Embed Size (px)

DESCRIPTION

Pricing Maturity Guarantee with Dynamic Living Benefit. 숭실대학교 정보통계 보험수리학과 고방원 [email protected]. I-1. Dynamic Fund Protection. 풋옵션을 업그레이드한 보증유형 (A Strengthened Version of Put Option) 계약기간 동안 펀드 계좌의 금액이 보증수준 K 이하로 떨어지지 않도록 보증 펀드 계좌의 금액이 K 이하가 되면 보증 판매자는 적당한 금액을 즉시 펀드에 추가하도록 설계 - PowerPoint PPT Presentation

Citation preview

I-1. Dynamic Fund Protection

• 풋옵션을 업그레이드한 보증유형 (A Strengthened Version of Put Option)

- 계약기간 동안 펀드 계좌의 금액이 보증수준 K 이하로 떨어지지 않도록 보증

- 펀드 계좌의 금액이 K 이하가 되면 보증 판매자는 적당한 금액을 즉시 펀드에 추가하도록 설계

- 흔히 Reset Guarantee 라 불림

I-2. Dynamic Fund Protection

• F(t) : 시간 t 에서의 unprotected 펀드계좌의 잔고

• 시간 t 에서의 DFP 펀드계좌의 잔고

•

:)(~

tF

Protection Level K

Time t

)(~

tF

F(t)

F(0)

I-3. Dynamic Fund Protection

• H. Gerber & E. S. W. Shiu (1998, 1999) - Dynamic fund protection 도입- Perpetual protection- Ruin theory approach

• H. Gerber & G. Pafumi (2000) - A closed form expression for finite time protection- Geometric Brownian motion

• J. Imai & P. P. Boyle (2001), H-K. Fung & L. K. Li (2003)- CEV (Constant Elasticity of Variance) process

- Discretely monitored protection- Numerical approach

• H. Gerber & E. S. W. Shiu (2003)- Dynamic fund protection with stochastic barrier- Optimal exercise strategy

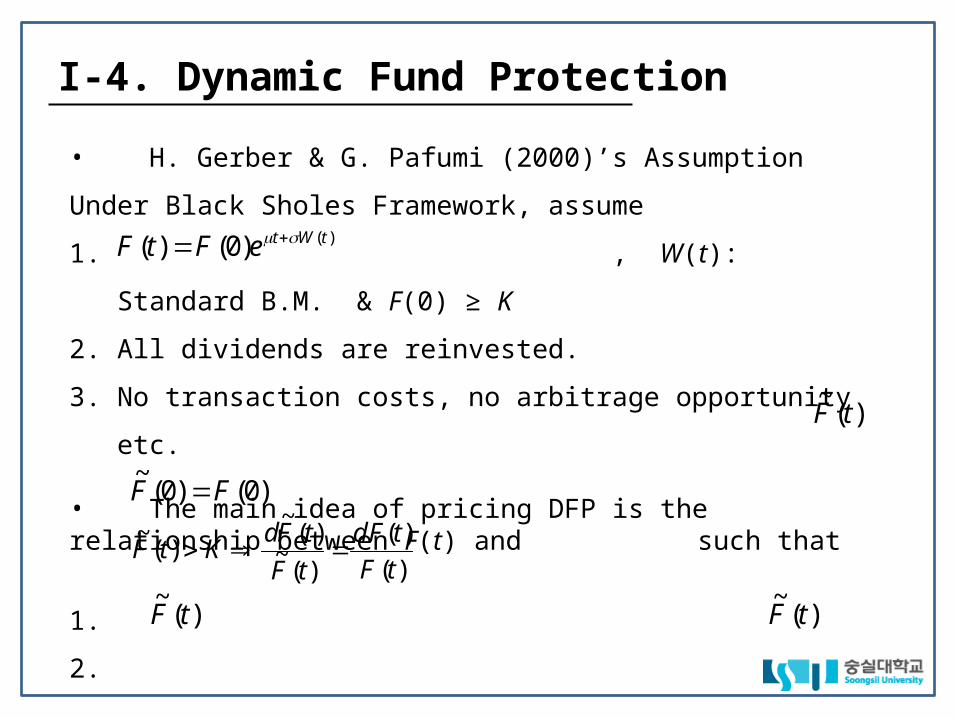

I-4. Dynamic Fund Protection

• H. Gerber & G. Pafumi (2000)’s Assumption

Under Black Sholes Framework, assume

1. , W(t): Standard B.M. & F(0) ≥ K

2. All dividends are reinvested.

3. No transaction costs, no arbitrage opportunity etc.

• The main idea of pricing DFP is the relationship between F(t) and such that

1.

