Embed Size (px)

Citation preview

Cognity Case studyAnalyzing Volatility: Assessment of September 2008 VIX Short in Dollars

Cognity Case Study

bisam.com

The challenges to overcome

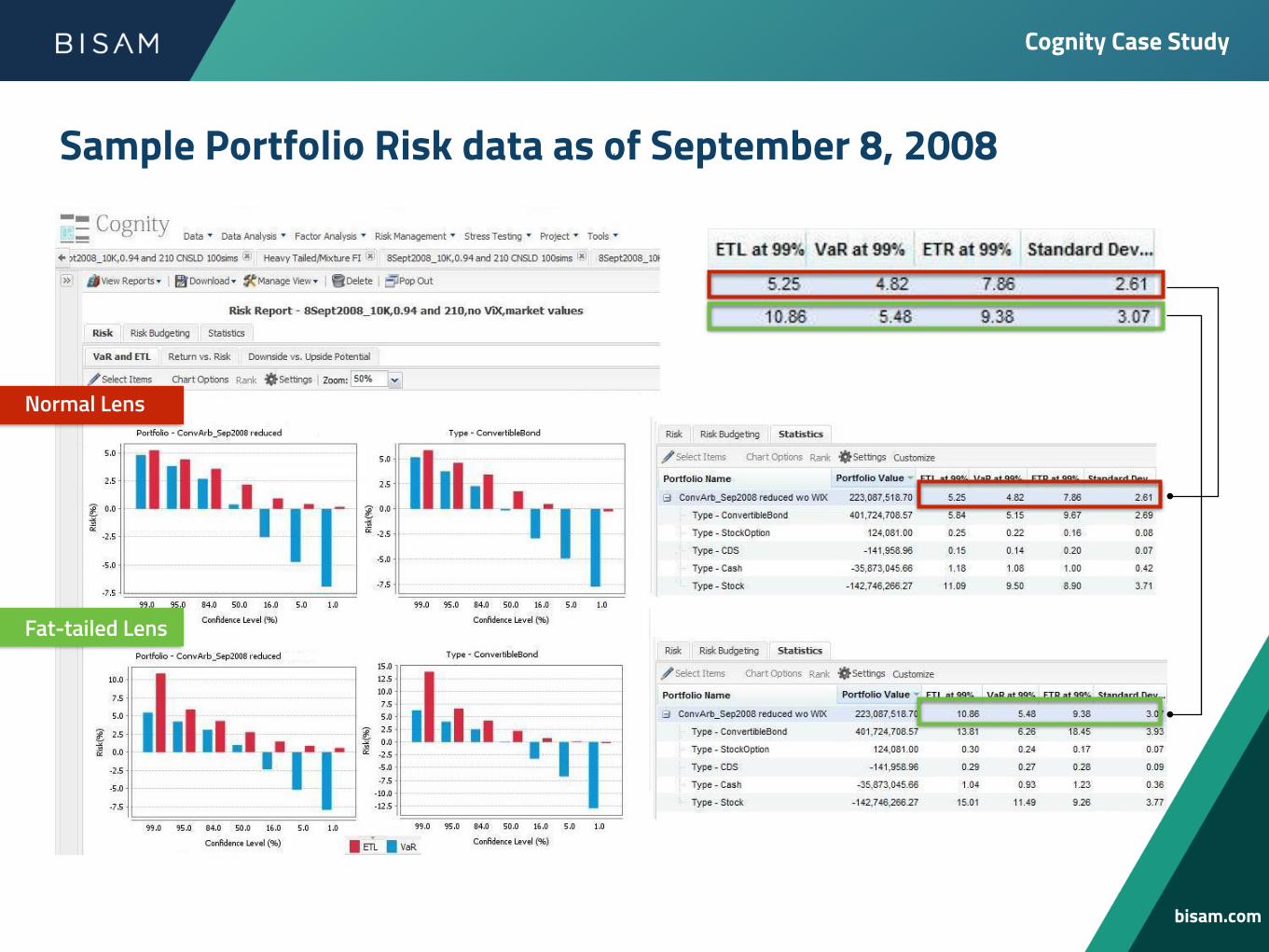

Sample Portfolio Risk data as of September 8, 2008

Normal Lens

Fat-tailed Lens

Cognity Case Study

bisam.com

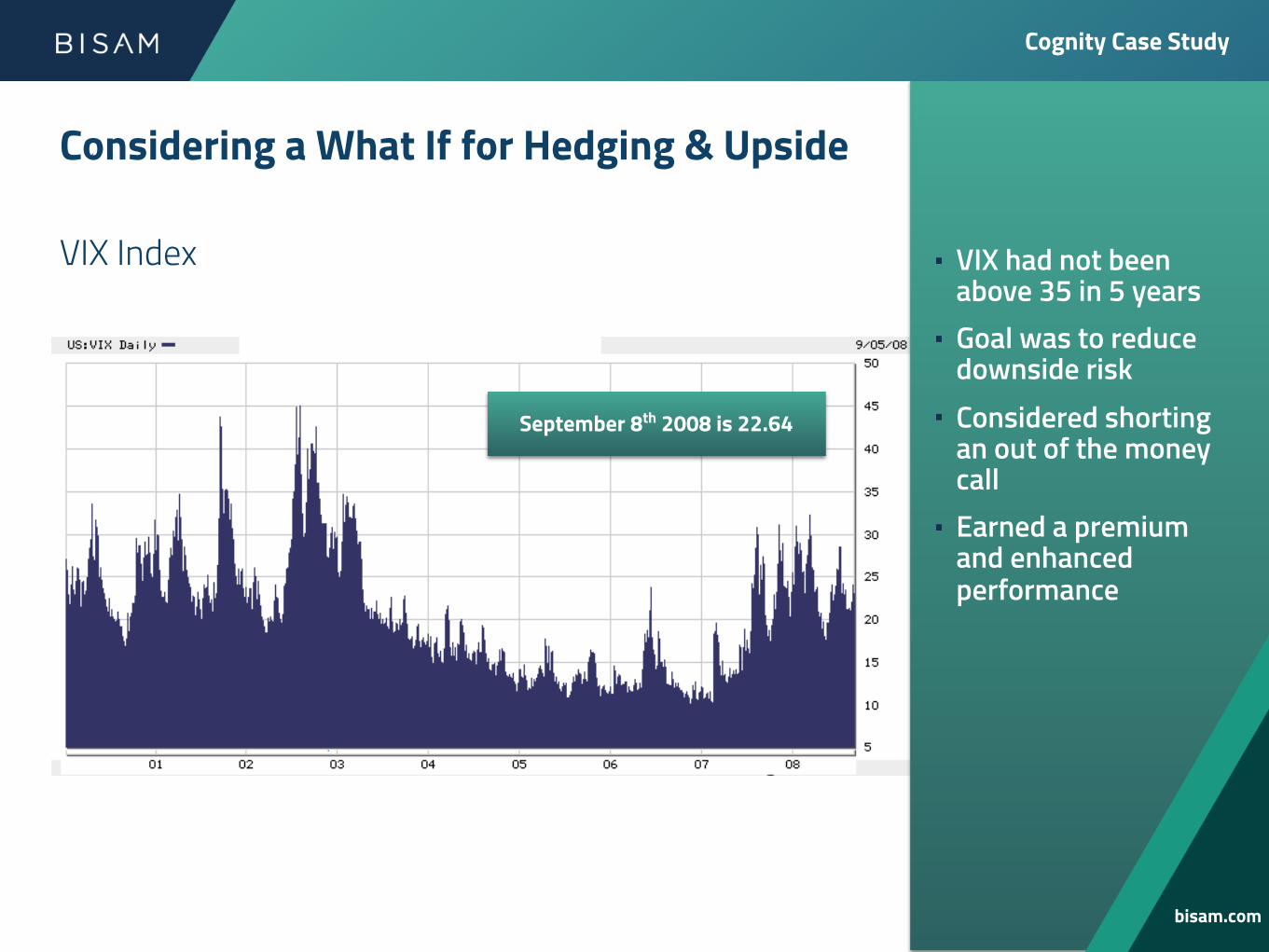

Considering a What If for Hedging & Upside

