Embed Size (px)

Citation preview

Project: VIX indexand CDS spreadNational Economics University

Advanced Finance Program intake 50

2011

9/12/2011

Group students:

Nguyễn Thị Thu Hà

Nguyễn Thị Ngọc Hà

Phạm Quang Huy

Quản Thị Hạnh Mai

I. Definitions

1. Credit default swap (CDS)

a. Definition:

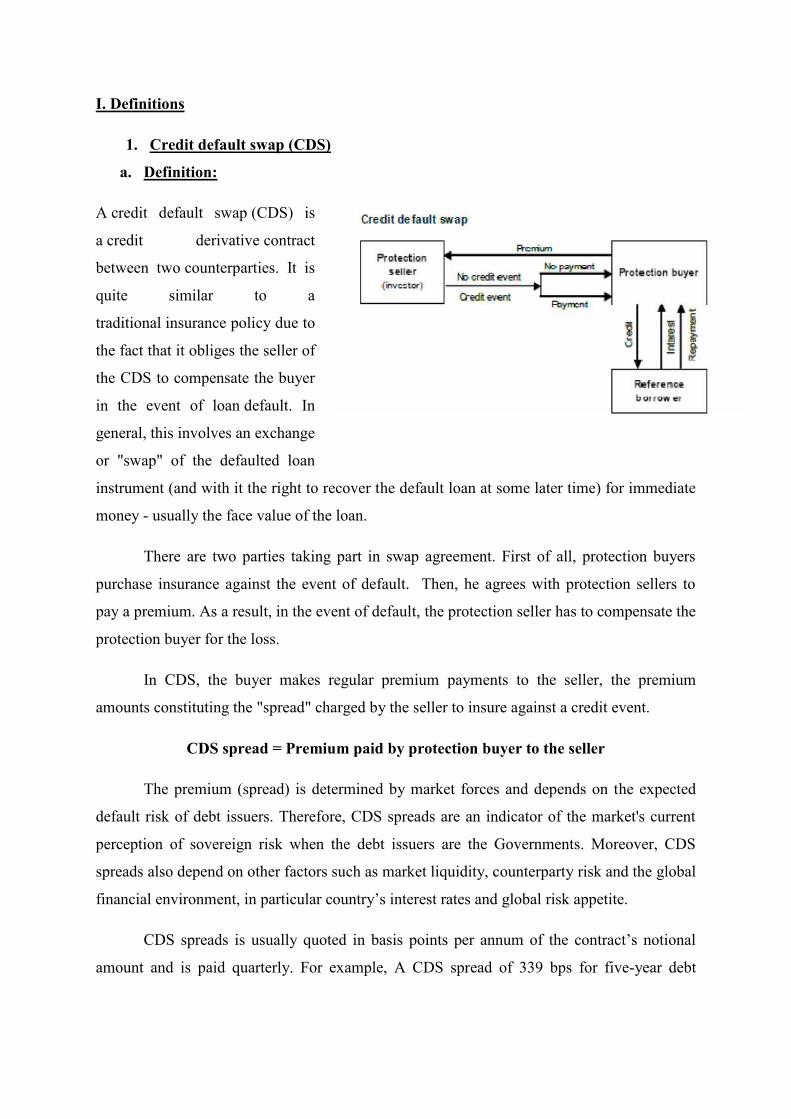

A credit default swap (CDS) is

a credit derivative contract

between two counterparties. It is

quite similar to a

traditional insurance policy due to

the fact that it obliges the seller of

the CDS to compensate the buyer

in the event of loan default. In

general, this involves an exchange

or "swap" of the defaulted loan

instrument (and with it the right to recover the default loan at some later time) for immediate

money - usually the face value of the loan.

There are two parties taking part in swap agreement. First of all, protection buyers

purchase insurance against the event of default. Then, he agrees with protection sellers to

pay a premium. As a result, in the event of default, the protection seller has to compensate the

protection buyer for the loss.

In CDS, the buyer makes regular premium payments to the seller, the premium

amounts constituting the "spread" charged by the seller to insure against a credit event.

CDS spread = Premium paid by protection buyer to the seller

The premium (spread) is determined by market forces and depends on the expected

default risk of debt issuers. Therefore, CDS spreads are an indicator of the market's current

perception of sovereign risk when the debt issuers are the Governments. Moreover, CDS

spreads also depend on other factors such as market liquidity, counterparty risk and the global

financial environment, in particular country’s interest rates and global risk appetite.

CDS spreads is usually quoted in basis points per annum of the contract’s notional

amount and is paid quarterly. For example, A CDS spread of 339 bps for five-year debt

means that default insurance for a notional amount of $1 million costs $ 33,900 per annum;

this premium is paid quarterly (or $ 8,475 per quarter).

