Embed Size (px)

Citation preview

OMC Card, Inc. and Consolidated Subsidiaries Consolidated Financial Statements for the Years Ended February 28, 2005 and February 29, 2004, and Independent Auditors' Report

OMC Card, Inc. and Consolidated Subsidiaries Consolidated Balance Sheets February 28, 2005 and February 29, 2004

Millions of Yen

Thousands ofU.S. Dollars

(Note 1) ASSETS 2005 2004 2005

Millions of Yen

Thousands ofU.S. Dollars

(Note 1) LIABILITIES AND STOCKHOLDERS' EQUITY 2005 2004 2005

CURRENT ASSETS:

Cash and cash equivalents ¥134,533 ¥ 107,465 $ 1,293,587 Marketable securities (Notes 4 and 10)

1,189

Operating receivables: Notes and accounts 199 Installment sales (Note 5) 117,839 134,262 1,133,067 Operating loans (Notes 5 and 6) 282,686 269,152 2,718,135 Deferred tax assets (Note 13) 21,595 19,615 207,644 Prepaid expenses and other current assets 33,279 46,603 319,990 Allowance for doubtful accounts

(28,368

) (22,755

) (272,769

)

Total current assets

561,564

555,730

5,399,654

PROPERTY AND EQUIPMENT:

Buildings and structures

4,267 4,469 41,029

Equipment

524 522 5,038 Land 8,164 8,250 78,500 Total 12,955 13,241 124,567 Accumulated depreciation

(2,935

)

(3,057

) (28,221

)

Net property and equipment

10,020

10,184

96,346

INVESTMENTS AND OTHER ASSETS:

Investment securities (Notes 4 and 10) 5,425 6,124 52,163 Long-term operating loans receivable, less allowance for doubtful accounts of ¥2,302 million ($22,135 thousand) in 2005 and ¥1,994 million in 2004 1,752 2,308 16,846 Software 8,472 8,747 81,462 Guarantee money deposited 12,492 14,013 120,115 Deferred tax assets (Note 13)

4,883 17,870 46,952

Other 6,367 6,133 61,222

Total investments and other assets 39,391

55,195

378,760

TOTAL ¥ 610,975 ¥ 621,109 $ 5,874,760

CURRENT LIABILITIES:

Short-term borrowings (Note 6) ¥ 161,590 ¥ 246,376 $ 1,553,750 Current portion of long-term debt (Note 6) 53,429 37,079 513,740 Accounts payable (Note 10) 26,676 30,859 256,500 Deposits received (Note 7)

56,912 68,564 547,231

Accrued expenses 7,651 6,615 73,567 Income taxes payable 173 165 1,663 Allowance for credit card points redemption (Note 3.a) 1,580 15,192 Deferred revenue (Note 5) 1,098 1,358 10,558 Other current liabilities

4,201

7,014

40,396

Total current liabilities

313,310

398,030

3,012,597

LONG-TERM LIABILITIES:

Long-term debt (Note 6) 235,985 176,289 2,269,087 Liability for retirement benefits (Notes 3.b and 8) 2,723 4,838 26,183 Other long-term liabilities

2,422

1,810

23,288

Total long-term liabilities

241,130

182,937

2,318,558

MINORITY INTERESTS

90

76

865

CONTINGENT LIABILITIES (Note 15)

STOCKHOLDERS' EQUITY (Notes 9 and 18): Common stock—authorized, 670,000,000 shares; issued, 213,561,082 shares in 2005 and 211,317,082 shares in 2004 43,313 42,809 416,471 Capital surplus 506 2

4,865

Retained earnings (accumulated deficit) (4,09911,724 112,731) Unrealized gain on available-for-sale securities 991 1,382 9,529 Treasury stock—at cost, 139,184 shares in 2005 and 81,449 shares in 2004 (89) (28) (856)

Total stockholders' equity

56,445

40,066

542,740

TOTAL ¥ 610,975 ¥ 621,109 $ 5,874,760

See notes to consolidated financial statements.

-22 - -23-

-24 -

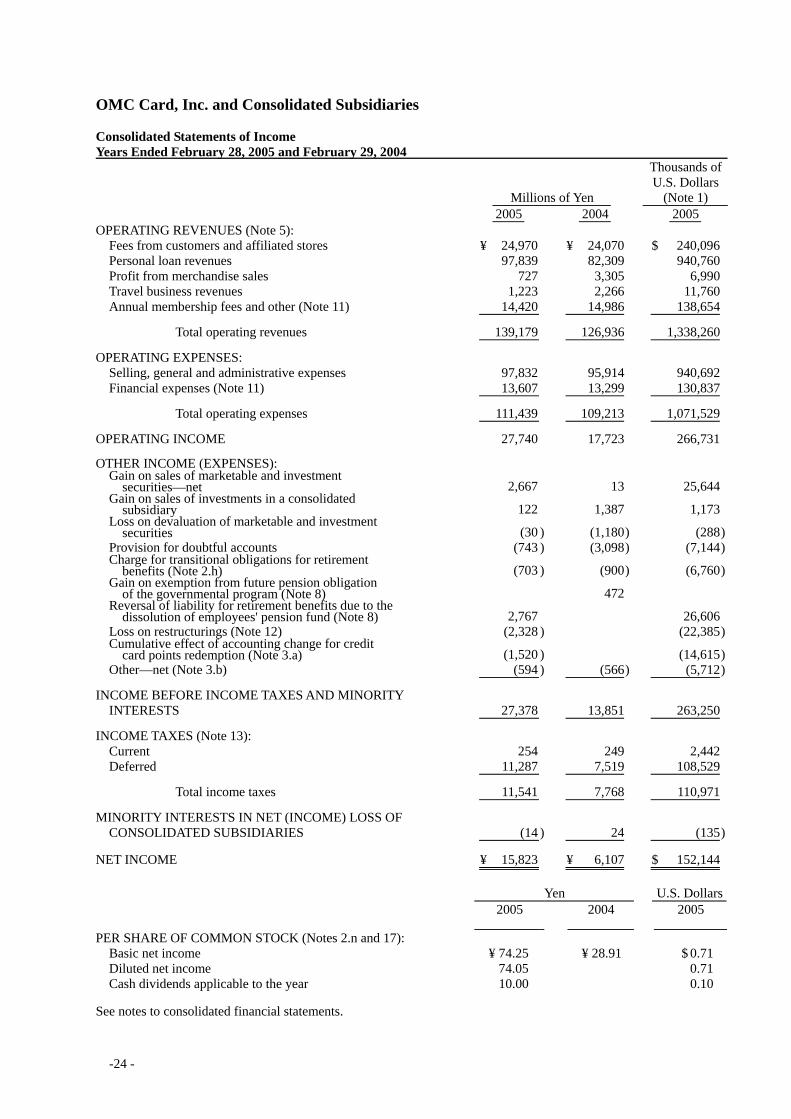

OMC Card, Inc. and Consolidated Subsidiaries Consolidated Statements of Income Years Ended February 28, 2005 and February 29, 2004

Millions of Yen

Thousands ofU.S. Dollars

(Note 1) 2005 2004 2005

OPERATING REVENUES (Note 5): Fees from customers and affiliated stores ¥ 24,970 ¥ 24,070 $ 240,096 Personal loan revenues 97,839 82,309 940,760 Profit from merchandise sales 727 3,305 6,990 Travel business revenues 1,223 2,266 11,760 Annual membership fees and other (Note 11) 14,420 14,986 138,654

Total operating revenues 139,179 126,936 1,338,260

OPERATING EXPENSES: Selling, general and administrative expenses 97,832 95,914 940,692 Financial expenses (Note 11) 13,607 13,299 130,837

Total operating expenses 111,439 109,213 1,071,529

OPERATING INCOME 27,740 17,723 266,731

OTHER INCOME (EXPENSES): Gain on sales of marketable and investment securities—net 2,667 13 25,644 Gain on sales of investments in a consolidated subsidiary 122 1,387 1,173 Loss on devaluation of marketable and investment securities (30 ) (1,180) (288) Provision for doubtful accounts (743 ) (3,098) (7,144) Charge for transitional obligations for retirement benefits (Note 2.h) (703 ) (900) (6,760) Gain on exemption from future pension obligation of the governmental program (Note 8) 472 Reversal of liability for retirement benefits due to the dissolution of employees' pension fund (Note 8) 2,767 26,606 Loss on restructurings (Note 12) (2,328 ) (22,385) Cumulative effect of accounting change for credit card points redemption (Note 3.a) (1,520 ) (14,615) Other—net (Note 3.b) (594 ) (566) (5,712)

INCOME BEFORE INCOME TAXES AND MINORITY INTERESTS 27,378 13,851 263,250

INCOME TAXES (Note 13): Current 254 249 2,442 Deferred 11,287 7,519 108,529

Total income taxes 11,541 7,768 110,971

MINORITY INTERESTS IN NET (INCOME) LOSS OF CONSOLIDATED SUBSIDIARIES

(14 ) 24 (135)

NET INCOME ¥ 15,823 ¥ 6,107 $ 152,144 Yen U.S. Dollars 2005 2004 2005 PER SHARE OF COMMON STOCK (Notes 2.n and 17): Basic net income ¥ 74.25 ¥ 28.91 $ 0.71 Diluted net income 74.05 0.71 Cash dividends applicable to the year 10.00 0.10 See notes to consolidated financial statements.

