Embed Size (px)

Citation preview

Kampf gegen Steuerstraftaten – Zusammenarbeit

zwischen den zentralen

Meldestellen (FIUs)

Ex-post-Folgenabschätzung

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 1

Kampf gegen Steuerstraftaten: Ex-post-Evaluierung der Zusammenarbeit zwischen den

zentralen Meldestellen (FIUs - Financial Intelligence Units)

Studie

Als Reaktion auf die Veröffentlichung der sogenannten Panama-Papiere hat das Europäische Parlament am 8. Juni 2016 beschlossen, einen Untersuchungsausschuss einzusetzen, um mutmaßliche Verstöße gegen das Unionsrecht und Missstände bei dessen Anwendung im Zusammenhang mit Geldwäsche, Steuervermeidung und Steuerhinterziehung zu prüfen (PANA-Untersuchungsausschuss). Das Referat Ex-post-Folgenabschätzungen (IMPT) der Generaldirektion Wissenschaftlicher Dienst (GD EPRS) wurde in einem Beschluss der PANA-Koordinatoren vom 12. Oktober 2016 ersucht, eine Studie zu folgendem Thema vorzulegen: Kampf gegen Steuerstraftaten: Ex-post-Evaluierung der Zusammenarbeit zwischen den zentralen Meldestellen (FIUs) auf europäischer und internationaler Ebene.

Die Studie gliedert sich in zwei Teile: (1) eine vom Referat Ex-post-Folgenabschätzungen der Generaldirektion Wissenschaftlicher Dienst intern erstellte einleitende Analyse, die die FIUs in der EU und den EU-Rechtsrahmen zum Gegenstand hat, und (2) eine extern erstellte vergleichende Analyse, die sich auf die FIUs in Kanada, Frankreich, der Schweiz und dem Vereinigten Königreich konzentriert.

Zusammenfassung

Seit Mitte der 1990er Jahre hat die Entwicklung von Strategien zur Bekämpfung der

Geldwäsche auf internationaler Ebene zur Einrichtung zentraler Meldestellen (FIUs) auf

nationaler Ebene geführt. Diese dienen als nationale Zentren für die Entgegennahme und

Analyse von Meldungen verdächtiger Transaktionen. Sie sammeln und analysieren

Daten, anhand deren Verbindungen zwischen verdächtigen finanziellen Transaktionen

und illegalen Aktivitäten hergestellt werden können. Somit handelt es sich bei den FIUs

um wichtige Akteure bei der Verhinderung von Geldwäsche. Des Weiteren ist der

Informationsaustausch zwischen den FIUs angesichts der ausgeprägten

grenzüberschreitenden Dimensionen der Geldwäsche von maßgeblicher Bedeutung, um

sicherzustellen, dass illegale Geldströme ordnungsgemäß aufgedeckt und die

Strafverfolgungsbehörden in der Folge Ermittlungen aufnehmen. In der vorliegenden

Studie soll aufgezeigt werden, wie sich Rolle, Befugnisse und Tätigkeiten der FIUs bei

der Bekämpfung von Finanzkriminalität im Allgemeinen und von Steuerkriminalität im

Besonderen sowohl auf europäischer als auch internationaler Ebene derzeit darstellen.

Ex-post-Folgenabschätzungen

PE 598.603 2

VERFASSERIN der einleitenden Analyse:

Dr Amandine Scherrer, Referat Ex-post-Folgenabschätzungen

VERFASSER der vergleichenden Analyse: Dr. Anthony Amicelle (International Centre for Comparative Criminology, Université de Montréal, Quebec, Kanada) mit Julien Berg (École de Criminologie, Université de Montréal) und Killian Chaudieu (École des sciences criminelles, Université de Lausanne, Schweiz)

Die vergleichende Analyse wurde auf Ersuchen des Referats Ex-post-Folgenabschätzungen der Direktion Folgenabschätzungen und europäischer Mehrwert innerhalb der Generaldirektion Wissenschaftlicher Dienst (GD EPRS) des Europäischen Parlaments erstellt. DANKSAGUNGEN Die Verfasser danken den Beamten der Europäischen Kommission, den Teilnehmern der FIU-Plattform sowie den Interessenträgern, die für die vorliegende Studie befragt wurden, für ihre hilfreichen Beiträge. VERANTWORTLICH

Amandine Scherrer, Referat Ex-post-Folgenabschätzungen Um Kontakt mit dem Referat aufzunehmen, senden Sie bitte eine E-Mail an [email protected]

ÜBER DEN HERAUSGEBER

Dieses Dokument wurde vom Referat Ex-post-Folgenabschätzungen der Direktion Folgenabschätzungen und europäischer Mehrwert innerhalb der Generaldirektion Wissenschaftlicher Dienst (GD EPRS) des Generalsekretariats des Europäischen Parlaments zusammengestellt. Um Kontakt mit dem Referat aufzunehmen, senden Sie bitte eine E-Mail an [email protected] SPRACHFASSUNGEN Original: EN Dieses Dokument ist auch online über folgende Website abrufbar: www.europarl.europa.eu/thinktank HAFTUNGSAUSSCHLUSS UND URHEBERRECHTSSCHUTZ Dieses Dokument wurde für die Mitglieder und Mitarbeiter des Europäischen Parlaments erarbeitet und soll ihnen als Hintergrundmaterial für ihre parlamentarische Arbeit dienen. Die Verantwortung für den Inhalt liegt ausschließlich bei den Verfassern dieses Dokuments. Die darin vertretenen Auffassungen entsprechen nicht unbedingt dem offiziellen Standpunkt des Europäischen Parlaments. Nachdruck und Übersetzung – außer zu kommerziellen Zwecken – mit Quellenangabe sind gestattet, sofern das Europäische Parlament vorab unterrichtet und ihm ein Exemplar übermittelt wird. Redaktionsschluss: März 2017. Brüssel, © Europäische Union, 2017 PE 598.603 ISBN 978-92-846-0701-3 doi:10.2861/2427 QA-02-17-248-EN-N

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 3

Table of Contents Liste von Abkürzungen und Akronymen ..................................................................................... 5 List of tables and charts .................................................................................................................... 6 Methodik ............................................................................................................................................ 7

Teil I: Die zentralen Meldestellen in der EU und der geltende EU-Rechtsrahmen .......... 9 Wichtigste Ergebnisse ...................................................................................................................... 9 1. Die FIU im Kontext der internationalen Normen und EU Anforderungen ...................... 10 1.1. Einrichtung von FIUs im Umfeld der Bekämpfung der Geldwäsche .............................. 10 1.2. Grenzen und Möglichkeiten der Bewertung der Zusammenarbeit der FIUs bei der

Bekämpfung von Steuerstraftaten ................................................................................................ 13 2. Strukturen, Ressourcen und Kooperationskanäle der zentralen Meldestellen .................. 16 2.1. Strukturelle Unterschiede ....................................................................................................... 16 2.2. Ressourcen ................................................................................................................................ 18 2.3. Meldungen verdächtiger Transaktionen: verschiedene Quellen und unterschiedliche

Qualität ............................................................................................................................................. 19 2.4. Kooperationskanäle ................................................................................................................. 22 2.5. Zusammenarbeit und Informationsaustausch zwischen FIUs .......................................... 23 3. Hauptprobleme bei der Bekämpfung von Steuerstraftaten durch die zentralen

Meldestellen ....................................................................................................................... 25 3.1. Auf nationaler Ebene: Zusammenarbeit zwischen zentralen Meldestellen und

Steuerbehörden ............................................................................................................................... 25 3.2. Zugang zu Informationen über die wirtschaftlichen Eigentümer .................................... 28 3.3. Steuerbezogene Fälle als Hindernis für die europäische und die internationale

Zusammenarbeit ............................................................................................................................. 30 3.4. Bewertung des Kulturwandels der Branche ........................................................................ 32

Part II: Comparative analysis of Financial Intelligence Units (FIUs) in Canada,

France, Switzerland and United Kingdom .................................................................. 35 Executive summary ........................................................................................................................ 36 Introduction ..................................................................................................................................... 39 1. National financial intelligence units in practice ..................................................................... 41 1.1. ‘FININT’ – the evolution of priorities ................................................................................... 41 The (re)definition of dirty money ................................................................................................. 42 The (re)definition of FIU identity ................................................................................................. 45 1.2. Questioning reporting practices ............................................................................................ 52 Reporting suspicious transactions ................................................................................................ 53 Typology of suspicious transaction reports ................................................................................ 56 1.3. FININT in Numbers ................................................................................................................ 57 2. Transnational financial intelligence in practice ...................................................................... 70 2.1. European and international communication channels ....................................................... 70 The Egmont Secure Web ................................................................................................................ 71 FIU.NET 74 Other recognised cooperation channels ....................................................................................... 78 2.2. Financial intelligence cooperation in face of obstacles ....................................................... 78

Ex-post-Folgenabschätzungen

PE 598.603 4

(Lack of) capacity to respond to FIU requests............................................................................. 79 (Lack of) spontaneous dissemination and ‘abusive’ restriction ............................................... 82 2.3. Information sharing in numbers ............................................................................................ 83 Conclusion ....................................................................................................................................... 87 References ........................................................................................................................................ 89

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 5

Liste von Abkürzungen und Akronymen

CAD: Kanadischer Dollar

CRA: Canada Revenue Agency (Kanadische Steuerverwaltungsbehörde)

ESW: Egmont Secure Web

EU: Europäische Union

FATF: Financial Action Task Force (Arbeitsgruppe "Bekämpfung der

Geldwäsche und der Terrorismusfinanzierung")

FinCEN: Financial Crimes Enforcement Network (Finanzermittlungsbehörde),

Vereinigte Staaten von Amerika

FININT: Financial Intelligence (Ermittlungen im Finanzbereich)

Fintrac: Financial Transactions and Reports Analysis Centre of Canada (Zentrum

zur Untersuchung von Finanztransaktionen und -angaben in Kanada)

FIU: Financial Intelligence Unit (Zentralstelle für Geldwäsche-

Verdachtsanzeigen)

HoFIUs: Head of Financial Intelligence Units (Leiter der Zentralstellen für

Geldwäsche-Verdachtsanzeigen)

ICO: Information Commissioner's Office (Datenschutzbehörde)

IWF: Internationaler Währungsfonds

MROS: Money Laundering Reporting Office Switzerland (Meldestelle für

Geldwäscherei), Schweiz

NCA: National Crime Agency (Nationales Kriminalamt), Vereinigtes

Königreich

Tracfin: Traitement du renseignement et action contre les circuits financiers

clandestins (Geldwäschebehörde), Frankreich

SAR: Suspicious Activity Report (Meldung verdächtiger Tätigkeiten)

STR: Suspicious Transaction Report (Meldung verdächtiger Transaktionen)

Ex-post-Folgenabschätzungen

PE 598.603 6

List of tables and charts

Tabelle 1 – EU-Rechtsrahmen: Die wichtigsten Bestimmungen in Bezug auf die EU-FIUs ........................................................................................................................................................ 13

