Embed Size (px)

Citation preview

October 2011

Magnitogorsk Steel (MMK)

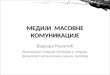

38%

33%

24%

6% 7%

10% 11%

5% 5% 4%

10%

7% 4% 5%

6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Russia NAFTA EU-27 China Middle East

2010 2011E 2012E

1 215 1 207

1 119

1 284

1 359

1 441

1 000

1 100

1 200

1 300

1 400

1 500

2007 2008 2009 2010 2011E 2012E

Global Steel Industry Highlights

World Steel Consumption, mln tonnes Apparent Steel Consumption Growth, % y-on-y

World Steel Production, mln tonnes Finished Steel Production/Consumption in China, mln tonnes

2

Source: WSA, Nomura

Source: WSA Source: WSA, Nomura

15%

6%

6% World steel consumption

continues to grow

Russian market demonstrates the

highest growth rates

576 632

657 677 680 685 690

535 573

602 620 630 639 649

-24 -24 -25 -26 -27 -28 -29 -100

0

100

200

300

400

500

600

700

800

2009 2010 2011E 2012E 2013E 2014E 2015E

Production Consumption Export

656 574

787

627

810

685

0

250

500

750

1 000

ROW China

2009 2010 2011Е

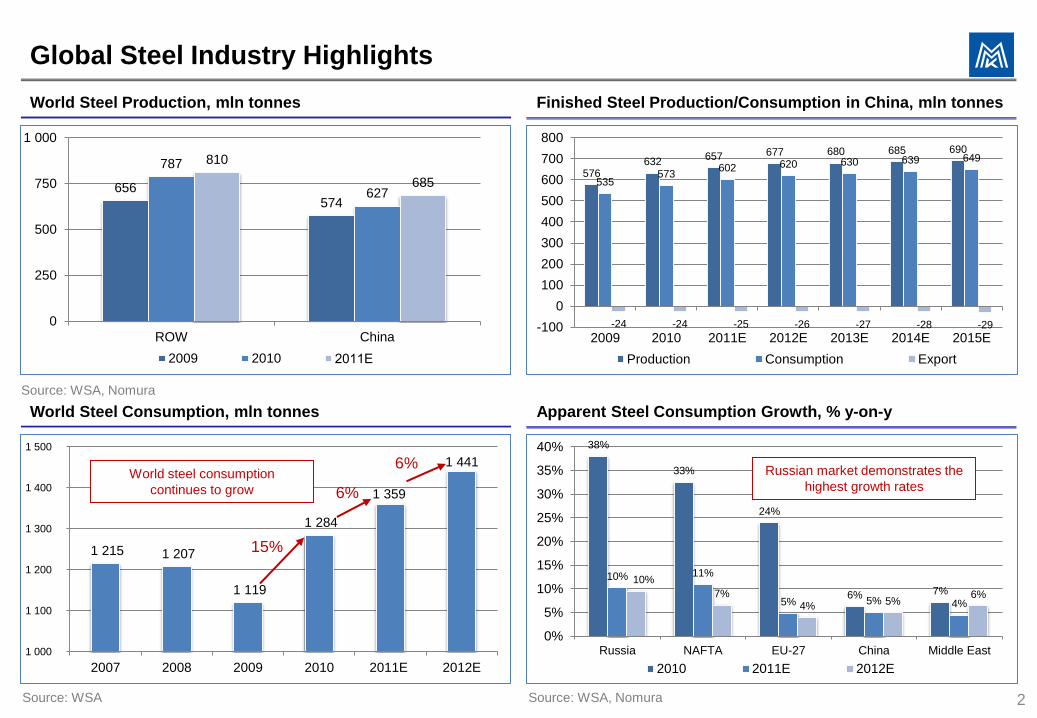

5,1 8,0 8,5 9,3

4,9

6,7 7,7

8,6

1,4

2,6 2,9

3,2

2,2

2,3 2,5

2,7

0,1

0,2 0,2

0,2

0

5

10

15

20

25

2009 2010 2011E 2012E

Construction Pipe plants Machinery Coating and metalwork Other

0,9 1,2 1,2 0,8 1,4 1,5 1,6

0,3 0,4 0,3

0,2

0,4 0,4 0,5 1,0 1,3

0,9 0,9

1,0 1,2

1,3 0,7

0,6 0,5

0,4

0,7 0,8

0,8 1,7

2,7

1,9

1,0

1,7 1,8

2,0

0

1

2

3

4

5

6

7

2006 2007 2008 2009 2010 2011E 2012E

Coated products C/r products Thick plate H/r products Long products

Russian Steel Dynamics

BOF Shop Domestic Flat Steel Consumption, mln tonnes

Steel Consumption in Russia and Export, mln tonnes Russian Import Structure, mln tonnes

3

Source: Metal Expert

HVA products

Source: Metal Courrier

Source: Metal Expert

13,7

19,8 21,9

24,0

Russia sees solid import

volumes, mostly of HVA

products

13,7 19,8 21,9 24,0

10,4

13,7 15,1

16,5 3,2

4,0 4,4

4,8 30,0

27,3 30,1

32,9

0

20

40

60

80

2009 2010 2011E 2012E

Flat steel Long steel Other steel products Export

6,1 6,2

1,1

2,2

0,9

9,1

7,8

2,1 2,6

1,2

10,4

8,6

2,5 2,9

1,3

11,0

9,4

2,8 3,2

1,4

0,0

2,0

4,0

6,0

8,0

10,0

12,0

Pipe making Construction Machine building(incl. car-makers)

Metalware Bridge&Shipbuilding

2009 2010 2011E 2012E

Russian Market Growth Prospects

Capacities Utilization in Russia, % MMK Finished Products Output, th. tonnes

Domestic Steel Price Dynamics, USD/tonne Russian Steel Consumption by Industry, mln tonnes

4

50%

60%

70%

80%

90%

100%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Cast Iron Crude Steel Rolled Steel Steel Pipes

Steel consumption by major

industries is bound to grow

by 20% on average

Pipe-making hits 100% utilization rate

Source: Chermet Source: MMK

Source: Metal Courrier Source: Metal Torg

0

500

1 000

1 500

2 000

2 500

3 000

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Q3 2

011

400

600

800

1 000

1 200

Re-bar H/r Flat Steel C/r Flat Steel Galvanized steel

5

MMK – Russian Steel Leader

Largest single-site steelmaker in Russia with current crude steel capacity of 14 mln tonnes

Currently planned production growth of more than 45% by 2013 from 2010

Production of HVA products currently expected to almost double by 2013 from 2010, representing 45% share of

total production volumes

Import substitution strategy: favorable geographical location to meet strong demand from the most intensive steel

consuming regions of Russia – the Urals and Volga regions

Great play on Russian infrastructure:

• 17.7% domestic steel market share enables MMK to benefit from premium pricing for domestic sales

• Largest exposure to pipe-manufacturing, auto-building and heavy machinery

Disciplined investment strategy with priority given to investments in high-return projects and high-quality assets

investments approach

The most modern asset base – over USD 7 bn of investments over the last 4 years

Mill 5000 Shop Mill 5000 Galvanizing Line

6

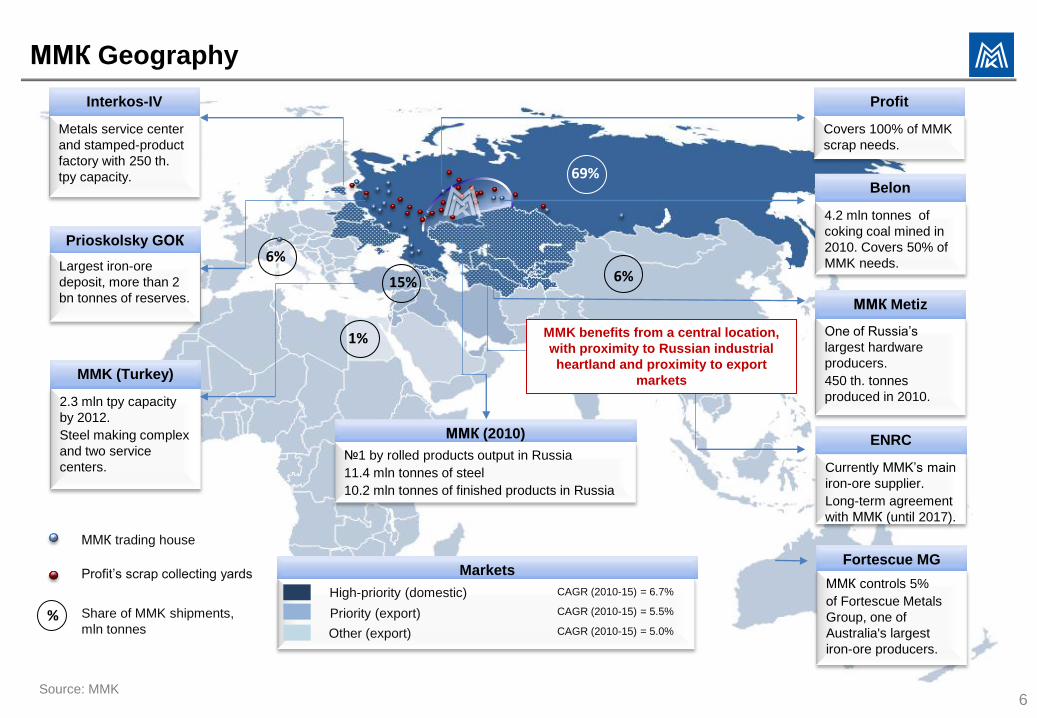

ММК Geography

2.3 mln tpy capacity

by 2012.

Steel making complex

and two service

centers.

Metals service center

and stamped-product

factory with 250 th.

tpy capacity.

4.2 mln tonnes of

coking coal mined in

2010. Covers 50% of

MMK needs. Largest iron-ore

deposit, more than 2

bn tonnes of reserves.

Interkos-IV

Prioskolsky GОК

MMK (Turkey)

ENRC

Belon

One of Russia’s

largest hardware

producers.

450 th. tonnes

produced in 2010.

ММК Metiz

Profit

Source: MMK

Covers 100% of MMK

scrap needs.

ММК trading house

69%

6% 15%

6%

1%

High-priority (domestic)

Priority (export)

Markets

Other (export)

ММК (2010)

№1 by rolled products output in Russia

11.4 mln tonnes of steel

10.2 mln tonnes of finished products in Russia

% Share of MMK shipments,

mln tonnes

Profit’s scrap collecting yards

CAGR (2010-15) = 5.5%

CAGR (2010-15) = 5.0%

CAGR (2010-15) = 6.7%

Currently MMK’s main

iron-ore supplier.

