-

8/6/2019 Priyank - Nuclear Energy Potential

1/34

2011

By : Priyank Jadav

School of Petroleum Management,

Gandhinagar

Nuclear Energy PotentialDo renewable sources of energy pose real

challenge to non-renewable ones?

-

8/6/2019 Priyank - Nuclear Energy Potential

2/34

Nuclear Energy Potential 2011

School of Petroleum Management, Gandhinagar 2 | P a g e

ACKNOWLEDGEMENT

It is my pleasure to acknowledge all those whose inspiration and

wisdom helped me in

completing my project. I would like to extend my gratitude to

EMERSON for giving me an

opportunity to make a project on very warm issue of nuclear

energy.

I would like to thank Mr. Sachin Sehgal for informing me about

the TALENT QUEST. I would

also like to thanks Poorva Chandra Shekhar and Mausam Joshi from

HR Department,

Emerson Process Management (India) Pvt. Ltd. for continuous

updating me and encouraging

for working hard to meet the project requirement and

deadlines.Lastly I would like to thank

my colleagues for the constant moral support.

Priyank Jadav

MBA 2nd

Year

School of Petroleum Management, Gandhinagar.

-

8/6/2019 Priyank - Nuclear Energy Potential

3/34

Nu r E r P t ti 2011

Sc

of Pe

ole

Manage

ent, Gandhinagar 3 |P a g e

Ex utiv Summ r

Statisticssays that in 2008, worlds total energycons

tion was 143,851 TWh and

near about 87% of total energy was produced by

non-renewablesources and only 13% of

total energy was produced by renewable sources If we see present

power generation

capacity of India, then 6819% energy is produced by

non-renewable sources and only

31.81% of total energy was produced by renewable sources. The

statistics say that

renewable energy sources do not pose real challenge to

non-renewable energy sources.

Renewable energy sources produces causes less pollution and

produced less green house

gases ascompared to non- renewableenergysources. Because

renewable resources do not

run out, they can power generators indefinitel y. Also, once

initial startup costs are taken

care of, these alternative fuels eventually pay for themselves.

But, unfortunately, some

renewable resources are not very reliable. Power generation from

renewable energy

sources iscostlier and it can be produced only at theselected

places where these resources

are available. Renewable energy sources like solar, tidal, wind

etc are impossible to

transport like coal, oil and other fossil fuels. Also e

uipments and machineries used to

produce power from renewable energysources are verycostly and at

present, there is no

technological support available to bring down power generation

cost by renewableenergy

sources and make them comparable with cost of power production

by non-renewable

energysources.

Current nuclear waste in the US is over 90% Uranium. If

reprocessing were made

legal again in the US we would haveenough nuclear material to

last 100s ofyears. Nuclear

power provides about 6% of the world's energy and 1314% of the

world's electricity.

Worlds total nuclear power generation capacity is 378,910MW with

the highestcontribution of U.S. with 101,229MW. In India, currently

20 nuclear reactors produce

4780MW which is only2.9% of total installed base. There are five

more nuclear projects are

under construction with 9 reactors and total production capacity

of 6700MW. India is

epected to generate an additional 25,000 MW of nuclear power by

2020, bringing total

estimated nuclear power generation to 45,000 MW. Based on

India's known commercially

-

8/6/2019 Priyank - Nuclear Energy Potential

4/34

Nu r E r P t ti 2011

School of Petroleum Management, Gandhinagar 4 |P a g e

viable reserves of 80,000 to 112,000 tons of uranium, this

represents a 40 to 50 years

uranium supply for India's nuclear power reactors. This domestic

reserve of 80,000 to

112,000 tons of uranium (approx 1% of global uranium

reserves

is largeenough to supply

all of India's commercial and military reactors as well as

supply all the needs of India's

nuclear weapons arsenal.

-

8/6/2019 Priyank - Nuclear Energy Potential

5/34

Nu r E r P t ti 2011

School of Petroleum Management, Gandhinagar 5|P a g e

Contents

INTRODUCTION ................................

................................ ................................

................................ .... 8

EVOLUTION OF NUCLEAR ENERGY ................................

................................ ................................

......... 10

PRESENT SCENARIO................................

................................ ................................

............................. 11

OPPORTUNITIES FOR NUCLEAR EXPANSION

................................ ................................

............................. 14

CHALLENGES FOR NUCLEAR EXPANSION

................................ ................................

................................ . 15

RISKS OF NUCLEAR PROJECTS AND THEIR CONTROL

................................ ................................

................. 19

URANIUM ................................

................................ ................................

................................ .......... 20

THORIUM ................................

................................ ................................

................................ .......... 25

ECONOMIES OF NUCLEAR POWER ................................

................................ ................................

......... 26

COMPARISON OF NUCLEAR TO RENEWABLE

................................ ................................

............................ 28

RADIOACTIVE WASTES-MYTHS AND

REALITIES................................

................................ ....................... 29

FUTURE SCENARIO ................................

................................ ................................

.............................. 31

CONCLUSION ................................

................................ ................................

................................ ...... 33

REFERENCES ................................

................................ ................................

................................ ...... 34

-

8/6/2019 Priyank - Nuclear Energy Potential

6/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 6 |P a g e

ListofFigures

Figure 1: Nuclear energyconsumption by region

................................ ................................

