Embed Size (px)

Citation preview

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 1/20

Chapter Two Transaction Analysis

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 2/20

Transactions

• Business Transactions are events thathave a financial impact on the business(assign a $$ amount) and can bemeasured reliably.

• Transactions will impact the Assets,Liabilities, and Owners’ Equity of a firm.

• To analyze, determine how this impactsthe accounting equation (Assets =Liabilities + Owners’ Equity) of a firm.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 3/20

Accounts

• Accounts are a summary device thatrecord the changes that have occurredduring a period.

• Organizational system for businesses that

allow them to analyze the cumulativeeffects of transactions.

• Each account shows the effect of all of theincreases and decreases during a period.

• Accounts are organized via the basicaccounting equation (Assets =Liabilities + Owners’ Equity.)

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 4/20

Accounts

• Use a separate account for each particular:•Asset

•Liability

•Stockholders’ Equity (Owners’ Equity)

that is involved in a transaction. • Each transaction will affect at least two

accounts. This is reflective of the double-entrysystem used in accounting, which keeps the

accounting equation in balance.

**Know the different types of accounts on pages 50-52. You should also review the lecture material for Chapter 1.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 5/20

Transaction Analysis

• Remember, the accounting equation helpsto analyze the impact of transactions onfinancial position:

Assets = Liabilities + Owners’ Equity

**There are many examples of the analysis

of business transactions on pages 54-60 inthe text. Make sure to study andunderstand these examples.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 6/20

Debits and Credits

• Recall that each transaction affects atleast two accounts.

• In accounting, accounts can berepresented by the letter “T” andreferred to as T-accounts.

• Accountants designate:

• Left side of account = Debits.

• Right side of account = Credits.

Total Debits always equal total credits.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 7/20

Debits and Credits

Adapted from Harrison (2006)

Visualization of the T-Account

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 8/20

Debits and Credits

• Rules for Assets – on the left-handside of the accounting equation:

• Assets have a normal debit balance.*

• Increases in assets are recorded on theleft (debit) side.

• Decreases in assets are recorded on theright (credit) side.

*The “balance” in the account is calculated as the beginning balance (what wasin the account at the beginning of the period) + increases - decreases

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 9/20

Debits and Credits

• Rules for Liabilities and Owners’ Equity – onthe right-hand side of the accountingequation:

• Liabilities and Owners’ Equity (LOE) have a

normal credit balance.*• Increases in LOE are recorded on the right

(credit) side.

• Decreases in LOE are recorded on the left (debit)side.

*The “balance” in the account is calculated as the beginning balance (what was in the account at the beginning of the period) + increases - decreases