Long-term agreement

with ММК (until 2017).

ММК controls 5%

оf Fortescue Metals

Group, one of

Australia's largest

iron-ore producers.

Fortescue MG

MMK benefits from a central location,

with proximity to Russian industrial

heartland and proximity to export

markets

0

5 000

10 000

15 000

20 000

2010 2011E 2012E 2013E 2014Е

ММК, currently run capacities MMK, upside on current capacities MMK-Turkey

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

2009 2010 2011E 2012E 2013E 2014Е MMK MMK (Turkey) HVA products

75 79

146

240 279

392

212

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

50

100

150

200

250

300

350

400

450

Long steel HR flatsteel

CR flatsteel

Mill 5000plate

Galvanizedsteel

Formedsections

Colour -coated steel

EBITDA/t (LHS) EBITDA margin (RHS)

13% 14% 13% 17% 18% 19%

12% 10% 9% 9% 11% 11%

5% 13% 15% 14% 14% 14%

58% 51% 50% 47% 45% 42%

11% 10% 12% 13% 13% 14%

0%

20%

40%

60%

80%

100%

2009 2010 2011E 2012E 2013Е 2014Е

Downstream products Flat cold-rolled products Thick plate (Mill 5000)

Flat hot-rolled products Long products Slabs and billets

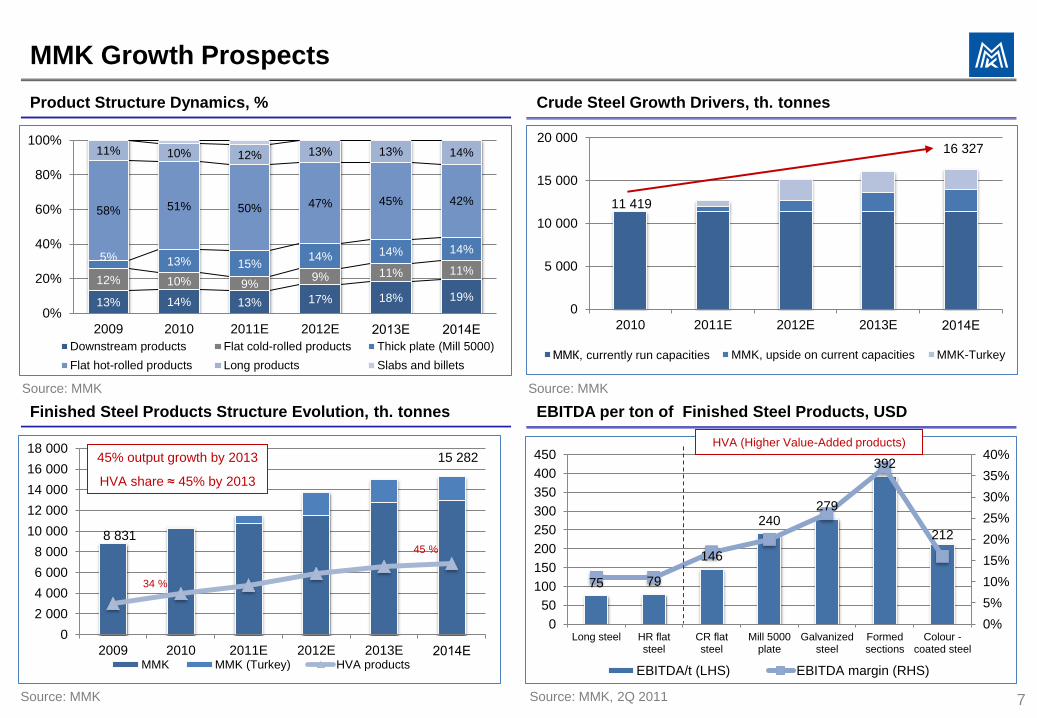

MMK Growth Prospects

Finished Steel Products Structure Evolution, th. tonnes EBITDA per ton of Finished Steel Products, USD

Product Structure Dynamics, % Crude Steel Growth Drivers, th. tonnes

7

45% output growth by 2013

HVA share ≈ 45% by 2013

HVA (Higher Value-Added products)

8 831

15 282

34 %

Sourсe: MMK Sourсe: MMK

Sourсe: MMK, 2Q 2011 Sourсe: MMK

11 419

16 327

45 %

252

230

329

452

400

261

110

66

10 000

10 500

11 000

11 500

2011Е 2012Е

Coated steel Cold-rolled steel Thick plate Hot-rolled steel Long product Other

1 495

127

1 638

415

87

455

1 157

289

1 266

452

752 823

400

1 839

661

2 014

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

ММК 2011Е (growth to 2010)

Import 2011Е ММК 2012Е (growth to 2010)

Import 2012Е

Coated steel Cold-rolled steel Thick plate Hot-rolled steel Long product

7%

40%

29%

22%

32%

8%

41%

34%

26%

34%

11%

32% 32%

31%

51%

0%

10%

20%

30%

40%

50%

Long steel H/r steel Thick plate C/r steel Coated steel

2010 2011E 2012E

-5 381

-1 583

453

995

-5 932

-1 746

500

1 097

-6 496

-1 911

547 1 202

-7 000

-6 000

-5 000

-4 000

-3 000

-2 000

-1 000

0

1 000

2 000

Hot-rolled steel Long product Thick plate Coated steel

2010 2011E 2012E

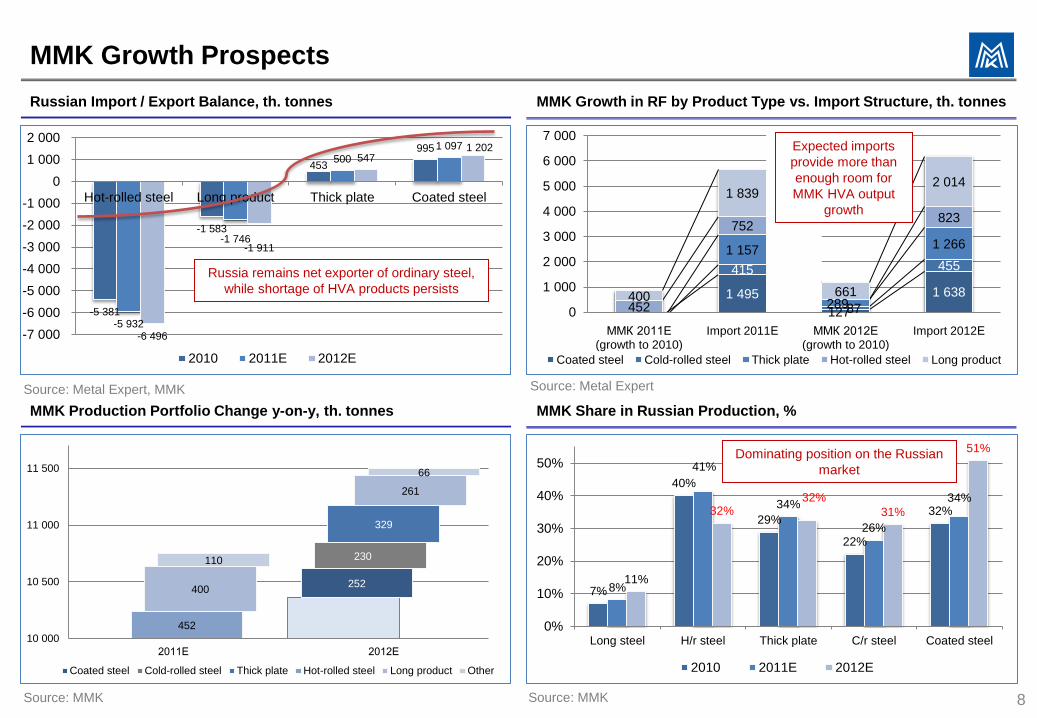

MMK Growth Prospects

MMK Production Portfolio Change y-on-y, th. tonnes MMK Share in Russian Production, %

Russian Import / Export Balance, th. tonnes MMK Growth in RF by Product Type vs. Import Structure, th. tonnes

8 Source: MMK Source: MMK

Source: Metal Expert, MMK Source: Metal Expert

Russia remains net exporter of ordinary steel,

while shortage of HVA products persists

Dominating position on the Russian

market

Expected imports

provide more than

enough room for

MMK HVA output

growth

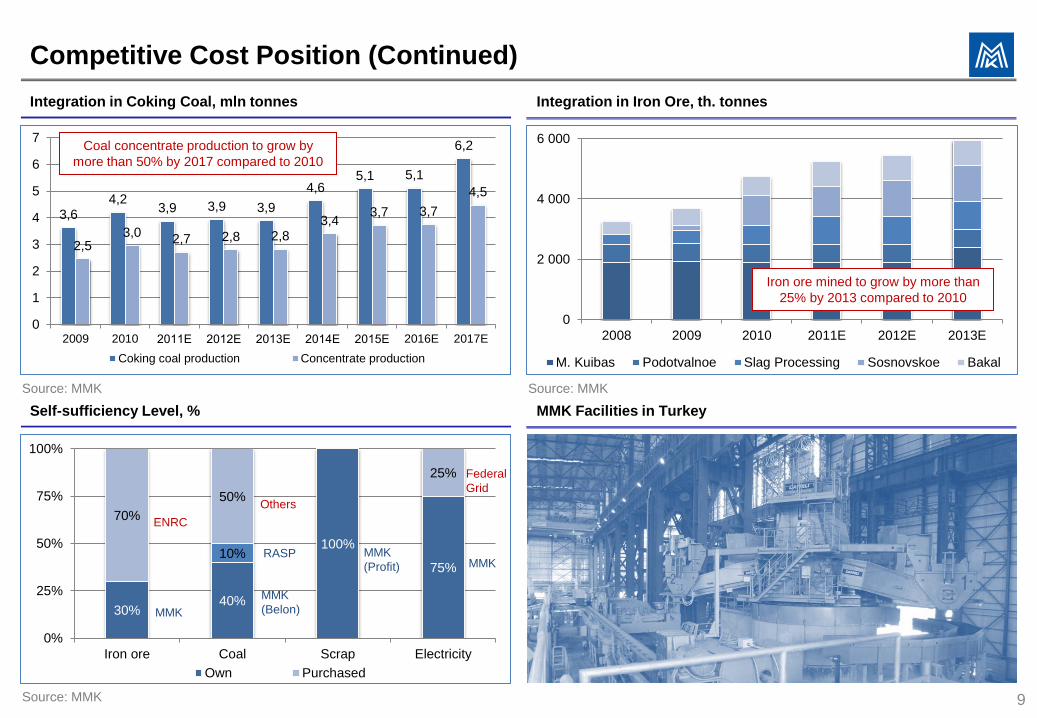

Competitive Cost Position (Continued)