VIX Index

September 8th 2008 is 22.64

• VIX had not been above 35 in 5 years

• Goal was to reduce downside risk

• Considered shorting an out of the money call

• Earned a premium and enhanced performance

Cognity Case Study

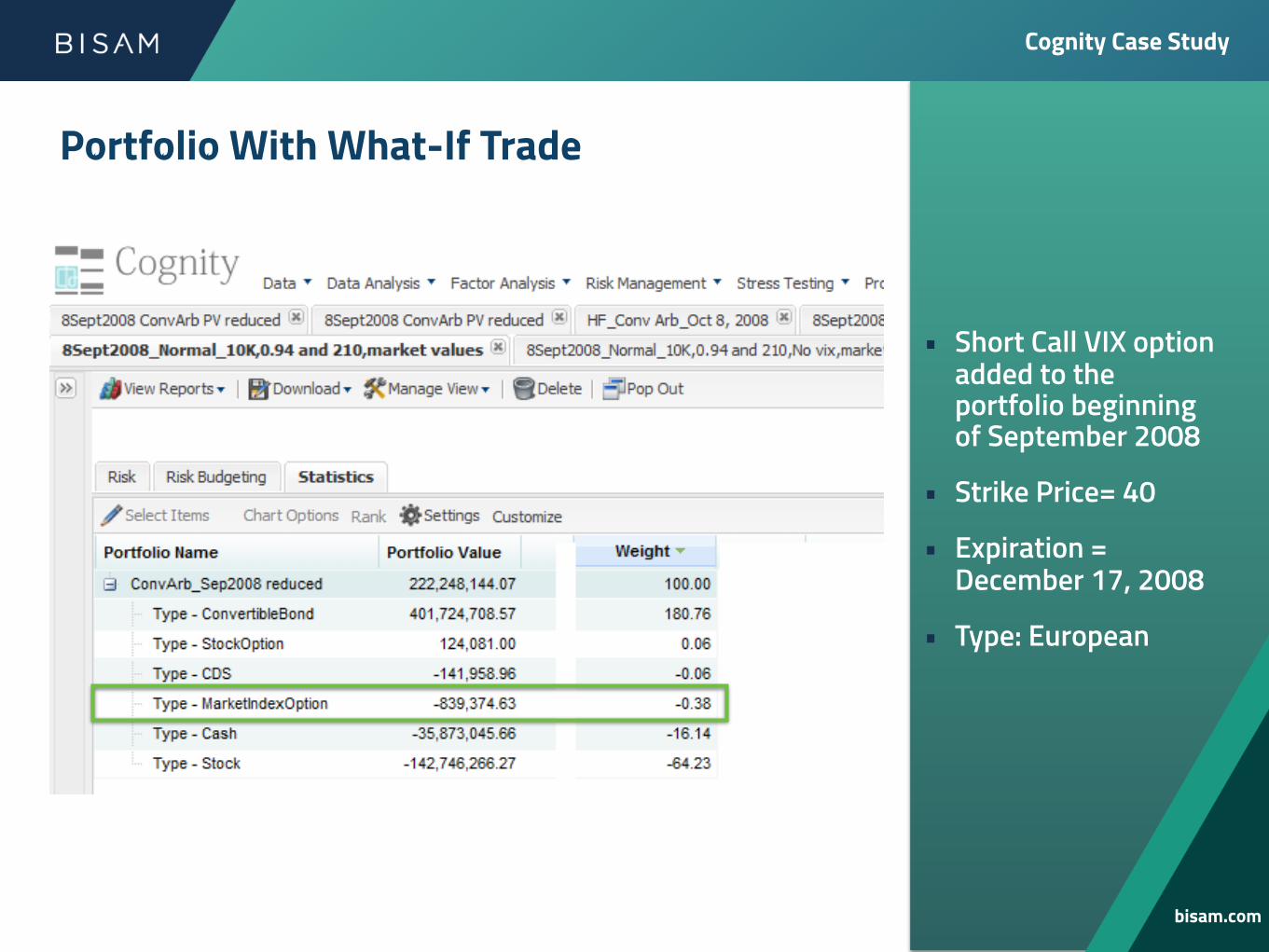

Portfolio With What-If Trade

• Short Call VIX option added to the portfolio beginning of September 2008

• Strike Price= 40

