Embed Size (px)

DESCRIPTION

February 2012 EPM

Citation preview

www.ethanolproducer.com

INSIDE: ETHANOL INTELLECTUAL PROPERTY EVOLVES

PlusHedging: Vital in Risk Management, Complex in Execution Page 35

Certifying Ethanolfor Export to the EU Page 47

FEBRUARY 2012

Golden Opportunities

Corn Oil Renders New Synergies for Ethanol and Biodiesel Page 40

Produced by:

June 4 – 7, 2012Minneapolis, Minnesota

www.fuelethanolworkshop.com

The World’s Largest and Longest Running Ethanol Conference

The International Fuel Ethanol Workshop & Expo is the largest gathering of private and public sector ethanol professionals in the world. Your customers will be here seeking tailored solutions to the unique challenges they face. Attendees will include current and future producers of ethanol, industry vendors, technology providers, equipement manufacturers, project developers, investors and policymakers. Demonstrate your commitment to the future of the ethanol industry and plan to exhibit at this once-a-year opportunity.

Put Yourself in Front of the Largest Gathering of Ethanol Producers in the World

Sponsorships and Exhibit Space Now Available

Become a sponsor and position yourself as a leader and supporter of the renewable fuels industry.

Thank you to our 2012 sponsors:Tranter, Inc.WINBCOPremium Plant Services, Inc.AIAT AnstaltFreez-it-CleenBurns & McDonnellSiemens Industry, Inc.A&B Process SystemsWB Services, LLCSulzer Process Pumps, Inc.DuPont FermaSureJohn Crane Mechanical SealsFagen, Inc.Highmark RenewablesHydro-Klean, Inc.ICM, Inc.NovozymesAshland Hercules Water TechnologiesChemtex International, Inc.BuckmanAGRA IndustriesLallemand Ethanol TechnologyGENENCORFermentisPioneer Hi-Bred InternationalBetaTec Hop ProductsRockwell SoftwareDedert CorporationBuhler Inc.Inbicon Biomass RefineryButamax Advanced Biofuels LLCUS Water ServicesVerenium CorporationEnogen SyngentaPhibroChem Ethanol Performance Group

Become a part of the world’s largest, longest running ethanol conference.Contact an account representative today.866-746-8385 | [email protected] | www.fuelethanolworkshop.com

4 | Ethanol Producer Magazine | FEBRUARY 2012

FEBRUARY iSSUE 2012 VOL. 18 iSSUE 2

contents

Ethanol Producer Magazine: (USPS No. 023-974) February 2012, Vol. 18, issue 2. Ethanol Producer Magazine is published monthly. Principal Office: 308 Second Ave. N., Suite 304, Grand Forks, ND 58203. Periodicals Postage Paid at Grand Forks, North Dakota and additional mailing offices. POSTMAS-TER: Send address changes to Ethanol Producer Magazine/Subscriptions, 308 Second Ave. N., Suite 304, Grand Forks, North Dakota 58203.

fEaturES

On the Cover Clayton McNeff is co-creator of the McGyan Biodiesel Process, a unique catalytic reactor, that can convert corn oil and a wide range of other low-grade and prime feedstocks to biodiesel. PHOTO: MCGYAN

DEPARTMENTS

6 Editor’s Note Effective Outreach By SuSanne Retka Schill

7 ad Index

10 the Way I See It The Power of Pride and Passion By Mike BRyan

11 Events Calendar Upcoming Conferences & Trade Shows

12 View from the Hill The ILUC Debate, Four Years Later By BoB dinneen

14 Drive Reaping the Benefits of a Strong Biofuels Industry By toM BuiS

16 Grassroots Voice Ethanol’s Octane Provides Proactive Opportunity By BRian JenningS

18 Europe Calling A Pragmatic Approach to Fuel Taxation By RoB VieRhout

20 Business Matters The Ethanol IP Evolution By caMille l. uRBan

22 Business Briefs

24 Commodities report

28 Distilled

52 Marketplace

www.ethanolproducer.com

INSIDE: ETHANOL INTELLECTUAL PROPERTY EVOLVES

PlusHedging: Vital in Risk Management, Complex in Execution Page 35

Certifying Ethanolfor Export to the EU Page 47

FEBRUARY 2012

Golden Opportunities

Corn Oil Renders New Synergies for Ethanol and Biodiesel Page 40

46

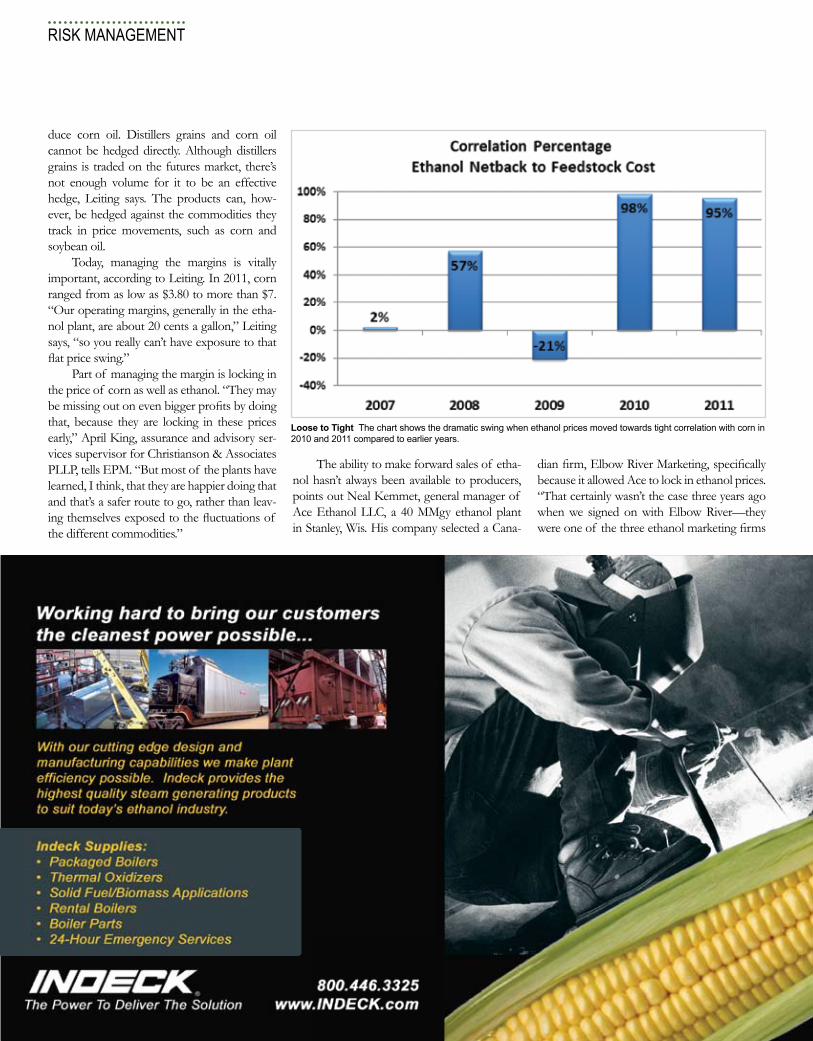

RISK MANAGEMENT Pieces of the Puzzle Hedging strategies have evolved in the ethanol industry BY HOLLY JESSEN

SUSTAINABILITYCertifying SustainabilityExporting ethanol to EU requires a new certification stepBY KRIS BEVILL

34

40 CORN OiLGolden OpportunitiesCorn oil presents potential ethanol, biodiesel cooperation, co-location opportunitiesBY HOLLY JESSEN

6 | Ethanol Producer Magazine | FEBRUARY 2012

In need of a morale booster? Mike Bryan’s column this month is a good exposition of the passion, drive and perseverance that the ethanol industry has exhibited over the years. Building this industry has never been an easy sell with the public, he reminds us.

There may be a trend emerging in the ethanol industry to communicate with and engage the general public more effectively. In the past several months, I have noticed more ethanol plant managers are being quoted in their regional daily papers. From the stories I see, I can’t tell if the contact was initiated by the newspaper or the plant managers, but it is effective. Any newspaper worth its salt will jump at the chance to localize the national news. When an issue comes up that lends itself to comment, I urge you to contact your local newspaper and explain that you’d like to discuss the issue and how it impacts your busi-ness and the community. Take advantage of our industry organizations, too, to get some background information and facts to use. And be honest—if the reporter asks a question you don’t know the answer to, simply say you’d rather not comment since you aren’t well-versed on that topic.

Mike Jerke, general manager of the Benson, Minn., ethanol plant, took a different approach. When he saw an article that troubled him about an orga-nization’s stance, he wrote to the head of the organization. The letter is brief, courteous but pointed. We share that letter below with the readers of Ethanol Producer Magazine.SuSanne Retka SchIll, edItoR

EffECtIVE OutrEaCH

editor’s note

FOR INDUSTRY NEwS: WWW.EtHaNOlPrODuCEr.COM OR FOLLOw US: tWIttEr.COM/EtHaNOlMaGazINE

LETTER Mike Jerke, general manager of Chippewa Valley Ethanol shared the

following letter he sent to Rob Green, executive director of the National Council of Chain Restaurants, saying, “It’s one thing to be beaten up by Big Oil, it’s another to have Appleby’s, Chilis, McDonalds, IHOP and Cracker Barrel pile on.” He added that he has not yet gotten answers to the questions he poses.

Dear Mr. Green,i read with concern the article by Sasha Orman on the Food and

Drink Digital website, “National Council of Chain Restaurants Takes on Ethanol,” regarding your association’s position on ethanol from corn. i would appreciate your expounding on the quote attributed to you in the article that states in part, “These subsidies have artificially increased the price of corn, which in turn has driven up costs for restaurants and the customers they serve.”

