Embed Size (px)

Citation preview

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 1/42

qwertyuiopasdfghjklzxcvbnmqwerty

opasdfghjklzxcvbnmqwertyuiopasdfg

klzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwe

yuiopasdfghjklzxcvbnmqwertyuiopa

dfghjklzxcvbnmqwertyuiopasdfghjklz

vbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyu

pasdfghjklzxcvbnmqwertyuiopasdfgh

klzxcvbnmqwertyuiopasdfghjklzxcvbmqwertyuiopasdfghjklzxcvbnmqwer

uiopasdfghjklzxcvbnmqwertyuiopasd

ghjklzxcvbnmqwertyuiopasdfghjklzxvbnmqwertyuiopasdfghjklzxcvbnmrt

uiopasdfghjklzxcvbnmqwertyuiopasd

ghjklzxcvbnmqwertyuiopasdfghjklzx

Letter of Credit & The Performance of

AB Bank

Back-to-Back Letter of Credit

January 05, 2011

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 2/42

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 3/42

i

LETTER OF TRANSMITTAL

Sumaiya Zaman

Lecturer

Department of Business Administration

University of Liberal Arts Bangladesh

Subject: Submission of BBA Internship Report

Dear Madam,

With due respect and honor, I would like to submit internship report, which was done on AB Bank Ltd., a

study on its Karwan Bazar Branch. The internship program has given me the opportunity to combine my

theoretical knowledge with practical experience. I tried my level best to make this report meaningful

and informative.

I have done my internship in AB Bank Ltd. for the period of three months. The off icers of ABBL were very

cordial and extended their hands within the limit of their authority. As the time was limited, the report

could not be done more comprehensively and analytical.

Your valuable advice, suggestion and guidance have helped me a lot to prepare the report. I will be very

grateful, if you kindly accept this report.

Sincerely yours,

Nazmin Akhter

ID-BBA 071011

Department of Business AdministrationUniversity of Liberal Arts, Bangladesh

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 4/42

ii

Contents

LETTER OF TRANSMITTAL ................................................................................................................... 1

Executive Summary ................................................................................................................................. 1

Paper work is must for Back to Back LC. Due to the proper documentation every year defaulters areincreasing rapidly..................................................................................................................................... 2

Though Ive worked in the LC department of this bank I observed the following f indings- ........................ 2

1.1. Origin of the Report .......................................................................................................................... 4

1.2. Objective of the report...................................................................................................................... 4

The main objectives of the study are: ...................................................................................................... 4

The Secondary objectives of this report are: ............................................................................................ 4

1.3. Methodology of the Study ................................................................................................................ 5

1.3.1. Primary Sources of Data: ................................................................................................................ 5

1.3.2. Secondary Sources of Data: ............................................................................................................ 5

1.4. Scope of the Study ............................................................................................................................ 6

1.5. Limitations of the Study .................................................................................................................... 6

2.0. Introduction ...................................................................................................................................... 7

2.1. AB Bank over View ............................................................................................................................ 8

2.2. Management Committee ................................................................................................................ 10

2.3. Corporate Information .................................................................................................................... 103.0. Letter Of Credit ............................................................................................................................... 11

3.1. Parties involved in LC transaction: ................................ ....................... ................................ ............ 11

3.2. Letter of Credit Process: .................................................................................................................. 12

3.3. Commercial Letter of Credit Flow .................................................................................................... 12

3.4. Settlements under a Letter of Credit ............................................................................................... 13

3.5. Types of Letter of Credit ............................. ...................... ................................ ...................... ......... 13

3.6. Advantages of Letter of Credit: ....................................................................................................... 15

3.7. Risks involved in Letter of Credit. .................................................................................................... 15

3.8. 1. Account Party Benef iciary ............................ ........................ ............................... ...................... 16

3.8.2. Account Party -- Issuing Bank ....................................................................................................... 18

3.8.3. Issuing Bank Benef iciary ............................................................................................................ 18

3.9. Functions of a Commercial Credit ............................ ...................... ................................ .................. 19

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 5/42

iii

3.10. Back to Back Letter of Credit (LC s) ................................................................................................ 20

3.10.2. Opening of Back-to-back Import LCs ............................ ........................ ................................ ....... 20

3.10.3. Payment against Back-to-back Letter of Credit (LCs) .................................................. ................. 21

3.10.4. Back-to-Back LC .......................................................................................................................... 22

3.10.5. Advance against Red Clause Letter of Credit (LC) .................................................. ...................... 23

3.10.6. Reshipment Investment facilities ............................ ....................... ................................ ............. 23

3.10.7. Foreign Back-to-Back Letter of Credit ......................................................................................... 24

3.11. Formalities & Procedure................................................................................................................ 25

3.12. In land Back-to-back Letter of Credit (LC) ...................................................................................... 26

3.12.1. Documents Required for Opening of Back-to-back LCs ............................................................... 26

3.12.2. Additional Documents ................................ ......................... .............................. ......................... 26

3.12.3. Charge Documents ..................................................................................................................... 26

3.12.4. Payment of Back-to-back LC, and Ad justment of Investment facilities .......................... .............. 27

4.0. My Activities at AB Bank Ltd, Kawran Bazar Branch ......................... .............................. .................. 28

4.1. SWOT Analysis ................................................................................................................................ 29

4.2. My Understanding: ......................................................................................................................... 31

While working with the company Ive come up with the following understandings that- ....................... 31

Paper work is must for Back to Back LC. Due to the proper documentation every year defaulters are

increasing rapidly. A proper documentation with full phase having fair evaluation can bring back faith to

the bank as well as the consistent clients of the bank. ........................................................................... 31

4.3. Findings .......................................................................................................................................... 31

AB Bank is one of the recognized banks in Bangladesh banking sector and its accomplishing its activities

in LC sector for a long time. Though Ive worked in the LC department of this bank I observed the

following f indings- ................................................................................................................................. 31

4.4. Recommendations .......................................................................................................................... 32

5.0. Case Study on a practical Back-to-Back L/C...................................................................................... 32

6.0. Conclusion ...................................................................................................................................... 37

7.0. Reference ....................................................................................................................................... 37

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 6/42

i

Executive Summary

AB Bank Limited, the f irst private sector bank was incorporated in Bangladesh on 31st

December 1981 as Arab Bangladesh Bank Limited and started its operation with effect from

April 12, 1982.

AB Bank Limited is now well growing and its operating 77 branches in different parts of Bangladesh. The scope of the study will be limited to the organizational setup, function and

operation of the ABBL in the Bangladesh.

I was assigned at the karwan Bazar Branch and this provided me the way to get myself

familiarized with banking environment for the f irst time indeed. I have an opportunity to gather

experience by working in different departments of the Branch.

A letter of credit is a document typically issued by a bank or financial institution, which

authorizes the recipient of the letter (the "customer" of the bank) to draw amounts of money up

to a specified total, consistent with any terms and conditions set forth in the letter. This usually

occurs where the bank's customer seeks to assure a seller (the "benef iciary") that it will receive

payment for any goods it sells to the customer. These are the following intermediaries of LC-

The Applicant is

The Beneficiary The Issuing or Opening Bank

An Advising Bank

The Paying Bank

The Confirming Bank

The branch may open back-to-back import LCs against export LCs received by export oriented

industrial units operating under the bonded warehouse system, subject to observance of

domestic value addition requirement (stated in terms of permissible limit of CFR value of

imported inputs as percentage of FOB export value of output) prescribed by the Ministry of

Commerce from time to time.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 7/42

2

Paper work is must for Back to Back LC. Due to the proper documentation every year defaulters

are increasing rapidly.

Followings the rules and regulation can also play a vital role for the bank though in some cases

its very diff icult to maintain the rules in the corporate dealings but above all rules and

regulations should be managed in a proper manner.

While working here I came to understand that dealing client especially in the LC department is

not an easy task for this though each of the staffs are very sincere about their activities but they

cannot do it properly due to the work pressure.