• Expiration = December 17, 2008

• Type: European

bisam.com

Cognity Case Study

bisam.com

The challenges to overcome

Normal Lens

Fat-tailed Lens

Portfolio Risk with Short Call

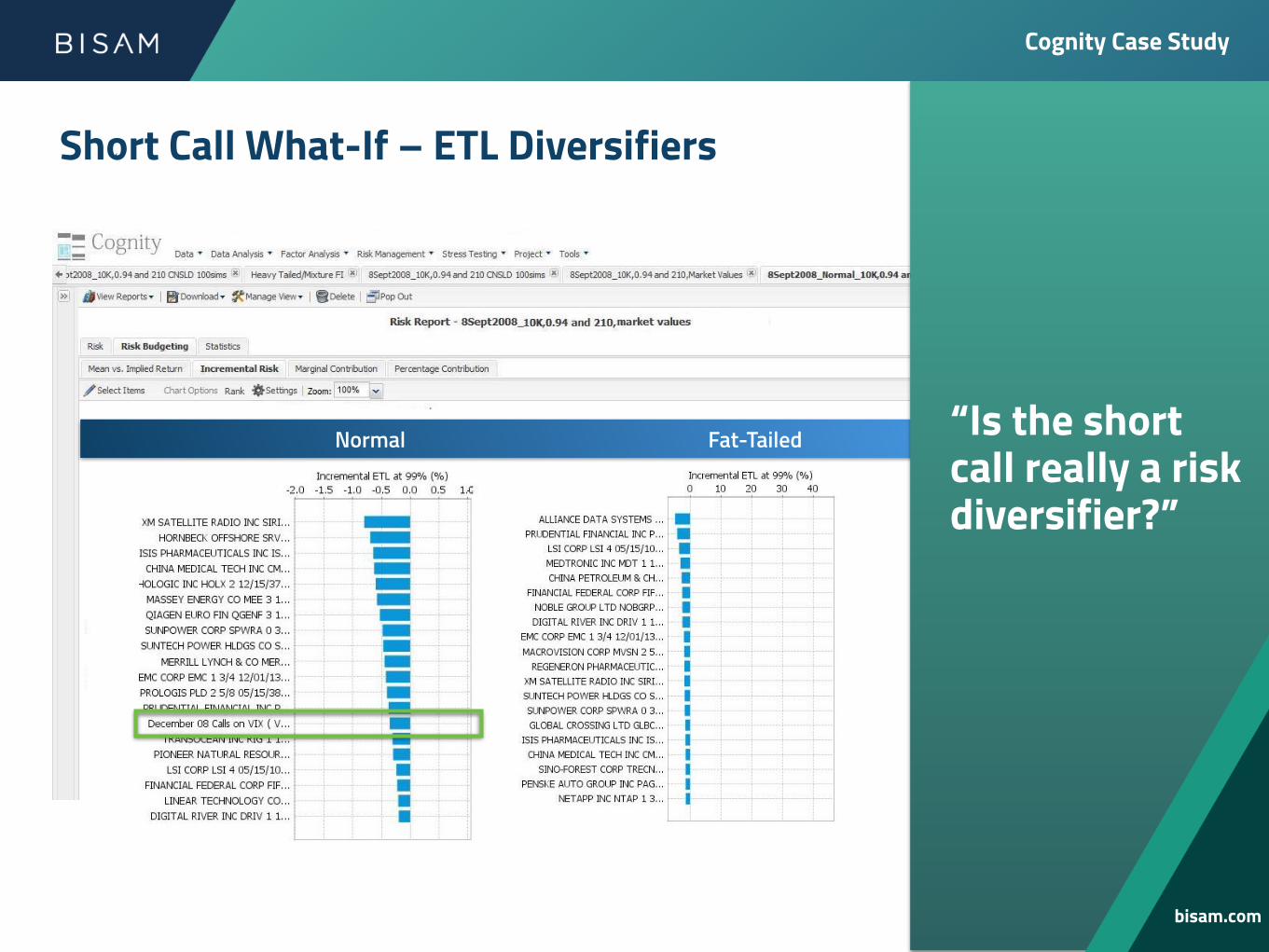

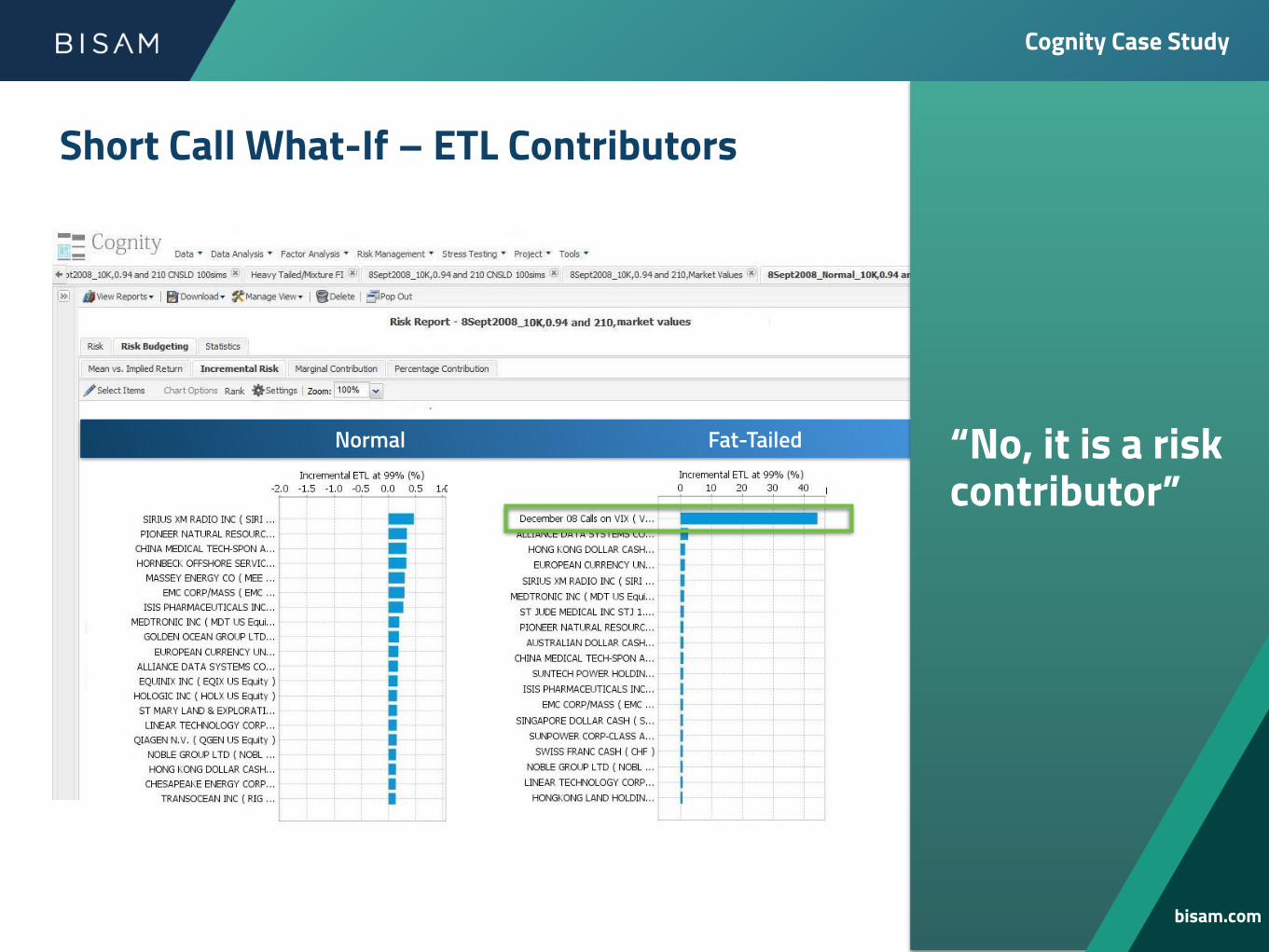

“Is the short call really a risk diversifier?”

Cognity Case Study

bisam.com

Short Call What-If – ETL Diversifiers

Normal Fat-Tailed

“No, it is a risk contributor”