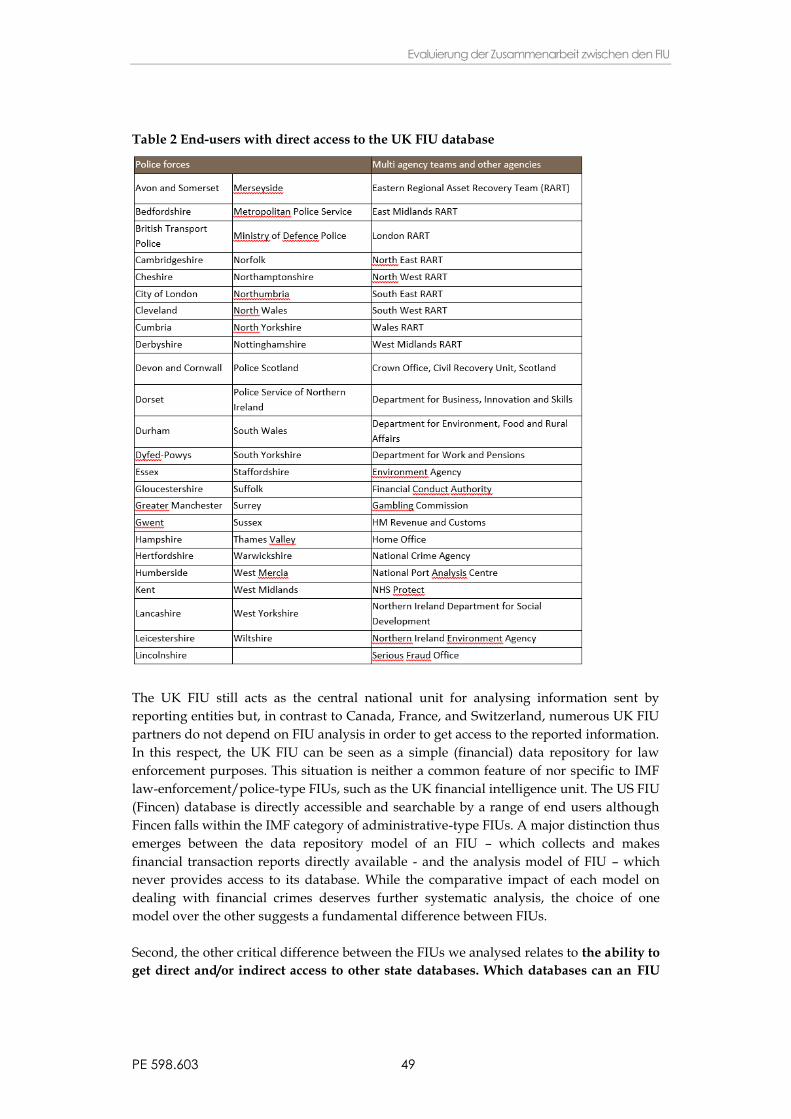

Table 2 End-users with direct access to the UK FIU database ............................................... 49

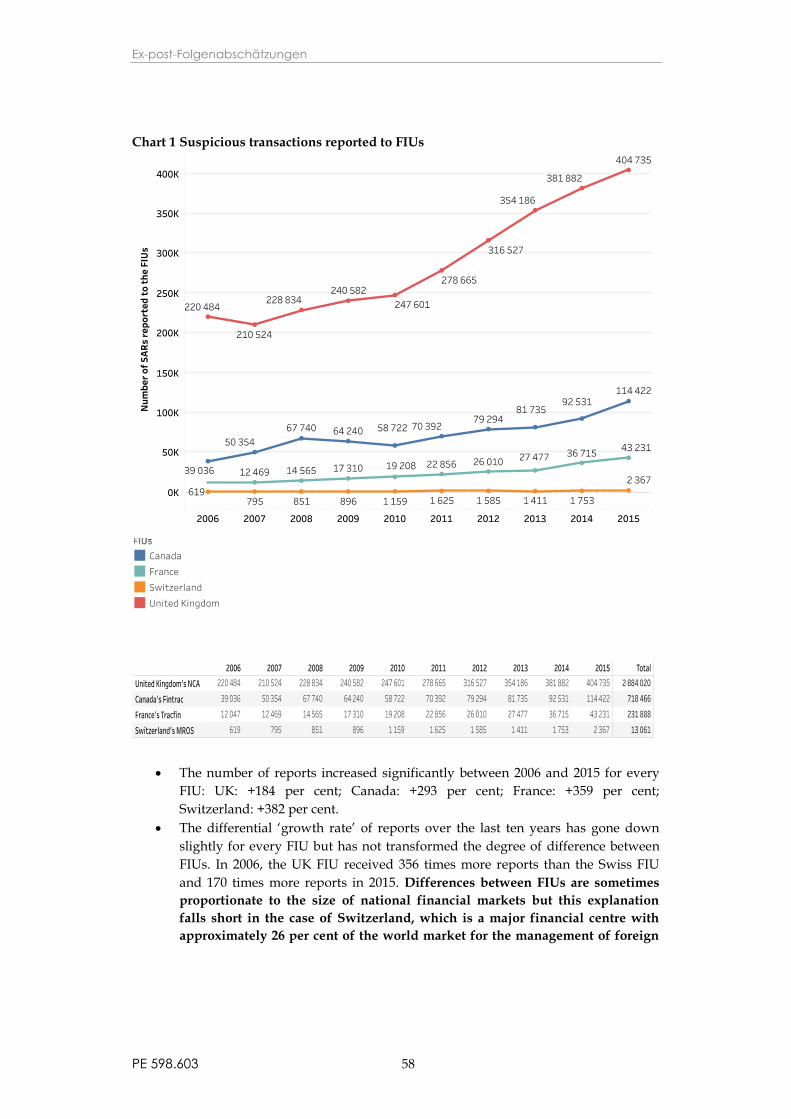

Chart 1 Suspicious transactions reported to FIUs ................................................................... 58

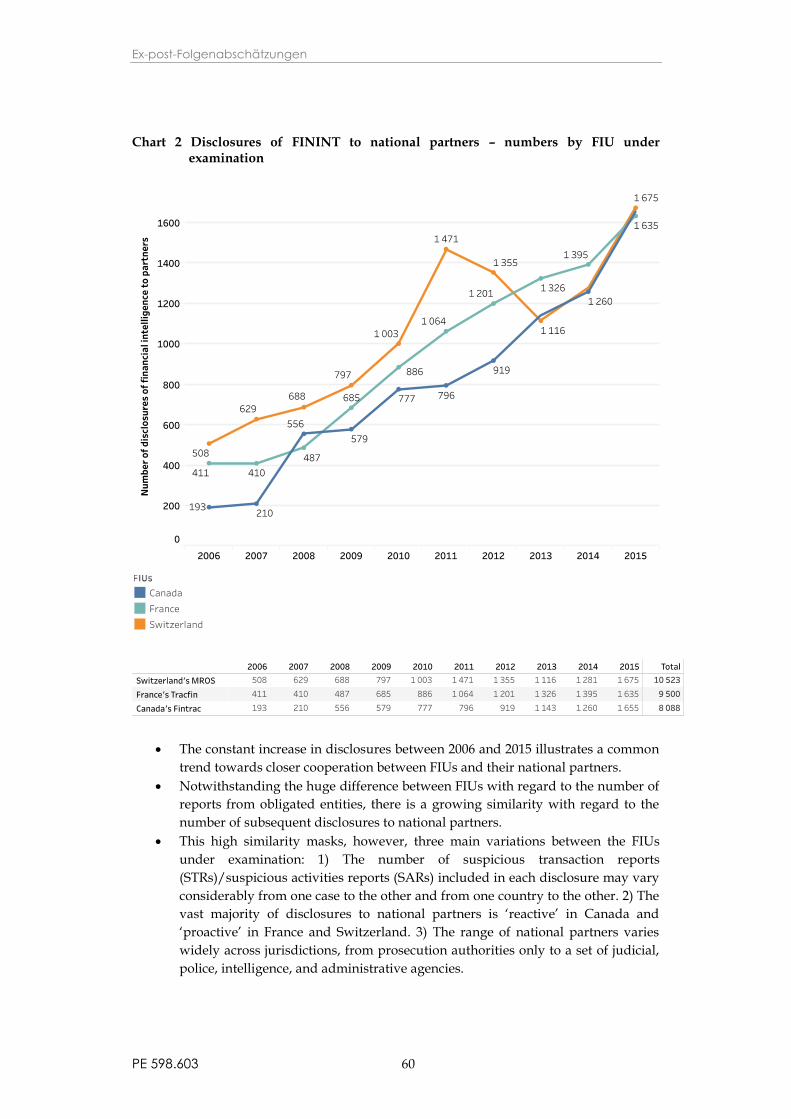

Chart 2 Disclosures of FININT to national partners ............................................................... 60

Chart 3 Switzerland’s FIU: suspicious transaction reports by predicate offence ................ 61

Chart 4 Switzerland’s FIU: suspicious transaction reports by reporting entity .................. 63

Chart 5 France’s FIU: suspicious transaction reports by reporting entity ........................... 64

Chart 6 France’s FIU: disclosures of FININT to partners ....................................................... 65

Chart 7 UK FIU: suspicious transactions reports by reporting entity .................................. 67

Chart 8 Canada’s FIU: financial transactions reports ............................................................. 68

Chart 9 Canada’s FIU: disclosures of FININT to partners ..................................................... 68

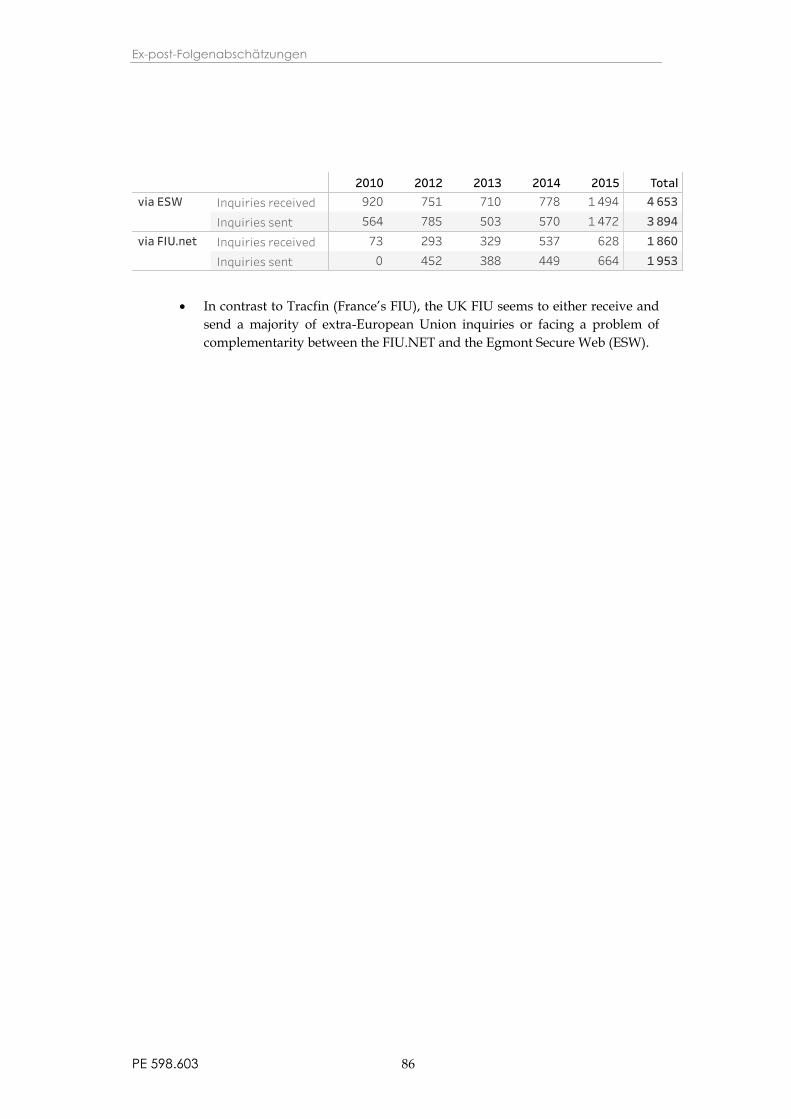

Chart 10 FIUs in Canada, France, Switzerland and the UK: Inquiries received/sent ........ 83

Chart 11 France’s FIU: information exchanged ....................................................................... 84

