Embed Size (px)

Citation preview

The Global LED Lighting Market

Key Trends and Opportunities

Presented toTekes

June 2015

2

Year/USD bn Lightsources Control Gear Fixtures

2014 24.4 7.9 55.0

2020 25.7 11.2 60.5

CAGR (2014-20) 1.0% 7.4% 1.9%

Global Lighting Market: Historical and Forecast Mar ket Size by Segment, 2014 & 2020

Total Lighting Market, including TraditionalControl Gear is the Fastest Growing Segment

• Control gear to gain a pivotal role with the

rise of LED due to the long term increase on

functionality

• The possibilities that LED offers will give

rise to increasingly complex control gear

giving comfort, security and flexibility to

lighting that has thus far only been seen in

niche markets

• The average price of control gear is

expected to rise notably in Europe and North

America by 2019 on top of the increase in

units globally

US

D m

illio

n

. Source: Frost & Sullivan

0

20,000

40,000

60,000

80,000

100,000

120,000

2012 2013 2014 2015 2016 2017 2018 2019

Fixtures

Control gear

Lightsources

0

20,000

40,000

60,000

80,000

100,000

120,000

2012 2013 2014 2015 2016 2017 2018 2019

LED

Traditional

3

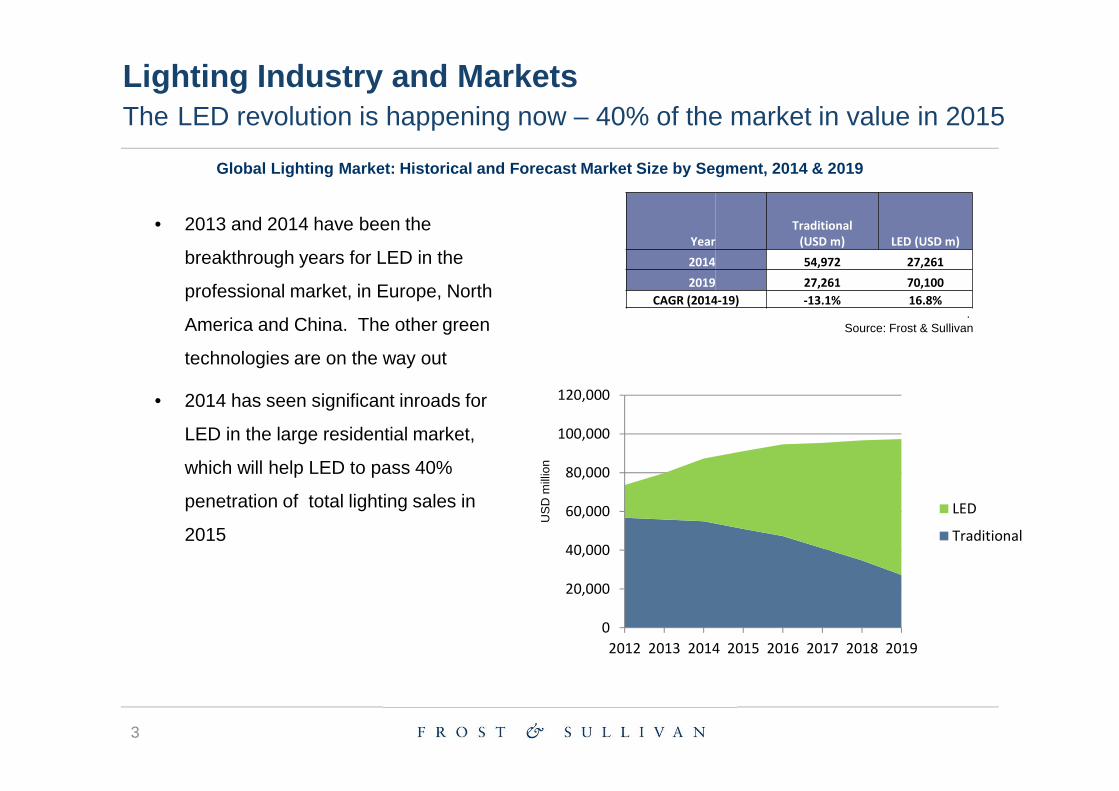

Global Lighting Market: Historical and Forecast Mar ket Size by Segment, 2014 & 2019

Year

Traditional

(USD m) LED (USD m)

2014 54,972 27,261

2019 27,261 70,100

CAGR (2014-19) -13.1% 16.8%

Lighting Industry and MarketsThe LED revolution is happening now – 40% of the market in value in 2015

