Embed Size (px)

Citation preview

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 1/120

media fact bookROMANIA

2008

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 2/120

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 3/120

media fact bookROMANIA 2008

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 4/120

This book is a product of Initiative Romania.

In putting together the Media Fact Book we haveused audience data and information supplied byThe Romanian Association for Audience Measurement (ARMA),The Romanian Bureau of Circulation Audit (BRAT),The Romanian Association for Radio Audience Measurement(ARA), TNS-AGB INTERNATIONAL, Alfacont, GfK Romania,Mercury Research, IMAS, Initiative Moldova (Evghenii Crecesco) ARBOmedia, netBridge, CableDirect,

Hollywood Multiplex, International Advertising Association (IAA), The National Audio-Visio Council (CNA),The National Institute of Statistics (INS) andThe National Bank of Romania (BNR).

Acknowledgements to the following members of the teamwho significantly contributed to this book:

Octavian Popescu, Alexandra Olteanu, Nicoleta Florescu,Maruan Trascu, Cristina Chinde, Laurentiu Pop,Rodica Caraghina, Marcela Tuila.

INITIATIVE MEDIA S.A, Bucharest, 2008 All rights reserved

This publication is protected by copyright.No parts of this book may be reproduced without the prior writtenconsent of the copyright owner.

Readers should understand that the data containedin the Media Fact Book is as actual and accurate asthe sources could provide it.

Your comments and suggestions are welcomed asa valuable input for the future issues of this book.

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 5/120

www.initiative.com table of contents 1

editor’s foreword 3

about initiative 5

media market 6

media research 10

television 16

radio 22

press 30

outdoor & indoor 61

cinema 65

internet 68

new media 73

romania - economiclandscape 76

professionalassociations 81

legislationsand taxes 87

the nationalaudio-visual council 99

moldavianmedia market 100

media dictionary 108

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 6/120

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 7/120

It seems 2007 has brought a new media jargon in our business vocabulary where Television is regarded.It’s the “program break” and occurs whenever a trailer of advertising is paused by a program window.We’ve gotten this far in 2007.Television seems to have abandoned its original aim to provide news, entertainment and education for

the mass audience in order to become a 24/7 advertising broadcasting service.In 2007, except for Jan, Feb, Jul, and Aug, the ad loading at the top five commercial channels, in Prime

Time, reached nearly 14 minutes per hour of program in Prime Time.

The legal limitation for broadcasting advertising had been exceeded at times by as much as 148%,translating into a 31 minute ad break.

Is it then a wonder that people don’t watch TV as much as they used to? The most sought-after agesegment for advertisers 18-49 has spent ca. 9% less time watching TV than they did a year ago.

Can broadcasters afford to further alienate this ‘goldmine’?One way to turn the trend around is to invest if the single, most popular sport amongst Romanian public:

football. It’s been an amazing battle over the rights to broadcast various football competitions. Only few of many in need to make football the driving force behind their trailing audiences succeeded to secure thoserights.

Less audience means less GRPs to sell, which in turn means more spots, for each advertiser has toreach its objectives.

Price is just one lever in regulating these anomalies.Did you notice that more audience migrates from the major, generalist channels towards the specialty

ones?They seem to be able to respond to public’s need to watch programs they prefer, which are paused by

advertising instead of the other way around.

Programming should be the other lever in keeping the audience tuned in and generalist channels shouldfind a way to achieve that.

It is no easy job as at end of 2007 some 38 channels were selling advertising. In the beginning of 2008this number already jumped up to 42.

2007 started on a very optimist note when assessing the budgets in the market, despite the high inflation

and the reduced inventory from the major TV groups. It turned out the market could no longer sustain anestimated 40% growth and so in the end the TV market grew by 35%. For 2008 we estimate a growth of ca. 25% of the TV market.

The market growth will relent further in 2008 along with the increasing audience fragmentation andclutter.

In contrast with the calming growth of traditional media, online keeps thrusting ahead as the inventoryis increasing in both quantity and diversity and the Internet penetration is rapidly expanding within 18-49age groups.

In 2007 the most active spending category in online was Banking/Finance.In 2008 we expect online to maintain a 50% growth rate as well as into the following 3 to 5 years.The e-revolution is not here yet, but it’s not too far away either.

All in all, after a 32% growth in 2007, a media market growth of nearly 22% of is expected in 2008 to atotal of ca. 590 Mio €, of which TV will take some 385 Mio €, Print 90 Mio €, Outdoor 70 Mio € (includingDigital Outdoor and Indoor), Radio 38 Mio € and Online ca. 15 Mio €.

Obviously, the media market has passed the maximum growth moment and is slowly maturing, priceinflation is cooling down, ownership consolidation is occurring in almost every market segment, be it TV,Outdoor, Print, Radio or Online, media audit companies are increasingly involved in the business,competition for content is more acute than ever while margins are shrinking.

Efficiency, accountability, innovation, team stability and responsible service delivery will make thedifference in the market place.

Initiative is here doing just that.

Enjoy this edition and let us know what you think.

Initiative Team

3www.initiative.com editor’s foreword

Dear reader,

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 8/120

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 9/120

Initiative Romania is affiliated to Initiative Worldwide, part of Interpublic Group of Co’s (IPG). Along with

other reputed agency networks such as Lowe & Partners Worldwide, Lowe PR and Brand Connection, all

part of IPG, Initiative Worldwide is a truly global network, offering capitalised brain synergy, innovative and

effective consumer approach in more than 51 countries on 5 continents.

Initiative Romania started operations 14 years ago as the first true media management specialist

company in the market. Currently the 3rd largest media agency in Romania, Initiative focuses on offering

its clients thorough brand and marketing thinking, innovation through deep understanding of the modern

consumer touch-points, negotiation power, commitment on delivery and measurable performance.

The client portfolio of Initiative Romania includes strong brands and successful companies: Orange,

Johnson&Johnson, BMW, Millennium Bank, GlaxoSmithKline, Pernod Ricard, MOL Romania, Sarantis,

Georgia Pacific, Carrefour (commercial galleries), Provident Financial, Power Horse, Kika, Reinert etc.

Initiative Romania provides the whole range of media services: quantitative research, media strategy,

conceptual planning, implementation planning, buying, special media projects (event and mediasponsorship, product integration, etc).

Initiative Romania offers enhanced quality standards through usage of top-of-the-range proprietary tools

aimed to better determine the optimum investment required to achieve the communication objective.

Initiative Romania offers added value:

• Media Landscape – quarterly analysis of the media market;

• Media Fact Book – starting 1997, Initiative Romania is the exclusive publisher of this media annual

guide, unique on the Romanian market. In 2007 Initiative, celebrated the 10th annual edition of the

Media Fact Book.• Wireless communication portal aimed to improve the ef ficiency and smoothness of information

management and client communication.

• Media training – Presentation of media basics (terminology, methods) and on-the-job training in

Initiative’s office.

• Media PR – Initiative provides media coverage to PR events organised by clients, upon request and

project specifics.

• Outdoor Mapping – providing clients a better campaign management

• Digital concept & design management – offering clients integrated digital solutions by managing the

entire process from ideation, concept and design to media buying, planning and implementation of

digital campaigns..

2007 was a dynamic year of growth for Initiative, the business increasing by 36% over 2006.

We put forward to our clients a solid team of experienced media professionals with a deep understanding

of client’s marketing communication needs and advanced knowledge of efficient and creative planning

and buying.

We are committed to create value for brands by engaging consumers at best prices.

Find out more about Initiative Romania at www.initiative.com, call at +4021 301 01 00 or write to us [email protected].

5www.initiative.com about initiative

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 10/120

Overview

The Romanian media market has grown in size and diversity in recent years. Despite that the largest budgets

were allocated primarily to television, all other media such as outdoor, internet, radio and press kept growing

and diversifying in keeping with the general development of the market over the past few years.

The media landscape is characterized by:

• Media pricing inflation

• Rapidly increasing advertisers base and the subsequent demand for inventory

• Media fragmentation

• Decreasing inventory on main TV channels

• Lack of quality inventory in on-line, radio, OOH

• Sold out during Q2 and Q4

In 2007, the Romanian media market grew in net value by 32%.

The fastest growth belongs to the Internet. Initiative estimates a 50-60% increase of the on-line spend

compared to 2006. According to the World Association of Newspapers (WAN), the on-line advertising revenues

increased by 32% in 2007 and by more than 200% in the 4 years period 2003-2007.

Ad-spend has increased also in the Print market; in 2007 we estimate 11% increase of the net ad spend,

compared to last year.

For the International market a similar increase of the ad spends is recorded, especially for free sheets and

on-line journals. WAN estimates that the worldwide revenue from on-line newspaper advertising will doubleover the next five years to reach 12% of newspapers total revenue.

Graph 1: Total net Ad-spend by medium (Mil €) 2003-2008 - Initiative Estimation

www.initiative.commedia market

“Advertising is the art of arresting the human intelligence just long enough to get money from it.”