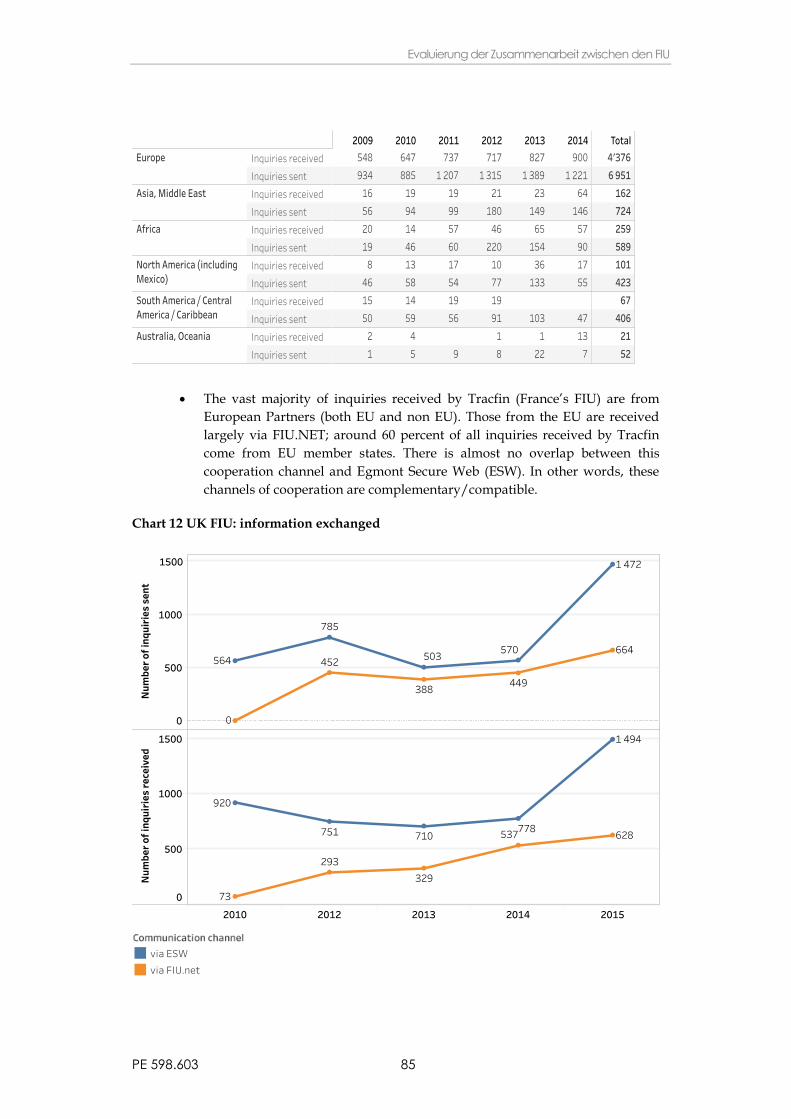

Chart 12 UK FIU: information exchanged ................................................................................ 85

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 7

Methodik

Die vorliegende Studie gliedert sich in zwei Teile: (1) eine vom Referat Ex-post-

Folgenabschätzungen der Generaldirektion Wissenschaftlicher Dienst intern erstellte

einleitende Analyse zu den zentralen Meldestellen in der EU (EU-FIUs) und dem EU

Rechtsrahmen und (2) eine extern erstellte vergleichende Analyse, die sich auf die FIUs in

Kanada, Frankreich, der Schweiz und dem Vereinigten Königreich konzentriert.

Ziel der einleitenden Analyse ist es, den EU-Rechtsrahmen für die EU-FIUs und deren

vorhandene Kapazitäten zur Bekämpfung der Steuerkriminalität zu analysieren. Es wird

daher untersucht, inwieweit die auf die FIUs bezogenen Bestimmungen der dritten

Geldwäscherichtlinie – die von den Mitgliedstaaten bis zum 15. Dezember 2007

umzusetzen waren – ordnungsgemäß zur Anwendung kommen. Zwar sind in der Studie

auch die mit der Annahme der vierten Geldwäscherichtlinie im Jahr 2015

vorgenommenen Änderungen berücksichtigt, doch werden keine voreiligen Schlüsse

hinsichtlich der ordnungsgemäßen Anwendung dieser neuen Vorschriften gezogen, da

die Mitgliedstaaten die vierte Richtlinie erst bis Ende Juni 2017 umsetzen müssen. Der

Untersuchung des EU-Rahmens liegen verschiedene Quellen zugrunde, die für die

Bewertung der Kapazitäten der EU-FIUs zur Erfüllung ihrer Aufgaben und zum

Informationsaustausch auf EU- und auf internationaler Ebene außerordentlich nützlich

waren.1 In der einleitenden Analyse ist selbstverständlich auch die extern erstellte

vergleichende Analyse berücksichtigt.2

Die vergleichende Analyse hat vier einzelne FIUs zum Gegenstand und untersucht die

Unterschiede und die Probleme, auf die diese im Rahmen der transnationalen

Zusammenarbeit bei Ermittlungen im Finanzbereich stoßen. Mit dieser Stichprobe, in der

FIUs aus zwei EU-Mitgliedstaaten (Frankreich und dem Vereinigten Königreich), eine

FIU eines europäischen Landes mit einem wichtigen Finanzplatz (Schweiz) und eine

nordamerikanische FIU (Kanada) betrachtet werden, soll aufgezeigt werden, wie sich

Rolle, Befugnisse und Tätigkeiten der FIUs bei der Bekämpfung von Finanzkriminalität

im Allgemeinen und von Steuerstraftaten im Besonderen derzeit darstellen. Die

vergleichende Analyse stützt sich sowohl auf qualitative als auch auf quantitative Daten.

Für ihre Erstellung wurden einerseits Dokumente ausgewertet (offizielle Berichte und

Statistiken der Egmont-Gruppe, der EU, der FATF und der untersuchten FIUs) und

andererseits teilstrukturierte Befragungen von Beamten der FIUs und Europols

durchgeführt.

1 Hierzu gehören: der Abschlussbericht 2013 zum ECOLEF-Projekt (The Economic and Legal Effectiveness of Anti-Money Laundering and Combating Terrorist Financing Policy, mit Mitteln der Europäischen Kommission, GD "Inneres" finanziert); ein im Jahr 2015 veröffentlichter Bericht der OECD: Improving co-operation between tax and anti-money laundering authorities. Access by tax administrations to information held by financial intelligence units for criminal and civil purposes; ein für die FIU-Plattform erstellter Bericht (2017): Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information.

2 Amicelle A., Berg J. und Chaudieu K., Comparative analysis of Financial Intelligence Units (FIUs) in Canada, France, Switzerland and the United Kingdom.

Ex-post-Folgenabschätzungen

PE 598.603 8

Die gesamte Studie wurde intern von Mitarbeitern des Referats Ex-ante-

Folgenabschätzungen (IMPA) der Generaldirektion Wissenschaftlicher Dienst fachlich

begutachtet; die einleitende Analyse wurde darüber hinaus auch Vertretern der FIU-

Plattform zur Stellungnahme vorgelegt.

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 9

Teil I: Die zentralen Meldestellen in der EU und der

geltende EU-Rechtsrahmen

Wichtigste Ergebnisse

Die zentralen Meldestellen der verschiedenen EU-Mitgliedstaaten unterscheiden sich

hinsichtlich ihrer Strukturen, Ressourcen und Befugnisse. Diese Unterschiede wirken sich

auf die Art und Weise aus, in der die EU-FIUs Informationen sammeln und analysieren,

und letztlich auch auf ihren Informationsaustausch untereinander:

(1) Auf praktischer Ebene beeinflussen zeitliche Verzögerungen bei der Beantwortung

von Ersuchen die Zusammenarbeit zwischen den FIUs negativ, und Qualität und Inhalt

der Antworten sind nicht unbedingt hilfreich.

(2) Nicht alle EU-FIUs sind befugt, Auskunftsersuchen an Banken und Finanzinstitute zu

richten. Demzufolge kann die Fähigkeit einiger FIUs, Informationen von meldenden

Stellen für ausländische FIUs einzuholen, unter Umständen beeinträchtigt sein.

Im Zusammenhang mit Steuerstraftaten treten spezielle Probleme auf:

(3) Steuerstraftaten wurden erst vor kurzem (in der vierten Geldwäscherichtlinie) als

Vortaten für Geldwäsche anerkannt. Auch wenn in der Richtlinie ausdrücklich

angegeben ist, dass Unterschiede zwischen den Definitionen von Steuerstraftaten in den

einzelstaatlichen Rechtsvorschriften dem Informationsaustausch zwischen den FIUs nicht

entgegenstehen dürfen, kann die FIU-Zusammenarbeit nach wie vor aufgrund der

Tatsache verweigert werden, dass sich die Definition und die Strafbewehrung von

Vortaten für Geldwäsche in den einzelnen Mitgliedstaaten erheblich voneinander

unterscheiden.

(4) In einigen EU-Mitgliedstaaten fehlt für die gegenseitige Amtshilfe zwischen FIU und

Steuerbehörden noch immer eine klare Übereinkunft und/oder Vereinbarung, um die

Einhaltung der Steuervorschriften sicherzustellen.

(5) Nicht alle EU-FIUs haben ausreichenden Zugang zu Informationen über die Inhaber

von Bankkonten und die wirtschaftlichen Eigentümer. Nicht in allen EU-Mitgliedstaaten

existieren zentrale Bankkontenregister. Zwar wird den EU-Mitgliedstaaten in der vierten

Geldwäscherichtlinie nahegelegt, solche Systeme einzurichten, doch ist dies nicht

verpflichtend. Was den Zugang zu Informationen über die wirtschaftlichen Eigentümer

angeht, so sind nicht alle Mitgliedstaaten bislang der in der vierten Geldwäscherichtlinie

niedergelegten Verpflichtung zur Einrichtung entsprechender Zentralregister

nachgekommen. Derzeit können sich daher nur einige wenige EU-FIUs solche

Informationen beschaffen. Zahlreiche EU-FIUs stimmen darin überein, dass dieses Fehlen

zentraler nationaler Spezialdatenbanken problematisch ist.

Ex-post-Folgenabschätzungen

PE 598.603 10

1. Die FIU im Kontext der internationalen Normen und EU

Anforderungen

1.1. Einrichtung von FIUs im Umfeld der Bekämpfung der

Geldwäsche

Auf internationaler Ebene:

Seit Anfang der 1990er Jahre Strategien zur Bekämpfung der Geldwäsche (anti-money

laundering – AML) auf nationaler Ebene (insbesondere in den USA) entwickelt und auf

internationaler Ebene verbreitet wurden, wurde die Einziehung der Erträge aus

Straftaten in zunehmendem Maße als wichtiges Instrument zur Bekämpfung der

Schwerkriminalität gesehen.3 Wie in einem Bericht des Internationalen Währungsfonds

(IWF) von 2004 über die FIUs4 hervorgehoben wird, stellten die Länder bei der

Entwicklung ihrer Strategien zur Bekämpfung der Geldwäsche fest, dass die

Strafverfolgungsbehörden nur begrenzten Zugang zu den einschlägigen

Finanzinformationen hatten. Folglich "wurde deutlich, dass die Länder das Finanzsystem

in ihre Strategien zur Bekämpfung der Geldwäsche einbeziehen und sich gleichzeitig

darum bemühen mussten, die notwendigen Voraussetzungen für sein wirksames

Funktionieren dauerhaft sicherzustellen"5. Die ersten FIUs wurden in den frühen 1990er

Jahren eingerichtet, da eine Zentralstelle zur Entgegennahme, Analyse und Weitergabe

von Finanzinformationen zur Bekämpfung der Geldwäsche erforderlich geworden war.6

Die FIUs wurden als spezialisierte Einheiten geschaffen, die sich mit der Analyse

verdächtiger finanzieller Transaktionen befassen, also mit anderen Aufgaben

(Intelligence-Analyse) als die Verfolgung von Straftaten (im Gegensatz zu

Verdachtsfällen).

1995 wurde auf Initiative der FIU der USA (FinCen) die "Egmont-Gruppe" (die eine

Kerngruppe von FIUs umfasst) gegründet; ihr Name ist vom Egmont-Arenberg-Palais in

Brüssel (Belgien) abgeleitet, in dem die erste Sitzung der Gruppe stattfand. Die Egmont-

Gruppe war ursprünglich als internationales und informelles Netzwerk von FIUs zur

Förderung und Verbesserung der internationalen Zusammenarbeit gedacht, die

3 Siehe: Woodiwiss M., "Transnational organized crime: The strange career of an American concept", in Beare M. (Hrsg.), Transnational Organized Crime, Ashgate, 2003; Scherrer A., G8 against

transnational organised crime, Ashgate, 2009.

4 IWF, Financial Intelligence Units: An Overview, 2004.

5 "... became clear that the strategy required them to engage the financial system in the effort to combat laundering while, at the same time, seeking to ensure the retention of the conditions necessary for its efficient operation.", IWF-Bericht, a.a.O., S. 1, Zitat aus Gilmore W.C., Dirty Money: The Evolution Of Money-Laundering Counter-Measures, Council of Europe Press, 1999, S. 103.

