Embed Size (px)

Citation preview

at a glance…Mukesh Raj & Company,

C-63, 1st Floor, Preet Vihar, Delhi-110092Contact : 011-22050790 ; www.mukeshraj.com

Key Proposals

Direct Taxes

Indirect Taxes

For Ease of Doing Business

Startups

Key Economic Indicators

Budget at a glance….

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

• Affirming that the economy is on the right track, Finance Minister Mr.Arun Jaitley presented the Union Budget for 2016-2017, on 29th February 2016.

• This Union Budget is a bitter sweet pillar for the common man. While incentivizing the “AAM AADMI” to buy homes, Finance Minister ArunJaitley has made cars expensive.

• Direct taxes as the name suggests , are taxes that are directly paid to the government by the taxpayer. It is a tax applied on individuals and organizations directly by the government. Some examples of Direct taxes are :

• Income Tax

• Corporation Tax

• Wealth tax, which is no longer in effect now.

Key proposals in Direct Taxes

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Conatct : 011-22050790 ; www.mukeshraj.com

• Income Tax is paid by an individual based on his/her taxable income in a given financial year.

• Under the Income Tax Act, the term “Individual”, also includes Hindu Undivided Family(HUF’s), Cooperative Societies, Trusts and any artificial judicial person.

• Taxable Income refers to total income minus applicable deductions and exemptions.

• Tax is payable if the taxable income is above the minimum taxable limit and is paid as per the different rates announced for each tax slab for the financial year.

• Finance Minister Mr. Arun Jaitley, did not propose any change in the income tax slab rates. However various changes have been proposed in the income tax provisions which impact the taxable income of an individual.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

Income Tax

• If the total income of an individual exceeds Rs.1 Crore, then the rate of surcharge will be 15%(against earlier 12%)

• In case of a resident individual, HUF or a firm, if dividend received by them from a domestic company exceeds Rs.10,00,000, then an additional tax at the rate of 10% of gross amount of dividend shall be paid. This will come into effect from 1st

April 2017.

• In order to provide relief to small taxpayers , the Relief under Section 87A is proposed to be increased from Rs.2000/- to Rs.5000/-

However this relief is available to a resident individual if his total income does not exceed Rs.5,00,000. For the Assessment Year 2017-2018, the relief shall be allowed up to income-tax liability or Rs.5,000/- whichever is less.

• The Finance Bill proposes an amendment to provide that income tax is payable at 10% on long term capital gains (LTCG), arising from the transfer of unlisted securities or shares of a closely held company.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

Income Tax

• Currently the non-corporate taxpayers, pay the advance tax in three installments, viz. @30%, 60% & 100% of tax on or before 15th September , 15th December & 15th March of each fiscal year respectively. The new Finance Bill 2016 proposes to treat the non-corporate at par with the corporate taxpayers. This can be seen as follows :

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

Advance Tax

Due Date For All Taxpayers ( Corporate and Non-Corporate Taxpayers )

15th June 15% of Tax

15th September 45% of Tax

15th December 75% of Tax

15th March 100% of Tax

• Earlier the tax-payers opting for presumptive taxation scheme under Section 44AD were not able to pay advance tax. Further these taxpayers were not liable for interest under Sections 234B & 234C. It is now proposed that such taxpayers shall also pay the advance tax on or before 15th

March of each previous year. Consequently interest for default and deferment of advance tax under Section 234B & Section 234C respectively , shall also be levied.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

Advance Tax

Budget at a glance….

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011- 22050790 ; www.mukeshraj.com