Chuck Blore, a partner in the advertising firm Chuck Blore & Don Ruchman, Inc.,quoted by Ben H. Bagdikian, “The Media Monopoly, Sixth Edition”, (Beacon Press, 2000)

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 11/120

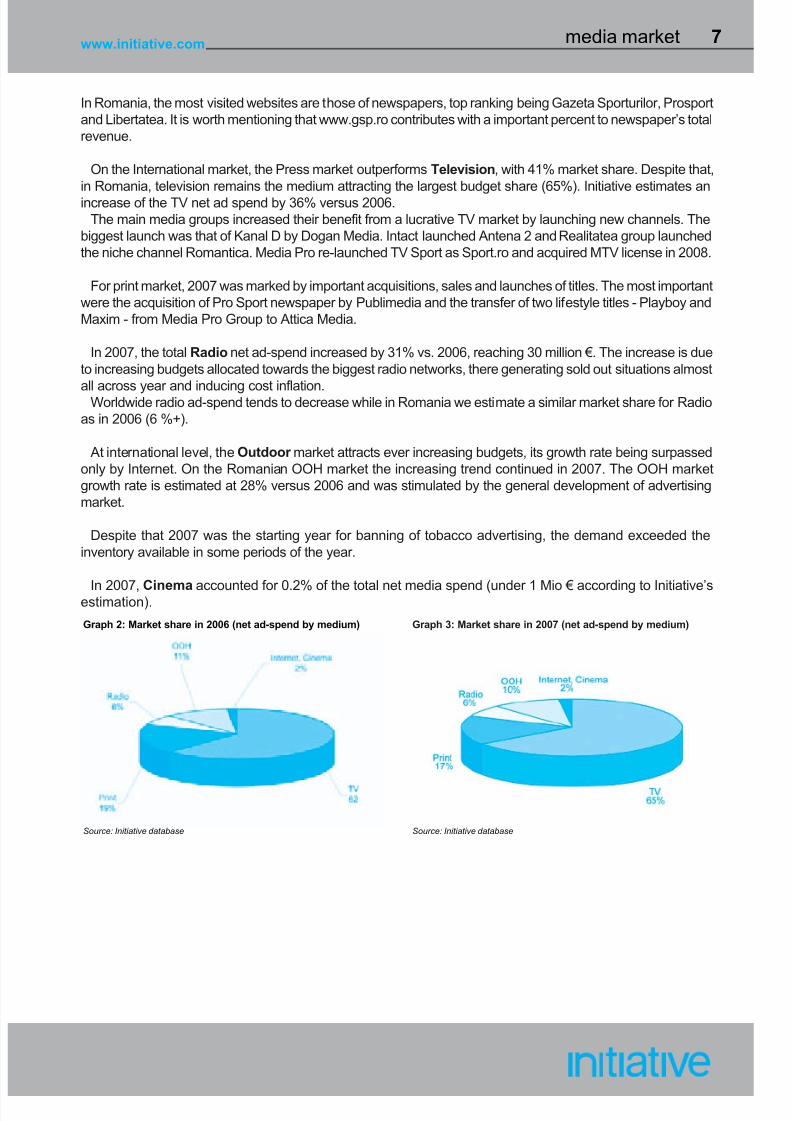

In Romania, the most visited websites are those of newspapers, top ranking being Gazeta Sporturilor, Prosportand Libertatea. It is worth mentioning that www.gsp.ro contributes with a important percent to newspaper’s totalrevenue.

On the International market, the Press market outperforms Television, with 41% market share. Despite that,in Romania, television remains the medium attracting the largest budget share (65%). Initiative estimates anincrease of the TV net ad spend by 36% versus 2006.

The main media groups increased their benefit from a lucrative TV market by launching new channels. Thebiggest launch was that of Kanal D by Dogan Media. Intact launched Antena 2 and Realitatea group launchedthe niche channel Romantica. Media Pro re-launched TV Sport as Sport.ro and acquired MTV license in 2008.

For print market, 2007 was marked by important acquisitions, sales and launches of titles. The most importantwere the acquisition of Pro Sport newspaper by Publimedia and the transfer of two lifestyle titles - Playboy andMaxim - from Media Pro Group to Attica Media.

In 2007, the total Radio net ad-spend increased by 31% vs. 2006, reaching 30 million €. The increase is dueto increasing budgets allocated towards the biggest radio networks, there generating sold out situations almost

all across year and inducing cost inflation.Worldwide radio ad-spend tends to decrease while in Romania we estimate a similar market share for Radioas in 2006 (6 %+).

At international level, the Outdoor market attracts ever increasing budgets, its growth rate being surpassedonly by Internet. On the Romanian OOH market the increasing trend continued in 2007. The OOH marketgrowth rate is estimated at 28% versus 2006 and was stimulated by the general development of advertisingmarket.

Despite that 2007 was the starting year for banning of tobacco advertising, the demand exceeded theinventory available in some periods of the year.

In 2007, Cinema accounted for 0.2% of the total net media spend (under 1 Mio € according to Initiative’sestimation).

7www.initiative.com media market

Graph 3: Market share in 2007 (net ad-spend by medium)

Source: Initiative database

Graph 2: Market share in 2006 (net ad-spend by medium)

Source: Initiative database

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 12/120

www.initiative.commedia market

Top 10 Categories in 2007 vs. 2006 - all media (TV, Press, Radio) - Rate Card Budget

2006 2007Category Exp. (000’€) Category Exp. (000’€)

Mobile Telecomunication Services 233,465 Cosmetics 480,161

Beer 229,126 Hair Care 434,801

Cosmetics 216,487 Banking & Insurance Services 423,019

Hair Care 206,192 Mobile Telecomunication Services 349,907

Cars & 4x4 Vehicles 173,651 Beer 297,126Milk Products 172,267 Laundry Products 290,433

Medical & Optical Products & Services 163,145 Hygienics 286,450

Hygienics 159,166 Household Cleaners 275,810

Laundry Products 150,956 Medical & Optical Products & Services 268,671

Carbonate Soft Drinks 149,339 Milk Products 252,564

Source: TV – TNS AGB INTERNATIONAL, Press and radio: AlfaCont

Top 10 Advertisers in 2007 vs. 2006 - all media (TV, Press, Radio) - Rate Card Budget

2006 2007Advertisers Exp. (000’€) Advertisers Exp. (000’€)

Procter & Gamble 260,380 Procter & Gamble 526,909

European Drinks & Foods 194,977 L’Oreal 345,859

Unilever 146,353 Unilever 315,663

L’Oreal 138,409 European Drinks & Foods 188,160

Danone 124,600 Danone 177,601

Kraft Foods Romania 114,570 Coca-Cola Co. 163,681

Coca-Cola Co. 92,963 Colgate Palmolive 143,341

Quadrant Amroq Beverages 88,433 Kraft Foods Romania 134,301

Henkel 81,762 Henkel 128,939

Nestle Romania 79,558 Nestle Romania 120,204

Source: TV – TNS AGB INTERNATIONAL, Press and radio: AlfaCont

Top 10 Brands in 2007 vs. 2006 - all media (TV, Press, Radio) - Rate Card Budget

2006 2007Brands Exp. (000’€) Brands Exp. (000’€)

Danone 115,539 Danone 189,594

Orange 71,165 L’Oreal 180,115

Garnier 62,044 Garnier 162,421

Connex/Vodafone 60,330 Nivea 120,498

L’Oreal 56,561 Vodafone 102,784

Pepsi 53,112 Orange 92,124

Jacobs 51,405 BCR Erste 78,751

Cosmote 51,176 Jacobs 76,521

Nivea 40,599 Cosmote 68,392

Germanos 38,769 Colgate 64,793

Source: TV – TNS AGB INTERNATIONAL, Press and radio: AlfaCont

Top Investors 2007 vs. 2006

In last two years the biggest categories wereprimarily belonging to the FMCG sector; however,some top-spending categories switched emergedin 2007. Thus, Cosmetics category climbs two

places and leads the 2007 ranking. It is followed byHair Care and the Banking & Insurance Services. Actually, 2007 was the year with importantinvestments in Insurance category.

Beer category went down to 5th position in top.Carbonated Soft Drinks and Cars/4x4 vehiclecategories went out of the Top 10.

2007 was a good year for Laundry products andHousehold Cleaning categories. Mobile tele-

communication services keep a similar marketshare, around 5.6%, but falls on to 4th place.

Top 10 categories cumulate 54% of totalad-spending.

As for advertisers, P&G maintains the leading position from 1999 through to 2007, with the biggest TVbudget. L’Oreal climbs on second place and Unilever maintains its 3 rd position in top. Quadrant AmroqBeverages goes out of top and Colgate Palmolive is a new entry, going directly to the 7 th place.

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 13/120

9www.initiative.com media market

Perspectives 2008

• According to Initiative’s estimation, the total net ad spend will increase by 23-24%. The growth rate willslow down in the forthcoming years, until Romanian media market will reach a growth rate of 5-8%, in linewith the developed markets of Western Europe (5-7 years).

• TV remains the strongest media channel. In 2008, we estimate TV will attract 66% of all advertisingrevenues, roughly 383-385 million € net.

• The press spend will maintain an ascending trend in 2008 mostly due to election campaigns (+10% net)

• Despite the descending trend of its audience, radio ad spend is expected to grow in 2008by ca. 26%.

• In 2008, the increase rate of the net OOH ad revenues is estimated at 18%.

• The Indoor market will continue its development at a higher rate than other media. We estimate a 40%growth for this media by end of 2008, due to diversification and emergence of new locations inside mallsand hypermarkets.

• The Online advertising continues to grow by 50-60% annually. The main investing categories will be:Banking/Finance (the Financial services category became leader in 2007, surpassing Telecom),Telecommunications, Automotive, IT&C; a significant budget growth will involve the FMCG category(personal care, food and drink) followed by Online Retail, Tourism.

• For 2008 we estimate the Cinema advertising revenue will remain constant. The main obstaclesresponsible for slow development of cinema advertisement are:

• Low number of cinema halls• Inconsistent development of cinema network – 7 counties were cinema halls do not exist while most

are concentrated in Bucharest• Escalating price of cinema admission• High rate of piracy for new released movies• Competition of home-cinema viewing.

Even if currently the Romanian media market is geared towards traditional media we can notice a fastgrowth of new media. The development of mobile advertising is hindered by the lack of technical

capabilities. We expect the two important GSM operators in Romania, Orange and Vodafone, to cater tothis market by implementing specialized mobile platforms.

