Embed Size (px)

Citation preview

Oil & Gas Markets:Risks and Opportunities

India Energy ConferenceCEO Forum

3 October, 2008New Delhi

R S SharmaChairman & Managing Director, ONGC

Chairman, ONGC Group of Companies

With 16% of global population;

0.5% of world’s Petroleum reserve & 6.7 % of

world’s Coal reserve; with a 8- 9% GDP growth

target and 4.5% CAGR (’97-’07) in primary

energy demand

the situation is pretty Challenging…

India: Energy ScenarioIndia: Energy Scenario

2361

1863

692

518404

322 311255 234 216

USA China Russia Japan India Canada Germany France SouthKorea

UK

India: Energy scenarioIndia: Energy scenario

• India: the 5th largest energy consumer– CAGR (1996-2006): 4.5% (global CAGR: 2.1%)– Per capita energy consumption to rise from 375 Kgoe in 2007 to about 1200 Kgoe in 2030

Source: BP Statistical Review 2008

Primary Energy Consumption (MTOE)

3.6% of total

Nuclear6%

Hydel6%

Gas24%

Oil35%

Coal29%

Energy BasketEnergy Basket

Source: BP Statistical Review 2008

World India*

• Gas consumption in India increased at a CAGR of 6.1% (Global: 2.6%), next only to China (13%) in last ten years (1997-2007)

Nuclear1%

Hydel7%

Gas9%

Oil32%

Coal51%

*India’s consumption based scenario excluding export

Source: BP Statistical Review 2008

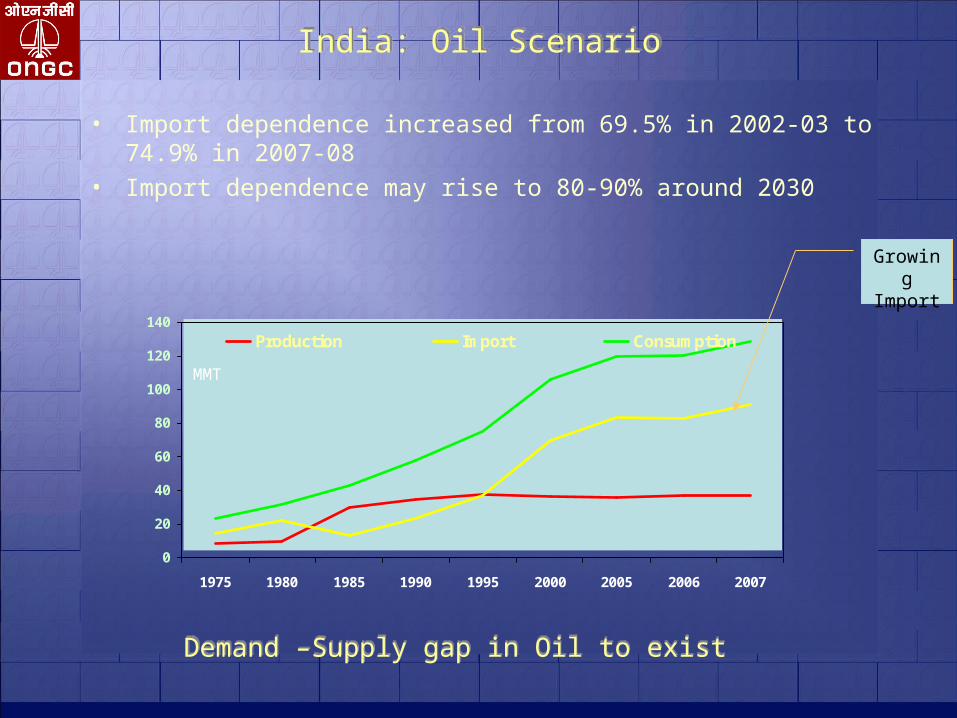

India: Oil ScenarioIndia: Oil Scenario

943

368

229129 126 113 108 102

USA China J apan India Russia Germany S.Korea Canada

• India’s oil consumption (2007) 128.5 Million Tonnes– the 4th largest consumer of Oil: 3.3% of total– Oil consumption increased at CAGR of 4 % (1997-2007) against

the world CAGR of 1.4%.