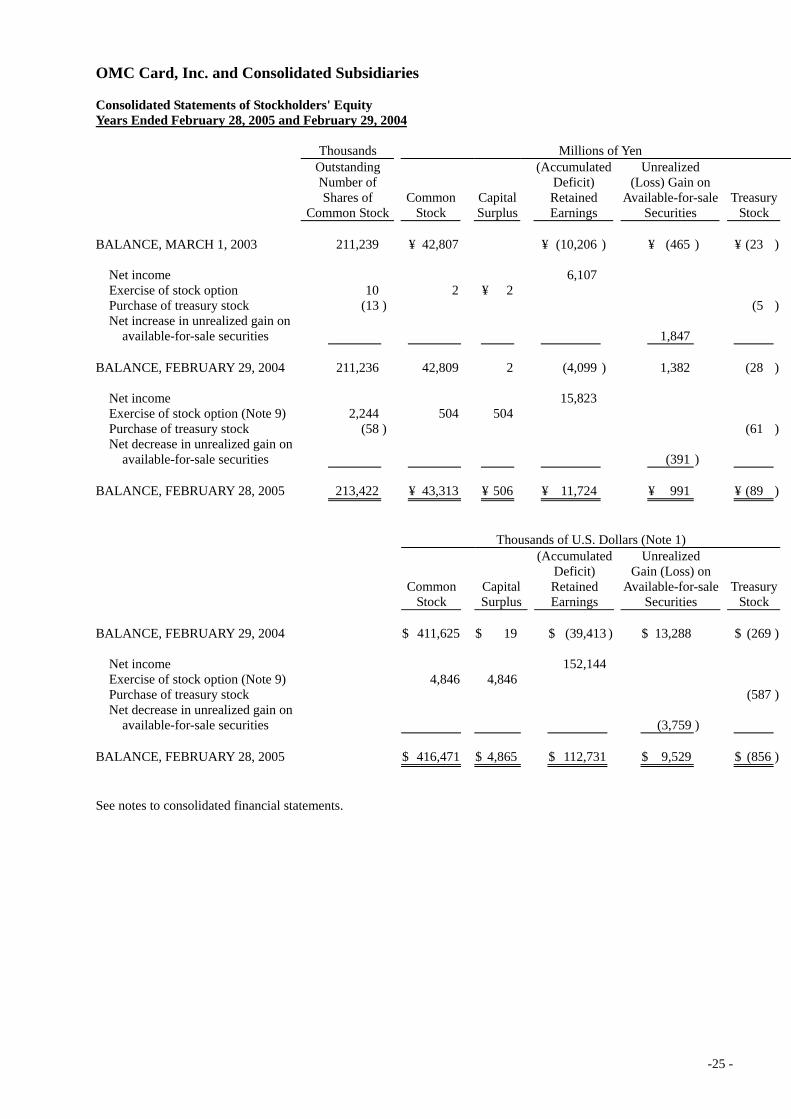

OMC Card, Inc. and Consolidated Subsidiaries Consolidated Statements of Stockholders' Equity Years Ended February 28, 2005 and February 29, 2004 Thousands Millions of Yen

Outstanding Number of Shares of

Common StockCommon

Stock CapitalSurplus

(Accumulated Deficit) Retained Earnings

Unrealized (Loss) Gain on

Available-for-saleSecurities

Treasury Stock

BALANCE, MARCH 1, 2003 211,239 ¥ 42,807 ¥ (10,206 ) ¥ (465 ) ¥ (23 ) Net income 6,107 Exercise of stock option 10 2 ¥ 2 Purchase of treasury stock (13 ) (5 ) Net increase in unrealized gain on available-for-sale securities 1,847 BALANCE, FEBRUARY 29, 2004 211,236 42,809 2 (4,099 ) 1,382 (28 ) Net income 15,823 Exercise of stock option (Note 9) 2,244 504 504 Purchase of treasury stock (58 ) (61 ) Net decrease in unrealized gain on available-for-sale securities (391 ) BALANCE, FEBRUARY 28, 2005 213,422 ¥ 43,313 ¥ 506 ¥ 11,724 ¥ 991 ¥ (89 ) Thousands of U.S. Dollars (Note 1)

Common

Stock CapitalSurplus

(Accumulated Deficit) Retained Earnings

Unrealized Gain (Loss) on

Available-for-saleSecurities

Treasury Stock

BALANCE, FEBRUARY 29, 2004 $ 411,625 $ 19 $ (39,413 ) $ 13,288 $ (269 ) Net income 152,144 Exercise of stock option (Note 9) 4,846 4,846 Purchase of treasury stock (587 ) Net decrease in unrealized gain on available-for-sale securities (3,759 ) BALANCE, FEBRUARY 28, 2005 $ 416,471 $ 4,865 $ 112,731 $ 9,529 $ (856 ) See notes to consolidated financial statements.

-25 -

(Continued) -26-

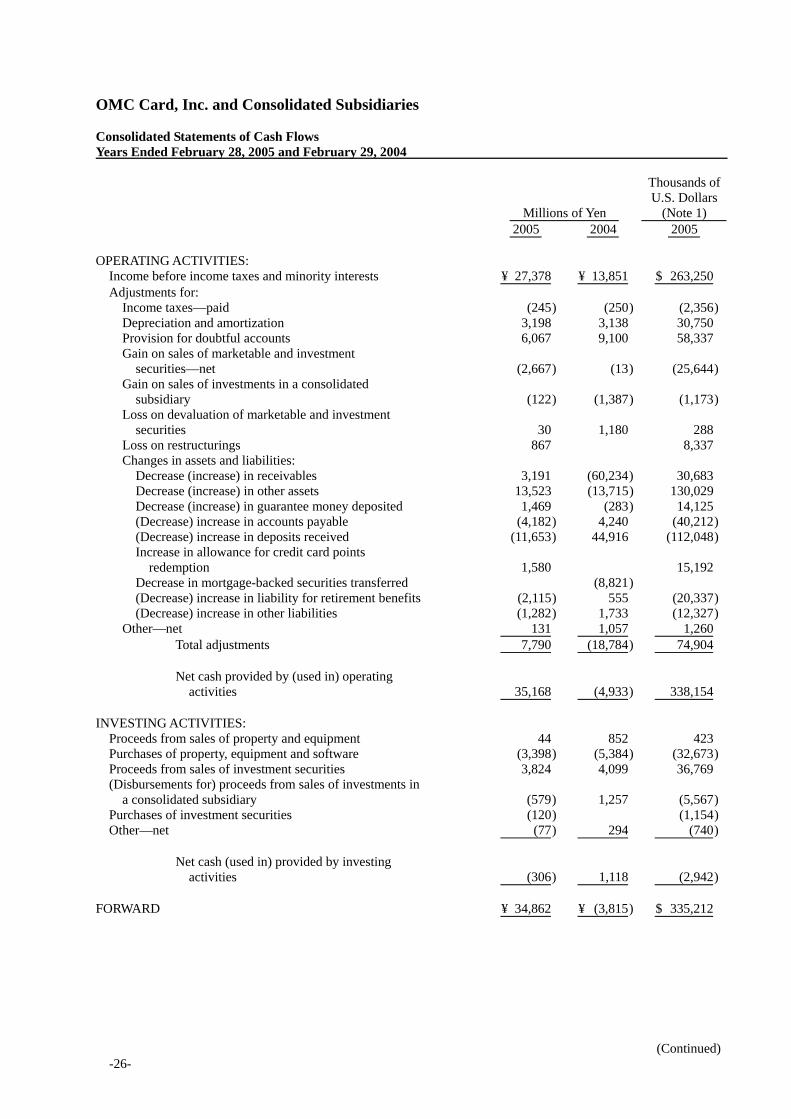

OMC Card, Inc. and Consolidated Subsidiaries Consolidated Statements of Cash Flows Years Ended February 28, 2005 and February 29, 2004

Millions of Yen

Thousands ofU.S. Dollars

(Note 1) 2005 2004 2005

OPERATING ACTIVITIES: Income before income taxes and minority interests ¥ 27,378 ¥ 13,851 $ 263,250 Adjustments for: Income taxes—paid (245) (250) (2,356) Depreciation and amortization 3,198 3,138 30,750 Provision for doubtful accounts 6,067 9,100 58,337 Gain on sales of marketable and investment securities—net (2,667) (13) (25,644) Gain on sales of investments in a consolidated subsidiary (122) (1,387) (1,173) Loss on devaluation of marketable and investment securities 30 1,180 288 Loss on restructurings 867 8,337 Changes in assets and liabilities: Decrease (increase) in receivables 3,191 (60,234) 30,683 Decrease (increase) in other assets 13,523 (13,715) 130,029 Decrease (increase) in guarantee money deposited 1,469 (283) 14,125 (Decrease) increase in accounts payable (4,182) 4,240 (40,212) (Decrease) increase in deposits received (11,653) 44,916 (112,048) Increase in allowance for credit card points redemption 1,580 15,192 Decrease in mortgage-backed securities transferred (8,821) (Decrease) increase in liability for retirement benefits (2,115) 555 (20,337) (Decrease) increase in other liabilities (1,282) 1,733 (12,327) Other—net 131 1,057 1,260 Total adjustments 7,790 (18,784) 74,904 Net cash provided by (used in) operating activities 35,168 (4,933) 338,154 INVESTING ACTIVITIES: Proceeds from sales of property and equipment 44 852 423 Purchases of property, equipment and software (3,398) (5,384) (32,673) Proceeds from sales of investment securities 3,824 4,099 36,769 (Disbursements for) proceeds from sales of investments in a consolidated subsidiary (579) 1,257 (5,567) Purchases of investment securities (120) (1,154) Other—net (77) 294 (740) Net cash (used in) provided by investing activities (306) 1,118 (2,942) FORWARD ¥ 34,862 ¥ (3,815) $ 335,212

