Embed Size (px)

Citation preview

Edgewood Management LLC Gavin Durham

June 15, 2015 40.47

Mondelez International (MDLZ) Buy

Market Cap 65.83B FY2015 FCF 2,462mln

Hist. Rev. Growth Rate -1.5% Debt//EBITDA 3.16

EPS Growth Rate for ‘FY15

44% Dividend Yield 1.46%

LT Future EPS Growth 38% 2015 EPS $1.94

ROE 8.38% 2016 P/E 17x

Shares Outstanding 1.63B Avg. Daily Volume 9.8mln

Required Return Category

10.5% Sector Consumer Goods

Investment Thesis

• Mondelez has adopted an efficient Zero Based Budgeting (ZBB) strategy that will increase operating margins dramatically and provide infrastructure necessary for top line growth.

• Mondelez has upgraded key areas of management.

• Mondelez is extremely well positioned in a number emerging markets, especially Brazil.

• Share repurchases in 2015 and 2016 will increase value for shareholders.

Company Overview Mondelez International is one of the world’s largest snack companies, generating revenue of $34.2b in 2014. Mondelez produces a number of big name brands such as Oreo, Ritz, Milka, Cadbury, and Trident. These

ß 2

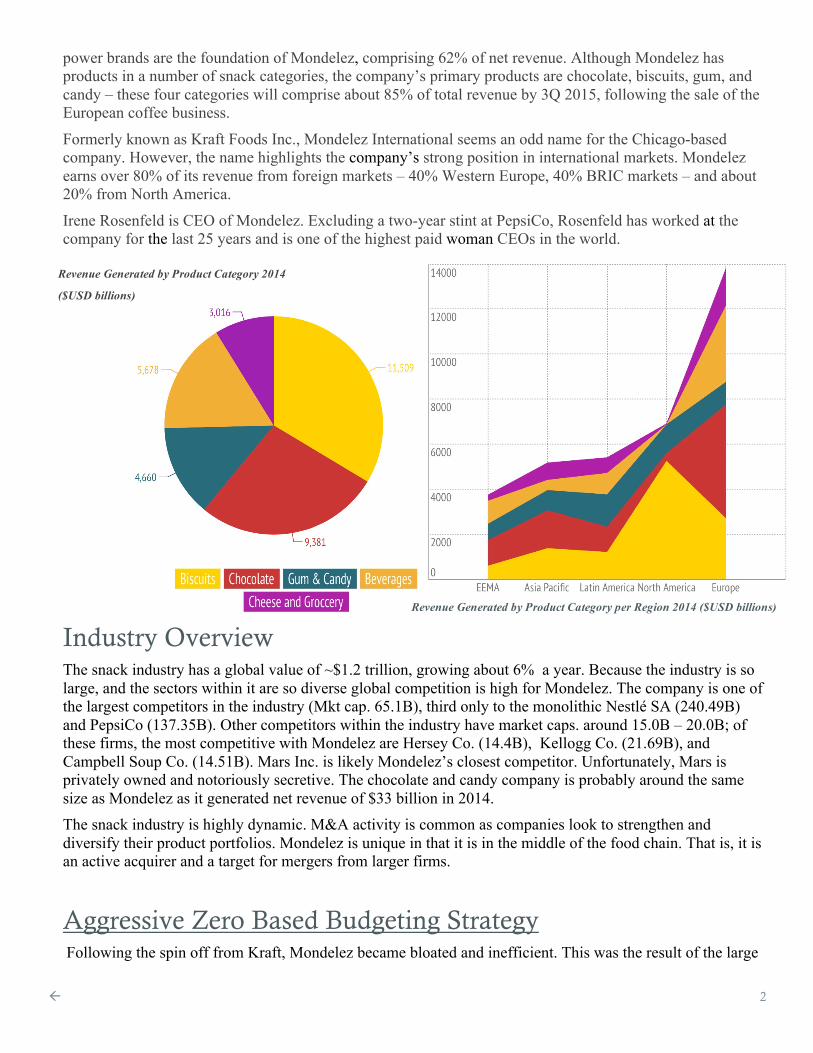

power brands are the foundation of Mondelez, comprising 62% of net revenue. Although Mondelez has products in a number of snack categories, the company’s primary products are chocolate, biscuits, gum, and candy – these four categories will comprise about 85% of total revenue by 3Q 2015, following the sale of the European coffee business.

Formerly known as Kraft Foods Inc., Mondelez International seems an odd name for the Chicago-based company. However, the name highlights the company’s strong position in international markets. Mondelez earns over 80% of its revenue from foreign markets – 40% Western Europe, 40% BRIC markets – and about 20% from North America.

