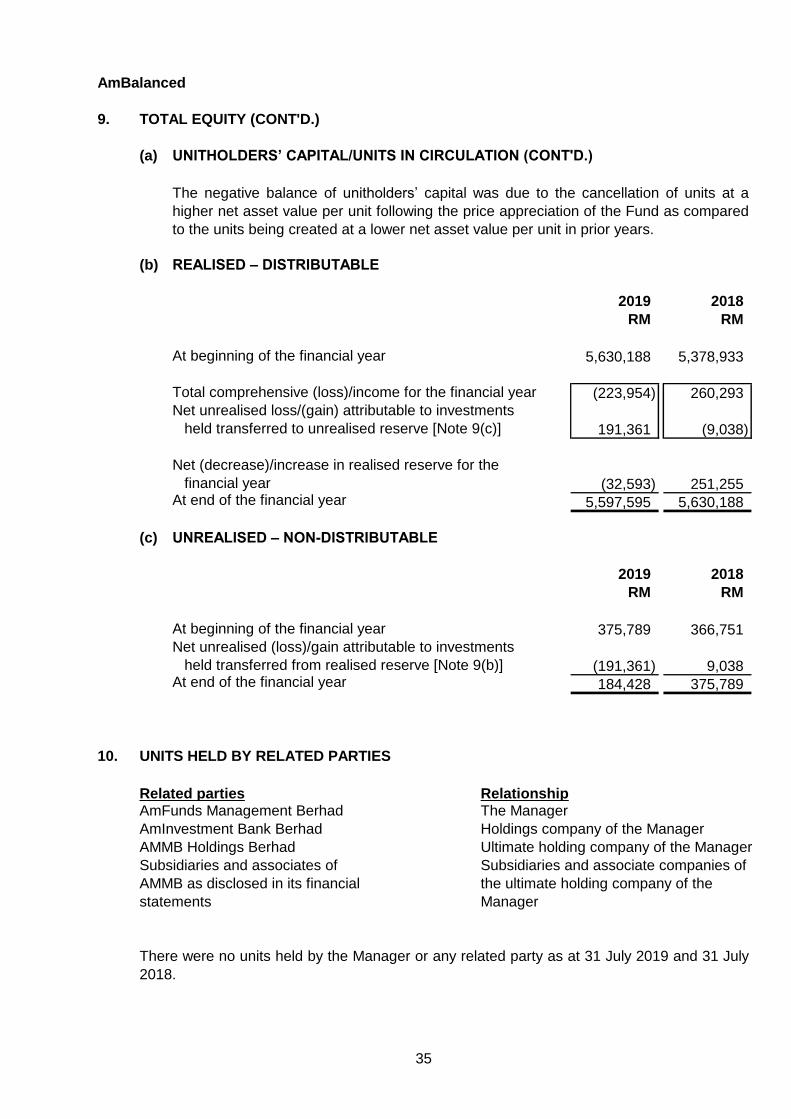

9. TOTAL EQUITY (CONT'D.)

(a) UNITHOLDERS’ CAPITAL/UNITS IN CIRCULATION (CONT'D.)

(b) REALISED – DISTRIBUTABLE

2019 2018

RM RM

At beginning of the financial year 5,630,188 5,378,933

Total comprehensive (loss)/income for the financial year (223,954) 260,293

Net unrealised loss/(gain) attributable to investments

held transferred to unrealised reserve [Note 9(c)] 191,361 (9,038)

Net (decrease)/increase in realised reserve for the

financial year (32,593) 251,255 At end of the financial year 5,597,595 5,630,188

(c) UNREALISED – NON-DISTRIBUTABLE

2019 2018

RM RM

At beginning of the financial year 375,789 366,751

Net unrealised (loss)/gain attributable to investments

held transferred from realised reserve [Note 9(b)] (191,361) 9,038 At end of the financial year 184,428 375,789

10. UNITS HELD BY RELATED PARTIES

Related parties RelationshipAmFunds Management Berhad The Manager

AmInvestment Bank Berhad Holdings company of the Manager

AMMB Holdings Berhad Ultimate holding company of the Manager

There were no units held by the Manager or any related party as at 31 July 2019 and 31 July

2018.

Subsidiaries and associates of

AMMB as disclosed in its financial

statements

The negative balance of unitholders’ capital was due to the cancellation of units at a

higher net asset value per unit following the price appreciation of the Fund as compared

to the units being created at a lower net asset value per unit in prior years.

