Embed Size (px)

Citation preview

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 1/68

A Training Project reportOn Life Insurance

At TATA AIGLife Insurance Co. Pvt. Ltd ., c-scheme, JAIPUR.

Submitted in partial fulfilment of the requirementof Bachelor of Business Administration (BBA), Guru

Jambheshwar University of Science & Technlogy,Hisar .

Training SupervisorSubmitted byName & Designation SHIVKUMAR

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 2/68

of the SupervisorEnrolment No.Mr. AMIT CHOUHAN

07511001003

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 3/68

Acknowledgement

I owe my sincere & heartiest gratitude to Mr. Areejit Gupta (Branch Manager of

TATA AIG Life Insurance Corporation of India, c-scheme, Jaipur, Rajasthan) who

gave me the opportunity to work in TATA AIG Life Insurance Company as a

summer trainee & helped with whenever I needed him.

I also thank Mr .Amit Chouhan (Operation Manager, TATA-AIG Life InsuranceCompany, C-scheme, Branch)& Mr. kunal Dutta (Sales Manager of TATA-AIGLife Insurance Company, C-scheme, Branch) who helped to carry out the training

successfully.

I also thank management of insurance brokerage firms, banks & corporate agents

& many people to whom I visited during my training period.

Besides above I am grateful to everyone who has helped me in completing mytask to my satisfaction level.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 4/68

DECLARATION

I, SHIV KUMAR, Student of BBA Session 2007-2010, declare that the present work titled “ LIFE INSURANCE ” is an original work. I anywhere

else for the award of any degree/ diploma/ certificate or for any prize have

not submitted this project report. All the data given in the report is to the

best of my knowledge and all references whether of any person or

organization can be crosschecked.

SHIV KUMAR

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 5/68

Preface

Place allotted t me for my summer training in TATA AIG LIFE INSURNACE

COMPANY LTD as Jaipur. It is the place which needs no introduction to any

person in at least India. It is the capital of state Rajasthan. It is the largest city of Rajasthan and approx 35 lack people are living here. It is also a historical place.

Being a state capital all the big government office are situated here and all the

commercial activities are happen here. The main industries are Gems and

Jewellery, Printing and Tourism situated here. There are many Engineering,

Management and other Technology colleges situated. So the availability of trained

human resources is sufficient here.

In the recent past there has been a significant amount of investment had been done

by government to improve the basic infrastructure that is why the investors from

India as well as foreign are investing at Jaipur.

So there are plenty of scope for insurance business at Jaipur.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 6/68

ContentsIntroduction 5

1.History Of insurance

2.Liberalization of the Insurance Sector

Industry Overview 8

1.What is Insurance?

2.Reason for Insurance

3.Importance for Insurance

4.Advantages of Life Insurance

Company Profile 12

1.TATA-AIG Life Insurance Pvt. Ltd.

2.Sponsors

3.Prudential Plc.

4.Bank Assurance

5.Technology

6.Vision of the company7.market place

8.Market Share

8.Sales Channel

9.Advisors

Finding Suitable Profile For Insurance Sales 21

Search And Fix Criteria About Suitable Profile Of Insurance Sales 22

Questionnaires and Research Findings Charts 25

Regulations- The Agency Laws 32

The Insurance Regulatory & Development Authority 33

Advisors 39

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 7/68

The Typical Career Progression Path 55

Recommendations 62

Conclusion 63

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 8/68

Introduction

History of Insurance

Historians believe that insurance first developed in Summer & Babylonia. The merchants &

traders of these societies transferred & pooled their money to protect themselves from pirates.

In the 18 th century BC, Babylonian king, Hammurabi developed a code of law known as the code

of specific rules governing the practices of early risk-sharing activities.

Insurance developed during the 1700’s in the North American colonies. In 1730, Benjamin Frank

contributed for the Insurance of Houses from Loss by Fire. The company collected contributions& this money went into an investment fund. Interest on this fund went towards paying claims

dividends to those who contributed money.

The Industrial Revolution in the US, in the early & mid 1800’s prompted dramatic group. During

this time, many companies were establishes to sell life insurance policies & annuities. Several

shared profits among policyholders, also developed. In addition, some life insurance companies

charged premiums according to age of people & health.

Life insurance, in its present form, came to India from the United Kingdom with the

establishment of a British firm, Oriental Life Insurance Company in Calcutta in 1818, followed

by Bombay Life Insurance Assurance Company in 1823, the Madras Equitable Life Insurance

Society in 1829, & the Oriental Government Security Life Assurance Company in 1874. Prior to

1871, Indian lives were treated as sub-standard & charged extra premium of 15% to 20%.

Bombay Mutual Life Assurance Society, an Indian insurer which came into existence in 1871,

was the first to cover Indian lives at normal rates.

The Indian Life Assurance Companies Act, 1912 was the first statutory measure to regulate life

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 9/68

insurance business. Later in 1928, the Indian Insurance Companies Act was enacted, to enable

the govt. to collect statistical information about both life & non-life insurance business transacted

in India by Indian & foreign insurers, including the provident insurance society. Comprehensive

arrangements were, however, brought into effect with the enactment of the Insurance Act, 1938.

Efforts in this direction continued progressively & the Act was amended in1950, making far

reaching changes, such as requirement of equity capital for companies carrying on life insurance

business, stricter controls on investment of life insurance companies, ceiling on the expenses of

management & agency commission etc.

By 1956, 154 insurers, 16 non-Indian insurers & 75 provident societies were carrying on life

insurance business in India. On 19 th January 1956, the management of the entire life insurance

business of 229 Indian insurers & provident insurance societies & the Indian life insurance business of 16 non-Indian life insurance companies then operating in India, was taken over by

the central govt. & then nationalized on 1 st September 1956 when Life Insurance Corporation

came into existence.

An ordinance was passed in 1968 to amend the Insurance Act to regulate/control non-life

insurance resulting in set up of GIC in 1973. Malhotra committee submitted its report in 1994 &

recommended means to reintroduce an element of competition by withdrawing the exclusivity of

LIC & GIC. In 1997, Insurance Regulatory Authority (IRA) was established which was later re-

styled as IRDA in 1999.

Liberalization of the Insurance Sector

Liberalization commitments of the country to help in disciplining future economic policies will

include the insurance reforms. When the world over, insurance, markets

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 10/68

have been opened up, India cannot remain in isolation. Globalization is the new economic

reality, which is here to stay, heralding a new era of insurance in India. With the opening of the

insurance industry, India stands to gain the following major advantages:

1.Globalization will provide improved opportunities to the customers for better products,

with more reasonable & affordable pricing.

2.The customer will get quicker servicing.

3.It will enhance the savings rate.

4.Long-term funds for infrastructure development will be available to the country.

5.It will secure for India larger inflows of foreign capital needed to sustain our GDP growth.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 11/68

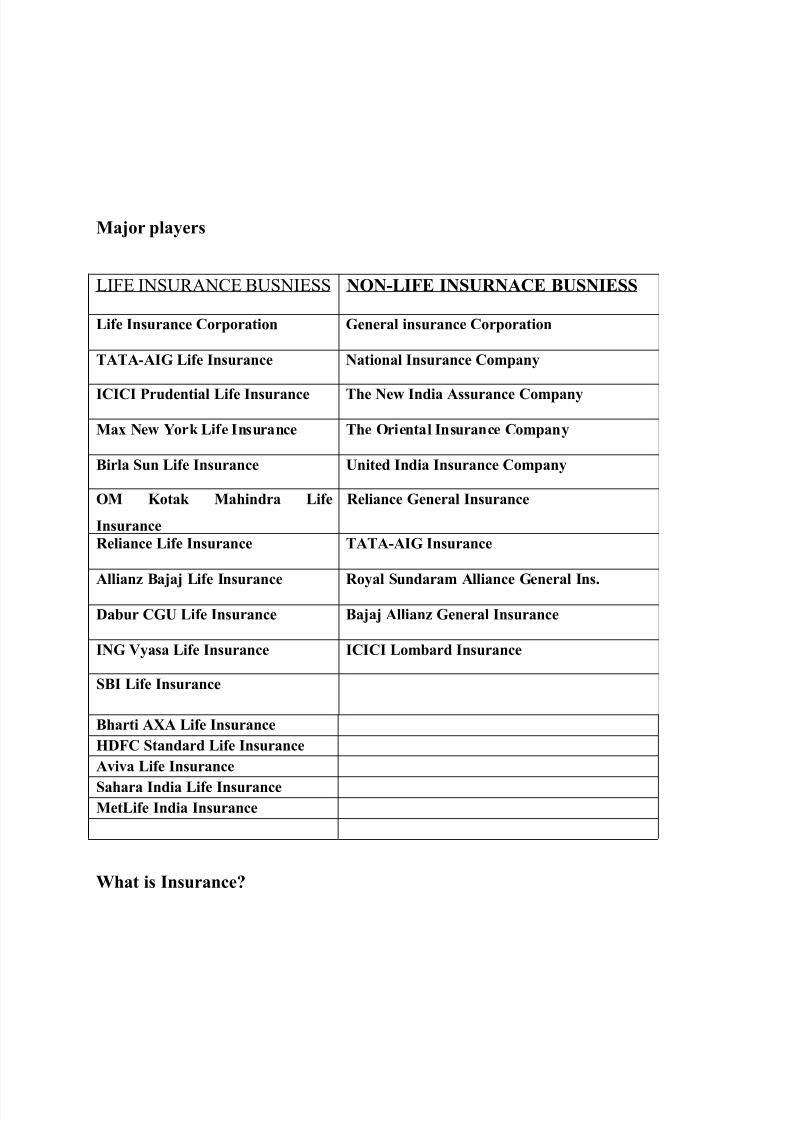

Major players

LIFE INSURANCE BUSNIESS NON-LIFE INSURNACE BUSNIESS

Life Insurance Corporation General insurance Corporation

TATA-AIG Life Insurance National Insurance Company

ICICI Prudential Life Insurance The New India Assurance Company

Max New York Life Insurance The Oriental Insurance Company

Birla Sun Life Insurance United India Insurance Company

OM Kotak Mahindra Life

Insurance

Reliance General Insurance

Reliance Life Insurance TATA-AIG Insurance

Allianz Bajaj Life Insurance Royal Sundaram Alliance General Ins.

Dabur CGU Life Insurance Bajaj Allianz General Insurance

ING Vyasa Life Insurance ICICI Lombard Insurance

SBI Life Insurance

Bharti AXA Life InsuranceHDFC Standard Life InsuranceAviva Life Insurance

Sahara India Life InsuranceMetLife India Insurance

What is Insurance?

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 12/68

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 13/68

replace risk with known costs- the costs of buying & maintaining insurance policies.

Insurance pools risks shared by many people, thereby, reducing the risks faced by a group.

People pay to buy insurance coverage (protection from risk). In exchange, all policy holders

(people who own insurance policies) receive a promise that the group of policyholders as

represented by the insurance organization will pay when any policyholder experience any kind of

loss.

Importance of Insurance

Insurance benefits society by allowing individuals to share the risks faced by many people. But it

also serves many other important economic & societal functions. Insurance provides the capital

that communities need to quickly rebuild & recover economically from natural disasters.

Insurance itself has become a significant economic force in most of the industrialized countries.

Businessmen buy insurance to cover their employees against work related injuries & health

problems. They also insure their assets against any kind of wear n tear by natural forces &

forcibly.

Insurance companies perform a type of monetary redistribution- they collect premiums &

eventually redistribute that money as payments. Depending on the type of insurance,

redistribution can take place anywhere from a month to many decades. Because of this delay

between collecting & paying out funds, insurance companies invest their funds to bring extrarevenue. Such investments help business & government finance their operations, & few profits

from these investments support the operations of insurance companies. With these investment

earnings, insurance companies can keep rates much lower than would otherwise be possible.

Advantages of Life Insurance

1.It is superior to an ordinary saving plan : Unlike other saving plans, it affords

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 14/68

2.full protection against risk of death. In case of death, the full sum assured is made available

under a life assurance policy; whereas under saving scheme the total accumulated savingalone will be available. The later will be considerably less than the sum assured, if death

occurs during early years.

2. Easy settlement & protection against creditors : The life assured can name person(s)

called Nominee to whom the policy money would be payable in the event of his death.

The proceeds of a life policy can be protected against the claim

of the creditors of the life assured by effecting a valid assignment of the policy.

3.Ready marketability & suitability for quick borrowing: After an initial period, if the

policyholder finds him unable to continue payment of premiums, he can surrender the

policy for a cash sum. Alternatively, ha can tide over a temporary difficulty by taking

loan on the sole security of the policy without delay. Further, a life insurance policy is

sometimes acceptable as security for a commercial loan.

4.Tax Relief: The Indian Income-Tax Act allows deduction of certain portion of the taxable

income, which is diverted to payment of life insurance premiums from the total income

tax liability. When this tax relief is taken into account, it will be found that the assured is

in effect paying a lower premium for his insurance.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 15/68

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 16/68

term products, endowment products as well as money-back products. For groups and individuals,

various types of add-ons and options are available to give consumers flexibility and choice. The

company has also designed specific products for the financially challenged and underpriviledged.

Sponsors

Tata AIG Life Insurance Company Limited (Tata AIG Life) is a joint venture company, formed

by the Tata Group and American International Group, Inc. (AIG). Tata AIG Life combines

the Tata Group’s pre-eminent leadership position in India and AIG’s global presence as the

world’s leading international insurance and financial services organization. The Tata Group

holds 74 per cent stake in the insurance venture with AIG holding the balance 26 percent. Tata

AIG Life provides insurance solutions to individuals and corporates. Tata AIG Life Insurance

Company was licensed to operate in India on February 12, 2001 and started operations on April

1, 2001.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 17/68

THE TATA GROUP

The Tata Group (www.tata.com) is one of India's largest and most respected businessconglomerates, with revenues in 2006-07 of $28.8 billion (Rs.129,994 crores), the equivalent of about 3.2 per cent of the country's GDP, and a market capitalization of $72.2 billion as onDecember 6, 2007. Tata companies together employ some 289,500 people. The Tata Group hasoperations in more than 85 countries across six continents, and its companies export productsand services to 80 countries.

The Tata Group comprises 98 operating companies in seven business sectors: information

systems and communications; engineering; materials; services; energy; consumer

products; and chemicals. The Group was founded by Jamsetji Tata in the mid 19 th

century, a period when India had just set out on the road to gaining independence from

British rule. Consequently, Jamsetji Tata and those who followed him aligned business

opportunities with the objective of nation building. This approach remains enshrined in

the Group's ethos to this day.

The Tata Group is one of India's largest and most respected business conglomerates, with

revenues in 2006-07 of $28.8 billion (Rs129,994 crore), the equivalent of about 3.2 per

cent of the country's GDP, and a market capitalisation of $65.32 billion as on February 7,

2008. Tata companies together employ some 289,500 people. The Group's 27 publicly

listed enterprises — among them stand out names such as Tata Steel, Tata Consultancy

Services, Tata Motors and Tata Tea — have a combined market capitalisation that is the

highest among Indian business houses in the private sector, and a shareholder base of

over 2.9 million. The Tata Group has operations in more than 80 countries across sixcontinents, and its companies export products and services to 85 countries.

The Tata family of companies shares a set of five core values: integrity, understanding,

excellence, unity and responsibility. These values, which have been part of the Group's

beliefs and convictions from its earliest days, continue to guide and drive the business

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 18/68

decisions of Tata companies. The Group and its enterprises have been steadfast and

distinctive in their adherence to business ethics and their commitment to corporate social

responsibility. This is a legacy that has earned the Group the trust of many millions of

stakeholders in a measure few business houses anywhere in the world can match.

Industries and companies

Tata companies offer an abundance of products and services for industry and companies in India

and a host of other countries around the world. These products and services have been arranged

in alphabetical order here, with links leading to specific pages that highlight individual products

and services.

Agricultural inputsAgrochemicals (Rallis)Fertilisers (Tata Chemicals)

Automotive Automotive accessories (Tata AutoComp GY Batteries)Automotive components (TACO)Automotive services (TACO, Tata Technologies)Commercial vehicles (Tata Motors)Diesel engines (Tata Cummins)

Aviation

Charter flights (Taj Air)

Chemicals

Chemicals (Tata Chemicals, Rallis)De-sulphurising compounds (Jamipol)

Communications Broadband services (Tata Indicom)Telecommunications (Tata Indicom)

Consultancy Management consultancy (Tata Economic Consultancy Services, Tata Strategic Management Group)

Electronics

Digital disc recorder (Tata Elxsi) Energy

Oil and gas (Tata Power)Power (Tata Power, Tata Projects)Solar energy (Tata BP Solar)

Engineering

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 19/68

Air-conditioning products and services (Voltas)

Bearings (Tata Steel)

Construction equipment (Telcon, Voltas)

Engineering consultancy (TCE Consulting Engineers)

Engineering equipment and services (TRF, Voltas)

Engineering projects and project services (Tata Projects, Voltas)

Industrial electronics (Nelco)

Industrial machinery (Voltas)

Manufacturing engineering (TAL Manufacturing Solutions)

Mining and material handling equipment (Voltas)

Precision equipment (Tata Precision Industries)

Financial services

Insurance (Tata AIG General, Tata AIG Life)Investment (Tata Asset Management, Tata Capital, Tata Investment Corporation,Tata International AG)

Food products Coffee (Tata Coffee)Food additives (Tata Chemicals)Spices (Tata Tea, Tata Coffee)Tea (Tata Tea, Tata Tea Inc)

Hospitality

Hospitality (Indian Hotels)

Information technology

IT-enabled services (SerWizSol)

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 20/68

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 21/68

Publishing

E-learning (Tata Interactive)

Publishing (Tata McGraw-Hill)

Trading

E-trading (mjunction services)

Trading (Tata International, Tata AG, Tata Incorporated, Tata Limited)

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 22/68

American International Group, Inc. (AIG) , a world leader in insurance and financial services,

is the leading international insurance organization with operations in more than 130 countries

and jurisdictions. AIG companies serve commercial, institutional and individual customers

through the most extensive worldwide property-casualty and life insurance networks of any

insurer. In addition, AIG companies are leading providers of retirement services, financial

services and asset management around the world. AIG's common stock is listed on the New

York Stock Exchange, as well as the stock exchanges in Paris, Switzerland and Tokyo.

American International Group, Inc. (AIG) is a major American insurance corporation based in

New York City. It has its European HQ in Croydon in London, England, UK and its Asian HQ in

Hong Kong, China. AIG is the sixth-largest company in the world according to the 2007

Forbes Global 2000 list. The company became a component of the Dow Jones Industrial

Average on April 8, 2004. It is also the sponsor of Manchester United F.C. On December 11,

2006 it was announced that a division of AIG would purchase from Dubai Ports World disputed

North American ports.

History

AIG's history dates back to 1919 by when Cornelius Vander Starr set up an insurance agency in

Shanghai, China. Starr was the first Westerner in Shanghai to sell insurance to the Chinese.

When his business was successful there, he expanded to Asia, Latin America, Europe, and the

Middle East.

In 1962, Starr gave management of the company's unsuccessful U.S. holdings to Maurice R."Hank" Greenberg, who shifted the company's U.S. focus from personal insurance to high-

margin corporate coverage. Greenberg focused on selling the insurance through independent

brokers rather than agents because Greenberg wanted to avoid selling insurance at prices which

occasionally became too low (to cover the future payouts) given marketplace competition; a

company with agents must pay their salary even while selling little to no insurance. Instead, with

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 23/68

brokers, AIG could price insurance properly even if it suffered decreased sales of certain

products for long lengths of time with very little extra expense. In 1968, Starr named Greenberg

his successor. The company went public in 1969. Greenberg resigned as the company's CEO in

February 2005 amid concern from the board about regulatory inquiries.

On 6 April 2006, AIG president and chief executive Martin J. Sullivan, announced American

International Group (AIG) as the new shirt sponsors of English football team Manchester United,

in a British record shirt sponsorship deal of £56.5 million (£14.1 million a year) over four years.

Sponsorship

In 2006, AIG became main sponsors of Manchester United Football Club.

Accounting fraud claims

In 2005 AIG came under investigation for accounting fraud.

A major focus of AIG's insurance business model is the concept of an underwriting profit . For

example, an auto insurer collects money every month from its customers in the form of premium.

Should a customer have a covered auto accident, the company pays out a claim. In the time

between the receipt of each premium payment and the paying of the claim, the money received

by the insurer can be invested. Returns from investments are the primary source of profits for an

insurance company. If the amount of premiums taken in is greater than the claims paid out even

before taking into account investment returns the excess additional profit is called an

"underwriting profit". Greenberg believed that it was necessary for an insurance company to

make an underwriting profit, even though typically most insurance companies do not.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 24/68

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 25/68

A proud father of two boys and one girl, he aligns his hobbies with theirs and connects with them

through a game of tennis or football regularly.

Technology

The company continuously leverages on the state of art technology that it posses. The modern &

updated technology infrastructure helps not only to provide superior quality of products &

services to the customers but at the same time helps in creating a prudent reward & recognition

program for the company itself. The company can leverage on this advantage to drive out one of

the best CRM industry at the present. The parent company also is in a move to duplicate the

ICICI model in other world market. It is nothing but a result of the superb all-round performance

that the company has shown in all the facets of business & over the period of time. But one

important has been the continued focus on growth & the strife for results from the workforce

itself.

Vision of the Company

Their vision is to make TATA-AIG Life Insurance Company the dominant new insurer in the life

insurance industry. This they hope to achieve through their commitment to excellence, focus on

service, speed and innovation, and leveraging our technological expertise.

To be the fastest growing Life Insurance Company in India, measured by annualized premium

growth, procuring persistent business, delivering first class customer service, adding shareholder

value by 2007.

The success of the organization will be founded on its strong focus on values and clarity of

purpose. These include:

• Understanding the needs of customers and offering them superior products and service

• Leveraging technology to serve customers quickly, efficiently, & conveniently.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 26/68

• Developing & implementing superior risk management & investment strategies to offer

sustainable & stable returns to the policyholders.

• Building long lasting relationships with their partners

• Providing an enabling environment to foster growth and learning for their employees

They believe that they can play a significant role in redefining and reshaping the sector. Given

the quality of their parentage and the commitment of their team, they feel that there will be no

limits to their growth. The success of the company lies in its unflinching commitment to five

core values: - Integrity, Customers first, Boundary less, Ownership, & Passion.

Market Place

At the moment, India is one of the best markets to be in. Over 75 per cent of its vast population

has no insurance. Global reinsurance major, Swiss Re, points out that the industry will touch a

growth of up to $50 billion in the next 10 years, with individual life insurance accounting for

almost $40 billion. Little wonder, then, that top global names such as AIG, Allianz, AMR Aviva,

ING, Metlife, New YorkLife, Old Mutual, Prudential, Standard Life and Sun Life are here in

joint ventures with eminent Indian companies such as TATA, Birla, HDFC, Kotak and ICICI,

among others. The Insurance Regulatory and Development Authority (IRDA) regulations too

encourage best practices in the marketplace.

The Indian customer, like his global counterpart, buys policies for tax benefits and to ensure

secure savings for the future. Although he is price sensitive, he still deserves value and sound

services for his money. This has not been available to him. To fill this void, many private players

have initiated education campaigns explaining the benefits and need for insurance.

In its first year Tata AIG sold 33,000 policies . This fiscal the company is expected to sell morethan 1 lakh policies . The success of private players has been attributed to their innovative

offers, customer-centric products, increasing awareness levels of consumers through a need-

based, structured approach of selling, sound risk-management practices, enhanced service

standards, reaching out to the customer through a number of distribution and communications

channels, and providing advice to the customer.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 27/68

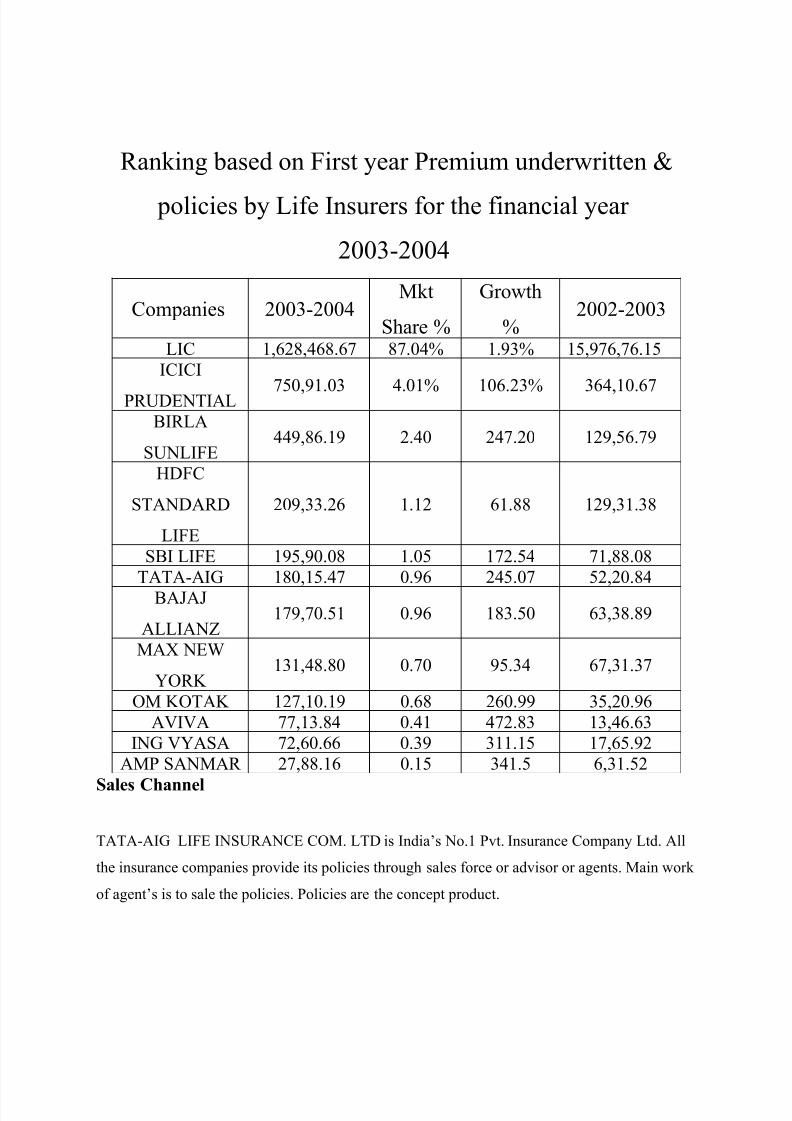

Market Share

Error: Reference source not found

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 28/68

Ranking based on First year Premium underwritten &

policies by Life Insurers for the financial year

2003-2004

Companies 2003-2004Mkt

Share %

Growth

%2002-2003

LIC 1,628,468.67 87.04% 1.93% 15,976,76.15ICICI

PRUDENTIAL 750,91.03 4.01% 106.23% 364,10.67BIRLA

SUNLIFE449,86.19 2.40 247.20 129,56.79

HDFC

STANDARD

LIFE

209,33.26 1.12 61.88 129,31.38

SBI LIFE 195,90.08 1.05 172.54 71,88.08TATA-AIG 180,15.47 0.96 245.07 52,20.84

BAJAJ

ALLIANZ179,70.51 0.96 183.50 63,38.89

MAX NEW

YORK 131,48.80 0.70 95.34 67,31.37

OM KOTAK 127,10.19 0.68 260.99 35,20.96AVIVA 77,13.84 0.41 472.83 13,46.63

ING VYASA 72,60.66 0.39 311.15 17,65.92AMP SANMAR 27,88.16 0.15 341.5 6,31.52

Sales Channel

TATA-AIG LIFE INSURANCE COM. LTD is India’s No.1 Pvt. Insurance Company Ltd. All

the insurance companies provide its policies through sales force or advisor or agents. Main work

of agent’s is to sale the policies. Policies are the concept product.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 29/68

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 30/68

advisor is an important asset not only for the organization from the business point of view but

also to the society on the whole as he/she is someone who provide valuable service to the

community be helping people attain financial security & build funds for their future needs

thereby assisting them in getting their financial freedom.

If looked from the other side of the business where the company is operating the competitive

Indian market & more so in the business of life insurance where the customers looks for self-

belief & faith then the advisor certainly holds the vital link in the overall business proposition.

They represent the company’s face & words on which the customers can trust because the

customer knows that face. The advisor helps to create a web fro the business to grow & driving

the customer to come to the company with complete trust & faith.

Finding Suitable Profile For Insurance Sales

Since privatization of insurance sector in India is a new concept for insurance market in India

hence people are not much Know about business opportunity of in the insurance field in the

insurance sector company want those persons whom are self motivated have great

communication skills and desired to earn handsome amount of money so my work in this

project to search the suitable profile for insurance sales or advisor or agent.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 31/68

First of all I researched on company`s working advisors profile. That which kind of advisors

are giving maximum sales for TATA-AIG LIFE INSURANCE COMPANY LTD. So I

collected information about current advisors working in company. Finally I selected 10 best

policies seller advisors and made observation that in Jaipur people who are between 20 to 25

year age are making business frequently on a large scale.

This age group has these basic skills and competencies:

1. The level of sincerity much more than other.

2. Want to earn a handsome amount of money .

3. Want growth in life .

4. Want recognition from society and organization .

5. Reliability in this age group much more than other.

6. They have many contact in society .

So I found that a city like Jaipur where the population approx 35 lack over 25% of this

population earns high amount of money. If an advisors makes plan on this segment of

society than he can earn great money. So I came to the conclusion that the age group of

20 to 25 year age is the best profile for advisors. The advisors who has 2 or 3 year

experience of sales market and a decent communication skill will an edit advantage to the

profile of advisors.

Search and Fix Criteria About Suitable Profile Of Insurance Sales

TATA-AIG LIFE INSURANCE COM. LTD. All the insurance company. Provide it’s policies

through sales force or advisor or agents. Main work of agent’s is to sale the policies. Policies are

the concept product.

Role of an advisor in this industry is to presents and sales the concepts in the market. An

advisors wants healthy management support and professional environment. So in this project I

am searching the suitable profile for insurance sales. I divided my project in week by week

activities and I followed these activities in this manner.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 32/68

1 week: In first week I collected general introduction about TATA-AIG LIFE

INSURANCE COMPANY LTD. then I gathered data from different sources for

suitable profile for insurance sales. First week I gathered data from my market

100 and secondary data sources like as under –

• From Yellow Pages

• From the list of employment exchange

• From Telephone Directory

• From list of student advisor bureau of university of rajasthan.

In this week I taken the knowledge about insurance sector and concept product of the

company.

First of all I researched on company`s working advisors profile. That which kind of advisors

are giving maximum sales for TATA-AIG LIFE INSURANCE COMPANY LTD. So I

collected information about current advisors working in company. Finally I selected 10 best

policies seller advisors and made observation that in Jaipur people who are between 20 to 25

year age are making business frequently on a large scale.

2 week: In second week I prepared a questionnaire for survey to collect primary data. I

surveyed at different places at Jaipur. The places are given as under

• Grand Post Office

• Central Park

• Petrol Pumps

• Clubs of different society• ATM

• Near by banks

• Cinema hall

• Big complexes and commercial showrooms

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 33/68

• Jaipur stock exchange office

• Career fair

3 week I selected some suitable profile persons and made calls . this process of collection,

selection and calling had done by me continuously or on going process.

I also sent E-mails and letters to them. I continuously met with them face to face

and give knowledge about business opportunity from TATA-AIG LIFE

INSURANCE COMPANY LTD.

4 week In this week some of the suitable profile people filled the form of advisors and I

helped them in this documentation work. I also complete the different formalities

and remaining things. Finally I gave my forms to the operation department.

5 week In this week I told about the advisors training time and venue to the persons

whom filled the forms. I continuously done my survey activity and data

collection.

6 week In this week I selected persons for advisor work. The survey, data, collection,

calling selection meeting all these activities done by me continuously.I also gained some brief knowledge about the policies of ICICI TATA-AIG LIFE

INSURANCE and other company. I compared ICICI TATA-AIG LIFE

INSURANCE COMPANY`S policies with other companies policies.

7 week I solved the problems and obligations of IRDA trainees with best of my

knowledge and communicated with then properly. I also helped them in

preparation of their IRDA Examination and solved the problem of them. I

attended the brief product training, which had given by trainer of ICICI TATA-

AIG LIFE INSURANCE COMPANY LTD.

8 week I stopped my data collection activities. I accumulated all my primary and

secondary data. I also gathered the literature about company of the insurance

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 34/68

sector and policies. I made up the sharp observation and research on data.

Regulations - The Agency Laws

The basics of the insurance business in India are governed by the Agency Law, which is part of

the Indian Contracts Act, 1872. Further, after the industry got opened up the regulatory authorityhas been the Insurance Regulatory & Development Authority (IRDA).

Agent- The Definition.

According to the section 182 of the Indian Contract Act, 1872, “an agent is a person employed to

do any act for another or to represent another in dealing with a third person”. In the insurance

sector the term “Agent” is ordinarily applied to a person engaged by the insurer to procure new business.

Powers of the Agent

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 35/68

An agent can act only to the extent of authority may be expressed or implied. An authority is said

to be expressed when it is given by words spoken or written. It is implied when it is to be

inferred from the circumstances of the case.

Life Insurance Agent

The Insurance Act, 1938 defines an agent as “one who is licensed under the act & is paid

consideration of his soliciting or procuring insurance business including business relating to

continuance, renewal or revival of policies of insurance”.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 36/68

The Insurance Regulatory & Development Authority

Duties, Powers & Functions

Section 14 of IRDA Act, 1999 lays down the duties, powers & functions of IRDA.

1Subject to the provisions of the Act & any other law for the time being in force, the

Authority shall have the duty to regulate, promote & ensure orderly growth of the

insurance business & re-insurance business.

2Without prejudice to the generality of the provisions contained in sub-section(1), the powers& functions of the Authority shall include,

1.Issue to the applicant a certificate of registration, renew, modify, withdraw, suspend or

cancel such registration.

2.protection of the interests of the policy holders, insurable interest, settlement of insurance

claim, surrender value of policy & other terms & conditions of contracts of insurance.

3.specifying requisite qualifications, code of conduct, & practical training for intermediary or

insurance intermediaries & agents;

4.specifying the code of conduct for surveyors & loss assessors;

5.promoting efficiency in the conduct of insurance business;

6.promoting & regulating organizations connected with the insurance & re-insurance

business;

7.levying fees & other charges for carrying out the purpose of this Act;

8.calling for information from, undertaking inspection of, conducting enquiries &

investigations including audit of the insurers, intermediaries, insurance intermediaries &

other organizations connected with the insurance business;

9.control & regulations of the rates, advantages, terms & conditions that may be offered by

insurer in respect of general insurance business not so controlled & regulated by the

Tariff Advisory Committee under the section 64U of the Insurance Act, 1938 (4 of 1938);

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 37/68

10.specifying the firm & manner in which books of account shall be maintained & statement

of accounts shall be rendered by insurers & other insurance intermediaries;

11.regulating investments of funds by insurance companies;

12.regulating maintenance of margin of solvency;

13.adjudications of disputes between insurers & intermediaries or insurance intermediaries;

14.supervising the functioning of the Tariff Advisory Committee;

15.Specifying the percentage of premium income of the insurer to finance schemes for

promoting & regulating professional organizations referred to in clause(f);

16.Specifying the percentage of life insurance business & general insurance business to be

undertaken by the insurer in the rural or social sector; &

17.Exercising such other powers as may be prescribed.

Essentials for the License

The IRDA has prescribed both qualifications & the disqualifications for a person to be given a

license

Qualifications

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 38/68

The person must be

1Be at least 18 years old.

2Must have passed at least 12 th standard or more (if he is appointed in a place with

population of 50,000 or more), 10 th standard otherwise.

3Have undergone training for at least 100 hours in life or general insurance business as the

case may be from an institute, approved & notified by the authority.

4Should have also passed the pre-recruitment examination conducted by the Insurance

Institute of India or any other examination body recognized by the authority.

5In case of an applicant for the composite insurance agent, he/she should have completed at

least 150 hours practical training in life & general insurance business, which may be

spread over six to eight weeks.

Disqualification

The factors that would debar a person from obtaining a license are that he/she

1Has been found to be of unsound mind by a court of competent jurisdiction

2Has been found guilty of criminal breach of trust, misappropriation, cheating, forgery or

abetment or attempt to commit any such offence.

The license once issued can be cancelled whenever the person acquires a disqualification. In the

case of companies & firms who want to become agents, the test of qualification &

disqualification would be applied to all the directors or partners.

There are two separate forms, one for individuals & another for those other than individuals, in

which the applications are to be made. The two forms are numbered by IRDA-Agent VB & are

annexed to the regulation. The applications in the respective forms have to be made to the

designated person appointed buy the insurer sponsoring the application.

The application for the license should be accomplished by proofs.

1.Of fee having been remitted to the authority.

2.Of age

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 39/68

3.Of having completed the training & passed the prescribed examination.

The fee to be sent to the authority directly is Rs. 250 for new license & for renewals applied for

within the prescribed period, viz, at least 30 days before the date of expiry. If the application is

made after the date of expiry it would be normally refused. But, if the authority is satisfied that

hardship would be caused otherwise, the license may be renewed. Prior to renewal of the license

of the license the agent should have completed at least 25 hours practical training in life or

general insurance business or at least 50 hours practical training in life & general insurance

business in the case of a composite insurance agent.

The Duties & Obligations of the Agent

As per the IRDA guidelines every advisor must be trained & licensed to sell life insurance. The

responsibilities & obligations of the advisors have been clearly defined.

1Every insurance agent should himself & the insurance company that he represents along

with the license particulars.

2The advisors should take into the actual needs of the clients before recommending a plan.

3All requisite information in respect of the products recommended should be provided with a

‘Sales Illustration’ & the premium to be paid.4The agent is obligated to disclose the scales of commission likely to be earned by him

through sale of the recommended product, should the client wish to know it.

5The nature of information required in the application form should be adequately explained

along with the requirement for supporting documents.

6Once the proposal is submitted, the advisor shall inform the status of decision by insurer

promptly.

7In case of a claim, the advisor is required to render necessary assistance in complying with

the requirements for settlement of claims by the insurer.

8He/she should not interfere with any proposal introduced by any other any insurance

advisor/agent or force the client to terminate an existing policy taken from him/her &

take a new proposal within 3 years.

9An advisor cannot induce the client to omit any material information or submit any wrong

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 40/68

information in the proposal form.

10Further no rebating or offering any inducements in lieu of taking a policy is allowed.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 41/68

Code of Conduct for the Agent

The licensing of Insurance Agent Regulations, 2000 lays down a code of conduct for the agents,

which state that, the agent shall

1Disclose the license to the prospect on demand.

2Explain all available options to the prospect.

3Disclose the scales of commission, if asked for by the prospect.

4Impress upon the prospect need to disclose all information

5Inform the insurer about any adverse habits & materials facts of the person to be insured.

6Convey to the proper about the acceptance or rejection of the proposal.

7Render necessary assistance to policyholders or claimants or beneficiaries in complying

with the requirements, asked for by the insurer.

8Advise policyholders to affect nomination.

9Make every attempts to ensure remittance of premiums by the policyholders within the

stipulated time by giving notice orally or in written.

10Not induce the prospect to submit any wrong information.

11Not interfere with the proposal introduced by other insurance agents.

12Not demand or receive share of proceeds under an insurance contract. Not cause the termination of an existing policy with a view to effect a new proposal.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 42/68

Advisors

The importance of advisors

TATA-AIG Life Insurance Co. Ltd. aspires to provide state of the art of customers’ service &

opportunities & avenues for enterprising people to grow & prosper. The company wish to grow

exponentially that is backed by the latest technology, hence offering its customers:

5Complete & diversified product portfolio.

6Faster & more accurate service.

7Multi-channel distribution systems.

8Highly trained professional sales people offering quality pre & post sales service.

It is in the above mentioned areas of personal specialization where the importance of an advisor

clearly stands out the advisor not only contribute in brining in new business for the company, but

also plays an important part in offering world class pre & post sales service to the clients to the

clients with the support of the organization. But the company in its principles clearly states outthat an advisor to means “ much more than a salesman or a saleswoman, we at TATA-AIG

recognize our advisors as the ambassadors of our organization in the market place & we

consider the advisor force would be our biggest differentiating factor in the coming years”. The

advisor is an important asset not only for the organization from the business point of view but

also to the society on the whole as he/she is someone who provide valuable service to the

community be helping people attain financial security & build funds for their future needs

thereby assisting them in getting their financial freedom.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 43/68

If looked from the other side of the business where the company is operating the competitive

Indian market & more so in the business of life insurance where the customers looks for self-

belief & faith then the advisor certainly holds the vital link in the overall business proposition.

They represent the company’s face & words on which the customers can trust because the

customer knows that face. The advisor helps to create a web fro the business to grow & driving

the customer to come to the company with complete trust & faith.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 44/68

The principle of channel development

The company in its vision out the urge to become the dominant players in the players in the

industry. The company believes that a high level of self-motivation & a coherent teamwork for

the organization can only achieve this on the whole. The company stresses great emphasis on its

core values, which are:

1Integrity

2Customer first

3Boundary less

4Ownership

5Passion

These are the foundation on which the organization works & the base for the overall business

environment of the company. based on the above mentioned ‘Pillars’ of the company the

management has devised the basic principles for the program as a whole which are as following.

Recruit the best

Experts in knowing what exactly their customers wants is well versed in spotting the talents fromthe pools & recruiting only those who have the intellect, energy, drive & the passion to initiate

new beginnings & even a lot of changes if they feel so. The incumbents are treated as winners &

the ‘custom hiring’ principle necessitates the factor of having the right person at the right place

with the right work. And definitely no compromises on expertise & competencies.

Personal Responsibility

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 45/68

The company believes that it is the prerogative of the company to create the team that it wants.

Therefore it aims at providing the learning & development conduits to employees to enhance the

domain of knowledge the important leadership & team skills.

Empowered Teams

Each employee is a stake holder in the organization & its growth. It is the one of the important

specialty here that the responsibility comes with a degree of autonomy & accountability. The

area of operation & growth is to be decided by the individuals himself. But the communication is

across the channels & ranks whereby the targets are sent & the corrective measures & rewards

also come to them. The most important factor is the employee participation & empowerment.

Rewards & Recognition

The rewards in the company are directly proportional to the work & targets achieved & gone

beyond. You work hard you earn more. The contributions done are recognized in the most

objective & transparent manner & on the demonstrated competence level. But yes there is

certainly an extra for the people who go beyond then what is expected from them.

Shared Vision & Purpose

The company focuses on having the organizations striving towards a common goal, which is

easily done through the effective communication & work channel. Large scale interactive

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 46/68

process at the organization & group level helps in getting the employees know of what is

expected of them & how has been achieved. This factor encompasses through all the critical

intervention by the team members or the mentor of the team.

The working environment

The company is in a continuous search for the best of talents in the market, which align with the

vision & mission of the organization. The company states out its working culture in certain

important factors for the interested incumbents:

1Urge from the incumbent to be a part of a world class sales steam.

2The freedom of working from his/her own office/residence.

3The flexibility of working hours, full time or part time.

4Opportunity to earn commission, bonus & incentives.

5Unlimited earnings- directly proportional to your efforts.

6Most important- the chance of flexible career.

The company is aware of the current trends in the market & the essential factors of increasing the

personal & human feeling to business. Thus, the company has got some underlying facts &

reasons for the working in a specific manner.

The company gives the space & time required to grow, achieve & to seek new domains &

opportunities. The changing dynamics of business makes it evident that the new opportunities

will come from the gaps & needs in the market. Therefore, the need is to be alert enough to

notice these new happenings & tap them as & when they arise. The people in the company are its

most important asset but the real focus should be on delivering on the promises undertaken.

The company also stresses out that the incumbents should have that urge & self-belief so that

they are confident enough of driving the innovation & change drives that they think are essential.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 47/68

The company believes in being innovative & tenacious enough to open a new domains &

horizons of business & hence regularly in the process of developing new products & offerings

state of art services to all its clients, brokers & agents in the business. Further, with the growing

symbiosis of technology in the business the company also focuses on this aspect in the sense that

it takes e-commerce & technology on a very high priority with increasing resource being targeted

at the new business economy & the internet.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 48/68

THE PROFILE OF AN ADVISOR

Qualifications

1.Age should be ideally between 25-60 years.

2.Minimum education qualification is 10 + 2.

3.Good & convincing communication skills.

4.Capacity to build an impressive network.

5.Engaged in gainful business or corporation.

6.Willing to undergo extensive training & development programs

7.Pleasing personality.

Skills & Competencies

As quoted by Mr. Shubro Mitra, Head HR, ICICI Prudential Life Insurance the company is

always on a look out for people who have the following the skills & competencies that we

require in business are:

1Actuarial skills.

2Investment management skills.

3Core operation skills.

4Core underwriting skills.

5Relationship management skills.

6Project management skills.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 49/68

Leadership & Team skills

1A passion for achieving results.

2High energy levels & infectious enthusiasm

3Open to ideas

4Strong team players

5High caliber & ability

6And above all, unyielding integrity.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 50/68

Job profile

As an advisor for the company, the role of the individual is no way limited to sell the policies of

the company. But the role basically starts from the basics of explaining the life insurance aspects

& the potential benefits to the customers. Further he is required to assist them in deciding upon

the plan that suits them the best in terms of finance and security provided. Therefore the

opportunity provided to the advisor is unlimited in no way and the typical benefits can be

mentioned as followings:

1There is absolutely no need of a startup capital.

2There is the benefit of flexible working hours.

3The freedom to work from anywhere & being one’s own boss.

4The unlimited earning benefits in form of remuneration & incentives.

5And the privilege of being a part of a world class sales team.

The role of an advisor is multifaceted in the sense that his work scope is in no way limited. But

in a nut shell the expectations from an advisor has been laid down by the management in the

following manner under two main headings:

1.Providing continuous financial advise to clients

Identifying prospective clients.

Making appointments

Conducting reviews with the prospective/existing clients.

Closing the sales contracts

Getting more referrals so as to increase the network

Providing pre & post sales services to clients

2.The advisor is also required to regularly follow the internal sales & the internal reporting

system so as to get the feed back & further leads for the prospective areas of business &

improvement.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 51/68

Benefits & Support Provided

The benefits have already been mentioned very often in the previous section but it’s necessary to

look into them as a comprehensive criterion. The main benefits & supports that an advisor would

be availing of are the distinct TATA AIG life advantages:

Rewarding career

The job profile as mentioned earlier is unlimited & an advisor will help people realize their

dreams & provide them the financial & psychological security & faith. The ultimate rewards will

be the differences made to all these lives & that would be most satisfying in the real sense.

Successful Team

Being at TATA-AIG gives the opportunity to be a part of India’s best team of life insurance

advisors. The company is numero uno among the private players in the industry & has won

numerous recognition & awards that give it the international edge.

Attractive remuneration

TATA-AIG offers the most competitive remuneration benefits at person in the industry, which

proves to be very useful from long term perspective of financial security. There is absolutely nolimit to one’s earnings & the added incentives just help as advisor to get more than what he/she

expects.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 52/68

Independence.

At TATA-AIG, the advisor is a boss in himself & in the real sense. There is the freedom to

choose the workplace, the work timings & the amount of earnings one wants to have. Moreover

there is no need of any initial capital investment, yet one can become an entrepreneur in the most

unexpected manner.

World Class Team

The company leverages on the international linkages that it has got to provide the best training

available in the industry at the present. The company aims to impart the necessary skills &

competencies to all even if there is no previous experience with the individual. The presence of

trained in-house trainers & professionals provide the necessary aspects of training required.

Moreover, the training is being provided with the help of professional institutions & centers like

the RNIS College.

Career Agency System

TATA-AIG’S commitment to Career Agency System imparts support to the advisors at every

stage of the business. The company believes in encouraging the advisors to the highest level of

success all through their career. One of the distinct factor is the opportunity & the option of a

management career option for the successful performers.

Best Infrastructure

The huge investments that the company has made to develop the state of art infrastructure

throughout the business. The infrastructure provides the necessary tools, technology & human

support that enable to build a profitable long term relationship.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 53/68

Extensive Product Portfolio

The company has got more than four hundred policies for its customers. This consists of the

unique individuals, groups, & rider policies. This extensive, diversified & comprehensive range

provides the competitive edge that no other advisor would be having in the market.

Sales & Marketing Support

The company has got unique sales & marketing tools to help & support the advisors at every

stage of the career. The sales, promotions & marketing collaterals that the company posses help

to achieve just that.

Financial Strength

TATA AIG Prudential offers the advisors & the customers’ unmatched financial strength &

solidity. The huge amount of paid up capital & growing revenues are an indicator of the same.

Support provided by the BRANCH Manager

1Field visits for the incumbents

2Training on products & selling skills

3Regular business reviews to monitor the progress

4The UM acts both as a coach & a mentor 5The UM recognizes the high performers

6Helps in becoming financially independent

But- The expectations from the team

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 54/68

1To achieve the sales targets given

2To participate in all the meetings being placed

3Attending all the training programs being arranged

4Report for the weekly reviews at the office

5Regularly following the sales process

6And the advisors are also required to follow the weekly reporting process.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 55/68

Career progression

The Tiger team

It is an exclusive program achievers among the advisors but the scope of progression is limited

only to a few hand picked all round performers. The TIGER TEAM represents a fast track career

path for the advisors. The successful candidates are recognized as Tigers. One continues to do

his/her business but the benefits come added on. The criteria for selections are:

1Age 25-40 years

2At least one year of working in the system

3Case count should be at least of two per month.

The Mobile Tigers

This program offers the following benefits:

1Part time career as a trainee

2To conduct foundation programs

3Opportunity to share the best field practices

4Chance to replicate one’s own business

5Freedom to continue with one’s business

The selection criteria for this program are:

1Age 25-40 years

2At least six months of working in the system

3Case count of at least two per month

The Pinnacle Program

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 56/68

This program is for the high achievers in the system & the major benefits that are on offer are as

following:

1A full time career as a Unit Manager

2The possibility of growth within TATA AIG.

3Greater earning potential

4The scope for personal development

The selection criteria for this program are:

4Age 25-40 years

5At least six months of working in the system

6Case count of at least two per month

Fast Track Pinnacle Program

This program offer following features:

5Offering a full time career as a Operation Manager

6Opportunity of growth within TATA AIG7Scope of greater earning potential

8The scope for personal development

The selection criteria for this program are:

7Age 25-40 years

8At least six months of working in the system

9Case count of at least five per month (for 6 months)

Agency Champion

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 57/68

This is the highest level of career progression on offer. It has got several distinct features, which

sets it apart from all the above mentioned programs. This program aims at rewarding the super-

achievers working with the company. The features of this program are as follows:

1The chance of taking one’s business to higher level.

2To develop one’s own business, i.e. to develop into an entrepreneur

3The freedom of recruiting new advisors & making one’s own team

4The potential of increased reach of network

The selection criteria for this program are as following:

1At least one year of working I the system

2Minimum of 36 policies & Rs. 3.60 lacs premium3Selection process (assessment center)

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 58/68

The Typical Career Progression Path

UM

TRAINER 12-18

MONTH ADVISOR

SALES MANAGER

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 59/68

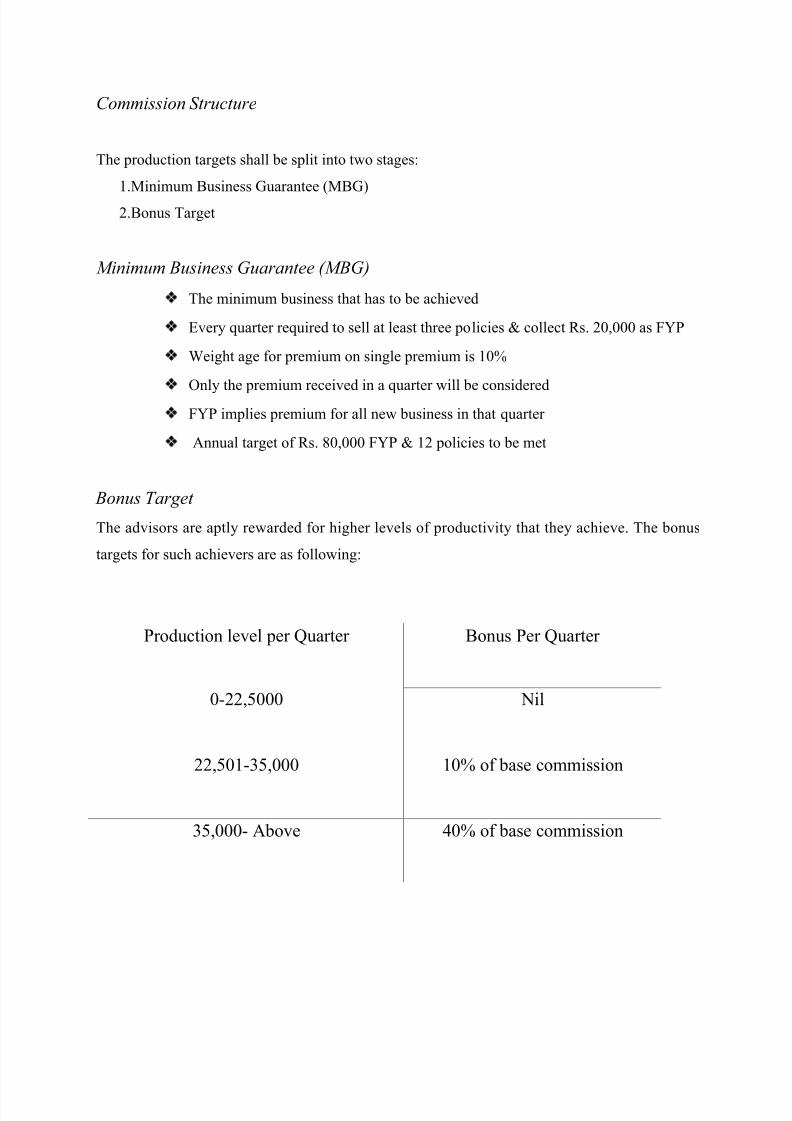

Commission Structure

The production targets shall be split into two stages:

1.Minimum Business Guarantee (MBG)

2.Bonus Target

Minimum Business Guarantee (MBG)

The minimum business that has to be achieved

Every quarter required to sell at least three policies & collect Rs. 20,000 as FYP

Weight age for premium on single premium is 10%

Only the premium received in a quarter will be consideredFYP implies premium for all new business in that quarter

Annual target of Rs. 80,000 FYP & 12 policies to be met

Bonus Target

The advisors are aptly rewarded for higher levels of productivity that they achieve. The bonus

targets for such achievers are as following:

Production level per Quarter Bonus Per Quarter

0-22,5000 Nil

22,501-35,000 10% of base commission

35,000- Above 40% of base commission

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 60/68

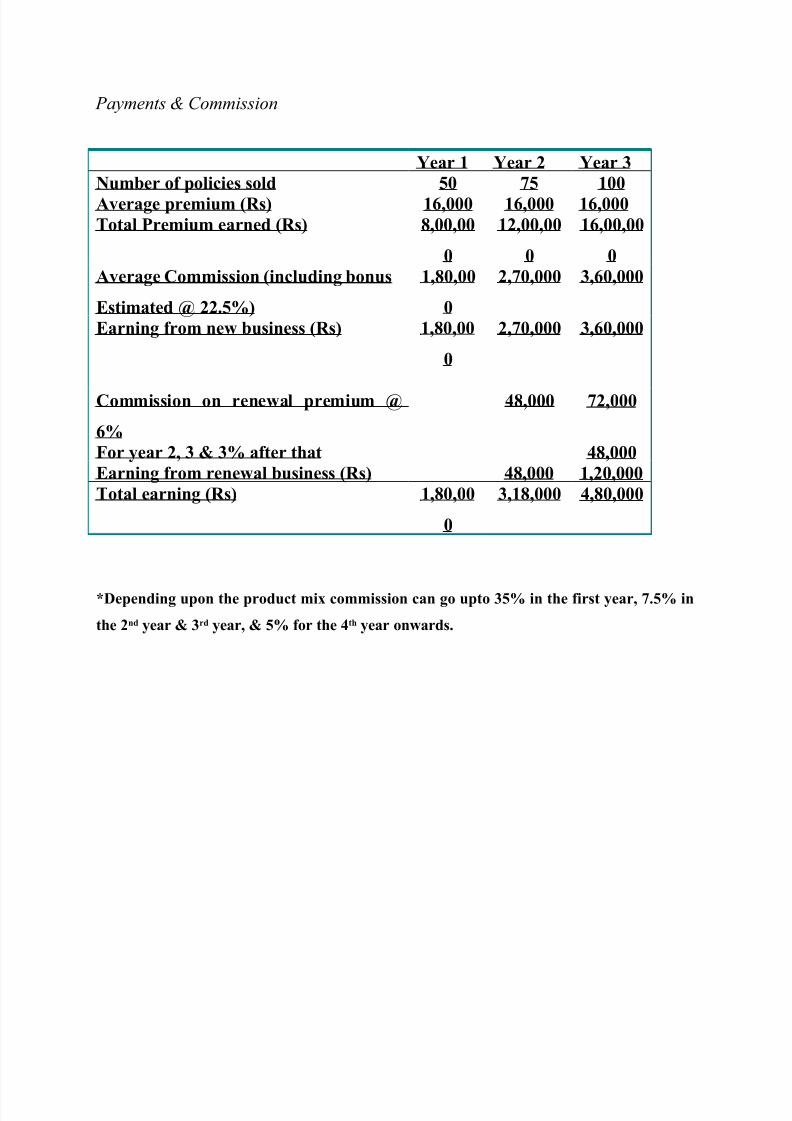

Payments & Commission

Year 1 Year 2 Year 3Number of policies sold 50 75 100Average premium (Rs) 16,000 16,000 16,000Total Premium earned (Rs) 8,00,00

0

12,00,00

0

16,00,00

0Average Commission (including bonus

Estimated @ 22.5%)

1,80,00

0

2,70,000 3,60,000

Earning from new business (Rs) 1,80,00

0

2,70,000 3,60,000

Commission on renewal premium @

6%

48,000 72,000

For year 2, 3 & 3% after that 48,000Earning from renewal business (Rs) 48,000 1,20,000Total earning (Rs) 1,80,00

0

3,18,000 4,80,000

*Depending upon the product mix commission can go upto 35% in the first year, 7.5% in

the 2 nd year & 3 rd year, & 5% for the 4 th year onwards.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 61/68

The procedures of becoming an advisor

TATA believes in getting who can align with the company’s principle & beliefs well enough to

grow on their own. In the words of the top management the company believes that one can

become an advisor for the leader only & only if he/she has the following:

1Confidence

2Self-motivation

3Persuasion

4Urge to be financially independent

5Relationship skills

The broad steps that best describe the procedure of becoming an advisor in the company are as

following:

1Confirmation of mutual interest as between the company & the individual

2Appearing & clearing the selection interview

3Profiling of the test dates between parties

4Draft payment favoring ‘TATA Life Insurance Co. Ltd.’, payable Mumbai

5Finalizing of the training dates & the venue

The company provides for the all-round development of the individual & any previous

experience or inexperience in the related field is not an obstacle. The professional approach of

the company in the training module helps it to train the incumbents in the best possible manner.

The company has got a professional in-house training staff that is one of the best in the practice.

The company has laid down for a State-of-art training on:

1Selling skills

2Product knowledge

3Relationship skills

The training is delivering through several convenient options keeping in view the requirements

of the individuals & the target of the company. The training is done at the timing & venue

decided upon by the parties concerned.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 62/68

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 63/68

STRENGTH

TATA AIG Life Insurance Company Limited is right now the market leader in Private Insurer

segment.

WEAKNESS

The company right now has lesser number of agents (i.e. financial advisors) than LIC of Indiawhich affects their sales in comparison to LIC of India.

OPPURTUNITY:

TATA AIG Life Insurance Company Limited can give LIC of INDIA agents an opportunity to

join TATA AIG Life Insurance Company Limited as TATA AIG has got more incentive packages & servicing quality better than LIC of INDIA. Doing this they can reduce their cost of

training and can exploit their experience.

THREAT:

Other big brand names like BIRLAS, ICICI PRUDENTIAL, HDFC, SBI, and AVIVA. etc.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 64/68

POLITICAL

Right one TATA AIG Life Insurance Company Limited, can go for opening up more & more

offices as the present political environment is business friendly.

ECONOMIC

Insurance as we have already discussed is very essential for every person on this face of earth.

Being an insurance company, the responsibility of the company also increases by many multiples

as they have to keep an eye on each & every happening going around & provide better & fast

service to customers. Along with this, insurance is also very important for building up the

infrastructure of any country. The money collected from the people is invested in many sectors to

develop the infrastructure & hence ultimately make the life of the citizens better.

SOCIAL

TATA AIG Life Insurance Company Limited enjoys a good brand name; they can use it for their

profit.

TECHNOLOGICAL

TATA AIG Life Insurance Company Limited uses latest technology for their operations which

give them an edge over the competition.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 65/68

Recommendations

After going through the above table regarding market share of various companies in the financial

year 2006-2007, there is no reason why TATA AIG should rejoice of being the number one

company in the country. The growth that companies like BIRLA SUNLIFE, SBI LIFE

INSURANCE, ICICI PRUDENTIAL , BAJAJ ALLIANZ, OM KOTAK MAHINDRA, AVIVA,

ING VYASA, METLIFE, & AMP SANMAR have produced that can be quite a big unseen

threat for the company in the coming years. So the company should start thinking of what they

want from the market & where they want to see themselves after a span of 10 years because if

the popularity of these companies continues then one day they will become good competitors of

ICICI Prudential & then the consequences can be quite disturbing for the company.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 66/68

Conclusion

1. TATA AIG LIFE INSURANCE COMPANY has great goodwill in market in liberalizedIndian market there are approximately 13 big companies in Indian market and TATA

AIG is the No.1 private insurance company. I found this fact in my recent survey.

2. There are lot of scope of life insurance in India only 2.5 people are secure with

life insurance so the insurance sector is it's booming stage this boom will more increase

in 2 or 3 years.

3. Good profile insurance advisor could do the better job. If TATA AIG mention the level

of advisor then they may give great sales to the company.

4. TATA AIG has tuff competition with LIC as well as ICICI PRUDENTIAL, BAJAJ

ALLIAZE, BIRLA SUNLIFE INSURANCE, SAHARA, ING VYSVA, OM KOTAK

MAHINDRA, HDFC INSURANCE AND SBI LIFE, MET LIFE, BHARTI AXA LIFE,

MAX NEW YORK LIFE.

5. If the company start to concentrate on village segment market. Then company can get

great business.

6. TATA AIG has interested and profitable planes for different age groups like smart kids

plan unit link insurance plane and pension plan.

7. I got the good profile people near by bank and share market. When I concentrated on the20-25 year age group people I found good result.

8. Within 20-25 year age group the sincerity level is high. They are career oriented and want

to earn more.

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 67/68

8/8/2019 Tata Shyam Sundar (1)

http://slidepdf.com/reader/full/tata-shyam-sundar-1 68/68

![· chandan raj arnab sarkar arnab majumder ran]it mandi ashok yadav suchand saha mondal jishu ghosh shyam sundar adai< rick tava saha pankaj kumar prasoon kumar tiwari satyendra](https://img.pdfslide.tips/doc/110x75/5e77bac1eac2172ee07bc0d3/chandan-raj-arnab-sarkar-arnab-majumder-ranit-mandi-ashok-yadav-suchand-saha-mondal.jpg)