What costs, specifically, are higher for the restaurants you serve? Recognizing that ethanol now displaces 10 percent of the gasoline

supply that would otherwise be derived from petroleum sources, studies have estimated that the average American household is saving approxi-

mately $200 to $400 per year because of ethanol. That savings repre-sents dollars that can be spent at the establishments that make up your organization.

i was especially troubled by the statement in the article that, “…the organization (NCCR) has now vowed to devise a sustained effort to ad-dress these issues and fight for reformed policies, especially once the current VEETC and the tariff expire at the end of December.” [Emphasis added.] if this is an accurate description of the NCCR’s focus there must have been a significant effort to define and quantify the perceived threat. Once again, i would appreciate your sharing what the cost to the restau-rant industry is that you attribute to corn-derived ethanol.

As misguided as your policy position on ethanol is, your position on commodity speculation is right on. i would submit that is the real issue.

Chippewa Valley Ethanol Co. is owned by 900-plus members that have a direct or indirect connection to production agriculture. They will, I am sure, be keenly interested in why the National Council of Chain Res-taurants, which represents many eating establishments they frequent, has taken such a strong position against farming, national energy inde-pendence and rural economic development.

Mike JerkeGeneral Manager

Chippewa Valley Ethanol CompanyBenson, Minn.

correctionThe story “Good Digestion,” in the January issue of EPM, incorrectly

stated the anticipated annual production of biomethane at the Heyburn, ida-ho, anaerobic digester owned by Natural Chem Group LLC. Once upgraded, it will produce about 2 million MMBtu of pipeline quality biomethane.

FEBRUARY 2012 | Ethanol Producer Magazine | 7

TM

EDItOrIalEDITOR

Susanne retka Schill [email protected]

ASSOCIATE EDITORS Holly Jessen [email protected]

Kris Bevill [email protected]

COPY EDITOR Jan tellmann [email protected]

artART DIRECTOR

Jaci Satterlund [email protected]

GRAPHIC DESIGNERlindsey Noble [email protected]

PuBlISHINGCHAIRMAN

Mike Bryan [email protected]

CEO Joe Bryan [email protected]

VICE PRESIDENTtom Bryan [email protected]

SalES VICE PRESIDENT, SALES & MARKETING Matthew Spoor [email protected]

EXECUTIVE ACCOUNT MANAGER Howard Brockhouse [email protected]

SENIOR ACCOUNT MANAGER Jeremy Hanson [email protected]

ACCOUNT MANAGERSChip Shereck [email protected] Steen [email protected] Brown [email protected]

andrea anderson [email protected] austin [email protected]

CIRCULATION MANAGER Jessica Beaudry [email protected]

ADVERTISING COORDINATOR Marla Defoe [email protected]

SENIOR MARKETING MANAGER John Nelson [email protected]

EDItOrIal BOarDMike Jerke, Chippewa Valley Ethanol Co. LLLP

Jeremy Wilhelm, Cilion Inc.Mick Henderson, Commonwealth Agri-Energy LLC

Keith Kor, Pinal Energy LLCWalter Wendland, Golden Grain Energy LLC

Neal Jakel Illinois River Energy LLCBert farrish Lifeline Foods LLC

Eric Mosebey Lincolnland Agri-Energy LLCSteve roe Little Sioux Corn Processors LP

Bernie Punt Siouxland Energy & Livestock Co-op

Customer Service Please call 1-866-746-8385 or email us at [email protected]. Subscriptions to Ethanol Producer Magazine are free of charge to everyone with the exception of a shipping and handling charge of $49.95 for any country outside the United States, Canada and Mexi-co. To subscribe, visit www.EthanolProducer.com or you can send your mailing address and payment (checks made out to BBI International) to: Ethanol Producer Magazine Subscriptions, 308 Second Ave. N., Suite 304, Grand Forks, ND 58203. You can also fax a subscription form to (701) 746-5367. Back Issues, Reprints and Permissions Select back issues are available for $3.95 each, plus shipping.

Article reprints are also available for a fee. For more information, contact us at (866) 746-8385 or [email protected]. advertising Ethanol Producer Magazine provides a specific topic delivered to a highly targeted audience. we are committed to editorial excellence and high-quality print production. To find out more about Ethanol Producer Magazine advertising opportunities, please contact us at (866) 746-8385 or [email protected]. letters to the Editor we welcome letters to the editor. Send to Ethanol Producer Magazine Letters to the Editor, 308 2nd Ave. N., Suite 304, Grand Forks, ND 58203 or e-mail to [email protected]. Please include your name, address and phone number. Letters may be edited for clarity and/or space.

COPYRIGHT © 2012 by BBI International

Please recycle this magazine and remove inserts or samples before recycling

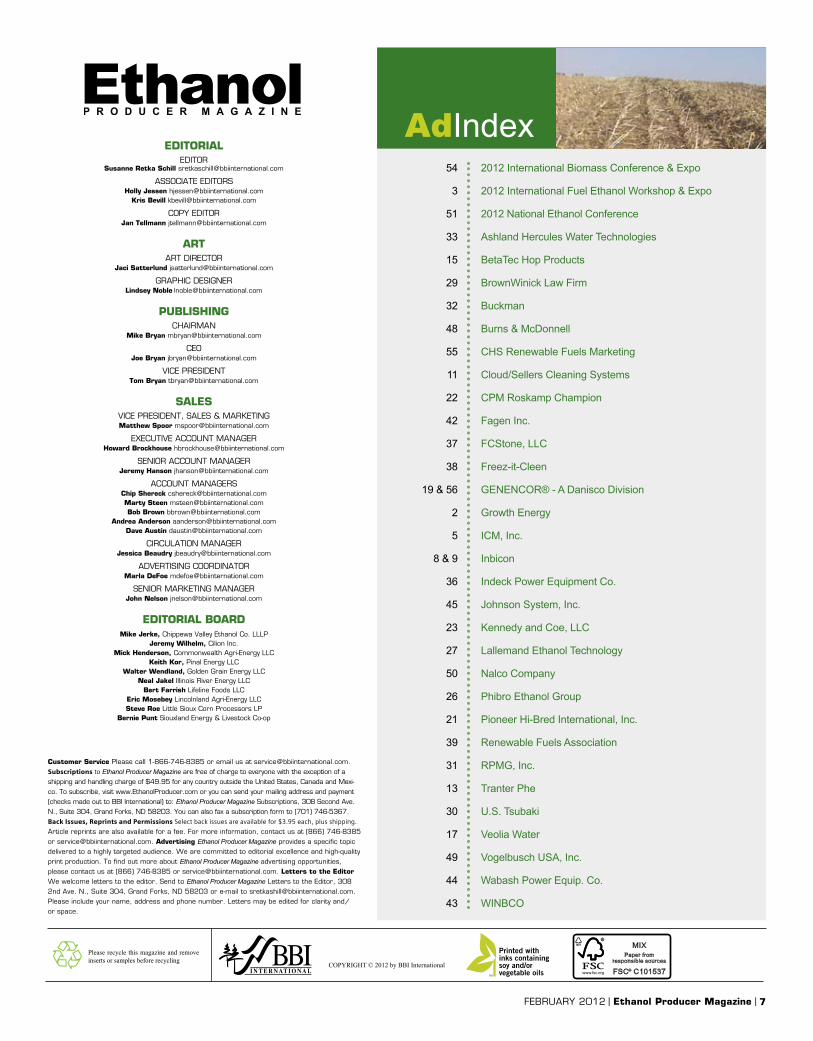

54 2012 international Biomass Conference & Expo

3 2012 international Fuel Ethanol Workshop & Expo

51 2012 National Ethanol Conference

33 Ashland Hercules Water Technologies

15 BetaTec Hop Products

29 BrownWinick Law Firm

32 Buckman

48 Burns & McDonnell

55 CHS Renewable Fuels Marketing

11 Cloud/Sellers Cleaning Systems

22 CPM Roskamp Champion

42 Fagen inc.

37 FCStone, LLC

38 Freez-it-Cleen

19 & 56 GENENCOR® - A Danisco Division

2 Growth Energy

5 iCM, inc.

8 & 9 inbicon

36 indeck Power Equipment Co.

45 Johnson System, Inc.

23 Kennedy and Coe, LLC

27 Lallemand Ethanol Technology

50 Nalco Company

26 Phibro Ethanol Group

21 Pioneer Hi-Bred international, inc.

39 Renewable Fuels Association

31 RPMG, inc.

13 Tranter Phe

30 U.S. Tsubaki

17 Veolia Water

49 Vogelbusch USA, inc.

44 Wabash Power Equip. Co.

43 WiNBCO

Adindex

The New Ethanol.

Refined, retailed,and rolling across America now.

The New Ethanol.

Refined, retailed,and rolling across America now.

10 | Ethanol Producer Magazine | FEBRUARY 2012

have you ever wondered what really drives the ethanol industry? Given the challenges it has faced over the years, it would seem as though it should have been dead and buried long ago. Thirty-five years later it’s still moving forward.

The progress can’t be credited to overwhelming consumer demand, ease of market penetration, lack of competition, or any of the normal things that propel most industries to success. in fact, just about every roadblock imaginable has been laid before this industry.

i have concluded that it’s pure passion. Passion for what we all believe to be for the greater good and passion for a cause has a profound effect on so many people living in rural communities and the country as a whole. So just below the surface of making a profit, there is an abiding sense of honor, pride and commitment that few other industries possess, or frankly even need to succeed.

i believe that without that sense

of pride and passion, we would have long ago been simply another chapter in the energy history book. instead, we’re making history, carving new innovative pathways to the world’s energy future. What began as a plan by President Carter to appease the public outrage over the Arab oil embargo, has become a national commitment that has spread globally. i doubt when President Carter called Archer Daniels Midland in 1977 and asked them to consider producing ethanol, he could have imagined what the real outcome of that call would be.

Those who have witnessed the grand opening of an ethanol plant and seen the pride well up in the eyes of farmers who struggled, sometimes for years, to find funding to build the plant, understand what i mean when i use the term passion. in the formative years of this industry, the decision to build wasn’t made in the boardroom on the 50th floor, it was made in the local cafe over coffee and donuts. it wasn’t a decision based on bottom line profits, it was a decision predicated on improving the lot of those in the community and building a future for the next generation to help keep them on the farm.