• 2013 and 2014 have been the

breakthrough years for LED in the

professional market, in Europe, North

America and China. The other green

technologies are on the way out

• 2014 has seen significant inroads for

LED in the large residential market,

which will help LED to pass 40%

penetration of total lighting sales in

2015 U

SD

mill

ion

. Source: Frost & Sullivan

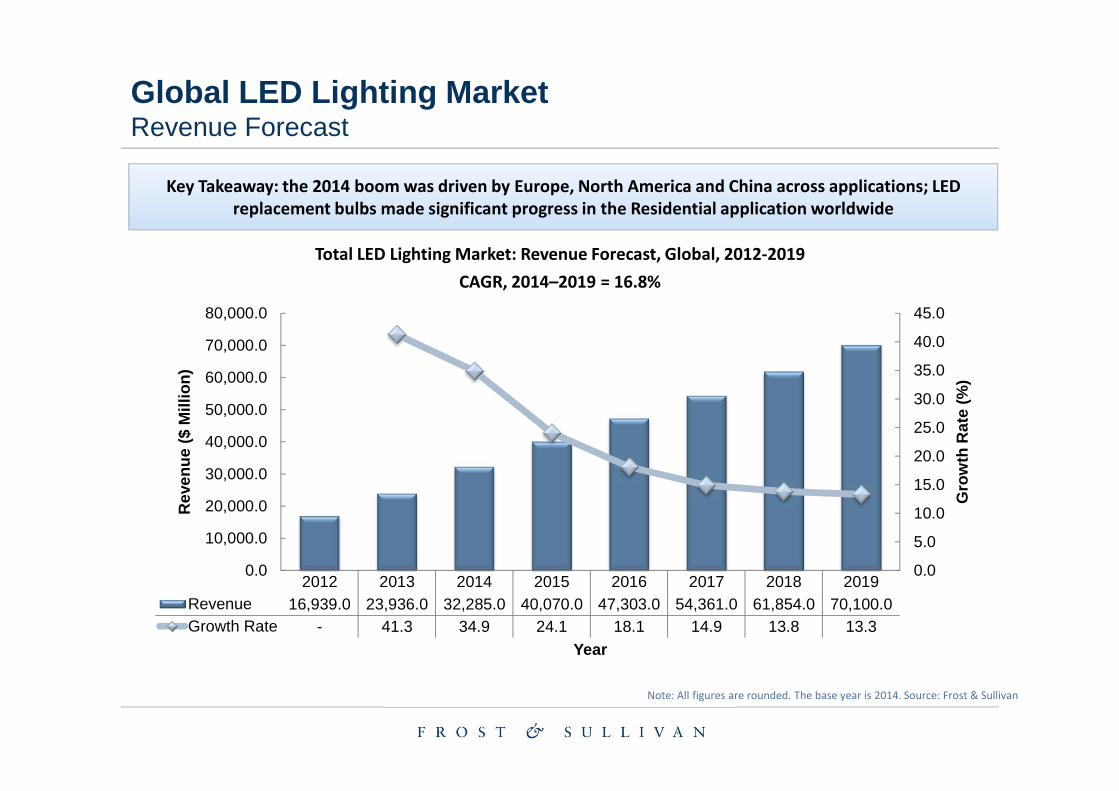

Global LED Lighting MarketRevenue Forecast

Key Takeaway: the 2014 boom was driven by Europe, North America and China across applications; LED

replacement bulbs made significant progress in the Residential application worldwide

Note: All figures are rounded. The base year is 2014. Source: Frost & Sullivan

Total LED Lighting Market: Revenue Forecast, Global, 2012-2019

CAGR, 2014–2019 = 16.8%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

0.0

10,000.0

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

70,000.0

80,000.0

2012 2013 2014 2015 2016 2017 2018 2019Revenue 16,939.0 23,936.0 32,285.0 40,070.0 47,303.0 54,361.0 61,854.0 70,100.0Growth Rate - 41.3 34.9 24.1 18.1 14.9 13.8 13.3

Gro

wth

Rat

e (%

)

Rev

enue

($

Mill

ion)

Year

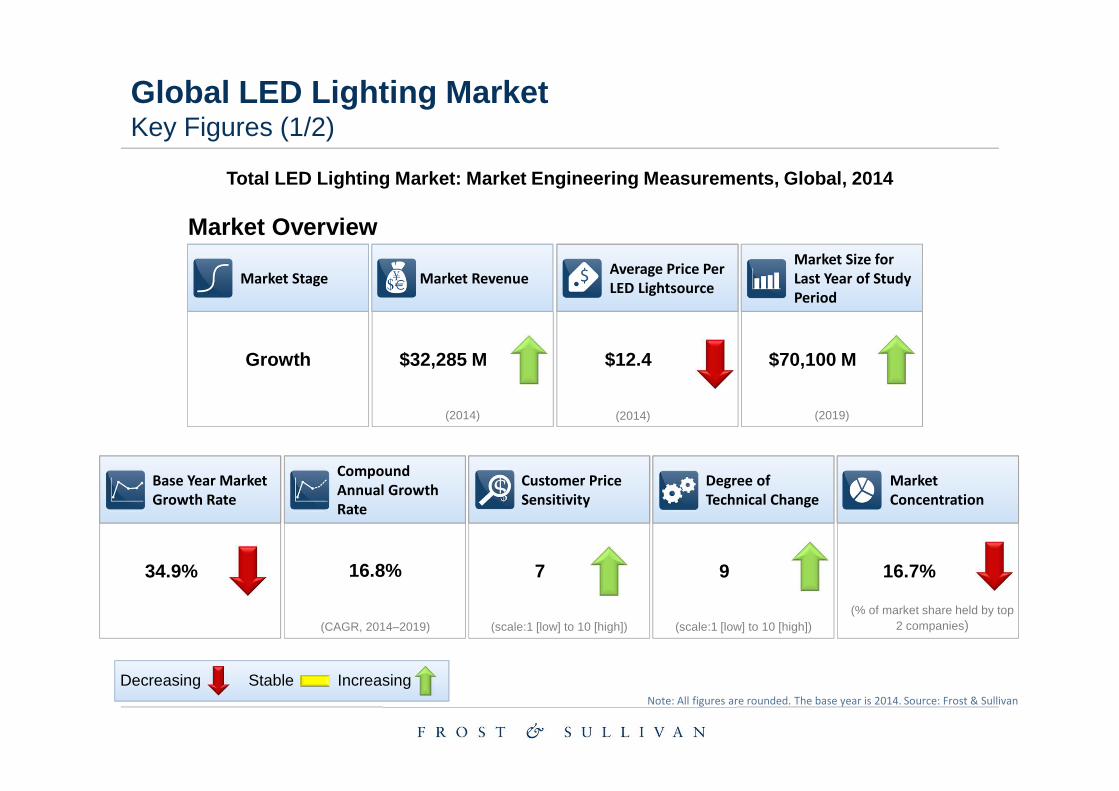

Compound

Annual Growth

Rate

16.8%

(CAGR, 2014–2019)

Market

Concentration

16.7%

(% of market share held by top 2 companies)