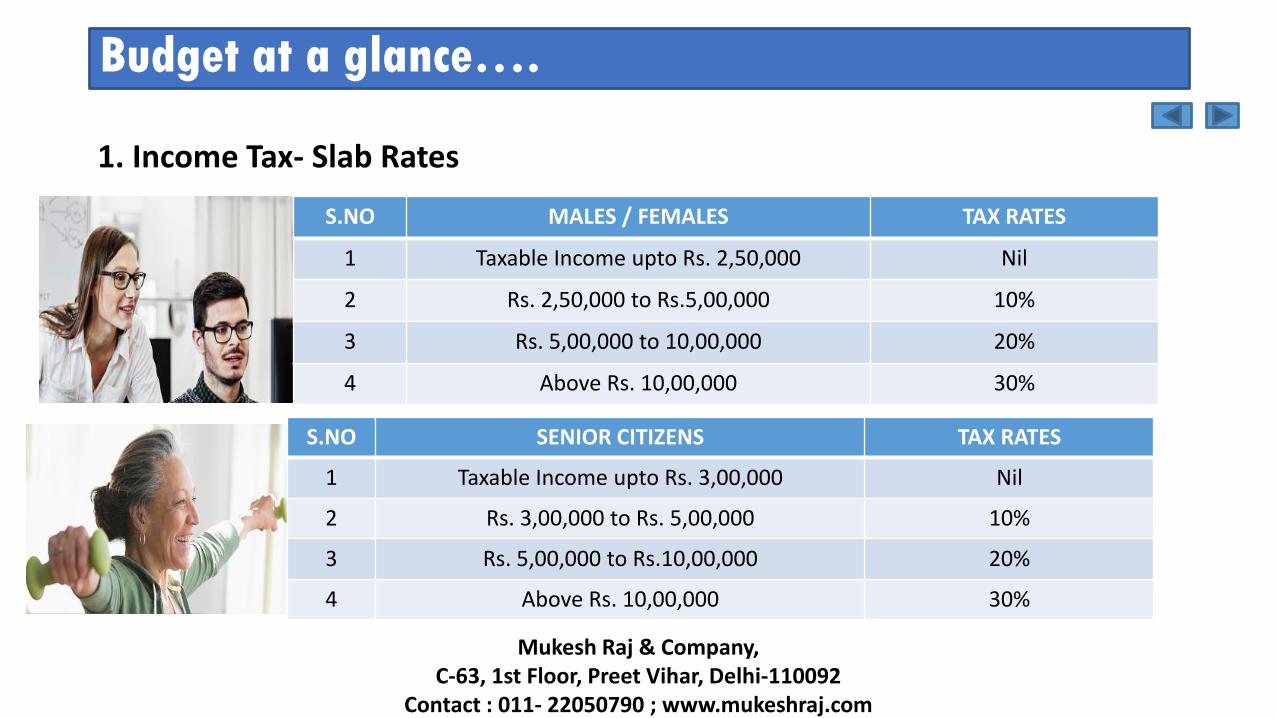

S.NO MALES / FEMALES TAX RATES

1 Taxable Income upto Rs. 2,50,000 Nil

2 Rs. 2,50,000 to Rs.5,00,000 10%

3 Rs. 5,00,000 to 10,00,000 20%

4 Above Rs. 10,00,000 30%

S.NO SENIOR CITIZENS TAX RATES

1 Taxable Income upto Rs. 3,00,000 Nil

2 Rs. 3,00,000 to Rs. 5,00,000 10%

3 Rs. 5,00,000 to Rs.10,00,000 20%

4 Above Rs. 10,00,000 30%

1. Income Tax- Slab Rates

Budget at a glance….

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011- 22050790

S.NO SUPER SENIOR CITIZEN TAX RATES

1 Taxable Income upto Rs. 5,00,000 Nil

2 Rs. 5,00,000 to Rs. 10,00,000 20%

3 Above Rs. 10,00,000 30%

Income Tax- Slab Rates

2. Co-operative SocietyS.NO Income Slabs TAX RATES

1 Where taxable income doesn’t exceed Rs. 10,000 10%

2 Where the taxable income exceeds Rs. 10,000 but doesn’t exceed Rs. 20,000

1,000 + 20% of income in excess of Rs. 10,000

3 Where the taxable income exceeds Rs. 20,000 3,000 + 30% of amount by which the taxable income

exceeds Rs. 20,000

3.Firm / Local AuthorityIncome Tax: 30% of Taxable Income

Plus: Surcharge: 12% of income tax if taxable income exceeds Rs. 1Crore Education Cess: 3% of total of income tax and surcharge

4. Domestic Company

• Income Tax: 30% of Taxable Income• Tax Rate is 29% if Turnover or Gross Receipts of the company doesn’t exceed Rs.5 Crores.

Plus:Surcharge:7% of the Income Tax if taxable income exceeds Rs. 1 crore12% of the Income Tax if taxable Income exceeds Rs. 10 croreEducation Cess: 3% of total of income tax and surcharge

Budget at a glance….

5. Foreign Company

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Income Tax: 40% of Taxable Income

Plus:• Surcharge:

2% of the Income Tax if taxable income exceeds Rs. 1crore5% of the Income Tax if taxable income exceeds Rs. 5crore

•Education Cess: 3% of the total of Income Tax and surcharge

Budget at a glance….

• It is proposed that filing of return by an individual/HUF/AOP/BOI/artificial juridical person shall be mandatory even if their entire income is exempt from tax under Section 10(38). However, in such case the total income without giving effect to the provisions of Section 10(38) should exceed the maximum exemption limit to require the assessee to file the return of income.