Oil Consumption (MMT)

*India’s consumption excluding export

India: Oil ScenarioIndia: Oil Scenario

• Import dependence increased from 69.5% in 2002-03 to 74.9% in 2007-08

• Import dependence may rise to 80-90% around 2030

0

20

40

60

80

100

120

140

1975 1980 1985 1990 1995 2000 2005 2006 2007

Production Import Consumption

Growing Import

Demand –Supply gap in Oil to existDemand –Supply gap in Oil to exist

MMT

Source: BP Statistical Review 2008

India: Gas ScenarioIndia: Gas Scenario

• Gas constitutes ~9% in Pry energy basket; likely to increase, thanks to Gas strikes at East coast

• Situation to improve by 2012. • Demand-supply gap to exist

0

5

10

15

20

25

30

35

40

1975 1980 1985 1990 1995 2000 2005 2006 2007

Production Import Consumption

MTOE

Growing Primary Energy demand … IndiaGrowing Primary Energy demand … India

0

500

1000

1500

2007* 2011 2016 2021 2026 2031

Coal Oil Natural Gas Hydro Nuclear

*Source: BP Statistical Review 2007 Projected figure Source: Integrated Energy Policy

• With development of East Coast, new & marginal fields of West coast, CBM, UCG, and likely trans-national gas trunk lines- the gas demand seems to be achievable

• For oil, though importer for over 25 years, considering the dramatic rise in volume demand, the balance of trade for oil is a critical issue

404MTOE

1633MTOE

CAGR= 6%

Gas CAGR= 7.9%

Oil CAGR= 5.2%

Risks & Opportunities:

(UPSTREAM)

Risks & Opportunities:

(UPSTREAM)

Indian Oil & Gas BusinessIndian Oil & Gas Business

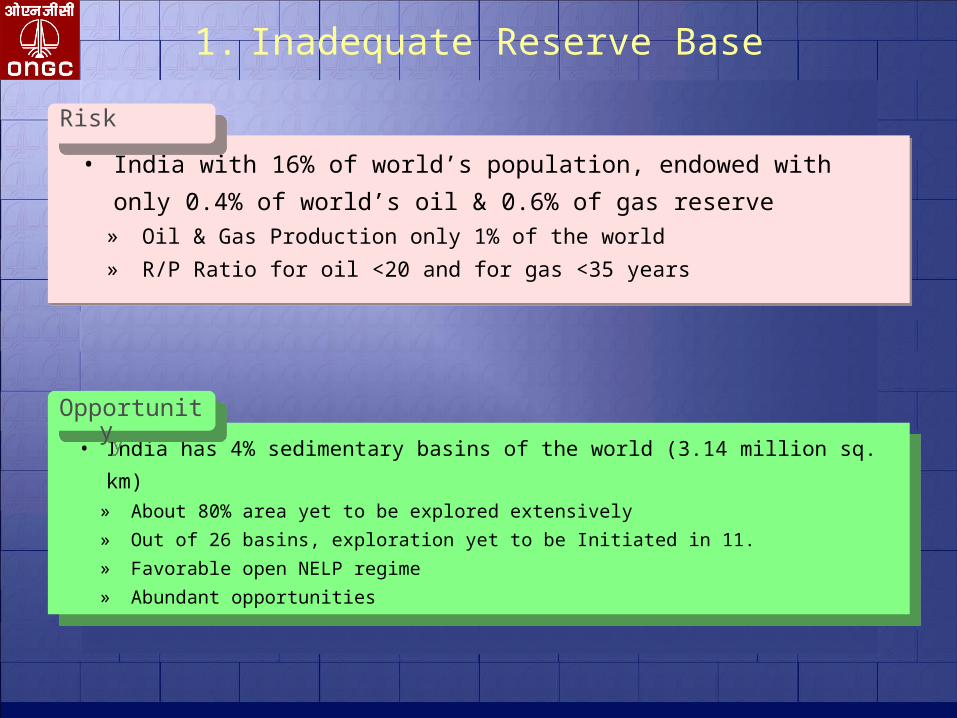

1. Inadequate Reserve Base

• India with 16% of world’s population, endowed with only 0.4% of

world’s oil & 0.6% of gas reserve» Oil & Gas Production only 1% of the world

» R/P Ratio for oil <20 and for gas <35 years

• India with 16% of world’s population, endowed with only 0.4% of

world’s oil & 0.6% of gas reserve» Oil & Gas Production only 1% of the world

» R/P Ratio for oil <20 and for gas <35 years

• India has 4% sedimentary basins of the world (3.14 million sq. km)» About 80% area yet to be explored extensively

» Out of 26 basins, exploration yet to be Initiated in 11.

» Favorable open NELP regime

» Abundant opportunities

• India has 4% sedimentary basins of the world (3.14 million sq. km)» About 80% area yet to be explored extensively

» Out of 26 basins, exploration yet to be Initiated in 11.