There are few industries indeed, that have survived and prospered solely on pride, passion and unyielding determination. Today’s ethanol industry

stands as a monument to those people who had the vision, the commitment and, yes, the passion to forge ahead when the odds were so stacked against them.

As we enter a new era of public policy for this industry, I am confident that it will not only survive, but will prosper like never before and move to the next level of excellence. The billions of dollars that America’s ethanol industry pumps into the economy and the contribution it makes to energy security and the wellbeing of rural communities will never be overshadowed by a few self-serving naysayers.

The Renewable Fuels Association’s National Ethanol Conference in Orlando, Fla., Feb. 22-24,will once again demonstrate to the world the vibrancy and passion of the ethanol industry. We’ll see you there.

That’s the way I see it!

the way i see it

The Power of Pride and PassionBy Mike Bryan

author: Mike BryanChairman, BBi international

FEBRUARY 2012 | Ethanol Producer Magazine | 11

events calendar

call for SpeakersThe FEW is the ethanol industry’s largest and longest running annual exchange of ideas, progress and

discovery. Don’t miss this unparalleled opportunity to share your knowledge and expertise with the largest assembled ethanol audience in the country.

National Ethanol ConferenceFebruary 22-24, 2012 Gaylord Palms Resort | Orlando, FloridaSince 1996, the RFA’s national ethanol conference has been recognized as the preeminent conference for delivering accu-rate, timely information on marketing, legislative and regulatory issues facing the ethanol industry. With numerous networking opportunities, pivotal business meetings are conducted that bring together some of the most influential companies and organizations in the ethanol industry. (202)315-2466 | www.nationalethanolconference.com

International Biomass Conference & ExpoApril 16-19, 2012Colorado Convention Center | Denver, Coloradoa new era in energy: the Future is growingOrganized by BBI International and coproduced by Biomass Power & Thermal and Biorefining Magazine, this event brings current and future producers of Bioenergy and biobased products together with waste generators, energy crop growers, municipal leaders, utility executives, technology providers, equipment manufacturers, project developers, investors and policy makers. it’s a true one-stop shop—the world’s premier educational and networking junction for all biomass industries. Presentation ideas are being accepted online.(866)746-8385 | www.biomassconference.com

International fuel Ethanol Workshop & ExpoJune 4 -7, 2012Minneapolis Convention Center | Minneapolis, Minnesotaevolution through innovationNow in its 28th year, the FEW provides the ethanol industry with cutting-edge content and unparalleled networking opportunities in a dynamic business-to-business environment. As the largest, longest running ethanol conference in the world, the FEW is renowned for its superb programming—powered by Ethanol Producer Magazine. Presentation ideas are being accepted online through Feb.10. (866) 746-8385 | www.fuelethanolworkshop.com

algae Biomass SummitSeptember 24-27, 2012Sheraton Denver Downtown Hotel | Denver, Coloradoadvancing technologies and Markets derived from algaeOrganized by the Algae Biomass Organization and coproduced by BBi international, this event brings current and future producers of biobased products and energy together with algae crop growers, municipal leaders, technology providers, equipment manufacturers, project developers, investors and policy makers. it’s a true one-stop shop—the world’s premier educational and networking junction for all algae industries.(866) 746-8385 | www.algaebiomasssummit.org

Jumbo™

Tankman™

Sellers 360

ROTATING WASH HEADS FOR ALL PROCESS VESSELS

Effi cient, Powerful, Dependable cleaning heads for tanks and fermenters up to 70 feet in diameter.

Unmatched versatility Low-maintenance operation Long-term reliability Industry specifi ed

Cloud/Sellers, 4120-A Horizon Lane, San Luis Obispo, CA 93401 USAPhone: 805-549-8093 Fax: 805-549-0131E-mail: [email protected] Web: www.cloudinc.com

2012 fuel Ethanol Workshop & ExpoSpeaker Presentation Deadline feb. 10Don’t Miss Your Opportunity to Present

Speakers at BBi international events enjoy:• Complimentary registration• Inclusion in both print and electronic marketing campaigns• Captive audience of key decision makers and stakeholders• Opportunity to appear in targeted ‘panel preview’ marketing efforts• Exposure to message through post conference presentation

Select from Four Presentation categories:track 1: Production and Operationstrack 2: Leadership and Financial Management track 3: Coproducts and Product Diversificationtrack 4: Cellulosic Ethanol

866-746-8385speakers@bbiinternational.comwww.fuelethanolworkshop.com

12 | Ethanol Producer Magazine | FEBRUARY 2012

view from the hill

The ILUC Debate, Four Years LaterBy Bob Dinneen

Four years ago, the biofuels industry was boorishly introduced to the theory of indirect land use change, or iluc. Timothy Searchinger’s now infamous article in the February 2008 edition of Science magazine boldly suggested increased corn ethanol production in the United States would lead to massive deforestation and conversion of grassland in nations halfway around the world. These hypothetical land conversions, he proffered, would release large amounts of stored carbon, indirectly making ethanol’s carbon footprint twice as bad as gasoline’s.

We knew it was a crazy theory four years ago. But it seems even crazier today, as the understanding of ethanol’s impact on land use has significantly progressed over the past four years. The scientific community has better data, improved modeling tools, and a better appreciation of the uncertainty and complexity involved in iLUC analysis. But, above all, they have the benefit of some experience and hindsight.

Real world data show that Searchinger was dead wrong in his predictions that ethanol expansion would cause U.S. farmers to plant fewer soybean acres, or that they would “…directly plow up more forest or grassland.” in fact, soybean acreage increased to record levels in 2008, 2009 and 2010. And a

recent report from USDA shows U.S. grassland has increased to its highest level since 1964 and forestland is at its highest point since 1978. Meanwhile, total U.S. cropland has dropped to its lowest level since USDA began collecting data in the 1940s. From 2002 to 2007 alone, cropland dropped by 34 million acres, or nearly 8 percent (incidentally, ethanol production tripled during that period).

Empirical data also prove wrong Searchinger’s notion that “higher prices triggered by biofuels will accelerate forest and grassland conversion” in South America. Data from Brazil’s Ministry of Science and Technology show dramatic reductions in Amazon deforestation over the past five years. In fact, 2010 saw the lowest level of deforestation since the government began collecting the data in 1988.

Academics have recently begun to examine this empirical data to scientifically test the Searchinger hypothesis. One recent study, led by Michigan State University Professor Bruce Dale, used a “bottom-up, data-driven, statistical approach,” to determine that biofuel production in the United States through 2007 “probably has not induced any indirect land use change.” Researchers at Oak Ridge National Laboratory similarly found “…minimal to zero indirect land use change was induced by use of corn for ethanol over the last decade.” The Oak Ridge findings are based on a rigorous examination of empirical data from the 2001-‘08 time period, a span in which U.S. ethanol production more than quadrupled.

While methods to empirically verify the past occurrence and magnitude of

iLUC continue to improve, the economic models used to predict potential future ILUC also are being refined. For instance, recent updates and improvements to Purdue University’s GTAP model resulted in a dramatic reduction of predicted iLUC emissions. in the latest Purdue analysis, the corn ethanol iLUC factor was found to be 14 grams CO2 equivalent per megajoule (g/MJ), compared to the value of 30 g/MJ used by California regulators and the EPA. A 2011 analysis conducted for the European Commission by the international Food Policy Research institute placed the corn ethanol iLUC factor at 10 g/MJ. Contrasting these latest estimates with Searchinger’s outrageous value of 104 g/MJ shows his worst-case analysis was simply out of touch with reality.

Unfortunately, advancements in the science of iLUC have not been mirrored by improvements in biofuels regulations that penalize ethanol for hypothetical ILUC emissions. California and EPA continue to rely on outdated and inflated estimates of iLUC, to the detriment of our industry. As highlighted by U.C. Berkeley economist David Zilberman at a recent Coordinating Research Council workshop (which RFA co-sponsored), the current regulatory treatment of iLUC is “pretentious,” “shifts attention from real problems,” and “creates uncertainty for investors.” We couldn’t agree more. And that’s why RFA continues to push for improvements in both the science and the policy of iLUC.

author: Bob DinneenPresident and CEO of the

Renewable Fuels Association(202) 289-3835

14 | Ethanol Producer Magazine | FEBRUARY 2012

drive

Reaping the Benefits of a Strong Biofuels IndustryBy Tom Buis

We are still at the beginning of the new year but, as expected, ethanol critics are wasting no time in attacking us. Last year, our opponents blocked our efforts to reform the blenders tax credit and open the transportation fuels market to true competition. Now they are focusing on the renewable fuel standard (RFS), which serves as a crucial support for the ethanol market.

The RFS was enacted by a bipartisan Congress as part of the 2005 Energy Policy Act, and expanded in 2007 under the Energy independence and Security Act. The RFS has been the single most effective tool at producing the only large-scale, commercially viable alternative to gasoline refined from oil—ethanol. Today, just four years into what is defined as a 15 year plan, we are on target to reach the 15 billion gallon threshold from grain-based ethanol. And with a continued commitment to the RFS, we can achieve the 36 billion gallon goal with cellulosic and advanced biofuel.

But, we must stick to the plan. Abandoning the RFS now would be a step backward. it would put OPEC further in control of our economy and perpetuate our addiction to foreign oil—an addiction that has significantly impacted our

national economy and our geopolitical standing. Over the last 40 years, we’ve spent trillions of dollars importing oil, often from nations that are corrupt, politically unstable or outright hostile to U.S. interests. We have been at constant war in the Middle East for the past 20 years for access to oil, at a cost of untold trillions in taxpayer dollars, the loss of more than 6,000 soldiers and creation of a whole new class of wounded warriors, thousands of whom will need long-term care funded by our government.

The intent of Congress when it wrote the renewable fuel standard was to grow an American fuels industry that would help us break free from this addiction and its dire consequences. in fact, the RFS is the only national energy policy in place designed to reduce our dependence on foreign oil through the increased use of biofuel. We can accelerate our progress toward reaching the RFS through the widespread use of E15 and installation of flex-fuel pumps.

