Embed Size (px)

Citation preview

Consistently solid in a dynamic environment Annual Results 2015

Willem van Duin Chairman of the Executive Board

Huub Arendse Chief Financial Officer

Program

General overview

Group results

Acceleration & Innovation

Financial overview

Questions

2 | Achmea Jaarresultaten 2015

Consistently solid in a dynamic environment

Net profit increases to €386 million

Acceleration & Innovation in full flow:

Leader in online and mobile services

Reduction in operating costs on schedule; €300 million reduction realised

Chosen for strong positioning in pension market with Centraal Beheer APF

Achmea Investment Management manages over €100 billion assets under management

Financial position solid with solvency ratio of 210% under Solvency I

A+ credit rating for insurance entities by S&P.

3 | Achmea Jaarresultaten 2015

Net profit increases to €386 million

Net profit increased to €386 million due to, among other things, cost savings

Positive developments in Pensions and Life, International and Banking activities and higher investment results all contributed to an improved result

2014 results strongly influenced by goodwill write-offs and restructuring costs

Operational result negatively influenced by:

Allocation of €481 million to limit increase in health insurance premiums in 2016

Storms caused €120 million in damages for our customers

Stable development in written premiums confirms market leadership in health care and non-life insurances

Total cost savings of €300 million realised since the start of Acceleration & Innovation In 2015, costs decreased by €132 million (or 5%)

Financial position remains solid with solvency ratio of 210% under Solvency I. Approval obtained for use of a internal model for Non-Life Insurance under Solvency II.

4 | Achmea Jaarresultaten 2015

368 388 386

16

Net profit (in € m)

Solvency ratio (IGD) (in %)

Gross written premiums (in € m)

Operational result (in € m)

* Operating expenses 2014 corrected for one-off costs including restructuring costs

2014

Operating expenses* (in € m)

2014 2014 2015

2,759 2,633 215 9,818 10,280

Equity (in € m)