» Favorable open NELP regime

» Abundant opportunities

RiskRisk

OpportunityOpportunity

2. Depletion of Mature Fields

• All major producing fields are more than 30 years old

• Most of them have produced through their peaks» 80% of total indigenous production coming from such mature fields

» Pressure of almost all of these fields are depleting fast

» Cost-intensive IOR/ EOR processes required to keep them flowing

• All major producing fields are more than 30 years old

• Most of them have produced through their peaks» 80% of total indigenous production coming from such mature fields

» Pressure of almost all of these fields are depleting fast

» Cost-intensive IOR/ EOR processes required to keep them flowing

RiskRisk

• Established IOR/ EOR technologies to enhance recovery

• Fast track monetization of New & Marginal field to make up the

‘less’ from existing assets

• Looking for new source of energy like, CBM, UCG, Winds, Nuclear

etc.

• Established IOR/ EOR technologies to enhance recovery

• Fast track monetization of New & Marginal field to make up the

‘less’ from existing assets

• Looking for new source of energy like, CBM, UCG, Winds, Nuclear

etc.

OpportunityOpportunity

3. Growing Dependence on Imports

• Over dependence on oil & gas leading to import dependence from 70-85%

• 92% Import dependent on geo-politically sensitive Middle East and Africa» 37% of total M-East crude comes from Iraq & Iran

» About 45% of total African crude comes from volatile Nigeria

• Over dependence on oil & gas leading to import dependence from 70-85%

• 92% Import dependent on geo-politically sensitive Middle East and Africa» 37% of total M-East crude comes from Iraq & Iran

» About 45% of total African crude comes from volatile Nigeria

Region w ise India's oil import

73%

19%2%4%2%

M-East Africa FSU Asia Pac Latin Am

Source: PPAC

RiskRisk

4. Suitable & cost-effective technology

• Technology development lead time is long- but economic cycle often

short

• Less Focus on R&D- a global oil & gas industry phenomenon

• Unavailability of suitable technology at cost-effective price- threat to

realizing discovered assets» Deepwater development still at embryonic stage

» Gas hydrate not out of laboratory

» G&G accuracy still dependent on costly drilling

• Technology development lead time is long- but economic cycle often

short

• Less Focus on R&D- a global oil & gas industry phenomenon

• Unavailability of suitable technology at cost-effective price- threat to

realizing discovered assets» Deepwater development still at embryonic stage

» Gas hydrate not out of laboratory

» G&G accuracy still dependent on costly drilling

RiskRisk

• Rising affordability for investing in R&D, Technology acquisition and

assimilation» Globalization has increased the access to global technological developments

» Empowered policy might help in fast and direct access to latest technology

» Strong Indian Academia: Greater Industry-Academia synergy possible

• Rising affordability for investing in R&D, Technology acquisition and

assimilation» Globalization has increased the access to global technological developments

» Empowered policy might help in fast and direct access to latest technology

» Strong Indian Academia: Greater Industry-Academia synergy possible

OpportunityOpportunity

5. Technical Manpower Crunch

• Growing human capital deficit- most significant strategic threat

to the industry» Huge exodus to abroad, especially Middle East

» Less interest by young generation to pursue G&G

» Badly suffered NOCs

• Growing human capital deficit- most significant strategic threat

to the industry» Huge exodus to abroad, especially Middle East

» Less interest by young generation to pursue G&G

» Badly suffered NOCs

• Huge Young Population» More institutes like RGIPT, Bareilly

» Assurance of encouraging career and compensation

» Competitive compensations for NOCs

• Huge Young Population» More institutes like RGIPT, Bareilly

» Assurance of encouraging career and compensation

» Competitive compensations for NOCs

OpportunityOpportunity

RiskRisk

6. Procedural Constraints

• Procedural constraints affecting the process of Resource acquisition– Acquiring patented technology or single-owner technology; Hiring Drilling

rigs or FPSO; procuring Hi-tech equipments; acquiring Land…

– Time… the essence of decision making affected by regulations

» Deepwater drilling rig day-rate has increased 3-5 times in last four years

» Availability constrained in near future

• Regulation & less empowerment resulted in many lost-opportunities

for OVL

• Procedural constraints affecting the process of Resource acquisition– Acquiring patented technology or single-owner technology; Hiring Drilling

rigs or FPSO; procuring Hi-tech equipments; acquiring Land…

– Time… the essence of decision making affected by regulations

» Deepwater drilling rig day-rate has increased 3-5 times in last four years

» Availability constrained in near future

• Regulation & less empowerment resulted in many lost-opportunities

for OVL

RiskRisk

• Regulatory bodies may become facilitator through guidance » Making energy security a prime national agenda would remove many

hierarchical constrictions

» Coordination between MoEF, MoHA, MoF, MoP&NG, MoD etc

• More Empowerment of OVL essential for energy security» Time, secrecy & aggressive bidding- key factors in acquiring overseas assets