Top 10 Brands in 2007, by medium - Rate Card Budget

Television Exp. (000’€) Press Exp. (000’€) Radio Exp. (000’€)

Procter & Gamble 529,508 Orange 8,983 Orange 4,173L’Oreal 347,808 Vodafone 7,565 Group Renault 3,807

Unilever 317,547 L’Oreal 5,774 Vodafone 3,764

European Drink & Foods 191,876 BCR Erste 5,055 Romtelecom 2,585

Danone 171,070 Romtelecom 4,348 Tiriac Group Auto 2,554

Coca-Cola Company 164,122 Unilever 3,540 Romaqua Group Borsec 2,372

Colgate Palmolive 144,269 Procter & Gamble 3,145 Carrefour 2,192

Kraft Foods Romania 134,494 Beiersdorf Romania 2,897 Eurial Invest/Trust Motors 1,592

Henkel 129,651 Petrom 2,673 BCR Erste 1,501

Nestle Romania 121,125 Porsche Romania 2,656 Coca Cola Company 1,495

Source: TV – TNS AGB INTERNATIONAL, Press and radio: AlfaCont (media barters were excluded)

Press continues to be dominated by the Mobile telecommunication category. Banking servicesconsiderably increased their total spend. Banca Comerciala Romana was the most important advertiser in its category due to the re-branding process under Erste Bank management.

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 14/120

Research is increasingly developing reflecting the

sophistication of the advertising and media toolsand processes. Started just a few years back, localresearch tends to get aligned to Europeanstandards. Reliable and complex audiencemeasurement, industry-standard studies have beenalready established for television, press and radio.

• October 2001: the launch of the national TVpeople meter system.

• October 2002: the launch of the NationalReadership Survey (SNA) for press.

• 2003: IMAS and Mercury Research wereappointed to deliver radio audience data.

• January 2004: the establishment of the new TVpanel based on 1,150 HH’s (vs. 750 initially).

• June 2004: the launch of the first wave of radioaudience data.

• October 2005: the launch of the first wave of SNA FOCUS (audience and consumption data).

• October 2006: the deliver of the first results of SNA FOCUS

• November 2006: BRAT organized the first tender for the technical solution of the future IAM.

• September 2006 - January 2007, ARMAorganized the tender for the company which shallprovide SNMATV for ARMA members starting withJanuary 2008.

• January 2007 - GFK was appointed as the officialsupplier of TV audience data for period 2008-2011.Other participants to the tender wereMediaResearch Czech Republic and TNS AGBInternational.

• September 2007 - IMAS and Mercury Researchwere announced as the of ficial suppliers for radioaudience data for period 2008-2011.

• October 2007 - BRAT deliver for the first time the

results for the traffic measurement according to theSATI system. BRAT provided to the members anapplication, available online, for the usage of thesedata.

• November 2007 – first event dedicated to Indoor Romanian market – Indoor 2007

Acknowledging the importance of media researchin building a competitive and professionaladvertising market, Initiative is an active member of all relevant associations supporting theimplementation of audience research tools.

Accordingly, Initiative uses all media research toolsavailable as industry standard.

Audience measurement

1. TV

1.1. TNS AGB International - National TV

Audience Measurement Service (SNMATV)

In 2003, TNS and AGB Group, two of the largestTAM operators in the world created a joint venture.TNS AGB Int’l is the exclusive provider of TVaudience data on the Romanian market.

The data supplied by TNS AGB Internationalbecame the unique ‘currency’ used by televisionstations, media agencies and advertisers in their

media transactions, given the reliability,independence and transparency of themeasurement system.

The universe is all individuals aged 4 and over,living in private households having at least one TVset, without distinction based on race, language,nationality or socio-economic status.

The national panel includes 1,150 households(around. 3,000 individuals) and representative assuch for the total population of 21.6 million.

The size and the composition of the universe areannually established through EstablishmentSurveys.

There are control procedures aimed to ensure thepanel is according to standards:

• The panel activity has been developed withthe supervision of the Members’ TechnicalCommittee (representatives of agencies, TVstations and advertisers).

• Members are informed about the technicalparameters of the service (Panel ManagementReport, Quality Report, Work Order etc.) on amonthly basis.

Features of the service:

The households in the panel are equipped with aTARIS 4900 or TVM2 people meter device. Wherea telephone landline is not available, the pollingoperation is performed through GSM modems. InSeptember 2007, TNS AGB INTERNATIONALstarted to monitor digital TV and used latest type of people meters, TVM5. Thus, the panel included 70households with digital reception.

Minute by minute viewing data is delivered thefollowing day (by noon on workdays). The data for

weekend is delivered on Monday and the data for public holidays is delivered the next workday.

www.initiative.commedia research

“Research is to see what everybody else has seen and to think what nobody else has thought”

Albert Fzent-Gyorgyi (Hungarian Biochemist, 1937 Nobel Prize for Medicine, 1893-1986)

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 15/120

Pollux is the systems employed for themanagement of the TV panel. The system includesthe following modules:

• Panel management• Data validation• Weighting• Quality report

Software:

InfoSys TV is an integrated analysis system:• Day part Analysis• Program Analysis• Commercial Monitoring• Audience Profiles• Graphical Reporting• Planning & Optimization

TV Monitoring Service records and publishesdetailed information on TV programs andcommercials aired.

At the end of 2007 Audience and Monitoring dataare available for 38 TV stations: TVR 1, TVR 2, ProTV, Antena 1, Antena 3, Euforia, Acasa TV, PrimaTV, Kiss TV , UTV, Jetix, Discovery, MTV Romania,B1TV, Realitatea TV, Minimax, NationalGeographic, TVR Cultural, Sport.ro, Telesport,National TV, Pro Cinema, AXN, OTV, N24, Senso,Favorit TV, Hallmark, Sport Klub, Romantica,

Eurosport (from 1st

February), MGM (from5th September), Kanal D (from 18th February), Antena 2 (from 9th April), Etno TV (from15th January), Taraf (from 15th October), Sport One(from 1st June) and Cartoon Network (from1st November).

The Monitoring System is designed to record,store and digitally processes the transmissions of all TV stations. An archive of commercials isavailable at http://www.tns-agb.ro, where clientscan view all the TV commercials monitored since

1999.

2. PRESS

2.1. BRAT (Romanian Audit Bureau of

Circulation) - National Readership Survey

Romania (SNA FOCUS)

In 2005, BRAT organized a new tender for thepress audience measurement. In May 2005 BRATannounced the research companies appointed tocontinue the work for SNA for the next two years.The survey covers 227 titles (82 monthlies,

19 bimonthlies, 48 weeklies, 69 dailies and11 supplements).

The SNA universe is based on a 27,500 sample,14-64 y.o., urban areas inhabitants, living in privatehouseholds and being able to understand andspeak Romanian well (includes the Hungarianminority). Only one eligible respondent per HH is

considered. The sample is wide enough to makedata valid at local level, as well. The data isgathered by face-to-face interviews. The fieldworkis carried on throughout the year and the number of interviews is balanced by the day of the week.

The questionnaire covers the followingcategories:

• Primary media (local, regional and nationalnewspapers, supplements, magazines - 227titles)

• Secondary media (TV stations, radio stations,cinema, internet, outdoor)

• Topics of interest• General consumption• Yesterday time budget• Socio-demographics

The audience indices are calculated through the“Recent Reading Method”, the best methodologyat the moment, internationally recognized andused.

The Software is Sesame.The main variables in the study are: age, sex,

social grade, area, and education level, shoppingand consumption behavior, HH composition,children in HH, personal and HH income, HHexpenditures, marital status, holidays, travel,ownership of mobile phone and home products,cinema attendance, PC and internet usage,smoking habits, pet ownership. Sesame is softwarefor media and consumer insights analysis andplanning. Its strong points are:

• Easy-to-use tables• Quick data analysis• Title ranking based on specific indicators

• Simultaneous analysis and optimization for upto 10 media plans

The application includes 2 major modules thatcan be accessed from the main menu:

• Exploring Markets (target group definition andevaluation)

• Media Evaluation and Media Planning (mediaranking, accumulation, duplication)

The study is delivered on a quarterly basis.Data is available upon subscription and is limited

to BRAT members. Audience data is available onlyfor BRAT member titles.

11www.initiative.com media research

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 16/120

3. RADIO

3.1. The Radio Audience Survey (SAR) is a

syndicated research program in co-operation with

the Radio Audience Association (ARA). In 2003,

IMAS and Mercury Research were appointed to

implement the new radio audience measurement.The new service is available since June 2004.

The frequency of the study is two waves per year:

March - April and September - October (8 weeks

each), for a four-year period: 2004 - 2007. Starting

with 2008, SAR will delivery audience data in three

waves (first in June 2008, second in September

2008 and last in January 2009).

The universe covers the urban population, aged

11+. The sample size is 11,000 individuals per

wave totaling 20,000 interviews/year (universe

19,169,422 individuals).

Sample structure:

a) 11 regions (quite homogeneous areas

identified through a multifactor cluster

analysis)

b) 4 categories of towns and cities (over

200,000; 100,000-200,000; 50,000-100,000;lower than 50,000) = 219 totally (106 in

urban and 114 in rural areas)

Data collection is performed at the respondent’s

residence, on a printed questionnaire. The

audience measurement uses the ‘Day-After Recall’

method. Respondents are assisted to recall as

accurately as possible the listening sequence from

previous day.

