Embed Size (px)

Citation preview

1

风向

China Insights 中国市场洞察中国市场洞察对中国的战略性投资:回答“如何?”和“谁?”之前先要问“为什么?”Strategic investing in China:to answer ‘how?’ and ‘who?’ fi rst know ‘why?’

Viewpoint 观点观点

揭开COO的神秘面纱Unmasking the COO mystery

Industry Focus 行业焦点行业焦点民以食为天,食以安为先For food, nothing is more important than safety

第一期 Issue 1 | 2014

3

风向

新年快乐!2014年伊始,我很高兴为大家介绍安永大

中华区全新的季刊《风向》杂志。

安永去年公布采用“EY”作为我们的全球品牌,并

以“建设更美好的商业世界”作为企业目标。

我们希望看到市场信任度提升,资本市场更加稳健,

投资者能掌握充分的信息以作决策。我们希望看到企

业持续增长、就业增加、消费意欲上扬,政府乐意投

资于民。我们也希望在人才培训和推动协作方面恪尽

本分。

《风向》是这个宏大蓝图的重要组件,旨在把安永丰

富的商业洞察带到大中华市场,同时建立一个新的渠

道与各利益关联方沟通,帮助他们及时洞悉市场最新

发展及行业趋势。通过这个渠道,我们能更接近客

户,更迅速和准确地回应他们的需求。

《风向》的作者背景多元,云集安永各行各业的专

家。季刊的内容广泛,然而主题都紧扣大中华市场。

创刊号内容非常丰富,探讨主题包括食品安全、社交

媒体和制药业的并购趋势;我们深入分析中国战略投

资的多种考虑因素、中国生产力,以及中国作为吸引

全球的新兴市场的潜能。此外,我们也有专文帮助企

业辨识首席营运官的合适基因。

如果您对某篇报道特别感兴趣,即可通过超连结阅读

有关报告全文。您也可联系相关作者和我们的编辑团

队,获取更多信息。

希望您喜欢《风向》,也欢迎您提供意见,协助我们

不断改进。

吴港平吴港平

安永中国主席

大中华首席合伙人

Happy New Year! At the beginning of 2014 I proudly introduce to you our new quarterly magazine On the Beam.

We launched our brand “EY” globally last year and set building a better working world our purpose.

We want to see trust increase in the world, so capital markets are strong and investors make informed decisions. We want to see businesses grow sustainably, employment rise, consumers spend and governments invest in their citizens. We want to do our part in developing talent and encouraging collaboration.

On the Beam fi ts perfectly into this ambitious blueprint – it contributes the rich EY thought leadership to the Greater China market and opens up an additional channel for us to communicate with our stakeholders and keep them abreast of the latest market and industry trends. Through this channel, we get closer to our clients and respond to them more quickly and precisely.

Our contributors are of diverse backgrounds but are all experts in their respective fi elds. This magazine covers a wide range of topics while maintaining a clear focus on the Greater China market.

In this debut issue, we look at food safety, social media, M&A trends in the pharmaceutical industry and much more. We provide in-depth analysis on strategic investment in mainland China, on the country’s productivity and potential as a developing market drawing the world’s attention. We help enterprises identify the right DNA for chief operating offi cers.

If you are interested in particular topics, you can read in greater detail by accessing the full reports online. You may also contact our contributors and editorial team for more information.

I hope you enjoy reading On the Beam. We welcome your feedback to help us improve the quality of this publication.

Albert NgChairman, China Managing Partner, Greater China

前言Foreword

通过这个渠道,我们能更接近客户,

更迅速和准确地回应他们的需求。

Through this channel, we get closer to our clients and respond to them more quickly and precisely.

“

“

4

On

the

BEA

M

5

风向

对中国的战略性投资:对中国的战略性投资:回答“如何?”和“谁?”之前先要问“为什么?”

Strategic investing in China: To answer ‘how?’ and ‘who?’ fi rst know ‘why?’

10

24

揭开揭开COOCOO的神秘面的神秘面

Unmasking the COO mystery

32

民以食为天,民以食为天,食以安为先食以安为先

For food, nothing is more important than safety

46

建设更美好的建设更美好的商业世界商业世界

Building a better working world

54

中国医药企业之中国医药企业之并购重组并购重组

Mergers and Acquisitions among China’s Pharmaceutical Enterprises

8866

税务透明与风险管理一体两面税务透明与风险管理一体两面

Tax Transparency and Risk Management: Two sides of the same coin

76驾驭盈利性增长,驾驭盈利性增长,

应对中国生产率挑战应对中国生产率挑战

Driving profi table growth: the productivity challenge in China

您是否已为国际财务报告准则您是否已为国际财务报告准则(IFRSIFRS)下一轮变化做好准备)下一轮变化做好准备?Are you ready for the next waves of changes to International Financial Reporting Standards (IFRS)?

84社群媒体社群媒体

企业两面刃企业两面刃

Social media:A double-edged sword for companies

第一期 Issue 1 | 2014

Inside...数字世界数字世界

World in numbers8

EY 安永安永 | Assurance 审计 | Tax 税务 | Transactions 财务交易 | Advisory 咨询

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confi dence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member fi rms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

www.ey.com/china

关于安永关于安永

安永是全球领先的审计、税务、财务交易和咨询服务机构之一。我们的深刻

洞察和优质服务有助全球各地资本市场和经济体建立信任和信心。我们致力

培养杰出领导人才,通过团队协作落实我们对所有利益关联方的坚定承诺。

因此,我们在为员工、客户及社会各界建设更美好的商业世界的过程中担当

重要角色。

安永是指Ernst & Young Global Limited的全球组织,也可指其一家或以上的成

员机构,各成员机构都是独立的法人实体。Ernst & Young Global Limited是英国一家担保有限公司,并不向客户提供服务。如欲进一步了解安永,请浏览

www.ey.com。

© 2014 Ernst & Young, China. All Rights Reserved. © 2014 安永,中国。版权所有。APAC no. 00000144 ED None.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specifi c advice.

本材料是为提供一般信息的用途编制,并非旨在成为可依赖的会计、税务或其他专业意见。请向您的顾问获取具体意见。

内文内文

Managing EditorAlbert Ng

EditorAnnesa Leung

Editorial teamClaudia ChuEllen WS ChanWinnie WY CheungTom Pauken

Design Andy YeungLeane Chan

Editor’s note: On The Beam is published exclusively for clients of EY. If you would like to receive copies of our publication or wish to suggest topics of interest to be covered in the future issues, please write to: The editor, On The Beam, EY at [email protected]

编辑的话:《风向》为安永客

户而刊发。如果您希望获取我

们的出版物或希望提出感兴趣

的课题,以便本刊跟进探讨,

请电邮安永《风向》编辑,

电邮地址:[email protected]

Printed by Yi Dun Printing Ltd上海奕顿印务技术有限公司

Contributors作者作者

吴港平吴港平 Albert Ng

安永中国主席

大中华首席合伙人

Chairman, China Managing Partner, Greater [email protected]

庞若柏庞若柏 Robert Partridge

大中华区财务交易咨询服务

主管合伙人

Managing PartnerGreater China Transaction [email protected]

麦耀波麦耀波 Yew-Poh Mak

亚太区运营交易合伙人

Partner, Transaction Advisory ServicesOperational Transaction Services, Asia-Pacifi [email protected]

孙毅孙毅 Arnold Sun

大中华区交易咨询合伙人

Partner, Transaction Advisory ServicesOperational Transaction Services, Greater [email protected]

Tom Pauken

Editor, Beijing [email protected]

丘昌和丘昌和 Tyrone Yau

审计合伙人

Partner, [email protected]

钱晓云钱晓云 Olivia Qian

审计合伙人

Partner, [email protected]

谢枫谢枫 Eric Feng Xie

审计合伙人

Partner, [email protected]

陈世宇陈世宇 Leo Chan

审计合伙人

Partner, [email protected]

钟育文钟育文 German Chung

审计合伙人

Partner, [email protected]

张耀樑张耀樑 Andy Cheung

大中华区审计服务主管合伙人

Managing Partner, Greater China [email protected]

许旭明许旭明 Steven Xu

安永中国金融服务部合伙人

Partner, [email protected]

侯捷侯捷 Jacky Hou

审计合伙人

Partner, [email protected]

张丽丽张丽丽 Lillian Zhang

审计合伙人

Partner, [email protected]

孙羽孙羽 Carrie Sun

审计經理

Manager, [email protected]

张腾龙张腾龙 Tony Chang

企业管理咨询服务执行副总经理

Managing Director, Advisory [email protected]

李志荣李志荣 Chee Weng Lee

大中华区企业税务服务主管

Greater China Business Tax Services [email protected]

唐荣基唐荣基 Walter Tong

大中华区税务服务主管合伙人

Managing Partner, Greater China Tax [email protected]

李海强李海强 Albert Lee亚太区税务绩效提升主管合伙人

Partner, Tax Performance [email protected]

孙新宇孙新宇 Karen Sun亚太区税务绩效提升高级经理

Senior Manager, Tax Performance [email protected]

黎俊伟黎俊伟 Nigel Knight

亚太区咨询服务主管合伙人

Managing PartnerAdvisory Services, Asia-Pacifi c [email protected]

刘国华刘国华 Lawrence Lau

审计合伙人

Partner, [email protected]

8

On

the

BEA

M

9

风向

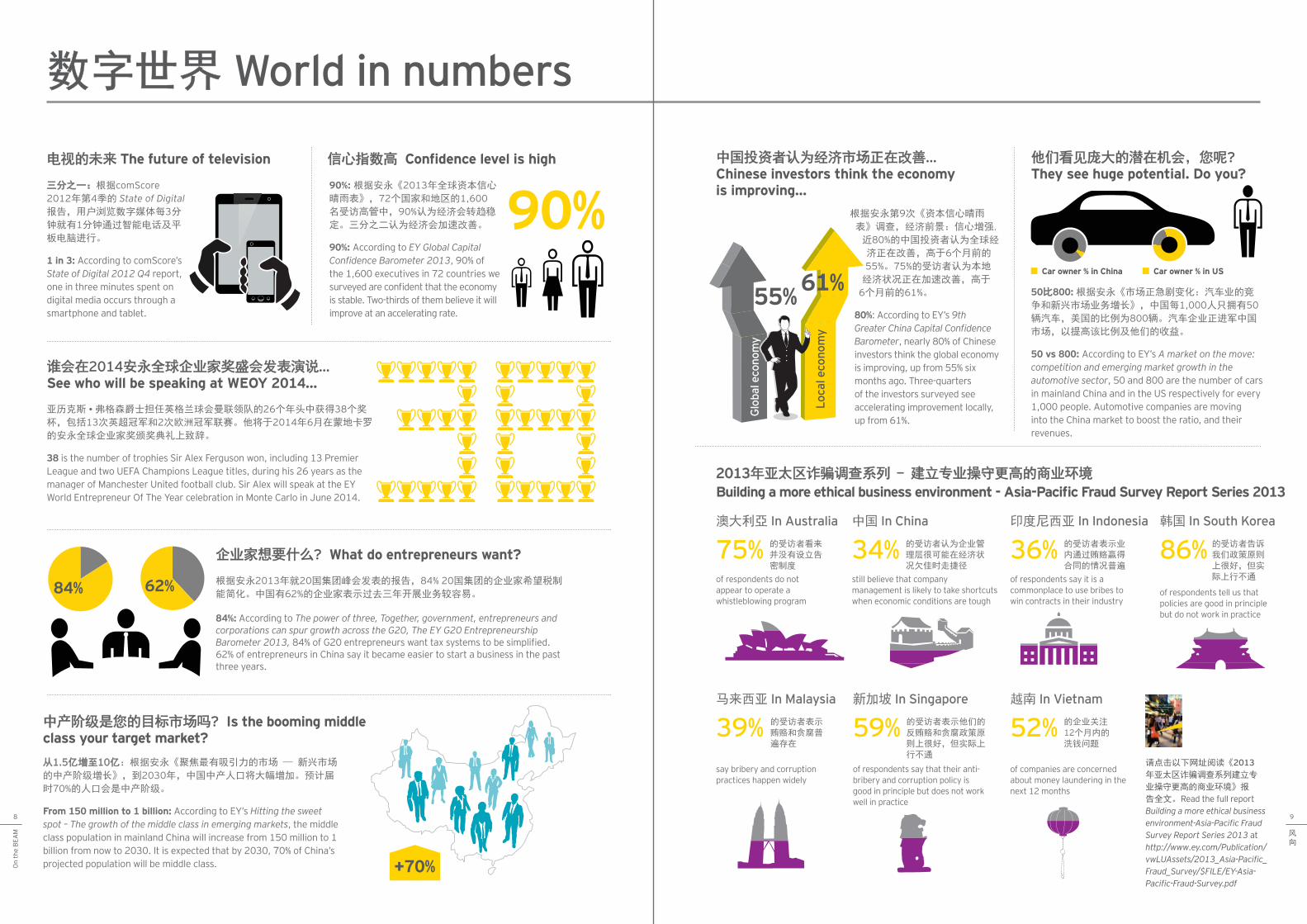

数字世界数字世界 World in numbers

企业家想要什么企业家想要什么? What do entrepreneurs want?