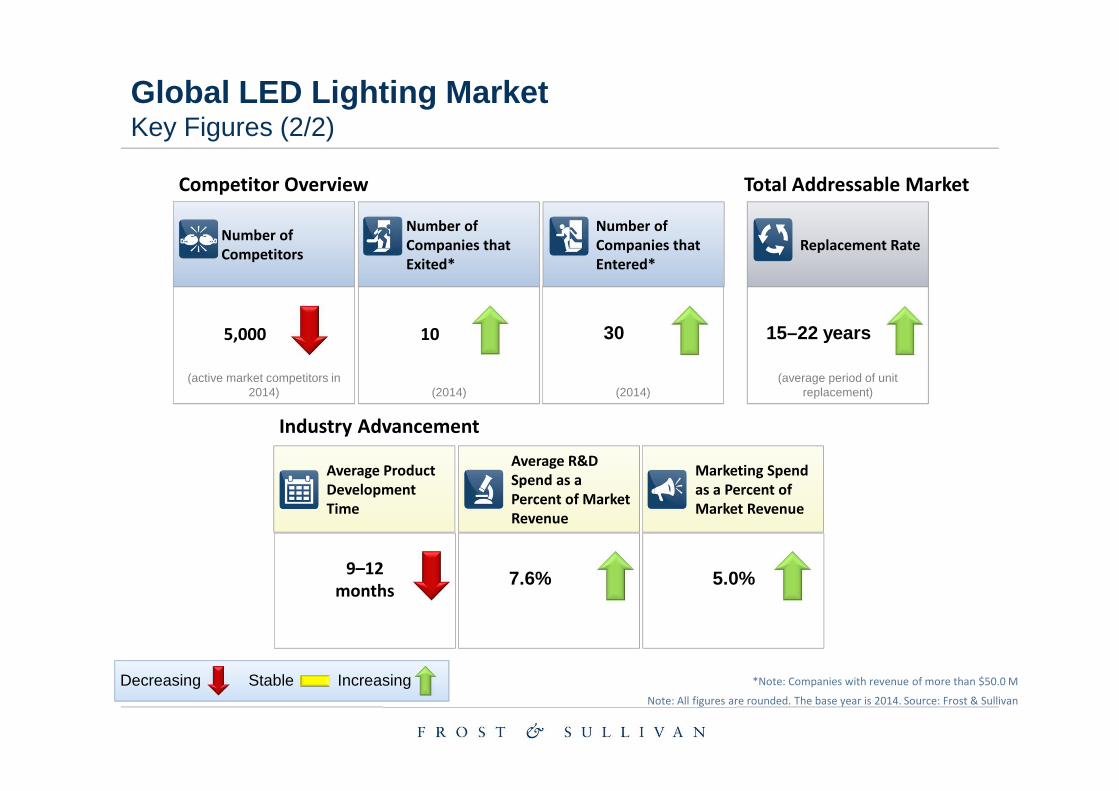

Global LED Lighting MarketKey Figures (1/2)

Market Stage

Growth

Average Price Per

LED Lightsource

$12.4

Market Size for

Last Year of Study

Period

$70,100 M

(2019)

Customer Price

Sensitivity

7

(scale:1 [low] to 10 [high])

Degree of

Technical Change

9

(scale:1 [low] to 10 [high])

Market Revenue

$32,285 M

(2014)

Total LED Lighting Market: Market Engineering Measu rements, Global, 2014

Base Year Market

Growth Rate

34.9%

Stable IncreasingDecreasingNote: All figures are rounded. The base year is 2014. Source: Frost & Sullivan

Market Overview

(2014)

Replacement Rate

15–22 years

(average period of unit replacement)

Average Product

Development

Time

9–12

months

Number of

Companies that

Exited*

10

(2014)

Number of

Companies that

Entered*

30

(2014)

Number of

Competitors

5,000

(active market competitors in 2014)

Global LED Lighting MarketKey Figures (2/2)

Competitor Overview Total Addressable Market

Industry Advancement

Marketing Spend

as a Percent of

Market Revenue

5.0%

Average R&D

Spend as a

Percent of Market

Revenue

7.6%

*Note: Companies with revenue of more than $50.0 M Stable IncreasingDecreasingNote: All figures are rounded. The base year is 2014. Source: Frost & Sullivan

Source: Frost & Sullivan

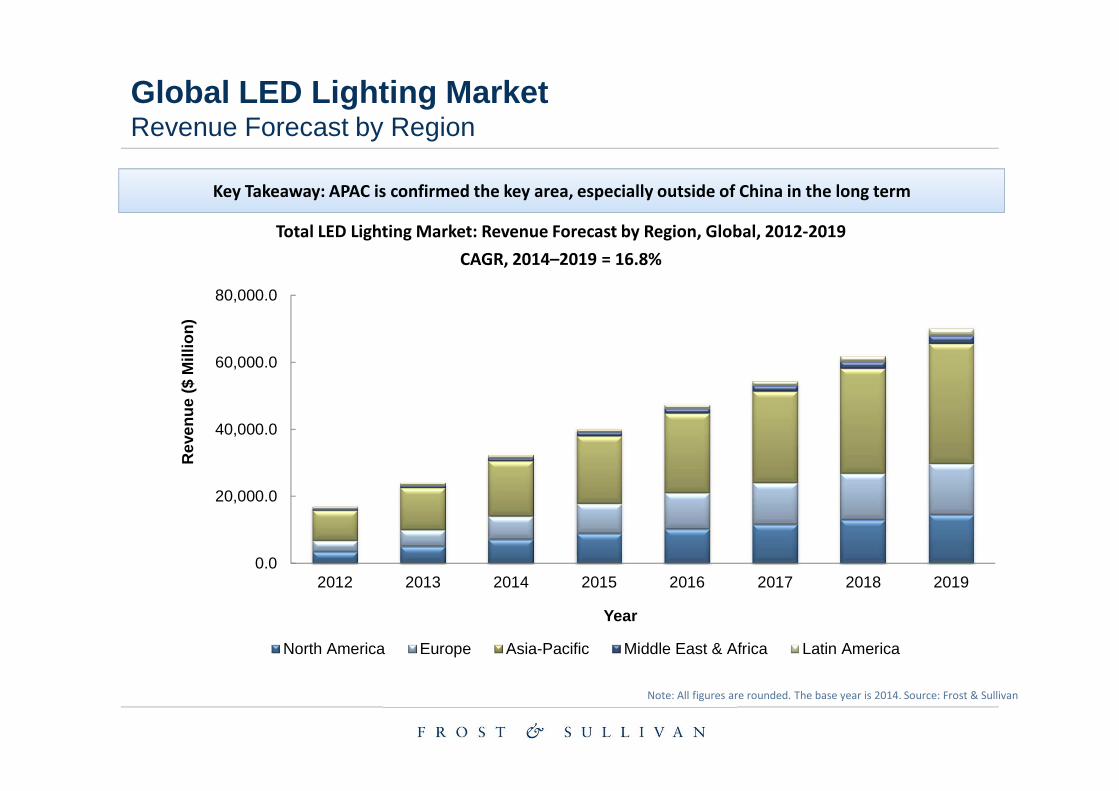

Global LED Lighting MarketEurope and North America to mature first; higher growth rates during the forecast period in younger markets

North America: Incandescent ban stimulates demand; utilities rebates make SSL affordable.

