Embed Size (px)

Citation preview

$95.00 USA/$114.00 CAN

The bankruptcy process is not always well understood from a practical level by those making business decisions and evaluating strategic alternatives. Business Valuation and Bankruptcy helps you—whether you are an accountant dealing with a troubled company, a lender, an investor, a bankruptcy and restructuring lawyer, fi nancial advisor, or a private equity player—to understand case-determinative issues when creditors, lenders, and debtors have differing views of value. It lets you understand the context of the issues and get far below the surface of the analysis you will be making.

Introducing valuation issues early on in the restructuring/bankruptcy process so you can plan accordingly, this book offers:

• A description of the life cycle of a troubled company and the various stages of a restructuring

• An analysis of the valuation issues that confront practitioners in the real-world application of the law

• Coverage of the key principals in practice• An in-depth look at the legal environment

in which both the valuation testimony is received and how the testimony is measured to determine its admissibility

Written by practitioners who have practical experience in the courtroom as experts and lawyers, as well as at the negotiating table, Business Valuation and Bankruptcy is packed with many real-life examples to demonstrate the applicable sections of the bankruptcy laws.

IAN RATNER, CPA, ABV, ASA, CFE, of GlassRatner Advisory & Capital Group LLC, is a nationally recognized fi nancial advisor, focused in the area of forensic accounting, litigation support, business valuation, and bankruptcy consulting. He has a proven track record as an expert advisor and has led high-profi le and complex assignments including failed transactions, SEC investigations, fi nancial reporting frauds, large corporate bankruptcies, and countless commercial litigation matters. In many of these cases, he is asked to decipher contradictory valuation opinions and testimony by getting behind the numbers relied on by others. Ian has testifi ed as an expert on dozens of occasions in state and federal courts in various jurisdictions around the country.

GRANT T. STEIN is partner in the law fi rm of Alston & Bird LLP in the Bankruptcy, Reorganization and Workouts Group. He is a Fellow of the American College of Bankruptcy, Chair and past president of the Southeastern Bankruptcy Law Institute, and is identifi ed as a top practitioner in Chambers USA: America’s Leading Lawyers for Business, The Best Lawyers in America, and Super Lawyers magazine. During his more than twenty-fi ve years of practice, he has amassed extensive bankruptcy and litigation experience dealing with valuation questions.

JOHN C. WEITNAUER is a partner with the law fi rm of Alston & Bird LLP in the Bankruptcy, Reorganization and Workouts Group. In 2006, he was co-trial counsel for plaintiffs in a jury trial that involved many business valuation issues, and obtained a verdict stating that over $965,000,000 in transfers were made with the actual intent to defraud the plaintiffs, with $350,000,000 in punitive damages. He has been included in The Best Lawyers in America reference books since 1995. He is profi led in Chambers USA: America’s Leading Lawyers for Business. He is a Contributing Editor of two bankruptcy treatises, Norton Bankruptcy Law and Practice and the Bankruptcy Litigation Manual.

BUSINESS VALUATION

AND BANKRUPTCY

Ian RatnerGrant T. Stein

John C. Weitnauer

BUSINESS VALUATION A

ND BANKRUPTCY

Ratner

Stein W

eitnauer

Praise for Business Valuation and Bankruptcy“For the restructuring lawyer or anyone else seeking a cogent and accessible exposition of the fi rst principles of valuation and how valuation issues fi t in the bankruptcy process, this timely and clearly written book is the natural place to turn.”

— Professor Douglas G. Baird, The University of Chicago Law School, Scholar in Residence for the American College of Bankruptcy

“There are no easy business valuation issues in bankruptcy. However, armed with this treatise, bankruptcy professionals and courts can confront the valuation challenges in a thoughtful and deliberate manner. I found this book a remarkable effort in addressing the issues presented in distressed business valuations. The work is thoughtful, broad in scope, detailed in areas where necessary, and a substantial contribution to the literature. I was especially impressed that the book has much to offer to attorneys, judges, and valuation professionals. I highly recommend the work to any serious student of business valuations in bankruptcy.”