Moving the nation to E15 will create 136,000 new jobs and will reduce carbon emissions the equivalent of taking 1.35 million cars off the road—and reduce the need to import 7 billion gallons of oil a day. And, a full move to E15 will send the right signals to investors, creating the market that will drive the growth and commercialization of cellulosic ethanol—ethanol produced from biomass feedstock, such as citrus waste, wood waste or corn stover—which is nearing commercial

viability. Today, several leading grain ethanol makers are nearing market-scale production for cellulosic ethanol and with the right market signals we will continue to see more producers enter the market.

The cellulosic ethanol industry will create significant jobs for rural communities, help deliver energy security to the U.S. and reduce harmful emissions in the air. The U.S. DOE’s Argonne National Laboratory found that cellulosic ethanol promises to reduce carbon emissions by 86 percent compared to gasoline.

While it may take some time to bring all the pieces together, we are well on our way to reaping the economic and national security benefits of a strong, domestic biofuels industry. A strong commitment to the RFS and an open fuels market will strengthen our energy security, generate more U.S. jobs that can’t be outsourced and improve our environment.

author: Tom BuisCEO, Growth Energy

(202)[email protected]

Put BetaTec® natural hop extracts to work in your fermentation process to replace antibiotics and enhance yeast propagation. IsoStab® is the natural way to effectively control gram-positive bacteria while eliminating antibiotics and harsh chemicals. Plus, antibiotic-free DDGS adds value to your co-products. VitaHop® Silver yeast nutrient enhances yeast performance and vitality, inducing faster fermentations and larger yields. Combined with BetaTec® fermentation expertise and training, these technologies will significantly increase your plant’s efficiency.

BetaTec®…the natural hop to higher profits. For more information specific to fuel ethanol producers, visit www.bthp.info.

www.betatechopproducts.com

16 | Ethanol Producer Magazine | FEBRUARY 2012

Grassroots voice

Ethanol’s Octane Provides Proactive OpportunityBy Brian Jennings

over the past 25 years, the american coalition for ethanol has recognized the need to be nimble and adapt tactics in pursuit of our mission to make american ethanol the consumer fuel of choice.

in 1987, our initial emphasis was to educate legislators in a few core states and sponsor ethanol-fueled dirt track races to familiarize mechanics and gas station owners with ethanol’s high-octane performance. Those efforts soon expanded to provide desperately needed policy leadership at the federal level and to educate petroleum marketers nationwide about the benefits and blending economics of ethanol. indeed, ACE took the initiative to be the first group to support enactment of a renewable fuels standard (RFS) in Congress and to sponsor studies on midlevel ethanol blends such as E30 which led to blender pump promotion.

in 2012, much of our focus will pivot to states to help ensure the remaining hurdles to E15 use are cleared. This will involve working with other groups to change laws and regulations at the state level and proactively promoting the benefits of E15 for consumers and petroleum marketers. We can and will apply the lessons we learned from the expansion of E10 use in the states to help make the transition to E15.

Congressional gridlock prevented the enactment of ethanol legislation last year, but that doesn’t mean federal energy policy stood still. To the contrary, President Obama rode herd over two landmark energy policy changes in 2011, rules controlling emissions from coal-fired power plants and proposed aggressive new fuel economy standards (corporate average fuel economy, or CAFE rules) for automobiles.

Given the ongoing partisan bickering and legislative logjam in Congress, which will likely worsen in this presidential election year, ACE will play an active role in the CAFE and other key federal rulemakings in 2012.

The new CAFE standards apply to light-duty vehicles beginning in model year 2017, requiring a nationwide average of 54.5 miles per gallon by model year 2025. While the automakers agreed to this overall fuel savings goal in negotiations with the Obama administration, it will nevertheless be very challenging for them to meet. In fact, unless refiners are compelled to clean up their fuel in tandem with new CAFE rules, automakers, at no fault of their own, will be unable to meet the new fuel economy standards and keep the air we breathe clean and safe. The reason is aromatics, which are classified as hazardous air pollutants.

This is where ethanol enters the picture, as the cleanest and most affordable form of octane on the planet. ACE will make the case in the CAFE and other rulemakings this year that if ethanol’s

clean octane is allowed to replace the toxic, expensive, and energy-inefficient aromatics (benzene, toluene, xylene) that refiners use to add octane to fuel, the resulting benefits will be substantial—reduced oil use, cleaner and safer air, and more demand for American-made ethanol.

Replacing benzene, toluene and xylene in transportation fuel with ethanol’s clean octane would be analogous to getting the lead out of gasoline and would set up the predicate for how we can someday fulfill a goal many in the industry have for widespread use of E30 or similar midlevel blends.

Tactically, focusing on these rulemakings allows ACE to go on offense for ethanol, doing an end-run on Congress in a way that could have a profound impact on the future of ethanol use. That is not to say we’re ignoring Capitol Hill. indeed, as we’ve indicated numerous times already, ACE and other groups will work together to protect the RFS in 2012 and address other legislative priorities.

in that spirit, i’ll close this month by encouraging everyone to participate in ACE’s upcoming grassroots fly-in to Washington, D.C., scheduled for March 27-28. i hope to see you in D.C. next month.

author: Brian JenningsExecutive Vice President,

American Coalition for Ethanol(605) 334-3381

HPD’s High Efficiency StillageConcentration System (HESC™)reduces energy consumption in theDDG drying process.

This proven, unique design concentrateshighly viscous stillage with minimalfouling while decreasing the evaporationload to the dryer. The benefits of theconcentrator system include:

> More efficient method of removingwater from stillage compared tostandard drying processes

> Concentrates syrup greater than 50% TS with minimal fouling

> Reduced natural gas usage decreasesemissions to allow more ethanolproduced for given air permit

> Modular system for simplifiedintegration into existing plants,expansions or new facilities

USA23563 W. Main Street, IL Route 126Plainfield, IL 60544Tel.: 815-609-2000Fax: 815-609-2044

SPAINAvenida de Neguri, 9 - 1˚48992 GetxoTel.: +34 94 491 40 92Fax: +34 41 491 11 40

Contact HPD for further information on the High Efficiency

Stillage Concentration System and completeevaporation and crystallization capabilities.

18 | Ethanol Producer Magazine | FEBRUARY 2012

europe callinG

A Pragmatic Approach to Fuel TaxationBy Robert Vierhout

one would think that a relatively easy way for governments to promote biofuels would be to tax biofuels less than fossil fuels—avoid lengthy debates on mandates and simply change the taxation structure in such a way that biofuels will have by far the competitive edge over fossil fuel. Unfortunately, it isn’t that straightforward to create such a level playing field in the EU.

Problem 1: Not only is an adjustment needed between taxing fossil fuels and biofuels, but also to balance the fuel market between diesel and gasoline. Under existing EU law, member states need to respect minimum levels of fuel taxation. These EU minimum levels are different between diesel (33 eurocents per liter) and gasoline (36 eurocents per liter). Not a huge difference, but member states can play with the tax level to promote one over the other and also to willingly distort the internal market. For example, diesel/gasoline taxes in eurocents per litre in Luxemburg is 32/46, in Germany, 47/66, whereas in the UK, 66/66. The highest tax for gasoline is in the Netherlands (80 eurocents) which has a diesel tax of only 42. Clearly, there are several other taxes that influence the consumer’s choice, but the fuel tax is decisive.

Problem 2: Changing the taxation

structure at EU level seems often more difficult than changing the EU treaty. Several states see fiscal change as intervening in what is considered, deep down, a national prerogative. The UK is a case in point. Equalizing the tax level in the entire EU would help in obtaining a balanced fuel market and undoing competition distortion—something the UK could only support. But the fact that Europe is determining the level of taxation nationally (even if these are indirect taxes) is unpalatable for the Brits.

Problem 3: Some EU member states gain a lot of money by keeping taxes on fossil fuel artificially low with the purpose either to support the trucking sector through low diesel prices or to boost sales of diesel to nonresidents. Take Luxemburg (500,000 inhabitants) luring lorries to their country with low fuel taxes. The result is that the neighboring country, Germany (75 million inhabitants), is losing revenues big time by having a diesel tax 15 eurocents per liter higher. The weird thing is that Germany doesn’t like the taxation proposal because the diesel car manufacturers, a major political force in Germany, fear loss of market share if taxes become more equal. Giving in to the car lobby means hundreds of millions of euros per year less tax income for the German state. The estimate is that for Luxemburg the extra income per capita is around 1,400 Euro per year.

The present energy taxation law results in perverse effects causing shortages of diesel, surpluses of gasoline,

discrimination of biofuels when taxed as fossil fuels and loss of government income when taxes are unequal in neighboring countries. So, change is needed, but any substantial progress does not seem to be happening.

Since April, member states are trying to agree on a more balanced tax law. After a delay of more than a year before the bill was put to the member states, the Polish president of the EU spent most of the past six months derailing the proposal, because it runs counter to Poland’s coal policy.

All hopes are now set for the first half of this year when the Danes hold the presidency. Even though a brand new government and not very experienced, the Danes want a pragmatic approach: Focus the law on what really will deliver a change in European transport fuel consumption by aligning taxation of diesel and gasoline and forget about all the other goodies, such as introducing a CO2-based tax, taxation on energy density or a higher tax on coal.

Such a pragmatic approach would resolve the perversities we are having with the present law. Even though it would not be the best possible outcome for biofuels in general, it would be still beneficial for ethanol in the long run. Fiscal equalization between fossil fuel will benefit gasoline and, hence, ethanol.

author: Robert VierhoutSecretary-general, ePURE

C

M

Y

CM

MY

CY

CMY

K

GEN-00811_PrintAd_Mountains_FINAL.pdf 1 5/27/11 9:18 AM

20 | Ethanol Producer Magazine | FEBRUARY 2012

business matters

The Ethanol IP EvolutionBy Camille L. Urban

Working with a firm that provides services to numerous ethanol plants provides an interesting outside/in perspective that has provided an opportunity to witness a present-day evolution.