根据安永2013年就20国集团峰会发表的报告,84% 20国集团的企业家希望税制

能简化。中国有62%的企业家表示过去三年开展业务较容易。

84%: According to The power of three, Together, government, entrepreneurs and corporations can spur growth across the G20, The EY G20 Entrepreneurship Barometer 2013, 84% of G20 entrepreneurs want tax systems to be simplifi ed. 62% of entrepreneurs in China say it became easier to start a business in the past three years.

84% 62%

90%: 根据安永《2013年全球资本信心

晴雨表》,72个国家和地区的1,600名受访高管中,90%认为经济会转趋稳

定。三分之二认为经济会加速改善。

90%: According to EY Global Capital Confi dence Barometer 2013, 90% of the 1,600 executives in 72 countries we surveyed are confi dent that the economy is stable. Two-thirds of them believe it will improve at an accelerating rate.

三分之一:三分之一:根据comScore 2012年第4季的 State of Digital 报告,用户浏览数字媒体每3分钟就有1分钟通过智能电话及平

板电脑进行。

1 in 3: According to comScore’s State of Digital 2012 Q4 report, one in three minutes spent on digital media occurs through a smartphone and tablet.

电视的未来电视的未来 The future of television 信心指数高信心指数高 Confi dence level is high

90%

亚历克斯 • 弗格森爵士担任英格兰球会曼联领队的26个年头中获得38个奖

杯,包括13次英超冠军和2次欧洲冠军联赛。他将于2014年6月在蒙地卡罗

的安永全球企业家奖颁奖典礼上致辞。

38 is the number of trophies Sir Alex Ferguson won, including 13 Premier League and two UEFA Champions League titles, during his 26 years as the manager of Manchester United football club. Sir Alex will speak at the EY World Entrepreneur Of The Year celebration in Monte Carlo in June 2014.

谁会在谁会在2014安永全球企业家奖盛会发表演说安永全球企业家奖盛会发表演说…See who will be speaking at WEOY 2014…

中产阶级是您的目标市场吗中产阶级是您的目标市场吗? Is the booming middle class your target market?从1.51.5亿增至亿增至1010亿亿:根据安永《聚焦最有吸引力的市场 — 新兴市场

的中产阶级增长》,到2030年,中国中产人口将大幅增加。预计届

时70%的人口会是中产阶级。

From 150 million to 1 billion: According to EY’s Hitting the sweet spot – The growth of the middle class in emerging markets, the middle class population in mainland China will increase from 150 million to 1 billion from now to 2030. It is expected that by 2030, 70% of China’s projected population will be middle class. +70%

根据安永第9次《资本信心晴雨

表》调查,经济前景:信心增强,

近80%的中国投资者认为全球经

济正在改善,高于6个月前的

55%。75%的受访者认为本地

经济状况正在加速改善,高于

6个月前的61%。

80%: According to EY’s 9th Greater China Capital Confi dence Barometer, nearly 80% of Chinese investors think the global economy is improving, up from 55% six months ago. Three-quarters of the investors surveyed see accelerating improvement locally, up from 61%.

55% 61%

Loca

l eco

nom

y

Glob

al e

cono

my

他们看见庞大的潜在机会他们看见庞大的潜在机会,您呢您呢?They see huge potential. Do you?

中国投资者认为经济市场正在改善中国投资者认为经济市场正在改善…Chinese investors think the economy is improving…

50比800: 根据安永《市场正急剧变化:汽车业的竞

争和新兴市场业务增长》,中国每1,000人只拥有50辆汽车,美国的比例为800辆。汽车企业正进军中国

市场,以提高该比例及他们的收益。

50 vs 800: According to EY’s A market on the move: competition and emerging market growth in the automotive sector, 50 and 800 are the number of cars in mainland China and in the US respectively for every 1,000 people. Automotive companies are moving into the China market to boost the ratio, and their revenues.

Car owner % in China Car owner % in US

20132013年亚太区诈骗调查系列 - 建立专业操守更高的商业环境年亚太区诈骗调查系列 - 建立专业操守更高的商业环境

Building a more ethical business environment - Asia-Pacifi c Fraud Survey Report Series 2013

的受访者看来并没有设立告密制度

of respondents do not appear to operate a whistleblowing program

75%澳大利亞 In Australia

的受访者表示贿赂和贪腐普遍存在

say bribery and corruption practices happen widely

39%马来西亚 In Malaysia

中国 In China的受访者认为企业管理层很可能在经济状况欠佳时走捷径

still believe that company management is likely to take shortcuts when economic conditions are tough

34%

的受访者表示他们的反贿赂和贪腐政策原则上很好,但实际上行不通

of respondents say that their anti-bribery and corruption policy is good in principle but does not work well in practice

59%新加坡 In Singapore

的受访者告诉我们政策原则上很好,但实际上行不通

of respondents tell us that policies are good in principle but do not work in practice

86%韩国 In South Korea

的受访者表示业内通过贿赂赢得合同的情况普遍

of respondents say it is a commonplace to use bribes to win contracts in their industry

36%印度尼西亚 In Indonesia

的企业关注12个月内的洗钱问题

of companies are concerned about money laundering in the next 12 months

52%越南 In Vietnam

请点击以下网址阅读《2013年亚太区诈骗调查系列建立专

业操守更高的商业环境》报

告全文。Read the full report Building a more ethical business environment-Asia-Pacifi c Fraud Survey Report Series 2013 at http://www.ey.com/Publication/vwLUAssets/2013_Asia-Pacifi c_Fraud_Survey/$FILE/EY-Asia-Pacifi c-Fraud-Survey.pdf

10

On

the

BEA

M

11

风向

对中国的战略性投资:对中国的战略性投资:回答“如何?”和“谁?”之前先要问“为什么?”

Strategic investing in China: To answer ‘how?’ and ‘who?’ fi rst know ‘why?’

China Insight 中国市场洞察中国市场洞察

庞若柏庞若柏亚太区私募基金咨询服务主管合伙人大中华区财务交易咨询服务首席合伙人

Robert PartridgePrivate Equity Leader - Asia-Pacifi cTransaction Advisory Services LeaderGreater China

孙毅孙毅大中华区交易咨询合伙人

Arnold SunPartner, Transaction Advisory ServicesOperational Transaction ServicesGreater China

麦耀波麦耀波亚太区运营交易合伙人

Yew-Poh MakPartner, Transaction Advisory ServicesOperational Transaction ServicesAsia-Pacifi c

12

On

the

BEA

M

13

风向

中国市场充满着吸引力,仍然是外资投资的热点。中国的吸引力不仅来

自于作为面向北美和西欧的出口基地,更来自于其庞大的本地市场。

虽然近年来中国GDP增长可能放缓,但中国市场的扩张速度仍然远超

于大部分发达国家。最后,中国的地理位置十分理想,是亚洲,也是东欧、中东

和大洋洲等快速增长经济体的出口及物流基地。

对外国企业而言,投资中国往往可能涉及财务

交易。大部分企业需要通过并购行为来设立外

商独资企业或通过合资企业形式与一家本地企

业合作,进入中国市场。熟悉中国地区的人士

大都认可中国市场拥有庞大的发展机遇,但他

们也明了进行财务交易可能会面临的挑战。这

些挑战往往具有中国特色,因此即使经验丰富

的海外投资者都可能感到意外。

头等大事:不是“谁”,不是“如头等大事:不是“谁”,不是“如

何”,而是“为什么”何”,而是“为什么”?

选择的交易对手是“谁”。投资形式是“如

何”。可以说,成功投资中国的关键始于简单

的概念:了解自己。了解自己和了解“为什

么”十分关键。

要拥有自知意识,需要深入了解在中国市场上

理想的增长战略的细节。经常会有企业没有进

行类似初步分析就直接进入交易阶段。结果导

致他们往往目标不明确,期望不现实,可能因

此出现多种意料之外的事件,包括延误、交易

进展不理想和结果令人失望等等。

潜在投资者需要对中国业务的宏远目标深思熟

虑,目光着眼长远,既有批判性,也有战略

性。计划的中国业务重点是主要对全球或其他

地区的出口,还是致力进入本地市场(或两者

混合的方案)? 资本“耐性”有多大? 以短期

为目标,还是长期?

最后,企业会使用什么里程碑定义和标志成

功? 理想的结果是怎样? 我们建议寻求短期回

报的人士可能要去其他市场寻找合适目标。只

有明确这些,企业才能确定一项财务交易是否

有较大的成功几率。

就投资形式而言,也就是“如何”,多年来合

资企业一直是较好的财务交易形式。这是因为

过去中国市场限制较多,外资往往不能直接拥

有企业。目前,这一情况有很大改观。过去的

十到十五年,中国对很多行业在很大程度上放

松了管制。现在,外国投资者在所有权结构方

面有更大的自由度。

目前,是选择合资企业还是接近外商独资企业

的形式更多程度上取决于业务的战略和风险

考量。接着的问题是:投资者希望获得什么结

果? 投资者是否希望改变收购对象的文化及运

营,为其本地和全球增长做好准备? 投资者的

运营能力如何? 对要严格依赖本地管理人员运

营及取得业务成功的依赖程度有多大?