2014 2015

2015

2015

210

2014 2015

19,922 20,002

2015 2014

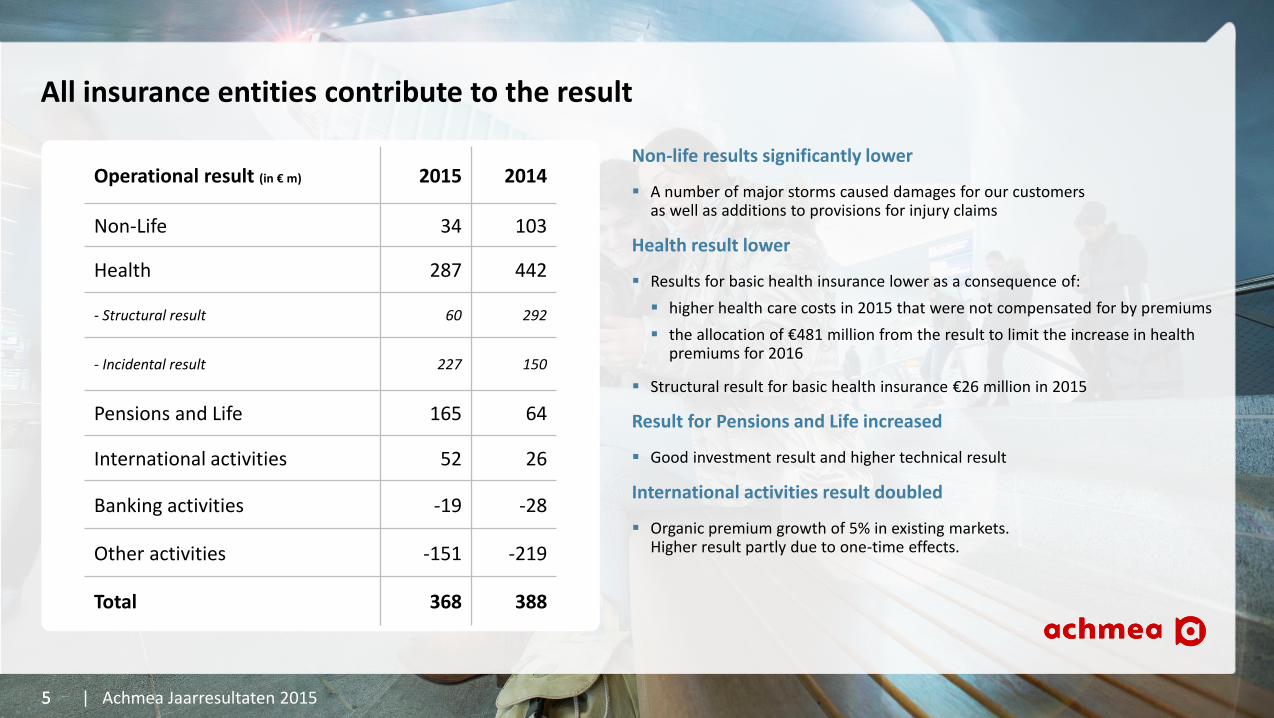

All insurance entities contribute to the result

Non-life results significantly lower

A number of major storms caused damages for our customers as well as additions to provisions for injury claims

Health result lower

Results for basic health insurance lower as a consequence of:

higher health care costs in 2015 that were not compensated for by premiums

the allocation of €481 million from the result to limit the increase in health premiums for 2016

Structural result for basic health insurance €26 million in 2015

Result for Pensions and Life increased

Good investment result and higher technical result

International activities result doubled

Organic premium growth of 5% in existing markets. Higher result partly due to one-time effects.

5 | Achmea Jaarresultaten 2015

5

Operational result (in € m) 2015 2014

Non-Life 34 103

Health 287 442

- Structural result 60 292

- Incidental result 227 150

Pensions and Life 165 64

International activities 52 26

Banking activities -19 -28

Other activities -151 -219

Total 368 388

Acceleration & Innovation: accelerated change in terms of customer focus in 2014

Background

Acceleration in terms of customer focus and cost savings

Innovation of processes and online services

These changes are driven by customers’ fast-changing needs

Acceleration & Innovation Ambitions

Providing our customers with new solutions

Maintaining the current high level of customer satisfaction

Maintaining long-term financial health

Objectives for the end of 2016

€450 million cost reduction

Reduction of approximately 4,000 jobs.

6 | Achmea Jaarresultaten 2015

Competitive costs

Responsible returns

Employees Employees

Customer-driven

Customer-driven: responding to customers’ fast-changing wishes

More than 150 innovations initiated since the start of Acceleration & Innovation

All brands are better accessible online for our customers

Centraal Beheer app offers a complete and up to date overview of insurance and services

Centraal Beheer handles small car damage matters completely online

More than 700,000 visitors to the Zilveren Kruis online platform are discussing health and vitality

Zilveren Kruis is collaborating on an app over the necessity of a visit to the doctor: ‘Should I go to the doctor?’

Interpolis advises entrepreneurs on protection against cybercrime

Interpolis offers legal advice to everyone through the RechtsHulp app

Interpolis increases youth traffic safety with the experiment ‘Slim Op Weg’ and driving skills training

Direct medical advice via the FBTO video app ‘Arts op Zak’

Extending customer service by 15,412 employees through the ‘Klantsignalen’ app for all Achmea employees.

7 | Achmea Jaarresultaten 2015

Medewerkers

Customer-driven: responding to customers’ fast-changing needs

8 | Achmea Jaarresultaten 2015

Medewerkers

Centraal Beheer app offers a complete and up to date overview of insurance

and services

More than 700,000 online platform visitors

Zilveren Kruis discuss about health and vitality

Interpolis offers legal advice to everyone through the

RechtsHulp app

Interpolis advises entrepreneurs on protection against

cybercrime

Customer-driven: renewing our business operations

Strong brands with high customer rating (NPS)

AFM scores Klantbelang Centraal further increased towards the market average of 3.4