Europe: The implemented EU ban on incandescent and the prospective ban on halogen drive LED adoption in the region.

Asia-Pacific: China is embracing LED and will lead the change for the region.

Middle East and Africa: Growth expected in the second half of the forecast period, thanks to a sharp price decline.

Latin America: Price is the key barrier to adoption outside of high-end projects. LED will increasingly be able to challenge CFL.

CAGR 2014–2019 = 15.2%

CAGR 2014–2019 = 17.2%

CAGR 2014–2019 =

16.8%

CAGR 2014–2019 = 18.4%CAGR 2014–2019 = 23.1%

Global LED Lighting MarketRevenue Forecast by Region

Key Takeaway: APAC is confirmed the key area, especially outside of China in the long term

Note: All figures are rounded. The base year is 2014. Source: Frost & Sullivan

Total LED Lighting Market: Revenue Forecast by Region, Global, 2012-2019

CAGR, 2014–2019 = 16.8%

0.0

20,000.0

40,000.0

60,000.0

80,000.0

2012 2013 2014 2015 2016 2017 2018 2019

Rev

enue

($

Mill

ion)

Year

North America Europe Asia-Pacific Middle East & Africa Latin America

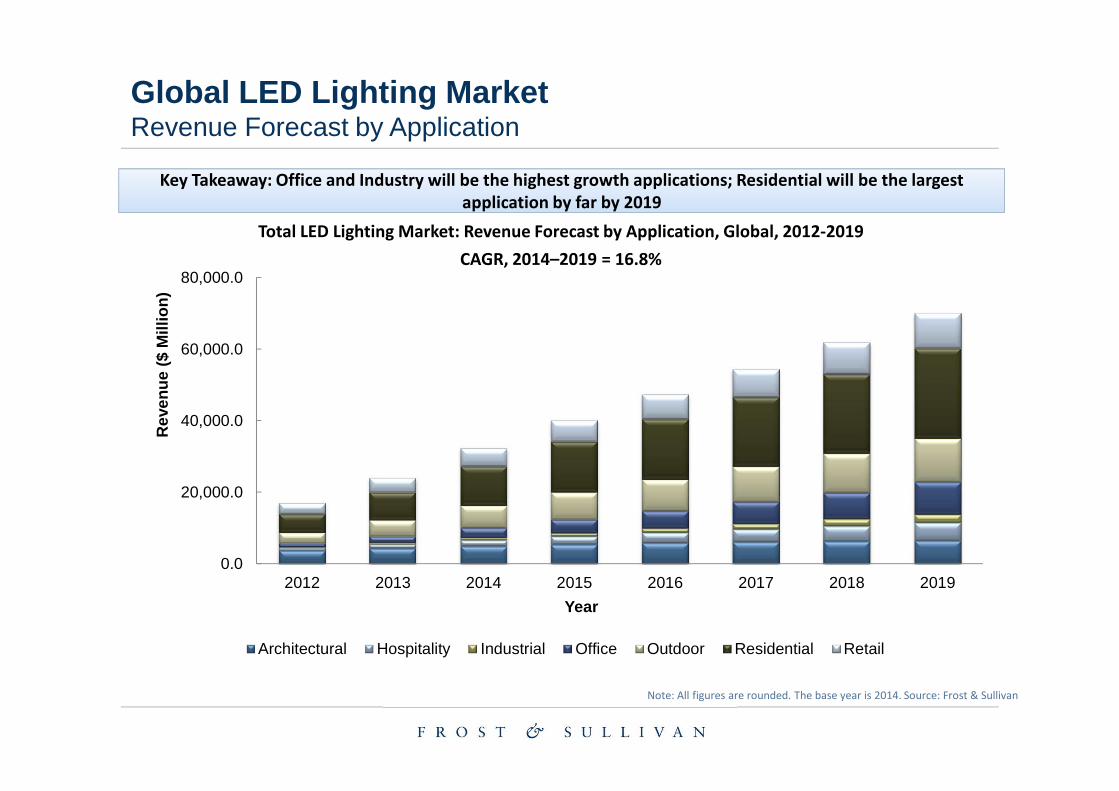

Global LED Lighting MarketRevenue Forecast by Application

Key Takeaway: Office and Industry will be the highest growth applications; Residential will be the largest

application by far by 2019

Key Takeaway: Office and Industry will be the highest growth applications; Residential will be the largest

application by far by 2019

Note: All figures are rounded. The base year is 2014. Source: Frost & Sullivan

Total LED Lighting Market: Revenue Forecast by Application, Global, 2012-2019

CAGR, 2014–2019 = 16.8%

0.0

20,000.0

40,000.0

60,000.0

80,000.0

2012 2013 2014 2015 2016 2017 2018 2019

Rev

enue

($

Mill

ion)