最后,企业能够承受多大的风险? 一般而言,

愿景越宏大,投资者越愿意增强控制及承担更

大风险,外商独资企业的形式就更合理。由此

推出,希望本地合作伙伴提供更多协助,及藉

此减少中国市场资本投入的投资者,则可能更

倾向于采用合资企业形式。

中国独有的风险中国独有的风险

的确,中国市场存在重大商机。可是企业同时

需要全面了解在中国进行财务交易的特定挑

战。除了考虑与所有财务交易相关的一般风险

外,投资中国市场必须考虑该市场的独特情

况。

首先,识别可行目标比较困难:“谁”。中国

是一个大国,市场庞大、复杂并具多样化。例

如,除民营企业以外,企业也需要考虑众多国

有企业,后者可能成为很有吸引力的交易对手

或目标。因此,投资者想要深入了解任何行业

都颇具挑战性。

有关挑战不但涉及竞争对手分析,也涉及深入

了解政府目标,以及监管环境可能造成的影

响。目前,中国很多行业的监管都已经放宽或

正在放宽。

表面上看来这可能是好消息,但同时也使竞争

格局更加复杂。在监管严格环境下发展良好的

本地企业可能在监管放开后逐渐或突然丧失优

势。例如消费品、农用器具或旅游业等行业之

前一直就处于监管度较高的环境,而现在环境

相对自由。这对整体经济形势是正面的,但也

可能会造成生产能力过剩、竞争激烈的局面,

只有适者才能生存。

14

On

the

BEA

M

15

风向

整体而言,中国正进入竞争出现深刻巨变的年代。投资

者必须付出努力才能建立对一个行业的战略性观点,

建立一个潜在交易对手清单则更难。然而下一步就是接

触潜在交易对手,并搜集更详细和更有针对性的企业信

息。这在不足够标准报告的国家特别具有挑战性。

本地企业,无论国有还是民营企业,在某程度上对外国

企业所需的报告形式并不熟悉。事实上,他们甚至可能

从未为自己的管理层搜集类似信息。因此,搜集所需数

据,作为初步估值所需的时间可能会比外企高管通常习

惯的正常时间要超出几个月之久。

此外,对外国投资者而言最终获得的信息可能在某些方

面不完整或不准确。对本地的认识和沟通技能在这种情

况下特别重要,因为如果没有准确信息,就需要对很多

工作进行推论。这就是中国市场的尽职调查需要由了解

复杂的信息需求,并且熟悉本地操作的人士扮演更重大

角色的主要原因之一。

行业分析后,就需要更深入了解监管法规的发展趋势,

然后是企业初步筛选,得出的潜在交易对手名单可能会

很长,也可能比较短,但关键在于被考虑的企业条件必

须符合战略考量。这些企业有什么能力? 强项在什么地

方? 什么能激励这些企业目前的所有者? 他们是否愿意与

外国投资者更进一步交易? 毫无疑问,对于匆忙地与不

合适的对手进行外商独资投资、合资企业或合伙制形式

的并购行为,应该尽量避免。

了解文化上的挑战了解文化上的挑战

财务交易的可能性增大以后,要必须充分考虑所有中国

独有的挑战,并考虑其文化风险。在中国要获得交易

对手明确的合作意向和认同可能特别困难,阻力往往更

难以捉摸,并不明显。除了与本地企业所有者开展讨论

外,外国投资者也需要更深入了解中层管理人员,甚至

工人的需求和权益。

挑战也包括合同条款的难以落实,因为不同文化往往对

协议有不同的解释。因此,必须与咨询人员协作,他们

不但了解条款的设立目的,也了解任何可能需要遵守的

本地惯例。另一文化冲突与中国司法制度有关。虽然法

制不断稳步发展,但利用司法制度解决纠纷仍然需时慢

且不可靠预测。

在中国的投资也可能会受到政府的广泛干预。虽然趋势

是更开放和放松监管,但过程漫长。政府不但很可能介

入交易前的协议,也出现过交易后,政府介入,进行再

次监管或重新协商的案例。因此,最好的战略之一是任

何交易一开始就将其定位为支持政府目标,例如,为政

府鼓励发展的行业或地区提供技术支持、流程方面的专

业知识、资本或品牌等。这一点并不容易,也不能保证

这样做就一定成功,但这就是最佳做法。

中国特定风险并不止于此。其它还包括知识产权和贿赂

行为等。虽然中国对知识产权的官方立场已在不断改

善,但中国文化还没有完全了解到企业拥有知识产权的

权利(因此出现专利或流程盗窃)。此外,很遗憾,利

益输送和贿赂仍然存在于某些行业的文化里。

因此在很多情况下,必须委任法务团队去调查贿赂、回

扣和其他违规事件的发生及其程度。如情况太严重,企

业可能被迫放弃该机会。可是,在很多其他情况下,外

国投资者可能有更大机会提高透明度,如检讨与供应商/

客户的商业条款,以及销售团队和采购人员的工资和激

励措施等。公开与被收购企业讨论这些问题,然后深入

介绍所建议的改变措施,着重沟通“新方法”为何不会

大幅改变相关状况往往是好的办法,企业往往也会因此

改变商业做法。

守规会得到回报守规会得到回报

如果匆忙建立中国业务,外国企业往往倾向于直接进行

交易而没有进行必要的前期分析。这往往会导致目标不

明确,期望不现实,最后出现更多意料之外及/或项目延

误,导致交易成果不理想或令人失望。如在前期多花点

时间,这种情况则可以避免。关键步骤包括:

• 阐述明确的战略:阐述明确的战略:企业需要有明确的目标。期望达

到什么结果? 愿景是否只是某种程度地参与中国的增

长,还是增加市场占有率? 投资是否从长远着眼? 如果短期内没有财务回报,所有者及董事会是否会失去

耐心? 必须明确:里程碑是什么? 希望实现什么? 什么时候? 如何实现?

• 准确评估市场:准确评估市场:相关行业如何运作? 主要行业参与者

有哪些? 每个行业的竞争程度如何? 公司自身的业务

战略能够填补哪些空白? 特别地,需要花时间了解政

府对某个行业有什么目标,这些目标可能如何影响法

规。注意在这样一个变化迅速的市场里,监管法规和

评估的企业都是流动的目标。这项工作十分重要,是

识别为数较少的投资目标,进行更深入的交易前分析

的最佳方法。

• 了解中国特定风险:了解中国特定风险:所有财务交易都有风险,但中国

整体的风险与其他任何国家不同。需要用时间了解将

可能遇到的各种风险。了解这些风险将有助投资者选

择本地行业、交易对手,甚至投资的结构。风险不能

完全避免,但事前了解风险让企业可根据更多信息做

出资本决策并采取适当行动以减少风险。一般而言,

识别和管理风险的能力越高,抓住机遇的能力也越

大。

中国的市场充满吸引力。但

首先需要回答的问题是“为

什么”。回答了这个问题以

后,企业才能研究“谁”

和“如何”的问题。企业如

能多花点时间在战略制定

上,就能大大增加在中国市

场上的胜算。

16

On

the

BEA

M

17

风向

China beckons. The nation remains a hotbed for foreign investment. Not solely because of its appeal as a manufacturing export base to North America and Western Europe but also owing to the sheer size of its domestic market. And though GDP growth may have slowed in recent years, China’s rate of

expansion still well exceeds that of most developed nations. Finally, China is ideally situated to serve as an export and logistics base for not only the fast-growing economies throughout Asia, but also Eastern Europe, the Middle East and Oceania.

For foreign enterprises, investing in China, more often than not, implies a transaction. That is, the majority will need to enter the nation either through an acquisition of an existing enterprise – a so-called wholly foreign-owned enterprise (WFOE) – or by partnering with a local company through a joint venture (JV). Those who know the country and the region recognize the profound opportunities to be found in China. But in terms of transactions, they are also keenly aware of the challenges – many unique to China and often surprising to even the most experienced global investors.

First things fi rst: not who, not how, but why? The chosen counterparty is the “who.” The form of investment is the “how.” It can be said that the key to successful investment in China begins with a simple notion: know thyself. Knowing thyself, knowing “why,” is critical.

Self-awareness requires building details around a desired growth strategy for the China marketplace. Too often, companies move straight toward a transaction without performing this preliminary analysis. And as a result, they often have unclear objectives and unrealistic expectations, which can lead to more than a few surprises including delays, underperforming deals and disappointing results.

So would-be investors need to think long and hard – critically and strategically – about their China aspirations. Will the envisioned business focus primarily on global or regional export or will it seek to participate in the domestic marketplace (or some combination)? How “patient” is the capital – is the focus on the near term or the long term?

Finally, what mileposts will the company use to defi ne and track its success – and what is the desired end-game? Those looking for short-term returns would be advised to look elsewhere. It is only with such clarity going in that a company will be able to determine if a specifi c transaction has a good chance for success.

As to the form of any transaction, the “how,” for many years, the preferred route has been the JV (joint venture). The key reason for this, at one time, was the restricted nature of the China marketplace. That is, foreign companies simply were not allowed to pursue direct ownership. Matters today are much different. The last 10-15 years have seen remarkable deregulation through many of China’s key sectors. Where this leads is to an era where foreign investors have much greater freedom in terms of ownership structure.

Today, the choice between JV or something closer to a wholly foreign-owned enterprise (WFOE) is much more a question of business strategy and risk. Again, what is the investor’s end-game? Does it want to transform the culture and operations of an acquired local company – preparing it for both domestic and global growth? And what are the investor’s operational capabilities – to what degree will it need to strictly rely on local managers for operations and commercial success?

Finally, how much risk is much does the company want to accept? Generally speaking, the grander the vision, the more control and risk an investor is willing to take, the more sense it makes to pursue a WFOE structure. By corollary, an investor looking for more help along the way from a local partner as well as a means of reducing capital exposed to the China marketplace should lean more towards a JV.

18

On

the

BEA

M

19

风向

China’s unique risk profi le Indeed, the China marketplace offers signifi cant opportunities. But hand in hand with such promise, companies need to develop a full appreciation for the specifi c challenges of transacting in China. Beyond all of the customary risks associated with transactions, the China marketplace introduces an array of unique considerations.

Start fi rst with the diffi culty of identifying viable targets – the “who.” China is a vast nation, and its markets are large, complex and diverse. For example, beyond privately owned enterprises (POE), companies will also need to look at the many state owned enterprises (SOE) which may also prove to be attractive counterparties or targets. As a result, it will be very challenging for an investor to develop an in-depth understanding of any given sector.

The challenges relate not only to competitor analysis but also developing insight into government objectives and the likely impact on the regulatory climate. Many industries in China are now largely deregulated or deregulating.

And while that may seem good news on the surface, at the same time, it adds complication to the competitive landscape. Local companies that may have fl ourished in a regulated environment may gradually or even suddenly lose their edge in a freer marketplace. Sectors such as consumer goods, farm equipment or tourism have moved from somewhat or highly regulated to now relatively

freewheeling. While this is a positive outcome for the economy overall, it also leads to overcapacity, hyper-competition and survival of only the fi ttest.

Overall, China is experiencing an era of profound competitive upheaval. So it is only through considerable effort that an investor will be able to competently develop a strategic view of any given sector, let alone a short list of appropriate prospects. But next begins the task of approaching potential counterparties and gathering even more detailed, company-specifi c information. This can be particularly challenging in a nation with insuffi cient standardized reporting.

Local companies, whether an SOE or POE, are often unfamiliar with the sort of reporting required by foreign enterprises. In fact, they may not even collect anything remotely similar on behalf of their own management. So collecting data necessary for an initial valuation will likely take longer – often many months longer – than executives may be accustomed to.

Moreover, the resulting information may be largely incomplete or inaccurate from the foreign investor’s point of view. Local knowledge and communication skills become particularly vital in such instances, as much of the work may become inferential if not forensic. This is one of the key reasons why due diligence, executed by those who understand both sophisticated information needs and local practices, tends to play a more critical role in the China marketplace.

Following sector analysis, a close look at regulatory trends and then fi rst impressions of individual companies, the resulting list of potential counterparties may be long or it could be quite short. But the critical element here is that whatever companies are being considered are a good match for the strategy. What are their capabilities? What are their strengths? What motivates their current ownership – would they even be willing to enter into a transaction with a foreign investor? Without question, it is better to pass on executing an WFOE-style acquisition, JV or partnership for the time being rather than rush into a transaction with the wrong counterparty.

Understanding the cultural challengesThe deal is getting warmer. But before going too much further, it will be important to consider the full range of challenges that are specifi c to China. Consider its cultural risks. Obtaining a counterparty’s unequivocal cooperation and buy-in can be especially challenging in China, where resistance is often more subtle than overt. Beyond discussions with the owners of a local business, a foreign investor will also need to dig deeper to understand the needs and interests of mid-level managers and even workers.