Irene Rosenfeld is CEO of Mondelez. Excluding a two-year stint at PepsiCo, Rosenfeld has worked at the company for the last 25 years and is one of the highest paid woman CEOs in the world.

Industry Overview The snack industry has a global value of ~$1.2 trillion, growing about 6% a year. Because the industry is so large, and the sectors within it are so diverse global competition is high for Mondelez. The company is one of the largest competitors in the industry (Mkt cap. 65.1B), third only to the monolithic Nestlé SA (240.49B) and PepsiCo (137.35B). Other competitors within the industry have market caps. around 15.0B – 20.0B; of these firms, the most competitive with Mondelez are Hersey Co. (14.4B), Kellogg Co. (21.69B), and Campbell Soup Co. (14.51B). Mars Inc. is likely Mondelez’s closest competitor. Unfortunately, Mars is privately owned and notoriously secretive. The chocolate and candy company is probably around the same size as Mondelez as it generated net revenue of $33 billion in 2014. The snack industry is highly dynamic. M&A activity is common as companies look to strengthen and diversify their product portfolios. Mondelez is unique in that it is in the middle of the food chain. That is, it is an active acquirer and a target for mergers from larger firms.

Aggressive Zero Based Budgeting Strategy Following the spin off from Kraft, Mondelez became bloated and inefficient. This was the result of the large

Revenue Generated by Product Category 2014

($USD billions)

Revenue Generated by Product Category per Region 2014 ($USD billions)

ß 3

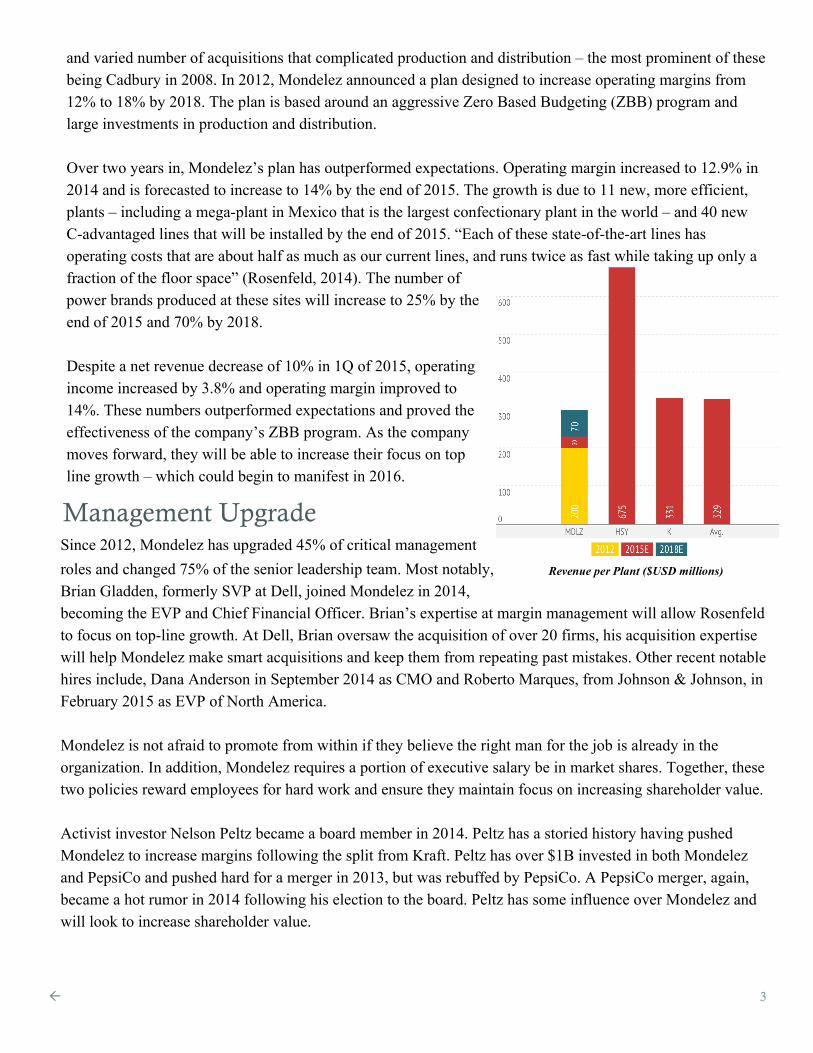

and varied number of acquisitions that complicated production and distribution – the most prominent of these being Cadbury in 2008. In 2012, Mondelez announced a plan designed to increase operating margins from 12% to 18% by 2018. The plan is based around an aggressive Zero Based Budgeting (ZBB) program and large investments in production and distribution.