............... 9

Figure2: Nuclear Power production by top 10countriescompared to

India................................ .... 12

Figure 3: World Annual power sector CO2emission reductions

................................ ........................ 14

Figure 4: Contribution ofenergysources in electricity generation

in world and OECD countries ...... 15

Figure5: Evolution of Nuclear Power since 1991 to 2009

................................ ................................ .

15

Figure 6: Nuclear power project risk matrix

................................ ................................

..................... 19

Figure7: Risk control and monitoring in nuclear power

projects................................ ......................

20

Figure8: World Uranium Production and Demand

................................ ................................

........... 22

Figure 9: Uranium Production Cost Curve : 2007 - 2030

................................ ................................

... 23

Figure 10: Uranium SupplyScenario 2009

................................ ................................

........................ 25

Figure 11: Net Additions to Global Electricity Grid from New

Renewable and Nuclear (in GW) ......... 28

Figure 12: Electricity Production from Non-Fossil Fuel Sources

................................ ........................ 28

Figure 13: Future global electricity production

bysource................................

................................ . 32

-

8/6/2019 Priyank - Nuclear Energy Potential

7/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 7|P a g e

ListofTables

Table 1: World Energy & Indian Power Sector Scenario

................................ ................................

......8

Table2: Top 10 Countries by Nuclear Power production and

percentage share................................ 11

Table 3: India's operating nuclear power reactors

................................ ................................

........... 13

Table 4: Countries with Permanently Shutdown Nuclear Power

Reactors in the World..................... 18

Table5: Uranium Production and Recoverable Reserves

................................ ................................

.. 21

Table 6: The approx cost to get 1 kg of uranium as UO2 reactor

fuel................................ ................ 26

Table7: Construction Time of Nuclear Power Plants Worldwide

................................ ...................... 27

Table8: Estimates investment in nuclear energy in the BLUE Map

scenario................................ ...... 31

-

8/6/2019 Priyank - Nuclear Energy Potential

8/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 8|P a g e

IN

R

UC

ION

In 2008, worlds total energyconsumption was 143,851 TWh and near

about 87% of

total energy was produced by non-renewable sources and only 13%

of total energy was

produced by renewablesources. If wesee present power generation

capacity of India, then68.19%energy is produced by

non-renewablesources and only 31.81% of total energy was

produced by renewable sources. The statistics say that renewable

energy sources do not

pose real challenge to non-renewableenergysources. In the world,

only5.8% of total power

production is from nuclear.

Table 1: World Energy & Indian Power Sector Scenario

World Energy by power source2008

Power Sector Indi

- 2010

TWh % MW %

Oil 48204 33.50% Thermal 111294.5 65.38%

Coal 38497 26.80% Nuclear 4780 2.81%

Gas 30134 20.90% Hydro 37367.4 21.95%

Nuclear 8283 5.80% RES 16786.98 9.86%

Hydro 3208 2.20% Total 170228.9 100%

Other RE 15284 10.60% Source: Ministry of Power - Annual Report

2010

Others 241 0.20%

Total 143 851 100%

Source: IEA =solar, wind, geothermal and

biofuels

Renewableenergysources (RES) are alternatives available to meet

increasing energy

demand but they cant replace non-renewable energy sources for

energy generation. RES

are alternative not the substitute of Non-RES. Power generation

from non-renewable

energysources ischeaper than renewableenergysources. Hence, cost

of generation is low

and profit margin can becomparatively higher. Non-renewable

resources helped bring the

age of tomorrow, today. With theexception of nuclear power

plants, using these r esources

-

8/6/2019 Priyank - Nuclear Energy Potential

9/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 9 |P a g e

to create energy is fairly simple. Even after all these

advantages of fossil fuel, one thing is

sure that one day they will eventually run out and these fuels

are also responsible for many

types of pollution and green houseeffect. And unfortunate ly, as

powerful as nuclear power

plants are, they generate nuclear waste, which iscannot be

recycled, isvery dangerous to

the environment, and cannot be cleaned or reduced through

filtration systems. These

arguments lead us to think about an alternative solution which

is renewableenergysources.

Figure 1: Nuclearenergyconsumption byregion

Renewable energy sources produces causes less pollution and

produced less green

house gases ascompared to non- renewableenergysources. Because

renewable resources

do not run out, they can power generators indefinitely. Also,

once initial startup costs are

taken care of, these alternative fuels eventually pay for

themselves. But, unfortunately,

some renewable resources are not very reliable. Power generation

from renewableenergy

sources iscostlier and it can be produced only at theselected

places where these resources

are available. Renewable energy sources like solar, tidal, wind

etc are impossible to

transport like coal, oil and other fossil fuels. Also e uipments

and machineries used to

produce power from renewable energysources are verycostly and at

present, there is no

technological support available to bring down power generation

cost by renewableenergy

sources and make them comparable with cost of power production

by non-renewable

energysources.