Year

Architectural Hospitality Industrial Office Outdoor Residential Retail

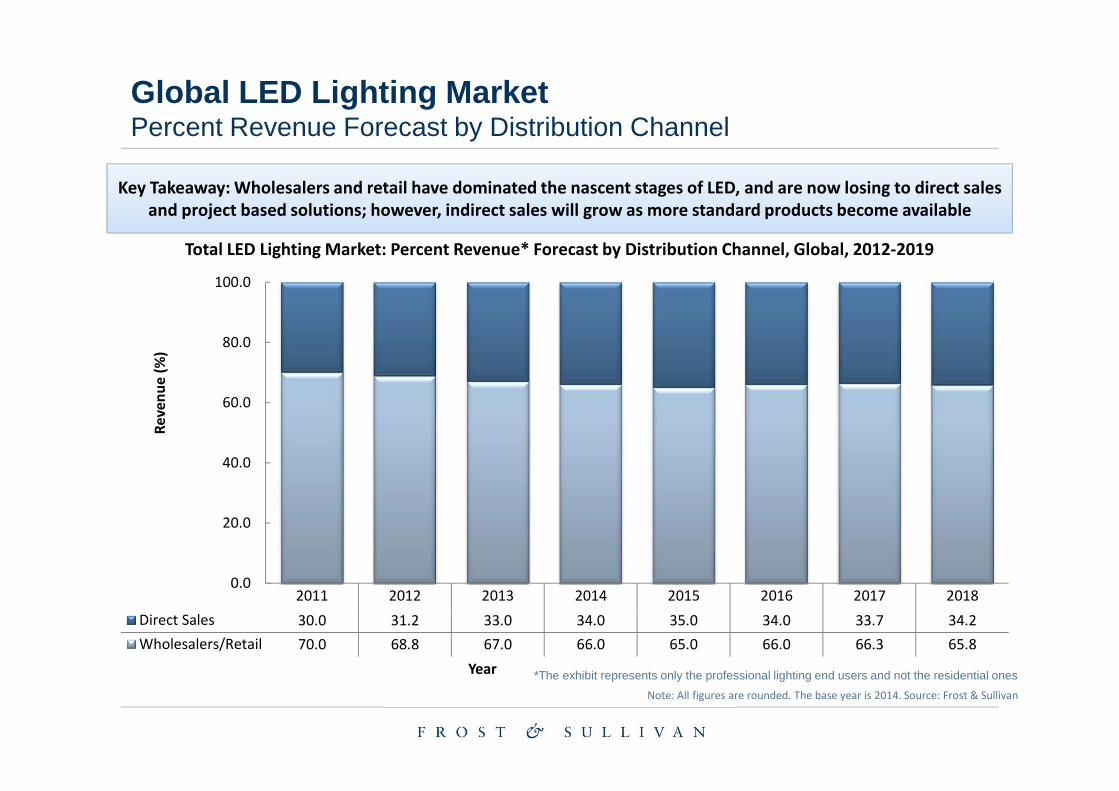

Global LED Lighting MarketPercent Revenue Forecast by Distribution Channel

Key Takeaway: Wholesalers and retail have dominated the nascent stages of LED, and are now losing to direct sales

and project based solutions; however, indirect sales will grow as more standard products become available

0.0

20.0

40.0

60.0

80.0

100.0

2011 2012 2013 2014 2015 2016 2017 2018

Direct Sales 30.0 31.2 33.0 34.0 35.0 34.0 33.7 34.2

Wholesalers/Retail 70.0 68.8 67.0 66.0 65.0 66.0 66.3 65.8

Re

ve

nu

e (

%)

Year

Note: All figures are rounded. The base year is 2014. Source: Frost & Sullivan

Total LED Lighting Market: Percent Revenue* Forecast by Distribution Channel, Global, 2012-2019

*The exhibit represents only the professional lighting end users and not the residential ones

Global LED Lighting MarketKey Messages

2

LED replacement lamps are already at a price

point that successfully challenge traditional

technologies and will take over that market

completely by 2020.

3

The challenge is to offer noncommoditised

products that make the most of digital LED light

advantages. LED drivers and lighting

management services will be key.

4

The market for luminaires will be particularly

challenged, as LED requires new knowledge and

expensive R&D. Concentration in this very

fragmented market is expected.

5

New markets for services and solution designs

open up, but require good contacts and

customer knowledge, which might favour local

companies above global participants.

1

The LED revolution has happened, driven by

Europe, North America, and China. Further

growth will be less centralised and will challenge

the leading global participants.