Cognity Case Study

bisam.com

Short Call What-If – ETL Contributors

Normal Fat-Tailed

Cognity Case Study

bisam.com

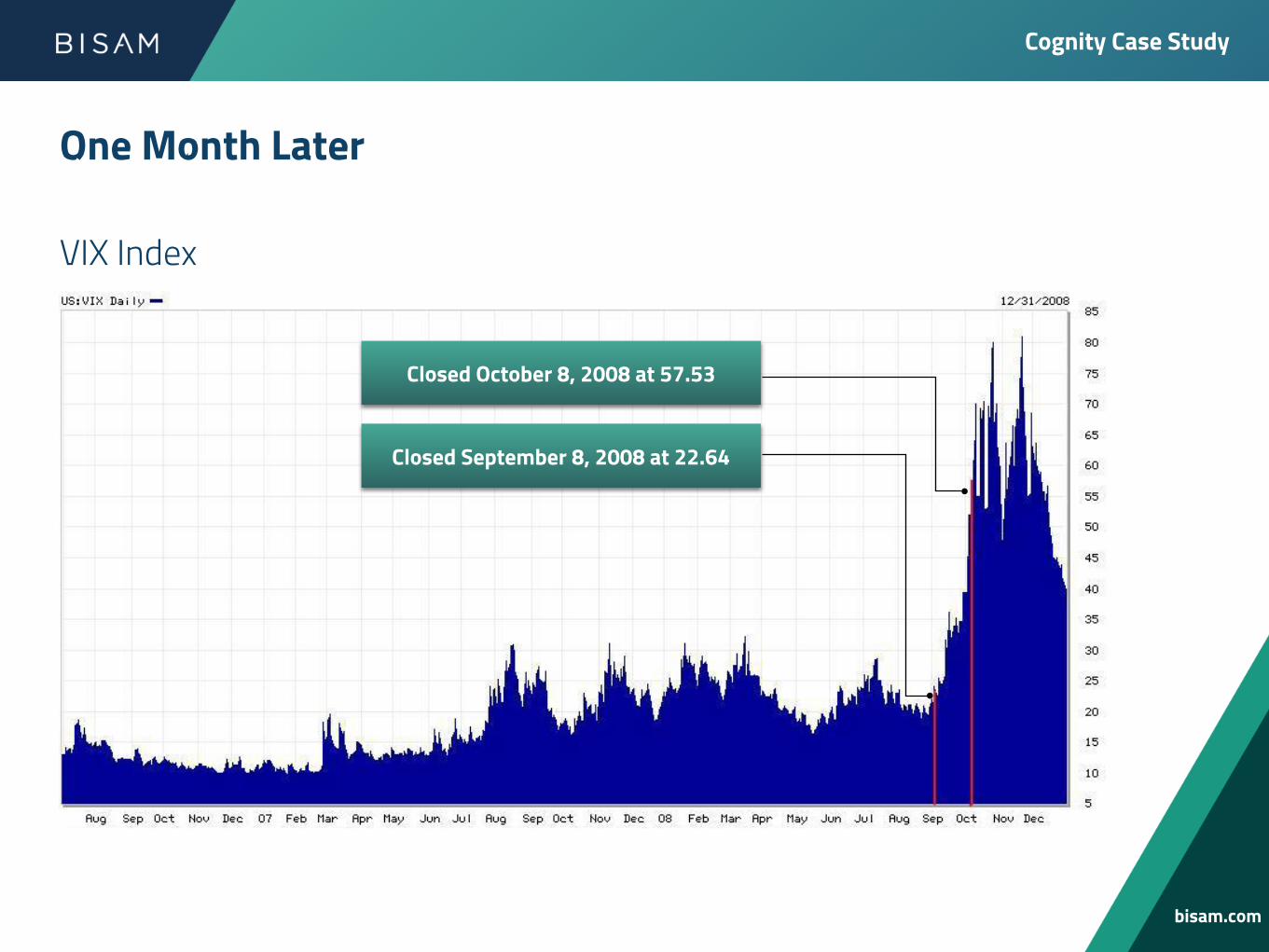

One Month Later

VIX Index

Closed October 8, 2008 at 57.53

Closed September 8, 2008 at 22.64

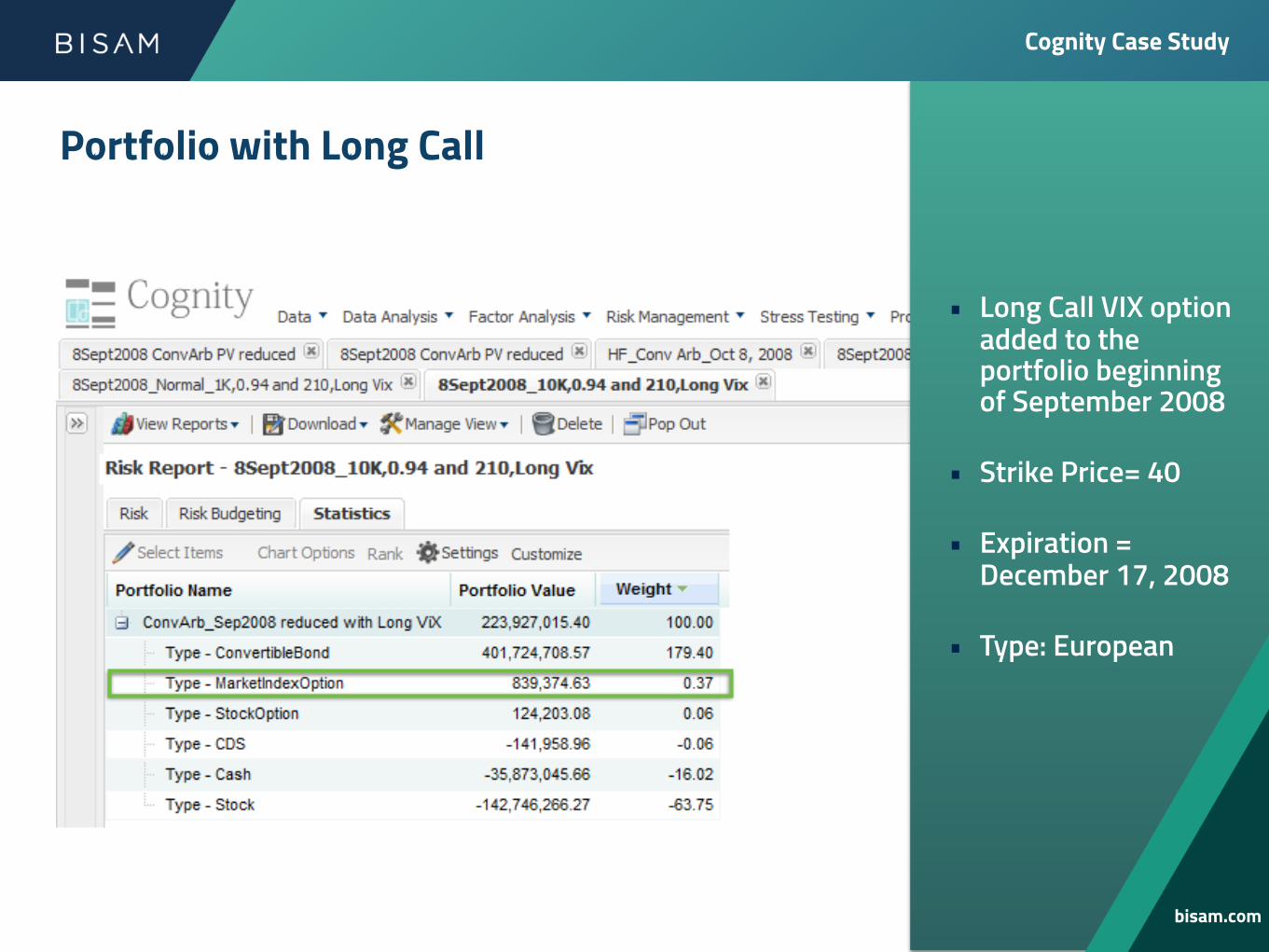

• Long Call VIX option added to the portfolio beginning of September 2008