• Currently, the belated return can be filed even after expiry of relevant AY, But it is now proposed that belated return cannot be filed after expiry of relevant Assessment Year. Thus, belated return can be filed before the end of relevant AY or before completion of assessment, whichever is

earlier.

• It is also proposed that return which is otherwise valid shall not be treated as defective return just because self-assessment tax and interest have not been paid on or before date of furnishing of the return.

• It has been proposed that belated return can also be revised if there is any omission or wrong statement in the return of income.

• It has been proposed that processing of return is necessary before making scrutiny assessment.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

Return Of Income

Deductions : Section 80EE ( Income Tax Benefit on Home Loan Interest)

• In furtherance of the goal of the Government of providing “Housing for all” , it is proposed to incentivise First Home Buyers availing home loans, by providing additional deduction in respect of interest on loan taken for residential house property from any financial institution up to Rs. 50,000/-

• This incentive is proposed to be extended to a house property :

• Whose value is less than Rs. 50,00,000 in respect of which a loan of an amount not

exceeding Rs.35,00,000 has been sanctionedduring the period from 1st April 2016 to 31st March 2017.

• It is also proposed to extend the benefit of deduction till the repayment of loan continues.

• The deduction under the proposed Section is over and above the limit of Rs.2,00,000/- provided for a self occupied property under Section 24 of the Act.

• These amendments will take effect from 1st

April,2017

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact :011-22050790 ; www.mukeshraj.com

Budget at a glance….

• An assessee is allowed to claim deduction of up to Rs. 2,00,000 in respect of interest on loan taken for acquisition or construction of self occupied house property, if the following conditions are fulfilled :

• House property has been acquired or constructed within a period of 3 years from the end of the financial year in which loan was taken.

• In view of the fact that housing projects often take longer time for completion, it is proposed that the deduction shall be available if property is acquired or constructed within 5 years from the end of the financial year in which capital was borrowed.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

• An individual can claim deduction under Section 80GG if he is paying house rent but not receiving any HRA from the employer. The least of following is allowed as deduction:

• Rent paid in excess of 10% of total income;

• Rs. 2,000 per month; or

• 25% of total income.

The existing limit of Rs. 2,000 per month is proposed to be increased to Rs. 5,000 per month.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Deductions : Section 80 GG (In Respect of Rent Paid)

Budget at a glance….

• Deduction under Section 80JJAA is proposed to be allowed to all assesses who are required to get their accounts audited.

• 30% of emoluments paid to employees would be allowed as a deduction provided emolument per employee per month is less than or equal to Rs. 25,000.

• However, no deduction is available where Government is paying for EPF of such employees

• It is further proposed to reduce the minimum number of days of employment in a financial year from 300 days to 240 days and also the condition of 10% increase in number of employees every year is proposed to be withdrawn.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

Deductions : Section 80 JJAA

Incentives for promoting “Housing for All”

• In order to promote “Housing For All”, it is proposed to provide for 100% deduction of profitsof an assessee developing or building affordable housing projects if the housing project is approved by competent authorities before 31/03/2019, subject to following conditions:

• Project is completed within 3 years from date of approval.

• where residential unit is allotted to an individual, no such unit shall be allotted to him or any member of his family, etc

• The project is on a plot of land measuring not less than 1000 sq. metres where the project is within 25 km from the municipal limits of four metros namely Delhi, Mumbai, Chennai & Kolkata and

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….Budget at a glance….

in any other area, it is measuring not less than 2000 sq. metres where the size of the residential unit in the said areas is not more than thirty sq. metres and sixty sq. metres, respectively,

Taxation of Unrealised Rent and Arrears of Rent

• It is proposed to simplify the earlier Sections and merge them under a single new section 25A so as to bring uniformity in tax treatment of arrears of rent and unrealised rent.

• It is proposed to provide that the amount of rent received in arrears or the amount of unrealised rent realised subsequently by an assessee shall be charged to income-tax in the financial year in which such rent is received or realised, whether the assessee is the owner of the property or not in that financial year.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact :011-22050790 ; www.mukeshraj.com

Budget at a glance….

• It is also proposed that thirty per cent of the arrears of rent or the unrealised rent realised subsequently by the assessee shall be allowed as deduction. From 01/04/2017.

Budget at a glance….