Features

There is negative correlation between a company stock price and its CDS spreads. If

the outlook for a company improves and its share price should go up then its CDS spread

should tighten. It can be explained that the company has less probability to default so the

CDS will decline. On the other hand, if company or market’s outlook deteriorates then CDS

spread should widen and its stock price will decline to reflect the bad situation. Thus, it can

be said that the worse the credit rating, the higher the CDS spread. Nevertheless, there is still

a special situation in which the inverse correlation between a company's stock price and CDS

spread breaks down. This is when the companies apply Leveraged buyout (LBO). Frequently

this leads to the company's CDS spread widening due to the extra debt. But at the same time,

the share price increases, since buyers of a company usually end up paying a premium.

How do CDS spreads relate to the probability of default? The simple case

For simplicity, consider a 1-year CDS contract and assume that the total premium is

paid up front.

Let S: CDS spread (premium), p: default probability, R: recovery rate

When two parties enter a CDS trade, S is set so that the value of the swap transaction is zero,

i.e.

S= (1-R) p

S/ (1-R) =p

Example: If the recovery rate is 40%, a spread of 200 bps would translate into an implied

probability of default of 3.3%.

So a spread of 200 basis points is equivalent to the notion that the market is pricing in an

annual chance of about 3% that the issuing government will default.

2. VIX

In 1993, the first VIX, introduced by Prof. Robert Whaley at Vanderbilt

University, was a weighted measure of the implied volatility of eight S&P 100 at-the-money

put and call options. Ten years later, it expanded to use options based on a broader index, the

S&P 500, which allows for a more accurate view of investors' expectations on future market

volatility.

By definition, VIX is the ticker symbol for the Chicago Board Options Exchange

Market Volatility Index, a popular measure of the implied volatility of S&P 500 index

options. The index is calculated using the price of near-term options on S&P 500 index.

Because the value of an option is closely linked to the expected volatility of its underlying

security, options prices can be a useful indicator of investors' expectations of volatility. Thus,

people might call VIX as the "fear index" because a high VIX represents uncertainty about

future prices (over next 30 days period).

The VIX is quoted in percentage points and translates, roughly, to the expected

movement in the S&P 500 index over the next 30-day period, which is then annualized.

Given an example, if the VIX is 15 means an expected annualized change of 15% over the

next 30 days, it then can implies that the index option markets expect the S&P 500 to move

up or down (1.15%)1 / 12 = 1.17% over the next 30-day period.

By taking the weighted average of implied volatility for the Standard and Poor's

Index, this index can point out number of critical things to investor looking at the near future

market.

-A low VIX indicates trader’s confidence with low volatility of market.

-A high VIX indicates indicate that investors expect the value of the S&P 500 to fluctuate

wildly - up, down, or both - in the next 30 days.

In practice, VIX which is greater than 30 are generally implies a large amount

of volatility as a result of investor fear or uncertainty, while value below 20

generally corresponds to less stressful period in the markets.