Many ethanol plants were the result of a vision held by a group of investors, a design/build plan that included a license to a specified process, and a lot of hard work. But it wasn’t long until the operators of these plants began to add components to the design/build and to tweak conditions of the licensed process to produce ethanol better, faster, cheaper.

The evolution includes equipment and processes developed for production of value-added byproducts to extend the ethanol profit. During the past few years, the role of the process and equipment providers began to change, as well. Now, design/build providers design and build in cooperation with the ethanol company, rather than provide a turnkey, nearly take-it-or-leave it project. But this evolution is not without rough patches.

Now, the operators of the plants make adjustments, add components and tweak conditions of the processes provided for turnkey plants. A few of these improvements rise to the level of invention. And that raises an interesting question: Who owns the innovations made by those using the processes or equipment, when the original process or equipment was provided by another?

One would think that an entity supporting and/or funding the innovation (the ethanol plant) would be the hands-

down rightful owner, right? But the combination of inventor’s rights under United States patent law and the fine print in some of the provider contracts may obliterate that assumption.

inventors in the United States are the owners of their inventions unless a) there is a contract in place stating otherwise or, b) the inventor is an employee who invented something that is within the scope of his employment, in which case the employer owns the invention. For comfort and certainty related to scope of employment, it is advisable to include invention assignment obligations in all employment contracts.

Many of the provider contracts include an assignment provision that requires assignment to the provider of any improvements made by the plant to the process or equipment. You may want to read that sentence again. Technically, that means the provider owns the improvement and could exclude the very plant that developed the innovation from using it. You may want to dig out that agreement before you invest in improvements. if such a clause exists, the provider should be willing to pay for some of the development costs. More importantly, the process provider should agree to a royalty-free and perpetual license back to the plant. Many provider contracts have addressed this issue by including just such a license. The provider retains commercial benefit of the plant’s improvement; the plant retains a right to use.

What’s both wonderful and terrible about innovation, though, is that it is often the result of collaboration, with two

entities working toward, and finding, a solution to a problem. Without contractual obligations to the contrary, under United States patent law an invention resulting from such collaboration will be deemed jointly invented. This means either joint inventor may sell or license its interest to any other party it wishes and could result in no competitive advantage. Even if both parties wish to out-license the invention, there will quickly be a race to the bottom for royalty rates. What’s the remedy for this unfortunate situation? Careful drafting of an agreement BEFORE the collaboration begins is crucial to a happy ending. The terms should cover the uses allowed for each party and structure accounting as necessary. Further, the agreement must address later improvements made by only one of the parties.

it is important to remember that inventions and innovations are the logical and beneficial result of evolution. If you wish to enjoy the benefits of your own evolution in the ethanol production world, however, checking current agreement terms or drafting addendums may be a necessary evil.

author: Camille UrbanAttorney, Patents, Trademarks and Copyrights

BrownWinick Law Firm(515) 242-2451

Right Feedstock. Right Value.

More Ethanolper BushelMeasuring

the Results

Access to grain markets 24/7

BetterGrain Quality

PioneerQualiTrak®

System

DPPSM

Grain Desk

®, TM, SM Trademarks and service marks of Pioneer Hi-Bred. DPPSM is a service mark of Farms Technology.All purchases are subject to the terms of labeling and purchase documents. © 2011 PHII. ENDUS021973P238AVAR1

22 | Ethanol Producer Magazine | FEBRUARY 2012

800-366 -2563 | WATERLOO, IOWA

WWW.CPM.NET

When you need to perform maintenance, time wasted is money lost.

Reduce downtime—make your spare parts inventory THE prime directive of your maintenance department.

We will handle all of your hammermill spare parts needs. Call our parts sales department today for the professional service and expert advice you have come to expect from Roskamp Champion.

Preserve th e integrity of your mills.Use original replacement parts. Buy genuine Roskamp Champion parts.

ARE YOU STOCKED?

CPM Roskamp Champion

@CPMRoskamp

BuSINESS BRIEFS People, Partnerships & Deals

Greenville, s.c.,-based Lincoln Energy Solutions recently hired three new managers to bring industry expertise to the growing biofuels solutions supplier. Lar-ry Breeding joins lin-coln as a fuel specialist/product manager with experience in biodiesel production and engi-neering. Ralph Roberts has oversight for safety procedures, policies, customer reviews, staff management and fleet maintenance in the com-pany’s truck fleet. Tom-my Rose is responsible for bulk ethanol and biodiesel sales, serves as renewable identification number coordinator and manages the hedge desk.

John Castle has been appointed presi-dent and ceo of Aventine Renewable Energy Holdings Inc., having served as the interim ceo since August. he joined the company as chief financial officer in April and on July 20 was promoted to executive vice president and chief operating officer. The company also appointed Calvin Stewart as chief financial officer, having served as in-terim cFo since August.

ZeaChem Inc. added Nancy Buese as the third independent member and audit chair on its board of directors. she brings 20 years of financial leadership to the board and currently serves as senior vice president and chief financial officer of Denver-based Mark-West energy Partners lP.

Chase Lane has joined the technical op-timization team at Ferm solutions Inc. he will serve in the southwest, including Texas, south-west kansas, colorado and new Mexico. he joins the ethanol indus-try service provider with several years experience at the former hockley county ethanol plant in levelland, Texas.

John Harangody has been promoted to chief operating officer of Houston-based At-las Commodity Markets. he most recently held the same position with Atlas Grain in chicago and previously served as director of commodity products for cMe Group. “com-ing changes in the regulatory environment for oTc derivatives present challenges, but also significant opportunities,” Harangody said. “Atlas is in a strong position to assist our cus-tomers to successfully adapt to new market structures.”

Marquis Management Services Inc. has tapped Beth Steinhour to become its

director of environmen-tal affairs. With her 21 years of experience, Ja-son Marquis, company president, said steinhour will bring a new level of expertise to the regula-tory and environmental compliance issues that biorefineries face. “We believe with our plan for continued growth in the biorefining industry, Beth is a strategic addition to the Marquis Management team,” he said.

trucking Manager Ralph Roberts joins Lincoln Energy as general manager, transportation, overseeing all operation aspects related to the trucking fleet.

Biofuels traderTommy Rose brings a background as an ethanol trader to Lincoln Energy.

tech Support Chase Lane brings several years experience working at a Texas ethanol plant to his new position with Ferm Solutions.

consultant to director As senior consultant with Weaver Boos Consulting, Beth Steinhour advised ethanol, agrichemical and biomass facilities across illinois and the Midwest on development, permitting and compliance.

FEBRUARY 2012 | Ethanol Producer Magazine | 23

Sponsored by

business briefs

share your industry briefs to be included in business briefs, send information (including photos and logos if available) to: business briefs, Ethanol Producer Magazine, 308 second ave. n., suite 304, Grand forks nd 58203. you may also fax information to (701) 746-8385, or e-mail it to [email protected]. please include your name and telephone number in all correspondence.

Mark Beemer is the new president of R3Fusion Inc.’s ethanol division, respon-sible for the development and deployment of the ethanol water separation business for north America. he will oversee the manu-facturing partnerships, installation arrange-ments and operation startup of r3Fusions’ patented sPacer, water separation and pu-rification technology. Most recently Beem-er served as chief commercial officer for osage Bio Products and as a board member at hawkeye renewables llc.

Speedling Inc., specialists in feedstock

propagation, named four to its biomass feedstock advisory committee. Iowa state University assistant professor of agronomy Emily Heaton focuses on best manage-ment practices for perennial energy crops, with particular emphasis on miscanthus and switchgrass. Tom Voigt, associate professor and extension specialist in crop sciences at the University of Illinois-Urbana-cham-paign, leads the energy Biosciences Institute feedstock program and north central sun Grant feedstock partnership in miscanthus. Lynn Sollenberger, professor of grassland science, University of Florida, specializes in the ecology and management of tall grasses for bioenergy applications. John Caveny, president of environmentally correct con-cepts Inc., partnered with the University of Illinois in planting an on-farm miscanthus research plot in 2002, now the oldest re-search plot in the U.s. speedling propagates and sells plugs of the sterile Illinois clone of miscanthus from caveny Farm.

Poet LLC is more than 75 percent of the way to achieving its water reduction goal set in its environmental initiative dubbed “Ingreenuity.” With startup of the proprie-tary Total Water recovery system at its 18th ethanol production facility, Poet Biorefin-ing – Chancellor (S.D.), the company has

now reduced water use by more than 770 million gallons per year from 2009 use. The goal is to reduce water use by 1 billion gal-lons annually by 2015. chancellor’s Total Water recovery system saves the plant 131 million gallons of water per year. That sav-ings means chancellor uses 2.6 gallons of water for each gallon of ethanol produced, down from 3.5.

Interstates Companies has earned the Safety Training and Evaluation Process Dia-mond status, the highest safety designation awarded by Associated Builders and con-tractors Inc., for its safety performance. It is the only company to achieve this designa-tion in each of the four chapters it belongs to, Iowa, rocky Mountain, cornhusker and Arizona. headquartered in sioux center, Iowa, Interstates companies specializes in turnkey electrical systems for industrial, haz-ardous and value-added agriculture facilities, including ethanol plants.

In 2012, Lee Enterprises Consulting Inc. of little rock, Ark., intends to expand its services now concentrated on the biod-iesel sector into the ethanol, biomass, wind, solar and geothermal sectors. “We are cur-rently the world’s largest biodiesel consult-ing group, and most of our consultants and strategic partners are already very involved in the other alternative fuels,” said Wayne lee, principal owner. The group’s current appraiser, environmental expert, QA experts and grant writers have backgrounds and experience in these areas, and each of the group’s larger strategic partners—stoel rives (legal), Christianson & Associates (account-ing), IMA of Kansas (insurance), FCStone Merchant Services (feedstock financing), and executive leadership solutions (staff-ing) —already has a very significant pres-ence in these other alternative fuels sectors.