30% 40%

100%

75% 10%

70%

50%

25%

0%

25%

50%

75%

100%

Iron ore Coal Scrap Electricity

Own Purchased

Self-sufficiency Level, % MMK Facilities in Turkey

3,6 4,2

3,9 3,9 3,9

4,6 5,1 5,1

6,2

2,5 3,0

2,7 2,8 2,8 3,4

3,7 3,7

4,5

0

1

2

3

4

5

6

7

2009 2010 2011Е 2012Е 2013Е 2014Е 2015Е 2016E 2017E

Coking coal production Concentrate production

Integration in Coking Coal, mln tonnes

0

2 000

4 000

6 000

2008 2009 2010 2011E 2012E 2013E

M. Kuibas Podotvalnoe Slag Processing Sosnovskoe Bakal

Integration in Iron Ore, th. tonnes

9

-19

Sourсe: MMK

ENRC

Others

Federal

Grid

MMK

MMK

(Belon)

MMK

(Profit) MMK RASP

Sourсe: MMK

Sourсe: MMK

Coal concentrate production to grow by

more than 50% by 2017 compared to 2010

Iron ore mined to grow by more than

25% by 2013 compared to 2010

7 000

8 000

9 000

10 000

11 000

12 000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

ММК Severstal NLMK

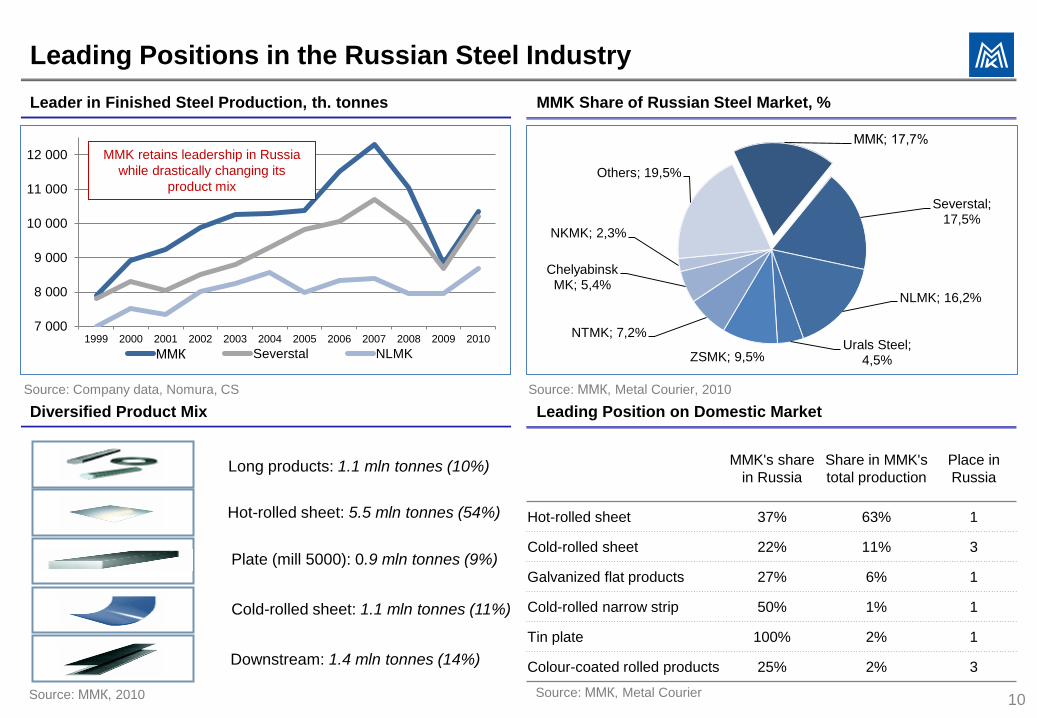

Leading Positions in the Russian Steel Industry

Diversified Product Mix Leading Position on Domestic Market

Leader in Finished Steel Production, th. tonnes MMK Share of Russian Steel Market, %

10

Hot-rolled sheet: 5.5 mln tonnes (54%)

Cold-rolled sheet: 1.1 mln tonnes (11%)

Long products: 1.1 mln tonnes (10%)

Downstream: 1.4 mln tonnes (14%)

Plate (mill 5000): 0.9 mln tonnes (9%)