-

8/6/2019 Priyank - Nuclear Energy Potential

10/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 10|P a g e

EVOLUTION OF NUCLEARENERGY

y 1938 Scientistsstudy Uranium nucleus y 1941 Manhattan Project

begins y 1942 Controlled nuclear chain reactiony 1945 U.S. uses two

atomic bombs on Japany 1949 Soviets develop atomic bomby 1952 U.S.

tests hydrogen bomby 1955 First U.S. nuclear submarine

From the late 1970s to about 2002 the nuclear power

industrysuffered some decline

and stagnation. Few new reactors were ordered, the number coming

on line from mid

1980s little more than matched retirements, though capacity

increased by nearly one third

and output increased 60% due to capacity plus improved load

factors. Theshare of nuclear

in world electricity from mid 1980s was fairlyconstant at

16-17%. Many reactor orders from

the 1970s werecancelled. The uranium price dropped accordingly,

and also because of an

increase in secondary supplies. Oil companies which had entered

the uranium field bailed

out, and there was a consolidation of uranium producers.

By 1989 there were a total of 424 reactors operating in the

world. A historic peak

was reached in 2002 with 444 units, five more than the 439

operating reactors as of August

2010. In 2009 the 370 GW of nuclear capacity generated about

2,600 TWh a 1.3% decline,

the third in a row that is about 13% of commercial electricity

or 5.5% of commercial

primaryenergy, or between 2% and 3% of all energy in the world

all on a downward trend.

-

8/6/2019 Priyank - Nuclear Energy Potential

11/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 11 |P a g e

PRESENT SCENARIO

Nuclear power provides about 6% of the world'senergy and 1314%

of the world's

electricity. Worlds total nuclear power generation capacity is

378,910MW with the highest

contribution of U.S. with 101,229MW. Today there are some 440

nuclear power reactorsoperating in 30countries plus Taiwan, with a

combined capacity of over 376 GWe. In 2009

these provided 2560 billion kWh, about 15% of the world's

electricity. Over 60 power

reactors arecurrently being constructed in 15countries.

In India, currently20 nuclear reactors produce 4780MW which is

on ly2.9% of total

installed base. Based on India's known commercially viable

reserves of 80,000 to 112,000

tons of uranium, this represents a 40 to 50years uranium supply

for India's nuclear power

reactors. This domestic reserve of 80,000 to 112,000 tons o f

uranium (approx 1% of global

uranium reserves) is largeenough to supply all of

India'scommercial and military reactors as

well assupply all the needs of India's nuclear weapons

arsenal.

Table2: Top 10 Countries by Nuclear Power production and

percentage share

Top 10 Countries in Nuclear Power

production

Top 10 Countries by share of

NuclearPower

Ran

Country Production (TWh) Ran

Country Share (%)

1 USA 807.1 1 France 74.1

2 France 410.1 2 Slovakia 51.8

3 Japan 280.3 3 Belgium 51.1

4 Russia 159.41 4 Ukraine 48.1

5South

Korea141.9

5 Hungary 42.1

6 Germany 133 6 Armenia 39.4

7 Canada 85.5 7 Sweden 38.1

8 Ukraine 84 8 Switzerland 38

9 Mainland 70.1 9 Slovenia 37.3

10 Spain 59.3 10 Czech 33.3

-

8/6/2019 Priyank - Nuclear Energy Potential

12/34

Nuclear Energy Potential 2011

School of Petroleum Management, Gandhinagar 12 | P a g e

Fi

ure2: Nuclear Powerproduction bytop 10 countriescompared to

India

Statistics shows that India is still far behind in terms of

nuclear power development.

Due to trade bans and lack of indigenous uranium, India has

uniquely been developing a

nuclear fuel cycle to exploit its reserves of thorium. Now,

foreign technology andfuel are

expected to boost India's nuclear power plants considerably. All

plants will have high

indigenous engineering content. India has a vision of becoming a

world leader in nuclear

technology due to its expertise in fast reactors and thorium

fuel cycle. India has a flourishing

and largely indigenous nuclear power program and expects to have

20,000 MWe nuclear

capacity on line by 2020 and 63,000 MWe by 2032. It aims to

supply 25!

of electricity from

nuclear power by 2050. Presently India has 20 reactors with

total production capacity of

4385 MWe.

807.1

410.1

280.3

159.41 141.9 13385.5 84 70.1 59.3

20.5

Produ tion (TWhProduction (TWh)