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 10/20

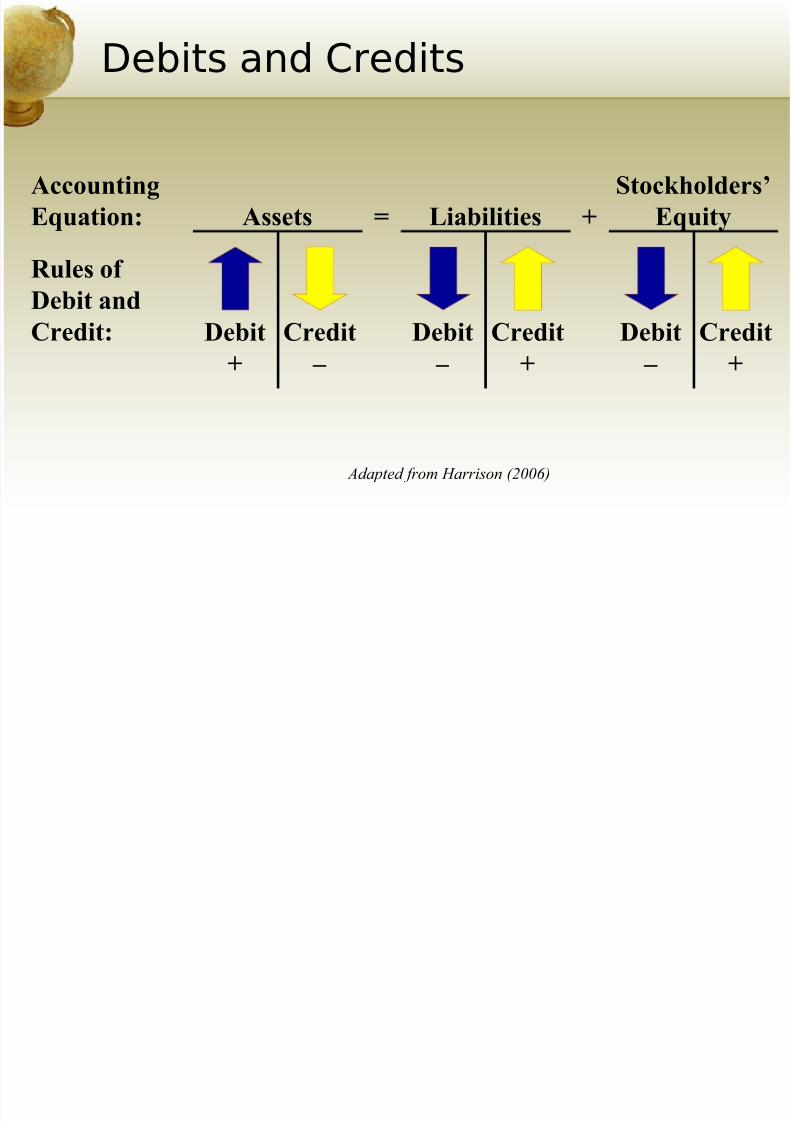

Debits and Credits

Accounting

Equation: Assets = Liabilities +

Stockholders’

Equity

Rules of Debit and

Credit: Debit

+

Debit

–

Debit

–

Credit

–

Credit

+

Credit

+

Adapted from Harrison (2006)

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 11/20

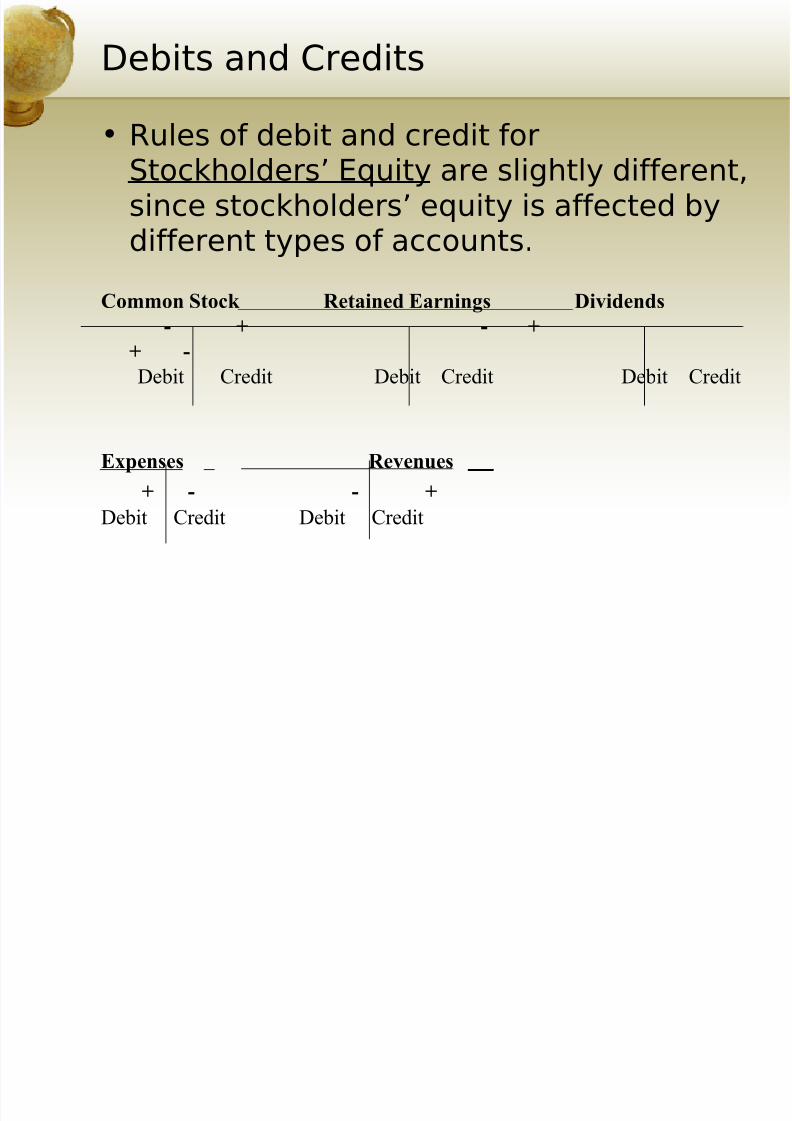

Debits and Credits

• Rules of debit and credit forStockholders’ Equity are slightly different,since stockholders’ equity is affected bydifferent types of accounts.