• Strike Price= 40

• Expiration = December 17, 2008

• Type: European

Cognity Case Study

bisam.com

Portfolio with Long Call

Cognity Case Study

bisam.com

Portfolio with What-If Long Call

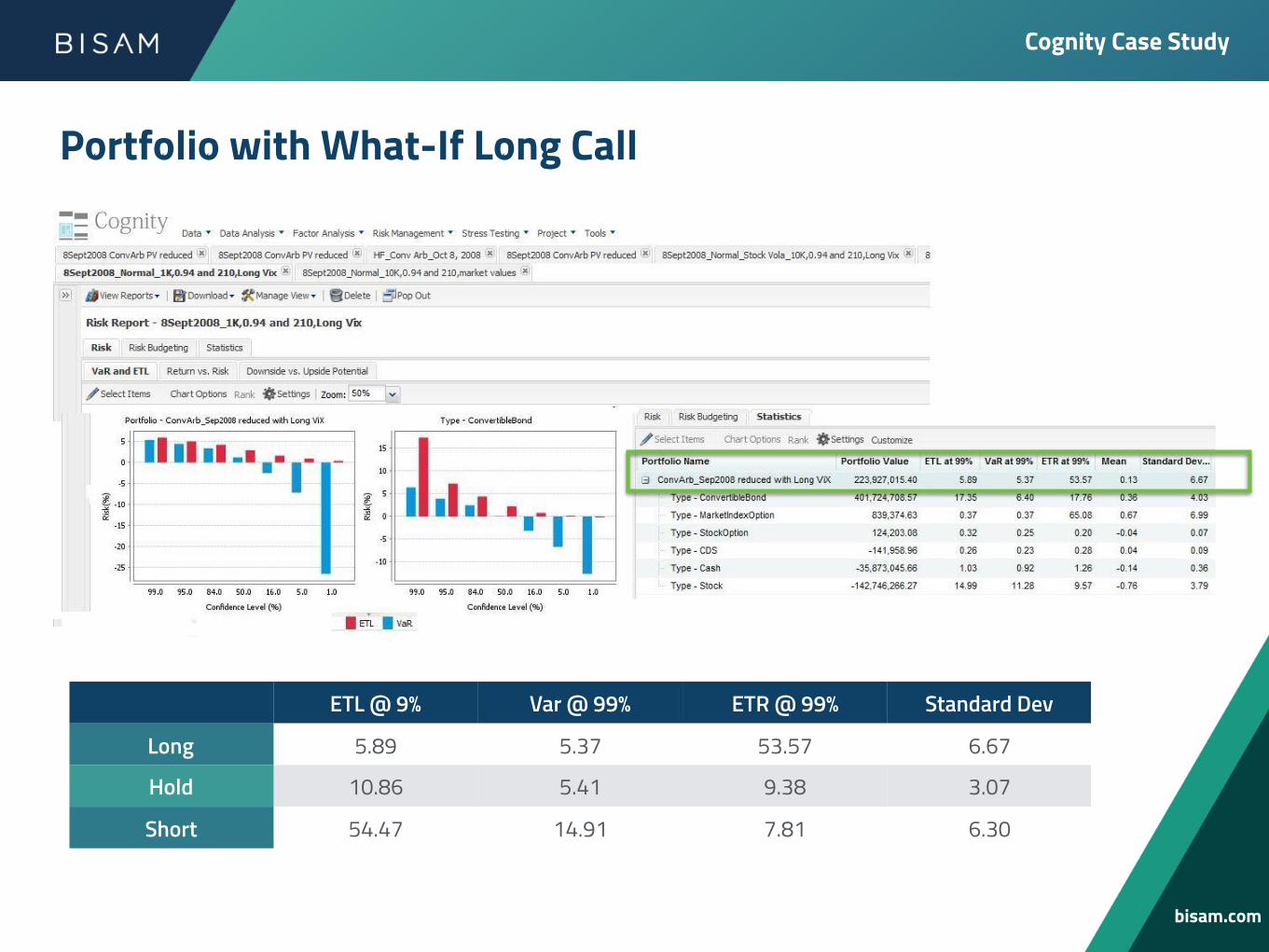

ETL @ 9% Var @ 99% ETR @ 99% Standard Dev

Long 5.89 5.37 53.57 6.67