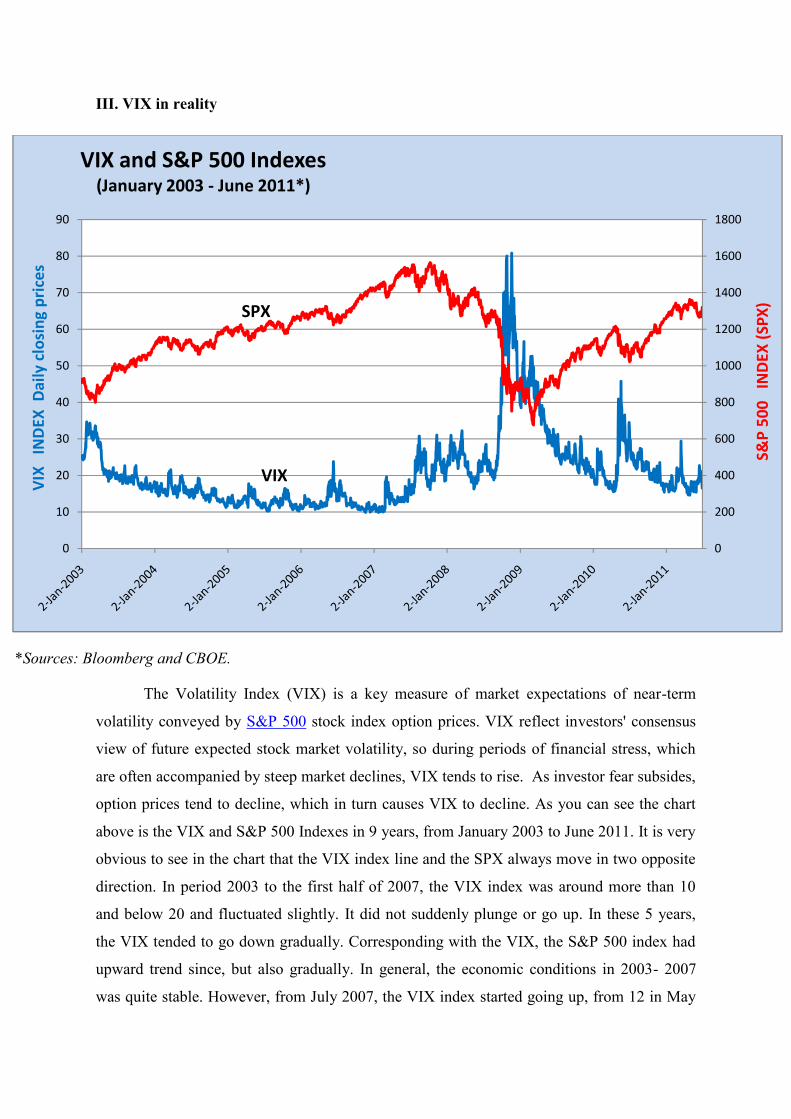

III. VIX in reality

*Sources: Bloomberg and CBOE.

The Volatility Index (VIX) is a key measure of market expectations of near-term

volatility conveyed by S&P 500 stock index option prices. VIX reflect investors' consensus

view of future expected stock market volatility, so during periods of financial stress, which

are often accompanied by steep market declines, VIX tends to rise. As investor fear subsides,

option prices tend to decline, which in turn causes VIX to decline. As you can see the chart

above is the VIX and S&P 500 Indexes in 9 years, from January 2003 to June 2011. It is very

obvious to see in the chart that the VIX index line and the SPX always move in two opposite

direction. In period 2003 to the first half of 2007, the VIX index was around more than 10

and below 20 and fluctuated slightly. It did not suddenly plunge or go up. In these 5 years,

the VIX tended to go down gradually. Corresponding with the VIX, the S&P 500 index had

upward trend since, but also gradually. In general, the economic conditions in 2003- 2007

was quite stable. However, from July 2007, the VIX index started going up, from 12 in May

0

200

400

600

800

1000

1200

1400

1600

1800

0

10

20

30

40

50

60

70

80

90

S&P

500

IN

DEX

(SPX

)

VIX

IN

DEX

Dai

ly c

losi

ng p

rice

s

VIX and S&P 500 Indexes(January 2003 - June 2011*)