-

8/6/2019 Priyank - Nuclear Energy Potential

13/34

Nuclear Energy Potential 2011

School of Petroleum Management, Gandhinagar 13 | P a g e

Table 3 " Ind# a $%

op & ' a ( # ngnu ) 0 & a ' po 1 & ' rea ) ( ors

India'soperating nu2

lear po 3 er reactors

Reactor State Type Mwe Operation

Tarapur 1 & 2 Maharashtra BWR 150 1969

4 aiga 1 & 2 4 arnataka PHWR 202 1999-2000

4 aiga 3 & 4 4 arnataka PHWR 202 2007

4akrapar 1 & 2 Gujarat PHWR 202 1993-95

Madras 1 & 2 (MAPS) Tamil Nadu PHWR 202 1984-86

Narora 1 & 2

Uttar

Pradesh PHWR 202 1991-92

Rajasthan 1 Rajasthan PHWR 90 1973Rajasthan 2 Rajasthan PHWR 187

1981

Rajasthan 3 & 4 Rajasthan PHWR 202 1999-2000

Rajasthan 5 & 6 Rajasthan PHWR 202

Feb & April

2010

Tarapur 3 & 4 Maharashtra PHWR 490 2006, 05

Advantages & DisadvantagesofNuclear Energy

ADVANTAGES

Relatively low fuel cost

Suitable for baseloadcapacity

Long life time

Low external costs Guarantee for energy

supply

Capacity development

Low carbon emission

DISADVANTAGES

Highly capital intensive

Sensitive to interest rates

Long lead times

Long payback periods

Regulatory/policy risks New financing structures

required to attract privateinvestors

-

8/6/2019 Priyank - Nuclear Energy Potential

14/34

Nuclear Energy Potential 2011

School of Petroleum Management, Gandhinagar 14 | P a g e

OPPORT 5 NITIES FOR N 5 CLEAR EXPANSION

The analysis in Energy Technology Perspectives 2010 (ETP) (IEA,

2010) projects that

energy-related CO2 emissions will double from 2005 levels by

2050. Strategies for reducingenergy-related CO2 emissions by 50 6

from 2005 levels by 2050, concludes that nuclear

power will have a large role to play in achieving this goal in

the most cost-effective manner

(Figure 1). Nuclear capacity is assumed to reach about 1 200 GW

by 2050, providing about

24% of global electricity supply.

Although the growth of nuclear energy has stalled in the last

two decades, it is a

mature technology with more than 50 years of commercial

operating experience that does

not require major technological breakthroughs to enable its

wider deployment. Providing

around 38% of global electricity by 2050, would reduce the

average electricity generation

cost in 2050 by about 11%. One factor that sets nuclear apart

from most other low-carbon

energy technologies is that, in some countries at least,

adopting or expanding a nuclear

programme will be the subject of considerably greater public and

political opposition.

Fi7

ure3: World Annualpowersector CO2emission reductions

Source: IEA, 2010

Keypo 8 n 9 @ Nuclearpo A er ma B es a major con 9 ribu 9 ion

toreducingCC 2 emissions

0%

17%

0%

28%

2%1%1%

51%

CO2emission reduction

Uranium Production by

Country, 2010

Country

Australia

Brazil

Canada

-

8/6/2019 Priyank - Nuclear Energy Potential

15/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 15|P a g e

Figure 4:

Contributionofenergysourcesinelectricitygenerationin

world and OECDcountries

Source: IEA, 2009

Key point: Nuclear and hydropower are the main low-carbon energy

sources at present.

.

CHALLENGES FORNUCLEAREXPANSION

Figure 5: EvolutionofNuclearPowersince 1991 to 2009

Source: IAEA PRIS

Key point: The average operating performance of nuclear power

plants improved markedly in the

1990s and early 2000s, but has fallen in the last few years.

-

8/6/2019 Priyank - Nuclear Energy Potential

16/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 16 |P a g e

Safety

Although no plant design can be risk-free, new research has

brought claims of a new

generation of nuclear reactors with advanced safety features.

However, they haveyet to be

tested at full scale, and all reactors now on order

useconventional technology. Moreover,

nuclear power plants are now considered plausible targets for

terrorist attacks. Whether

caused by accident or malice, a sudden dispersal of radio

activity would have severe

community impact, perhaps exacerbated by inade D uateevacuation

plans. Ifsuch an event

triggered a renewal of anti-nuclear sentiment in the general

public and led to demands for a

nuclear moratorium, the resilience and sustainability of

theenergysystem would be greatly

compromised.

Cost

The full economic costs of nuclear energy are difficult to

determine. A comprehensive

accounting would include accident insurance, safety assurance,

decommissioning, and

radioactive waste disposal costs that are often buried in

generous publicsub sidies for the

nuclear industry or shifted to future generations. As

theexperience in the U.S. with the first

wave of nuclear plants indicated, projected costs can soar as

the full costs of the nuclear

fuel-cycle are reflected in the price ofelectricity. Ofcourse,

high costs might not be a key

issue if nuclear power were the only option for climate

mitigation.

Waste Storage&UraniumRecyclingThe need to safely dispose of

long-lived, highly radioactive waste for tens of thousands of

years poses daunting technical challenges. Indeed, as no country

has yet implemented a

functioning long-term waste repository, much of the worlds

inventory of waste remains

seD

uestered in temporary casks at dispersed plant sites. It reD

uires considerable

technological optimism to be sanguine about finding satisfac

tory geologic repositories:

2,000 reactors would reD

uire new capacity the size of the controversial Yucca

Mountain

storagesite in the United Statesevery few years into the

foreseeable future. It is difficult to

imagine that this level of storage capacity could be found and

activated. Indeed, after 20

years and $9 billion of investment.

Proliferation

Nuclear power cannot be decoupled from nuclear weapons. Two

paths lead from a nuclear

energy program to weapons-grade material; one involves uranium

and the other plutonium.

-

8/6/2019 Priyank - Nuclear Energy Potential

17/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 17|P a g e

For use as a nuclear fuel, naturally occurring uranium

undergoesen richment to increase the

concentration of the fissionable U-235 isotope, and further

enrichment can produce

weapons-grade material. ConseE

uently, a wide deployment of nuclear power and

associated technology would increase the risk of nuclear weapons

proli feration. This link is

underscored in todays headlines on disputes over enrichment

programs in North Korea and

Iran, putatively for electricity generation, possibly for

more.

Security

Another pathway from nuclear power to nuclear weapons would be

through the recovery of

plutonium from spent uranium fuel, either directly or as a

by-product of re-processing. A

meresix kilograms ofsuch highly fissible plutonium is needed for

a simple nuclear weapon,

and much less to fabricate a dirty conventional bomb. At t he

large scale of nuclear

generation under consideration, it would becomeextremely

difficult to track and secure the

movement ofsuch small amounts of material.

OtherChallenges:

y Financing the large investments needed, especially where

nuclear construction is tobe led by the privatesector.

y Developing the necessary industrial capacities and skilled

human resources tosupport sustained growth in nuclear capacity.

y Expanding the supply of nuclear fuel in line with increased

nuclear generatingcapacity, and ensuring all users of nuclear

energy have access to reliablesupplies of

fuel.

y Implementing plans for building and operating geological

repositories for thedisposal ofspent fuel and high-level

radioactive wastes.

y Maintaining and strengthening where necessary the safeguards

and security forsensitive nuclear materials and technologies, to

avoid their misuse for non -peaceful

purposes.

y In the past, because of above mentioned challenges, 124

nuclear power reactors(37,788 MWe) wereclosed down permanently.

-

8/6/2019 Priyank - Nuclear Energy Potential

18/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 18|P a g e

Table 4: Countries with Permanently Shutdown Nuclear Power

Reactors in the World

CountryEnergy Output PermanentlyClosed

Total MW(e) Nuclear Power Reactors

United States 9,764 28

U.K. 3,301 26

Germany 5,879 19

France 3,789 12

Japan 1,618 5

Russia 786 5

Bulgaria 1,632 4

Italy 1,423 4

Ukraine 3,515 4

Canada 478 3

Slovakia 909 3

Sweden 1,210 3

Lithuania 2,370 2

Spain 621 2

Armenia 376 1

Belgium 10 1

Kazakhstan 52 1

Netherlands 55 1

World Total: 37,788 124

-

8/6/2019 Priyank - Nuclear Energy Potential

19/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 19 |P a g e

RISKS OF NUCLEARPROJECTS AN F THEIRCONTROL

Structuring a nuclear new-build project for success reG

uires the identification and

understanding of the various risks associated with a project of

such magnitude and

complexity. Some risks are quite similar to those in any power

investment project; others are clearly unique to nuclear. In

developing a project, a utility will undertake a

comprehensive risk assessment, which will be reviewed and

updated as the project

progresses.

Nuclear projects are capital intensive, with long project

schedules. They hav e

significant fixed operating and maintenancecosts and relatively

low fuel costs. Theyexist in

a rigorous regulatoryenvironment where the regulator actively

patrols plant operations and

has considerable authority to impact unit construction and

operations. Nuclear plants are

also subject to public scrutiny and concern. In normal

operation, nuclear plants are

environmentally friendly. At thesame time, publicconcerns often

focus on the questions of

long-term management of nuclear waste and potential consequences

of low-probability

safetyevents.

Figure 6: Nuclearpowerprojectriskmatrix

Source: Economics Report, WNA, 2010

-

8/6/2019 Priyank - Nuclear Energy Potential

20/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 20|P a g e

Figure 7: Riskcontrol andmonitoringinnuclearpowerprojects

Source: Economics Report, WNA, 2010

URANIUM

Production & Demand

About 435 reactors with combined capacity of over 370 GWe,

require77,000 tonnes

of uranium oxideconcentratecontaining 65,500 tonnes of uranium

(tU ) from mines (or the

equivalent from stockpiles or secondarysources) each year.

Thecapacity is growing slowly,

and at the same time the reactors are being run more

productively, with higher capacity

factors, and reactor power levels. However, these factors

increasing fuel demand are offset

by a trend for increased efficiencies, so demand is dampened -

over the20years from 1970

-

8/6/2019 Priyank - Nuclear Energy Potential

21/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 21 |P a g e

there was a 25% reduction in uranium demand per kWh output in

Europe due to such

improvements, which continue today.

Each GWe of increased capacity will require about 200 tU/yr of

extra mine

production routinely, and about 400 -600 tU for the first fuel

load. Fuel burnup is measured

in MW days per tonne U, and many utilities are increasing the

initial enrichment of their fuel

(eg from 3.3 to more than 4.0% U-235) and then burning it longer

or harder to leave only

0.5% U-235 in it (instead of twice this).

Table5: Uranium Production and Recoverable Reserves

Uranium Production by

Country, 2010

Uranium Recoverable Reserves by

Country, 2009

Country Production (tU) Country Reserves Percentage

Australia 5900 Australia 1673000 31.0%

Brazil 148 Kazakhstan 651000 12.0%

Canada 9783 Canada 485000 9.0%

China 827 Russia 480000 9.0%

Czech

Republic

254 South

Africa

295000 5.0%

India 400 Namibia 284000 5.0%

Kazakhstan 17803 Brazil 279000 5.0%

Namibia 4496 Niger 272000 5.0%

Niger 4198 USA 207000 4.0%

Russia 3562 China 171000 3.0%

South Africa 583 Jordan 112000 2.0%

Ukraine 850 Uzbekistan 111000 2.0%

United States 1660 Ukraine 105000 2.0%Uzbekistan 2400 India

80000 1.5%

Others 799 Mongolia 49000 1.0%

Total 53633 other 150000 3.5%

World 5404000 100%

Source: WNA, 2010

-

8/6/2019 Priyank - Nuclear Energy Potential

22/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 22|P a g e

Coal ash is easily-accessible though minor uranium resource in

many parts of the

world. In central Yunnan province in China thecoal uranium

content varies up to 315 ppm

and averages about 65 ppm. The ash averages about 210 ppm U

(0.021%U) - above thecut-

off level for some uranium mines. The Xiaolongtang power station

ash heap contains over

1000 tU, with annual arisings of 190 tU. Recovery of this by

acid leaching is about 70%.

Figure 8: World UraniumProduction andDemand

Source: WNA, 2010

Cost

Looking ten years ahead, the market is expected to grow

significantly. The WNA

reference scenario shows a 33% increase in uranium demand over

2010-20 (for a 27%

increase in reactor capacity - many new cores will be required).

Demand thereafter will

depend on new plant being built and the rate at which older

plant is retired - the reference

scenario has a 16% increase in uranium demand for the decade to

2030. Licensing of plantlifetime extensions and the economic

attractiveness of continued operation of older

reactors arecritical factors in the medium-term uranium market.

However, with electricity

demand by 2030 expected (by the OECD's International Energy

Agency, 2008) to double

from that of2004, there is plenty ofscope for growth in nuclear

capacity in a greenhouse -

conscious world.

-

8/6/2019 Priyank - Nuclear Energy Potential

23/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 23 |P a g e

Figure 9: UraniumProductionCostCurve : 2007 - 2030

The above graph, from International Nuclear Inc. as of end of

2007, shows a cost

curve for world uranium producers, and suggests that for 50,000

tU/yr production from

mines (approximately the present level) and up to 60,000 tU/yr,

US$30/lb plus profit marg in

is a plausible price. Costs may now haveescalated somewhat, but

htecost curve only rises

steeply at higher uranium requirements.

Supply

Mines in 2009 supplied some 60,000 tonnes of uranium oxide

concentrate (U 3O8)

containing 50,772 tU, about 78% of utilities' annual

requirements. The balance is made up

from secondary sources including stockpiled uranium held by

utilities, but those civil

stockpiles are now largely depleted. The perception of imminent

scarcity drove the "spot

price" for non-contracted sales to over US$ 100 per pound U3O8

in 2007 but it hassettled

back to $40-45 over the twelve months to July 2010. Most uranium

however is supplied

under long term contracts and the prices in new contracts have,

in the past, reflected a

premium above thespot market.

-

8/6/2019 Priyank - Nuclear Energy Potential

24/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 24 |P a g e

Supplyfromelsewhere

As well asexisting and likely new mines, nuclear fuel supply may

be from secondarysources

including:

y Recycled uranium and plutonium from spent fuel, as mixed oxide

(MOX) fuely Re-enriched depleted uranium tails y Ex military

weapons-grade uraniumy Civil stockpilesy Ex-military weapons-grade

plutonium, as MOX fuel.

Major commercial reprocessing plants are operating in France and

UK, with capacity

of over 4000 tonnes of used fuel per year. The product from

these re -enters the fuel cycle

and is fabricated into fresh mixed oxide (MOX) fuel elements.

About 200 tonnes of MOX is

used each year, equivalent to less than 2000 tonnes of U3O8 from

mines. Military uranium

for weapons isenriched too much higher levels than that for the

civil fuel cycle. Weapons-

grade is about 97% U-235, and this can be diluted about 25:1

with depleted uranium (or

30:1 with enriched depleted uranium) to reduce it to about 4%,

suitable for use in a power

reactor.

From 1999 to 2013 the dilution of 30 tonnessuch material is

displacing about 10,600

tonnes per year of mine production. The USA and Russia have

agreed to dispose of 34

tonneseach of military plutonium by2014. Most of it is likely to

be used as feed for MOX

plants, to make about 1500 tonnes of MOX fuel which will

progressively be burned in civil

reactors.

The following graph suggests how thesevarioussources ofsupply

might look in the decades

ahead:

-

8/6/2019 Priyank - Nuclear Energy Potential

25/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 25|P a g e

Figure 10: Uranium Supply Scenario 2009

Source: WNA 2009 World reference scenario

THORIUM

Another potential nuclear fuel, thorium, is plentiful in one or

two Latin American

countries (Brazil, and to a much lesser extent Venezuela).

However, currently there is

limited interest in developing a thorium-based fuel cycle, apart

from in India. Indeed, there

is such little demand for thorium currently that there is little

exploration for it. There are

significant conflicts in the estimates of world thorium

reserves. The 2005 IAEA-NEA Red

Book suggests a probable thorium reserve of 4.5 million tons

worldwide, though

acknowledges that the lack of figures for many parts of the

world makes this little more

than an educated guess. It is nevertheless known that thorium is

3 to 4 times ascommon on

thesurface of theearth as uranium.

According to some figures, Australia has the largest reserves,

with India coming

second, each with about 25% the worlds total. However, both the

IAEA and OECD put Brazil

at the top of the list by a significant amount, over Turkey then

India.

-

8/6/2019 Priyank - Nuclear Energy Potential

26/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 26 |P a g e

ECONOMIES OF NUCLEARPOWER

Nuclear energy is competitive with fossil fuels for electricity

generation, despite

relatively high capital costs and the need to internalise all

waste disposal and

decommissioning costs. If thesocial, health and environmental

costs of fossil fuels are alsotaken into account, theeconomics of

nuclear power are outstanding

Table 6: The approx cost to get 1 kg of uranium as UO2 reactor

fuel

Theapproxcosttoget 1 kgofuraniumas UO2reactor

fuel

Kg

Cost

($) TotalC

ostUranium 8.9 146 1299

Conversion 7.5 13 98

Enrichment 7.3 155 1132

Fuel Fabrication 1 240 240

Total 2768

At 45,000 MWd/t burn-up this gives 360,000 kWh electrical per

kg, hence fuel cost:

0.77c/kWh. Fuel costs are one area ofsteadily increasing

efficiency and cost reduction. For

instance, in Spain the nuclear electricity cost was reduced by

29% over 1995-2001. This

involved boosting enrichment levels and burn-up to achieve 40%

fuel cost reduction.

Prospectively, a further 8% increase in burnup will give another

5% reduction in fuel cost.

Uranium has the advantage of being a highlyconcentrated source

ofenergy which iseasily

and cheaply transportable. The quantities needed are very much

less than for coal or oil.

One kilogram of natural uranium will yield about 20,000 times as

much energy as thesame

amount ofcoal. It is therefore intrinsically a very portable and

tradablecommodity.

Nuclear power has a history of delays in construction, and

analysis undertaken by

the World Energy Council54 hasshown the global trend in

increased construction times for

nuclear reactors. In Germany, in the period from 1965 to 1976,

construction took 76

months, increasing to 110 months in the period from 1983 to

1989. In Japan average

construction time in the period from 1965 to 2004 was in the

range of 44 to 51 months.

-

8/6/2019 Priyank - Nuclear Energy Potential

27/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 27|P a g e

Finally in Russia, the average construction time from 1965 to

1976 was 57 months, then

from 1977 to 1993 it was between 72 and 89 months, but the four

p lants that have been

completed since then have taken around 180 months (15 years),

due to increased

opposition following the Chernobyl accident, economicconstraints

and the political changes

after 1992.

As per World Nuclear Industry Status Report 2009 , calculating a

global average

construction time it would be around nineyears for the 16 most

recent grid connections

does not make much sense because of the differences between

countries. Theconstruction

period for four reactorsstarted up in Romania, Russia and

Ukraine lasted between 18 and

24 years. In contrast, it took hardly more than five years on

average to complete the 12

units that wereconnected to the grid in China, India, Japan and

South Korea.

Table7: Construction Time of Nuclear Power Plants Worldwide

Period of

Reference

No. of

Reactors

Avg.

Construction

Time (Months)

1965-1970 48 60

1971-1976 112 66

1977-1982 109 80

1983-1988 151 98

1995-2000 28 116

2001-2005 18 82

2005-2009 6 77

Sources: Clerici, 2006; IAEA

-

8/6/2019 Priyank - Nuclear Energy Potential

28/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 28|P a g e

COMPARISON OF NUCLEAR TO RENEWABLE

Figure 11: NetAdditionsto Global Electricity Gridfrom New

Renewable

and Nuclear (in GW)

Source: Amory Lovins, 2010

Figure 12: ElectricityProductionfrom Non-Fossil Fuel Sources

Source: Earth Policy Institute, 2009

Figures 11 and 12 show the net additions to the grid from new

renewable (not

including large hydropower) and nuclear and the contributions of

all so -called low-carbon

-

8/6/2019 Priyank - Nuclear Energy Potential

29/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 29 |P a g e

energy sources to the global electricity mix. Although at first

glance these figures may

appear contradictory, they are two sides of the same narrative.

Figure 11 details the net

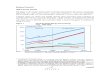

additions to the grid over the global grid over the last two

decades. Thesize of the individual

stations, coupled with theclosure of reactors, is why the

nuclear trend -line lacks an overall

direction, but it could be summarized to an average net annual

additional capacity of

around 2 GW per year in the beginning of the Speriod, compared

to a global installed

capacity ofsome 370 GW. However, this trend hasstagnated or

decreased since2005. Over

thesame period, wind power has increased itscapacity by over 10

GW on average per year,

with capacity additions steadily increasing to reach over 37 GW

in 2009.

RADIOACTIVE WASTES -MYTHS AND REALITIES

1. The nuclear industrystill has no solution to the 'waste

problem'Today, safe management practices are implemented or planned

for all categories of

radioactive waste. Low-level waste (LLW) and most

intermediate-level waste (ILW), which

make up most of the volume of waste produced (97%), are being

disposed of securely in

near-surface repositories in manycountriesso as to cause no harm

or risk in the long-term.

This practice has been carried out for manyyears in

manycountries as a matter of routine.

2. The transportation of this waste poses an unacceptable risk

to people and theenvironment

The primary assurance of safety in the transport of nuclear

materials is the way in

which they are packaged. Packages that store waste during

transportation are designed to

ensure shielding from radiation and containment of waste, even

under the most extreme

accident conditions. Since 1971, there have been more than

20,000safeshipments of highly

radioactive used fuel and high-level wastes (over 50,000 tonnes)

over more than 30 million

kilometres (about 19 million miles) with no property damage or

personal injury, no breach

ofcontainment, and very low radiation dose to the personnel

involved.