Challenges can also extend to the enforceability of contract provisions, as such agreements are often subject to cultural interpretation. So it will be important to work with advisors who understand not

only the intent of any given provision, but also any potential local practice. Yet another potential culture clash relates to China’s judiciary system, which, though steadily developing, remains a relatively protracted and unpredictable means for dispute resolution.

Investments in China are also subject to extensive government involvement. Yes, the trend is toward greater openness and deregulation. But this is an extended journey. The government may still become involved in pre-deal negotiations, and there have been instances of re-regulation or renegotiation after-the-fact. For this reason, one of the best strategies is to position any transaction up-front in ways that support government objectives, perhaps providing technology, process know-how, capital or branding in a favored sector or region. This is by no means easy nor is it a recipe for guaranteed success – but it is best practice.

And this is by no means the end of China-specifi c risks. Consider intellectual property and corruption issues. Though the nation’s offi cial stance on intellectual property rights has further improved, the culture does not yet fully recognize a corporation’s right to own an idea (leading to patent or process theft). In addition, payoffs and bribes, regrettably, still exist in the business culture in certain segments.

So in many instances, it will be important to hire a forensic team to explore the existence of bribes, kickbacks and other violations, and their degree. If conditions are too severe, a foreign investor may

20

On

the

BEA

M

21

风向

be forced to walk away from the opportunity. But recognize that in many other instances, a foreign investor can have great success in introducing greater transparency. It can, for example, revisit commercial terms with suppliers/customers as well as compensation and incentives with sales teams and procurement. By discussing the problem openly and then explaining the proposed changes in depth – focusing on how the “new way” will not materially alter relative positions – companies can often change business practices.

Discipline will be rewarded In the rush to forge a China presence, there is a tendency for companies to move straight toward a transaction without performing the needed up-front analysis. All too often, this results in unclear objectives and unrealistic expectations which in turn leads to more surprises, delays, underperforming deals and disappointing results. The likelihood of such a scenario can be avoided by spending more time up-front. The key steps include:

• Articulate a concrete strategyCompanies need to be clear in their expectations. What do you want to accomplish? Is your vision to merely participate in China’s growth to some degree or are you seeking a larger presence? Is the investment long-term oriented? Or will the ownership and board grow impatient if fi nancial returns don’t soon materialize. Be clear: what are the milestones? What do we want to accomplish, by when and how?

• Accurately assess the marketplaceHow do the relevant sectors operate? Who are the primary players? What is the level of competition in each segment and where are the gaps your business strategy could fi ll? In particular, spend time to understand the objectives of government offi cials for any given sector and how those goals might impact regulations. Note that in such a dynamic marketplace, the regulations and companies being evaluated are moving targets. Nonetheless, this work is essential, and is the best method for identifying a short list of investment prospects for still deeper pre-transaction analysis.

• Understand China-specifi c risksAll transactions have risk. But China’s overall risk profi le is unlike that of any other nation. Take the time needed to understand the sorts of risks that will be encountered. Understanding these risks will aid an investor in choosing its local sectors, its counterparties – even the structuring of its investment. Risk cannot be completely avoided. But knowledge of risk beforehand arms enables companies to make informed capital decisions and take appropriate actions to mitigate risk. In general, the greater the skill in identifying and managing risks, the greater the ability to capitalize on opportunity.

China beckons. But the fi rst question to answer is “why”? Only then will a company be ready to move on to “who” and “how.” By spending more time on strategy, companies can substantially improve their chances for success in the China marketplace. EY

22

On

the

BEA

M

23

风向

头痛岂能只头痛岂能只专注医头。专注医头。FOCUSING ONA PIECE OFTHE PROCESSONLY FIXESA PIECE OFTHE PROCESS.了解如何改善您的供应链。Find out how to strengthenyour supply chain.

请浏览 Visit ey.com/china.

24

On

the

BEA

M

25

风向

Viewpoint 观点观点

揭开揭开COOCOO的神秘面纱的神秘面纱Unmasking the COO mysteryTom Pauken, 编辑 Editor

中国已经成为世界第二大经济体;部分分析师预测,中国GDP在今

后10至15年将攀升至全球第一。过去三十年,中国吸引了大量

外国直接投资。很多跨国公司已经在中国开展业务;与此同时,

越来越多中国公司也在拓展业务,发展成为跨国企业。中国经济似乎已经进

入“大企业”时代。有鉴于此,很多中国公司应当更多了解企业管理架构。

他们应当了解企业高管层的所有方面,包括CEO(首席执行官)、CFO(首

席财务官)、CIO(首席信息官),以及COO(首席营运官)。

26

On

the

BEA

M

27

风向

尽管CEO、CFO和CIO的工作职责看来可顾名思义,但

COO却始终笼罩着一层神秘的面纱。多数COO似乎安

于躲在幕后,以问题的解决者自居,而不是曝光在公

众的视线之中。尽管他们可能不被公众所熟知,但这

对于他们所效力的企业而言或许倒是个好消息。

COO负责企业的运营,以确保实现效率最大化。安永

最近发布了一份有关COO公众形象的详细调研报告:

《首席运营官的基因:抓住时机,赢得关注》。报告

的作者安永欧洲、中东、印度及非洲 (EMEIA) 区首席

营运官Pascal Macioce在报告中指出了COO在商业世界

扮演重要角色的原因。

该安永调研报告指出:“首席运营官的角色 … 从根

本上讲,他的职责与首席执行官的个人需求和目标密

切相关。…我们发现有很多首席运营官将丰富的运营

知识和宽广的战略视野相结合,并具备成为下一任首

席执行官的潜质。”

COO可被视为企业的二把手。CEO是企业的名义领

袖,COO则充当着“实施者”的角色。人们对许多CEO的期望是有愿景、站在公司战略的最前沿,而COO则

应将CEO传达的信息实践出来。

COO应被视为企业中的“执行人”,负责将企业的战

略计划转化为“可实现的任务”目标。

然而,看起来具有讽刺意味的是,企业最积极的公司

高管却似乎并不喜欢曝光在公众面前。但经过进一步

的观察,我们发现,作为一种商业策略曝光在公众面

前十分合理。

当一家企业高效运营时,有些人可能会说:“这本就

是意料之中的”或问:“这不正好说明为何一开始就

聘用COO吗?”因此,对媒体或公众而言,并没有令人

感兴趣的故事。

然而,如果企业遭遇严重的内部纷争、运营混乱或其

他难以战胜的困难,则COO应慎重处理这些问题,以

免事态发展成一场公关危机。因此,CEO或许会是那个

出现在电视上,面对观众侃侃而谈公司运营一切顺利

的那个角色,而在幕后确保一切诚如所言的却是COO的工作。

无论如何,安永调研报告认为,“隐匿的COO”的时

代或许很快就会结束。报告称:“对运营角色灵魂人

物的需要比以往更加迫在眉睫。其中最主要的原因是

复杂性的不断提高,这也是过去五年中这一角

色发生的最重要变化。… 企业必须具有高度

的灵活性和敏捷性,同时还应比以往更注重成

本控制和效益。”

就为什么建议COO应更多地从幕后走到台前,

安永调研报告给出了一系列的理由。许多人认

为,当CEO离职时,他们的职位常常会被COO接任。此外,COO还应表现出“执行人”的形

象,以加强其领导技能。

安永调研报告称:“应对这些挑战需要具备强

大的领导力,只有这样才能促进和实施战略议

程。在许多企业中,首席运营官正是担此重任

的理想人选,然而这份工作却绝非易事。”

从历史上来看,COO更擅长作为技术型专家,

不会过多地卷入办公室人际政治。安永调研报

告披露:“不久前,许多首席运营官都出身于

工程或其他技术背景。”

然而,很多跨国公司的业务都涉及先进技术和

工程。因此,假如说一家公司在中国开设了一

家工厂,生产计算机芯片。人们可能就会期望

公司的COO具体了解该项技术,以便确保运营

按计划进行,他们自己可以根据实际经验解决

经常突然出现的小型技术问题。

听起来似乎是常理,安永调研报告(对全球

306位高级营运专业人士进行的调查)披露,

所有受访COO中,17%的最高学历为工程硕

士,15%拥有工程学士学位。

然而,受访者概况数据同样显示出新的发展趋

势:25%的COO拥有工商管理硕士学位,16%拥有工商管理学士学位,11%拥有MBA学位。

企业已经转向更为倚重聘用更多工商管理毕业

生,而不是任命技术和工程学专家负责公司运

营。

根据安永调研报告,“现在许多年轻的首席运

营官比他们的前任更具商业意识、更加以业务

为导向。他们通常拥有商科学位,如MBA,而

不是技术背景。”

但持有MBA学位是否就真的应被视为COO职位

的合适人选? 只是因为某人毕业于哈佛商学院 (Harvard Business School) 并不表示他们就是

解决企业技术问题的合适人选。

尽管如此,新一代COO的行为方式更像是商

人,能够调派适当的人员处理适当的工作。他

们不大可能自己解决技术性问题,但大家期待

他们會找适当人员完成那些技术性工作。

许多COO已经开始接受这一理念。安永调研报

告称, Russian Post首席营运官Denis Chuiko表示:“我的职责是保持一切运转良好,确保

在战略框架内实现目标。”

安永调研报告还补充称:“这与人力资源发展

有着密切联系,如果没有合适的团队参与企业

运营,那么战略就无从实施。因此,首席运营

官必须深化人才管理,确保企业有足够的经理

人员储备,并且能够适应不断变化的外部世界

和企业的转型日程。”

好了,有人可能会提出,COO应该从幕后走出

来,更多地与记者、投资方沟通,可能还需要

参与公司的营销活动。当今的COO已不再仅仅

被视为技术问题的解决者,而被视为高级管理

人士。无论喜欢也好,不喜欢也罢,他们都必

须参与到办公室政治之中,确保员工支持和实

施CEO制定的目标。

此外,安永调研报告还指出了人们对于发达国

家和新兴市场COO期望的主要不同。安永调研

报告称,“他们既要在发达市场争取份额,又

要拓展在快速增长市场的业务规模和产能。”

美国一家《财富》(Fortune) 500强企业的

COO的工作职责可能会迥异于一家中国公司的

COO。如果公司已经取得巨大成功的话, 人们

对于美国公司COO的期望值, 只是希望他们保

持现状即可,而中国公司的COO则必须应对更

严峻的挑战。

安永调研报告称,快速增长市场的COO的任务

应该是“能力建设,扩大生产,确保为把握增

长机遇提供适当资源。这需要首席运营官具有

企业家精神和战略性思维,同时兼顾效率和流

程优化,帮助企业实现可持续的增长。”

因此,在大中华市场,具备企业家精神的COO可能最有效用。随着中国经济发展持续突破,

市场可能会更迫切需要找到具有适当观念的管

理人士,以提高中国公司以及在华跨国公司的

营运能力。

更多地走向台前的COO可能会适合着重在大

中华地区开展业务的公司。人们期待他们实施

更为全面的组织计划,行为具有创新精神,以

适应持续变化的商业环境。因此,是时候揭开

COO的神秘面纱、让其工作职责和成就更多曝

光在公众面前。

28

On

the

BEA

M

29

风向

China has emerged as the world’s second biggest economy, while top-notch business analysts forecast its GDP to rank number one globally in the next 10

to 15 years. The nation has attracted a major infl ux of foreign direct investment over the past three decades. Numerous multinationals have launched business operations in the country while more Chinese companies have expanded to become multinationals as well. China appears to have entered the ‘Big Business’ stage of its economy. Hence, many Chinese companies should familiarize themselves more with the management structure of corporations. They should know all about the ‘Big Cs,’ which are: CEO (Chief Executive Offi cer); CFO (Chief fi nancial Offi cer); CIO (Chief Information Offi cer) and COO (Chief Operations Offi cer).