6 Siehe die vergleichende Analyse in Teil II: Amicelle A., Berg J. und Chaudieu K., Comparative analysis of Financial Intelligence Units (FIUs) in Canada, France, Switzerland and the United Kingdom. In dem Aufsatz werden die Entstehung und Weiterentwicklung der FIU eingehend beschrieben (siehe Abschnitt 1).

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 11

angesichts der Zunahme der grenzüberschreitenden Finanzströme zu einem

Schlüsselfaktor geworden war.7 Die Gruppe verfasste die erste Definition einer FIU:

Eine zentrale Meldestelle (FIU) ist eine zentrale nationale Stelle mit der Aufgabe,

zum Zwecke der Bekämpfung der Geldwäsche und der Terrorismusfinanzierung

Finanzinformationen entgegenzunehmen (und, soweit zulässig, um solche

Informationen zu ersuchen), sie zu analysieren und sie an die zuständigen

Behörden weiterzugeben, die i) mutmaßliche Erträge aus Straftaten und

potenzielle Terrorismusfinanzierung betreffen oder ii) aufgrund nationaler

Vorschriften oder Regelungen erforderlich sind.

Das Sekretariat der Egmont-Gruppe befindet sich seit 2008 in Toronto (Kanada); zum

Zeitpunkt der Abfassung dieses Textes besteht die Gruppe aus 152 Mitgliedern.8

2003 nahm die Arbeitsgruppe "Bekämpfung der Geldwäsche und der

Terrorismus¬finanzierung" (Financial Action Task Force , FATF) – das 1989 eingerichtete

zwischenstaatliche Gremium, das Normen festlegt und eine wirksame Durchführung

rechtlicher, regulatorischer und operativer Maßnahmen zur Bekämpfung von

Geldwäsche fördert – eine überarbeitete Reihe von Empfehlungen zur Geldwäsche an;

erstmals waren ausdrücklich Empfehlungen zur Einrichtung und zur Funktionsweise

von FIUs vorgesehen, die von der oben erwähnten Definition der Egmont-Gruppe

abgeleitet sind:

(Empfehlung 26): Die Länder sollten eine FIU einrichten, die als nationales

Zentrum zur Entgegennahme (und, soweit zulässig, zum Abfragen), zur Analyse

und Weitergabe von Meldungen verdächtiger Transaktionen und anderen

Informationen bezüglich potenzieller Geldwäsche oder Terrorismusfinanzierung

dient. Die FIU sollte direkt oder indirekt rechtzeitig Zugang zu den Finanz-,

Verwaltungs- und Strafverfolgungs¬informationen erhalten, die sie zur

ordnungsgemäßen Wahrnehmung ihrer Aufgaben benötigt, zu denen auch die

Analyse von Meldungen verdächtiger Transaktionen gehört.9

Was die Zusammenarbeit angeht, so hat die Egmont-Gruppe seit ihrer Anfangsphase die

Festlegung von Vereinbarungen und Mustern für gemeinsame Absichtserklärungen

zwischen FIUs weltweit ermöglicht.10

7 Egmont Group, Annual report, 2015; Siehe: United State General Accounting Office - GAO, Statement submitted to the Subcommittee on General Oversight and Investigations, Committee on Banking and Financial Services, House of Representatives, FinCen's Law enforcement Support, Regulatory, and International Roles, 1998, GAO/T-GDD-98-83. 8 Egmont-Gruppe website. 9 Financial Action Task Force (FATF), Recommendations, 2003. 10 Neueste Fassung dieser Grundsätze siehe: Egmont Group, Principles for information exchange between FIUs, Juni 2013, abrufbar auf der Website der Egmont Gruppe. 10 So ausgeführt in Erwägungsgrund 2 des Beschlusses des Rates vom 17. Oktober 2000 über Vereinbarungen für eine Zusammenarbeit zwischen den zentralen Meldestellen der Mitgliedstaaten beim Austausch von Informationen (2000/642/JI).

Ex-post-Folgenabschätzungen

PE 598.603 12

Auf europäischer Ebene:

Die FIUs sind zwar nicht explizit genannt, wurden aber bereits in der ersten und zweiten

Geldwäscherichtlinie der EU aus den Jahren 1991 und 2001 als die Behörden in Betracht

gezogen, die für die Entgegennahme und Analyse von Meldungen verdächtiger

Transaktionen zuständig sein sollten. Seit 2000 bestehen in allen EU-Mitgliedstaaten

FIUs, welche Informationen sammeln und analysieren, damit zum Zwecke der

Verhinderung und Bekämpfung der Geldwäsche Zusammenhänge zwischen

verdächtigen Finanztransaktionen und zugrunde liegenden kriminellen Tätigkeiten

hergestellt werden können.11

In der ersten Geldwäscherichtlinie12, die 1991 erlassen wurde, wurden Regelungen für

die Meldung verdächtiger Transaktionen festgelegt. Im Aktionsplan zur Bekämpfung der

organisierten Kriminalität, der 1997 vom Europäischen Rat auf seiner Tagung in

Amsterdam gebilligt wurde, wurde empfohlen, die Zusammenarbeit zwischen den

Kontaktstellen, die nach der genannten ersten Geldwäscherichtlinie für die

Entgegennahme von Meldungen verdächtiger Transaktionen zuständig waren, zu

verbessern. Dies führte zum Erlass des Beschlusses des Rates vom 17. Oktober 2000 über

Vereinbarungen für eine Zusammenarbeit zwischen den zentralen Meldestellen der

Mitgliedstaaten beim Austausch von Informationen.13 In diesem Beschluss wurden die

Vorschriften für die Organisation der FIU auf der Ebene der Mitgliedstaaten und für die

Zusammenarbeit zwischen ihnen festgelegt. Außerdem wurden spezifische Vorschriften

hinsichtlich gesicherter Meldewege zwischen den EU-FIUs festgelegt, woraufhin in den

Jahren 2007-2008 das FIU.NET mit finanzieller Unterstützung der Europäischen

Kommission eingerichtet wurde.

In der zweiten Geldwäscherichtlinie14, die 2001 erlassen wurde, wird zwar nicht explizit

auf die FIU Bezug genommen, aber es werden die "für die Bekämpfung der Geldwäsche

zuständigen Behörden" genannt und es wird eine weiter gefasste Definition von

Geldwäsche verwendet, bei der zugrunde liegende Straftaten wie etwa Bestechung

berücksichtigt werden und somit das Spektrum von Vortaten erweitert wird.

Mit der 2005 erlassenen dritten Geldwäscherichtlinie15 wurde das Ziel der Bemühungen

der EU zur Bekämpfung der Geldwäsche ausgedehnt, indem der Geltungsbereich der

11 So ausgeführt in Erwägungsgrund 2 des Beschlusses des Rates vom 17. Oktober 2000 über Vereinbarungen für eine Zusammenarbeit zwischen den zentralen Meldestellen der Mitgliedstaaten beim Austausch von Informationen (2000/642/JI).

12 Richtlinie 91/308/EWG des Rates vom 10. Juni 1991 zur Verhinderung der Nutzung des Finanzsystems zum Zwecke der Geldwäsche.

13 Beschluss des Rates vom 17. Oktober 2000 über Vereinbarungen für eine Zusammenarbeit zwischen den zentralen Meldestellen der Mitgliedstaaten beim Austausch von Informationen.

14 Richtlinie 2001/97/EG des Europäischen Parlaments und des Rates vom 4. Dezember 2001 zur Änderung der Richtlinie 91/308/EWG des Rates zur Verhinderung der Nutzung des Finanzsystems zum Zwecke der Geldwäsche.

15 Richtlinie 2005/60/EG vom 26. Oktober 2005 zur Verhinderung der Nutzung des Finanzsystems zum Zwecke der Geldwäsche und der Terrorismusfinanzierung.

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 13

Anforderungen zur Bekämpfung der Geldwäsche auf schwere Straftaten und

Terrorismusfinanzierung ausgeweitet wurde. Darüber hinaus wird darin ausdrücklich

verlangt, dass die Mitgliedstaaten nationale FIUs einrichten.

Die Europäische Kommission ist beauftragt, Unterstützung zu leisten, um die

Koordinierung, einschließlich des Informationsaustauschs zwischen den FIUs innerhalb

der Gemeinschaft, zu erleichtern (Artikel 38 der dritten Geldwäscherichtlinie). 2006

richtete die Kommission die Plattform der zentralen Meldestellen der EU ein, die die EU-

FIUs miteinander verbindet und ihre Zusammenarbeit fördert.16

1.2. Grenzen und Möglichkeiten der Bewertung der Zusammenarbeit

der FIUs bei der Bekämpfung von Steuerstraftaten

Steuerstraftaten werden nicht von allen EU-FIUs unbedingt einheitlich behandelt, da

diese Straftaten in einigen Mitgliedstaaten nicht als Vortaten für die Geldwäsche

angesehen werden. Obgleich in der vierten Geldwäscherichtlinie ausdrücklich auch

"Steuerstraftaten" als Vortaten für Geldwäsche erfasst werden, wird darin keine

Harmonisierung der Definition auf EU-Ebene vorgenommen. Es fehlt eindeutig ein

Konsens über Steuerstraftaten, wie in Abschnitt 3 ausgeführt wird.

Zudem ist zum Zeitpunkt der Abfassung dieses Textes die Umsetzung der neuen

Bestimmungen, die mit der vierten Geldwäscherichtlinie17 von 2015 eingeführt wurden,

schwer zu beurteilen. In der Tat sind diese Bestimmungen von den Mitgliedstaaten im

Einklang mit Artikel 67 der vierten Richtlinie bis Ende Juni 2017 umzusetzen. Die

nachstehende Tabelle gibt einen Überblick über die wichtigsten Bestimmungen der

dritten und der vierten Geldwäscherichtlinie in Bezug auf die FIUs. Wie daraus

hervorgeht, wird in der vierten Richtlinie die Organisation der Zusammenarbeit

zwischen den EU-FIU sehr viel genauer geregelt:

Tabelle 1 – EU-Rechtsrahmen: Die wichtigsten Bestimmungen in Bezug auf die EU-FIUs

Dritte Geldwäscherichtlinie (2005) Zusätzliche Bestimmungen in der vierten Geldwäscherichtlinie von 2015, bis Juni 2017 umzusetzen

Jeder Mitgliedstaat richtet eine zentrale Meldestelle zur Bekämpfung der Geldwäsche und der Terrorismusfinanzierung (Artikel 21 Absatz 1).

Über den Zugang zu Informationen:

Die Mitgliedstaaten schreiben vor, dass die zuständigen Behörden und die zentralen Meldestellen zeitnah auf die Angaben zu den rechtlichen und wirtschaftlichen Eigentümern zugreifen können (Artikel 30 Absatz 2). Angaben zu den wirtschaftlichen Eigentümern müssen in

16 Die EU-FIU-Plattform hat keinen operationellen Charakter. Sie soll Diskussionen erleichtern und den Austausch bewährter Verfahren auf EU-Ebene zwischen den FIU ermöglichen. Die Sitzungen der Plattform finden in der Regel vierteljährlich statt.

17 Richtlinie (EU) 2015/849 vom 20. Mai 2015 zur Verhinderung der Nutzung des Finanzsystems zum Zwecke der Geldwäsche und der Terrorismusfinanzierung.

Ex-post-Folgenabschätzungen

PE 598.603 14

Dritte Geldwäscherichtlinie (2005) Zusätzliche Bestimmungen in der vierten Geldwäscherichtlinie von 2015, bis Juni 2017 umzusetzen

Zur Erfüllung ihrer Aufgaben wird jede nationale zentrale Meldestelle mit angemessenen Mitteln ausgestattet (|Artikel 21 Absatz 2).

Die zentralen Meldestellen müssen rechtzeitig Zugang zu den Finanz-, Verwaltungs- und Strafverfolgungsinformationen erhalten, die sie zur ordnungsgemäßen Erfüllung ihrer Aufgaben benötigen (Artikel 21 Absatz 3).

Die dieser Richtlinie18 unterliegenden Institute und Personen müssen die zentrale Meldestelle umgehend informieren, wenn sie den Verdacht haben, dass eine Geldwäsche oder Terrorismusfinanzierung begangen oder zu begehen versucht wurde oder wird. Sie müssen ferner auf Verlangen alle erforderlichen Auskünfte erteilen (Artikel 22 Absatz 1).