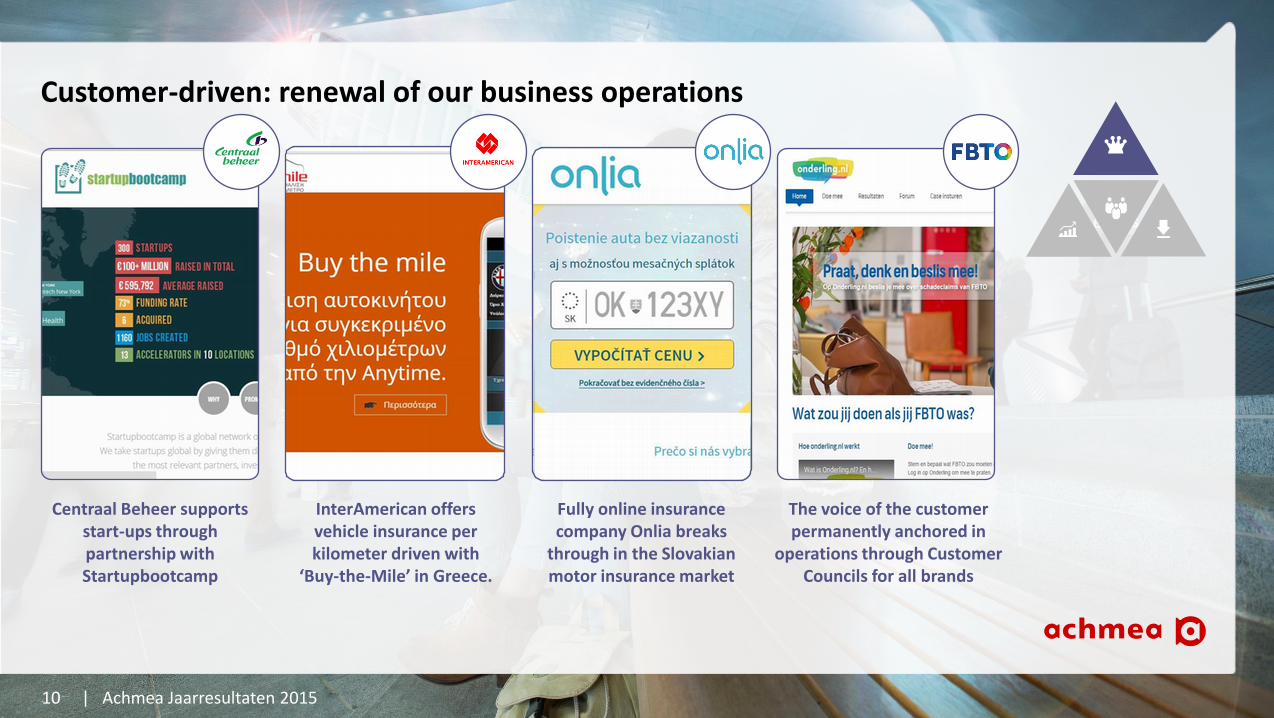

Centraal Beheer supports start-ups through partnership with Startupbootcamp

Zilveren Kruis promotes a healthy lifestyle with Actify website

Fully online insurance company Onlia breaks through in the Slovakian motor insurance market

InterAmerican offers vehicle insurance per kilometer driven with ‘Buy-the-Mile’ in Greece.

The voice of the customer permanently anchored in operations through Customer Councils for all brands

Further revitalisation of cooperative identity through the stronger role of the Members Council in Vereniging Achmea.

9 | Achmea Jaarresultaten 2015

Medewerkers

Customer-driven: renewal of our business operations

10 | Achmea Jaarresultaten 2015

Medewerkers

Centraal Beheer supports start-ups through partnership with Startupbootcamp

InterAmerican offers vehicle insurance per kilometer driven with

‘Buy-the-Mile’ in Greece.

Fully online insurance company Onlia breaks

through in the Slovakian motor insurance market

The voice of the customer permanently anchored in

operations through Customer Councils for all brands

Responsible returns

Chosen for strong positioning in pension market with Centraal Beheer APF

Merging asset management activities into Achmea Investment Management (AuM €102 bln)

Limited increase in health premiums due to the allocation of 2015 result

Retaining the market leadership of Zilveren Kruis offers purchasing advantages

Approval of DNB for use of internal model Non-Life Insurance for Solvency II

Enhance commercial effectiveness with market-focused chains Non-Life, Pensions and Health care

International activities achieve a broad-based result recovery with a new strategy

More intensified collaboration with Rabobank: fully digital servicing of individuals; improved advice for SME’s

A+ credit rating for insurance units at Standard & Poor’s.