24 | Ethanol Producer Magazine | FEBRUARY 2012

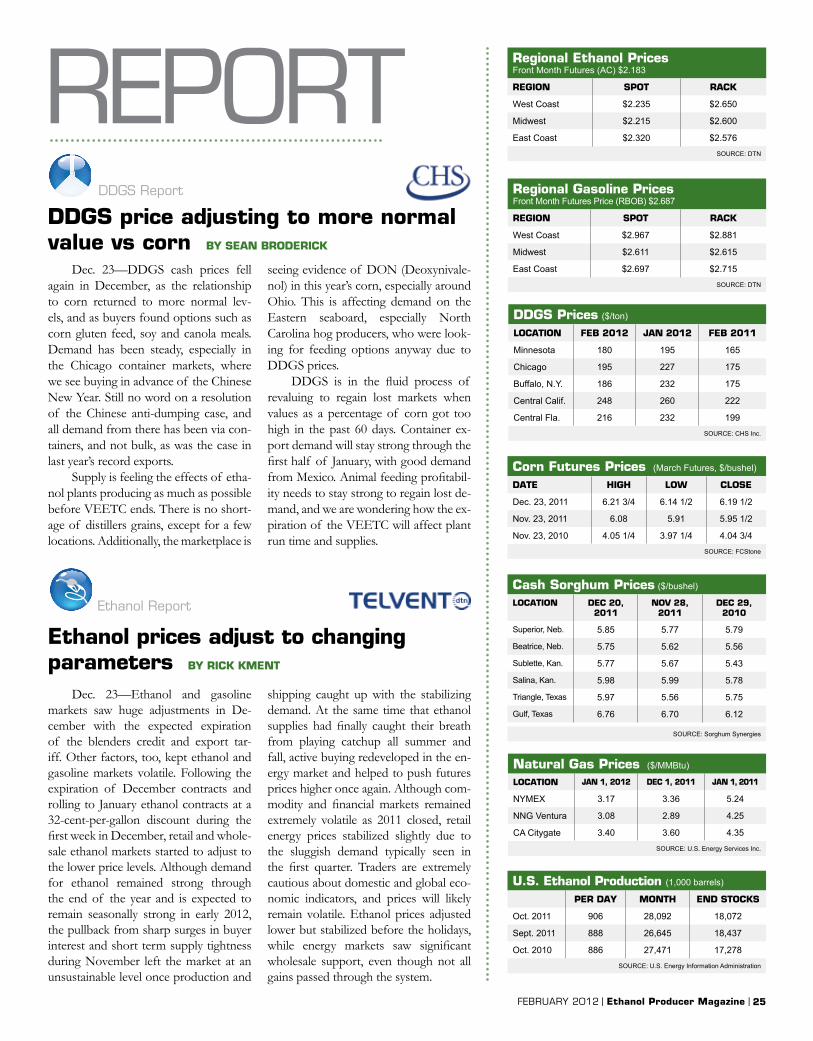

Dec. 23—It is useful to step back and look at a longer timeline. The accompanying chart shows the weekly, closing natural gas price for January 2012 on the nYMeX from 2007 to Dec. 22. It’s been quite a ride! The perceived value has varied from $11.46 per million Btu (MMBtu) in June 2008 to $3.13 on Dec. 12, a 73 percent drop. The average price has been $7.20 per MMBtu, 130 per-cent higher than the current price.

A killer combination of reduced de-mand and increased supply absolutely crushed prices. natural gas prices generally rallied from 2007 through mid-2008 as the economy boomed with increasing demand from robust housing construction, strong industrial demand and rapid development of natural gas-fired electric generation. The economy fell off the cliff in mid- to late 2008 and demand destruction started the precipi-tous price drop.

Prices flattened out in 2009 at about $7.50 per MMBtu as the economy stabi-lized. Then, supply-side shocks kicked in as the energy industry began to realize the size and scope of natural gas shale resources. We moved from a need to import to meet growing natural gas demand to concerns about excess supplies. Adding to the complexity, and facilitating price drops, was the fact that shale formations generally can be developed and operated profitably at much lower prices than traditional resources. soft demand, strong supply and changes in natural gas production economics explain

Natural Gas Report

Corn Report

Natural gas price chart shows collapse By CaSEy WHElaN

South american weather to impact market next By JaSON SaGEBIEl

COMMODItIES REPORT

Dec. 23—The grain markets observed new recent lows in December. March corn traded as low as $5.76 1/4 amidst turmoil in the eU and slowing global economy. The mar-ket began to exhibit short covering just before Christmas and was influenced by weather is-sues in Argentina and Brazil. Already, Argen-tine corn production has been forecast lower than the current USDA estimate of 29 million metric tons (mmt). Argentina’s production in 2010-’11 was 22.5 mmt. Argentina was ex-pected to export 20 mmt corn during 2011-’12 as compared to 15 mmt the previous year. The accompanying chart illustrates historical U.s. and Argentine corn exports.

The cash domestic market was tighter than normal during harvest, and basis levels a year ago at some processors were 30 to 40 cents wider than this fall. Producers were re-

luctant to make sales as prices slipped from summer highs. Ba-sis was strong as ethanol mar-gins remained robust into the fourth quarter.

The main change in the Dec. 9 USDA supply and de-mand report was to lower the food, seed and industrial sec-tor by 5 million bushels due to decreased sweetner produc-tion. carryout was 848 million bushels, up from the previous month, and down from last year’s 1.128 billion bushels. A year ago, the corn market rallied 24 cents on the mid-January USDA report as yield de-creased by 1.5 bushels per acre and carryout was estimated at 745 million bushels—a 5.5

why the market dropped by more than 70 percent in less than four years. What will the next four years bring? I doubt it will be another 70 percent drop; however, we have seen $1 in the past.

percent carryout-to-use ratio, one of the low-est figures to date. Since then, however, the market has experienced carryout-to-use ratios under that level.

FEBRUARY 2012 | Ethanol Producer Magazine | 25

DDGS Report

Ethanol Report

DDGS price adjusting to more normal value vs corn By SEaN BrODErICK

Ethanol prices adjust to changing parameters By rICK KMENt

COMMODItIES REPORT

DDGS Prices ($/ton)

lOCatION fEB 2012 JaN 2012 fEB 2011

Minnesota 180 195 165

Chicago 195 227 175

Buffalo, N.Y. 186 232 175

Central Calif. 248 260 222

Central Fla. 216 232 199SOURCE: CHS inc.

Natural Gas Prices ($/MMBtu)

lOCatION JaN 1, 2012 DEC 1, 2011 JaN 1, 2011

NYMEX 3.17 3.36 5.24

NNG Ventura 3.08 2.89 4.25

CA Citygate 3.40 3.60 4.35

SOURCE: U.S. Energy Services inc.

regional Ethanol Prices Front Month Futures (AC) $2.183

rEGION SPOt raCK

West Coast $2.235 $2.650

Midwest $2.215 $2.600

East Coast $2.320 $2.576SOURCE: DTN

regional Gasoline Prices Front Month Futures Price (RBOB) $2.687

rEGION SPOt raCK

West Coast $2.967 $2.881

Midwest $2.611 $2.615

East Coast $2.697 $2.715SOURCE: DTN

Corn futures Prices (March Futures, $/bushel)

DatE HIGH lOW ClOSE

Dec. 23, 2011 6.21 3/4 6.14 1/2 6.19 1/2

Nov. 23, 2011 6.08 5.91 5.95 1/2

Nov. 23, 2010 4.05 1/4 3.97 1/4 4.04 3/4SOURCE: FCStone

Cash Sorghum Prices ($/bushel)

lOCatION DEC 20, 2011

NOV 28, 2011

DEC 29, 2010

Superior, Neb. 5.85 5.77 5.79

Beatrice, Neb. 5.75 5.62 5.56

Sublette, Kan. 5.77 5.67 5.43

Salina, Kan. 5.98 5.99 5.78

Triangle, Texas 5.97 5.56 5.75

Gulf, Texas 6.76 6.70 6.12

SOURCE: Sorghum Synergies

u.S. Ethanol Production (1,000 barrels)

PEr Day MONtH END StOCKS

Oct. 2011 906 28,092 18,072

Sept. 2011 888 26,645 18,437

Oct. 2010 886 27,471 17,278SOURCE: U.S. Energy information Administration

Dec. 23—Ethanol and gasoline markets saw huge adjustments in De-cember with the expected expiration of the blenders credit and export tar-iff. other factors, too, kept ethanol and gasoline markets volatile. Following the expiration of December contracts and rolling to January ethanol contracts at a 32-cent-per-gallon discount during the first week in December, retail and whole-sale ethanol markets started to adjust to the lower price levels. Although demand for ethanol remained strong through the end of the year and is expected to remain seasonally strong in early 2012, the pullback from sharp surges in buyer interest and short term supply tightness during november left the market at an unsustainable level once production and

shipping caught up with the stabilizing demand. At the same time that ethanol supplies had finally caught their breath from playing catchup all summer and fall, active buying redeveloped in the en-ergy market and helped to push futures prices higher once again. Although com-modity and financial markets remained extremely volatile as 2011 closed, retail energy prices stabilized slightly due to the sluggish demand typically seen in the first quarter. Traders are extremely cautious about domestic and global eco-nomic indicators, and prices will likely remain volatile. ethanol prices adjusted lower but stabilized before the holidays, while energy markets saw significant wholesale support, even though not all gains passed through the system.

Dec. 23—DDGS cash prices fell again in December, as the relationship to corn returned to more normal lev-els, and as buyers found options such as corn gluten feed, soy and canola meals. Demand has been steady, especially in the chicago container markets, where we see buying in advance of the chinese new Year. still no word on a resolution of the chinese anti-dumping case, and all demand from there has been via con-tainers, and not bulk, as was the case in last year’s record exports.

supply is feeling the effects of etha-nol plants producing as much as possible before VeeTc ends. There is no short-age of distillers grains, except for a few locations. Additionally, the marketplace is

seeing evidence of DON (Deoxynivale-nol) in this year’s corn, especially around ohio. This is affecting demand on the eastern seaboard, especially north carolina hog producers, who were look-ing for feeding options anyway due to DDGS prices.