Subsidiaries and associate companies of

the ultimate holding company of the

Manager

35

AmBalanced

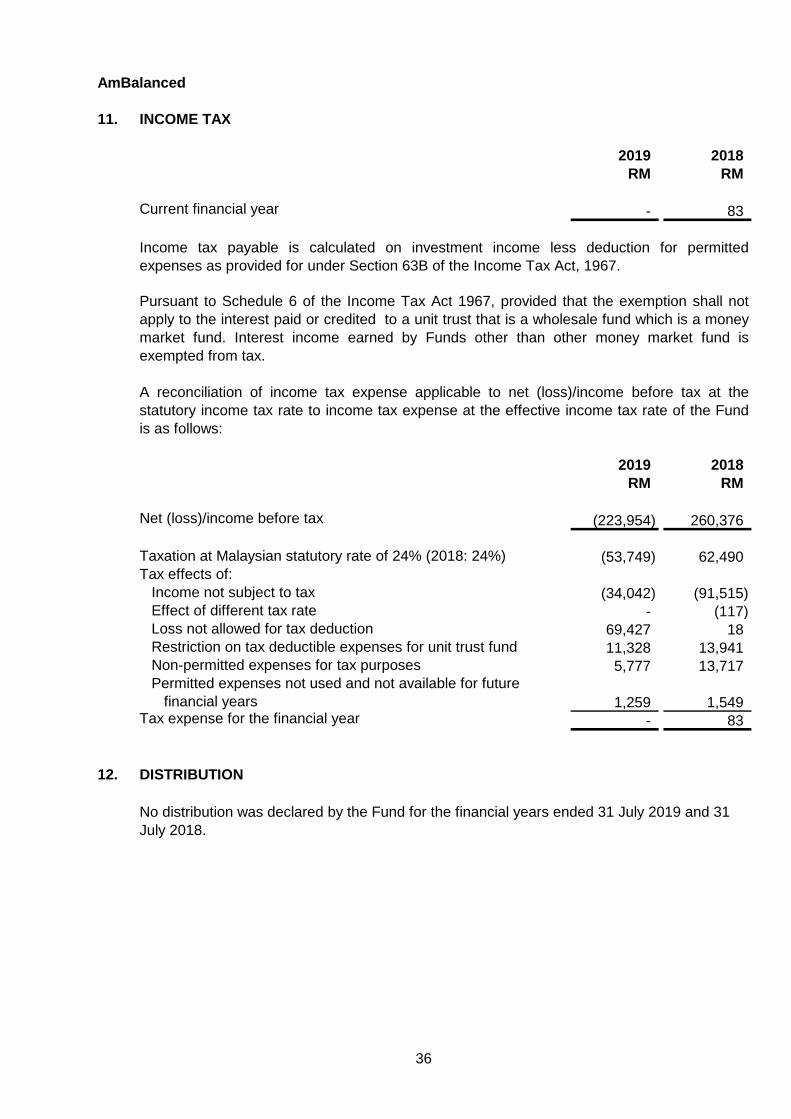

11. INCOME TAX

2019 2018

RM RM

Current financial year - 83

2019 2018

RM RM

Net (loss)/income before tax (223,954) 260,376

Taxation at Malaysian statutory rate of 24% (2018: 24%) (53,749) 62,490

Tax effects of:

Income not subject to tax (34,042) (91,515)

Effect of different tax rate - (117)

Loss not allowed for tax deduction 69,427 18

Restriction on tax deductible expenses for unit trust fund 11,328 13,941

Non-permitted expenses for tax purposes 5,777 13,717

Permitted expenses not used and not available for future

financial years 1,259 1,549 Tax expense for the financial year - 83

12. DISTRIBUTION

Pursuant to Schedule 6 of the Income Tax Act 1967, provided that the exemption shall not

apply to the interest paid or credited to a unit trust that is a wholesale fund which is a money

market fund. Interest income earned by Funds other than other money market fund is

exempted from tax.

A reconciliation of income tax expense applicable to net (loss)/income before tax at the

statutory income tax rate to income tax expense at the effective income tax rate of the Fund

is as follows:

Income tax payable is calculated on investment income less deduction for permitted

expenses as provided for under Section 63B of the Income Tax Act, 1967.

No distribution was declared by the Fund for the financial years ended 31 July 2019 and 31

July 2018.