11 | Achmea Jaarresultaten 2015

Medewerkers

Competitive costs: on track with cost reduction objectives

On track for reduction of costs by €450 million by end 2016

Operating expenses reduced by €300 million since 2014

€132 million in cost reduction achieved in 2015 or 5%

Reduction achieved of approximately 2.500 FTE; excluding strategic investments in APF

Reductions realised in support services and staff functions

Good employership, even during challenging times with sustainable social plan and ATC

Accelerated migration to target IT systems, in particular with Pension & Life for better service provision at lower cost.

12 | Achmea Jaarresultaten 2015

Medewerkers

Employees: dedication crucial for improvement of service provision

Achmea wants to become the digital insurer and our people make that difference

Investments in and working on making employees ‘digitally savvy’

Attention for the required competencies in a digital, flexible environment

Increasing the long-term employability of staff

Attention along three tracks: ‘vitality and health’, ‘learning and development’ and ‘mobility and careers’

Flexibility, employability and customer centricity in recently closed Collective Labor Agreement

Employee engagement remains high despite drastic measures

Very high response of 89% between employees

Persistently high general employee satisfaction increased further to 84%.

13 | Achmea Jaarresultaten 2015

Medewerkers

Acceleration & Innovation: Stay on course, complete and accelerate

Maintain the chosen strategic course:

Further strengthening of existing core competencies Non-life, Income and Health insurances

Supplemented with strong positioning in the pension market and of international activities

Provide our customers with innovative solutions

Keep customer satisfaction high

Maintain solid, long-term financial strength

Further acceleration consists of:

Continuing with further digitisation and innovating of services provided to customers

Continued focus on cost reduction

Start of market focused chains Non-Life, Health and Pensions

Intensified collaboration with Rabobank

Further cost savings arising from the Migration to Digital Customer Service program.

14 | Achmea Jaarresultaten 2015

program

General overview

Financial overview

Results per segment

Capital position and solvency ratio

Investments

Questions

15 | Achmea Jaarresultaten 2015

Net profit increases to €386 million

Net profit increased

Net profit greatly increased. 2014 results influenced by one-off effects such as:

Restructuring costs associated with the Acceleration & Innovation program

Goodwill write-off and transaction result due to the sale of Russian insurance activities

Sale and partial closure of Achmea Health Centers

In 2015, positive transaction results partly as result of the sale of asset management activities in Ireland.

16 | Achmea Jaarresultaten 2015

Result (in € m) 2015 2014

Operational result 368 388

Reorganisation expenses - 239

Goodwill write-off - 143

Transaction results/M&A 10 14

Profit before tax 378 -8

Taxes 8 24

Net profit 386 16

Non-life: large one-off effects, underlying results improved

Property and Casualty

Operational result strongly affected by major storm damage and increased personal injuries:

Major storms (€70 million) and increasingly fierce local weather conditions. In total, our customers have been compensated for around €120 million

Higher benefits are expected for existing injury claims

Corrected for incidental storm damage and injury claims, the operational result increased through lower costs and higher investment results

Income protection

In 2015, there were higher damage claims due to illness leading to longer work absence and an increasing average of disability

Positive results from previous years:

Faster recovery of individual and collective disability insurance

Lower inflows in collective disability insurance

Higher expenses for profit sharing, in particular through favorable developments in disability in previous years

Lower costs as a consequence of initiatives introduced as part of the Acceleration & Innovation program.

17 | Achmea Jaarresultaten 2015

Operational result Income protection

(in € m)

Operational result Property and Casualty

(in € m)

40

20

2014 2015

63

13

116

129

2015 2014

Normalised for incidental damage

Non-life: Premiums stable and lower cost levels

Property and Casualty

Premium revenue reasonable stable despite the termination of loss-making contracts and the signing of multiple year policies in 2014

Great inflow of new individual customers at Centraal Beheer

Further reduction in costs gained through, among other things, product innovations and reduction of complexity in processes and systems

Major storms and higher injury claims increase the claims ratio by 4.7 precentage point

Income Protection

Increase in premium revenue through growth in WIA contracts and premium increases

Cost ratios reduced through Acceleration & Innovation initiatives

Lower claims ratio through the availability of provisions due to reduced disability duration and lower WIA inflows

Better combined ratio; underlying favourable development in income protection.