Common Stock Retained Earnings Dividends

- + - +

+ -

Debit Credit Debit Credit Debit Credit

Expenses Revenues

+ - - +

Debit Credit Debit Credit

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 12/20

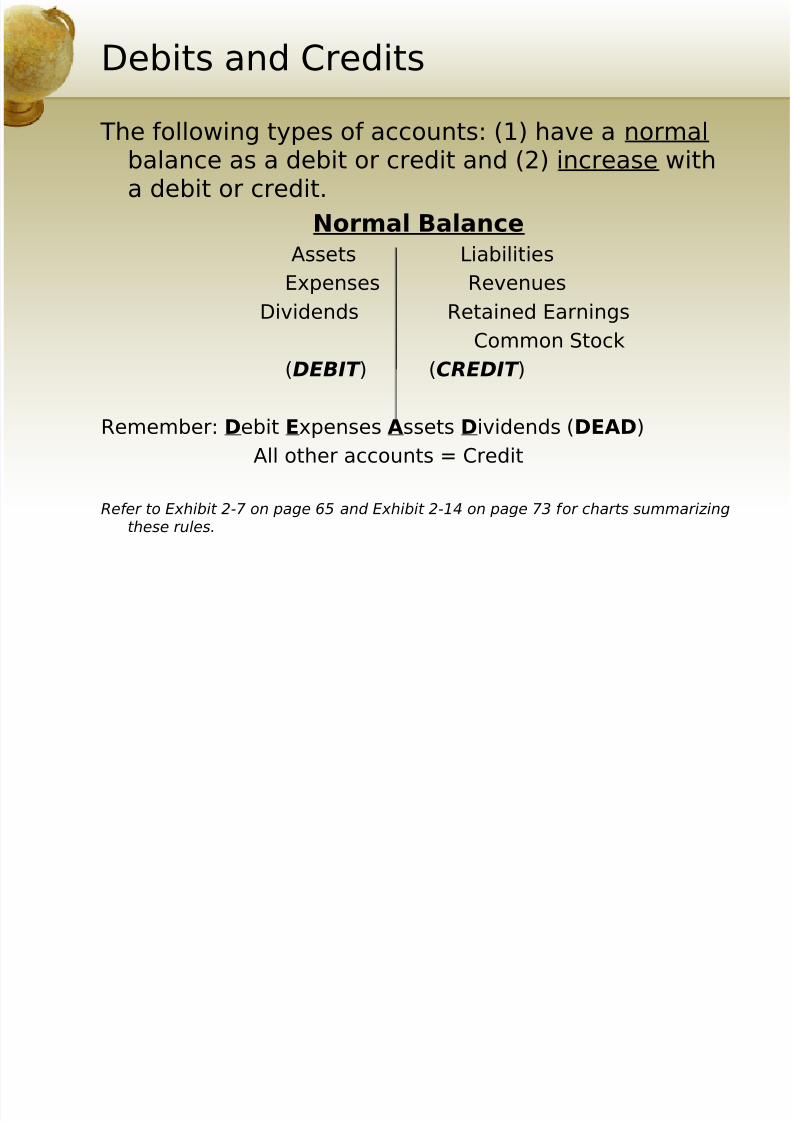

Debits and Credits

The following types of accounts: (1) have a normalbalance as a debit or credit and (2) increase witha debit or credit.