DDGS is in the fluid process of revaluing to regain lost markets when values as a percentage of corn got too high in the past 60 days. container ex-port demand will stay strong through the first half of January, with good demand from Mexico. Animal feeding profitabil-ity needs to stay strong to regain lost de-mand, and we are wondering how the ex-piration of the VeeTc will affect plant run time and supplies.

A Tradition of Industry Education

For 31 years, The Alcohol School has been educatingfuel ethanol and distilled beverage producers in thescience of alcohol production. The weeklong programme in Toulouse, France, is designed for lab,plant, and management personnel and is organizedaround a series of lectures and laboratory demonstrations presented by a faculty of academic,industry and Ethanol Technology Institute experts.

The programme will cover the process of ethanol andbeverage alcohol production from milling and mashpreparation through fermentation and distillation.Enzyme usage, yeast biology, bacterial contaminationand control will also be discussed along with otherissues currently affecting both industries.

Registration is limited, with preference given to fuelethanol and distilled beverage producers.

Additional information is available online atwww.ethanoltech.com.

6120 West Douglas AvenueMilwaukee, WI 53218 USA+1 414 393-0410Fax +1 414 358-8012

For More Information

ToulouseMercure Toulouse Atria

April 23–27, 2012

28 | Ethanol Producer Magazine | FEBRUARY 2012

Next up Abengoa in early planning for second cellulosic plant

It’s only been a few months since Aben-goa Bioenergy broke ground on its 23 MMgy multifeedstock cellulosic ethanol plant in hugoton, kan., but so far, construction of its first commercial-scale cellulosic facility is still “right on track,” according to Executive Vice President chris standlee, and should be ready for commissioning by the end of 2013. “We are very anxious to prove our technology at the commercial level and we are comfortable and confident that it’s going to be as expect-ed,” he says. “It will be efficient, effective and meet our expectations.”

The company is also already exploring options for the location of its second com-mercial-scale cellulosic plant, but won’t begin constructing that facility until 2014, after the hugoton plant is operational. “We’re not look-ing to start construction on a new facility in the immediate future by any means, but it’s never too early to be planning our next move,” standlee says.

Future Abengoa cellulosic plants will likely be co-located with its existing corn etha-nol facilities, primarily because the necessary infrastructure already exists in those locations. “We have the facilities, the roads, the offices, the relationships with the local producers and the states,” Standlee says. “So we’re just simply building on what we already have. It’s going to be much more efficient to do that.” Abengoa’s hub of ethanol production is in nebraska, where the company operates an 88 MMgy plant in ravenna and a 55 MMgy plant in York. Its cellulosic technology was also first proven at a pilot scale in York. other Aben-goa corn ethanol plants are located in kansas, new Mexico, Illinois and Indiana. The two smallest of those plants, the 30 MMgy plant in Portales, n.M., and the 25 MMgy plant in colwich, kan., were temporarily shut down at the end of the year due to depressed market conditions.

Doug Bice, corporate project develop-

ment manager at Abengoa Bioenergy, says that aside from logistical considerations, the avail-ability of biomass and other natural resources, namely water, will be major factors in the selec-tion of future cellulosic sites. “Water is a criti-cal component for functionality of the plant,” he says. While the hugoton plant is expected to use mostly corn stover and switchgrass as feedstocks, the company’s technology is multi-feedstock capable and future plants will need to be located near an abundance of various en-ergy crops and residues. “It’s difficult to build a facility and rely on dedicated energy crops because farmers are reluctant to plant those crops until a facility is constructed,” Standlee says. “For our next plant, we’ll be looking at ar-eas that have existing feedstocks available and the potential to develop more. Particularly, we think the dedicated feedstocks will have a great opportunity to provide the highest yields on a feedstock-per-acre basis.”

Abengoa has received numerous federal financial awards over the past few years to sup-port the Hugoton plant. In 2011 the USDA approved a Biomass crop Assistance Pro-gram project to assist in establishing switch-grass acres near the plant. The company also

received a $132.4 million loan guarantee from the U.S. DOE in late September. Standlee says government support has been instrumental in developing the hugoton plant and BcAP has been especially important in establishing new feedstocks. “one of the major challenges in the cellulosic industry is feedstock,” he says. “That’s not just in the growth of the feed-stock, but also the harvesting, the storage, the delivery. Any time you’re dealing with a brand new use for a feedstock there are challenges to overcome. The BcAP program has the poten-tial to ease the pain of developing cellulosic ethanol production.”

recent challenges to BcAP, federal loan guarantee programs and other federal incen-tives to support renewable energy industries make it difficult to predict whether financial assistance will be available to aid future Aben-goa projects and standlee says he’s not sure whether the company will continue to pursue those projects with federal backing. “We’re still in the process of trying to build hugoton and prove the economics at a commercial scale in that facility,” he says. “A lot of things can hap-pen in two or three years. We’ll see what hap-pens.” —Kris Bevill

distilled Ethanol News & Trends

Feedstock centric As Abengoa Bioenergy continues construction on its first commercial-scale cellulosic ethanol plant in Kansas, the company is making plans for the second. The availability of water is a prime concern, as is the availability of existing feedstocks and the potential to develop more.

PH

OTO

: BB

I IN

TER

NAT

ION

AL

FILE

PH

OTO

Ethanol News & Trends

distilled

A quick glance at the “Major Land Uses” report released in December by the USDA’s economic research service, reveals some in-teresting statistics about total cropland area. The report, which was first released in 1945, is compiled about every five years, coinciding with the latest census of Agriculture.

This year’s report is based on 2007 land uses and puts cropland at 408 million acres—the lowest level since the first records were taken in 1945. That’s 34 million acres, or 8 per-cent, below the previous low in 2002.

however, digging deeper into the re-port shows that the decline is partly due to a change in how the 2007 census of Agriculture estimated cropland pasture, one part of total cropland. From 2002 to 2007 there was a 26 million acre decline in cropland pasture, offset by a 27 million acre increase in grassland pas-ture and range. In other words, the method-ological change by the census of Agriculture meant millions of acres of cropland pasture were reclassified from temporary to perma-nent pasture. “Indeed, a comparison with na-tional resources Inventory data suggests that much of the change may be a result of the methodological change rather than an actual

land use change due to farm operator or owner decisions,” the report said. “Because of the change in methodology, these two estimates are not strictly comparable with prior years.”

What of ethanol’s po-tential impact on land use change, which critics have so loudly decried? The report does briefly address this ques-tion, concluding that since the data is presented only though 2007, it doesn’t address more recent developments. “In re-cent years, higher corn prices, driven partly by increased demand for corn as an ethanol feedstock, have contributed to complex changes in the production of princi-pal crops,” the report said.

It also examines data from a survey of corn and soybean farmers published in “The Ethanol Decade: An Expansion of U.S. Corn Production.” This USDA report found that expansions in corn acreage from 2006 to 2008 were a result of soybean farmers shifting acre-

age to corn production. That shift from soy to corn was offset, however, by other shifts, primarily cotton into soybeans. “Total acreage in harvested crops on corn and soybean farms expanded, with about a third of the increase due to shifts from hay and crP land, as well as increases in double-cropping and a reduction in idle land,” the land use report said. —Holly Jessen

Cropland Decline? USDA releases latest accounting of U.S. land uses

Principal u.S. crops harvested, 48 contiguous states, 2002-20072002 2007 1963-’81 1981-’07 2002-’07

Million acres Percent change

Food crops 130.8 126.9 78.3 -35.3 -4.0Feed crops

Corn, all 76.8 92.6 14.9 9.4 15.8Sorghum, all 7.7 7.2 -1.5 -8.3 -0.5Oats 2.1 1.5 -11.9 -7.9 -0.6Barley 4.1 3.5 -2.2 -5.5 -0.6Hay 64.5 61.0 -6.8 1.4 -3.5

total feed crops 155.2 165.8 -7.5 -10.9 10.6other crops 12.6 11.2 -3.2 -4.2 -1.4

total principal crops1 298.6 303.9 67.6 -50.4 5.21Distribution may not add due to rounding. Sources: USDA, Economic Research Service calculations based on data for principal crops harvested from Daugherty (1995) USDA/National Agricultural Statistics ervice (1999b, 2005, and 2009b).

30 | Ethanol Producer Magazine | FEBRUARY 2012

distilled

sales of e85 throughout 2011 in several Midwestern states easily exceeded their previ-ous year’s totals, according to data from the American lung Association and the Iowa re-newable Fuels Association. The increased de-mand can be attributed to growing consumer awareness of the fuel and consumers’ desire to

burn cleaner, domestically produced fuel, the groups say.

In Iowa, the nation’s top ethanol-pro-ducing state, e85 sales in 2011 had already topped the entire previous year by the end of september. nearly 9.8 million gallons of e85 were sold between January and september,

compared to a total of 9.3 million gallons in 2010. “It’s exciting to see Iowans increasing their commitment to mid-and high-level etha-nol blends,” IRFA Executive Director Monte shaw says. “e85 keeps money here at home and reduces our dependence on foreign oil. ethanol blends from e15 to e85 are the fu-ture for Iowa and America.”

consumers north of Iowa’s border are also consuming more e85. The American lung Association says Minnesota e85 sales were up 26 percent for the first eight months of 2011 compared to the same time period in 2010. Between January and August, the state’s retailers sold a whopping 14.2 million gallons of e85, compared to about 11.3 million gal-lons sold during the same months in 2010.

The state also made headway in increasing the amount of renewable fuels used in state vehicles. From January to september 2010, state agencies used about 724,800 gallons of E85. During the same months in 2011, that number was up by about 12,000 gallons. The Minnesota smartFleet committee says e85 now accounts for approximately 19 percent of its light-duty fuel purchases, which is an im-provement toward meeting the state directive of reducing gasoline use in state vehicles by 50 percent from the 2005 baseline by 2015.