36

AmBalanced

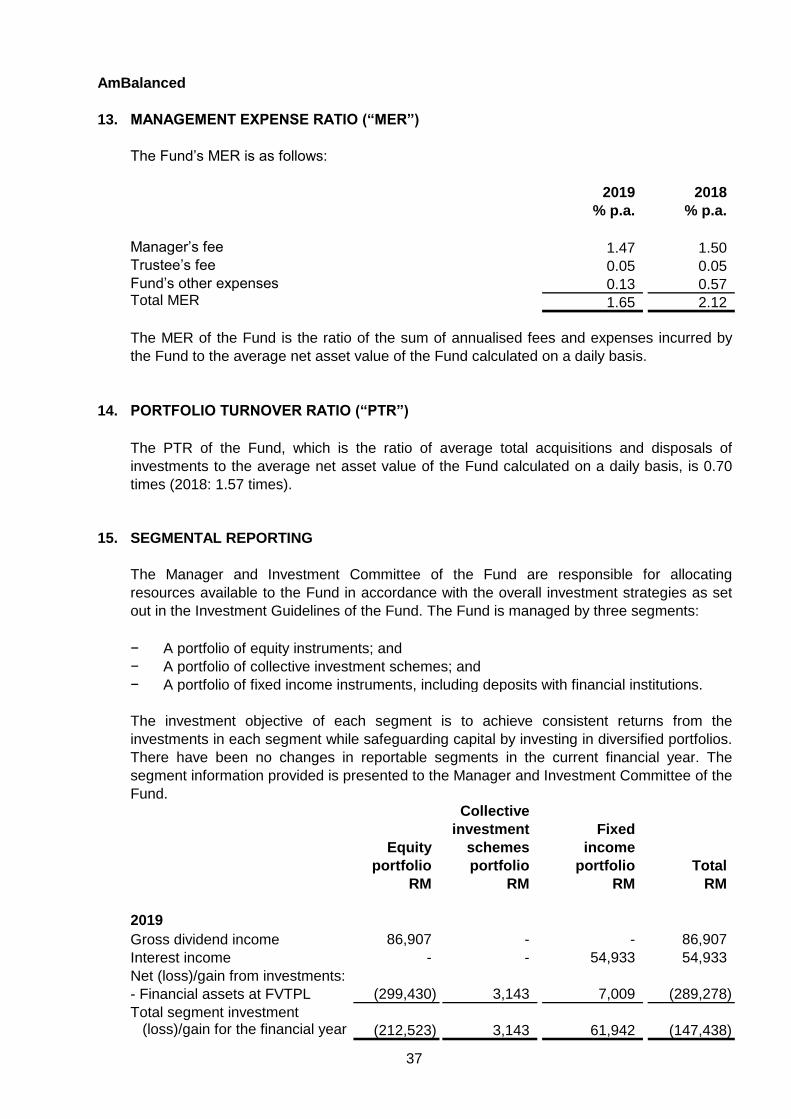

13. MANAGEMENT EXPENSE RATIO (“MER”)

The Fund’s MER is as follows:

2019 2018

% p.a. % p.a.

Manager’s fee 1.47 1.50

Trustee’s fee 0.05 0.05

Fund’s other expenses 0.13 0.57 Total MER 1.65 2.12

14. PORTFOLIO TURNOVER RATIO (“PTR”)

15. SEGMENTAL REPORTING

− A portfolio of equity instruments; and

− A portfolio of collective investment schemes; and

− A portfolio of fixed income instruments, including deposits with financial institutions.

Collective

investment Fixed

Equity schemes income

portfolio portfolio portfolio Total

RM RM RM RM

Gross dividend income 86,907 - - 86,907

Interest income - - 54,933 54,933

Net (loss)/gain from investments:

- Financial assets at FVTPL (299,430) 3,143 7,009 (289,278)

Total segment investment(loss)/gain for the financial year (212,523) 3,143 61,942 (147,438)

The MER of the Fund is the ratio of the sum of annualised fees and expenses incurred by

the Fund to the average net asset value of the Fund calculated on a daily basis.

The Manager and Investment Committee of the Fund are responsible for allocating

resources available to the Fund in accordance with the overall investment strategies as set

out in the Investment Guidelines of the Fund. The Fund is managed by three segments:

The investment objective of each segment is to achieve consistent returns from the

investments in each segment while safeguarding capital by investing in diversified portfolios.

There have been no changes in reportable segments in the current financial year. The

segment information provided is presented to the Manager and Investment Committee of the

Fund.

The PTR of the Fund, which is the ratio of average total acquisitions and disposals of

investments to the average net asset value of the Fund calculated on a daily basis, is 0.70

times (2018: 1.57 times).

2019

37

AmBalanced

15. SEGMENTAL REPORTING (CONT'D.)

Collective

investment Fixed

Equity schemes income

portfolio portfolio portfolio Total

RM RM RM RM

2019 (cont'd.)

Financial assets at FVTPL 1,973,101 102,687 307,352 2,383,140

Dividends receivable 16,830 - - 16,830

Deposits with financial institutions - - 845,070 845,070 Total segment assets 1,989,931 102,687 1,152,422 3,245,040

Gross dividend income 56,382 - - 56,382

Interest income - - 51,866 51,866

Net gain from investments:

- Financial assets at FVTPL 272,400 - 1,424 273,824

Total segment investmentincome for the financial year 328,782 - 53,290 382,072

Financial assets at FVTPL 2,455,471 - 1,019,938 3,475,409

Dividends receivable 475 - - 475

Deposits with financial institutions - - 282,026 282,026 Total segment assets 2,455,946 - 1,301,964 3,757,910

There were no segment liabilities as of 31 July 2019 and 31 July 2018.