Although the job duties of a CEO, CFO and CIO seem self explanatory, the COO remains wrapped in a shroud of mystery. Most COOs appear comfortable working behind-the-scenes as problem fi xers, rather than be seen in the public eye. Even though they may be unrecognizable to the public, perhaps that’s good news for the companies they work for.

A COO is responsible for taking charge of corporate operations to ensure maximum effi ciency. Meanwhile, EY has recently published a detailed study on the public image of a COO. In the report, ‘The DNA of the COO: Time to claim the spotlight,’ the author Pascal Macioce, COO Europe, Middle East, India and Africa EY, highlights why COOs play an essential role in the business world.

According to the EY study, “a COO is described as … The role of the chief operating offi cer … essentially is a job whose responsibilities are defi ned closely in tandem with the individual needs and goals of the chief executive offi cer … What we fi nd is a breed of executive who combines deep operational knowledge with broad local strategic insight, and who has what it takes to become the next CEO.”

The COO could be viewed as the second-in-command of a corporation. While the CEO assumes a fi gurehead role, the COO acts as the ‘implementer.’ Many CEOs are expected to act in a visionary manner and standing at the forefront of corporate strategy, while the COO should translate the CEO’s message into reality.

The COO deserves recognition as the ‘doer’ of the company, and is responsible for making the strategic plans of a corporation transform into a ‘Mission Accomplished’ objective.

30

On

the

BEA

M

31

风向

However, it seems ironic that the most active-oriented senior executive of a company is someone who appears reluctant to bask in the limelight. Yet upon closer observation, that would make logical sense as a business strategy.

When a company is running effi ciently, some would say, “That’s to be expected,” or ask, “Isn’t that why a COO is hired in the fi rst place?” Consequently, there’s no intriguing story for the media or public.

However, if a corporation struggles with serious internal discord, operational chaos or other overwhelming diffi culties, the COO should handle these matters with discretion to prevent a public relations nightmare from developing. Accordingly, A CEO may appear on TV to say their corporation is running smoothly, but it’s the COO’s job to make sure that it is really happening behind-the-scenes.

Nevertheless, an era of the ‘Invisible COO’ may soon vanish, according to an EY study, which is quoted as saying, “the need for a fi gurehead in the operations role is more pressing than ever. More than anything else, this is due to increasing complexity, the single most important shift in the role over the past fi ve years … Companies must be highly fl exible and agile, while retaining a sharper-than-ever focus on cost containment and effi ciency.”

The EY report offers a few reasons for suggesting why the COO should play a more visible role. Many believe that when a CEO departs from the fi rm, they are often replaced by the COO. Additionally, the COO should convey an image as a “doer” to enhance their leadership skills.

“The challenges require strong leadership to catalyze and implement the strategic data,” said the EY report. “In many companies, COOs are ideally placed to lead this charge. But doing so is far from easy.”

Yet historically, COOs have been more adept as technical experts rather than getting too involved with offi ce politics. As disclosed by the EY COO report, “Many COOs from yesteryear hailed from an engineering or technical background.”

Yet, many multinationals are engaged in businesses that that deal with highly advanced technology and engineering. So, let’s say a company opens a factory to manufacture computer chip technology in China. One would expect the COO to have a detailed understanding of the technology that would be utilized to ensure that operations go according to plan and they could take a hands-on approach to fi x technical glitches that commonly occur.

Sounds like basic common sense and according to the EY report, a survey of 306 senior operational professionals from around the world, revealed that 17 percent of all COOs have a Master’s degree in Engineering as their highest (educational) qualifi cation, while 15 percent have a Bachelor’s degree in Engineering.

However, the demographics also show a new developing trend: 25 percent of COOs have a Master’s degree in Business Management Administration, while 16 percent hold Bachelor’s degree in the fi eld and 11 percent have an MBA. Corporations have shifted towards a greater reliance on hiring more business administration students, rather than appoint technology and engineering experts to take charge of corporate operations.

“Many younger COOS ... are more commercially aware and business-oriented than their predecessors. They typically have business qualifi cations, such as an MBA, rather than a technical background,” said the EY study.

But should an MBA degree holder really be considered the right person for a COO position? Just because somebody has graduated from Harvard Business School does not mean they are the proper person to solve technical problems for a corporation.

Nonetheless, the current generation of COOs act more as business people, who assign the right people to the right tasks. They are unlikely to solve technical problems on their own, but they are expected to fi nd the appropriate person to accomplish those technical tasks.

Many COOs have already embraced the concept. “My duty is to create a well-oiled machine that will guarantee that targets can be accomplished within the framework of the strategy,” Denis Chuiko, COO, Russian Post, is quoted as saying in the EY study.

The EY report added, “There is a strong link between the aspect of the role and people development, because without the right teams in place across the company’s operations there is no execution of strategy. COOs must therefore, be deeply involved in talent management to ensure that there is a strong pipeline of managers who are aligned with the changing world outside, and the company’s own transformation agenda.”

Well, one could argue that a COO should come out of hiding and communicate more with journalists, investors and perhaps participate in corporate marketing campaigns. COOs are no longer perceived as just tech-fi xers, but now viewed as senior administrators, who whether they like it or not, must play offi ce politics to make certain that employees support and implement the goals set forth by their CEO.

Additionally, the EY study also pointed out key differences between the expectations of COOs in developed countries than with those working in the emerging markets. “They have to fi ght for market share in developed markets, while also building scale and capacity in rapid growth markets,” the EY report said.

The responsibilities of a COO working for a Fortune 500 corporation in the US may vastly differ from a COO employed at a company based in China. A US-based COO is expected to maintain the status quo, if the company is already enjoying tremendous success, while a China-based COO must respond to greater challenges.

COOs in rapid growth markets should “build capacity, scale production and ensure that the right resources are in place to capture growth opportunities,” the EY study said. “This agenda demands a highly entrepreneurial and strategic mindset, along with the ability to introduce effi ciency and process optimization so that growth can be sustainable.”

Therefore, the entrepreneurial COO could be most effective in the Greater China market. As China’s economy continues to soar to new heights, there would be a deeper need for fi nding the right mindset to boost operational capacities of Chinese companies, as well as multinationals doing business here.

A more visible COO would be a good fi t for companies that focus on operating in the Greater China region. They would be expected to implement a more comprehensive organizational plan and act in a creative spirit to adapt to constantly changing business circumstances. Hence, it’s about time to unveil the shroud of mystery of a COO and shine a brighter light on their job responsibilities and accomplishments.

请点击以下网址阅读《首席运营官的基因:抓住

时机,赢得关注》报告全文。Read the full report The DNA of the COO: Time to claim the spotlight at http://docs.iweb.ey.com/GLOBAL//CKR//CHTHOUCKR.NSF/($VERITY)/3BEC15D15D0108CFC1257AB8002647FC/$FILE/DNA%20OF%20THE%20COO%20REPORT%20FINAL.PDF

EY

32

On

the

BEA

M

33

风向

Industry Focus 行业焦点行业焦点

民以食为天,民以食为天,食以安为先食以安为先For food, nothing is more important than safety

32

On

the

BEA

M

33

风风向向

丘昌和,钱晓云,谢枫,陈世宇,钟育文丘昌和,钱晓云,谢枫,陈世宇,钟育文审计合伙人

Tyron Yau, Olivia Qian, Eric Feng Xie, Leo Chan, German ChungPartners, Assurance

34

On

the

BEA

M

35

风向

古语云:“民以食为天,食以安为

先”。当今的社会是坚持以人为本

的社会,是倡导健康消费、科学消

费、安全消费、和谐消费的社会。

食品安全问题涉及到每个人的身体

健康和生命。在党的十八大报告中

指出:加强社会建设,必须保障和

改善民生为重点。提高我国食品安

全总体水平就是保障和改善民生的

一项重要内容。

食品安全是食品企业的首要社会责

任.近年来接连发生的食品安全事

件,如“地沟油”、“塑化剂”

、“问题奶粉”和“食品添加剂”

等等,凸显了我国食品企业在食品

安全方面社会责任的严重缺失。上

市公司作为我国国民经济的重要组

成部分及其巨大的社会影响力、品

牌知名度,如何通过完善内部控制

加强食品安全的风险及控制措施,

以食品安全为核心推进企业社会责

任的建设,将对食品安全的保障作

出巨大贡献。因此提高食品企业的

社会责任意识,保障消费者权益显

得尤为迫切和重要。

监管机构的要求监管机构的要求

香港交易及结算所有限公司香港交易及结算所有限公司

作为全球其中一间发达经济体的证

卷交易所,香港交易及结算所有限

公司更是于2013年刊发《环境、

社会及管治报告指引》咨询总结的

详细内容,包括主要范畴及各范畴

下的层面、汇报范围及方针等。他

们提出上市公司如能就环境、社会

及管治等,作出全面及持续性的披

露,将有助提升公司的可信性及声

誉,并且建议公司设立相关的内部

监控程序,尽早为汇报作准备。其

中营运惯例中的产品责任便涉及到

披露有关产品或服务的健康与安

全、广告、标签及保障私隐事宜的

政策。

中华人民共和国财政部中华人民共和国财政部

《企业内部控制基本规范》自

2011年1月1日起在境内外同时上

市的公司施行,自2012年1月1日起在上海证券交易所、深圳证券交

易所主板上市公司施行;其中企业

内部控制应用指引涉及到社会责

任、是指企业在经营发展过程中应

当履行的社会职责和义务,主要包

括安全生产、产品质量、环境保

护、资源节约、促进就业、员工权

益保护等。

食品企业的社会责任食品企业的社会责任

食品安全是我国食品企业最基本的

社会责任,这一社会责任主要体现

在生产环节、流通环节和消费环

节。食品企业只有在生产、流通、

消费环节上承担相应的社会责任,

才能保证向消费者提供安全的食

品。

生产环节侧重于食品生产安全,要

求食品企业按照国家规定的国家

标准、地方标准和企业标准3个层

次的食品安全标准进行生产。流通

环节侧重于食品在各个环节中的流

通安全。不仅要保证本企业所负责

的食品安全,而且要承担供应链上

企业互相监督的责任。消费环节侧

重消费以及对安全事故处理的反应

能力。企业要提高食品风险意识,

定期检查本企业各项食品安全防范

措施的落实情况,及时消除食品安

全事故隐患。制定食品安全事故处

置方案,建立事故处理机制和赔偿

制度,对产品设计、制造、销售等

环节上的缺陷产品实行产品召回制

度,一旦出现问题按照相应的惩罚

性赔偿和民事赔偿责任优先规定承

担责任。

以食品安全为核心,推进食以食品安全为核心,推进食

品企业社会责任建设品企业社会责任建设

企业社会责任的内部环境企业社会责任的内部环境

内部环境是企业实施内部控制的基

础控制,环境要素是推动企业发展

的发动机。食品企业应该营造良好

的控制环境以实现食品安全目标,

这一点主要体现在企业文化方面。

食品企业在经营价值观上要把食品

安全社会责任作为企业文化建设的

重要内容要树立以人为本的观念,

坚持诚信的态度。食品企业还要改

变传统经营理念,从战略的高度出

发,把社会责任贯穿于企业的整体

经营中做到为消费者提供安全的产

品、正确的产品信息、及时的售后

服务以及为消费者开发绿色产品。

企业社会责任的风险评估企业社会责任的风险评估

风险评估是企业及时识别、系统分

析经营活动中与实现内部控制目标

相关的风险,合理确定风险应对策

略,是实施内部控制的重要环节。

食品企业应当重视风险评估的持续

性,及时收集风险及与风险变化相

关的各种信息,定期或不定期地开

展风险评估。食品安全风险主要体

现在以下几个方面。

民以食为天的观念如此源远流长,反映了中国几千年

文明史和农业关系至为密切,粮食至关重要。人们

对于吃的重要性的认识始终贯穿于中国文明发展的

历史长河。随着人民生活水平的日渐提高及对食品安全要求的

提升,食品企业在食品安全问题方面社会责任的严重缺失已经

引起了各界的关注。

生产环节风险主要有:

• 有毒物质大量在食品中残留微生物

指标不合格

• 部分食品的生产加工、储存、销售

过程达不到规定的卫生要求

• 食品加工中天然有害物未完全消除

引起的食源性问题

• 食品加工中产生的有毒有害物质

• 滥用食品添加剂甚至滥用工业添加

剂等。

流通环节风险主要有:由于食品行业

链条长,保质期短的产品极其容易在

流通环节出现问题,而企业对流通中

食品安全的漠视,比如过期食品继续

销售,也是造成食品安全问题的主要

原因。消费环节的风险一方面来自于

生产和流通环节,另一方面是缺少食

品安全事故处置方案。

企业社会责任的控制活动企业社会责任的控制活动

对于常规性的企业社会责任,企业应

按照确定的原则和标准,通过内部建

立不相容职务分离控制、授权审批控

制、会计系统控制等手段,确保此类

社会责任的切实履行。对于突发性企

业社会责任、应建立应急处理机制控

制食品安全风险措施主要包括以下方

面。

• 建立健全产品质量标准体系建立健全产品质量标准体系

企业可以选择质量体系认证或产品

质量认证方式,如ISO系列标准认

证。良好作业规范是一套适用于制

药、食品等行业的强制性标准,要

求企业从原料、人员、设施设备、

生产过程、包装运输、质量控制等

方面按国家有关法规达到卫生质量

要求形成一套可操作的作业规范。

“ 王者以民人为天,而民人以食为天。”《史记 • 郦生陆贾列传》

“ For a king, the populace is his utmost concern. For a populace, food is their utmost concern.”

The Records of the Grand Historian: Biographies of Li Sheng and Lu Jia

36

On

the

BEA

M

37

风向

• 建立健全食品安全管理制度建立健全食品安全管理制度

食品生产企业除具备食品安全好的意识外,还必须不

断完善食品安全管理制度,提高职工综合素质。根据

食品生产工艺持点,从原材料进厂检验到生产的各个

环节,再到产品最终检验,全过程确定关键控制点和

关键控制要素,并配备必要的监测人员和检测设备,

完善企业内部质量控制、监测系统和质量可追溯体

系,全程监测和控制食品生产,在食品安全问题上要

在思想和行动上高度统一,尽量减少或避免食品安全

问题的出现。

• 加强产品售后服务加强产品售后服务

企业要提高食品风险意识,定期检查本企业各项食品

安全防范措施的落实情况及时消除食品安全事故隐

患。企业要制定食品安全事故处置方案,建立事故处

理机制和赔偿制度,对产品设计、生产、销售等环节

上的缺陷产品实行产品召回制度,一旦出现问题,按

照相应的惩罚性赔偿和民事赔偿责任优先规定承担责

任。

• 建立和完善食品安全机制建立和完善食品安全机制

第一、按照分段管理为主、品种管理为辅,谁审批、

谁监管、谁负责的原则和食品安全事故行政责任追究

制; 第二、建立权威高效的食品安全监测部门;第

三、建设精干高素质的食品安全监督队伍,要从指导

思想、依据和原则、机构设置、主要任务、设备配置

能力开展、经费保障等方面制定切实可行的标准,全

面加强食品安全监督能力。

• 建立责任危机处理机制建立责任危机处理机制

首先,当食品安全危机来临时,食品企业应在第一时

间核查信息、迅速沟通媒体,公开相关信息,以诚恳

的积极的态度为化解危机铺平道路。其次,食品危机

爆发后,媒体舆论会大量跟进这时企业要关注媒体,

扩大正面影响。最后,在食品公关安全危机有一个阶

段性的结果之后,食品企业借机可以宣传自己的企业

品牌和产品质量。

企业社会责任的内部监督企业社会责任的内部监督

企业社会责任的内部监督除通过内部审计机构定期和不

定期地就企业社会责任内部控制制度执行情况进行审核

外,企业应主动跟踪内外部环境变化,及时调整相关内

控措施和手段。食品企业要聘请注册会计师对内部控制

有效性进行评价并出具鉴证报告,及时对食品安全内部

控制部分进行监督检查并提出改善建议。

37

风向

结论结论

食品安全与居民生活和整个社会

的发展息息相关,作为食品安全

的责任人,食品企业应担当起对

消费者的社会责任感,规范自身

行为,完善内部控制制度,强化

社会责任意识提高履行社会责任

的自觉性,满足消费者和社会的

需求。

38

On

the

BEA

M

39

风向

Food is a daily necessity for everyone and that includes the Chinese in China, as the standard of living of residents has risen, and so has the demand for greater food safety. Nevertheless, numerous Chinese companies have

struggled to overcome food safety concerns.

As an old saying goes, “nothing is more important than food; for food, nothing is more important than safety.” Modern society takes humanity as its central value, which should adhere to healthy, scientifi c, and safe consumption. According to a report by the 18th Party Congress (Chinese government), “Raising the overall level of food safety has become a key task.

Nonetheless, there has been a spate of food safety incidents in recent years, such as selling sewage cooking oil, plasticizers and tainted infant formulas. A few Chinese food enterprises are publicly-listed corporations and have become an essential component of the national economy. Apparently, they should upgrade their internal controls over food safety risks, while promoting more enhanced corporate social responsibility. Government should raise greater awareness to protect consumers’ rights.

Requirements of Regulatory Authorities

Hong Kong Exchanges and Clearing Limited

As an internationally-renowned exchange, the Hong Kong Exchanges and Clearing Limited has published a “Report on Guidelines to Environment, Society and Governance,” in 2013, which explains its fi ndings. It stated that publicly-listed companies must provide comprehensive disclosures in areas such as the environment, society and corporate governance to enhance their credibility. The Exchanges recommended that these companies should establish more internal controls and monitors for early reporting. Accordingly, product liability should become part of its disclosure policies to improve its health and safety issues of products and services, along with playing a more honest role with its advertisements, labeling and privacy issues.

Ministry of Finance of the People’s Republic of China

Since 1 January 2011, the Essential Requirements on Corporate Internal Controls were implemented in companies that have been publicly-listed overseas, while the same rules applied for companies listed on the Shanghai Stock Exchange and Shenzhen Stock Exchange as of 1 January 2012. Internal controls have touched on social responsibility, which would entail safe production, product quality, environmental protection, energy economy, job promotion, and protection of workers’ rights.

Social responsibility of food enterprises

Food safety is refl ected in their production, distribution, and consumption processes. The production process focuses on the safety of food production, so that enterprises conform to the national, local and corporate standards. The distribution process concentrates on the distribution safety in regards to various links. Enterprises must ensure food safety and supervise companies engaged in the whole supply chain. The consumption process targets safety in consumption along with measures to react to safety contingencies. Enterprises must hold a heightened awareness of food risks

and check enforcement regularly to implement various food safety prevention measures. They should formulate a food safety incident disposal program, set up contingency response mechanisms and compensation programs, while adopting a recall system for products. When a problem occurs, enterprises should bear responsibility according to the priority set by punitive damages and civil compensation liability.

Promote the social responsibility of food enterprises with food safety as the focus

Internal environment of enterprise’s social responsibility

The internal environment of an enterprise refers to the fundamental mechanisms for internal controls. These elements would transform into the drivers of corporate growth. A food enterprise should build a proper control environment to achieve its food safety objectives They should promote integrity. They should change their traditional operating outlook to embed a strong sense of social responsibility. They should develop green products for consumers.

40

On

the

BEA

M

41

风向

Risk assessment on enterprises’ social responsibility

Risk assessments must be pivotal for an enterprise to identify and analyze risks related to its operations and to achieve stronger internal controls. They should adopt appropriate measures to address risks food enterprises should collect information on risks and risk-related issues in an expedited manner, and conduct regular or irregular risk assessments.

Food safety risks appear in the following areas:

• food with large amounts of residuals of toxic substances, failing the microbe concentration indicator standard;

• failure in the production and processing, storage and sales processes of some foods to measure up to hygienic requirements;

• food source problems caused by natural harmful substances not fully eliminated in the food processing;

• toxic and harmful substances produced in the course of food processing;

• and abuses of food additives and industrial additives.

Risks in the distribution area have occurred, such as products of short shelf life. Another example includes selling expired food items. Risks come from the production and distribution areas, and a lack of food safety contingencies.

Control measures for enterprises’ social responsibility

Regarding routine social responsibilities, enterprises should set up internal controls that separate incompatible work duties, authorized approval controls, accounting systems, and other means of control to ensure effective implementation. Enterprises should establish an emergency response mechanism to control food safety risks.

• Upgrade product quality standardsEnterprises can choose between the quality system certifi cation and product quality certifi cation system such as the ISO standard certifi cation series. Good operating specifi cations must become mandatory standards in the pharmaceutical, food and other essential industries. They require enterprises to formulate a package of operable practice codes in the raw materials, personnel, facility and equipment, production, packaging, transportation, and quality control processes, so enterprises can conform to quality health requirements stipulated by local regulations.

• Upgrade food safety management systemIn addition to having good awareness of food safety, food production companies must upgrade their food safety management systems and quality of their employees.

Based on specifi c features of different food production processes, enterprises should identify critical control point’s elements throughout the process, from incoming raw material acceptance, through inspections of all aspects of production. Enterprises should equip the process with necessary testing equipment and assign necessary monitoring personnel; improve the internal quality control system, monitoring system and quality traceability system of the production process. They should unify their actions for more enhanced food safety.

• Strengthen after-sales serviceCompanies should improve food risk awareness; implement and check food safety prevention measures on a regular basis.

• Upgrade food safety mechanismsImplement an administrative accountability system characterized by sectional management and supplemented by product range management, so offi cials will be held accountable for regulatory actions. Secondly, establish an effi cient food safety monitoring department. Assemble an oversight team to coincide with practicable standards and to observe the performance of allocated equipment to ensure that appropriate funding has been allocated.

• Establish a crisis management responsibility systemWhen a food safety crisis develops, the company should verify relevant information, communicate with the media, and portray a positive attitude to pave the way for a satisfactory resolution. When a food crisis erupts, the public would pay much attention to it. The company should take a proactive approach by acting in a transparent manner to show they are trying to resolve the matter as soon as possible. Additionally, by enhancing their ability to handle a food safety crisis, the company could promote its corporate brand and product quality later on.

Internal supervision of corporate social responsibility

In addition to regular and irregular audits by internal oversight departments on the implementation of the internal controls on corporate social responsibility, enterprises should take the initiative to track changes in the external environment and adjust their internal control measures in a timely manner. Companies should hire certifi ed public accountants to evaluate the effectiveness of internal controls to issue verifi cation reports, conduct supervision and inspections of its internal controls while providing recommendations for more food safety.

Conclusion

As entities have been charged with the responsibility of food safety, these companies should assume greater social responsibility to their consumers, regulate their behavior, upgrade internal control systems, and satisfy the needs of consumers and society. EY

41

风向

42

On

the

BEA

M

43

风向

The retail world in developed countries is undergoing a dramatic transformation. Driven by the seemingly

unstoppable rise of e-commerce and online market models, extensive smart phone and 3G/4G penetration, social media adoption, and maturing technology such as contactless payments, GPS, image recognition and augmented reality, the way shoppers buy and merchants sell in all contexts is entering a new, digitally enhanced era. We choose to refer to this developing digital retail landscape in its entirety as “Smart Commerce”.

Ernst & Young conducted in-depth interviews with 41 senior executives between December 2012 and April 2013, either face-to-face or by telephone. The interviews covered a variety of industries involved in Smart Commerce (fi nancial services, retail, technology and telecommunications). One of the most surprising insights from this study was the real and widespread fear articulated by established organizations that Smart Commerce develop will result in intermediation – and the decline in

bank relevance to customers, with potentially signifi cant consequences for banks that go well beyond payment service revenues. These fears are well founded. The new players in the Smart Commerce value chain are already demonstrating aggressive business models that are vastly different from the traditional payment and banking model. These models are based on rich data on consumer transactions that cross-subsidize payment services by promoting and sharing in merchant and manufacturer profi t pools with potential to further displace banks’ traditional place in the purchasing experience.

Banks are planning to deliver ambitious Smart Commerce services to counter the threat of intermediation. Most banks want to be s Smart Commerce “solution provider” offering integrated solutions incorporating both payments and broader “purchasing facilitation” services (e.g., digital loyalty, promotions and receipting), and most intend to deliver this within two years.

The Chinese banks have also participated in the battles for

customers at the front line of Smart Commerce. A number of banks have established the online shopping platforms and are diversifying their scope of services gradually to extend their presence from payment and funding to promotion, selection of products and after-purchase service across the Smart Commerce value chain. Although the banks’ e-commerce platforms currently do not stand comparison with the traditional e-commerce businesses such as Taobao and Jingdong in terms of the number of active users and the volume of transactions, they enjoy the advantage of providing the fi nancial services to the customers by leveraging on their e-commerce platforms. We believe that the key to win the battle for customers lies in who is capable of acquiring the core data of customers. Banks may segment their customer base to provide more targeted and convenient services by analyzing the customers’ transaction information and other core data and conducting in-depth information mining, thus increasing the customer viscidity.

发达国家的零售业正在经

历一场巨变。受看似势

不可挡的电子商务和在

线市场模式的崛起、智能手机与

3G/4G技术的广泛应用、社交媒体

的普及以及日渐成熟的技术(如非

接触式支付、全球定位系统、图像

识别和增强现实技术等)的推动,

在这所有商业环境下的消费者购物

和商户销售方式正步入一个全新的

数字化时代。我们将这一不断演变

的数字零售格局统称为“智能商

务”(Smart Commerce)。

安永于2012年12月至2013年4月间对智能商务涉及的多个行业(金

融服务、零售、科技与电信)的41

名高管进行了深入的面对面或电话

采访。本次调研最令人惊讶的一个

发现是,成功的金融机构普遍有

实际而广泛的担心:智能商务的发

展将催生中介渠道,导致银行与客

户的相关性降低,从而给银行带来

远远超过其支付服务收入的严重后

果。这种担心不无道理。智能商务

价值链中的新进参与者采用咄咄逼

人的商业模式,与传统的支付和银

行业务模式有很大的不同。这些模

式均基于丰富的消费者交易数据,

通过推动和共享商户与制造商的利

润领域,交叉补贴支付服务,可能

会进一步取代银行在购物体验中的

传统地位。

银行正计划提供大规模的智能商务

服务,以对抗这种中介的威胁。大

部分银行希望成为智能商务“解决

方案提供商”,提供集支付和更广

泛的“购物便利”服务(如数字忠

诚度、数字促销和数字收据)于一

体的综合解决方案,且大多数计划

在两年内提供。

中国的银行也已加入这场智能商务

的客户争夺战。多家银行都开办了

网上商城且逐步丰富其服务范围,

将触角从智能商务价值链中的支付

和融资扩展到促销、产品选择和购

买后服务。尽管目前银行的电子商

务平台在活跃用户数量、交易量等

方面还无法和淘宝、京东等传统电

商相比,但银行的优势是可以通过

其电商平台同时为客户提供金融服

务。我们认为,这场客户争夺战的

关键是谁能掌握客户的核心数据。

通过对客户的交易信息等核心数据

进行分析和深度挖掘,可以对客户

群进行细分,为其提供有针对性

的、便捷的服务,从而进一步增加

客户黏性。

智能商务:智能商务:银行面临的威胁及应对措施

Smart Commerce: threat to banks and banks’ responses

EY

请点击以下网址阅读《智能商务——银行

在数字零售前线展开客户争夺战》报告

全文。http://www.ey.com/Publication/vwLUAssets/Smart-commerce_CN/$FILE/EY-Smart-Commerce-Report_CN.pdf

Read the full report Smart Commerce – Banks battle for customers at the frontline of digital retail at http://www.ey.com/Publication/vwLUAssets/Smart_Commerce_-_Battling_for_customers_in_digital_retail/$FILE/EY-Smart_Commerce_Battling_for_customers_in_digital_retail.pdf

Industry Focus 行业焦点行业焦点

许旭明许旭明金融服务部合伙人

Steven XuPartner, Financial Services

44

On

the

BEA

M

45

风向

WHO WILL INSPIRE US NEXT?Inspiration comes from the most unexpected places, from a whiz kid in a dorm to a visionary world leader. So when we look for the next big idea, we look everywhere. And then we bring it to Monaco.

Join us 4-8 June 2014 at EY World Entrepreneur Of The YearTM and see for yourself. Inspiration has no boundaries or borders.

ey.com/weoy

谁开启我们新一谁开启我们新一

个灵感之窗个灵感之窗?灵感往往来自最难预料的地方,可能

是学生宿舍中的一名天才儿童,也可

能是一位世界级的梦想家。因此,我

们躺开心灵,到处寻觅好的意念,并

把这些能启发新灵感、创新的意念带

赴摩纳哥。

请于2014年6月4-8日出席安永全球

企业家奖,自己找找灵感。我们的信

念是灵感没有疆域或界限。

ey.com/weoy

46

On

the

BEA

M

47

风向

Building a better working

world从这里启程更为理想 Better begins here:

ey.com/betterworkingworld

At EY we are committed to building a better working world — one with increased trust and confi dence in business, sustainable growth, development of talent in all its forms, and

greater collaboration. Every day, thousands of EY professionals – and people from other organizations around the world – engage in an extraordinary range of activities that grow businesses and economies.

建设更美好建设更美好的商业世界的商业世界

安永致力建设更美好的商业世界,一个

对企业有更大信任度和信心,增长持

续,以各种方式培养人才和协作得以

加强的世界。在全球各地的每一天,数以千计安

永专业人员和各地其他机构的人员携手协作,为

企业和经济增长进行各种互动与交流。

吴港平,中国主席及大中华首席合伙人吴港平,中国主席及大中华首席合伙人Albert Ng, Chairman, China Managing Partner, Greater China

我们希望看到市场信任度提升,资本市场

更加稳健,投资者能掌握充分的信息以

作决策。我们希望看到企业持续增长、

就业增加、消费意欲上扬,政府乐意投资于民。我

们也希望在人才培训和推动协作方面恪尽本分。

We want to see trust increase in the world, so capital markets are strong and investors make informed decisions. We want to see businesses grow sustainably, employment rise, consumers spend and governments invest in their citizens. We want to do our part in developing talent and encouraging collaboration.

王金来,台湾地区董事长王金来,台湾地区董事长

James Wang, Managing Partner, Taiwan

建设更美好的商业世界”不但营造更

清晰和崭新的形象,也显示我们对

员工、客户和社会作出的重大承

诺。相信共同努力,秉承锲而不舍的精神,

我们定能携手获得更美好的成果!

“Building a better working world” not only creates a clearer and fresh image, but also demonstrates our strong commitment to our people, clients and community - I believe with collective efforts and determination, we can achieve more together!

“

陈瑞娟,香港及澳门地区主管合伙人陈瑞娟,香港及澳门地区主管合伙人Agnes Chan, Managing Partner, Hong Kong & Macau

安永以敢为人先的态度为自己订立了新的宗

旨:建设更美好的商业世界。这将给我们服

务客户的团队新的能量和明确目标,最终得

以转化为客户的具体业绩。安永致力与客户保持紧密

联系,迅速回应要求,时刻为客户提供我们的深刻见

解和卓越服务。

EY’s bold new purpose of building a better working world gives account teams energy and a clear goal which will turn into business results. Account teams will focus on staying connected, responsive and insightful by delivering exceptional client service in every client encounter.

梁伟立,华中地区主管合伙人梁伟立,华中地区主管合伙人Philip Leung, Managing Partner, China Central

我们通过培养人才,建立最佳团队为

客户提供出色服务来建立更美好的

商业世界。

We build a better working world by developing our people, putting together the best teams to provide the most outstanding services to clients.

唐荣基,大中华区税务服务主管合伙人 唐荣基,大中华区税务服务主管合伙人

Walter Tong, Greater China Tax Managing Partner

我们协助客户应对迅速变化的本地和国际税务

环境的复杂情况,协助管理风险、减少成本

和保护声誉。这涉及整合最佳的技术技能、

行业知识和团队整体的商业触觉。

We help our clients navigate the complexities of the rapidly changing domestic and international tax landscape by managing risk, minimizing costs and safeguarding reputations. This involves blending the very best technical skills, industry knowledge and overall business acumen of our teams.

曾鹏森,华北地区主管合伙人曾鹏森,华北地区主管合伙人Joe Tsang, Managing Partner, China North

建设更美好的商业世界”是推动我们的

动力,让安永机构上下都有一个十分

明确的宗旨。

‘Building a better working world’ is our driving force which gives a strong sense of purpose for the entire EY organization.

“

张小璐,大中华区咨询服务主管合伙人张小璐,大中华区咨询服务主管合伙人Cecilia Zhang, Greater China Advisory Managing Partner

我们与各行业中的领袖们一起,相

互扶持、共同增长、并肩创新和

提升业绩。当我们都恪尽本分做

到最好时,本地的经济和全球的资本市场也

会随之提升。这就是安永咨询支持建立一个

更好的世界商业环境的方式。

Our high performing teams work with leading organisations to grow, innovate, protect and optimize their performance. And when businesses are performing well, domestic economies and global capital markets perform well. That’s how Advisory helps our working world, work better.

“

张耀樑,大中华区审计服务主管合伙人张耀樑,大中华区审计服务主管合伙人Andy Cheung, Greater China AssuranceManaging Partner

建设更美好的商业世界”就是指通过提供审

计、诈骗审查服务及对气候变化与可持续

发展服务,增加对企业、资本市场和经济

体的信任度和信心。

“Building a better working world” is about increasing trust and confi dence in business, capital markets and economies through our audits, fraud and investigation services and climate change and sustainability services.

庞若柏,大中华区财务交易咨询服务主管合伙人庞若柏,大中华区财务交易咨询服务主管合伙人Robert Partridge, Greater China Transaction Advisory Managing Partner

每项交易、估值和整合,我们都提供超越落实交

易的独特观点和战略性意见。我们协助客户作

出更好的资本议程决策,让他们的业务有所改

善。当企业运转得更好,商业世界也会运转得更好。

In every transaction, valuation and integration, we deliver insightful and strategic advice that goes beyond the transaction delivery. We help our clients make better decisions about their capital agenda, so they can build better businesses. And when business works better, the business world works better.

蔡伟荣,华南地区主管合伙人蔡伟荣,华南地区主管合伙人Ringo Choi, Managing Partner, China South

建设更美好的商业世界”加上新的安永标

识体现了我们进入新时代对机构发展的祝

贺。我相信我们长期的努力工作精神、客

户、员工和社会都会有更美好的未来。

The new EY logo with “building a better working world” marks the celebration of EY’s development as we are entering into a new era. I believe that with our long-standing spirit of hard work, our clients, our people and our communities will have a better future.