Die Mitgliedstaaten müssen vorschreiben, dass ihre Kredit- und Finanzinstitute Systeme einrichten, die es ihnen ermöglichen, auf Anfragen der zentralen Meldestelle gemäß ihrem nationalen Recht vollständig und rasch Auskunft zu geben (Artikel 32).

allen Fällen und ohne Einschränkung für die zentralen Meldestellen zugänglich sein (Artikel 30 Absatz 5).

Über die Zusammenarbeit:

Die Mitgliedstaaten stellen sicher, dass zentrale Meldestellen unabhängig von ihrem Organisationsstatus miteinander im größtmöglichen Umfang zusammenarbeiten (Artikel 52), selbst wenn zum Zeitpunkt des Austauschs die Art der Vortaten, die einen Zusammenhang aufweisen könnten, nicht feststeht (Artikel 53 Absatz 1). Geht bei einer zentralen Meldestelle eine Meldung verdächtiger Transaktionen ein, die einen anderen Mitgliedstaat betrifft, so leitet sie diese Meldung umgehend an die zentrale Meldestelle des betreffenden Mitgliedstaats weiter (Artikel 53 Absatz 1). Darüber hinaus sind die zentralen Meldestellen der EU berechtigt, sämtliche im Inland verfügbaren Befugnisse zur Beantwortung ausländischer Ersuchen zu nutzen (Artikel 53).

Wird ein Auskunftsersuchen von einer zentralen Meldestelle an eine andere zentrale Meldestelle der EU gerichtet, so erteilt die zentrale Meldestelle, an die das Ersuchen gerichtet ist, zeitnah Antwort. Wenn eine zentrale Meldestelle zusätzliche Informationen von einem in ihrem Hoheitsgebiet tätigen Verpflichteten, der in einem anderen Mitgliedstaat eingetragen ist, einholen möchte, ist das Ersuchen an die zentrale Meldestelle des Mitgliedstaats zu richten, in dessen Hoheitsgebiet der Verpflichtete niedergelassen ist. Diese zentrale Meldestelle leitet das Ersuchen und die Antworten umgehend weiter (Artikel 53 Absatz 2).

Eine zentrale Meldestelle kann den Informationsaustausch nur in Ausnahmefällen verweigern, wenn der Austausch im Widerspruch zu den Grundprinzipien ihres nationalen Rechts stehen könnte (Artikel 53 Absatz 3).

Beim Austausch von Informationen und Dokumenten kann die übermittelnde zentrale Meldestelle Einschränkungen und Bedingungen für die Verwendung der Informationen festlegen (Artikel 54).

Die Mitgliedstaaten stellen sicher, dass die ausgetauschten Informationen nur zu dem Zweck verwendet werden, zu dem sie verlangt oder zur Verfügung gestellt wurden, und

18 Diese Richtlinie gilt für (Artikel 2): Kreditinstitute; Finanzinstitute; Abschlussprüfer, externe Buchprüfer und Steuerberater; Notare und andere selbstständige Angehörige von Rechtsberufen; Dienstleister für Trusts und Gesellschaften; Immobilienmakler; andere natürliche oder juristische Personen, die mit Gütern handeln, sowie Kasinos.

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 15

Dritte Geldwäscherichtlinie (2005) Zusätzliche Bestimmungen in der vierten Geldwäscherichtlinie von 2015, bis Juni 2017 umzusetzen

dass für jegliche Weitergabe der Informationen die vorherige Zustimmung der übermittelnden zentralen Meldestelle erforderlich ist (Artikel 55 Absatz 1). Eine Verweigerung der Zustimmung ist angemessen zu begründen (Artikel 55 Absatz 2).

Unterschiedliche Definitionen von Steuerstraftaten im jeweiligen nationalen Recht sollten dem nicht entgegenstehen, dass die zentralen Meldestellen Informationen austauschen oder einer anderen zentralen Meldestelle im Einklang mit ihrem nationalen Recht im größtmöglichen Umfang Hilfe leisten (Artikel 57).

Zusätzlich beschloss die Europäische Kommission – bedingt durch die Terroranschläge

Ende 2015 und die Enthüllungen der "Panama Papers" im April 2016 –, den EU-Rahmen

zur Geldwäschebekämpfung ein weiteres Mal zu überprüfen und neue Änderungen

vorzuschlagen, über die zum Zeitpunkt der Abfassung dieses Textes verhandelt wird.19

Der Beurteilung der Rolle der FIU bei der Bekämpfung von Steuerstraftaten unter

solchen sich rasch verändernden Rahmenbedingungen sind daher offenkundig gewisse

Grenzen gesetzt.

Wie aus der vergleichenden Analyse in Teil II (in der FIUs in Kanada, Frankreich, der

Schweiz und im Vereinigten Königreich verglichen werden) hervorgeht, sollte jedoch im

Zusammenhang mit der Umsetzung der dritten Geldwäscherichtlinie (2005), die bis zum

15. Dezember 2007 zu erfolgen hatte, erwähnt werden, dass in der dritten Richtlinie

Steuerhinterziehung an sich zwar nicht erwähnt wird, "schwere Straftaten" aber im

Geltungsbereich der Geldwäscherichtlinie aufgeführt sind. Letztere werden definiert als

"alle Straftaten, die mit einer Freiheitsstrafe oder einer die Freiheit beschränkenden

Maßregel der Sicherung und Besserung im Höchstmaß von mehr als einem Jahr oder —

in Staaten, deren Rechtssystem ein Mindeststrafmaß für Straftaten vorsieht — die mit

einer Freiheitsstrafe oder einer die Freiheit beschränkenden Maßregel der Sicherung und

Besserung von mindestens mehr als sechs Monaten belegt werden können"20 und

schließen daher Steuerstraftaten in einer Reihe von Mitgliedstaaten ein.21

Darüber hinaus gibt es verschiedene Bewertungen zur Umsetzung der dritten

Geldwäscherichtlinie in einzelstaatliches Recht und zu deren Anwendung, in denen

erhebliche Probleme aufgezeigt werden, was die Kapazitäten der FIUs bei der wirksamen

19 Vorschlag für eine Richtlinie zur Änderung der Richtlinie (EU) 2015/849 zur Verhinderung der Nutzung des Finanzsystems zum Zwecke der Geldwäsche und der Terrorismusfinanzierung und zur Änderung der Richtlinie 2009/101/EG, Straßburg, 5. Juli 2016, COM(2016) 450 final. Zu einer ersten Bewertung der Folgenabschätzung der Europäischen Kommission durch den wissenschaftlichen Dienst des Europäischen Parlaments siehe: Collovà C., Prevention of the use of the financial system for the purposes of money laundering or terrorist financing, PE 587.354, 2016.

20 Richtlinie 2005/60/EG, a.a.O. 21 Siehe Abschnitt 1 der vergleichenden Analyse in Teil II: Amicelle A., Berg J. und Chaudieu K., Comparative analysis of Financial Intelligence Units (FIUs) in Canada, France, Switzerland and United Kingdom.

Ex-post-Folgenabschätzungen

PE 598.603 16

Bekämpfung der Geldwäsche und der Terrorismusfinanzierung betrifft. Von diesen

Problemen sind einige besonders relevant für die Bekämpfung von Steuerstraftaten und

die wirksame Zusammenarbeit in diesem Bereich, wie in Abschnitt 3 ausgeführt wird.

2. Strukturen, Ressourcen und Kooperationskanäle der

zentralen Meldestellen

2.1. Strukturelle Unterschiede

Die aufeinanderfolgenden EU-Geldwäscherichtlinien enthalten keine spezifischen

Bestimmungen darüber, wie die FIUs auf Ebene der Mitgliedstaaten strukturiert und

organisiert sein sollten. In seinem Bericht aus dem Jahr 200422 hat der IWF eine Typologie

zur Klassifizierung der FIUs vorgeschlagen, die seither verwendet wird. Je nachdem, wo

die FIUs in den administrativen Strukturen der Mitgliedstaaten angesiedelt sind, werden

in dem IWF-Bericht vier Typen unterschieden:

FIU im Bereich Verwaltung

FIU im Bereich Strafverfolgung

FIU im Bereich Justiz/Staatsanwaltschaft

FIU-Mischformen.

In dem im Jahr 2013 veröffentlichten Abschlussbericht über das von der EU finanzierte

"ECOLEF"-Projekt 23(im Folgenden "ECOLEF-Studie") wurde versucht, ein vollständiges

und umfassendes Verzeichnis der FIUs in den damals 27 EU-Mitgliedstaaten zu erstellen

und eine Einstufung nach der IWF-Typologie vorzunehmen.24 Dem Bericht zufolge war

die überwiegende Mehrheit der EU-FIUs entweder dem Bereich Verwaltung oder dem

Bereich Strafverfolgung zuzuordnen; lediglich vier FIUs betrachteten sich selbst als dem

Bereich Justiz zugehörig oder als Mischform. Die ECOLEF-Studie gelangte zu dem

Schluss, dass die Mitgliedstaaten – da nur eine Handvoll FIUs sich als einer anderen

Typologie zugehörig einstuften – weitgehend mit der Typologie übereinstimmten, der

ihre FIUs zugeordnet wurden..25

Bestätigt werden diese Erkenntnisse in einem neueren Bericht für die EU-Plattform für

zentrale Meldestellen (im Folgenden "Bericht für die FIU-Plattform")26, in dem allerdings

22 IWF, Financial Intelligence Units: An Overview, 2004.

23 Projekt "Economic and Legal Effectiveness of Anti-Money Laundering and Combating Terrorist Financing Policy - ECOLEF" (mit Mitteln der Europäischen Kommission finanziert – GD "Inneres", JLS/2009/ISEC/AG/087), Abschlussbericht, Februar 2013.

24 Ebd., S. 140. 25 S. 143.

26 Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information, Bericht für die Plattform der zentralen Meldestellen der EU, Dezember 2016 (Federführung: FIU Italien - Unità di Informazione Finanziaria per l'Italia - UIF). Dieser Bestandsaufnahme liegt eine umfassende Erhebung bei den EU-FIU zugrunde. Anhand der Ergebnisse der Erhebung sollen Probleme, die bei der Anwendung der EU-Vorschriften zur

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 17

nur drei FIU-Modelle genannt werden: Verwaltung, Strafverfolgung (oder Justiz) und

"Mischform". Die EU-FIU verteilen sich derzeit wie folgt:27

12 EU-FIUs haben angegeben, dass sie dem Verwaltungstyp zuzuordnen sind

(diese sind beispielsweise bei den Finanz-, Justiz- oder Innenministerien

angesiedelt oder in die Zentralbank oder eine Aufsichtsbehörde eingegliedert):

Belgien, Bulgarien, Kroatien, die Tschechische Republik, Frankreich, Italien,

Lettland, Malta, Polen, Rumänien, Slowenien und Spanien;

11 EU-FIUs haben angegeben, dass sie dem Bereich Strafverfolgung (Polizei

und/oder Justiz) zuzuordnen sind: Österreich, Estland, Finnland, Deutschland,

Irland, Litauen, Portugal, die Slowakei, Schweden, Luxemburg und das

Vereinigte Königreich;

5 EU-FIUs stufen sich selbst als Mischform ein, da bei ihnen sowohl

administrative als auch polizeiliche Elemente vertreten sind: Zypern, Dänemark,

Griechenland, Ungarn und die Niederlande.