Though Ive worked in the LC department of this bank I observed the following

f indings-

y In the department Fax is one of the key instruments to maintain LC activities but in most

cases I found it is out of service which is unexpected.

y Clients from different corporate sector are coming for opening LC without having proper

documentation and also not that much respective about the law.

y Staffs here are so busy that they cannot cooperate as they should with the clients.

y As a bank ABBL does have that suff icient support to the client as well as its clients which

is also unexpected.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 8/42

3

ACKNOWLEDGEMENT

At f irst, I must show my gratitude to the Almighty Allah for giving me capabilities to prepare thisreport. Then, I would like to remember the contribution and keen interest of my parents that

has made me able to come to this stage. Then I would like to express my sincere gratitude and

thanks to my honorable program supervisor Sumaia Zaman, Assistant Professor, Department of

Business Administration of University of Liberal Arts Bangladesh for her brilliant and excellent

guidance and assistance to complete this report.

I am very much grateful to the off icials of the Kazi Ashraf Ali, AVP & Operation Manager,

Karwan Bazar Branch for their support and co-operation. After that, I especially express my

thanks to Ms. Sumaiya Zaman, my supervisor of that branch for guiding me throughout theinternship program.

Finally I like to extend my thanks to all of my teachers and friends who have helped me in

different ways.

Nazmin Akhter

ID # B.B.A-

School Of Business

University of Liberal Arts

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 9/42

4

1.1. Origin of the Report

Placement or internship program is an indispensable part of BBA (Bachelor of Business

Administration) program, University of Liberal Arts that bridge the gap between the theoretical

knowledge and practical situation. I was assigned to the AB bank at karwan bazar branch,

Dhaka to take the real banking experience in order to reinforce knowledge acquired so far from

the BBA program. In this internship program, each student selects a pro ject for study,

completes the study and prepares a report with recommendation for solution of the problem.

This report is tentatively prepared to complete my BBA program and assigned by Sumaia

Zaman.

1.2. Objective of the report

The main objectives of the study are:

To f ind out the actual banking activities happening in a private commercial bank in

Bangladesh.

To fulf ill the requirement for the completion of BBA program.

The Secondary objectives of this report are:

To know the operation of karwan bazar Branch of AB Bank Ltd.

To describe the customer service process of AB Bank Limited.

To analyze the barriers faced by the ABBL in providing service to their customers.

To suggest a supportive role in the progress of banking system in f inancial sector.

To know about the objectives and planning of ABBL.

To know how the branches are eff iciently controlled.

To identify whether all process are perfectly and effectively practiced or not.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 10/42

5

1.3. Methodology of the Study

Different data and information are required to meet the goal of this report. Those data and

information were collected from various sources, such as, primary and secondary which is

shown below:

1.3.1. Primary Sources of Data:

Personal observation.

Face to face conversation with the off icers.

Face to face conversation with the client.

Working at different desks of the bank.

1.3.2. Secondary Sources of Data:

File study.

Annual report of AB Bank Ltd.

Statement of affairs.

Bank Rate sheet.

Internet.

Progress report of the Bank.

Bangladesh Bureau of Statistics report.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 11/42

6

1.4. Scope of the Study

AB Bank Limited is now well growing and its operating 77 branches in different parts of

Bangladesh. The scope of the study will be limited to the organizational setup, function and

operation of the ABBL in the Bangladesh. This report mainly encompasses the performance of

AB Bank Limited in comparison to the overall banking system in Bangladesh. For the purpose of

my internship program, I was assigned at the karwan Bazar Branch and this provided me the

way to get myself familiarized with banking environment for the f irst time indeed. I have an

opportunity to gather experience by working in different departments of the Branch.

1.5. Limitations of the Study

During the study, I have faced the following limitations:

Due to some legal obligation and business secrecy bank was reluctant to provide data.

For this reason, the study limits only on the available published data and certain degree

of formal and informal interview.The bankers are very busy with their jobs, which lead a little time to consult with them.

Category wise export, import and guarantee business, amount and percentage of

classif ied loan originated from the international trade are missing in the report for their

restriction.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 12/42

7

2.0. Introduction

This usually occurs where the bank's customer seeks to assure a seller (the "benef iciary") that it

will receive payment for any goods it sells to the customer.

For example, the bank might extend the letter of credit conditioned upon the benef iciary's

providing documentation that the goods purchased with the line of credit have been shipped to

the customer. The customer may use the letter of cred it to assure the benef iciary that, if it

satisf ies the conditions set forth in the letter, it will be paid for any goods it sells and ships to

the customer.

In simple terms, a letter of credit could be said to document a bank customer's line of credit,

and any terms associated with its use of that line of credit. Letters of credit are most commonly

used in association with long-distance and international commercial transactions.

A letter of credit is a document

typically issued by a bank or financial

institution, which authorizes therecipient of the letter (the "customer" of

the bank) to draw amounts of money up

to a specified total, consistent with any

terms and conditions set forth in the

letter.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 13/42

8

2.1. AB Bank over View

AB Bank Limited, the f irst private sector bank was incorporated in Bangladesh on 31st

December 1981 as Arab Bangladesh Bank Limited and started its operation with effect from

April 12, 1982.

AB Bank is known as one of leading bank of the country since its commencement 28 years ago.

It continues to remain updated with the latest products and services, considering consumer and

client perspectives. AB Bank has thus been able to keep their consumers and clients trust

while upholding their reliability, across time.

During the last 28 years, AB Bank Limited has opened 77 Branches in different Business Centers

of the country, one foreign Branch in Mumbai, India and also established a wholly owned

Subsidiary Finance Company in Hong Kong in the name of AB International Finance Limited. To

facilitate cross border trade and payment related services, the Bank has correspondent

relationship with over 220 international banks of repute across 58 countries of the World.

In spite of adverse market conditions, AB Bank Limited which turned 28 this year, concluded the

2008 f inancial year with good results. The Banks consolidated prof it after taxes amounted to

Taka 230 cr which is 21% higher than that of 2007. The asset base of AB grew by 32% from 2007

to stand at over Tk 8,400 cr as at the end of 2008.

The Bank showed strong growth in loans and deposits. Deposit of the Bank rose by Tk. 1518 cr

ie., 28.45% while the diversif ied Loan Portfolio grew by over 30% during the year and recorded

a Tk 1579 cr increase. Foreign Trade Business handled was Tk 9,898 cr indicating a growth of

over 40% in 2008.

The Bank maintained its sound credit rating in 2008 to that of the previous year. The Credit

Rating Agency of Bangladesh Limited (CRAB) awarded the Bank an A1 rating in the long term

and ST-2 rating in the short Term.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 14/42

9

The Bank decided to change its traditional color and logo to bring about a fresh approach in the

f inancial world; an approach, which like its new logo is based on bonding, and trust. The bank

has developed its logo considering the contemporary time. The new logo represents our

cultural Sheetal pati as it reflects the bonding with its clientele and fulf illing their every need.

Thus the new spirit of AB is Bonding. The Logo of the bank is primarily red, as red

represents velocity of speed and purity. Our new logo innovates, bonding of aff iliates that

generate changes considering its customer demand. AB Bank launched the new Logo on its

25th Anniversary year.

AB Bank commits to nation to take a lead in the Banking sector through not only its strong

f inancial position, but also through innovation of products and services. It also ensures creating

higher value for its respected customers and shareholders. The bank has focused to bring

services at the doorstep of its customers, and to bring millions into banking channels those who

are outside the mainstream banking arena. Innovative products and services were introduced

in the f ield of Small and Medium Enterprise (SME) credit, Womens Entrepreneur, Consumer

Loans, Debit and Credit Cards (Local & International), ATMs, Internet and SMS Banking,

Remittance Services, Treasury Products and Services, Structured Finance for Corporate,

strengthening and expanding its Islamic Banking activities, Investment Banking, specialized

products and services for NRBs, Priority Banking, and Customer Care. The Bank has successfully

completed its automation pro ject in mid 2008. It envisages enabling customers to get banking

services within the comfort of their homes and off ices.

AB Bank has continuously invests into its biggest asset, the human resource to drive forward

with its mission to be the best performing bank in the country. The bank has introduced Dress

Code for its employees. Male employees wear designed ties and females wear Sharee or Salwar

Kamiz, all the dresses are consisted with the unique AB Bank logo.