Source: Frost & Sullivan

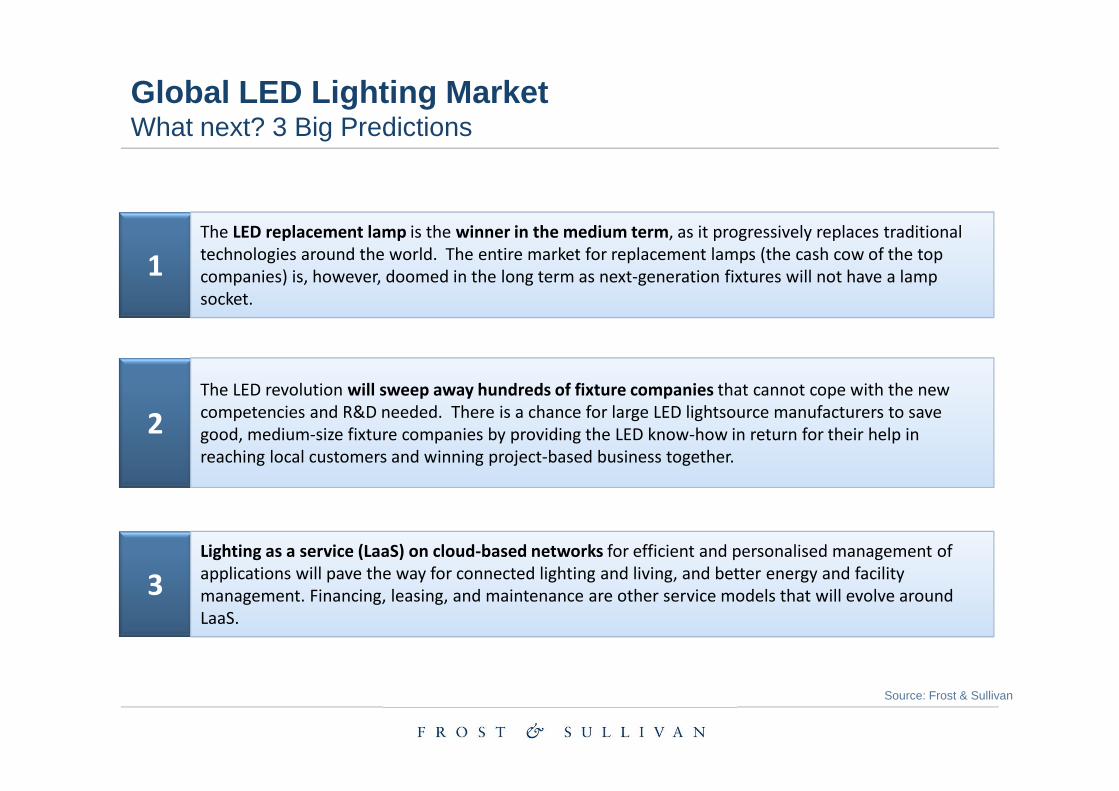

Global LED Lighting MarketWhat next? 3 Big Predictions

Source: Frost & Sullivan

2

The LED revolution will sweep away hundreds of fixture companies that cannot cope with the new

competencies and R&D needed. There is a chance for large LED lightsource manufacturers to save

good, medium-size fixture companies by providing the LED know-how in return for their help in

reaching local customers and winning project-based business together.

3

Lighting as a service (LaaS) on cloud-based networks for efficient and personalised management of

applications will pave the way for connected lighting and living, and better energy and facility

management. Financing, leasing, and maintenance are other service models that will evolve around

LaaS.

1

The LED replacement lamp is the winner in the medium term, as it progressively replaces traditional

technologies around the world. The entire market for replacement lamps (the cash cow of the top

companies) is, however, doomed in the long term as next-generation fixtures will not have a lamp

socket.

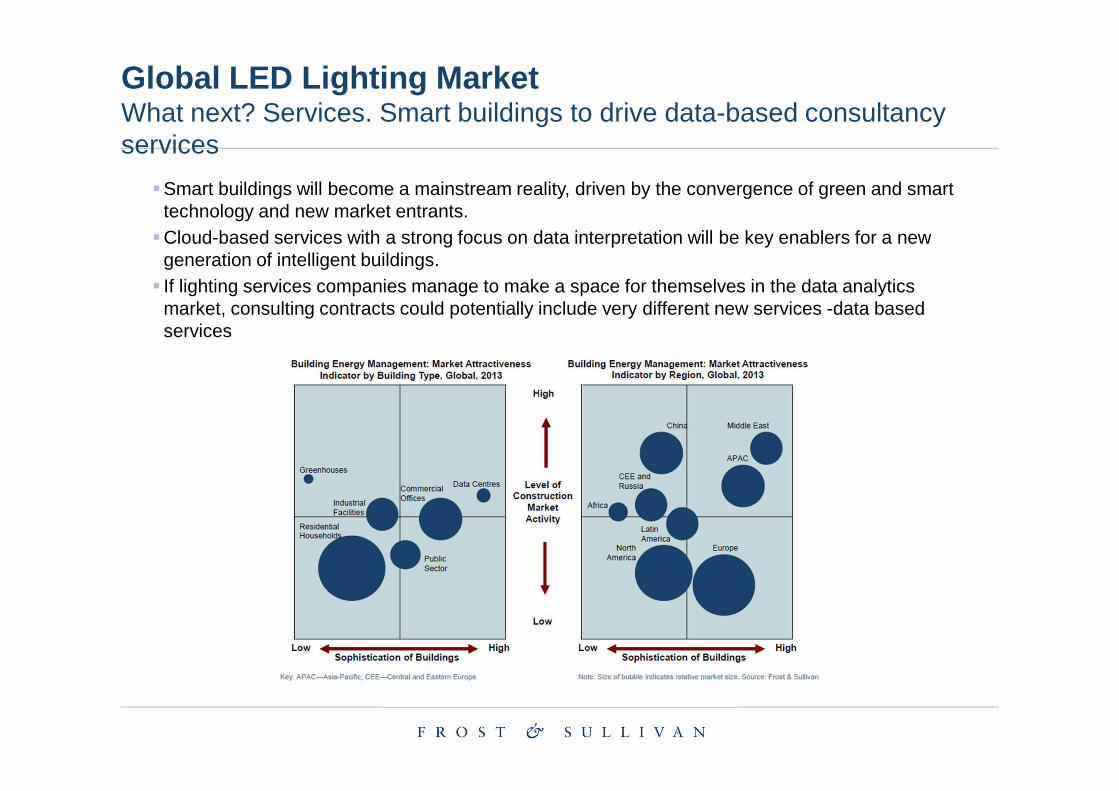

Key Key Takeaway: Offices to focus on energy saving aspects, residential to focus on ambience

Global LED MarketWhat next? Leveraging Lighting Management Systems to target verticals

Global LED Lighting MarketWhat next? Services. Smart buildings, performance contracting and light-as-a-service are key trends driving future growth

Key Trends

• Smart buildings, representing the convergence of green and smart technology trends, will become increasingly important and a driver for consultancy based services.

• Performance contracting is increasingly becoming a mainstay of the market; end users are keen to maximise cost savings and improve efficiency.

• Light-as-a-service (essentially leasing-type models and ‘pay-as-you-use’ services) is a concept that is gaining traction in the industry through its ability to enable businesses to minimise upfront capital expenditure.

Competitive Landscape

• The increasing importance and value of lighting projects is attracting ever greater competition within the sector.

• BMS & FM companies are both actively targeting the sector.

Competitive Success Factors

• Market participants need to be able to work in partnership with BMS companies, and need to be able to work with not just light but also HVAC etc. With strong growth forecast, establishing a market presence, a network of connections, and customer relationships will be vital for future success. Supplies want to establish an entrenched position.

• With performance contracting becoming the customers’ preferred business model, suppliers will need to develop service capabilities, or partner with facility management companies, or energy service providers, to participate in the most dynamic part of the market.