Presumptive Taxation Scheme

• Currently, the presumptive tax regime does not apply to an assessee engaged in specifiedprofession [as referred to in Section 44AA(1) such as legal, medical, engineering or architectural profession or the profession of accountancy or technical consultancy or interior decoration or any other profession as is notified]. A new Section 44ADA is proposed to be inserted for computing professional income on presumptive basis at 50% of gross receipts. Professionals can take benefit of such presumptive Scheme if their receipts do not exceed Rs.50,00,000.

• Under existing provisions of Section 44AD eligible assessee can take benefit of presumptive taxation Scheme if his turnover or gross receipts in

previous year does not exceed an amount of Rs.1 Crore Such threshold limit has been proposed to be increased from Rs.1 Crores to Rs.2 Crores.

• If partnership firm is computing its business income on presumptive basis, it is proposed that salary and interest paid to its partners shall not be allowed as deduction from such presumptive income.

• As a measure against misuse of presumptivetaxation scheme, it is proposed that where an assessee declares profit on presumptive basis under Section 44AD for any previous year but does not declare profit on presumptive basis for subsequent five years, he shall not be eligible to

Budget at a glance….

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011- 22050790 ; www.mukeshraj.com

Budget at a glance….

Presumptive Taxation Scheme

claim the benefit of presumptive taxation again for next five years subsequent to the year in which the profit has not been declared in accordance with Section 44AD

• It is also proposed that the assessee will not be required to maintain books of account under sub-section (1) of section 44AA and get the accounts audited under section 44AB in respect of such income unless the assessee claims that the profits and gains from the aforesaid profession are lower than the profits and gains deemed to be his income under sub-section (1) of section 44ADA and his income exceeds the maximum amount which is not chargeable to income-tax. However this will be applicable from 01/04/2017

Budget at a glance….

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011- 22050790 ; www.mukeshraj.com

Budget at a glance….

Accounts and Audit

Budget at a glance….

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011- 22050790 ; www.mukeshraj.com

Budget at a glance….

• The threshold limit for audit under Section 44ABhas been proposed to be increased to Rs. 50 lakhsfrom existing Rs. 25 lakhs in case of specified professions.

• It is proposed that a taxpayer covered under new proposed Section 44ADA [presumptive taxation scheme for specified professionals], shall get its accounts audited if he claims that the profits and gains from the profession are lower than the presumptive income and his income exceeds the maximum amount which is not chargeable to income-tax.

Changes Related to TDS/TCS

• Section 206AA is proposed to be amended so that the withholding tax at higher rate shall not apply in case of a non-resident subject to prescribed conditions. Currently such exemption is given only in respect of payment of interest on long term bonds as referred to in Section 194LC.

• As per Section 206C the seller shall collect tax at source at a rate of 1% from purchaser

• on sale of motor vehicles of value exceeding Rs.10 lakhs,

• on sale of any goods or service in cash (other than bullions and jewelleries or providing any services other than payments on which tax is deducted at source) exceeding Rs.2lakhs.

• In order to rationalise the rates and base for TDS provisions, the threshold limit and the rates of deduction of tax at source have been revised substantially.

• It is proposed to amend Section 206AA of the Income Tax Act so as to provide that TDS shall not be deducted at a higher rate in case of non-residentsnot having PAN, subject to prescribed conditions.

• TCS is proposed to be levied at 1% in case of sale of goods or services, if value thereof exceeds Rs.2,00,000/-

• TCS is proposed to be levied at 1% in case of sale of motor vehicle, if value thereof exceeds Rs.10,00,000/-

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011- 22050790 ; www.mukeshraj.com

Budget at a glance….