The questionnaire, developed by IMAS, includes

the following sections:

a. Mass media:

• Primary mass media (the stations listed

by ARA). The main stations to be

measured are: Romanian public

stations (national, regional, local);

Romanian private stations; this section

also includes questions regarding

stations’ awareness, radio receptionequipment and radio usage habits.

b. Mobile/PC/Internet usage

(necessary for an accurate audiencesegmenting)

c. Consumption and purchase behavior

(necessary for an accurate audienceprofile)

• Purchase intention regarding durablegoods in the next 12 months

• Alcoholic beverages consumptiond. Socio-demographic

• Respondent’s socio-demographiccharacteristics

• Household characteristics

The processing and analysis of audience data areperformed with a specialized application of IMAS,MasoR.7. The audience segmentation considers all

the variables in the questionnaire on the basis of which the user can build specific target groups.

4. OUTDOOR

Neither in 2007, the OOH industry could releasethe audience study promised to clients since 2006. Affichage, News and EpaMedia tried, using their own classification for billboard values, to sustainprice increasing, but they couldn’t offer studiesabout the reach and efficiency for campaigns. Inabsence of modern instruments for planning andselection, OOH suppliers used photographs, maps,

location previews.In some towns were approved restrictive

regulations regarding outdoor, but in Bucharestthese regulations are not very precise. Even theinternational suppliers and local authorities met at“Mediafax talks about OOH” conference anddiscussed about necessity of new regulationsregarding this activity in Bucharest, 2007 didn’tbrought positive changes. Affichage, in partnership with JCDecaux,

EpaMedia and News Outdoor asked an auction for

urban furniture, but this haven’t been materializedin 2007.

5. INTERNET

The BRAT members working in the field of internet, 60 companies, founded in 2006 a newdepartment inside the bureau, aimed to produce aninternet audience study. The objectives set forth for these new department are the objectivity of measurement and standardization, finalized in aInternet Measurement System. The IAM, namedSATI will provide to the market the results for the

traffic, audience and socio-demographic profiles of the websites included in the survey.

www.initiative.commedia research

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 17/120

In 2006, BRAT organized the first tender for thetechnical solution of the future IAM. BRAT received7 valid offers. BRAT was assisted in the tender process by an independent consultant, Mr. ManuelSala – Technical Director of OJD Iterativa Spania.BRAT chooses at the end of the evaluating processthe German company Spring as the supplier for thenext four years.

In 2007 the Internet Department of BRAT gather almost 76 members, between them all the major players in the online industry.

The method used for measuring the traffic,audience and profiles of the websites is alreadyused for many years in other 4 European countriesand is widely accepted and recognized. It fulfils theIFABC guidelines regarding the traffic

measurement.

In October 2007 BRAT deliver for the first time theresults for the traffic measurement according to theSATI system. BRAT provided to the members anapplication, available online, for the usage of thesedata.

The results for the audience and profiles of thewebsites will be available for the first time in June2008. The audience and profile results of thewebsites will be available to the member through a

specialized media planning software.

This will create for BRAT a new stage of development, being the first step for the advertisingindustry in Romania to gather all the strategicinformation about media in one single source.

Consumption & Lifestyle Research

SNA FOCUS

In 2003 BRAT decided to develop a consumption

survey based on the already established SNAresearch. SNA FOCUS field research waslaunched in October 2005 and the first results weredelivered in October 2006, thus replacing the TGI®service (former consumer lifestyle survey). SNAFOCUS is a syndicated research, controlled by theadvertising industry (BRAT).

The research objectives reached by SNAFOCUS: obtain comprehensive information aboutmedia penetration, products and servicespurchase/usage patterns and the socio-cultural

behavior. Types of media analyzed: print, radio, TV,internet, cinema and outdoor.

Information:

• Penetration of print titles / media channels• Qualitative data referring to usage behavior,

product and services consumption, includingbrands

• Qualitative data referring to socio-culturalbehavior

The description of the target group permits theusage of socio-demographics, consumptionbehavior and psycho-graphic variables. Theinformation related to respondents’ lifestyle:purchase behavior, information habits and sources,their attitudes and values are available, linked tothe media usage.

SNA FOCUS has the same universe as SNA

survey, urban area living people, 14 – 64 years old. At the end of the SNA face to face interview, theinterviewer has to ask the respondent if he/sheagree to fill in another questionnaire, theconsumption one (FOCUS). The FOCUSquestionnaire is self completed by the respondent;the interviewer had only to help the respondent tounderstand the way the questionnaire has to befilled in and to collect the completed questionnaire.

The SNA-FOCUS survey from BRAT will build thecomplex profile of the specific media consumer in

one consolidated media resource. The researchcombines media penetration data, product andservices consumption and with socio-culturalbehavior.

SNA FOCUS will test the possibility of implementing a CAPI method for the face to facepart of the interview. In autumn 2008, BRAT willtake a decision regarding this new method

Media Monitoring

The services available with most of the

specialized companies include:• Advertising activity reports covering all media(see each company below)

• Special analysis reports:• trends, rankings• brand, campaign analysis• category, sector analysis• producer, advertiser analysis

• Data reports:• at any level of detail• for specific brands, products,

categories

• for all selected media• for a specific day, month, year

13www.initiative.com media research

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 18/120

• Campaign tracking:• monitoring and follow up on the

implementation of any advertisingcampaign

Additional services:

• Copy Service• Early Warning Service: interested parties

can be informed about competitiveadvertisements just gone on air , as early aspossible.

The most important media monitoring companies are:

1. ALFA CONT - monitoring data for TV, pressand radio. They offer:• Detailed and summarized reports;

• Info regarding advertisers, manufacturers,brands, media names, reports regardingmarket cluttering (total ad minutes, number of breaks, number of spots) etc;

• Copies of TV and Radio spots and programson VHS video tapes or on CD

• Color, black and white copies of advertisements on magazines andnewspapers (Xerox copies, scannedand/or printed)

• Early warning service (for new ads, differentnews or programs)

Database starting March 1999The monitoring covers a total number of over

227 media channels:• 15 TV channels• 9 radio stations• 202 press titles (22 central newspapers, 68

local newspapers and 112 magazines)

2. MEDIA IMAGE – monitoring data for press,

TV and radio.• Media Image Group is the only Romanianmonitoring agency that covers, beside thecentral media, all the regional newspapersand magazines in the 40 Romanian countycapitals.

• The monitoring covers a total number of over 450 media channels (27 central dailies,109 magazines, 301 regional newspapers,9 TV channels and 7 radio stations).

• The whole radio and TV broadcasts are

recorded digitally and clients have access tothe latest 14 days full program data.

Media Image offers back search monitoringfor a maximum period of four years in case of central newspapers.

• Beside English and French translations, allMedia Image Group reports allow access to

all original materials (scanned articles, digitalcaptures of TV and radio news, talk shows)In parallel, customers have access tocomplete daily-updated web archives of their monitoring reports, submitted to powerfulsearch engines.

3. MEDIAFAX - monitoring data for press, radioand TV stations:

• Mediafax, the leading general and business

information provider in Romania, has beenproviding professional press clipping servicesfor 9 years now, to more than 200 corporateand institutional clients.

• Mediafax Monitorizare, the specialized pressclipping department of the company, monitorsmore than 240 central, local and foreignpublications, in both Romanian and Englishlanguages, 12 national TV channels and 9national radio stations. Mediafax Monitorizarealso offers access to an archive of all pressarticles monitored since 2001, through anelectronic interactive database, availableonline at www.monitorizarepresa.ro.

Theirs press monitoring products include:• Daily press monitoring reports - summaries

and clippings of press articles published in thecentral press, TV and radio newscasts

• Daily local press monitoring reports -summaries and clippings of press articles put

out by over 140 local publications althoughthe country

• Event coverage reports - summaries andclippings of press articles published by thecentral press covering a certain event

• Media image assessment analyses -periodical analyses, tailored to our customers’needs, assessing their media coverage bothquantitatively and qualitatively

• On-demand recordings of TV and radio

newscasts, talk-shows and programs• Transcripts of prime-time talk-shows

www.initiative.commedia research

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 19/120

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 20/120

Overview

2007 brought yet again significant developments on Romanian media market. TV followed the trend withthe launch of new stations by all important media groups. Intact launched Antena 2, an entertainmentchannel, Realitatea group launched a niche channel named Romantica targeting women and Media Prore-launched its sport channel under the name Sport.ro. The Turkish media giant, Dogan Media Groupentered the Romanian market by launching, in co-ownership with Ringier Romania, the generalist channelKanal D.

At the end of 2007 Audience and Monitoring data are available for 38 TV stations: TVR 1, TVR 2, ProTV, Antena 1, Antena 3, Euforia, Acasa TV, Prima TV, Kiss TV , UTV, Jetix, Discovery, MTV Romania,B1TV, Realitatea TV, Minimax, National Geographic, TVR Cultural, Sport.ro, Telesport, National TV, ProCinema, AXN, OTV, N24, Senso, Favorit TV, Hallmark, Sport Klub, Romantica, Eurosport (1 st February),MGM (from 5th September), Kanal D (from 18th February), Antena 2 (from 9th April), Etno TV (from15th January), Taraf (from 15th October), Sport One (from 1st June) and Cartoon Network (from 1st

November).

Television is the most important entertainment source for Romanians due to a large number and varietyof channels and a robust cable penetration. According to the Establishment Survey of 2007 developed byIMAS and TNS CSOP, cable penetration was 71.2% at national level and 82.6% in urban area. This rateis one of the biggest in Europe. Moreover, Direct to Home (DTH) penetration increased over the past fewyears. According to IMAS and TNS CSOP, the penetration rate of DTH in 2007 is 11.2% at national level,20, 6% in rural area and 5.1 % in urban area.

In 2007 TV grew stronger by attracting 65% of all net advertising revenue to a total of 310 million €.Despite the high CPP inflation starting back in 2004 television is still the most effective media channel

with an average net CPT of 1.9 € - 2 € (All urban).