18 | Achmea Jaarresultaten 2015

Operational costs (in € m)

Income protection insurance (in %)

Gross written premiums (in € m)

Non-life insurances (in %)

Non-Life Income

Claims ratio Expense ratio Claims ratio¹ Expense ratio

587

2,576 2,518

610

3,128 3,163

2015 2014

2014

99.7%

69.7%

30.0%

2015

103.3%

69.5%

4.7%

29.1%

2014

99.2%

70.4

28.8

2015

94.9%

69.1%

25.8%

¹Corrected for the interest accrual for the insurance provision

760

2014 2015

741

Health: allocation of €481 million to limit premium increase despite growth of health costs

Basic health insurance

Structural result in 2015 falls significantly to €26 million. Increased health costs not fully compensated for through premiums

In 2015 we used €481 million from the result to restrict increases to premiums for our customers. In 2014, we used €335 million from the result for this

Higher incidental results through the release of provisions from previous years and incidental positive results from the settlement and lower costs than had been estimated

Supplemental health insurance

The result for our supplemental health insurance was €39 million (2014: €99 million). The lower result was due to lower number of insured and lower cover. There was less result from previous years

Total health insurances

Results for health insurances fell to €287 million, versus €442 million in 2014.

19 | Achmea Jaarresultaten 2015

Structural result for basic health insurance

Underwriting year 2014/2015

(in € m)

99

222

2014 2015

Incidental result for basic health insurance

Previous underwriting years

(in € m)

243

26

2014 2015

434

703

2014 2015

-335-481

2014 2015

Release of provisions (in € m)

Allocation of result for limiting premiums

Health: stable premium revenue and lower operating costs

Health insurance

Premium revenues for basic insurance increased mainly through transfer of parts of the former AWBZ

Increase in number of insured with supplementary insurance

Lower cost ratio as consequence of initiatives around Acceleration & Innovation

Decreasing premium on supplemental insurances as consequence of lower number of insured in basic health and lower cover

Basic Insurance

Claims ratio increased mainly through allocation of €481 million from the incidental result

Supplemental insurance

Claims ratio higher due to lower premium income and decreased availability of provisions through increasing health costs.

20 | Achmea Jaarresultaten 2015

Supplemental insurance (in %)

Gross written premiums (in € m)

Basic insurance (in %)

Basic Supplemental

Claims ratio Expense ratio Claims ratio Expense ratio

93.9 95.1

11,825 11,881

2015

12,179

1,310

2014

11,881

1,359

2014

98.7%

95.1%

3.6%

2015

98.7%

95.5%

3.2%

2014

93.0%

82.2%

10.8%

2015

96.4%

87.3%

9.1%

Operational costs (in € m)

634592

2014 2015

Pension & Life: Further decreases in costs

Pension & Life

Lower gross written premiums through the sale of lower priced insurances and natural premium run-off. Further more, in 2014 there was a one-off higher premium revenue through the large, multiple year single premiums drawn up in that year

The operational result more than doubled through good investment results and better technical results

Better investment results driven through the recovery of the property market and realisations achieved through adjusting the equity portfolio

Continued focus on cost reduction leads to a good starting position for sustainable management ‘closed book’ in pensions

Operating expenses 7% reduced as result of less complexity and streamlining of IT.

21 | Achmea Jaarresultaten 2015

Operational result (in € m)

Operating expenses (in € m)

Gross written premiums (in € m)

New sales (APE) (in € m)

495729

Annual premium

Single premium

2014

2,485

1,756

2015

2,160

1,665 64

165

2014 2015

197

122

2014 2015

378348

2014 2015

International: higher results in Greece, Turkey, Slovakia and Ireland

International activities

Increased profitability in Greece, Turkey, Slovakia and Ireland

The total increase in premiums of 5% in countries where we are active

Doubling of operational result to €52 million partly due to nonrecurring items

Corrected for the nonrecurring items, the operational result increased by 15% to €30 million

The sale of unprofitable units contributes to the improvement of the result

Turkey

Increased share in the Non-Life market. Gross written premiums increased by 20% despite devaluation of the Lira

Greece

Increased market share due in particular to growth in online channel with Anytime

Slovakia

Premium revenue increased by 8% due to growth in online sales through Onlia

Number of online customers up by 12%.