Normal Balance

Assets Liabilities

Expenses Revenues

Dividends Retained Earnings

Common Stock

(DEBIT ) (CREDIT )

Remember: Debit Expenses Assets Dividends (DEAD)

All other accounts = Credit

Refer to Exhibit 2-7 on page 65 and Exhibit 2-14 on page 73 for charts summarizingthese rules.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 13/20

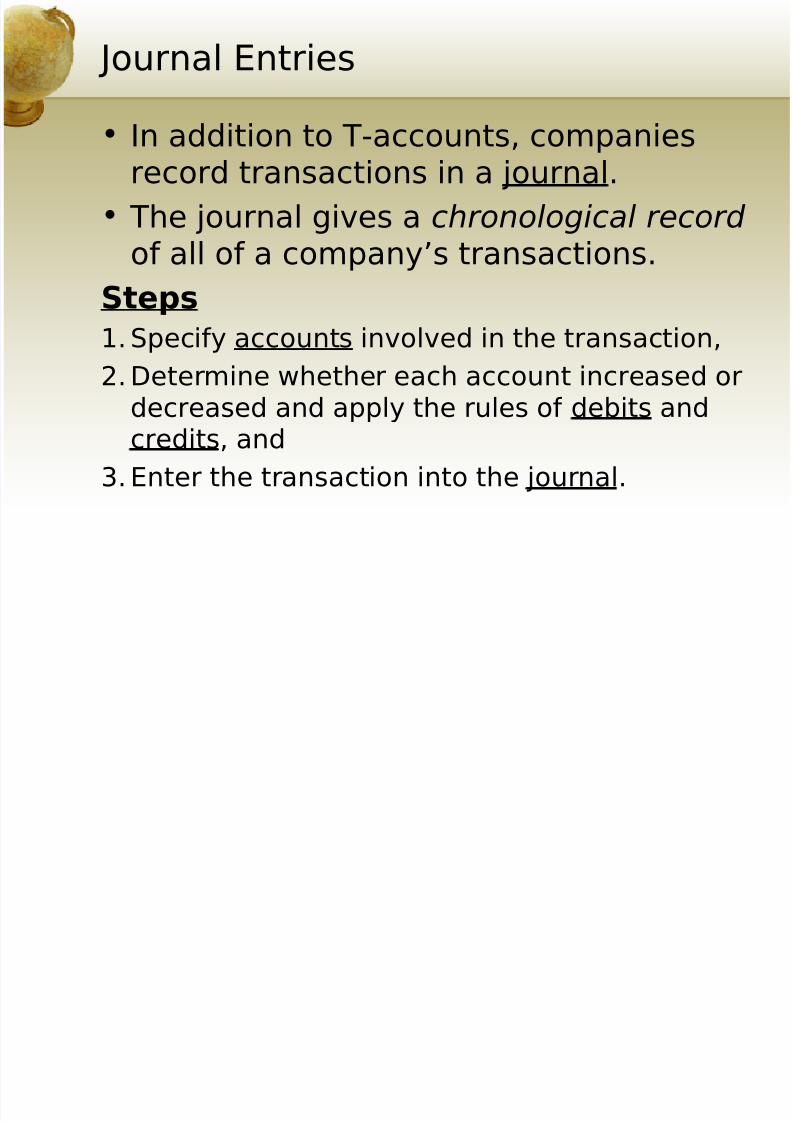

Journal Entries

• In addition to T-accounts, companiesrecord transactions in a journal.

• The journal gives a chronological record of all of a company’s transactions.