In 2007, we estimates that Media Pro (Pro TV, Acasa TV, Pro Cinema and Sport.ro) attracted the largestbudget share, ca. 50% of total net TV ad-spend. Intact (Antena 1, Antena 2, Antena 3, Euforia, Telesport)follows with a share of about 23%, then SBS (Prima TV and Kiss TV) with ca. 9% share. SRTV (TVR1, TVR2, and TVR Cultural) attracted ca. 8% of total TV spends while Realitatea Media (Realitatea TV andRomantica) gathered about 5% share. However, the cumulated market share of first five TV channels ison a decreasing trending which begun two years ago: in 2005 the Top 5 stations cumulated ca 90% of totalTV investments, while in 2007 this share decreased to 78%. The trend is due to the continuing increase

of the niche stations both in terms of revenue share as well as in audience share. The share of GRP30”sold by niche stations increased from 20% in 2005 to 35% in 2007.

In 2007 the number of GRP30” sold increased by 5% compared to 2006 (GRP30”), yet clutter and sold-out kept occurring, for the demand grew stronger still.

The total inventory sold in 2007 by TV stations was 1.700.000 GRP30”, of which 21% by ProTV, 16% by Antena 1, 14% by Acasa TV, 7% by Prima TV and 7% by TVR1.

The primary cause for the increasing inventory is the increase of the number of monitored TV channels,mainly niche channels. In 2005 the cumulated share of all monitored channels was 82.3%. In 2007 it

reached 86.3%. Besides, there is around 13% share of audience which is not monitored, belonging tolocal television, satellite transmission, international channels, yet this share is decreasing every year.

www.initiative.comtelevision

“I hate television. I hate it as much as peanuts.But I can't stop eating peanuts.”

Orson Welles (American motion-picture actor, director, producer and writer, 1915-1985)

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 21/120

Another cause is the unprecedented loading level achieved by TV stations over 9 months of 2007.

In 2005 the average TV loading for the 07:00 - 26:00 time interval at all stations was 57%; in 2007 theloading reached 72%, with peaks in Prime Time and High Season months going as high as 140% (e.g.November 2007).

Compared to 2006, the average no of TV advertisements a person (all urban, including guest) is exposedto during the weekday, increased by 7%. According to TNS AGB, at the end of 2007, the average grossnumber of weekly TV impacts was 7.110.492 (for adults), 3% more than in 2006.

Graph 1: Volume of advertising in no. of seconds/ month

Source: TNS AGB INTERNATIONAL

The average spot-length in 2007 was 24 sec., where short spots (5-20 sec.) weigh is 47%. Comparedto previous year, in 2007 short spots and solo spots were widely used. In 2007 the weigh of short spotswas 47%, from 45% in 2006. The number of solo spots increased from 6,117 in 2006 to 6,925 in 2007.

Graph 2: Spot-lengths – share %

Source: TNS AGB INTERNATIONAL

Years 2005 2006 2007

Buying target GRP30” (000) sold 1,500 1,600 1,700

Share of TV monitored (all urban, %) 82% 85% 86%

TV loading (%) 57% 66% 72%

17www.initiative.com television

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 22/120

www.initiative.comtelevision

The time spent viewing in 2007 decreased by 5% compared to 2006 to an average of 3.9 hrs/day.Graph 3: Time spent viewing 2006-2007 - All urban incl. Guest - (avg. no. of minutes/day) - Monthly dynamic

Source: TNS AGB INTERNATIONAL

TV Channel’s profile

Total Audience observes the seasonal trend, peaking in winter and decreasing over summer, yet thereare no important changes versus 2006. ProTV remains leader (Rtg 2.5 %, Shr 15.5% - all urban), followedby Antena 1 (Rtg 1.9%, Shr 11.8% - all urban) and TVR 1 (Rtg 1.3%, Shr 8.2% - all urban), with ratingslower than those of 2006. In 2007, all main channels lost audience in favor of niche stations. Prima TVkeeps a similar average audience level, hence maintaining its 5 th rank (Rtg 0.8%, Shr 4.9% - all urban).Graph 4: Monthly Dynamic – Program’s analysis (Rtg %) – all urban (whole day) 2007

Source: TNS AGB INTERNATIONAL

Graph 5: Share of audience evolution by station / by month – all urban (whole day) 2007

Source: TNS AGB INTERNATIONAL

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 23/120

19www.initiative.com television

S o u r c e : T N S A G B I N T E R N A T I O N A L

G r a p h

6 : T V C h a n n e l ’ s p r o f i l e 2 0 0 7 ( s o c i a l s t a

t u s v s . a g e ) - a l l u r b a n ( R t g , w h o l e d a y )

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 24/120

www.initiative.comtelevision

Pro TV (87.5% national coverage) remainsleader in viewers’ preference for the 4thconsecutive year. According to TNS AGB, the topaudience scoring programs were ChampionsLeague transmissions with 1,770,000 urban

viewers. “Pro TV News at 19” with Andreea Escasurpassed news programs of other stations,registering 1,673,000 viewers. Another showdelivering high ratings was “Dansez pentru tine”,continuing its success from starting year (2006)with 812,000 viewers. As “Teo” was discontinued in2006, Pro TV found a success recipe to revive the17:45 – 19:00 time slot with a new entertainmentprogram “Happy Hour” hosted by Catalin Maruta.Being launched in October, the show attracted asizeable audience (483,000 viewers). Also, someshows dedicated to special events were top

audience scoring: “Made in Romania”, dedicated toRomanian National Day Dec 1st brought in646,000 viewers and “Happy End 2007” whichattracted 762,000 viewers.

Pro TV delivered a good affinity on almost alltargets vs. buying target ‘18-49 y.o., urban’ thusmaking the station a top advertisers’ preference.

Antena 1 (88.3% national coverage) is thesecond commercial station by 2007 audiences.Football transmissions brought the highestaudience: Champions League with 1,740,000urban viewers, Romania’s Super Cup with

1,349,000 viewers and Romanian Cup with965.000 viewers.

The well-known entertainment shows continuedto deliver constant high ratings against urbanaudience: “Piata Divertis” (977.000 viewers),“Genialii” – a show dedicated to Romanianpersonalities (Maria Ciobanu, Alexandru Arsinel,Gheorghe Hagi, Angela Similea, etc) - attracted800,000 – 970,000 viewers per show, “Dindragoste” hosted by Mircea Radu (877,000viewers). The New Year’s show, “RevansaStarurilor” with 1,290,000 viewers surpassed ProTV’s show. Another top rating show was “Vreau safiu mare vedeta” with 1,239,000 viewers.

In 2007, the buying target of Antena 1 was “All,urban”.

TVR 1 (98 % national coverage) is the mainpublic channel and ranks 3rd in terms of urbanaudience. TVR 1 was the audience leader for

sports transmissions in 2007 with 1,845,000viewers for the qualification rounds to the EuropeanFootball Championship, 1,134,000 viewers for UEFA Cup transmissions and 1,063,000 viewersfor Handball Women World Championship. 2007brought important programming changes due todiscontinuity of success formats such as “Surprize,Surprize” (last show in December) and “Iarta-ma”(last show in January). Special events as “GalaUnicef” and Eurovision national pre-selectionattracted top audiences: 877,000, respectively798,000 viewers.

TVR1 programming target group is “All, 25+ y.o.,national” and the buying target is “18+, all urban.

Graph 8: Antena 1 – Audience profile - TgAfin.%

Source: TNS AGB INTERNATIONAL (reference target: all urban)

Graph 7: ProTV – Audience profile - TgAfin.%

Source: TNS AGB INTERNATIONAL (reference target: all urban)

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 25/120

21www.initiative.com television

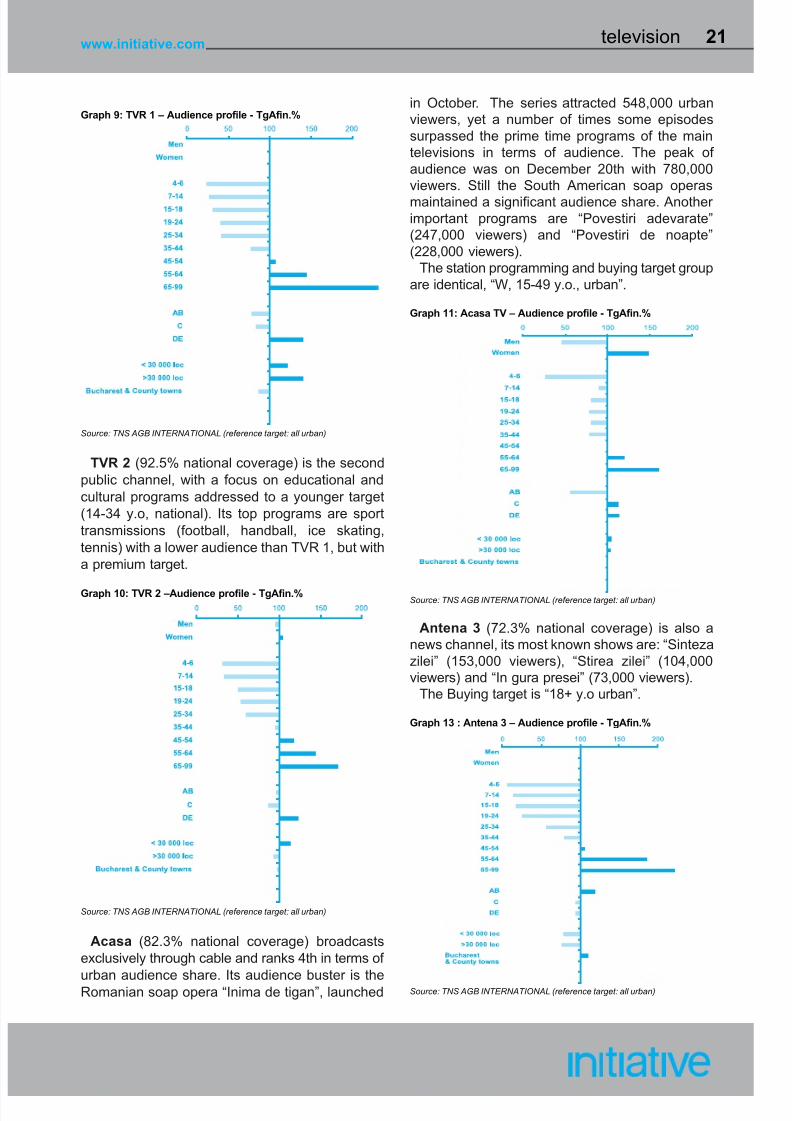

TVR 2 (92.5% national coverage) is the secondpublic channel, with a focus on educational andcultural programs addressed to a younger target(14-34 y.o, national). Its top programs are sporttransmissions (football, handball, ice skating,tennis) with a lower audience than TVR 1, but witha premium target.