Hold 10.86 5.41 9.38 3.07

Short 54.47 14.91 7.81 6.30

Cognity Case Study

bisam.com

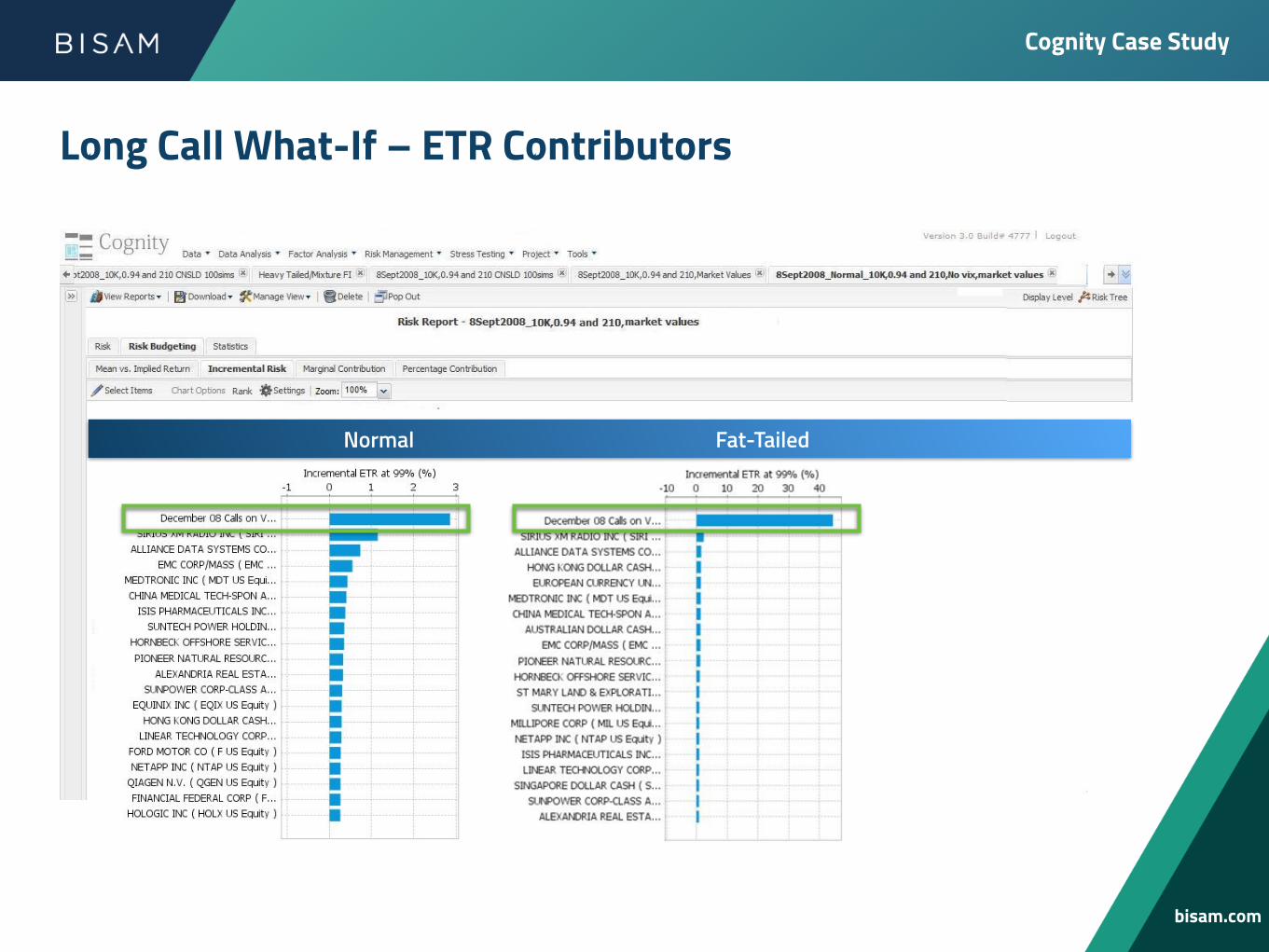

Long Call What-If – ETR Contributors

Normal Fat-Tailed

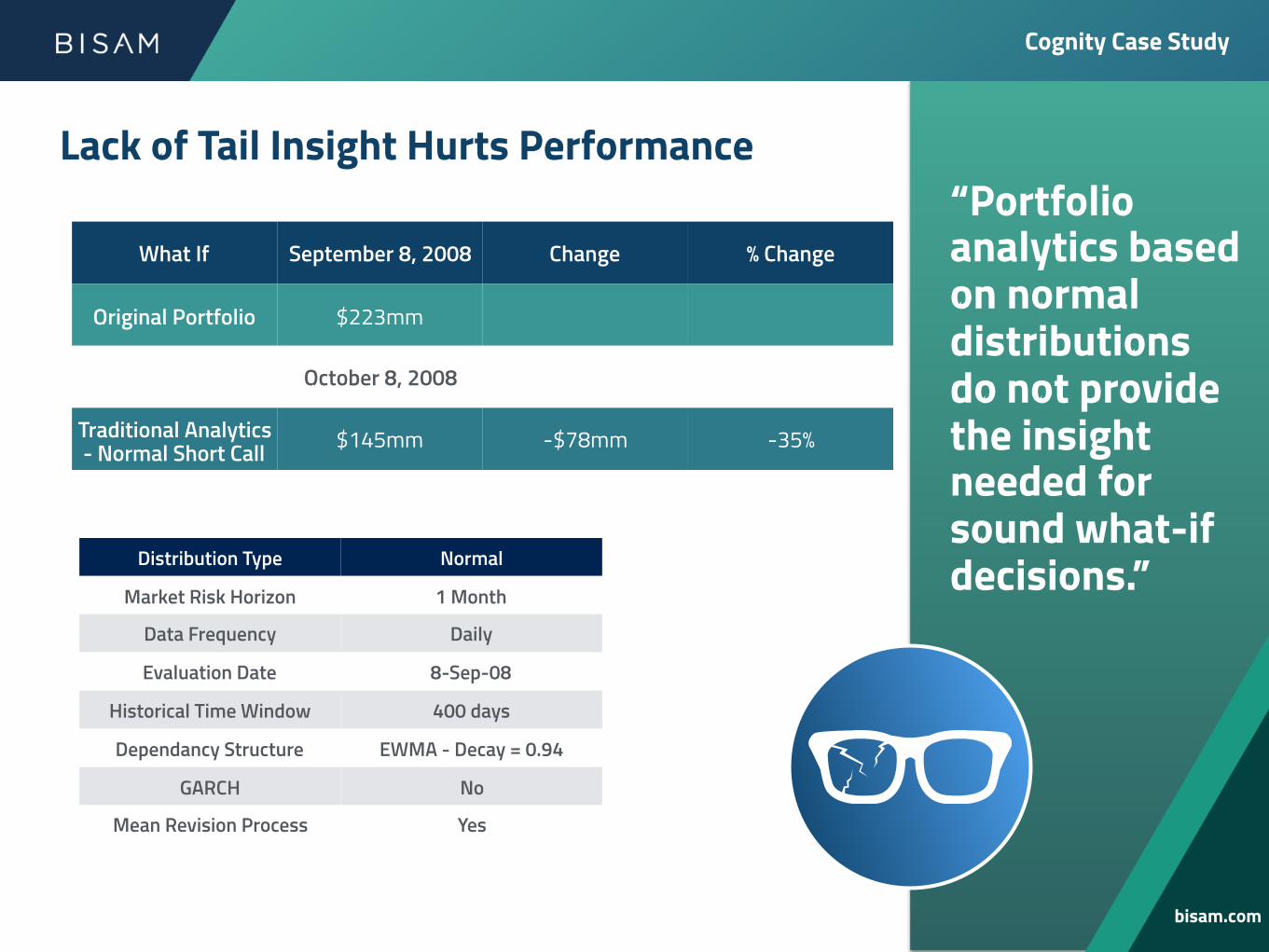

“Portfolio analytics based on normal distributions do not provide the insight needed for sound what-if decisions.”