2.

3. If drops to K, just enough money will be added so that

does not fall below K.

)()0()( tWteFtF

)(~

tF

)0()0(~

FF

)(

)(

)(~

)(~

)(~

tF

tdF

tF

tFdKtF

)(~

tF )(~

tF

I-5. Dynamic Fund Protection

More precisely,

Why?

1. Consider as the number of fund units.

2. Note that n(0) = 1 & n(t) is nondecreasing.

3.

4. The equal sign is chosen to minimize the guarantee cost.

See Gerber & Shiu (2003).

)(

max,1max)()(~

0 sF

KtFtF

ts

tssF

KsntsKsnsFsF 0,

)()(0,)()()(

~

)(max)(0 sF

Ksn

ts

)(

max,1max)(0 sF

Ktn

ts

I-6. Dynamic Fund Protection

• An interpretation of the process

Consider when

After simple algebra,

By Graversen and Shiryaev (2000), we recognize as

a reflecting Brownian motion with drift = μ, volatility = σ, started at

0)(~

ttF

0

)(~

ln

tK

tF.)0()( )(tWteFtF

.)(max,)0(

lnmax)()(

~ln

0

sWs

K

FtWt

K

tFts

0

)(~

ln

tK

tF

.)0(

lnK

F

I-7. Dynamic Fund Protection

• A useful result about a reflecting B. M. with drift from Graversen and

Shiryaev (2000)

For any

where satisfies the stochastic differential equation

• Sometimes, |μt + W(t)| is called a reflecting B. M. with drift.

,)()(max,max)(0

tYsWsytWtlaw

ts

,, RR y

0)( ttY

.)0(),()(sign)( yYtdWdttYtdY

( )t W t

0 0

)(max,max0

sWsyts

y y

I-8. Dynamic Fund Protection

)(tY

t t

I-9. Dynamic Fund Protection

• For a reflecting B. M. with drift, an explicit expression of the transi-

tion density is available.

- See Cox & Miller (1965) for the derivation.

Let denote the probability that a reflecting B.M.

started at will be observed in the interval between x and

x + dx after time T.

dxTK

Fxp

,)0(

ln;

K

F )0(ln

T

TKFxe

TTK

Fxn

F

KTT

K

FxnT

K

Fxp

x

/)0(ln1

2

,)0(

ln;)0(

,)0(

ln;,)0(

ln;

2

2

2

2

2

2

2

I-10. Dynamic Fund Protection

• Pricing formula for DFP – Gerber & Pafumi (2000)

By the fundamental theorem of asset pricing,

And,

After some tedious calculation, one may obtain the following formula:

cost. guarantee DFP)0()(~

EQ FTFe rT

.,)0(

ln;E)(~

E0

/)(~

lnQQ

dxT

K

FxpeKeeKeTFe xrTKTFrTrT

I-11. Dynamic Fund Protection

• Pricing formula for DFP – Gerber & Pafumi (2000)

T

TFKe

rKe

T

TeF

K

F

KrK

T

TeF

K

F

KrK

T

TFKe

FT

TFKe

rKe

rT

rTrT

r

rTr

rTrT

rT

22

22

2

22

2

222

21

)0(ln

221

)0(ln

)0(

2

Price)Put Scholes-(Black BSP

21

)0(ln

)0(

2

21

)0(ln

)0(21

)0(ln

21cost guarantee DFP

2

2

I-12. Dynamic Fund Protection

• Esscher Transform

Discussion paper by Y-C. Huang and E. S. W. Shiu (2000, NAAJ) derives

the pricing formula by using the reflection principle and the method

of Esscher Transforms.