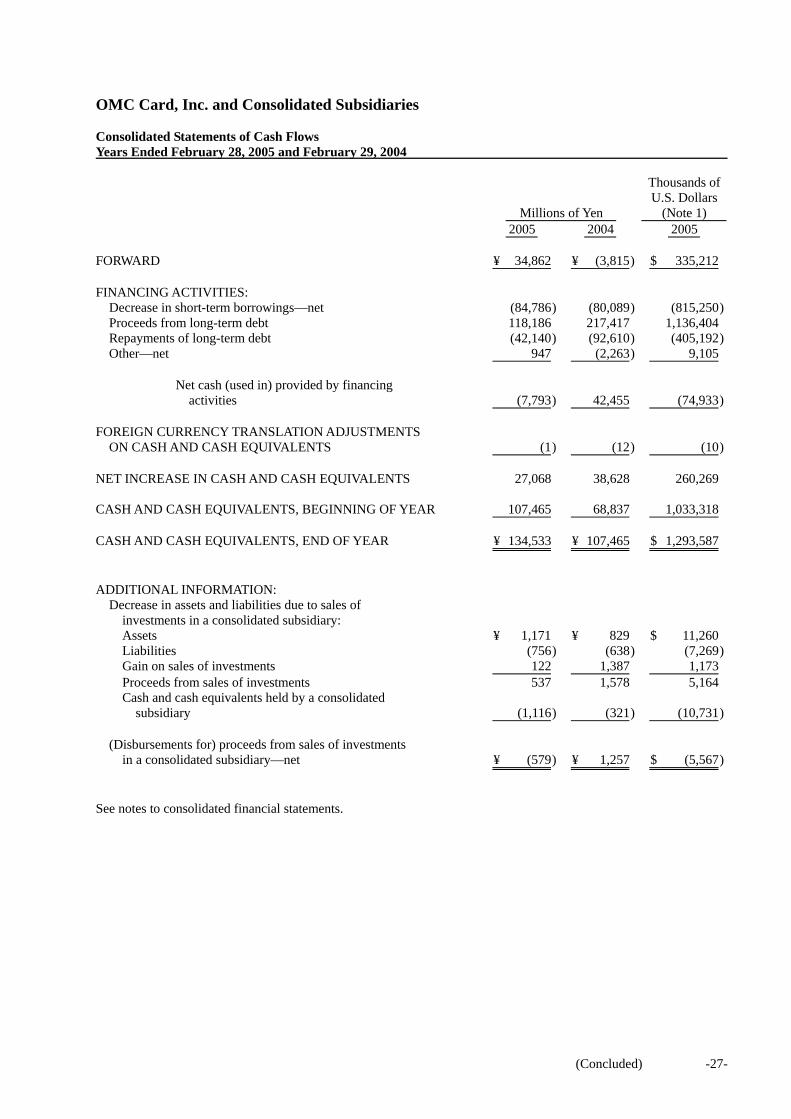

OMC Card, Inc. and Consolidated Subsidiaries Consolidated Statements of Cash Flows Years Ended February 28, 2005 and February 29, 2004

Millions of Yen

Thousands ofU.S. Dollars

(Note 1) 2005 2004 2005

FORWARD ¥ 34,862 ¥ (3,815) $ 335,212 FINANCING ACTIVITIES: Decrease in short-term borrowings—net (84,786) (80,089) (815,250) Proceeds from long-term debt 118,186 217,417 1,136,404 Repayments of long-term debt (42,140) (92,610) (405,192) Other—net 947 (2,263) 9,105 Net cash (used in) provided by financing activities (7,793) 42,455 (74,933) FOREIGN CURRENCY TRANSLATION ADJUSTMENTS ON CASH AND CASH EQUIVALENTS (1) (12) (10) NET INCREASE IN CASH AND CASH EQUIVALENTS 27,068 38,628 260,269 CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR 107,465 68,837 1,033,318 CASH AND CASH EQUIVALENTS, END OF YEAR ¥ 134,533 ¥ 107,465 $ 1,293,587 ADDITIONAL INFORMATION: Decrease in assets and liabilities due to sales of investments in a consolidated subsidiary: Assets ¥ 1,171 ¥ 829 $ 11,260 Liabilities (756) (638) (7,269) Gain on sales of investments 122 1,387 1,173 Proceeds from sales of investments 537 1,578 5,164 Cash and cash equivalents held by a consolidated subsidiary (1,116) (321) (10,731) (Disbursements for) proceeds from sales of investments in a consolidated subsidiary—net ¥ (579) ¥ 1,257 $ (5,567) See notes to consolidated financial statements.

(Concluded) -27-

OMC Card, Inc. and Consolidated Subsidiaries Notes to Consolidated Financial Statements Years Ended February 28, 2005 and February 29, 2004 1. BASIS OF PRESENTING CONSOLIDATED FINANCIAL STATEMENTS

The accompanying consolidated financial statements have been prepared in accordance with the provisions set forth in the Japanese Securities and Exchange Law and its related accounting regulations, and in conformity with accounting principles generally accepted in Japan, which are different in certain respects as to application and disclosure requirements of International Financial Reporting Standards. In preparing these consolidated financial statements, certain reclassifications and rearrangements have been made to the consolidated financial statements issued domestically in order to present them in a form which is more familiar to readers outside Japan. In addition, certain reclassifications have been made in the 2004 financial statements to conform to the classifications used in 2005. The consolidated financial statements are stated in Japanese yen, the currency of the country in which OMC Card, Inc. (the "Company") is incorporated and operates. The translations of Japanese yen amounts into U.S. dollar amounts are included solely for the convenience of readers outside Japan and have been made at the rate of ¥104 to $1, the approximate rate of exchange as of February 28, 2005. Such translations should not be construed as representations that the Japanese yen amounts could be converted into U.S. dollars at that or any other rate.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a. Consolidation—The consolidated financial statements as of February 28, 2005 and February 29, 2004, include the accounts of the Company and its 13 significant subsidiaries (together, the "Companies"). Under the control or influence concept, those companies in which the Company, directly or indirectly, is able to exercise control over operations are fully consolidated, and those companies over which the Company has the ability to exercise significant influence are accounted for by the equity method. Investments in 2 (1 in 2004) associated companies are accounted for by the equity method. Investment in an unconsolidated subsidiary is stated at cost. If the equity method of accounting had been applied to the investment in this company, the effect on the accompanying consolidated financial statements would not be material. The cost in excess of net assets of subsidiaries and associated companies at the time of acquisition which cannot be specifically assigned to individual assets is amortized on the straight-line basis over 5 years with the exception of minor amounts which are charged to income in the period of acquisition. All significant intercompany balances and transactions have been eliminated in consolidation. All material unrealized profits included in assets resulting from transactions within the Companies are also eliminated.

b. Cash Equivalents—Cash equivalents are short-term investments that are readily convertible into cash and

that are exposed to insignificant risk of changes in value. Cash equivalents include time deposits, all of which mature or become due within three months of the date of acquisition.

- 28 -

c. Allowance for Doubtful Accounts—The allowance for doubtful accounts is stated in amounts considered to be appropriate based on the Companies' past credit loss experience and an evaluation of potential losses in the receivables outstanding.

d. Marketable and Investment Securities—Marketable and investment securities are classified as

available-for-sale securities and are reported at fair value, with unrealized gains and losses, net of applicable taxes, reported in a separate component of stockholders' equity. Non-marketable available-for-sale securities are stated at cost determined by the moving-average method. For other than temporary declines in fair value, investment securities are reduced to net realizable value by a charge to income.

e. Property and Equipment—Property and equipment are stated at cost. Depreciation is computed by the

declining-balance method while the straight-line method is applied to buildings (excluding facilities incidental to buildings). The range of useful lives is from 3 to 50 years for buildings and structures and from 3 to 15 years for equipment.

f. Software—Software is amortized by the straight-line method over 5 years. g. Allowance for Credit Card Points Redemption—The allowance for credit card points redemption is stated

in amounts considered to be appropriate based on the Companies' past redemption experience (see Note 3.a).

h. Retirement Benefits—The Company and certain consolidated subsidiaries have a contributory trust

pension plan and non-contributory trust pension plans covering substantially all of their employees. Effective March 1, 2001, the Companies adopted a new accounting standard for employees' retirement benefits and accounted for the liability for retirement benefits based on the projected benefit obligations and plan assets at the balance sheet date. The transitional obligation determined as of March 1, 2001, is being amortized over 5 years and is presented as other expense in the consolidated statements of income. Retirement benefits to directors and corporate auditors are provided at the amount which would be required if all directors and corporate auditors retired at the balance sheet date (see Note 3.b).

i. Leases—All leases are accounted for as operating leases. Under Japanese accounting standards for leases,

finance leases that deem to transfer ownership of the leased property to the lessee are to be capitalized, while other finance leases are permitted to be accounted for as operating lease transactions if certain "as if capitalized" information is disclosed in the notes to the lessee's consolidated financial statements.

j. Recognition of Operating Revenues—The operations of the Companies are mainly comprised of the

following areas, and the recognition of operating revenues differs for each business. See Note 5 for amounts of transactions and realized operating revenues by each business.

(1) Credit Card Contracts and Personal Credit Contracts for Shopping

Installment sales receivable is recorded when the Company purchases these receivables from the affiliated stores, and fees for collection and administrative services to be received from the affiliated stores are recognized at the same time.

- 29 -

The Company also receives fees from customers under credit card contracts, and such fees are recorded when the Company bills customers the amount of fees charged at the contract rate on the outstanding balances of the credit cards, and fees from customers for personal credit contracts for shopping are recognized as profit on the installment basis computed using the sum-of-the-digits method.

(2) Loan Contracts

Operating loans receivable from cardholders are recorded when they receive cash from the Companies. Monthly billings to borrowers include principal and interest, the total of which generally remains constant for the contract period. The interest is recognized as revenue monthly on a declining-balance basis. Personal loans and other operating loans receivable are recorded when loan contracts become effective. The interest on personal loans is recognized as revenue according to the installment plan computed using the sum-of-the-digits method. The interest on certain other contracts is recognized as revenue according to the declining-balance basis.