— Professor Jack F. Williams, Georgia State University College of Law, author, lecturer, and American Bankruptcy Institute Resident Scholar

“An excellent guide to the wide variety of valuation issues that professionals face on a daily basis, in the insolvency world. This work provides us with a wide range of analyses, taking us from the initial stages of an engagement, determining a company’s viability, up through the entire insolvency process. An essential tool for any bankruptcy professional”

— John Ames,Greenbaum Doll & McDonald PLLC,President, American Bankruptcy Institute (2007–2009)

“I have read several books on valuation principles and theory. Business Valuation and Bankruptcy is by far the best written, best organized, and most approachable. The valuation methodologies and theories are explained in plain language, and the inclusion of the application of those methodologies and theories to the Bankruptcy Code and reported cases is immensely helpful. I have asked our entire Business Reorganization Team to read Business Valuation and Bankruptcy, and I intend to keep it handy as a reference.”

— Paul Steven Singerman, Berger Singerman, former chair of the Florida Bar Bankruptcy Commitee

BUSINESS VALUATION

AND BANKRUPTCY

E1FFIRS 10/06/2009 12:31:56 Page 2

E1FFIRS 10/06/2009 12:31:56 Page 1

BusinessValuation andBankruptcy

E1FFIRS 10/06/2009 12:31:56 Page 2

E1FFIRS 10/06/2009 12:31:56 Page 3

IAN RATNERGRANT STEIN

JOHN C. WEITNAUER

John Wiley & Sons, Inc.

BusinessValuation andBankruptcy

E1FFIRS 10/06/2009 12:31:56 Page 4

Copyright# 2009 by John Wiley & Sons, Inc. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.

Published simultaneously in Canada.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by

any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted

under Section 107 or 108 of the 1976 United States Copyright Act, without either the prior written

permission of the Publisher, or authorization through payment of the appropriate per-copy fee to the

Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, 978-750-8400, fax 978-646-

8600, or on the web at www.copyright.com. Requests to the Publisher for permission should be addressed to

the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, 201-748-

6011, fax 201-748-6008, or online at www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in

preparing this book, they make no representations or warranties with respect to the accuracy or

completeness of the contents of this book and specifically disclaim any implied warranties of merchantability

or fitness for a particular purpose. No warranty may be created or extended by sales representatives or

written sales materials. The advice and strategies contained herein may not be suitable for your situation.

You should consult with a professional where appropriate. Neither the publisher nor author shall be liable

for any loss of profit or any other commercial damages, including but not limited to special, incidental,

consequential, or other damages.

For general information on our other products and services, or technical support, please contact our

Customer Care Department within the United States at 800-762-2974, outside the United States at 317-572-

3993 or fax 317-572-4002.

Wiley also publishes its books in a variety of electronic formats. Some content that appears in print may not

be available in electronic books.

For more information about Wiley products, visit our Web site at www.wiley.com.

Library of Congress Cataloging-in-Publication Data:

Ratner, Ian.

Business valuation and bankruptcy / Ian Ratner, Grant Stein, John Weitnauer.

p. cm. — (Wiley finance series; 521)

Includes index.

Summary: ‘‘An essential guide to business valuation and bankruptcy, Business Valuation and Bankruptcy

helps you—whether you are an accountant dealing with a troubled company, a lender, an investor, a

bankruptcy and restructuring lawyer/financial advisor, or a private equity player—to focus on solving

everyday and case determinative disputes when creditors, lenders, and debtors have differing views of value.

Introducing valuation issues early on in the restructuring/bankruptcy process so you can plan accordingly,

this book offers many real-life case examples and case descriptions. Business Valuation and Bankruptcy

includes a review of the various approaches and methods to value a business and insight into when to apply

each, a description of the life cycle of a troubled company and the various stages of a restructuring, an

analysis of the valuation issues that confront practitioners in the real world of troubled companies and

bankruptcy, and the application of business valuation issues to bankruptcy law. Business Valuation and

Bankruptcy is written in terms that are common to bankruptcy professionals and is essential, timely reading

for players in the bankruptcy and restructuring environment’’—Provided by publisher.