Acasa (82.3% national coverage) broadcastsexclusively through cable and ranks 4th in terms of

urban audience share. Its audience buster is theRomanian soap opera “Inima de tigan”, launched

in October. The series attracted 548,000 urbanviewers, yet a number of times some episodessurpassed the prime time programs of the maintelevisions in terms of audience. The peak of audience was on December 20th with 780,000viewers. Still the South American soap operasmaintained a significant audience share. Another important programs are “Povestiri adevarate”(247,000 viewers) and “Povestiri de noapte”(228,000 viewers).

The station programming and buying target groupare identical, “W, 15-49 y.o., urban”.

Antena 3 (72.3% national coverage) is also anews channel, its most known shows are: “Sintezazilei” (153,000 viewers), “Stirea zilei” (104,000viewers) and “In gura presei” (73,000 viewers).

The Buying target is “18+ y.o urban”.

Graph 13 : Antena 3 – Audience profile - TgAfin.%

Source: TNS AGB INTERNATIONAL (reference target: all urban)

Graph 11: Acasa TV – Audience profile - TgAfin.%

Source: TNS AGB INTERNATIONAL (reference target: all urban)Graph 10: TVR 2 –Audience profile - TgAfin.%

Source: TNS AGB INTERNATIONAL (reference target: all urban)

Graph 9: TVR 1 – Audience profile - TgAfin.%

Source: TNS AGB INTERNATIONAL (reference target: all urban)

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 26/120

www.initiative.comtelevision

Prima TV (84.8% national coverage) ranks 5th inurban audience share. In 2007 it attains aremarkable audience share with two main footballtransmissions UEFA (1,099,000 viewers) andChampions League (824,000 viewers). Its topscoring shows are “Tradati in dragoste” (545,000viewers), “Cronica carcotasilor” (431,000 viewers),“Schimb de mame” (419,000 viewers), “Mondenii”(206,000 viwers), but all these programs have lostaudience compared to 2006.

It’s programming target group is “All, 15-44 y.o.,urban” and the buying target is “18-49, all urban”.

Kanal D (62.7% national coverage) was launchedon 18th of February 2007 by Dogan MediaInternational. It is an entertainment channel,focusing on local productions as “Nora pentrumama” (171,000 viewers), “Fluier final” (115,000viewers), “Vacanta Mare Reloaded” (71,000viewers). Its main achievement was the acquiringof the broadcasting rights for the RomanianFootball League 1, which delivered top audiencessuch as 1,290,000 viewers for Steaua – Dinamo.

The station’s target is “18-49 y.o Urban”.

Realitatea TV (80.8% national coverage) is theleader on the News specialty. Its audience isattracted by its qualitative social, political andeconomic programming. Its top audience programsare: “Tu ai decis” (251,000 viewers), “Putere laputerea a patra” (225,000 viewers), “Tu facirealitatea” (172,000 viewers), “Tanase si Dinescu”(168,000 viewers).

Realitatea’s programming target group is “25+y.o., urban” and its buying target is “18+ urban”.Graph 15: Realitatea TV – Audience profile - TgAfin.%

Source: TNS AGB INTERNATIONAL (reference target: all urban)

Graph 14: Kanal D – Audience profile - TgAfin.%

Source: TNS AGB INTERNATIONAL (reference target: all urban)

Graph 12: Prima TV – Audience profile - TgAfin.%

Source: TNS AGB INTERNATIONAL (reference target: all urban)

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 27/120

23www.initiative.com television

TV Buying Perspectives 2008

Due to inflation announced for 2008 sales, theyear had gone off to a very slow start.

There are categories which are likely to reducetheir investment relative to previous year:

banking/finance, automotive and some of theFMCG categories. The overall growth rate isexpected to decrease from significant double digitpercentage to a single digit percentage over thenext 3 to 5 years.

Our estimations for the 2008 TV market are:• ca. 24% increase of the net TV spends vs.

2007. We expect the net TV market to reachca. 385 million €.

• a decrease of 5% in the total inventory of GRP30” sold, assuming that in Q4 the loadinglevel will be under that of 2007 while the

cumulated weight of the Top 5 channels willdiminish.

• an overall CPP increase of 30% to 45%.

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 28/120

Overview

Over the past years, Romanian radio marketwitnessed many launches; at the end of 2007 thenumber of radio licenses issued by CNA stands at671.

The most important radio owners on Romanianmarket are SBS Broadcasting Media and Radio 21with 127 radio licenses. The radio groups with theleading market share, SBS Broadcasting Media

and Lagardere (main shareholder of Europa FMand owner of 21% of Radio 21) have consolidatedtheir strong position by purchasing new stations.Group Lagardere made one of the most importantacquisitions by taking over Radio Deea whichprovides national coverage through its 23 licenses. Another important development on the market isthe purchase of Mix FM and One FM by SBSBroadcasting Media and the launch of Pro FMDance by Radio Pro Company. The number of niche stations increased with the launch of NewsFM (owner Intact Media) and Realitatea FM (owner Realitatea Catavencu). Radio Guerrilla increasedthe number of local stations to 26 at the end of 2007.

According to CNA, top 10 owners of radiolicenses in 2007 are the following:

1. SC. SBS BROADCASTING MEDIA SRLwith Kiss FM and Magic FM76 licenses

2. SC. RADIO XXI SRLwith Radio 21

51 licenses3. SC. ABC PLUS MEDIA SAwith National FM and Favorite FM35 licenses

4. SC. COMPANIA DE RADIO PRO SRLwith Pro FM, InfoPro, Pro Clasic31 licenses

5. SC. REALITATEA MEDIA SAwith Realitatea FM, Radio Guerrilla andRadio Alpha29 licenses

6. PATRIARHIA ROMANA

with Radio Trinitas27 licenses

7. SC AUDIO DELTA SRL

with Micul Samaritean

27 licenses

8. SC GRUPUL MEDIA CAMINA (G. M. C.)

with Romantic FM

24 licenses

9. SC MINISAT TELECOM SRL

with Radio Minisat

19 licenses10. SC RADIO TRANSILVANIA

with Radio Translivania

15 licensesSource: www.cna.ro

In 2007, the total radio net ad-spend increased by

31% vs. 2006, reaching over 30 million €. This is

due to rate card tariffs increase and also to bigger

budgets invested by advertisers.

According to Alfa Cont, the total gross ad-spendincreased by 33% compared to 2006, reaching 91

million €. The market is dominated by SBS

Broadcasting Media and Europe Development

International, with a combined share of 78% of total

radio revenues.

Just as in 2006, Kiss FM remained the station

with the biggest share of ad spend (30%), followed

by Radio 21 (23%) and Europa FM (21%). The

growth of ad spend is partly generated by the

increase of audience at the leading stations, as

Kiss FM, Radio 21 and Europa FM, which were

often sold-out in Prime Time. Another reason for a

good evolution of sales was the special projects

organized by these stations, such as concerts,

contests launching events, etc.

The main radio station owned by Romanian

Society of Radio Broadcasting increased

adverstising sales by 113%. As of March 2007,

Clir Media is administrating the advertising salesfor RRA.

www.initiative.comradio

“You see, wire telegraph is a kind of very, very, long cat.You pull his tail in New York and his head is meowing in Los Angeles.Do you understand this? And radio operates exactly the same way: you send signals here, they

receive them there. The only difference is that there is not a cat.” Albert Einstein (1879-1955)

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 29/120

“Cars & 4x4 vehicles” and “Mobile Telecommunication services” categories remained the leading

categories in 2007. The most important budgets were invested by GSM operators (Orange, Vodafone)

and Group Renault Romania.

Despite the fact that in 2007 Banking & Insurance category had the highest growth on overall media

market (with leading spend from BCR-Erste), on Radio it was surpassed by Mobile Telecommunicationscategory.

Last year, “Beer” category allocated a budget half that of 2006, and so the category exited the “Top 10

most advertised categories on Radio”. On the other hand, “Carbonated soft drinks” spend increased by

80% than 2006.

Radio 21, RRA and Kiss FM maintained the leading position with 65% market share. Radio 21’s first

position is due to its Bucharest station which has around 146,400 listeners per day and growing. In January

2008, Radio 21 already had 42 stations. In September 2007, Radio 21 launched “Nunta PeNeve”, event

which generated an audience growth. Kiss FM is still in top, even though its market share in Bucharest issignificantly lower compared to 2006.