SPX

VIX

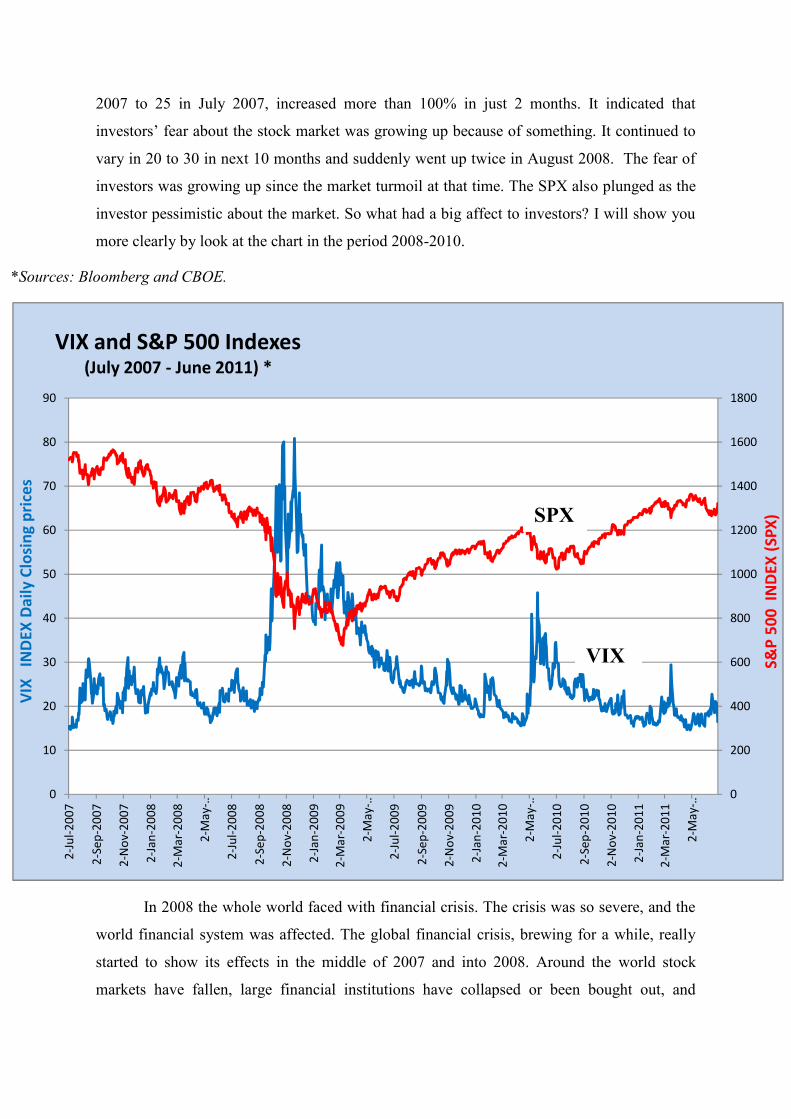

2007 to 25 in July 2007, increased more than 100% in just 2 months. It indicated that

investors’ fear about the stock market was growing up because of something. It continued to

vary in 20 to 30 in next 10 months and suddenly went up twice in August 2008. The fear of

investors was growing up since the market turmoil at that time. The SPX also plunged as the

investor pessimistic about the market. So what had a big affect to investors? I will show you

more clearly by look at the chart in the period 2008-2010.

*Sources: Bloomberg and CBOE.

In 2008 the whole world faced with financial crisis. The crisis was so severe, and the

world financial system was affected. The global financial crisis, brewing for a while, really

started to show its effects in the middle of 2007 and into 2008. Around the world stock

markets have fallen, large financial institutions have collapsed or been bought out, and

0

200

400

600

800

1000

1200

1400

1600

1800

0

10

20

30

40

50

60

70

80

90

2-Ju

l-200

7

2-Se

p-20

07

2-N

ov-2

007

2-Ja

n-20

08

2-M

ar-2

008

2-M

ay-…

2-Ju

l-200

8

2-Se

p-20

08

2-N

ov-2

008

2-Ja

n-20

09

2-M

ar-2

009

2-M

ay-…

2-Ju

l-200

9

2-Se

p-20

09

2-N

ov-2

009

2-Ja

n-20

10

2-M

ar-2

010

2-M

ay-…

2-Ju

l-201

0

2-Se

p-20

10

2-N

ov-2

010

2-Ja

n-20

11

2-M

ar-2

011

2-M

ay-…

S&P

500

IND

EX (S

PX)

VIX

IN

DEX

Dai

ly C

losi

ng p

rice

s

VIX and S&P 500 Indexes(July 2007 - June 2011) *

SPX

VIX

governments in even the wealthiest nations have had to come up with rescue packages to bail

out their financial systems. Because American financial firms followed the Subprime

Mortgage loan which allowed the consumers could borrow money even with substandard

credit rating. It created the housing bubble crisis, and became the global financial crisis. Both

investors and mortgage companies were in trouble. On the 14th September 2008, it came to

light that the financial services firm, Lehman Brothers, would file for bankruptcy after being

denied support by the Federal Reserve Bank. Later the same day, the Bank of America

announced that it would be purchasing Merrill Lynch. On the 16th September, the American

International Group (AIG) suffered due to its credit rating being reduced. Over the next two

weeks, more banks failed and the two remaining banks-Goldman Sachs and Morgan Stanley

converted into 'bank holding companies' so that they had more access to market liquidity.

Due to the above factors, there was major instability on the global stock markets with

major decreases in market value between the 15th and 17th of September 2008. In 17th

September, the VIX index closed at 36.22, increasing more than 6 with 16th.

In October 2008, the S&P 500 index fell from around nearly 1200 in September to hit

848.92, the lowest in the first 10 months of 2008. At the same time, the VIX also increased

rapidly to 80.06, the highest record until October 2008.

The situation was even worst in November when in 20th Nov, the SPX index dropped

to 752.44, the lowest in 2008; and the VIX hit the record of 80.86, the highest number in 16

years (from 1995 to 2010) (VIX has 21 years of history).

The double tops in the VIX index in 2 months showed a very obvious message:

investors were losing their confidence about the future of economy. Investors were afraid of

the high volatility of market, not only in U.S but in all over the world. Numerous plans were

put forward with intent to solve the crisis and in the end President George W. Bush and the

Secretary of the Treasury announced a $700 billion financial aid package intended to limit the

damage that the previous few week's events caused. The plan was received well by investors

on Wall Street and around the world. Government gave some simulation packages to improve

the situation, along with other solutions, the stock market recovered in around June 2009. The

VIX index also decreased and became more stable.