AB is recognized as the peoples choice, catering to the satisfaction of its cliental. Their

satisfaction is ABs success.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 15/42

10

2.2. Management Committee

Following members are also in the Management Committee:

Head of HR & Transformation

Head of Financial Institutions and Treasury

Head of Internal Control & Compliance

Head of Information Technology

Head of Credit Risk Management

Head of Credit Administration Management

Head of Islami Banking Division

Head of Retail Banking

Head of SME

Head of Risk Management Unit

Head of Corporate & Structured Finance

Head of Regions

2.3. Corporate Information

Name of the Company

AB Bank Ltd

Legal Form: A public limited company incorporated on 31st December, 1981 under the

Companies Act, 1913 and listed in the Dhaka Stock Exchange Ltd and Chittagong Stock

Exchange Ltd.

Commencement of Business

27th February 1982

Registered Off ice

BCIC Bhaban, 30-31, Dilkusha C/A

Dhaka 1000, Bangladesh.

Tel: +88-02-9560312

Fax: +88-02-9564122, 23

SWIFT: ABBLBDDHE-mail: [email protected]

Web: www.abbank.com.bd

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 16/42

11

3.0. Letter Of Credit

In International trade, the buyer and the seller who are located in different countries, may not

know each other and hence many times the problem of Buyers Creditworthiness hampers the

trade between the buyer and the seller. The main objectives of the buyer and the seller in any

international trade and contradictory in terms of Buyer will always try to delay the paymentwhile the seller would like to receive funds at the earliest.

To mitigate this problem, Seller always request Buyer to arrange for a Letter of Credit to be

issued by Buyers Bank. Upon issuance of Letter of Credit, the Buyers bank replaces its own

Creditworthiness to that of the Buyer, it undertakes to reimburse the Seller for the value of the

Letter of Credit Irrevocably provided two underline conditions are fulf illed by the Seller:

All the documents stated in the LC are presented;

All the terms and conditions of the LC are complied with.

The beauty of the LC is that if above two conditions are fulf illed, Issuing Bank will effect

payment to the Benef iciary, irrespective of Applicant reimburses the Issuing Bank or not. Thus,

a Letter of Credit is an undertaking issued by a bank in favor of a Benef iciary (Seller), which

substitutes the banks creditworthiness for that of the Applicant (Buyer).

It is named a Letter because initially the LCs were issued manually in a Letter format address by

Issuing Bank to Benef iciary conf irming its conditional undertaking to reimburse the Benef iciary,

the amount of the LC provided above 2 basic conditions are fulf illed.

3.1. Parties involved in LC transaction:

The Applicant is the party that arranges for the letter of credit to be issued.

The Beneficiary is the party named in the letter of credit in whose favor the letter of

credit is issued.

The Issuing or Opening Bank is the applicants bank that issues or opens the letter of

credit in favor of the benef iciary and substitutes its creditworthiness for that of the

applicant.

An Advising Bank may be named in the letter of credit to advise the benef iciary that the

letter of credit was issued. The role of the Advising Bank is limited to establish apparent

authenticity of the credit, which it advises.The Paying Bank is the bank nominated in the letter of credit that makes payment to

the benef iciary, after determining that documents conform, and upon receipt of funds

from the issuing bank or another intermediary bank nominated by the issuing bank.

The Confirming Bank is the bank, which, under instruction from the issuing bank,

substitutes its creditworthiness for that of the issuing bank. It ultimately assumes the

issuing banks commitment to pay.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 17/42

12

3.2. Letter of Credit Process:

3.3. Commercial Letter of Credit Flow

Applicant approaches Issuing/ Opening Bank with LC application form duly f illed and requests

Issuing Bank to issue a Letter of Credit in favor of Benef iciary.

Issuing Bank issues a Letter of Credit as per the application submitted by an Applicant

and sends it to the Advising Bank, which is located in Benef iciarys country, to formally

advise the LC to the benef iciary.

Advising Bank advises the LC to the Benef iciary.

Once Benef iciary receives the LC and if it suits his/ her requirements, he/ she prepares

the goods and hands over them to the carrier for dispatching to the Applicant.

He/ She then hands over the documents along with the Transport Document as per LC

to the Negotiating Bank to be forwarded to the Issuing Bank.

Issuing Bank reimburses the Negotiating Bank with the amount of the LC post

Negotiating Banks conf irmation that they have negotiated the documents in strictconformity of the LC terms. Negotiating Bank makes the payment to the Benef iciary.

Simultaneously, the Negotiating Bank forwards the documents to the Issuing Bank to be

released to the Applicant to claim the goods from the carrier.

Applicant reimburses the Issuing Bank for the amount, which it had paid to the

Negotiating Bank.

Issuing Bank releases all documents along with the titled Transport Documents to the

Applicant.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 18/42

13

3.4. Settlements under a Letter of Credit

All commercial letters of credit must clearly indicate whether they are payable by sight

payment, by deferred payment, by acceptance, or by negotiation. These are noted as formal

demands under the terms of the commercial letter of credit.

In a sight payment, the commercial letter of credit is payable when the benef iciary presents thecomplying documents and if the presentation takes place on or before the expiration of the

commercial letter of credit.

In a deferred payment, the commercial letter of credit is payable on a specif ied future date.

The benef iciary may present the complying documents at an earlier date, but the commercial

letter of credit is payable only on the specif ied future date.

An acceptance is a time draft drawn on, and accepted by, a banking institution, which promises

to honor the draft at a specif ied future date. The act of acceptance is without recourse as it is a

commitment to pay the face amount of the accepted draft.

Under negotiation, the negotiating bank, a third party negotiator, expedites payment to the

benef iciary upon the benef iciarys presentation of the complying documents to the negotiating

bank. The bank pays the benef iciary, normally at a discount of the face amount of the value of

the documents, and then presents the complying documents, including a sight or time draft, to

the issuing bank to receive full payment at sight or at a specif ied future date.

3.5. Types of Letter of Credit

Irrevocable

An irrevocable letter of credit can neither be amended nor cancelled without the agreement of

all parties to the credit. Under UCP500 all letters of credit are deemed to be irrevocable unless

otherwise stated. Here, the importer's bank gives a binding undertaking to the supplier

provided all the terms and conditions of the credit are fulf illed.

Unconfirmed

The advising bank forwards an unconf irmed letter of credit directly to the exporter without

adding its own undertaking to make payment or accept responsibility for payment at a future

date, but conf irming its authenticity.

Confirmed

A conf irmed letter of credit is one in which the advising bank, on the instructions of the issuing

bank, has added a conf irmation that payment will be made as long as compliant documents are

presented. This commitment holds even if the issuing bank or the buyer fails to make payment.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 19/42

14

The added security to the exporter of conf irmation needs to be considered in the context of the

standing of the issuing bank and the current political and economic state of the importer's

country. A bank will make an additional charge for conf irming a letter of credit. In many cases,

the conf irming bank is located in Benef iciarys country.

Conf irmation costs will vary according to the country involved, but for many countries

considered a high risk will be between 2%-8%. There also may be countries issuing letters of

credit, which banks do not wish to conf irm - they may already have enough exposure in that

market or not wish to expose themselves to that particular risk at all.

Standby Letters of Credit

A standby letter of credit is used as support where an alternat ive, less secure, method of

payment has been agreed. They are also used in the United States of America in place of bank

guarantees. Should the exporter fail to receive payment from the importer he may claim under

the standby letter of credit. Certain documents are likely to be required to obtain payment

including: the standby letter of credit itself; a sight draft for the amount due; a copy of the

unpaid invoice; proof of dispatch and a signed declaration from the benef iciary stating that

payment has not been received by the due date and therefore reimbursement is claimed by

letter of credit. The International Chamber of Commerce publishes rules for operating standby

letters of credit - ISP98 International Standby Practices.

Revolving Letter of Credit

The revolving credit is used for regular shipments of the same commodity to the same

importer. It can revolve in relation to time or value. If the credit is time revolving once utilised itis re-instated for further regular shipments until the credit is fully drawn. If the credit revolves

in relation to value once utilized and paid the value can be reinstated for further drawings. The

credit must state that it is a revolving letter of credit and it may revolve either automatically or

subject to certain provisions. Revolving letters of credit are useful to avoid the need for

repetitious arrangements for opening or amending letters of credit.