Picture

Picture

Picture

Picture

Source: Company data, Nomura, CS Source: ММК, Metal Courier, 2010

Source: ММК, Metal Courier

MMK retains leadership in Russia

while drastically changing its

product mix

ММК; 17,7%

Severstal; 17,5%

NLMK; 16,2%

Urals Steel; 4,5% ZSMK; 9,5%

NTMK; 7,2%

Chelyabinsk MK; 5,4%

NKMK; 2,3%

Others; 19,5%

Source: ММК, 2010

MMK's share

in Russia

Share in MMK's

total production

Place in

Russia

Hot-rolled sheet 37% 63% 1

Cold-rolled sheet 22% 11% 3

Galvanized flat products 27% 6% 1

Cold-rolled narrow strip 50% 1% 1

Tin plate 100% 2% 1

Colour-coated rolled products 25% 2% 3

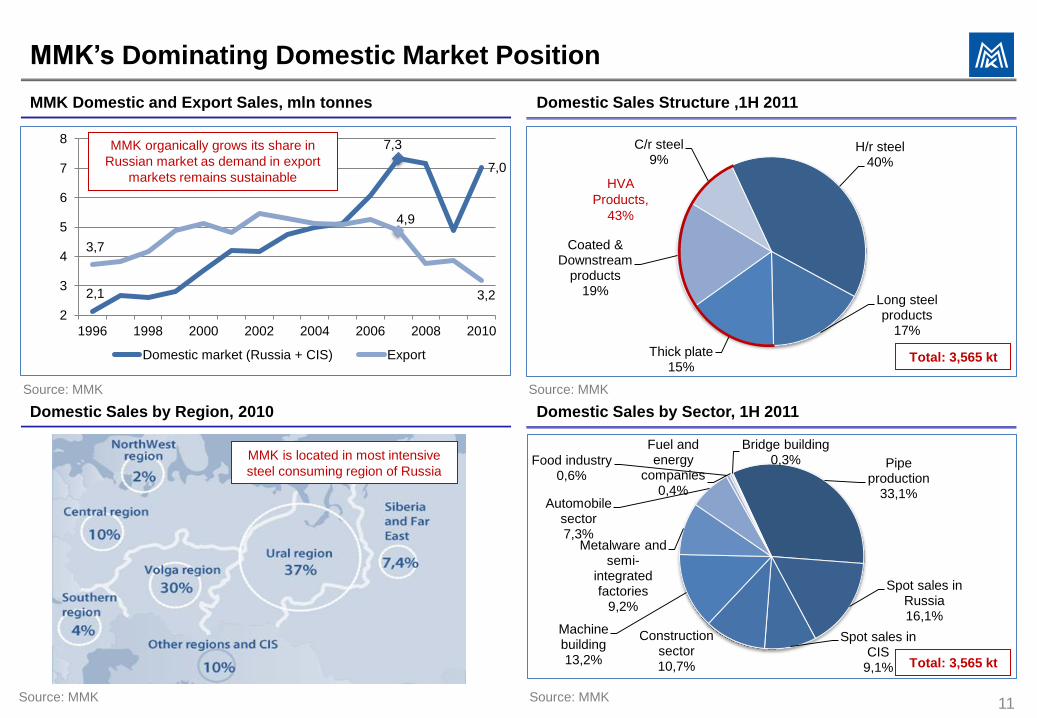

2,1

7,3

7,0

3,7

4,9

3,2

2

3

4

5

6

7

8

1996 1998 2000 2002 2004 2006 2008 2010

Domestic market (Russia + CIS) Export

Pipe production

33,1%

Spot sales in Russia 16,1%

Spot sales in CIS

9,1%

Construction sector 10,7%

Machine building 13,2%

Metalware and semi-

integrated factories

9,2%

Automobile sector 7,3%

Food industry 0,6%

Fuel and energy

companies 0,4%

Bridge building 0,3%

H/r steel 40%

Long steel products

17%

Thick plate 15%

Coated & Downstream

products 19%

C/r steel 9%

MMK’s Dominating Domestic Market Position

Domestic Sales by Region, 2010 Domestic Sales by Sector, 1H 2011

MMK Domestic and Export Sales, mln tonnes Domestic Sales Structure ,1H 2011

11

HVA

Products,

43%

Total: 3,565 kt

Source: MMK

Source: MMK Source: MMK

Source: MMK

MMK organically grows its share in

Russian market as demand in export

markets remains sustainable

Total: 3,565 kt

MMK is located in most intensive

steel consuming region of Russia

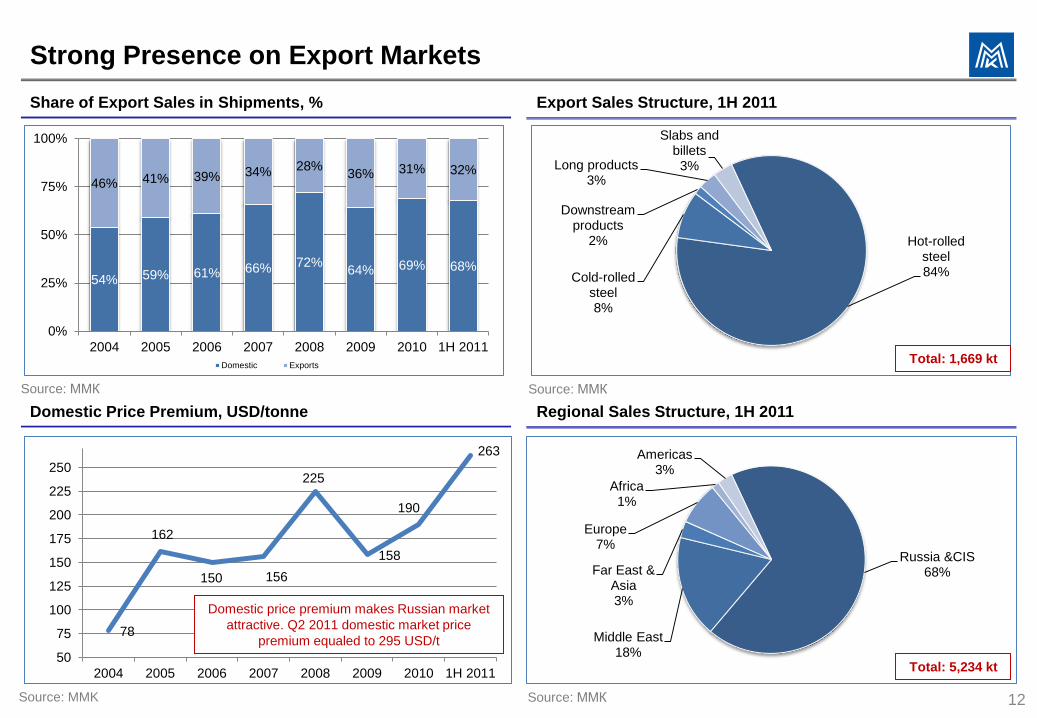

78

162

150 156

225

158

190

263

50

75

100

125

150

175

200

225

250

2004 2005 2006 2007 2008 2009 2010 1H 2011

Russia &CIS 68%

Middle East 18%

Far East & Asia 3%

Europe 7%

Africa 1%

Americas 3%

Hot-rolled steel 84% Cold-rolled

steel 8%

Downstream products

2%

Long products 3%

Slabs and billets 3%

Strong Presence on Export Markets

Domestic Price Premium, USD/tonne Regional Sales Structure, 1H 2011

Share of Export Sales in Shipments, % Export Sales Structure, 1H 2011

12

Total: 1,669 kt

Total: 5,234 kt

Source: ММК Source: ММК

Source: ММК Source: MMK

Domestic price premium makes Russian market

attractive. Q2 2011 domestic market price

premium equaled to 295 USD/t

54% 59% 61% 66% 72% 64% 69% 68%

46% 41% 39% 34% 28% 36% 31% 32%

0%

25%

50%

75%

100%

2004 2005 2006 2007 2008 2009 2010 1H 2011

Domestic Exports

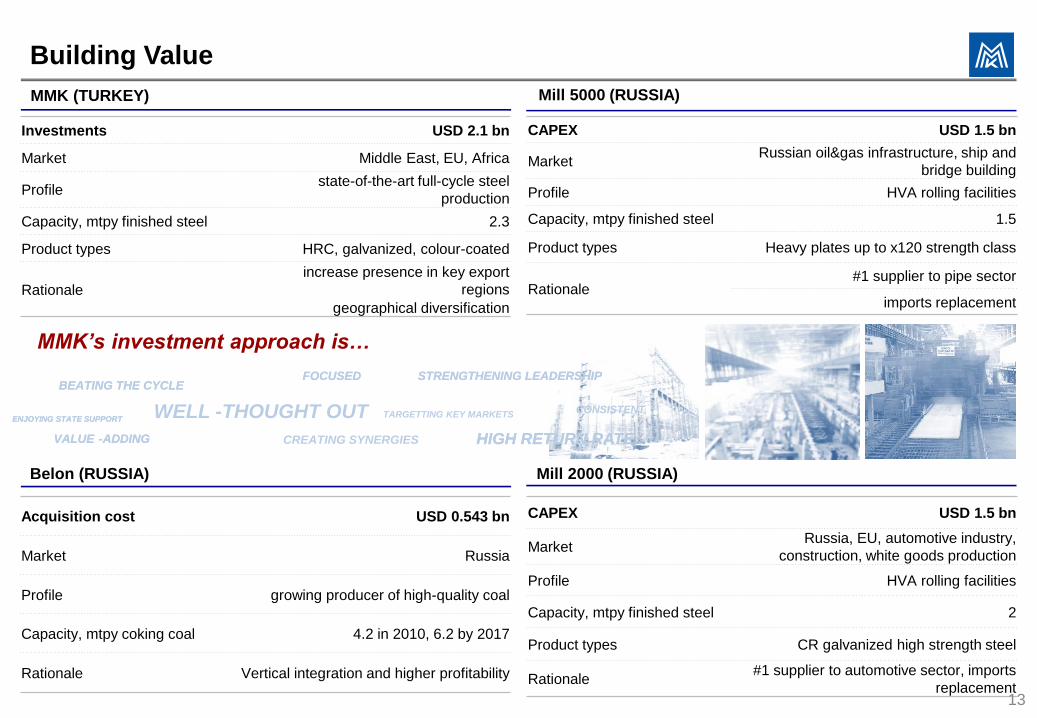

CAPEX USD 1.5 bn

Market Russia, EU, automotive industry,

construction, white goods production

Profile HVA rolling facilities

Capacity, mtpy finished steel 2

Product types CR galvanized high strength steel

Rationale #1 supplier to automotive sector, imports

replacement

Acquisition cost USD 0.543 bn

Market Russia

Profile growing producer of high-quality coal

Capacity, mtpy coking coal 4.2 in 2010, 6.2 by 2017

Rationale Vertical integration and higher profitability

CAPEX USD 1.5 bn

Market Russian oil&gas infrastructure, ship and

bridge building

Profile HVA rolling facilities

Capacity, mtpy finished steel 1.5

Product types Heavy plates up to x120 strength class

Rationale #1 supplier to pipe sector

imports replacement

Investments USD 2.1 bn

Market Middle East, EU, Africa

Profile state-of-the-art full-cycle steel

production

Capacity, mtpy finished steel 2.3

Product types HRC, galvanized, colour-coated

Rationale

increase presence in key export

regions

geographical diversification

Building Value

Belon (RUSSIA) Mill 2000 (RUSSIA)

MMK (TURKEY) Mill 5000 (RUSSIA)

13

MMK’s investment approach is…

HIGH RETURN RATE VALUE - ADDING

ENJOYING STATE SUPPORT

STRENGTHENING LEADERSHIP FOCUSED BEATING THE CYCLE

HIGH RETURN RATE CREATING SYNERGIES VALUE - ADDING

CONSISTENT TARGETTING KEY MARKETS WELL - THOUGHT OUT ENJOYING STATE SUPPORT

STRENGTHENING LEADERSHIP FOCUSED BEATING THE CYCLE

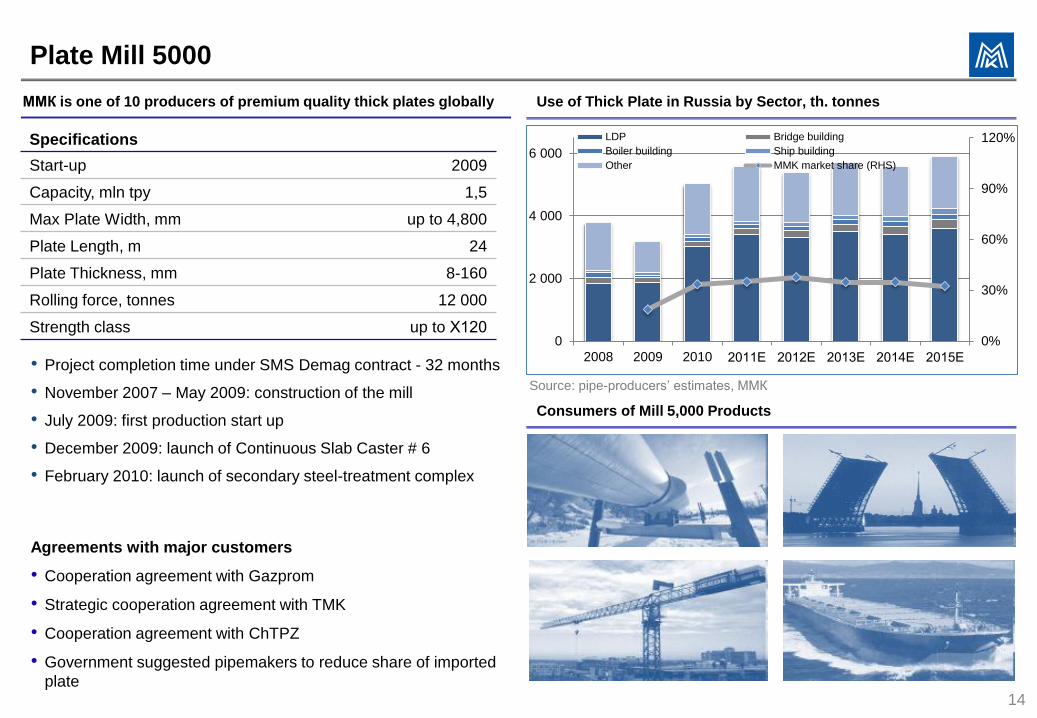

Plate Mill 5000

Consumers of Mill 5,000 Products

ММК is one of 10 producers of premium quality thick plates globally Use of Thick Plate in Russia by Sector, th. tonnes

• Project completion time under SMS Demag contract - 32 months

• November 2007 – May 2009: construction of the mill

• July 2009: first production start up

• December 2009: launch of Continuous Slab Caster # 6

• February 2010: launch of secondary steel-treatment complex

Agreements with major customers

• Cooperation agreement with Gazprom

• Strategic cooperation agreement with TMK

• Cooperation agreement with ChTPZ

• Government suggested pipemakers to reduce share of imported

plate

14

Specifications

Start-up 2009

Capacity, mln tpy 1,5

Max Plate Width, mm up to 4,800

Plate Length, m 24

Plate Thickness, mm 8-160

Rolling force, tonnes 12 000

Strength class up to Х120

Source: pipe-producers’ estimates, ММК

0%

30%

60%

90%

120%

0

2 000

4 000

6 000

2008 2009 2010 2011Е 2012Е 2013Е 2014Е 2015Е

LDP Bridge building

Boiler building Ship building

Other MMK market share (RHS)

MMK; 35%

Import; 19%

Others; 47%

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2009 2010 2011Е Nord Stream Yamal-Europe