Over two years in, Mondelez’s plan has outperformed expectations. Operating margin increased to 12.9% in

2014 and is forecasted to increase to 14% by the end of 2015. The growth is due to 11 new, more efficient, plants – including a mega-plant in Mexico that is the largest confectionary plant in the world – and 40 new C-advantaged lines that will be installed by the end of 2015. “Each of these state-of-the-art lines has operating costs that are about half as much as our current lines, and runs twice as fast while taking up only a fraction of the floor space” (Rosenfeld, 2014). The number of power brands produced at these sites will increase to 25% by the end of 2015 and 70% by 2018.

Despite a net revenue decrease of 10% in 1Q of 2015, operating

income increased by 3.8% and operating margin improved to 14%. These numbers outperformed expectations and proved the effectiveness of the company’s ZBB program. As the company moves forward, they will be able to increase their focus on top line growth – which could begin to manifest in 2016.

Management Upgrade Since 2012, Mondelez has upgraded 45% of critical management roles and changed 75% of the senior leadership team. Most notably, Brian Gladden, formerly SVP at Dell, joined Mondelez in 2014, becoming the EVP and Chief Financial Officer. Brian’s expertise at margin management will allow Rosenfeld to focus on top-line growth. At Dell, Brian oversaw the acquisition of over 20 firms, his acquisition expertise will help Mondelez make smart acquisitions and keep them from repeating past mistakes. Other recent notable hires include, Dana Anderson in September 2014 as CMO and Roberto Marques, from Johnson & Johnson, in February 2015 as EVP of North America. Mondelez is not afraid to promote from within if they believe the right man for the job is already in the organization. In addition, Mondelez requires a portion of executive salary be in market shares. Together, these two policies reward employees for hard work and ensure they maintain focus on increasing shareholder value. Activist investor Nelson Peltz became a board member in 2014. Peltz has a storied history having pushed Mondelez to increase margins following the split from Kraft. Peltz has over $1B invested in both Mondelez and PepsiCo and pushed hard for a merger in 2013, but was rebuffed by PepsiCo. A PepsiCo merger, again, became a hot rumor in 2014 following his election to the board. Peltz has some influence over Mondelez and will look to increase shareholder value.

Revenue per Plant ($USD millions)