Transferable Letter of Credit

A transferable letter of credit is one in which the exporter has the right to request the paying,

or negotiating bank to make either part, or all, of the credit value available to one or more third

parties. This type of credit is useful for those acting as middlemen especially where there is a

need to f inance purchases from third party suppliers.

Back-to-Back Letter of Credit

A back-to-back letter of credit can be used as an alternative to the transferable letter of credit.

Rather than transferring the original letter of credit to the supplier, once the letter of credit is

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 20/42

15

received by the exporter from the opening bank, that letter of credit is used as security to

establish a second letter of credit drawn on the exporter in favor of his importer. Many banks

are reluctant to issue back-to-back letters of credit due to the level of risk to which they are

exposed, whereas a transferable credit will not expose them to higher risk than under the

original credit.

3.6. Advantages of Letter of Credit:

The benef iciary is assured of payment as long as it complies with the terms and

conditions of the letter of credit. The letter of credit identif ies which documents must

be presented and the data content of those documents. The credit risk is transferred

from the applicant to the issuing bank.

The benef iciary can en joy the advantage of mitigating the issuing banks country risk by

requiring that a bank in its own country conf irm the letter of credit. That bank then

takes on the country and commercial risk of the issuing bank and protects the

benef iciary.

The benef iciary minimizes collection time as the letter of credit accelerates payment of

the receivables.

The benef iciarys foreign exchange risk is eliminated with a letter of credit issued in the

currency of the benef iciarys country.

3.7. Risks involved in Letter of Credit.

Since all the parties involved in Letter of Credit deal with the documents and not with

the goods, the risk of Benef iciary not shipping goods as mentioned in the LC is stillpersists.

The Letter of Credit as a payment method is costlier than other methods of payment

such as Open Account or Collection

The Benef iciarys documents must comply with the terms and conditions of the Letter of

Credit for Issuing Bank to make the payment.

The Benef iciary is exposed to the Commercial risk on Issuing Bank, Political risk on the

Issuing Banks country and Foreign Exchange Risk in case of Usance Letter of Credits.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 21/42

16

3.8. 1. Account Party Beneficiary

The commercial credit functions as the method of payment in a sales contract between the

Account Party (the buyer) and the Benef iciary (the seller). In the course of negotiating this

sales contract, the Account Party and the Benef iciary agree to the terms and conditions underwhich the commercial credit will be issued. The following are basic issues which should be

resolved in these negotiations.

The maximum amount of drawings

All credits must include a maximum amount of liability, which usually is the purchase price of

the goods.

the expiration date for the credit

All credits must be of limited duration, although "evergreen clauses" may be used to

automatically renew credits.

The credit revocable or irrevocable

A revocable credit can be modif ied or rescinded by the Account Party at any time. Therefore, a

Benef iciary should insist that the credit be irrevocable (i.e. that the credit cannot be modif ied or

rescinded after issuance without the Benef iciary's approval.)

The Benef iciary present in order to receive payment under the credit

This is a critical issue. The Benef iciary will not be paid unless she produces each of these

documents. Thus, a Benef iciary should make every effort to keep the documents as simple as

possible. None of the documents should require the signature or approval of the Account Party

or the Account Party's agent. Further, to the extent possible, the Benef iciary should not agree

to the inclusion of foreign government documents because they may be diff icult to obtain in a

timely fashion.

The following is a short description of documents frequently required in commercial credits.

A Bill of Lading is a receipt that a common carrier gives to the seller for the goods that

the carrier will transport. It frequently serves as a document of title, giving the person

who possesses it ownership of the goods.

A Commercial Invoice is a bill prepared by the seller for submission to the buyer which

details all items bought, together with amounts owed.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 22/42

17

A Draft or bill of exchange is a negotiable instrument that is payable to the seller and

drawn on the issuing bank and/or the buyer. This document is prepared by the seller,

but is analogous to a check written from the buyer to the seller. Drafts can be either

"sight drafts" where the bank pays the full amount of the draft upon the seller's

presentation, or "time drafts" where the bank's obligation at the time of presentation is

merely to accept the draft for payment at a later date (e.g. 90 days after the seller'spresentation). Time drafts provide the buyer with short-term f inancing. Often, banks

will purchase their accepted time drafts at a discounted rate.

A Consular Document shows that the goods satisfy the relevant regulatory requirements

of the importing country.

An Insurance Certif icate shows that the Benef iciary obtained insurance for

transportation of the goods. (Appropriate only if the seller agrees to be responsible for

the insurance.)

An Inspection Certif icate shows that the goods have passed a quality inspection prior to

shipping. Either an independent third party or an agent of the buyer can perform the

inspection. However, if it is an agent of the buyer, the seller should recognize that the

buyer may block payment under the Credit until any dispute regarding the conformity of

the goods is resolved.

The Benef iciary present the documents required under the credit

The Benef iciary may f ind it diff icult to make a document presentation in a foreign country.

Therefore, the appropriate place for presentation may be the Issuing Bank's off ice in the

Benef iciary's country. If none exists, the credit may designate another bank (the Nominated

Bank) to serve as the place for presentation. I t is important to note that while the Nominated

Bank is authorized to act on behalf of the Issuing Bank to honor the credit obligation, the

Nominated Bank itself has no obligation that runs directly to the Benef iciary.

Should the credit be conf irmed by another bank

A commercial credit is only as good as the bank that issued it. A Benef iciary that is uncertain of

the creditworthiness of the Issuing Bank or uncertain of the political risks associated with the

country in which the Issuing Bank is located, should consider requesting that the credit be

conf irmed by another bank (the Conf irming Bank). The Conf irming Bank adds its obligation to

that of the Issuing Bank to honor the credit. A conf irmation from a strong bank in the

Benef iciary's country affords the Benef iciary a high degree of protection from the risk of non-

payment.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 23/42

18

3.8.2. Account Party -- Issuing Bank

The Account Party applies with the Issuing Bank (typically the Account Party's own bank) for a

commercial credit that satisf ies the specif ications in the sales contract. The Issuing Bank examines the Account Party's credit in the same manner as it would for any loan application,

and decides whether to issue the credit. Assuming the bank decides to issue the credit in the

form requested, the Account Party enters into a reimbursement agreement with the Issuing

Bank.

If and when the Issuing Bank ultimately pays money under the credit, it will seek

reimbursement from the Account Party. n exchange, the Issuing Bank will forward the bill of

lading and other relevant documents to the Account Party. This will enable the Account Party

to claim the goods from the independent carrier.

3.8.3. Issuing Bank Beneficiary

Issuing Bank Advises Benef iciary that the Credit is open. The Issuing Bank advises the

Benef iciary that the credit is open in its favor. The letter in which the Issuing Bank

provides this advice is literally the "letter of credit." It specif ies the terms and

conditions under which the credit operates.

As soon as the Benef iciary receives the credit, she should review it to ensure that it is consistent

with the terms and conditions in the underlying sales contract (or any amendments to the sales

contract). The Benef iciary should promptly contact the Issuing Bank and the Account Party if

there are any errors in the credit.

Benef iciary Performs in Accordance with the Terms in the Credit. The Benef iciary will

only be paid under the credit if she makes a documentary presentation that conforms to

the time, place and manner requirements in the commercial credit.

Time: The Benef iciary must meet at least two deadlines.

Date of Expiry: The documents must be presented on or before the date of expiry

specif ied in the credit. The Benef iciary, however, should make her presentation well

ahead of this date of expiration. Banks have a reasonable period of time (not to exceed

7 days) to examine a presentation, and decide whether the documents conform to the

credit. A Benef iciary who has made her presentation less than 7 days before the date of expiry may not have an opportunity to cure any defects.

Expiration of Transport Documents: Unless the credit specif ies otherwise, banks will not

accept bills of lading and other transport documents which are not presented within 21

days after the date of shipment.

Manner: It is critical that the Benef iciary present all the documents specif ied in the

credit in a form that complies with the requirements in the credit. Banks traditionally

apply a high standard, known as the strict compliance rule, for determining whether

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 24/42

19

documents comply with the credit. If the documents (especially the commercial

invoice) vary in any respect, the bank may re ject the presentation.

In one case, the credit described the goods in the underlying contract as "100% Acrylic Yarn."