North Dakota has also notably increased its use of e85 in the past year. The state’s re-tailers surpassed the 1 million gallon mark for the first time by the end of September, far exceeding the previous year’s total e85 sales of about 660,000 gallons. In 2009, only about 275,000 gallons of e85 were sold in the state. The sudden skyrocketing of e85 sales in North Dakota is at least partially due to a program launched in late 2009 that provides financial incentives to retailers who install blender pumps in the state. To date, there are about 71 E85 fueling stations in North Dako-ta, according to the AlA. Minnesota is home to more e85 stations than any other state and has about 360 sites. Iowa has nearly 160 e85 locations, according to the IrFA. —Kris Bevill

More Selections More Solutions Tsubaki: The choice for chain

E85 on the riseND E85 sales top 1 million gallons for first time; other states also show strong growth

FEBRUARY 2012 | Ethanol Producer Magazine | 31

distilled

financing BreakthroughMascoma gains support from Valero, DOE

Mascoma corp. received some early holiday presents that will help the company construct its commercial-scale hardwood cel-lulosic ethanol plant in kinross, Mich. Two weeks before christmas, it settled with Valero Energy Corp. for the oil refiner and ethanol producer to provide the majority of the fund-ing for the $232 million project to construct, commission and start up the facility. less than a week later, Mascoma announced up to $80 million in funding from the U.S. DOE, in ad-dition to $20 million previously awarded.

kinross cellulosic ethanol llc is a joint venture of Frontier renewable re-sources llc, a subsidiary of Mascoma, and Diamond Alternative Energy LLC, a subsid-iary of Valero. construction on the 20 MMgy cellulosic ethanol plant is expected to begin this spring and should be completed by late 2013.

Valero will hold a majority interest in the joint venture, provide project management during construction and operate the com-pleted plant. The oil refiner will also market the ethanol and has the option to expand the facility to up to 80 MMgy. A minority interest holder, Mascoma developed the proprietary consolidated bioprocessing (CBP) technolo-gy over the past five years and will also receive royalties based on ethanol yield milestones for a certain time period. The two will partner on additional cellulosic ethanol facilities.

“This partnership provides an exciting opportunity to combine Mascoma’s innova-tive cBP technology platform and expertise with Valero’s project management, operating, distribution and marketing capabilities,” says George stutzmann, Valero vice president of alternative energy. “We view this first com-mercial-scale cellulosic ethanol facility in kin-ross and our partnership with Mascoma as an important foundation for potential expansion beyond Kinross.” —Holly Jessen

Big GrowthBig River adds capacity

A fourth ethanol plant now bears the Big river name. Big river resources llc closed the acquisition of the former Western Wisconsin Energy LLC plant Dec. 1. “The plant continued operations as normal through the acquisition and continues to operate at full capacity as Big river Resources Boyceville LLC,” Jim Leiting, general manager of Big river resources tells ePM.

The 55 MMgy Boyceville, Wis., plant began producing ethanol in 2006. Big river resources

was formed as a cooperative but evolved into a joint venture holding company structured for multiple ethanol plants. The company operates ethanol plants in West Burlington, Iowa, and Gal-va, Ill., as well as being a majority shareholder and managing partner in a plant in Dyersville, Iowa. With the recent purchase, Big river resources’ plants have a combined capacity of 380 MMgy. The company is also an investor in Absolute energy llc, a 100 MMgy ethanol plant in st. Ansgar, Iowa, and owns a development site in Grinnell, Iowa, as well as 10 million bushels of grain holding capacity in five locations in Illinois. —Holly Jessen

distilled

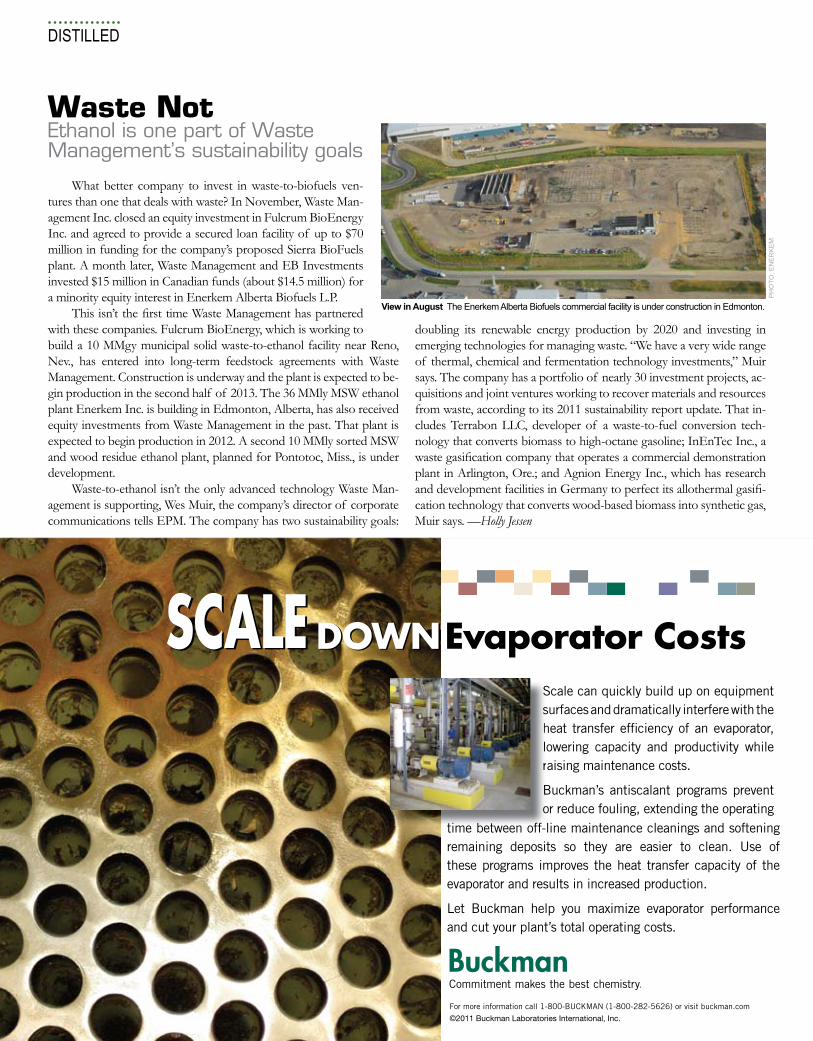

Waste NotEthanol is one part of waste Management’s sustainability goals

What better company to invest in waste-to-biofuels ven-tures than one that deals with waste? In november, Waste Man-agement Inc. closed an equity investment in Fulcrum Bioenergy Inc. and agreed to provide a secured loan facility of up to $70 million in funding for the company’s proposed sierra BioFuels plant. A month later, Waste Management and eB Investments invested $15 million in Canadian funds (about $14.5 million) for a minority equity interest in enerkem Alberta Biofuels l.P.

This isn’t the first time Waste Management has partnered with these companies. Fulcrum Bioenergy, which is working to build a 10 MMgy municipal solid waste-to-ethanol facility near reno, nev., has entered into long-term feedstock agreements with Waste Management. construction is underway and the plant is expected to be-gin production in the second half of 2013. The 36 MMly MsW ethanol plant enerkem Inc. is building in edmonton, Alberta, has also received equity investments from Waste Management in the past. That plant is expected to begin production in 2012. A second 10 MMly sorted MsW and wood residue ethanol plant, planned for Pontotoc, Miss., is under development.

Waste-to-ethanol isn’t the only advanced technology Waste Man-agement is supporting, Wes Muir, the company’s director of corporate communications tells EPM. The company has two sustainability goals:

doubling its renewable energy production by 2020 and investing in emerging technologies for managing waste. “We have a very wide range of thermal, chemical and fermentation technology investments,” Muir says. The company has a portfolio of nearly 30 investment projects, ac-quisitions and joint ventures working to recover materials and resources from waste, according to its 2011 sustainability report update. That in-cludes Terrabon llc, developer of a waste-to-fuel conversion tech-nology that converts biomass to high-octane gasoline; InenTec Inc., a waste gasification company that operates a commercial demonstration plant in Arlington, ore.; and Agnion energy Inc., which has research and development facilities in Germany to perfect its allothermal gasifi-cation technology that converts wood-based biomass into synthetic gas, Muir says. —Holly Jessen

View in august The Enerkem Alberta Biofuels commercial facility is under construction in Edmonton.

PH

OTO

: EN

ER

KE

M

For more information call 1-800-BUCKMAN (1-800-282-5626) or visit buckman.com

©2011 Buckman Laboratories International, Inc.

Scale can quickly build up on equipment surfaces and dramatically interfere with the heat transfer efficiency of an evaporator, lowering capacity and productivity while raising maintenance costs.

Buckman’s antiscalant programs prevent or reduce fouling, extending the operating

Sshlr

Bo

time between off-line maintenance cleanings and softening remaining deposits so they are easier to clean. Use of these programs improves the heat transfer capacity of the evaporator and results in increased production.

Let Buckman help you maximize evaporator performance and cut your plant’s total operating costs.

Evaporator Costs DOWN DOWN

With good chemistry great things happen.™

We off er more thanjust chemistry — we deliver improved profi tability.Armed with innovative chemistries and a thorough understanding of biorefi ning, Ashland is well positioned to help you operate more effi ciently and profi tably. Our state-of-the-art product portfolio for biorefi neries includes:

– Corn oil extraction aids – Ethanol corrosion inhibitors – Liquid/solid separation aids

– Boiler water treatments – Cooling water treatments – Wastewater treatments

To learn more, visit us online at ashland.com

® Registered trademark, Ashland or its subsidiaries, registered in various countries

™ Trademark, Ashland or its subsidiaries, registered in various countries

* Trademark owned by a third party© 2011, AshlandAD-11031

34 | Ethanol Producer Magazine | FEBRUARY 2012

risK manaGement

FEBRUARY 2012 | Ethanol Producer Magazine | 35

risK manaGement

The ethanol industry’s understanding of hedging has evolved over the years, making it a vital puzzle piece in profitable operationBy HOlly JESSEN