Although we only show the VIX index until June 2011, but after that, especially from

August 2011, the debt crisis in U.S and Euro zone emerged which made the big affect to

expectation of investors. The problems that have weighed on investors - The European debt

and fear of a new recession in the United States, in addition the under-expected reports about

unemployment, economic growth, hammered the stock market. Traders fear that one of the

continent's heavily indebted economies could default, an event that would ripple through the

global banking system and make it difficult for other European countries to borrow money.

Moreover, the U.S. economic growth is already slowing, and unemployment is stuck above 9

percent. In 9 September 2011, the Standard & Poor's 500 closed down 32, or 2.7 percent, at

1,154. The VIX closed up 4.2 at 38.52 in 9 September. 1

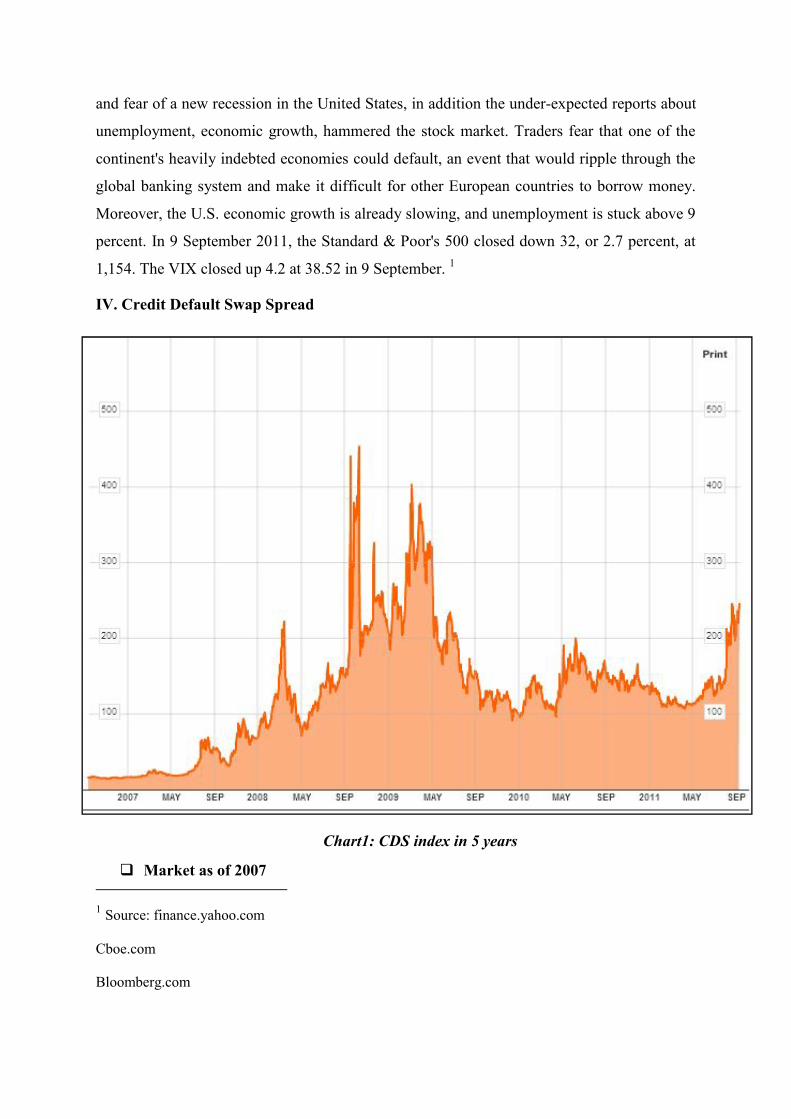

IV. Credit Default Swap Spread

Market as of 2007

1 Source: finance.yahoo.com

Cboe.com

Bloomberg.com

Chart1: CDS index in 5 years

- After U.S. house sales prices peaked in mid-2006 and began their steep decline forthwith,

refinancing became more difficult. As adjustable-rate mortgages began to reset at higher

interest rates, mortgage delinquencies soared, and securities backed with mortgages lost

most of their value. Concerns about the soundness of U.S. credit and financial markets led

to tightening credit around the world and slowing economic growth in the U.S. and

Europe. Initial subprime concerns appeared made CDS spread began its trend of

increasing.

- In the second half of 2007, Bear Stearns, a global investment bank and securities trading

and brokerage experienced difficulties. The most significant outcome was the record of

61 percent drop in net profits due to their hedge fund losses reported on September 21 in

New York Time note. CDS spread was widen during the last quarter of 2007.