Der Bericht für die FIU-Plattform gibt allerdings zu bedenken, dass "die Festlegung

dieser verschiedenen institutionellen Typen der herkömmlichen Struktur entspricht und

dass die Verteilung der EU-FIUs auf die einzelnen Typen in gewisser Weise willkürlich

ist. Auch innerhalb der jeweiligen Kategorie behält jede einzelne FIU ihre

charakteristischen Besonderheiten bei".28 Bereits in der ECOLEF-Studie war darauf

hingewiesen worden, dass entscheidende Aspekte (etwa der Hintergrund der FIU-

Mitarbeiter, die Aufgabenverteilung oder der Zugang zu Datenbanken) nicht

notwendigerweise mit dem FIU-Typ korrelieren.29

Dieser Aspekt wird in der vergleichenden Analyse (Teil II der vorliegenden Studie)

bestätigt, in der betont wird, dass zwischen FIUs desselben Typs große Unterschiede

bestehen, unter anderem was die Arten der bei ihnen eingehenden Meldungen oder

ihren Zugang zu den verschiedenen nationalen Datenbanken angeht.30 Auch die

gemeinhin geltende Annahme, wonach "Strafverfolgungs"-FIUs besseren Zugang zu

polizeilichen und ermittlungs¬dienstlichen Informationen haben, hat sich im Falle der

vier untersuchten FIUs nicht bestätigt.31 Wie in Abschnitt 3.1 und mit Blick auf

Steuerstraftaten weiter analysiert wird, spielen andere Elemente – etwa das

Funktionieren der Zusammenarbeit mit den Steuerbehörden in der Praxis – bei der

Bekämpfung der Geldwäsche und der Terrorismusfinanzierung auftreten, und mögliche Lösungen bzw. Gegenmaßnahmen aufgezeigt werden. Sämtliche Informationen und Daten, die in diese Bestandsaufnahme eingeflossen sind, wurden durchgehend vertraulich und anonym behandelt. Der Bericht enthält demzufolge keine Angaben zu einzelnen FIU. 27 Ebd., S. 5-7.

28 In dem Bericht wird in diesem Zusammenhang daran erinnert, dass ein wichtiges organisatorisches Element – neben dem "Status" einer FIU – ihre Einbettung in größere Organisationen ist, da sich dies auf ihre Autonomie auswirkt. Siehe: Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information, a.a.O. 29 Siehe: ECOLEF-Studie, a.a.O., S. 162.

30 Siehe unsere vergleichende Analyse (Teil II): Amicelle A., Berg J. und Chaudieu K., Comparative analysis of Financial Intelligence Units (FIUs) in Canada, France, Switzerland and United Kingdom, Abschnitt 1.1. 31 Ebd.

Ex-post-Folgenabschätzungen

PE 598.603 18

Bewertung der Fähigkeit der FIUs, ihre Aufgaben ordnungsgemäß wahrzunehmen, eine

größere Rolle.

2.2. Ressourcen

Was die personellen Ressourcen angeht, so variiert gemäß dem Bericht für die FIU-

Plattform die Zahl der Mitarbeiter, die speziell mit den FIU-Kernaufgaben (d. h.

Entgegennahme von Meldungen verdächtiger Transaktionen, Analysen,

Informationsweitergabe und internationale Zusammenarbeit) befasst sind, zwischen den

Mitgliedstaaten erheblich: zwischen fünf (in Irland) und 289 Beschäftigten (in

Deutschland).32 Auch die Prozentzahlen der mit diesen Kernaufgaben befassten FIU-

Mitarbeiter gehen weit auseinander: Sie liegen zwischen 33 % (in Malta) und 100 % (im

Vereinigten Königreich).

FIUs können indessen auch andere Aufgaben wahrnehmen, etwa die Ausarbeitung von

Rechtsvorschriften zur Bekämpfung von Geldwäsche, die Herausgabe von Leitlinien für

die meldenden Stellen zur Gestaltung der Meldungen, die Überwachung der meldenden

Stellen und Vorschläge für Sanktionen bei der Feststellung von Unregelmäßigkeiten

während der Überwachung/Kontrollen.33 Diese Mitarbeiterzahlen dürfen jedoch nicht zu

stark vereinfachten Schlüssen führen: Wie in dem Bericht für die FIU-Plattform angeregt

wird, sollte nämlich die Angemessenheit der verfügbaren personellen Ressourcen vor

dem Hintergrund der jeweiligen Arbeitsbelastung der FIU, insbesondere dem

Meldeaufkommen, der Art der durchgeführten Analysen und der

Informationsweitergabe und des Umfangs des internationalen Austauschs bewertet

werden.34 So sind beispielsweise in Deutschland im Jahr 2014 ca. 24 000 Meldungen

verdächtiger Transaktionen eingegangen.35 Irland hat demgegenüber im Jahr 2012 etwa

12 400 Verdachtsmeldungen erhalten.36

Beim Haushaltsvolumen können die Zahlen dem Bericht für die FIU-Plattform zufolge

extrem weit auseinanderliegen: zwischen 600 000 EUR und mehr als 14 Mio. EUR pro

Jahr.37 Auch hier gilt allerdings, dass diese Unterschiede nicht unbedingt hilfreich sind,

um zu bewerten, ob die Finanzausstattung der FIU ausreicht, damit diese die ihnen

zugewiesenen Aufgaben erfüllen können. Aussagekräftiger sind in diesem

32 Für Kanada, Frankreich, die Schweiz und das Vereinigte Königreich werden in der vergleichenden Analyse folgende Zahlen genannt: 350 Mitarbeiter (Kanada); 150 Mitarbeiter (Frankreich); 20 Mitarbeiter (Schweiz); 150 Mitarbeiter (Vereinigtes Königreich). Siehe: Amicelle A., Berg J. und Chaudieu K., Comparative analysis of Financial Intelligence Units (FIUs) in Canada, France, Switzerland and United Kingdom (Einleitung).

33 Siehe hierzu: ECOLEF-Studie, a.a.O., S. 149.

34 Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information, a.a.O., S. 12.

35 Siehe: Financial Intelligence Unit (FIU) Deutschland - Jahresbericht 2014. 36 Siehe: Department of Justice and Equality of Ireland, Anti-Money Laundering Compliance Unit, Statistikbericht, 2012.

37 Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information, a.a.O., S. 13.

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 19

Zusammenhang Angaben zur budgetären Unabhängigkeit der FIU. Wie sowohl in der

ECOLEF-Studie als auch in dem Bericht für die FIU-Plattform dargelegt wird, erhöht die

Budgetunabhängigkeit die Fähigkeit der FIU, die für ihre funktionellen Anforderungen

erforderlichen Beträge eigenständig zu verwalten. Weniger als die Hälfte der EU-FIUs

haben im Rahmen des Berichts für die FIU-Plattform angegeben, dass sie über einen

eigenen Haushalt verfügen, das heißt über Mittel, die speziell (und ausschließlich) ihnen

für die Deckung ihrer Ausgaben zugewiesen und von ihnen unabhängig verwaltet

werden. Die Mehrzahl der EU-FIUs hat angegeben, dass ihr Haushalt Teil des

Haushaltsplans einer größeren Einrichtung ist.38 In der ECOLEF-Studie wird darauf

hingewiesen, dass diese Abhängigkeit, insbesondere in Zeiten von Mittelkürzungen, zu

Problemen führen kann39

In dem Bericht für die FIU-Plattform wird festgestellt, dass die verfügbaren finanziellen,

personellen und technischen Mittel im Großen und Ganzen für ausreichend erachtet

werden, um den derzeitigen Bedarf der EU-FIUs zu decken. Es wird jedoch auch

hervorgehoben, dass EU-weit vonseiten der FIU-Mitarbeiter Bedenken laut werden, ob

die FIUs auch weiterhin in der Lage sein werden, mit den im Zuge der Umsetzung der

vierten Geldwäscherichtlinie erwarteten Entwicklungen Schritt zu halten, wenn die

verfügbaren Mittel nicht wesentlich aufgestockt werden. In dem Bericht wird

insbesondere darauf hingewiesen, dass die FIUs gemäß der vierten Geldwäscherichtlinie

künftig auf verfügbare nationale Kräfte zurückgreifen müssen, um ausländische

Anfragen zu beantworten und Verdachtsmeldungen, die einen anderen Mitgliedstaat

betreffen, an die betreffenden ausländischen Partner weiterzuleiten, was das

Tätigkeitsspektrum weiter ausdehnt, obwohl die Arbeitsbelastung bereits kontinuierlich

zunimmt; zu nennen sind hier insbesondere die Zahl der eingehenden

Verdachtsanzeigen, die zwischen den Partner-FIUs ausgetauschten Informationen und

die mit den verschiedenen Formen der innerstaatlichen Zusammenarbeit verbundenen

Erfordernisse.40

2.3. Meldungen verdächtiger Transaktionen: verschiedene Quellen

und unterschiedliche Qualität

Die Tätigkeiten der FIU basieren auf Informationen über verdächtige finanzielle

Transaktionen. Gemäß der dritten Geldwäscherichtlinie nehmen alle FIUs ausgefüllte

Meldungen verdächtiger Transaktionen vonseiten meldepflichtiger Einrichtungen

entgegen.41

38 Ebd., S. 12. 39 ECOLEF-Studie, a.a.O., S. 146. 40 Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information, a.a.O., S. 25.

41 Verpflichtete im Sinne des Artikels 2 der dritten Geldwäscherichtlinie sind: Kreditinstitute; Finanzinstitute; Abschlussprüfer, externe Buchprüfer und Steuerberater; Notare und andere selbstständige Angehörige von Rechtsberufen; Dienstleister für Trusts und Gesellschaften; Immobilienmakler; andere natürliche oder juristische Personen, die mit Gütern handeln, sowie Kasinos.

Ex-post-Folgenabschätzungen

PE 598.603 20

Wenn man Quantität und Qualität der Meldungen der Verpflichteten betrachtet, treten

verschiedene Probleme auf. In unserer vergleichenden Analyse (Teil II dieser Studie)

wird im Einzelnen erläutert, wie das Meldeverfahren in der Praxis funktioniert.

Analysiert wird darin ferner die Herkunft der Verdachtsmeldungen, die die FIUs in den

vier untersuchten Ländern (Kanada, Frankreich, Schweiz und Vereinigtes Königreich)

entgegennehmen, wobei Folgendes festgestellt wird:42

Erstens: Der Großteil der Meldungen verdächtiger Transaktionen/Tätigkeiten an

die FIUs stammt von Finanzinstituten. Nur ein geringer Anteil der

Verdachtsmeldungen stammt von Angehörigen der Rechtsberufe und von

Wirtschaftsprüfern.

Zweitens: Die Anzahl der eingehenden Verdachtsmeldungen korreliert nicht

zwangsläufig mit der Größe des betreffenden nationalen Finanzmarkts. Als

Beispiel wird in dem Papier die Schweiz genannt, die immer wieder aufgrund

des zu geringen Meldeaufkommens in der Kritik steht.

Drittens: Für die Finanzinstitute ist die Vermeidung eines Rufschadens ein

zentraler Faktor bei der Erfüllung ihrer Meldepflichten: Dies kann entweder zu

ausufernden Meldungen oder zu einer zu geringen Zahl von Meldungen führen.

Hier besteht die Herausforderung darin zu wissen, wo die Grenze zwischen

defensivem Meldeverhalten (zur Vermeidung von Kritik aufgrund einer

Nichteinhaltung der Rechtsvorschriften zur Bekämpfung der Geldwäsche) und

erkenntnisrelevantem Meldeverhalten zu ziehen ist.

Trotz erheblicher methodischer Einschränkungen wurde versucht zu quantifizieren, wie

hoch der Gesamtanteil der an die FIUs gerichteten Verdachtsmeldungen war, die von

den FIUs analysiert und im Anschluss an die Strafverfolgungsbehörden weitergeleitet

wurden und die schließlich tatsächlich zu einer strafrechtlichen Verfolgung geführt

haben, um eine durchschnittliche "Effizienzquote" für diese Art der Meldepflicht zu

bestimmen. In dem Bericht über die Kosten des Verzichts auf EU-politisches Handeln

("Cost of non-Europe") im Bereich der organisierten Kriminalität, den der

Wissenschaftliche Dienst des Europäischen Parlaments 2016 veröffentlicht hat, wurden

beispielsweise die EU-Mitgliedstaaten betrachtet, für die vergleichbare Daten vorlagen

(Belgien, die Tschechische Republik, Estland, Deutschland, Lettland, Litauen,

Luxemburg, Rumänien, die Slowakei und Slowenien); auf der Grundlage der

EUROSTAT-Daten aus dem Jahr 2013 wurde dabei festgestellt, dass von der Gesamtzahl

der Meldungen verdächtiger Transaktionen, die in diesen Mitgliedstaaten ausgefüllt und

den jeweiligen FIUs übermittelt wurden, 29 % in der Folge an Strafverfolgungsbehörden

weitergeleitet wurden und dass davon wiederum 54 % zu einem Gerichtsverfahren

geführt haben. Somit haben etwa 16 % aller eingereichten Verdachtsmeldungen

42 Siehe unsere vergleichende Analyse (Teil II): Amicelle A., Berg J. und Chaudieu K., Comparative analysis of Financial Intelligence Units (FIUs) in Canada, France, Switzerland and United Kingdom (Abschnitte 1.2 und 1.3).