I-13. Dynamic Fund Protection

• Numerical Illustration – Table 3 from Gerber & Pafumi (2000)

When F(0) = 100, T = 1, σ = 0.2, r = 0.04

• Interesting Fact

One may verify that

K 80 85 90 95 100

European Put Price 0.7693 1.4654 2.5315 4.0325 6.0040

DFP Price 1.7709 3.4239 6.0120 9.7476 14.7931

Ratio 2.30 2.34 2.37 2.42 2.46

.)0(any for 2BSP

Price Guarantee DFPlim

0KF

T

II-1. Maturity Guarantee with DLB

• Maturity Guarantee with Dynamic Living Benefit 의 제안

- 펀드의 잔고가 미리 정한 일정 수준 (B) 을 넘어가면 그 초과액을 고객에게 배당금과 같은 형태로 바로 지급하고 만약 만기일에 펀드잔고가 보장수준 (K) 이하로 떨어지면 부족한 부분을 보장

• Maturity Guarantee with Dynamic Living Benefit 의 제안 배경

- 변액연금에서 GLB (Guaranteed Living Benefit) 상품인 GMWB, GMIB, GMAB 의 선택비율이 높음

- Dynamic Fund Protection 의 쌍대 (Dual) 문제로 명시적 가격 결정공식 유도가 가능

- B 와 K 를 동시에 조정 , Dynamic Fund Protection 보다 Cheap

F(0)

Protection Level K

Deficit covered by protection issuer

B

DLB payment level

II-2. Maturity Guarantee with DLB

II-3. Maturity Guarantee with DLB

• F(t) : 시간 t 에서의 펀드계좌의 잔고

• 시간 t 에서의 DLB 를 지급하는 펀드계좌의 잔고

• F(t) 와 의 관계식

이 성립함

:)(ˆ tF

)(ˆ tF

)(

min,1min)()(ˆ0 sF

BtFtF

ts

II-4. Maturity Guarantee with DLB

• Under the same framework with Gerber and Pafumi (2000),

1.

2. 0 < K ≤ F(0) = 1 ≤ B

3. Denote k = ln K, b = ln B (k ≤ 0 ≤ b)

4. VL(B, T): time-0 value of the aggregate DLB payments

5. VP(K, B, T): time-0 value of the maturity guarantee with payoff

6. Investor pays 1 + VP(K, B, T) at the beginning of the contract.

)(ˆ tFK

1)0( F

II-5. Maturity Guarantee with DLB

• Similarly in DFP,

Thus, the process is a reflecting B. M. started at b with

drift (– μ), volatility σ, and reflecting barrier at 0.

• The pricing formulas for VL(B, T) and VP(K, B, T) can be found

by using the transition density.