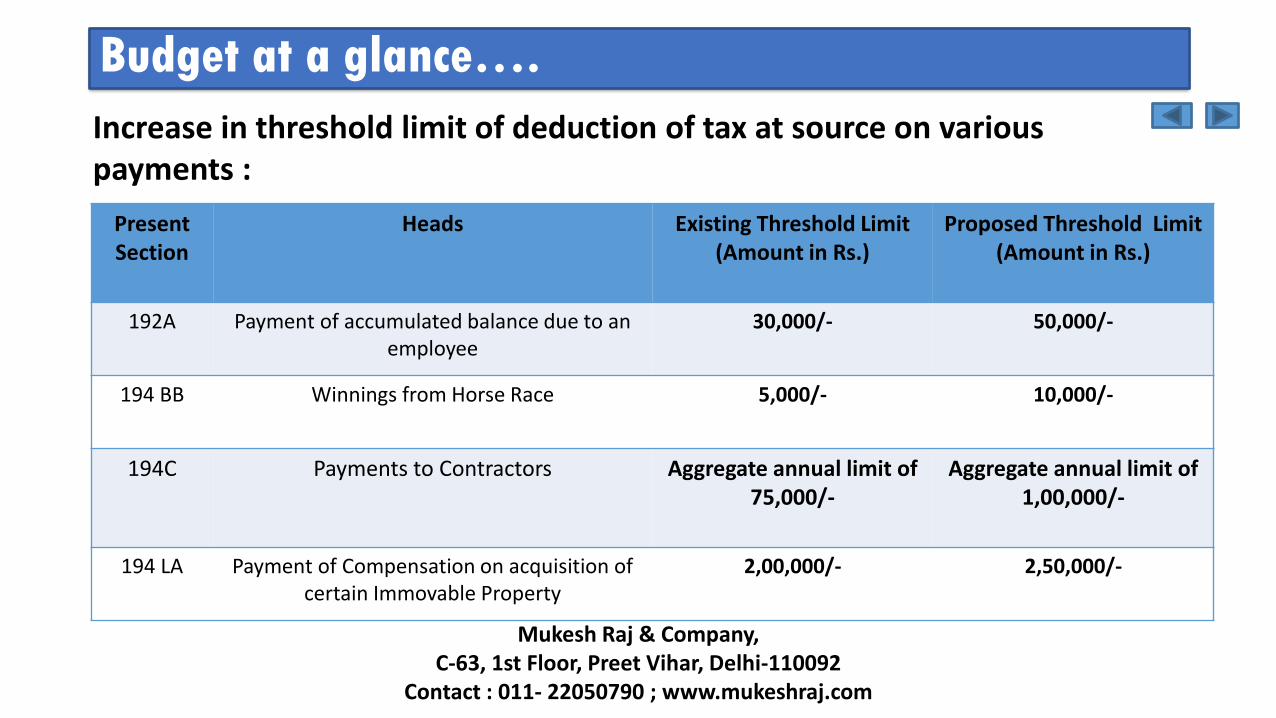

Increase in threshold limit of deduction of tax at source on various payments :

Budget at a glance….

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011- 22050790 ; www.mukeshraj.com

Budget at a glance….

PresentSection

Heads Existing Threshold Limit(Amount in Rs.)

Proposed Threshold Limit (Amount in Rs.)

192A Payment of accumulated balance due to an employee

30,000/- 50,000/-

194 BB Winnings from Horse Race 5,000/- 10,000/-

194C Payments to Contractors Aggregate annual limit of 75,000/-

Aggregate annual limit of 1,00,000/-

194 LA Payment of Compensation on acquisition of certain Immovable Property

2,00,000/- 2,50,000/-

Increase in threshold limit of deduction of tax at source on various payments :

Budget at a glance….

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011- 22050790 ; www.mukeshraj.com

Budget at a glance….

PresentSection

Heads Existing Threshold Limit(Amount in Rs.)

Proposed Threshold Limit(Amount in Rs.)

194D Insurance Commission 20,000/- 15,000/-

194G Commission on Sale of Lottery Tickets 1,000/- 15,000/-

194H Commission or Brokerage 5,000/- 15,000/-

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011- 22050790 ; www.mukeshraj.com

Budget at a glance….