2019 2018

RM RM

Net reportable segment investment (loss)/income (147,438) 382,072

Less: Expenses (76,516) (121,696)

Net (loss)/income before tax (223,954) 260,376

Less: Income tax - (83) Net (loss)/income after tax (223,954) 260,293

2018

Expenses of the Fund are not considered part of the performance of any investment

segment. The following table provides reconciliation between the net reportable segment

income and net (loss)/income after tax:

38

AmBalanced

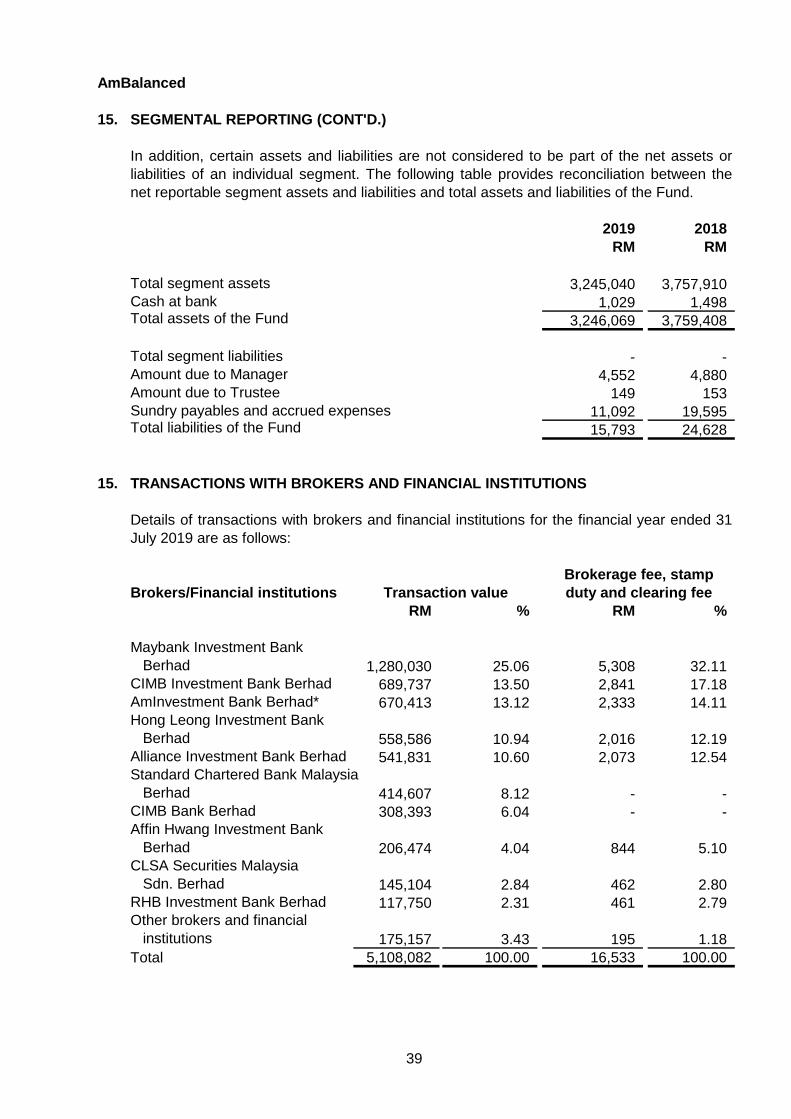

15. SEGMENTAL REPORTING (CONT'D.)

2019 2018

RM RM

Total segment assets 3,245,040 3,757,910

Cash at bank 1,029 1,498 Total assets of the Fund 3,246,069 3,759,408

Total segment liabilities - -

Amount due to Manager 4,552 4,880

Amount due to Trustee 149 153

Sundry payables and accrued expenses 11,092 19,595 Total liabilities of the Fund 15,793 24,628

15. TRANSACTIONS WITH BROKERS AND FINANCIAL INSTITUTIONS

Brokerage fee, stamp

Brokers/Financial institutions Transaction value duty and clearing fee

RM % RM %

Maybank Investment Bank

Berhad 1,280,030 25.06 5,308 32.11

CIMB Investment Bank Berhad 689,737 13.50 2,841 17.18

AmInvestment Bank Berhad* 670,413 13.12 2,333 14.11

Hong Leong Investment Bank

Berhad 558,586 10.94 2,016 12.19

Alliance Investment Bank Berhad 541,831 10.60 2,073 12.54

Standard Chartered Bank Malaysia

Berhad 414,607 8.12 - -

CIMB Bank Berhad 308,393 6.04 - -