• Regulatory bodies may become facilitator through guidance » Making energy security a prime national agenda would remove many

hierarchical constrictions

» Coordination between MoEF, MoHA, MoF, MoP&NG, MoD etc

• More Empowerment of OVL essential for energy security» Time, secrecy & aggressive bidding- key factors in acquiring overseas assets

OpportunityOpportunity

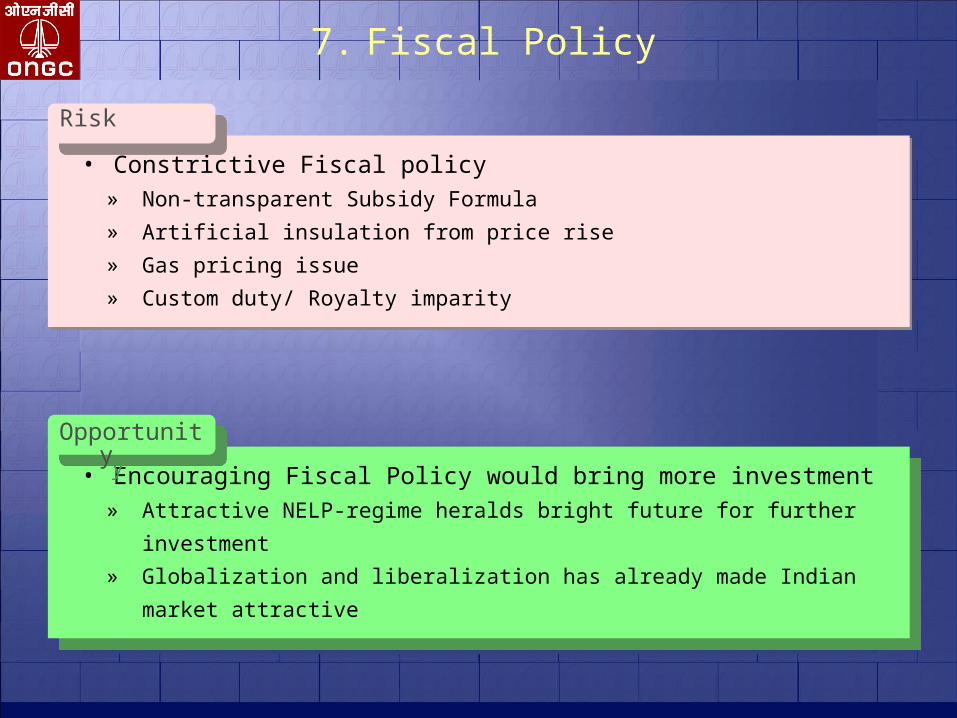

7. Fiscal Policy

• Constrictive Fiscal policy» Non-transparent Subsidy Formula

» Artificial insulation from price rise

» Gas pricing issue

» Custom duty/ Royalty imparity

• Constrictive Fiscal policy» Non-transparent Subsidy Formula

» Artificial insulation from price rise

» Gas pricing issue

» Custom duty/ Royalty imparity

RiskRisk

• Encouraging Fiscal Policy would bring more investment » Attractive NELP-regime heralds bright future for further investment

» Globalization and liberalization has already made Indian market

attractive

• Encouraging Fiscal Policy would bring more investment » Attractive NELP-regime heralds bright future for further investment

» Globalization and liberalization has already made Indian market

attractive

OpportunityOpportunity

8. Environmental legislation

• Over-activism or Adventurism regarding environmental issues may

pose a threat in near future» Drilling & exploration in forest lands/ river bed might be required in the

greater interest of energy security & growth

» A balance between conservation and energy generation might be needed

• Over-activism or Adventurism regarding environmental issues may

pose a threat in near future» Drilling & exploration in forest lands/ river bed might be required in the

greater interest of energy security & growth

» A balance between conservation and energy generation might be needed

RiskRisk

• Oil & Gas industry, by virtue of its resource, may play

even greater role » in Carbon emission control, afforestation and climate control

» in R&D for new and alternate source of energy

• Oil & Gas industry, by virtue of its resource, may play

even greater role » in Carbon emission control, afforestation and climate control

» in R&D for new and alternate source of energy

OpportunityOpportunity

Thank You Thank You