Steps

1. Specify accounts involved in the transaction,

2. Determine whether each account increased or

decreased and apply the rules of debits andcredits, and

3. Enter the transaction into the journal.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 14/20

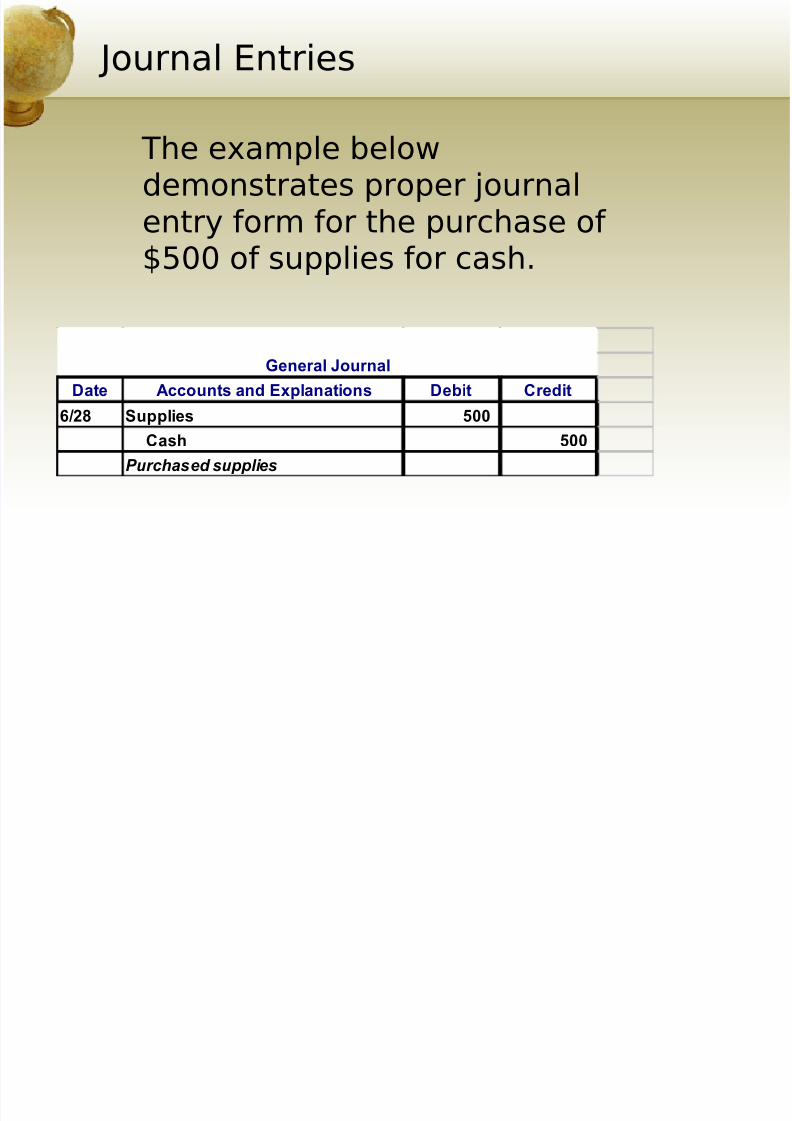

Journal Entries

General Journal

Date Accounts and Explanations Debit Credit

6/28 Supplies 500 Cash 500

Purchased supplies

The example belowdemonstrates proper journalentry form for the purchase of $500 of supplies for cash.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 15/20