ß 4

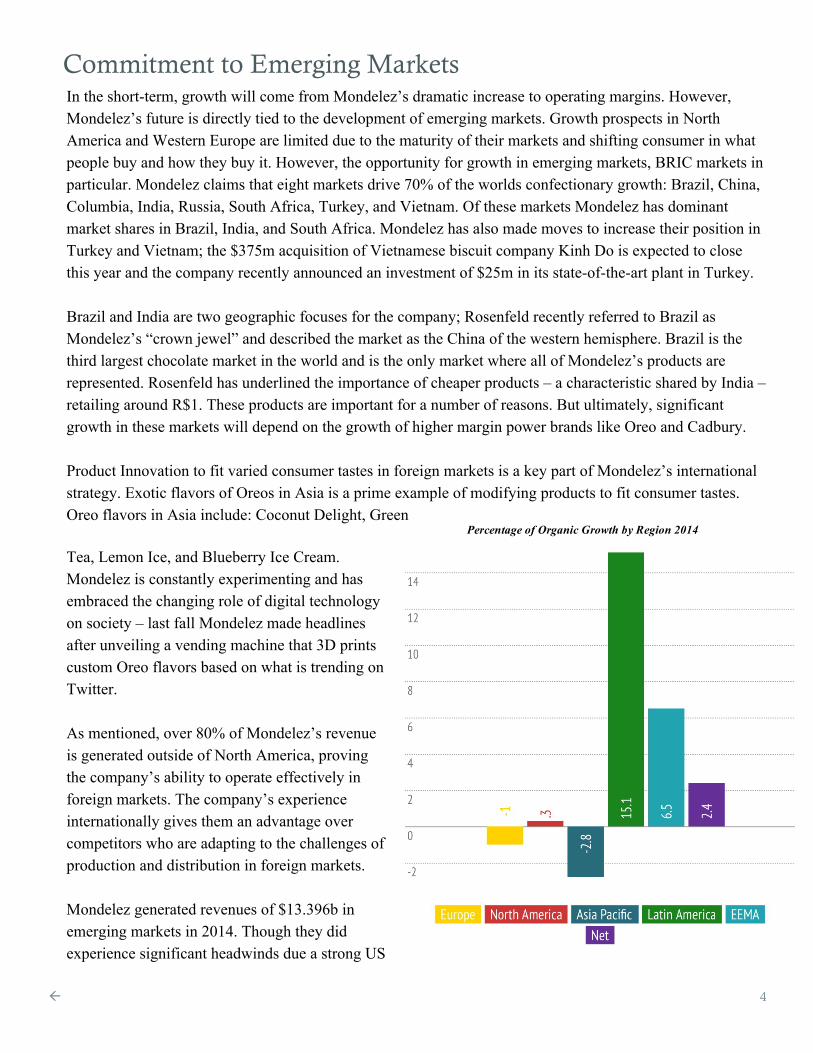

Commitment to Emerging Markets In the short-term, growth will come from Mondelez’s dramatic increase to operating margins. However, Mondelez’s future is directly tied to the development of emerging markets. Growth prospects in North America and Western Europe are limited due to the maturity of their markets and shifting consumer in what people buy and how they buy it. However, the opportunity for growth in emerging markets, BRIC markets in particular. Mondelez claims that eight markets drive 70% of the worlds confectionary growth: Brazil, China, Columbia, India, Russia, South Africa, Turkey, and Vietnam. Of these markets Mondelez has dominant market shares in Brazil, India, and South Africa. Mondelez has also made moves to increase their position in Turkey and Vietnam; the $375m acquisition of Vietnamese biscuit company Kinh Do is expected to close this year and the company recently announced an investment of $25m in its state-of-the-art plant in Turkey. Brazil and India are two geographic focuses for the company; Rosenfeld recently referred to Brazil as Mondelez’s “crown jewel” and described the market as the China of the western hemisphere. Brazil is the third largest chocolate market in the world and is the only market where all of Mondelez’s products are represented. Rosenfeld has underlined the importance of cheaper products – a characteristic shared by India – retailing around R$1. These products are important for a number of reasons. But ultimately, significant growth in these markets will depend on the growth of higher margin power brands like Oreo and Cadbury. Product Innovation to fit varied consumer tastes in foreign markets is a key part of Mondelez’s international strategy. Exotic flavors of Oreos in Asia is a prime example of modifying products to fit consumer tastes. Oreo flavors in Asia include: Coconut Delight, Green

Tea, Lemon Ice, and Blueberry Ice Cream. Mondelez is constantly experimenting and has embraced the changing role of digital technology on society – last fall Mondelez made headlines after unveiling a vending machine that 3D prints custom Oreo flavors based on what is trending on Twitter. As mentioned, over 80% of Mondelez’s revenue is generated outside of North America, proving the company’s ability to operate effectively in foreign markets. The company’s experience internationally gives them an advantage over competitors who are adapting to the challenges of production and distribution in foreign markets.

Mondelez generated revenues of $13.396b in emerging markets in 2014. Though they did experience significant headwinds due a strong US

Percentage of Organic Growth by Region 2014

ß 5

dollar and weak foreign currencies, emerging markets have a sizable strength in that they all have a tax rate below 7%.

Share Repurchases In 2014, Mondelez committed to a plan to repurchase $7.7 billion of market shares through 2016. Mondelez repurchased ~$1.5b of shares in the 1Q of 2015, and will buyback at least 500m through 2015. However, the company acknowledge the likelihood of further buybacks due to the $5b in cash the company will receive following the closure of their Jacobs Douwe Egberts coffee joint venture in the 3Q of 2015. It is likely Mondelez will buyback at least $2.5b of shares in 2015 and could potentially repurchase as much as ~$3b by the end of the year. Depending on the company’s activity in 2015, share repurchases in 2016 can be forecasted between $2.7b - $3.2b.

RISKS Government Regulations: Government regulations restricting ingredients used in products and increasing information disclosed on packaging would likely have a negative impact for Mondelez. In the United States, proposed regulations that require detailed information on packages and an increased tax on sugar would drive sales down and cost of goods up.

Volatile Emerging Markets: Mondelez’s strong position internationally exposes them to the volatile nature of developing markets. For example, Mondelez a $287m loss in operating income was realized in 2014 due to weak currencies in Latin America and a strong US dollar. Shifting consumer tastes: Consumer tastes has a strong impact on Mondelez. In North America, consumer tastes have trended away from snack food, favoring healthier products. Online Grocery shopping: The online Grocery industry has grown rapidly in developed markets – Amazon Fresh is growing in popularity and Walmart is expected to increase its online grocery business. Many of Mondelez’s products are reliant on “impulse decisions,” as cookies and gum products are rarely the purpose for grocery shopping. “Hot spots,” such as on the end of aisles and at the cash register, are the primary locations for impulse buys. Hot spots in online shopping are virtually nonexistent and thus limit the number of impulse buys.