The bank denied payment because the Benef iciary's invoice described the goods as "Imported

Acrylic Yarn." The Benef iciary sued, but the court ultimately held in favor of the bank, statingthat the invoice did not "strictly comply" with the requirements of the credit. Curtails North

America, Inc. v. North Carolina National Bank, 528 F. 2d 802 (4th Cir. 1975).

At its discretion, the Issuing Bank may ask the Account Party to waive any discrepancies

between the document presentation and the credit. However, a Benef iciary should not rely on

the generosity of the Issuing Bank and Account Party to accept non-conforming presentations.

Place: The Benef iciary must make her document presentation at the place specif ied in

the credit. Note that if the credit identif ies a Nominated Bank as the place of

presentation, and the Nominated Bank refuses to honor, the Benef iciary may be

required to make its presentation directly to the Issuing Bank.

Issuing Bank's Duty to Honor if Presentation Conforms to Credit: n determining

whether to honor drafts under the credit, the Issuing Bank does not examine the good,

or otherwise consider whether the Benef iciary has complied with the underlying

contract. The Issuing Bank focuses on the documents. If the documents comply with

the credit, and are not fraudulent, the Issuing Bank must honor the Benef iciary's drafts.

This separation between the commercial credit and the

Underlying contract is called the independence principle.

"Honor" means different actions depending on the Issuing Bank's obligations under the credit.If the credit calls for a sight draft, the Issuing Bank will honor by paying the draft promptly. If

the credit calls for a time draft, the Issuing Bank will honor by accepting (i.e. signing) the draft

promptly, and paying it upon maturity. Benef iciaries often sell accepted time drafts to Issuing

Banks at a discounted rate immediately after acceptance.

3.9. Functions of a Commercial Credit

A commercial credit has several basic functions. It is important to note, however, that the

parties can modify or change these basic functions to tailor the credit to their own needs.

Prompt Payment: The Benef iciary is paid promptly after shipping her goods. Without

the credit, the Benef iciary would have to require pre-payment for the goods or would

have to wait until after the Account Party received the goods.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 25/42

20

Substituting Credit: The Benef iciary may be reluctant to sell on open account if it does

not know enough about the credit worthiness of the Account Party. The credit helps to

overcome the Benef iciary's reluctance to do business with the Account Party.

Shifting Litigation Costs: Every sales contract carries a risk of a dispute concerning

whether the goods conform to the contract. If the method of payment is an open

account, the seller most likely will bear the cost of litigating that dispute without thepurchase price. A commercial credit re-allocates this cost to the buyer, because the

seller receives the purchase price promptly when he presents conforming documents to

the Issuing Bank.

Shifting the Forum: The holder of the purchase money has little incentive to initiate

litigation. Since the commercial credit places the purchase money in the hands of the

seller, the buyer will likely need to pursue the purchase money by entering the forum of

the seller.

3.10. Back to Back Letter of Credit (LC s)

3.10.1. General

The branch may open back-to-back import LCs against export LCs received by export oriented

industrial units operating under the bonded warehouse system, subject to observance of

domestic value addition requirement (stated in terms of permissible limit of CFR value of

imported inputs as percentage of FOB export value of output) prescribed by the Ministry of

Commerce from time to time.

3.10.2. Opening of Back-to-back Import LCs

In addition to the general instructions in the foregoing sections, the following instructions

should be complied with while opening back-to-back import LCs:

Only recognized export oriented industrial units operating under bonded warehouse

system will be allowed the back-to-back LC facility. The unit requesting this facility

should possess valid registration with the CCI&E and valid bonded warehouse license.

The master export LC (against which opening of back-to-back LC is requested) should

have validity period adequate to cover the time needed for import of inputs,

manufactures of merchandise, and shipment to the consignee.

The back-to-back LC value shall not exceed the admissible percentage of net FOB value

of the relative master export LC (as per prescribed value addition requirement). For

computation of net FOB value of a master export LC, the freight charge, insurance cost

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 26/42

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 27/42

22

goods in the bonded warehouse. A copy of the letter to NBR reporting the export failure should

be submitted to Bangladesh Bank along with the application for post facto approval of

remittance towards back-to-back import payment.

Also, all applications for post facto approval of such remittance in the event of export failure

and short realisation/non-realisation of export proceeds should be accompanied by theexchange control copy of the relative Bill of Entry evidencing actual receipt of the back-to-back

imports. The branch should maintain effective watch on the stock of inputs procured under the

back-to-back arrangement and of the f inished products made therewith. Any indication of

illegal disposal of stocks from the bond coming to the knowledge of the branch should

immediately be reported to the concerned commissioner of Customs and NBR.

3.10.4. Back-to-Back LC

Under this arrangement opening an inland or overseas LC on Back-to-Back basis on the request

of the benef iciary of an Irrevocable Letter of Credit received from the foreign buyer f inances

export trade. The benef iciary is normally a middleman who does not manufacture the goods to

be exported under the credit. This back-to-back LC is opened by the bank in favor of the actual

manufacturer or producer of the goods on the strength of the original foreign LC. A lien is

created on the original export LC as security. Export of jute goods and ready-made garments

from Bangladesh are f inanced under this type of LC. The actual supplier of the goods effects the

shipment on behalf of the benef iciary of original LC and submits the shipping documents to the

bank that opened the Inland LC for payment. The letters of credit opened in Bangladesh for

import of inputs for export of RMG are known popularly as back-to-back letter of credit. Strictly

speaking these are not back-to-back letter of credit but are in fact separate letters of credit, not

different from other ordinary letters of credit.

Under the back-to-back letter of credit of the ordinary type some of the documents, such as

drafts, invoice etc. are replaced by a fresh set of corresponding documents prepared by the

benef iciary of the original foreign LC, who submits his own drat and invoice, etc. for the full

amount of original LC for negotiation. The local bank negotiates the documents submitted by

the benef iciary of the foreign LC and makes payment of the bill drawn against the Inland LC. In

this case also the bank may sometimes need to insist on collateral securities on the merits of

the cases.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 28/42

23

The back to back LC must conform to the terms and conditions of the original foreign LC with

the following exceptions:

The name of the actual supplier is substituted by that that of the benef iciary.

The amount of LC should be somewhat smaller than the original LC, to cover the prof it

margin and other expenses incurred by the original benef iciary.

The period of validity for shipment and negotiation should be a few days earlier than

the expiry date of the original LC.

3.10.5. Advance against Red Clause Letter of Credit (LC)

Under this facility, which is not commonly used in Bangladesh, the LC opening bank authorizes

the exporters bank (negotiating bank under LC) to make advances to the exporter (benef iciary

of LC) prior to shipment. This special arrangement is intended to enable the exporter to procure

the goods and execute the order of the fore ign buyer. It presupposes a strong commercial

relation between the buyer and the seller. The advance is liquidated against the export bills

negotiated under the LC. This clause in the LC authorizing the negotiating bank to make

advance to the benef iciary of the LC is written or typed in red ink. It gives the name Red Clause

LC. This advance is made at the risk of LC opening bank and is restricted to the amount

authorized under the red clause.

Before disbursement of the advance all necessary documents including an undertaking, must

be obtained from the benef iciary of the LC (exporter) in conformity with the terms and

conditions of the LC and Red Clause.

3.10.6. Reshipment Investment facilities

Credit worthiness of the exporter should be properly assessed by preparing credit report in the

Banks prescribed perform. Past export performance and behavior of the exporter should be

verif ied from the banks records and f inancial statements. Similarly, credit worthiness and

solvency of the foreign buyer should also be verif ied through foreign correspondents. Period for

which the investment is sanctioned should be clearly mentioned in the sanction letter.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 29/42

24

Charge documents as well as any other documents as mentioned in the sanction letter should

be obtained and got properly executed by the borrower. The banks legal adviser should be

asked, if necessary, to vet the memorandum of deposit under equitable mortgage.

Export documents should be carefully scrutinized before negotiation of export bills. If the

export bill is negotiated under LC, it should be ensured that all its terms and conditions have

been fully complied with.

The LC should be from our correspondent bank or a reputable foreign bank whose status

should be verif ied. The LC must be irrevocable (preferably conf irmed) and unrestricted. The

original LC should remain deposited with the bank and a lien mark should be given on it. But

before marking lien the LC terms should be thoroughly scrutinized to see that no clause

detrimental to the banks interest or contrary to existing exchange control and regulation has

been incorporated in it.