ISBN 978-0-470-46238-6

1. Business—Valuation. 2. Bankruptcy. I. Stein, Grant.

II. Weitnauer, John. III. Title.

HG4028.V3R37 2010

658.15—dc22 2009025212

Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

E1FTOC 10/07/2009 19:3:7 Page 5

Contents

Preface ix

CHAPTER 1Introduction 1

The Troubled Company Continuum 1Operational and Financial Disstress 3The Troubled Company Response 3Valuation in Reorganization or Bankruptcy 5Conclusion 6

CHAPTER 2Industry Practitioners and Standards 7

Professional Organizations and Business Valuation Standards 7Business Valuation Practitioners and Certifications 14Conclusion 19Notes 19

CHAPTER 3The Basics of Business Valuation 21

The Purpose of the Valuation 21Standard of Value 22Premise of Value—Going Concern or Liquidation 23Valuation Approaches 25Fundamentals 29Conclusion 38Notes 38

CHAPTER 4Income Approach 39

Discounted Cash FlowMethod 41Capitalized Cash FlowMethod 57Conclusion 58Note 59

v

E1FTOC 10/07/2009 19:3:7 Page 6

CHAPTER 5Market Approach 61

Guideline Company Method 61Comparable Transaction Method 73Conclusion 81

CHAPTER 6United States Bankruptcy Code 83

Introduction to the Structure of the Bankruptcy Code 83Commencement of a Bankruptcy Case and Filing of Schedules 84Chapter 7 of the Bankruptcy Code 85Chapter 11 of the Bankruptcy Code 85Avoiding Powers under the Bankruptcy Code—Preferences 94Avoiding Powers under the Bankruptcy Code—Fraudulent

Transfers 95Valuation Principles from the Bankruptcy Courts 95Conclusion 96Notes 96

CHAPTER 7Valuations in Bankruptcy as of the Date of the Hearing 97

Introduction 97Relief from the Automatic Stay and Adequate Protection 98§ 363 Sales 100Use of Cash Collateral 105Disclosure Statement 105Plan Confirmation—Feasibility 105Plan Confirmation—Best-Interests-of-Creditors Test 106Plan Confirmation—Cram Down 106Conclusion 111Notes 111

CHAPTER 8Valuations in Bankruptcy at a Time in the Past—Avoidance Actions 121

Overview 121Avoidance Actions—Preferences 121Avoidance Actions—Fraudulent Transfers 123The Applicable Legal Tests for Insolvency 128Insolvency Test: Valuation of Debts 129Insolvency Test: The Valuation of Assets 132Proof of Insolvency by Retrojection 135The Insolvency Test: Comparing Assets and Debts 135

vi CONTENTS

E1FTOC 10/07/2009 19:3:7 Page 7

Is the Public Market’s Assessment in the Past ConclusiveProof of Solvency, Even If the Company Later Fails? 135

Use of Hindsight in the Valuation Process 136Conclusion 143Notes 143

CHAPTER 9Solvency Opinions 149

Introduction 149Who Uses Solvency Opinions? 149Solvency Opinion Preparation 151Solvency Metrics 153Case Studies 155Conclusion 157Notes 157

CHAPTER 10Daubert 159

Challenges to Experts or Their Testimony 159Lack of Relevance 171Practical Lessons fromDaubert Cases for Experts and Lawyers 171Conclusion 173Notes 173

APPENDIXAICPA Statement on Standards for Valuation Services

No. 1, Valuation of a Business, Business OwnershipInterest, Security, or Intangible Asset 179

Index 255

Contents vii

E1FTOC 10/07/2009 19:3:7 Page 8

E1FPREF 10/06/2009 12:49:24 Page 9

Preface

This book is an integrated reference source for those involved in the valu-ation of a business in a commercial environment, with the focus on for-

mal bankruptcy proceedings and distressed situations. It has been written bypractitioners who have practical experience in the commercial courtroom,and the insights and analysis it contains are reflective of their collective sub-stantial experience.

Ian Ratner is a CPA accredited in business valuation by the AICPA andthe American Society of Appraisers. He is also a Certified Fraud Examinerand one of the founding members of GlassRatner Advisory & CapitalGroup LLC. Ian is a nationally known bankruptcy advisor and forensic ac-countant who regularly performs business valuations and deals with com-plex valuation issues in commercial disputes and bankruptcy-relatedmatters. Ian regularly acts as a trial preparation consultant and expert wit-ness in commercial disputes and bankruptcy cases. Kit Weitnauer and GrantStein are senior partners with Alston & Bird LLP who practice commercialbankruptcy law and try commercial cases throughout the United States, in-cluding cases involving valuation issues. Mr. Stein began working on valua-tion issues in the distressed debt environment while at business school atEmory University in the mid 1970’s, and has carried that through intohis legal practice having tried numerous commercial valuation disputesin the federal bankruptcy courts, federal district courts and state courts.Mr. Weitnauer was one of the two trial lawyers for the plaintiff in the $1.35billion fraudulent conveyance jury verdict obtained in MAN AG et al.v. Freightliner LLC et al.MANwas tried in Oregon under Oregon’s versionof the Uniform Fraudulent Transfer Act. The verdict included $350 millionin punitive damages. This constituted the largest jury verdict in the UnitedStates in 2006. Mr. Weitnauer’s primary responsibilities at trial was todirect the cross-examination the of all of the valuation experts. The authorswere assisted by Leanne Gould, Prashanth Setty, and Wayne Weitz, allqualified and experienced professionals in the area of financial statementanalysis and business valuation.