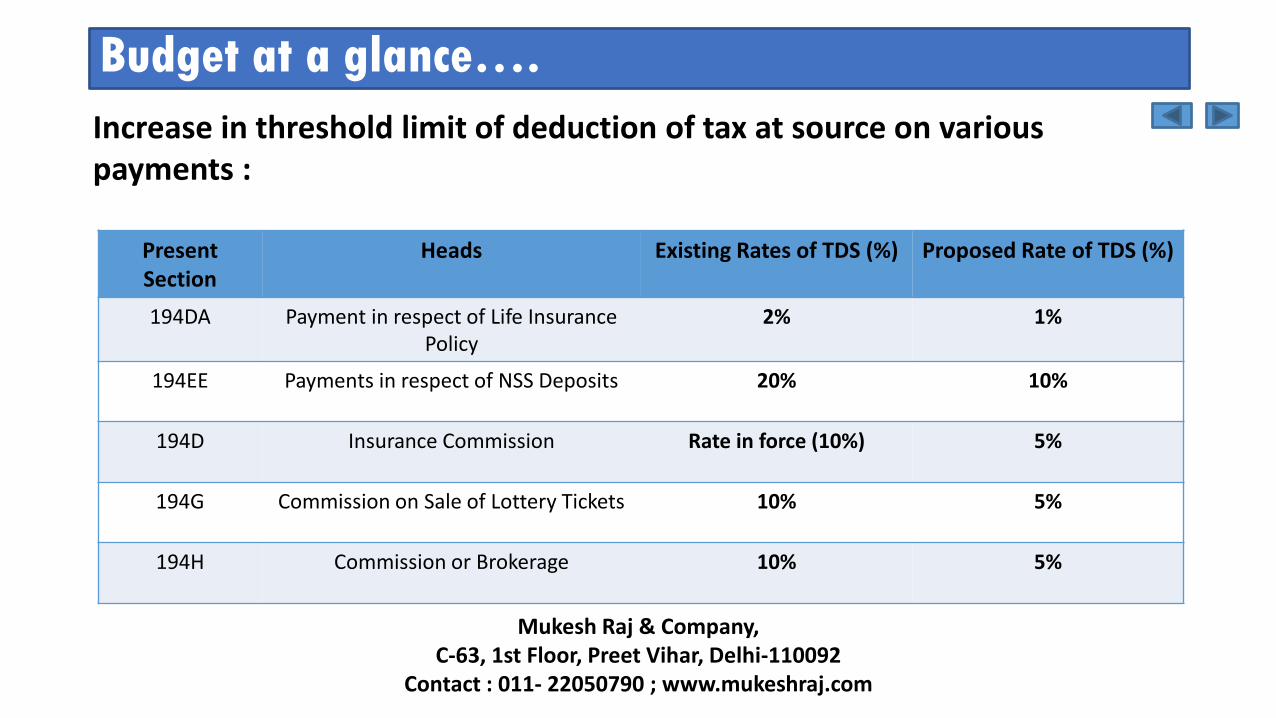

Increase in threshold limit of deduction of tax at source on various payments :

PresentSection

Heads Existing Rates of TDS (%) Proposed Rate of TDS (%)

194DA Payment in respect of Life Insurance Policy

2% 1%

194EE Payments in respect of NSS Deposits 20% 10%

194D Insurance Commission Rate in force (10%) 5%

194G Commission on Sale of Lottery Tickets 10% 5%

194H Commission or Brokerage 10% 5%

Other Amendments

• The Government will contribute 8.33% for all new employees enrolling in EPFO for first three years of their employment.

• To provide relief to newly setup Domestic Companies engaged in business of manufacturing or production, it is proposed to amend the act by insertion of new Section 115BA from A.Y. 2017-18 shall be computed @ 25% if-

a) Company has been setup and registered on or after 1st March 2016.

b) The company while computing its total income has not claimed any benefit u/s 10AA, benefit of accelerated depreciation, additional depreciation,

investment allowance, expenditure on scientific research and any deduction in respective of certain income under part C of chapter VIA other than the provisions of 80JJAA.

c) The option is furnished in the prescribed manner before the due date of furnishing of income.

d) Companies engaged in the business of manufacturing or production of any article or thing and is not engaged in other business.

• With a view to ensure the prompt payment of dues to Railways for the use of Railway Assets it is proposed to amend Section 43B so as to expand its scope to include payments made to Indian Railways for use of Railway assets within its ambit. From 01/04/2017

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact :011-22050790 ; www.mukeshraj.com

Budget at a glance….Budget at a glance….

• Indirect Taxes are applied on the manufacture or sale of goods and services.

• These are initially paid to the government by an intermediary, who then adds the amount of the tax paid to the value of the goods / services and passes on the total amount to the end user. Some examples of Indirect taxes are :

• Service Tax

• Sales Tax

• Excise Duty

Key proposals in Indirect Taxes

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

• Service Tax is applicable on all services provided in India, except a specified negative list of services that are exempt. It is paid by the service provider to the government who in turn collects it from the end user by the service provider at the time of provision of such service.

• The benefit of quarterly payment of Service tax Is being extended to One Person Company & HUF w.e.f 1st April 2016.

• Interest Rate will be 24% if service tax is collected but not deposited to ex-chequer.

• Various changes have taken place in the Service Tax. This can be seen in the table presented on the next slide.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Service Tax•The abatement rate in respect of services by way of construction of residential complex, building, civil structure or a part thereof is being rationalized at 70% by merging two existing rates.(70% for high end flats & 75% for low end flats.)

•Quarterly payment of service tax being extended to “One Person Company”(OPC) and HUF also, w.e.f. 1st

April 2016.

• Facility of payment of service tax being extended on receipt basis to “One Person Company” (OPC)Also, w.e.f. 1st April 2016.

Budget at a glance….