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 21

tatsächlich eine strafrechtliche Verfolgung nach sich gezogen. Es existieren allerdings

keine Statistiken dazu, wie viele dieser Fälle letztlich zu Verurteilungen geführt haben.43

Des Weiteren nehmen zwar alle FIUs Verdachtsmeldungen entgegen, doch haben einige

zusätzlich auch Zugang zu anderen Informationsquellen, in erster Linie auf der

Grundlage von Schwellenbeträgen.44 Informationen auf Schwellenwertbasis beziehen

sich auf bestimmte Arten von Transaktionen (zum Beispiel Bargeldeinlagen oder

Abhebungen/Überweisungen), die – unabhängig davon, ob die zugrundeliegenden

Tätigkeiten verdächtig sind – gemeldet werden müssen, sobald ein bestimmter

quantitativer Schwellenwert erreicht oder überschritten ist. Diese Meldung unterscheidet

sich von einer Verdachtsmeldung, bei der die Höhe des betreffenden Betrags nicht

relevant ist.

Wie in dem Bericht für die FIU-Plattform erwähnt, hat die Mehrheit der EU-FIUs Zugang

zu den gemäß der Verordnung (EG) Nr. 1889/2005 bei den Zollbehörden eingereichten

obligatorischen Anmeldungen von physischen grenzüberschreitenden

Barmitteltransporten.45 Allerdings erhält nur eine Minderheit der EU-FIUs46 zusätzlich

schwellenwertbasierte Meldungen der Verpflichteten (dieselben wie diejenigen, die zur

Meldung verdächtiger Transaktionen verpflichtet sind). Der Grenzwert, der die

Barmittelmeldepflicht in den EU Mitgliedstaaten auslöst, in denen diese Bestimmung

gilt, liegt zwischen 10 000 EUR und 32 000 EUR.

Wie in unserer vergleichenden Analyse (Teil II) festgestellt, werden

schwellenwertbasierte Informationen von einigen Ländern als wichtiges Instrument im

Kampf gegen Steuerhinterziehung betrachtet, so etwa von Kanada, wo die

Finanzinstitute seit 2015 verpflichtet sind, im elektronischen Zahlungsverkehr ab einem

Betrag von 10 000 CAD (ca. 7000 EUR) nicht nur der nationalen FIU, sondern zusätzlich

auch der kanadischen Steuerbehörde Meldung zu machen. In der Tat scheint die

Vermeidung von Entdeckung über das Bankensystem durch die Nutzung von Barmitteln

weit verbreitet zu sein, insbesondere in Volkswirtschaften, die auf Barmitteln basieren.

Auf EU-Ebene sind schwellenwertbasierte Meldungen derzeit nicht verpflichtend. In der

vierten Geldwäscherichtlinie ist lediglich vorgesehen, dass FIUs zusätzlich zu den

43 Siehe Anhang 1 (Organisierte Kriminalität) in: van Ballegooij W. und Zandstra T., The Cost of Non-Europe in the area of Organised Crime and Corruption, PE 579.318, 2016, S. 60.

44 Siehe beigefügte vergleichende Analyse. Diese zusätzliche Informationsquelle findet sich bei zwei der vier untersuchten FIU, nämlich Frankreich und Kanada.

45 Verordnung (EG) Nr. 1889/2005 über die Überwachung von Barmitteln, die in die Gemeinschaft oder aus der Gemeinschaft verbracht werden. Nach Artikel 3 muss jede natürliche Person, die in die Gemeinschaft einreist oder aus der Gemeinschaft ausreist und Barmittel in Höhe von 10 000 EUR oder mehr mit sich führt, diesen Betrag bei den zuständigen Behörden des betreffenden Mitgliedstaats anmelden.

46 Hierzu gehören Bulgarien, Kroatien, Estland, Frankreich, Litauen, die Niederlande, Polen, Rumänien, Slowenien und Spanien. Siehe: Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information, a.a.O., S. 81.

Ex-post-Folgenabschätzungen

PE 598.603 22

Verdachtsmeldungen auch andere Informationen entgegennehmen können, darunter

auch auf Schwellenwerten beruhende Angaben (siehe Erwägungsgrund 37).

In Bezug auf virtuelle Währungen sollte erwähnt werden, dass die Europäische

Kommission eine Änderung des Artikels 2 der vierten Geldwäscherichtlinie vorschlägt,

über die derzeit diskutiert wird, wonach Umtausch-Plattformen für virtuelle Währungen

sowie Anbieter elektronischer Geldbörsen in die Liste der Verpflichteten

mitaufgenommen werden sollen.47

2.4. Kooperationskanäle

Wie in unserer vergleichenden Analyse (Teil II) beschrieben, haben die FIUs zahlreiche

Gründe, mit anderen FIUs auf europäischer und internationaler Ebene

zusammenzuarbeiten. Grenzüberschreitende Transaktionen, Bankkunden ausländischer

Staatsangehörigkeit sowie Bürgerinnen und Bürger, die in einem anderen Land leben

oder arbeiten, sind einleuchtende Gründe dafür, warum der Informationsaustausch

zwischen den FIUs von entscheidender Bedeutung ist. Zwei zentrale

Kommunikationskanäle existieren für die Zusammenarbeit zwischen den FIUs: weltweit

über die Egmont-Gruppe (mit dem Egmont Secure Web (ESW), dessen technischer

Betrieb dem FinCen, der zentralen Meldestelle der Vereinigten Staaten, obliegt), und für

die EU-Mitgliedstaaten über ein dezentralisiertes System, das FIU.NET, das seit Januar

2016 in das Europol-System eingebunden ist.

Beide Plattformen bieten sichere Kommunikationskanäle für den Informationsaustausch.

Doch auch wenn dem ESW und dem FIU.NET dasselbe Ziel der Informationsweitergabe

zwischen FIUs zugrunde liegt, zeigt unsere vergleichende Analyse (Teil II) dennoch eine

Reihe von Unterschieden zwischen ihnen auf, die darauf schließen lassen, dass das

FIU.NET einen klaren Mehrwert48 auf europäischer Ebene bietet. Das FIU.NET mit seiner

hohen Komplexität wird aus folgenden Gründen als überlegen angesehen:49

Daten können direkt aus den FIU-Datenbanken abgerufen und in diese

eingegeben werden, während das ESW im Wesentlichen als sichere E-Mail-

Verbindung funktioniert.

Das FIU.NET ermöglicht den multilateralen Austausch. Die dem FIU.NET

angeschlossenen zentralen Meldestellen können einen bilateralen, einen

multilateralen oder sogar einen uneingeschränkten Austausch mit allen

angeschlossenen Partnerbehörden wählen. Dabei sind unterschiedliche Konzepte

möglich, von einem Minimalansatz (etwa Anfragen "bekannt/unbekannt", um zu

47 Siehe: Vorschlag zur Änderung der Richtlinie (EU) 2015/849 zur Verhinderung der Nutzung des Finanzsystems zum Zwecke der Geldwäsche und der Terrorismusfinanzierung und zur Änderung der Richtlinie 2009/101/EG, Straßburg, 5. Juli 2016, COM(2016) 450 final.

48 Siehe: Europol-Website. 49 iehe unsere vergleichende Analyse (Teil II): Amicelle A., Berg J. und Chaudieu K., Comparative analysis of Financial Intelligence Units (FIUs) in Canada, France, Switzerland and United Kingdom (Abschnitt 2.1).

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 23

prüfen, ob bestimmte Namen in der Datenbank eines anderen EU-Mitgliedstaats

zu finden sind) bis hin zu einem "Einzelfalldossier", bei dem weitere Einzelheiten

und Gründe für die Anforderung von Informationen vonseiten anderer FIUs

angegeben werden. In letzterem Szenario kann die FIU einen Zugang

verschiedener Stellen zu dem Dossier herstellen.

Das FIU.NET hat vor kurzem die "Ma3tch technology" eingeführt: Die EU-FIUs

verfügen nunmehr über eine Reihe von Optionen, darunter einfache Anfragen

"bekannt/unbekannt" oder "Treffer/kein Treffer" an eine oder mehrere

Partnerbehörde(n).

Ein Personenabgleich über das FIU.NET wird auch mit anderen angeschlossenen

Datensätzen mithilfe quelloffener Tools wie World-Check vorgenommen.

Insgesamt gesehen werden aus europäischer Perspektive das ESW und das FIU.NET

weitgehend als komplementär betrachtet. Das FIU.NET wird in Zusammenarbeit mit EU

Partnerbehörden genutzt, während das ESW dem Informationsaustausch mit Partnern

außerhalb der EU dient. Für den Austausch von Informationen mit zentralen

Meldestellen, die weder an das FIU.NET noch an das ESW angeschlossen sind, werden

traditionelle Kommunikationsmittel wie sichere E-Mail-Verbindungen oder sogar

Faxnachrichten verwendet.50

2.5. Zusammenarbeit und Informationsaustausch zwischen FIUs

Sowohl aus dem Bericht für die FIU-Plattform als auch aus unserer vergleichenden

Analyse (Teil II) wird deutlich, dass es bei der Zusammenarbeit zwischen den FIUs

erhebliche Hindernisse gibt. Unter anderem sind dies folgende:

Nicht alle EU-FIUs sind befugt, Informationsersuchen an Verpflichtete zu

richten. In vielen Fällen müssen dafür vorher Verdachtsmeldungen eingegangen

sein. Dies bedeutet auch, dass einige FIUs keine Informationen von meldenden

Einrichtungen für ausländische FIUs anfordern können, wenn in ihrer Datenbank

keine relevante verdächtige Transaktion registriert ist.

Zeitliche Verzögerungen bei der Beantwortung von Anfragen wirken sich

negativ auf die Zusammenarbeit zwischen den zentralen Meldestellen aus, und

die Antworten auf Anfragen sind nicht unbedingt hilfreich: Manchmal sind sie

auf die Auskunft "bekannt/unbekannt" beschränkt, ohne dass weitere

Erläuterungen gegeben werden.

Andere Hindernisse ergeben sich aus der unterschiedlichen Natur und den

unterschiedlichen Befugnissen der FIUs aufgrund inländischer Besonderheiten (siehe

oben). Einige dieser Probleme sind in der vierten Geldwäscherichtlinie zum Teil

angegangen worden. Gemäß Artikel 32 Absatz 3 müssen die zentralen Meldestellen in

der Lage sein, von allen Verpflichteten Informationen einzuholen, ungeachtet der

Tatsache, ob vorher eine Informationsweitergabe erfolgt ist. Gemäß Artikel 53 der

Richtlinie sind die zentralen Meldestellen im Übrigen verpflichtet, den EU-

50 Ebd.

Ex-post-Folgenabschätzungen

PE 598.603 24

Partnerbehörden "zeitnah" Antwort zu erteilen. Mit den Änderungen der vierten

Geldwäscherichtlinie, über die derzeit diskutiert wird, sollen unter anderem die

Verzögerungen beim Informationsaustausch reduziert werden; ferner soll eine Pflicht zur

Beantwortung von Auskunftsersuchen eingeführt werden.51

Voraussetzung für den Informationsaustausch zwischen zentralen Meldestellen ist stets

die ausdrückliche Festlegung zielgerechter Verwendungsbedingungen (Zweckbindung),

die weitgehend von den innerstaatlichen Anforderungen abhängt, wie der

vergleichenden Analyse (Teil II) zu entnehmen ist. Die Regelung für die

Informationsweitergabe umfasst im Wesentlichen drei Optionen:

Generell gilt – und hierüber herrscht Konsens bei allen FIUs weltweit –, dass eine

FIU Informationen, die sie von einer anderen FIUs erhalten hat, nicht ohne

vorherige schriftliche Genehmigung letzterer nach außen weitergeben darf.52

Die FIU, von der die Informationen ursprünglich stammen, kann ihrem FIU-

Partner gestatten, die Informationen ausschließlich zu Zwecken der

Erkenntnisgewinnung (z. B. informell), nicht jedoch zu Beweiszwecken nach

außen weiterzugeben.

Die FIU erklärt sich damit einverstanden, dass ihr FIU-Partner die Informationen

auch zu anderen als Zwecken der Erkenntnisgewinnung, also beispielsweise

auch zu Beweiszwecken, weitergibt und verwendet.