(3) Merchandise Sales and Income from the Travel Business

Revenues from sales of merchandise inventories such as furniture, household items, etc. and from the travel business are recorded when they are sold to consumers by means of direct marketing by the Companies and by the travel business which is operated by the Company.

k. Income Taxes—The provision for income taxes is computed based on the pretax income included in the

consolidated statements of income. The asset and liability approach is used to recognize deferred tax assets and liabilities for the expected future tax consequences of temporary differences between the carrying amounts and the tax bases of assets and liabilities. Deferred taxes are measured by applying currently enacted tax laws to the temporary differences.

l. Appropriations of Retained Earnings—Appropriations of retained earnings at each year end are reflected

in the financial statements for the following year upon stockholders' approval. m. Derivative Financial Instruments—The Companies enter into interest rate swap agreements as a means of

managing their interest rate exposures on short-term borrowings and long-term debt. It is the Companies' policy not to hold or issue derivatives for speculative or trading purposes. Derivative financial instruments are classified and accounted for as follows: (a) all derivatives are recognized as either assets or liabilities and measured at fair value, and gains or losses on derivative transactions are recognized in the income statement and (b) for derivatives used for hedging purposes, if derivatives qualify for hedge accounting because of high correlation and effectiveness between the hedging instruments and the hedged items, gains or losses on derivatives are deferred until maturity of the hedged transactions. Interest rate swaps are utilized to hedge interest rate exposures of long-term debt. These swaps which qualify for hedge accounting are measured at market value at the balance sheet date and the unrealized gains or losses are deferred until maturity as other liabilities or assets.

- 30 -

However, interest rate swaps which qualify for hedge accounting and meet specific matching criteria are not remeasured at market value but rather, the differential paid or received under the swap agreements is recognized and included in interest expense or income.

n. Per Share Information—Basic net income per share is computed by dividing net income available to

common stockholders by the weighted-average number of common shares outstanding for the period, retroactively adjusted for stock splits. Diluted net income per share reflects the potential dilution that could occur if securities were exercised into common stock. Diluted net income per share of common stock assumes full exercise of outstanding warrants. Diluted net income per share for the year ended February 29, 2004 is not disclosed because the average fair value of the Company's common stock was less than the exercise price for outstanding stock options, and would thus be antidilutive. Cash dividends per share for the year ended February 28, 2005, presented in the accompanying consolidated statements of income, are dividends applicable to the year including dividends to be paid after the end of the year. No cash dividends applicable to the year ended February 29, 2004 were declared.

o. New Accounting Pronouncements—In August 2002, the Business Accounting Council issued a Statement

of Opinion, "Accounting for Impairment of Fixed Assets," and in October 2003 the Accounting Standards Board of Japan ("ASB") issued ASB Guidance No. 6, "Guidance for Accounting Standard for Impairment of Fixed Assets." These new pronouncements are effective for fiscal years beginning on or after April 1, 2005 with early adoption permitted for fiscal years ending on or after March 31, 2004. The new accounting standard requires an entity to review its long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset or asset group may not be recoverable. An impairment loss would be recognized if the carrying amount of an asset or asset group exceeds the sum of the undiscounted future cash flows expected to result from the continued use and eventual disposition of the asset or asset group. The impairment loss would be measured as the amount by which the carrying amount of the asset exceeds its recoverable amount, which is the higher of the discounted cash flows from the continued use and eventual disposition of the asset or the net selling price at disposition. The Companies expect to adopt these pronouncements as of March 1, 2006 and are currently in the process of assessing the effect of adoption of these pronouncements.

3. ACCOUNTING CHANGES

a. Credit Card Points Redemption Prior to March 1, 2004, costs for credit card points redemption were recorded on a cash basis. Effective March 1, 2004, the Companies changed their method of accounting for such redemption to an accrual basis to reflect income and expenses more appropriately due to a system improvement allowing the Companies to obtain information on the Companies' past redemption experience. The effect of this change was to decrease income before income taxes and minority interests for the year ended February 28, 2005 by ¥1,580 million ($15,192 thousand), which included a cumulative effect of ¥1,520 million ($14,615 thousand) which was presented as cumulative effect of accounting change for credit card points redemption in the 2005 consolidated statement of income.

- 31 -

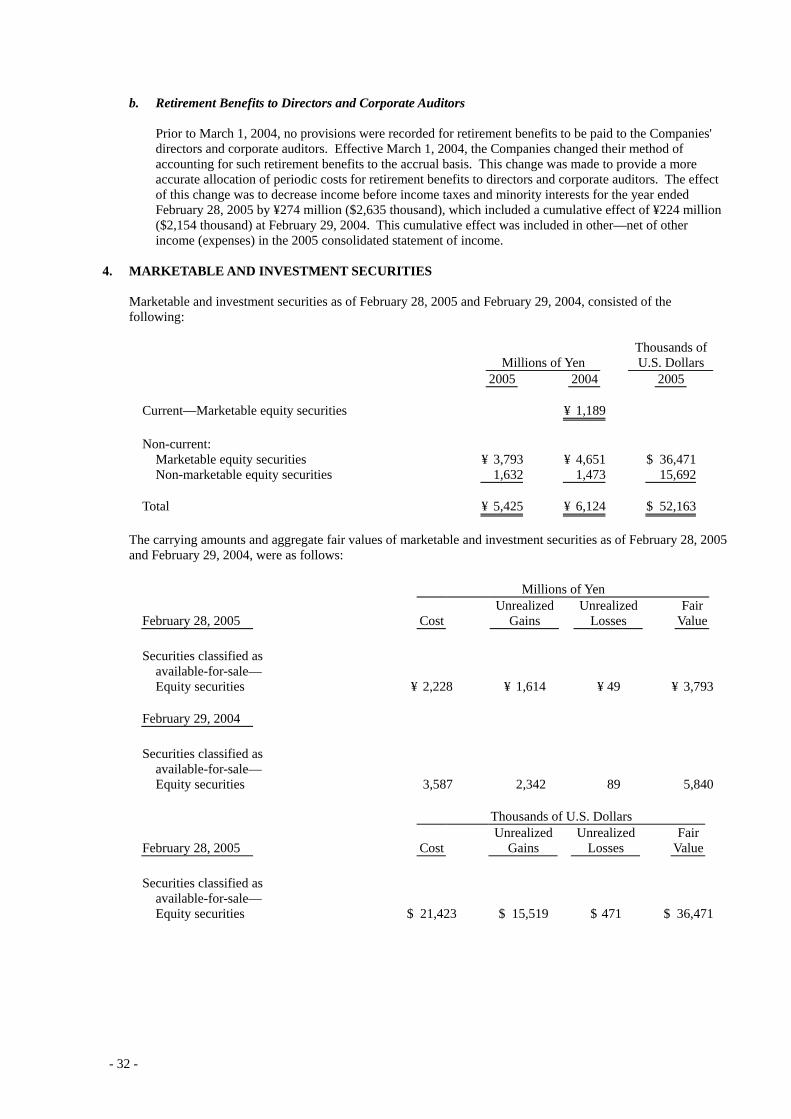

b. Retirement Benefits to Directors and Corporate Auditors Prior to March 1, 2004, no provisions were recorded for retirement benefits to be paid to the Companies' directors and corporate auditors. Effective March 1, 2004, the Companies changed their method of accounting for such retirement benefits to the accrual basis. This change was made to provide a more accurate allocation of periodic costs for retirement benefits to directors and corporate auditors. The effect of this change was to decrease income before income taxes and minority interests for the year ended February 28, 2005 by ¥274 million ($2,635 thousand), which included a cumulative effect of ¥224 million ($2,154 thousand) at February 29, 2004. This cumulative effect was included in other—net of other income (expenses) in the 2005 consolidated statement of income.

4. MARKETABLE AND INVESTMENT SECURITIES

Marketable and investment securities as of February 28, 2005 and February 29, 2004, consisted of the following:

Millions of Yen Thousands ofU.S. Dollars

2005 2004 2005

Current—Marketable equity securities ¥ 1,189 Non-current: Marketable equity securities ¥ 3,793 ¥ 4,651 $ 36,471 Non-marketable equity securities 1,632 1,473 15,692 Total ¥ 5,425 ¥ 6,124 $ 52,163

The carrying amounts and aggregate fair values of marketable and investment securities as of February 28, 2005

and February 29, 2004, were as follows:

Millions of Yen

February 28, 2005 Cost Unrealized

Gains Unrealized

Losses Fair

Value

Securities classified as available-for-sale— Equity securities ¥ 2,228 ¥ 1,614 ¥ 49 ¥ 3,793

February 29, 2004

Securities classified as available-for-sale— Equity securities 3,587 2,342 89 5,840

Thousands of U.S. Dollars

February 28, 2005 Cost Unrealized

Gains Unrealized

Losses Fair

Value

Securities classified as available-for-sale— Equity securities $ 21,423 $ 15,519 $ 471 $ 36,471