Cognity Case Study

bisam.com

Lack of Tail Insight Hurts Performance

Distribution Type Normal

Market Risk Horizon 1 Month

Data Frequency Daily

Evaluation Date 8-Sep-08

Historical Time Window 400 days

Dependancy Structure EWMA - Decay = 0.94

GARCH No

Mean Revision Process Yes

What If September 8, 2008 Change % Change

Original Portfolio $223mm

October 8, 2008

Traditional Analytics - Normal Short Call $145mm -$78mm -35%

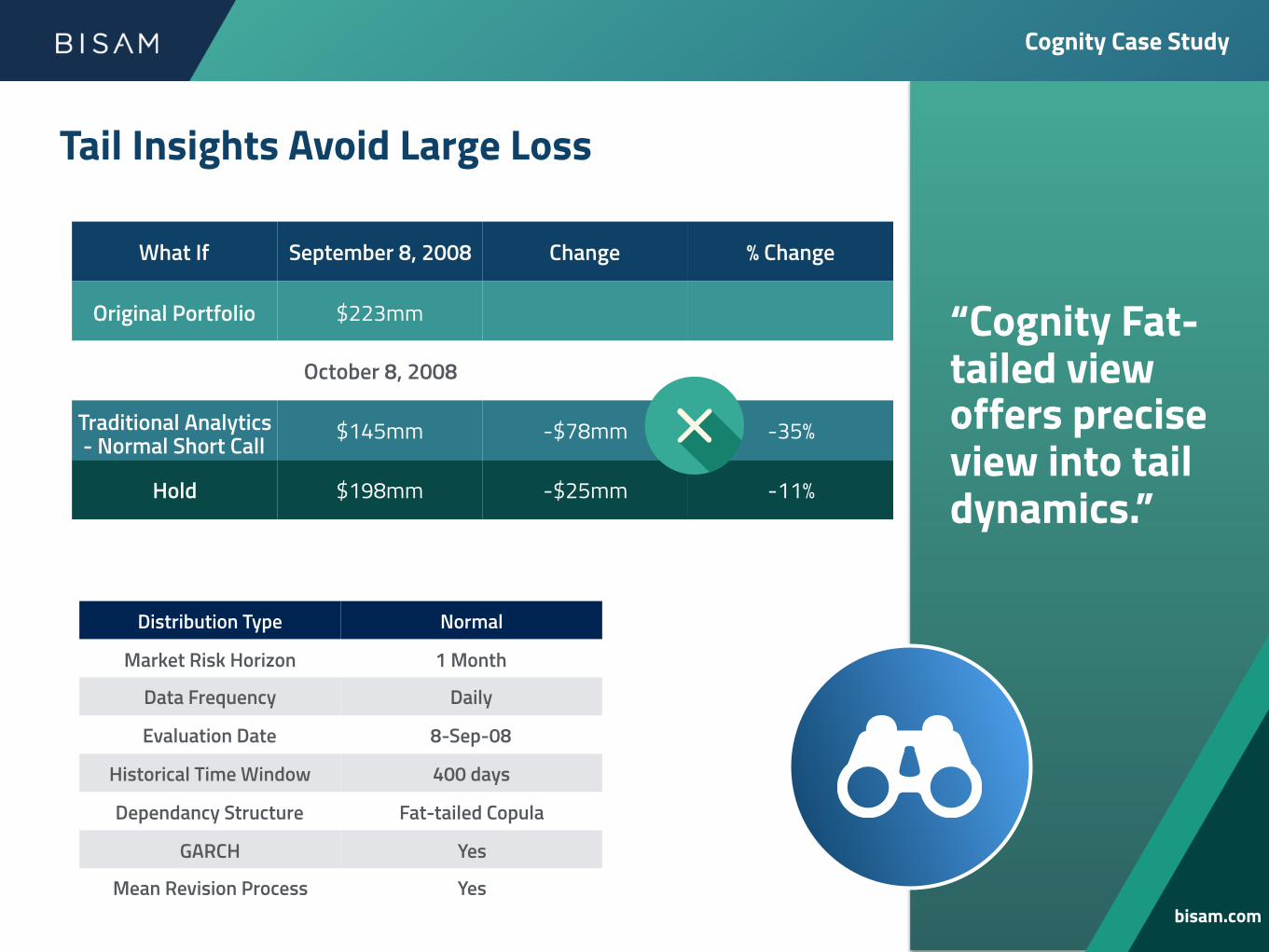

“Cognity Fat-tailed view offers precise view into tail dynamics.”

Cognity Case Study

bisam.com

Tail Insights Avoid Large Loss

Distribution Type Normal

Market Risk Horizon 1 Month

Data Frequency Daily

Evaluation Date 8-Sep-08

Historical Time Window 400 days

Dependancy Structure Fat-tailed Copula

GARCH Yes

Mean Revision Process Yes

What If September 8, 2008 Change % Change

Original Portfolio $223mm

October 8, 2008