Radio Top 10 Categories

Jan - Dec 2006 Jan - Dec 2007Category Exp. (000’€) Category Exp. (000’€)

Cars & 4x4 vehicles 7,603,428 Cars & 4x4 vehicles 11,313,166

Mobile telecommunications service 5,678,605 Mobile telecommunications service 8,856,265

Banking & Insurance Services 5,630,908 Banking & Insurance Services 7,419,045

Store, Comercial Centres, Supermarkets 5,093,462 Store, Comercial Centres, Supermarkets 7,279,487Culture & Education 4,644,003 Culture & Education 4,968,074

Multimedia 2,930,911 Multimedia 3,851,703

Entertainment Services 2,287,912 Entertainment Services 2,860,894

Other Business Services 1,716,862 Other Business Services 2,553,862

Beer 1,525,398 Beer 2,412,786

Carbonated Soft Drinks 1,430,689 Carbonated Soft Drinks 1,943,010

Source; Alfacont – MediaWatch - excluding media barters

25www.initiative.com radio

Graph 1: Radio ad-spend evolution 2006-2007

Source; Alfacont – MediaWatch (‘000 €) - excluding media barters

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 30/120

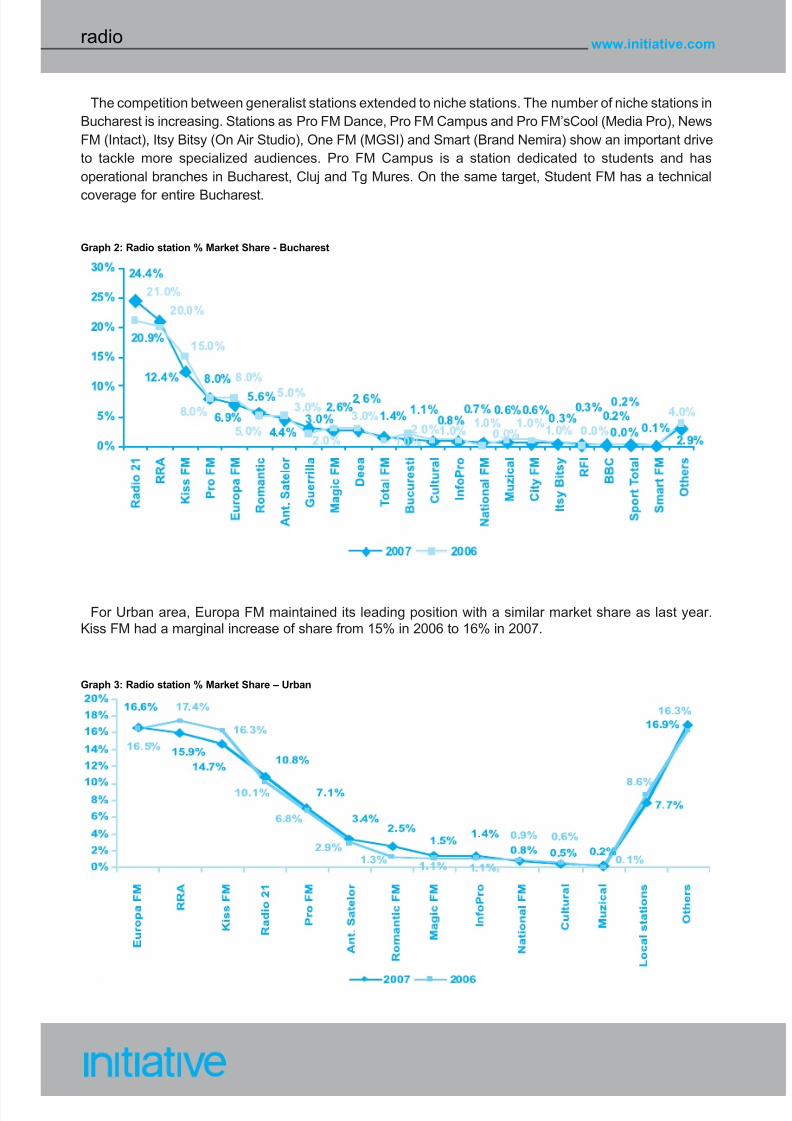

The competition between generalist stations extended to niche stations. The number of niche stations inBucharest is increasing. Stations as Pro FM Dance, Pro FM Campus and Pro FM’sCool (Media Pro), NewsFM (Intact), Itsy Bitsy (On Air Studio), One FM (MGSI) and Smart (Brand Nemira) show an important driveto tackle more specialized audiences. Pro FM Campus is a station dedicated to students and hasoperational branches in Bucharest, Cluj and Tg Mures. On the same target, Student FM has a technical

coverage for entire Bucharest.

www.initiative.comradio

For Urban area, Europa FM maintained its leading position with a similar market share as last year.Kiss FM had a marginal increase of share from 15% in 2006 to 16% in 2007.

Graph 2: Radio station % Market Share - Bucharest

Graph 3: Radio station % Market Share – Urban

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 31/120

27www.initiative.com radio

2 6 5

1 6 6

1 4 3

9 6

4 1

2 , 7 6 0

2 , 4 1 3

2 , 3 9 9

1 ,

5 2 1

1 , 1 0 2

9 2 5

2 7 6

2 1 1

2 , 5 9 8

37

194166

194

166

168

233

189 191

207

188

140

128

177

0

500

1,000

1,500

2,000

2,500

3,000

R R A

K i s s F M

E u r o p a F M

R a d i o 2 1

P r o F M

A n t . S a t e l o r

I n f o P r o

R o m a n t i c F M

B B C

M a g i c F M

N a t i o n a l F M

C u l t u r a l

M u z i c a l

O t h e r s

0

50

100

150

200

250

Daily Reach (000) ATS (min.)

Radio consumption

According to Masor data, the average time spent listening to radio in 2007 is 4.6 hrs / day in provincecities and 5 hrs / day in Bucharest.

Graph 4: Radio stations % Market Share - National

Graph 5: ATS (min) and Daily reach - National

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 32/120

www.initiative.comradio

Kiss FM, Radio 21, Magic FM and National FM target a young audience, most of its listeners having20-29 y.o. Last year they reached 2,091,000 listeners per day.

Europa FM, ProFM, Info Pro and Romantic attracted most of their listeners from 30-39 y.o group,respectively an average of 1,076,000 listeners per day. RRA and Cultural are targeted on a matureaudience, aged over 60.

Graph 6: ATS (min) and daily reach (000) - National

Source: IMAS all 2007

Graph 7: Radio stations by group age - National

Source: IMAS all 2007 (the figures show the dominant age group

2 0

- 2 9 y . o .

3 0

- 3 9 y . o .

4 0

- 4 9 y . o .

5 0

- 5 9 y . o .

O v e r 6 0 y . o .

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 33/120

29www.initiative.com radio

Perspectives for 2008

The radio audience measurement system SARcontinues to offer clients and agencies valuable data.Starting in 2008, SAR will deliver audience data inthree waves (first in June 2008, second in September 2008 and last in January 2009).

In 2008, most of Romanian radio networks continueto develop by launching new stations or bystrengthening the existing ones. Beginning of 2008was already marked by new launches. Radio 21 isextending its network to reach 42 stations while inMarch announced the launch of Vibe FM, a stationwhich will broadcast electronic dance music.

Also, Radio Pro Company is enlarging its networkto include 28 stations and 13 affiliates. Info Proestimates that at the end of April will have activateda total of 39 stations, thus providing nationalcoverage. Pro FM’sCool is trying to extend thenetwork in 40 high schools, all over the country.

The launch of new on-line stations contributessignificantly to radio market development. Pro FM

launches Pro FM Alternative and Pro FM Love in thissegment.

Q1 2008

According Alfa Cont, for the Q1 2008, radioad-spend reached 22 million €, that is 37% morethan Q1 2007. Group Renault, Orange andCarrefour are the biggest investors.

“Cars & 4x4 vehicles”, “Stores, commercialcentres, supermarkets” and “Mobile tele-communication services” are the leading spendingcategories.

Despite the descending trend of radio audience,radio ad spend is expected to grow in 2008

(estimated net growth of 26%).

According to SNA Focus (Jan 07 – Jan 08) Kiss FM occupied the first position in top of mind with 16.5%of persons declaring they use to listen to radio more than one hour per day. The followers in the notorietytop are Europa FM (14%), RRA (12.7%) and Radio 21 (9.5%). The topics of interest proved to be weather news, national and local news and traditional & party music. 62% of persons use to listen to radioprogrammes in the first part of day.

Graph 8: Top of mind radio stations

Source: SNA Focus (Jan 07 – Jan 08)

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 34/120

Market overview 2007

One indisputable fact after 2000 is the explosionof the Romanian press market. Today, we deal witha really developed industry, that is maturing at avery fast pace. This reality is sustained by thevariety of new titles and consolidation of existingbrands, covering a wide variety of publications fromthe point of view of frequency, type, target etc.

Supporting those affirmations is that fact that themost recent National Readership Survey (SNA)delivery includes 161 publications (66 monthlies,15 fortnightlies, 30 weeklies, 41 dailies and 11

supplements). In addition to this, the FOCUScomponent of the National Readership Surveymeasures the consumption of an almost exhaustivenumber of products and services.

“Dynamic” would best describe the evolution of the print market in 2007. The 23% increase inratecard advertising revenue in 2007 compared to2006 (generated by increases in rate card valueand organic growth of the market), that brought thetotal value of the total rate card ad revenue for theprint market to approximately 324 Million EUR (withmedia barters excluded) and the slight change innewspapers / magazines ad revenue ratio (51.1%newspapers / 48.9% magazines in 2007 comparedto 49.6% newspapers / 50.4% magazines in 2006)are just a glimpse of the big picture.

2007 was the year of media acquisitions andsales, new publications launched and some old or young publications cancelled, preoccupation for increasing the added value delivered to consumer by means of covermounts (most frequent ones

being CDs/DVDs, books, fashion items andcosmetic products) and restyling, increase of market presence of already establishedpublications by means of new spin-offs andspecials, increase in the number of point-of-presence websites, publications’ content starting tobe delivered on mobile communication platforms,readership fragmentation and so on.