Wie nachstehend in Abschnitt 3.3 ausgeführt, können diese Grundsätze für die

Informationsweitergabe die Zusammenarbeit in erheblichem Maße behindern, auch bei

der Aufdeckung von Steuerstraftaten. So kann etwa der Fall eintreten, dass einige FIUs

dem Austausch bestimmter Informationen zustimmen, jedoch angeben, dass diese nicht

für steuerrechtliche Angelegenheiten verwendet werden dürfen.

Ein weiteres übergreifendes Problem, das in dem Bericht für die FIU-Plattform dargelegt

wird, ist die unscharfe Unterscheidung zwischen Erkenntnisgewinnung und Ermittlung.

Dem Bericht zufolge "besteht das ausschließliche Ziel der Zusammenarbeit zwischen den

FIUs darin, die Untersuchung von Verdachtsfällen als typische Aufgabe der FIUs zu

erleichtern, wobei dies eine Tätigkeit ist, die sich klar von Ermittlung und

Strafverfolgung desselben Sachverhalts (durch Strafverfolgungsbehörden und

Staatsanwaltschaften) unterscheidet und davon getrennt ist. Zwischen FIUs

ausgetauschte Informationen sind daher nicht für die Verwendung im Zusammenhang

51 In der ECOLEF-Studie wurde die durchschnittliche Antwortdauer zwischen den FIU untersucht, wobei festgestellt wurde, dass die Antwort auf ein Ersuchen zwischen 24 Stunden und 30 Tagen dauern kann. Anhand der erhobenen Daten wurde ferner festgestellt, dass die Zusammenarbeit zwischen den EU-FIU nicht unbedingt schneller war als mit FIU aus Drittländern. Siehe: ECOLEF-Studie, S. 237. Bestätigt wird dies auch in dem Bericht für die FIU-Plattform, wonach Informationsersuchen seitens der Partnerbehörden in einem Zeitraum von zwei Stunden bis zu zwei Monaten oder länger beantwortet werden. Siehe: Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information, a.a.O., S. 154. 52 Operative Leitlinien der Egmont-Gruppe für die Tätigkeiten und den Informationsaustausch der FIU, 2013 (abrufbar über die Website der Egmont-Gruppe).

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 25

mit Ermittlungen, Strafverfolgungsmaßnahmen oder Gerichtsverfahren bestimmt."53 In

dem Bericht wird jedoch auch festgestellt, dass "zwischen Analyse und Ermittlung nicht

immer klar zu unterscheiden ist und die Grenze zwischen diesen beiden Aufgaben nicht

in allen Fällen klar genug gezogen werden kann, was sowohl für die innerstaatlichen

Funktionen der FIU als auch für den Ablauf der Zusammenarbeit zwischen den FIUs

gilt". Folglich wird "in einigen Fällen die Fähigkeit, zur Unterstützung analytischer

Aufgaben mit anderen FIUs zusammenzuarbeiten, dadurch behindert, dass im Land der

ersuchten FIU zeitgleich Ermittlungen oder Strafverfolgungsmaßnahmen durchgeführt

werden und dass vorherige Genehmigungen vonseiten der zuständigen

Staatsanwaltschaft eingeholt werden müssen (wobei diese Einschränkungen notabene

gleichermaßen auch für FIUs im Bereich Polizei und andere FIU-Typen gelten können)".

Um hier Abhilfe zu schaffen, wird in dem Bericht vorgeschlagen, Analyse und

Ermittlung stärker und deutlicher voneinander abzugrenzen, sowohl was die

innerstaatlichen Tätigkeiten der FIUs als auch ihre Zusammenarbeit untereinander

angeht.

3. Hauptprobleme bei der Bekämpfung von

Steuerstraftaten durch die zentralen Meldestellen

Zusätzlich zu den oben genannten Herausforderungen, mit denen die FIUs bei der

Erfüllung ihrer Aufgaben generell konfrontiert sind, treten im Zusammenhang mit

Steuerstraftaten spezielle Probleme auf:

Auf nationaler Ebene sind die FIUs nicht zwangsläufig die einzigen Empfänger

von Meldungen verdächtiger Transaktionen. Dies wirkt sich auf das

Funktionieren der Zusammenarbeit mit den Steuerbehörden aus.

Der Zugang zu Informationen über Inhaber von Bankkonten und wirtschaftliche

Eigentümer sowohl auf nationaler, europäischer und internationaler Ebene ist

mit erheblichen Hindernissen verbunden.

Der "steuerliche Vorwand" (wonach die erhaltenen Informationen nicht für

steuerliche Ermittlungen genutzt werden dürfen) wird häufig verwendet, um

den Austausch von Informationen und die Zusammenarbeit einzuschränken.

3.1. Auf nationaler Ebene: Zusammenarbeit zwischen zentralen

Meldestellen und Steuerbehörden

Das Problem der Mehrfachmeldung:

In der Praxis handeln die EU-FIUs bei der Entgegennahme von Meldungen verdächtiger

Transaktionen, insbesondere bei steuerlichen Straftaten, nicht in abgeschotteten

53 Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information, a.a.O., S. 140-142.

Ex-post-Folgenabschätzungen

PE 598.603 26

Bereichen. Zwar sind in den meisten Mitgliedstaaten die FIUs die alleinigen Empfänger

von Verdachtsmeldungen, doch übermitteln die Verpflichteten in einigen Mitgliedstaaten

ihre Meldungen gegebenenfalls gleichzeitig sowohl an die FIU als auch an die

zuständigen Behörden. Dies schließt die Steuerbehörden mit ein, die dann in den Fällen

tätig werden können, in denen verdächtige Transaktionen vorliegen.54

Im Zusammenhang mit Steuerstraftaten kann eine Analyse der Verdachtsmeldungen

daher von verschiedenen Einrichtungen vorgenommen werden. In dem Bericht für die

FIU Plattform wird darauf hingewiesen, dass dieses System der Mehrfachmeldung dort,

wo es existiert, zu verschiedenen Problemen führt, etwa dazu, dass individuelle

Ermittlungen vonseiten verschiedener Stellen "zu denselben Sachverhalten und auf der

Grundlage derselben Informationen" eingeleitet werden können, "was sicherlich zu

besonderen Herausforderungen mit Blick auf die Koordinierung der Maßnahmen der

einzelnen Stellen und auf die Konsistenz der Erkenntnisse und Ergebnisse führen

kann“.55

Modelle der Zusammenarbeit zwischen zentralen Meldestellen und

Steuerbehörden:

In ihrem Bericht aus dem Jahr 2015 zur Zusammenarbeit zwischen den Steuerbehörden

und den FIUs56 hat die OECD auf der Grundlage einer Erhebung in 28 Ländern (darunter

16 EU-Mitgliedstaaten) verschiedene Formen des Zugangs der Steuerbehörden zu

Meldungen verdächtiger Transaktionen identifiziert:57

Uneingeschränkter unabhängiger Zugang der Steuerverwaltung zu

Verdachtsmeldungen (wobei sowohl die FIU als auch die Steuerverwaltung

gleichermaßen die Möglichkeit haben, die Meldungen zu verwenden, und

jeweils unabhängig voneinander entscheiden können, in welchen Fällen und wie

sie diese nutzen wollen);

gemeinsame Entscheidungen der FIU und der Steuerverwaltung hinsichtlich der

Zuweisung der Verdachtsmeldungen (wobei in einem gemeinsamen

Entscheidungsprozess festgelegt wird, wie die Verdachtsmeldungen zu nutzen

sind);

eine Entscheidung der FIU über die Zuweisung der Verdachtsmeldungen (wobei

die FIU gemäß den nationalen Rechtsvorschriften entscheidet, welche

Informationen im Zusammenhang mit der Verdachtsmeldung sie an die

Steuerverwaltung weiterleitet).

54 Mapping exercise and gap analysis on FIUs powers and obstacles for obtaining and exchanging information, a.a.O., S. 30. 55 Ebd., S. 31.

56 OECD, Improving co-operation between tax and anti-money laundering authorities. Access by tax administrations to information held by financial intelligence units for criminal and civil purposes, September 2015. 57 Ebd., S. 15 ff.

Evaluierung der Zusammenarbeit zwischen den FIU

PE 598.603 27

In dem OECD-Bericht werden sowohl die Vor- als auch die Nachteile dieser drei Modelle

begutachtet. Zwar wird in dem Bericht kein abschließendes Fazit gezogen, mit welchem

Modell am besten gegen Steuerstraftaten vorgegangen werden kann, doch vermittelt er

interessante Rückschlüsse darauf, wie man die Nachteile der einzelnen Modelle abfedern

und die Einhaltung der Steuervorschriften in größtmöglichem Umfang sicherstellen

könnte:

Bei Modell 1 sollte eine klare (Verwaltungs-)Vereinbarung geschlossen werden,

auch um Konflikte zwischen der Herangehensweise der einzelnen Behörden an

einen gegebenen Fall zu vermeiden.

Bei Modell 2 sollte (beispielsweise durch eine Vereinbarung) für den Aufbau

enger Arbeitsbeziehungen zwischen den Zuständigen der einzelnen Behörden

und für regelmäßige Treffen gesorgt werden, in denen die Verdachtsmeldungen

zugewiesen werden.

Bei Modell 3 könnten gezielte Schulungen der FIU-Mitarbeiter zu Steuerfragen

hilfreich sein, auch um sicherzustellen, dass die Mitarbeiter der FIU die Elemente

von Steuerstraftaten korrekt erkennen. Eine andere Option wäre es, Personal an

die FIU abzuordnen, um Unterstützung bei der Aufdeckung von Steuerrisiken

zu leisten.

Zugang zu steuerlichen Informationen:

Für die wechselseitige Zusammenarbeit und gegenseitige Vereinbarungen zwischen FIUs

und Steuerbehörden ist es außerdem erforderlich, dass die FIUs Zugang zu

steuerrelevanten Daten und Informationen haben, um wirksam gegen Steuerstraftaten

vorgehen zu können.

Wie in dem Bericht für die FIU-Plattform festgestellt, haben einige EU-FIUs nur

eingeschränkten Zugang zu Informationen der nationalen Finanz-, Verwaltungs- und

Strafverfolgungseinrichtungen. In dem Bericht wird auf die Problematik der engen und

nur geringfügig vereinheitlichten Bandbreite der Informationen und Datenbanken, die

den FIUs für Analysezwecke und für die Zusammenarbeit zur Verfügung steht,

hingewiesen.

Das Forschungsteam der ECOLEF-Studie hat vor kurzem neuere Erkenntnisse58

vorgelegt, die diese Bedenken bestätigen, wonach die FIUs von mindestens zwei

Mitgliedstaaten keinen Zugang zu steuerlichen Informationen haben.59 Der Sachstand auf

Ebene der EU lässt somit darauf schließen, dass bei der wechselseitigen Zusammenarbeit

zwischen FIUs und Steuerbehörden noch Raum für Verbesserungen ist.

Um die Einhaltung der Steuervorschriften zu gewährleisten, ist es schließlich von

zentraler Bedeutung, die Zusammenarbeit zwischen den Steuerverwaltungen und den

58 Prof. Dr. Brigitte Unger, für den PANA-Ausschuss organisierter Workshop zu Geldwäsche und Steuerhinterziehung, 27. Januar 2017: Powerpoint-Präsentation.

59 Deutschland und Irland.

Ex-post-Folgenabschätzungen

PE 598.603 28

FIUs auszubauen, den Informationsaustausch zu intensivieren und ein abgestimmtes

Konzept für die Analyse der Verdachtsmeldungen auszuarbeiten.

3.2. Zugang zu Informationen über die wirtschaftlichen Eigentümer

Artikel 8 der dritten Geldwäscherichtlinie enthält Bestimmungen zur Feststellung der

Identität der wirtschaftlichen Eigentümer, die die Meldeverpflichteten im Rahmen ihrer

kundenbezogenen Sorgfaltspflichten (Customer Due Diligence – CDD) vorzunehmen

haben. Die vierte Geldwäscherichtlinie enthält weitere detaillierte Bestimmungen, die

sich auch auf den Zugang der FIUs zu Informationen über die wirtschaftlichen

Eigentümer beziehen: