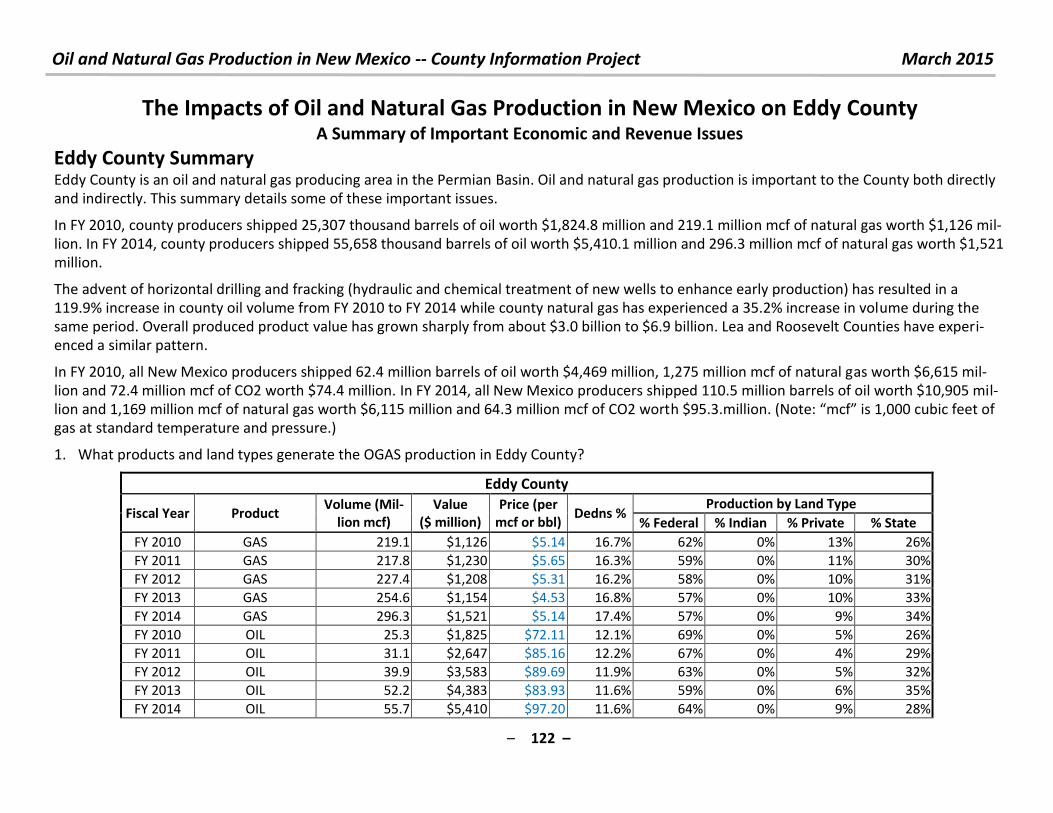

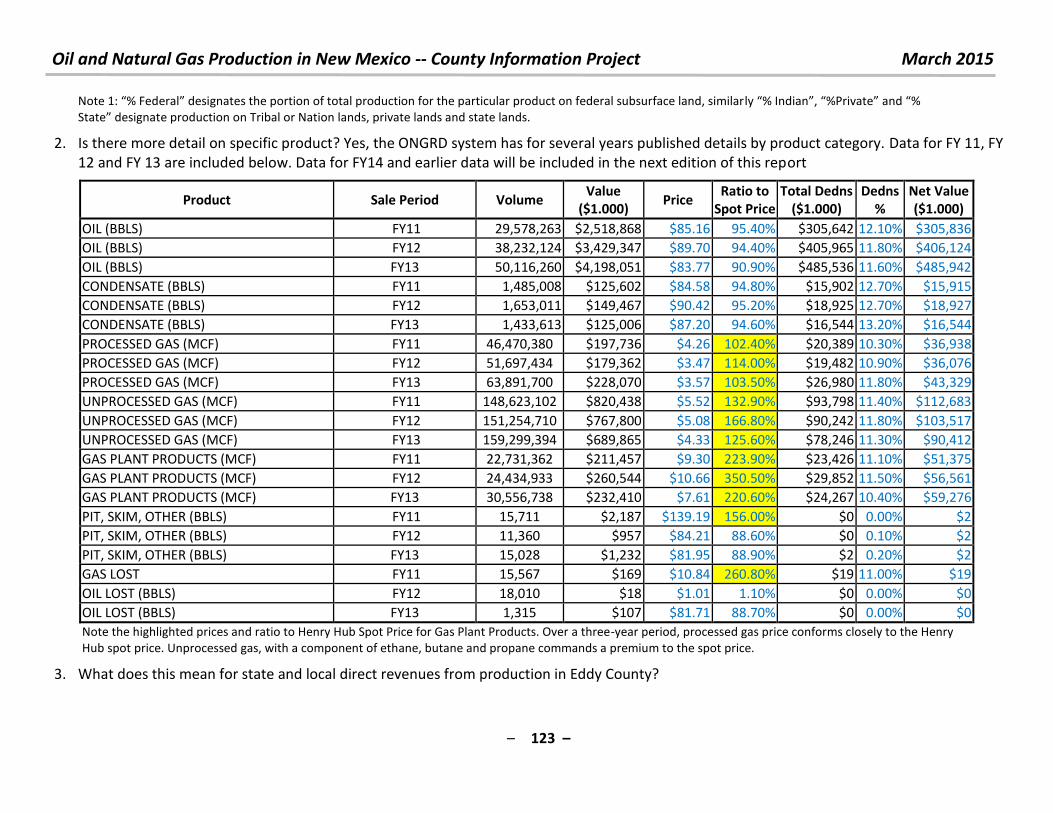

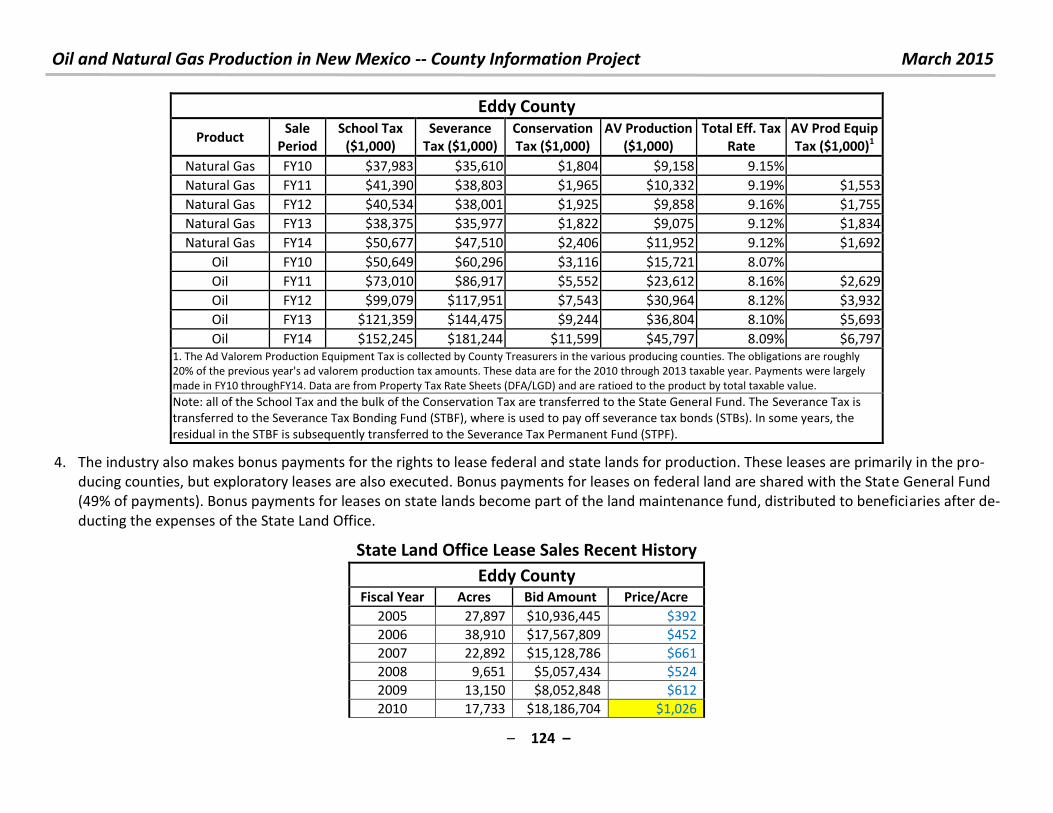

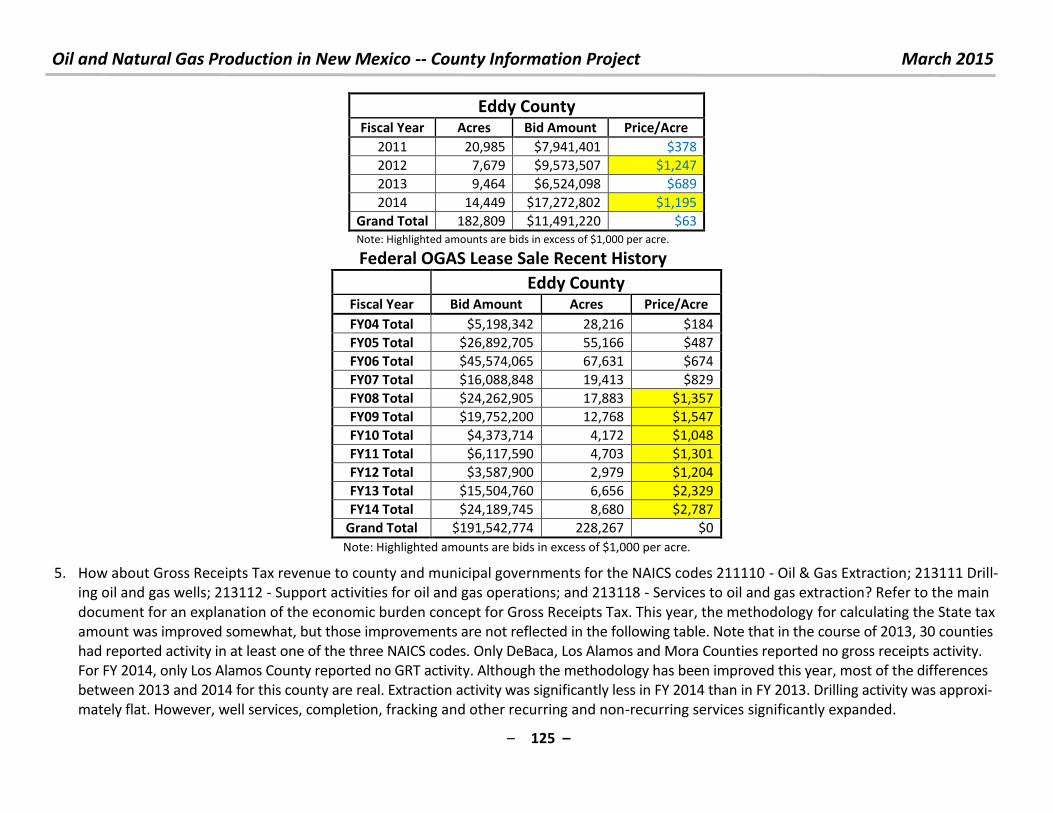

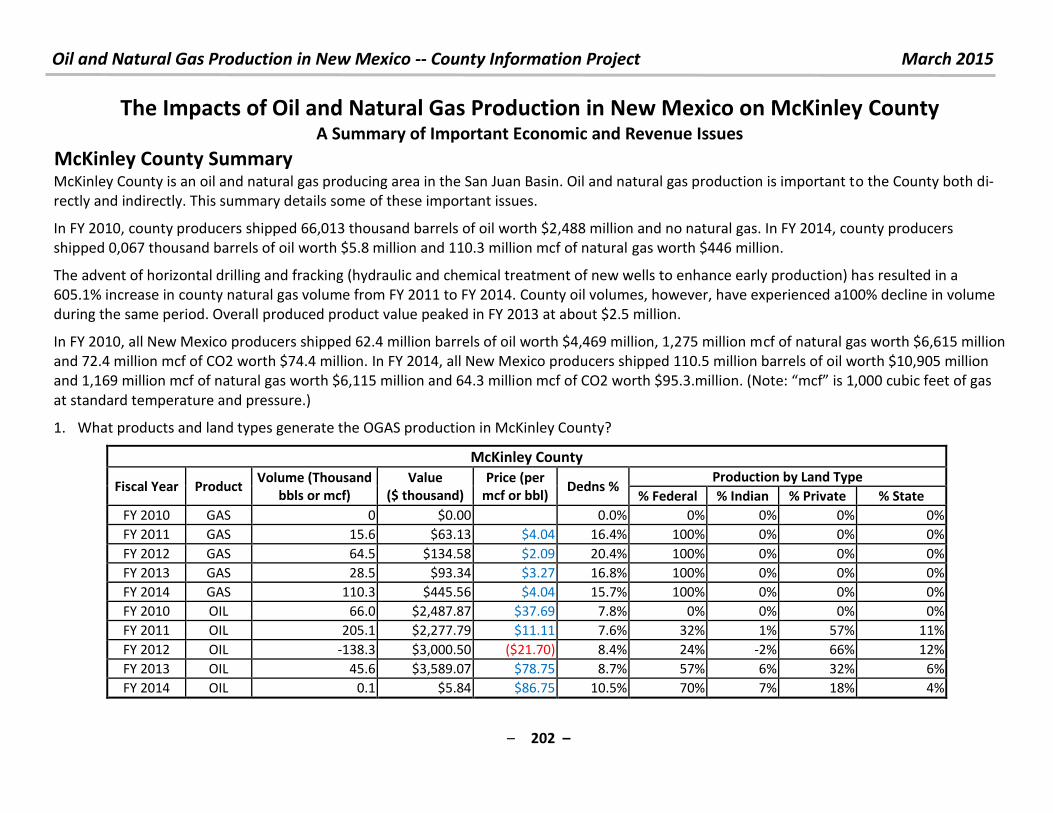

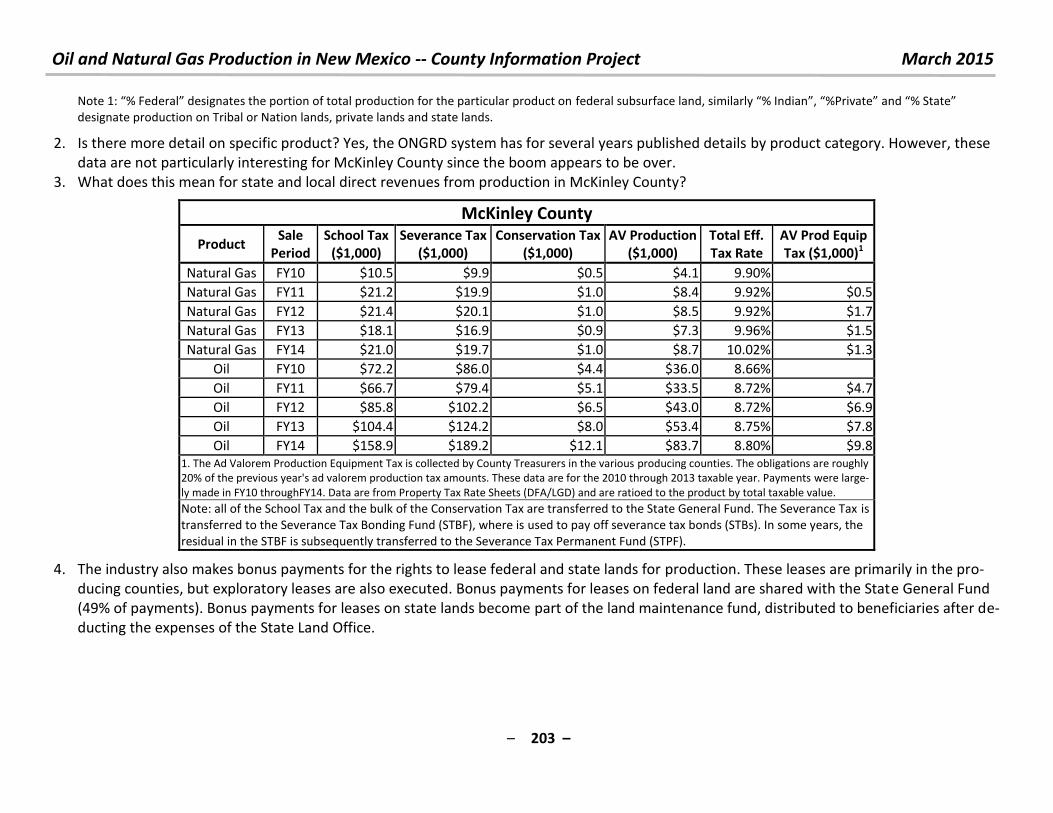

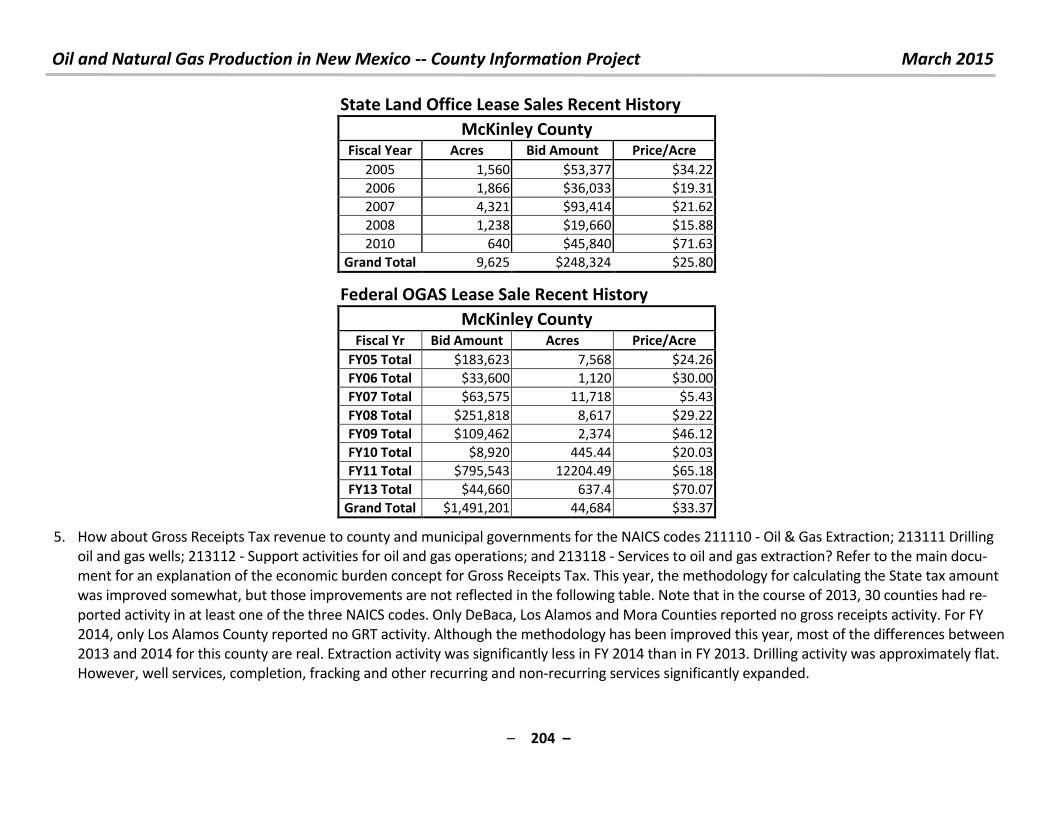

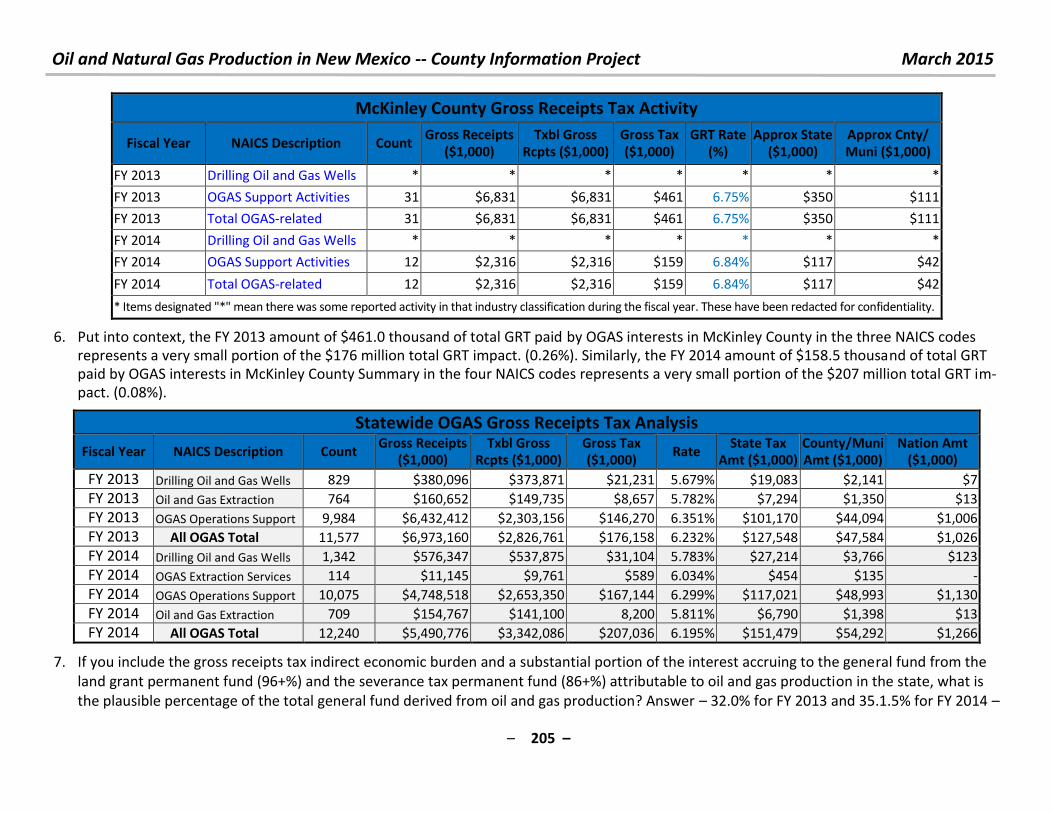

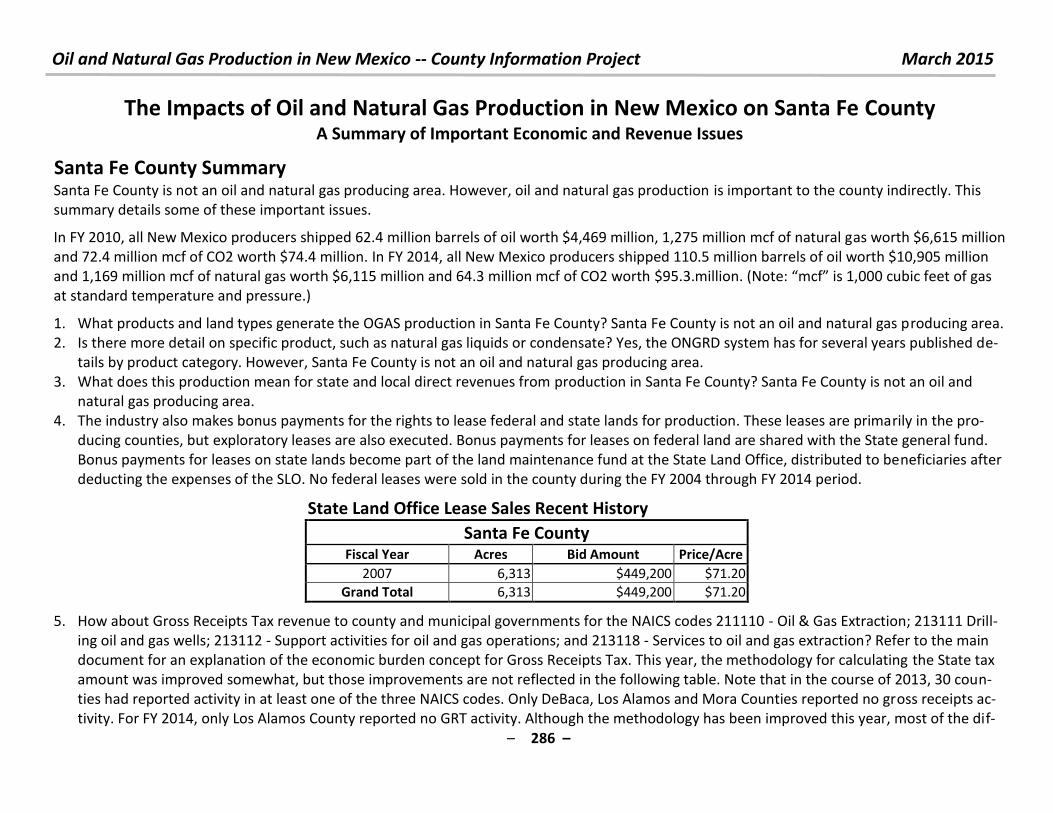

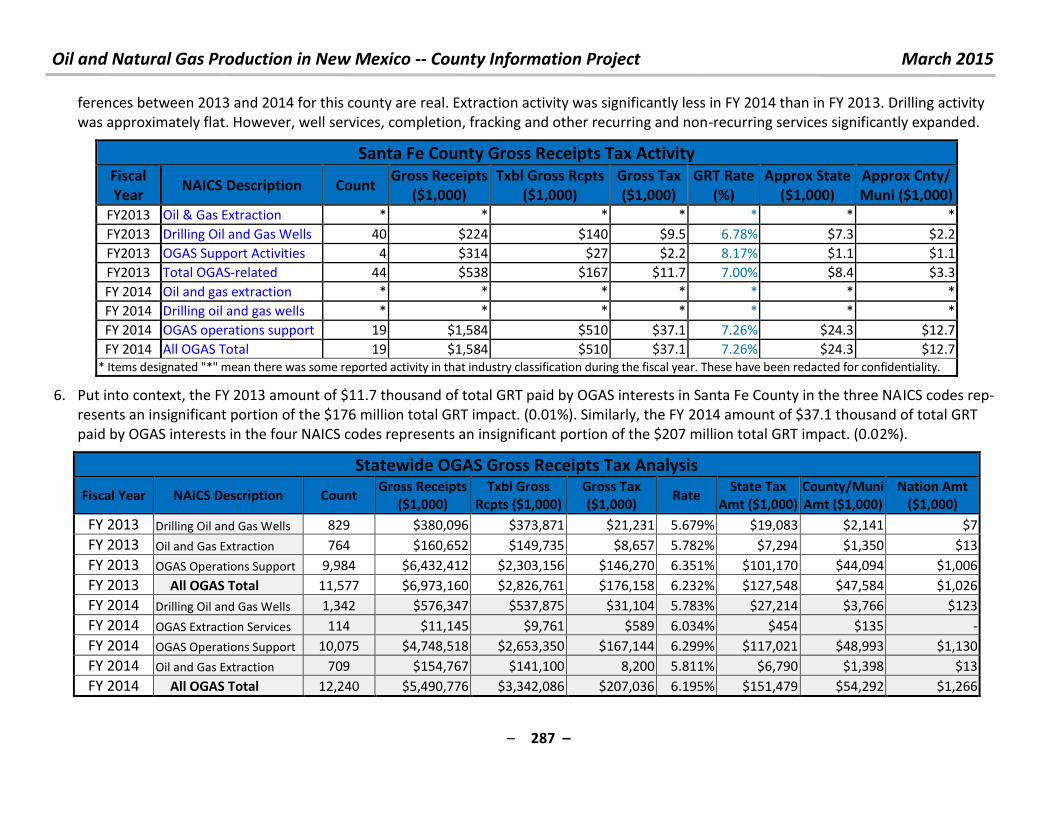

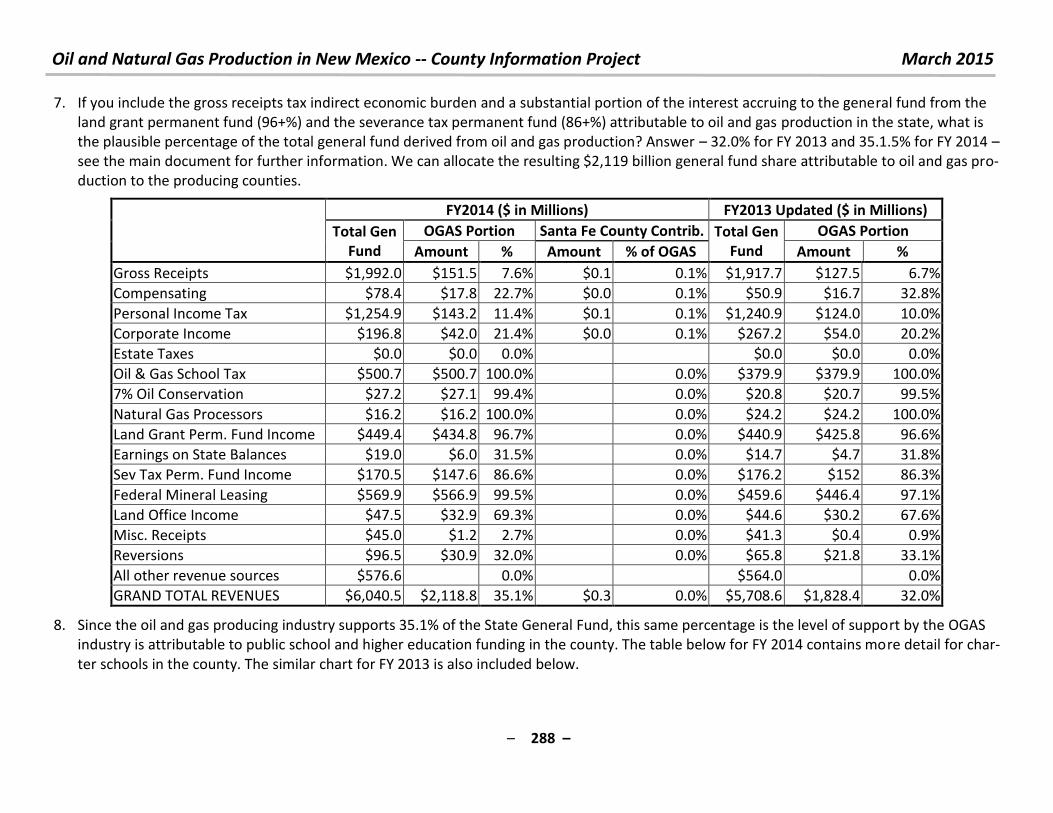

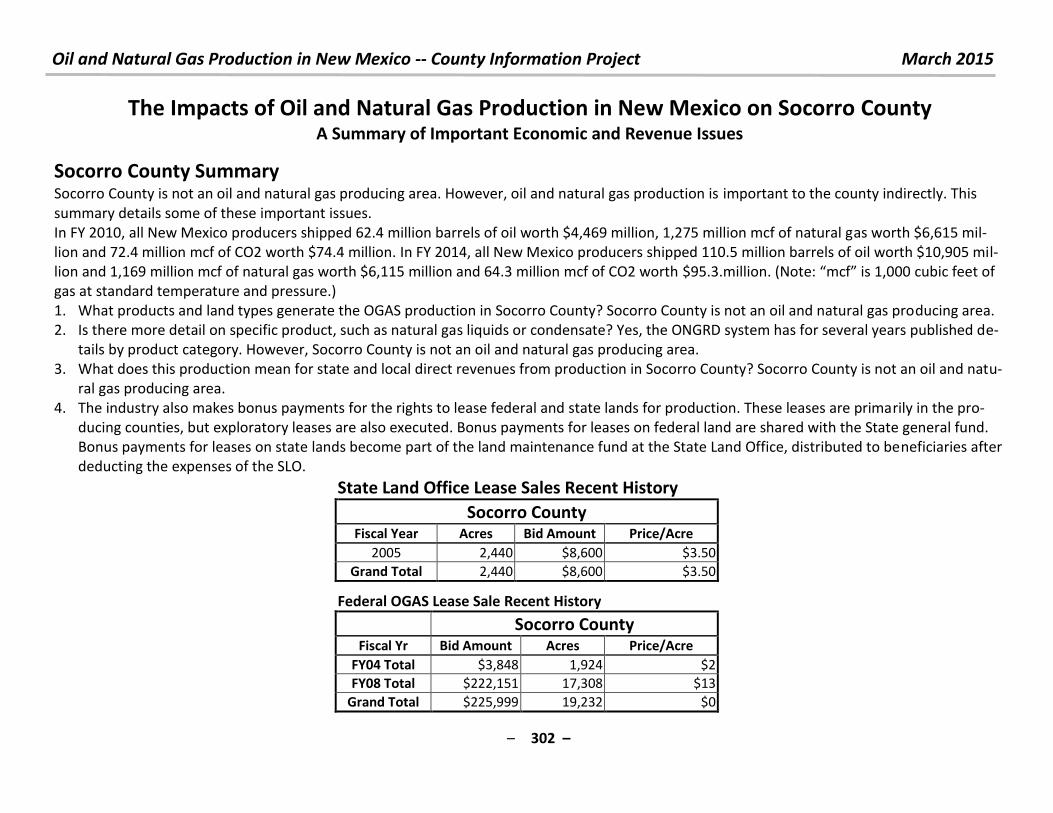

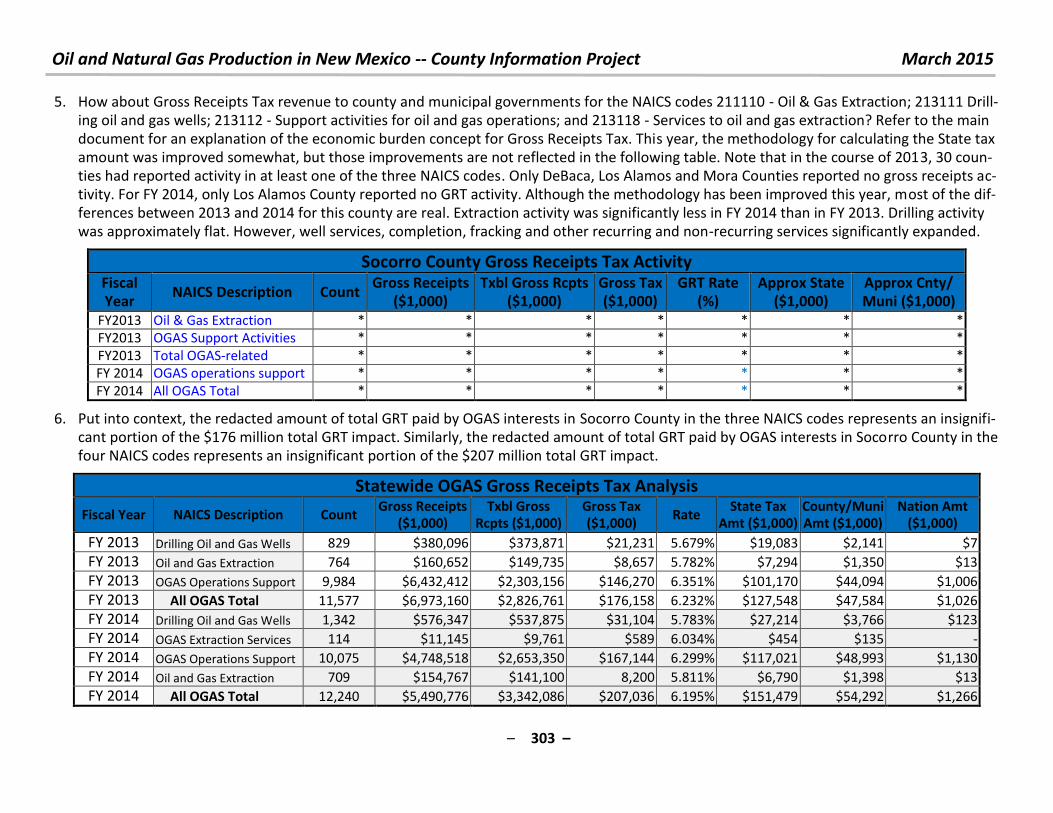

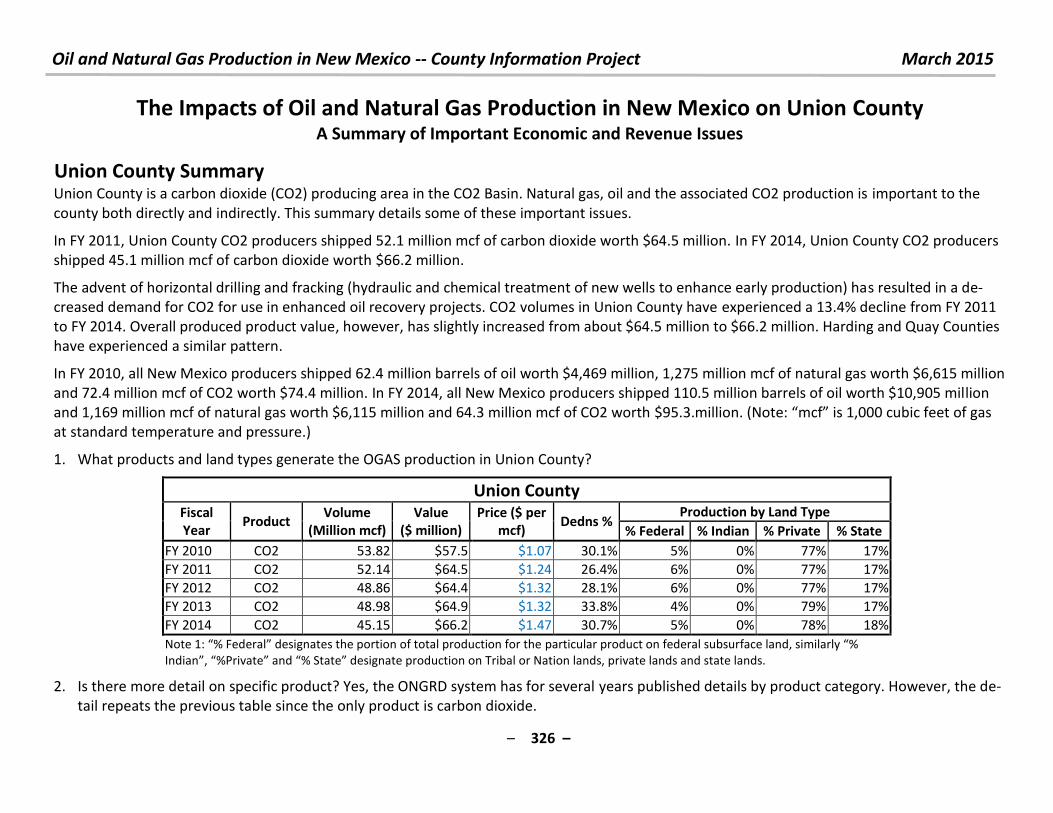

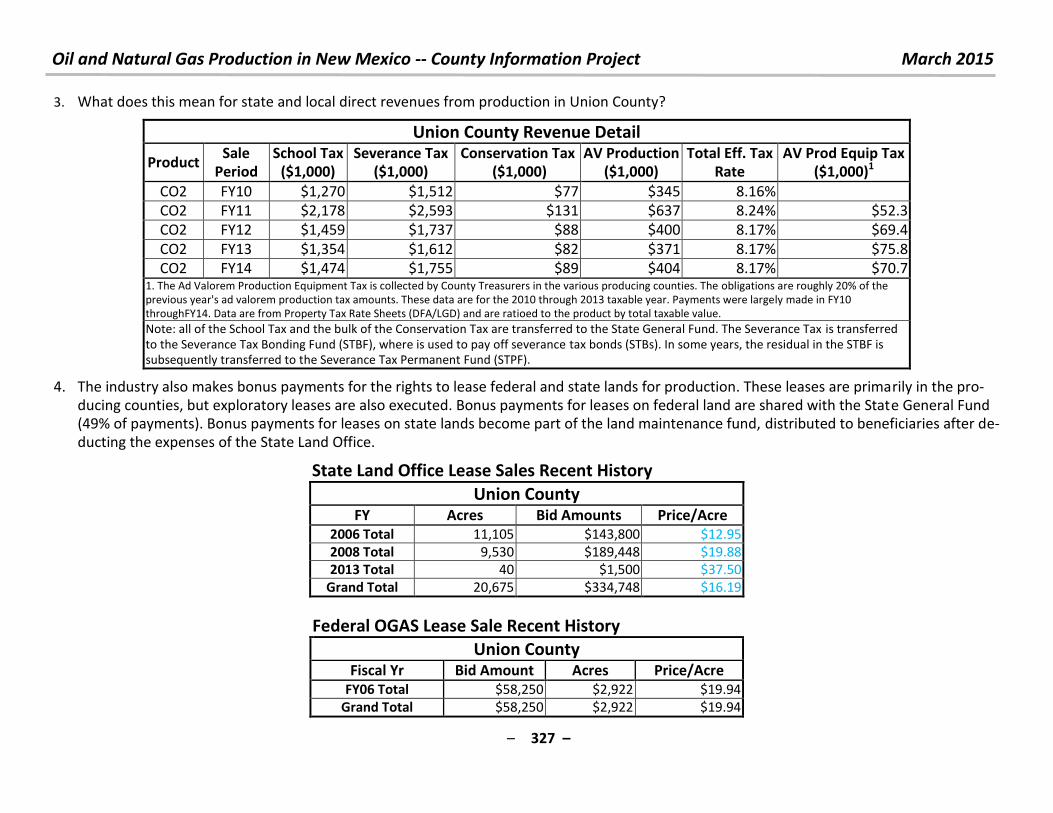

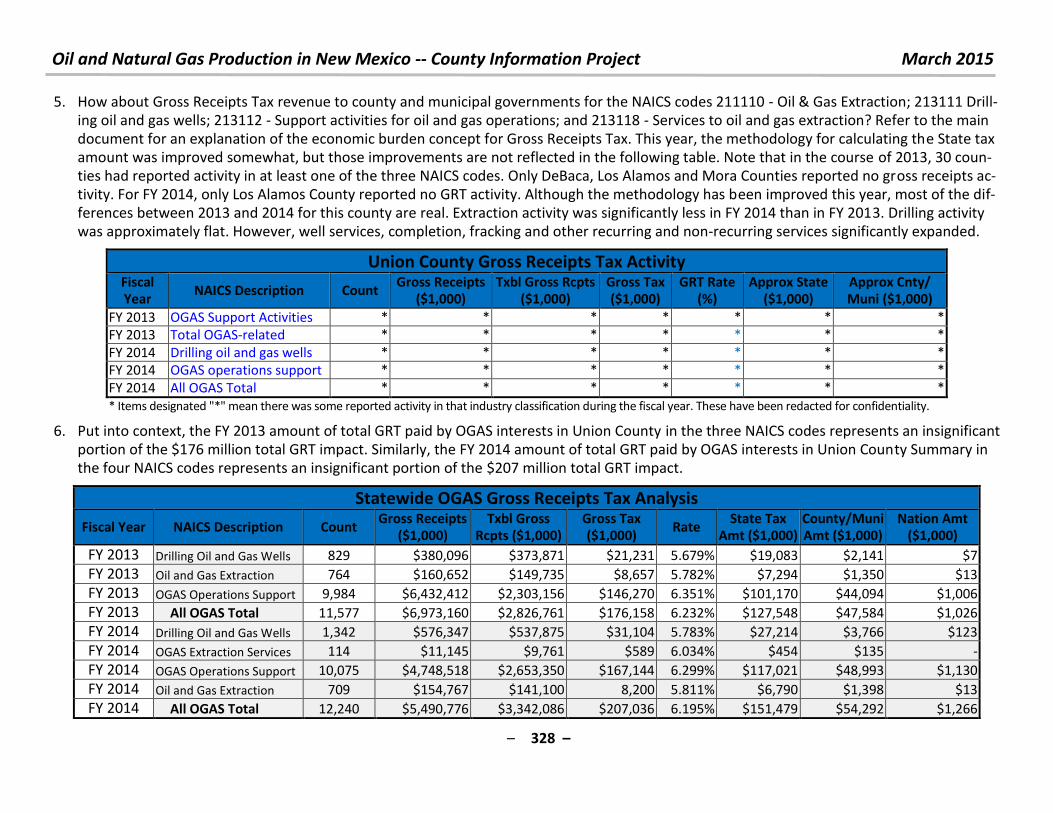

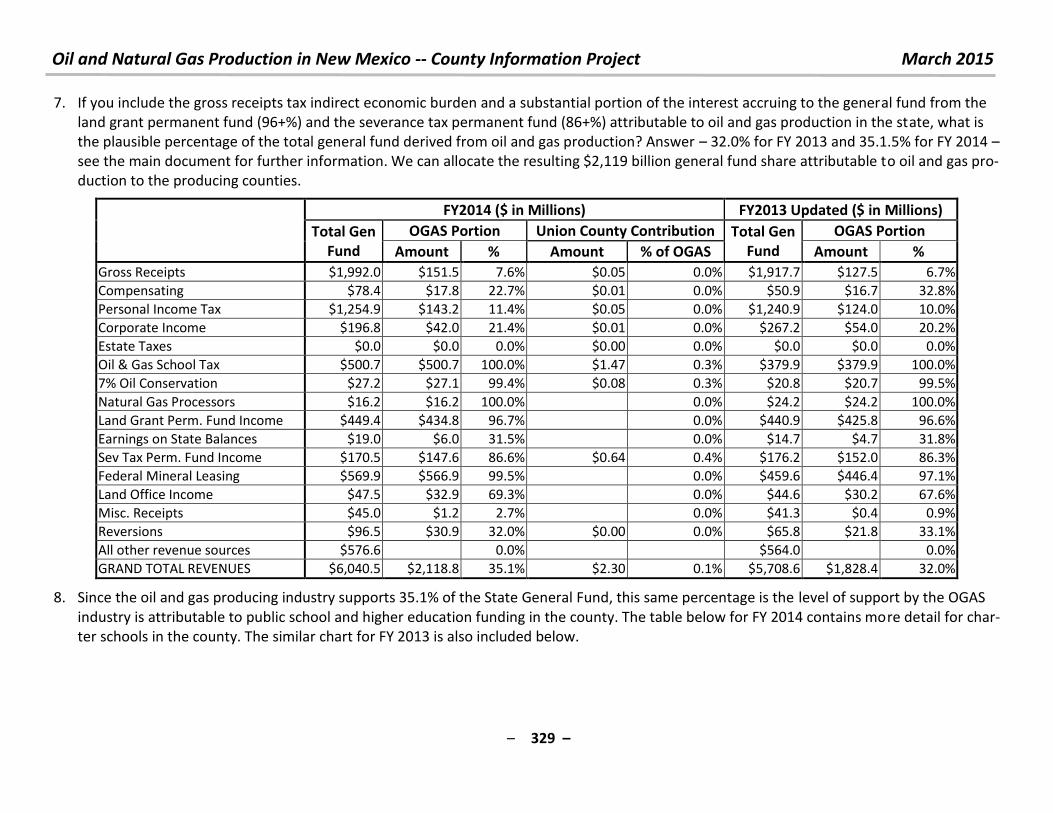

Embed Size (px)

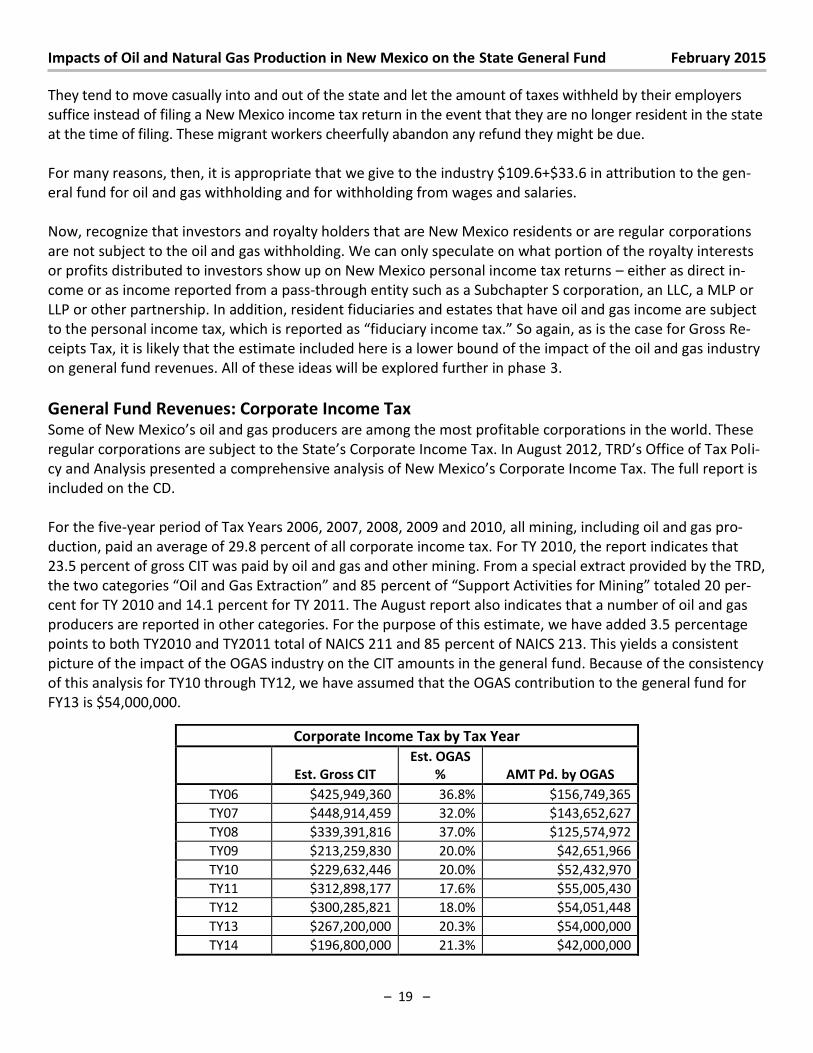

Citation preview

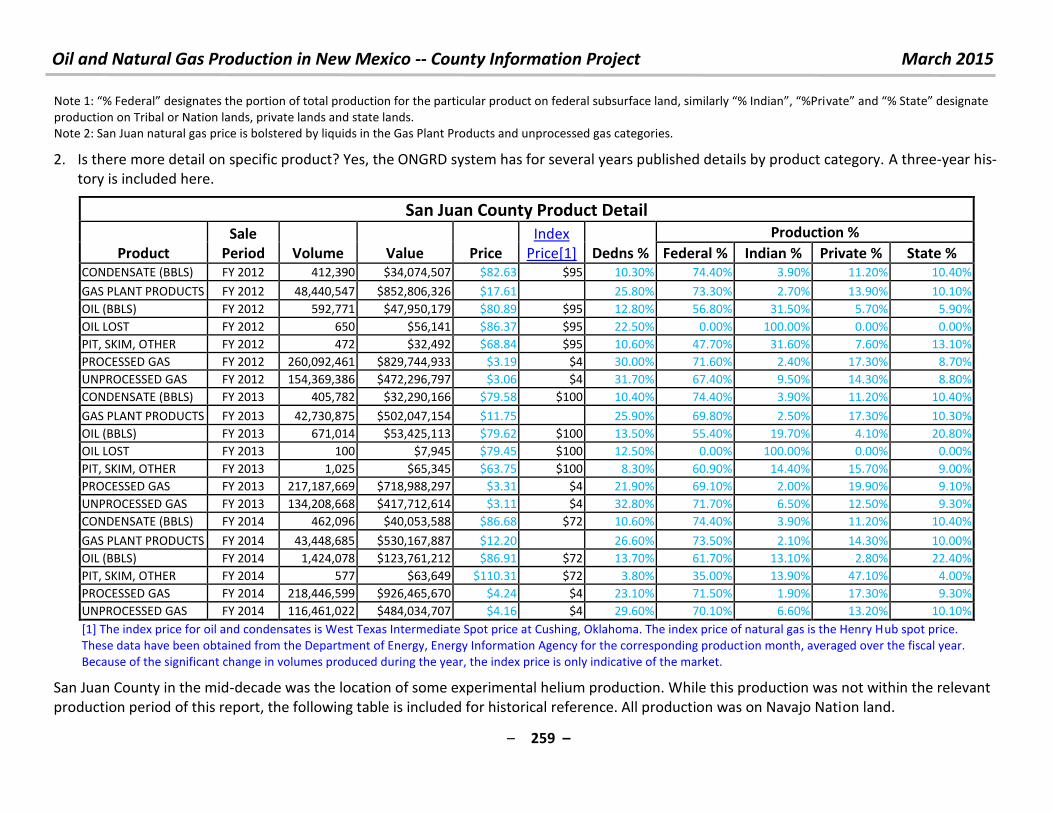

– 1 –

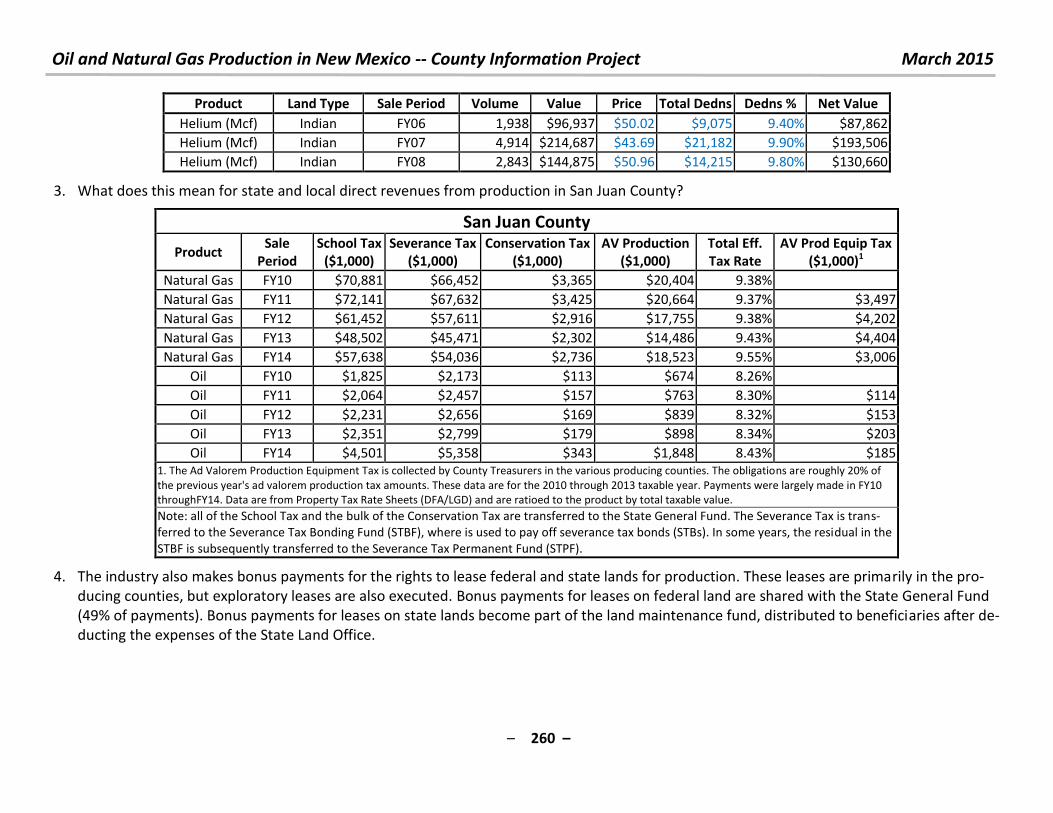

The Fiscal Im-

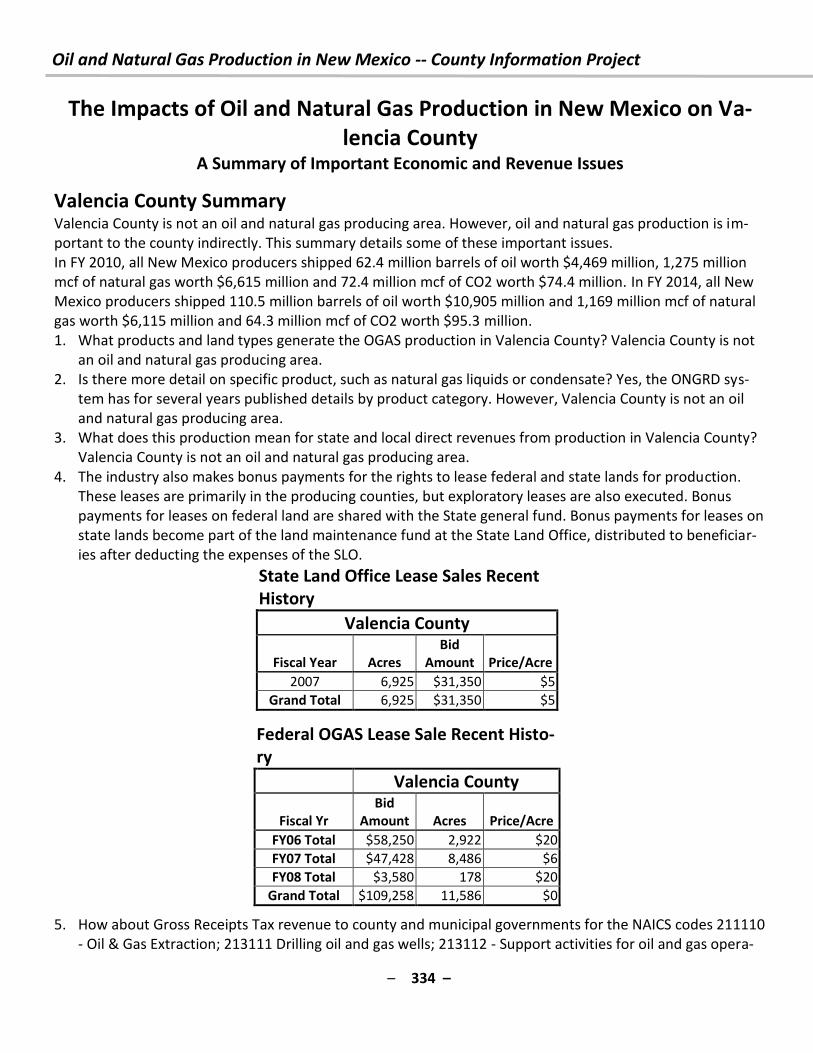

pacts of Oil and

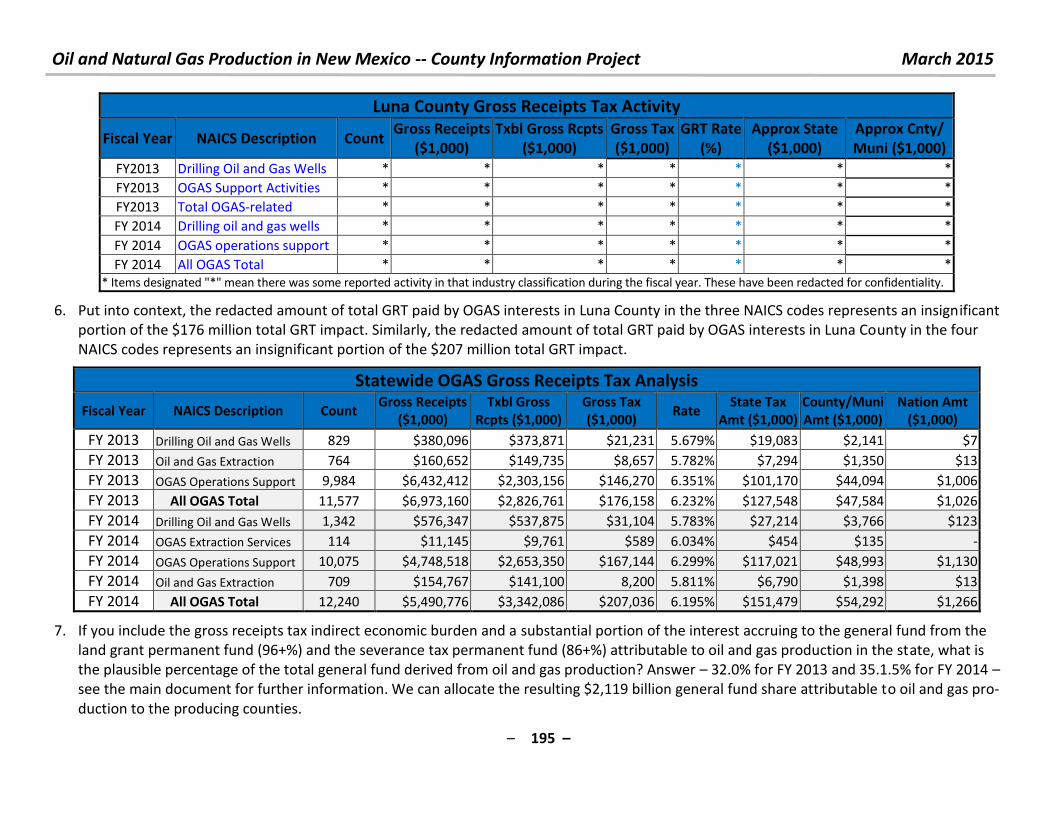

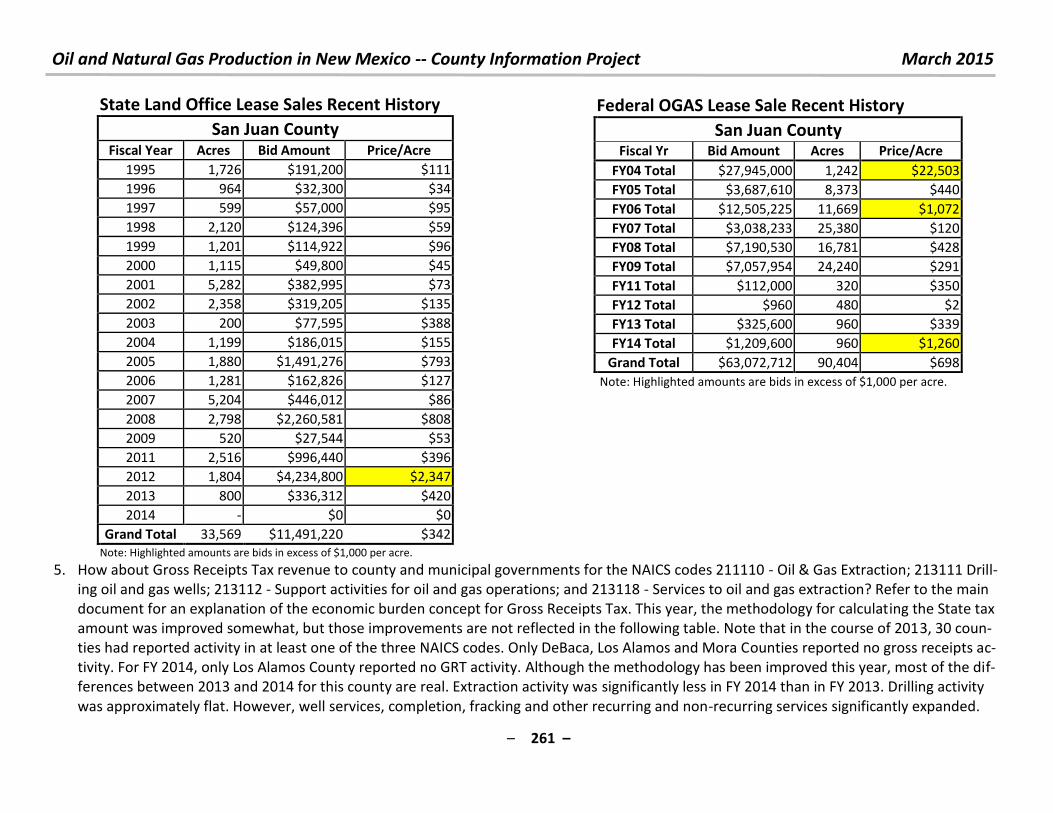

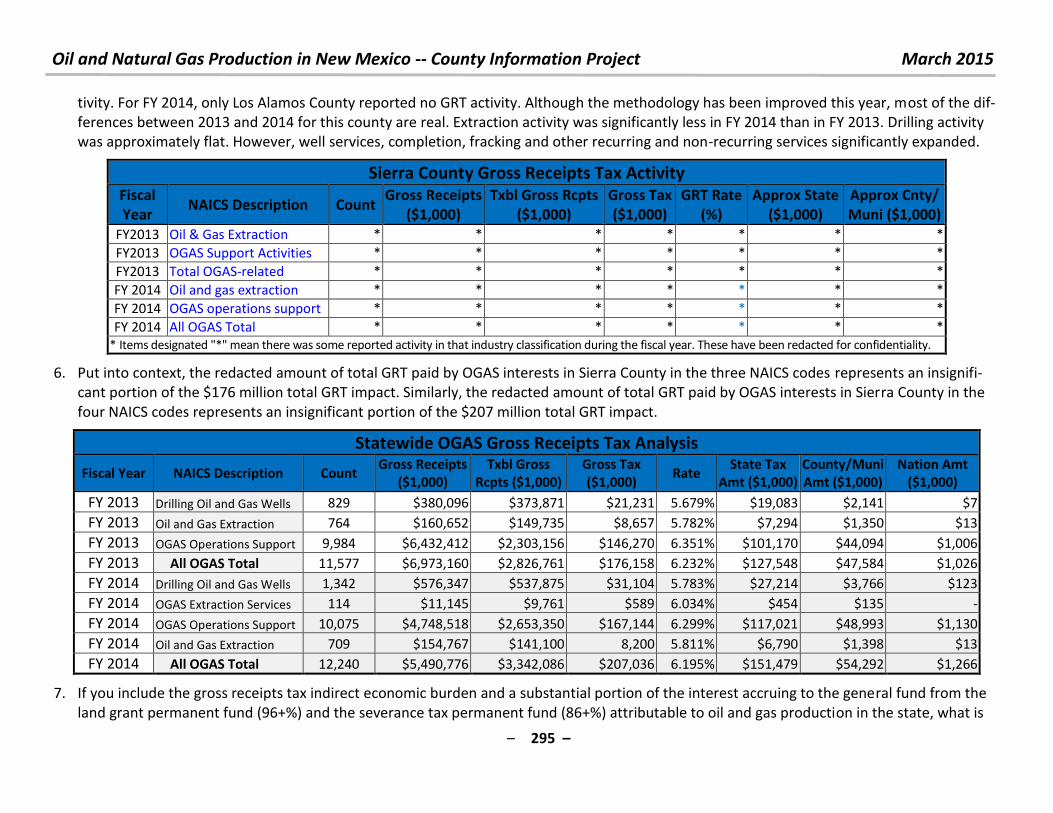

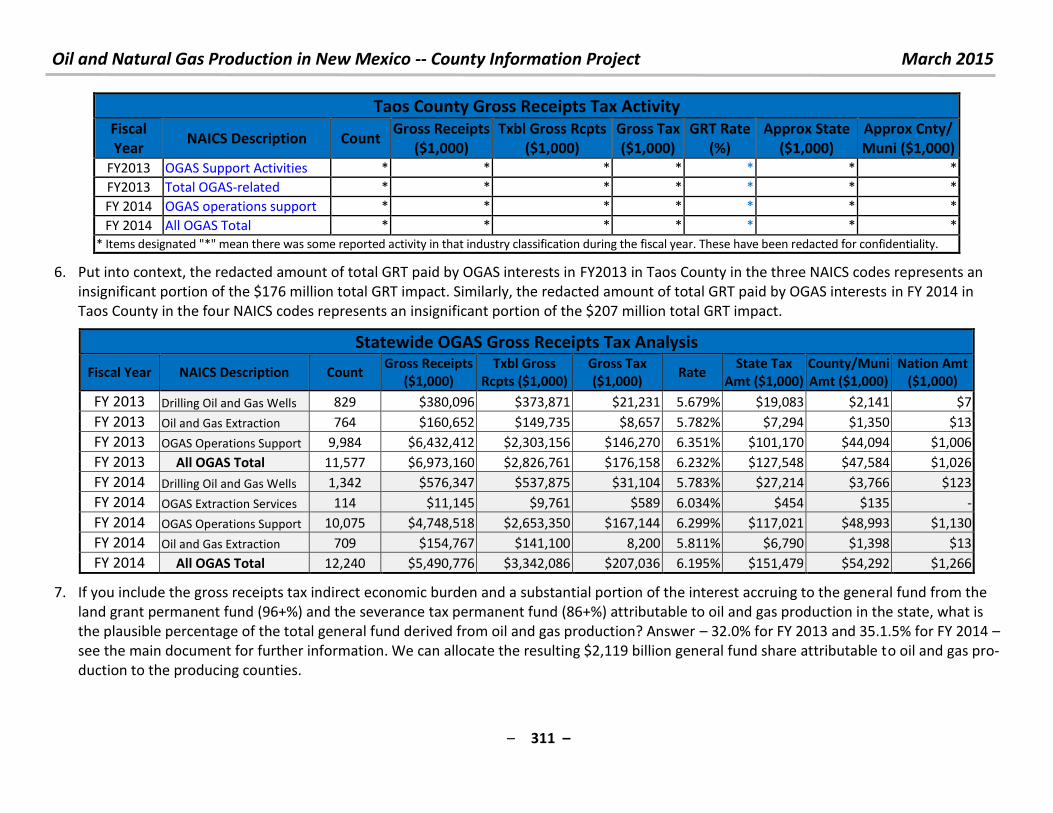

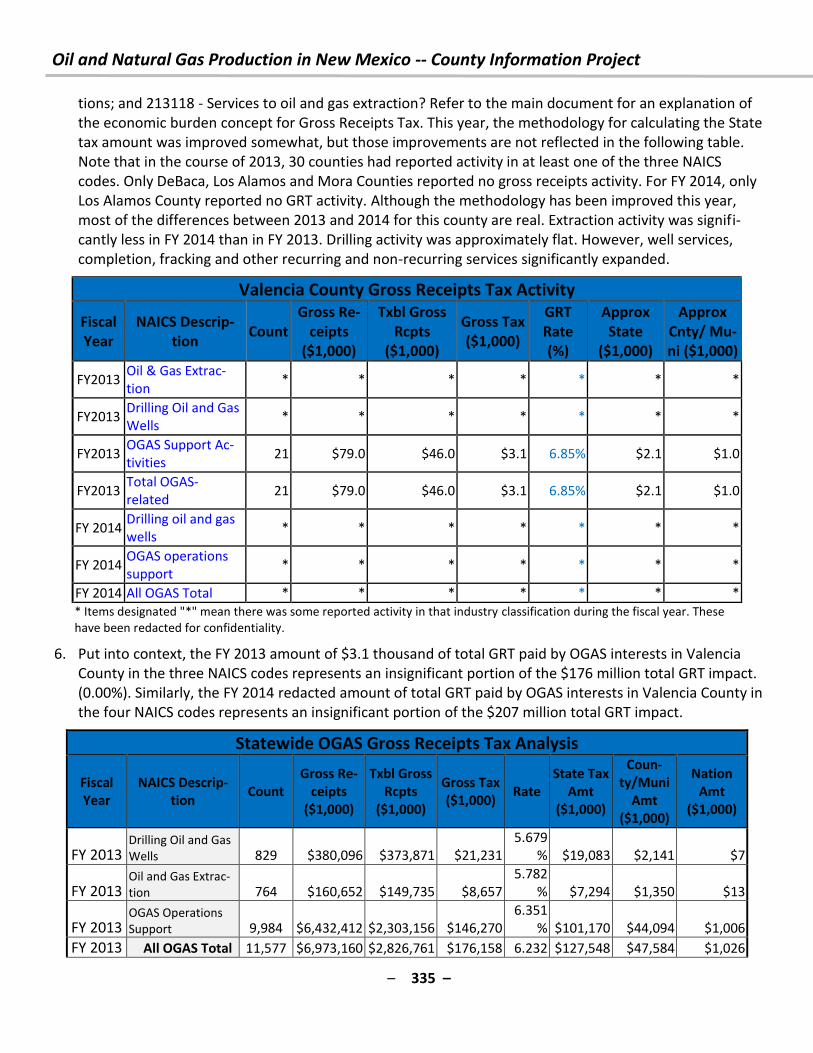

Gas Production in

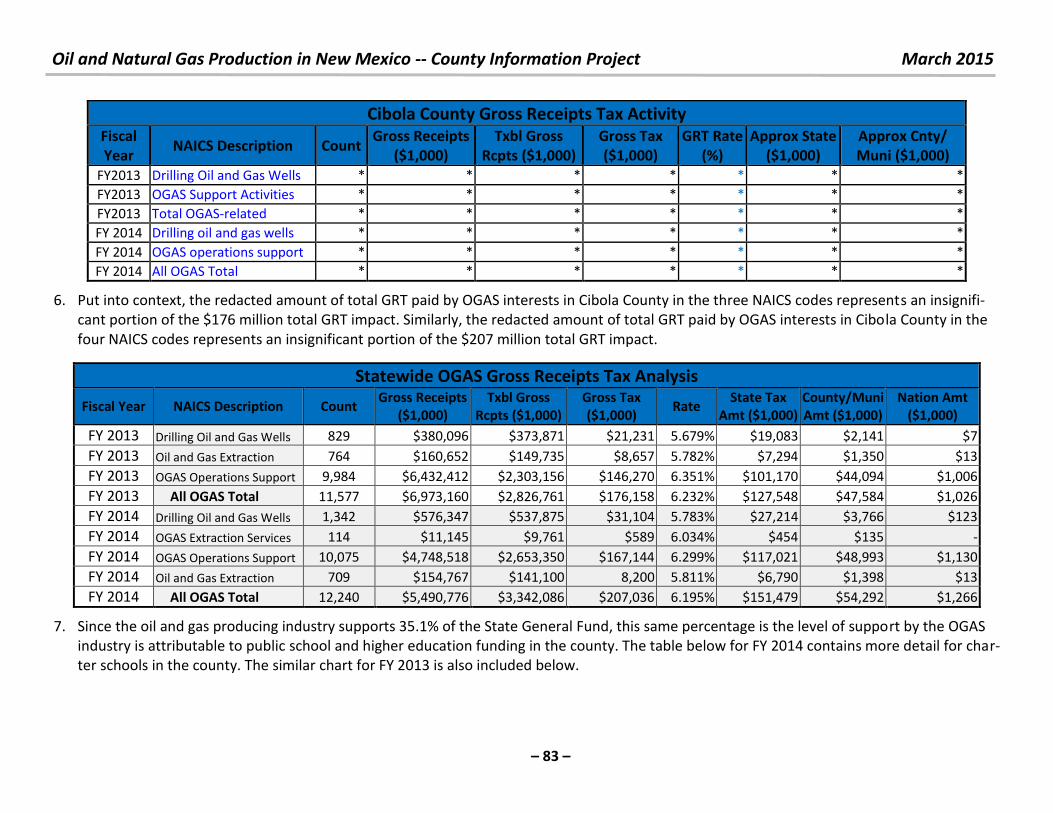

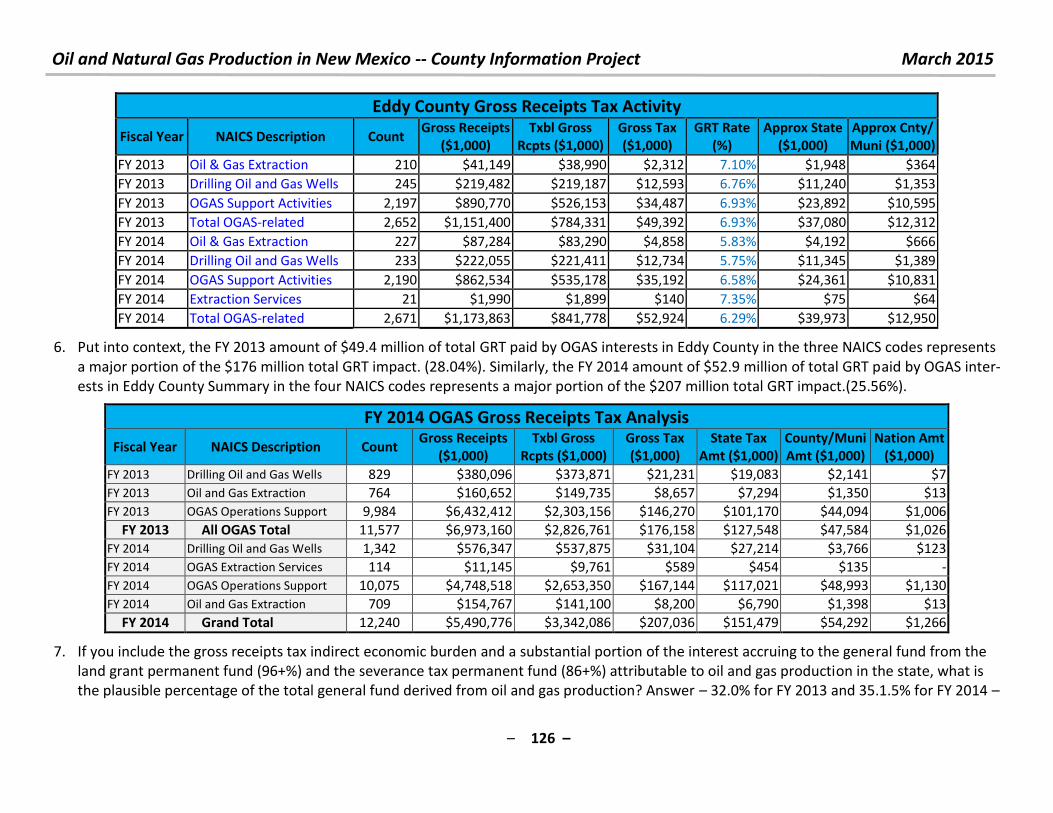

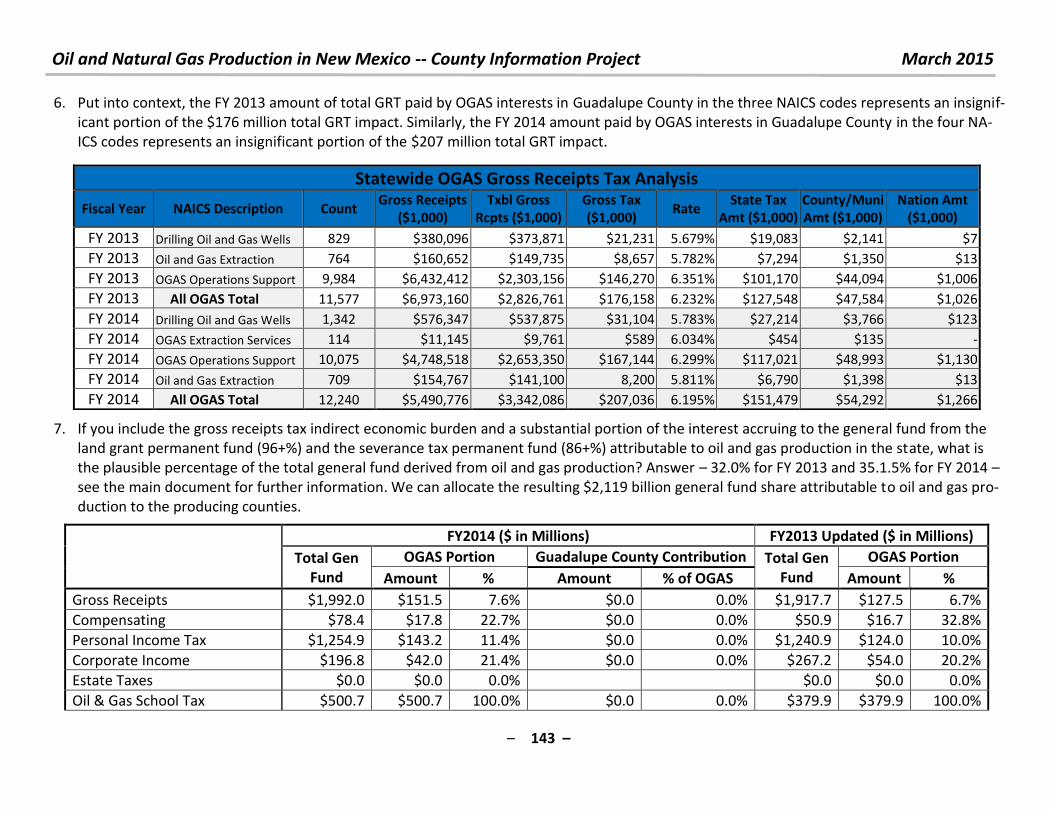

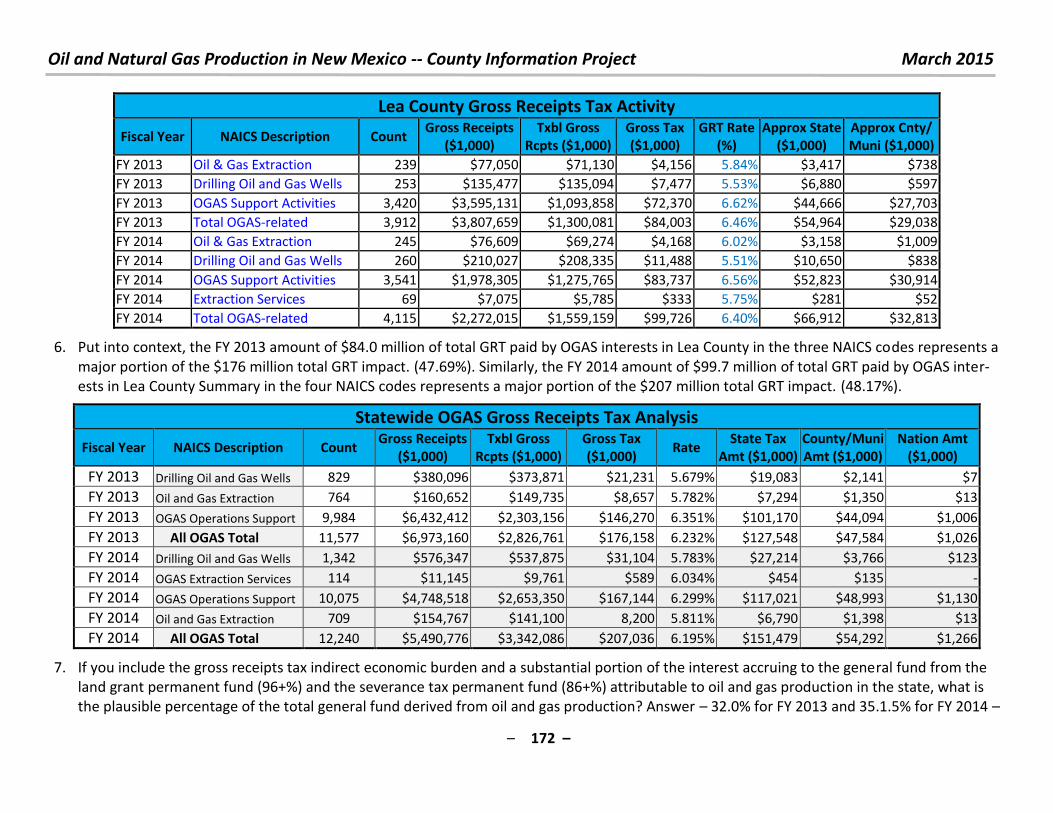

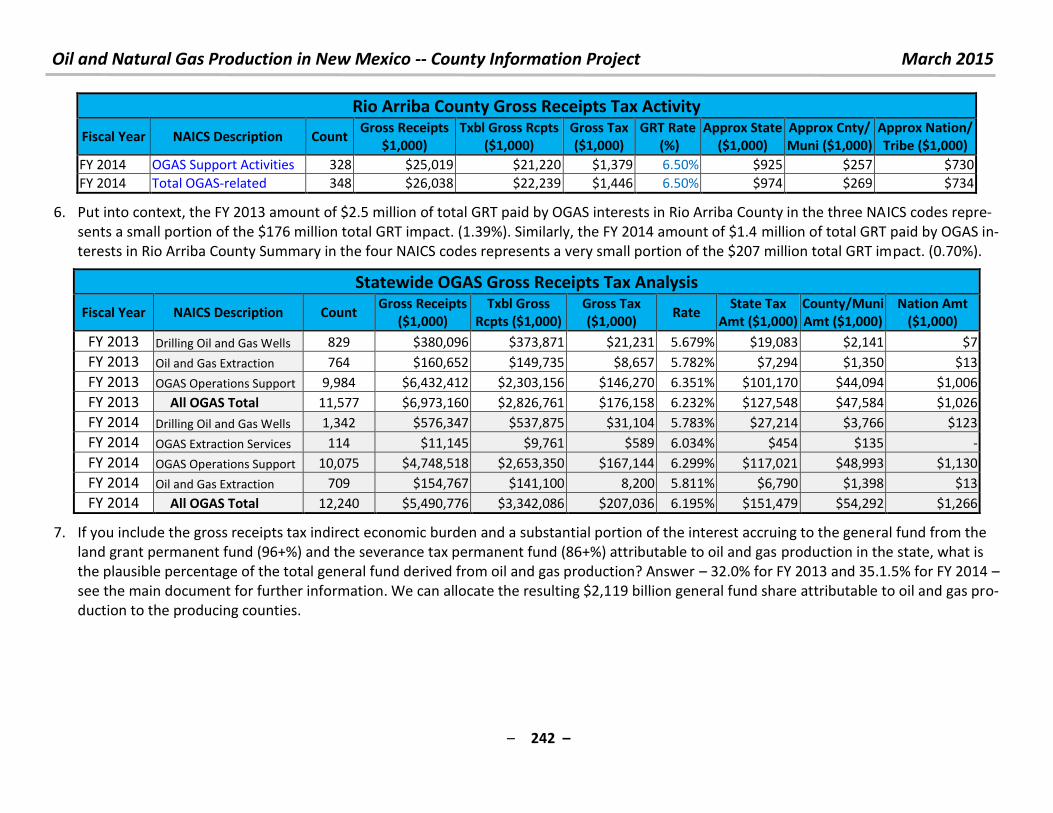

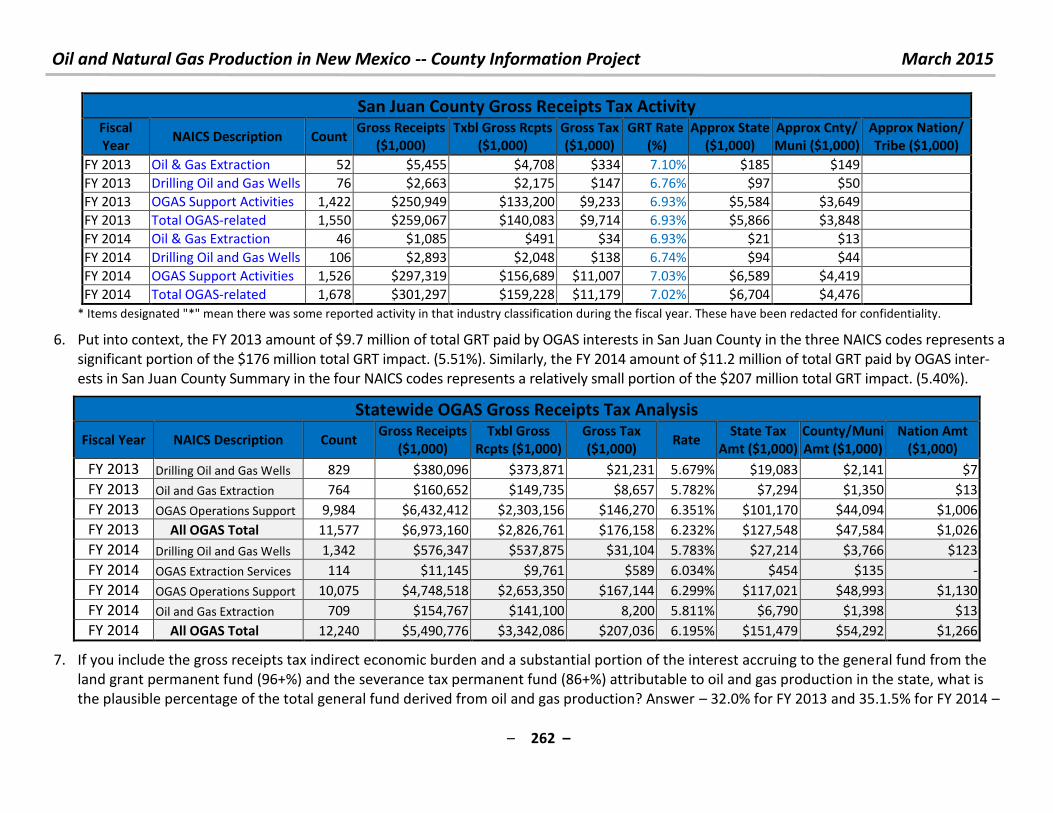

New Mexico

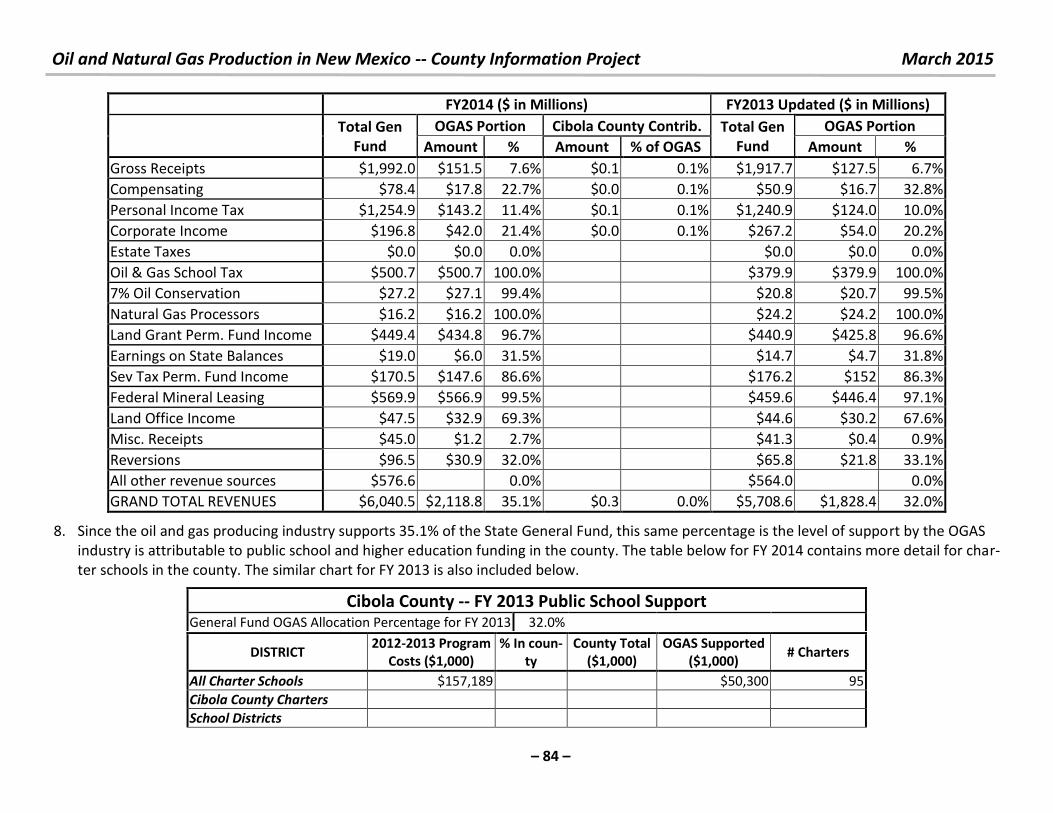

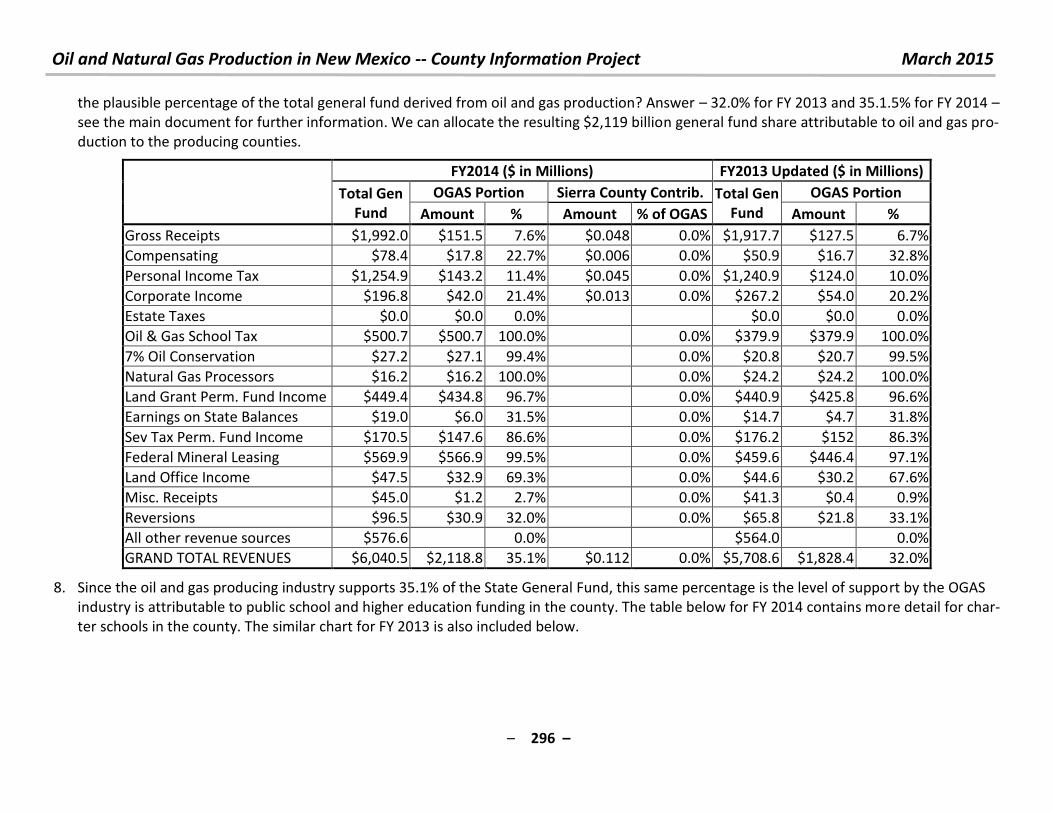

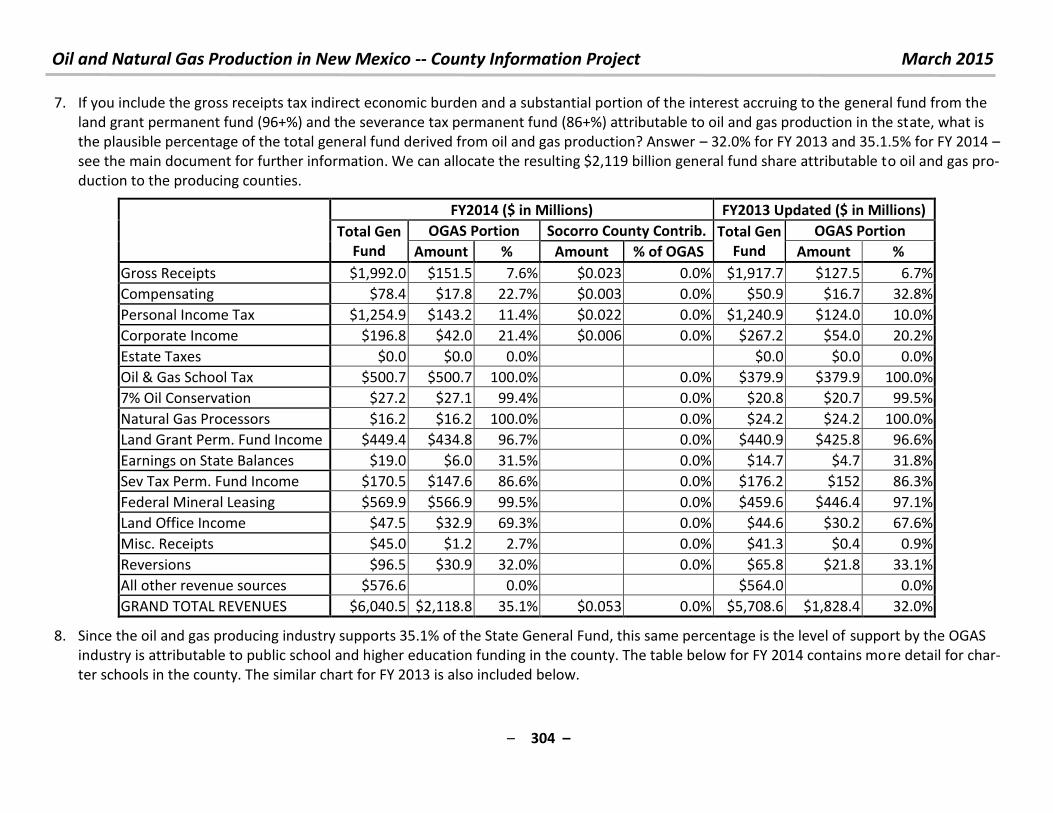

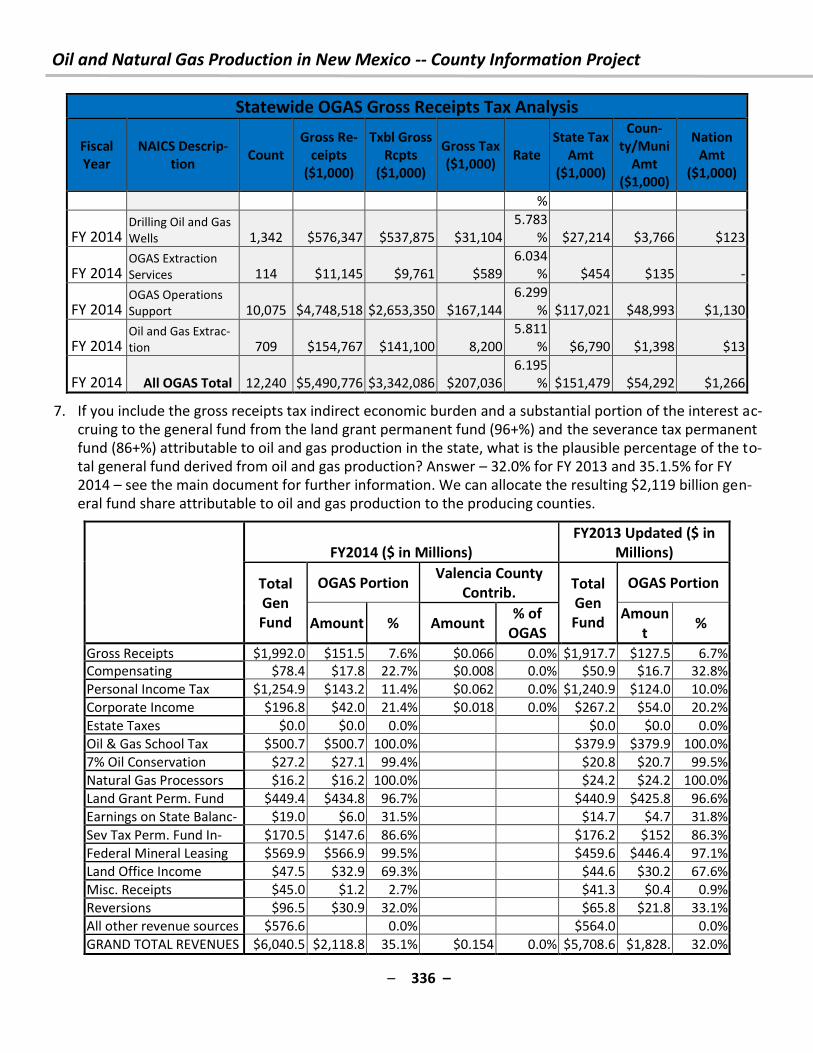

2014 Fiscal Year End

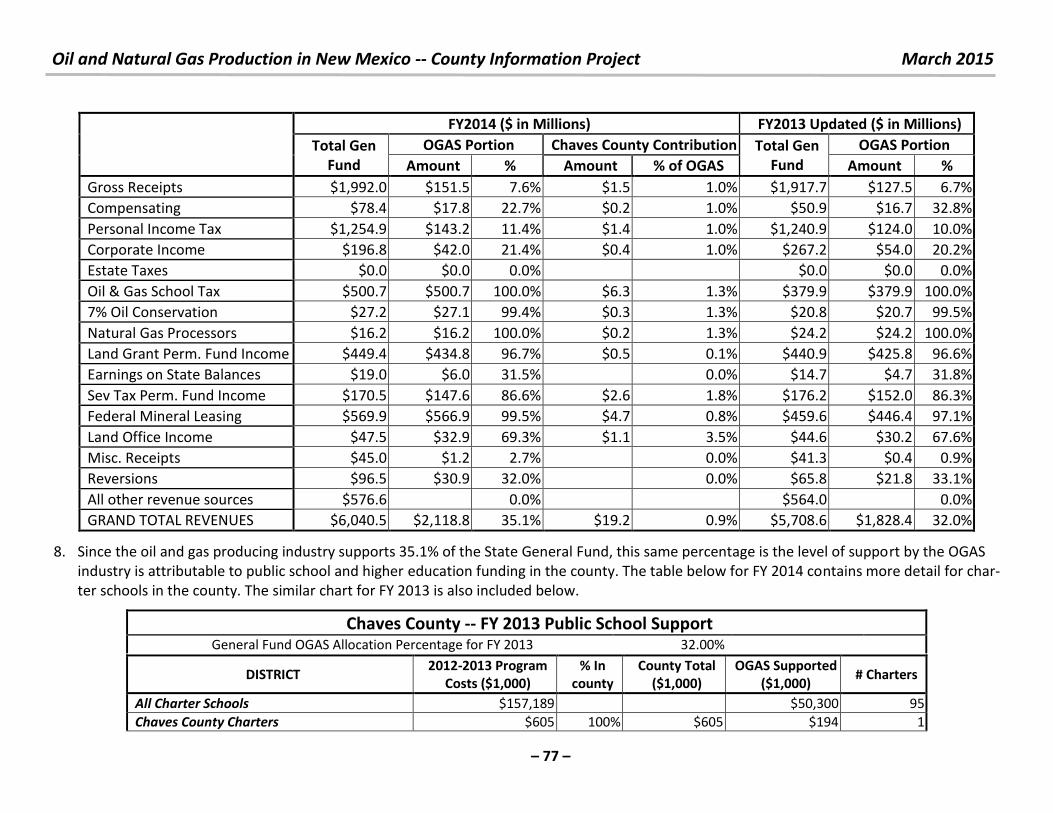

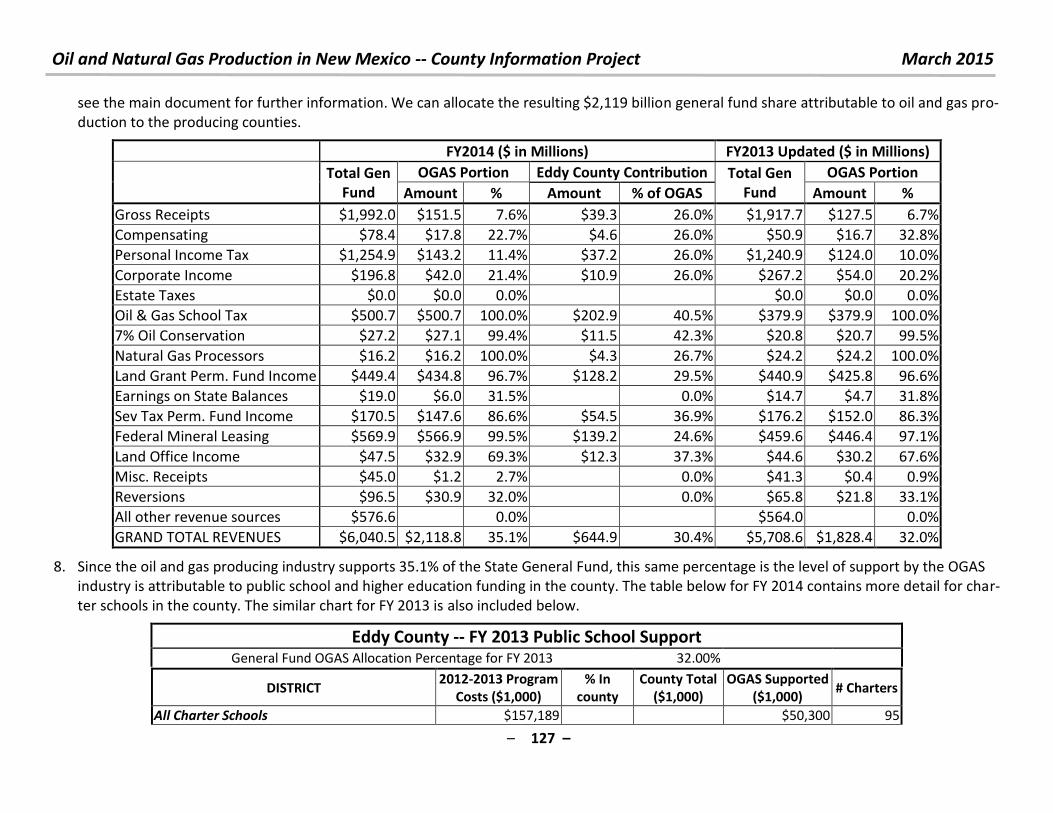

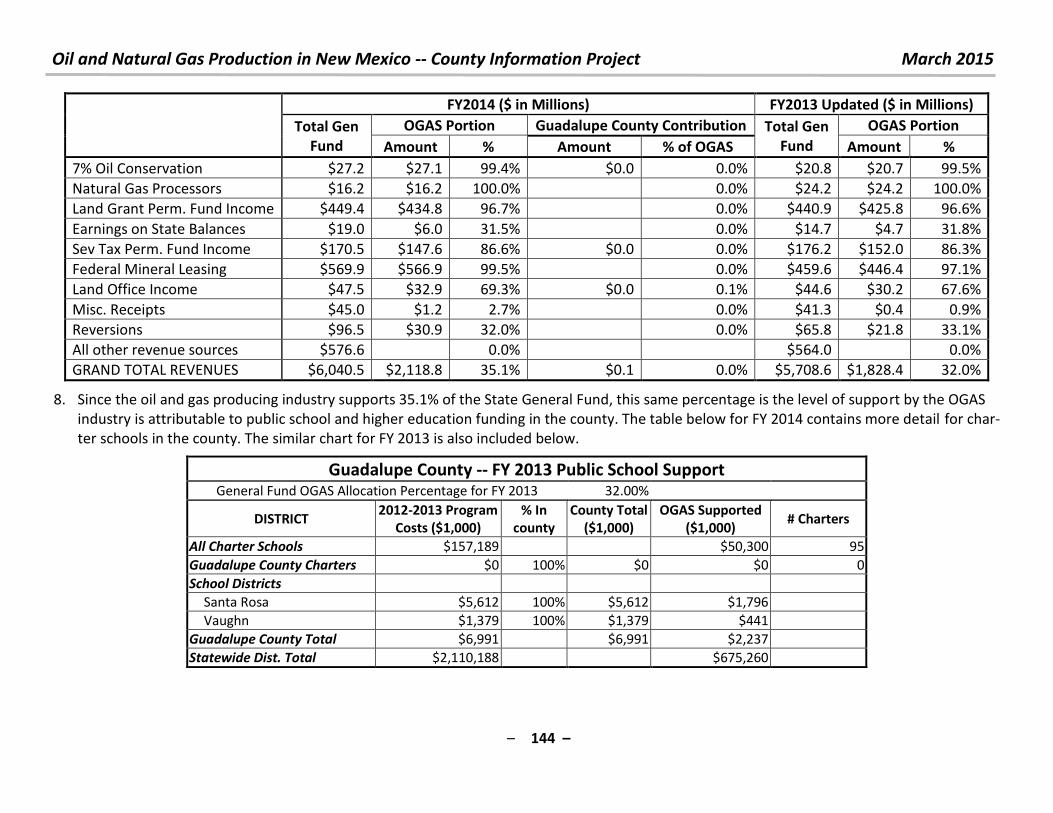

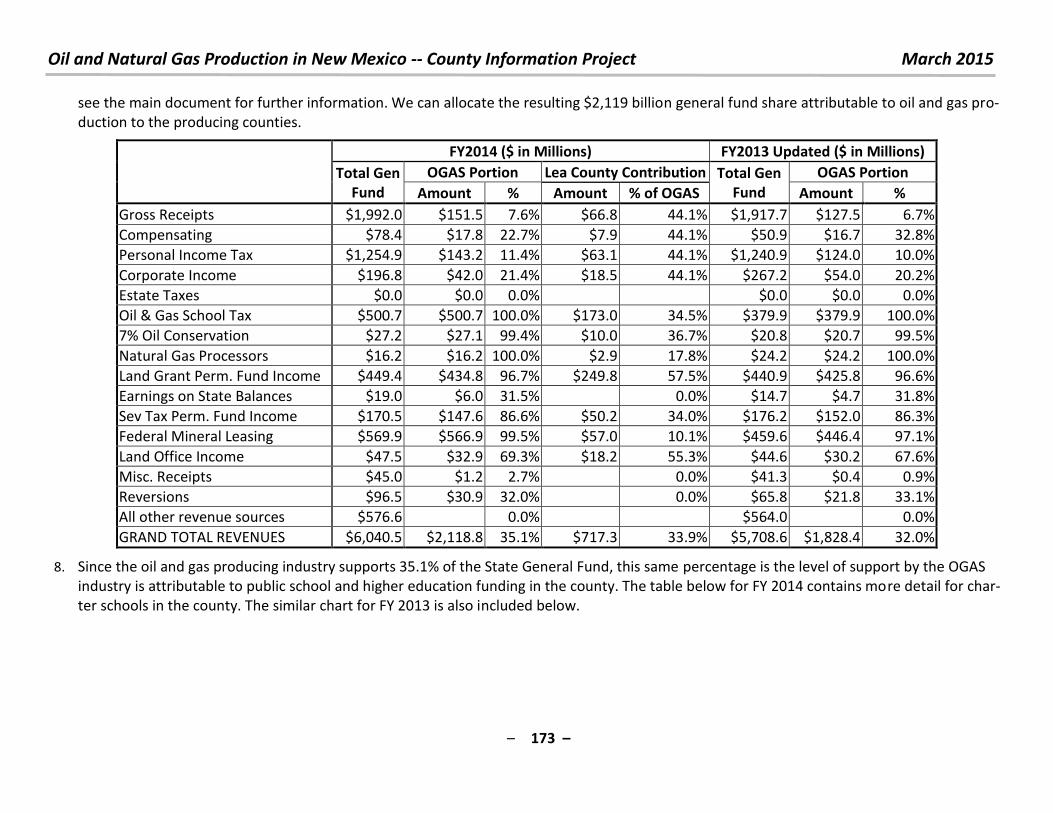

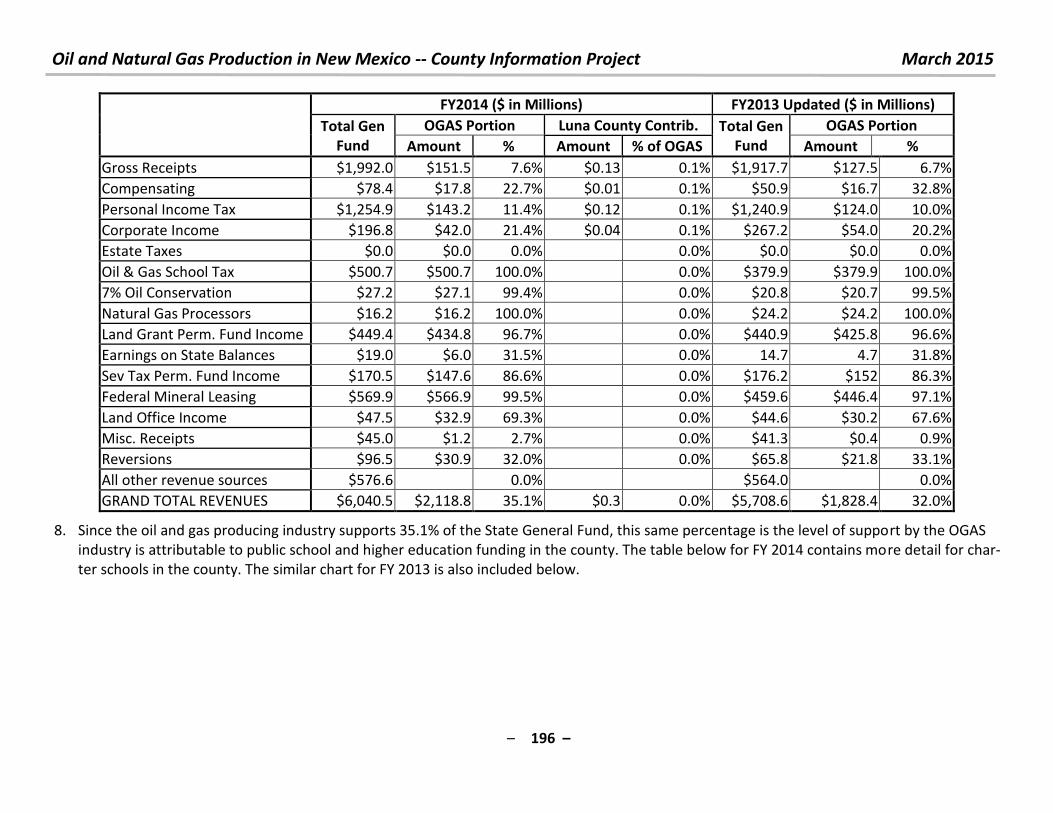

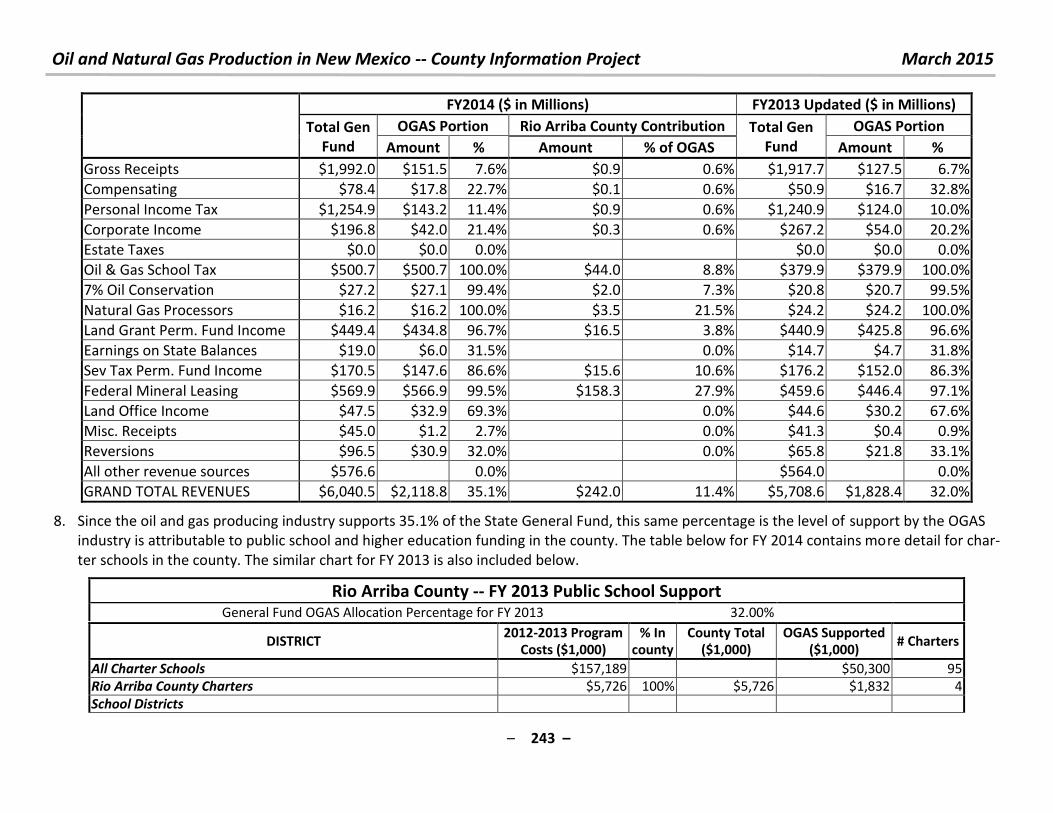

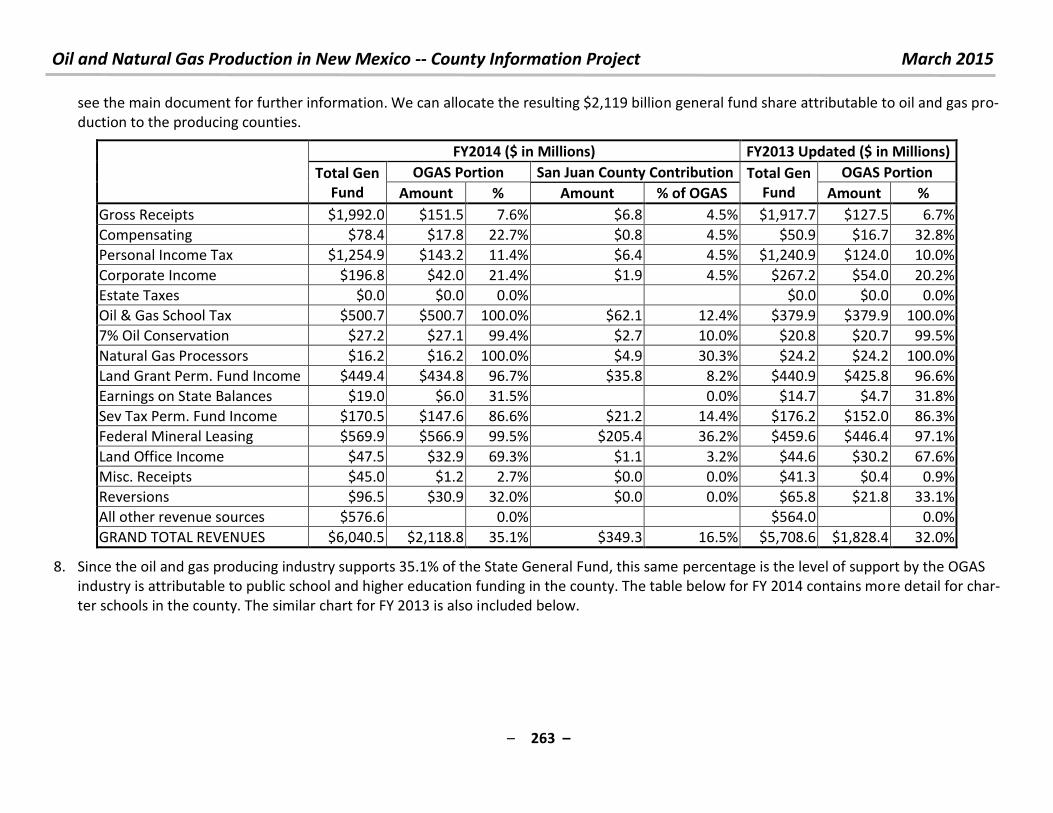

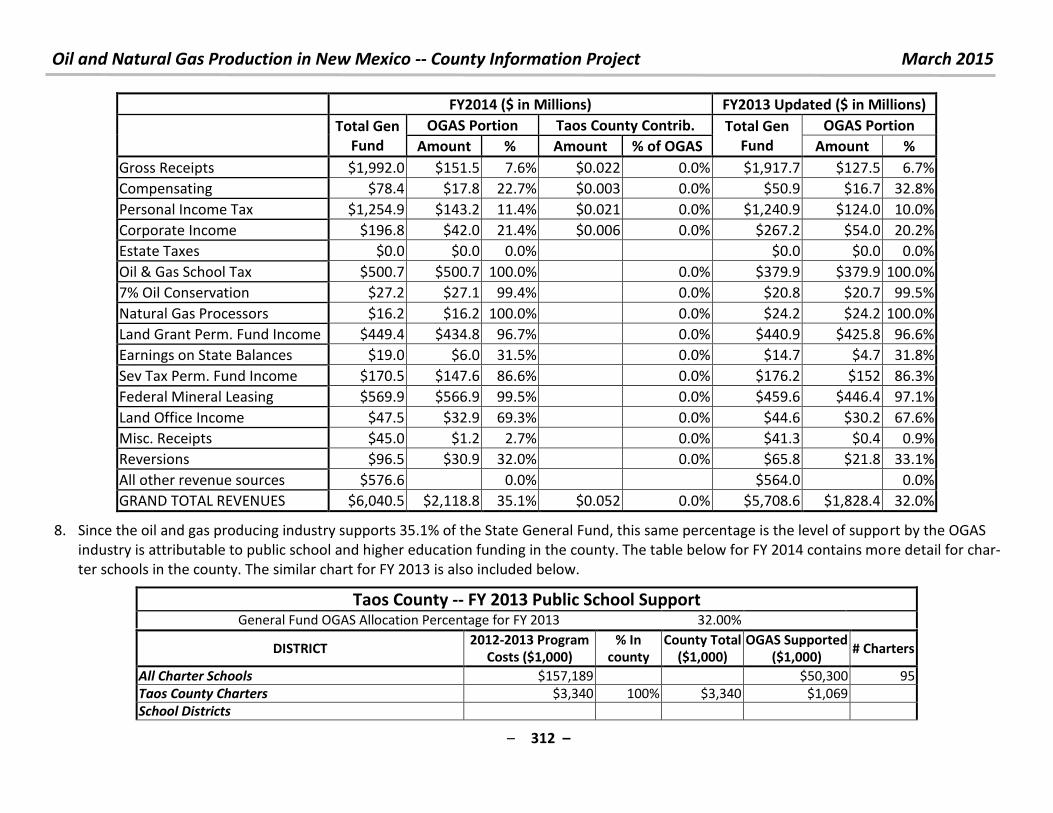

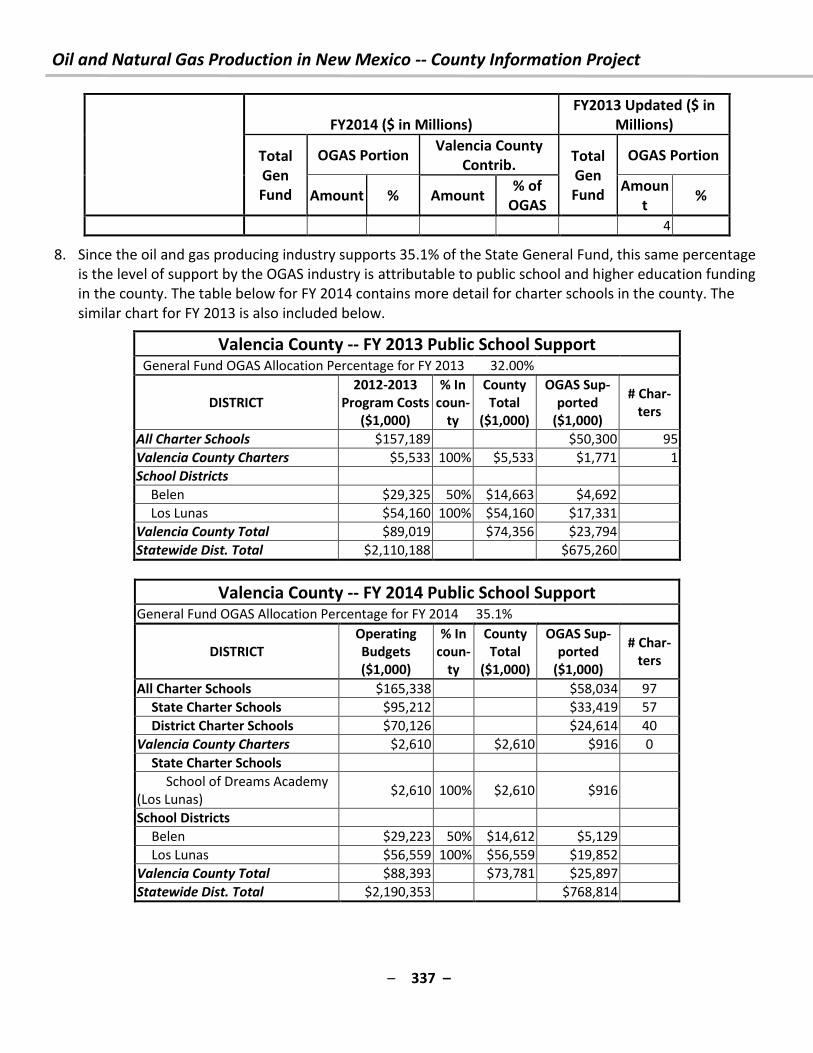

New Mexico Tax Research Institute © 2015 all

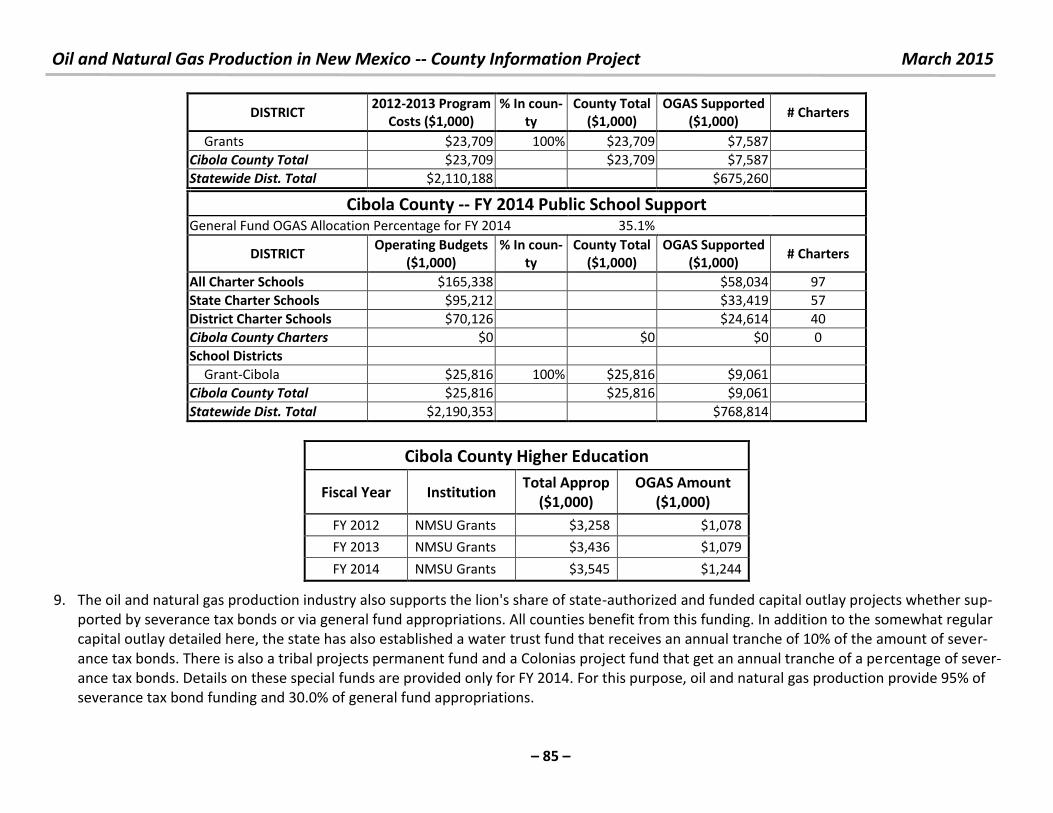

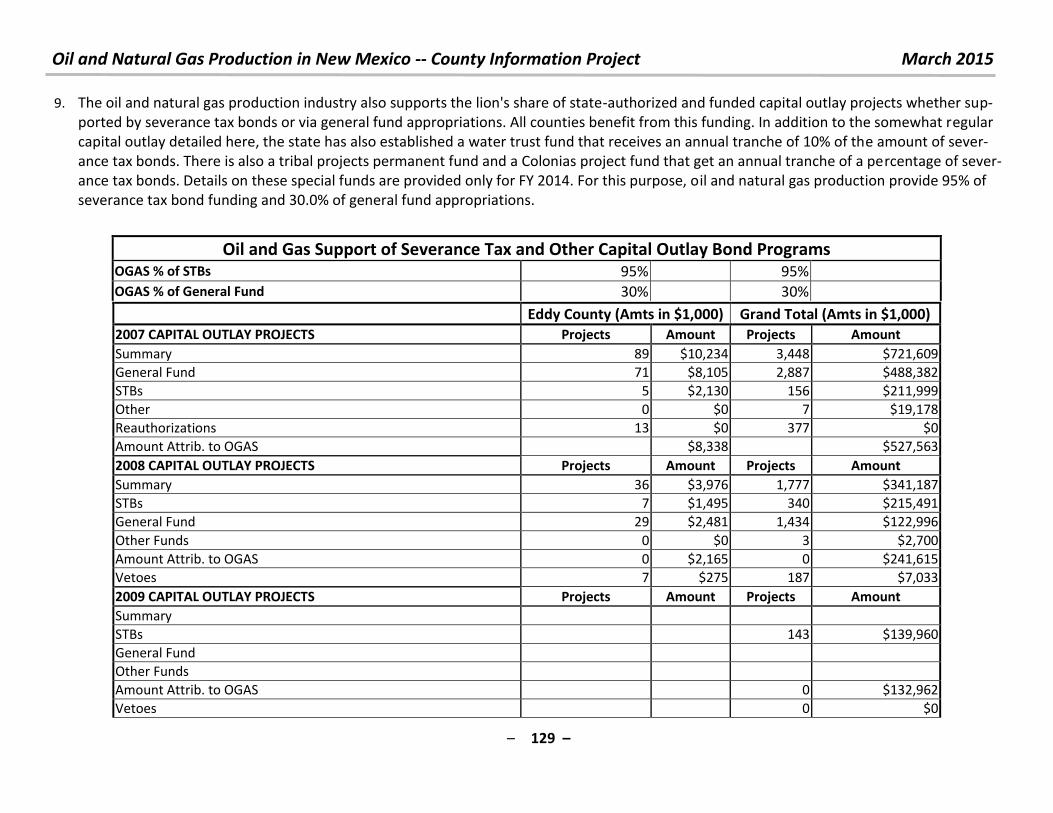

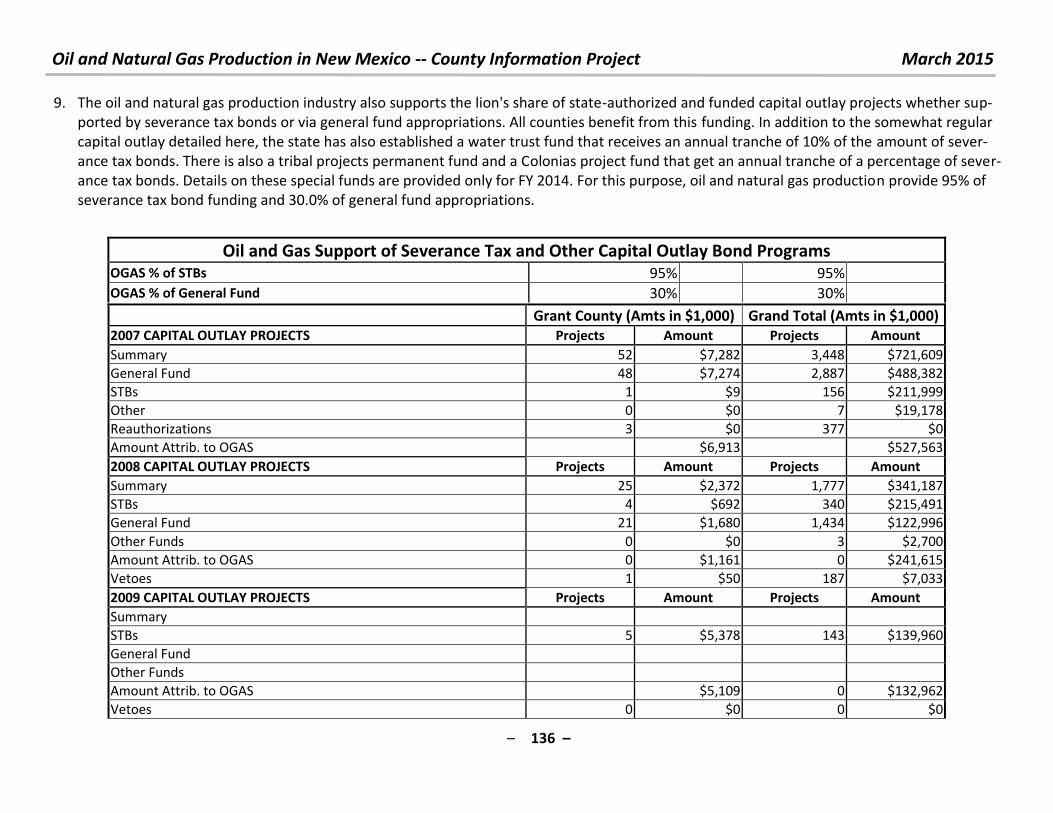

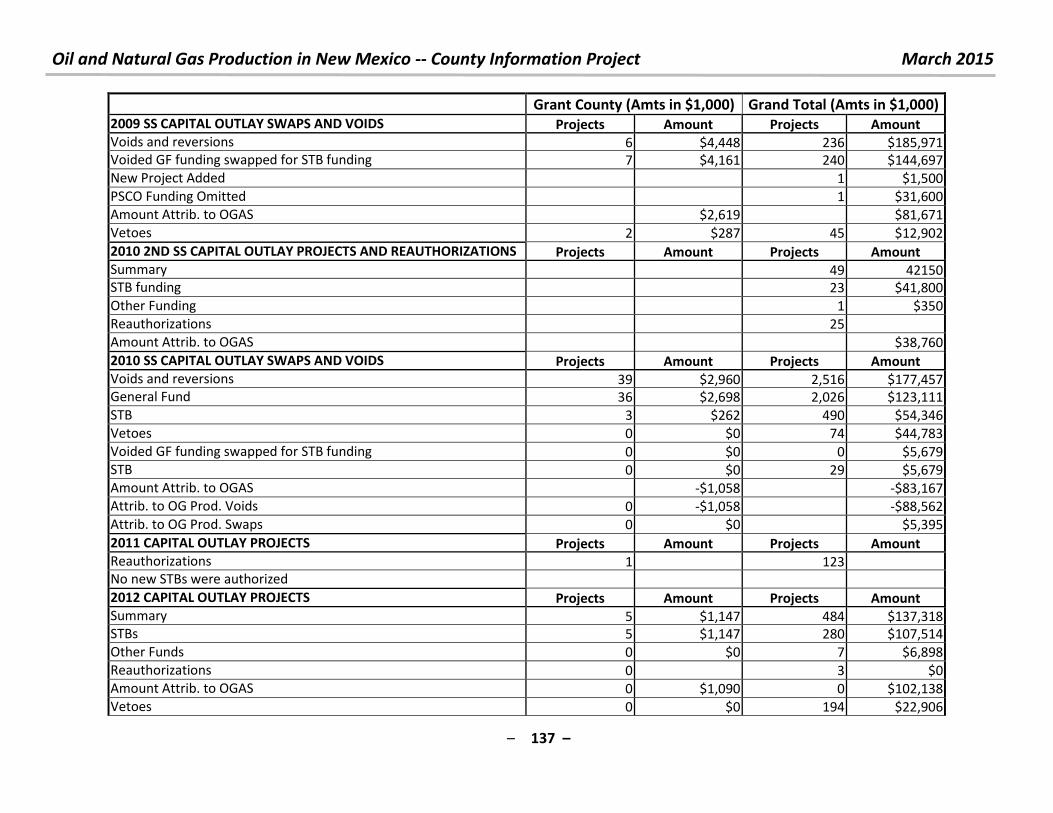

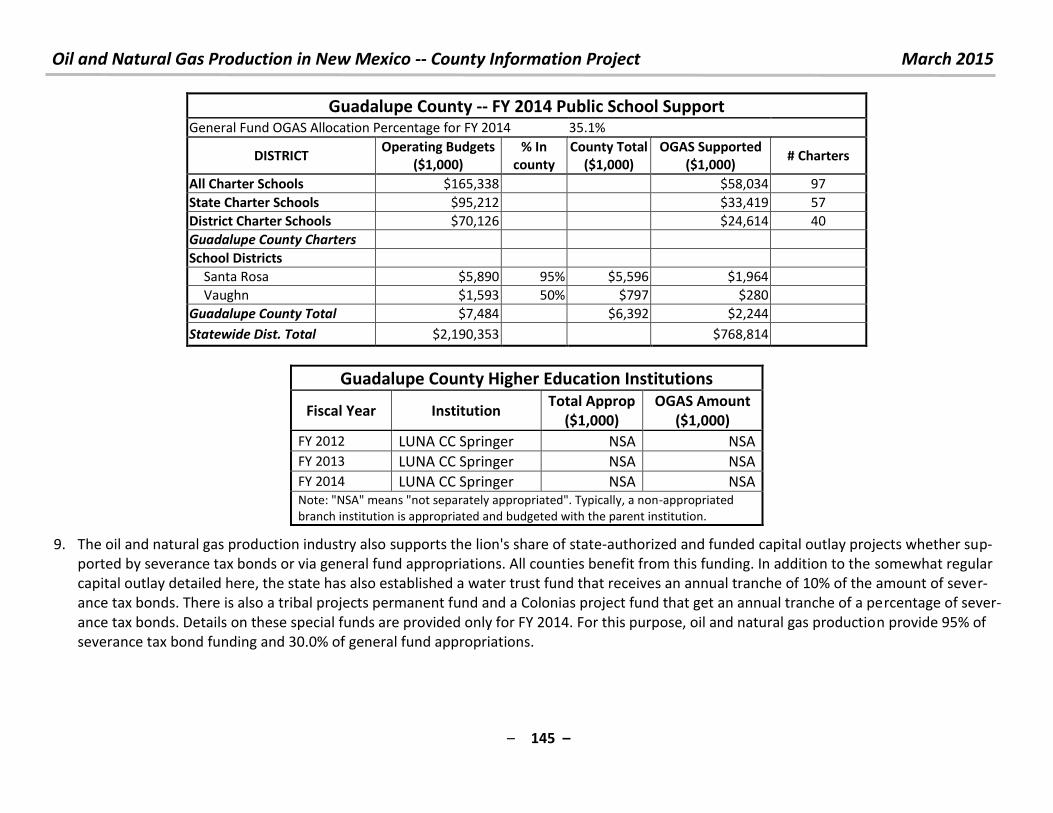

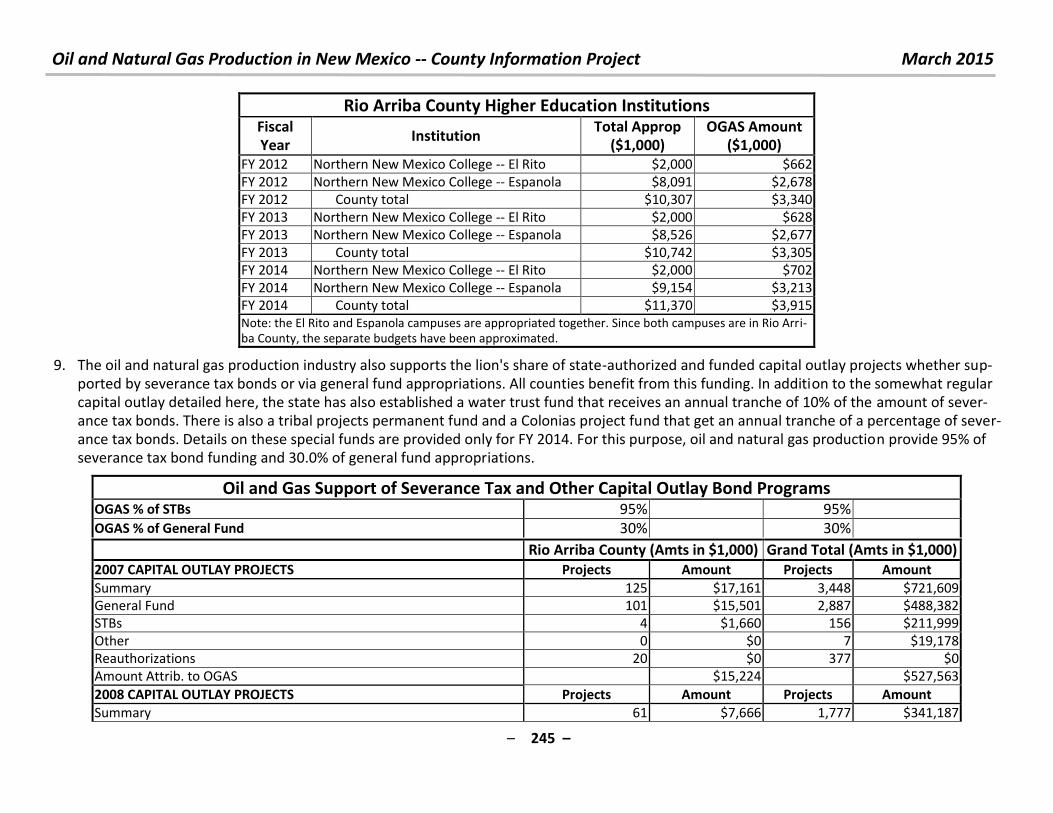

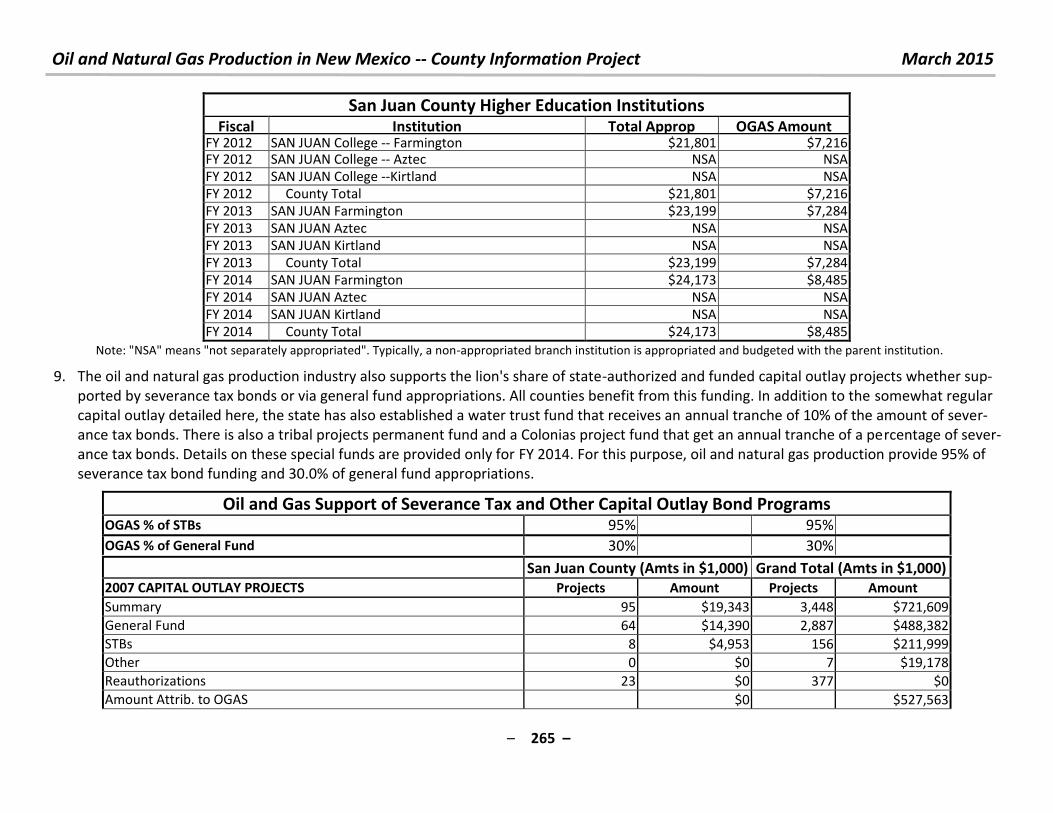

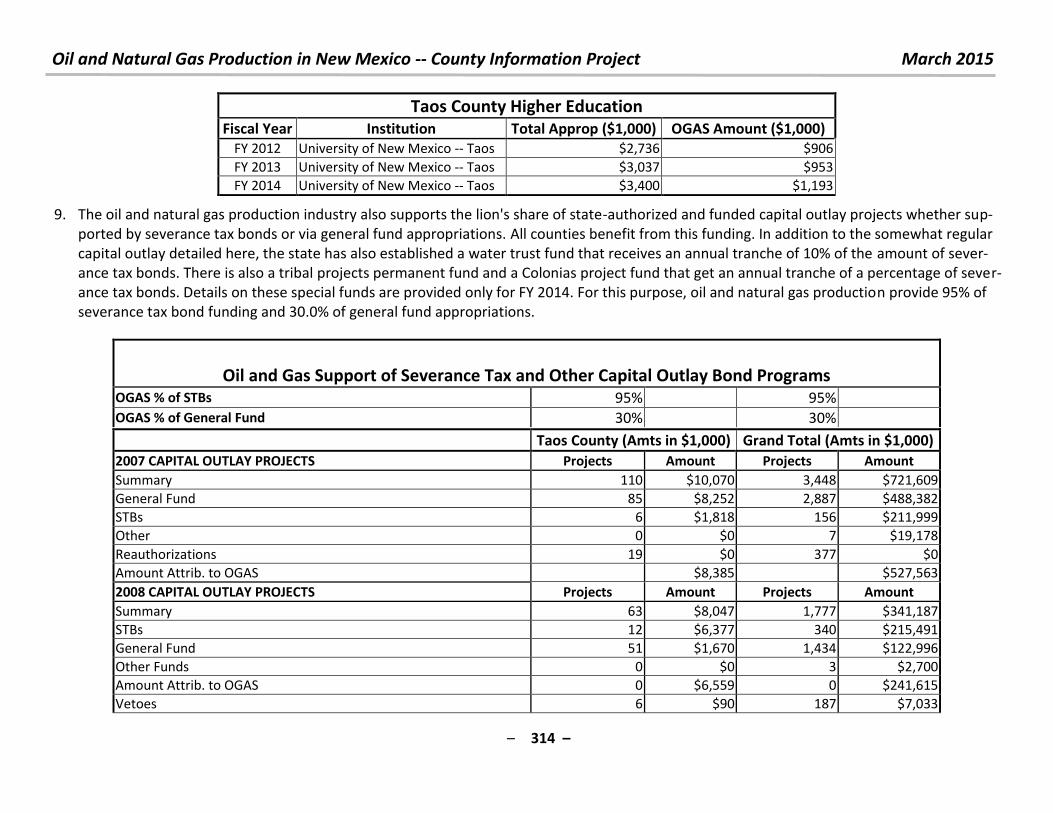

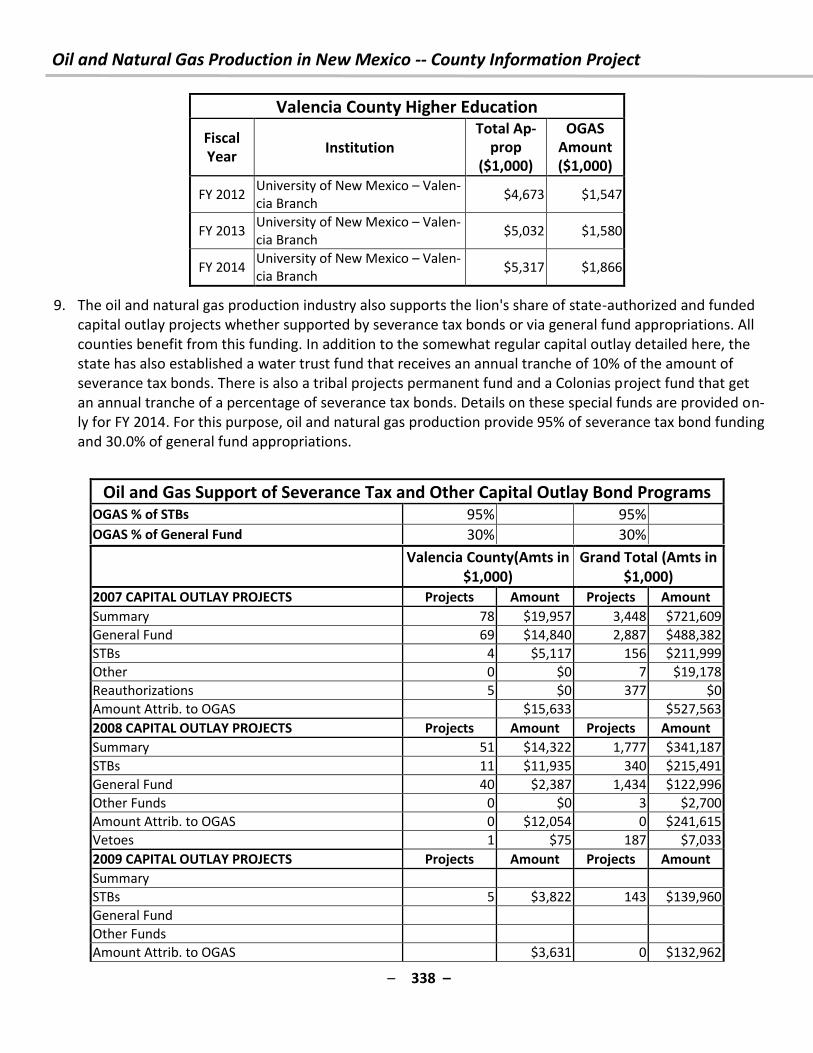

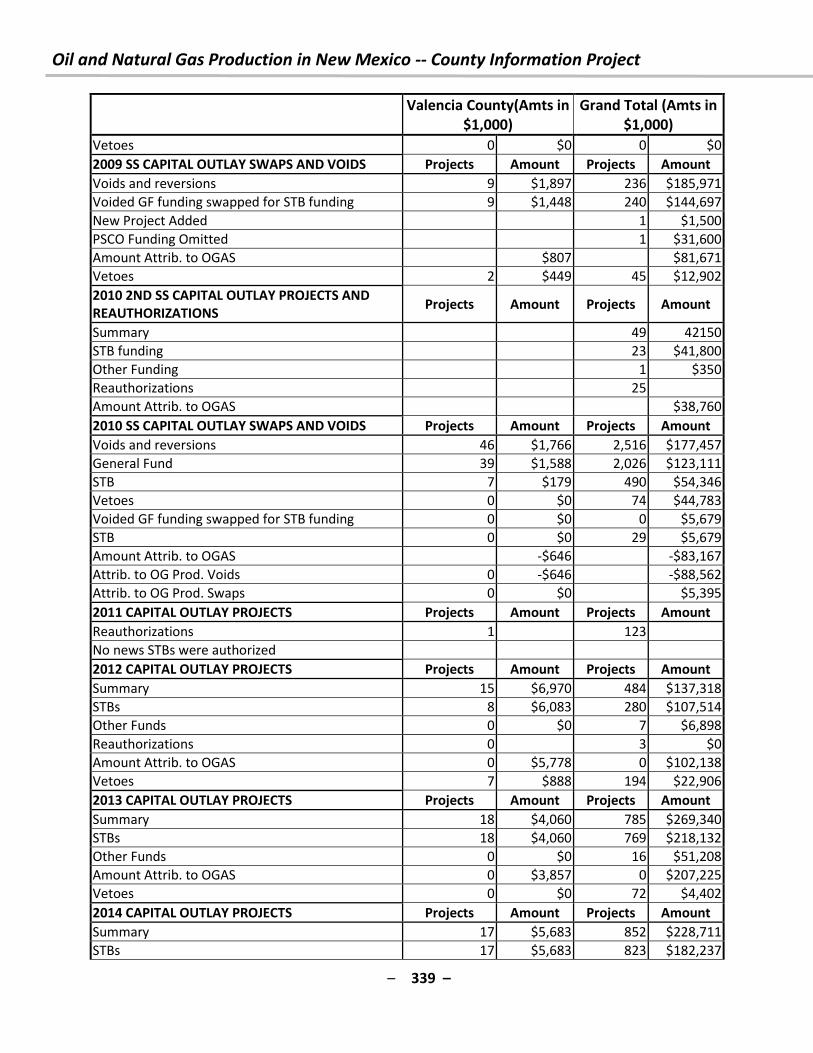

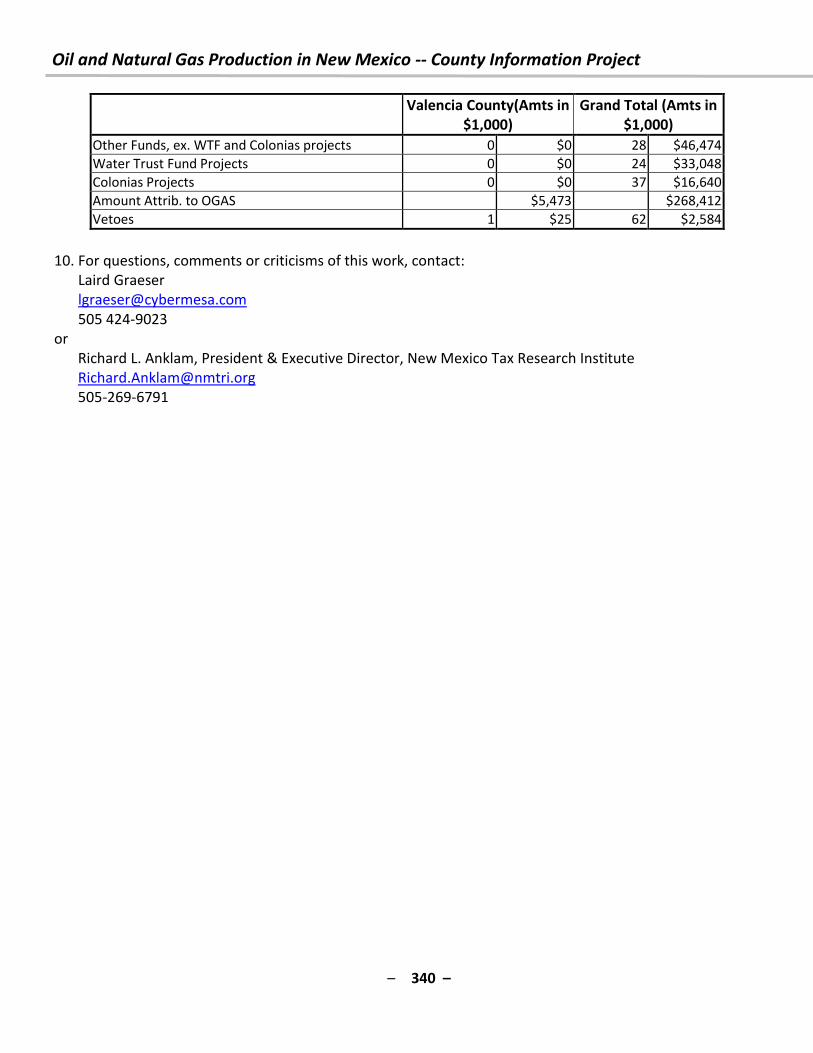

rights reserved www.nmtri.org P.O. Box 91657

Albuquerque, NM 87199 505 842-5833

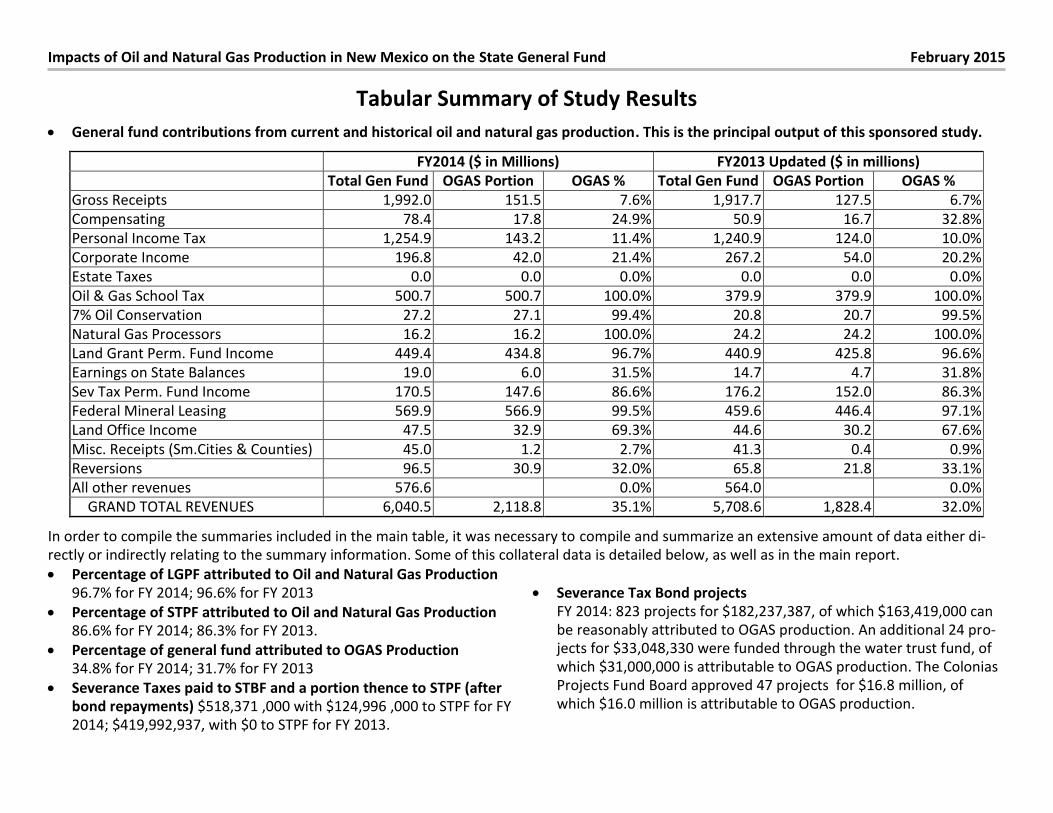

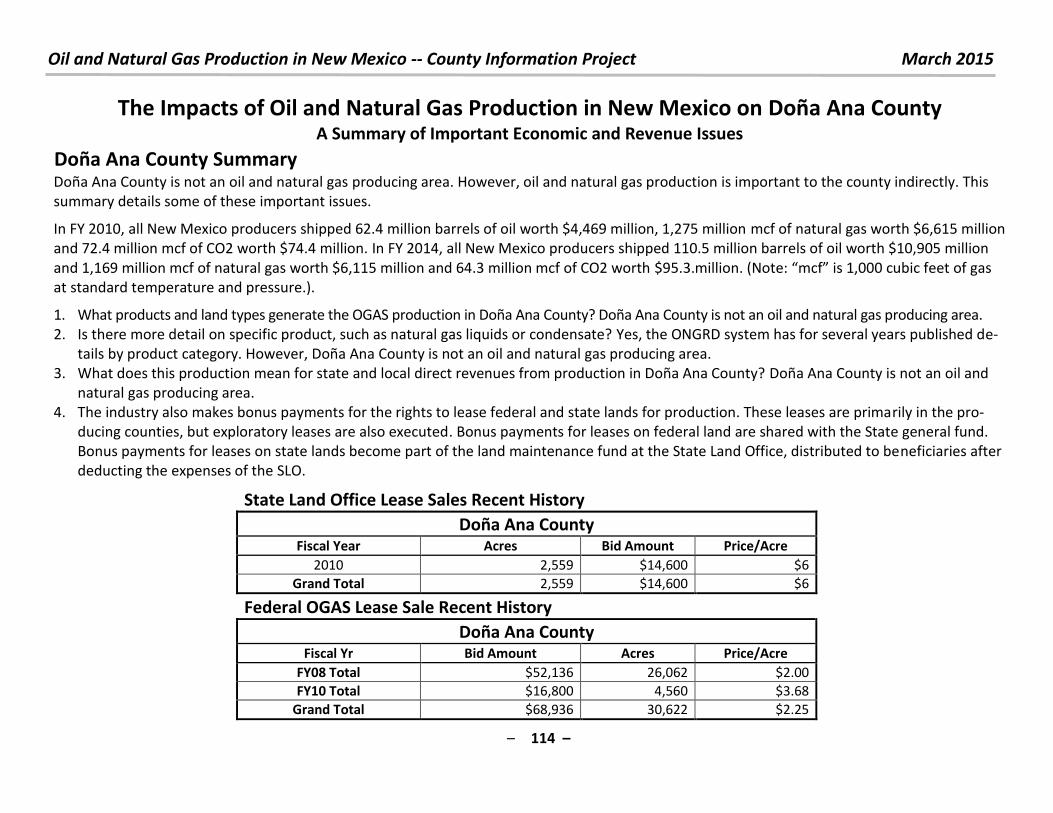

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

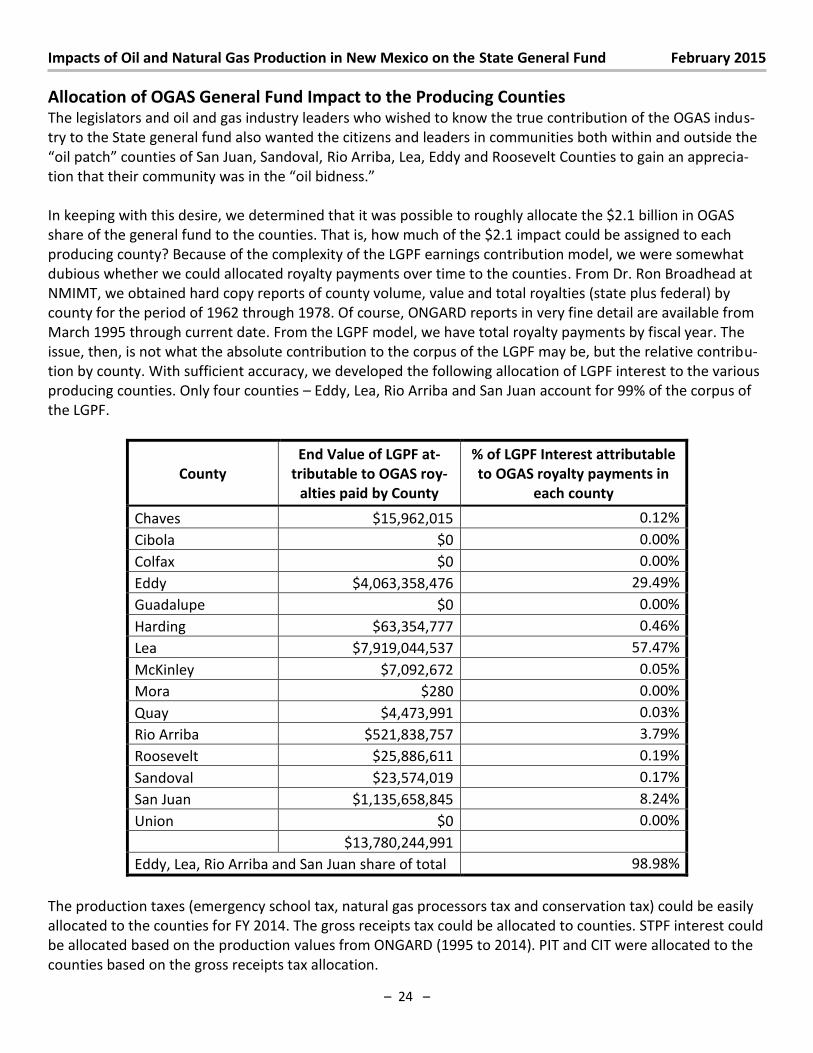

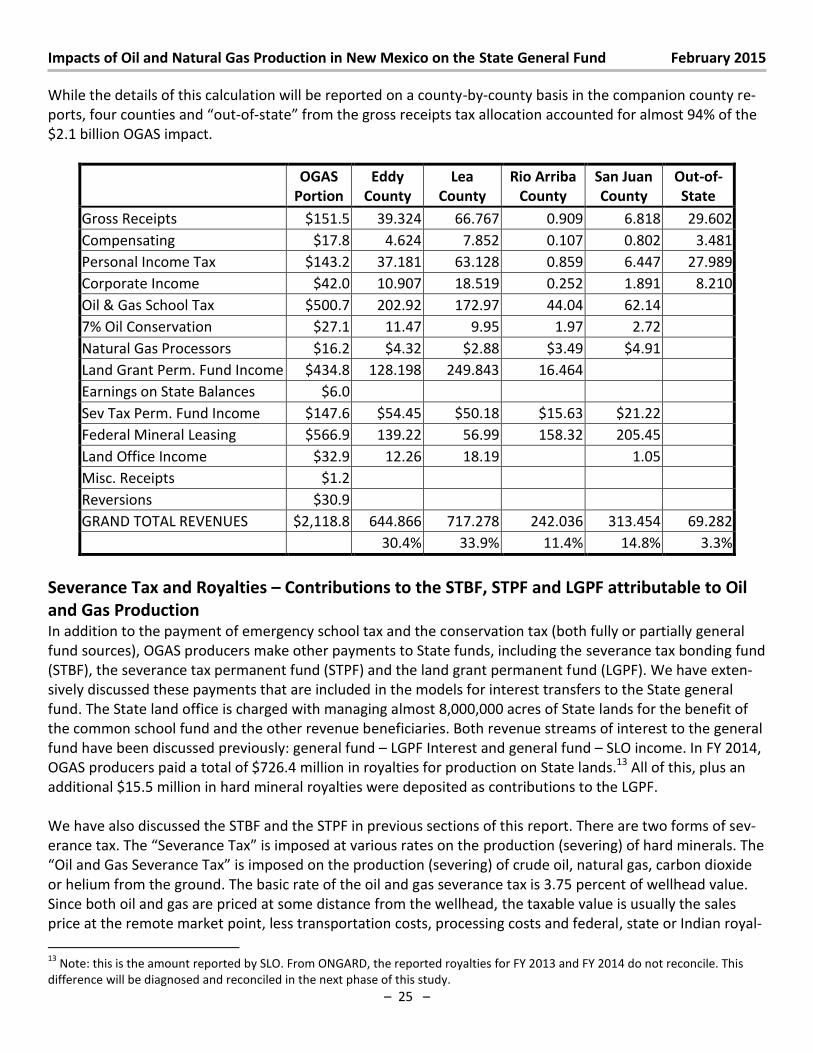

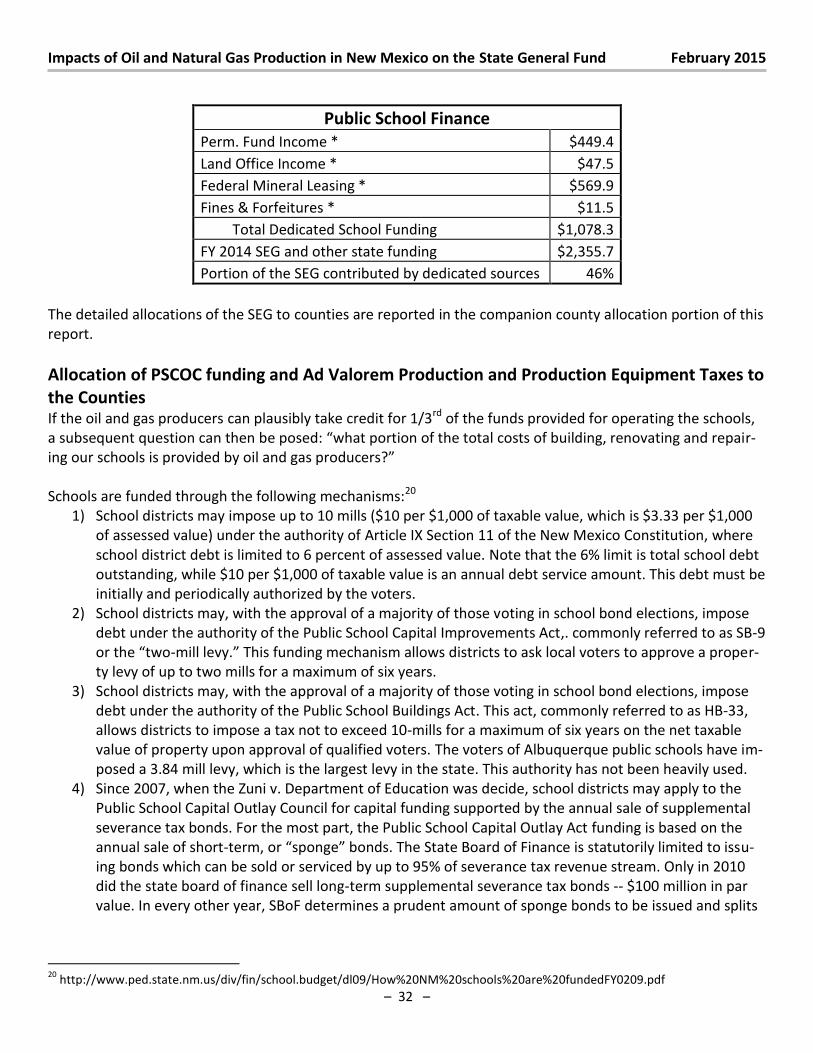

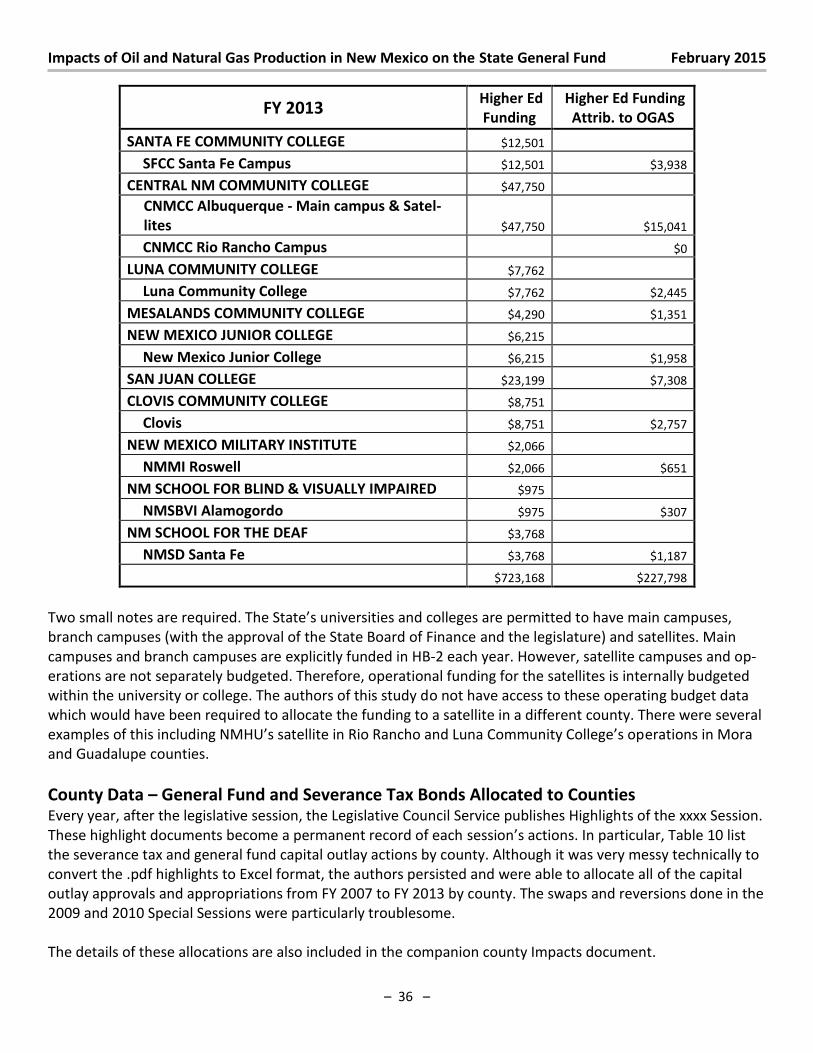

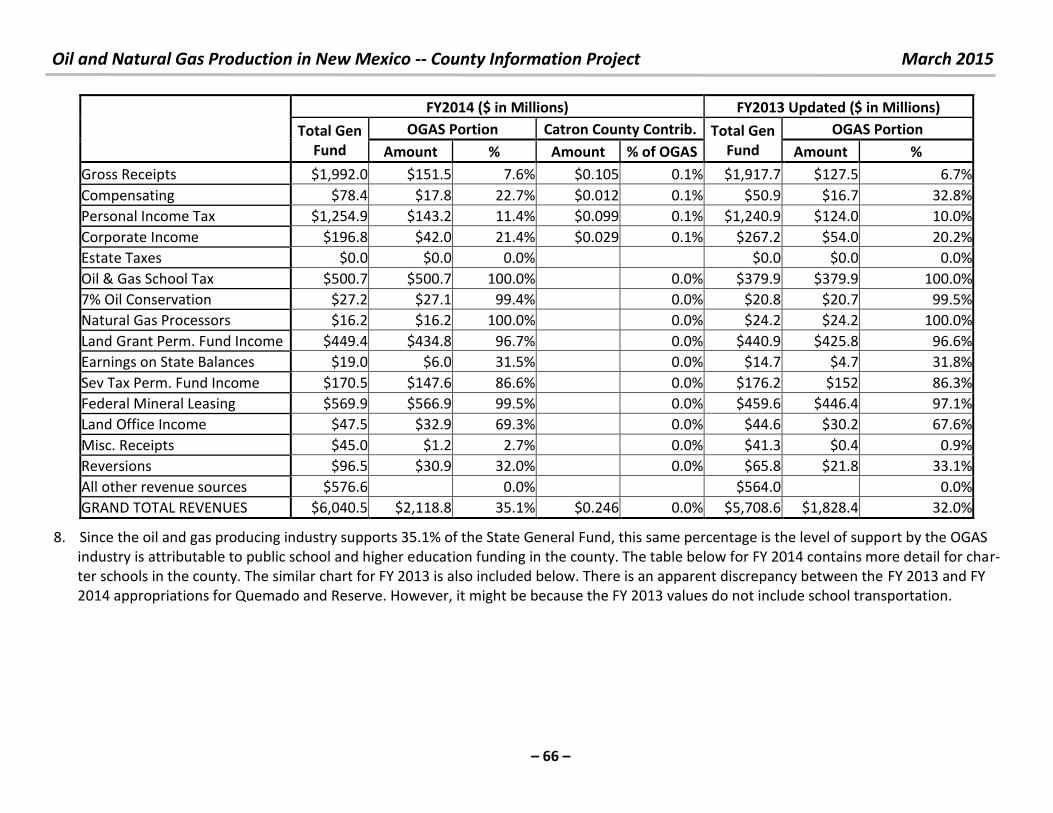

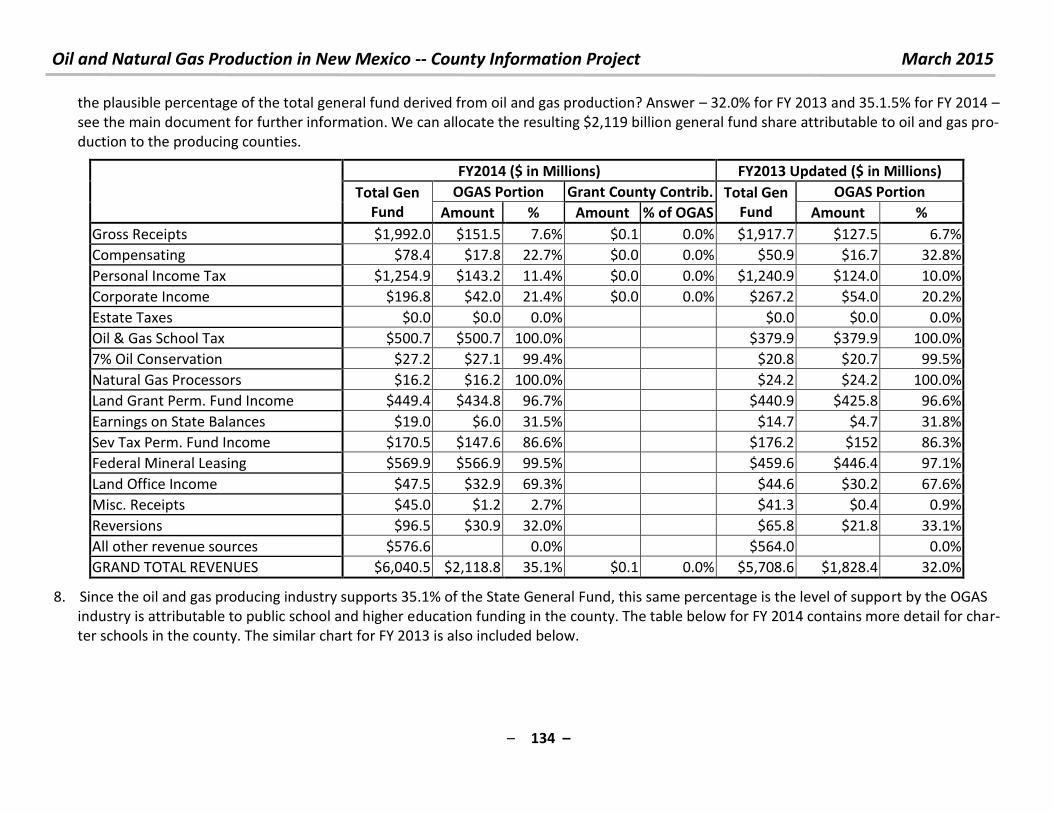

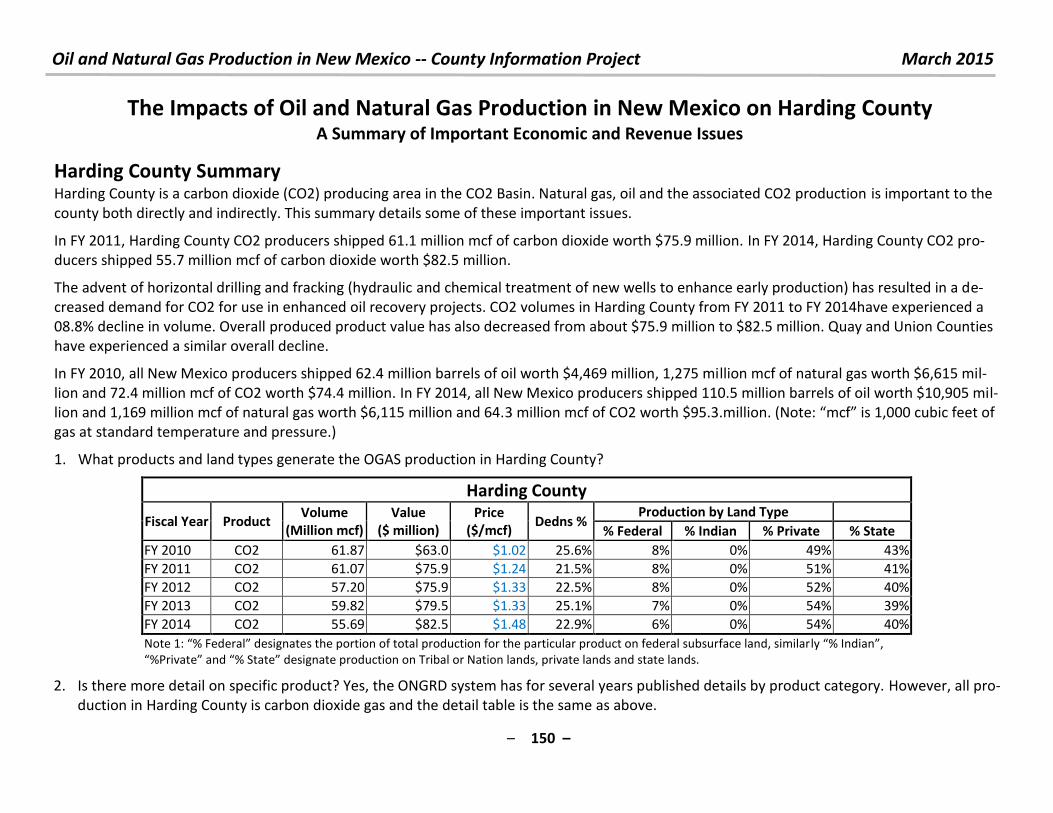

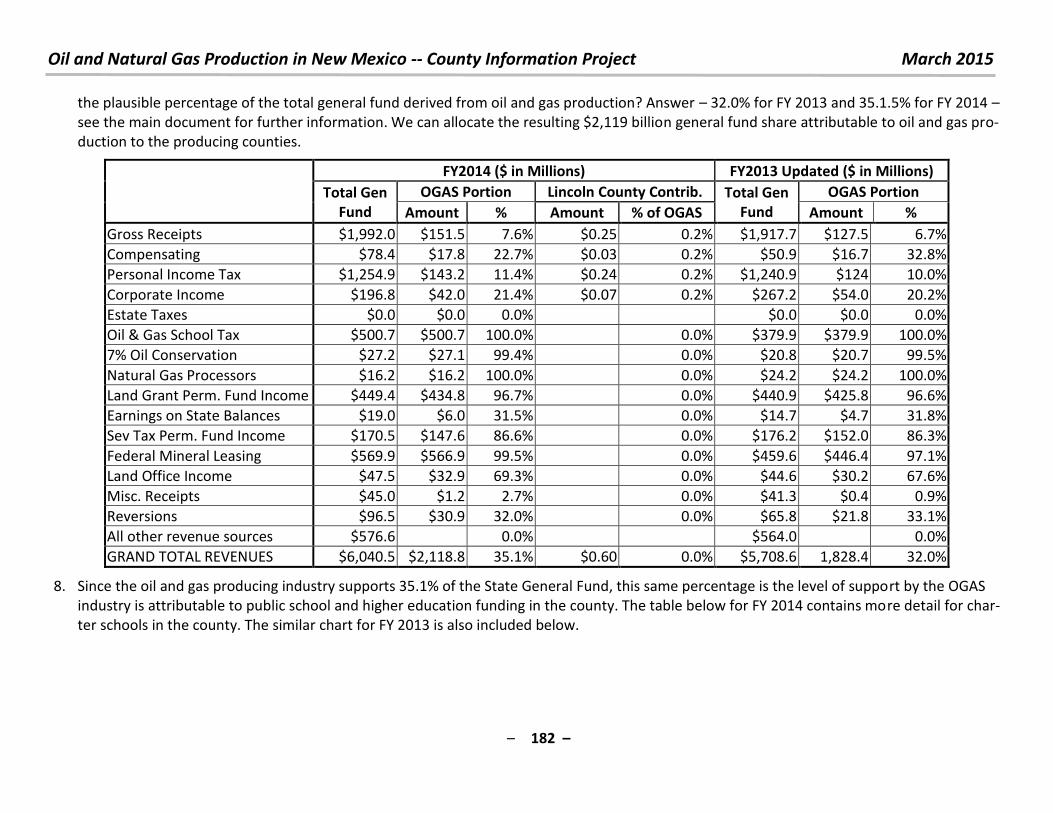

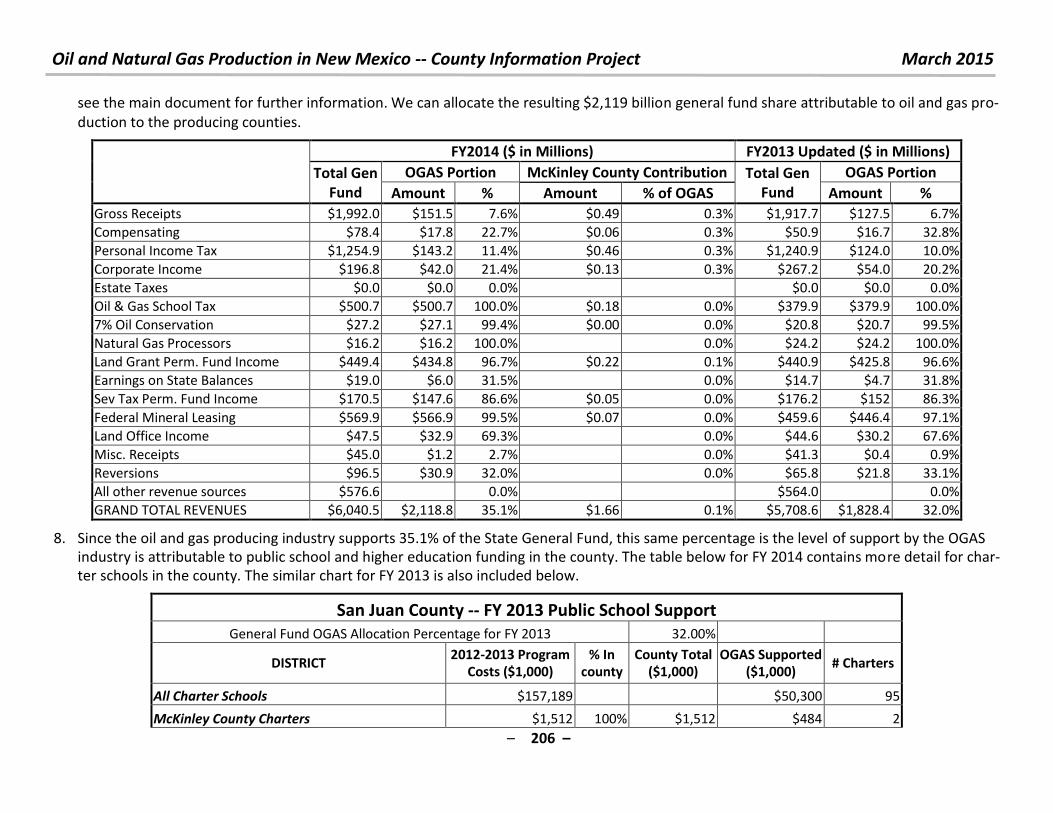

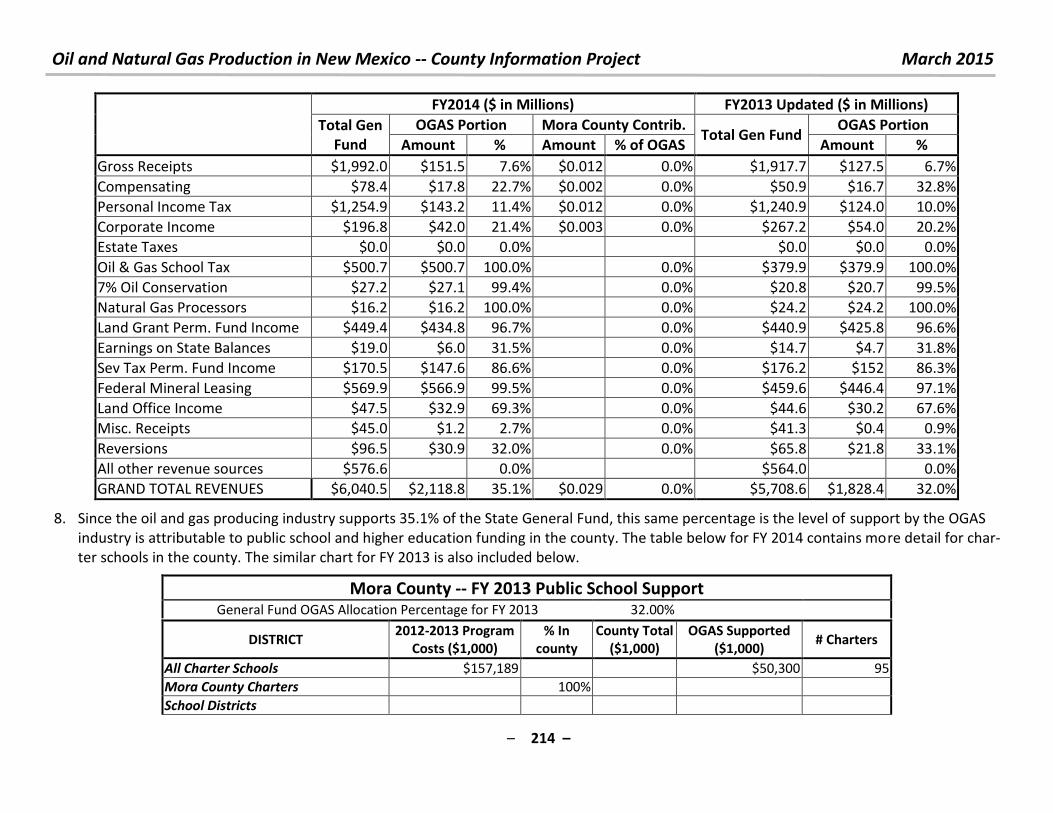

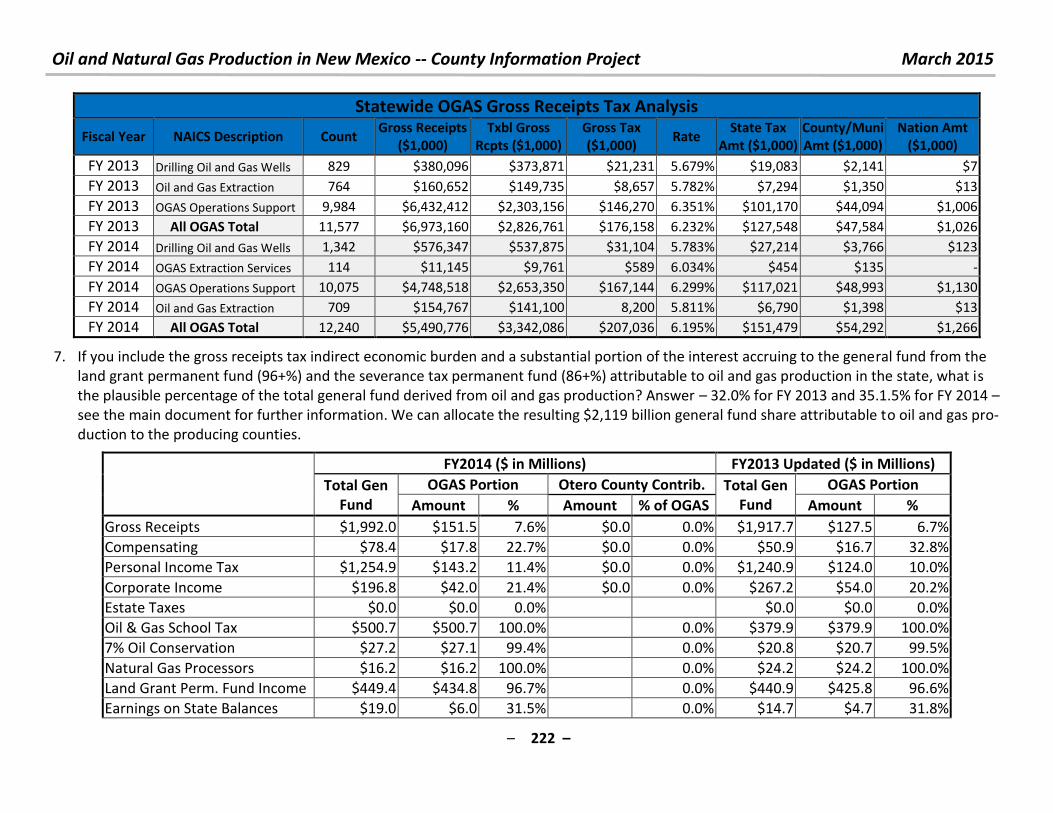

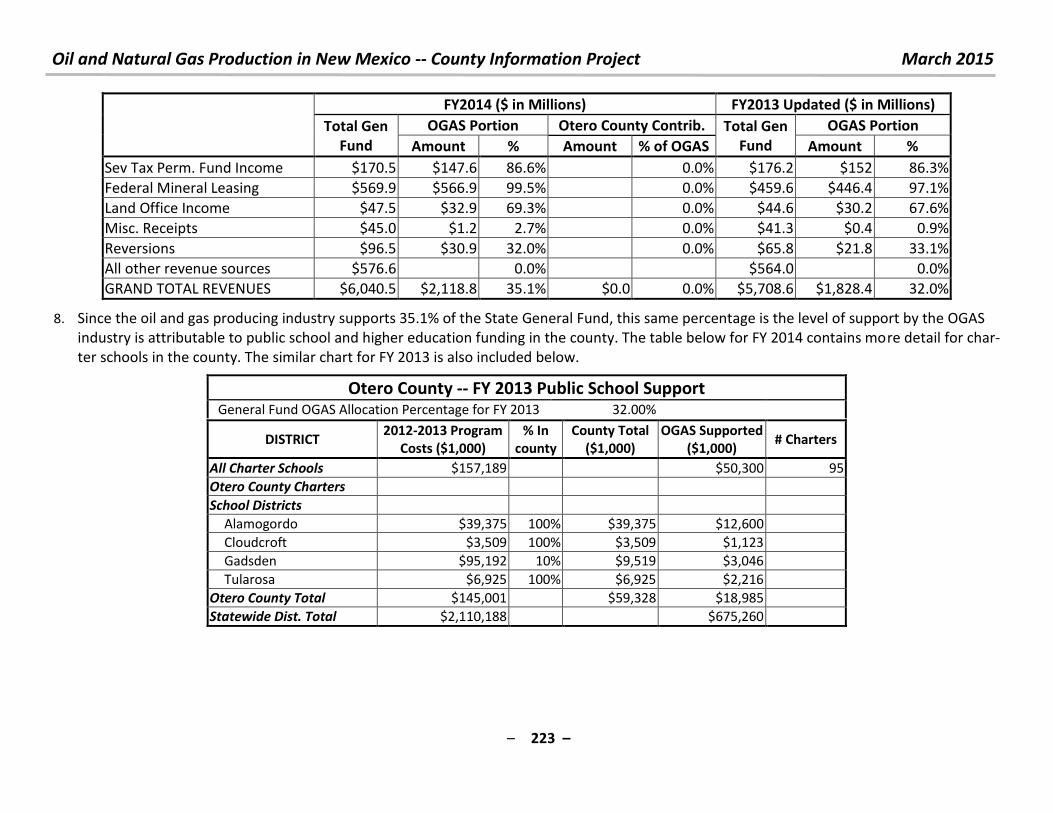

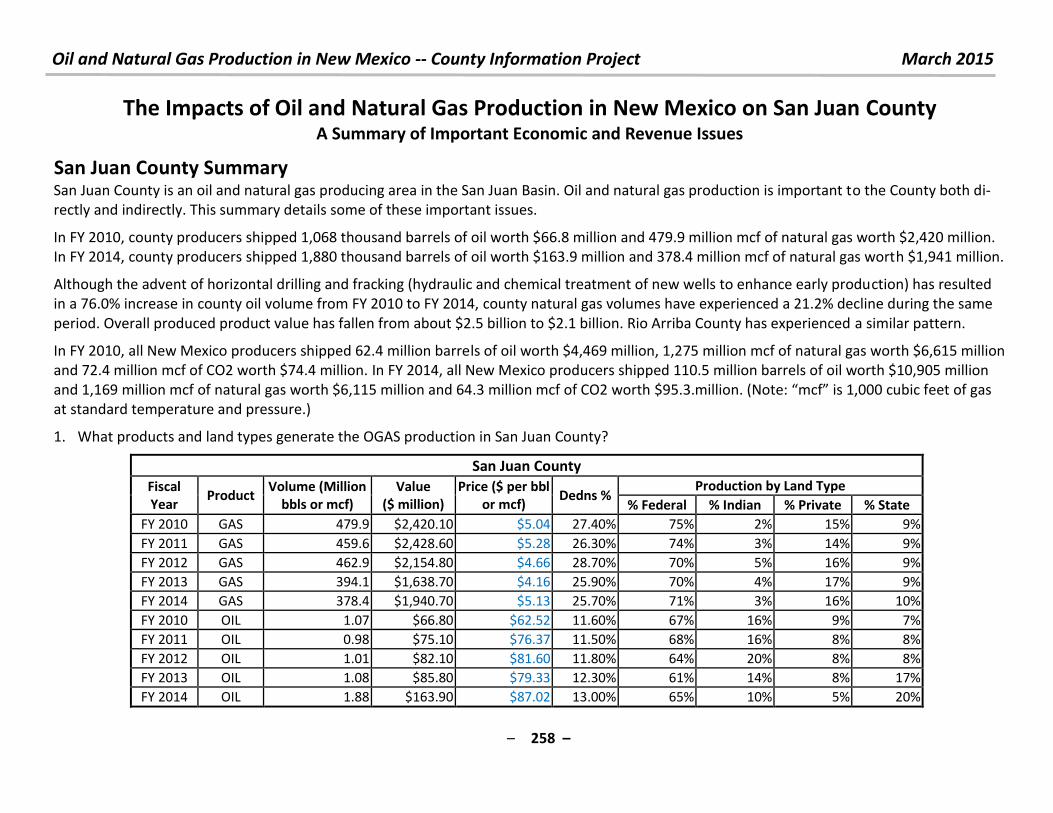

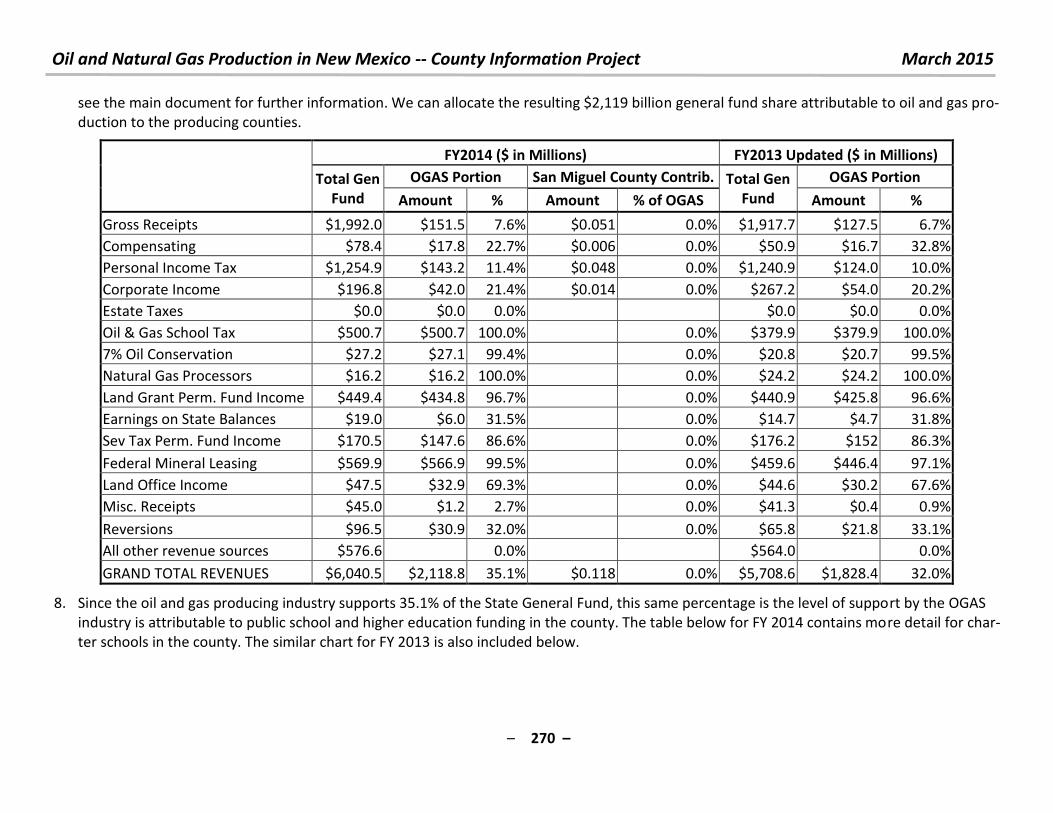

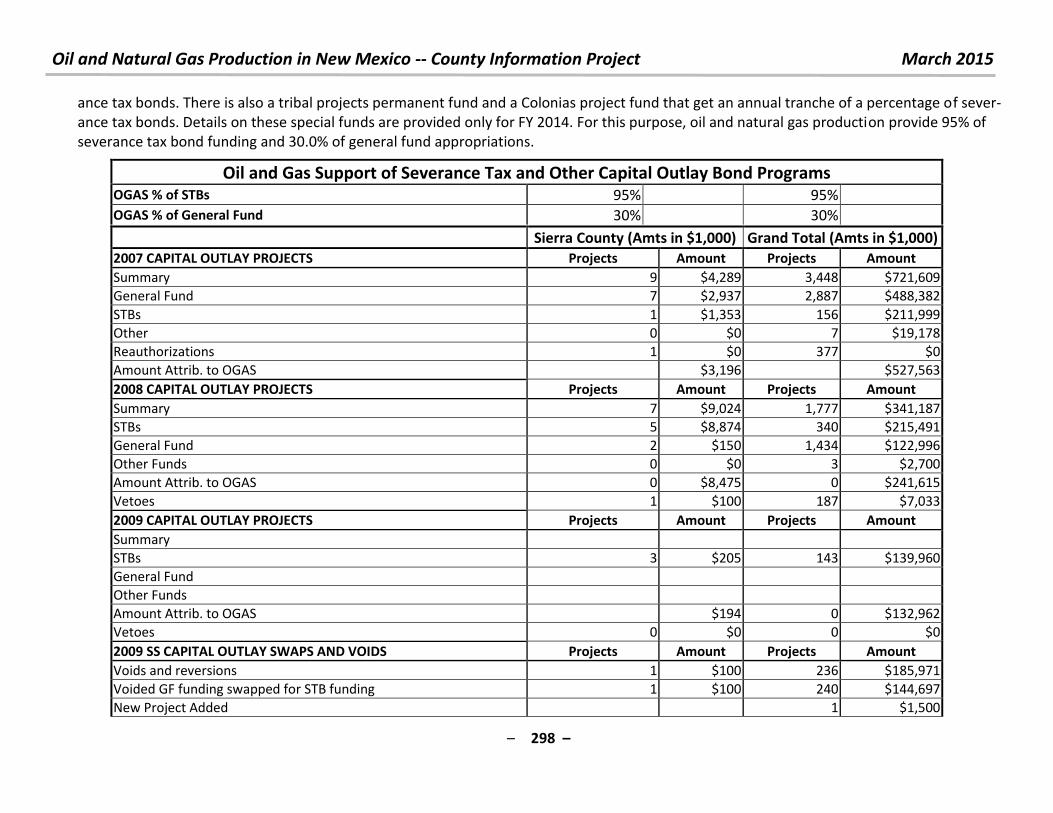

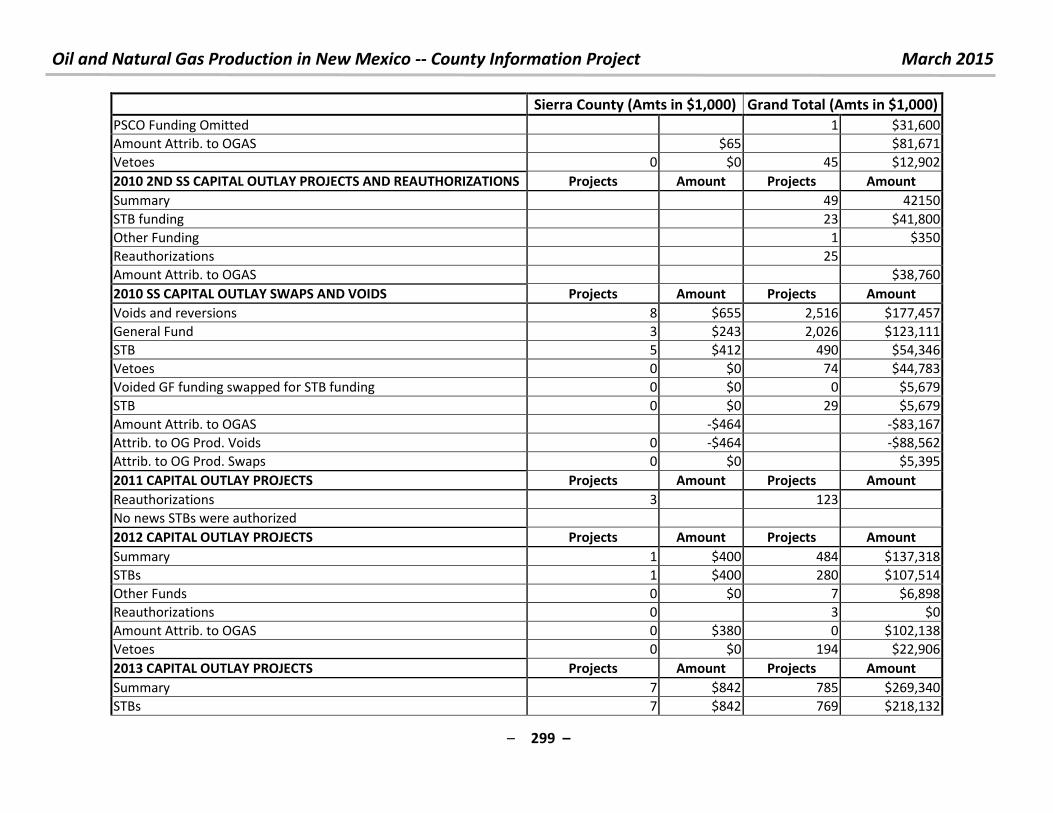

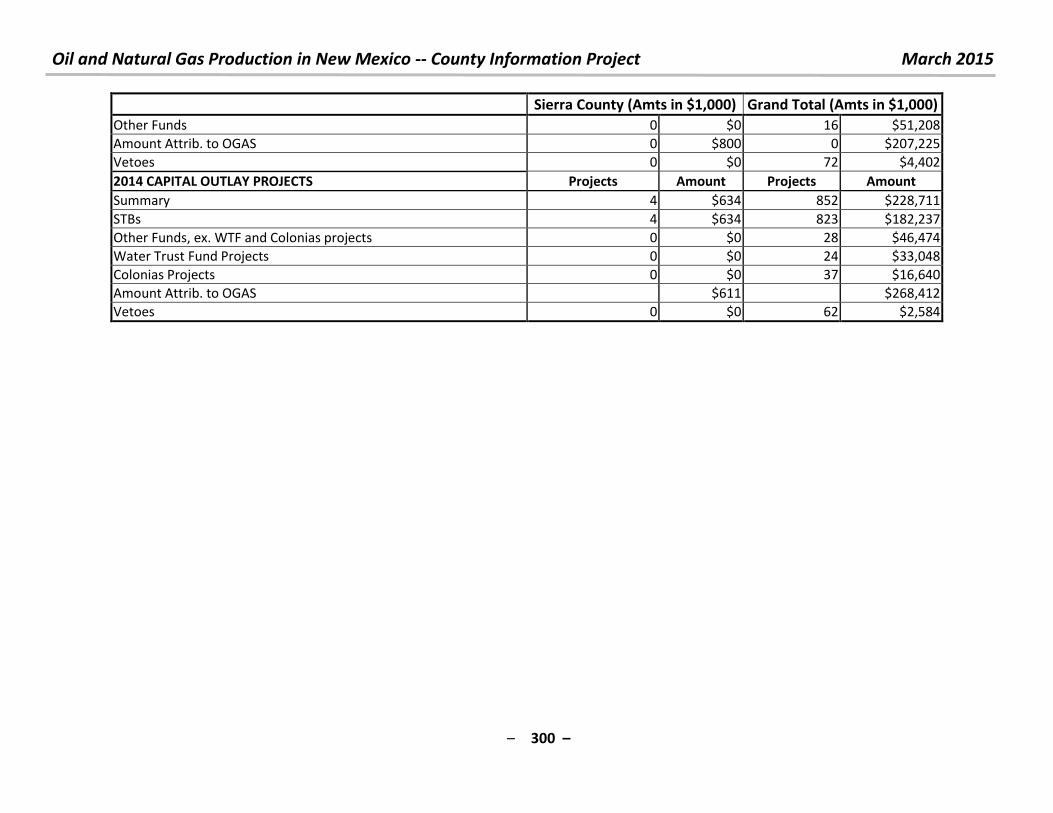

Tabular Summary of Study Results General fund contributions from current and historical oil and natural gas production. This is the principal output of this sponsored study.

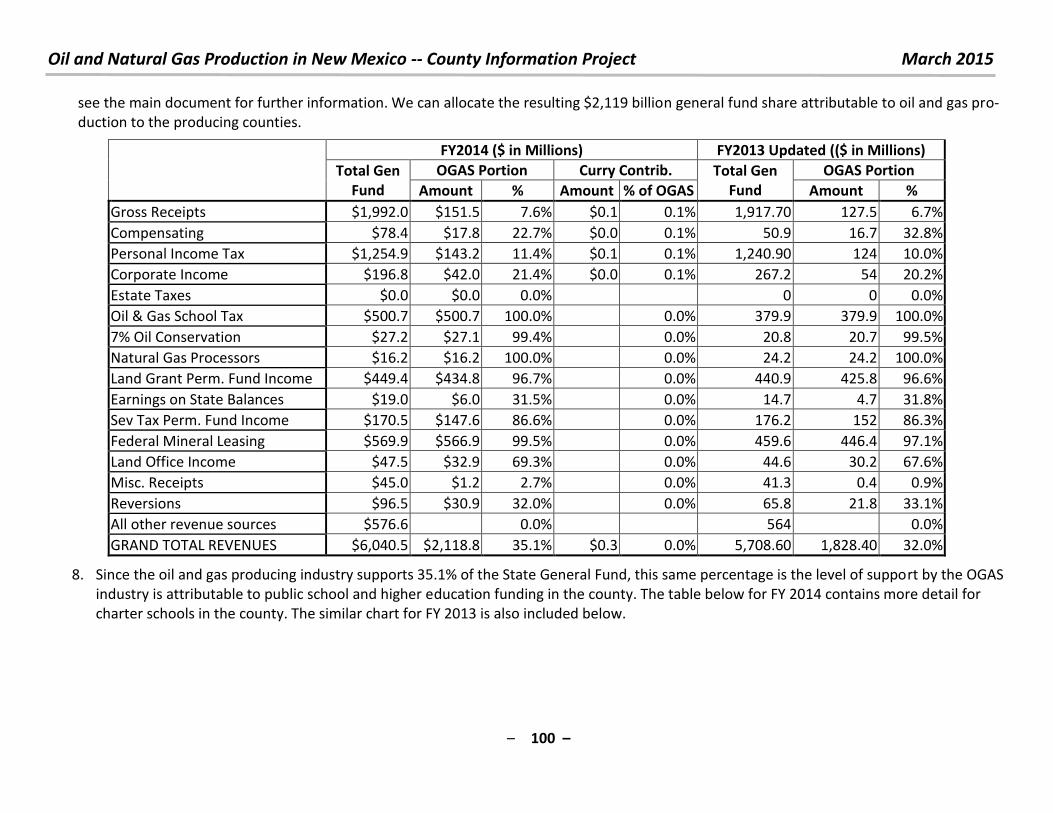

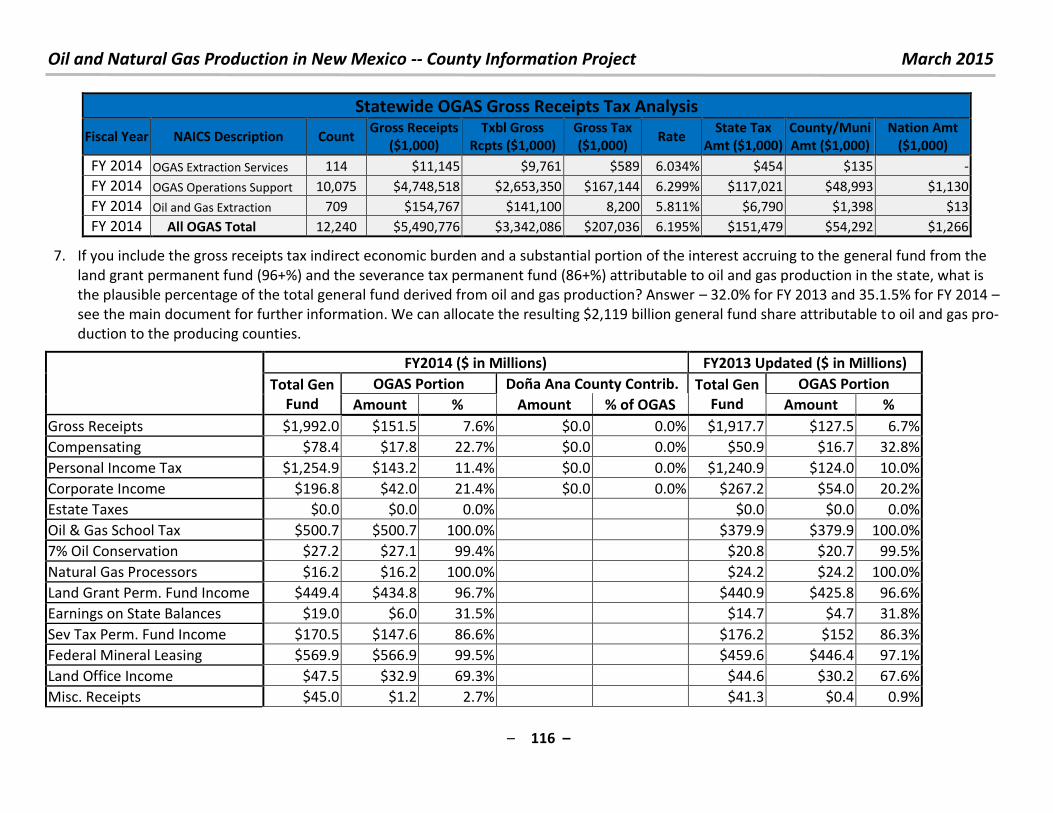

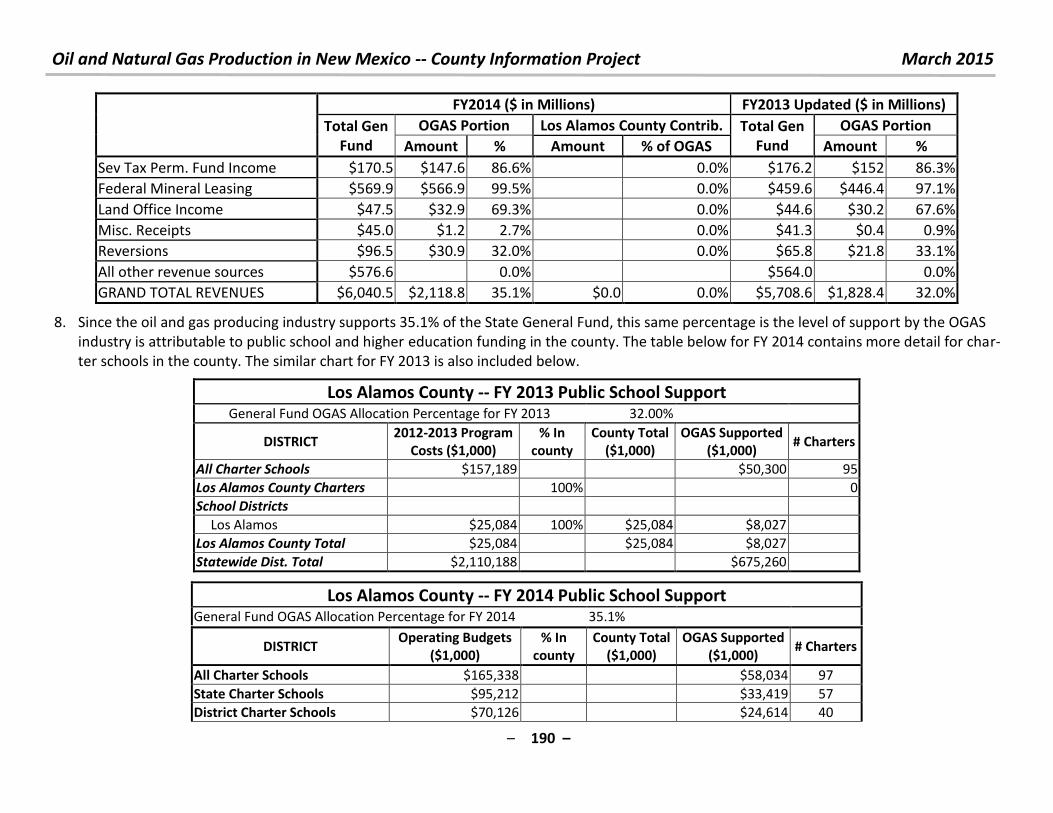

FY2014 ($ in Millions) FY2013 Updated ($ in millions)

Total Gen Fund OGAS Portion OGAS % Total Gen Fund OGAS Portion OGAS %

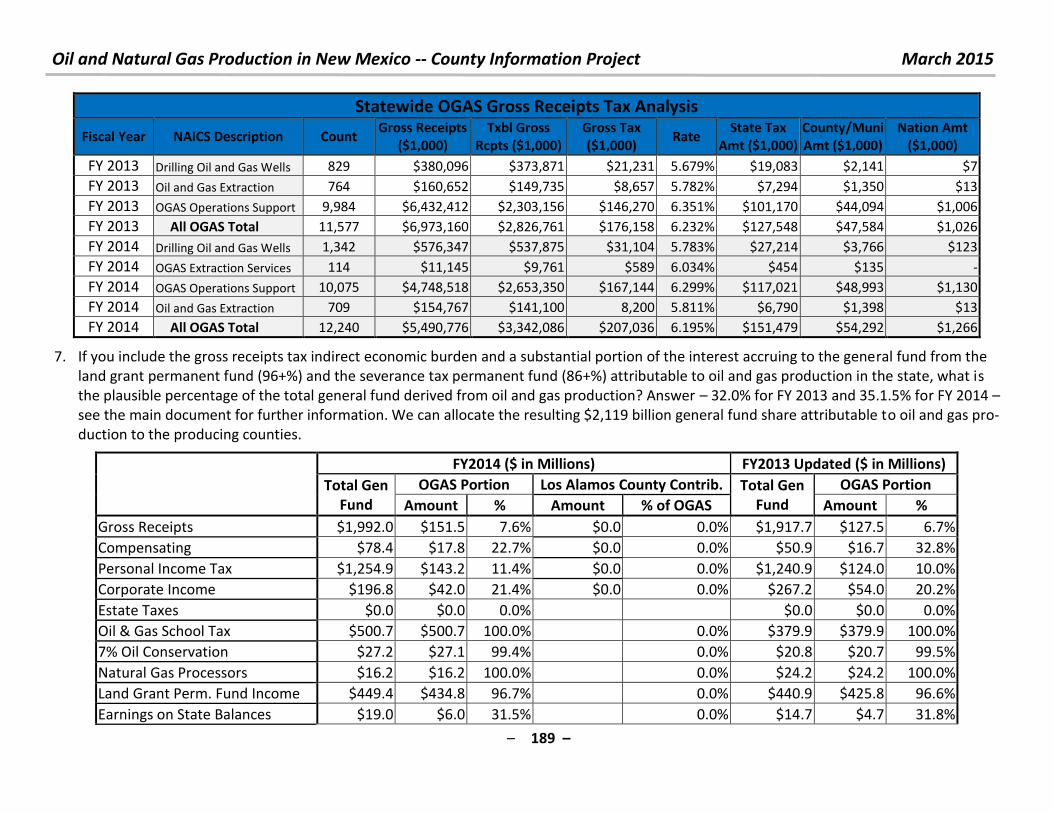

Gross Receipts 1,992.0 151.5 7.6% 1,917.7 127.5 6.7%

Compensating 78.4 17.8 24.9% 50.9 16.7 32.8%

Personal Income Tax 1,254.9 143.2 11.4% 1,240.9 124.0 10.0%

Corporate Income 196.8 42.0 21.4% 267.2 54.0 20.2%

Estate Taxes 0.0 0.0 0.0% 0.0 0.0 0.0%

Oil & Gas School Tax 500.7 500.7 100.0% 379.9 379.9 100.0%

7% Oil Conservation 27.2 27.1 99.4% 20.8 20.7 99.5%

Natural Gas Processors 16.2 16.2 100.0% 24.2 24.2 100.0%

Land Grant Perm. Fund Income 449.4 434.8 96.7% 440.9 425.8 96.6%

Earnings on State Balances 19.0 6.0 31.5% 14.7 4.7 31.8%

Sev Tax Perm. Fund Income 170.5 147.6 86.6% 176.2 152.0 86.3%

Federal Mineral Leasing 569.9 566.9 99.5% 459.6 446.4 97.1%

Land Office Income 47.5 32.9 69.3% 44.6 30.2 67.6%

Misc. Receipts (Sm.Cities & Counties) 45.0 1.2 2.7% 41.3 0.4 0.9%

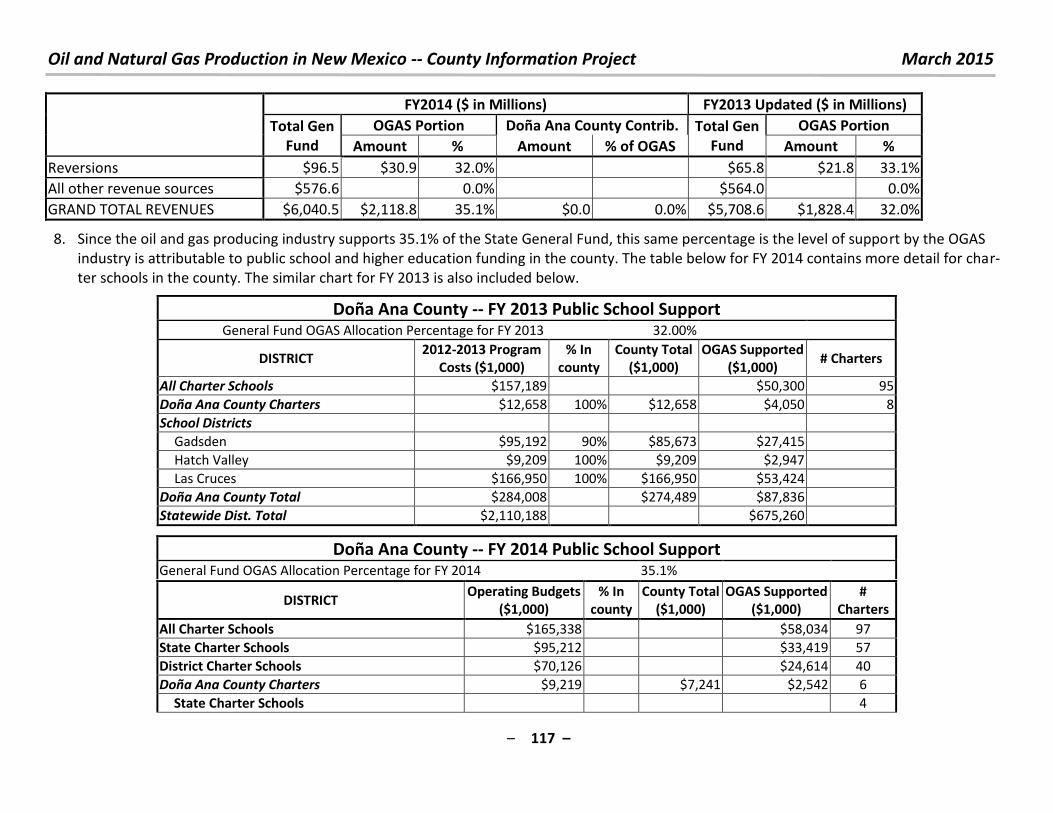

Reversions 96.5 30.9 32.0% 65.8 21.8 33.1%

All other revenues 576.6

0.0% 564.0

0.0%

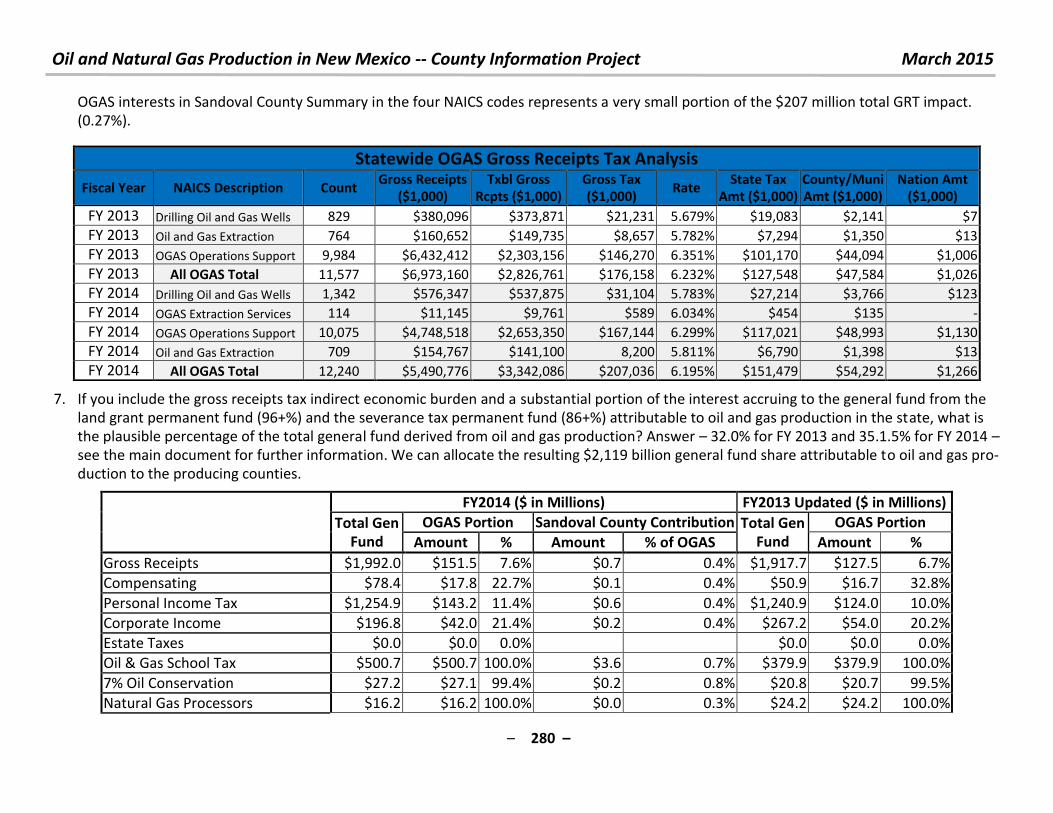

GRAND TOTAL REVENUES 6,040.5 2,118.8 35.1% 5,708.6 1,828.4 32.0%

In order to compile the summaries included in the main table, it was necessary to compile and summarize an extensive amount of data either di-

rectly or indirectly relating to the summary information. Some of this collateral data is detailed below, as well as in the main report.

Percentage of LGPF attributed to Oil and Natural Gas Production

96.7% for FY 2014; 96.6% for FY 2013

Percentage of STPF attributed to Oil and Natural Gas Production 86.6% for FY 2014; 86.3% for FY 2013.

Percentage of general fund attributed to OGAS Production 34.8% for FY 2014; 31.7% for FY 2013

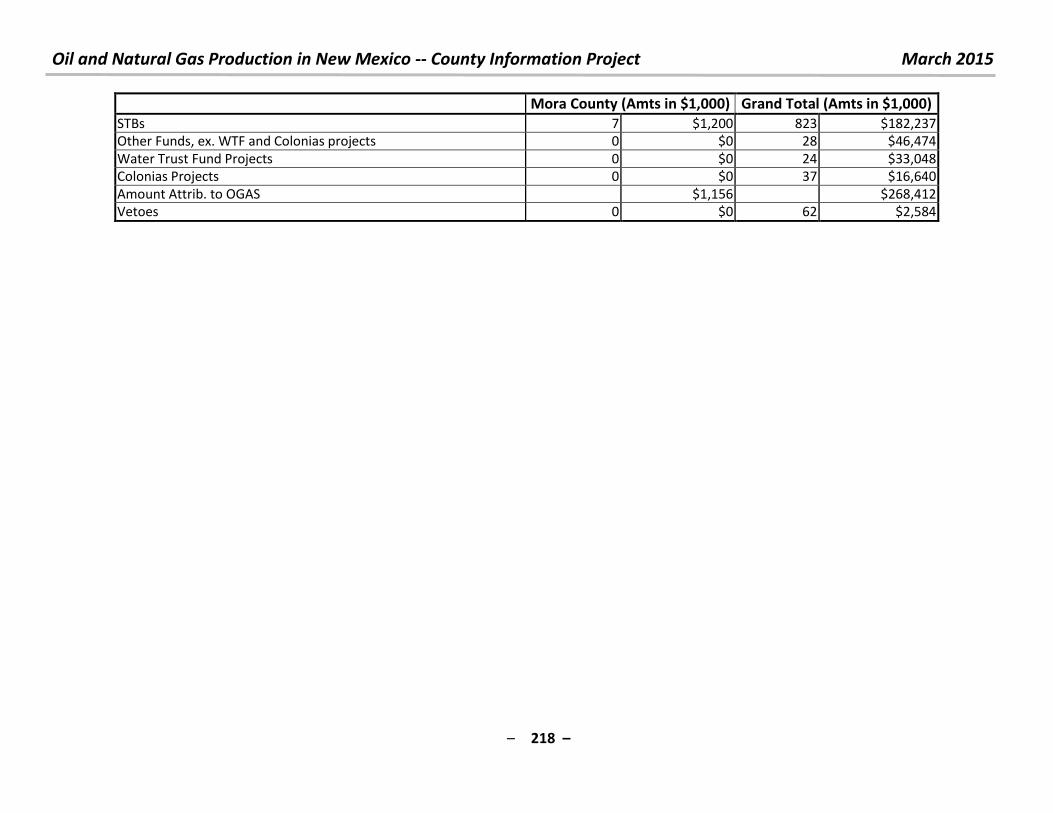

Severance Taxes paid to STBF and a portion thence to STPF (after bond repayments) $518,371 ,000 with $124,996 ,000 to STPF for FY

2014; $419,992,937, with $0 to STPF for FY 2013.

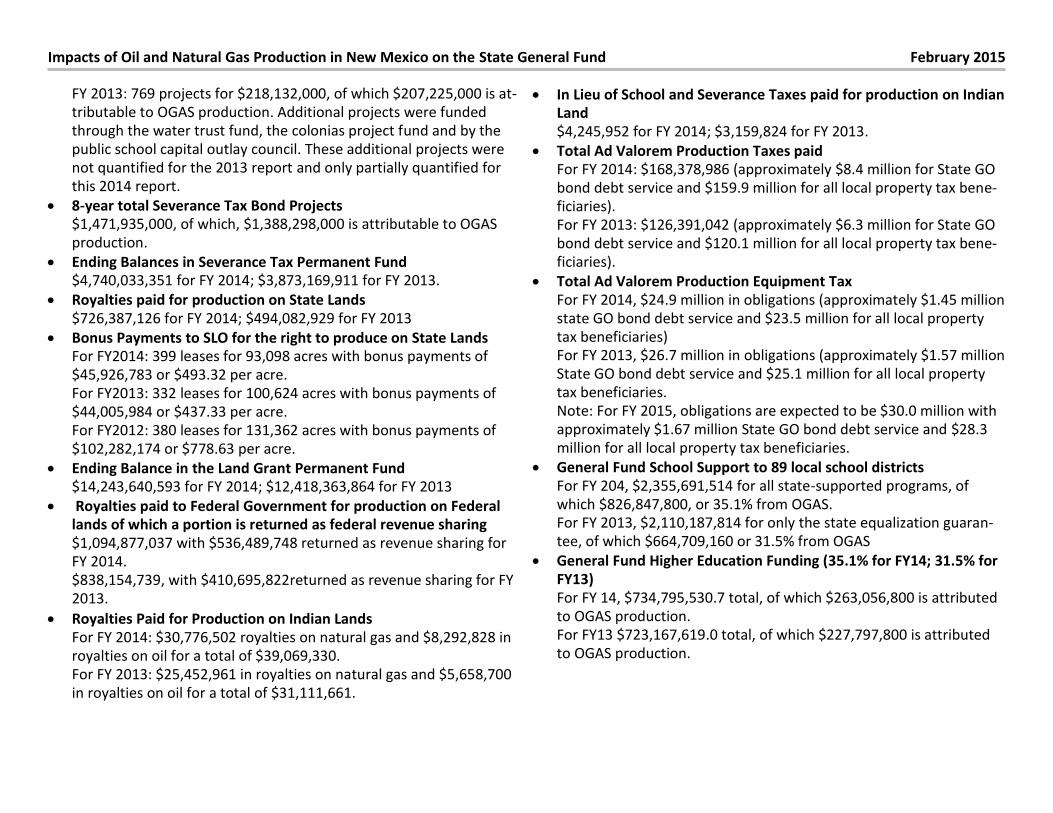

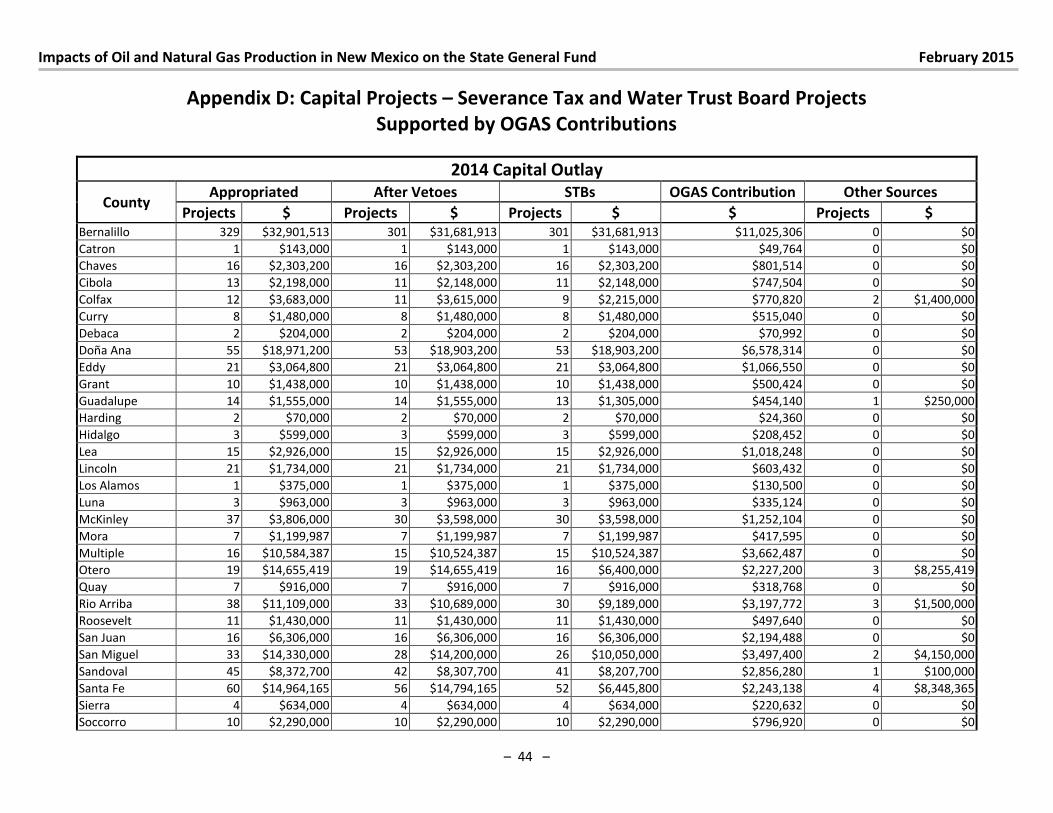

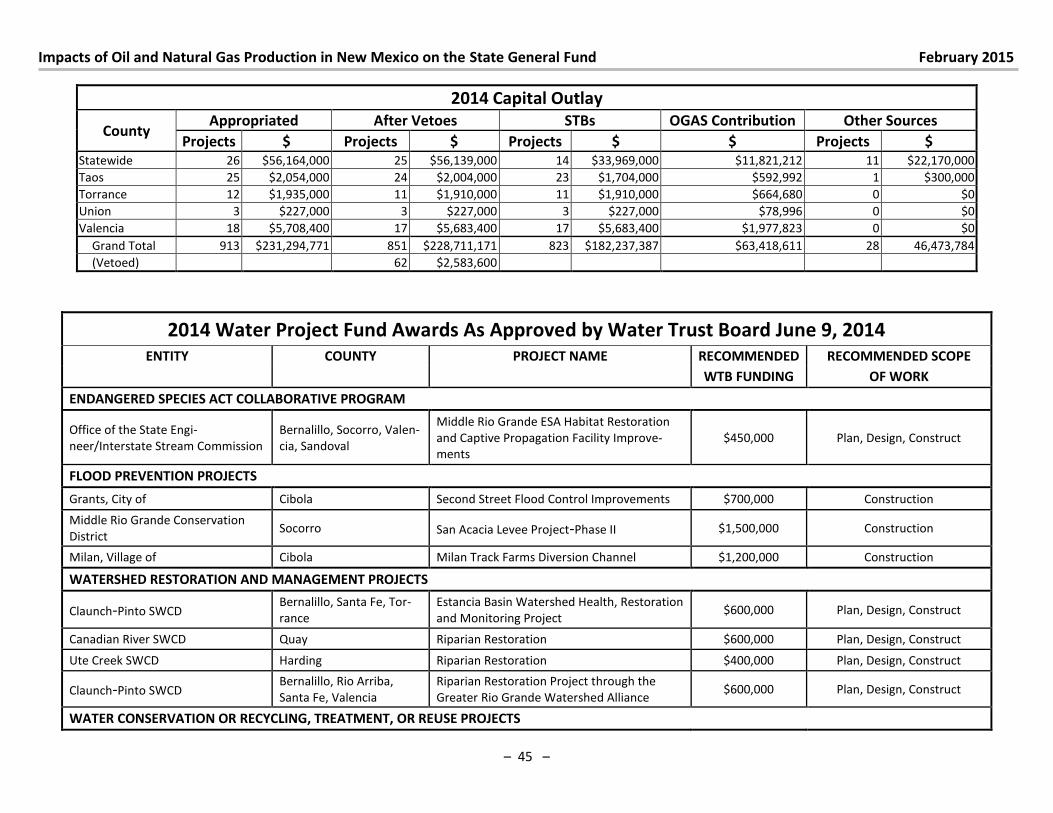

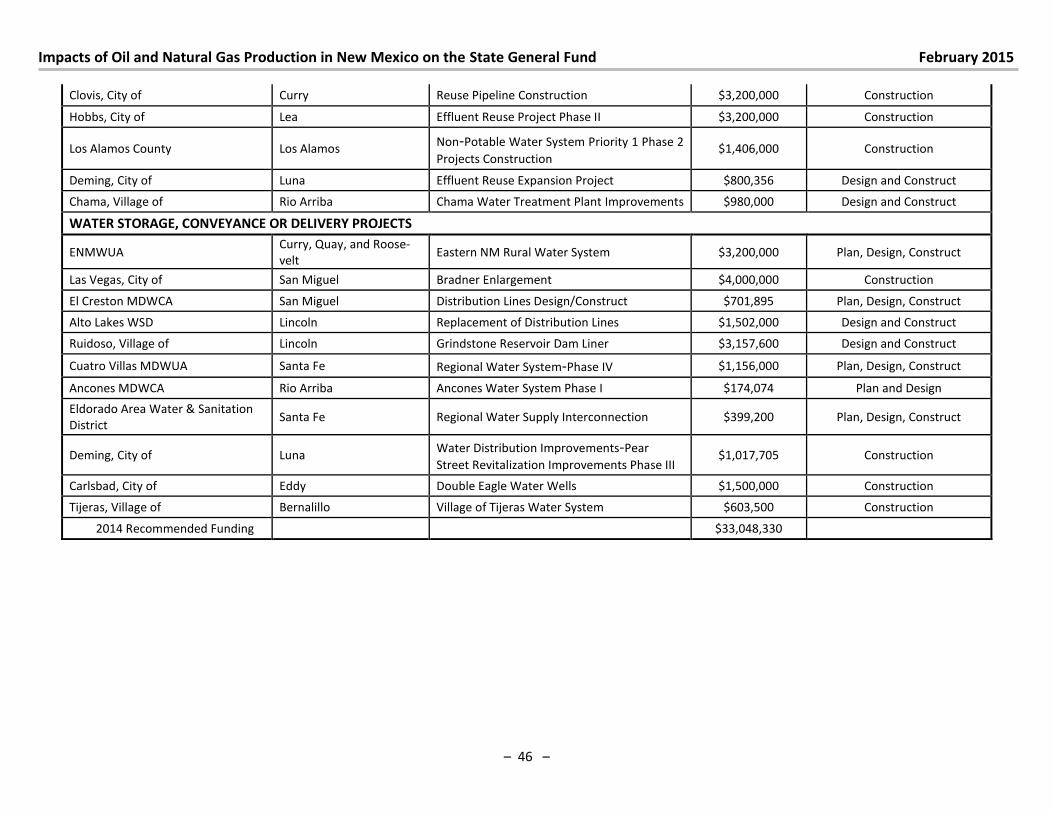

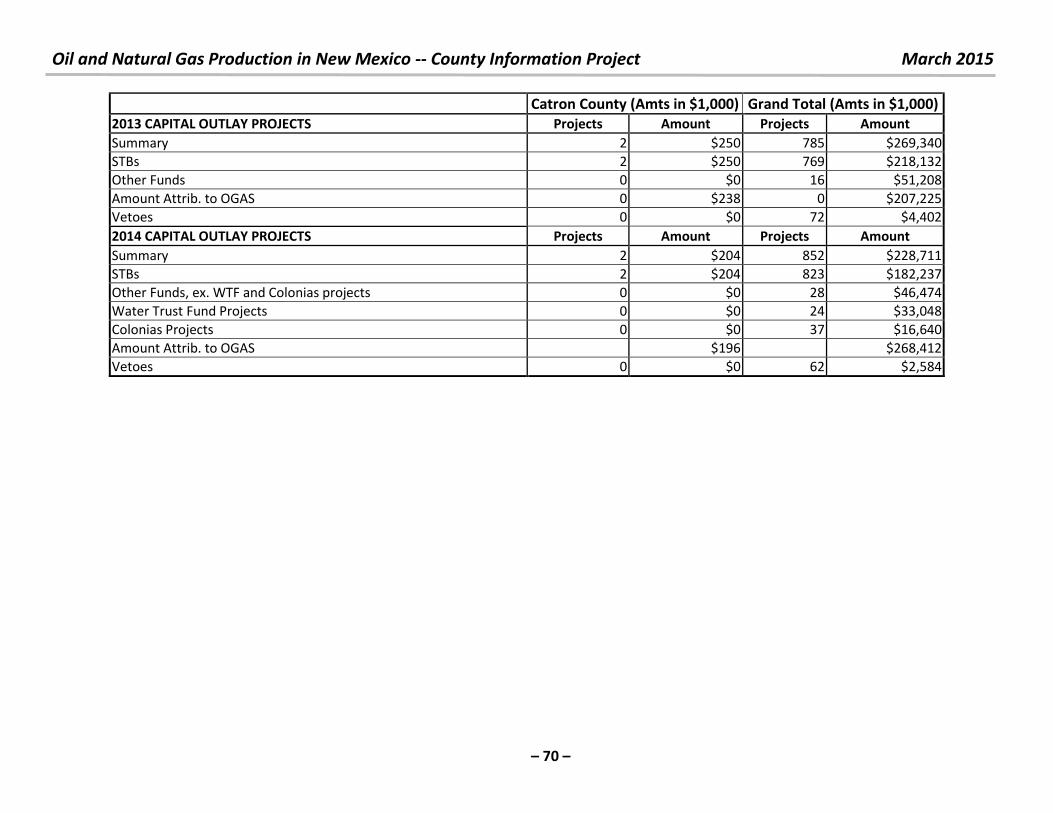

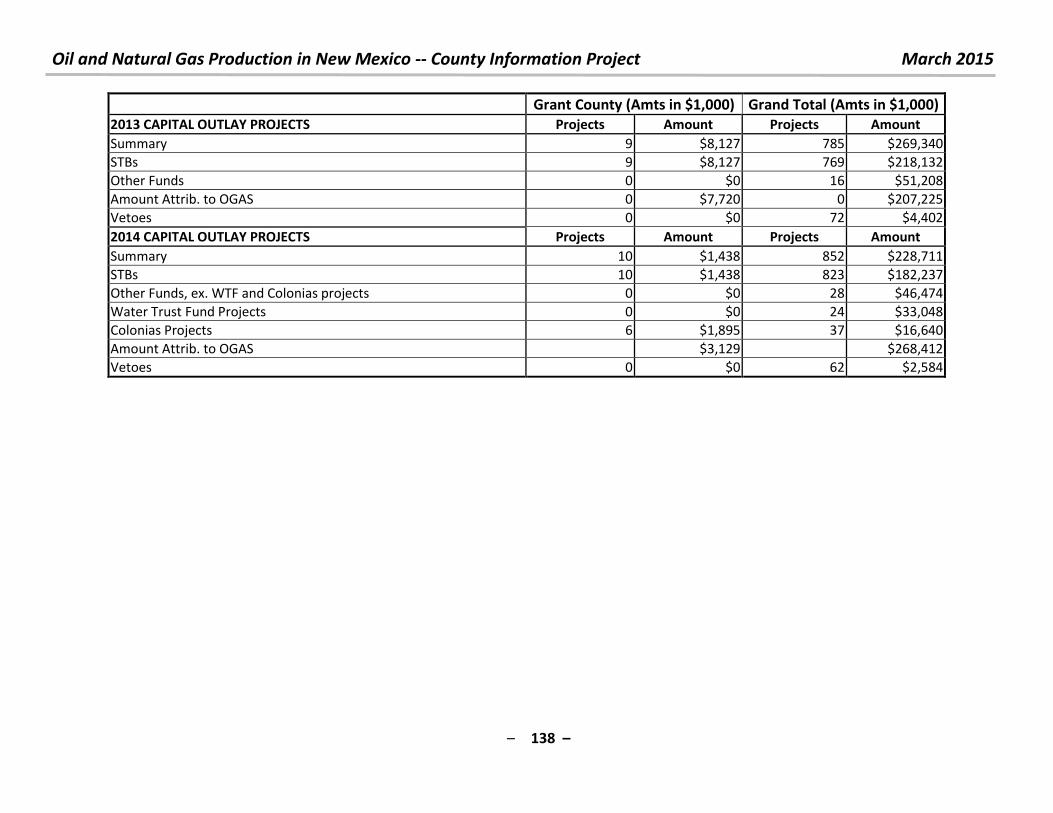

Severance Tax Bond projects

FY 2014: 823 projects for $182,237,387, of which $163,419,000 can

be reasonably attributed to OGAS production. An additional 24 pro-jects for $33,048,330 were funded through the water trust fund, of

which $31,000,000 is attributable to OGAS production. The Colonias

Projects Fund Board approved 47 projects for $16.8 million, of

which $16.0 million is attributable to OGAS production.

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

FY 2013: 769 projects for $218,132,000, of which $207,225,000 is at-

tributable to OGAS production. Additional projects were funded

through the water trust fund, the colonias project fund and by the

public school capital outlay council. These additional projects were

not quantified for the 2013 report and only partially quantified for

this 2014 report.

8-year total Severance Tax Bond Projects $1,471,935,000, of which, $1,388,298,000 is attributable to OGAS

production.

Ending Balances in Severance Tax Permanent Fund $4,740,033,351 for FY 2014; $3,873,169,911 for FY 2013.

Royalties paid for production on State Lands

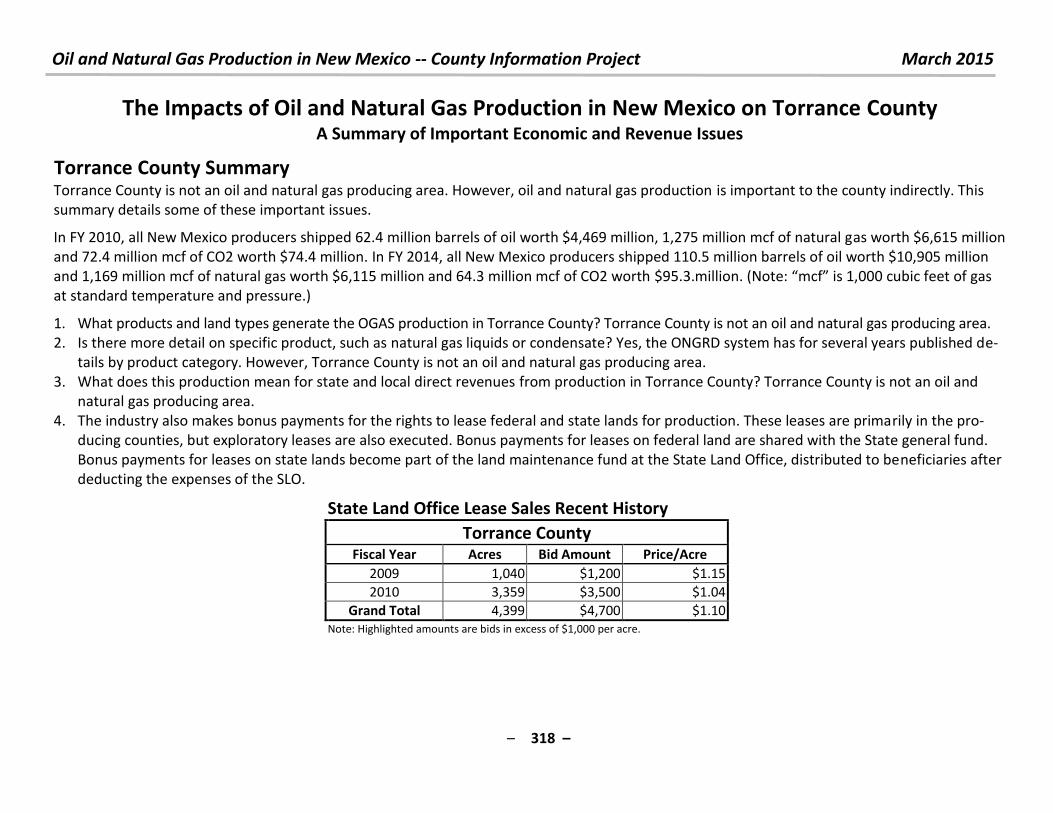

$726,387,126 for FY 2014; $494,082,929 for FY 2013

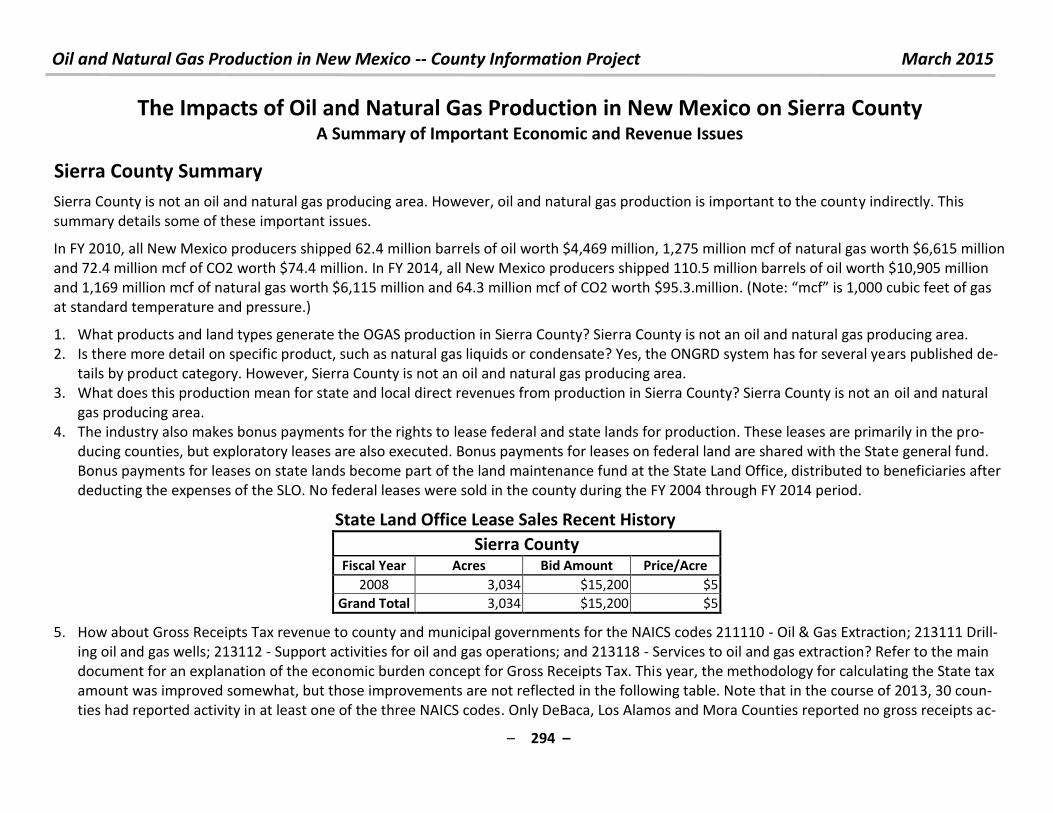

Bonus Payments to SLO for the right to produce on State Lands For FY2014: 399 leases for 93,098 acres with bonus payments of

$45,926,783 or $493.32 per acre.

For FY2013: 332 leases for 100,624 acres with bonus payments of

$44,005,984 or $437.33 per acre.

For FY2012: 380 leases for 131,362 acres with bonus payments of

$102,282,174 or $778.63 per acre.

Ending Balance in the Land Grant Permanent Fund $14,243,640,593 for FY 2014; $12,418,363,864 for FY 2013

Royalties paid to Federal Government for production on Federal lands of which a portion is returned as federal revenue sharing

$1,094,877,037 with $536,489,748 returned as revenue sharing for

FY 2014.

$838,154,739, with $410,695,822returned as revenue sharing for FY

2013.

Royalties Paid for Production on Indian Lands

For FY 2014: $30,776,502 royalties on natural gas and $8,292,828 in

royalties on oil for a total of $39,069,330.

For FY 2013: $25,452,961 in royalties on natural gas and $5,658,700

in royalties on oil for a total of $31,111,661.

In Lieu of School and Severance Taxes paid for production on Indian Land

$4,245,952 for FY 2014; $3,159,824 for FY 2013.

Total Ad Valorem Production Taxes paid For FY 2014: $168,378,986 (approximately $8.4 million for State GO

bond debt service and $159.9 million for all local property tax bene-

ficiaries).

For FY 2013: $126,391,042 (approximately $6.3 million for State GO

bond debt service and $120.1 million for all local property tax bene-

ficiaries).

Total Ad Valorem Production Equipment Tax

For FY 2014, $24.9 million in obligations (approximately $1.45 million

state GO bond debt service and $23.5 million for all local property

tax beneficiaries) For FY 2013, $26.7 million in obligations (approximately $1.57 million

State GO bond debt service and $25.1 million for all local property

tax beneficiaries.

Note: For FY 2015, obligations are expected to be $30.0 million with

approximately $1.67 million State GO bond debt service and $28.3

million for all local property tax beneficiaries.

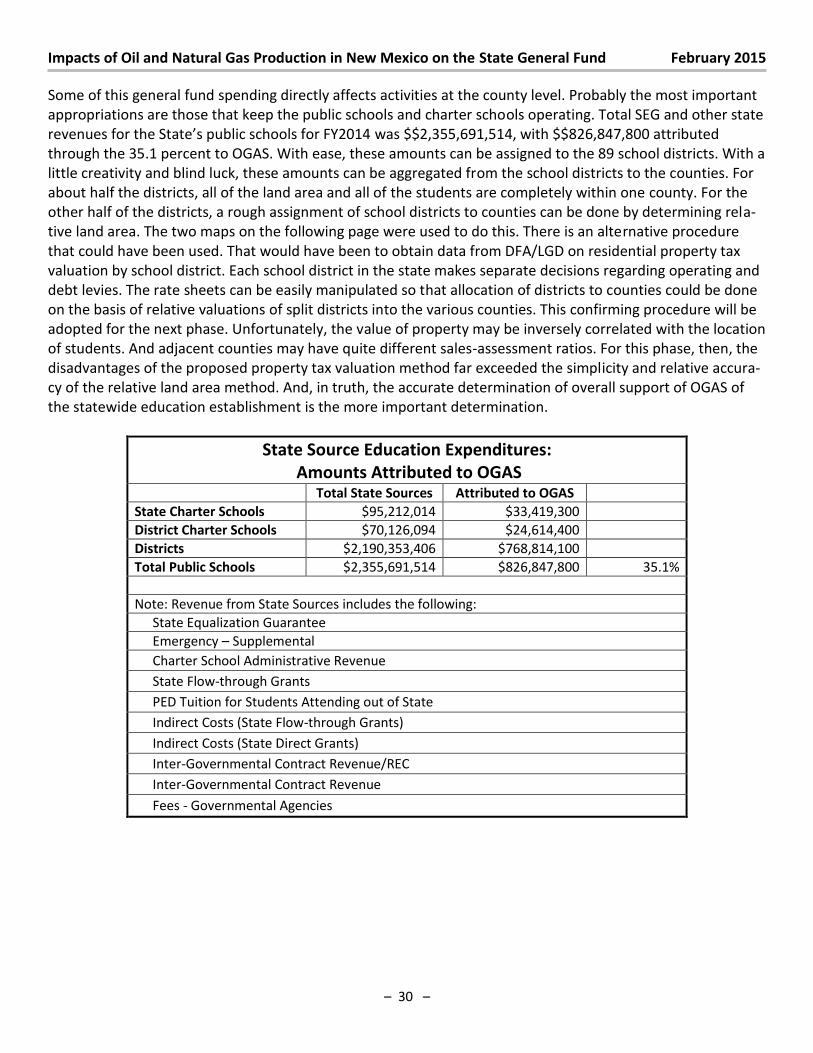

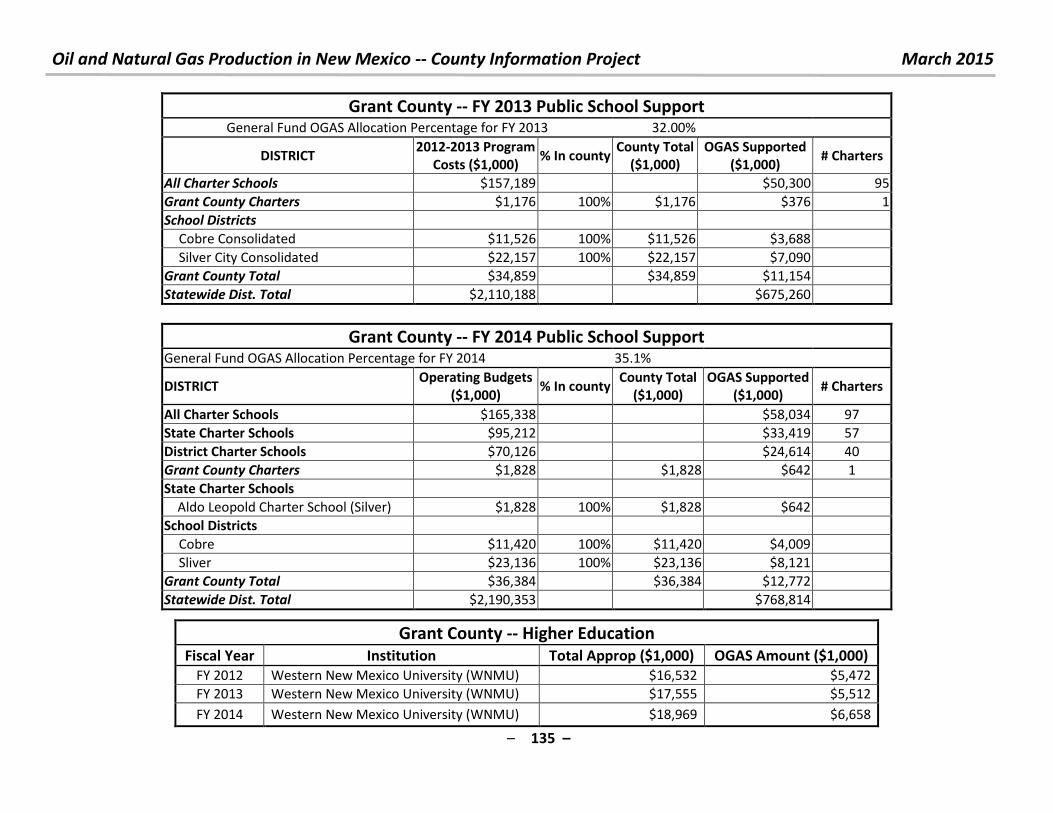

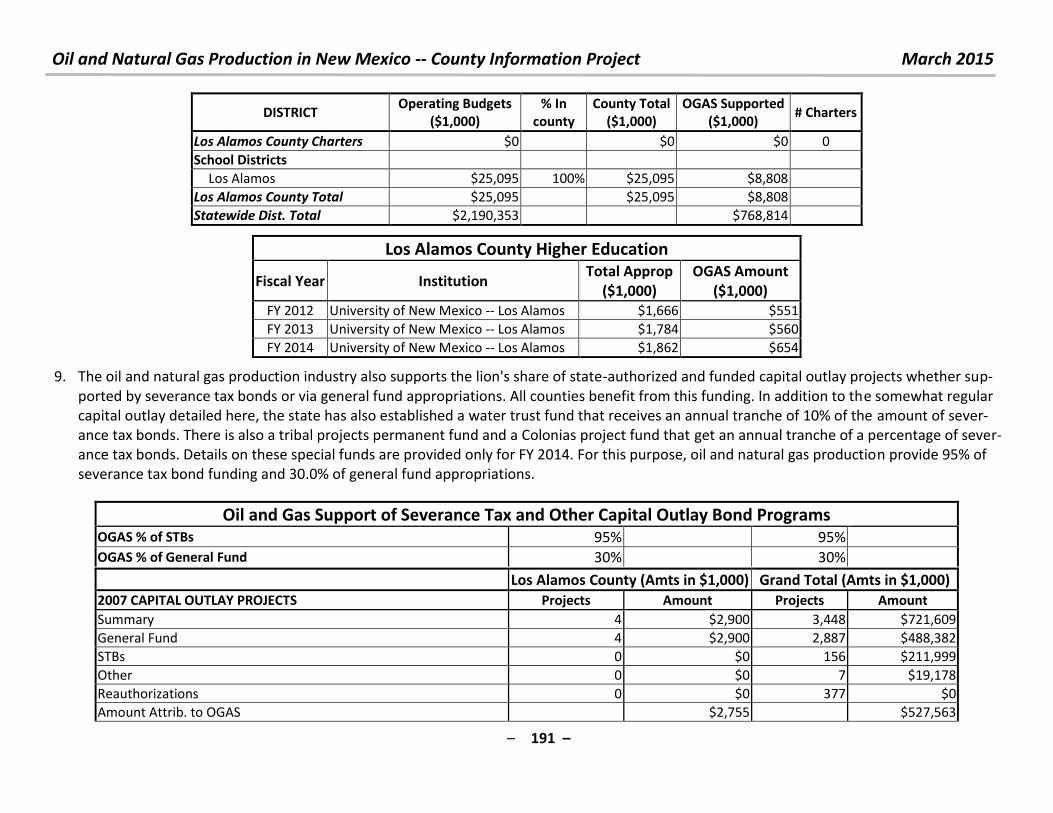

General Fund School Support to 89 local school districts

For FY 204, $2,355,691,514 for all state-supported programs, of

which $826,847,800, or 35.1% from OGAS. For FY 2013, $2,110,187,814 for only the state equalization guaran-

tee, of which $664,709,160 or 31.5% from OGAS

General Fund Higher Education Funding (35.1% for FY14; 31.5% for

FY13)

For FY 14, $734,795,530.7 total, of which $263,056,800 is attributed

to OGAS production.

For FY13 $723,167,619.0 total, of which $227,797,800 is attributed

to OGAS production.

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

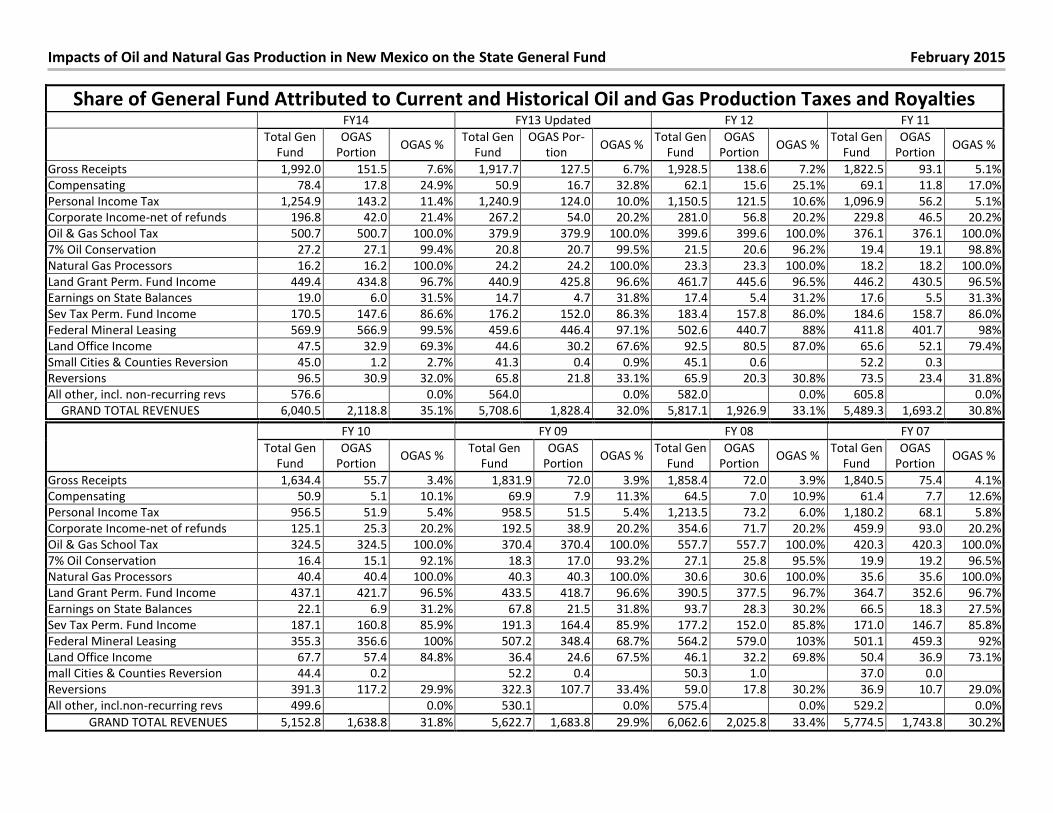

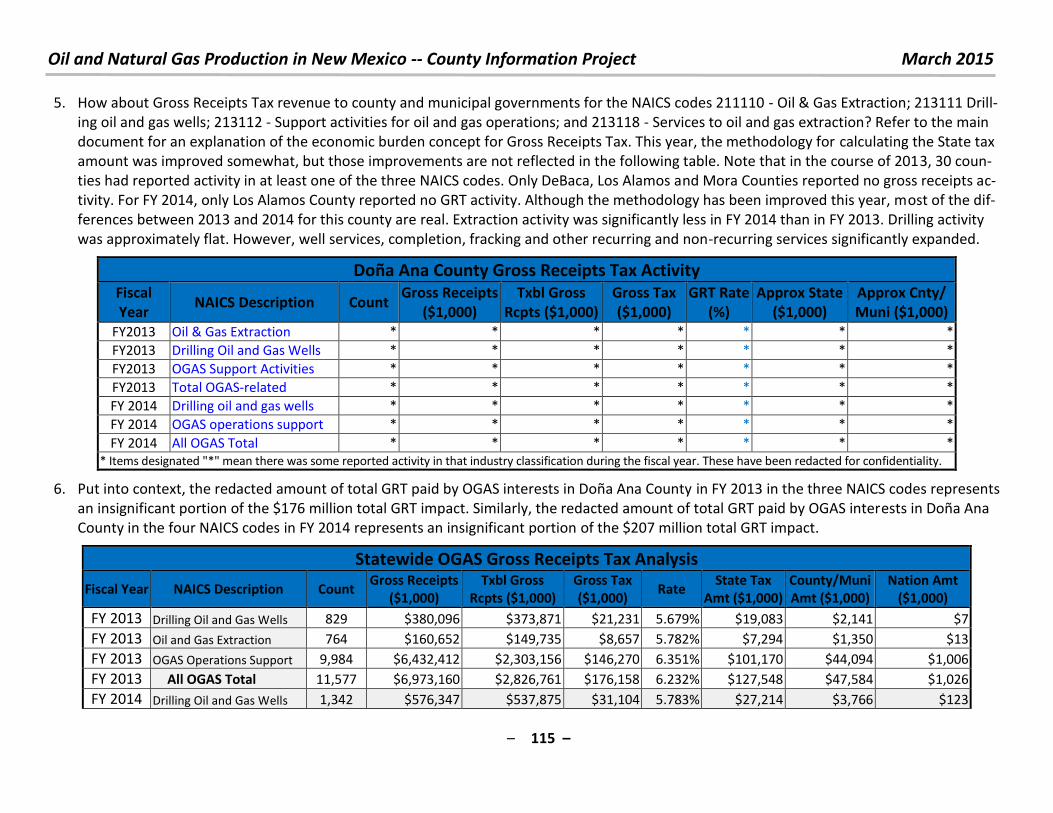

Share of General Fund Attributed to Current and Historical Oil and Gas Production Taxes and Royalties FY14 FY13 Updated FY 12 FY 11

Total Gen

Fund

OGAS

Portion OGAS %

Total Gen

Fund

OGAS Por-

tion OGAS %

Total Gen

Fund

OGAS

Portion OGAS %

Total Gen

Fund

OGAS

Portion OGAS %

Gross Receipts 1,992.0 151.5 7.6% 1,917.7 127.5 6.7% 1,928.5 138.6 7.2% 1,822.5 93.1 5.1%

Compensating 78.4 17.8 24.9% 50.9 16.7 32.8% 62.1 15.6 25.1% 69.1 11.8 17.0%

Personal Income Tax 1,254.9 143.2 11.4% 1,240.9 124.0 10.0% 1,150.5 121.5 10.6% 1,096.9 56.2 5.1%

Corporate Income-net of refunds 196.8 42.0 21.4% 267.2 54.0 20.2% 281.0 56.8 20.2% 229.8 46.5 20.2%

Oil & Gas School Tax 500.7 500.7 100.0% 379.9 379.9 100.0% 399.6 399.6 100.0% 376.1 376.1 100.0%

7% Oil Conservation 27.2 27.1 99.4% 20.8 20.7 99.5% 21.5 20.6 96.2% 19.4 19.1 98.8%

Natural Gas Processors 16.2 16.2 100.0% 24.2 24.2 100.0% 23.3 23.3 100.0% 18.2 18.2 100.0%

Land Grant Perm. Fund Income 449.4 434.8 96.7% 440.9 425.8 96.6% 461.7 445.6 96.5% 446.2 430.5 96.5%

Earnings on State Balances 19.0 6.0 31.5% 14.7 4.7 31.8% 17.4 5.4 31.2% 17.6 5.5 31.3%

Sev Tax Perm. Fund Income 170.5 147.6 86.6% 176.2 152.0 86.3% 183.4 157.8 86.0% 184.6 158.7 86.0%

Federal Mineral Leasing 569.9 566.9 99.5% 459.6 446.4 97.1% 502.6 440.7 88% 411.8 401.7 98%

Land Office Income 47.5 32.9 69.3% 44.6 30.2 67.6% 92.5 80.5 87.0% 65.6 52.1 79.4%

Small Cities & Counties Reversion 45.0 1.2 2.7% 41.3 0.4 0.9% 45.1 0.6 52.2 0.3

Reversions 96.5 30.9 32.0% 65.8 21.8 33.1% 65.9 20.3 30.8% 73.5 23.4 31.8%

All other, incl. non-recurring revs 576.6

0.0% 564.0

0.0% 582.0

0.0% 605.8

0.0%

GRAND TOTAL REVENUES 6,040.5 2,118.8 35.1% 5,708.6 1,828.4 32.0% 5,817.1 1,926.9 33.1% 5,489.3 1,693.2 30.8% FY 10 FY 09 FY 08 FY 07

Total Gen

Fund

OGAS

Portion OGAS %

Total Gen

Fund

OGAS

Portion OGAS %

Total Gen

Fund

OGAS

Portion OGAS %

Total Gen

Fund

OGAS

Portion OGAS %

Gross Receipts 1,634.4 55.7 3.4% 1,831.9 72.0 3.9% 1,858.4 72.0 3.9% 1,840.5 75.4 4.1%

Compensating 50.9 5.1 10.1% 69.9 7.9 11.3% 64.5 7.0 10.9% 61.4 7.7 12.6%

Personal Income Tax 956.5 51.9 5.4% 958.5 51.5 5.4% 1,213.5 73.2 6.0% 1,180.2 68.1 5.8%

Corporate Income-net of refunds 125.1 25.3 20.2% 192.5 38.9 20.2% 354.6 71.7 20.2% 459.9 93.0 20.2%

Oil & Gas School Tax 324.5 324.5 100.0% 370.4 370.4 100.0% 557.7 557.7 100.0% 420.3 420.3 100.0%

7% Oil Conservation 16.4 15.1 92.1% 18.3 17.0 93.2% 27.1 25.8 95.5% 19.9 19.2 96.5%

Natural Gas Processors 40.4 40.4 100.0% 40.3 40.3 100.0% 30.6 30.6 100.0% 35.6 35.6 100.0%

Land Grant Perm. Fund Income 437.1 421.7 96.5% 433.5 418.7 96.6% 390.5 377.5 96.7% 364.7 352.6 96.7%

Earnings on State Balances 22.1 6.9 31.2% 67.8 21.5 31.8% 93.7 28.3 30.2% 66.5 18.3 27.5%

Sev Tax Perm. Fund Income 187.1 160.8 85.9% 191.3 164.4 85.9% 177.2 152.0 85.8% 171.0 146.7 85.8%

Federal Mineral Leasing 355.3 356.6 100% 507.2 348.4 68.7% 564.2 579.0 103% 501.1 459.3 92%

Land Office Income 67.7 57.4 84.8% 36.4 24.6 67.5% 46.1 32.2 69.8% 50.4 36.9 73.1%

mall Cities & Counties Reversion 44.4 0.2 52.2 0.4 50.3 1.0 37.0 0.0

Reversions 391.3 117.2 29.9% 322.3 107.7 33.4% 59.0 17.8 30.2% 36.9 10.7 29.0%

All other, incl.non-recurring revs 499.6

0.0% 530.1

0.0% 575.4

0.0% 529.2

0.0%

GRAND TOTAL REVENUES 5,152.8 1,638.8 31.8% 5,622.7 1,683.8 29.9% 6,062.6 2,025.8 33.4% 5,774.5 1,743.8 30.2%

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 1 –

Impacts of Oil and Natural Gas Production in New Mexico on the

State General Fund

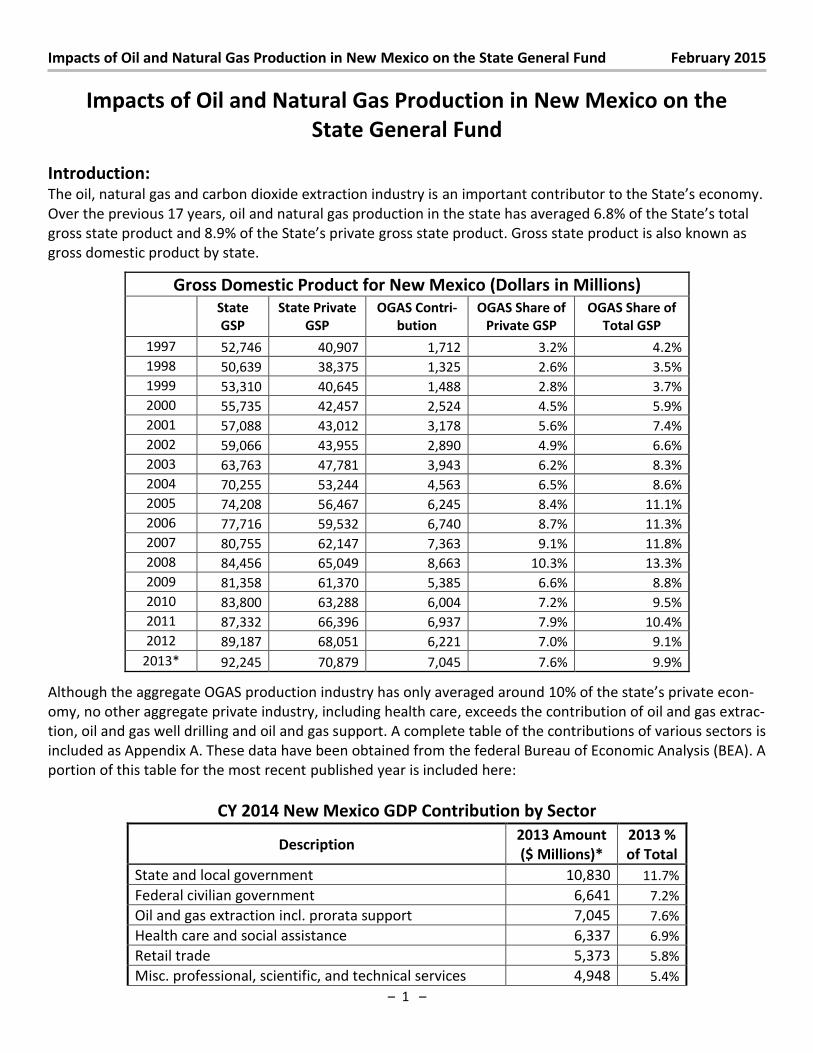

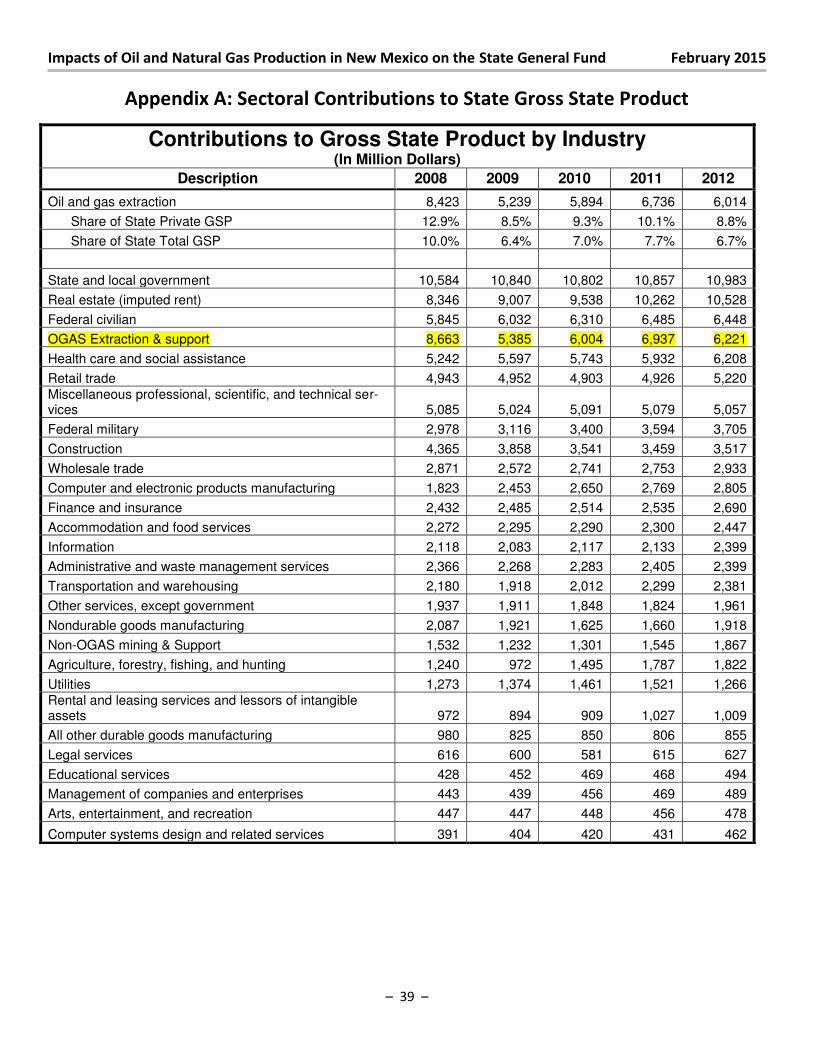

Introduction: The oil, natural gas and carbon dioxide extraction industry is an important contributor to the “tate’s e o o .

Over the previous 17 years, oil and natural gas p odu tio i the state has a e aged . % of the “tate’s total gross state product a d . % of the “tate’s p i ate gross state product. Gross state product is also known as

gross domestic product by state.

Gross Domestic Product for New Mexico (Dollars in Millions)

State

GSP

State Private

GSP

OGAS Contri-

bution

OGAS Share of

Private GSP

OGAS Share of

Total GSP

1997 52,746 40,907 1,712 3.2% 4.2%

1998 50,639 38,375 1,325 2.6% 3.5%

1999 53,310 40,645 1,488 2.8% 3.7%

2000 55,735 42,457 2,524 4.5% 5.9%

2001 57,088 43,012 3,178 5.6% 7.4%

2002 59,066 43,955 2,890 4.9% 6.6%

2003 63,763 47,781 3,943 6.2% 8.3%

2004 70,255 53,244 4,563 6.5% 8.6%

2005 74,208 56,467 6,245 8.4% 11.1%

2006 77,716 59,532 6,740 8.7% 11.3%

2007 80,755 62,147 7,363 9.1% 11.8%

2008 84,456 65,049 8,663 10.3% 13.3%

2009 81,358 61,370 5,385 6.6% 8.8%

2010 83,800 63,288 6,004 7.2% 9.5%

2011 87,332 66,396 6,937 7.9% 10.4%

2012 89,187 68,051 6,221 7.0% 9.1%

2013* 92,245 70,879 7,045 7.6% 9.9% Although the aggregate OGAS production industry has only averaged around % of the state’s p i ate e on-

omy, no other aggregate private industry, including health care, exceeds the contribution of oil and gas extrac-

tion, oil and gas well drilling and oil and gas support. A complete table of the contributions of various sectors is

included as Appendix A. These data have been obtained from the federal Bureau of Economic Analysis (BEA). A

portion of this table for the most recent published year is included here:

CY 2014 New Mexico GDP Contribution by Sector

Description 2013 Amount

($ Millions)*

2013 %

of Total

State and local government 10,830 11.7%

Federal civilian government 6,641 7.2%

Oil and gas extraction incl. prorata support 7,045 7.6%

Health care and social assistance 6,337 6.9%

Retail trade 5,373 5.8%

Misc. professional, scientific, and technical services 4,948 5.4%

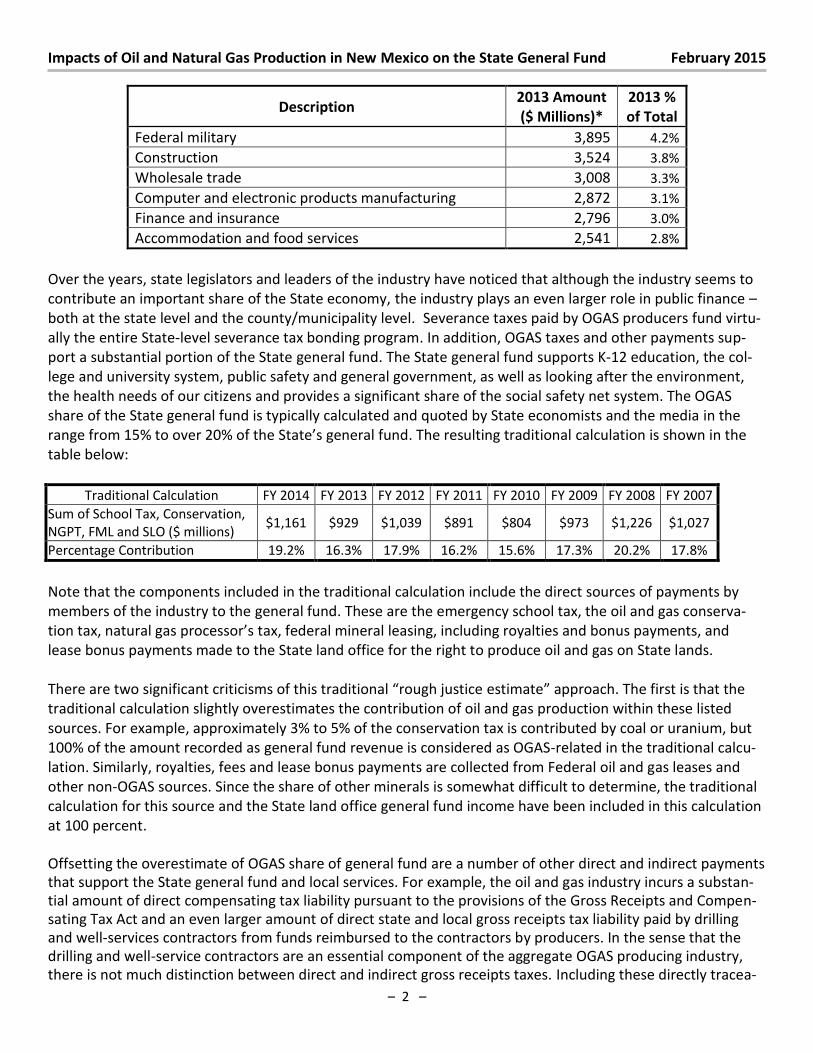

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 2 –

Description 2013 Amount

($ Millions)*

2013 %

of Total

Federal military 3,895 4.2%

Construction 3,524 3.8%

Wholesale trade 3,008 3.3%

Computer and electronic products manufacturing 2,872 3.1%

Finance and insurance 2,796 3.0%

Accommodation and food services 2,541 2.8%

Over the years, state legislators and leaders of the industry have noticed that although the industry seems to

contribute an important share of the State economy, the industry plays an even larger role in public finance –

both at the state level and the county/municipality level. Severance taxes paid by OGAS producers fund virtu-

ally the entire State-level severance tax bonding program. In addition, OGAS taxes and other payments sup-

port a substantial portion of the State general fund. The State general fund supports K-12 education, the col-

lege and university system, public safety and general government, as well as looking after the environment,

the health needs of our citizens and provides a significant share of the social safety net system. The OGAS

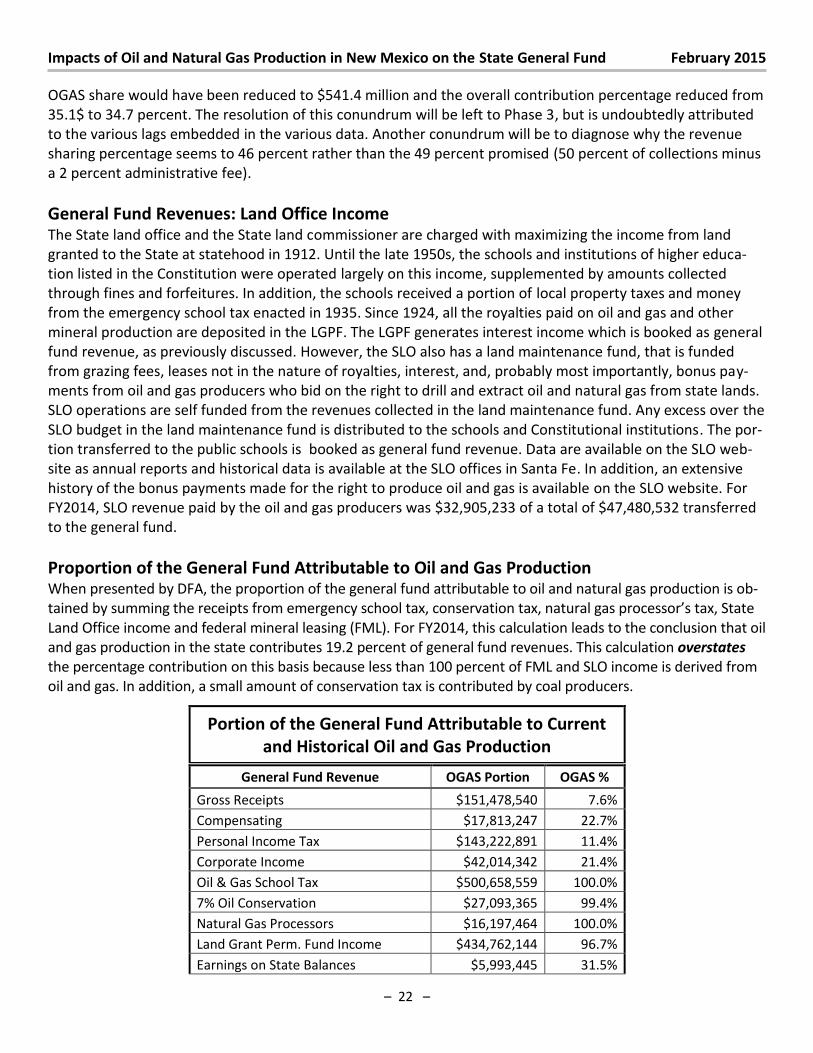

share of the State general fund is typically calculated and quoted by State economists and the media in the

range from 15% to over 20% of the State’s general fund. The resulting traditional calculation is shown in the

table below:

Traditional Calculation FY 2014 FY 2013 FY 2012 FY 2011 FY 2010 FY 2009 FY 2008 FY 2007

Sum of School Tax, Conservation,

NGPT, FML and SLO ($ millions) $1,161 $929 $1,039 $891 $804 $973 $1,226 $1,027

Percentage Contribution 19.2% 16.3% 17.9% 16.2% 15.6% 17.3% 20.2% 17.8%

Note that the components included in the traditional calculation include the direct sources of payments by

members of the industry to the general fund. These are the emergency school tax, the oil and gas conserva-

tion tax, natural gas p o esso ’s tax, federal mineral leasing, including royalties and bonus payments, and

lease bonus payments made to the State land office for the right to produce oil and gas on State lands.

There are two significa t iti is s of this t aditio al ough justi e estimate app oa h. The fi st is that the traditional calculation slightly overestimates the contribution of oil and gas production within these listed

sources. For example, approximately 3% to 5% of the conservation tax is contributed by coal or uranium, but

100% of the amount recorded as general fund revenue is considered as OGAS-related in the traditional calcu-

lation. Similarly, royalties, fees and lease bonus payments are collected from Federal oil and gas leases and

other non-OGAS sources. Since the share of other minerals is somewhat difficult to determine, the traditional

calculation for this source and the State land office general fund income have been included in this calculation

at 100 percent.

Offsetting the overestimate of OGAS share of general fund are a number of other direct and indirect payments

that support the State general fund and local services. For example, the oil and gas industry incurs a substan-

tial amount of direct compensating tax liability pursuant to the provisions of the Gross Receipts and Compen-

sating Tax Act and an even larger amount of direct state and local gross receipts tax liability paid by drilling

and well-services contractors from funds reimbursed to the contractors by producers. In the sense that the

drilling and well-service contractors are an essential component of the aggregate OGAS producing industry,

there is not much distinction between direct and indirect gross receipts taxes. Including these directly tracea-

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 3 –

ble tax payments made by the industry increases the estimated OGAS share of general fund by almost three

percentage points.

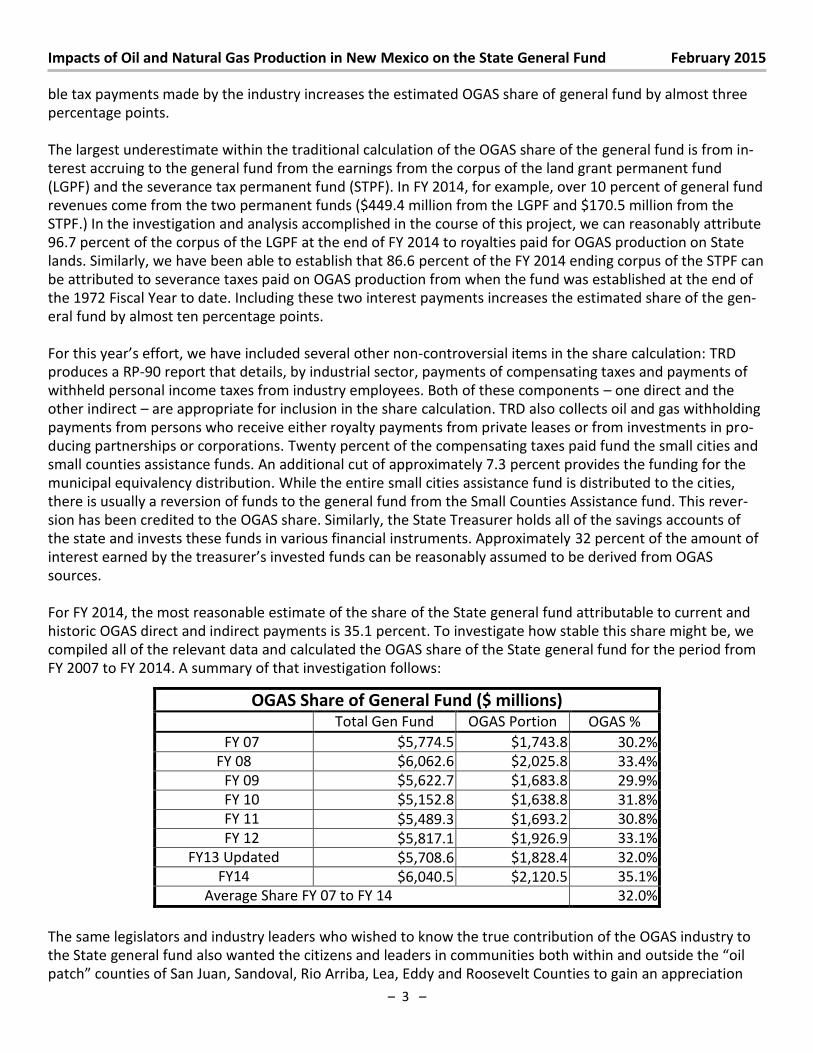

The largest underestimate within the traditional calculation of the OGAS share of the general fund is from in-

terest accruing to the general fund from the earnings from the corpus of the land grant permanent fund

(LGPF) and the severance tax permanent fund (STPF). In FY 2014, for example, over 10 percent of general fund

revenues come from the two permanent funds ($449.4 million from the LGPF and $170.5 million from the

STPF.) In the investigation and analysis accomplished in the course of this project, we can reasonably attribute

96.7 percent of the corpus of the LGPF at the end of FY 2014 to royalties paid for OGAS production on State

lands. Similarly, we have been able to establish that 86.6 percent of the FY 2014 ending corpus of the STPF can

be attributed to severance taxes paid on OGAS production from when the fund was established at the end of

the 1972 Fiscal Year to date. Including these two interest payments increases the estimated share of the gen-

eral fund by almost ten percentage points.

Fo this ea ’s effo t, e have included several other non-controversial items in the share calculation: TRD produces a RP-90 report that details, by industrial sector, payments of compensating taxes and payments of

withheld personal income taxes from industry employees. Both of these components – one direct and the

other indirect – are appropriate for inclusion in the share calculation. TRD also collects oil and gas withholding

payments from persons who receive either royalty payments from private leases or from investments in pro-

ducing partnerships or corporations. Twenty percent of the compensating taxes paid fund the small cities and

small counties assistance funds. An additional cut of approximately 7.3 percent provides the funding for the

municipal equivalency distribution. While the entire small cities assistance fund is distributed to the cities,

there is usually a reversion of funds to the general fund from the Small Counties Assistance fund. This rever-

sion has been credited to the OGAS share. Similarly, the State Treasurer holds all of the savings accounts of

the state and invests these funds in various financial instruments. Approximately 32 percent of the amount of

interest earned by the t easu e ’s i ested funds can be reasonably assumed to be derived from OGAS

sources.

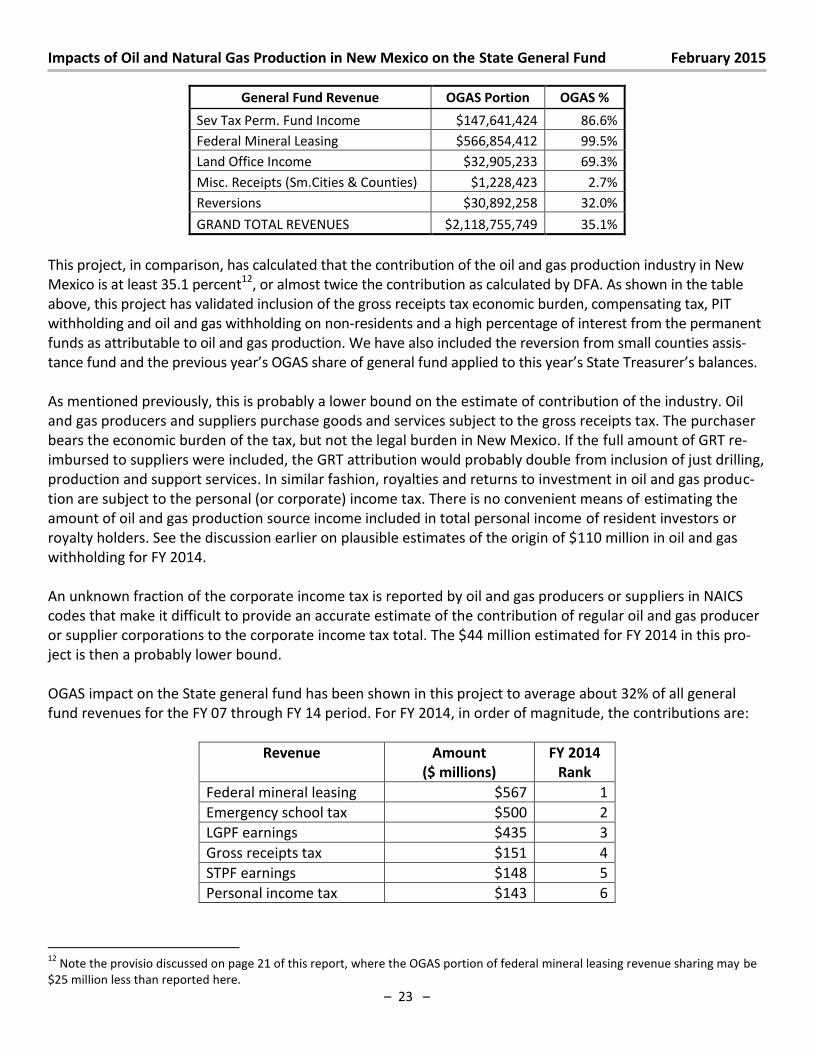

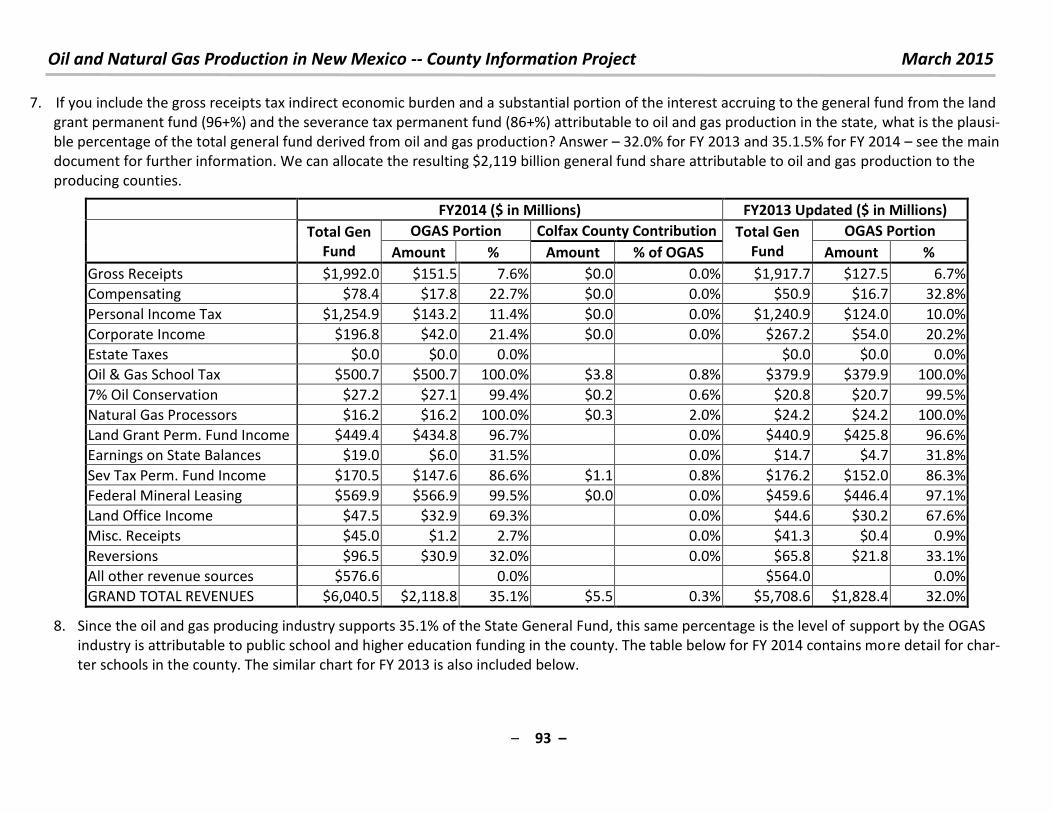

For FY 2014, the most reasonable estimate of the share of the State general fund attributable to current and

historic OGAS direct and indirect payments is 35.1 percent. To investigate how stable this share might be, we

compiled all of the relevant data and calculated the OGAS share of the State general fund for the period from

FY 2007 to FY 2014. A summary of that investigation follows:

OGAS Share of General Fund ($ millions)

Total Gen Fund OGAS Portion OGAS %

FY 07 $5,774.5 $1,743.8 30.2%

FY 08 $6,062.6 $2,025.8 33.4%

FY 09 $5,622.7 $1,683.8 29.9%

FY 10 $5,152.8 $1,638.8 31.8%

FY 11 $5,489.3 $1,693.2 30.8%

FY 12 $5,817.1 $1,926.9 33.1%

FY13 Updated $5,708.6 $1,828.4 32.0%

FY14 $6,040.5 $2,120.5 35.1%

Average Share FY 07 to FY 14 32.0%

The same legislators and industry leaders who wished to know the true contribution of the OGAS industry to

the State general fund also wanted the citizens and leaders in communities both within and outside the oil pat h ou ties of “a Jua , “a do al, Rio A i a, Lea, Edd a d Roose elt Cou ties to gai a app e iatio

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 4 –

that thei o u it as i the oil id ess. If a a e age of 32 percent of the State general fund can be

reasonably attributed to current and historical OGAS production in the State, it must follow logically that an

average of 32 percent of all state governmental services, 32 percent of K-12 public education and 32 percent

of the higher education funding fo ula suppo t of the “tate’s olleges a d u i e sities ust e fu ded current and historical oil and gas production in the state.

This is a somewhat controversial statement. According to one view, once general taxes, such as personal in-

come tax, corporate income tax or the gross receipts and compensating taxes leave the pockets of the taxpay-

ers, these taxpayers lose all control or ownership of the tax payments. However, the des iptio of ge e al ta es e tai l does ot fit as a des iptio of p odu tio ta es su h as the atu al gas p o esso ’s ta , the severance tax or the emergency school tax. In addition, the atio et ee the i dust ’s pa ti ipatio i the “tate’s e o o oughl percent of the “tate’s p i ate e o o as easu ed G“P a d the oughl

percent share of the State general fund puts the industry in a special and unique position.

Another criticism leveled at the statement concerning contribution to the general fund is that it is alleged that OGAS production still bears a relatively low burden of taxes, compared to the value of product produced and

sold. Let us look at that contention for just the general fund and not consider the severance taxes that support

the “tate’s apital outlay program. The CY 2013 GSP for New Mexico is about $92 billion. The general fund for

FY 2014 was about $6 billion. Thus, each $100 of GSP should contribute about $6.50 in general taxes and other

payments to the general fund.

For CY 2013, BEA has determined that the oil and gas industry produces about $7 billion in value-added on

about $15 billion in total production value. Applying these same ratios to FY 2014 production, the $7.8 billion

in OGAS industry contributions for FY 2014 should account for about $500 million in general fund taxes and

other revenues. Instead, this project indicates that the industry contributes on the order of $2.1 billion to the

general fund or about four times the i dust ’s fai sha e.

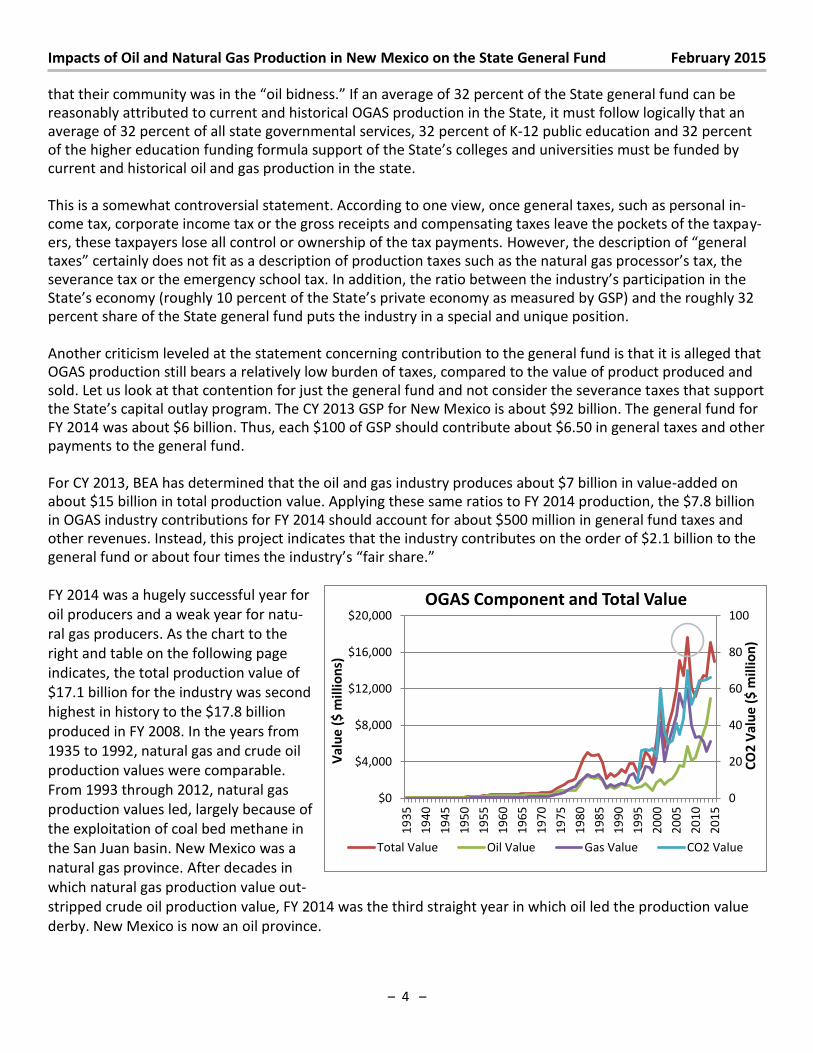

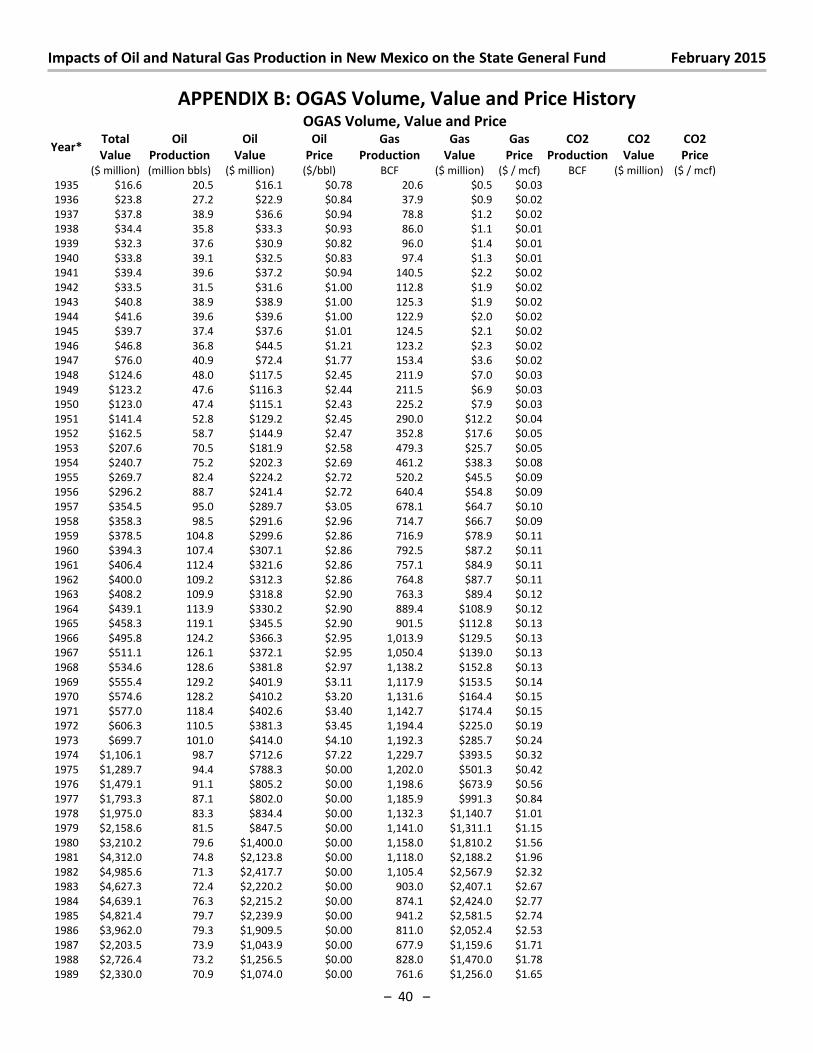

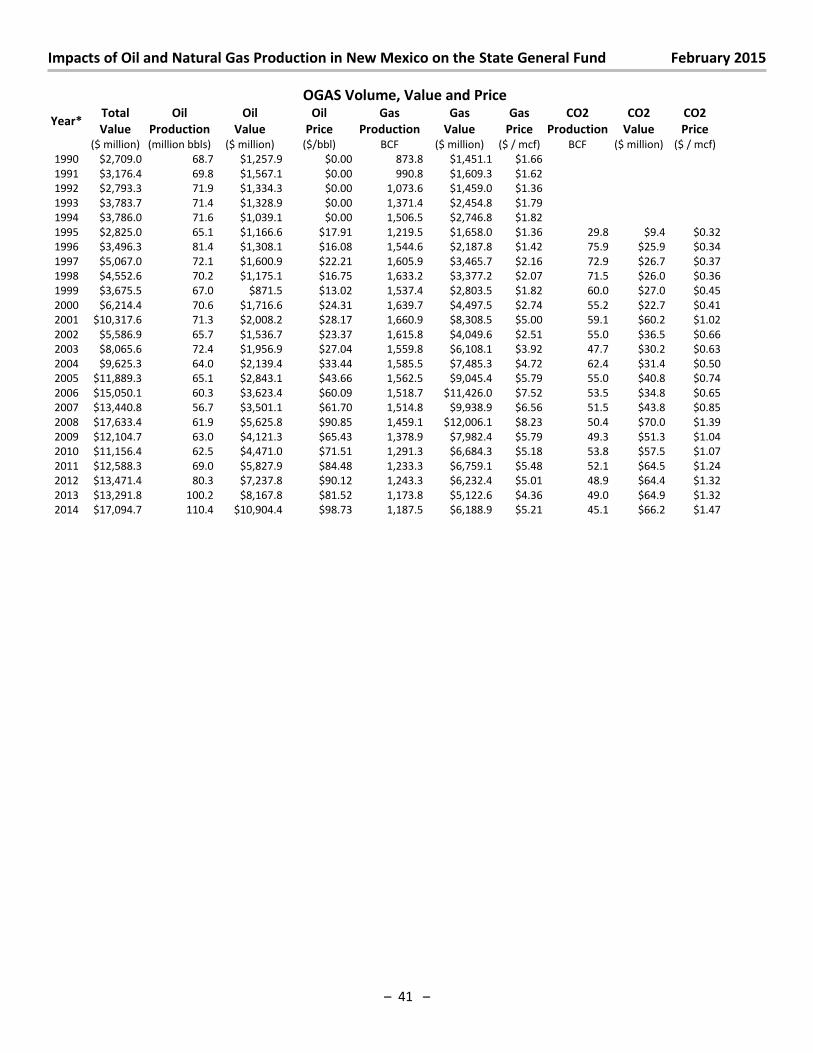

FY 2014 was a hugely successful year for

oil producers and a weak year for natu-

ral gas producers. As the chart to the

right and table on the following page

indicates, the total production value of

$17.1 billion for the industry was second

highest in history to the $17.8 billion

produced in FY 2008. In the years from

1935 to 1992, natural gas and crude oil

production values were comparable.

From 1993 through 2012, natural gas

production values led, largely because of

the exploitation of coal bed methane in

the San Juan basin. New Mexico was a

natural gas province. After decades in

which natural gas production value out-

stripped crude oil production value, FY 2014 was the third straight year in which oil led the production value

derby. New Mexico is now an oil province.

0

20

40

60

80

100

$0

$4,000

$8,000

$12,000

$16,000

$20,000

19

35

19

40

19

45

19

50

19

55

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15

CO

2 V

alu

e (

$ m

illi

on

)

Va

lue

($

mil

lio

ns)

OGAS Component and Total Value

Total Value Oil Value Gas Value CO2 Value

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 5 –

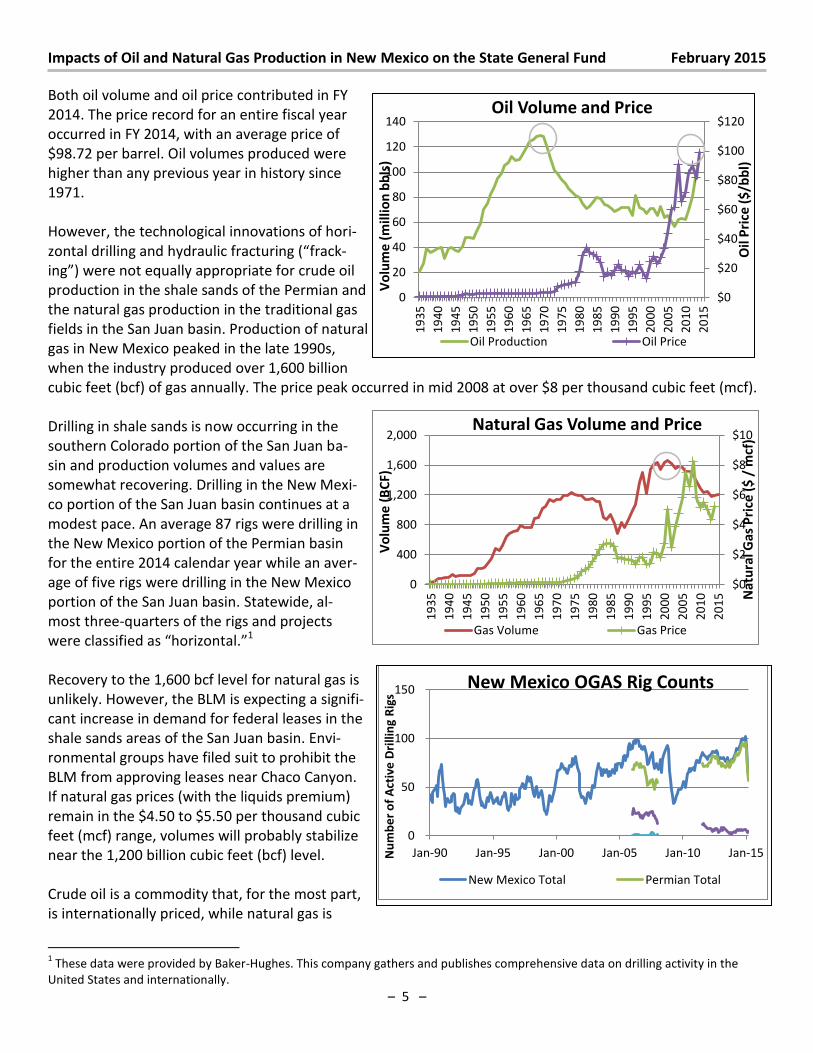

Both oil volume and oil price contributed in FY

2014. The price record for an entire fiscal year

occurred in FY 2014, with an average price of

$98.72 per barrel. Oil volumes produced were

higher than any previous year in history since

1971.

However, the technological innovations of hori-

zontal drilling and h d auli f a tu i g frack-

ing were not equally appropriate for crude oil

production in the shale sands of the Permian and

the natural gas production in the traditional gas

fields in the San Juan basin. Production of natural

gas in New Mexico peaked in the late 1990s,

when the industry produced over 1,600 billion

cubic feet (bcf) of gas annually. The price peak occurred in mid 2008 at over $8 per thousand cubic feet (mcf).

Drilling in shale sands is now occurring in the

southern Colorado portion of the San Juan ba-

sin and production volumes and values are

somewhat recovering. Drilling in the New Mexi-

co portion of the San Juan basin continues at a

modest pace. An average 87 rigs were drilling in

the New Mexico portion of the Permian basin

for the entire 2014 calendar year while an aver-

age of five rigs were drilling in the New Mexico

portion of the San Juan basin. Statewide, al-

most three-quarters of the rigs and projects

e e lassified as ho izo tal. 1

Recovery to the 1,600 bcf level for natural gas is

unlikely. However, the BLM is expecting a signifi-

cant increase in demand for federal leases in the

shale sands areas of the San Juan basin. Envi-

ronmental groups have filed suit to prohibit the

BLM from approving leases near Chaco Canyon.

If natural gas prices (with the liquids premium)

remain in the $4.50 to $5.50 per thousand cubic

feet (mcf) range, volumes will probably stabilize

near the 1,200 billion cubic feet (bcf) level.

Crude oil is a commodity that, for the most part,

is internationally priced, while natural gas is

1 These data were provided by Baker-Hughes. This company gathers and publishes comprehensive data on drilling activity in the

United States and internationally.

$0

$2

$4

$6

$8

$10

0

400

800

1,200

1,600

2,0001

93

5

19

40

19

45

19

50

19

55

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15 N

atu

ral

Ga

s P

rice

($

/ m

cf)

Vo

lum

e (

BC

F)

Natural Gas Volume and Price

Gas Volume Gas Price

$0

$20

$40

$60

$80

$100

$120

0

20

40

60

80

100

120

140

19

35

19

40

19

45

19

50

19

55

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15

Oil

Pri

ce (

$/b

bl)

Vo

lum

e (

mil

lio

n b

bls

)

Oil Volume and Price

Oil Production Oil Price

0

50

100

150

Jan-90 Jan-95 Jan-00 Jan-05 Jan-10 Jan-15Nu

mb

er

of

Act

ive

Dri

llin

g R

igs

New Mexico OGAS Rig Counts

New Mexico Total Permian Total

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 6 –

largely regionally or nationally priced. While there is some substitution between natural gas and crude oil, the

linkage is weak2. However, there is certainly predictability year-over-year in other aspects of production statis-

tics, such as deductions ratios or location of production. The following table, showing some aspects of produc-

tion for the most recent five-year period, is interesting.

As natural gas production on federal lands has declined in proportion, production on state lands has taken up

the slack. With the advent of horizontal drilling and fracking in oil production, the federal lands share of oil

production has increased from 48 percent of oil production to 52 percent. At the same time, production on

private lands has declined from 17 percent to 11 percent or 12 percent.

While oil production value increased from $4.5 billion in FY 2010 to $10.9 billion in FY 2014, natural gas pro-

duction softened slightly, as production value dipped to $5.1 billion in FY 2013 then recovered somewhat to

$6.1 billion in FY 2014.

Background and History of the Project: As mentioned above, this research study has been partially funded by the New Mexico Oil and Gas Association

(NMOGA). The principal investigator, Laird Graeser, has used this funding to work toward assembling the data

f o hi h he ould pu lish a ook oughl e titled, A Histo of Pu li Fi a e i Ne Me i o. 3 During the

2 There is substitution between crude oil and components of natural gas such as ethane as a a substitute for naphtha as a feedstock

for plastics manufacture. 3 There is virtually no quantitative history of taxes or spending in the Spanish Colonial period or the Mexican Colonial period alt-

hough there is some descriptive material that can be used. During the territorial period, there is a good record of enacted revenue

and budget laws, including a record of abuses and failures, but little quantitative data. Beginning roughly with the Ferguson Act in

1898, however, two entities began recording data regarding budgets and revenue collections. The State land office, primarily under

the leadership of Commissioner Ray Powell, scanned an almost complete set of annual reports of the Commissioners and made

All Counties Production Statistics

Fiscal

Year Product

Volume

(Million mcf

or bbls)

Value

($ millions) Price

Deductions

%

Production by Land Type

% Federal % Indian % Private % State

FY 2010 GAS 1,274.6 $6,614.7 $5.19 24.0% 65% 3% 15% 17%

FY 2011 GAS 1,215.5 $6,693.9 $5.51 23.3% 65% 4% 14% 17%

FY 2012 GAS 1,223.1 $6,180.4 $5.05 24.5% 64% 5% 14% 18%

FY 2013 GAS 1,155.0 $5,063.6 $4.38 23.5% 63% 4% 15% 19%

FY 2014 GAS 1,168.7 $6,115.0 $5.23 23.0% 62% 4% 14% 20%

FY 2010 OIL 62.43 $4,469.0 $71.59 10.6% 48% 1% 17% 35%

FY 2011 OIL 68.97 $5,824.5 $84.45 10.7% 49% 1% 14% 36%

FY 2012 OIL 80.31 $7,239.7 $90.15 10.7% 50% 1% 13% 37%

FY 2013 OIL 100.23 $8,169.0 $81.50 11.0% 50% 0% 11% 39%

FY 2014 OIL 110.46 $10,905.3 $98.72 11.6% 52% 1% 12% 36%

FY 2010 CO2 72.43 $74.4 $1.03 26.3% 7% 0% 53% 40%

FY 2011 CO2 71.49 $90.1 $1.26 22.2% 8% 0% 54% 38%

FY 2012 CO2 66.99 $89.3 $1.33 23.3% 7% 0% 55% 38%

FY 2013 CO2 68.69 $91.2 $1.33 26.2% 6% 0% 57% 37%

FY 2014 CO2 64.33 $95.3 $1.48 23.9% 6% 0% 57% 37%

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 7 –

years that Graeser spent at Taxation and Revenue Department and then at the Department of Finance and

Administration he took several opportunities to capture and save quantitative data on revenue collections and

corresponding expenditures. These antique data need a medium for archiving. The offer of some funding cou-

pled with the opportunity to extend knowledge was

irresistible.

In response to the enquiry and offer, NMTRI and the

PI prepared a proposal that included the following

elements:

The study would be divided into phases, with

each phase extending the analysis into different

areas. The results of each phase would be avail-

able concurrent with each annual legislative ses-

sion and each phase would update the previous

phase’s data gathe i g a d a al sis. It was ex-

pected that there would be new areas to ex-

plore after the initial phase for approximately

three or four phases in total.

The phase 1 study would determine the plausi-

ble total contribution of the industry to the

State general fund for FY 2013 that would in-

clude not just the traditional reckoning of emer-

ge s hool ta , atu al gas p o esso ’s ta , the

conservation tax and federal royalty sharing, but

other revenues contributed by the industry. The

most important non-traditional inclusion in this

reckoning is interest paid to the general fund

from the Land Grant and the Severance Tax

Permanent Funds. Also to be included in the

phase 1 study would be the economic burden of

the gross receipts tax paid by OGAS producers

for oil and gas support services, drilling and pe-

troleum production. Finally, working with Taxa-

tion and Revenue Department, the study would

also determine the OGAS contribution to per-

sonal income tax withholding, oil and gas with-

holding and compensating tax.

The phase 1 study would then determine, on a county-by-county basis, the contribution of OGAS to each

county – directly, in terms of the ad valorem production and production equipment taxes in the producing

counties, and indirectly, in terms of the amount of general fund support of K through 12 public schools,

charter schools and higher education. If time allowed, the phase 1 study would determine the contribution

of the industry to capital outlay, whether the local capital projects in each county were funded via general

these scans available to the public. The records of the Territorial and State Treasurers are similarly available from about 1895 for-

ward.

Project Background In September, 2013, the New Mexico Oil and Gas

Association (NMOGA) contacted the New Mexico

Tax Research Institute (NMTRI) to assess interest in

having NMTRI research, analyze and report on the

direct and indirect economic impacts of the Oil and

Gas exploration, drilling and production industry in

New Mexico. The query and implicit RFP fit nicely

i to a eti e e t p oje t of NMTRI’s p i ipal investigator, Laird Graeser. This project is to re-

search and write a definitive history of revenue and

public finance in New Mexico starting from the first

property tax imposed in the State to fund free pub-

lic education. This is an ongoing story. However,

NMOGA offered financial support to NMTRI and the

PI to investigate and document the portions of the

overall story having to do with oil and gas produc-

tion in the state, the role of the oil and natural gas

production industries o the state’s apital outla through the severance tax bond fund and the pro-

portion of the general fund that the oil and natural

gas i dust a plausi l lai to o . That is, what proportion or percentage of the general fund,

which is used to fund public school education, high-

er education, Medicaid and some other public wel-

fare programs, general government, environmental

protection, tourism support and promotion and

economic development efforts , will reasonable

people, when presented with unbiased analysis and

data, understand is attributable to current or his-

torical taxes, royalties and other money paid by the

oil and gas production industry in New Mexico?

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 8 –

fund appropriations or Severance Tax Bonds. Thus, the phase 1 study would generate a partial economic

impact estimate for producing and non-producing Counties.

To ensure that the study would be independent and professional, NMOGA would fund a portion of the

research, analysis, documentation and report-writing, but not all. (Note, NMOGA funded approximately

1/3rd the cost of the phase 1 study reported last year and a somewhat greater share of the phase 2 study

reported here.) NMOGA would have the unlimited right to all data, data tables and would have the right to

republish any portions of the final report, but would not own the copyright.

To ensure preservation of all of the rare, antique data gathered in the course of the project, NMOGA

would provide a website or cloud location for the PI and NMTRI to mount a searchable database of all of

the data developed in the course of the study. (Note: while all of the data are available to the public, me-

dia and other researchers by request, we have been unable to provide easy Internet access. This will be a

major goal of phase 3 of the study.

The most important tasks in phase 2 of the study would be to reconcile the various data sources to im-

prove both the LGPF and the STPF models. These reconciliations will not materially affect the estimate of

OGAS attribution to the general fund performed in phase 1, but will provide an increased level of confi-

dence in the models.

What was originally scheduled for Phase 2 was to extend the study to other general fund revenue sources

that can be attributed to OGAS. These could include motor vehicle excise tax and insurance premiums tax.

Via survey of the OGAS industry, we might be able to refine the CIT attribution and the compensating tax

and PIT withholding directly attributed to OGAS. The survey would also e te d the e o o i u de analysis for Gross Receipts Tax to all other categories of taxable purchases and extend the analysis to MVX

and insurance premiums tax. However, there were sufficient glitches in this phase 2 year that the originally

scheduled Phase 2 work has now become Phase 3 work.

Phase 3 will also extend the study to other general fund supported programs that can be assigned to

ou ties. These a eas ould i lude pu li s hool t a spo tatio , elo -the-li e s hool g a t p og a s, pre-K education funding, Medicaid funding, other state-funded income support, LICTR and elderly property

tax rebate. The linkages here between OGAS production and the expenditures are weaker than for the

linkages developed in Phases 1 and 2.

In phase 4 we will extend the analysis to some Other State Funds , including unemployment insurance

(direct and indirect) and the State road fund. In this phase, the full impact of the OGAS industry on all gov-

ernment funds will be determined. This oade s the assess e t of the i dust ’s itical importance as a

major source of funding for cities, counties, some Indian tribes or nations and many other activities of

state government.

In phase 4, as well, working with the Taxation and Revenue Department, we will attempt to assign person-

al income tax withholding and total personal income taxes paid by oil and gas industry employees to coun-

ties and refine the assumption that PIT withholding and oil and gas withholding are good surrogates for

net personal income taxes contributed by employees and contractors to the industry.

In phase 4, we might also be able to piggy-back on an NMSU IMPLAN study of direct, indirect and induced

employment effects of OGAS to claim a greater amount of PIT withholding than in Phases 1 and 2.

Accomplishing these various analytic tasks required unearthing and assembling a vast amount of data. In some

cases, the data were gathered from 1986-2001 when the PI was chief economist for the New Mexico Taxation

and Revenue Department (TRD) or from 2006-2010 when the PI was chief economist for the Department of

Finance and Administration (DFA). Other data were obtained from the Anderson School Library at UNM or the

Oil Recovery project at New Mexico Institute for Mining and Technology (NMIMT). Data for the land grant

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 9 –

permanent fund (LGPF) model were obtained directly from the State land office (SLO), where staff graciously

provided access to the entire series of annual reports of the State land commissioner. These data will be dis-

cussed later in the report as supporting the individual taxes and revenue sources contributing to the State

general fund, the severance tax bonding fund (STBF) and county-level capital outlay, operating and school

funding from the same revenue sources as the State general fund. These data will be made available to other

researchers through a mechanism to be developed.

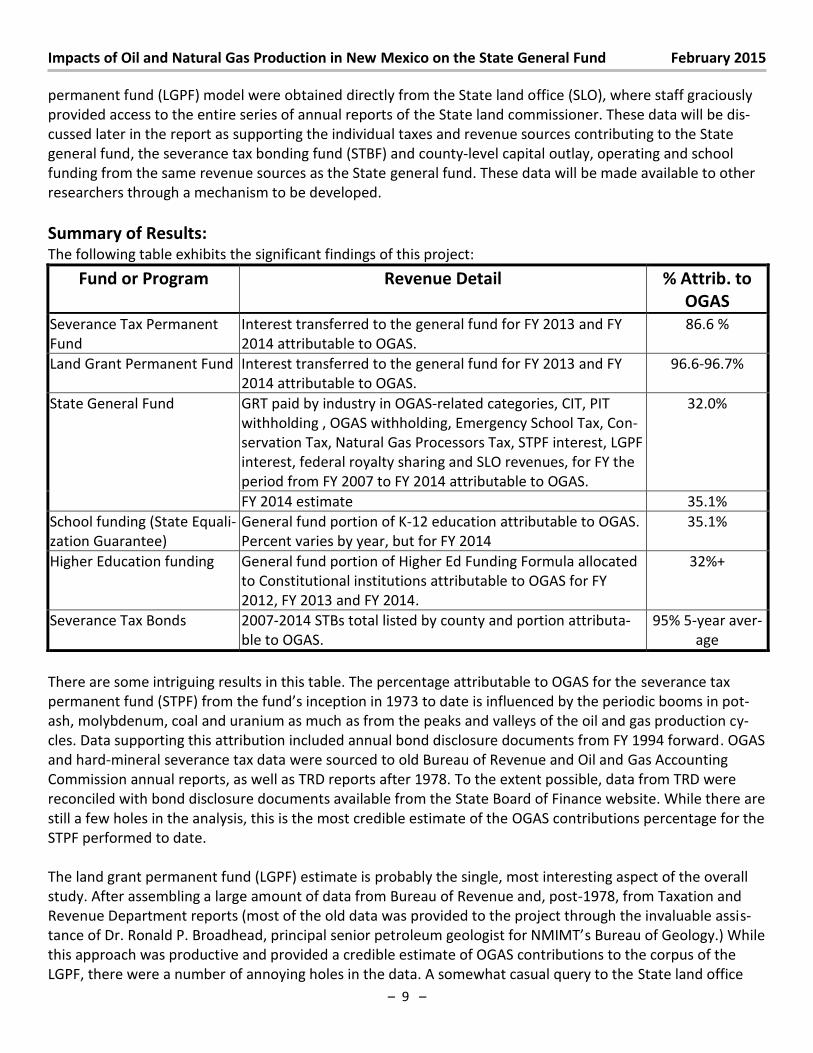

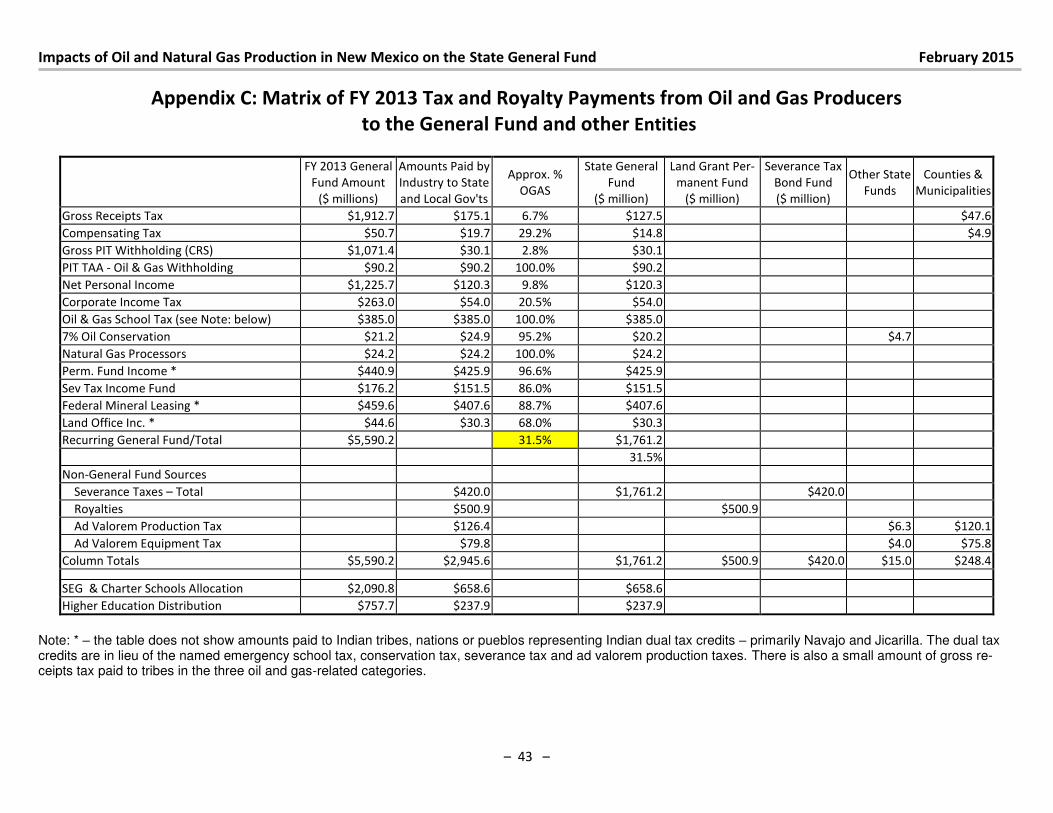

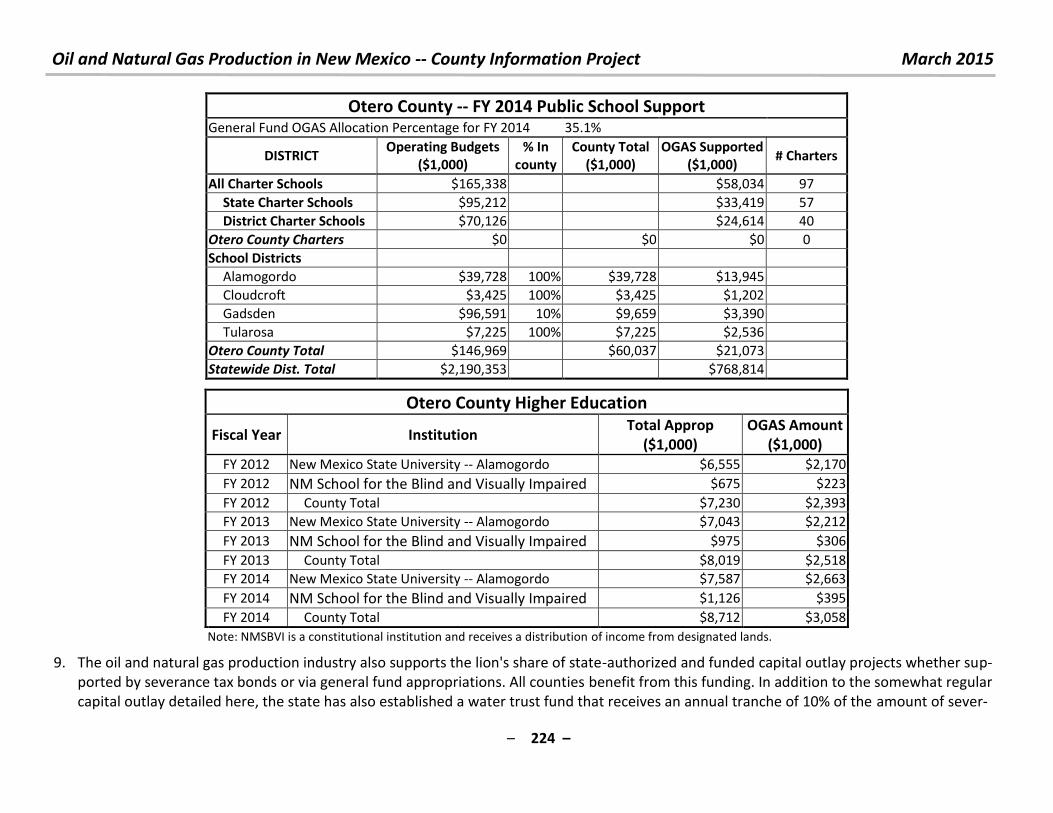

Summary of Results: The following table exhibits the significant findings of this project:

Fund or Program Revenue Detail % Attrib. to

OGAS

Severance Tax Permanent

Fund

Interest transferred to the general fund for FY 2013 and FY

2014 attributable to OGAS.

86.6 %

Land Grant Permanent Fund Interest transferred to the general fund for FY 2013 and FY

2014 attributable to OGAS.

96.6-96.7%

State General Fund GRT paid by industry in OGAS-related categories, CIT, PIT

withholding , OGAS withholding, Emergency School Tax, Con-

servation Tax, Natural Gas Processors Tax, STPF interest, LGPF

interest, federal royalty sharing and SLO revenues, for FY the

period from FY 2007 to FY 2014 attributable to OGAS.

32.0%

FY 2014 estimate 35.1%

School funding (State Equali-

zation Guarantee)

General fund portion of K-12 education attributable to OGAS.

Percent varies by year, but for FY 2014

35.1%

Higher Education funding General fund portion of Higher Ed Funding Formula allocated

to Constitutional institutions attributable to OGAS for FY

2012, FY 2013 and FY 2014.

32%+

Severance Tax Bonds 2007-2014 STBs total listed by county and portion attributa-

ble to OGAS.

95% 5-year aver-

age

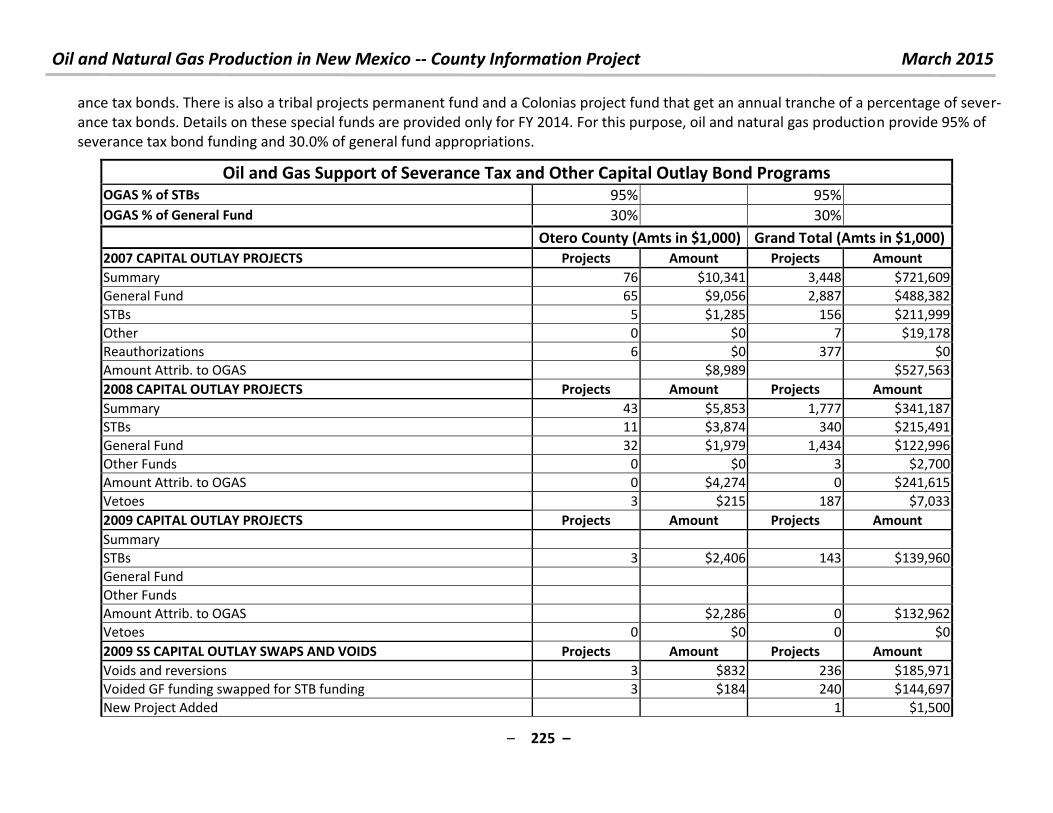

There are some intriguing results in this table. The percentage attributable to OGAS for the severance tax

permanent fund (STPF) f o the fu d’s i eptio i 3 to date is influenced by the periodic booms in pot-

ash, molybdenum, coal and uranium as much as from the peaks and valleys of the oil and gas production cy-

cles. Data supporting this attribution included annual bond disclosure documents from FY 1994 forward. OGAS

and hard-mineral severance tax data were sourced to old Bureau of Revenue and Oil and Gas Accounting

Commission annual reports, as well as TRD reports after 1978. To the extent possible, data from TRD were

reconciled with bond disclosure documents available from the State Board of Finance website. While there are

still a few holes in the analysis, this is the most credible estimate of the OGAS contributions percentage for the

STPF performed to date.

The land grant permanent fund (LGPF) estimate is probably the single, most interesting aspect of the overall

study. After assembling a large amount of data from Bureau of Revenue and, post-1978, from Taxation and

Revenue Department reports (most of the old data was provided to the project through the invaluable assis-

ta e of D . Ro ald P. B oadhead, p i ipal se io pet oleu geologist fo NMIMT’s Bureau of Geology.) While

this approach was productive and provided a credible estimate of OGAS contributions to the corpus of the

LGPF, there were a number of annoying holes in the data. A somewhat casual query to the State land office

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 10 –

resulted in being granted access to scans of a virtually complete set of annual reports of the State land com-

missioner, going back to the first report dated 1900. Data from these reports were hand entered into a com-

prehensive database, from which a highly credible and robust model was built. With an uncertainty of less

than .5 percent, we assert that the current proportion of the amount of annual interest transferred to the

general fund from investments of the LGPF is 96.7 percent. This year, we were able to plug some of the an-

noying gaps left at the conclusion of the FY 2013 report with another tranche of data from the old SLO annual

reports.

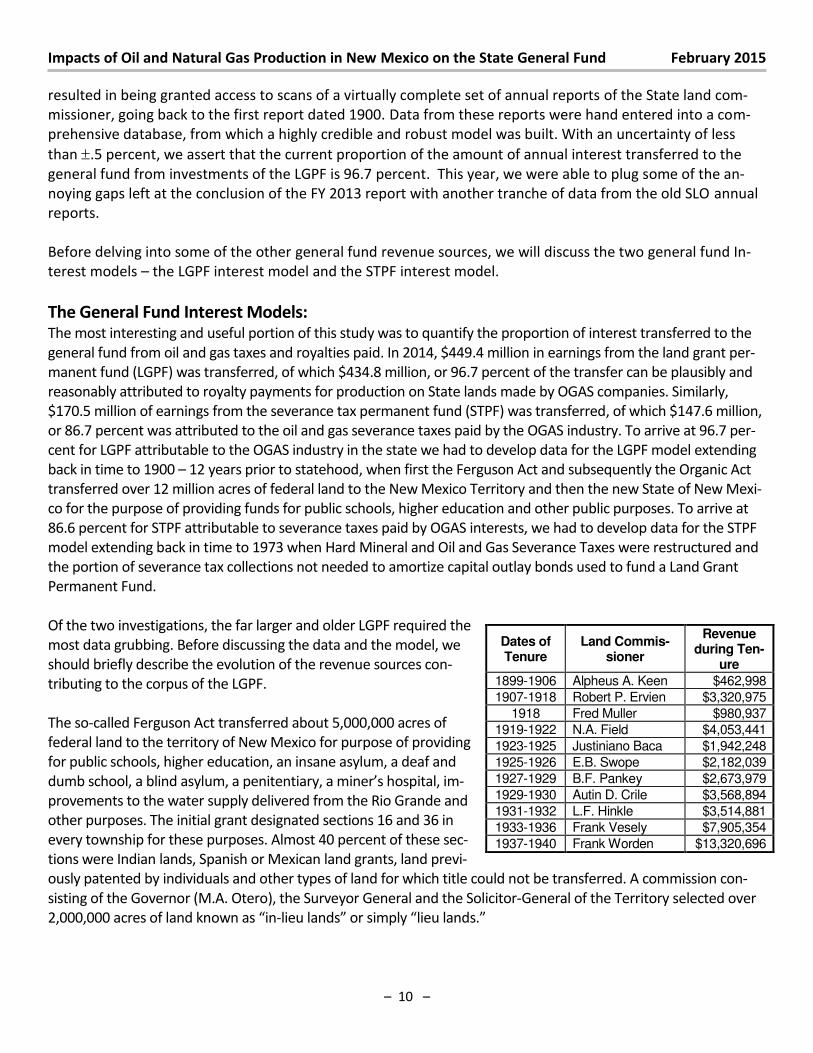

Before delving into some of the other general fund revenue sources, we will discuss the two general fund In-

terest models – the LGPF interest model and the STPF interest model.

The General Fund Interest Models: The most interesting and useful portion of this study was to quantify the proportion of interest transferred to the

general fund from oil and gas taxes and royalties paid. In 2014, $449.4 million in earnings from the land grant per-

manent fund (LGPF) was transferred, of which $434.8 million, or 96.7 percent of the transfer can be plausibly and

reasonably attributed to royalty payments for production on State lands made by OGAS companies. Similarly,

$170.5 million of earnings from the severance tax permanent fund (STPF) was transferred, of which $147.6 million,

or 86.7 percent was attributed to the oil and gas severance taxes paid by the OGAS industry. To arrive at 96.7 per-

cent for LGPF attributable to the OGAS industry in the state we had to develop data for the LGPF model extending

back in time to 1900 – 12 years prior to statehood, when first the Ferguson Act and subsequently the Organic Act

transferred over 12 million acres of federal land to the New Mexico Territory and then the new State of New Mexi-

co for the purpose of providing funds for public schools, higher education and other public purposes. To arrive at

86.6 percent for STPF attributable to severance taxes paid by OGAS interests, we had to develop data for the STPF

model extending back in time to 1973 when Hard Mineral and Oil and Gas Severance Taxes were restructured and

the portion of severance tax collections not needed to amortize capital outlay bonds used to fund a Land Grant

Permanent Fund.

Of the two investigations, the far larger and older LGPF required the

most data grubbing. Before discussing the data and the model, we

should briefly describe the evolution of the revenue sources con-

tributing to the corpus of the LGPF.

The so-called Ferguson Act transferred about 5,000,000 acres of

federal land to the territory of New Mexico for purpose of providing

for public schools, higher education, an insane asylum, a deaf and

du s hool, a li d as lu , a pe ite tia , a i e ’s hospital, im-

provements to the water supply delivered from the Rio Grande and

other purposes. The initial grant designated sections 16 and 36 in

every township for these purposes. Almost 40 percent of these sec-

tions were Indian lands, Spanish or Mexican land grants, land previ-

ously patented by individuals and other types of land for which title could not be transferred. A commission con-

sisting of the Governor (M.A. Otero), the Surveyor General and the Solicitor-General of the Territory selected over

2,000,000 acres of land k o as i -lieu la ds o si pl lieu la ds.

Dates of Tenure

Land Commis-sioner

Revenue during Ten-

ure

1899-1906 Alpheus A. Keen $462,998 1907-1918 Robert P. Ervien $3,320,975

1918 Fred Muller $980,937 1919-1922 N.A. Field $4,053,441 1923-1925 Justiniano Baca $1,942,248 1925-1926 E.B. Swope $2,182,039 1927-1929 B.F. Pankey $2,673,979 1929-1930 Autin D. Crile $3,568,894 1931-1932 L.F. Hinkle $3,514,881 1933-1936 Frank Vesely $7,905,354 1937-1940 Frank Worden $13,320,696

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 11 –

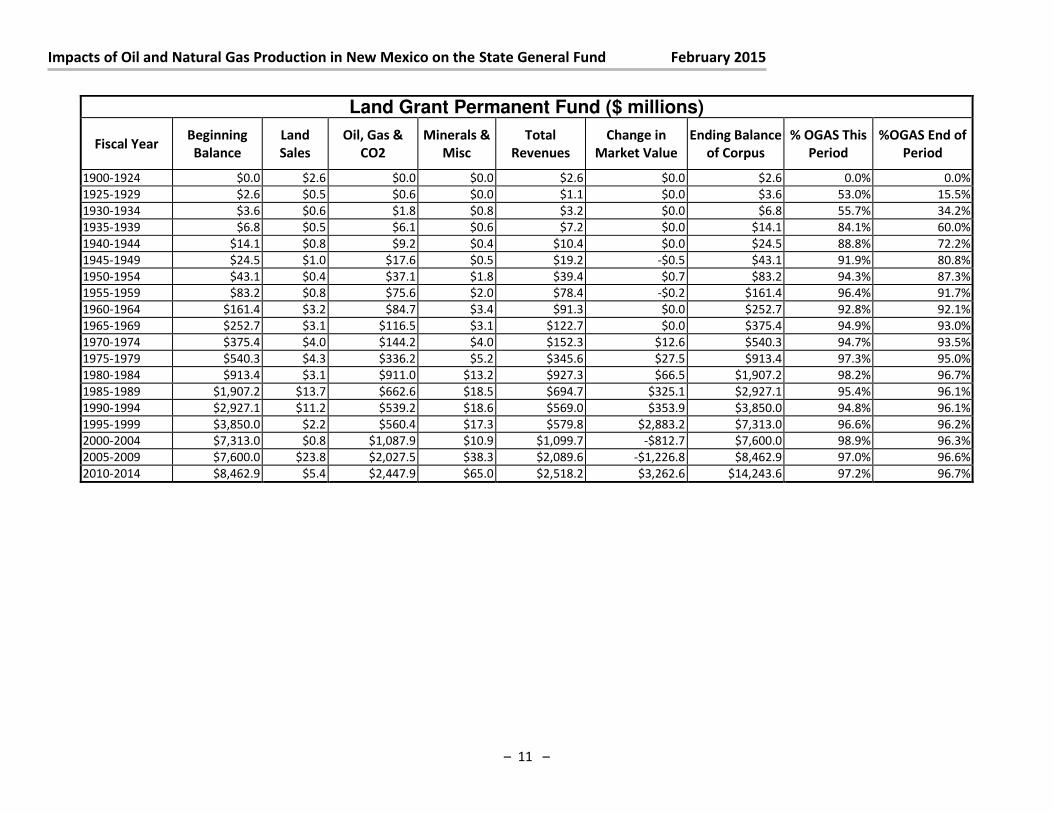

Land Grant Permanent Fund ($ millions)

Fiscal Year Beginning

Balance

Land

Sales

Oil, Gas &

CO2

Minerals &

Misc

Total

Revenues

Change in

Market Value

Ending Balance

of Corpus

% OGAS This

Period

%OGAS End of

Period

1900-1924 $0.0 $2.6 $0.0 $0.0 $2.6 $0.0 $2.6 0.0% 0.0%

1925-1929 $2.6 $0.5 $0.6 $0.0 $1.1 $0.0 $3.6 53.0% 15.5%

1930-1934 $3.6 $0.6 $1.8 $0.8 $3.2 $0.0 $6.8 55.7% 34.2%

1935-1939 $6.8 $0.5 $6.1 $0.6 $7.2 $0.0 $14.1 84.1% 60.0%

1940-1944 $14.1 $0.8 $9.2 $0.4 $10.4 $0.0 $24.5 88.8% 72.2%

1945-1949 $24.5 $1.0 $17.6 $0.5 $19.2 -$0.5 $43.1 91.9% 80.8%

1950-1954 $43.1 $0.4 $37.1 $1.8 $39.4 $0.7 $83.2 94.3% 87.3%

1955-1959 $83.2 $0.8 $75.6 $2.0 $78.4 -$0.2 $161.4 96.4% 91.7%

1960-1964 $161.4 $3.2 $84.7 $3.4 $91.3 $0.0 $252.7 92.8% 92.1%

1965-1969 $252.7 $3.1 $116.5 $3.1 $122.7 $0.0 $375.4 94.9% 93.0%

1970-1974 $375.4 $4.0 $144.2 $4.0 $152.3 $12.6 $540.3 94.7% 93.5%

1975-1979 $540.3 $4.3 $336.2 $5.2 $345.6 $27.5 $913.4 97.3% 95.0%

1980-1984 $913.4 $3.1 $911.0 $13.2 $927.3 $66.5 $1,907.2 98.2% 96.7%

1985-1989 $1,907.2 $13.7 $662.6 $18.5 $694.7 $325.1 $2,927.1 95.4% 96.1%

1990-1994 $2,927.1 $11.2 $539.2 $18.6 $569.0 $353.9 $3,850.0 94.8% 96.1%

1995-1999 $3,850.0 $2.2 $560.4 $17.3 $579.8 $2,883.2 $7,313.0 96.6% 96.2%

2000-2004 $7,313.0 $0.8 $1,087.9 $10.9 $1,099.7 -$812.7 $7,600.0 98.9% 96.3%

2005-2009 $7,600.0 $23.8 $2,027.5 $38.3 $2,089.6 -$1,226.8 $8,462.9 97.0% 96.6%

2010-2014 $8,462.9 $5.4 $2,447.9 $65.0 $2,518.2 $3,262.6 $14,243.6 97.2% 96.7%

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 12 –

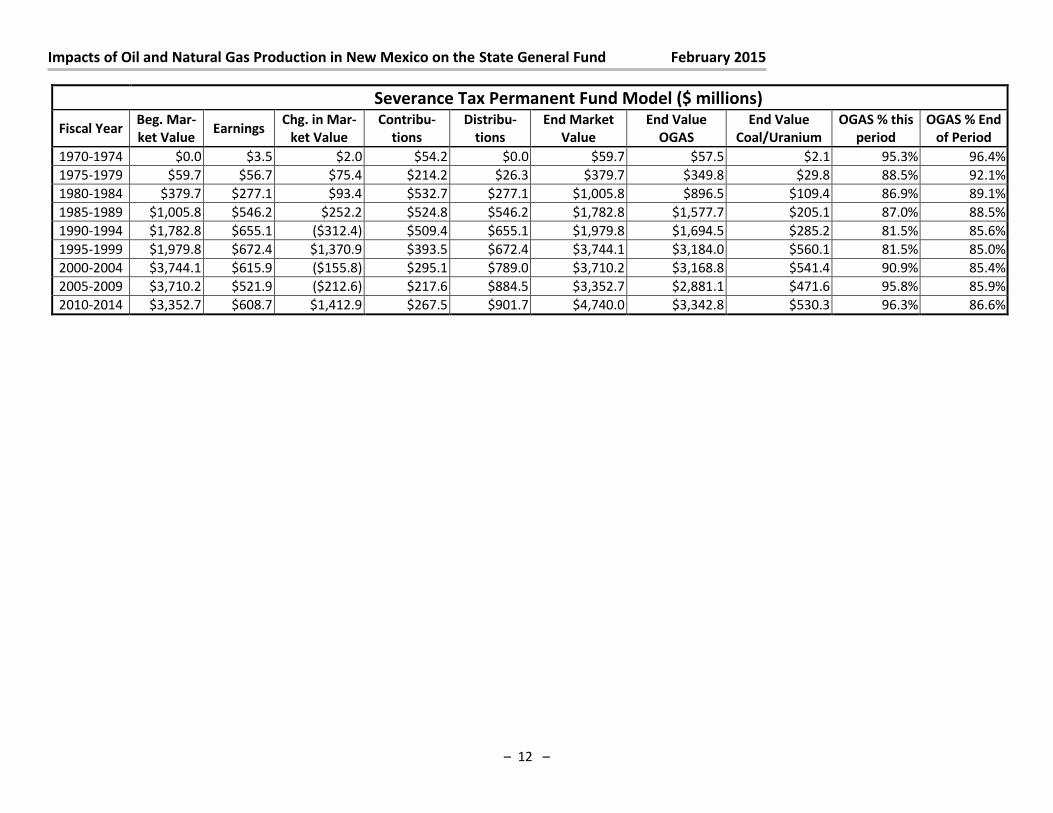

Severance Tax Permanent Fund Model ($ millions)

Fiscal Year Beg. Mar-

ket Value Earnings

Chg. in Mar-

ket Value

Contribu-

tions

Distribu-

tions

End Market

Value

End Value

OGAS

End Value

Coal/Uranium

OGAS % this

period

OGAS % End

of Period

1970-1974 $0.0 $3.5 $2.0 $54.2 $0.0 $59.7 $57.5 $2.1 95.3% 96.4%

1975-1979 $59.7 $56.7 $75.4 $214.2 $26.3 $379.7 $349.8 $29.8 88.5% 92.1%

1980-1984 $379.7 $277.1 $93.4 $532.7 $277.1 $1,005.8 $896.5 $109.4 86.9% 89.1%

1985-1989 $1,005.8 $546.2 $252.2 $524.8 $546.2 $1,782.8 $1,577.7 $205.1 87.0% 88.5%

1990-1994 $1,782.8 $655.1 ($312.4) $509.4 $655.1 $1,979.8 $1,694.5 $285.2 81.5% 85.6%

1995-1999 $1,979.8 $672.4 $1,370.9 $393.5 $672.4 $3,744.1 $3,184.0 $560.1 81.5% 85.0%

2000-2004 $3,744.1 $615.9 ($155.8) $295.1 $789.0 $3,710.2 $3,168.8 $541.4 90.9% 85.4%

2005-2009 $3,710.2 $521.9 ($212.6) $217.6 $884.5 $3,352.7 $2,881.1 $471.6 95.8% 85.9%

2010-2014 $3,352.7 $608.7 $1,412.9 $267.5 $901.7 $4,740.0 $3,342.8 $530.3 96.3% 86.6%

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 13 –

The Ferguson Act provided some guidelines as to suitable lieu lands, but there was some contentious squabbling

between Territorial and Federal interests. Laws of 1901, Chapter 74, established the office of State land commis-

sioner. The initial act set the salary of the State land commissioner at $2,500 per annum, which was six to seven

times the wages of a working cowboy4. The State land commissioner was allowed to hire clerks to assist in the op-

erations of the office with an initial appropriation of $1,500, which was probably enough for two or three clerks. Of

course, the cowboy was provided with horses to ride, a bed in a bunkhouse and grub. The Land Commissioner had

to furnish his own food, housing and transportation. This law replaced the Surveyor General on the Commission

charged with designating the lieu lands with the State Land Commissioner. The first State Land Commissioner was

Alpheus A. Keen, who served from 1899 to 1906, which was two years longer than the statutory authority for the

position. For the e ti e pe iod of M . Kee ’s te u e, he olle ted e e ue e ual to about 10 times the costs of the

“tate La d Co issio e ’s ope atio s. Total e pe ses of the “tate La d Offi e du i g the ou se of e e $5,707. One other interesting note, the Ferguson Act assumed that the state would sell the land outright to farm-

ers and ranchers, thus contributing to the settlement of the American West. However, the 1901 laws required that

5 percent of the money received from outright sales of land or from land contracts would be transferred to a per-

manent fund. At the end of calendar year 1901, the total corpus of the permanent funds stood at $70,069.After

1913, proceeds from land which was sold on contract that extended the purchase over 30 years at a 5 percent

annual interest rate were transferred to the permanent fund. The contract principal could be paid on a self-

amortizing basis or a lump sum basis. The federal establishment designated some lands as $5 lands (per acre)

and some as $3 lands. Grazing leases were priced roughly based on these designations, with the annual charge

for grazing leases on land without water of $12.80 per section per year and $30 per section for land with wa-

ter. A section is 640 acres.

At statehood in 1912, virtually all of the 5,584809.03 acres granted to the Territory in the Ferguson Act had

been selected. 2,072,000 acres were leased – primarily for ranching. About 75,000 acres had been sold out-

right or via contracts. The remainder of the original allotment was vacant. The Organic Act, also known locally

as the Enabling Act transferred an additional 6,569,520 acres of federal land to the new State of New Mexico

for the purpose of providing funds for public schools and higher education. The total of over 12 million acres is

but little smaller than the entire states of Maryland, New Jersey and Delaware 5. By the end of 1914, all but 2

million of the 12 million acres total had been selected and title vested in the State. The Federal Government

contested about 1 million acres of the 2 million unconfirmed. The 1910 grant gave sections 2 and 32 to the

state, with about half of the new grants being already entailed or otherwise withdrawn, either as Indian reser-

vations, federal forest reservations, residual Spanish or Mexican land grants, military reservations, patented

mining claims, mineral and oil reservations, homesteads and patented lands, small holding claims, reserva-

tions for irrigation purposes and Indian allotments. Between the 1898 and 1910 grants, over 4,000,000 acres

were lieu lands.

In the early going, the corpus of the LGPF consisted of five percent of the amount realized from sales of State

land. In 1924, oil royalties began flowing to the LGPF. Somewhat later, mineral royalties (primarily from coal

production on state lands) and timber sales were added to 100 percent of land sales and contracts and OGAS

4 F o the s th ough , o ki g o o ’s ages e e ge e all $ pe da plus oo i a u khouse, eals a d o ki g

horses. Cowboys provided a saddle and other tools of the trade. Young apprentices were frequently paid $15 a month or less.

(http://www.lemen.com/qa261.html … A working cowhand in the late 1800s was paid $25 to $30 a month "and found." The

phrase "and found" meant he also got his meals (and a bunk when he was at the ranch headquarters.) A top hand might even get

$40 a month and a foreman $50 or more. On a drive, a trail boss was sometimes paid as much as $100. For comparison, back then a

typical school teacher's wage was $30 a month, and dinner in a restaurant would usually cost about 25 cents. 5 “tate La d Co issio e ’s 1914 Annual Report of the State Land Commissioner

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 14 –

royalties. By State Law, all royalties and proceeds from the sale of State land are transferred to the LGPF. The

FY2014 ending balance in the fund was $14,243,600,000. In building the general fund interest model, we de-

termined that the first flow of OGAS royalties to the permanent fund occurred in CY 19246, when the State

land commissioner required all royalties paid on oil and gas production on state lands, as well as hard mineral

production on state lands to be transferred to the permanent funds maintained on behalf of each of the insti-

tutions. By June 30, 1932, the book value of transfers to the permanent funds stood at $4,767,590 with the

cumulative contribution from OGAS of $1,289,143, mean-

ing that 36 percent of the contributions to the permanent

funds from the beginning in 1900 were from OGAS royal-

ties from production on State Lands and the remainder

represented land sales, contracts and hard mineral royal-

ties. By the end of FY 1964 (52nd fiscal year), contributions

from OGAS has steadily increased in comparison to land

sales and hard mineral royalties. At the end of the year,

92.1 percent of the LGPF could be reasonably attributed to

OGAS. The table to the right exhibits this estimate of the

history of the OGAS contribution to the LFPF through the

decades.

The current LGPF interest model is not perfect. The various sources of information about OGAS and hard min-

eral royalties for production on State Lands cannot be perfectly reconciled. Part of the problem is that some

early SLO data is expressed in calendar years and not fiscal years. Another part of the problem is that SLO has

booked royalty revenue on an as-received basis while BOR, the Oil and Gas Accounting Commission (pre-1978)

and the TRD have booked the revenue first on a distribution month basis, then on a receipt month basis and

finally, after July 1, 2004 on an accrual basis which lags two months from the returns month. Over a long peri-

od, these differences do not matter greatly (with the

exception of the extra month of revenue recognized at

the end of FY 2004), but matter significantly in trying to

reconcile individual years. On the other hand, during

the course of the Phase 2 investigation relative to FY

2014, about half of the data gaps in the FY 2013 study

were resolved.

The STPF model was considerably easier to construct,

since actual oil and gas severance and hard mineral

severance data were available for the entire period from inception of the STPF in 1973 to date. The model,

with a few uncertainties, indicates that OGAS percentage of the STPF is 86.6 percent. The uncertainty in this

estimate is perhaps .5 percent, similar to the uncertainty in the LGPF general fund Interest model. As for the

LGPF model, this result is robust. As shown in the table to the right, for the most part, the average contribu-

tion ratio differed little from 86 percent for the first 20-years of the STPF. The contributions over the last dec-

ade have not influenced the aggregate estimate significantly since residual contributions from the STBF to the

STPF have fallen with the advent of aggressive bonding programs where the state sells not only senior bonds,

6 In FY 1924, over $9,700 in oil royalties were collected. Only $1,611.71 of this total was transferred to the permanent funds as State

Land Commissioner Justiniano Baca determined that the royalties from depleting the oil and gas reserves should be treated differ-

ently than proceeds from grazing leases (sustainable) and similar to the sales of land. By 1925, 100% of land sales, hard mineral and

oil and gas lease royalties were being transferred to the permanent funds.

Contributions Attributable to OGAS

Land Grant Permanent Fund

Average

During Period At end of period

Pre-1965 62.4% 92.1%

1965-1974 94.4% 93.5%

1975-1984 97.1% 96.7%

1985-1994 95.9% 96.1%

1995-2004 95.9% 96.3%

2005-2014 97.5% 96.7%

Contributions Attributable to OGAS Severance Tax Permanent Fund

Average during

decade At end of period

1972 -1984 89.1% 89.1%

1985-1994 84.2% 85.6%

1995-2004 86.2% 85.4%

2005-2014 96.4% 86.6%

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 15 –

but subordinate bonds, and short-te spo ge o ds of oth se io a d su o di ate lasses. This means

that the earlier data is critical in determining the percent of STPF interest attributable to oil and gas severance

taxes.

The FY2013 ending market value of the LGPF is $4,740,000,000. There is a minor defect of the model in that

the portion of total severance taxes used to retire bonds is not directly available prior to 1994 when the Board

of Finance bond disclosure documents have been available. During the period from 1973 through the late

1980s/early 1990s, only senior bonds were issued. These were, generally, five-year bonds with a two-to-one

coverage ratio. Since there was always uncertainty in the amount of severance tax revenue available for semi-

annual bonding, somewhat more than 50 percent of the severance tax stream was transferred in this period to

the STPF. Board of Finance disclosure documents exhibit the details of the STBF for the period 1995 through

2012 by fiscal year. This affects in a minor way the timing of transfers to the STPF.

Another minor defect is that these data do not directly reconcile with the data obtained from ONGARD for

that period. It should be noted that the STBF records both oil and gas and hard mineral severance taxes when

received. The State general fund was converted to full accrual accounting at the end of FY 2004. This essen-

tially means that production from May through April is reported to TRD (and paid) from July through June, but

accrued to the general fund based on the production months of May through April. This similar accrual con-

version was not implemented for the STBF. This reconciliation problem is high on the list of issued for the next

phase of this study.

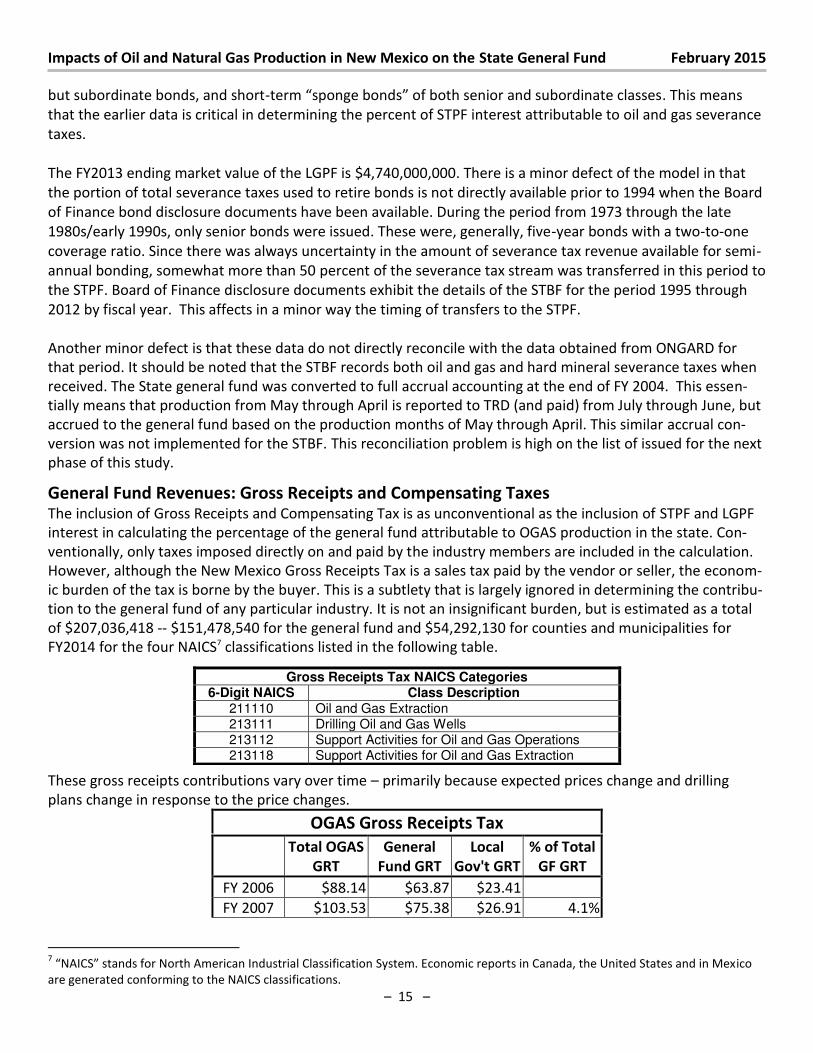

General Fund Revenues: Gross Receipts and Compensating Taxes The inclusion of Gross Receipts and Compensating Tax is as unconventional as the inclusion of STPF and LGPF

interest in calculating the percentage of the general fund attributable to OGAS production in the state. Con-

ventionally, only taxes imposed directly on and paid by the industry members are included in the calculation.

However, although the New Mexico Gross Receipts Tax is a sales tax paid by the vendor or seller, the econom-

ic burden of the tax is borne by the buyer. This is a subtlety that is largely ignored in determining the contribu-

tion to the general fund of any particular industry. It is not an insignificant burden, but is estimated as a total

of $207,036,418 -- $151,478,540 for the general fund and $54,292,130 for counties and municipalities for

FY2014 for the four NAICS7 classifications listed in the following table.

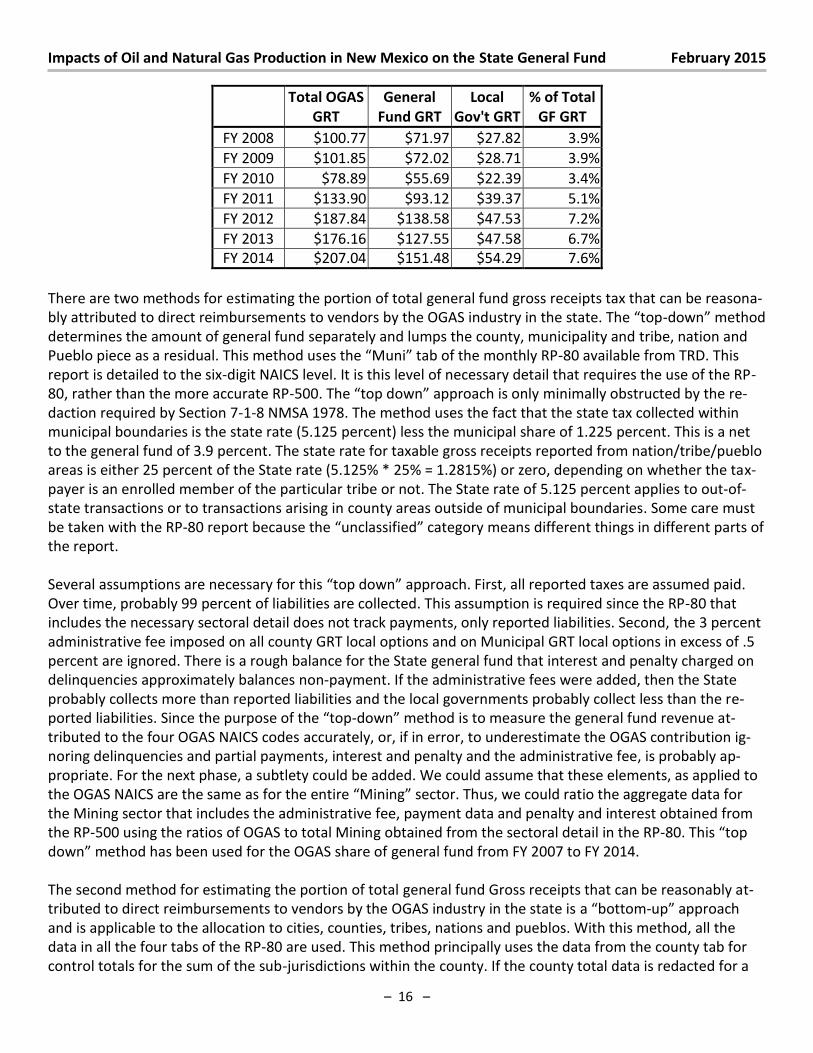

These gross receipts contributions vary over time – primarily because expected prices change and drilling

plans change in response to the price changes.

OGAS Gross Receipts Tax

Total OGAS

GRT

General

Fund GRT

Local

Gov't GRT

% of Total

GF GRT

FY 2006 $88.14 $63.87 $23.41

FY 2007 $103.53 $75.38 $26.91 4.1%

7 NAIC“ sta ds fo No th A e i a I dust ial Classifi atio “ ste . E o o i epo ts i Ca ada, the U ited “tates a d i Me ico

are generated conforming to the NAICS classifications.

Gross Receipts Tax NAICS Categories 6-Digit NAICS Class Description

211110 Oil and Gas Extraction 213111 Drilling Oil and Gas Wells 213112 Support Activities for Oil and Gas Operations 213118 Support Activities for Oil and Gas Extraction

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 16 –

Total OGAS

GRT

General

Fund GRT

Local

Gov't GRT

% of Total

GF GRT

FY 2008 $100.77 $71.97 $27.82 3.9%

FY 2009 $101.85 $72.02 $28.71 3.9%

FY 2010 $78.89 $55.69 $22.39 3.4%

FY 2011 $133.90 $93.12 $39.37 5.1%

FY 2012 $187.84 $138.58 $47.53 7.2%

FY 2013 $176.16 $127.55 $47.58 6.7%

FY 2014 $207.04 $151.48 $54.29 7.6%

There are two methods for estimating the portion of total general fund gross receipts tax that can be reasona-

bly attributed to direct reimbursements to vendors the OGA“ i dust i the state. The top-do ethod determines the amount of general fund separately and lumps the county, municipality and tribe, nation and

Pueblo piece as a residual. This method uses the Mu i ta of the o thl RP-80 available from TRD. This

report is detailed to the six-digit NAICS level. It is this level of necessary detail that requires the use of the RP-

80, rather than the more accurate RP-500. The top do app oa h is o l minimally obstructed by the re-

daction required by Section 7-1-8 NMSA 1978. The method uses the fact that the state tax collected within

municipal boundaries is the state rate (5.125 percent) less the municipal share of 1.225 percent. This is a net

to the general fund of 3.9 percent. The state rate for taxable gross receipts reported from nation/tribe/pueblo

areas is either 25 percent of the State rate (5.125% * 25% = 1.2815%) or zero, depending on whether the tax-

payer is an enrolled member of the particular tribe or not. The State rate of 5.125 percent applies to out-of-

state transactions or to transactions arising in county areas outside of municipal boundaries. Some care must

be taken with the RP-80 report because the u lassified atego means different things in different parts of

the report.

Several assumptions are necessary for this top do approach. First, all reported taxes are assumed paid.

Over time, probably 99 percent of liabilities are collected. This assumption is required since the RP-80 that

includes the necessary sectoral detail does not track payments, only reported liabilities. Second, the 3 percent

administrative fee imposed on all county GRT local options and on Municipal GRT local options in excess of .5

percent are ignored. There is a rough balance for the State general fund that interest and penalty charged on

delinquencies approximately balances non-payment. If the administrative fees were added, then the State

probably collects more than reported liabilities and the local governments probably collect less than the re-

ported liabilities. “i e the pu pose of the top-do ethod is to easu e the general fund revenue at-

tributed to the four OGAS NAICS codes accurately, or, if in error, to underestimate the OGAS contribution ig-

noring delinquencies and partial payments, interest and penalty and the administrative fee, is probably ap-

propriate. For the next phase, a subtlety could be added. We could assume that these elements, as applied to

the OGAS NAICS are the same as fo the e ti e Mi i g se to . Thus, e ould atio the agg egate data fo the Mining sector that includes the administrative fee, payment data and penalty and interest obtained from

the RP-500 using the ratios of OGAS to total Mining obtained from the sectoral detail in the RP-80. This top do ethod has ee used fo the OGA“ sha e of general fund from FY 2007 to FY 2014.

The second method for estimating the portion of total general fund Gross receipts that can be reasonably at-

tributed to direct reimbursements to vendors by the OGAS industry in the state is a otto -up app oa h and is applicable to the allocation to cities, counties, tribes, nations and pueblos. With this method, all the

data in all the four tabs of the RP-80 are used. This method principally uses the data from the county tab for

control totals for the sum of the sub-jurisdictions within the county. If the county total data is redacted for a

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 17 –

particular NAICS code, then the redaction is allowed to stand. If the county total data are not redacted, but

the sub-jurisdiction data are, then a judicious allocation of the county amounts to the municipalities, Indian

areas and remainder county are made. Tax rates are adopted effective only July 1 and January 1. The bottom

up method adds the first six months of the fiscal year together for each jurisdiction in the county and the sec-

ond six months separately together. The enactment table published by TRD for each six-month period pro-

vides the data to allocate reported tax by sub-jurisdiction to the county, to the city or to a tribe, nation or

pue lo. These a e the data epo ted o the o pa io Cou t I pa ts of Oil and Gas Production in New

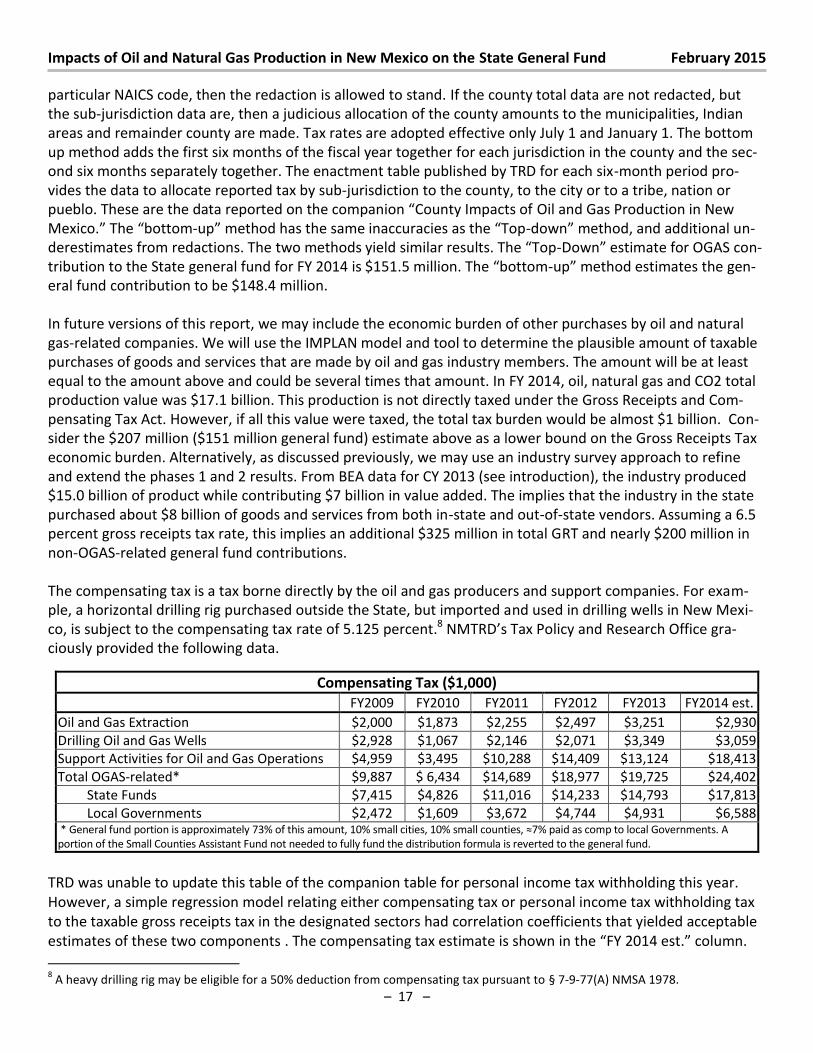

Me i o. The otto -up ethod has the sa e i a u a ies as the Top-do ethod, a d additio al un-

derestimates from redactions. The t o ethods ield si ila esults. The Top-Do esti ate fo OGA“ on-

tribution to the State general fund for FY 2014 is $151. illio . The otto -up ethod esti ates the gen-

eral fund contribution to be $148.4 million.

In future versions of this report, we may include the economic burden of other purchases by oil and natural

gas-related companies. We will use the IMPLAN model and tool to determine the plausible amount of taxable

purchases of goods and services that are made by oil and gas industry members. The amount will be at least

equal to the amount above and could be several times that amount. In FY 2014, oil, natural gas and CO2 total

production value was $17.1 billion. This production is not directly taxed under the Gross Receipts and Com-

pensating Tax Act. However, if all this value were taxed, the total tax burden would be almost $1 billion. Con-

sider the $207 million ($151 million general fund) estimate above as a lower bound on the Gross Receipts Tax

economic burden. Alternatively, as discussed previously, we may use an industry survey approach to refine

and extend the phases 1 and 2 results. From BEA data for CY 2013 (see introduction), the industry produced

$15.0 billion of product while contributing $7 billion in value added. The implies that the industry in the state

purchased about $8 billion of goods and services from both in-state and out-of-state vendors. Assuming a 6.5

percent gross receipts tax rate, this implies an additional $325 million in total GRT and nearly $200 million in

non-OGAS-related general fund contributions.

The compensating tax is a tax borne directly by the oil and gas producers and support companies. For exam-

ple, a horizontal drilling rig purchased outside the State, but imported and used in drilling wells in New Mexi-

co, is subject to the compensating tax rate of 5.125 percent.8 NMTRD’s Tax Policy and Research Office gra-

ciously provided the following data.

TRD was unable to update this table of the companion table for personal income tax withholding this year.

However, a simple regression model relating either compensating tax or personal income tax withholding tax

to the taxable gross receipts tax in the designated sectors had correlation coefficients that yielded acceptable

estimates of these two components . The co pe sati g ta esti ate is sho i the FY est. olu . 8 A heavy drilling rig may be eligible for a 50% deduction from compensating tax pursuant to § 7-9-77(A) NMSA 1978.

Compensating Tax ($1,000)

FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 est.

Oil and Gas Extraction $2,000 $1,873 $2,255 $2,497 $3,251 $2,930

Drilling Oil and Gas Wells $2,928 $1,067 $2,146 $2,071 $3,349 $3,059

Support Activities for Oil and Gas Operations $4,959 $3,495 $10,288 $14,409 $13,124 $18,413

Total OGAS-related* $9,887 $ 6,434 $14,689 $18,977 $19,725 $24,402

State Funds $7,415 $4,826 $11,016 $14,233 $14,793 $17,813

Local Governments $2,472 $1,609 $3,672 $4,744 $4,931 $6,588 * General fund portion is approximately 73% of this amount, 10% small cities, 10% small ou ties, ≈7% paid as comp to local Governments. A

portion of the Small Counties Assistant Fund not needed to fully fund the distribution formula is reverted to the general fund.

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 18 –

General Fund Revenues: Personal Income Tax Conventionally, when determining the portion of the general fund attributable to taxes and royalties paid by

the oil and natural gas industry, personal income taxes paid by employees or investors in production of the

industry are not included. This is a similar argument to the traditional exclusion of the economic burden im-

posed on the industry of the gross receipts tax. In that case, the argument advanced was that the tax is not

imposed directly on the producers. That argument, however, fails in the case of oil and gas withholding. This is

a tax collected by the producers from investors and persons with royalty interests in oil and gas production.

These taxes, when deducted from royalty payments or profit distributions made to out-of-state investors, are

then remitted to TRD. At personal income tax filing time, these withheld payments are applied to personal

income tax liabilities incurred by the payment of royalties by the producers. In the first few years following

enactment in 2004, this was not a significant revenue source. However, in FY2013, producers remitted

$90,195,333 to TRD on behalf of their royalty holders and investors and in FY 2014, the amount had increased

to $109,600,000. This is not a direct tax. The producers have a fiduciary responsibility to collect and remit this

withholding. Nor is the amount of oil and gas withholding a perfect estimate of the amount of New Mexico tax

liability incurred by the investors and royalty holders. On the other hand, it is likely that refunds will be mod-

est, since the vast majority of investors are subject to the maximum 4.9 percent current income tax rate,

which is the 2014 withholding rate. Thus, the allocated income from oil and gas interests will end up being

taxed at approximately the 4.9 percent tax rate. This may be a specious argument, however. Total production

on private lands in the state in FY 2014 was approximately $2.2 billion. If royalties are a usual 1/8th, or 12.5

percent and the withholding tax rate is 4.9 percent, the total withheld and remitted to TRD should be around

$13.6 million or less. However, royalties are not the only payments subject to OGAS withholding. Producers,

particularly independent producers, have company owners and other investors. Total production value for

FY14, including production on State, Federal and private lands was $17.1 billion. If, in addition to the $13.6

million in royalties on private lands, producers pay investors some portion of the profits from oil and gas pro-

duction and then deduct the oil and gas withholding amounts from dividends, $96 million in oil and gas with-

holding represents about $2.0 billion in profits subject to withholding. Thus, this is consistent with about 18

percent of production in New Mexico is financed by investors.

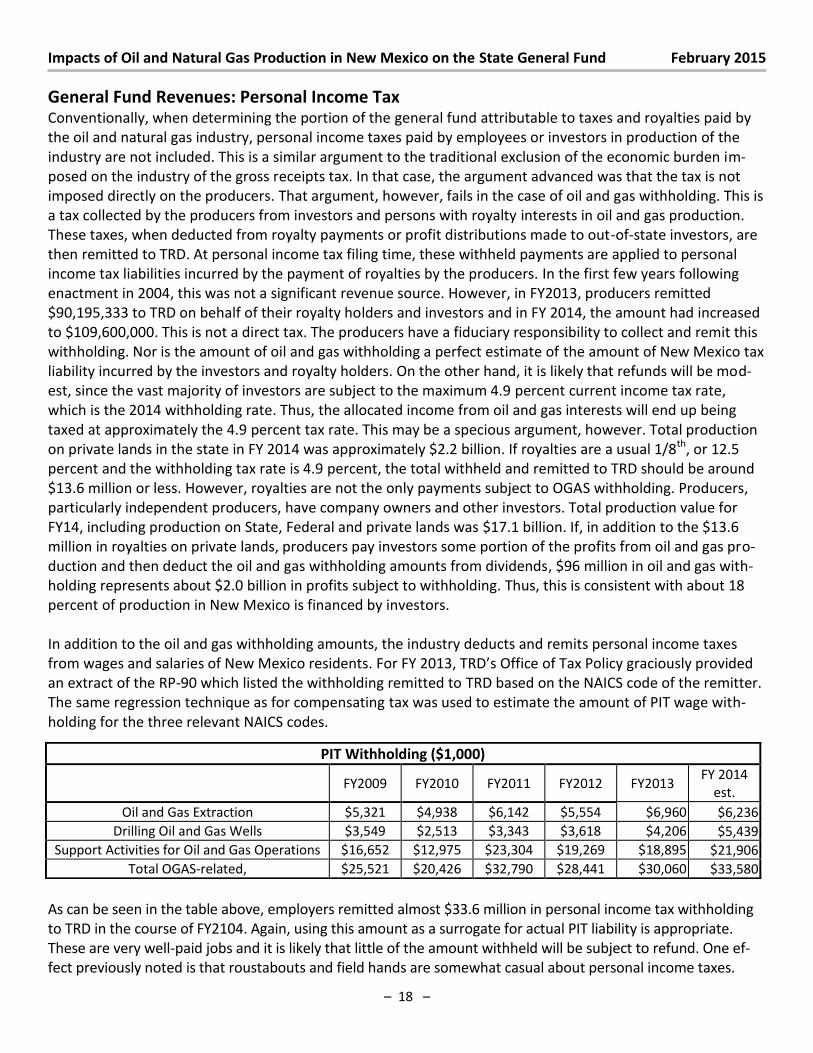

In addition to the oil and gas withholding amounts, the industry deducts and remits personal income taxes

from wages and salaries of New Mexico residents. For FY 2013, TRD’s Offi e of Ta Poli g a iousl p o ided an extract of the RP-90 which listed the withholding remitted to TRD based on the NAICS code of the remitter.

The same regression technique as for compensating tax was used to estimate the amount of PIT wage with-

holding for the three relevant NAICS codes.

As can be seen in the table above, employers remitted almost $33.6 million in personal income tax withholding

to TRD in the course of FY2104. Again, using this amount as a surrogate for actual PIT liability is appropriate.

These are very well-paid jobs and it is likely that little of the amount withheld will be subject to refund. One ef-

fect previously noted is that roustabouts and field hands are somewhat casual about personal income taxes.

PIT Withholding ($1,000)

FY2009 FY2010 FY2011 FY2012 FY2013

FY 2014

est.

Oil and Gas Extraction $5,321 $4,938 $6,142 $5,554 $6,960 $6,236

Drilling Oil and Gas Wells $3,549 $2,513 $3,343 $3,618 $4,206 $5,439

Support Activities for Oil and Gas Operations $16,652 $12,975 $23,304 $19,269 $18,895 $21,906

Total OGAS-related, $25,521 $20,426 $32,790 $28,441 $30,060 $33,580

Impacts of Oil and Natural Gas Production in New Mexico on the State General Fund February 2015

– 19 –

They tend to move casually into and out of the state and let the amount of taxes withheld by their employers

suffice instead of filing a New Mexico income tax return in the event that they are no longer resident in the state

at the time of filing. These migrant workers cheerfully abandon any refund they might be due.

For many reasons, then, it is appropriate that we give to the industry $109.6+$33.6 in attribution to the gen-

eral fund for oil and gas withholding and for withholding from wages and salaries.

Now, recognize that investors and royalty holders that are New Mexico residents or are regular corporations

are not subject to the oil and gas withholding. We can only speculate on what portion of the royalty interests