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

S.No Services Existing Proposed

1. Krishi Kalyan Cess is applicable on all taxable services w.e.f 1st June 2016 to finance and promote agriculture.

- 0.5%

2. Exemption on Services Provided by • A senior advocate to an advocate or partnership firm of advocates

providing legal services, &• A person represented on an arbitral tribunal to an arbitral tribunal

- 14%

3. Exemption on the services of transport of passengers, with or without accompanied belongings, by ropeway, cable car, or aerial tramway is being withdrawn with effect from 1st April 2016.

- 14%

4. The Negative List entry that covers “service of transportation of passengers with or without accompanied belongings, by a stage carrier ”, being omitted and tax proposed to be levied on service of transportation of passengers by air conditioned stage carriage, at the abatement of 60% without input tax credit with effect from 1st June 2016.

- 5.6%

• Excise Duty is applicable on the manufacture of

goods sold in India.

• Once goods are manufactured, it is originally paid

by the manufacturer directly to the Central

Government.

• When the goods change hands from the

manufacturer to the buyer, this tax is bundled by

the manufacturer along with the cost of goods and

passed on to the buyer.

• Excise Duty of “ 1% without input tax credit or

12.5% with input tax credit” on articles of

jewellery (excluding silver jewellery, other than

studded with diamonds and some other precious stones), with a higher exemption and eligibility limits of Rs.6 Crores and Rs.12 Crores respectively.

• Excise on readymade garments with retail price of Rs.1000 or more has been raised to 2% without input tax credit or 12.5% with input tax credit.

• Excise Duty on various tobacco products other than beedi has been raised from 10% to 15%.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Excise Duty

Budget at a glance….

• 13 Cesses levied by other Ministries/Departments and administered by the Department of Revenue, where

the revenue collection from each of them is less than Rs. 50crore in a year being abolished.

Interest Rates on delayed payment of duty/tax across all indirect taxes being rationalized at 15% , except in case of service tax collected but not deposited to the exchequer, in which case the rate of interest will be 24% from the date on which the service tax payment became due.For assesses with taxable value during preceding year/years covered by the notice is less than Rs.60 lakhs, the rate of interest on delayed payment of service tax will be 12%. This will come into effect from date of enforcement of Finance Bill,2016.

Customs18%

Excise18%

CustomsExcise

Service Tax15%

Service Tax18%24%30%

24% In case of tax collected but not deposited

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

For Ease of Doing Business

Budget at a glance….

Budget at a glance….

• With a view to providing an impetus to start-ups

and facilitate their growth in the initial phase of

their business, it is proposed to provide a

deduction of one hundred percent of the profits &

gains derived by an eligible start-up from a

business involving innovation development,

deployment or commercialization of new

products, processes or services driven by

technology or intellectual property.

• The benefit of 100% deduction of the profits derived from such business shall be available to an eligible start up which is setup before 1April 2019.

Key proposals for Start Up

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact :011-22050790 ; www.mukeshraj.com

Budget at a glance….

Budget at a glance….

• Section 54GB proposes that long-term capital gains arising from transfer of residential propertyof individual or HUF shall not be charged to tax if such capital gain is invested in shares of an eligible start-up. Such exemption shall be available if:

• Individual or HUF holds more than 50% shares of such start-up; and

• Such investment is utilized by the start-up to purchase new assets before due date of filing of return of investor.

• A new Section 54EE is inserted to provide for exemption up to Rs. 50 lakhs for long-term capital gains invested in units of funds set-up by Government to promote start-ups.

Capital Gain Exemptions for Investment in Start Ups

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact :011-22050790 ; www.mukeshraj.com

Budget at a glance….

• Exemption shall be reversed

• if amount invested is withdrawn within 3 years from date of making investment in specified funds.

• Further, if assessee takes any loan and/or advance against such investment then he is deemed to have transferred such specified asset on the date on which such loan or advance is taken.

Budget at a glance….

• Economic Indicators allow analysis of economic performance and and predictions of future performance.