.)(max,max)()(ˆ

ln0

sWsbtWttF

Bts

)(ˆ/ln tFB

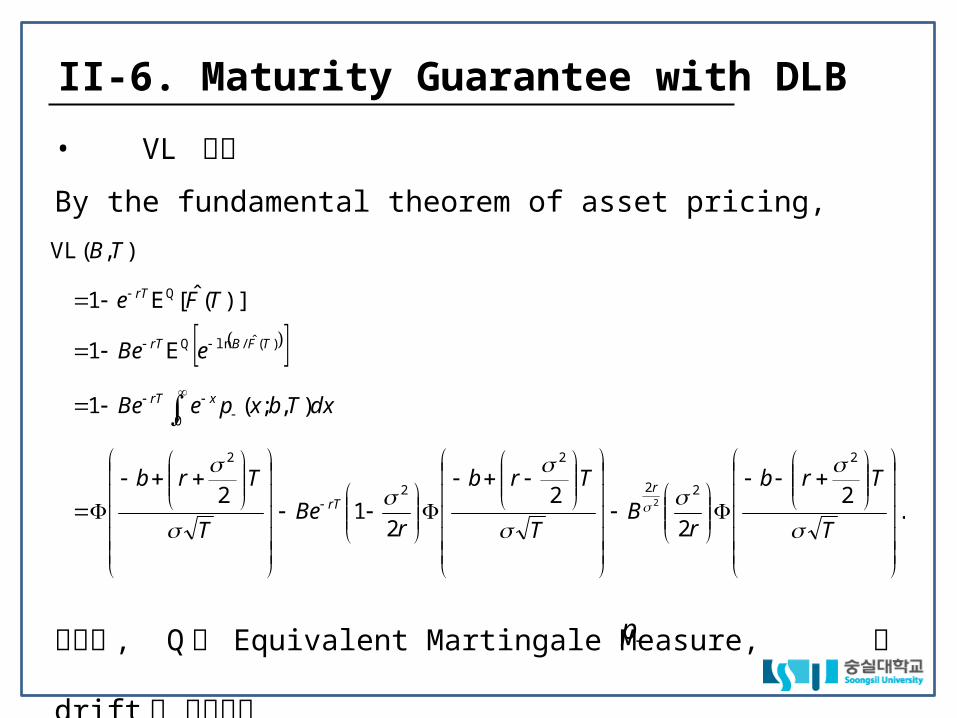

II-6. Maturity Guarantee with DLB

• VL 공식

By the fundamental theorem of asset pricing,

여기서 , Q 는 Equivalent Martingale Measure, 은 drift 가

반대부호

.2

2

2

21

2

),;(1

E1

)](ˆ[E1

),(VL

2

22

2

2

2

0

)(ˆ/lnQ

Q

2

T

Trb

rB

T

Trb

rBe

T

Trb

dxTbxpeBe

eBe

TFe

TB

rrT

xrT

TFBrT

rT

p

II-7. Maturity Guarantee with DLB

• VP 공식

T

Trbk

rB

T

Trbk

re

B

KK

T

Trk

T

Trk

Ke

dxTbxpBeKe

BeKeTFKe

TBK

rrT

r

rT

KB

xrT

TFBrTrT

2

2

2

22

2

22

),;(

E)(ˆE

),,(VP

2

212

2

212

22

)/ln(

)(ˆ/lnQQ

22

II-8. Maturity Guarantee with DLB

• In the derivation of the pricing formulas, we have used two extensions from

Gerber and Pafumi (2000, NAAJ):

• Similarly with DFP,

Because VP ≥ BSP, the sum of the last terms should always be positive.

.11

1

,,;

22

22

2

1

22

12

ae

c

ae

cdx

xe

caedxxne

ccac

a

cx

cc

a

cx

T

Trbk

rB

T

Trbk

re

B

KKTBK

rrT

r

22

2

22

2BSP),,(VP

2

212

2

212

22

II-9. Maturity Guarantee with DLB

• The pricing formulas can be derived by using the method of Esscher

Transforms.

• The pricing formulas can be easily extended to the case with exponen-

tially varying barriers.

• Numerical Illustration – 1 (r = 5%, σ = 20%)

0

0.2

0.4

0.6

0.8

1.0

20 40 60 80 Maturity (Years)

: B = 1.0

: B = 1.5

: B = 2.0

: B = 2.5

II-10. Maturity Guarantee with DLB

VL(B, T)

0

0.02

0.04

0.06

0.08

20 40 60 80 Maturity (Years)

0.10 K = 1.0

K = 0.9

K = 0.8

K = 0.7

K = 0.6

• Numerical Illustration – 2 (r = 5%, σ = 20%)

II-11. Maturity Guarantee with DLB

VP(K, B, T)

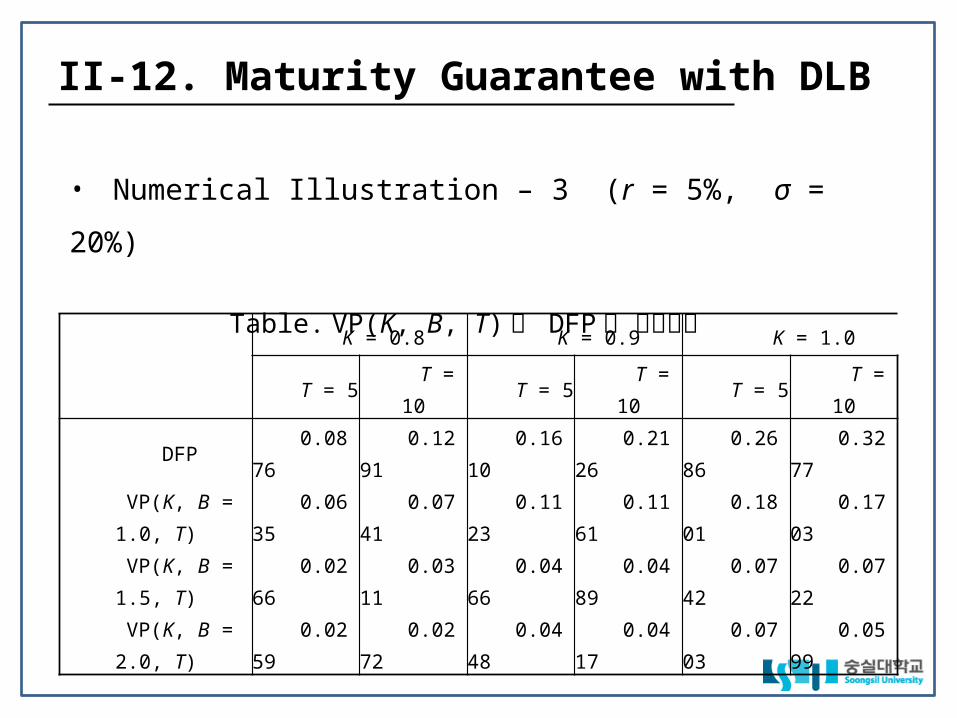

• Numerical Illustration – 3 (r = 5%, σ = 20%)