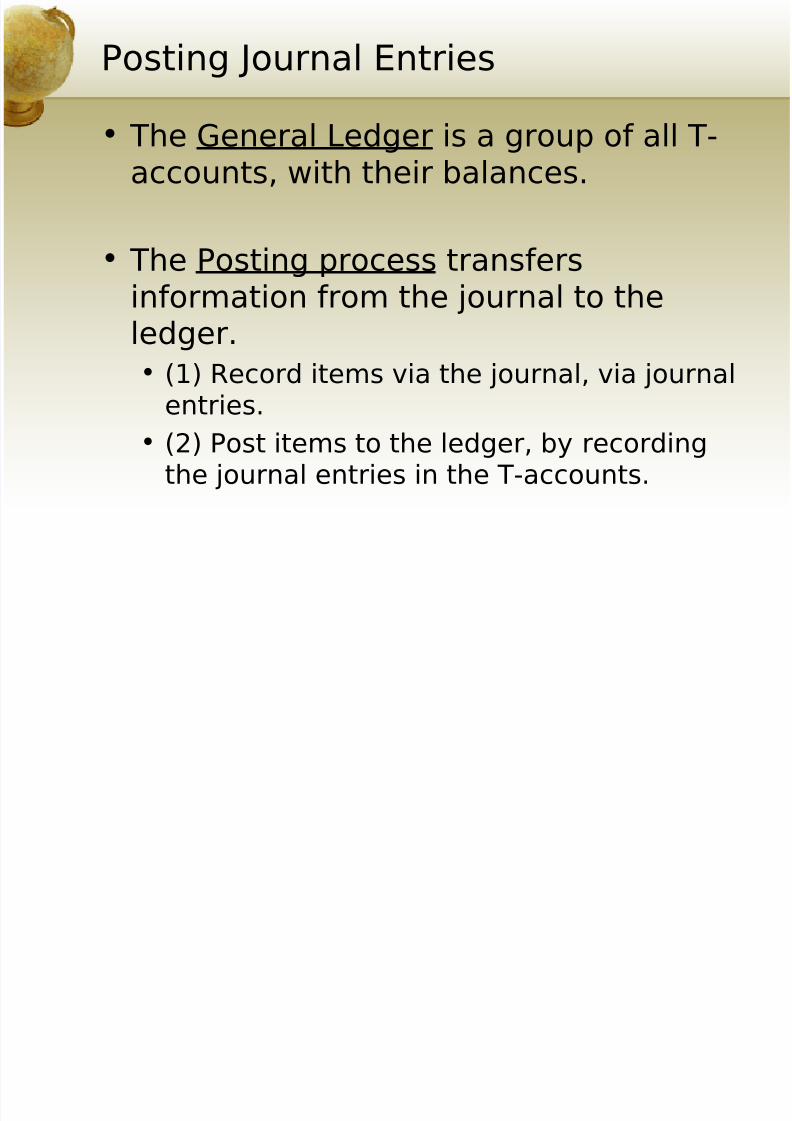

Posting Journal Entries

• The General Ledger is a group of all T-accounts, with their balances.

• The Posting process transfersinformation from the journal to theledger.

• (1) Record items via the journal, via journal

entries.• (2) Post items to the ledger, by recording

the journal entries in the T-accounts.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 16/20

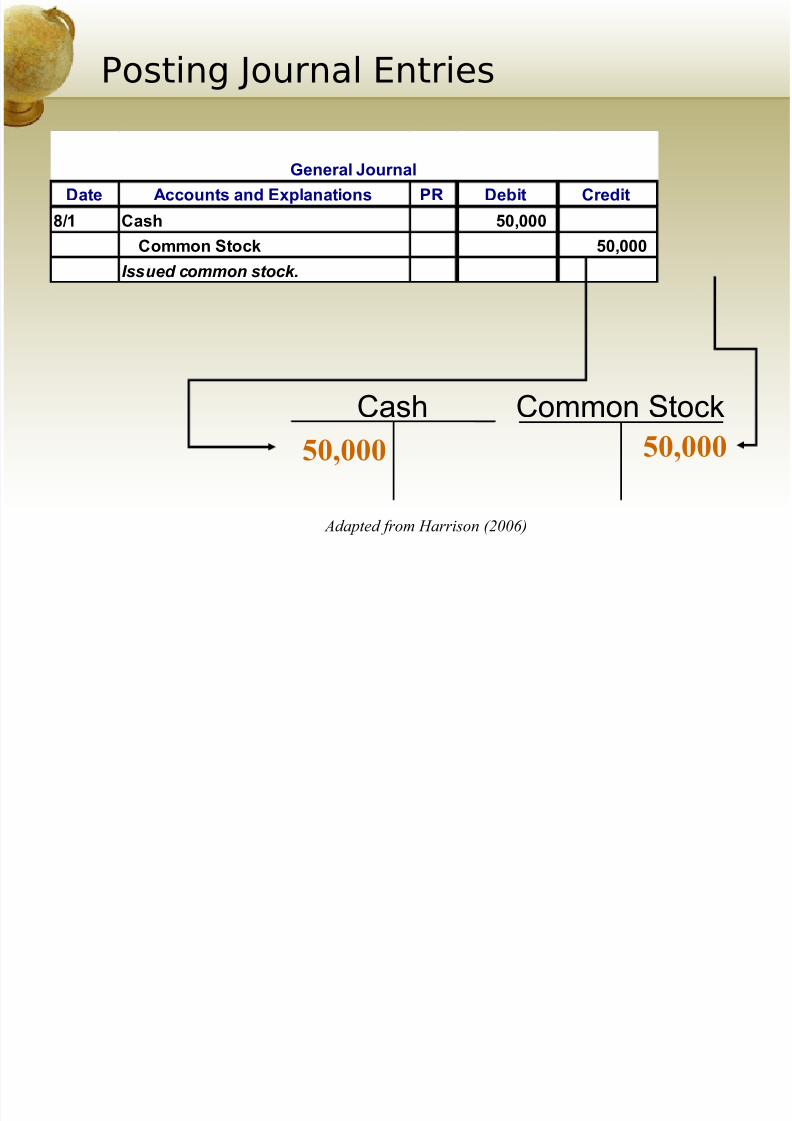

Posting Journal Entries

50,000

General Journal

Date Accounts and Explanations PR Debit Credit

8/1 Cash 50,000

Common Stock 50,000

Issued common stock.