Sakhalin-Khabarovsk-Vladivostok VSTO-2

BTS-2 Current pipelines replacement

Export

-1 000

0

1 000

2 000

3 000

4 000

Production of LDP LDP imports

LDP exports Consumption of LDP in Russia

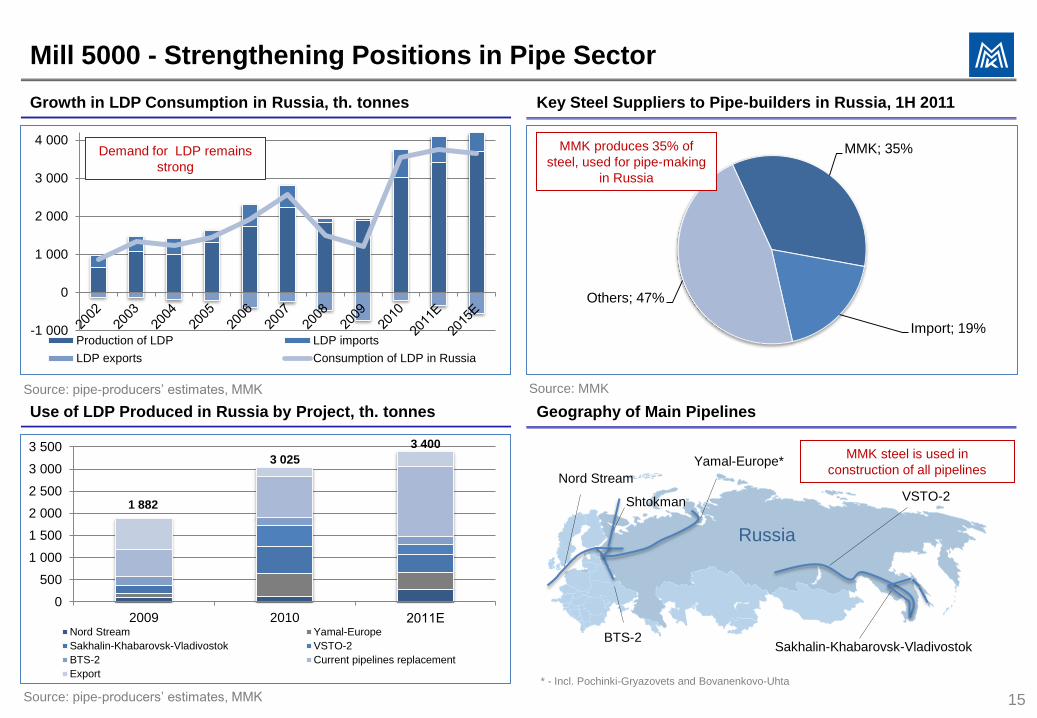

Mill 5000 - Strengthening Positions in Pipe Sector

Use of LDP Produced in Russia by Project, th. tonnes Geography of Main Pipelines

Growth in LDP Consumption in Russia, th. tonnes Key Steel Suppliers to Pipe-builders in Russia, 1H 2011

15

BTS-2

VSTO-2

Sakhalin-Khabarovsk-Vladivostok

Yamal-Europe*

Nord Stream

Russia

1 882

3 025

Source: pipe-producers’ estimates, MMK

Source: pipe-producers’ estimates, MMK Source: MMK

MMK produces 35% of

steel, used for pipe-making

in Russia

MMK steel is used in

construction of all pipelines

Demand for LDP remains

strong

3 400

* - Incl. Pochinki-Gryazovets and Bovanenkovo-Uhta

Shtokman

765

565 519

426 399

261

156

67 12 10

0

100

200

300

400

500

600

700

800

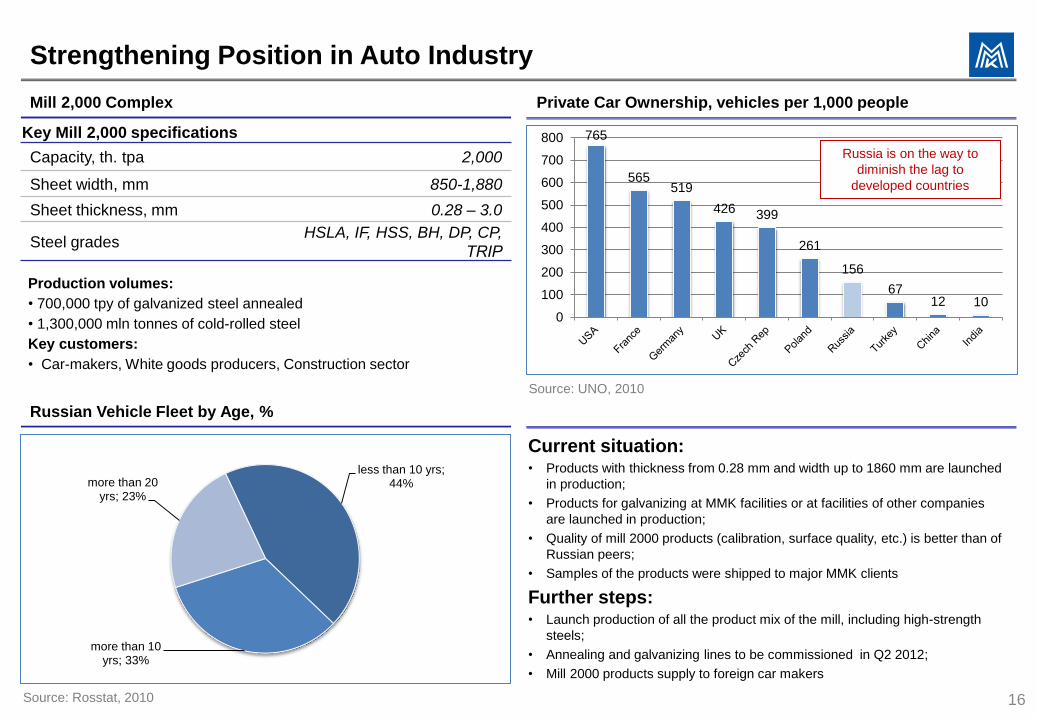

Strengthening Position in Auto Industry

Russian Vehicle Fleet by Age, %

Mill 2,000 Complex Private Car Ownership, vehicles per 1,000 people

16

Key Mill 2,000 specifications

Capacity, th. tpa 2,000

Sheet width, mm 850-1,880

Sheet thickness, mm 0.28 – 3.0

Steel grades HSLA, IF, HSS, BH, DP, CP,

ТRIP

Production volumes:

• 700,000 tpy of galvanized steel annealed

• 1,300,000 mln tonnes of cold-rolled steel

Key customers:

• Car-makers, White goods producers, Construction sector

Source: Rosstat, 2010

Source: UNO, 2010

Russia is on the way to

diminish the lag to

developed countries

less than 10 yrs; 44%

more than 10 yrs; 33%

more than 20 yrs; 23%

Current situation: • Products with thickness from 0.28 mm and width up to 1860 mm are launched

in production;

• Products for galvanizing at MMK facilities or at facilities of other companies

are launched in production;

• Quality of mill 2000 products (calibration, surface quality, etc.) is better than of

Russian peers;

• Samples of the products were shipped to major MMK clients

Further steps: • Launch production of all the product mix of the mill, including high-strength

steels;

• Annealing and galvanizing lines to be commissioned in Q2 2012;

• Mill 2000 products supply to foreign car makers

3 678

4 240

0

1 000

2 000

3 000

4 000

2008 2009 2010 2011Е 2012Е 2013Е 2014Е 2015Е 2020Е

All vehicle types output, th.pieces Steel consumption by car-makers

75%

51% 40%

17%

24%

10%

7%

22%

40%

2% 3% 10%

0%

25%

50%

75%

100%

2010 2015Е 2020Е

Mild Steel AHSS HSS UHSS

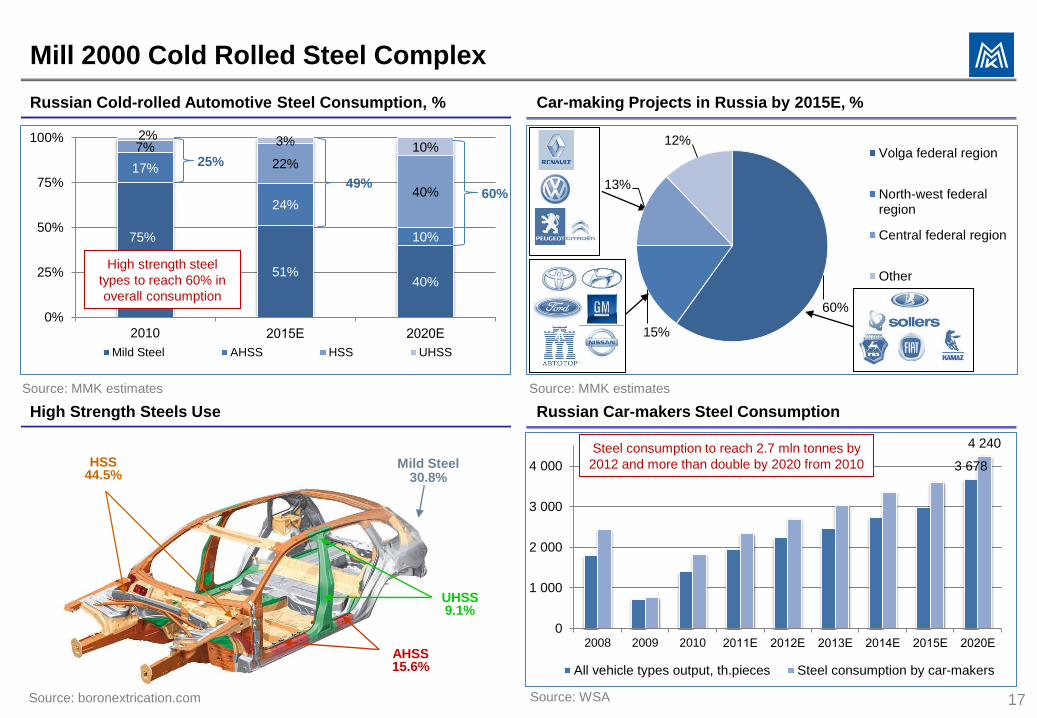

Mill 2000 Cold Rolled Steel Complex

High Strength Steels Use Russian Car-makers Steel Consumption

Russian Cold-rolled Automotive Steel Consumption, % Car-making Projects in Russia by 2015E, %