-

8/6/2019 Priyank - Nuclear Energy Potential

30/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 30|P a g e

3. Nuclear wastes are hazardous for tens of thousands of years.

This clearly isunprecedented and poses a huge threat to our future

generations in the long -term

International conventions define what is hazardous in terms of

radiation dose, and

national regulations limit allowable doses accordingly.

Well-developed industry technology

ensures that these regulations are met so that any hazardous

wastes are handled in a way

that poses no risk to human health or the environment. Waste is

converted into a stable

form that issuitable for disposal. In thecase of high-level

waste, a multi-barrier approach,

combining containment and geological disposal, ensures isolation

of the waste from people

and theenvironment for thousands ofyears.

4. Nobody knows the truecosts of waste management. Thecosts

areso high that nuclearpower can never beeconomic

Because it is widely accepted that producers of radioactive

wastes should bear the

costs of disposal, most countries with nuclear power programmes

make estimates of the

costs of disposal and update these periodically. International

organisations such as the

Nuclear Energy Agency (NEA) of the Organisation for Economic

Co-operation and

Development (OECD) have also coordinated exercises to compare

theseestimates with one

another. For low-level waste, the costs are well-known because

numerous facilities have

been built and have operated for manyyears around the world. For

high level-waste (HLW),cost estimates are becoming increasingly

reliable as projects get closer to imple mentation.

5. The wasteshould be disposed of into space The option of

disposal of waste into space has been examined repeatedlysince

the

1970s. This option has not been implemented and further studies

have not been performed

because of the high cost of this option and the safety aspects

associated with the risk of

launch failure.

-

8/6/2019 Priyank - Nuclear Energy Potential

31/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 31 |P a g e

FUTURE SCENARIO

Studies and statisticssay that nuclear energy will play a vital

role in energy market in

future. World is spending billions of dollars to develop

sustainabl e nuclear energy. All the

governments also support investments made in nuclear field

because now due to latesttechnologies, handling of nuclear energy

has becomesafer than earlier and nuclear energy

produce least CO2; it isclean source ofenergy.

Table8: Estimates investment in nuclear energy in the BLUE Map

scenario

Region/country Estimatedinvestmentrequired (USD billions)

2010-2020 2020-2030 2030-2040 2040-2050

US& Canada 75 342 243 224OECD Europe 60 333 105 88

OECD Pacific 68 296 153 97

China 57 193 295 350

India 9 57 91 230

Latin America 11 30 36 39

Other developing

Asia5 39 24 39

Economies in

transition55 156 80 39

Africa & Middle East 2 23 18 12

World 342 1469 1045 1118

The IEAs Energy Technology Perspectives 2010 BLUE Map scenario

(IEA, 2010) projects an

installed nuclear capacity of almost 1200 GW in 2050, compared

to 370 GW at the end of

2009, making nuclear a major contributor to cutting energy

related CO2emissions by50%.

This nuclear capacity would provide 9600 TWh ofelectricity

annually by that date, or around

24% of the electricity produced worldwide. IEA has projected

that by 2050, nuclear will

contribute highest in electricity generation in the world.

-

8/6/2019 Priyank - Nuclear Energy Potential

32/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 32|P a g e

Figure 13: Futureglobal electricityproduction bysource

Source: IEA, 2010

Key point: In the BLUE Map scenario, nuclear power is the

largest single source of electricity in 2050.

In India, nuclear power is growing at a rocket speed. As per

Indian Economy Review

March 2011, thermal power & hydro power generation recorded

growth of 6.7% and

18.68% while nuclear power generation recorded 78.77% growth

over the last year. In April

January2011, the all India power generation recorded a 5.18 %

growth compared to April

January 2010 and Nuclear power generation recorded 37.94% growth

till January in

current fiscal. In 12th five year plan is to add 100GW out of

which 3.4GW will be from

nuclear energy. India isexpected to generate an additional

25,000 MW of nuclear power by

2020, bringing total estimated nuclear power generation to

45,000 MW. There are five more

nuclear projects are under construction with 9 reactors and

total production capacity of

6700MW.

-

8/6/2019 Priyank - Nuclear Energy Potential

33/34

Nu rE r P t ti 2011

School of Petroleum Management, Gandhinagar 33 |P a g e

CONCLUSION

Above analysis and studyshows that nuclear energy has potential

market in near future. At

present, we have technology to develop nuclear power but its

very costly and takes long

time. It hassomeenvironmental and safety issues also to

takecare. Nuclear energy marketis growing at a very high speed and

to continue this growth there aresome points which all

the countries of the world should consider as near milestone in

nuclear energy

development.

Keynuclear powerdevelopmentmilestones include:

y Demonstrate the ability to build the latest nuclear plant

designs on time and withinbudget.

y Develop the industrial capacities and skilled human resources

to support sustainedgrowth in nuclear capacity.

y Establish the required legal frameworks and institutions in

countries where th ese donot yet exist.

y Encourage the participation of privatesector investors in

nuclear power projects.y Make progress in implementing plans for

permanent disposal of high-level

radioactive wastes.

y Enhance public dialogue to inform stakeholders about the r ole

of nuclear in energystrategy.

y Expand thesupply of nuclear fuel in line with increased

nuclear generating capacity.

-

8/6/2019 Priyank - Nuclear Energy Potential

34/34