“

52

On

the

BEA

M

53

风向

• 2013年9月于法国知名商业信息集团Naseba在上海

举办的中国女性领袖经济论坛上荣膺Most Women friendly International Employer(“女性最友好国际雇主”)

• 全球而言,1998年以来,连续15年获选为一间 Most Admired Knowledge Enterprise(“最受推崇知识型

机构”)

• 2012年获Asia Risk颁发The Consultancy of the Year Award(“年度咨询机构奖”)

• 2012年获Mediazone选为Hong Kong’s Most Valuable Companies(香港最具价值企业)之一

• 我们在2013年Universum的The World’s Most Attractive Employers(“全球最具吸引力雇主”)

调研中排名第二,更是业内之冠

• 2010年及2012年《金融时报》及财务数据供应

商并购市场资讯有限公司颁发Asia-Pacifi c M&A Awards(“亚太区并购奖”)时获评为 Accounting Firm of the Year(“年度会计师事务所”)。排名按并购工作成绩计算

• In Sept 2013 we were awarded by Naseba as the “Most Women-friendly International Employer” at the Women in Leadership (WIL) Economic forum held in Shanghai.

• Globally, we have been named a Most Admired Knowledge Enterprise (MAKE) for the past 15 consecutive years (since 1998).

• We won the Consultancy of the Year Award from Asia Risk in 2012.

• In 2012, we were named by Mediazone as one of the Hong Kong’s Most Valuable Companies.

• Globally, we ranked 2nd in the Universum Survey 2013 of the World’s Most Attractive Employers, and were 1st among other organizations in our industry

• We were named Accounting Firm of the Year in 2010 and again in 2012 by the Financial Times and Mergermarket, the financial data provider, at the Asia Pacific M&A Awards, based on our league table standings in mergers and acquisitions.

安永正在建设更美好的商业世界

EY is building a better working world

携手安永,携手安永,建设更美好建设更美好商业世界商业世界

Start buildingwith EY安永人每天与客户或同事的每次交

流,都为建设较前更美好的商业世

界作出贡献。

我们了解到不能仅靠个人达到安永

的目标。通过聚焦共同目标,就能

携手建设更美好的商业世界。

Every day, every EY person is part of building a better working world - every interaction with a client or colleague, contributes to making the working world better than it was before.

We realize we won’t achieve our purpose alone. By focusing on a shared agenda, we can help build a better working world together.

请浏览 Visit ey.com/china.

54

On

the

BEA

M

55

风向

中国医药企业之中国医药企业之

并购重组并购重组Mergers and Acquisitions among China’s Pharmaceutical Enterprises

Industry Focus 行业焦点行业焦点

张丽丽张丽丽审计合伙人

孙羽孙羽

审计經理

Lillian ZhangPartner, Assurance

Carrie SunManager, Assurance

56

On

the

BEA

M

57

风向

中国医药企业并购重组的现状中国医药企业并购重组的现状

目前,我国医药行业的并购重组正风起云涌。

根据清科研究中心发布的《2012年中国并购市

场年度研究报告》显示,2012年中国并购市

场生物技术、医疗健康行业共发生67起并购,

平均每个星期就有一起并购案发生,并购总金

额达103.957亿元人民币,其激烈程度可见一

斑。在2012年的药企收购中并购金额超过2亿元人民币以上的案例就有近十单,包括中新

药业收购宏仁堂药业、康恩贝制药并购伊泰药

业、永泰投资并购联环集团、现代制药并购容

生制药、华润三九并购顺峰药业、仁和药业收

购江西药都樟树制药以及沃森生物收购上海泽

润等。

2012年12月11日,国家食品药品监管局、国

家发展改革委、工业和信息化部、卫生部等四

部门印发《关于加快实施新修订药品生产质量

管理规范促进医药产业升级有关问题的通知》,

推出兼并重组、认证检查、药品注册审评审

批、委托生产、价格调整、招标采购和技术改

造等七个方面的鼓励措施,鼓励和引导药品生

产企业尽快达到新修订药品生产质量管理规范

的要求。据政府部门相关人士表示,未来我国

医药产业政策的发展重点包括推动自主创新能

力提升,促进仿制药发展水平提高以及推动兼

并重组和提高产业集中度。预期医药行业在未

来几年中迎来新一轮的并购重组热潮。

中国医药企业并购重组的原因中国医药企业并购重组的原因

从国际上看,发达国家的医药商业集中度都在

90%以上。而我国医药行业一直处于“分散的

小本经营”的态势,国内制药企业达6000多家、GMP生产车间达4000多家、医药包装生

产企业有1500多家、医疗器械领域企业超过了

10000家,行业集中度仍然较低,企业重复建

设情况频发,资源未达到最优配置,药企之间恶

意竞争的现象十分严重。在行业环境不甚理想

的情况下,一些中小型药企的经营举步维艰,

特别是对于一些创新能力及研发能力较弱的企

业,自身发展受到了极大的限制,激烈的产品

同质化竞争令其面临严峻的生存危机,在此形

势下,被收购成为这些企业较为理想的选择。

针对当前不合理的产业结构,政府部门也在制

定相关产业政策进行积极调整,以促进医药产

业的升级。2011年3月1日,新版《药品生产质

量管理规范(2010年修订)》(简称“新版药品

GMP”)开始施行。现有药品生产企业将给予不

超过5年的过渡期,达到新版药品GMP的要求。

新建药品生产企业、药品生产企业新建

(改、扩建)车间应符合新版药品GMP的要

求。然而,新版药品GMP的认证情况却不容乐

观。根据国家食品药品监督管理局摸底调查,

大约有23%无菌药品生产企业计划在2012年底

前通过新版药品GMP认证,有60%计划在2013年底通过认证,另有17%在2013年底前不能通

过认证。如果在限定日期前无法通过新版GMP认证的话,等待这些企业的只有停产歇业。

58

On

the

BEA

M

59

风向

企业并购中的关注点企业并购中的关注点

企业发起并购,从根本上来说是受

到了资本的逐利性驱使,通过并购

来实现增加效益、提升利润,扩大

企业规模。要达到这一目的,在兼

并收购的目标对象的选择上就要慎

之又慎,要明确并购后能为企业带

来哪些竞争优势。选择有如下几

种:

• 一是选择生产和销售同类产品或

生产工艺相近的企业进行并购,

这样一方面可以降低同业之间的

恶意竞争,获得技术共享利益,

扩大市场份额,增强在未来市场

中的竞争优势;另一方面并购后

企业也可以迅速扩大生产,达到

规模经济效应,在更大范围内和

更高水平上实现专业化分工协

作,从而提高产品质量,降低产

品成本,提高收益率。例如力生

制药收编中央药业以降低双方

在头孢地尼药物生产上的同业竞

争,康芝药业通过收购延风制药

以形成药业产品互补。

• 二是必须识别上游目标,如原材

料供应商。这可压缩成本,统筹

安排原材料采购和产品的销售和

分销,更好地确保供给和需求。

企业也可选择一个下游目标,如

从事分销的企业。这可通过纵向

收购扩大销售渠道,从而影响生

产链整合。一致药业收购苏州万

庆,向上游原料药延伸以降低成

本,科伦药业收购上游生产塑料

输液容器用盖的企业君健塑胶,

双鹭药业收购普仁鸿药业,向医

药业务领域延伸以弥补自身的

营销能力不足,沃森生物收购

医药销售公司宁波普诺和莆田

圣泰,复星医药先后收购了安

徽济民肿瘤医院、岳阳广济医

院、宿迁钟吾医院和高端医疗

服务连锁机构和睦家医院来扩

充其医疗服务板块。

• 三是为了获得某一品牌、专利、

某一知名产品或是进入某一新

的产业领域而进行的收购,注

重自身与被并购方资产或资源

的互补性,这样可以完善企业

自身的产品组合,赢得细分市

场,产生独特的竞争优势。例如

先声药业通过烟台麦得津公司

获得重磅抗癌药恩度,济民可

信通过收购江西金水宝制药厂

获得其旗舰产品金水宝胶囊,

山东绿叶制药集团通过收购四

川宝光,奠定了其在糖尿病领

域市场地位,丰富了绿叶制药

消化科和骨科领域的产品线。

• 此外,在并购重组的案例中,

医药行业与其他行业有个明显

不同的是企业的并购一般涉

及到大量的知识产权和资质资

格,这也是一个企业的核心竞

争力。当前,医药企业要想依

靠自身实力来取得专利等知识

产权,不仅耗资大,周期长,

也要克服严格的监管规定造成

的障碍。相比之下,通过并购

来获取知识产权以迅速提升企

业的竞争力成为了一个不错的

选择。

当然,在企业并购过程中还有一

个不容忽视的问题就是资源的整

合。实践证明,许多企业并购重

组后在组织结构、人力资源和

企业文化整合方面缺乏足够的

重视和必要的管理,企业间的

资源融合配置不甚理想,甚至

在局部由于缺乏沟通理解而产

生冲突矛盾,这也使得并购后

的业绩无法达到预期目标。换

言之,要想实现成功的并购,

不单单是机器设备、人员技术

的简单叠加,更重要的是企业

资源文化的优化配置与组合,

只有在业务整合和文化整合都

完成的情况下,才能使企业的

并购获得1+1>2的效果。

中国医药企业并购的未来趋中国医药企业并购的未来趋

势展望势展望

当前,在产业政策和宏观经济环境

的驱动下,我国医药行业洗牌进一

步加速,大量属于重复建设型的医

药企业将被兼并重组,市场集中度

将进一步得到提高,朝着规模化、

集约化的方向发展,产业结构更加

合理。在不断升温的并购重组中,

资源逐步集中到了少数优势企业的

手中,医药行业将会由少数医药巨

头所把控,采用战略资源互补的强

强联合模式以面对来自国外医药巨

头的竞争压力,行业垄断的态势将

初步呈现。商务部在《药品流通企

业“十二五”规划》已明确提出未

来5年要形成1~3家年销售额过千

亿元人民币的全国性大型医药商业

集团和20家年销售额过百亿元人民

币的区域性药品流通企业。

根据IMS市场预测,中国医药市场

在2010至2020年的年递增幅度高

达15.5%。在一波又一波的并购潮

中,少数中国医药企业的实力不断

提升,资本日益雄厚,这些企业完

全有能力通过收购国外一些规模

不大、但是产品、研发、营销有其

独特优势的中小型企业来获取其研

发技术和人力资源,营销渠道,扩

大企业生产经营规模,降低成本费

用,提升行业地位,提高市场份

额。因此,跨国医药企业并购也成

为了未来行业发展的一个新趋势。

例如海普瑞收购Prometic 10.02%股权,切入蛋白质技术和生物制药

产品技术研发,人福医药通过并购

美国普克医药公司,计划从品牌

药、仿制药和非处方药这3个方面

开拓美国市场。药明康德并购美国

百奇生物公司,打造国际生物试剂

产业“航母”。

从医药工业“十二五”发展规划来

看,现代中药、生物技术药物、化

学药新品种等被规划为未来行业重

点发展领域。跨领域并购、多元化

发展也必将成为未来医药企业并购

的一个亮点。

60

On

the

BEA

M

61

风向

Currently, China’s pharmaceutical industry is undergoing a wave of mergers and acquisitions. According to the “Annual Report on the Research in China’s

Merger and Acquisition Market 2012” published by Zero2IPO Group, there were 67 mergers and acquisitions in the domestic biotech and medical and health industries in 2012, averaging one each week. The total amount reached 10.3957 billion yuan in revenues. In 2012, close to ten M&As among drug companies topped 200 million yuan in revenues. Zhongxin Pharmaceuticals acquired Hongrentang; Conba merged with Yitai Pharmaceuticals; Yongtai acquired Lianhuan; Shyndec merged with Rongsheng Pharmaceutical; China Resources Sanjiu acquired ShunFeng Pharmaceutical; Renhe Pharmacy acquired Zhangshu zhiyao of the Drug Capital of Jiangxi; and Walvax Biotechnology acquired Shanghai Zerun Biotech.