Table. VP(K, B, T) 와 DFP 의 가격비교

K = 0.8 K = 0.9 K = 1.0

T = 5 T = 10 T = 5 T = 10 T = 5 T = 10

DFP 0.0876 0.1291 0.1610 0.2126 0.2686 0.3277

VP(K, B = 1.0, T) 0.0635 0.0741 0.1123 0.1161 0.1801 0.1703

VP(K, B = 1.5, T) 0.0266 0.0311 0.0466 0.0489 0.0742 0.0722

VP(K, B = 2.0, T) 0.0259 0.0272 0.0448 0.0417 0.0703 0.0599

II-12. Maturity Guarantee with DLB

0

1

2

3

4

Maturity (Years)8 12 16

B = 1.2

B = 1.1

B = 1.0

: K = 1.0

: K = 0.9

: K = 0.8

• Numerical Illustration – 4 (r = 5%, σ = 20%)

VP(K, B, T) 와 European Put Price 의 가격비

II-13. Maturity Guarantee with DLB

II-14. Maturity Guarantee with DLB

• Asymptotic Result

By the asymptotic formula in Abramowitz and Stegun (1972), it can

be shown that for 0 < K ≤ 1,

.1),(BSP

),1,(VPlim

,2),(BSP

),1,(VPlim

0

0

TK

TBK

TK

TBK

T

T

0

0.1

1 2 3 4

0.2

0.3

0.4

K = 1.0

K = 0.9

K = 0.8

VL(B, T = 5)

VP(K, B, T = 5)

B

Break-even if B = 2.01

• Numerical Illustration – 5 (r = 5%, σ = 20%)

II-15. Maturity Guarantee with DLB

II-16. Maturity Guarantee with DLB

• Future Research

1. For reflected processes more general than Brownian Motion, see Linetsky (2005).

2. What if reflection is replaced by refraction? See, for example, Gerber & Shiu

(2006).

Withdrawal Level

Protection Level

참고문헌

• Abramowitz, M. and Stegun, I. (1972) Handbook of Mathematical Functions. Dover

Publications: New York

• Cox, D. R. and Miller, H. (1965) The Theory of Stochastic Processes. Chapman &

Hall

• Fung, H-K. and Li, L. K. (2003) Pricing Discrete Dynamic Fund Protections. North

American Actuarial Journal 7(4): 23-31.

• Graversen, S. E. and Shiryaev, A. N. (2000) An Extension of P. Lévy’s Distributional

Properties to the Case of a Brownian Motion with Drift. Bernoulli 6(4): 615-620.

• Gerber, H. U. and Pafumi, G. (2000) Pricing Dynamic Investment Fund Pro-

tection. North American Actuarial Journal 4(2): 28-37. Discussion Paper by

Huang, Y-C. & Shiu, E. S. W.

• Gerber, H. U. and Shiu, E. S. W. (1998) Pricing Perpetual Options for Jump

Processes. North American Actuarial Journal 2(3): 101-107.

• Gerber, H. U. and Shiu, E. S. W. (1999) From Ruin Theory to Pricing Reset

Guarantees and Perpetual Put Options. Insurance: Mathematics and Econom-

ics 24(1): 3-14.

• Gerber, H. U. and Shiu, E. S. W. (2003) Pricing Perpetual Fund Protection with

Withdrawal Option. North American Actuarial Journal 7(2): 60-92.

• Gerber, H. U. and Shiu, E. S. W. (2006) On Optimal Dividends: From Reflection

to Refraction. Journal of Computational and Applied Mathematics 186: 4-22.

• Imai, J. and Boyle, P. P. (2001) Dynamic Fund Protection. North American Actuarial

Journal 5(3): 31-51.

• Linetsky, V. (2005) On the Transition Densities for Reflected Diffusions. Advances

in Applied Probability 37: 435-460.