The date of expiry of LC should be properly recorded in the Register. No drawings should be

allowed after the expiry of the credit unless extended. If shipment could not be made within

the date stipulated in the LC, the advance should be called back.

If the shipment is covered by policies issued by Sadharan Bima Corporation under the Export

credit guarantee scheme, the related policy should be obtained in favor of the bank. It should

also be ensured that the exporter/bank fulf ils all the terms and conditions of the Insurance

Policy.

3.10.7. Foreign Back-to-Back Letter of Credit

The Government of Bangladesh has devised a special procedure under which the export

oriented garment units are allowed to import their inputs free of duty under the bonded

warehouse arrangement. Back-to-back letter of credit, in essence, is used to import the inputs

generally on credit terms up to 180 days on the strength of the foreign LC received from the

overseas buyers.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 30/42

25

3.11. Formalities & Procedure

For opening back-to-back LC for readymade garment industries engaged in export the branches

should follow the following guidelines meticulously:

The industry applying for opening the LC should be recognized by the Textile Division of the

Ministry of Textiles as an export oriented readymade garment industry and possesses a valid

Bonded Warehouse License.

For new customers, the branch should satisfy itself, if necessary from the Credit Information

Bureau of Bangladesh Bank, that they have no outstanding liability with any other bank.

The irrevocable export LC, on the strength of which the back-to-back LC is desired to be

opened, should be from a f irst class internationally reputed bank. The LC should conform to the

Uniforms Customs and Practices for Documentary Credit--ICC Publication (Brochure No. 500).

The branch should ascertain whether there is any quota restriction for the item of export. In

case of quota restriction, branch shall ensure that the party has obtained quota

allocation/license from EPB.

Finally the branch should satisfy itself that the industry has organizational and necessary

logistics to fulf ill the export order within the stipulated period.

The import LC will be opened to the extent prescribed by the government from time to time for

knit items and woven/ jacket on the basis of value addition. For computation of FOB value,

freight charges, insurance and commission involved in shipment of the merchandise under

export LC must be deducted. If the freight is not shown separately, a certif icate from the

shipping company or the shipping agent should be obtained.

The import order for fabrics should clearly describe the fabrics, and details as composition of

the fabrics, stripe, checks, prints, solid (white or dyed) yarn count, length flannel, shirting,

poplin, drill, twill etc. should be inserted in the LC. These descriptions should also be mentioned

in the LC. The LC should provide for submission of packing list showing the gross and net weight

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 31/42

26

of each bale and carton or crate or wooden boxes. These descriptions are necessary to ensure

that the fabrics imported are actually required to meet the export order.

3.12. In land Back-to-back Letter of Credit (LC)

Readymade garment units under bonded warehouse system may open inland back-to-back LC

against export LC in favor of local manufacturer-cum-supplier of fabrics and accessories. Banks

may open inland back-to-back LC on account of local manufacturers-cum-supplier up to the

extent of the net FOB value of the export LC for import of cotton yarn, dyes, chemicals, sizing

materials etc as may be permitted by the government.

3.12.1. Documents Required for Opening of Back-to-back LCs

LC Authorization Form duly f illed in and signed;

LC application and agreement form duly stamped and signed;

IMP Form;

Performa Invoice;

Insurance Cover Note (from the port of shipment to the Bonded Warehouse) and money

receipt.

3.12.2. Additional Documents

Valid membership certif icate from the concerned Chamber of Commerce & Industry or

from the concerned Trade Association as per provision of the Import Policy.

Valid IRC/ERC

Valid Bonded Warehouse License

3.12.3. Charge Documents

Besides other documents, the following charge documents duly stamped should be obtained

prior to disbursement:

Demand Promissory Note

Letter of Arrangement

Letter of Lien for Packing Credit (on special adhesive stamp)

For Packing Credit ---Letter of Disbursement

For Export Cash Credit--Letter of Continuity

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 32/42

27

Bai Salaam Agreement

3.12.4. Payment of Back-to-back LC, and Adjustment of Investment facilities

On manufacturing the garments is exported and the party submits the related shipping

documents to the bank for negotiation / collection. After receipt of the documents, the same is

duly scrutinized with the respective export LC and if found drawn strictly in conformity with LC

terms and conditions up to 20% of the documents value is negotiated if requested by the party.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 33/42

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 34/42

29

4.1. SWOT Analysis

Strengths

The Bank has been rated by CRAB Single a Two (A2) in terms of long term lending.

The banks asset portfolio consists of above 60% in long term lending.

The Banks Loan disbursement rate is growing largely, suggesting its high growth in

lending to deposit ratio (currently 79.4%).

The team of Letter of Credit Department are skilled enough to maintain all the

circumstance and proper paperwork related to the total procedure of LC

The Correspondents both National and International are strongly attached.

Weaknesses

Internal communication system procedural equipments are not well developed.

Net Interest Margin on the decline.

Due to favoritism often LC department face documentation problem.

Opportunities

The bank should focus on expanding its loan syndication and pro ject f inancing

business bigger pro jects.

Improving capital market conditions and developing equity culture should help the

bank to improve its fee-based revenue by further developing its existing investment

management and advisory business.

Threats

There is intense competition in the local market, not only from the local banks but

also from the foreign banks.

The lack of concentrate on equipment development can be a reason of future

backward.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 35/42

30

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 36/42

31

4.2. My Understanding:

While working with the company Ive come up with the following understandings that-

Paper work is must for Back to Back LC. Due to the proper documentation every year defaulters

are increasing rapidly. A proper documentation with full phase having fair evaluation can bring

back faith to the bank as well as the consistent clients of the bank.

Followings the rules and regulation can also play a vital role for the bank though in some cases

its very diff icult to maintain the rules in the corporate dealings but above all rules and

regulations should be managed in a proper manner.

While working here I came to understand that dealing client especially in the LC department is

not an easy task for this though each of the staffs are very sincere about their activities but they

cannot do it properly due to the work pressure.

4.3. Findings

AB Bank is one of the recognized banks in Bangladesh banking sector and its

accomplishing its activities in LC sector for a long time. Though Ive worked in the

LC department of this bank I observed the following f indings-

y In the department Fax is one of the key instruments to maintain LC activities but in most

cases I found it is out of service which is unexpected.

y Clients from different corporate sector are coming for opening LC without having proper

documentation and also not that much respective about the law.

y Staffs here are so busy that they cannot cooperate as they should with the clients.

y As a bank ABBL does have that suff icient support to the client as well as its clients which

is also unexpected.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 37/42

32

4.4. Recommendations

With my little experience in the bank with vast and complex banking system, it is very diff icult

for me to recommend. I have observed some shortcomings regarding operational activities of

the bank. On the basis of my observation I would like to recommend the following points:

y Though the performance of L/c is good, but their employees are not well trained. The

department needs to recruit expert human resources to provide good customer service,

which will bring effectiveness of the banks operation.

y The employees are given deposit target, which creates extra pressure to them for that

reason they cannot freely provide customer service. They had to spend some time to f ill

up their target. If the bank can reduce the pressure then they could be able to provide

good service.

y In many cases, the foreign banks choose for a conf irmation from other foreign banks,

which is dishonor for the local bank. It proves the poor f inancial condition of our

country. Bank should try to improve this situation.

y AB Bank ltd should organize various seminars and symposium so that both national and

international people can be more familiar.y To provide quality service to the customer, it is necessary to have a trained team of an

organization or an institution. For this reason the bank should recruit fresher, bright

energetic persons.

y One of the business strategies is promotion. Successful business depends on how they

can promote their products or services to the customer. In this connection to improve

the business status bank should introduce more promotional programs.

y AB needs more specialized personnel in Foreign Exchange department.

y International communication is weaker in AB Bank.

y More Training on Foreign Exchange is necessary for the AB Bank off icials.