One of the major media acquisitions of 2007 tookplace when Publimedia International bought backsports daily ProSport from Ringier. Changes in

graphics, style and editorial structure are expectedfor 2008.

A new important international publisher, Attica

Media entered the Romanian market in 2007 byacquiring the license of the two men glossiesMaxim and Playboy (formerly published by PBRPublishing, owned by Publimedia International).The magazines were also restyled and Attica Mediaincreased its presence on the market by launchingthe women glossy InStyle in 2008. It is expectedthat the next move from Attica will be the launch of Grazzia magazine. Another important move was the acquisition of

25% of the Dogan’s Media Romania shares (owner of Kanal D) by the publishing house Ringier Romania. This move continues the internationalline of partnership between Dogan Media andRingier and could also be the start of the 4th mediacluster on the Romanian market (in addition to thealready established Publimedia-MediaPro, Intactand Realitatea-Catavencu clusters).

In 2007 and continuing in Q1 2008, the mostattractive segments for new publication launcheswere the up-market / exclusivist glossy magazines(Harper’s Bazaar, Eve, Esquire, Temporis) and

business/financial segments (Money Express,Business Standard, Financial Director, Financiarul).

The preoccupation to increase the added valueof publications and make them more attractive for both readers and advertisers brought a new trendin the print market: the extensive use of covermounts as marketing tools to increase sales.This strategy was mostly used on the womenmagazines segment (Glamour, Beau Monde, Joy,Unica, Avantaje, Tabu etc.) and quality newspaperssegment (Jurnalul National, Cotidianul). However,

the effects of this trend on a long term perspectivecould backfire when covermounts would turn fromnice-to-haves to must-haves, forcing the respectivepublishers to always have covermounts.

In addition, tabloids and daily sports newspapers(e.g.: Libertatea, ProSport) as well as mass-marketmagazines for women (e.g.: Libertatea pentrufemei, Femeia de azi) offered promotional contestswith various prizes (instant winning of magazines,money, houses) as a way to increase circulation,brand awareness and allegiance to the magazine.

Newspapers (e.g.: Adevarul) and semi-glossyand mass-market magazines for women (e.g.:

www.initiative.compress

“It's amazing that the amount of news that happens in the world every day always just exactly fits the newspaper.”

Jerry Seinfeld

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 35/120

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 36/120

The publishers

Romania has a large variety of publishers,containing international publishers directly presentlike Edipresse-AS, Ringier, Sanoma Hearst,Burda, Motorpresse, Liberis, Attica, internationalpublishers present by means of publishing licenseslike Hearst, Emap, Rodale etc. and localcompanies like Publimedia, Intact, Catavencu,R Publicatii, Business Media Group, Inform Media,Media Sud Management etc.

By using the share of ratecard ad revenue,publishers on the Romanian market can be dividedin 4 groups:

• publishers with 10%+ share of ad revenue:Ringier Romania (magazines and newspapers,specialized in mass-market publication, owner of Libertatea - the best performing tabloid on theRomanian market), Catavencu (magazines andnewspapapers, part of the Realitatea-Catavencumedia cluster, owner of 24-FUN, the best per-forming free city guide), Publimedia International(magazines and newspapers, very diverseportfolio, part of the Publimedia-MediaPro mediacluster) and Editura Intact (magazines andnewspapers, part of Intact media cluster)

• publishers with 2% to 10% share of adrevenue: Edipresse-AS (diverse magazineportfolio, specialized in women magazines),Sanoma Hearst (idem), Kopa Publicatii (owner of the second best performing free city guide,Sapte Seri), Burda Romania (diverse portfolio,specialized in semi-glossy magazines for women)and R Publicatii (only one title in its portfolio -quality newspaper Romania Libera)

• publishers with 1% to 2% share of adrevenue: Business Media Group (specialized in

business magazines), Adevarul (publisher of qualitynewspaper Adevarul), Media Sud Management(publisher of national newspaper Curierul Nationaland local newspaper Gazeta de Sud), DomusMagazin (specialized in home and decomagazines), Inform Media (specialized exclusivelyin local publications and the only publisher of exclusively local publications with a market share of more that 1%) and Crucisatorul (publisher of newspaper Gandul)

• other small publisher with a share of ad

revenue lower than 1%, who together represent28.6% of the market

Graph 1: Share of ratecard ad revenue of publishing groupsin 2007

Source: Alfacont

Developments in 2007 and Q1 2008

Publimedia

• buys back the sports daily ProSport from Ringier,while announcing graphics, format and editorialstructure changes for 2008• buys the franchise of the fortnightly city guideTime Out in September 2007 and re-launches it asa October 2007 as a weekly• re-launches business magazine Target in October 2007, improving its content and layout• re-launches newspaper Gandul with a new formatand content• closes at the beginning of 2008 Acasa Magazinand Go4it!• increases its sales portfolio with gossip/paparazzimagazine Ciao! and the Cancan tabloid

Adevarul Holding

• launches Click de Duminica in February 2007• launches a TV guide common to both Adevaruland Averea• transforms Averea into Click in March 2007,keeping it a tabloid

• re-launches Adevarul in April 2007 in a newformat, more compact, together with twosupplements: Adevarul Artistic si Literar and Adevarul TV (the previously mentioned TV guide)• launches Foreign Policy, a global and economicalpolicies magazine, in December 2007• launches Expert Imobiliar, a real estatesupplement freely distributed with each Tuesdayissue of Adevarul

Catavencu

• launches business magazine Money Express in

May 2007 and business newspaper BusinessStandard in June 2007

www.initiative.compress

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 37/120

• re-launches the quality newspaper Cotidianul witha new graphics, content and editorial structure;starting April 2007 Cotidianul is accompanied byColectia Enciclopedica (quality books) and startingJuly 2007 the newspaper is also accompanied byColectia Simfonica (CD’s with classical music)• free city guide 24-FUN extents its network,reaching a total of 11 local editions (in Brasov, Cluj,Timis & Arad, Iasi, Mures, Dolj, Arges, Sibiu,Harghita & Covasna, Nord-Vest) besides theBucharest edition

Intact

• changes in September 2007 the format, layoutand content of Felicia magazine, a mass-marketmagazine for women• launches financial/economy daily Financiarul

Edipresse-AS

• launches parenting magazine Baby in January2007 and psychology magazine Psychologies inthe autumn of 2007• cancels Familia Mea in the autumn of 2007 andSana at the end of 2007

Sanoma Hearst

• launches in the autumn of 2007 the up-marketfashion and beauty magazine for women Harper’sBazaar with a quarterly frequency and the up-

market glossy magazine for men Esquire with amonthly frequency• in April 2008 launches Marie Claire, an up-marketglossy magazine.

Liberis Publications

• launches Prevention, a pocket size health andfitness glossy for women in November 2007

Attica Media

• enters the market by buying PBR Publishing(Playboy and Magazines) from Publimedia in

September 2007• launches the international up-market glossymagazine for women InStyle in April 2008

Inform Media

• transform the local newspaper Cuvantul Liber intoHunedoara Expres in September 2007• launches daily newspaper Cluj Expres in October 2007, thus expanding its coverage from 6 to 7counties

ARBOvision

• edits Alege as for October 2007, a periodicalsupplement with specialized thematic, freely

distributed through insertion in 40 local newspapersand weeklies within the ARBO network, covering36 counties

Business Media Group

• closes Autocar magazine in December 2007

The Marketer

• launches Business Woman in March 2007 withan annual frequency then re-launches it inFebruary 2008 in the form of a glossy magazine for (business) women with monthly frequency

Dramiral Media Group

• transforms newspaper Curentul into a daily freenewspaper

Other launches include:• Green Report (January 2007, business magazinefor the environment industry),• Freestyle (January 2007, free lifestyle glossymagazine, monthly frequency),• Temporis (March 2007, up-market glossymagazine on watches and lifestyle, monthlyfrequency, launche by Automedia),• Q-Magazine (general content semi-glossymagazine, launched with a fortnightly frequency inMarch 2007)• Motociclismo (launched in April 2007 by

Supercar),• MBike (cycling magazine, launched in May 2007by Action Publishing with a frequency of 6 issuesper year),• Grand’Or (launched in May 2007 by Double Click)• Financial Director (free monthly magazinelaunched by Business Publishing Group, targetedto CFOs, controlled distribution),• Avocati de Top (top of Romanian law houses,published first time in June 2007 by Fin MediaGroup),

• Igloo Guide Bucharest (cultural guide, launchedby Igloo Media in October 2007),• Scooby-Doo (cartoon-comics book, launched inOctober 2007 under Warner Bross license),• Medic4all (November 2007, free, distributedwithin hospitals and clinics),• Sapte Seri Covasna (the bilingual Romanian-Hungarian edition of Sapte Seri launched inNovember 2007 by Kopa Publicatii)• Be Blue Air (6 issues per year magazinedistributed to airline passengers of Blue Air airlines,launched December 2007),

• Bestbanking (banking magazine, 6 issues per year, edited by Bestbanking Median),

33www.initiative.com press

8/10/2019 MFB2008

http://slidepdf.com/reader/full/mfb2008 38/120

• anTREN (free weekly magazine, launched inMarch 2008, distributed in high-speed trains andtrain ticket booths in Bucharest and Brasov, willcover 10 cities by the end of 2008),• RING (April 2008, daily free sheet/tabloid,

launched by Confort Media, distributed inBucharest),• Alege TV (April 2008, common product of European Media Invest and Media Sud Europa,distributed within the regional publications Gazetade Sud, Monitorul de Alba, Monitorul de Cluj,Monitorul de Medias, Monitorul de Sibiu, Obiectiv –Editie de Vaslui, Viata Libera Galati, Ziarul de Brailaand Ziarul de Iasi)

In addition to that ARBOmedia increased itsportfolio in 2008 with two new publications –