- Fed's dramatic action that lowered rates by 50 bps cheered investors, which CDS spread

declined in August and September. However, from the beginning of October, the news

that U.S brokers reported huge losses and write downs, plus the failure of Bear Stearns,

stimulated the growth of CDS spread.

Market as of 2008

- In March 2008, Bear Stearns went to debacle and eventually led to its forced sale to JP

Morgan. In the days and weeks leading up to Bear’s collapse, the bank’s CDS spread

widened dramatically, indicating a surge of buyer talking out protection on the bank.

- During the middle of 2008, the fears concerning about Lehman, Fannie/Freddie and

monoclines (such as MBIA, Ambac) downgrade continuously raised the spread of CDS.

- On September 7, 2008, the Federal Housing Finance Agency (FHFA) announced that

Fannie Mae and Freddie Mac were being placed into its conservatorship.

- In September 2008, the bankruptcy of Lehman Brothers caused a drastically fluctuation

of CDS spread.

- Also in September, American International Group AIG required a federal bailout because

it had been excessively selling CDS protection without hedging against the possibility

that the reference entities might decline in value, which exposed the insurance giant to

potential losses over $100 billion.

- Lehman Brother auction settled the CDS smoothly.

- In November, DTCC announced that it would release market data on the outstanding

notional of CDS trades on weekly basic, and Intercontinental Exchange was granted to

begin guaranteeing credit default swaps.

Market as of 2010

- Stable due to recover of economy, improvement of investor expectation

- Some fluctuate and still high due to high deficit level of US government budget

Market as of 2011

- Still high due to Government deficit of Greece, Portugal, and many other countries in

Euro zone and US.

- Lower credit rating for US

V. Correlation and interpretation for VIX index and CDS spread

First of foremost, we will draw the route that our group will go through. To get the

ball rolling, we start by showing the correlation between VIX index and CDS spread in the

short term. Then we will pick up some key events over 6 years from 2007 to 2011, and

finally, we will show everything in long term and draw our conclusion about this relationship.

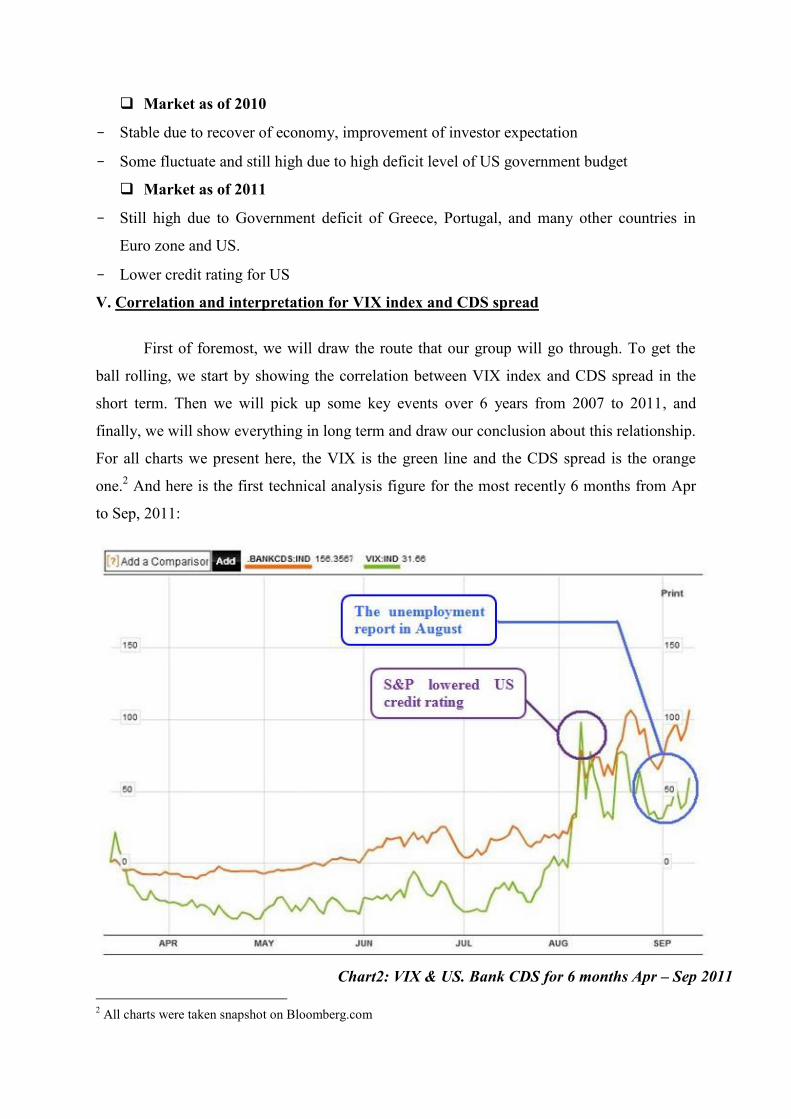

For all charts we present here, the VIX is the green line and the CDS spread is the orange

one.2 And here is the first technical analysis figure for the most recently 6 months from Apr

to Sep, 2011:

2 All charts were taken snapshot on Bloomberg.com

Chart2: VIX & US. Bank CDS for 6 months Apr – Sep 2011

As you can see via the chart, both VIX and CDS are moving quite similar to each

other over 6 months. The trend is fluctuating consistently between the two from Apr to at the

end of July. Significantly, we should focus on the 2 circle in the chart as we marked. As

looked at the violet circle, both VIX and CDS were raised incredibly, almost double

compared to four previous months (approximately 100 points). Indeed, this peak point was on

5 Aug, 2011, this day was considered as the first day in history the US was lowered down

credit rating by S&P. This news impacted a lot on investors and the economy as a whole, not

only US but also any countries which hold the US Government bonds. The VIX was high

also means that other basic indices decreased. That’s true when the DJIA, S&P500,

NASDAQ and other indices in Europe and Asia were so low the past few days. At the same

time, the CDS spread soared from 16.7 to 77.2 points.

The same story is for the second circle, the blue one. At the beginning of Sep, it was

time for US announced its unemployment report. In fact, the unemployment rate keeps level

up from the beginning of 2011 until now, about 9.1% recently. The bad news one more time

affected the market that forced president Obama had to take action. He also announced his

proposal 447 billion USD to create job and social stability. To react to the news, both VIX

and CDS spread immediately responded by the dropping more than 50 points for VIX and 20

points for CDS. As here we also disclose the relationship between the two in one year.

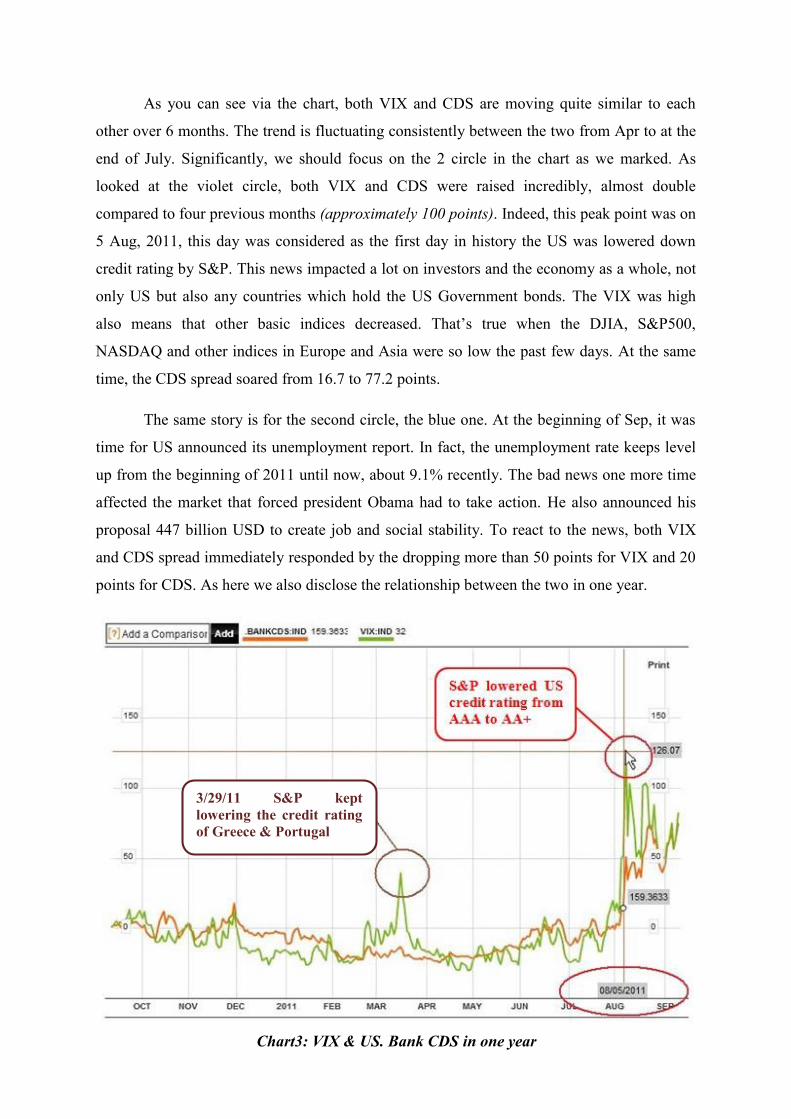

3/29/11 S&P keptlowering the credit ratingof Greece & Portugal

Chart3: VIX & US. Bank CDS in one year

Take a glance over one year, the two indices move closely to each other, except for

the brown circle, the time when S&P lowered credit rating of both Greece (BB-) and Portugal

(BBB-).