22 | Achmea Jaarresultaten 2015

Operational result (in € m)

Gross written premiums (in € m)

1,109

2014 2015

1,123

26

52

2014 2015

Other activities

Banking activities

Improved operational result due to higher interest margin, lower costs and release of credit provisions

Important role of Achmea Bank within pension strategy

Strategic focus of Staalbankiers on ‘private banking activities’

Achmea Investment Management

Achmea Investment Management started with managed assets of over €102 billion as of 1 January 2016

Managed assets of existing customers in 2015 increased by €4.2 billion, resulting in higher management fees

Other activities

Positive development of results for pension services, property management and Independer

Further cost reduction in staff and facility services.

23 | Achmea Jaarresultaten 2015

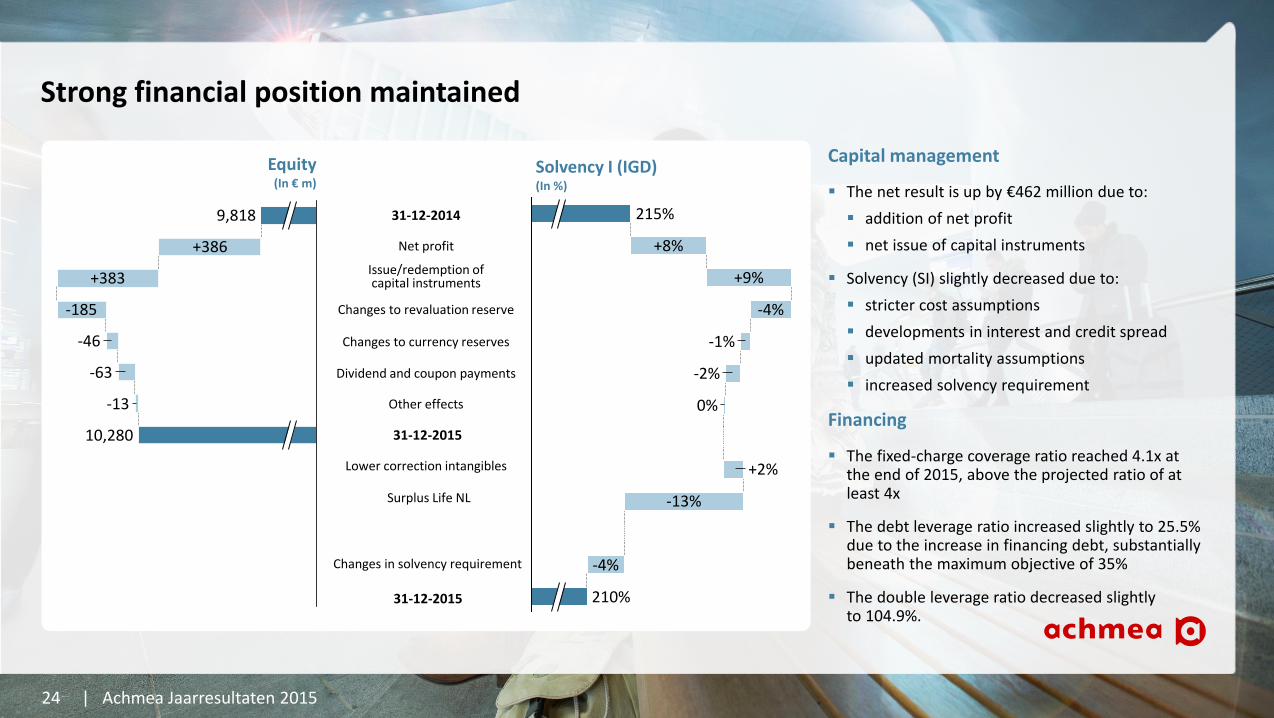

Strong financial position maintained

Capital management

The net result is up by €462 million due to:

addition of net profit

net issue of capital instruments

Solvency (SI) slightly decreased due to:

stricter cost assumptions

developments in interest and credit spread

updated mortality assumptions

increased solvency requirement

Financing

The fixed-charge coverage ratio reached 4.1x at the end of 2015, above the projected ratio of at least 4x

The debt leverage ratio increased slightly to 25.5% due to the increase in financing debt, substantially beneath the maximum objective of 35%

The double leverage ratio decreased slightly to 104.9%.