Traditional Analytics - Normal Short Call $145mm -$78mm -35%

Hold $198mm -$25mm -11%

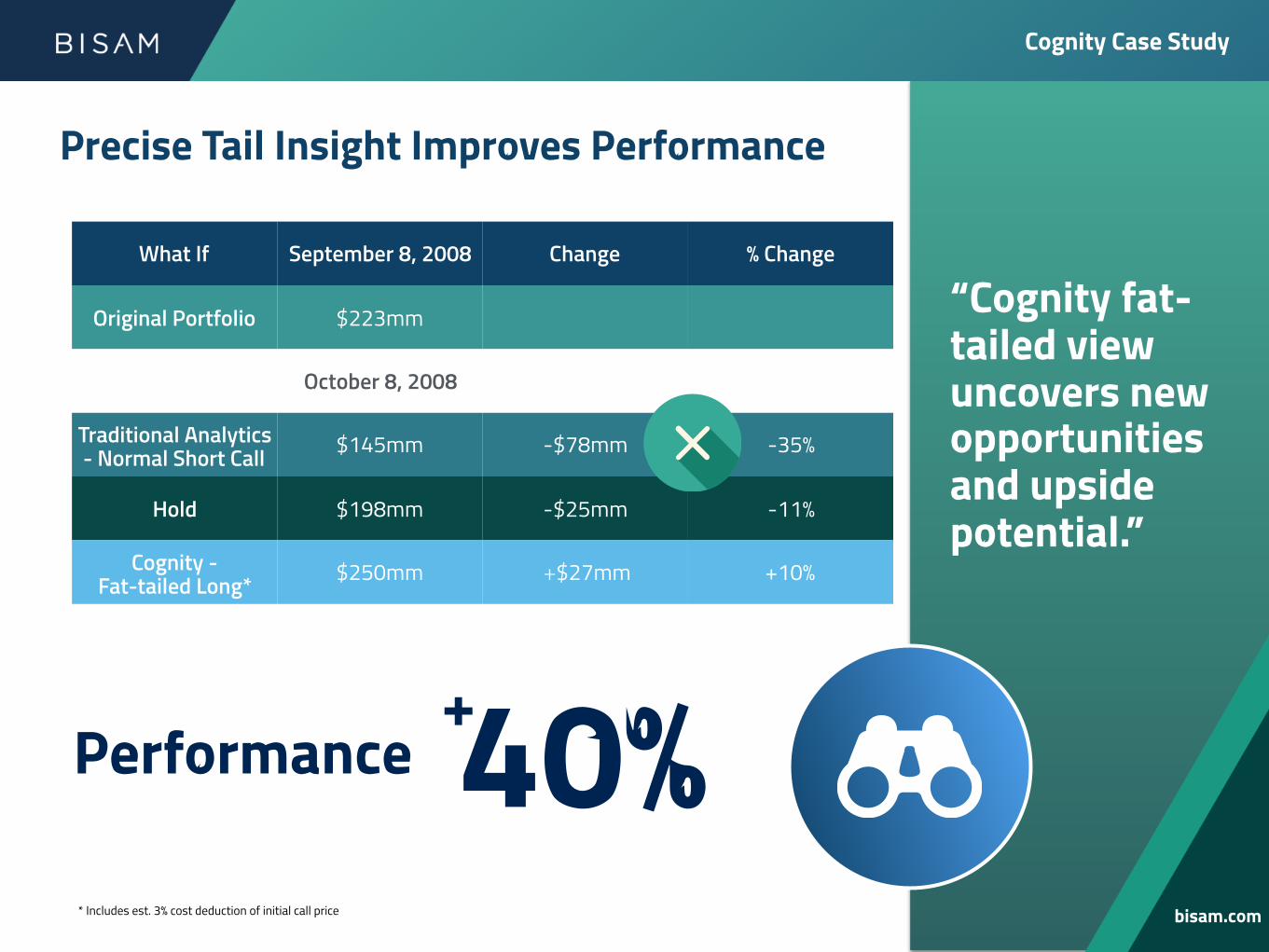

“Cognity fat-tailed view uncovers new opportunities and upside potential.”

Cognity Case Study

bisam.com

Precise Tail Insight Improves Performance

What If September 8, 2008 Change % Change

Original Portfolio $223mm

October 8, 2008

Traditional Analytics - Normal Short Call $145mm -$78mm -35%

Hold $198mm -$25mm -11%

Cognity - Fat-tailed Long* $250mm +$27mm +10%

Performance 40%+

* Includes est. 3% cost deduction of initial call price

Adaptive Risk Analytics

Cognity, part of BISAM's suite of market-leading portfolio analytics, is a comprehensive, multi-asset class market risk solution for multi-factor modeling, risk budgeting & portfolio construction, stress-testing and real world fat-tail risk measurement.

www.bisam.com/cognity Discover more:

Cognity®