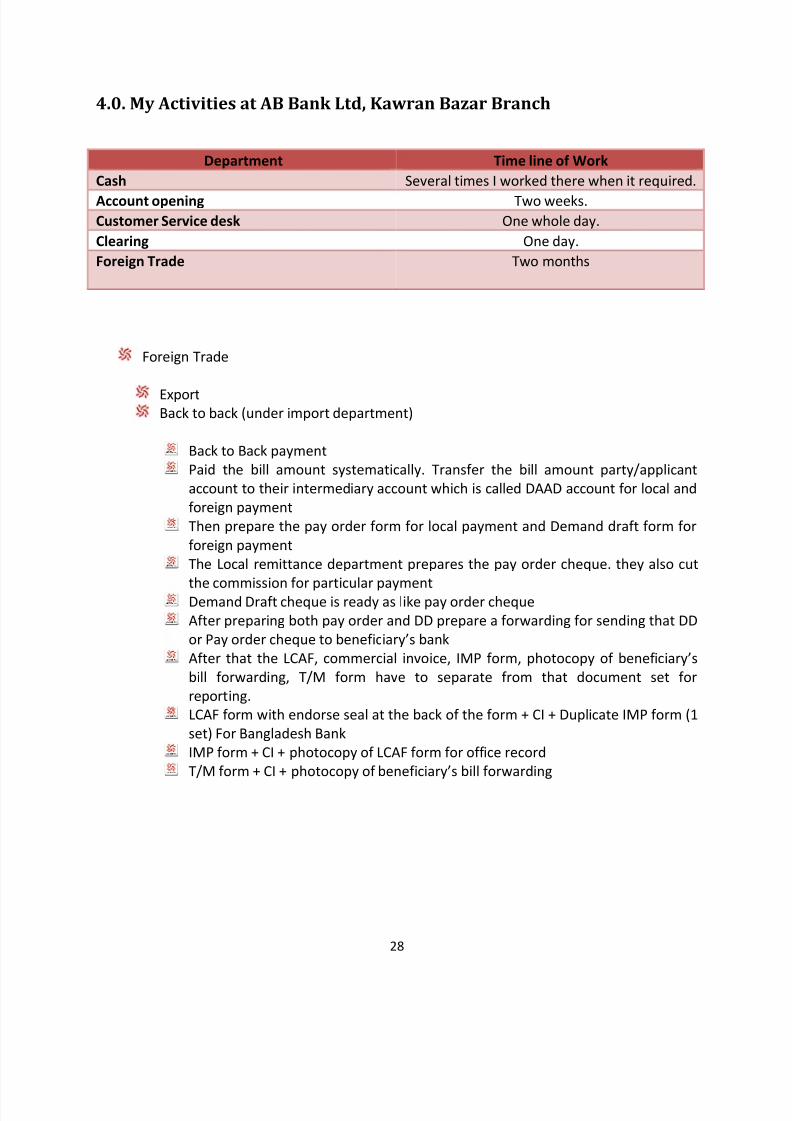

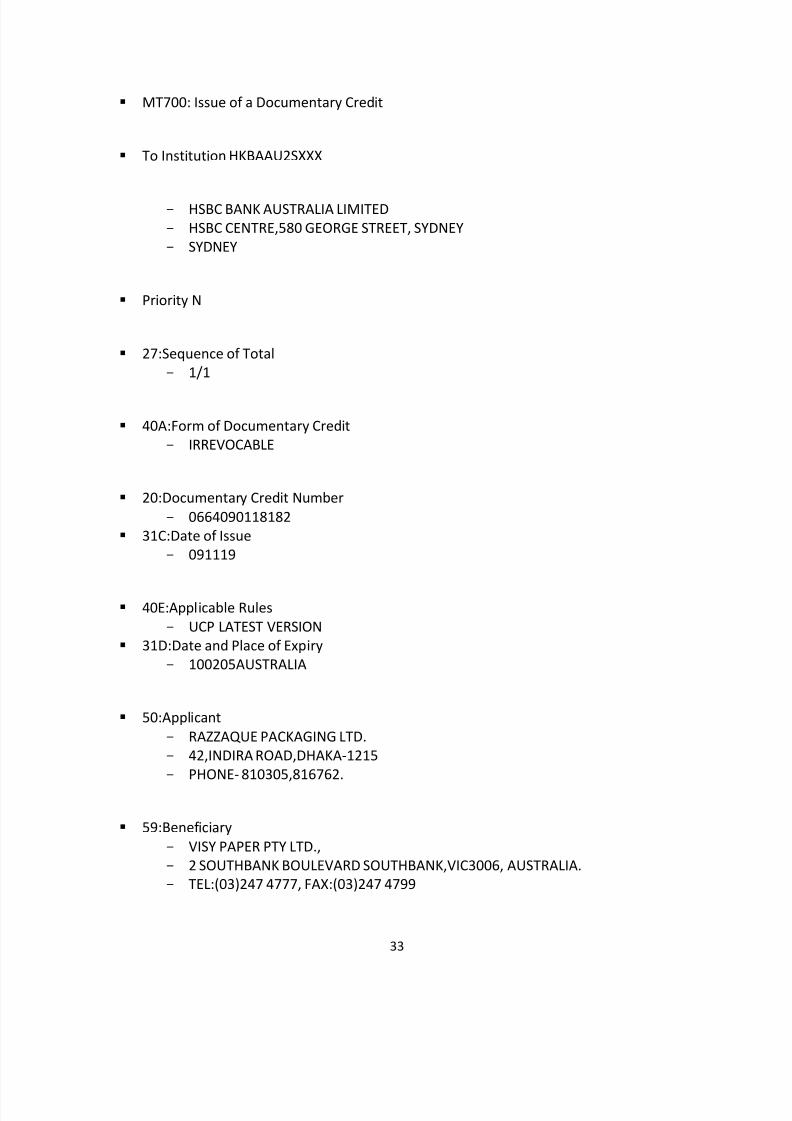

5.0. Case Study on a practical Back-to-Back L/C

In internship period I used to work in L/C department. Among many L/Cs one of my work I have

showed one of that L/C.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 38/42

33

MT700: Issue of a Documentary Credit

To Institution HKBAAU2SXXX

- HSBC BANK AUSTRALIA LIMITED

- HSBC CENTRE,580 GEORGE STREET, SYDNEY

- SYDNEY

Priority N

27:Sequence of Total

- 1/1

40A:Form of Documentary Credit

- IRREVOCABLE

20:Documentary Credit Number

- 0664090118182

31C:Date of Issue

- 091119

40E:Applicable Rules

- UCP LATEST VERSION

31D:Date and Place of Expiry

- 100205AUSTRALIA

50:Applicant

- RAZZAQUE PACKAGING LTD.

- 42,INDIRA ROAD,DHAKA-1215

- PHONE- 810305,816762.

59:Benef iciary

- VISY PAPER PTY LTD.,

- 2 SOUTHBANK BOULEVARD SOUTHBANK,VIC3006, AUSTRALIA.

- TEL:(03)247 4777, FAX:(03)247 4799

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 39/42

34

32B:Currency Code, Amount

- USD14305,00

39A:Percentage

- 10/10

- 41D:Available With ... By ...- Any bank in AUSTRALIA

- BY NEGOTIATION

42C:Drafts At ...

- SIGHT

42A:Drawee

- ABBLBDDH002

- AB BANK LIMITED

- KARWAN BAZAR BRANCH

- 102, KAZI NAZRUL ISLAM AVENUE

- DHAKA

43P:Partial Shipments

- ALLOWED

43T: Transhipment

- ALLOWED

44A:Place of Taking in Charge/Dispatch from.../Place of Receipt

- ANY SEA PORT OF AUSTRALIA

44B:Place of Final Destination/For Transportation to.../Place of Delivery- CHITTAGONG SEA PORT, BANGLADESH ON CFR BASIS.

44C:Latest Date of Shipment

- 100120

45A: Description of Goods and/or Services

- +KRAKT LINER PAPER- 270 GSM (K270X) 17 MT AT THE RATE OF USD 565.00 PER

MT AND MEDIUM PAPER- 180 GSM (M180) 10 MT AT THE RATE OF USD 470.00

PER MT. QUANTITY, QUALITY, DESCRIPTION OF GOODS, UNIT PRICE AND ALL

OTHER DETAILS AS PER PROFORMA INVOICE NO. VP/FVL-172/09 DATED

14.11.2009.