24 | Achmea Jaarresultaten 2015

9,818

-46

10,280

+383

+386

-185

-13

-63

Net profit

Issue/redemption of capital instruments

Changes to currency reserves

Dividend and coupon payments

Changes to revaluation reserve

Other effects

31-12-2015

Lower correction intangibles

31-12-2015

31-12-2014

+8%

+9%

215%

-4%

-1%

210%

0%

-4%

-2%

+2%

-13%

Equity (In € m)

Solvency I (IGD) (In %)

Changes in solvency requirement

Surplus Life NL

Solvency II position strong

Solvency

Approval was received from DNB for the internal model for Solvency II for non-life

Solvency II ratio increased to 185% as of Q2 2015

Main factors for available and required capital:

Addition of results and issuance of capital instruments

Rising stock markets and increasing investments in mortgages

Adjustment of products within the life portfolio

Adjustments to models.

25 | Achmea Jaarresultaten 2015

Solvency II PIM (approved model) 30-06-2015 31-12-2014 D

Available capital € 10,504 million €9,471 million 11%

Required capital €5,664 million €5,547 million 2%

Solvency II ratio (PIM) 185% 171% 14%-pt

30-06-2015 31-12-2014 D

Solvency II ratio (SF) 182% 169% 13%-pt

Quality of investment portfolio remains high

Total investment portfolio

Slight decrease in the investment portfolio due to increase in market interest

Fixed income portfolio

86% of portfolio invested in fixed income securities with investment grade rating (BBB or higher). Slight decrease in rating profile relative to 2014 through expansion of mortgages (NR*)

Mortgage portfolio has risen by €2.2 billion to €3.8 billion at year end 2015

Financing of the mortgage portfolio through Government bonds

Exposure was also expanded to other illiquid fixed income securities such as WSW loans, Senior Real Estate and Senior Secured Loans.

26 | Achmea Jaarresultaten 2015

Total investment portfolio 31-12-2015 (in %)

Fixed income portfolio 31-12-2015 (in %)

Fixed income portfolio 31-12-2014 (in %)

2

3

3

6

8

3

75Fixed income securities

Real estate

Alternative investments

Other investments

Shares

Derivatives

Deposits

46.0 €

billion

2

3

3

6

8

4

74

Deposits

Fixed income securities

Derivatives

Alternative investments

Shares

Real estate

Other investments

Total investment portfolio 31-12-2014 (in %)

48.3 €

billion

1

1

23

3

14

14

39

4

Convertible bonds

Fixed income securities

Corporate bonds

Secured bonds

Asset-backed bonds

Loans and mortgages

GOV-related and GOV-guaranteed bonds

Government bonds

34.6 €

billion

35.7 €

billion

1

1

25

5

4

6

10

48

GOV-related and GOV-guaranteed bonds

Loans and mortgages

Convertible bonds

Secured bonds

Corporate bonds

Asset-backed bonds

Fixed income securities

Government bonds

* Not rated

Higher investment result due to realisation of equities and fixed income securities

Investment results

Investment result for own account €47 million higher than in 2014

Direct investment results

Direct investment results on fixed income securities strongly influenced by low interest rate

Higher dividend from investment funds (including private equity and infrastructure) heightens direct investment results in shares

Indirect investment results

Indirect investment results in real estate improved by lower impairments

Higher realisations in fixed income securities due to mandate changes

Higher indirect results for shares due to realisations. This increase is however partly cancelled out by lower results in commodities

Realised and unrealised results in fixed income securities in Pension & Life do not form part of the profit and loss account but run through the FFA (Fund for Future Appropriation)

The scope of the FFA in 2015 is €6.2 billion (2014: €6.7 billion).

27 | Achmea Jaarresultaten 2015

90

38

1,273

+47

Investment result own

account 2015

1,320 6

Other Indirect income

Direct income Investment result own

account 2014

Changes in investment results¹ own account Achmea Group

¹The investment results own account is adjusted for fair value results and other investment yields that have a direct relationship with insurance requirements.

Program

General overview

Financial overview

Questions

28 | Achmea Jaarresultaten 2015

Consistently solid in a dynamic environment

Net profit increases to €386 million

Acceleration & Innovation in full flow:

Leader in online and mobile services

Reduction in operating costs on schedule; €300 million reduction realised

Chosen for strong positioning in pension market with Centraal Beheer APF

Achmea Investment Management oversees over €100 billion Assets under Management

Financial position solid with solvency ratio of 210% under Solvency I

A+ credit rating for insurance entities by S&P.

29 | Achmea Jaarresultaten 2015