Global LED Lighting MarketWhat next? Services. Smart buildings to drive data-based consultancy services

�Smart buildings will become a mainstream reality, driven by the convergence of green and smart technology and new market entrants.

�Cloud-based services with a strong focus on data interpretation will be key enablers for a new generation of intelligent buildings.

� If lighting services companies manage to make a space for themselves in the data analytics market, consulting contracts could potentially include very different new services -data based services

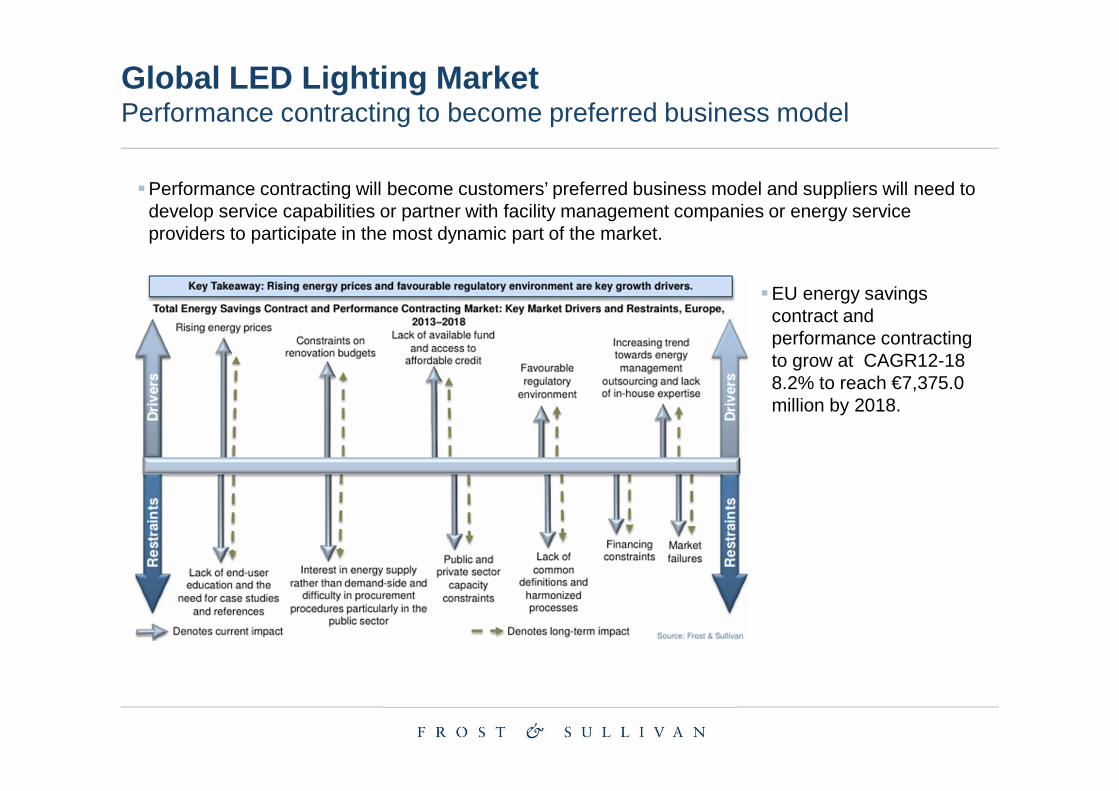

Global LED Lighting MarketPerformance contracting to become preferred business model

�Performance contracting will become customers’ preferred business model and suppliers will need to develop service capabilities or partner with facility management companies or energy service providers to participate in the most dynamic part of the market.

�EU energy savings contract and performance contracting to grow at CAGR12-18 8.2% to reach €7,375.0 million by 2018.

Global LED Lighting MarketLight-as-a-service (LAAS)

�Future trends in terms of business models include leasing-type models and ‘pay-as-you-use’ services.

�The concept of light-as-a-service is expected by most market participants to pick-up as a service offering in the future . Key advantages for the end-customer is the ability to use new technology, increase comfort levels, and bringing related energy savings, whilst taking away the up-front weight on the balance sheet of customers.

�Where budgeting is a barrier for upgrades/retrofit, lease-type services will strive . Uptake is expected to be faster in the industrial and public sectors.

�X-as-a-service proposition is developing in adjacent and unrelated markets, and is proving a success story. It would be interesting to study how quickly this type of services have picked up in other markets (penetration rate), to understand typical conditions for success, and learn from these other industries.

� As reference, in the European passenger vehicle market, one of the oldest leasing markets, the share of leased cars was 19% in 2011 and will grow to 23% by 2018.