50,000Cash Common Stock

Adapted from Harrison (2006)

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 17/20

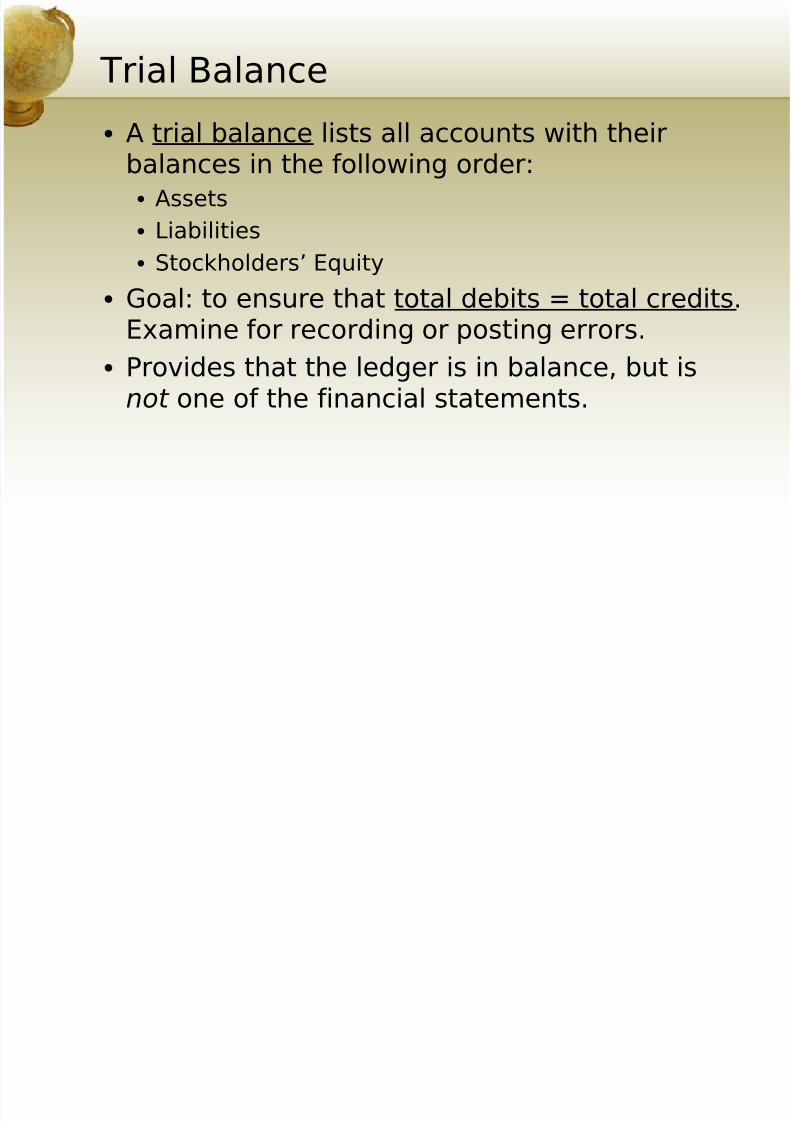

Trial Balance

• A trial balance lists all accounts with theirbalances in the following order:

• Assets

• Liabilities

• Stockholders’ Equity

• Goal: to ensure that total debits = total credits.Examine for recording or posting errors.

• Provides that the ledger is in balance, but isnot one of the financial statements.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 18/20

Trial Balance

• Common Errors in the TrialBalance:

• Missing accounts

• Reversal of debits or credits• Divide the account by 2 to detect

• Mathematical errors

• Divide the account by 9 to detect

• Slide

• Transposition

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 19/20

Chart of Accounts

• A chart of accounts is a listing of all of acompany’s accounts and their accountnumbers.

• Referenced when posting journal

entries or deciding how to codetransactions.

• Additional accounts may be added as a

company participates in additionaltransactions.

8/14/2019 Ucf Acg2021 Ch 2 Ppt

http://slidepdf.com/reader/full/ucf-acg2021-ch-2-ppt 20/20

Questions?

• Any questions or concerns?

![Ch 06 - My PPT [F07]](https://img.pdfslide.tips/doc/110x75/577d34c91a28ab3a6b8ed8a1/ch-06-my-ppt-f07.jpg)