• Out of various economic indicators we will take a brief overview of the main indicators in the coming slides :

India’s Key Economic Indicators

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

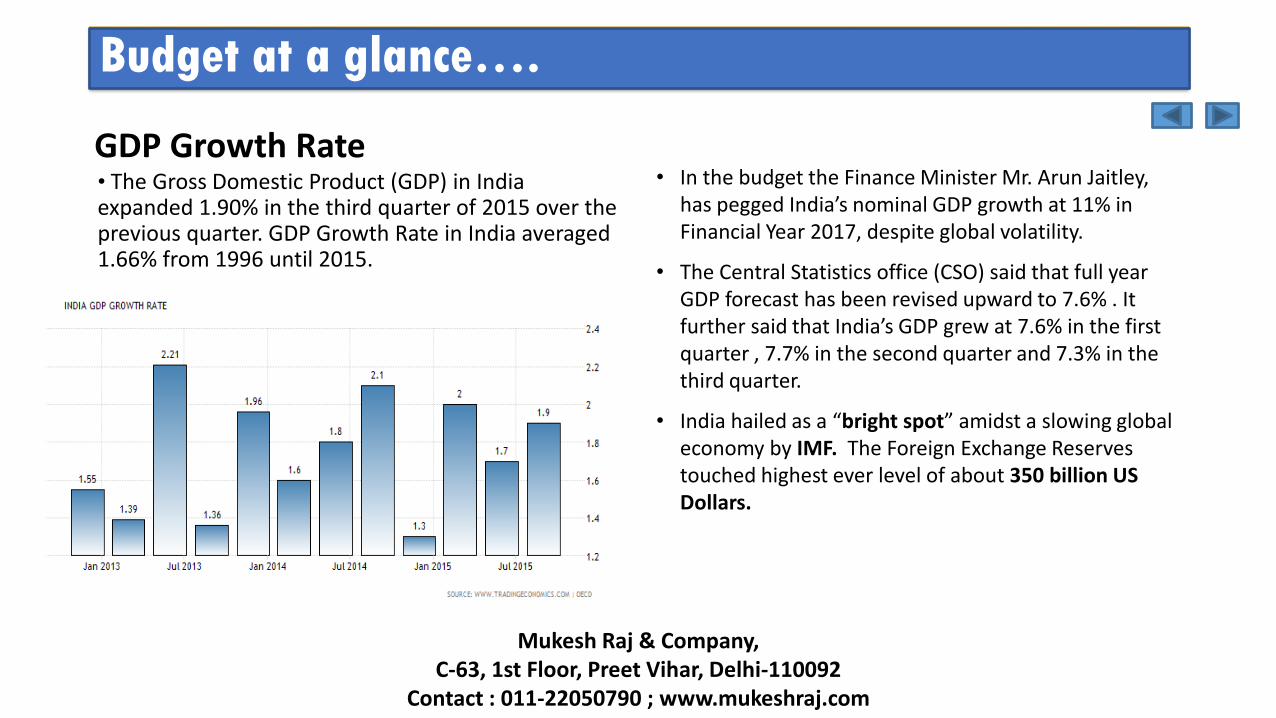

• The Gross Domestic Product (GDP) in India expanded 1.90% in the third quarter of 2015 over the previous quarter. GDP Growth Rate in India averaged 1.66% from 1996 until 2015.

• In the budget the Finance Minister Mr. Arun Jaitley, has pegged India’s nominal GDP growth at 11% in Financial Year 2017, despite global volatility.

• The Central Statistics office (CSO) said that full year GDP forecast has been revised upward to 7.6% . It further said that India’s GDP grew at 7.6% in the first quarter , 7.7% in the second quarter and 7.3% in the third quarter.

• India hailed as a “bright spot” amidst a slowing global economy by IMF. The Foreign Exchange Reserves touched highest ever level of about 350 billion US Dollars.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

GDP Growth Rate

Budget at a glance….

• It has been decided to done away with Plan and Non-Planned expenditure from fiscal 2017-2018.

• To improve the quality of Government expenditure, every new scheme being sanctioned by Government will have a sunset date and outcome review. A redeeming feature of this year’s budget Is that the Government has improved upon the Revenue Deficit Target from 2.8% to 2.5% of GDP in RE 2015-2016.

Mukesh Raj & Company, C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com

Budget at a glance….

• The fiscal deficit in RE 2015-2016 and BE 2016-2017 have been retained at 3.9% and 3.5% of GDP respectively.

• The total expenditure in the Budget for 2016-2017 has been projected at Rs.19.78lakh crore, consisting of Rs.5.50 lakh crore under Plan and Rs. 14.28 lakhcrore under Non Plan.

• The increase in Plan Expenditure is in the order of 15.3% over current year BE. Plan allocations have given special emphasis to sectors like agriculture, irrigation, social sector including health, women and child development, welfare of Scheduled Castes and Scheduled tribes, minorities, infrastructure etc.

Fiscal Discipline

Budget at a glance….

Mukesh Raj & Company,C-63, 1st Floor, Preet Vihar, Delhi-110092

Contact : 011-22050790 ; www.mukeshraj.com