The bankruptcy process is a judicial process that is not always wellunderstood by the noninitiated. For the accountant and business

ix

E1FPREF 10/06/2009 12:49:24 Page 10

professional, this book provides background on the bankruptcy process,acts as a basic tool in the area of business valuation, and demonstrates theconnection between these disciplines.

For the valuation expert, this book highlights the application of thebusiness valuation discipline to the bankruptcy environment. It covers thekey principles in practice, and explains both the legal environment in whichthe valuation testimony is received, and how the testimony is evaluated todetermine its admissibility. Plan confirmation, preferences, fraudulent con-veyance, adequate protection, timing issues on each of these, going-concernvalues, liquidation values, and the whens, whats, and whys are all explored.Valuation professionals will do a better job for their clients with a fullunderstanding of the context of their work and the issues facing the triallawyers.

For the lawyer, the book is a concise compendium of valuation stand-ards and legal principles, including an outstanding discussion of Daubertprinciples dealing with the standards for admission of expert testimony ap-plicable in the valuation context focusing on bankruptcy and insolvencyquestions.

x PREFACE

E1C01 09/15/2009 Page 1

CHAPTER 1Introduction

THE TROUBL ED COMPANY CONT INUUM

Companies can have four stages in their life cycle: the start-up or develop-ment phase, the growth phase, the maturity or stabilization phase, and inmany cases, the disruption or decline phase.

Start-up or development-stage companies are early stage companiesseeking financing for product development and market testing. In manycases commercialization of the companies’ products or services is not fullyestablished. During this early stage of development, proof of concept is thegoal. Once companies live through the start-up stage, they move on to thegrowth stage, where they have gained momentum in sales and market ac-ceptance. During this stage, companies hire experienced management, andsome form of permanent financing has been obtained. Mature companieshave an established customer base, vendor network, business processes, andproducts or services. Mature companies often expand to new regions or at-tempt to grow in a horizontal or vertical manner both organically andthrough mergers and acquisitions. During this period, private companies of-ten deal with wealth and ownership transfer issues.

If all companies followed the process just described and the economymaintained a stable growth rate, business would be less complicated, andthere would be no need for this book. However, there is usually a disruptionor period of decline either at some stage of a company’s development, or aspart of a general economic cycle that affects companies in the same industryor region. Business professionals and economists agree that it is highly un-likely for any company (or the economy) to maintain an upward trend in-definitely. This truth is playing out in the current downturn of the globaleconomy.

Not all problems are similar or have the same level of severity; troubledcompanies move along a continuum. The continuum goes from a short-termliquidity crunch to the realization that the existing business model is simply