46A: Documents Required

- + A CERTIFICATE REGARDING COUNTRY OF ORIGIN MUST BE ISSUED/CERTIFIED

BY THE GOVERNMENT APPROVED AUTHORITY/ORGANISATION OF THE

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 40/42

35

EXPORTER'S COUNTRY AND MUST ACCOMPANY THE ORIGINAL SHIPPING

DOCUMENTS.

- + BENEFICIARY'S AT SIGHT DRAFT (S) IN DUPLICATE DRWAN ON OURSELVES

BEARING THE CLAUSE DRAWN UNDER AB BANK LIMITED, KARWAN BAZAR

BRANCH, DHAKA, BANGLADESH L/C NO. AND DATE.- + BENEFICIARY'S SIGNED COMMERCIAL INVOICE IN OCTUPLICATE CERTIFYING

MERCHANDISE TO BE OF AUSTRALIA ORIGIN AND INDICATING THAT THE GOODS

ARE BEING IMPORTED UNDER I.R.C.NO. BA-115229, LCAF NO.12423, H.S. CODE

NO. 4804.11.00. AND 4805.11.00.

- + DETAILED PACKING LIST IN TRIPLICATE SHOWING GROSS AND NETWEIGHT.

- + ONE FULL SET OF CLEAN SHIPPED ON BOARD OCEAN BILL OF LADING

SHOWING FREIGHT PREPAID DRAWN TO THE ORDER OF AB BANK LIMITED,

KARWAN BAZAR BRANCH, DHAKA, BANGLADESH AND MARKED NOTIFY

APPLICANTS OF THE CREDIT BEARING OUR LETTER OF CREDIT NO. AND DATE.

- + INSURANCE COVERED IN BANGLADESH. CERTIFICATE OF SHIPMENT TO BE SENT

DIRECTLY TO AGRANI INSURANCE COMPANY LTD, DILKUSHA BRANCH, 44

DILKUSHA C/A (6TH FLOOR), DHAKA-1000, BANGLADESH AND TO THE OPENER

BY COURIER /FAX IMMEDIATELY AFTER SHIPMENT QUOTING MARINE COVER

NOTE NO. AICL/DK/MC-325/11/2009 DATED 15.11.2009 AND THIS CREDIT

NUMBER A COPY OF WHICH SUPPORTED BY RELEVANT ORIGINAL COURIER

RECEIPT AS EVIDENCE TO THIS EFFECT MUST ACCOMPANY THE ORIGINAL

SHIPPING DOCUMENTS.

- + INVOICE TO BE DRAWN ON CFR BASIS AND ALL SHIPPING DOCUMENTS MUST

BEAR L/C NUMBER AND DATE.

47A: Additional Conditions

- + BENEFICIARY MUST CERTIFY ON THE INVOICES THAT GOODS SHIPPED ARE

STRICTLY IN ACCORDANCE WITH THE IPROFORMA INVOICE NO. VP/FVL-172/09

DATED 14.11.2009.

- +BENEFICIARY SHOULD SEND A MESSAGE THROUGH FAX NO.88-02-9128545 TO

L/C OPENING BANK WITHIN 72 HOURS FROM THE DATE OF SHIPMENT ADVISING

THE DATE OF SHIPPMENT, NAME OF VESSEL, And AMOUNT OF BILL TO BE

DRAWN AGAINST THE SHIPPMENT AND L/C NUMBER AND A COPY OF THIS FAX

MESSAGE SHOULD ACCOMPANY THE SHIPPING DOCUMENTS.

- +PACKING: EXPORT STANDARD PACKING.

- + ONE FULL SET OF SHIPPING DOCUMENT (NON NEGOTIABLE) SHOULD BE SENT

TO THE L/C APPLICANT BY ANY COURIER WITHIN 07 DAYS FROM THE DATE OF

SHIPMENT. BENEFICIARY'S STATEMENT TO THIS EFFECTSUPPORTED BY

RELEVANT ORIGINAL RECEIPT IS REQUIRED FOR NEGOTIATION.

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 41/42

36

- +ALL SHIPING MARKS MUST BE LABEL PRINTED ON THE BOTH CORES SIDE OF

THE ROLLS.

- +A DISCREPANT DOCUMENTS FEES OF USD 100.00 WILL BE DEDUCTED FROM

DRAWING IF DOCUMENTS ARE PRESENTED WITH DISCREPANCIES.

- +THIS L/C IS OPENED UNDER BOND.

- +TOLERANCE OF 10 PERCENT PLUS/MINUS ON BOTH QUANTITY AND AMOUNT

TO BE ALLOWED.

- +THE ALTERNATE NUMBER OF THIS DOCUMENTARY CREDIT FOR OUR CENTRAL

BANK REPORTING PURPOSES IS 066409010532. ALL DOCUMENTS THAT ARE

REQUIRED TO BEAR THE L/C NUMBER WILL HAVE TO MENTION BOTH

066409010532 AND 0664090118182. ALL CORRESPONDENCES FROM

NEGOTIATING/CONFIRMING BANK SHOULD QUOTE BOTH 066409010532 AND

0664090118182.

71B: Charges

- ALL EXPENSES OUT SIDE BANGLADESH ARE ON BENEFICIARY'S ACCOUNT.

48: Period for Presentation

- DOCUMENTS TO BE PRESENTED WITHIN 15 DAYS FROM THE DATE OF SHIPMENT

BUT WITHIN THE VALIDITY OF THE CREDIT.

49: Conf irmation Instructions

- WITHOUT

78: Instructions to the Paying/Accepting/Negotiating Bank

- + UPON RECEIPT OF DOCUMENTS COMPLYING WITH THE TERMS AND

CONDITIONS OF THE CREDIT WE SHALL EFFECT PAYMENT AS PER

NOMINATED/COLLECTING BANK INSTRUCTION

- + ALL DOCUMENTS WILL BE FORWARED TO US BY SEPARATE COURIER/ AIR MAIL

TO AB BANK LIMITED, KARWAN BAZAR BRANCH, DHAKA, BANGLADESH.

- + NEGOTIATING BANK MUST CERTIFY ON THEIR COVERING SCHEDULE THAT

EACHDRAWING HAS BEEN ENDORSED ON REVERSE OF THE CREDIT AND ALSO

CERTIFY THAT THE TERMS AND CONDITIONS OF THE CREDIT HAVE BEEN DULY

COMPLIED WITH.

57A:'Advise Through Bank

- ANZBAU3MXXX

- AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED

- 570 CHURCH STREET VICTORIA MELBOURNE MELBOURNE 301

72: Sender to Receiver Information

8/6/2019 Mishu Final Report

http://slidepdf.com/reader/full/mishu-final-report 42/42

- + THIS CREDIT IS SUBJECT TO THE UNIFORM CUSTOMS AND PRACTICE FOR

DOCUMENTARY CREDITS, ICC PUBLICATION LATEST VERSION

6.0. Conclusion

A back-to-back letter of credit can be used as an alternative to the transferable letter of credit.

Rather than transferring the original letter of credit to the supplier, once the letter of credit is

received by the exporter from the opening bank, that letter of credit is used as security to

establish a second letter of credit drawn on the exporter in favor of his importer. Many banks

are reluctant to issue back-to-back letters of credit due to the level of risk to which they are

exposed, whereas a transferable credit will not expose them to higher risk than under the

original credit. That was all about the Back to back LC but the most important thing is to handle

the overall procedure with proper care and for this bank like ABBL should be more active to

improve its off ice maintenance by improving its staffs and instruments. Moreover the clients

also be patient and should show its respect to the rules and regulations set by the central bank

and for this the bank can arrange some motivational programme for the clients and at the same

time can train its staffs by providing some effective clients behavior. And f inally the govt. should

be caring about the term because its all about money inflow in the country which is the most

important thing than any other issue. If they come forward and empower the banking sector by

imposing a bit easy rules to LC than export and import will be more earning issue for the

countrys economy I believe.

7.0. Reference

Ali Ashraf Kazi,(2010, pers. comm. 15 December).

2010, AB Bank Manual, AB Bank Ltd. Bangladesh, Dhaka.

2010, Foreign Exchange Guide Line, Bangladesh Bank, Dhaka

Ministry of Commerce, 2009-2012, Import Policy Order.