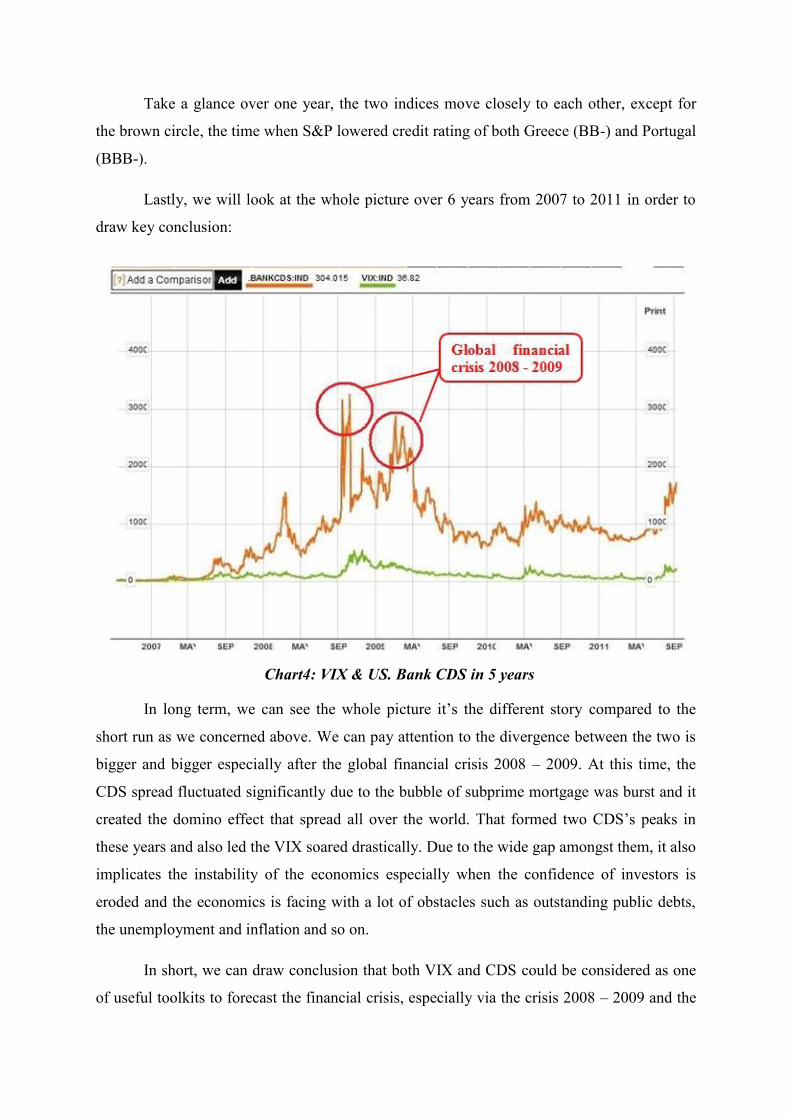

Lastly, we will look at the whole picture over 6 years from 2007 to 2011 in order to

draw key conclusion:

In long term, we can see the whole picture it’s the different story compared to the

short run as we concerned above. We can pay attention to the divergence between the two is

bigger and bigger especially after the global financial crisis 2008 – 2009. At this time, the

CDS spread fluctuated significantly due to the bubble of subprime mortgage was burst and it

created the domino effect that spread all over the world. That formed two CDS’s peaks in

these years and also led the VIX soared drastically. Due to the wide gap amongst them, it also

implicates the instability of the economics especially when the confidence of investors is

eroded and the economics is facing with a lot of obstacles such as outstanding public debts,

the unemployment and inflation and so on.

In short, we can draw conclusion that both VIX and CDS could be considered as one

of useful toolkits to forecast the financial crisis, especially via the crisis 2008 – 2009 and the

Chart4: VIX & US. Bank CDS in 5 years

national debts issue, the two shows us something in expectation toward the market and near

future. Or in other word, we can say about the relation amongst them is positive correlation.

Even no one what will happen to the market and no unique tool is perfect for forecasting, we

just use VIX and CDS like a referent ones before making any final conclusion.

![TUGAS I [VIX]](https://img.pdfslide.tips/doc/110x75/55cf97fc550346d03394db12/tugas-i-vix.jpg)