1

E1C01 09/15/2009 Page 2

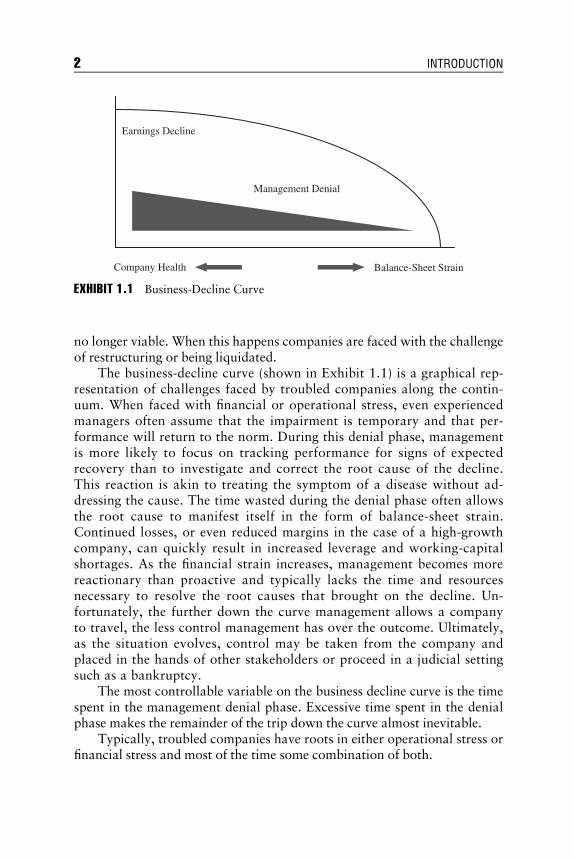

no longer viable. When this happens companies are faced with the challengeof restructuring or being liquidated.

The business-decline curve (shown in Exhibit 1.1) is a graphical rep-resentation of challenges faced by troubled companies along the contin-uum. When faced with financial or operational stress, even experiencedmanagers often assume that the impairment is temporary and that per-formance will return to the norm. During this denial phase, managementis more likely to focus on tracking performance for signs of expectedrecovery than to investigate and correct the root cause of the decline.This reaction is akin to treating the symptom of a disease without ad-dressing the cause. The time wasted during the denial phase often allowsthe root cause to manifest itself in the form of balance-sheet strain.Continued losses, or even reduced margins in the case of a high-growthcompany, can quickly result in increased leverage and working-capitalshortages. As the financial strain increases, management becomes morereactionary than proactive and typically lacks the time and resourcesnecessary to resolve the root causes that brought on the decline. Un-fortunately, the further down the curve management allows a companyto travel, the less control management has over the outcome. Ultimately,as the situation evolves, control may be taken from the company andplaced in the hands of other stakeholders or proceed in a judicial settingsuch as a bankruptcy.

The most controllable variable on the business decline curve is the timespent in the management denial phase. Excessive time spent in the denialphase makes the remainder of the trip down the curve almost inevitable.

Typically, troubled companies have roots in either operational stress orfinancial stress and most of the time some combination of both.

Earnings Decline

Management Denial

Balance-Sheet StrainCompany Health

EXHIBIT 1.1 Business-Decline Curve

2 INTRODUCTION

E1C01 09/15/2009 Page 3

OPERAT I ONAL AND F INANC IA L D I SSTRESS

Operational stress may occur for a number of reasons, including competitionfrom other companies, competition from replacement products and services,the departure of key employees or management, rapid changes in raw mate-rial quality or availability, changes in cost structure that cannot be passed onto consumers, or a change in the demand for the company’s products or ser-vices. Whatever the reason for the operational stress, the financial outcomesare typically declining revenues or market share, increasing operatingexpenses, decreasing operating margins, and liquidity constraints. If the trou-bled company is unable to address the business issues causing the operationalstress and react to reduce expenses, increase revenues, raise capital to meetshort-term requirements, or some combination, then the business will sooninevitably experience financial stress and possibly insolvency.

Financial stress is likely to occur when the company’s existing leverageis excessive, and the company finds it hard or impossible to make scheduleddebt or principal payments. This is often the case when a company has beensubject to a leveraged buyout transaction or other leveraged transaction. Fi-nancial stress is also evident in companies whose capitalization ultimatelydoes not support its operations going forward. One common example ofthis type of capitalization is a company that has financed long-term assets,such as plant and equipment, through short-term financing, such asaccounts payable and short-term lines of credit. When this happens, thebusiness will starve for working capital because all the working capitalsources are being consumed to sustain the long-term assets.

The expression, ‘‘good company with a bad balance sheet,’’ is oftenused to describe a company that has a strong operational base but is in fi-nancial stress. If the troubled company is unable to refinance its existingdebt or to divest noncore assets to cover its interest expense, then the com-pany may face insolvency.

Operational and financial stresses are not mutually exclusive, meaningthat a company with a strong financial position may be struggling opera-tionally, and a company with strong operating activity may be strugglingfinancially.

THE TROUBL ED COMPANY RESPONSE

Prebankrup t cy Op t i o ns f or t he Troub l ed Company

Troubled companies do not immediately file for bankruptcy. Instead, oncethe operational or financial distress is recognized, the troubled company cantake corrective steps.

The Troubled Company Response 3