- 32 -

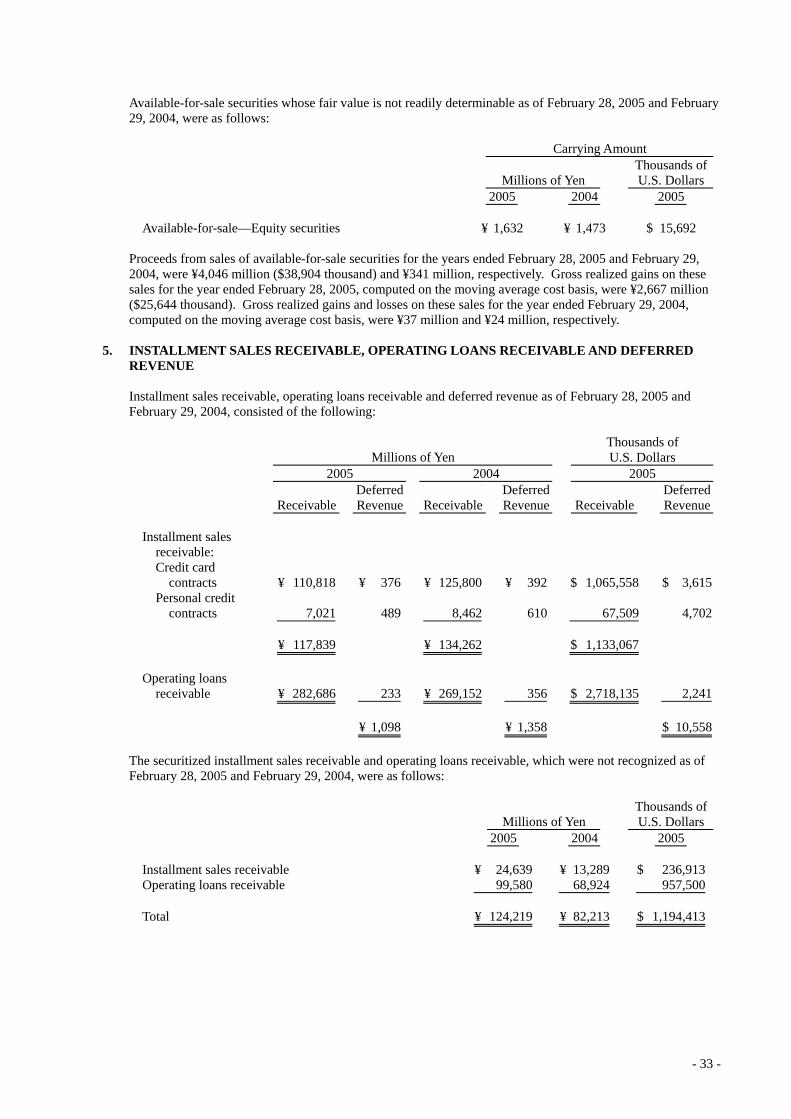

Available-for-sale securities whose fair value is not readily determinable as of February 28, 2005 and February 29, 2004, were as follows:

Carrying Amount

Millions of Yen Thousands ofU.S. Dollars

2005 2004 2005

Available-for-sale—Equity securities ¥ 1,632 ¥ 1,473 $ 15,692 Proceeds from sales of available-for-sale securities for the years ended February 28, 2005 and February 29,

2004, were ¥4,046 million ($38,904 thousand) and ¥341 million, respectively. Gross realized gains on these sales for the year ended February 28, 2005, computed on the moving average cost basis, were ¥2,667 million ($25,644 thousand). Gross realized gains and losses on these sales for the year ended February 29, 2004, computed on the moving average cost basis, were ¥37 million and ¥24 million, respectively.

5. INSTALLMENT SALES RECEIVABLE, OPERATING LOANS RECEIVABLE AND DEFERRED

REVENUE Installment sales receivable, operating loans receivable and deferred revenue as of February 28, 2005 and February 29, 2004, consisted of the following:

Millions of Yen Thousands of U.S. Dollars

2005 2004 2005

ReceivableDeferred Revenue Receivable

Deferred Revenue Receivable

Deferred Revenue

Installment sales receivable: Credit card contracts ¥ 110,818 ¥ 376 ¥ 125,800 ¥ 392 $ 1,065,558 $ 3,615 Personal credit contracts 7,021 489 8,462 610 67,509 4,702 ¥ 117,839 ¥ 134,262 $ 1,133,067 Operating loans receivable ¥ 282,686 233 ¥ 269,152 356 $ 2,718,135 2,241 ¥ 1,098 ¥ 1,358 $ 10,558

The securitized installment sales receivable and operating loans receivable, which were not recognized as of

February 28, 2005 and February 29, 2004, were as follows:

Millions of Yen Thousands ofU.S. Dollars

2005 2004 2005

Installment sales receivable ¥ 24,639 ¥ 13,289 $ 236,913 Operating loans receivable 99,580 68,924 957,500 Total ¥ 124,219 ¥ 82,213 $ 1,194,413

- 33 -

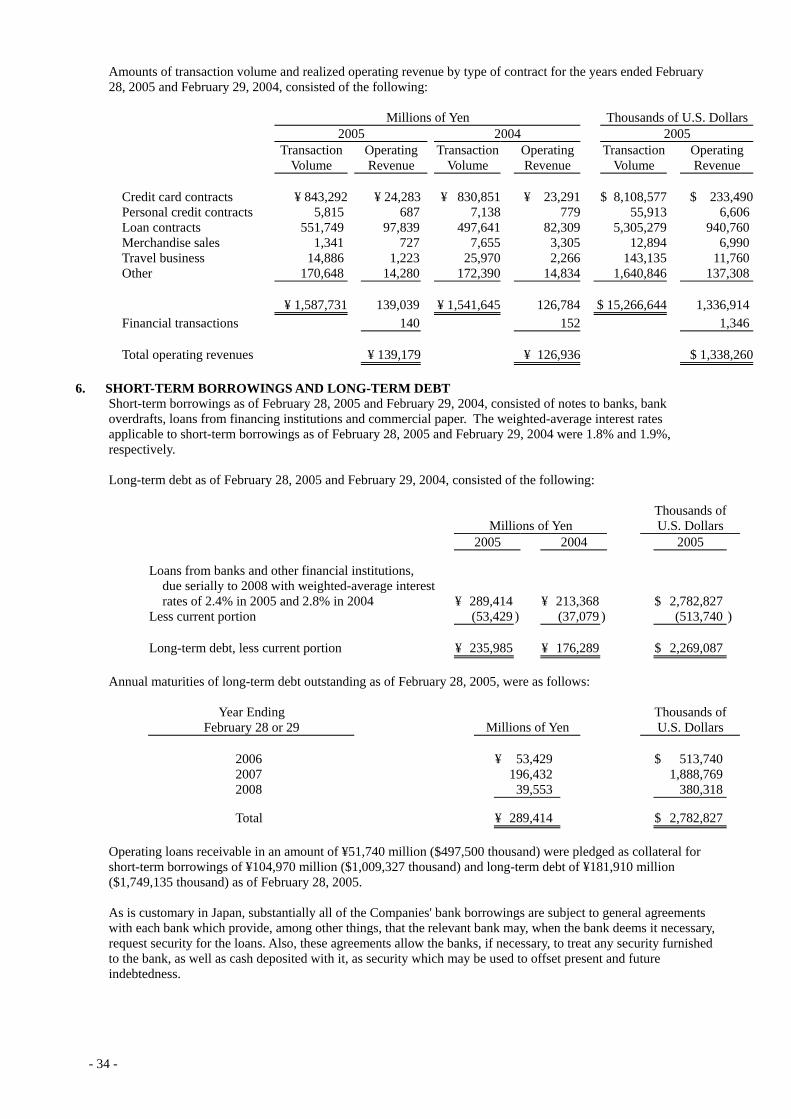

Amounts of transaction volume and realized operating revenue by type of contract for the years ended February

28, 2005 and February 29, 2004, consisted of the following:

Millions of Yen Thousands of U.S. Dollars 2005 2004 2005

Transaction

Volume OperatingRevenue

TransactionVolume

Operating Revenue

TransactionVolume

OperatingRevenue

Credit card contracts ¥ 843,292 ¥ 24,283 ¥ 830,851 ¥ 23,291 $ 8,108,577 $ 233,490Personal credit contracts 5,815 687 7,138 779 55,913 6,606Loan contracts 551,749 97,839 497,641 82,309 5,305,279 940,760Merchandise sales 1,341 727 7,655 3,305 12,894 6,990Travel business 14,886 1,223 25,970 2,266 143,135 11,760Other 170,648 14,280 172,390 14,834 1,640,846 137,308 ¥ 1,587,731 139,039 ¥ 1,541,645 126,784 $ 15,266,644 1,336,914Financial transactions 140 152 1,346 Total operating revenues ¥ 139,179 ¥ 126,936 $ 1,338,260

6. SHORT-TERM BORROWINGS AND LONG-TERM DEBT

Short-term borrowings as of February 28, 2005 and February 29, 2004, consisted of notes to banks, bank overdrafts, loans from financing institutions and commercial paper. The weighted-average interest rates applicable to short-term borrowings as of February 28, 2005 and February 29, 2004 were 1.8% and 1.9%, respectively. Long-term debt as of February 28, 2005 and February 29, 2004, consisted of the following:

Millions of Yen Thousands of U.S. Dollars

2005 2004 2005

Loans from banks and other financial institutions, due serially to 2008 with weighted-average interest rates of 2.4% in 2005 and 2.8% in 2004 ¥ 289,414 ¥ 213,368 $ 2,782,827 Less current portion (53,429 ) (37,079 ) (513,740 ) Long-term debt, less current portion ¥ 235,985 ¥ 176,289 $ 2,269,087

Annual maturities of long-term debt outstanding as of February 28, 2005, were as follows:

Year Ending February 28 or 29 Millions of Yen

Thousands of U.S. Dollars

2006 ¥ 53,429 $ 513,740 2007 196,432 1,888,769 2008 39,553 380,318 Total ¥ 289,414 $ 2,782,827

Operating loans receivable in an amount of ¥51,740 million ($497,500 thousand) were pledged as collateral for

short-term borrowings of ¥104,970 million ($1,009,327 thousand) and long-term debt of ¥181,910 million ($1,749,135 thousand) as of February 28, 2005. As is customary in Japan, substantially all of the Companies' bank borrowings are subject to general agreements with each bank which provide, among other things, that the relevant bank may, when the bank deems it necessary, request security for the loans. Also, these agreements allow the banks, if necessary, to treat any security furnished to the bank, as well as cash deposited with it, as security which may be used to offset present and future indebtedness.

- 34 -

- 35 -

7. DEPOSITS RECEIVED Deposits received mainly consist of temporary cash collected from individual debtors on behalf of principal creditors such as other credit companies including those to which the Company sold its operating receivables on a securitizing basis.

8. RETIREMENT BENEFITS

The Company and certain consolidated subsidiaries have severance payment plans for employees, directors and corporate auditors. Under most circumstances, employees terminating their employment are entitled to retirement benefits determined based on the rate of pay at the time of termination, years of service and certain other factors. Such retirement benefits are made in the form of lump-sum severance payments from the Company or from certain consolidated subsidiaries and annuity payments from a trustee. Employees are entitled to larger payments if the termination is involuntary, by retirement at the mandatory retirement age, by death, or by voluntary retirement at certain specific ages prior to the mandatory retirement age. The Company and certain consolidated subsidiaries had the contributory funded defined benefit pension plan, which is established under the Japanese Welfare Pension Insurance Law and covers a substitutional portion of the governmental pension program managed by the parent company, The Daiei, Inc. (the "Parent") on behalf of the government and a corporate portion established at the discretion of the Parent. In accordance with the Defined Benefit Pension Plan Law enacted in April 2002, the Parent applied for an exemption from obligation to pay benefits for future employee services related to the substitutional portion which would result in the transfer of the pension obligations and related assets to the government upon approval. The Parent obtained approval for exemption from the future obligation by the Ministry of Health, Labour and Welfare on June 20, 2003 and the Companies recognized a gain on exemption from the future pension obligation of the governmental program in the amount of ¥472 million for the year ended February 29, 2004. The substitutional portion of the plan assets which would be transferred to the government in the subsequent year was measured to be approximately ¥5,272 million as of February 29, 2004. On January 28, 2005, the Parent obtained the approval of dissolution of the contributory funded defined benefit pension plan by the Ministry of Health, Labour and Welfare and dissolved the pension fund. The Companies applied accounting treatments specified in the guidance issued by the ASB. The effect of dissolution was ¥2,767 million ($26,606 thousand), recorded as reversal of liability for retirement benefits due to the dissolution of employees' pension fund in the consolidated statement of income for the year ended February 28, 2005. Also, the Company and certain consolidated subsidiaries have defined contribution plans on and after March 1, 2005. The liability (asset) for employees' retirement benefits as of February 28, 2005 and February 29, 2004, consisted of the following:

Millions of Yen Thousands ofU.S. Dollars

2005 2004 2005

Projected benefit obligation ¥ 4,477 ¥ 11,833 $ 43,048 Fair value of plan assets (1,353) (3,903) (13,009) Unrecognized prior service cost 99 Unrecognized actuarial gain (334) (1,696) (3,212) Unrecognized transitional obligation (341) (1,495) (3,279) Net liability ¥ 2,449 ¥ 4,838 $ 23,548

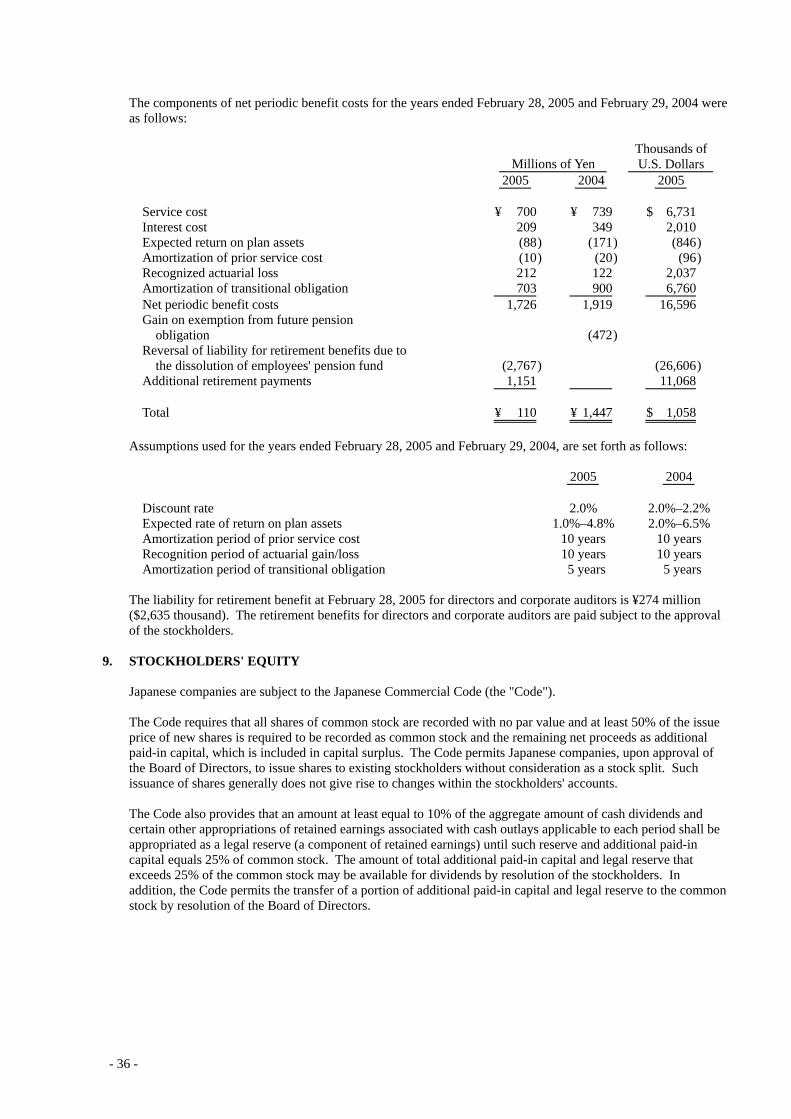

The components of net periodic benefit costs for the years ended February 28, 2005 and February 29, 2004 were as follows:

Millions of Yen Thousands ofU.S. Dollars

2005 2004 2005

Service cost ¥ 700 ¥ 739 $ 6,731 Interest cost 209 349 2,010 Expected return on plan assets (88) (171) (846) Amortization of prior service cost (10) (20) (96) Recognized actuarial loss 212 122 2,037 Amortization of transitional obligation 703 900 6,760 Net periodic benefit costs 1,726 1,919 16,596 Gain on exemption from future pension obligation (472) Reversal of liability for retirement benefits due to the dissolution of employees' pension fund (2,767) (26,606) Additional retirement payments 1,151 11,068 Total ¥ 110 ¥ 1,447 $ 1,058

Assumptions used for the years ended February 28, 2005 and February 29, 2004, are set forth as follows:

2005 2004

Discount rate 2.0% 2.0%–2.2% Expected rate of return on plan assets 1.0%–4.8% 2.0%–6.5% Amortization period of prior service cost 10 years 10 years Recognition period of actuarial gain/loss 10 years 10 years Amortization period of transitional obligation 5 years 5 years

The liability for retirement benefit at February 28, 2005 for directors and corporate auditors is ¥274 million

($2,635 thousand). The retirement benefits for directors and corporate auditors are paid subject to the approval of the stockholders.

9. STOCKHOLDERS' EQUITY

Japanese companies are subject to the Japanese Commercial Code (the "Code"). The Code requires that all shares of common stock are recorded with no par value and at least 50% of the issue price of new shares is required to be recorded as common stock and the remaining net proceeds as additional paid-in capital, which is included in capital surplus. The Code permits Japanese companies, upon approval of the Board of Directors, to issue shares to existing stockholders without consideration as a stock split. Such issuance of shares generally does not give rise to changes within the stockholders' accounts. The Code also provides that an amount at least equal to 10% of the aggregate amount of cash dividends and certain other appropriations of retained earnings associated with cash outlays applicable to each period shall be appropriated as a legal reserve (a component of retained earnings) until such reserve and additional paid-in capital equals 25% of common stock. The amount of total additional paid-in capital and legal reserve that exceeds 25% of the common stock may be available for dividends by resolution of the stockholders. In addition, the Code permits the transfer of a portion of additional paid-in capital and legal reserve to the common stock by resolution of the Board of Directors.

- 36 -

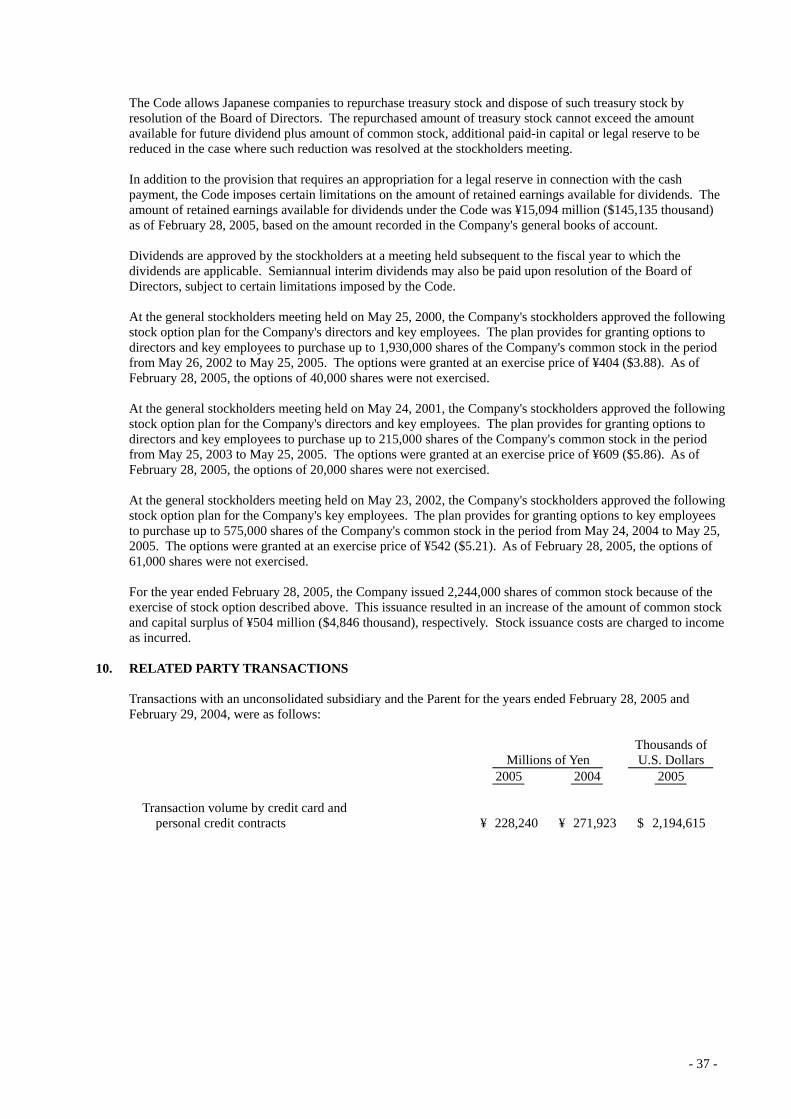

The Code allows Japanese companies to repurchase treasury stock and dispose of such treasury stock by resolution of the Board of Directors. The repurchased amount of treasury stock cannot exceed the amount available for future dividend plus amount of common stock, additional paid-in capital or legal reserve to be reduced in the case where such reduction was resolved at the stockholders meeting. In addition to the provision that requires an appropriation for a legal reserve in connection with the cash payment, the Code imposes certain limitations on the amount of retained earnings available for dividends. The amount of retained earnings available for dividends under the Code was ¥15,094 million ($145,135 thousand) as of February 28, 2005, based on the amount recorded in the Company's general books of account. Dividends are approved by the stockholders at a meeting held subsequent to the fiscal year to which the dividends are applicable. Semiannual interim dividends may also be paid upon resolution of the Board of Directors, subject to certain limitations imposed by the Code. At the general stockholders meeting held on May 25, 2000, the Company's stockholders approved the following stock option plan for the Company's directors and key employees. The plan provides for granting options to directors and key employees to purchase up to 1,930,000 shares of the Company's common stock in the period from May 26, 2002 to May 25, 2005. The options were granted at an exercise price of ¥404 ($3.88). As of February 28, 2005, the options of 40,000 shares were not exercised. At the general stockholders meeting held on May 24, 2001, the Company's stockholders approved the following stock option plan for the Company's directors and key employees. The plan provides for granting options to directors and key employees to purchase up to 215,000 shares of the Company's common stock in the period from May 25, 2003 to May 25, 2005. The options were granted at an exercise price of ¥609 ($5.86). As of February 28, 2005, the options of 20,000 shares were not exercised. At the general stockholders meeting held on May 23, 2002, the Company's stockholders approved the following stock option plan for the Company's key employees. The plan provides for granting options to key employees to purchase up to 575,000 shares of the Company's common stock in the period from May 24, 2004 to May 25, 2005. The options were granted at an exercise price of ¥542 ($5.21). As of February 28, 2005, the options of 61,000 shares were not exercised. For the year ended February 28, 2005, the Company issued 2,244,000 shares of common stock because of the exercise of stock option described above. This issuance resulted in an increase of the amount of common stock and capital surplus of ¥504 million ($4,846 thousand), respectively. Stock issuance costs are charged to income as incurred.

10. RELATED PARTY TRANSACTIONS

Transactions with an unconsolidated subsidiary and the Parent for the years ended February 28, 2005 and February 29, 2004, were as follows:

Millions of Yen Thousands ofU.S. Dollars

2005 2004 2005

Transaction volume by credit card and personal credit contracts ¥ 228,240 ¥ 271,923 $ 2,194,615

- 37 -

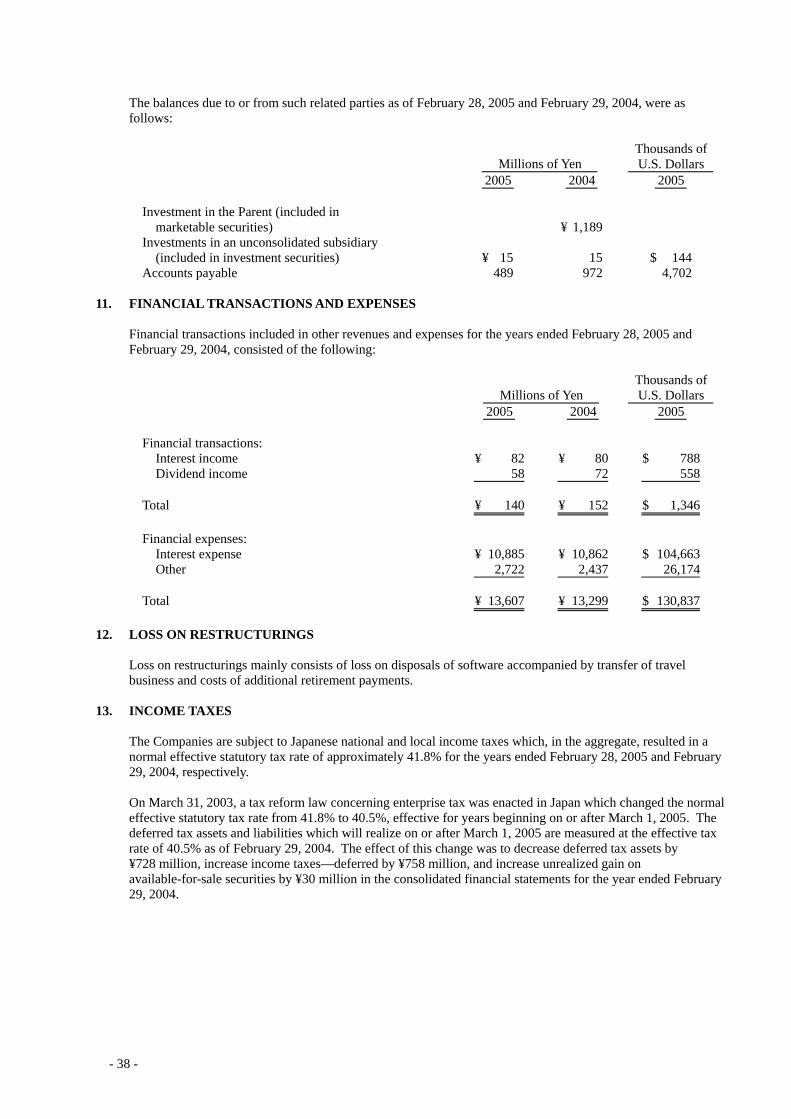

The balances due to or from such related parties as of February 28, 2005 and February 29, 2004, were as follows:

Millions of Yen Thousands ofU.S. Dollars

2005 2004 2005

Investment in the Parent (included in marketable securities) ¥ 1,189 Investments in an unconsolidated subsidiary (included in investment securities) ¥ 15 15 $ 144 Accounts payable 489 972 4,702

11. FINANCIAL TRANSACTIONS AND EXPENSES

Financial transactions included in other revenues and expenses for the years ended February 28, 2005 and February 29, 2004, consisted of the following:

Millions of Yen Thousands ofU.S. Dollars

2005 2004 2005

Financial transactions: Interest income ¥ 82 ¥ 80 $ 788 Dividend income 58 72 558 Total ¥ 140 ¥ 152 $ 1,346 Financial expenses: Interest expense ¥ 10,885 ¥ 10,862 $ 104,663 Other 2,722 2,437 26,174 Total ¥ 13,607 ¥ 13,299 $ 130,837

12. LOSS ON RESTRUCTURINGS

Loss on restructurings mainly consists of loss on disposals of software accompanied by transfer of travel business and costs of additional retirement payments.

13. INCOME TAXES

The Companies are subject to Japanese national and local income taxes which, in the aggregate, resulted in a normal effective statutory tax rate of approximately 41.8% for the years ended February 28, 2005 and February 29, 2004, respectively. On March 31, 2003, a tax reform law concerning enterprise tax was enacted in Japan which changed the normal effective statutory tax rate from 41.8% to 40.5%, effective for years beginning on or after March 1, 2005. The deferred tax assets and liabilities which will realize on or after March 1, 2005 are measured at the effective tax rate of 40.5% as of February 29, 2004. The effect of this change was to decrease deferred tax assets by ¥728 million, increase income taxes—deferred by ¥758 million, and increase unrealized gain on available-for-sale securities by ¥30 million in the consolidated financial statements for the year ended February 29, 2004.

- 38 -

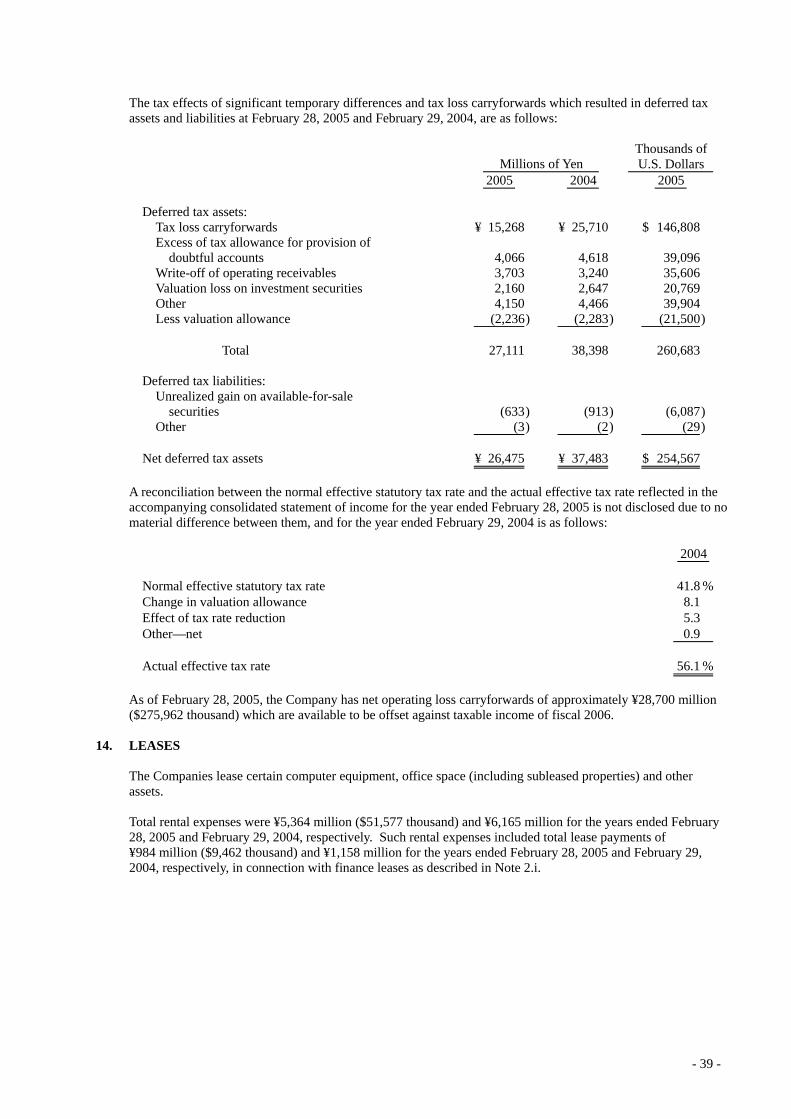

The tax effects of significant temporary differences and tax loss carryforwards which resulted in deferred tax assets and liabilities at February 28, 2005 and February 29, 2004, are as follows:

Millions of Yen Thousands of U.S. Dollars

2005 2004 2005

Deferred tax assets: Tax loss carryforwards ¥ 15,268 ¥ 25,710 $ 146,808 Excess of tax allowance for provision of doubtful accounts 4,066 4,618 39,096 Write-off of operating receivables 3,703 3,240 35,606 Valuation loss on investment securities 2,160 2,647 20,769 Other 4,150 4,466 39,904 Less valuation allowance (2,236) (2,283) (21,500) Total 27,111 38,398 260,683 Deferred tax liabilities: Unrealized gain on available-for-sale securities (633) (913) (6,087) Other (3) (2) (29) Net deferred tax assets ¥ 26,475 ¥ 37,483 $ 254,567

A reconciliation between the normal effective statutory tax rate and the actual effective tax rate reflected in the

accompanying consolidated statement of income for the year ended February 28, 2005 is not disclosed due to no material difference between them, and for the year ended February 29, 2004 is as follows:

2004

Normal effective statutory tax rate 41.8 % Change in valuation allowance 8.1 Effect of tax rate reduction 5.3 Other—net 0.9 Actual effective tax rate 56.1 %

As of February 28, 2005, the Company has net operating loss carryforwards of approximately ¥28,700 million

($275,962 thousand) which are available to be offset against taxable income of fiscal 2006. 14. LEASES

The Companies lease certain computer equipment, office space (including subleased properties) and other assets. Total rental expenses were ¥5,364 million ($51,577 thousand) and ¥6,165 million for the years ended February 28, 2005 and February 29, 2004, respectively. Such rental expenses included total lease payments of ¥984 million ($9,462 thousand) and ¥1,158 million for the years ended February 28, 2005 and February 29, 2004, respectively, in connection with finance leases as described in Note 2.i.

- 39 -

Pro forma information of leased property such as acquisition cost, accumulated depreciation, obligation under finance leases, depreciation expense, interest expense of financial leases that do not transfer ownership of the leased property to the lessee on an "as if capitalized" basis for the years ended February 28, 2005 and February 29, 2004, was as follows:

Millions of Yen Thousands of U.S. Dollars

2005 2004 2005

Acquisition cost—equipment ¥ 5,089 ¥ 5,908 $ 48,933 Accumulated depreciation 3,374 3,367 32,443 Net leased property ¥ 1,715 ¥ 2,541 $ 16,490

Obligations under finance leases:

Millions of Yen Thousands ofU.S. Dollars

2005 2004 2005

Due within one year ¥ 760 ¥ 929 $ 7,308 Due after one year 1,026 1,699 9,865 Total ¥ 1,786 ¥ 2,628 $ 17,173

The imputed interest expense portion which is computed using the interest method is excluded from the above

obligations under finance leases. Depreciation expense and interest expense, which are not reflected in the accompanying consolidated statements of income, computed by the straight-line method and the interest method were ¥892 million ($8,577 thousand) and ¥91 million ($875 thousand) for the year ended February 28, 2005 and ¥1,051 million and ¥112 million for the year ended February 29, 2004, respectively. Future minimum lease receipts as lessor under operating leases for remaining lease periods, as of February 28, 2005, were ¥366 million ($3,519 thousand), of which ¥34 million ($327 thousand) is due within one year.

15. CONTINGENT LIABILITIES

As of February 28, 2005, the Companies were contingently liable as a guarantor for borrowings of customers in an amount of ¥1,214 million ($11,673 thousand).

16. DERIVATIVES

The Companies enter into interest rate swap agreements as a means of managing their interest rate exposure on long-term debt. It is the Companies' policy not to hold or issue derivatives for speculative or trading purposes. Derivatives are subject to market risk and credit risk. Market risk is the exposure created by potential fluctuations in market conditions, including interest rates. Credit risk is the possibility that a loss may result from a counterparty's failure to perform according to the terms and conditions of the contract.

- 40 -

Because the counterparties to those derivatives are limited to major international financial institutions, the Companies do not anticipate any losses arising from credit risk. Derivative transactions entered into by the Companies have been made in accordance with internal policies which regulate the authorization and credit limit amount. Market value information for the years ended February 28, 2005 and February 29, 2004, is not disclosed because all of the derivatives qualified for hedge accounting and met specific matching criteria.

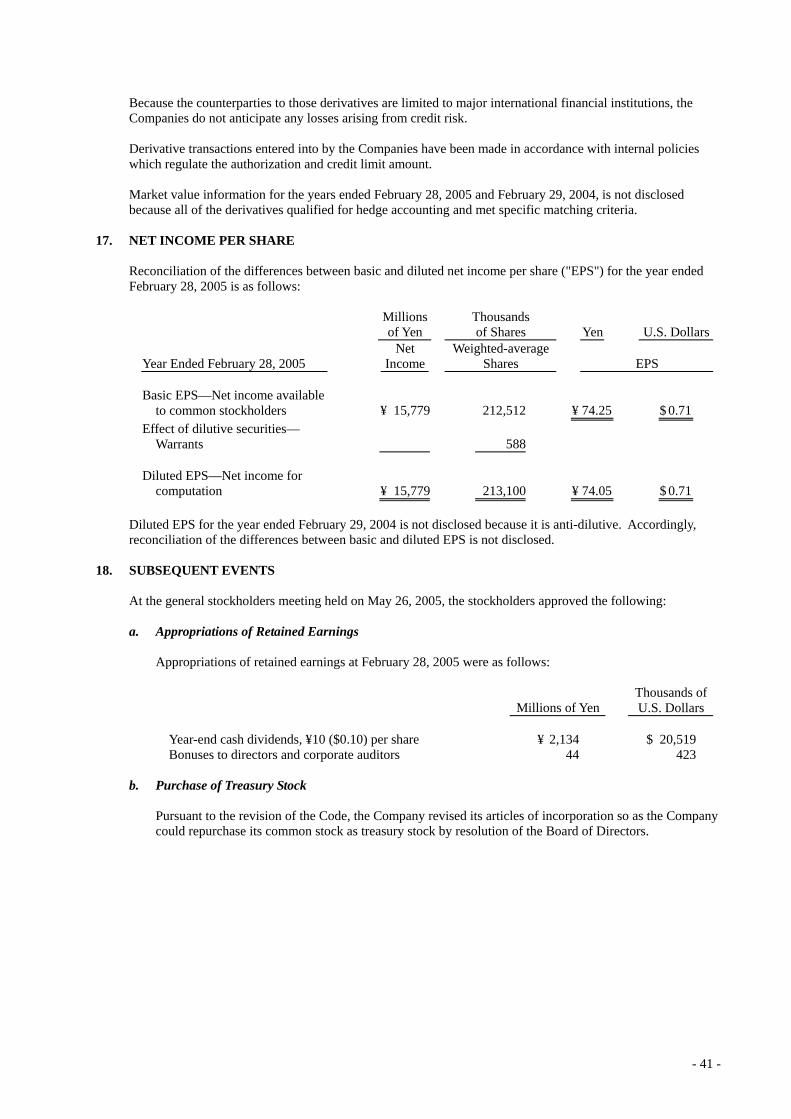

17. NET INCOME PER SHARE

Reconciliation of the differences between basic and diluted net income per share ("EPS") for the year ended February 28, 2005 is as follows:

Millions of Yen

Thousands of Shares Yen U.S. Dollars

Year Ended February 28, 2005 Net

IncomeWeighted-average

Shares EPS

Basic EPS—Net income available to common stockholders ¥ 15,779 212,512 ¥ 74.25 $ 0.71 Effect of dilutive securities— Warrants 588 Diluted EPS—Net income for computation ¥ 15,779 213,100 ¥ 74.05 $ 0.71

Diluted EPS for the year ended February 29, 2004 is not disclosed because it is anti-dilutive. Accordingly,

reconciliation of the differences between basic and diluted EPS is not disclosed. 18. SUBSEQUENT EVENTS

At the general stockholders meeting held on May 26, 2005, the stockholders approved the following:

a. Appropriations of Retained Earnings

Appropriations of retained earnings at February 28, 2005 were as follows:

Millions of Yen Thousands of U.S. Dollars

Year-end cash dividends, ¥10 ($0.10) per share ¥ 2,134 $ 20,519 Bonuses to directors and corporate auditors 44 423

b. Purchase of Treasury Stock

Pursuant to the revision of the Code, the Company revised its articles of incorporation so as the Company could repurchase its common stock as treasury stock by resolution of the Board of Directors.

- 41 -

42 43