17

Source: boronextrication.com

Mild Steel 30.8%

UHSS 9.1%

HSS 44.5%

AHSS 15.6%

High strength steel

types to reach 60% in

overall consumption

Source: WSA

Source: MMK estimates Source: MMK estimates

60%

15%

13%

12% Volga federal region

North-west federalregion

Central federal region

Other

Steel consumption to reach 2.7 mln tonnes by

2012 and more than double by 2020 from 2010

60%

25%

49%

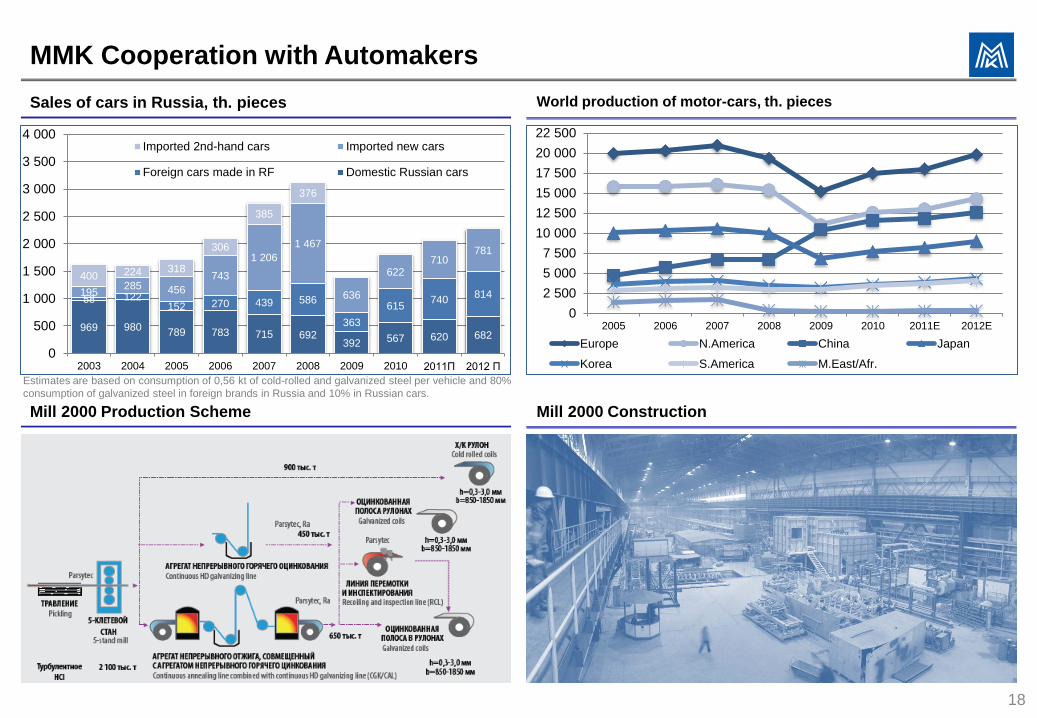

MMK Cooperation with Automakers

Mill 2000 Production Scheme

Sales of cars in Russia, th. pieces World production of motor-cars, th. pieces

18

Estimates are based on consumption of 0,56 kt of cold-rolled and galvanized steel per vehicle and 80%

consumption of galvanized steel in foreign brands in Russia and 10% in Russian cars.

0

2 500

5 000

7 500

10 000

12 500

15 000

17 500

20 000

22 500

2005 2006 2007 2008 2009 2010 2011E 2012E

Europe N.America China Japan

Korea S.America M.East/Afr.

969 980 789 783 715 692

392 567 620 682

58 122 152 270 439 586

363

615 740

814 195 285 456

743

1 206

1 467

636

622 710

781

400 224 318

306

385

376

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2003 2004 2005 2006 2007 2008 2009 2010 2011П 2012 П

Imported 2nd-hand cars Imported new cars

Foreign cars made in RF Domestic Russian cars

Mill 2000 Construction

Entry to Rapidly Growing Turkish Market

Flat Steel Market in Turkey, mln tonnes Long Steel Market in Turkey, mln tonnes

Locations of Key Markets

19 Source: Metal Expert

Source: ING

Istanbul

Iskenderun

Europe

Middle East

Africa

Priority export markets

Important export markets

Turkish Flat Steel Market Structure, %

4,0

5,5 6,8

8,7 9,2 9,2 9,2 8,0

8,6 9,2

9,9 10,6

11,3 12,2

-4,0 -3,1

-2,4 -1,2 -1,4

-2,1 -2,9

-6

-4

-2

0

2

4

6

8

10

12

14

2009 2010E 2011E 2012E 2013E 2014E 2015E

Flat steel production Flat steel consumption Balance

MMK will focus on flat steel in

Turkey, where there is a

structural shortfall

Pipe production;

25%

Metal Service Centers; 19%

Spot sales; 18%

Auto industry; 13%

Packaging; 7%

Boiler making; 6%

Other; 12%

20,5

24,0 24,5 24,9 25,7 25,7 25,7

9,7 10,2 10,7 11,3 11,9

12,5 13,2

10,8

13,8 13,7 13,6 13,8 13,2 12,5

0

5

10

15

20

25

30

2009 2010E 2011E 2012E 2013E 2014E 2015E

Long steel production Long steel consumption Balance

Source: Metal Expert

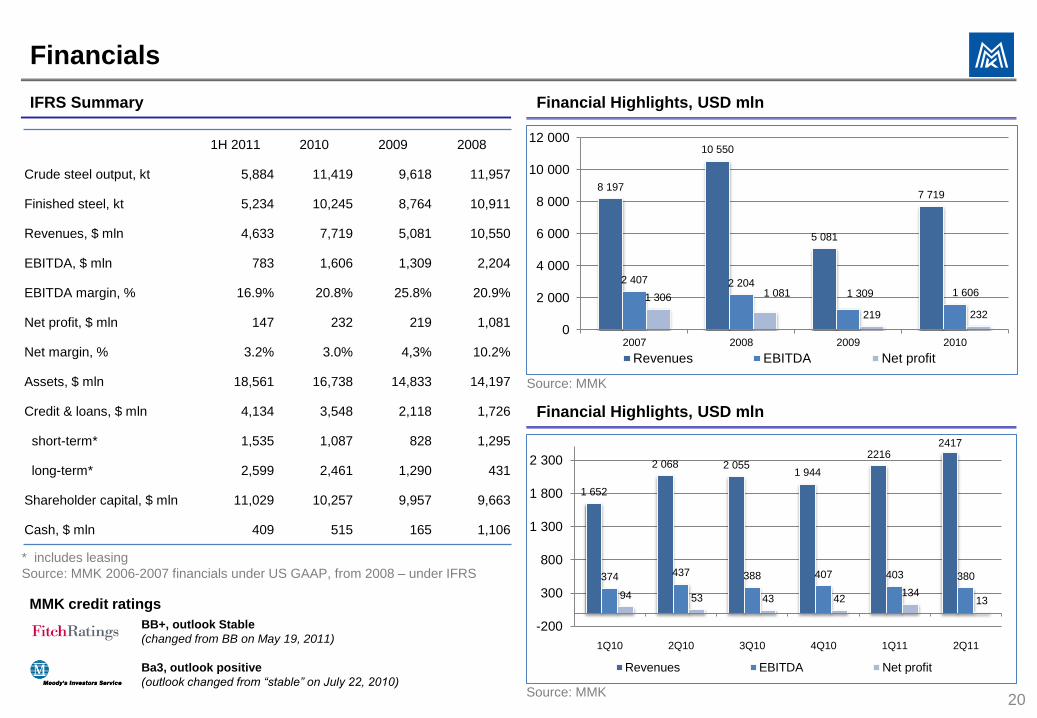

Financials

Financial Highlights, USD mln

IFRS Summary Financial Highlights, USD mln

20

Source: MMK

Source: MMK

* includes leasing

Source: MMK 2006-2007 financials under US GAAP, from 2008 – under IFRS

BB+, outlook Stable

(changed from BB on May 19, 2011)

Ba3, outlook positive

(outlook changed from “stable” on July 22, 2010)

MMK credit ratings

1H 2011 2010 2009 2008

Crude steel output, kt 5,884 11,419 9,618 11,957

Finished steel, kt 5,234 10,245 8,764 10,911

Revenues, $ mln 4,633 7,719 5,081 10,550

EBITDA, $ mln 783 1,606 1,309 2,204

EBITDA margin, % 16.9% 20.8% 25.8% 20.9%

Net profit, $ mln 147 232 219 1,081

Net margin, % 3.2% 3.0% 4,3% 10.2%

Assets, $ mln 18,561 16,738 14,833 14,197

Credit & loans, $ mln 4,134 3,548 2,118 1,726

short-term* 1,535 1,087 828 1,295

long-term* 2,599 2,461 1,290 431

Shareholder capital, $ mln 11,029 10,257 9,957 9,663

Cash, $ mln 409 515 165 1,106

8 197

10 550

5 081

7 719

2 407 2 204 1 309 1 606 1 306 1 081

219 232

0

2 000

4 000

6 000

8 000

10 000

12 000

2007 2008 2009 2010

Revenues EBITDA Net profit

1 652

2 068 2 055 1 944

2216 2417

374 437 388 407 403 380

94 53 43 42 134

13

-200

300

800

1 300

1 800

2 300

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11

Revenues EBITDA Net profit

21

Investment Highlights

• Key beneficiary of steel market recovery – fully financed production growth currently planned at >45%

by 2013

• Growing volumes and share of HVA products (45% by 2013) to secure sustainably high efficiency

• Focus on specialty steel products to replace imports in Russia and to capture domestic market price

premium

• Access to lucrative Turkish flat steel market with high-quality steel products

• Emphasized direct exposure to growing industry sectors in the domestic market – pipe-building,

automotive and heavy machinery industries

• Technological flexibility to address raw-material market fluctuations – crude steel production using

iron ore/coking coal vs. scrap

• Plans for further strengthening in commodities

Magnitogorsk Steel (MMK)