18

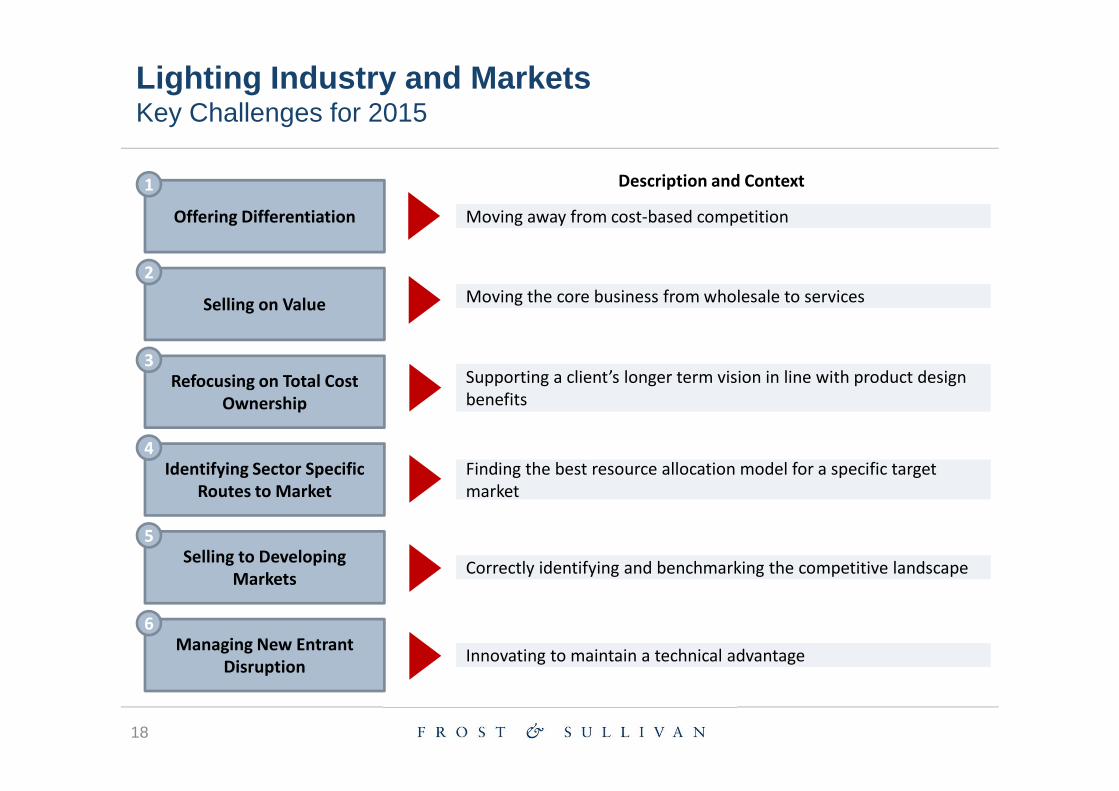

Lighting Industry and MarketsKey Challenges for 2015

Offering Differentiation

Selling on Value

Refocusing on Total Cost

Ownership

Identifying Sector Specific

Routes to Market

Selling to Developing

Markets

Managing New Entrant

Disruption

1

2

3

4

5

6

Moving away from cost-based competition

Moving the core business from wholesale to services

Supporting a client’s longer term vision in line with product design

benefits

Finding the best resource allocation model for a specific target

market

Correctly identifying and benchmarking the competitive landscape

Innovating to maintain a technical advantage

Description and Context

19

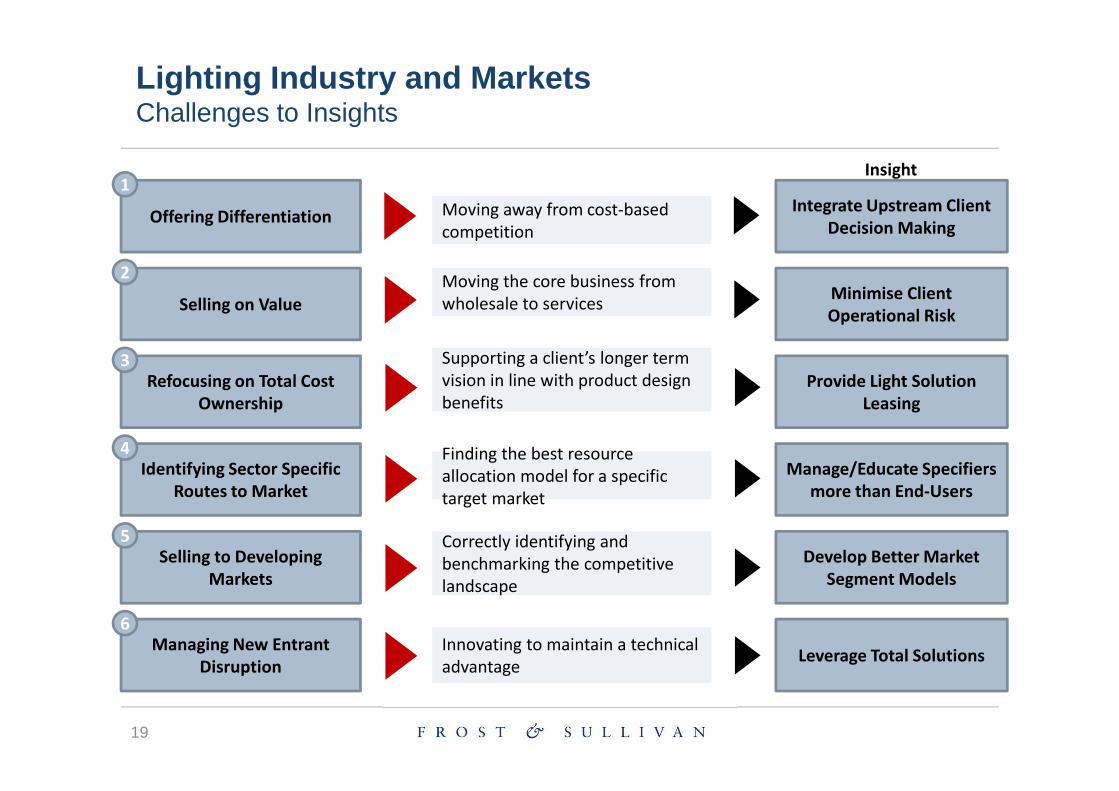

Lighting Industry and MarketsChallenges to Insights

Offering Differentiation

Selling on Value

Refocusing on Total Cost

Ownership

Identifying Sector Specific

Routes to Market

Selling to Developing

Markets

Managing New Entrant

Disruption

1

2

3

4

5

6

Moving away from cost-based

competition

Moving the core business from

wholesale to services

Supporting a client’s longer term

vision in line with product design

benefits

Finding the best resource

allocation model for a specific

target market

Correctly identifying and

benchmarking the competitive

landscape

Innovating to maintain a technical

advantage

Insight

Integrate Upstream Client

Decision Making

Minimise Client

Operational Risk

Provide Light Solution

Leasing

Manage/Educate Specifiers

more than End-Users

Develop Better Market

Segment Models

Leverage Total Solutions

![[ 01 ] Semiconductors – market of the future: Bosch …...The global semiconductor market is worth billions: the market research company Gartner expects global semiconductor sales](https://img.pdfslide.tips/doc/110x75/5fc38fb3c30e7051e35d15c5/-01-semiconductors-a-market-of-the-future-bosch-the-global-semiconductor.jpg)