Conclusion

The business model run under Kraft Food Inc. was inefficient and a poor long-term growth strategy. These problems were likely a core reason for the split from the North American grocery business and became exaggerated during the first few years of Mondelez International. Though Mondelez’s plan to increase operating margin was enacted in 2013, the company was burdened by outstanding debt from Kraft and $925m in restructuring costs to complete the split. 2014 represented the first year Mondelez was able to commit to its ZBB program. The program has proven its effectiveness as Mondelez continues to surpass their own goals and the markets expectation. This is reassuring for a program that Brian Gladden describes as “still in the early days.”

ß 6

Increasing operating margins through an aggressive ZBB program is the company’s plan to increase growth

in the short-term, but their long-plan plan for growth is clearly tied to the development of emerging markets. The infrastructure and brand Mondelez has established is essential for developing markets with an incipient middle class and and blossoming GDP per capita. That Mondelez’s ZBB program has shown to be effective is essential as many developing countries, such as Brazil, are experiencing growing pains.

Mondelez has a number of problems and their production and distribution remains inefficient. However,

management appears to have a clear understanding of what the problems are and how to fix them. It is encouraging to hear executives speak openly about the company’s struggles and Mondelez’s ability to draw talented professionals is impressive.

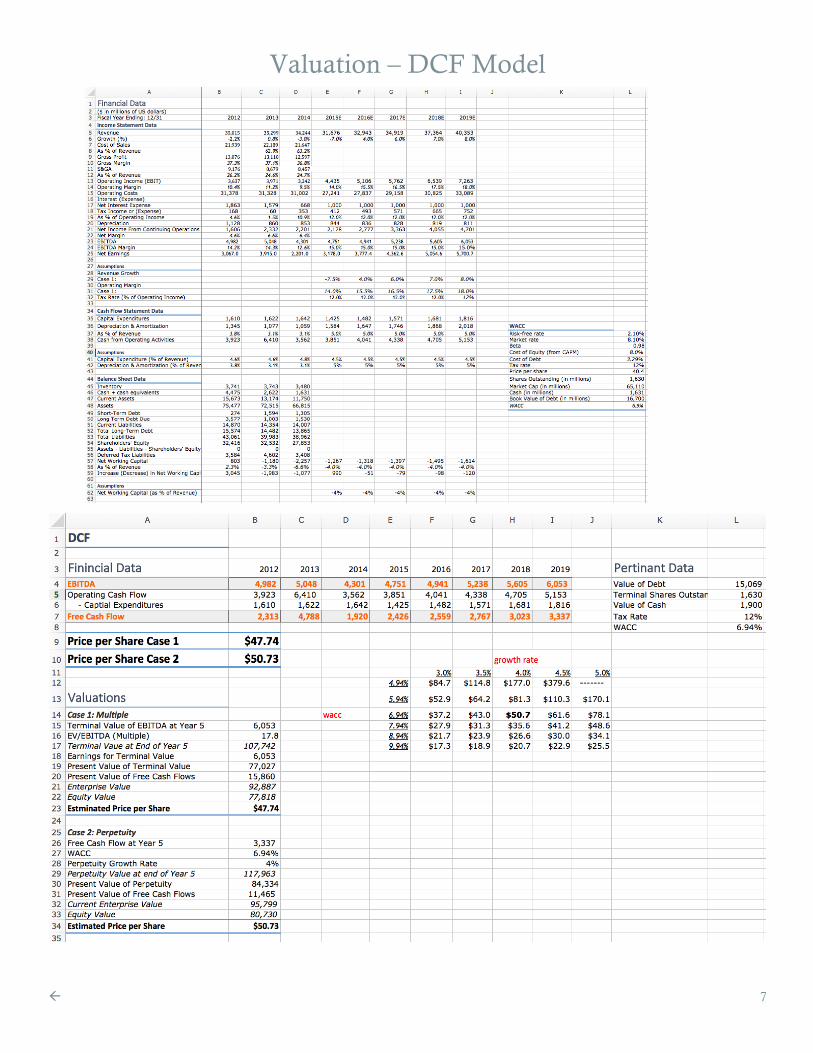

I rate Mondelez as a buy, valuing the company at $50.73 a share.

ß 7

Valuation – DCF Model