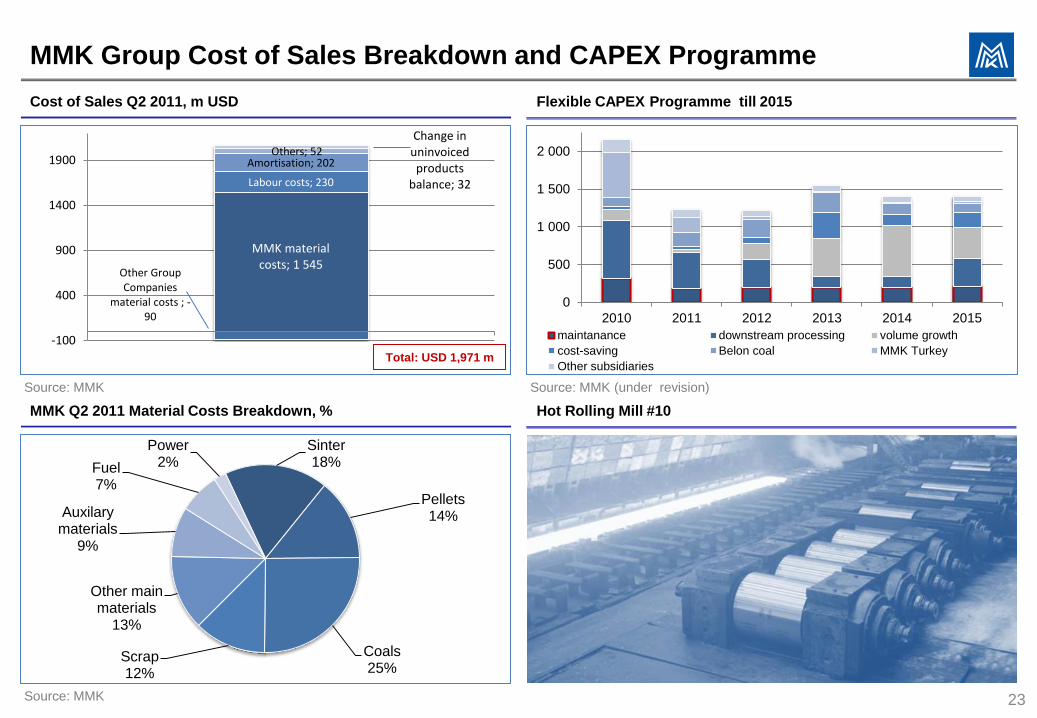

MMK material costs; 1 545

Other Group Companies

material costs ; -90

Labour costs; 230

Amortisation; 202 Others; 52

Change in uninvoiced products

balance; 32

-100

400

900

1400

1900

1

MMK Group Cost of Sales Breakdown and CAPEX Programme

MMK Q2 2011 Material Costs Breakdown, %

Cost of Sales Q2 2011, m USD Flexible CAPEX Programme till 2015

23

Sourсe: MMK (under revision)

Sourсe: MMK

Sourсe: MMK

Total: USD 1,971 m

0

500

1 000

1 500

2 000

2010 2011 2012 2013 2014 2015

maintanance downstream processing volume growth

cost-saving Belon coal MMK Turkey

Other subsidiaries

Hot Rolling Mill #10

Sinter 18%

Pellets 14%

Coals 25%

Scrap 12%

Other main materials

13%

Auxilary materials

9%

Fuel 7%

Power 2%

Iron ore; 37%

Coal; 26% Scrap

purchased; 12%

Other raw materials; 12%

Fuel and energy

purchased; 8%

Wages; 3%

Others; 3%

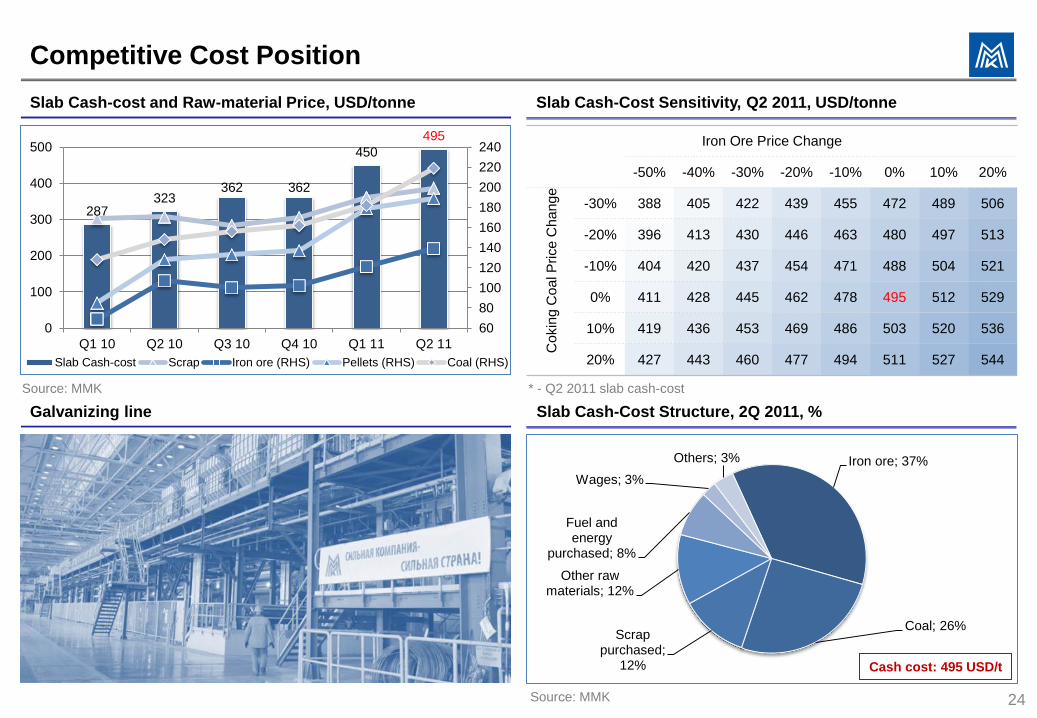

Competitive Cost Position

Galvanizing line Slab Cash-Cost Structure, 2Q 2011, %

Slab Cash-cost and Raw-material Price, USD/tonne

24

Cash cost: 495 USD/t

Slab Cash-Cost Sensitivity, Q2 2011, USD/tonne

Sourсe: MMK

Sourсe: MMK

* - Q2 2011 slab cash-cost

Iron Ore Price Change

-50% -40% -30% -20% -10% 0% 10% 20%

Co

kin

g C

oa

l P

rice

Ch

an

ge

-30% 388 405 422 439 455 472 489 506

-20% 396 413 430 446 463 480 497 513

-10% 404 420 437 454 471 488 504 521

0% 411 428 445 462 478 495 512 529

10% 419 436 453 469 486 503 520 536

20% 427 443 460 477 494 511 527 544

287 323

362 362

450

495

60

80

100

120

140

160

180

200

220

240

0

100

200

300

400

500

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11

Slab Cash-cost Scrap Iron ore (RHS) Pellets (RHS) Coal (RHS)

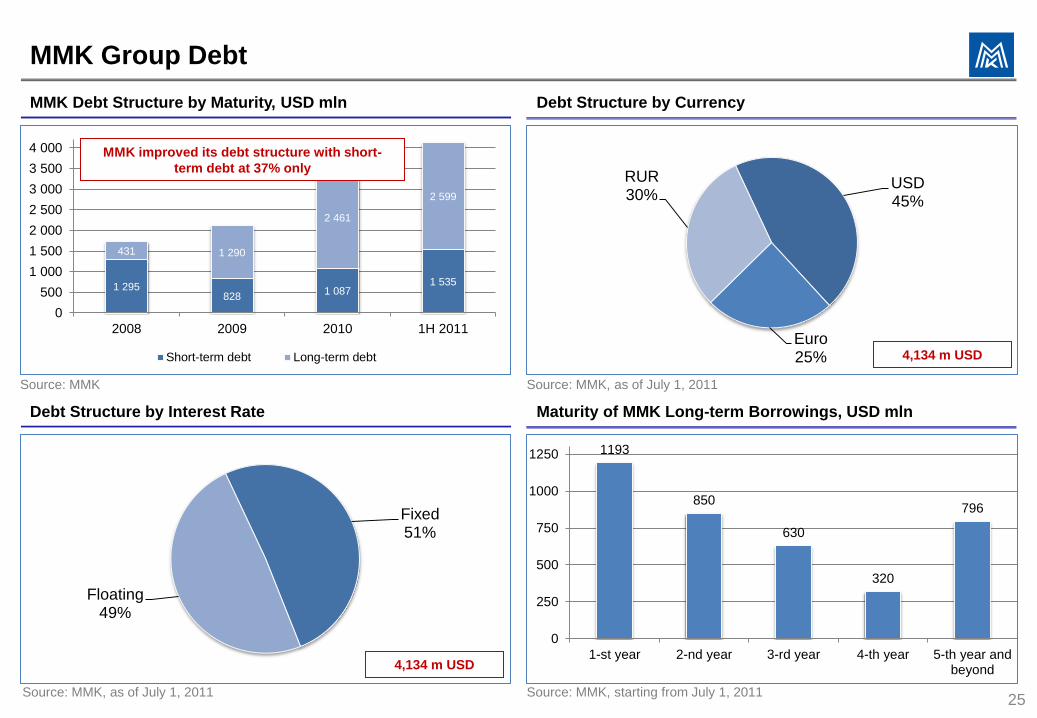

1 295 828

1 087 1 535

431 1 290

2 461

2 599

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2008 2009 2010 1H 2011

Short-term debt Long-term debt

MMK Group Debt

Debt Structure by Interest Rate Maturity of MMK Long-term Borrowings, USD mln

MMK Debt Structure by Maturity, USD mln Debt Structure by Currency

25

MMK improved its debt structure with short-

term debt at 37% only

Source: MMK, as of July 1, 2011

Source: MMK Source: MMK, as of July 1, 2011

Source: MMK, starting from July 1, 2011

4,134 m USD

4,134 m USD

1193

850

630

320

796

0

250

500

750

1000

1250

1-st year 2-nd year 3-rd year 4-th year 5-th year andbeyond

USD 45%

Euro 25%

RUR 30%

Fixed 51%

Floating 49%

0

500

1 000

1 500

2 000

2 500

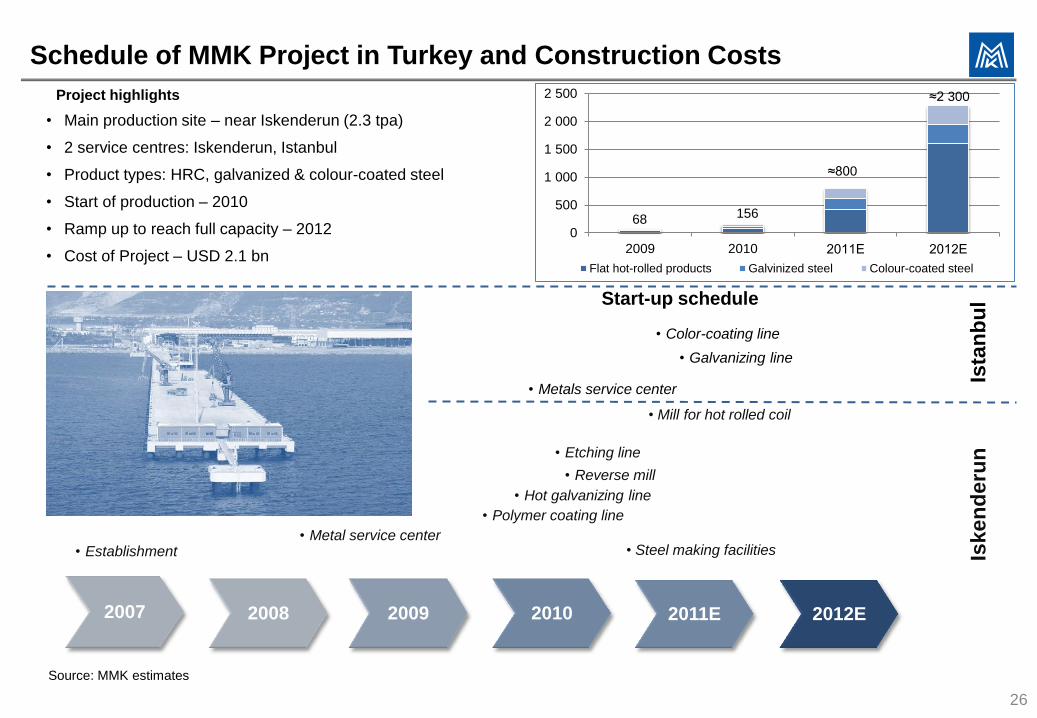

2009 2010 2011Е 2012Е

Flat hot-rolled products Galvinized steel Colour-coated steel

• Reverse mill

26

Schedule of MMK Project in Turkey and Construction Costs

• Establishment

2007 2008 2009 2010 2011E 2012E

• Metal service center

• Hot galvanizing line

• Etching line

• Polymer coating line

• Metals service center

• Galvanizing line

• Color-coating line

Iske

nd

eru

n

Ista

nb

ul

Source: MMK estimates

• Mill for hot rolled coil

Project highlights

• Main production site – near Iskenderun (2.3 tpa)

• 2 service centres: Iskenderun, Istanbul

• Product types: HRC, galvanized & colour-coated steel

• Start of production – 2010

• Ramp up to reach full capacity – 2012

• Cost of Project – USD 2.1 bn

Start-up schedule

68 156

≈800

≈2 300

• Steel making facilities

Contacts

THIS PRESENTATION IS FOR INFORMATION ONLY.

•THIS PRESENTATION IS FOR DISTRIBUTION IN UK ONLY AMONG THE PEOPLE HAVING PROFESSIONAL SKILL IN THE ISSUES RELATED TO INVESTMENTS WITHIN THE MEANING OF ARTICLE 19(5) OF DIRECTIVE ON FINANCIAL ADVERTISEMENT APPROVED IN 2005 ON THE BASIS OF LAW ON FINANCIAL SERVICES AND MARKETS 2000, OR THOSE PEOPLE, AMONG WHICH IT MAY BE LAWFULLY DISTRIBUTED. THIS INFORMATION IS CONFIDENTIAL AND PROVIDED TO YOU EXCLUSIVELY FOR YOUR REFERENCE. BY ACCEPTANCE OF THIS INFORMATION THE RECIPIENT HEREOF CONFIRMS THAT HE OR SHE IS A SPECIALIST IN THE SPHERE OF INVESTMENTS WITHIN THE MEANING OF ARTICLE 19(5) OF DIRECTIVE ON FINANCIAL ADVERTISEMENT APPROVED IN 2005 ON THE BASIS OF LAW ON FINANCIAL SERVICES AND MARKETS 2000, ACTING IN HIS OR HER NATURE.

•THIS PRESENTATION DOES NOT CONSTITUTE AN OFFER OR A PART THEREOF, OR INVITATION TO SELL OR TO ISSUE, OR TO SUBSCRIBE FOR OR OTHERWISE PURCHASE ANY SHARES IN THE COMPANY OR ANY OTHER SECURITIES AND NOTHING CONTAINED HEREIN SHALL FORM THE BASIS OF ANY CONTRACT OR COMMITMENT WHATSOEVER.

•THE INFORMATION CONTAINED HEREIN IS SUBJECT TO VERIFICATION, COMPLETION AND MAY BE SIGNIFICANTLY CHANGED. NONE OF THE PERSONS IS LIABLE TO UPDATE OR MAINTAIN TOPICALITY OF THE INFORMATION CONTAINED HEREIN, AND THIS INFORMATION AND OPINIONS REFLECTED THEREIN COULD BE CHANGED WITHOUT ANY NOTIFICATION THEREABOUT.

•THIS PRESENTATION SHOULD REMAIN CONFIDENTIAL UNTIL THE REPORT IS PUBLISHED. SOME INFORMATION CONTAINED HEREIN IS STILL A DRAFT INFORMATION AND WAS NOT LEGALLY CONFIRMED AND WILL BE FINALY DETERMINED ONLY AT THE MOMENT OF FILING THE APPLICATION FOR FINAL ACCEPTANCE FOR TRADING AT THE STOCK EXCHANGE.

•THIS INFORMATION DOES NOT CONSTITUTE AN OFFER OF THE SECURITIES TO BE SOLD IN RUSSIA, THE UNITED STATES OR ANY OTHER JURISDICTION. THE SECURITIES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE US SECURITIES ACT OF 1933,AS AMENDED, AND MAY NOT BE OFFERED OR SOLD INTO THE UNITED STATES EXCEPT IN A TRANSACTION REGISTERED UNDER SUCH ACT, OR NOT REQUIRED TO BE REGISTERED THERE UNDER, OR PURSUANT TO AND EXEMPTION FROM REGISTRATION REQUIREMENTS THEREOF. NO OFFERING OF SECURITIES IS BEING MADE INTO THE UNITED STATES. NO SECURITIES WILL BE REGISTERED UNDER THE APPLICABLE SECURITIES ACT OF ANY STATE OR TERRITORIAL ENTITY OF CANADA AND JAPAN. THIS PRESENTATION IS NOT SUBJECT TO MAILING, TRANSFERRING OR OTHER TYPE OF DISTRIBUTION IN THE UNITED STATES OF AMERICA, CANADA, AUSTRALIA AND JAPAN, OR TO THE TERRITORY OR FROM THE TERRITORY OF THE SPECIFIED COUNTRIES TO THE NAME OF ANY ANALYST IN THE SPHERE OF SECURITIES OR OTHER PERSON IN ANY OF THE SPECIFIED JURISDICTIONS. YOU AGREE TO AVOID FROM DISTRIBUTION OF ANY REPORT RESULTING FROM THE SURVEY OR SIMILAR DOCUMENTS ON THE TERRITORY OF THE UNITED STATES OF AMERICA, CANADA, AUSTRALIA AND JAPAN, SAVE AS IN ACCORDANCE WITH THE FEDERAL LAWS OF THE UNITED STATES ON SECURITIES INCLUDING SECURITIES ACT, AS WELL AS THE APPLICABLE LAWS OF CANADA, AUSTRALIA AND JAPAN, ACCORDINGLY.

•THIS PRESENTATION INCLUDES THE STATEMENTS RELATED TO THE FUTURE, WHICH REPRODUCE THE INTENTIONS, OPINIONS AND CURRENT EXPECTATIONS OF THE COMPANY. THE STATEMENTS FOR THE FUTURE INCLUDE ANYTHING, WHICH IS NOT A FACT OCCURED. THE COMPANY TRIED TO HIGHLIGHT SUCH STATEMENTS RELATED TO THE FUTURE BY MEANS OF THE WORDS, SUCH AS “MAY”, “WILL”, “SHOULD”, “EXPECT”, “INTEND”, “EVALUATE”, “ASSUME”, “PLAN”, “TO HAVE AN OPINION”, “TRY”, “FORECAST”, “CONTINUE” AND SIMILAR WORDS OR THEIR NEGATIVE FORMS. SUCH STATEMENTS HAD BEEN DONE BASING ON THE ASSUMPTIONS AND ASSESSMENTS, WHICH MAY OCCUR FAULTY, THOUGH THE COMPANY CONSIDERS THEM REASONABLE AT THE CURRENT MOMENT.

•SUCH STATEMENTS RELATED TO THE FUTURE ARE LINKED TO THE RISKS, UNCERTAINTIES AND ASSUMPTIONS, AS WELL AS TO OTHER FACTORS, WHICH MAY LEAD TO THE EVENT THAT ACTUAL RESULTS OF THE COMPANY’S ACTIVITY AND ACTIVITY OF THE MARKETS, ON WHICH IT OPERATES OR INTENDS TO OPERATE IN, THEIR FINANCIAL STATUS, LIQUIDITY, CHARACTERISTICS, PROSPECTS AND ABILITIES COUILD MATERIALLY DIFFER FROM THOSE, WHICH ARE EXPRESSED WITH THE HELP OF SUCH STATEMENTS RELATED TO THE FUTURE. THE IMPORTANT FACTORS, WHICH MAY RESULT IN SUCH DIFFERENCES, INCLUDE, INTER ALIA, CHANGING BUSINESS CONDITIONS AND OTHER MARKET CONDITIONS, COMMON ECONOMIC CONDITIONS IN RUSSIA, EU COUNTRIES, THE UNITED STATES OF AMERICA OR ANYWHERE ELSE, AS WELL AS THE ABILITY OF THE COMPANY TO MEET THE TRENDS IN THE INDUSTRY. THE MATERIAL DIFFERENCE OF THE ACTUAL RESULTS, FEATURES AND ACHIEVEMENTS MAY BE THE RESULT OF ADDITIONAL FACTORS. THE COMPANY AND ALL ITS DIRECTORS, OFFICERS, EMPLOYEES AND ADVISORS HEREWITH STATE THAT THEY ARE NOT OBLIGED TO ISSUE ANY UPDATE OF OR REVISE ANY STATEMENTS RELATED TO THE FUTURE CONTAINED HEREIN, OR DISCLOSE ANY CHANGES IN THE FORECASTS OF THE COMPANY OR EVENTS, CONDITIONS AND CIRCUMSTANCES, WHICH SUCH STATEMENTS RELATED TO THE FUTURE ARE BASED ON, SAVE AS IN THE CASES PROVIDED FOR BY THE APPLICABLE LAWS.

•RECEIPT OF ANY COPY OF THIS INFORMATION TESTIFIES THE ACCEPTANCE OF THE ABOVE LIMITATIONS.

Disclaimer

GDR Depositary - BNY Mellon

Contact person at the depositary

Ludmila Leliavskaia Vice President

Tel +1.212.815.4493 [email protected]

MMK (Magnitogorsk Iron & Steel works)

Ordinary shares listed at MICEX and RTS in June 2006.

GDRs listed at LSE in April 2007

ISIN / СUSIP US5591892048/559189105

Andrey Serov Head of IR

Tel +7 (3519) 24 52 97 [email protected]

www.mmk.ru

Contacts at MMK

Tickers

MICEX, RTS: MAGN

LSE: MMK

Bloomberg: MMK:LI

27